Exhibit 99.1 ITAÚ UNIBANCO HOLDING S.A. CNPJ 60.872.504/0001-23 A Publicly-Listed Company NIRE 35300010230 ANNOUNCEMENT TO THE MARKET Itaú Unibanco Holding S.A. st 1 Quarter 2019 Result Itaú Unibanco Holding S.A. (“Company”) announces to its stockholders and the market at large that the Complete Financial Statements for the year ended March 31, 2019 and the st Management Discussion & Analysis for the 1 quarter of 2019 are already available on the Company’s Investor Relations website (www.itau.com.br/investor-relations). Additionally, we forward the information described below: st • Institutional Presentation of the 1 quarter of 2019 (Attachment 01); • Presentation to be used at the conference call with the press on the quarterly result, to be held on May 3, 2019 at 8:30 am (Brasília official time) (Attachment 02); • Press release (Attachment 03); • Presentation to be used at public conference calls on the quarterly result, to be held on May 3, Thursday, in English at 10:00 am (Brasília official time) and in Portuguese at 11:30 pm (Brasília official time) (Attachment 04). The expectations presented are based on information available up to the moment and involve risks, uncertainties, and assumptions that may be beyond our control. These disclosures strengthen our commitment to transparency in our disclosures to the many strategic audiences we have. São Paulo ‐ SP, May 2, 2019. Alexsandro Broedel Group Executive Finance Director and Head of Investor Relations Exhibit 99.1 ITAÚ UNIBANCO HOLDING S.A. CNPJ 60.872.504/0001-23 A Publicly-Listed Company NIRE 35300010230 ANNOUNCEMENT TO THE MARKET Itaú Unibanco Holding S.A. st 1 Quarter 2019 Result Itaú Unibanco Holding S.A. (“Company”) announces to its stockholders and the market at large that the Complete Financial Statements for the year ended March 31, 2019 and the st Management Discussion & Analysis for the 1 quarter of 2019 are already available on the Company’s Investor Relations website (www.itau.com.br/investor-relations). Additionally, we forward the information described below: st • Institutional Presentation of the 1 quarter of 2019 (Attachment 01); • Presentation to be used at the conference call with the press on the quarterly result, to be held on May 3, 2019 at 8:30 am (Brasília official time) (Attachment 02); • Press release (Attachment 03); • Presentation to be used at public conference calls on the quarterly result, to be held on May 3, Thursday, in English at 10:00 am (Brasília official time) and in Portuguese at 11:30 pm (Brasília official time) (Attachment 04). The expectations presented are based on information available up to the moment and involve risks, uncertainties, and assumptions that may be beyond our control. These disclosures strengthen our commitment to transparency in our disclosures to the many strategic audiences we have. São Paulo ‐ SP, May 2, 2019. Alexsandro Broedel Group Executive Finance Director and Head of Investor Relations

Attachment 01 Attachment 01

1Q19 Institutional Information1Q19 Institutional Information

1Q19 This presentation contains forward-looking statements regarding Itaú Unibanco Holding, its subsidiaries and affiliates - anticipated synergies, growth plans, projected results and future strategies. Although these forward-looking statements reflect management’s good faith beliefs, they involve known and unknown risks and uncertainties that may cause the Company’s actual results or outcomes to be materially different from those anticipated and discussed herein. These statements are not guarantees of future performance. These risks and uncertainties include, but are not limited to our ability to realize the amount of the projected synergies and the timetable projected, as well as economic, competitive, governmental and technological factors affecting Itaú Unibanco Holding’s operations, markets, products and prices, and other factors detailed in Itaú Unibanco Holding’s filings with the Securities and Exchange Commission which readers are urged to read carefully in assessing the forward-looking statements contained herein. Itaú Unibanco Holding undertakes in duty to update any of the projections contained herein. This presentation contains managerial numbers that may be different from those presented in our financial statements. The calculation methodology for those managerial numbers is presented in Itaú Unibanco Holding’s quarterly earnings report. To obtain further information on factors that may give rise to results different from those forecast by Itaú Unibanco Holding, please consult the reports filed with the Brazilian Securities and Exchange Commission (Comissão de Valores Mobiliários - CVM) and with the U.S. Securities and Exchange Commission (SEC), including Itaú Unibanco Holding’s most recent Annual Report on Form 20F.1Q19 This presentation contains forward-looking statements regarding Itaú Unibanco Holding, its subsidiaries and affiliates - anticipated synergies, growth plans, projected results and future strategies. Although these forward-looking statements reflect management’s good faith beliefs, they involve known and unknown risks and uncertainties that may cause the Company’s actual results or outcomes to be materially different from those anticipated and discussed herein. These statements are not guarantees of future performance. These risks and uncertainties include, but are not limited to our ability to realize the amount of the projected synergies and the timetable projected, as well as economic, competitive, governmental and technological factors affecting Itaú Unibanco Holding’s operations, markets, products and prices, and other factors detailed in Itaú Unibanco Holding’s filings with the Securities and Exchange Commission which readers are urged to read carefully in assessing the forward-looking statements contained herein. Itaú Unibanco Holding undertakes in duty to update any of the projections contained herein. This presentation contains managerial numbers that may be different from those presented in our financial statements. The calculation methodology for those managerial numbers is presented in Itaú Unibanco Holding’s quarterly earnings report. To obtain further information on factors that may give rise to results different from those forecast by Itaú Unibanco Holding, please consult the reports filed with the Brazilian Securities and Exchange Commission (Comissão de Valores Mobiliários - CVM) and with the U.S. Securities and Exchange Commission (SEC), including Itaú Unibanco Holding’s most recent Annual Report on Form 20F.

Disclaimer Corpbanca Pro Forma Information st The merger between Itaú Chile and CorpBanca was concluded on April, 1 2016. As from the second quarter of 2016, Itaú CorpBanca, the company resulting from this merger, was consolidated in our financial statements, as we are the controlling shareholder of the new bank. In order to allow comparison with previous periods, we are presenting historical pro forma data, that is, the combined result of Itaú Unibanco and CorpBanca for the periods previous to the second quarter of 2016, in the Management Discussion & Analysis report and in this presentation. The pro forma statements above mentioned were prepared considering all lines of the income statement, including 100% of Itaú CorpBanca’s result. The result related to the minority shareholders is shown in the “minority interests in subsidiaries” line, for both CorpBanca and Itaú Chile. As the data was prepared to demonstrate, on a retroactively basis, the effect of a transaction occurred in a subsequent date, there are limits inherent to pro forma information. The data was provided for illustration purposes only and should not be taken as a demonstration of the result that would have been achieved if the merger had occurred on a previous date, nor do they indicate any future result of the combined company. Consolidation of Citibank The consolidation of Citibank began on October 31, 2017, with impact on our net income in November and December 2017. As from the first quarter of 2018, we have started to present Citibank’s operations in Brazil line by line in our managerial income statement. For comparison purposes, we reprocessed the fourth quarter of 2017 to also present Citibank’s operations in Brazil in all lines of our managerial income statement (presented on a specific line in the 4Q17). page 3Disclaimer Corpbanca Pro Forma Information st The merger between Itaú Chile and CorpBanca was concluded on April, 1 2016. As from the second quarter of 2016, Itaú CorpBanca, the company resulting from this merger, was consolidated in our financial statements, as we are the controlling shareholder of the new bank. In order to allow comparison with previous periods, we are presenting historical pro forma data, that is, the combined result of Itaú Unibanco and CorpBanca for the periods previous to the second quarter of 2016, in the Management Discussion & Analysis report and in this presentation. The pro forma statements above mentioned were prepared considering all lines of the income statement, including 100% of Itaú CorpBanca’s result. The result related to the minority shareholders is shown in the “minority interests in subsidiaries” line, for both CorpBanca and Itaú Chile. As the data was prepared to demonstrate, on a retroactively basis, the effect of a transaction occurred in a subsequent date, there are limits inherent to pro forma information. The data was provided for illustration purposes only and should not be taken as a demonstration of the result that would have been achieved if the merger had occurred on a previous date, nor do they indicate any future result of the combined company. Consolidation of Citibank The consolidation of Citibank began on October 31, 2017, with impact on our net income in November and December 2017. As from the first quarter of 2018, we have started to present Citibank’s operations in Brazil line by line in our managerial income statement. For comparison purposes, we reprocessed the fourth quarter of 2017 to also present Citibank’s operations in Brazil in all lines of our managerial income statement (presented on a specific line in the 4Q17). page 3

Agenda 1. Our Profile 2. Corporate Governance 3. Business Overview 4. Financial Highlights 5. Information Technology 6. Itaú Unibanco in Capital Markets 7. Sustainability As of May 02, 2019Agenda 1. Our Profile 2. Corporate Governance 3. Business Overview 4. Financial Highlights 5. Information Technology 6. Itaú Unibanco in Capital Markets 7. Sustainability As of May 02, 2019

Our Profile 1Our Profile 1

Itaú Unibanco at a Glance Financial Highlights and Ratios Leading position in Brazil As of and for the quarter ended March 2019 (1) § US$85.8 billion market cap Highlights § 99,661 employees in Brazil and abroad Total Assets R$1651.4 Bi § 4,934 branches and CSBs in Brazil and abroad (1) Total Loans R$647.1 Bi 47,953 ATMs in Brazil and abroad § Stockholders’ Equity R$119.8 Bi (2) § Around 50.4 million clients in the Retail Bank in Feb/19 R$25.7 Bi Recurring Net Income 2018 (3) R$6.9 Bi Recurring Net Income 1Q19 § Brazilian multinational bank Long Term Foreign Currency Moody´s: Ba3 § Major provider of finance for the expansion of Brazilian companies (Itaú Unibanco Holding) Fitch: BB In 2017 Itaú Unibanco was elected the The Best Company in People Management (by “Valor § S&P: BB- Carreira” magazine) and also recognized as a pro-ethics company (Pró-Ética), an initiative Financial Ratios (2) between the Office of the Comptroller General with the private sector, which encourages the voluntary adoption of integrity measures and corruption prevention in the business sector, (4) Recurring ROE 2018 21.9% being the only financial institution among the companies approved. (5) Global Footprint of Brazil’s Top Private Sector Bank | as of March 31, 2019 Recurring ROE 1Q19 23.6% (6) Efficiency Ratio 2018 47.6% (6) Efficiency Ratio 1Q19 46.3% Liquidity Coverage Ratio 164% (7) Tier I Capital - BIS III 14.6% (1) Includes financial guarantees provided and corporate securities. (2) Represents Net Income adjusted for certain non recurring events described in the 4Q18 MD&A – Executive Summary. (3) Represents Net Income adjusted for certain non recurring events described in the 1Q19 MD&A – Executive Summary. (4) Calculated using Recurring Net Income / Average Equity. For annualized calculation method, please refer to Historical Series Spreadsheet. (5) Calculated using Recurring Net Income / Average Equity. For annualized calculation method, please refer to the 1Q19 MD&A – Executive Summary. (6) See “Efficiency Ratio” slides in this presentation for criteria. (7) Includes impacts from schedule anticipation of deductions and does not consider the additional dividend and interest on own capital. (1) As of March 31, 2019. Source: Economatica. (2) Controladoria-Geral da União (CGU). page 6Itaú Unibanco at a Glance Financial Highlights and Ratios Leading position in Brazil As of and for the quarter ended March 2019 (1) § US$85.8 billion market cap Highlights § 99,661 employees in Brazil and abroad Total Assets R$1651.4 Bi § 4,934 branches and CSBs in Brazil and abroad (1) Total Loans R$647.1 Bi 47,953 ATMs in Brazil and abroad § Stockholders’ Equity R$119.8 Bi (2) § Around 50.4 million clients in the Retail Bank in Feb/19 R$25.7 Bi Recurring Net Income 2018 (3) R$6.9 Bi Recurring Net Income 1Q19 § Brazilian multinational bank Long Term Foreign Currency Moody´s: Ba3 § Major provider of finance for the expansion of Brazilian companies (Itaú Unibanco Holding) Fitch: BB In 2017 Itaú Unibanco was elected the The Best Company in People Management (by “Valor § S&P: BB- Carreira” magazine) and also recognized as a pro-ethics company (Pró-Ética), an initiative Financial Ratios (2) between the Office of the Comptroller General with the private sector, which encourages the voluntary adoption of integrity measures and corruption prevention in the business sector, (4) Recurring ROE 2018 21.9% being the only financial institution among the companies approved. (5) Global Footprint of Brazil’s Top Private Sector Bank | as of March 31, 2019 Recurring ROE 1Q19 23.6% (6) Efficiency Ratio 2018 47.6% (6) Efficiency Ratio 1Q19 46.3% Liquidity Coverage Ratio 164% (7) Tier I Capital - BIS III 14.6% (1) Includes financial guarantees provided and corporate securities. (2) Represents Net Income adjusted for certain non recurring events described in the 4Q18 MD&A – Executive Summary. (3) Represents Net Income adjusted for certain non recurring events described in the 1Q19 MD&A – Executive Summary. (4) Calculated using Recurring Net Income / Average Equity. For annualized calculation method, please refer to Historical Series Spreadsheet. (5) Calculated using Recurring Net Income / Average Equity. For annualized calculation method, please refer to the 1Q19 MD&A – Executive Summary. (6) See “Efficiency Ratio” slides in this presentation for criteria. (7) Includes impacts from schedule anticipation of deductions and does not consider the additional dividend and interest on own capital. (1) As of March 31, 2019. Source: Economatica. (2) Controladoria-Geral da União (CGU). page 6

Our Vision Vision: To be the leading bank in sustainable performance and customer satisfaction • Implement a customer satisfaction-oriented culture, that is business-driven, through a simplified operational structure • Maximize shareholder returns, aiming at firm-wide growth • We aspire to be the preferred bank for top talents at every level • Attract and retain committed professionals with high ethical standards and strong organizational pride • Shared leadership, conquered through talent and commitment to excellence, focused on meritocracy • Create an atmosphere that inspires creativity, entrepreneurialism and the exchange of ideas • Pursue a cutting-edge technology, striving to best serve our client needs, ultimately creating value • Uphold the highest ethical standards in the relationship with clients, employees, regulators, society and the markets page 7Our Vision Vision: To be the leading bank in sustainable performance and customer satisfaction • Implement a customer satisfaction-oriented culture, that is business-driven, through a simplified operational structure • Maximize shareholder returns, aiming at firm-wide growth • We aspire to be the preferred bank for top talents at every level • Attract and retain committed professionals with high ethical standards and strong organizational pride • Shared leadership, conquered through talent and commitment to excellence, focused on meritocracy • Create an atmosphere that inspires creativity, entrepreneurialism and the exchange of ideas • Pursue a cutting-edge technology, striving to best serve our client needs, ultimately creating value • Uphold the highest ethical standards in the relationship with clients, employees, regulators, society and the markets page 7

Our Way 1. It’s only good for us if it’s good for the client We are people providing service to people, with passion and excellence. We work with the client and for the client – because they are the main reason behind why we do what we do. 2. We’re passionate about performance Generating sustainable results is in our DNA. The continuous challenge of seeking leadership in performance has brought us to where we are – and will continue guiding our company towards our objectives. 3. People mean everything to us Everything we do is carried out by people. Talented people who enjoy working in a collaborative atmosphere, based on meritocracy and high performance. 4. The best argument is the one that matters We encourage a challenging work environment, which is open to questioning and constructive discussion. For us, the hierarchy which counts is the hierarchy of the best idea. 5. Simple. Always We believe that simplicity is the best path to efficiency. That’s why we strive not to mistake depth for complexity, and simplicity for simplism. 6. We think and act like owners We always think like business owners, leading by example and putting collective objectives before personal ambition. 7. Ethics are non-negotiable We do what is right, without using shortcuts or devious ways to do business. We exercise leadership in a transparent and responsible way, fully committed to society and the best governance and management practices. page 8Our Way 1. It’s only good for us if it’s good for the client We are people providing service to people, with passion and excellence. We work with the client and for the client – because they are the main reason behind why we do what we do. 2. We’re passionate about performance Generating sustainable results is in our DNA. The continuous challenge of seeking leadership in performance has brought us to where we are – and will continue guiding our company towards our objectives. 3. People mean everything to us Everything we do is carried out by people. Talented people who enjoy working in a collaborative atmosphere, based on meritocracy and high performance. 4. The best argument is the one that matters We encourage a challenging work environment, which is open to questioning and constructive discussion. For us, the hierarchy which counts is the hierarchy of the best idea. 5. Simple. Always We believe that simplicity is the best path to efficiency. That’s why we strive not to mistake depth for complexity, and simplicity for simplism. 6. We think and act like owners We always think like business owners, leading by example and putting collective objectives before personal ambition. 7. Ethics are non-negotiable We do what is right, without using shortcuts or devious ways to do business. We exercise leadership in a transparent and responsible way, fully committed to society and the best governance and management practices. page 8

Medium and Long-Term Strategic Agenda CORPORATE GOVERNANCE AND SUSTAINABILITY PERMEATE ALL EFFORTS ON KEY STRATEGIC OBJECTIVES Commitment to permanently improve corporate governance plays a vital role in protecting stakeholders’ interests. We incorporate sustainability into our strategy through a consolidated governance structure that is integrated with our business, thus making environmental and social issues part of our everyday activities, by incorporating variables on these issues into diverse processes, such as credit granting, investments, insurance activities, contracting of suppliers, and wealth management. We aim at creating a virtuous cycle on the path towards sustainable performance, which can only be met by collaborative work involving our main stakeholders: employees; clients; shareholders and society. TRANSFORMATION CONTINUOUS IMPROVEMENT Risk Management Client Centricity to endeavor our efforts to fully comply with the Risk Appetite to embrace this concept to the fullest in order to always develop products and a “service culture” focused on guidelines. Managing risks is the essence of our activity and a client satisfaction and long-term relationships. responsibility of all employees. Internationalization Digital moving forward in the internationalization process does to speed up our digital transformation process to increase the productivity of IT area and spread a not necessarily mean to take activities to new countries, digital mindset throughout the bank to improve but to reach, in the countries we are present in, the same efficiency, user experience and client satisfaction. management quality and results we have in Brazil. Sustainable Profitability People Management to continuously increase the efficiency of our to improve our incentive model and evaluation tools to contemplate the new dynamics of cooperative operations, having the ability to identify work, making them effective to fairly assess opportunities to reduce costs, managing investments to gain agility, in addition to individual deliveries within efficiently managing capital allocation cross-functional teams. through adequate cost of equity. page 9Medium and Long-Term Strategic Agenda CORPORATE GOVERNANCE AND SUSTAINABILITY PERMEATE ALL EFFORTS ON KEY STRATEGIC OBJECTIVES Commitment to permanently improve corporate governance plays a vital role in protecting stakeholders’ interests. We incorporate sustainability into our strategy through a consolidated governance structure that is integrated with our business, thus making environmental and social issues part of our everyday activities, by incorporating variables on these issues into diverse processes, such as credit granting, investments, insurance activities, contracting of suppliers, and wealth management. We aim at creating a virtuous cycle on the path towards sustainable performance, which can only be met by collaborative work involving our main stakeholders: employees; clients; shareholders and society. TRANSFORMATION CONTINUOUS IMPROVEMENT Risk Management Client Centricity to endeavor our efforts to fully comply with the Risk Appetite to embrace this concept to the fullest in order to always develop products and a “service culture” focused on guidelines. Managing risks is the essence of our activity and a client satisfaction and long-term relationships. responsibility of all employees. Internationalization Digital moving forward in the internationalization process does to speed up our digital transformation process to increase the productivity of IT area and spread a not necessarily mean to take activities to new countries, digital mindset throughout the bank to improve but to reach, in the countries we are present in, the same efficiency, user experience and client satisfaction. management quality and results we have in Brazil. Sustainable Profitability People Management to continuously increase the efficiency of our to improve our incentive model and evaluation tools to contemplate the new dynamics of cooperative operations, having the ability to identify work, making them effective to fairly assess opportunities to reduce costs, managing investments to gain agility, in addition to individual deliveries within efficiently managing capital allocation cross-functional teams. through adequate cost of equity. page 9

Itaú Unibanco Global Footprint Itaú Unibanco has an important presence in key financial centers supported by a unique recognition and reputation. We want to be recognized as: The Latin American Bank CIB London, Lisbon, Madrid, Paris, Frankfurt Institutional Clients / Asset London Private Banking Zurich CIB NY, Cayman, Bahamas Institutional Clients / Asset CIB / Institutional Clients / Asset NY, Cayman Tokyo, Dubai Private Banking Cayman, Bahamas, Miami CIB / Institutional Clients Mexico CIB Brazil, Argentina, Chile, Peru, Colombia, Uruguay, Paraguay, Panama Institutional Clients / Asset Brazil, Argentina, Chile Private Banking Brazil, Chile, Paraguay Retail Banking Brazil, Argentina, Chile, Paraguay, Uruguay, Colombia, Panama page 10Itaú Unibanco Global Footprint Itaú Unibanco has an important presence in key financial centers supported by a unique recognition and reputation. We want to be recognized as: The Latin American Bank CIB London, Lisbon, Madrid, Paris, Frankfurt Institutional Clients / Asset London Private Banking Zurich CIB NY, Cayman, Bahamas Institutional Clients / Asset CIB / Institutional Clients / Asset NY, Cayman Tokyo, Dubai Private Banking Cayman, Bahamas, Miami CIB / Institutional Clients Mexico CIB Brazil, Argentina, Chile, Peru, Colombia, Uruguay, Paraguay, Panama Institutional Clients / Asset Brazil, Argentina, Chile Private Banking Brazil, Chile, Paraguay Retail Banking Brazil, Argentina, Chile, Paraguay, Uruguay, Colombia, Panama page 10

1 A History of Successful Strategic Deals Acquisition of the remaining 50% of: Retail - Brazil Uruguay NACIONAL Acquisition of the Banco Itaú BMG Consignado minority interest of: Casa Moreira Salles Acquisition of a 1924 minority interest in: Unibanco 1995 - 1998 2000 - 2003 2004 - 2007 Merger 2008 2009 - 2018 Itaú 1943 Foundation of Banco Itaú Alliance with: BEG Banco del Buen Ayre (1) Includes mergers, acquisitions, joint-ventures and partnerships. page 111 A History of Successful Strategic Deals Acquisition of the remaining 50% of: Retail - Brazil Uruguay NACIONAL Acquisition of the Banco Itaú BMG Consignado minority interest of: Casa Moreira Salles Acquisition of a 1924 minority interest in: Unibanco 1995 - 1998 2000 - 2003 2004 - 2007 Merger 2008 2009 - 2018 Itaú 1943 Foundation of Banco Itaú Alliance with: BEG Banco del Buen Ayre (1) Includes mergers, acquisitions, joint-ventures and partnerships. page 11

Corporate Governance 2Corporate Governance 2

Corporate Governance at Itaú Unibanco Strengths of our structure Family ownership ensuring a long-term view • • Professional management team • Strong corporate governance • Broad shareholder base (52.88% of our shares in free float) Egydio de Souza Free Float* Moreira Salles Family Non Voting Shares Aranha Family Free Float Foreigners Brazilian 100.00% Total in NYSE investors in B3 33% 28% Cia. E. Johnston de 36.73% ON 63.27% ON 81.37% PN Participações 4.8 bn 18.63% PN 66.03% Total (number of 33.97% Total shares) 39% 50.00% ON 33.47% Total Foreigners in B3 50.00% ON 100.00% PN IUPAR Itaúsa Free Float* 66.53% Total 39.21% ON 7.82% ON 51.71% ON 0.004% PN 99.58% PN 26.32% Total 19.95% Total 52.88% Total Itaú Unibanco Holding S.A. Note: ON = Common Shares; PN = Non-voting Shares; (*) Excluding shares held by majority owners and treasury shares. page 13Corporate Governance at Itaú Unibanco Strengths of our structure Family ownership ensuring a long-term view • • Professional management team • Strong corporate governance • Broad shareholder base (52.88% of our shares in free float) Egydio de Souza Free Float* Moreira Salles Family Non Voting Shares Aranha Family Free Float Foreigners Brazilian 100.00% Total in NYSE investors in B3 33% 28% Cia. E. Johnston de 36.73% ON 63.27% ON 81.37% PN Participações 4.8 bn 18.63% PN 66.03% Total (number of 33.97% Total shares) 39% 50.00% ON 33.47% Total Foreigners in B3 50.00% ON 100.00% PN IUPAR Itaúsa Free Float* 66.53% Total 39.21% ON 7.82% ON 51.71% ON 0.004% PN 99.58% PN 26.32% Total 19.95% Total 52.88% Total Itaú Unibanco Holding S.A. Note: ON = Common Shares; PN = Non-voting Shares; (*) Excluding shares held by majority owners and treasury shares. page 13

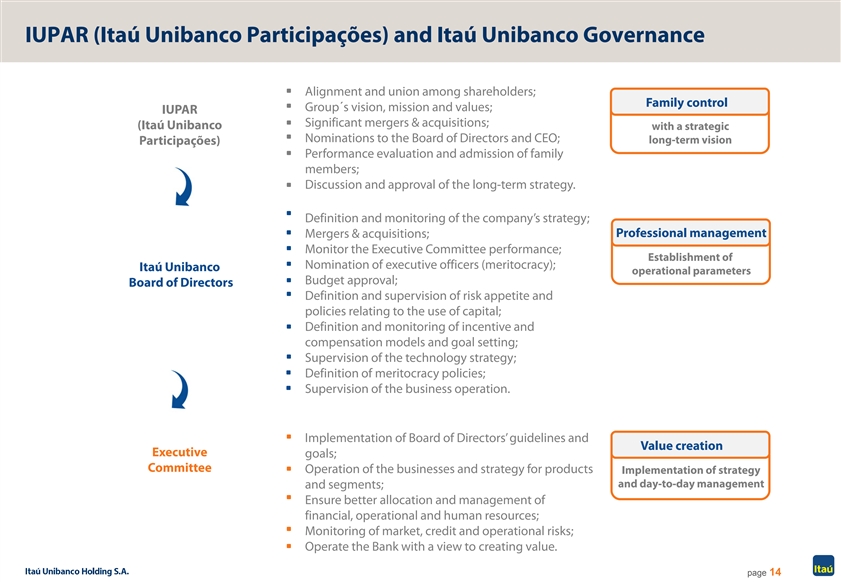

IUPAR (Itaú Unibanco Participações) and Itaú Unibanco Governance Alignment and union among shareholders; Family control Group´s vision, mission and values; IUPAR Significant mergers & acquisitions; (Itaú Unibanco with a strategic Nominations to the Board of Directors and CEO; long-term vision Participações) Performance evaluation and admission of family members; Discussion and approval of the long-term strategy. Definition and monitoring of the company’s strategy; Mergers & acquisitions; Professional management Monitor the Executive Committee performance; Establishment of Nomination of executive officers (meritocracy); Itaú Unibanco operational parameters Budget approval; Board of Directors Definition and supervision of risk appetite and policies relating to the use of capital; Definition and monitoring of incentive and compensation models and goal setting; Supervision of the technology strategy; Definition of meritocracy policies; Supervision of the business operation. Implementation of Board of Directors’ guidelines and Value creation Executive goals; Committee Operation of the businesses and strategy for products Implementation of strategy and day-to-day management and segments; Ensure better allocation and management of financial, operational and human resources; Monitoring of market, credit and operational risks; Operate the Bank with a view to creating value. page 14IUPAR (Itaú Unibanco Participações) and Itaú Unibanco Governance Alignment and union among shareholders; Family control Group´s vision, mission and values; IUPAR Significant mergers & acquisitions; (Itaú Unibanco with a strategic Nominations to the Board of Directors and CEO; long-term vision Participações) Performance evaluation and admission of family members; Discussion and approval of the long-term strategy. Definition and monitoring of the company’s strategy; Mergers & acquisitions; Professional management Monitor the Executive Committee performance; Establishment of Nomination of executive officers (meritocracy); Itaú Unibanco operational parameters Budget approval; Board of Directors Definition and supervision of risk appetite and policies relating to the use of capital; Definition and monitoring of incentive and compensation models and goal setting; Supervision of the technology strategy; Definition of meritocracy policies; Supervision of the business operation. Implementation of Board of Directors’ guidelines and Value creation Executive goals; Committee Operation of the businesses and strategy for products Implementation of strategy and day-to-day management and segments; Ensure better allocation and management of financial, operational and human resources; Monitoring of market, credit and operational risks; Operate the Bank with a view to creating value. page 14

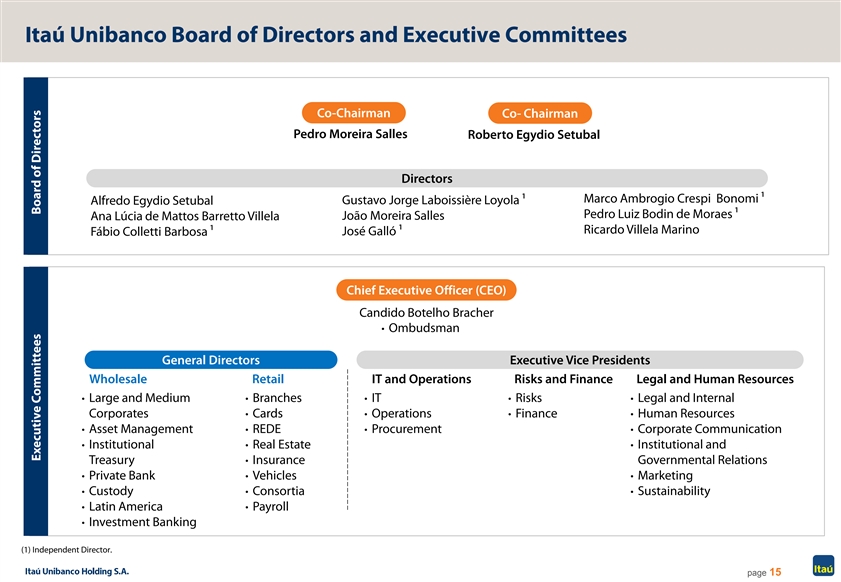

Itaú Unibanco Board of Directors and Executive Committees Co-Chairman Co- Chairman Pedro Moreira Salles Roberto Egydio Setubal . Directors Marco Ambrogio Crespi Bonomi 1 Alfredo Egydio Setubal Gustavo Jorge Laboissière Loyola 1 Pedro Luiz Bodin de Moraes 1 João Moreira Salles Ana Lúcia de Mattos Barretto Villela Ricardo Villela Marino Fábio Colletti Barbosa 1 José Galló 1 Chief Executive Officer (CEO) Candido Botelho Bracher • Ombudsman General Directors Executive Vice Presidents Wholesale Retail IT and Operations Risks and Finance Legal and Human Resources • Large and Medium • Branches • IT • Risks • Legal and Internal Corporates • Cards • Operations • Finance • Human Resources • Asset Management • REDE • Procurement • Corporate Communication • Institutional • Real Estate • Institutional and Treasury • Insurance Governmental Relations • Private Bank • Vehicles • Marketing • Custody • Consortia • Sustainability • Latin America • Payroll • Investment Banking (1) Independent Director. page 15 Executive Committees Board of DirectorsItaú Unibanco Board of Directors and Executive Committees Co-Chairman Co- Chairman Pedro Moreira Salles Roberto Egydio Setubal . Directors Marco Ambrogio Crespi Bonomi 1 Alfredo Egydio Setubal Gustavo Jorge Laboissière Loyola 1 Pedro Luiz Bodin de Moraes 1 João Moreira Salles Ana Lúcia de Mattos Barretto Villela Ricardo Villela Marino Fábio Colletti Barbosa 1 José Galló 1 Chief Executive Officer (CEO) Candido Botelho Bracher • Ombudsman General Directors Executive Vice Presidents Wholesale Retail IT and Operations Risks and Finance Legal and Human Resources • Large and Medium • Branches • IT • Risks • Legal and Internal Corporates • Cards • Operations • Finance • Human Resources • Asset Management • REDE • Procurement • Corporate Communication • Institutional • Real Estate • Institutional and Treasury • Insurance Governmental Relations • Private Bank • Vehicles • Marketing • Custody • Consortia • Sustainability • Latin America • Payroll • Investment Banking (1) Independent Director. page 15 Executive Committees Board of Directors

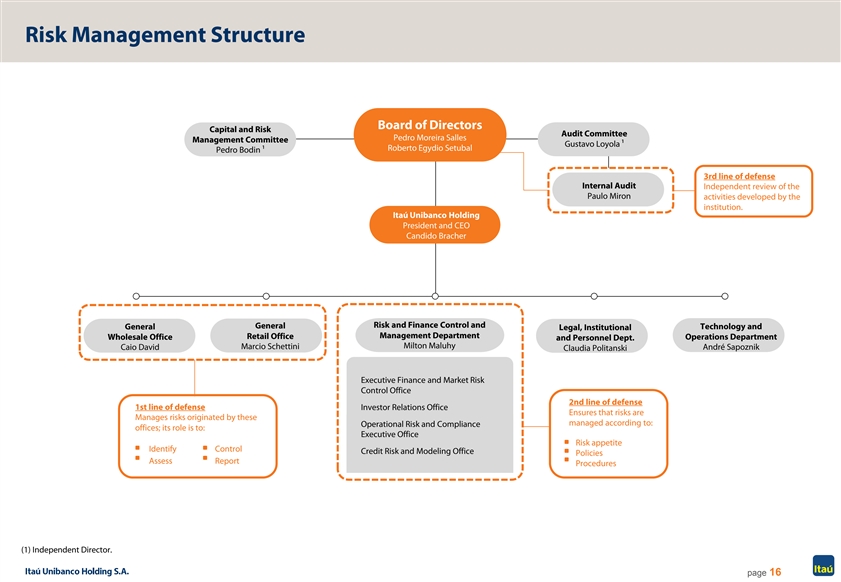

Risk Management Structure Board of Directors Capital and Risk Audit Committee Pedro Moreira Salles Management Committee Gustavo Loyola 1 Roberto Egydio Setubal Pedro Bodin 1 3rd line of defense Internal Audit Independent review of the Paulo Miron activities developed by the institution. Itaú Unibanco Holding President and CEO Candido Bracher Risk and Finance Control and General General Technology and Legal, Institutional Retail Office Management Department Wholesale Office Operations Department and Personnel Dept. Milton Maluhy Marcio Schettini André Sapoznik Caio David Claudia Politanski Executive Finance and Market Risk Control Office 2nd line of defense 1st line of defense Investor Relations Office Ensures that risks are Manages risks originated by these managed according to: Operational Risk and Compliance offices; its role is to: Executive Office Risk appetite Identify Control Credit Risk and Modeling Office Policies Assess Report Procedures (1) Independent Director. page 16Risk Management Structure Board of Directors Capital and Risk Audit Committee Pedro Moreira Salles Management Committee Gustavo Loyola 1 Roberto Egydio Setubal Pedro Bodin 1 3rd line of defense Internal Audit Independent review of the Paulo Miron activities developed by the institution. Itaú Unibanco Holding President and CEO Candido Bracher Risk and Finance Control and General General Technology and Legal, Institutional Retail Office Management Department Wholesale Office Operations Department and Personnel Dept. Milton Maluhy Marcio Schettini André Sapoznik Caio David Claudia Politanski Executive Finance and Market Risk Control Office 2nd line of defense 1st line of defense Investor Relations Office Ensures that risks are Manages risks originated by these managed according to: Operational Risk and Compliance offices; its role is to: Executive Office Risk appetite Identify Control Credit Risk and Modeling Office Policies Assess Report Procedures (1) Independent Director. page 16

Governance Structure at Itaú Unibanco Shareholder’s Meeting Fiscal Council Board of Directors Digital Audit Personnel Related Nomination Risk and Capital Strategy Compensation LATAM Committee Committee Parties and Corporate Management Committee Committee Strategy Advisory Board Committee Governance Committee Council Committee Internal Audit Social Responsibility Independent Committee Audit Board of Officers Disclosure and Trading Committee page 17Governance Structure at Itaú Unibanco Shareholder’s Meeting Fiscal Council Board of Directors Digital Audit Personnel Related Nomination Risk and Capital Strategy Compensation LATAM Committee Committee Parties and Corporate Management Committee Committee Strategy Advisory Board Committee Governance Committee Council Committee Internal Audit Social Responsibility Independent Committee Audit Board of Officers Disclosure and Trading Committee page 17

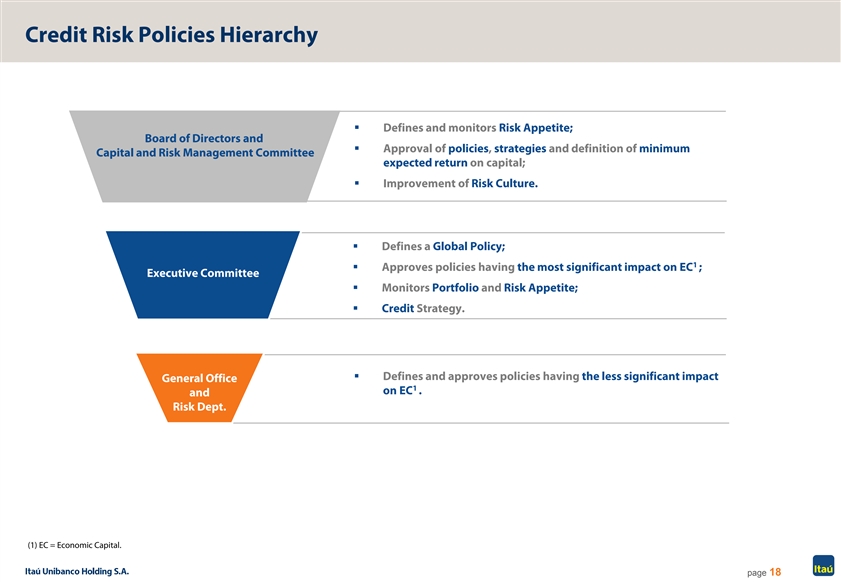

Credit Risk Policies Hierarchy § Defines and monitors Risk Appetite; Board of Directors and § Approval of policies, strategies and definition of minimum Capital and Risk Management Committee expected return on capital; § Improvement of Risk Culture. § Defines a Global Policy; 1 § Approves policies having the most significant impact on EC ; Executive Committee § Monitors Portfolio and Risk Appetite; § Credit Strategy. § Defines and approves policies having the less significant impact General Office 1 on EC . and Risk Dept. (1) EC = Economic Capital. page 18Credit Risk Policies Hierarchy § Defines and monitors Risk Appetite; Board of Directors and § Approval of policies, strategies and definition of minimum Capital and Risk Management Committee expected return on capital; § Improvement of Risk Culture. § Defines a Global Policy; 1 § Approves policies having the most significant impact on EC ; Executive Committee § Monitors Portfolio and Risk Appetite; § Credit Strategy. § Defines and approves policies having the less significant impact General Office 1 on EC . and Risk Dept. (1) EC = Economic Capital. page 18

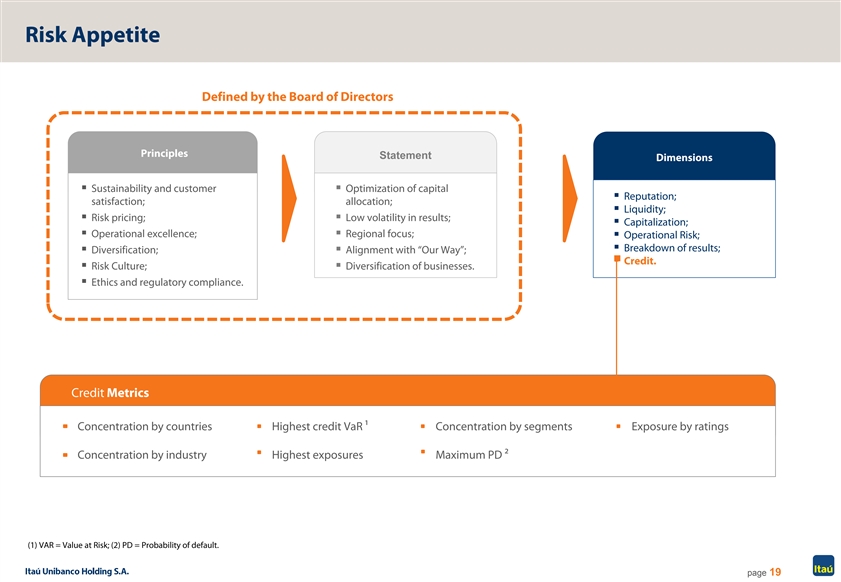

Risk Appetite Defined by the Board of Directors Principles Statement Dimensions § Sustainability and customer § Optimization of capital § Reputation; satisfaction; allocation; § Liquidity; § Risk pricing;§ Low volatility in results; § Capitalization; § Operational excellence;§ Regional focus; § Operational Risk; § Breakdown of results; § Diversification;§ Alignment with “Our Way”; § Credit. § Risk Culture;§ Diversification of businesses. § Ethics and regulatory compliance. Credit Metrics Concentration by countries Highest credit VaR 1 Concentration by segments Exposure by ratings Concentration by industry Highest exposures Maximum PD 2 (1) VAR = Value at Risk; (2) PD = Probability of default. page 19Risk Appetite Defined by the Board of Directors Principles Statement Dimensions § Sustainability and customer § Optimization of capital § Reputation; satisfaction; allocation; § Liquidity; § Risk pricing;§ Low volatility in results; § Capitalization; § Operational excellence;§ Regional focus; § Operational Risk; § Breakdown of results; § Diversification;§ Alignment with “Our Way”; § Credit. § Risk Culture;§ Diversification of businesses. § Ethics and regulatory compliance. Credit Metrics Concentration by countries Highest credit VaR 1 Concentration by segments Exposure by ratings Concentration by industry Highest exposures Maximum PD 2 (1) VAR = Value at Risk; (2) PD = Probability of default. page 19

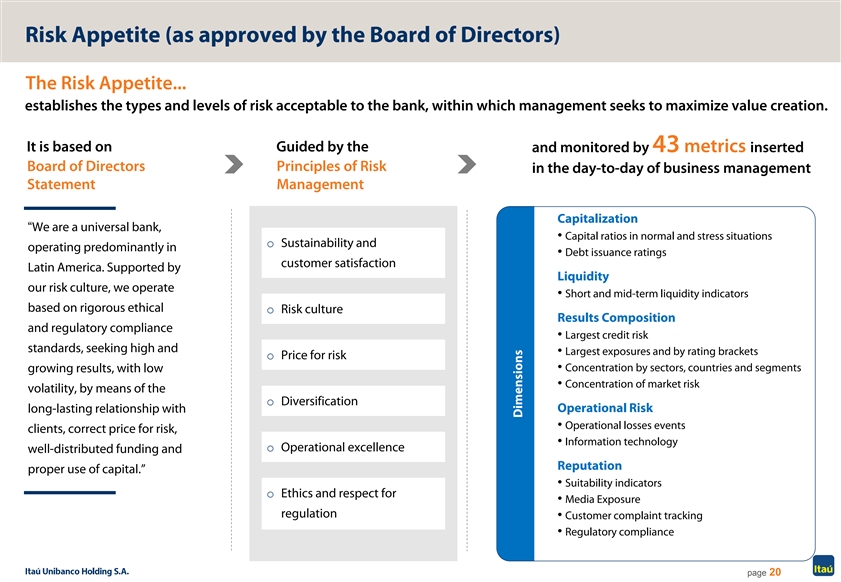

Risk Appetite (as approved by the Board of Directors) The Risk Appetite... establishes the types and levels of risk acceptable to the bank, within which management seeks to maximize value creation. It is based on Guided by the and monitored by 43 metrics inserted Board of Directors Principles of Risk in the day-to-day of business management Statement Management Capitalization “We are a universal bank, • Capital ratios in normal and stress situations o Sustainability and operating predominantly in • Debt issuance ratings customer satisfaction Latin America. Supported by Liquidity our risk culture, we operate • Short and mid-term liquidity indicators based on rigorous ethical o Risk culture Results Composition and regulatory compliance • Largest credit risk standards, seeking high and • Largest exposures and by rating brackets o Price for risk • Concentration by sectors, countries and segments growing results, with low • Concentration of market risk volatility, by means of the o Diversification long-lasting relationship with Operational Risk • Operational losses events clients, correct price for risk, • Information technology o Operational excellence well-distributed funding and Reputation proper use of capital.” • Suitability indicators o Ethics and respect for • Media Exposure regulation • Customer complaint tracking • Regulatory compliance page 20 DimensionsRisk Appetite (as approved by the Board of Directors) The Risk Appetite... establishes the types and levels of risk acceptable to the bank, within which management seeks to maximize value creation. It is based on Guided by the and monitored by 43 metrics inserted Board of Directors Principles of Risk in the day-to-day of business management Statement Management Capitalization “We are a universal bank, • Capital ratios in normal and stress situations o Sustainability and operating predominantly in • Debt issuance ratings customer satisfaction Latin America. Supported by Liquidity our risk culture, we operate • Short and mid-term liquidity indicators based on rigorous ethical o Risk culture Results Composition and regulatory compliance • Largest credit risk standards, seeking high and • Largest exposures and by rating brackets o Price for risk • Concentration by sectors, countries and segments growing results, with low • Concentration of market risk volatility, by means of the o Diversification long-lasting relationship with Operational Risk • Operational losses events clients, correct price for risk, • Information technology o Operational excellence well-distributed funding and Reputation proper use of capital.” • Suitability indicators o Ethics and respect for • Media Exposure regulation • Customer complaint tracking • Regulatory compliance page 20 Dimensions

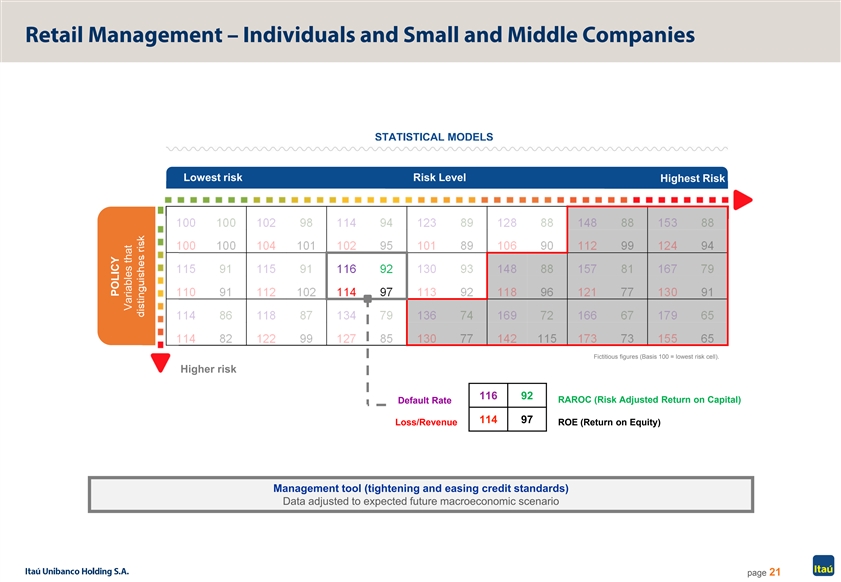

Retail Management – Individuals and Small and Middle Companies STATISTICAL MODELS Lowest risk Risk Level Highest Risk 100 100 102 98 114 94 123 89 128 88 148 88 153 88 100 100 104 101 102 95 101 89 106 90 112 99 124 94 115 91 115 91 116 92 130 93 148 88 157 81 167 79 v 110 91 112 102 114 97 113 92 118 96 121 77 130 91 114 86 118 87 134 79 136 74 169 72 166 67 179 65 114 82 122 99 127 85 130 77 142 115 173 73 155 65 Fictitious figures (Basis 100 = lowest risk cell). Higher risk 116 92 RAROC (Risk Adjusted Return on Capital) Default Rate 114 97 Loss/Revenue ROE (Return on Equity) Management tool (tightening and easing credit standards) Data adjusted to expected future macroeconomic scenario page 21 POLICY Variables that distinguishes riskRetail Management – Individuals and Small and Middle Companies STATISTICAL MODELS Lowest risk Risk Level Highest Risk 100 100 102 98 114 94 123 89 128 88 148 88 153 88 100 100 104 101 102 95 101 89 106 90 112 99 124 94 115 91 115 91 116 92 130 93 148 88 157 81 167 79 v 110 91 112 102 114 97 113 92 118 96 121 77 130 91 114 86 118 87 134 79 136 74 169 72 166 67 179 65 114 82 122 99 127 85 130 77 142 115 173 73 155 65 Fictitious figures (Basis 100 = lowest risk cell). Higher risk 116 92 RAROC (Risk Adjusted Return on Capital) Default Rate 114 97 Loss/Revenue ROE (Return on Equity) Management tool (tightening and easing credit standards) Data adjusted to expected future macroeconomic scenario page 21 POLICY Variables that distinguishes risk

Credit Offer Based on Future Scenario STATISTICAL MODELS Highest Lowest Risk Level risk risk Credit Available Base Scenario Credit Not Available Credit Not Available Highest risk Positive future expectation Negative future expectation Risk Level Risk Level Credit Available Credit Available Credit Not Available Credit Not Available Tightening of credit, maintaining the same Easing of credit, maintaining the same appetite appetite page 22 POLICY POLICYCredit Offer Based on Future Scenario STATISTICAL MODELS Highest Lowest Risk Level risk risk Credit Available Base Scenario Credit Not Available Credit Not Available Highest risk Positive future expectation Negative future expectation Risk Level Risk Level Credit Available Credit Available Credit Not Available Credit Not Available Tightening of credit, maintaining the same Easing of credit, maintaining the same appetite appetite page 22 POLICY POLICY

Business Overview 3Business Overview 3

Universal Bank 1 RETAIL BANKING WHOLESALE BANKING RETAIL AND REAL ESTATE CREDIT ITAÚ BBA 4,413 branches and client service branches and 46,784 ATMs in Brazil; Full coverage of corporate clients with RETAIL annual sales above R$ 200 million; AND REAL Premier banking brand in Brazil; ESTATE Leadership in IB products with top Strategically positioned for growth in mortgage market CREDIT ITAÚ BBA CREDIT positions in major league tables; (partnerships with Lopes). CARD AND (CORPORATE, Treasury operations for the CONSUMER IB AND conglomerate. CREDIT CARD AND CONSUMER FINANCE TREASURY) FINANCE Approximately 33.1 million credit card accounts LATAM and 28.6 million debit card accounts; Purpose: to be recognized as Leader in Brazilian credit card market, extensive “The Latin American Bank”; number of joint ventures and partnerships VEHICLES LATAM Retail presence in Latin America with retailers. (ex-Brazil): Argentina, Chile, Paraguay, Uruguay, VEHICLES Colombia, Panama. Total portfolio for individuals of R$16.6 billion; UNIVERSAL BANK Lease and finance through over 10 thousand dealers. WEALTH MANAGEMENT WEALTH AND SERVICES INSURANCE² MANAGEMENT INSURANCE OPERATIONS SERVICES Total assets under administration One of the largest players in Brazil based of approximately R$1,159 billion; on direct premiums; Leader in Private banking Association with Porto Seguro for auto and residential insurance; SMALL MIDDLE services in Latin America. COMPANY COMPANY 1Q19 net income: R$661 million MIDDLE COMPANY SMALL COMPANY Corporate clients with annual sales Small and Medium Enterprises with annual sales up to R$30 million. from R$30 million to R$200 million. (1) March 31, 2019 figures; (2) Includes Insurance, Pension Plan and Premium Bond operations. page 24Universal Bank 1 RETAIL BANKING WHOLESALE BANKING RETAIL AND REAL ESTATE CREDIT ITAÚ BBA 4,413 branches and client service branches and 46,784 ATMs in Brazil; Full coverage of corporate clients with RETAIL annual sales above R$ 200 million; AND REAL Premier banking brand in Brazil; ESTATE Leadership in IB products with top Strategically positioned for growth in mortgage market CREDIT ITAÚ BBA CREDIT positions in major league tables; (partnerships with Lopes). CARD AND (CORPORATE, Treasury operations for the CONSUMER IB AND conglomerate. CREDIT CARD AND CONSUMER FINANCE TREASURY) FINANCE Approximately 33.1 million credit card accounts LATAM and 28.6 million debit card accounts; Purpose: to be recognized as Leader in Brazilian credit card market, extensive “The Latin American Bank”; number of joint ventures and partnerships VEHICLES LATAM Retail presence in Latin America with retailers. (ex-Brazil): Argentina, Chile, Paraguay, Uruguay, VEHICLES Colombia, Panama. Total portfolio for individuals of R$16.6 billion; UNIVERSAL BANK Lease and finance through over 10 thousand dealers. WEALTH MANAGEMENT WEALTH AND SERVICES INSURANCE² MANAGEMENT INSURANCE OPERATIONS SERVICES Total assets under administration One of the largest players in Brazil based of approximately R$1,159 billion; on direct premiums; Leader in Private banking Association with Porto Seguro for auto and residential insurance; SMALL MIDDLE services in Latin America. COMPANY COMPANY 1Q19 net income: R$661 million MIDDLE COMPANY SMALL COMPANY Corporate clients with annual sales Small and Medium Enterprises with annual sales up to R$30 million. from R$30 million to R$200 million. (1) March 31, 2019 figures; (2) Includes Insurance, Pension Plan and Premium Bond operations. page 24

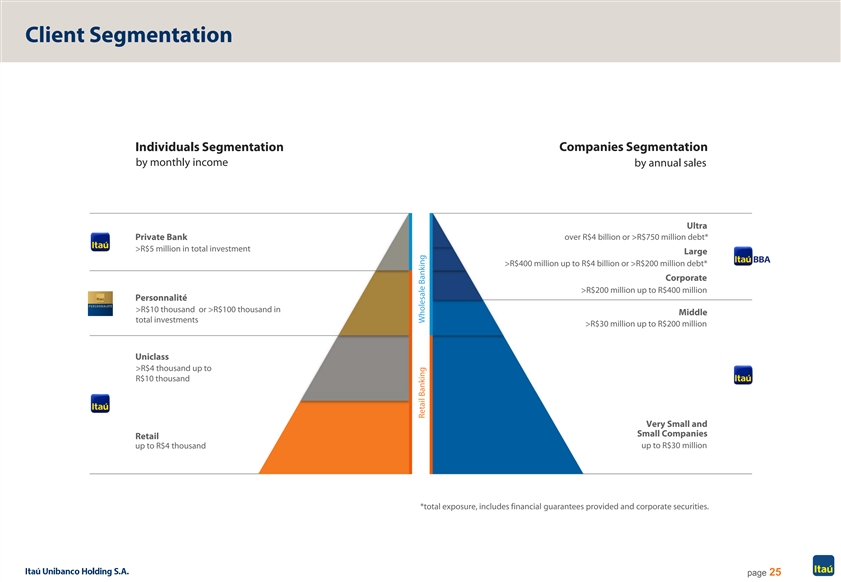

Client Segmentation Individuals Segmentation Companies Segmentation by monthly income by annual sales Ultra Private Bank over R$4 billion or >R$750 million debt* >R$5 million in total investment Large >R$400 million up to R$4 billion or >R$200 million debt* Corporate >R$200 million up to R$400 million Personnalité >R$10 thousand or >R$100 thousand in Middle total investments >R$30 million up to R$200 million Uniclass >R$4 thousand up to R$10 thousand Very Small and Small Companies Retail up to R$4 thousand up to R$30 million *total exposure, includes financial guarantees provided and corporate securities. page 25 Retail Banking Wholesale BankingClient Segmentation Individuals Segmentation Companies Segmentation by monthly income by annual sales Ultra Private Bank over R$4 billion or >R$750 million debt* >R$5 million in total investment Large >R$400 million up to R$4 billion or >R$200 million debt* Corporate >R$200 million up to R$400 million Personnalité >R$10 thousand or >R$100 thousand in Middle total investments >R$30 million up to R$200 million Uniclass >R$4 thousand up to R$10 thousand Very Small and Small Companies Retail up to R$4 thousand up to R$30 million *total exposure, includes financial guarantees provided and corporate securities. page 25 Retail Banking Wholesale Banking

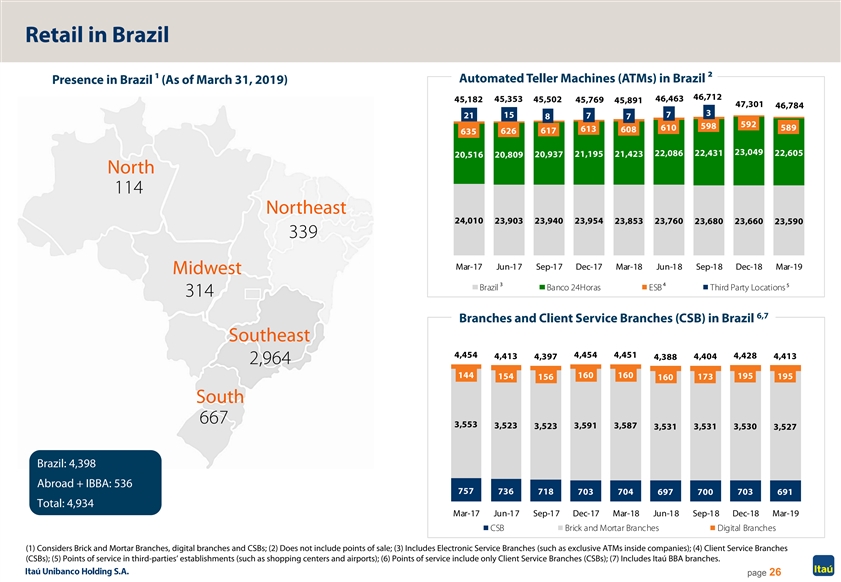

Retail in Brazil Automated Teller Machines (ATMs) in Brazil 2 Presence in Brazil 1 (As of March 31, 2019) 46,712 45,353 46,463 45,182 45,502 45,769 45,891 47,301 46,784 3 15 7 21 7 8 7 592 598 610 589 613 608 626 617 635 23,049 22,086 22,431 22,605 21,195 21,423 20,516 20,809 20,937 North 114 Northeast 24,010 23,903 23,940 23,954 23,853 23,760 23,680 23,660 23,590 339 Mar-17 Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 Midwest 3 4 5 Brazil Banco 24Horas ESB Third Party Locations 314 6,7 Branches and Client Service Branches (CSB) in Brazil Southeast 4,454 4,454 4,451 4,428 4,413 4,397 4,388 4,404 4,413 2,964 144 160 160 195 154 156 173 195 160 South 667 3,553 3,523 3,591 3,587 3,523 3,531 3,531 3,530 3,527 Brazil: 4,398 Abroad + IBBA: 536 757 736 718 703 704 697 700 703 691 Total: 4,934 Mar-17 Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 CSB Brick and Mortar Branches Digital Branches (1) Considers Brick and Mortar Branches, digital branches and CSBs; (2) Does not include points of sale; (3) Includes Electronic Service Branches (such as exclusive ATMs inside companies); (4) Client Service Branches (CSBs); (5) Points of service in third-parties’ establishments (such as shopping centers and airports); (6) Points of service include only Client Service Branches (CSBs); (7) Includes Itaú BBA branches. page 26Retail in Brazil Automated Teller Machines (ATMs) in Brazil 2 Presence in Brazil 1 (As of March 31, 2019) 46,712 45,353 46,463 45,182 45,502 45,769 45,891 47,301 46,784 3 15 7 21 7 8 7 592 598 610 589 613 608 626 617 635 23,049 22,086 22,431 22,605 21,195 21,423 20,516 20,809 20,937 North 114 Northeast 24,010 23,903 23,940 23,954 23,853 23,760 23,680 23,660 23,590 339 Mar-17 Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 Midwest 3 4 5 Brazil Banco 24Horas ESB Third Party Locations 314 6,7 Branches and Client Service Branches (CSB) in Brazil Southeast 4,454 4,454 4,451 4,428 4,413 4,397 4,388 4,404 4,413 2,964 144 160 160 195 154 156 173 195 160 South 667 3,553 3,523 3,591 3,587 3,523 3,531 3,531 3,530 3,527 Brazil: 4,398 Abroad + IBBA: 536 757 736 718 703 704 697 700 703 691 Total: 4,934 Mar-17 Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 CSB Brick and Mortar Branches Digital Branches (1) Considers Brick and Mortar Branches, digital branches and CSBs; (2) Does not include points of sale; (3) Includes Electronic Service Branches (such as exclusive ATMs inside companies); (4) Client Service Branches (CSBs); (5) Points of service in third-parties’ establishments (such as shopping centers and airports); (6) Points of service include only Client Service Branches (CSBs); (7) Includes Itaú BBA branches. page 26

Retail - Credit Cards, Joint Ventures and Partnerships with Retailers in Brazil Highlights Highlights JVs and Partnerships • Brazilian market leader in credit card transactions; • Focus on credit card instruments; • Qualification of the client base: proprietary channel x partnerships; • Long term agreements; • Credit card business comprises: • Alignment of incentives. • Issuance of cards; • Acquiring: REDE; • JVs and partnership with retailers; • Own brand: Hiper; • Approximately 61.7 million card accounts (1Q19): • 33.1 million credit card accounts; • 28.6 million debit card accounts; • R$ 119.5 billion in card transactions (1Q19): • R$ 89.3 billion in credit card transactions; • R$ 30.3 billion in debit card transactions; • High growth potential in credit card usage in Brazil. page 27Retail - Credit Cards, Joint Ventures and Partnerships with Retailers in Brazil Highlights Highlights JVs and Partnerships • Brazilian market leader in credit card transactions; • Focus on credit card instruments; • Qualification of the client base: proprietary channel x partnerships; • Long term agreements; • Credit card business comprises: • Alignment of incentives. • Issuance of cards; • Acquiring: REDE; • JVs and partnership with retailers; • Own brand: Hiper; • Approximately 61.7 million card accounts (1Q19): • 33.1 million credit card accounts; • 28.6 million debit card accounts; • R$ 119.5 billion in card transactions (1Q19): • R$ 89.3 billion in credit card transactions; • R$ 30.3 billion in debit card transactions; • High growth potential in credit card usage in Brazil. page 27

Retail - Cards in Brazil | Growing Penetration in Household Consumption Expenditure Credit and Debit Cards Billed Volume % at Household Consumption Expenditure 38.0% 35.1% 34.9% 34.1% 33.8% 32.4% 32.1% 31.4% 30.8% 14.6% 13.0% 13.3% 12.5% 12.7% 12.1% 12.4% 11.7% 11.6% 23.4% 22.1% 21.6% 21.6% 21.1% 20.3% 19.7% 19.7% 19.2% 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 Credit Card Debit Card Sources: ABECS (Brazilian Credit Card Companies Association) and IBGE (Statistics and Geography Brazilian Institute) brand view in Dec/18. Only the purchase volume is considered in the cards billing. page 28Retail - Cards in Brazil | Growing Penetration in Household Consumption Expenditure Credit and Debit Cards Billed Volume % at Household Consumption Expenditure 38.0% 35.1% 34.9% 34.1% 33.8% 32.4% 32.1% 31.4% 30.8% 14.6% 13.0% 13.3% 12.5% 12.7% 12.1% 12.4% 11.7% 11.6% 23.4% 22.1% 21.6% 21.6% 21.1% 20.3% 19.7% 19.7% 19.2% 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18 Credit Card Debit Card Sources: ABECS (Brazilian Credit Card Companies Association) and IBGE (Statistics and Geography Brazilian Institute) brand view in Dec/18. Only the purchase volume is considered in the cards billing. page 28

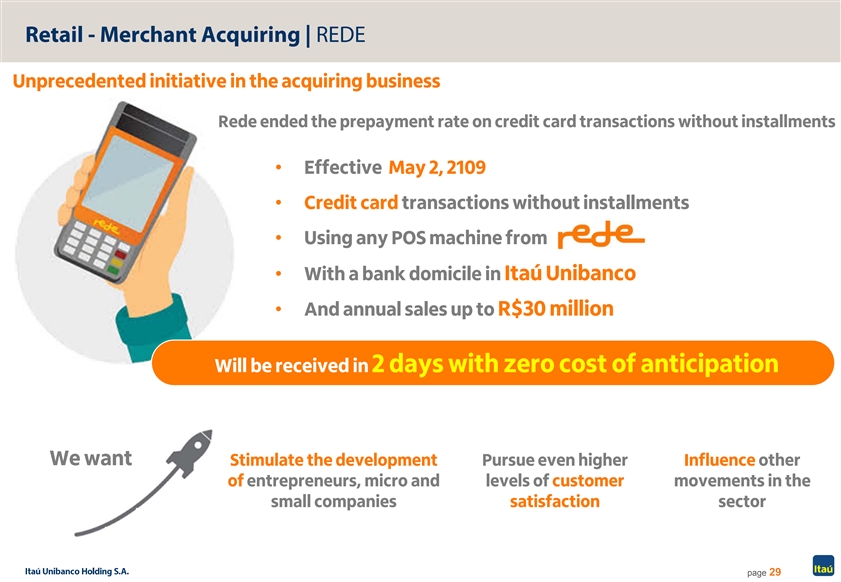

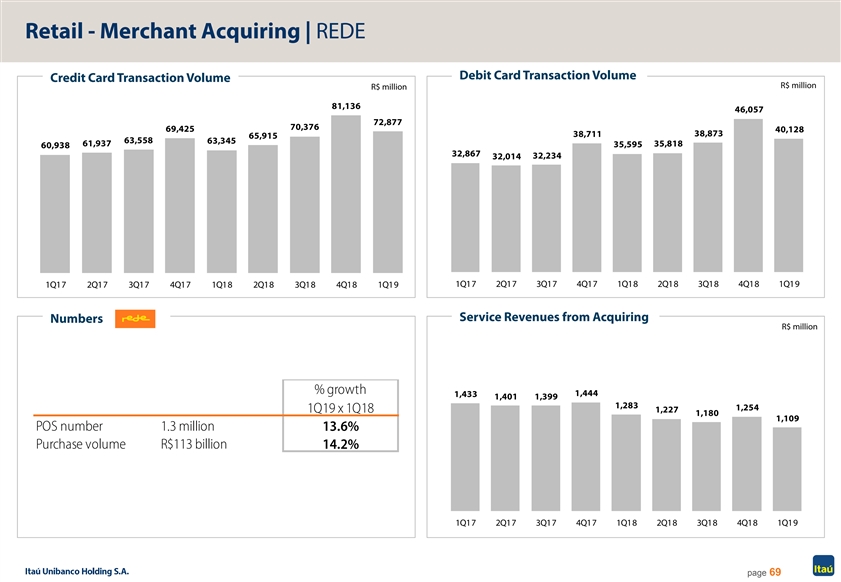

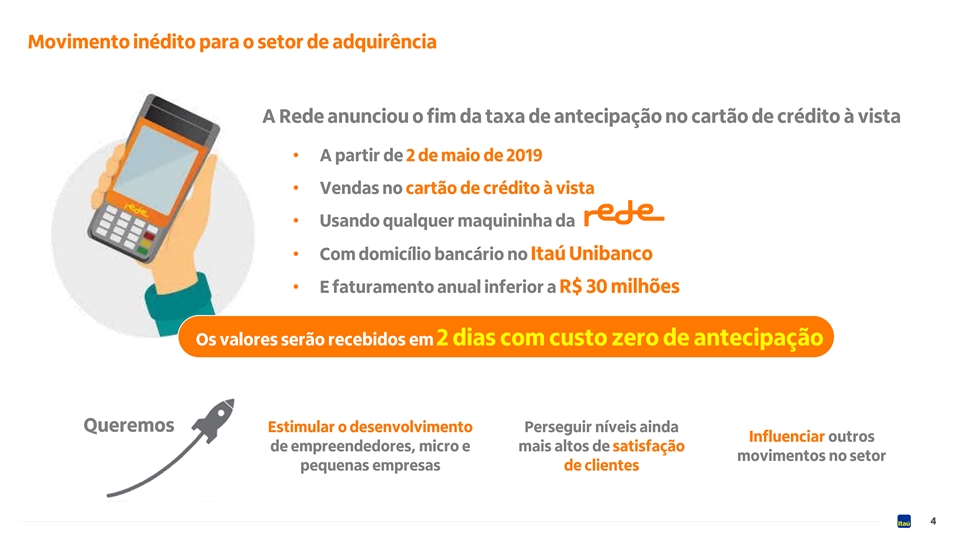

Retail - Merchant Acquiring | REDE Unprecedented initiative in the acquiring business Rede ended the prepayment rate on credit card transactions without installments • Effective May 2, 2109 • Credit card transactions without installments • Using any POS machine from • With a bank domicile in Itaú Unibanco • And annual sales up to R$30 million Will be received in 2 days with zero cost of anticipation We want Stimulate the development Pursue even higher Influence other of entrepreneurs, micro and levels of customer movements in the small companies satisfaction sector page 29Retail - Merchant Acquiring | REDE Unprecedented initiative in the acquiring business Rede ended the prepayment rate on credit card transactions without installments • Effective May 2, 2109 • Credit card transactions without installments • Using any POS machine from • With a bank domicile in Itaú Unibanco • And annual sales up to R$30 million Will be received in 2 days with zero cost of anticipation We want Stimulate the development Pursue even higher Influence other of entrepreneurs, micro and levels of customer movements in the small companies satisfaction sector page 29

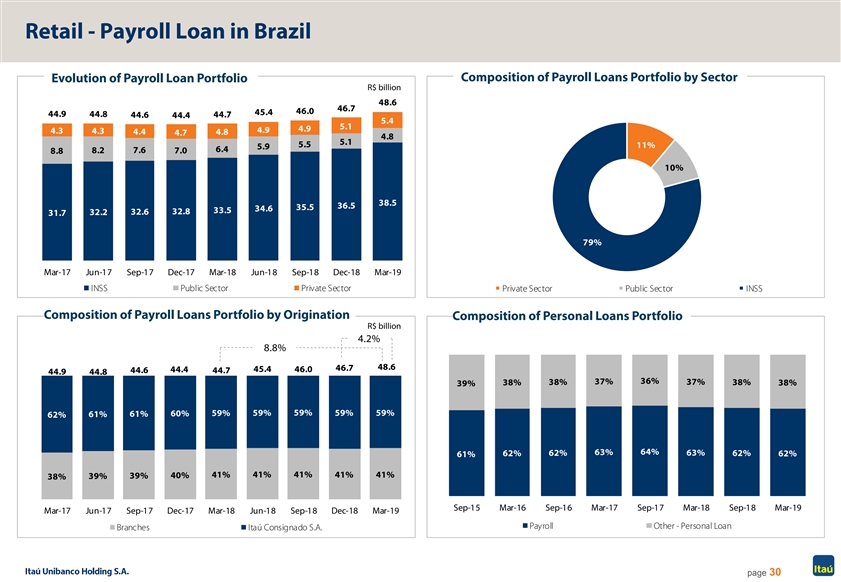

Retail - Payroll Loan in Brazil Composition of Payroll Loans Portfolio by Sector Evolution of Payroll Loan Portfolio R$ billion 48.6 46.7 46.0 45.4 44.9 44.8 44.6 44.4 44.7 5.4 5.1 4.9 4.9 4.3 4.3 4.4 4.8 4.7 4.8 5.1 5.5 11% 5.9 6.4 7.6 8.8 8.2 7.0 10% 38.5 36.5 35.5 34.6 33.5 32.6 32.8 31.7 32.2 79% Mar-17 Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 INSS Public Sector Private Sector Private Sector Public Sector INSS Composition of Payroll Loans Portfolio by Origination Composition of Personal Loans Portfolio R$ billion 4.2% 8.8% 48.6 46.7 44.4 45.4 46.0 44.6 44.7 44.9 44.8 37% 36% 37% 38% 38% 38% 38% 39% 59% 59% 59% 60% 59% 59% 62% 61% 61% 64% 63% 63% 62% 62% 62% 62% 61% 41% 41% 41% 41% 39% 40% 41% 38% 39% Sep-15 Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18 Mar-19 Mar-17 Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 Payroll Other - Personal Loan Branches Itaú Consignado S.A. page 30Retail - Payroll Loan in Brazil Composition of Payroll Loans Portfolio by Sector Evolution of Payroll Loan Portfolio R$ billion 48.6 46.7 46.0 45.4 44.9 44.8 44.6 44.4 44.7 5.4 5.1 4.9 4.9 4.3 4.3 4.4 4.8 4.7 4.8 5.1 5.5 11% 5.9 6.4 7.6 8.8 8.2 7.0 10% 38.5 36.5 35.5 34.6 33.5 32.6 32.8 31.7 32.2 79% Mar-17 Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 INSS Public Sector Private Sector Private Sector Public Sector INSS Composition of Payroll Loans Portfolio by Origination Composition of Personal Loans Portfolio R$ billion 4.2% 8.8% 48.6 46.7 44.4 45.4 46.0 44.6 44.7 44.9 44.8 37% 36% 37% 38% 38% 38% 38% 39% 59% 59% 59% 60% 59% 59% 62% 61% 61% 64% 63% 63% 62% 62% 62% 62% 61% 41% 41% 41% 41% 39% 40% 41% 38% 39% Sep-15 Mar-16 Sep-16 Mar-17 Sep-17 Mar-18 Sep-18 Mar-19 Mar-17 Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 Payroll Other - Personal Loan Branches Itaú Consignado S.A. page 30

Retail - Mortgage Market in Brazil Mortgage Loans Evolution Distribution Channels for Individuals Balance As of March 2019 R$ million 1.7% 47,754 48,337 48,544 Partnerships 13.0% 11.7% 16.3% 13% Real Estate Regular Brokers Branches 30% 11% 88.3% 87.0% 83.7% Developers 15% High Income Branches Mar-18 Dec-18 Mar-19 31% Individuals Companies Collaterals (LTV) Average Ticket and Average Origination Term (Loan to value ratio) 58.4% 58.6% 57.4% 1Q19 40.0% 38.7% 38.8% Average operation period ¹ 320 months Average value of the Property ² R$553 thousand Financing Average Ticket R$325 thousand Mar-18 Dec-18 Mar-19 Vintage (quarterly average) Portfolio (1) Average Operation Period for new developers contracts; (2) Value determined using monthly financing average ticket and quarterly average LTV. Production source: ABECIP. page 31Retail - Mortgage Market in Brazil Mortgage Loans Evolution Distribution Channels for Individuals Balance As of March 2019 R$ million 1.7% 47,754 48,337 48,544 Partnerships 13.0% 11.7% 16.3% 13% Real Estate Regular Brokers Branches 30% 11% 88.3% 87.0% 83.7% Developers 15% High Income Branches Mar-18 Dec-18 Mar-19 31% Individuals Companies Collaterals (LTV) Average Ticket and Average Origination Term (Loan to value ratio) 58.4% 58.6% 57.4% 1Q19 40.0% 38.7% 38.8% Average operation period ¹ 320 months Average value of the Property ² R$553 thousand Financing Average Ticket R$325 thousand Mar-18 Dec-18 Mar-19 Vintage (quarterly average) Portfolio (1) Average Operation Period for new developers contracts; (2) Value determined using monthly financing average ticket and quarterly average LTV. Production source: ABECIP. page 31

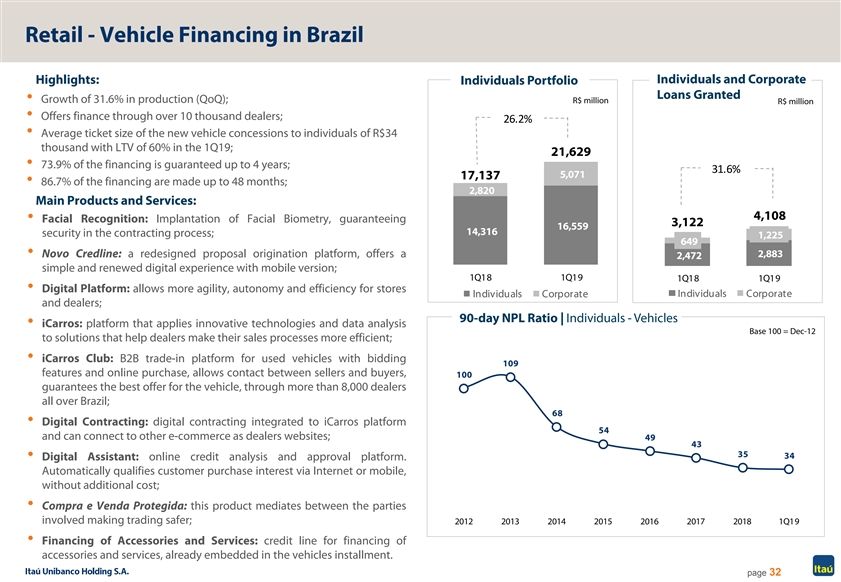

Retail - Vehicle Financing in Brazil Highlights: Individuals and Corporate Individuals Portfolio Loans Granted • Growth of 31.6% in production (QoQ); R$ million R$ million • Offers finance through over 10 thousand dealers; 26.2% • Average ticket size of the new vehicle concessions to individuals of R$34 thousand with LTV of 60% in the 1Q19; 21,629 • 73.9% of the financing is guaranteed up to 4 years; 31.6% 5,071 17,137 • 86.7% of the financing are made up to 48 months; 2,820 Main Products and Services: 4,108 • Facial Recognition: Implantation of Facial Biometry, guaranteeing 3,122 16,559 14,316 security in the contracting process; 1,225 649 • Novo Credline: a redesigned proposal origination platform, offers a 2,883 2,472 simple and renewed digital experience with mobile version; 1Q18 1Q19 1Q18 1Q19 • Digital Platform: allows more agility, autonomy and efficiency for stores Individuals Corporate Individuals Corporate and dealers; 90-day NPL Ratio | Individuals - Vehicles • iCarros: platform that applies innovative technologies and data analysis Base 100 = Dec-12 to solutions that help dealers make their sales processes more efficient; • iCarros Club: B2B trade-in platform for used vehicles with bidding 109 features and online purchase, allows contact between sellers and buyers, 100 guarantees the best offer for the vehicle, through more than 8,000 dealers all over Brazil; 68 • Digital Contracting: digital contracting integrated to iCarros platform 54 and can connect to other e-commerce as dealers websites; 49 43 35 34 • Digital Assistant: online credit analysis and approval platform. Automatically qualifies customer purchase interest via Internet or mobile, without additional cost; • Compra e Venda Protegida: this product mediates between the parties involved making trading safer; 2012 2013 2014 2015 2016 2017 2018 1Q19 • Financing of Accessories and Services: credit line for financing of accessories and services, already embedded in the vehicles installment. page 32Retail - Vehicle Financing in Brazil Highlights: Individuals and Corporate Individuals Portfolio Loans Granted • Growth of 31.6% in production (QoQ); R$ million R$ million • Offers finance through over 10 thousand dealers; 26.2% • Average ticket size of the new vehicle concessions to individuals of R$34 thousand with LTV of 60% in the 1Q19; 21,629 • 73.9% of the financing is guaranteed up to 4 years; 31.6% 5,071 17,137 • 86.7% of the financing are made up to 48 months; 2,820 Main Products and Services: 4,108 • Facial Recognition: Implantation of Facial Biometry, guaranteeing 3,122 16,559 14,316 security in the contracting process; 1,225 649 • Novo Credline: a redesigned proposal origination platform, offers a 2,883 2,472 simple and renewed digital experience with mobile version; 1Q18 1Q19 1Q18 1Q19 • Digital Platform: allows more agility, autonomy and efficiency for stores Individuals Corporate Individuals Corporate and dealers; 90-day NPL Ratio | Individuals - Vehicles • iCarros: platform that applies innovative technologies and data analysis Base 100 = Dec-12 to solutions that help dealers make their sales processes more efficient; • iCarros Club: B2B trade-in platform for used vehicles with bidding 109 features and online purchase, allows contact between sellers and buyers, 100 guarantees the best offer for the vehicle, through more than 8,000 dealers all over Brazil; 68 • Digital Contracting: digital contracting integrated to iCarros platform 54 and can connect to other e-commerce as dealers websites; 49 43 35 34 • Digital Assistant: online credit analysis and approval platform. Automatically qualifies customer purchase interest via Internet or mobile, without additional cost; • Compra e Venda Protegida: this product mediates between the parties involved making trading safer; 2012 2013 2014 2015 2016 2017 2018 1Q19 • Financing of Accessories and Services: credit line for financing of accessories and services, already embedded in the vehicles installment. page 32

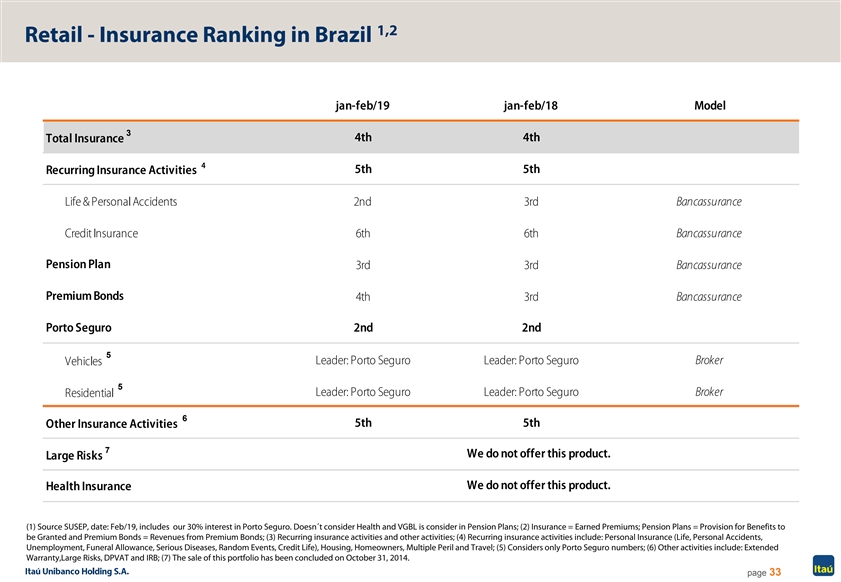

1,2 Retail - Insurance Ranking in Brazil jan-feb/19 jan-feb/18 Model 3 4th 4th Total Insurance 4 5th 5th Recurring Insurance Activities Life & Personal Accidents 2nd 3rd Bancassurance Credit Insurance 6th 6th Bancassurance Pension Plan Bancassurance 3rd 3rd Premium Bonds 4th 3rd Bancassurance Porto Seguro 2nd 2nd 5 Leader: Porto Seguro Leader: Porto Seguro Broker Vehicles 5 Broker Leader: Porto Seguro Leader: Porto Seguro Residential 6 5th 5th Other Insurance Activities 7 We do not offer this product. Large Risks We do not offer this product. Health Insurance (1) Source SUSEP, date: Feb/19, includes our 30% interest in Porto Seguro. Doesn´t consider Health and VGBL is consider in Pension Plans; (2) Insurance = Earned Premiums; Pension Plans = Provision for Benefits to be Granted and Premium Bonds = Revenues from Premium Bonds; (3) Recurring insurance activities and other activities; (4) Recurring insurance activities include: Personal Insurance (Life, Personal Accidents, Unemployment, Funeral Allowance, Serious Diseases, Random Events, Credit Life), Housing, Homeowners, Multiple Peril and Travel; (5) Considers only Porto Seguro numbers; (6) Other activities include: Extended Warranty,Large Risks, DPVAT and IRB; (7) The sale of this portfolio has been concluded on October 31, 2014. page 331,2 Retail - Insurance Ranking in Brazil jan-feb/19 jan-feb/18 Model 3 4th 4th Total Insurance 4 5th 5th Recurring Insurance Activities Life & Personal Accidents 2nd 3rd Bancassurance Credit Insurance 6th 6th Bancassurance Pension Plan Bancassurance 3rd 3rd Premium Bonds 4th 3rd Bancassurance Porto Seguro 2nd 2nd 5 Leader: Porto Seguro Leader: Porto Seguro Broker Vehicles 5 Broker Leader: Porto Seguro Leader: Porto Seguro Residential 6 5th 5th Other Insurance Activities 7 We do not offer this product. Large Risks We do not offer this product. Health Insurance (1) Source SUSEP, date: Feb/19, includes our 30% interest in Porto Seguro. Doesn´t consider Health and VGBL is consider in Pension Plans; (2) Insurance = Earned Premiums; Pension Plans = Provision for Benefits to be Granted and Premium Bonds = Revenues from Premium Bonds; (3) Recurring insurance activities and other activities; (4) Recurring insurance activities include: Personal Insurance (Life, Personal Accidents, Unemployment, Funeral Allowance, Serious Diseases, Random Events, Credit Life), Housing, Homeowners, Multiple Peril and Travel; (5) Considers only Porto Seguro numbers; (6) Other activities include: Extended Warranty,Large Risks, DPVAT and IRB; (7) The sale of this portfolio has been concluded on October 31, 2014. page 33

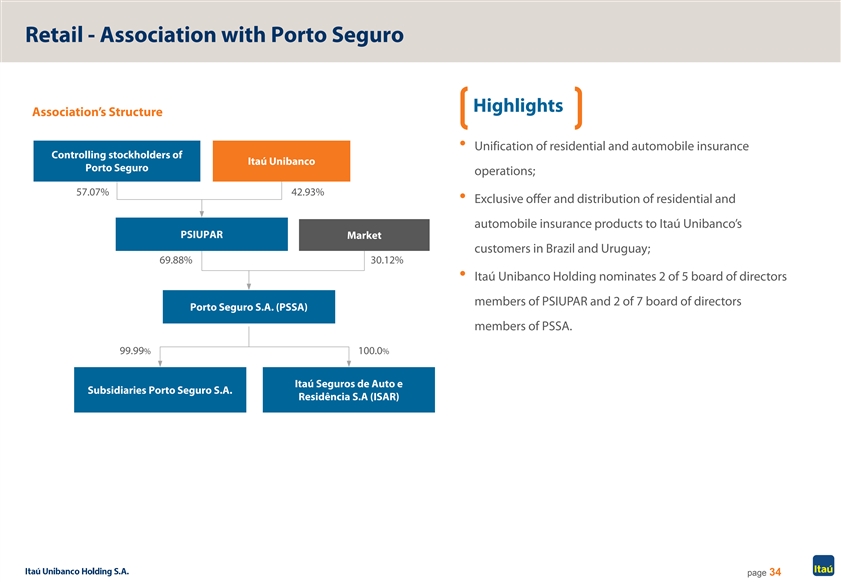

Retail - Association with Porto Seguro Highlights Association’s Structure • Unification of residential and automobile insurance Controlling stockholders of Itaú Unibanco Porto Seguro operations; 57.07% 42.93% • Exclusive offer and distribution of residential and automobile insurance products to Itaú Unibanco’s PSIUPAR Market customers in Brazil and Uruguay; 69.88% 30.12% • Itaú Unibanco Holding nominates 2 of 5 board of directors members of PSIUPAR and 2 of 7 board of directors Porto Seguro S.A. (PSSA) members of PSSA. 99.99% 100.0% Itaú Seguros de Auto e Subsidiaries Porto Seguro S.A. Residência S.A (ISAR) page 34Retail - Association with Porto Seguro Highlights Association’s Structure • Unification of residential and automobile insurance Controlling stockholders of Itaú Unibanco Porto Seguro operations; 57.07% 42.93% • Exclusive offer and distribution of residential and automobile insurance products to Itaú Unibanco’s PSIUPAR Market customers in Brazil and Uruguay; 69.88% 30.12% • Itaú Unibanco Holding nominates 2 of 5 board of directors members of PSIUPAR and 2 of 7 board of directors Porto Seguro S.A. (PSSA) members of PSSA. 99.99% 100.0% Itaú Seguros de Auto e Subsidiaries Porto Seguro S.A. Residência S.A (ISAR) page 34

Very Small, Small and Middle Market in Brazil SMEs Loan Portfolio 1 R$ million 79,649 75,433 74,137 72,002 70,795 68,974 61,869 61,547 2012 2013 2014 2015 2016 2017 2018 1Q19 Highlights Full range of financial products and services, including deposits accounts, investment options, insurance, cash management, credit products and collection, among others. Very Small and Small Market • Clients with annual revenues up to R$30 million. Middle Market • This sub-segment serves approximately 30 thousand clients (economic groups) with annual revenues between R$30 million and R$200 million. • Focus on high-rating clients, and 93% of loans are granted to clients rated B3 or better. (1) Includes financial guarantees provided. page 35Very Small, Small and Middle Market in Brazil SMEs Loan Portfolio 1 R$ million 79,649 75,433 74,137 72,002 70,795 68,974 61,869 61,547 2012 2013 2014 2015 2016 2017 2018 1Q19 Highlights Full range of financial products and services, including deposits accounts, investment options, insurance, cash management, credit products and collection, among others. Very Small and Small Market • Clients with annual revenues up to R$30 million. Middle Market • This sub-segment serves approximately 30 thousand clients (economic groups) with annual revenues between R$30 million and R$200 million. • Focus on high-rating clients, and 93% of loans are granted to clients rated B3 or better. (1) Includes financial guarantees provided. page 35

Wholesale - Corporate Companies in Brazil 1 Corporate Loans R$ million 219,418 213,815 194,472 181,541 165,052 163,437 153,302 152,625 2012 2013 2014 2015 2016 2017 2018 1Q19 Highlights • Corporate clients with annual sales above R$200 million. • We offer a broad portfolio of banking products and services, from cash management to structured operations and transactions in capital markets. • We serve approximately 5,900 large corporate groups and also more than 190 financial institutions. (1) Includes financial guarantees provided. page 36Wholesale - Corporate Companies in Brazil 1 Corporate Loans R$ million 219,418 213,815 194,472 181,541 165,052 163,437 153,302 152,625 2012 2013 2014 2015 2016 2017 2018 1Q19 Highlights • Corporate clients with annual sales above R$200 million. • We offer a broad portfolio of banking products and services, from cash management to structured operations and transactions in capital markets. • We serve approximately 5,900 large corporate groups and also more than 190 financial institutions. (1) Includes financial guarantees provided. page 36

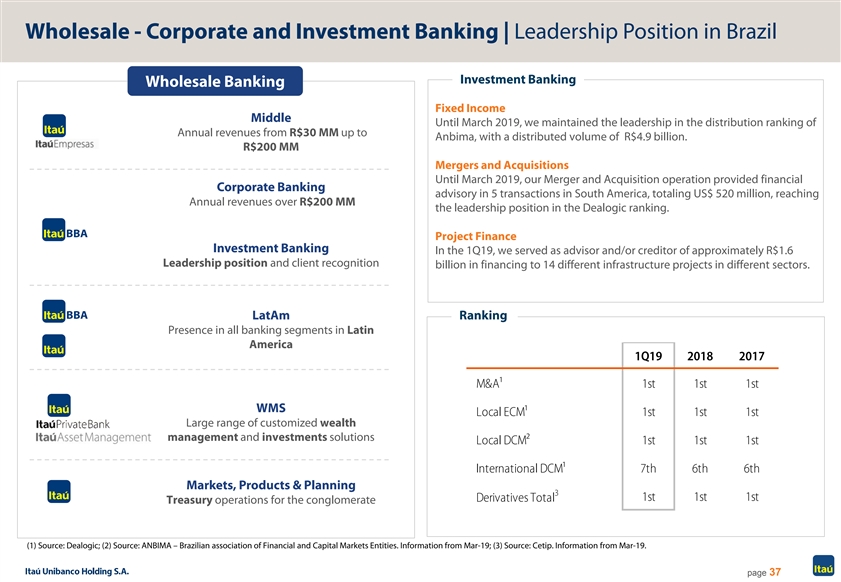

Wholesale - Corporate and Investment Banking | Leadership Position in Brazil Investment Banking Wholesale Banking Fixed Income Middle Until March 2019, we maintained the leadership in the distribution ranking of Annual revenues from R$30 MM up to Anbima, with a distributed volume of R$4.9 billion. R$200 MM Mergers and Acquisitions Until March 2019, our Merger and Acquisition operation provided financial Corporate Banking advisory in 5 transactions in South America, totaling US$ 520 million, reaching Annual revenues over R$200 MM the leadership position in the Dealogic ranking. Project Finance Investment Banking In the 1Q19, we served as advisor and/or creditor of approximately R$1.6 Leadership position and client recognition billion in financing to 14 different infrastructure projects in different sectors. LatAm Ranking Presence in all banking segments in Latin America 1Q19 2018 2017 M&A¹ 1st 1st 1st WMS Local ECM¹ 1st 1st 1st Large range of customized wealth management and investments solutions Local DCM² 1st 1st 1st International DCM¹ 7th 6th 6th Markets, Products & Planning 3 Derivatives Total 1st 1st 1st Treasury operations for the conglomerate (1) Source: Dealogic; (2) Source: ANBIMA – Brazilian association of Financial and Capital Markets Entities. Information from Mar-19; (3) Source: Cetip. Information from Mar-19. page 37Wholesale - Corporate and Investment Banking | Leadership Position in Brazil Investment Banking Wholesale Banking Fixed Income Middle Until March 2019, we maintained the leadership in the distribution ranking of Annual revenues from R$30 MM up to Anbima, with a distributed volume of R$4.9 billion. R$200 MM Mergers and Acquisitions Until March 2019, our Merger and Acquisition operation provided financial Corporate Banking advisory in 5 transactions in South America, totaling US$ 520 million, reaching Annual revenues over R$200 MM the leadership position in the Dealogic ranking. Project Finance Investment Banking In the 1Q19, we served as advisor and/or creditor of approximately R$1.6 Leadership position and client recognition billion in financing to 14 different infrastructure projects in different sectors. LatAm Ranking Presence in all banking segments in Latin America 1Q19 2018 2017 M&A¹ 1st 1st 1st WMS Local ECM¹ 1st 1st 1st Large range of customized wealth management and investments solutions Local DCM² 1st 1st 1st International DCM¹ 7th 6th 6th Markets, Products & Planning 3 Derivatives Total 1st 1st 1st Treasury operations for the conglomerate (1) Source: Dealogic; (2) Source: ANBIMA – Brazilian association of Financial and Capital Markets Entities. Information from Mar-19; (3) Source: Cetip. Information from Mar-19. page 37

Wholesale - Wealth Management Services | Brazil Asset Management Evolution of Assets Under Administration Investment Product management for the conglomerate and a full range of Asset Management investment options to Retail Banking. In March 2019, we reached R$686.51 bi llion in assets under management, 1,135 1,107 accounting for 14.4% of the market. 1,068 1,025 R$ billion 1,002 946 922 883 Kinea 849 It is an independent platform of management of differentiated investments. With R$56.5 billion in assets in March 2019, it operates in the segments of Multi-Markets, Real Estate, Pension Plan and Private Equity, Stock and Infrastructure. Private Banking With a full global wealth management platform, leadership position in Brazil. We have been recognized by the world’s top international Private Banking market publications: Mar-17 Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 Private Banker International • Outstanding Global Private Bank - Latin America, 2018 Securities Services The Banker Local Custody: we ended March with R$1,368 billion under custody • Best Private Bank in Brazil, 2018 (+10.0% from the same period of 2018). International Custody: we ended March with R$284.0 billion under custody (+43.7% from the volume under custody in the same period of 2018). Corporate Solutions: we are leaders in the bookkeeping of shares, providing services to 195 companies listed on B3, representing 58.4% of the total market, and in the bookkeeping of debentures, acting as the bookkeeper of 362 (35.4%) issues. (1) Source: ANBIMA (Brazilian Financial and Capital Markets Association) – March 2019. Considers Itaú Unibanco and Intrag. page 38Wholesale - Wealth Management Services | Brazil Asset Management Evolution of Assets Under Administration Investment Product management for the conglomerate and a full range of Asset Management investment options to Retail Banking. In March 2019, we reached R$686.51 bi llion in assets under management, 1,135 1,107 accounting for 14.4% of the market. 1,068 1,025 R$ billion 1,002 946 922 883 Kinea 849 It is an independent platform of management of differentiated investments. With R$56.5 billion in assets in March 2019, it operates in the segments of Multi-Markets, Real Estate, Pension Plan and Private Equity, Stock and Infrastructure. Private Banking With a full global wealth management platform, leadership position in Brazil. We have been recognized by the world’s top international Private Banking market publications: Mar-17 Jun-17 Sep-17 Dec-17 Mar-18 Jun-18 Sep-18 Dec-18 Mar-19 Private Banker International • Outstanding Global Private Bank - Latin America, 2018 Securities Services The Banker Local Custody: we ended March with R$1,368 billion under custody • Best Private Bank in Brazil, 2018 (+10.0% from the same period of 2018). International Custody: we ended March with R$284.0 billion under custody (+43.7% from the volume under custody in the same period of 2018). Corporate Solutions: we are leaders in the bookkeeping of shares, providing services to 195 companies listed on B3, representing 58.4% of the total market, and in the bookkeeping of debentures, acting as the bookkeeper of 362 (35.4%) issues. (1) Source: ANBIMA (Brazilian Financial and Capital Markets Association) – March 2019. Considers Itaú Unibanco and Intrag. page 38

Retail Footprint in Latin America | March 2019 Mexico | CIB Employees: 8 Panama Colombia1 Employees: 3,484 Branches + CSBs: 163 ATMs: 172 Brazil Employees: 86,204 Peru Branches + CSBs: 4,413 Representative ATMs: 46,784 Office Paraguay Chile Employees: 855 Employees: 5,777 Branches + CSBs: 44 Branches + CSBs: 202 ATMs: 298 ATMs: 463 Non-Bank Correspondents : 59 Uruguay Argentina CIB Employees: 1,104 Employees: 1,688 Retail and Wholesale Branches + CSBs: 27 Branches + CSBs: 85 Points of Service OCA: 35 ATMs: 176 ATMs: 60 (1) Considers employees and branches from Panama. page 39Retail Footprint in Latin America | March 2019 Mexico | CIB Employees: 8 Panama Colombia1 Employees: 3,484 Branches + CSBs: 163 ATMs: 172 Brazil Employees: 86,204 Peru Branches + CSBs: 4,413 Representative ATMs: 46,784 Office Paraguay Chile Employees: 855 Employees: 5,777 Branches + CSBs: 44 Branches + CSBs: 202 ATMs: 298 ATMs: 463 Non-Bank Correspondents : 59 Uruguay Argentina CIB Employees: 1,104 Employees: 1,688 Retail and Wholesale Branches + CSBs: 27 Branches + CSBs: 85 Points of Service OCA: 35 ATMs: 176 ATMs: 60 (1) Considers employees and branches from Panama. page 39

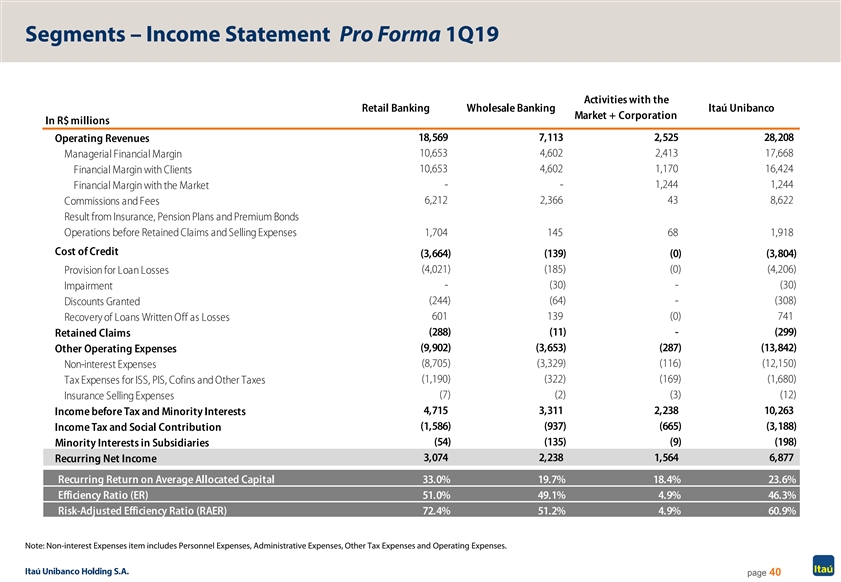

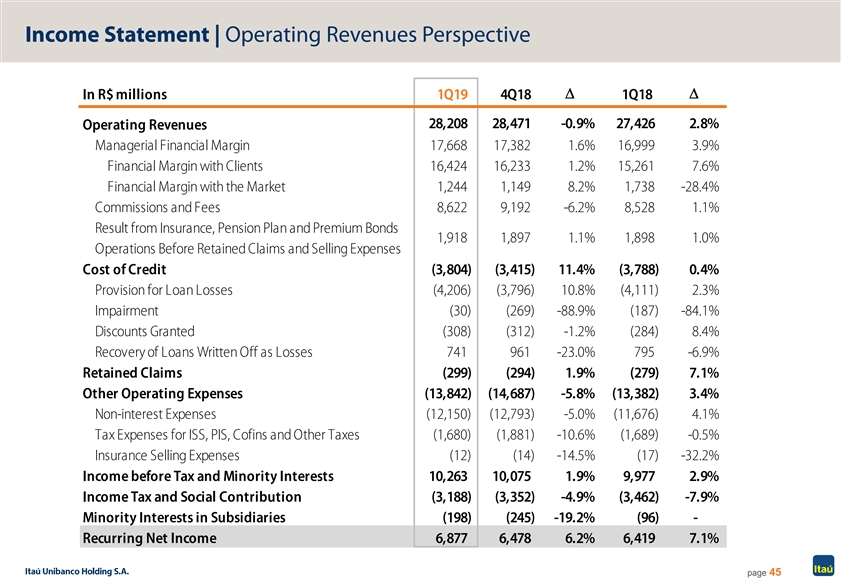

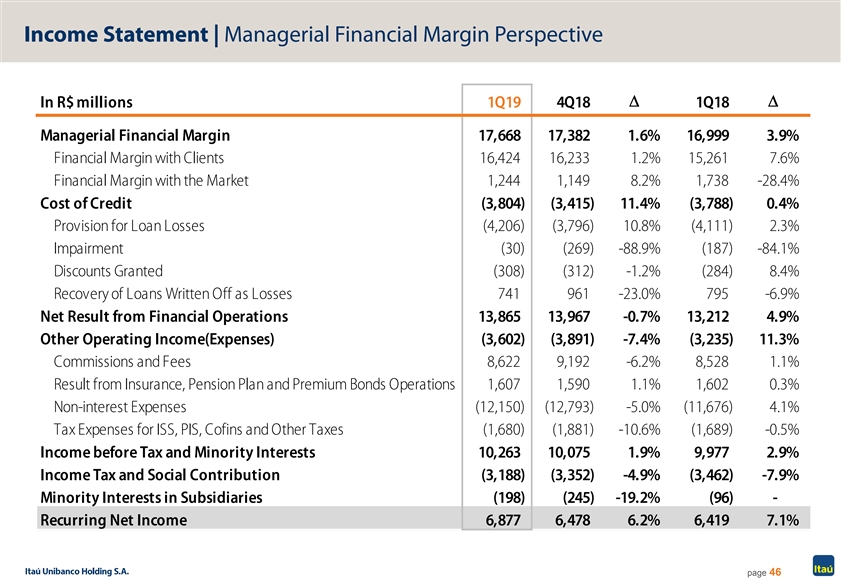

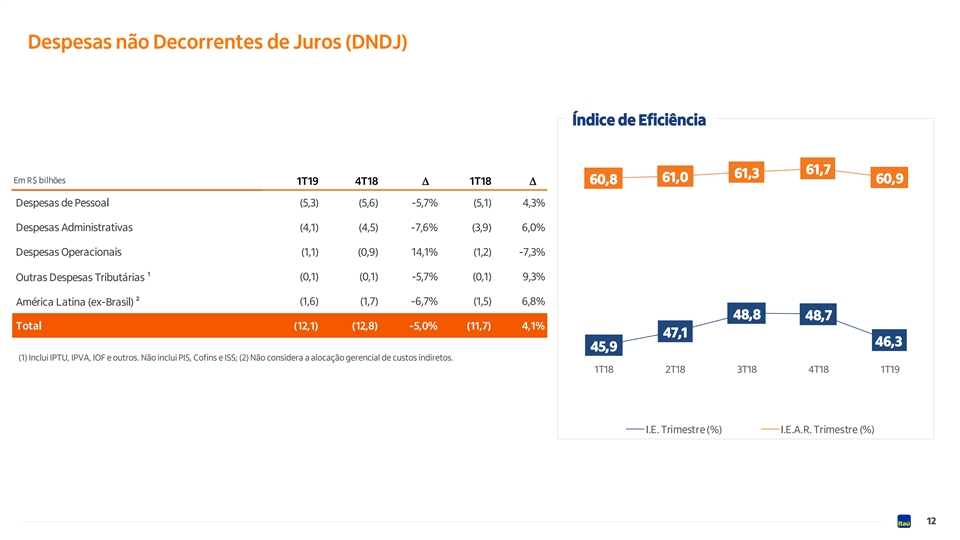

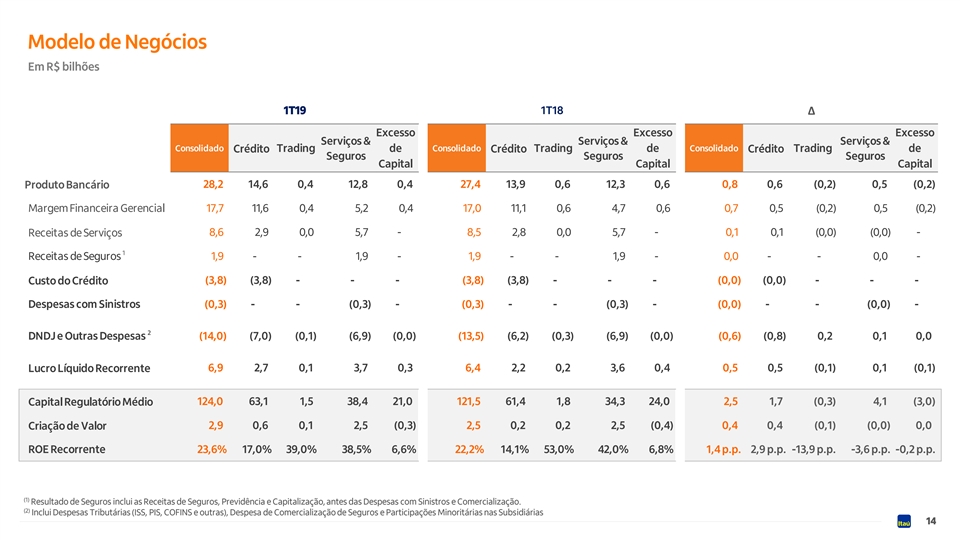

Segments – Income Statement Pro Forma 1Q19 Activities with the Retail Banking Wholesale Banking Itaú Unibanco Market + Corporation In R$ millions 18,569 7,113 2,525 28,208 Operating Revenues 10,653 4,602 2,413 17,668 Managerial Financial Margin 10,653 4,602 1,170 16,424 Financial Margin with Clients - - 1,244 1,244 Financial Margin with the Market 6,212 2,366 43 8,622 Commissions and Fees Result from Insurance, Pension Plans and Premium Bonds Operations before Retained Claims and Selling Expenses 1,704 145 68 1,918 Cost of Credit (3,664) (139) (0) (3,804) (4,021) (185) (0) (4,206) Provision for Loan Losses - (30) - (30) Impairment (244) (64) - (308) Discounts Granted 601 139 (0) 741 Recovery of Loans Written Off as Losses (288) (11) - (299) Retained Claims (9,902) (3,653) (287) (13,842) Other Operating Expenses (8,705) (3,329) (116) (12,150) Non-interest Expenses (1,190) (322) (169) (1,680) Tax Expenses for ISS, PIS, Cofins and Other Taxes (7) (2) (3) (12) Insurance Selling Expenses 4,715 3,311 2,238 10,263 Income before Tax and Minority Interests (1,586) (937) (665) (3,188) Income Tax and Social Contribution (54) (135) (9) (198) Minority Interests in Subsidiaries 3,074 2,238 1,564 6,877 Recurring Net Income Recurring Return on Average Allocated Capital 33.0% 19.7% 18.4% 23.6% Efficiency Ratio (ER) 51.0% 49.1% 4.9% 46.3% Risk-Adjusted Efficiency Ratio (RAER) 72.4% 51.2% 4.9% 60.9% Note: Non-interest Expenses item includes Personnel Expenses, Administrative Expenses, Other Tax Expenses and Operating Expenses. page 40Segments – Income Statement Pro Forma 1Q19 Activities with the Retail Banking Wholesale Banking Itaú Unibanco Market + Corporation In R$ millions 18,569 7,113 2,525 28,208 Operating Revenues 10,653 4,602 2,413 17,668 Managerial Financial Margin 10,653 4,602 1,170 16,424 Financial Margin with Clients - - 1,244 1,244 Financial Margin with the Market 6,212 2,366 43 8,622 Commissions and Fees Result from Insurance, Pension Plans and Premium Bonds Operations before Retained Claims and Selling Expenses 1,704 145 68 1,918 Cost of Credit (3,664) (139) (0) (3,804) (4,021) (185) (0) (4,206) Provision for Loan Losses - (30) - (30) Impairment (244) (64) - (308) Discounts Granted 601 139 (0) 741 Recovery of Loans Written Off as Losses (288) (11) - (299) Retained Claims (9,902) (3,653) (287) (13,842) Other Operating Expenses (8,705) (3,329) (116) (12,150) Non-interest Expenses (1,190) (322) (169) (1,680) Tax Expenses for ISS, PIS, Cofins and Other Taxes (7) (2) (3) (12) Insurance Selling Expenses 4,715 3,311 2,238 10,263 Income before Tax and Minority Interests (1,586) (937) (665) (3,188) Income Tax and Social Contribution (54) (135) (9) (198) Minority Interests in Subsidiaries 3,074 2,238 1,564 6,877 Recurring Net Income Recurring Return on Average Allocated Capital 33.0% 19.7% 18.4% 23.6% Efficiency Ratio (ER) 51.0% 49.1% 4.9% 46.3% Risk-Adjusted Efficiency Ratio (RAER) 72.4% 51.2% 4.9% 60.9% Note: Non-interest Expenses item includes Personnel Expenses, Administrative Expenses, Other Tax Expenses and Operating Expenses. page 40

Financial Highlights 4Financial Highlights 4