Exhibit 99.1

Itaú Unibanco Holding S.A. 2019 Reference Form

Itaú Unibanco Holding S.A. REFERENCE FORM Base Date: 12.31.2019 (in accordance with Attachment 24 to CVM Instruction No. 480 of December 7, 2009 “CVM Instruction No. 480”, as amended) Identification Itaú Unibanco Holding S.A., a corporation enrolled under the National Register of Legal Entities/ Ministry of Finance (CNPJ/MF) under No. 60.872.504/0001-23, with its Articles of Incorporation registered with the Trade Board of the State of São Paulo under NIRE No. 35.3.0001023-0, and registered as a publicly-held company with the Brazilian Securities and Exchange Commission (“CVM”) under No. 19348 (“Bank” or “Issuer”) Head Office The Issuer’s head office is located at Praça Alfredo Egydio de Souza Aranha, 100—Torre Olavo Setubal, in the City and State of São Paulo, CEP 04344-902. Investor Relations Office The Investor Relations department is located at AvenidaEngenheiro Armando de Arruda Pereira, 707—Torre EudoroVillela – Térreo, in the City and State of São Paulo. The Head of Investor Relations is Mr. AlexsandroBroedel. The Investor Relations Department’s telephone number is (0xx11) 2794-3547, fax number is +55 11 5019-8717 ,and email is relacoes.investidores@itau-unibanco.com.br. Independent Auditors Firm PricewaterhouseCoopers AuditoresIndependentes, for the years ended 12/31/2019, 12/31/2018 and 12/31/2017. Bookkeeping Agent Itaú Corretora de Valores S.A. Stockholders Service The Issuer’s stockholders’ service is carried out at the branches of Itaú Unibanco S.A., the head office of which is located at Praça Alfredo Egydio de Souza Aranha, 100 – Torre Olavo Setubal, in the City and State of São Paulo, CEP 04344-902. Newspapers from which the Official Gazette of the State of São Paulo (DiárioOficial do Estado de São Company discloses Paulo) and O Estado de São Paulo newspaper. Information http://www.itau.com.br/relacoes-com-investidores. The information included in the Company’s website is not an integral part of this Reference Form. Website Last update of this Reference Form 08/03/2020

Historical resubmission Version Reasons for resubmission Date of update V2 Update in itens 12.5/6, 12.7/8 and 12.12 07/10/2020 V3 Update in itens 11.1 and 11.2 08/03/2020

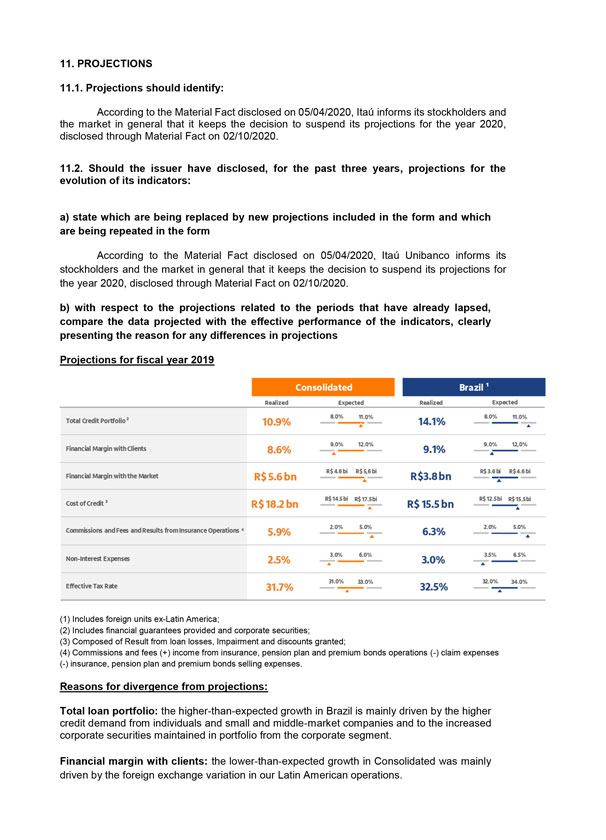

11. PROJECTIONS 11.1. Projections should identify: According to the Material Fact disclosed on 05/04/2020, Itaú informs its stockholders and the market in general that it keeps the decision to suspend its projections for the year 2020, disclosed through Material Fact on 02/10/2020. 11.2. Should the issuer have disclosed, for the past three years, projections for the evolution of its indicators: a) state which are being replaced by new projections included in the form and which are being repeated in the form According to the Material Fact disclosed on 05/04/2020, Itaú Unibanco informs its stockholders and the market in general that it keeps the decision to suspend its projections for the year 2020, disclosed through Material Fact on 02/10/2020. b) with respect to the projections related to the periods that have already lapsed, compare the data projected with the effective performance of the indicators, clearly presenting the reason for any differences in projections Projections for fiscal year 2019 (1) Includes foreign units ex-Latin America; (2) Includes financial guarantees provided and corporate securities; (3) Composed of Result from loan losses, Impairment and discounts granted; (4) Commissions and fees (+) income from insurance, pension plan and premium bonds operations (-) claim expenses (-) insurance, pension plan and premium bonds selling expenses. Reasons for divergence from projections: Total loan portfolio: the higher-than-expected growth in Brazil is mainly driven by the higher credit demand from individuals and small and middle-market companies and to the increased corporate securities maintained in portfolio from the corporate segment. Financial margin with clients: the lower-than-expected growth in Consolidated was mainly driven by the foreign exchange variation in our Latin American operations.

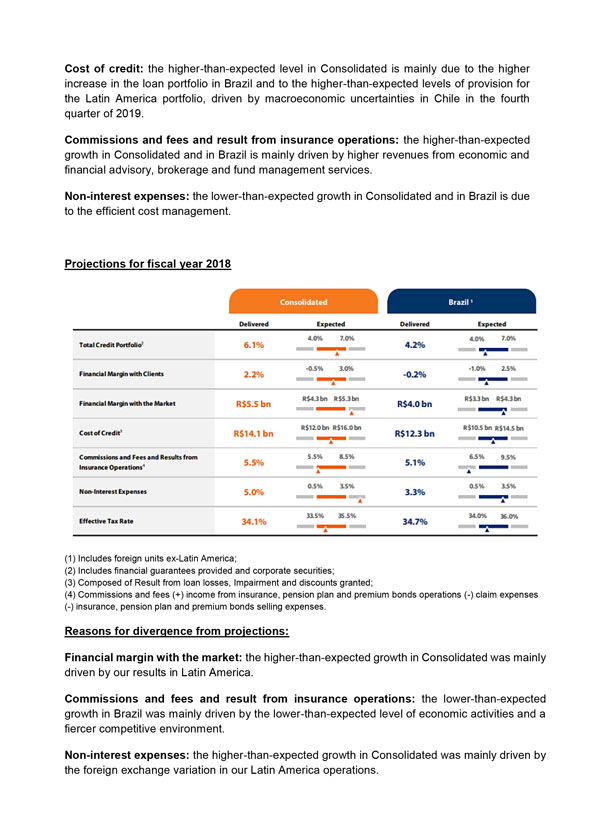

Cost of credit: the higher-than-expected level in Consolidated is mainly due to the higher increase in the loan portfolio in Brazil and to the higher-than-expected levels of provision for the Latin America portfolio, driven by macroeconomic uncertainties in Chile in the fourth quarter of 2019. Commissions and fees and result from insurance operations: the higher-than-expected growth in Consolidated and in Brazil is mainly driven by higher revenues from economic and financial advisory, brokerage and fund management services. Non-interest expenses: the lower-than-expected growth in Consolidated and in Brazil is due to the efficient cost management. Projections for fiscal year 2018 (1) Includes foreign units ex-Latin America; (2) Includes financial guarantees provided and corporate securities; (3) Composed of Result from loan losses, Impairment and discounts granted; (4) Commissions and fees (+) income from insurance, pension plan and premium bonds operations (-) claim expenses (-) insurance, pension plan and premium bonds selling expenses. Reasons for divergence from projections: Financial margin with the market: the higher-than-expected growth in Consolidated was mainly driven by our results in Latin America. Commissions and fees and result from insurance operations: the lower-than-expected growth in Brazil was mainly driven by the lower-than-expected level of economic activities and a fiercer competitive environment. Non-interest expenses: the higher-than-expected growth in Consolidated was mainly driven by the foreign exchange variation in our Latin America operations.

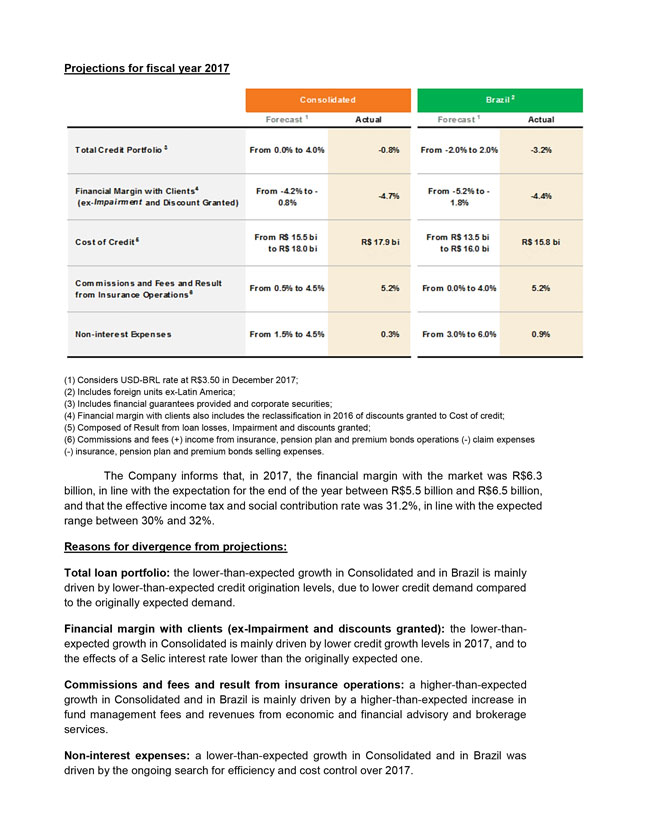

Projections for fiscal year 2017 (1) Considers USD-BRL rate at R$3.50 in December 2017; (2) Includes foreign units ex-Latin America; (3) Includes financial guarantees provided and corporate securities; (4) Financial margin with clients also includes the reclassification in 2016 of discounts granted to Cost of credit; (5) Composed of Result from loan losses, Impairment and discounts granted; (6) Commissions and fees (+) income from insurance, pension plan and premium bonds operations (-) claim expenses (-) insurance, pension plan and premium bonds selling expenses. The Company informs that, in 2017, the financial margin with the market was R$6.3 billion, in line with the expectation for the end of the year between R$5.5 billion and R$6.5 billion, and that the effective income tax and social contribution rate was 31.2%, in line with the expected range between 30% and 32%. Reasons for divergence from projections: Total loan portfolio: the lower-than-expected growth in Consolidated and in Brazil is mainly driven by lower-than-expected credit origination levels, due to lower credit demand compared to the originally expected demand. Financial margin with clients (ex-Impairment and discounts granted): the lower-than-expected growth in Consolidated is mainly driven by lower credit growth levels in 2017, and to the effects of a Selic interest rate lower than the originally expected one. Commissions and fees and result from insurance operations: a higher-than-expected growth in Consolidated and in Brazil is mainly driven by a higher-than-expected increase in fund management fees and revenues from economic and financial advisory and brokerage services. Non-interest expenses: a lower-than-expected growth in Consolidated and in Brazil was driven by the ongoing search for efficiency and cost control over 2017.

c) with respect to the projections related to current periods, state whether the projections are still valid on the date the form is submitted and, when applicable, explain why they were abandoned or replaced According to the Material Fact disclosed on 05/04/2020, Itaú Unibanco informs its stockholders and the market in general that it keeps the decision to suspend its projections for the year 2020, disclosed through Material Fact on 02/10/2020. The decision to suspend the projections is due to the low visibility of the extent and depth of the effects of the current crisis brought by the COVID-19 pandemic. Management understands that it is prudent not to disclose new forecast at this time, until it is possible to estimate the impacts and extent of the current situation in the Company’s operations more accurately. Itaú Unibanco reiterates its commitment to transparency towards its stakeholders and, as the Company has been doing since the beginning of the crisis generated by the COVID-19 pandemic, will keep its shareholders and the market informed about its initiatives and the effects of the crisis on its operation.