Exhibit 99.2

REPRESENTATION LETTER

The entities that are required to be included in the consolidated financial statements of affiliates in accordance with the “Criteria Governing Preparation of Affiliation Reports, Consolidated Business Reports and Consolidated Financial Statements of Affiliated Enterprises” for the year ended December 31, 2019 are all the same as those included in the consolidated financial statements of Chunghwa Telecom Co., Ltd. and its subsidiaries prepared in conformity with the International Financial Reporting Standard 10 “Consolidated Financial Statements”. Relevant information that should be disclosed in the consolidated financial statements of affiliates is included in the consolidated financial statements of Chunghwa Telecom Co., Ltd. and its subsidiaries. Hence, we do not prepare a separate set of consolidated financial statements of affiliates.

Very truly yours,

CHUNGHWA TELECOM CO., LTD.

By

/s/Chi-Mau Sheih |

| Chi-Mau Sheih |

| Chairman |

February 26, 2020

- 1 -

INDEPENDENT AUDITORS’ REPORT

The Board of Directors and Stockholders

Chunghwa Telecom Co., Ltd.

Opinion

We have audited the accompanying consolidated financial statements of Chunghwa Telecom Co., Ltd. and its subsidiaries (the Company), which comprise the consolidated balance sheets as of December 31, 2019 and 2018, and the consolidated statements of comprehensive income, changes in equity and cash flows for the years then ended, and the related notes to the consolidated financial statements, including a summary of significant accounting policies.

In our opinion, the accompanying consolidated financial statements present fairly, in all material respects, the consolidated financial position of the Company as of December 31, 2019 and 2018, and its consolidated financial performance and its consolidated cash flows for the years then ended in accordance with the Regulations Governing the Preparation of Financial Reports by Securities Issuers and International Financial Reporting Standards (IFRS), International Accounting Standards (IAS), IFRIC Interpretations (IFRIC), and SIC Interpretations (SIC) endorsed and issued into effect by the Financial Supervisory Commission of the Republic of China.

Basis for Opinion

We conducted our audits in accordance with the Regulations Governing Auditing and Attestation of Financial Statements by Certified Public Accountants and auditing standards generally accepted in the Republic of China. Our responsibilities under those standards are further described in the Auditors’ Responsibilities for the Audit of the Consolidated Financial Statements section of our report. We are independent of the Company in accordance with The Norm of Professional Ethics for Certified Public Accountant of the Republic of China, and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Key Audit Matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the consolidated financial statements for the year ended December 31, 2019. These matters were addressed in the context of our audit of the consolidated financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

- 2 -

The descriptions of the key audit matters of the consolidated financial statements for the year ended December 31, 2019 are as follows:

Revenue Recognition on Mobile Service

Key audit matter:

Refer to Notes 3 and 28 to the consolidated financial statements.

The Company’s mobile service revenue consists of subscriber-based charges made up of a significant volume oflow-dollar transactions. Because of the complexity and a variety of subscriber-based charges as well as a large number of transactions, the Company uses highly automated systems to process and record its revenue transactions.

Given the Company’s systems to process and record revenue are highly automated, auditing revenue was complex and challenging due to the extent of audit effort required and involvement of professionals with expertise in information technology (IT) necessary for us to identify, test, and evaluate the Company’s IT systems.

Corresponding audit procedures:

Our audit procedures related to the Company’s systems to process revenue transactions included the following, among others:

| • | With the assistance of our IT specialists, we: |

| • | Identified the significant systems used to process revenue transactions and tested the general IT controls over each of these systems, including testing of user access controls and change management controls. |

| • | Performed testing of system interface controls and automated controls within the relevant revenue streams, as well as the controls designed to ensure the accuracy and completeness of revenue. |

| • | We tested internal controls within the relevant revenue business processes, including those in place to reconcile the various systems to the Company’s accounting system. |

| • | We selected samples from mobile service revenue and agreed to customer contracts and records of cash receipts. |

Revenue Recognition on Project Business

Key audit matter:

Refer to Notes 3 and 4 to the consolidated financial statements.

The Company’s project business is highly customized and mainly provides customers with combinations of various equipment and/or services. Project business contracts may likely outsource partial or substantial part of the obligations or services to third parties. The accounting for these contracts requires judgement, particularly as it relates to the determination of the Company acting as a principal or an agent.

Given the judgments on whether the Company is acting as a principal or an agent is required in order to determine if revenue should be recognized gross as principal versus net as agent, auditing such revenue required extensive audit effort due to the volume of contracts and involved a high degree of judgment when performing audit procedures and evaluating the result of these procedures.

- 3 -

Corresponding audit procedures:

Our audit procedures related to management’s revenue recognition on project business included the following, among others:

| • | We tested the effectiveness of controls over project business revenue, including those over principal-versus-agent considerations and revenue recognition. |

| • | We performed the following audit procedures on a sample basis: |

| • | Obtained project business contracts and the evaluation documentation prepared by management and determined the reasonableness of management’s judgement on whether the Company is acting as a principal or an agent after considering whether the Company is the primary obligation provider, its exposures to inventory risks and the discretion in establishing the prices by reviewing the contractual terms, comparing to the business substance and evaluating if it is consistent with relevant accounting standards. |

| • | Performed detail transaction testing by agreeing the amounts recognized to source documents and testing the mathematical accuracy of the recorded revenue. |

| • | Confirmed project business contract terms with customers. |

Emphasis of Matter

As disclosed in Note 5 to the consolidated financial statements, the Company initially applied IFRS 16 “Leases” in 2019. Our audit opinion is not modified in respect of this matter.

Other Matter

We have also audited the parent company only financial statements of Chunghwa Telecom Co., Ltd. as of and for the years ended December 31, 2019 and 2018 on which we have issued an unmodified opinion with emphasis of matter.

Responsibilities of Management and Those Charged with Governance for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of the consolidated financial statements in accordance with the Regulations Governing the Preparation of Financial Reports by Securities Issuers and IFRS, IAS, IFRIC, and SIC endorsed and issued into effect by the Financial Supervisory Commission of the Republic of China, and for such internal control as management determines is necessary to enable the preparation of the consolidated financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the consolidated financial statements, management is responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do so.

Those charged with governance, including the audit committee, are responsible for overseeing the Company’s financial reporting process.

Auditors’ Responsibilities for the Audit of the Consolidated Financial Statements

Our objectives are to obtain reasonable assurance about whether the consolidated financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditors’ report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with the auditing standards generally accepted in the Republic of China will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these consolidated financial statements.

- 4 -

As part of an audit in accordance with the auditing standards generally accepted in the Republic of China, we exercise professional judgment and maintain professional skepticism throughout the audit. We also:

| 1. | Identify and assess the risks of material misstatement of the consolidated financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control. |

| 2. | Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control. |

| 3. | Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management. |

| 4. | Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Company’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditors’ report to the related disclosures in the consolidated financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditors’ report. However, future events or conditions may cause the Company to cease to continue as a going concern. |

| 5. | Evaluate the overall presentation, structure and content of the consolidated financial statements, including the disclosures, and whether the consolidated financial statements represent the underlying transactions and events in a manner that achieves fair presentation. |

| 6. | Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business activities within the Company to express an opinion on the consolidated financial statements. We are responsible for the direction, supervision, and performance of the group audit. We remain solely responsible for our audit opinion. |

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

We also provide those charged with governance with a statement that we have complied with relevant ethical requirements regarding independence, and to communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with those charged with governance, we determine those matters that were of most significance in the audit of the consolidated financial statements for the year ended December 31, 2019 and are therefore the key audit matters. We describe these matters in our auditors’ report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

- 5 -

The engagement partners on the audit resulting in this independent auditors’ report are Mr. Dien Sheng Chang and Mr. Ching Pin Shih.

/s/ Dien Sheng Chang | /s/ Ching Pin Shih | |||||

| Deloitte & Touche | ||||||

| Taipei, Taiwan | ||||||

| Republic of China | ||||||

February 26, 2020

Notice to Readers

The accompanying consolidated financial statements are intended only to present the consolidated financial position, financial performance and cash flows in accordance with accounting principles and practices generally accepted in the Republic of China and not those of any other jurisdictions. The standards, procedures and practices to audit such consolidated financial statements are those generally applied in the Republic of China.

For the convenience of readers, the independent auditors’ report and the accompanying consolidated financial statements have been translated into English from the original Chinese version prepared and used in the Republic of China. If there is any conflict between the English version and the original Chinese version or any difference in the interpretation of the two versions, the Chinese-language independent auditors’ report and consolidated financial statements shall prevail.

- 6 -

CHUNGHWA TELECOM CO., LTD. AND SUBSIDIARIES

CONSOLIDATED BALANCE SHEETS

DECEMBER 31, 2019 AND 2018

(In Thousands of New Taiwan Dollars)

| 2019 | 2018 | |||||||||||||||

| Amount | % | Amount | % | |||||||||||||

ASSETS | ||||||||||||||||

CURRENT ASSETS | ||||||||||||||||

Cash and cash equivalents (Notes 3 and 6) | $ | 34,049,643 | 7 | $ | 27,644,780 | 6 | ||||||||||

Financial assets at fair value through profit or loss (Notes 3, 4 and 7) | 516 | — | — | — | ||||||||||||

Hedging financial assets (Notes 3 and 20) | 327 | — | 1,069 | — | ||||||||||||

Contract assets (Notes 3 and 28) | 4,441,196 | 1 | 4,868,728 | 1 | ||||||||||||

Trade notes and accounts receivable, net (Notes 3, 4, 9 and 28) | 26,407,783 | 6 | 30,075,503 | 7 | ||||||||||||

Receivables from related parties (Note 36) | 16,834 | — | 24,270 | — | ||||||||||||

Inventories (Notes 3, 4, 10 and 37) | 17,344,276 | 4 | 15,120,715 | 3 | ||||||||||||

Prepayments (Notes 5, 11 and 36) | 1,883,259 | — | 1,872,984 | — | ||||||||||||

Other current monetary assets (Notes 12 and 26) | 7,498,564 | 2 | 9,504,203 | 2 | ||||||||||||

Other current assets (Notes 19, 30 and 37) | 2,429,664 | — | 2,576,084 | 1 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total current assets | 94,072,062 | 20 | 91,688,336 | 20 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

NONCURRENT ASSETS | ||||||||||||||||

Financial assets at fair value through profit or loss (Notes 3, 4 and 7) | 778,105 | — | 517,362 | — | ||||||||||||

Financial assets at fair value through other comprehensive income (Notes 3, 4 and 8) | 7,268,917 | 2 | 6,932,503 | 2 | ||||||||||||

Investments accounted for using equity method (Notes 3 and 14) | 7,354,226 | 2 | 2,944,890 | 1 | ||||||||||||

Contract assets (Notes 3 and 28) | 2,600,913 | — | 2,343,958 | — | ||||||||||||

Property, plant and equipment (Notes 3, 4, 5, 15, 36 and 37) | 283,694,215 | 59 | 288,914,228 | 61 | ||||||||||||

Right-of-use assets (Notes 3, 4, 5 and 16) | 11,364,249 | 2 | — | — | ||||||||||||

Investment properties (Notes 3, 4 and 17) | 8,169,393 | 2 | 8,287,212 | 2 | ||||||||||||

Intangible assets (Notes 3, 4 and 18) | 47,046,525 | 10 | 50,943,682 | 11 | ||||||||||||

Deferred income tax assets (Notes 3, 5 and 30) | 3,258,607 | 1 | 3,553,856 | 1 | ||||||||||||

Incremental costs of obtaining contracts (Notes 3 and 28) | 942,652 | — | 1,335,030 | — | ||||||||||||

Net defined benefit assets (Notes 3, 4 and 26) | 2,127,335 | — | 1,164,088 | — | ||||||||||||

Prepayments (Notes 5, 11 and 36) | 2,679,335 | 1 | 3,463,337 | 1 | ||||||||||||

Other noncurrent assets (Notes 19 and 37) | 6,101,704 | 1 | 5,180,222 | 1 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total noncurrent assets | 383,386,176 | 80 | 375,580,368 | 80 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

TOTAL | $ | 477,458,238 | 100 | $ | 467,268,704 | 100 | ||||||||||

|

|

|

|

|

|

|

| |||||||||

LIABILITIES AND EQUITY | ||||||||||||||||

CURRENT LIABILITIES | ||||||||||||||||

Short-term loans (Note 21) | $ | 90,000 | — | $ | 100,000 | — | ||||||||||

Financial liabilities at fair value through profit or loss (Notes 3, 4 and 7) | 239 | — | 1,114 | — | ||||||||||||

Contract liabilities (Notes 3, 5 and 28) | 16,839,830 | 4 | 10,687,772 | 2 | ||||||||||||

Trade notes and accounts payable (Note 23) | 15,312,274 | 3 | 20,464,792 | 5 | ||||||||||||

Payables to related parties (Note 36) | 653,983 | — | 917,951 | — | ||||||||||||

Current tax liabilities (Notes 3 and 30) | 4,020,670 | 1 | 4,390,203 | 1 | ||||||||||||

Lease liabilities (Notes 3, 4, 5, 16,33 and 36) | 3,291,330 | 1 | — | — | ||||||||||||

Other payables (Notes 5 and 24) | 22,952,488 | 5 | 23,315,383 | 5 | ||||||||||||

Provisions (Notes 3 and 25) | 206,942 | — | 128,200 | — | ||||||||||||

Other current liabilities (Note 5) | 983,789 | — | 1,381,606 | — | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total current liabilities | 64,351,545 | 14 | 61,387,021 | 13 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

NONCURRENT LIABILITIES | ||||||||||||||||

Contract liabilities (Notes 3, 5 and 28) | 6,841,485 | 2 | 2,595,149 | 1 | ||||||||||||

Long-term loans (Notes 22 and 37) | 1,600,000 | — | 1,600,000 | — | ||||||||||||

Deferred income tax liabilities (Notes 3, 5 and 30) | 1,912,305 | — | 1,991,843 | — | ||||||||||||

Provisions (Notes 3 and 25) | 97,382 | — | 78,627 | — | ||||||||||||

Lease liabilities (Notes 3, 4, 5, 16, 33 and 36) | 6,466,808 | 1 | — | — | ||||||||||||

Customers’ deposits (Note 36) | 4,747,644 | 1 | 4,716,571 | 1 | ||||||||||||

Net defined benefit liabilities (Notes 3, 4 and 26) | 3,504,617 | 1 | 3,533,936 | 1 | ||||||||||||

Other noncurrent liabilities (Note 5) | 1,542,687 | — | 4,793,237 | 1 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total noncurrent liabilities | 26,712,928 | 5 | 19,309,363 | 4 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total liabilities | 91,064,473 | 19 | 80,696,384 | 17 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

EQUITY ATTRIBUTABLE TO STOCKHOLDERS OF THE PARENT (Notes 5, 13 and 27) | ||||||||||||||||

Common stocks | 77,574,465 | 16 | 77,574,465 | 17 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Additionalpaid-in capital | 171,255,985 | 36 | 171,136,764 | 36 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Retained earnings | ||||||||||||||||

Legal reserve | 77,574,465 | 16 | 77,574,465 | 17 | ||||||||||||

Special reserve | 2,675,419 | 1 | 2,675,419 | 1 | ||||||||||||

Unappropriated earnings | 46,341,361 | 10 | 47,141,345 | 10 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total retained earnings | 126,591,245 | 27 | 127,391,229 | 28 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Other adjustments | 688,548 | — | 459,914 | — | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total equity attributable to stockholders of the parent | 376,110,243 | 79 | 376,562,372 | 81 | ||||||||||||

NONCONTROLLING INTERESTS (Notes 5, 13 and 27) | 10,283,522 | 2 | 10,009,948 | 2 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total equity | 386,393,765 | 81 | 386,572,320 | 83 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

TOTAL | $ | 477,458,238 | 100 | $ | 467,268,704 | 100 | ||||||||||

|

|

|

|

|

|

|

| |||||||||

The accompanying notes are an integral part of the consolidated financial statements.

- 7 -

CHUNGHWA TELECOM CO., LTD. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

YEARS ENDED DECEMBER 31, 2019 AND 2018

(In Thousands of New Taiwan Dollars, Except Earnings Per Share)

| 2019 | 2018 | |||||||||||||||

| Amount | % | Amount | % | |||||||||||||

REVENUES (Notes 3, 28, 36 and 41) | $ | 207,520,061 | 100 | $ | 215,483,158 | 100 | ||||||||||

OPERATING COSTS (Notes 3, 10, 26, 28, 29, 36 and 41) | 135,952,540 | 65 | 139,545,457 | 65 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

GROSS PROFIT | 71,567,521 | 35 | 75,937,701 | 35 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

OPERATING EXPENSES (Notes 3, 9, 26, 29, 36 and 41) | ||||||||||||||||

Marketing | 22,219,688 | 11 | 23,170,024 | 11 | ||||||||||||

General and administrative | 4,758,340 | 2 | 4,589,488 | 2 | ||||||||||||

Research and development | 3,941,446 | 2 | 3,725,249 | 2 | ||||||||||||

Expected credit loss (reversal of credit loss) | (125,111 | ) | — | 919,732 | — | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Total operating expenses | 30,794,363 | 15 | 32,404,493 | 15 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

OTHER INCOME AND EXPENSES (Notes 15, 17, 18, 29 and 41) | (127,304 | ) | — | 110,451 | — | |||||||||||

|

|

|

|

|

|

|

| |||||||||

INCOME FROM OPERATIONS | 40,645,854 | 20 | 43,643,659 | 20 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

NON-OPERATING INCOME AND EXPENSES | ||||||||||||||||

Interest income (Note 41) | 250,787 | — | 196,889 | — | ||||||||||||

Other income (Notes 8, 29 and 36) | 531,624 | — | 699,823 | — | ||||||||||||

Other gains and losses (Notes 14, 29, 35 and 36) | (36,471 | ) | — | (45,671 | ) | — | ||||||||||

Interest expenses (Notes 16, 29, 36 and 41) | (104,142 | ) | — | (17,596 | ) | — | ||||||||||

Share of profits of associates accounted for using equity method (Notes 14 and 41) | 462,140 | — | 501,600 | — | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Totalnon-operating income and expenses | 1,103,938 | — | 1,335,045 | — | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

INCOME BEFORE INCOME TAX | 41,749,792 | 20 | 44,978,704 | 20 | ||||||||||||

INCOME TAX EXPENSE (Notes 3 and 30) | 7,985,849 | 4 | 8,522,533 | 4 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

NET INCOME | 33,763,943 | 16 | 36,456,171 | 16 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

TOTAL OTHER COMPREHENSIVE INCOME (LOSS) | ||||||||||||||||

Items that will not be reclassified to profit or loss: | ||||||||||||||||

Remeasurements of defined benefit pension plans (Note 26) | 1,526,353 | 1 | (1,214,552 | ) | — | |||||||||||

(Continued)

- 8 -

CHUNGHWA TELECOM CO., LTD. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

YEARS ENDED DECEMBER 31, 2019 AND 2018

(In Thousands of New Taiwan Dollars, Except Earnings Per Share)

| 2019 | 2018 | |||||||||||||||

| Amount | % | Amount | % | |||||||||||||

Unrealized gain or loss on investments in equity instruments at fair value through other comprehensive income (Notes 3 and 35) | $ | 286,408 | — | $ | (346,330 | ) | — | |||||||||

Gain or loss on hedging instruments subject to basis adjustment (Notes 3 and 20) | (742 | ) | — | 1,919 | — | |||||||||||

Share of remeasurements of defined benefit pension plans of associates (Note 14) | (2,335 | ) | — | 1,707 | — | |||||||||||

Income tax relating to items that will not be reclassified to profit or loss (Note 30) | (305,271 | ) | — | 450,166 | — | |||||||||||

|

|

|

|

|

|

|

| |||||||||

| 1,504,413 | 1 | (1,107,090 | ) | — | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Items that may be reclassified subsequently to profit or loss: | ||||||||||||||||

Exchange differences arising from the translation of the foreign operations | (61,207 | ) | — | 89,319 | — | |||||||||||

Share of exchange differences arising from the translation of the foreign operations of associates (Note 14) | (700 | ) | — | 3,318 | — | |||||||||||

|

|

|

|

|

|

|

| |||||||||

| (61,907 | ) | — | 92,637 | — | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total other comprehensive income (loss), net of income tax | 1,442,506 | 1 | (1,014,453 | ) | — | |||||||||||

|

|

|

|

|

|

|

| |||||||||

TOTAL COMPREHENSIVE INCOME | $ | 35,206,449 | 17 | $ | 35,441,718 | 16 | ||||||||||

|

|

|

|

|

|

|

| |||||||||

NET INCOME ATTRIBUTABLE TO | ||||||||||||||||

Stockholders of the parent | $ | 32,788,546 | 16 | $ | 35,501,622 | 16 | ||||||||||

Noncontrolling interests | 975,397 | — | 954,549 | — | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| $ | 33,763,943 | 16 | $ | 36,456,171 | 16 | |||||||||||

|

|

|

|

|

|

|

| |||||||||

COMPREHENSIVE INCOME ATTRIBUTABLE TO | ||||||||||||||||

Stockholders of the parent | $ | 34,225,076 | 17 | $ | 34,496,742 | 16 | ||||||||||

Noncontrolling interests | 981,373 | — | 944,976 | — | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| $ | 35,206,449 | 17 | $ | 35,441,718 | 16 | |||||||||||

|

|

|

|

|

|

|

| |||||||||

EARNINGS PER SHARE (Note 31) | ||||||||||||||||

Basic | $ | 4.23 | $ | 4.58 | ||||||||||||

|

|

|

| |||||||||||||

Diluted | $ | 4.22 | $ | 4.57 | ||||||||||||

|

|

|

| |||||||||||||

The accompanying notes are an integral part of the consolidated financial statements.

| (Concluded) |

- 9 -

CHUNGHWA TELECOM CO., LTD. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

YEARS ENDED DECEMBER 31, 2019 AND 2018

(In Thousands of New Taiwan Dollars)

| Equity Attributable to Stockholders of the Parent (Notes 13, 20 and 27) | ||||||||||||||||||||||||||||||||||||||||||||

| Other Adjustments | ||||||||||||||||||||||||||||||||||||||||||||

Exchange Arising from the Translation of | Unrealized Gain Through Other Comprehensive | Gain or Loss on Hedging | Noncontrolling Interests | |||||||||||||||||||||||||||||||||||||||||

Additional | Retained Earnings | |||||||||||||||||||||||||||||||||||||||||||

| Common Stocks | Legal Reserve | Special Reserve | Unappropriated Earnings | Total | Total Equity | |||||||||||||||||||||||||||||||||||||||

BALANCE, JANUARY 1, 2018 | $ | 77,574,465 | $ | 169,466,883 | $ | 77,574,465 | $ | 2,680,823 | $ | 49,595,850 | $ | (174,593 | ) | $ | 883,420 | $ | (850 | ) | $ | 377,600,463 | $ | 8,693,650 | $ | 386,294,113 | ||||||||||||||||||||

Appropriation of 2017 earnings | ||||||||||||||||||||||||||||||||||||||||||||

Reversal of special reserve | — | — | — | (5,404 | ) | 5,404 | — | — | — | — | — | — | ||||||||||||||||||||||||||||||||

Cash dividends distributed by Chunghwa | — | — | — | — | (37,204,714 | ) | — | — | — | (37,204,714 | ) | — | (37,204,714 | ) | ||||||||||||||||||||||||||||||

Cash dividends distributed by subsidiaries | — | — | — | — | — | — | — | — | — | (958,446 | ) | (958,446 | ) | |||||||||||||||||||||||||||||||

Unclaimed dividend | — | 2,455 | — | — | — | — | — | — | 2,455 | — | 2,455 | |||||||||||||||||||||||||||||||||

Change in additionalpaid-in capital from investments in associates accounted for using equity method | — | (1,044 | ) | — | — | — | — | — | — | (1,044 | ) | 191 | (853 | ) | ||||||||||||||||||||||||||||||

Partial disposal of interests in subsidiaries | — | 826,047 | — | — | — | — | — | — | 826,047 | 348,353 | 1,174,400 | |||||||||||||||||||||||||||||||||

Change in additionalpaid-in capital for not participating proportionately in the capital increase of subsidiaries | — | 776,713 | — | — | — | — | — | — | 776,713 | 699,967 | 1,476,680 | |||||||||||||||||||||||||||||||||

Net income for the year ended December 31, 2018 | — | — | — | — | 35,501,622 | — | — | — | 35,501,622 | 954,549 | 36,456,171 | |||||||||||||||||||||||||||||||||

Other comprehensive income (loss) for the year ended December 31, 2018 | — | — | — | — | (756,817 | ) | 95,166 | (345,148 | ) | 1,919 | (1,004,880 | ) | (9,573 | ) | (1,014,453 | ) | ||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||

Total comprehensive income (loss) for the year ended December 31, 2018 | — | — | — | — | 34,744,805 | 95,166 | (345,148 | ) | 1,919 | 34,496,742 | 944,976 | 35,441,718 | ||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||

Share-based payment transactions of subsidiaries | — | 10,776 | — | — | — | — | — | — | 10,776 | 41,863 | 52,639 | |||||||||||||||||||||||||||||||||

Net increase in noncontrolling interests | — | 54,934 | — | — | — | — | — | — | 54,934 | 239,394 | 294,328 | |||||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||

BALANCE, DECEMBER 31, 2018 | 77,574,465 | 171,136,764 | 77,574,465 | 2,675,419 | 47,141,345 | (79,427 | ) | 538,272 | 1,069 | 376,562,372 | 10,009,948 | 386,572,320 | ||||||||||||||||||||||||||||||||

Effect of retrospective application (Note 5) | — | — | — | — | (50,823 | ) | — | — | — | (50,823 | ) | (19,603 | ) | (70,426 | ) | |||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||

BALANCE, JANUARY 1, 2019 AS ADJUSTED | 77,574,465 | 171,136,764 | 77,574,465 | 2,675,419 | 47,090,522 | (79,427 | ) | 538,272 | 1,069 | 376,511,549 | 9,990,345 | 386,501,894 | ||||||||||||||||||||||||||||||||

Appropriation of 2018 earnings | ||||||||||||||||||||||||||||||||||||||||||||

Cash dividends distributed by Chunghwa | — | — | — | — | (34,745,603 | ) | — | — | — | (34,745,603 | ) | — | (34,745,603 | ) | ||||||||||||||||||||||||||||||

Cash dividends distributed by subsidiaries | — | — | — | — | — | — | — | — | — | (709,817 | ) | (709,817 | ) | |||||||||||||||||||||||||||||||

Unclaimed dividend | — | 1,266 | — | — | — | — | — | — | 1,266 | — | 1,266 | |||||||||||||||||||||||||||||||||

Change in additionalpaid-in capital from investments in associates accounted for using equity method | — | 118,853 | — | — | — | — | — | — | 118,853 | 1,064 | 119,917 | |||||||||||||||||||||||||||||||||

Net income for the year ended December 31, 2019 | — | — | — | — | 32,788,546 | — | — | — | 32,788,546 | 975,397 | 33,763,943 | |||||||||||||||||||||||||||||||||

Other comprehensive income (loss) for the year ended December 31, 2019 | — | — | — | — | 1,207,896 | (68,950 | ) | 298,326 | (742 | ) | 1,436,530 | 5,976 | 1,442,506 | |||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||

Total comprehensive income (loss) for the year ended December 31, 2019 | — | — | — | — | 33,996,442 | (68,950 | ) | 298,326 | (742 | ) | 34,225,076 | 981,373 | 35,206,449 | |||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||

Share-based payment transactions of subsidiaries | — | (898 | ) | — | — | — | — | — | — | (898 | ) | 21,320 | 20,422 | |||||||||||||||||||||||||||||||

Net decrease in noncontrolling interests | — | — | — | — | — | — | — | — | — | (763 | ) | (763 | ) | |||||||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||

BALANCE, DECEMBER 31, 2019 | $ | 77,574,465 | $ | 171,255,985 | $ | 77,574,465 | $ | 2,675,419 | $ | 46,341,361 | $ | (148,377 | ) | $ | 836,598 | $ | 327 | $ | 376,110,243 | $ | 10,283,522 | $ | 386,393,765 | |||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||||||

The accompanying notes are an integral part of the consolidated financial statements.

- 10 -

CHUNGHWA TELECOM CO., LTD. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

YEARS ENDED DECEMBER 31, 2019 AND 2018

(In Thousands of New Taiwan Dollars)

| 2019 | 2018 | |||||||

CASH FLOWS FROM OPERATING ACTIVITIES | ||||||||

Income before income tax | $ | 41,749,792 | $ | 44,978,704 | ||||

Adjustments to reconcile income before income tax to net cash provided by operating activities: | ||||||||

Depreciation | 30,922,991 | 27,481,956 | ||||||

Amortization | 4,252,602 | 4,386,798 | ||||||

Amortization of incremental costs of obtaining contracts | 1,173,492 | 1,941,124 | ||||||

Expected credit loss (reversal of credit loss) | (125,111 | ) | 919,732 | |||||

Interest expenses | 104,142 | 17,596 | ||||||

Interest income | (250,787 | ) | (196,889 | ) | ||||

Dividend income | (296,360 | ) | (395,593 | ) | ||||

Compensation cost of share-based payment transactions | 1,597 | 17,302 | ||||||

Share of profits of associates accounted for using equity method | (462,140 | ) | (501,600 | ) | ||||

Loss (gain) on disposal of property, plant and equipment | 37,785 | (142,068 | ) | |||||

Loss on disposal of intangible assets | 146 | — | ||||||

Gain on disposal of financial instruments | (3,944 | ) | (5,763 | ) | ||||

Loss (gain) on disposal of investments accounted for using equity method | (30,152 | ) | 125 | |||||

Provision for inventory and obsolescence | 474,709 | 365,123 | ||||||

Impairment loss on property, plant and equipment | 93,073 | — | ||||||

Reversal of impairment loss on investment properties | (56,617 | ) | (19,133 | ) | ||||

Impairment loss on intangible assets | 8,946 | 50,750 | ||||||

Impairment loss on other assets | 43,971 | — | ||||||

Valuation loss on financial assets and liabilities at fair value through profit or loss, net | 38,314 | 20,763 | ||||||

Others | (26,524 | ) | (17,223 | ) | ||||

Changes in operating assets and liabilities: | ||||||||

Decrease (increase) in: | ||||||||

Financial assets mandatorily measured at fair value through profit or loss | — | 63,117 | ||||||

Contract assets | 172,489 | 2,750,594 | ||||||

Trade notes and accounts receivable | 4,038,731 | 1,353,807 | ||||||

Receivables from related parties | 7,436 | 25,097 | ||||||

Inventories | (2,698,270 | ) | (6,778,309 | ) | ||||

Prepayments | 114,991 | 417,569 | ||||||

Other current monetary assets | (154,780 | ) | (172,597 | ) | ||||

Other current assets | 146,420 | (261,240 | ) | |||||

Incremental cost of obtaining contracts | (781,114 | ) | (802,011 | ) | ||||

Increase (decrease) in: | ||||||||

Contract liabilities | 6,701,313 | 2,652,747 | ||||||

Trade notes and accounts payable | (5,151,740 | ) | 1,065,054 | |||||

Payables to related parties | (263,968 | ) | 233,766 | |||||

Other payables | 697,351 | (1,088,406 | ) | |||||

(Continued)

- 11 -

CHUNGHWA TELECOM CO., LTD. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

YEARS ENDED DECEMBER 31, 2019 AND 2018

(In Thousands of New Taiwan Dollars)

| 2019 | 2018 | |||||||

Provisions | $ | 97,497 | $ | 27,142 | ||||

Other operating liabilities | (159,881 | ) | 422,413 | |||||

Net defined benefit plans | 533,787 | (1,535,294 | ) | |||||

|

|

|

| |||||

Cash generated from operations | 80,950,187 | 77,275,153 | ||||||

Interest paid | (104,142 | ) | (17,524 | ) | ||||

Income tax paid | (8,419,360 | ) | (10,891,279 | ) | ||||

|

|

|

| |||||

Net cash provided by operating activities | 72,426,685 | 66,366,350 | ||||||

|

|

|

| |||||

CASH FLOWS FROM INVESTING ACTIVITIES | ||||||||

Acquisition of financial assets at fair value through other comprehensive income | (60,000 | ) | (289,580 | ) | ||||

Proceeds from return of financial assets at fair value through other comprehensive income | 9,167 | 6,690 | ||||||

Purchase of financial assets at fair value through profit or loss | (443,064 | ) | — | |||||

Proceeds from disposal of financial assets at fair value through profit or loss | 146,560 | — | ||||||

Acquisition of time deposits and negotiable certificates of deposit with maturities of more than three months | (14,381,653 | ) | (9,719,951 | ) | ||||

Acquisition of repurchase agreements collateralized by bonds with maturities of more than three months | (14,990 | ) | — | |||||

Proceeds from disposal of time deposits and negotiable certificates of deposit with maturities of more than three months | 16,519,781 | 5,654,941 | ||||||

Acquisition of investments accounted for using equity method | (4,190,000 | ) | (204,900 | ) | ||||

Proceeds from disposal of investments accounted for using equity method | 32,470 | 3,379 | ||||||

Proceeds from capital reduction of investments accounted for using equity method | — | 19,184 | ||||||

Acquisition of property, plant and equipment | (24,165,857 | ) | (28,549,929 | ) | ||||

Proceeds from disposal of property, plant and equipment | 48,157 | 264,446 | ||||||

Acquisition of intangible assets | (362,718 | ) | (498,005 | ) | ||||

Acquisition of investment properties | (523 | ) | (5,627 | ) | ||||

Increase in other noncurrent assets | (1,122,142 | ) | (80,640 | ) | ||||

Interest received | 256,432 | 186,617 | ||||||

Cash dividends received | 602,086 | 599,621 | ||||||

|

|

|

| |||||

Net cash used in investing activities | (27,126,294 | ) | (32,613,754 | ) | ||||

|

|

|

| |||||

CASH FLOWS FROM FINANCING ACTIVITIES | ||||||||

Proceeds from short-term loans | 575,000 | 360,000 | ||||||

Repayment of short-term loans | (585,000 | ) | (330,000 | ) | ||||

Increase in customers’ deposits | 7,311 | 30,997 | ||||||

Payment for the principal of lease liabilities | (3,727,792 | ) | — | |||||

Increase in other noncurrent liabilities | 232,357 | 83,613 | ||||||

(Continued)

- 12 -

CHUNGHWA TELECOM CO., LTD. AND SUBSIDIARIES

CONSOLIDATED STATEMENTS OF CASH FLOWS

YEARS ENDED DECEMBER 31, 2019 AND 2018

(In Thousands of New Taiwan Dollars)

| 2019 | 2018 | |||||||

Cash dividends | $ | (34,745,603 | ) | $ | (37,204,714 | ) | ||

Partial disposal of interests in subsidiaries without losing control | — | 1,174,400 | ||||||

Cash dividends distributed to noncontrolling interests | (709,817 | ) | (958,446 | ) | ||||

Change in other noncontrolling interests | 18,062 | 1,806,345 | ||||||

Unclaimed dividend | 1,266 | 2,455 | ||||||

|

|

|

| |||||

Net cash used in financing activities | (38,934,216 | ) | (35,035,350 | ) | ||||

|

|

|

| |||||

EFFECT OF EXCHANGE RATE CHANGES ON CASH AND CASH EQUIVALENTS | 38,688 | 102,599 | ||||||

|

|

|

| |||||

NET INCREASE (DECREASE) IN CASH AND CASH EQUIVALENTS | 6,404,863 | (1,180,155 | ) | |||||

CASH AND CASH EQUIVALENTS, BEGINNING OF THE YEAR | 27,644,780 | 28,824,935 | ||||||

|

|

|

| |||||

CASH AND CASH EQUIVALENTS, END OF THE YEAR | $ | 34,049,643 | $ | 27,644,780 | ||||

The accompanying notes are an integral part of the consolidated financial statements.

| (Concluded) |

- 13 -

CHUNGHWA TELECOM CO., LTD. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

YEARS ENDED DECEMBER 31, 2019 AND 2018

(In Thousands of New Taiwan Dollars, Unless Stated Otherwise)

| 1. | GENERAL |

Chunghwa Telecom Co., Ltd. (“Chunghwa”) was incorporated on July 1, 1996 in the Republic of China (“ROC”) pursuant to the Article 30 of the Telecommunications Act. Chunghwa is a company limited by shares and, prior to August 2000, was wholly owned by the Ministry of Transportation and Communications (“MOTC”). Prior to July 1, 1996, the current operations of Chunghwa were carried out under the Directorate General of Telecommunications (“DGT”). The DGT was established by the MOTC in June 1943 to take primary responsibility in the development of telecommunications infrastructure and to formulate policies related to telecommunications. On July 1, 1996, the telecom operations of the DGT werespun-off as Chunghwa which continues to carry out the business and the DGT continues to be the industry regulator.

Effective August 12, 2005, the MOTC completed the process of privatizing Chunghwa by reducing the government ownership to below 50% in various stages. In July 2000, Chunghwa received approval from the Securities and Futures Commission (the “SFC”) for a domestic initial public offering and its common stocks were listed and traded on the Taiwan Stock Exchange (the “TWSE”) on October 27, 2000. Certain of Chunghwa’s common stocks were sold, in connection with the foregoing privatization plan, in domestic public offerings at various dates from August 2000 to July 2003. Certain of Chunghwa’s common stocks were also sold in an international offering of securities in the form of American Depository Shares (“ADS”) on July 17, 2003 and were listed and traded on the New York Stock Exchange (the “NYSE”). The MOTC sold common stocks of Chunghwa by auction in the ROC on August 9, 2005 and completed the second international offering on August 10, 2005. Upon completion of the share transfers associated with these offerings on August 12, 2005, the MOTC owned less than 50% of the outstanding shares of Chunghwa and completed the privatization plan.

Chunghwa together with its subsidiaries are hereinafter referred to collectively as the “Company”.

The consolidated financial statements are presented in Chunghwa’s functional currency, New Taiwan dollars.

| 2. | APPROVAL OF FINANCIAL STATEMENTS |

The consolidated financial statements were approved by the Board of Directors on February 26, 2020.

| 3. | SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES |

The Company initial applied IFRS 16 “Leases” on January 1, 2019 and elected not to reflect the figures on a retrospective basis in comparative periods. Different accounting policies for each accounting period as a result of the application of new accounting standards are listed by year separately.

Statement of Compliance

The accompanying consolidated financial statements have been prepared in conformity with the Regulations Governing the Preparation of Financial Reports by Securities Issuers and the International Financial Reporting Standards (IFRS), International Accounting Standards (IAS), International Financial Reporting Interpretations Committee (IFRIC) and SIC Interpretations (SIC) endorsed and issued into effect by the Financial Supervisory Commission (FSC) (the “Taiwan-IFRS”).

- 14 -

Basis of Preparation

The consolidated financial statements have been prepared on the historical cost basis except for certain financial instruments that are measured at fair values and net defined benefit liabilities (assets) which are measured at the present value of the defined benefit obligation less the fair value of plan assets.

Current and Noncurrent Assets and Liabilities

Current assets include:

| a. | Assets held primarily for the purpose of trading; |

| b. | Assets expected to be realized within twelve months after the reporting period; and |

| c. | Cash and cash equivalents unless the asset is restricted from being exchanged or used to settle a liability for at least twelve months after the reporting period. |

Current liabilities include:

| a. | Liabilities held primarily for the purpose of trading; |

| b. | Liabilities due to be settled within twelve months after the reporting period; and |

| c. | Liabilities for which the Company does not have an unconditional right to defer settlement for at least twelve months after the reporting period. |

Assets and liabilities that are not classified as current are classified as noncurrent.

Light Era Development Co., Ltd. (LED) engages mainly in development of property for rent and sale. The assets and liabilities of LED related to property development within its operating cycle, which is over one year, are classified as current items.

Basis of Consolidation

| a. | Principles for preparing consolidated financial statements |

The consolidated financial statements incorporate the financial statements of Chunghwa and entities controlled by Chunghwa (its subsidiaries).

When necessary, adjustments are made to the financial statements of subsidiaries to bring their accounting policies in line with those used by the Company.

All inter-company transactions, balances, income and expenses are eliminated in full upon consolidation.

Attribution of total comprehensive income to noncontrolling interests

Total comprehensive income of subsidiaries is attributed to the stockholders of the parent and to the noncontrolling interests even if it results in the noncontrolling interests having a deficit balance.

Changes in the Company’s ownership interests in subsidiaries

Changes in the Company’s ownership interests in subsidiaries that do not result in the Company losing control over the subsidiaries are accounted for as equity transactions. The carrying amounts of the Company’s interests and the noncontrolling interests are adjusted to reflect the changes in their relative interests in the subsidiaries. Any difference between the amount by which the noncontrolling interests are adjusted and the fair value of the consideration paid or received is recognized directly in equity and attributed to stockholders of the parent.

- 15 -

| b. | The subsidiaries in the consolidated financial statements |

The detail information of the subsidiaries at the end of reporting period was as follows:

| Percentage of Ownership | ||||||||||||||||

| December 31 | ||||||||||||||||

| Name of Investor | Name of Investee | Main Businesses and Products | 2019 | 2018 | Note | |||||||||||

Chunghwa Telecom Co., Ltd. | Senao International Co., Ltd. (“SENAO”) | Handset and peripherals retailer, sales of CHT mobile phone plans as an agent | 28 | 28 | a | ) | ||||||||||

Light Era Development Co., Ltd. (“LED”) | Planning and development of real estate and intelligent buildings, and property management | 100 | 100 | |||||||||||||

Donghwa Telecom Co., Ltd. (“DHT”) | International private leased circuit, IP VPN service, and IP transit services | 100 | 100 | |||||||||||||

Chunghwa Telecom Singapore Pte., Ltd. (“CHTS”) | International private leased circuit, IP VPN service, and IP transit services | 100 | 100 | |||||||||||||

Chunghwa System Integration Co., Ltd. (“CHSI”) | Providing system integration services and telecommunications equipment | 100 | 100 | |||||||||||||

Chunghwa Investment Co., Ltd. (“CHI”) | Investment | 89 | 89 | |||||||||||||

CHIEF Telecom Inc. (“CHIEF”) | Network integration, internet data center (“IDC”), communications integration and cloud application services | 57 | 57 | b | ) | |||||||||||

CHYP Multimedia Marketing & Communications Co., Ltd. (“CHYP”) | Digital information supply services and advertisement services | 100 | 100 | |||||||||||||

Prime Asia Investments Group Ltd. (B.V.I.) (“Prime Asia”) | Investment | 100 | 100 | |||||||||||||

Spring House Entertainment Tech. Inc. (“SHE”) | Software design services, internet contents production and play, and motion picture production and distribution | 56 | 56 | c | ) | |||||||||||

Chunghwa Telecom Global, Inc. (“CHTG”) | International private leased circuit, internet services, and transit services | 100 | 100 | |||||||||||||

Chunghwa Telecom Vietnam Co., Ltd. (“CHTV”) | Intelligent energy saving solutions, international circuit, and information and communication technology (“ICT”) services | 100 | 100 | |||||||||||||

Smartfun Digital Co., Ltd. (“SFD”) | Providing diversified family education digital services | 65 | 65 | |||||||||||||

Chunghwa Telecom Japan Co., Ltd. (“CHTJ”) | International private leased circuit, IP VPN service, and IP transit services | 100 | 100 | |||||||||||||

Chunghwa Sochamp Technology Inc. (“CHST”) | Design, development and production of Automatic License Plate Recognition software and hardware | 51 | 51 | |||||||||||||

Honghwa International Co., Ltd. (“HHI”) | Telecommunications engineering, sales agent of mobile phone plan application and other business services, etc. | 100 | 100 | |||||||||||||

Chunghwa Leading Photonics Tech Co., Ltd. (“CLPT”) | Production and sale of electronic components and finished products | 75 | 75 | |||||||||||||

Chunghwa Telecom (Thailand) Co., Ltd. (“CHTT”) | International private leased circuit, IP VPN service, ICT and cloud VAS services | 100 | 100 | d | ) | |||||||||||

CHT Security Co., Ltd. (“CHTSC”) | Computing equipment installation, wholesale of computing and business machinery equipment and software, management consulting services, data processing services, digital information supply services and internet identify services | 80 | 80 | |||||||||||||

(Continued)

- 16 -

| �� | Percentage of Ownership | |||||||||||||||

| December 31 | ||||||||||||||||

| Name of Investor | Name of Investee | Main Businesses and Products | 2019 | 2018 | Note | |||||||||||

Senao International Co., Ltd. | Senao International (Samoa) Holding Ltd. (“SIS”) | International investment | 100 | 100 | ||||||||||||

Youth Co., Ltd. (“Youth”) | Sale of information and communication technologies products | 93 | 93 | e | ) | |||||||||||

Aval Technologies Co., Ltd. (“Aval”) | Sale of information and communication technologies products | 100 | 100 | |||||||||||||

Senyoung Insurance Agent Co., Ltd. (“SENYOUNG”) | Property and liability insurance agency | 100 | 100 | |||||||||||||

Youth Co., Ltd. | ISPOT Co., Ltd. (“ISPOT”) | Sale of information and communication technologies products | 100 | 100 | ||||||||||||

Youyi Co., Ltd. (“Youyi”) | Maintenance of information and communication technologies products | 100 | 100 | |||||||||||||

Aval Technologies Co., Ltd. | Wiin Technology Co., Ltd. (“Wiin”) | Sale of information and communication technologies products | 100 | — | f | ) | ||||||||||

Senyoung Insurance Agent Co., Ltd. | Seyoung Insurance Agent Co., Ltd. (“Seyoung”) | Life insurance services | 100 | — | g | ) | ||||||||||

Light Era Development Co., Ltd. | Taoyuan Asia Silicon Valley Innovation Co., Ltd. (“TASVI”) | Development of real estate | — | 60 | h | ) | ||||||||||

CHIEF Telecom Inc. | Unigate Telecom Inc. (“Unigate”) | Telecommunications and internet service | 100 | 100 | ||||||||||||

Chief International Corp. (“CIC”) | Telecommunications and internet service | 100 | 100 | |||||||||||||

Shanghai Chief Telecom Co., Ltd. (“SCT”) | Telecommunications and internet service | 49 | 49 | |||||||||||||

Chunghwa System Integration Co., Ltd. | Concord Technology Co., Ltd. (“Concord”) | Investment | — | — | i | ) | ||||||||||

Chunghwa Investment Co., Ltd. | Chunghwa Precision Test Tech. Co., Ltd. (“CHPT”) | Production and sale of semiconductor testing components and printed circuit board | 34 | 34 | j | ) | ||||||||||

Chunghwa Precision Test Tech. Co., Ltd. | Chunghwa Precision Test Tech. USA Corporation (“CHPT (US)”) | Design and after-sale services of semiconductor testing components and printed circuit board | 100 | 100 | ||||||||||||

CHPT Japan Co., Ltd. (“CHPT (JP)”) | Related services of electronic parts, machinery processed products and printed circuit board | 100 | 100 | |||||||||||||

Chunghwa Precision Test Tech. International, Ltd. (“CHPT (International)”) | Wholesale and retail of electronic materials, and investment | 100 | 100 | |||||||||||||

Senao International (Samoa) Holding Ltd. | Senao International HK Limited (“SIHK”) | International investment | 100 | 100 | ||||||||||||

Senao International HK Limited | Senao Trading (Fujian) Co., Ltd. (“STF”) | Sale of information and communication technologies products | — | 100 | k | ) | ||||||||||

Senao International Trading (Shanghai) Co., Ltd. (“SITS”) | Sale of information and communication technologies products | 100 | 100 | |||||||||||||

Senao International Trading (Shanghai) Co., Ltd. (“SEITS”) | Maintenance of information and communication technologies products | — | — | l | ) | |||||||||||

Senao International Trading (Jiangsu) Co., Ltd. (“SITJ”) | Sale of information and communication technologies products | — | 100 | m | ) | |||||||||||

Prime Asia Investments Group Ltd. (B.V.I.) | Chunghwa Hsingta Co., Ltd. (“CHC”) | Investment | 100 | 100 | ||||||||||||

Chunghwa Hsingta Co., Ltd. (“CHC”) | Chunghwa Telecom (China) Co., Ltd. (“CTC”) | Integrated information and communication solution services for enterprise clients, and intelligent energy network service | 100 | 100 | ||||||||||||

Jiangsu Zhenhua Information Technology Company, LLC. (“JZIT”) | Providing intelligent energy saving solution and intelligent buildings services | — | — | n | ) | |||||||||||

Chunghwa Precision Test Tech. International, Ltd. | Shanghai Taihua Electronic Technology Limited (“STET”) | Design of printed circuit board and related consultation service | 100 | 100 | ||||||||||||

Su Zhou Precision Test Tech. Ltd. (“SZPT”) | Assembly processed of circuit board, design of printed circuit board and related consultation service | 100 | — | o | ) | |||||||||||

(Concluded)

- 17 -

| a) | SENAO transferred its treasury stock to employees in June 2018 and the Company’s ownership interest in SENAO decreased to 28.18% as of December 31, 2018 and 2019. As Chunghwa continues to control over half of the seats of the Board of Directors of SENAO (six out of eleven seats as of December 31, 2019) through the support of large beneficial stockholders, the accounts of SENAO are included in the consolidated financial statements. |

| b) | CHIEF issued new shares in March and November 2019, March and November 2018 as its employees exercised their options. In addition, Chunghwa and CHI disposed some shares of CHIEF in May 2018 before CHIEF traded its shares on the General Stock Market of the Taipei Exchange according to the local requirements. Furthermore, Chunghwa and CHI did not participate in the capital increase of CHIEF in June 2018. Therefore, the Company’s ownership interest in CHIEF decreased to 60.23% and 59.75% as of December 31, 2018 and 2019, respectively. |

| c) | SHE reduced 19.72% of its capital to offset accumulated deficits in December 2019 and the Company’s ownership interest in SHE remained the same. |

| d) | The Company increased its investment in CHTT proportionally in October 2019 and the Company’s ownership interest in CHTT remained the same. |

| e) | SENAO subscribed for all the shares in the capital increase of Youth in December 2018. Therefore, the Company’s ownership interest in Youth increased from 89% to 93%. |

| f) | Aval invested 100% equity shares of Wiin Technology Co., Ltd. (“Wiin”) in September 2019. |

| g) | SENYOUNG invested 100% equity shares of Seyoung Insurance Agent Co., Ltd. (“Seyoung”) in November 2019. |

| h) | LED invested 60% equity shares of Taoyuan Asia Silicon Valley Innovation Co., Ltd. (“TASVI”) in March 2018. TASVI completed its liquidation in September 2019. |

| i) | Concord completed its liquidation in January 2018. |

| j) | CHI disposed some shares of CHPT from April to August 2018. Therefore, its ownership interest in CHPT decreased to 34.25% as of December 31, 2018 and 2019. However, considering the absolute and relative size of ownership interest, and the dispersion of shares owned by the other stockholders, the management concluded that the Company has a sufficiently dominant voting interest to direct the relevant activities; hence, CHPT is deemed as a subsidiary of the Company. |

| k) | STF completed its liquidation in May 2019. |

- 18 -

| l) | SEITS completed its liquidation in March 2018. |

| m) | SITJ completed its liquidation in March 2019. |

| n) | JZIT completed its liquidation in December 2018. |

| o) | CHPT (International) invested 100% equity shares of Su Zhou Precision Test Tech. Ltd. (“SZPT”) in October 2019. |

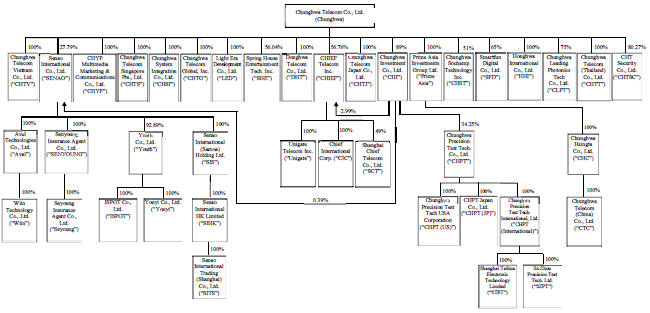

The following diagram presents information regarding the relationship and ownership percentages between Chunghwa and its subsidiaries as of December 31, 2019:

Foreign Currencies

In preparing the financial statements of each individual entity, transactions in currencies other than the entity’s functional currency (foreign currencies) are recognized at the rates of exchange prevailing at the dates of the transactions.

At the end of each reporting period, monetary items denominated in foreign currencies are retranslated at the rates prevailing at that date. Exchange differences on monetary items arising from settlement or translation are recognized in profit or loss in the period in which they arise.

Non-monetary items carried at fair value that are denominated in foreign currencies are retranslated at the rates prevailing at the date when the fair value was determined and related exchange differences are recognized in profit or loss. Conversely, when the fair value changes were recognized in other comprehensive income, related exchange difference shall be recognized in other comprehensive income.

Non-monetary items that are measured at historical cost in a foreign currency are not retranslated.

- 19 -

For the purposes of presenting consolidated financial statements, the assets and liabilities of the Company’s foreign operations (including of the subsidiaries and associates in other countries or currencies used different with Chunghwa) are translated into New Taiwan dollars using exchange rates prevailing at the end of each reporting period. Income and expense items are translated at the average exchange rates for the period. Exchange differences arising, if any, are recognized in other comprehensive income and attributed to stockholders of the parent and noncontrolling interests as appropriate.

Cash Equivalents

Cash equivalents include commercial paper, time deposits, negotiable certificates of deposit and repurchase agreements collateralized by bonds with original maturities within three months from the date of acquisition, highly liquid, readily convertible to a known amount of cash and are subject to an insignificant risk of changes in value. These cash equivalents are held for the purpose of meeting short-term cash commitments.

Inventories

Inventories are stated at the lower of cost or net realizable value item by item, except for those that may be appropriate to group items of similar or related inventories. Net realizable value is the estimated selling price of inventories less all estimated costs of completion and costs necessary to make the sale. The calculation of the cost of inventory is derived using the weighted-average method.

Buildings and Land Consigned to Construction Contractors

Inventories of LED are stated at the lower of cost or net realizable value item by item, except for those that may be appropriate to group as similar items or related inventories. Land acquired before construction is classified as land held for development, and then reclassified as land held under development after LED begins its construction project.

Upon the completion of the construction project, LED recognizes revenues in the amount of proceeds from customers for land and buildings and related costs when ownership is transferred to the customers. The unsold portion of the completed construction project is transferred to land and building held for sale.

Investments in Associates

An associate is an entity over which the Company has significant influence and that is neither a subsidiary nor an interest in a joint venture.

Investments accounted for using the equity method include investments in associates. Under the equity method, an investment in an associate is initially recognized at cost and adjusted thereafter to recognize the Company’s share of profit or loss and other comprehensive income of the associate as well as the distribution received. The Company also recognizes its share in changes in the associates.

When the Company subscribes for new shares of the associate at a percentage different from its existing ownership percentage, the resulting carrying amount of the investment differs from the amount of the Company’s proportionate interest in the associate. The Company records such a difference as an adjustment to investments with the corresponding amount charged or credited to additionalpaid-in capital. When the adjustment should be debited to additionalpaid-in capital but the additionalpaid-in capital recognized from investments accounted for using equity method is insufficient, the shortage is debited to retained earnings.

- 20 -

Any excess of the cost of acquisition over the Company’s share of the fair value of the identifiable net assets and liabilities of an associate at the date of acquisition is recognized as goodwill, which is included within the carrying amount of the investment and shall not be amortized. Any excess of the Company’s share of the net fair value of the identifiable assets and liabilities over the cost of acquisition is recognized immediately in profit or loss.

When necessary, the entire carrying amount of the investment (including goodwill) is tested for impairment as a single asset by comparing its recoverable amount with its carrying amount. Any impairment loss recognized is not allocated to any asset, including goodwill, that forms part of the carrying amount of the investment. Any reversal of that impairment loss is recognized to the extent that the recoverable amount of the investment subsequently increases.

When the Company transacts with its associate, profits and losses resulting from the transactions with the associate are recognized in the Company’s consolidated financial statements only to the extent of interests in the associate that are not related to the Company.

Property, Plant and Equipment

Property, plant and equipment are initially measured at cost and subsequently measured at cost less accumulated depreciation and accumulated impairment loss.

Property, plant and equipment in the course of construction are depreciated and classified to the appropriate categories of property, plant and equipment when completed and ready for their intended use.

Depreciation on property, plant and equipment is recognized using the straight-line method. Each significant part is depreciated separately. Freehold land is not depreciated. The estimated useful lives, residual values and depreciation method are reviewed at the end of each year, with the effect of any changes in estimate accounted for on a prospective basis.

On derecognition of an item of property, plant and equipment, the difference between the net disposal proceeds and the carrying amount of the asset is recognized in profit or loss in the period in which the property is derecognized.

Investment Properties

Investment properties are properties held to earn rentals and/or for capital appreciation. Investment properties also include land held for a currently undetermined future use.

Investment properties are measured initially at cost, including transaction costs. Subsequent to initial recognition, investment properties are measured at cost less accumulated depreciation and accumulated impairment loss. Depreciation is recognized using the straight-line method.

For a transfer from the investment properties to property, plant and equipment, the deemed cost of the property, plant and equipment for subsequent accounting is its carrying amount at the commencement of owner-occupation.

For a transfer from the property, plant and equipment to investment properties, the deemed cost of the investment properties for subsequent accounting is its carrying amount at the end of owner-occupation.

On derecognition of the investment properties, the difference between the net disposal proceeds and the carrying amount of the asset is recognized in profit or loss in the period in which the property is derecognized.

- 21 -

Goodwill

Goodwill arising from the acquisition of a business is carried at cost as established at the date of acquisition of the business less accumulated impairment loss.

For the purpose of impairment testing, goodwill is allocated to each of the Company’s cash-generating units or groups of cash-generating units (referred to as “cash-generating unit”) that are expected to benefit from the synergies of the business combination.

A cash-generating unit to which goodwill has been allocated is tested for impairment annually, or more frequently when there is an indication that the unit may be impaired, by comparing its carrying amount, including the attributable goodwill, with its recoverable amount. However, if the goodwill allocated to a cash-generating unit was acquired in a business combination during the current annual period, that unit shall be tested for impairment before the end of the current annual period. If the recoverable amount of the cash-generating unit is less than its carrying amount, the impairment loss is allocated first to reduce the carrying amount of any goodwill allocated to the unit and then to the other assets of the unit pro rata based on the carrying amount of each asset in the unit. Any impairment loss is recognized directly in profit or loss. An impairment loss recognized for goodwill is not reversed in subsequent periods.

Intangible Assets Other Than Goodwill

Intangible assets with finite useful lives that are acquired separately are initially measured at cost and subsequently measured at cost less accumulated amortization and accumulated impairment loss. Amortization is recognized on a straight-line basis. The estimated useful life, residual value, and amortization method are reviewed at the end of each reporting period, with the effect of any changes in estimate being accounted for on a prospective basis. The residual value of an intangible asset with a finite useful life shall be assumed to be zero unless the Company expects to dispose of the intangible asset before the end of its economic life.

Intangible assets acquired in a business combination and recognized separately from goodwill are initially recognized at their fair value at the acquisition date (which is regarded as their cost). Subsequent to initial recognition, they are measured on the same basis as intangible assets that are acquired separately.

Gains or losses arising from derecognition of an intangible asset, measured as the difference between the net disposal proceeds and the carrying amount of the asset, are recognized in profit or loss in the period in which the asset is derecognized.

Impairment of Tangible Assets, Intangible Assets Other Than Goodwill and Incremental Costs of Obtaining Contracts

At the end of each reporting period, the Company reviews the carrying amounts of its tangible and intangible assets, excluding goodwill, to determine whether there is any indication that those assets have suffered an impairment loss. If any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss. When it is not possible to estimate the recoverable amount of an individual asset, the Company estimates the recoverable amount of the cash-generating unit to which the asset belongs.

Intangible assets not yet available for use are tested for impairment at least annually, and whenever there is an indication that the asset may be impaired.

Recoverable amount is the higher of fair value less costs to sell and value in use. If the recoverable amount of an asset or cash-generating unit is estimated to be less than its carrying amount, the carrying amount of the asset or cash-generating unit is reduced to its recoverable amount, with the resulting impairment loss recognized in profit or loss.

- 22 -

Impairment loss from the assets related to incremental cost of obtaining contracts is recognized to the extent that the carrying amount of the assets exceeds the remaining amount of consideration that the Company expects to receive in exchange for related goods or services less the costs which relate directly to providing those goods or services.

When an impairment loss is subsequently reversed, the carrying amount of the asset or cash-generating unit is increased to the revised estimate of its recoverable amount, but only to the extent of the carrying amount that would have been determined had no impairment loss been recognized for the asset or cash-generating unit in prior years. A reversal of an impairment loss is recognized in profit or loss.

Financial Instruments

Financial assets and financial liabilities are recognized when the Company becomes a party to the contractual provisions of the instruments.

Financial assets and financial liabilities are initially measured at fair value. Transaction costs that are directly attributable to the acquisition of financial assets and financial liabilities (other than financial assets and financial liabilities at fair value through profit or loss) are added to the fair value of the financial assets or financial liabilities, as appropriate, on initial recognition. Transaction costs directly attributable to the acquisition of financial assets or financial liabilities at fair value through profit or loss are recognized immediately in profit or loss.

| a. | Financial assets |

All regular way purchases or sales of financial assets are recognized and derecognized on a trade date basis.

| 1) | Measurement category |

| a) | Financial assets at fair value through profit or loss (FVTPL) |

Financial asset is classified as at FVTPL when the financial asset is mandatorily classified as at FVTPL. Financial assets mandatorily classified as at FVTPL include investments in equity instruments which are not designated as at fair value through other comprehensive income (FVOCI).

Financial assets at FVTPL are stated at fair value, with any gains or losses arising on remeasurement recognized in profit or loss. The net gain or loss recognized in profit or loss does not incorporate any dividend earned on the financial asset. Fair value is determined in the manner described in Note 35.

| b) | Financial assets at amortized cost |

Financial assets that meet the following conditions are subsequently measured at amortized cost:

| i. | The financial asset is held within a business model whose objective is to hold financial assets in order to collect contractual cash flows; and |

| ii. | The contractual terms of the financial asset give rise on specified dates to cash flows that are solely payments of principal and interest on the principal amount outstanding. |

Subsequent to initial recognition, financial assets at amortized cost are measured at amortized cost, which equals to gross carrying amount determined by the effective interest method less any impairment loss, except for short-term receivables as the effect of discounting is immaterial. Exchange differences are recognized in profit or loss.

- 23 -

Interest income is calculated by applying the effective interest rate to the gross carrying amount of such financial assets.

| c) | Investments in equity instruments at FVOCI |

On initial recognition, the Company may make an irrevocable election to designate investments in equity instruments as at FVOCI. Designation at FVOCI is not permitted if the equity investment is held for trading or if it is contingent consideration recognized by an acquirer in a business combination.

Investments in equity instruments at FVOCI are subsequently measured at fair value with gains and losses arising from changes in fair value recognized in other comprehensive income and accumulated in other equity. The cumulative gain or loss will not be reclassified to profit or loss on disposal of the equity investments. Instead, it will be transferred to retained earnings.

Dividends on these investments in equity instruments are recognized in profit or loss when the Company’s right to receive the dividends is established, unless the dividends clearly represent a recovery of part of the cost of the investment.

| 2) | Impairment of financial assets and contract assets |

The Company recognizes a loss allowance for expected credit losses on financial assets at amortized cost (including accounts receivable) and contract assets.

The Company recognizes lifetime Expected Credit Loss (ECL) for accounts receivable and contract assets. For all other financial instruments, the Company recognizes lifetime ECL when there has been a significant increase in credit risk since initial recognition. If, on the other hand, the credit risk on the financial instrument has not increased significantly since initial recognition, the Company measures the loss allowance for that financial instrument at an amount equal to12-month ECL.

Expected credit losses reflect the weighted average of credit losses with the respective risks of a default occurring as the weights. Lifetime ECL represents the expected credit losses that will result from all possible default events over the expected life of a financial instrument. In contrast,12-month ECL represents the portion of ECL that is expected to result from default events on a financial instrument that are possible within 12 months after the reporting date.

The Company recognizes an impairment loss for all financial instruments with a corresponding adjustment to their carrying amount through a loss allowance account.

| 3) | Derecognition of financial assets |

The Company derecognizes a financial asset only when the contractual rights to the cash flows from the asset expire, or when it transfers the financial asset and substantially all the risks and rewards of ownership of the asset to another entity.

On derecognition of a financial asset measured at amortized cost in its entirety, the difference between the asset’s carrying amount and the sum of the consideration received and receivable is recognized in profit or loss.

On derecognition of investments in equity instruments at FVOCI in its entirety, the cumulative gain or loss is directly transferred to retained earnings, and it is not reclassified to profit or loss.

- 24 -

| b. | Financial liabilities |

| 1) | Subsequent measurement |

Except for financial liabilities at FVTPL, all the financial liabilities are subsequently measured at amortized cost using the effective interest method.