![[agm001.jpg]](https://capedge.com/proxy/6-K/0001378296-09-000165/agm001.jpg)

INTERNATIONAL TOWER HILL MINES LTD.

2009 | Notice of Annual General Meeting of Shareholders Management Information Circular |

Place: | Shangri-La Hotel |

Time: | 2:00 p.m. (Vancouver time) |

Date: | Thursday, October 15, 2009 |

INTERNATIONAL TOWER HILL MINES LTD.

CORPORATE DATA | Head Office |

Directors and Officers | |

Registrar and Transfer Agent | |

Legal Counsel | |

Auditor | |

Listing |

INTERNATIONAL TOWER HILL MINES LTD.

Suite 1920, 1188 West Georgia Street

Vancouver, BC V6E 4A2

Tel: 604.683-6332

Fax: 604.408-7499

INFORMATION CIRCULAR

For the Annual General Meeting to be held on October 15, 2009

(information is as at September 15, 2009, except as indicated)

This Information Circular is dated September 15, 2009 (“Information Circular”) and is being is furnished in connection with the solicitation of proxies by the management ofINTERNATIONAL TOWER HILL MINES LTD. (the “Company”) for use at the 2009 annual general meeting (the “Meeting”) of shareholders to be held on Thursday, October 15, 2009 at the time and place and for the purposes set forth in the accompanying Notice of Meeting, and at any adjournment thereof.

REVOCABILITY OF PROXY

In addition to revocation in any other manner permitted by law, you may revoke an executed and deposited proxy by (a) except to the extent otherwise noted on such later proxy, signing new proxy bearing a later date and depositing it at the place and within the time required for the deposit of proxies, (b) signing and dating a written notice of revocation (in the same manner as a proxy is required to be executed as set out in the notes to the proxy) and either depositing it at the place and within the time required for the deposit of proxies or with the Chairman of the Meeting on the day of the Meeting prior to the commencement of the Meeting, or (c) registering with the Scrutineer at the Meeting as a registered shareholder present in person, whereupon any proxy executed and deposited by such registered shareholder will be deemed to have been revoked.

Only registered shareholders have the right to revoke a proxy. If you are not a registered shareholder and you wish to change your vote you must, at least seven days before the Meeting, arrange for the intermediary which holds your common shares to revoke the proxy given by them on your behalf.

A revocation of a proxy does not affect any matter on which a vote has been taken prior to the revocation.

PERSONS MAKING THE SOLICITATION

The enclosed proxy is solicited by Management. Solicitations will be made by mail and possibly supplemented by telephone or other personal contact to be made, without special compensation, by regular officers and employees. The Company may reimburse shareholders’ nominees or agents (including brokers holding shares on behalf of clients) for the cost incurred in obtaining authorization from their principals to execute proxies. No solicitation will be made by specifically engaged employees or soliciting agents. The cost of solicitation will be borne by the Company. None of the directors have advised that they intend to oppose any action intended to be taken by management as set forth in this Information Circular.

The contents and the sending of this Information Circular have been approved by the directors of the Company.

PROXY INSTRUCTIONS

The persons named in the accompanying proxy are current directors and/or officers of the Company. If a shareholder wishes to appoint some other person (who need not be a shareholder) to represent that shareholder at the Meeting the shareholder may do so, either by striking out the printed names and inserting the desired person’s name in the blank space provided in the proxy or by completing another proper proxy and in either case delivering the completed and executed proxy to the Company’s transfer agent, Computershare Investor Services Inc., Proxy Dept., 100 University Avenue, 9thFloor, Toronto, Ontario, CANADA M5J 2Y1, not less than forty-eight (48) hours (excluding Saturdays, Sundays and holidays) before the time fixed for the Meeting or, with respect to any matter occurring after the reconvening of any adjournment of the Meeting, not less than 48 hours (excluding Saturdays, Sundays and holidays) prior to the time of recommencement of such adjourned Meeting. Proxies delivered after such times will not be accepted.

To be valid, the proxy must be dated and be signed by the shareholder or by a duly appointed attorney for such shareholder, or, if the shareholder is a corporation, it must either be under its common seal or signed by a duly authorized officer. If a proxy is signed by a person other than the registered shareholder, or by an officer of a registered corporate shareholder, the Chairman of the Meeting may require evidence of the authority of such person to sign before accepting such proxy.

THE SHARES REPRESENTED BY PROXY WILL, ON A POLL, BE VOTED OR WITHHELD FROM VOTING BY THE PROXY HOLDER IN ACCORDANCE WITH THE INSTRUCTIONS OF THE PERSON APPOINTING THE PROXYHOLDER ON ANY BALLOT THAT MAY BE CALLED FOR AND, IF A CHOICE HAS BEEN SPECIFIED WITH RESPECT TO ANY MATTER TO BE ACTED UPON, THE SHARES WILL BE VOTED ACCORDINGLY.

ON A POLL, IF A CHOICE WITH RESPECT TO SUCH MATTERS IS NOT SPECIFIED OR IF BOTH CHOICES HAVE BEEN SPECIFIED, THE PERSON APPOINTED PROXYHOLDER WILL VOTE THE SECURITIES REPRESENTED BY THE PROXY AS RECOMMENDED BY MANAGEMENT (WHICH, IN THE CASE OF THE MEETING, WILL BE IN FAVOUR OF EACH MATTER IDENTIFIED IN THE PROXY AND FOR THE NOMINEES OF MANAGEMENT FOR DIRECTORS AND AUDITORS).

The enclosed proxy, when properly completed and delivered and not revoked, confers discretionary authority upon the person(s) appointed proxyholder(s) thereunder to vote with respect to any amendments or variations of matters identified in the Notice of Meeting and which may properly come before the Meeting. At the time of the printing of this Information Circular, management knows of no such amendment, variation or other matter which may be presented to the Meeting.

NON-REGISTERED SHAREHOLDERS

Only registered shareholders or duly appointed proxyholders for registered shareholders are permitted to vote at the Meeting. Most of the shareholders of the Company are “non-registered” shareholders because the shares they own are not registered in their names but are instead registered in the name of the brokerage firm, bank or trust company through which they purchased the shares. More particularly, a person is not a registered shareholder in respect of shares of the Company which are held on behalf of that person (the “Non-Registered Holder”) but which are registered either (a) in the name of an intermediary (the “Intermediary”) that the Non-Registered Holder deals with in respect of the shares (Intermediaries include, among others, banks, trust companies, securities dealers or brokers and trustees or administrators of self-administ ered RRSP’s, RRIF’s, RESP’s and similar plans); or (b) in the name of a clearing agency (such as The Canadian Depository for

Securities Limited (“CDS”)) of which the Intermediary is a participant. In accordance with the requirements of National Instrument 54-101 of the Canadian Securities Administrators, the Company has distributed copies of the Notice of Meeting, Information Circular and proxy (collectively referred to as the “Meeting Material”) to the clearing agencies and Intermediaries for onward distribution to Non-Registered Holders.

Intermediaries are required to forward the Meeting Material to Non-Registered Holders unless a Non-Registered Holder has waived the right to receive them. Very often, Intermediaries will use service companies to forward the Meeting Material to Non-Registered Holders. Generally, if you are a Non-Registered Holder and you have not waived the right to receive the Meeting Material you will either:

(a)

be given a form ofproxy which has already been signed by the Intermediary (typically by a facsimile, stamped signature) which is restricted to the number of shares beneficially owned by you, but which is otherwise not complete. Because the Intermediary has already signed the proxy, this proxy is not required to be signed by you when submitting it. In this case, if you wish to submit a proxy you should otherwise properly complete the executed proxy provided and deposit it with theCompany’s Registrar and Transfer Agent, Computershare Investor Services Inc., as provided above; or

(b)

more typically, a Non-Registered Holder will be given a voting instruction form which is not signed by the Intermediary, and which, when properly completed and signed by the Non-Registered Holder andreturned to the Intermediary or its service company, will constitute voting instructions (often called a “proxy”, “proxy authorization form” or “voting instruction form”) which the Intermediary must follow. Typically, the proxy authorization form will consist of a one page pre-printed form. Sometimes, instead of the one page printed form, the proxy authorization form will consist of a regular printed proxy accompanied by a page of instructions that contains a removable label containing a bar-code and other information. In order for the proxy to validly constitute a proxy authorization form, the Non-Registered Sharehol der must remove the label from the instructions and affix it to the proxy, properly complete and sign the proxyand return it to the Intermediary or its service company (not the Company or Computershare Investor Services Inc.) in accordance with the instructions of the Intermediary or its service company.

In either case, the purpose of this procedure is to permit Non-Registered Holders to direct the voting of the shares that they beneficially own. If you are a Non-Registered Holder and you wish to vote at the Meeting in person as proxyholder for the shares owned by you, you should strike out the names of the management designated proxy holders named in theproxy authorization form or voting instruction form and insert your name in the blank space provided. In either case, you should carefully follow the instructions of your Intermediary, including when and where the proxy, proxy authorization or voting instruction form is to be delivered.

INTEREST OF CERTAIN PERSONS OR COMPANIES IN MATTERS TO BE ACTED UPON

Other than as disclosed elsewhere in this Information Circular, none of the current directors or executive officers, no proposed nominee for election as a director, none of the persons who have been directors or executive officers since the commencement of the last completed financial year and no associate or affiliate of any of the foregoing persons has any material interest, direct or indirect, by way of beneficial ownership of securities or otherwise, in any matter to be acted upon at the Meeting, with the exception of the annual re-approval of the Company’s 2006 Incentive Stock Option Plan.

VOTING SHARES AND PRINCIPAL HOLDERS OF VOTING SECURITIES

The authorized capital of the Company consists of 500,000,000 common shares without par value. As at September 15, 2009,57,713,628 common shares without par value were issued and outstanding. Each issued common share carries the right to one vote at the Meeting.

On a show of hands, every individual who is present and is entitled to vote as a registered shareholder or as a representative of one or more registered corporate shareholders will have one vote (regardless of how many shares such shareholder holds), and on a poll every shareholder present in person or represented by a valid proxy and every person who is a representative of one or more corporate shareholders will have one vote for each share registered in that shareholder’s name on the list of shareholders, which is available for inspection during normal business hours at Computershare Investor Services Inc. and will be available at the Meeting. Shareholders represented by proxyholders are not entitled to vote on a show of hands.

Only shareholders of record on the close of business onSeptember 16, 2008(the “Record Date”), who either personally attend the Meeting or who complete and deliver a proxy in the manner and subject to the provisions set out under the heading “Proxy Instructions” will be entitled to have their shares voted at the Meeting or any adjournment thereof.

To the knowledge of the Company’s directors and officers, the following are the only persons or companies who beneficially own, directly or indirectly, or exercise control or discretion over, shares carrying more than 10% of the voting rights attached to all outstanding shares of the Company:

Name of Shareholder | Number of Shares | Percentage of Issued and Outstanding |

Tocqueville Asset Management, L.P. | 8,384,959 | 14.52% |

AngloGold Ashanti (U.S.A.) Exploration Inc.(1) | 7,665,578 | 13.29% |

(1)

AngloGold Ashanti (U.S.A.) Exploration Inc. is an indirect wholly owned subsidiary of AngloGold Ashanti Limited, a South African public company whose securities are listed on the New York, Johannesburg, Ghanaian, London and Australian Stock Exchanges as well as the Paris and Brussels bourses.

FINANCIAL STATEMENTS

The audited financial statements of the Company for the fiscal year ended May 31, 2009, and the accompanying management discussion and analysis, were filed on SEDAR on August 31, 2009 and have been mailed to all registered and beneficial shareholders who had requested them by returning the “Annual/Interim Financial Statement and MD&A Request Form” mailed by the Company as part of its 2008 annual general meeting materials. If you wish to receive either or both of the annual audited financial statements and interim financial statements and accompanying MD&A for the 2009 fiscal year (which commenced on June 1, 2009), you must complete and return the “Annual/Interim Financial Statement and MD&A Request Form” accompanying this Information Circular.

ELECTION OF DIRECTORS

Election of Directors

There are presently six directors of the Company. Management intends to place before the meeting for approval, with or without modification, a resolution fixing the number of directors for the time being at six. Accordingly, it is anticipated that there will be six directors to be elected at the Meeting.

Each director is elected annually and holds office until the next annual meeting of shareholders, unless that person ceases to be a director before then. In the absence of instructions to the contrary, the shares represented by proxies will, on a poll, be voted in favour of the nominees herein listed. Management does not contemplate that any of the nominees will be unable to serve as a director.

The following table sets out the names of management’s nominees for election as directors, their province/state and country of residence, the positions and offices which they presently hold with, the length of time they have served as directors, their respective principal occupations or employments during the past five years and the number of shares which each beneficially owns, directly or indirectly, or over which control or direction is exercised as of the date of this Information Circular:

Name, Province and Country of | Date First Became | Number of Shares |

Anton J. Drescher(4)(5)(7) | October 1, 1991 | 489,218 |

Rowland Perkins(2)(3)(4)(7) | October 22, 1998 | 2,000 |

Hendrik Van Alphen(5)(6) | September 22, 2006 | 772,500 |

Michael Bartlett(2)(7) | May 23, 2007 | Nil |

Ronald Sheardown(2)(3)(7) | May 23, 2007 | Nil |

Steven Aaker(3)(6)(7) | March 12, 2009 | Nil |

(1)

The foregoing information as to province/state and country of residence and number of shares held, not being within the knowledge of the Company, has been furnished by the respective nominees themselves.

(2)

Member of Audit Committee.

(3)

Member of the Compensation Committee.

(4)

Member of the Corporate Governance and Nominating Committee

(5)

Member of the Sustainable Development Committee.

(6)

Member of the Corporate Mergers and Acquisitions Committee.

(7)

Member of the Special Committee.

There is no executive committee of the board of directors.

Unless otherwise stated, each of the below-named nominees has held the principal occupation or employment indicated for the past five years (information provided by the respective nominees):

Hendrik Van Alphen (Director, Chair) - Mr. Van Alphen has, since 1999, been the President of Cardero Resource Corp., a public mineral exploration company trading on the Toronto, American and Frankfurt Stock Exchanges. He is presently also the President (since 2006) and a director of Wealth Minerals Ltd. and a director of Athlone Energy Ltd., both companies listed on the TSXV.

Anton J. Drescher (Director) – Mr. Drescher ceased to act as President and CEO of the Company on September 22, 2006. Mr. Drescher has been Chief Financial Officer and a director of USA Video Interactive Corp., a public company listed for trading on the TSXV and the OTC Bulletin Board, since December 1994, which company is involved in streaming video and video-on-demand. He has also been a director of Dorato Resources Inc., a public mineral exploration company listed on the TSXV, since 1996; President of Westpoint Management Consultants Limited, a private company engaged in tax and accounting consulting for business reorganizations since 1979; and President of Harbour Pacific Capital Corp., a private British Columbia company involved in regulatory filings for businesses in Canada, since 1998; and a director of Trevali Resources Corp., a public natural res ource company listed on the CNSX, since 2007. Mr. Drescher has been a Certified Management Accountant since 1981.

Rowland Perkins (Director) - Mr. Perkins has been the President and a director of eBackup Inc. from 2001 to present. Previously, he was the Marketing Manager of Intellisave Datavaults Inc. (Securinet Inc.) from 1999 to 2000. Mr. Perkins has also served as a director of USA Video Interactive Corp. since 2005 and as a director of Waymar Resources Ltd. since 2005.

Michael Bartlett (Director) – Mr. Bartlett is the President (since 1989) of Leisure Capital & Management Inc., a company which specializes in pre-development start-ups and innovative strategic, conceptual, economic and financial solutions. He is also a director of Wealth Minerals Ltd., a public natural resource company listed on the TSXV. Mr. Bartlett has extensive experience with emerging companies in the public sector.

Ronald Sheardown (Director) – Mr. Sheardown is the president of Greatland Exploration, Ltd. and has been involved in Alaskan and Canadian exploration for over 50 years, with discoveries such as the co-discovery (with Murray Watts) of the Mary River Iron Ore Deposit of Baffinland Iron Mines Limited (reported indicated and inferred resources of 337Mt of 66% iron) to his credit. In addition, Mr. Sheardown was part of the team that discovered the Asbestos Hill and Raglan deposits in Quebec and the Black Angel mine in Greenland. More recently, he has served as a technical advisor to Rudnik Matrosova (a division of Norilsk Nickel) on the development of the Natalka deposit in eastern Russia. Mr. Sheardown has also held a number of important positions within the State of Alaska and various mining related organizations.

Steven Aaker (Director) – Mr. Aaker has more than 30 years’ experience in the mining industry, including 18 years association with the Franco-Nevada royalty portfolio, and served as Group Executive for Newmont Capital Limited from 2002 to 2007. Prior to the acquisition of Franco-Nevada Mining Company Limited (Old Franco-Nevada) by Newmont Mining Company in 2002, Mr. Aaker served as Vice President for Old Franco-Nevada, Euro-Nevada Mining Corp. Ltd. and Redstone Resources Inc., based in Reno, Nevada. Mr. Aaker has been associated with the majority of the U.S. acquisitions made by

those companies. Prior to joining Old Franco-Nevada, Mr. Aaker was an independent geological consultant. Mr. Aaker holds a Bachelor’s degree in geology from the University of Colorado.

Corporate Cease Trade Orders, Bankruptcies, Penalties or Sanctions

1.

Except as noted below, no proposed director is, as at the date of this Information Circular, or has been within ten years before the date of this Information Circular, a director, chief executive officer or chief financial officer of any company (including the Company) that:

(a)

was subject to an order that was issued while the proposed director was acting in the capacity as director, chief executive officer or chief financial officer; or

(b)

was subject to an order that was issued after the proposed director ceased to be a director, chief executive officer or chief financial officer and which resulted from an event that occurred while that person was acting in the capacity as director, chief executive officer or chief financial officer.

For the purposes hereof, the term “order” means:

(a)

a cease trade order;

(b)

an order similar to a cease trade order; or

(c)

an order that denied the relevant company access to any exemption under securities legislation,

that was in effect for a period of more than 30 consecutive days.

Michael Bartlett was President and a director of Creative Entertainment Technologies Inc. (“Creative”). On May 29, 2002 a cease trade order was issued against Creative for failure by Creative to file its financial statements for the year ended December 31, 2001, and such cease trade order remains in effect. Mr. Bartlett resigned as a director and officer of Creative in 2002.

2.

No proposed director:

(a)

is, as at the date of this information circular, or has been within the ten years before the date of this information circular, a director or executive officer of any company (including the Company) that, while such person was acting in such capacity, or within a year of that person ceasing to act in that capacity, became bankrupt, made a proposal under any legislation relating to bankruptcy or insolvency or was subject to or instituted any proceedings, arrangement or compromise with creditors or had a receiver, receiver-manager or trustee appointed to hold its assets; or

(b)

has, within ten years before the date of this information circular, become bankrupt, made a proposal under any legislation relating to bankruptcy or insolvency, or become subject to or instituted any proceedings, arrangement or compromise with creditors, or has a receiver, receiver manager or trustee appointed to hold the assets of the proposed director.

3.

No proposed director has been subject to:

(a)

any penalties or sanctions imposed by a court relating to securities legislation or by a securities regulatory authority or has entered into a settlement agreement with a securities regulatory authority; or

(b)

any other penalties or sanctions imposed by a court or regulatory body that would likely be considered important to a reasonable investor in deciding whether to vote for a proposed director.

EXECUTIVE COMPENSATION

Definitions

For the purpose of this Information Circular:

“Board” means the board of directors of the Company;

“Chief Executive Officer” or “CEO” means each individual who served as chief executive officer or acted in a similar capacity during the most recently completed financial year;

“Chief Financial Officer” or “CFO” means each individual who served as chief financial officer or acted in a similar capacity during the most recently completed financial year;

“closing market price” means the price at which the company’s security was last sold, on the applicable date, in the security’s principal marketplace in Canada;

“equity incentive plan” means an incentive plan, or portion of an incentive plan, under which awards are granted and that falls within the scope of section 3870 of the Handbook of the Canadian Institute of Chartered Accountants, as amended from time to time;

“executive officer” means an individual who is:

(a)

a chair, vice-chair or president,

(b)

a vice-president in charge of a principal business unit, division or function including, sales, finance or production, or

(c)

performing a policy-making function in respect of the Company;

“long-term incentive plan” or “LTIP” means a plan providing compensation intended to motivate performance over a period greater than one financial year. LTIPs do not include option or SAR plans or plans for compensation through shares or units that are subject to restrictions on resale;

“Named Executive Officers” or “NEO’s” means the following individuals:

(a)

each CEO;

(b)

each CFO;

(c)

each of the three most highly compensated executive officers, or the three most highly compensated individuals acting in a similar capacity, other than the CEO and CFO, at the end of the most recently completed financial year and whose total compensation was, individually, more than CAD 150,000 for that financial year; and

(d)

each individual who would be an NEO under paragraph (c) but for the fact that the individual was neither an executive officer of the company, nor acting in a similar capacity, at the end of that financial year;

“option-based award” means an award under an equity incentive plan of options, including, for greater certainty, share options, share appreciation rights, and similar instruments that have option-like features;

“plan” includes any plan, contract, authorization, or arrangement, whether or not set forth in any formal document, where cash, securities, similar instruments or any property may be received, whether for one or more persons;

“repricing” means, in relation to an option, adjusting or amending the exercise or base price of the option, but excludes any adjustment or amendment that equally affects all holders of the class of securities underlying the option and occurs through the operation of a formula or mechanism in, or applicable to, the option;

“stock appreciation right” means a right, granted by the Company or any of its subsidiaries as compensation for employment services or office to receive cash or an issue or transfer of securities based wholly or in part on changes in the trading price of the Company’s securities.

Compensation Discussion and Analysis

Compensation Committee

The Board has established a Compensation Committee (“CC”), and has adopted a written charter for the CC, effective September 22, 2006. There is no written position description for the Chair of the CC. However, as a general statement, the Chair is responsible for setting the tone for the work of the CC, ensuring that members have the information needed to do their jobs, overseeing the logistics of the CC’s operations, reporting to the Board on the committee’s decisions and recommendations and setting the agenda for the meetings of the CC.

The CC is responsible for assisting the Board in monitoring, reviewing and approving compensation policies and practises of the Company and its subsidiaries and administering the Company’s 2006 Incentive Stock Option Plan (the “Plan”). With regard to the CEO, the CC is responsible for reviewing and approving corporate goals and objectives relevant to the CEO’s compensation, evaluating the CEO’s performance in light of those goals and objectives and making recommendations to the Board with respect to the CEO’s compensation level based on this evaluation. In consultation with the CEO, the CC makes recommendations to the Board on the framework of executive remuneration and its cost and on specific remuneration packages for each of the directors and officers other than the CEO, including recommendations regarding awards under equity compensation p lans. The CC also reviews executive compensation disclosure before the Company publicly discloses the information. The CC’s decisions are typically reflected in consent resolutions.

The CC has the authority to engage and compensate, at the expense of the Company, any outside advisor that it determines to be necessary to permit it to carry out its duties (including compensation consultants and advisers), but it did not retain any such outside consultants or advisors during the financial year ended May 31, 2009.

General Compensation Strategy

The executive officers of the Company are compensated in a manner consistent with their respective contributions to the overall benefit of the Company, and in line with the criteria set out below.

Executive compensation is based on a combination of factors, including a comparative review of information provided to the CC by compensation consultants, recruitment agencies and auditors (if any) as well as historical precedent. The CC has not felt it necessary to retain any compensation consultants or other compensation advisers in respect of any prior fiscal years. In the case of a mineral exploration company such as the Company, the ability to determine and carry out generative programs based on new geological theories or concepts in previously unexplored areas, the ability to source and secure promising mineral properties, the ability to raise the necessary capital to explore such properties and maintain the Company’s ongoing activities, the ability to focus the Company’s resources and to appropriately allocate such resources to the benefit of the Company a s a whole, the ability to ensure compliance by the Company with applicable regulatory requirements and the ability to carry on business in a sustainable manner are considered by the CC to be of primary importance in assessing the performance of its executive officers.

The foregoing criteria are used to assess the appropriate compensation level for the CEO and other executive officers.

Executive Compensation Program

General

The executive compensation program formulated by the CC is designed to encourage, compensate and reward senior management of the Company on the basis of individual and corporate performance, both in the short term and the long term, while at the same time being mindful of the responsibility that the Company has to its shareholders. Members of the CC review the proxy materials of companies they consider to be peers of the Company in the mining industry to get a sense of the compensation paid by such companies to their NEO’s and thereby the current marketplace norms for such compensation. The members of the CC use their own experience and familiarity with the industry and the activities of companies within it to determine those companies that they believe are the peers to the Company. The companies considered to be peers of the Company can vary from year to year, depending primarily upon the activities of companies in the industry, their respective projects and their exploration successes (or lack thereof).

Substantially all of the senior management employees of the Company are US residents and are therefore employees of Talon Gold (US) Inc., a wholly owned subsidiary of the Company based in Colorado (“Talon US”). However, the compensation of such individuals is still within the mandate of the CC. The base salaries of senior management of the Company are set at levels which are competitive with the base salaries paid by companies of comparable or similar size within the mining industry, thereby enabling the Company to compete for and retain executives critical to the long term success of the Company. Initially, salaries and benefits are set through negotiation when an executive officer joins the Company (with direct input from the CC) and are reflected in the employment agreement executed at that time. The compensation of such individuals is then subsequ ently reviewed each financial year to determine if adjustments are required. The Company, through Talon US, also has an appropriate benefit program in place, including medical and dental benefits and basic life insurance, which applies to all permanent employees of Talon US, as it believes that such a plan is an important consideration in attracting the necessary personnel.

The incentive portion of the compensation package, consisting primarily of the awarding of stock options and cash bonuses, is directly tied to the performance of both the individual and the Company. Share ownership opportunities are provided to align the interests of senior management of the Company with the longer-term interests of the shareholders of the Company. Generally, the CC believes that incentive stock options should not be granted for longer than two years, except in exceptional circumstances. The CC does not view share appreciation rights, restricted stock units, securities purchase programs or long term incentive programs (other than incentive stock options) or pension plans as appropriate components of compensation programs for junior resource companies such as the Company. Accordingly, no such elements are included in the Company’s compensat ion program.

In general, the CC considers that its compensation program should be relatively simple in concept and that its focus should be balanced between reasonable annual compensation (base salaries in line with current industry standards) and longer term compensation tied to performance of the Company as a whole (incentive compensation in the form of stock options and cash bonuses where warranted). The CC has not established a formal set of benchmarks or performance criteria to be met by the Company’s NEO’s, rather, the members of the CC use their own assessments of the success (or otherwise) of the Company, both absolutely or in relation to its peers, to determine, collectively, whether or not the NEO’s are successfully achieving the Company business plan and strategy and whether they have over, or under, performed in that regard. The CC has not established any set or formal formula for determining NEO compensation, either as to the amount thereof or the specific mix of compensation elements.

Base Salaries

The level of the base salary for each employee of the Company, within a specified range, is determined by the level of responsibility and the importance of the position to the Company, within competitive industry ranges. The CC, in consultation with the CEO, makes recommendations to the Board regarding the base salaries and bonuses (if any) for senior management and employees of the Company other than the CEO. The CC is responsible for recommending the salary level of the CEO to the Board for approval (which must be by a vote of a majority of the independent directors). During the most recently completed fiscal year, based upon the CC’s assessment of the performance of the Company’s NEO’s in line with the factors noted above, the CC recommended, and the Board approved, an increase of 22.22% (from CAD 180,000 to CAD 220,000) in the CEO’s base salar y and an increase of 29.63% (from CAD 108,000 to CAD 160,000) for the Vice-President, Exploration (such increases were effective December 1, 2008). The primary driver for such increases was the exceptional success of the CEO and Vice-President, Exploration, in advancing the Company’s flagship Livengood property in Alaska in an accelerated time-frame and the positive reaction in the marketplace to such efforts.

Although the Company does not have a pension plan for its NEO’s or other executive officers, the Company, through Talon US, makes payments to a 401k plan on behalf of each of the CEO and Vice-President, Exploration in accordance with their employment agreements. Similar payments are made for the Company’s two other US employees. These amounts were negotiated at the time that such employees entered into their respective employment agreements.

Bonuses

The CEO presents recommendations to the CC with respect to bonuses (if any) to be awarded to the members of senior management (including himself) and to the other employees of the Company (if any). The CC evaluates each member of senior management and the other employees of the Company in terms of their performance and the performance of the Company (utilizing the overall assessment process described above). The CC then makes a determination of the bonuses, if any, to be awarded to each member of senior management (including the CEO) and to the employees of the Company, and

recommends such determination to the Board. Based on the overall performance of the Company, and the efforts of a number of members of senior management and employees in moving the Company’s Livengood Project forward (as noted above), in November 2008 the CC recommended, and the Board approved, a bonus of USD 130,000 for the CEO and USD 35,000 for the Vice-President, Exploration, as well as an aggregate of USD 33,000 in bonuses for other employees (paid in December, 2008).

2006 Incentive Stock Option Plan

The Plan is administered by the CC, and is intended to advance the interests of the Company through the motivation, attraction and retention of key employees, officers and directors of the Company and subsidiaries of the Company and to secure for the Company and its shareholders the benefits inherent in the ownership of common shares of the Company by key employees, officers, directors and consultants of the Company and subsidiaries of the Company. Grants of options under the 2006 Incentive Stock Option Plan are proposed/recommended by the CEO, and reviewed by the CC. The CC can approve, modify or reject any proposed grants, in whole or in part. In general, the allocation of available options among the eligible participants in the Plan is on anad hocbasis, and there is no set formula for allocating available options, nor is there any fixed benchmark or perfo rmance criteria to be achieved in order to receive an award of options. The timing of the grants of options is determined by the CC. In general, a higher level of responsibility will attract a larger grant of options. Because the number of options available is limited, in general, the CC aims to have individuals at the same levels of responsibility holding equivalent numbers of options, with additional grants being allocated for individuals who the CC believe are in a position to more directly affect the success or the Company through their efforts. The CC looks at the overall number of options held by an individual (including the exercise price and remaining term of existing options and whether any previously granted options have expired out of the money or were exercised) and takes such information into consideration when reviewing proposed new grants. After considering the CEO’s recommendations and the foregoing factors, the resulting proposed option grant (if any) is th en submitted to the Board for approval. Please see “Particulars of Matters to be Acted Upon – Annual Re-approval of Incentive Stock Option Plan” for a summary of the Plan. During the fiscal year ended May 31, 2009, the CC approved all recommendations for the grant of incentive stock options proposed by the CEO (of which an aggregate of 910,000 (49.18%) were granted to NEO’s and 300,000 (16.21%) were granted to directors who are not NEO’s).

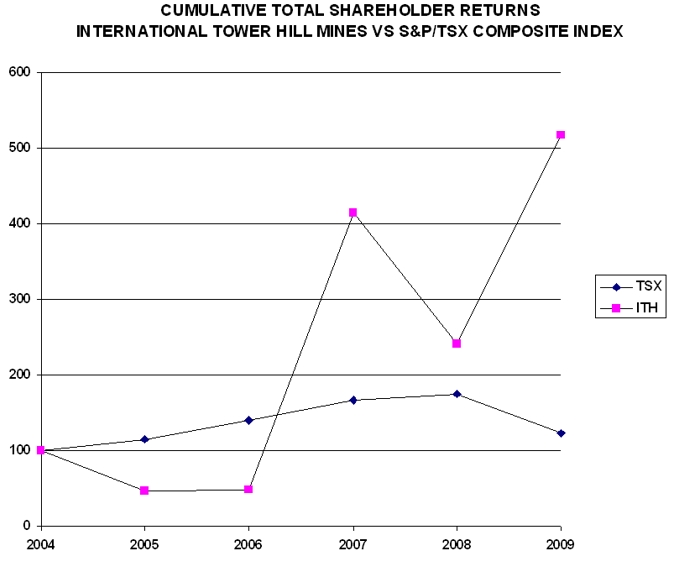

Performance Graph

The following chart compares the total cumulative shareholder return on CAD 100 invested in common shares of the Company on May 31, 2004 with the cumulative total returns of the S&P/TSX Composite Index for the five most recently completed financial years:

2004 | 2005 | 2006 | 2007 | 2008 | 2009 | |

International Tower Hill Mines | 100 | 47.1 | 48.6 | 414.3 | 241.4 | 517.1 |

S&P/TSX Composite Index | 100 | 114.1 | 139.5 | 166.9 | 174.8 | 123.2 |

As can be seen from the foregoing graph, during the fiscal year ended May 31, 2009, the Company’s performance significantly exceeded the performance of the S&P/TSX Composite Index. In fact, during the period commencing in the fiscal year ended May 31, 2007 (when present management assumed management of the Company) through to the fiscal year ended May 31, 2009, the cumulative shareholder total returns for the Company’s shareholders has significantly exceeded, by a large margin, the gain in the S&P/TSX Composite Index. This trend mirrors the trend in the compensation paid to the Company’s NEO’s, although the increase in the cumulative total shareholder return for the Company’s shareholders has significantly exceeded the increase in the compensation of the Company’s NEO’s over this three year period.

Option Based Awards

See discussion under “2006 Incentive Stock Option Plan” under “Compensation Analysis and Discussion” above.

Summary Compensation Table

Summary Compensation Table

During the financial year ended May 31, 2009, the Company had three NEO’s, being Jeffrey A. Pontius, President & Chief Executive Officer, Russell Myers, Vice-President, Exploration and Michael W. Kinley, Chief Financial Officer.

The following table is a summary of the compensation paid to the NEO’s during the three (3) most recently completed financial years, for services rendered:

Name and | Fiscal | Salary(5) | Share-based Awards | Option based Awards | Non-equity incentive Plan Compensation | Pension Value | All other compensation | Total | |

Annual incentive plans | Long-term incentive plans | ||||||||

Jeffrey Pontius | 2009 | 237,948 | Nil | 1,099,685(8) | Nil | Nil | Nil | 186,767(2)(4) | 1,524,400 |

Michael W. Kinley | 2009 | N/A | Nil | 433,767(8) | Nil | Nil | Nil | 60,000(5) | 493,767 |

Russell Myers | 2009 | 145,255 | Nil | 134,062(8) | Nil | Nil | Nil | 70,827(2)(4) | 350,144 |

(1)

Fiscal years ended May 31.

(2)

Includes amounts paid by Talon Gold (US) LLC (“Talon US”), an indirect wholly owned US subsidiary of the Company, to a 401k plan on behalf of each of Messrs. Pontius and Myers in accordance with their employment agreements.

(3)

Includes consulting fees paid to Mr. Pontius by the Company for consulting services rendered prior to the commencement of his employment by Talon on August 8, 2006 plus an amount paid by Talon US to a 401k plan on behalf of Mr. Pontius in accordance with his employment agreement.

(4)

Includes cash bonuses paid to Messrs. Pontius and Myers during the relevant fiscal year.

(5)

These amounts were paid for financial consulting services provided by Winslow Associates Management and Communications Inc., a private company wholly owned by Mr. Kinley.

(6)

Salary and other annual compensation paid in USD and converted to CAD at the weighted average of the quarterly USD to CAD exchange rates for the financial year ended May 31, 2009, being 1.14675 (2008 – 1.0381; 2007 1.13688).

(7)

Fair value of incentive stock option grants calculated using the Black-Scholes model based on the following assumptions:

(a)

for the fiscal year ended May 31, 2007:

May 23, 2007 grant | May 9, 2007 grant | January 26, 2007 grant | |

Expected life (years) | 2 | 2 | 2 |

Interest rate | 4.42% | 4.22% | 4.13% |

Volatility (average) | 110.59% | 110.61% | 110.56% |

Dividend yield | 0% | 0% | 0.0% |

Exercise price | $2.95 | $2.70 | $2.70 |

Stock price at grant date | $2.95 | $2.80 | $2.70 |

(b)

for the fiscal year ended May 31, 2008:

January 16, 2008 grant | |

Expected life (years) | 2 |

Interest rate | 3.28% |

Volatility (average) | 116.19% |

Dividend yield | 0% |

Exercise price | $1.52 |

Stock price at grant date | $1.52 |

(c)

for the fiscal year ended May 31, 2009:

July 16, 2008 repricing | March 12, 2009 grant | May 20, 2009 grant | |

Expected life (years) | 2 | 2 | 2 |

Interest rate | 3.07% | 0.99% | 1.10% |

Volatility (average) | 71.97% | 78.36% | 86.32% |

Dividend yield | 0% | 0% | 0.0% |

Exercise price | $1.75 | $2.66 | $3.15 |

Stock price at grant date | $1.50 | $2.85 | $3.11 |

The Company believes that the Black-Scholes model is an appropriate model to use for calculating the fair value of incentive stock options because, while the model was originally developed for valuing publicly traded options as opposed to non-transferrable incentive stock options and requires management to make estimates, which are subjective and may not be representative of actual results (changes in assumptions can materially affect estimates of fair values), this model is used by most companies in the Company’s peer group and therefore represents an approach to valuation reasonably consistent with the Company’s peer group. It is important to remember that, while incentive stock options can have a significant theoretical value (such as those reported above), until the option is actually exercised and the resulting common shares can be sold at a profit, it has n o value that can be realized by the holder.

(8)

This amount includes the incremental fair value arising from the reduction in the exercise price, and extension of the expiry date, on July 16, 2008 as approved by the shareholders of the Company at the annual general meeting held on October 21, 2008, of options originally granted on January 26, 2007 and May 23, 2007 as follows: Jeffrey Pontius (570,000 options, CAD 229,779), Michael Kinley (180,000 options, CAD 68,934) and Russell Myers (180,000 options, CAD 68,934).

Incentive Plan Awards

Outstanding Share-based Awards and Option Based Awards

The following table provides disclosure with respect to all share-based and option-based awards held by each NEO outstanding as at May 31, 2009, being the end of the most recently completed financial year:

(9)

Value using the closing market price of common shares of the Company on the TSX Venture Exchange (“TSXV”) on May 29, 2009, being the last trading day of the Company’s shares for the financial year, of $3.62 per share, less the exercise price per share.

Incentive Plan Awards – Value Vested or earned During the Year

The following table sets forth the aggregate dollar value that would have been realized if the incentive stock options granted during the most recently completed fiscal year had been exercised on the vesting date (as all incentive stock options vest immediately upon granting, the vesting date is the same as the grant date):

Name | Option-based awards – Value vested during the year | Share-based awards – Value vested during the year | Non-equity incentive plan compensation – Value earned during the year |

Jeffrey Pontius | 32,300 | Nil | Nil |

Michael Kinley | 3,800 | Nil | Nil |

Russell Myers | 22,800 | Nil | Nil |

1.

Value based upon the difference between the closing market price of the common shares on the TSXV on the vesting date (being the grant date), and the exercise price of the incentive stock options, on an aggregated basis. Market prices as follows: March 12, 2009 – CAD 2.85, May 20, 2009 – CAD 3.11.

Information with respect to the Plan is provided under “Particulars of Matters to be Acted Upon – Annual Re-approval of Incentive Stock Option Plan”.

Pension Plan Benefits

The Company does not operate any pension plans or provide any retirement benefits for its directors or employees.

Termination and Change of Control Benefits

Termination and Change of Control Benefits

The Company has no contracts, agreements, plans or arrangements that provide for payments to an NEO at, following or in connection with any termination (whether voluntary, involuntary or constructive), resignation, retirement, a change in control of the company or a change in an NEO’s responsibilities.

Director Compensation

Director Compensation Table

The following table discloses all amounts of compensation provided to the directors for the Company’s most recently completed financial year.

Name | Fees earned | Share-based awards | Option-based awards | Non-equity incentive plan compensation | Pension value | All other compensation | Total |

Hendrik Van Alphen | Nil | Nil | 198,703 | Nil | Nil | Nil | 198,703 |

Benjamin Guenther | Nil | Nil | Nil | Nil | Nil | Nil | Nil |

Anton Drescher | 24,000 | Nil | 138,960 | Nil | Nil | Nil | 162,960 |

Rowland Perkins | 24,500 | Nil | 86,112 | Nil | Nil | Nil | 110,612 |

Ronald Sheardown | 24,000 | Nil | 201,139 | Nil | Nil | Nil | 225,139 |

Michael Bartlett | 24,000 | Nil | 201,139 | Nil | Nil | Nil | 225,139 |

Steven Aaker | 4,000 | Nil | 226,738 | Nil | Nil | Nil | 230,738 |

Narrative Discussion

Except as noted below, the Company has no arrangements, standard or otherwise, pursuant to which directors are compensated by the Company for their services in their capacity as directors, or for committee participation, involvement in special assignments or for services as a consultant or expert during the fiscal year ended May 31, 2009.

Except as noted below, none of the Company’s current directors have received any manner of compensation for services provided in their capacity as directors, consultants or experts during the Company’s most recently completed financial year.

Effective February 1, 2008, the CC recommended, and the Board approved, the payment of annual retainer and meeting fees to the independent directors of the Company (in this case the directors other than Messrs. Van Alphen and Guenther), in recognition of the fact that service as a director in an active resource exploration company such as the Company requires a significant commitment of time and effort, as well as the assumption of increasing liability. Independent directors receive a monthly retainer fee of CAD 2,000 (CAD 24,000 per annum), plus an additional fee of CAD 500 per Board or Board committee meeting attended in person or by conference telephone. There is no additional compensation paid with respect to committee membership. In addition, the Company reimburses all directors for their out-of-pocket costs incurred in attending board meetings.

Incentive Plan Awards

Outstanding Share-based Awards and Option Based Awards

The following table provides disclosure with respect to all share-based and option-based awards held by each director outstanding as at May 31, 2009, being the end of the most recently completed financial year:

Option-based Awards | Share-based Awards | |||||

Name | Number of securities underlying unexercised options | Option exercise price | Option expiration date | Value of unexercised in-the-money options | Number of shares or units of shares that have not vested | Market or payout value of share-based awards that have not vested |

Hendrik Van Alphen | 300,000 | 1.75 | July 16, 2010 | 561,000 | Nil | Nil |

Rowland Perkins | 100,000 | 1.75 | July 16, 2010 | 187,000 | Nil | Nil |

Anton Drescher | 200,000 | 1.75 | July 16, 2010 | 374,000 | Nil | Nil |

Michael Bartlett | 40,000 | 1.75 | July 16, 2010 | 74,800 | Nil | Nil |

Ronald Sheardown | 100,000 | 1.75 | July 16, 2010 | 187,000 | Nil | Nil |

Benjamin Guenther | Nil | N/A | N/A | N/A | Nil | Nil |

Steven Aaker | 200,000 | 2.66 | March 12, 2011 | 192,000 | Nil | Nil |

(1)

Value using the closing market price of common shares of the Company on the TSXV on May 29, 2009, being the last trading day of the Company’s common shares for the financial year, of CAD 3.62 per share, less the exercise price per share.

Incentive Plan Awards – Value Vested or earned During the Year

The following table sets forth the aggregate dollar value that would have been realized if the incentive stock options granted during the most recently completed fiscal year had been exercised on the vesting date (as all incentive stock options vest immediately upon granting, the vesting date is the same as the grant date):

Name | Option-based awards – Value vested during the year | Share-based awards – Value vested during the year | Non-equity incentive plan compensation – Value earned during the year |

Hendrik Van Alphen | Nil | Nil | Nil |

Rowland Perkins | Nil | Nil | Nil |

Anton Drescher | Nil | Nil | Nil |

Michael Bartlett | Nil | Nil | Nil |

Ronald Sheardown | Nil | Nil | Nil |

Benjamin Guenther | Nil | Nil | Nil |

Steve Aaker | 38,000 | Nil | Nil |

1.

Value based upon the difference between the closing market price of the common shares on the TSXV on the vesting date (being the grant date), and the exercise price of the incentive stock options, on an aggregated basis. Market prices as follows: March 12, 2009 – CAD 2.85, May 20, 2009 – CAD 3.11.

AUDIT COMMITTEE

Under National Instrument 52-110 – Audit Committees (“NI 52-110”), companies are required to provide certain disclosure with respect to their audit committee, including the text of the audit committee’s charter, the composition of the audit committee and the fees paid to the external auditor, in their Annual Information Form. This information with respect to the Company is provided in Item 17 and Schedule “A” of the Company’s 2009 Annual Information Form dated August 25, 2009, available atwww.sedar.com.

STATEMENT OF CORPORATE GOVERNANCE PRACTICES

National Instrument 58-101 – Disclosure of Corporate Governance Practices requires full and complete annual disclosure of an issuer’s corporate governance practices in Form 58-101F1. The Company’s approach to corporate governance, with reference to the Corporate Governance Guidelines contained in National Policy 58-201, is provided in Schedule “A”.

SECURITIES AUTHORIZED FOR ISSUANCE UNDER EQUITY COMPENSATION PLANS

Table of Equity Compensation Plan Information

The following table sets forth details of all equity compensation plans of the Company as of May 31, 2009, being the end of Company’s last completed financial year.

- 21 -

Plan Category | Number of Securities to be Issued | Weighted-Average | Number of Securities |

Equity Compensation Plans Approved by Securityholders(2) | 5,645,000 | $2.13 | 797 |

Equity Compensation Plans Not Approved By Securityholders | Nil | Nil | N/A |

Total | 5,645,000 | N/A | 797 |

(1)

As at May31, 2009, being the Company’s last completed financial year.

(2)

The only equity compensation plan of the Company is the 2006 Incentive Stock Option Plan.

Incentive Stock Option Plan

The Company presently has a “rolling” stock option plan (the 2006 Incentive Stock Option Plan (“Plan”)), which reserves a number equal to 10% of the then issued common shares (calculated as at the time of any particular stock option grant) for the grant of stock options. The Plan was approved by the shareholders on October 21, 2008 and accepted for filing by the TSXV on March 24, 2009. The Plan requires re-approval by the shareholders at the Meeting. For details of the Plan, see “Particulars of Matters to be Acted Upon – Annual Re-approval of Incentive Stock Option Plan”.

INDEBTEDNESS OF DIRECTORS AND SENIOR OFFICERS

Aggregate Indebtedness

At no time during the last completed financial year was any current director, executive officer or employee or any former director, executive officer or employee of the Company or any of any of the Company’s subsidiaries, or any proposed nominee for election as a director of the Company:

(a)

indebted to the Company or any of its subsidiaries; or

(b)

indebted to another entity where such indebtedness is the subject of a guarantee, support agreement, letter of credit or other similar arrangement or understanding provided by the Company or any of its subsidiaries.

INTEREST OF INFORMED PERSONS IN MATERIAL TRANSACTIONS

Other than as set forth below, no informed person of the Company has, since June 1, 2008 (being the commencement of the Company’s last completed financial year), had any material interest, direct or indirect, in any transactions which materially affected or would materially affect the Company or any of its subsidiaries.

As defined in National Instrument 51-102 “informed person” means:

(a)

a director or executive officer of the Company:

(b)

a director or executive officer of a person or corporation that is itself an informed person or subsidiary of the Company;

(c)

any person or corporation who beneficially owns, or controls or directs, directly or indirectly, voting securities of a reporting issuer or a combination of both carrying more than 10 percent of the voting rights attached to all outstanding voting securities of the Company (other than voting securities held by the person or corporation as underwriter in the course of a distribution); and

(d)

the Company, if it has purchased, redeemed or otherwise acquired any of its securities, for so long as it holds any of its securities.

1.

The Company entered into a purchase agreement dated June 6, 2008 with AngloGold Ashanti (USA) Exploration Inc. (“AngloGold”) to acquire all of the interest of AngloGold in the Terra and LMS properties in Alaska (in which the Company has, or has the right to earn, an interest pursuant to option/joint venture agreements, each dated August 4, 2006, with AngloGold), plus certain other AngloGold rights. The purchase agreement encompasses all royalties and residual rights held by AngloGold in the Terra and LMS properties, as well as AngloGold’s first refusal rights on transactions involving the West Pogo and Gilles properties held by the Company (and originally acquired from AngloGold). Under the terms of the purchase agreement, the Company acquired all of the right, title and interest of AngloGold in the Terra and LMS projects (including AngloGold ’s right of first offer on any disposition thereof by the Company). In addition, AngloGold also relinquished its right of first offer on two of the Company’s other 100% owned projects, being the West Pogo project (which is situated on the western boundary of the Pogo joint venture land package) and the Gilles project (which is located along the Pogo mine road, 25 kilometres southwest of the West Pogo property). The total purchase price was CAD 751,500, which was satisfied by the issuance of an aggregate of 450,000 common shares (valued, for this purpose, at CAD 1.67 per share). The transaction was been accepted for filing by both the TSXV and the NYSE-Amex, and closed on November 24, 2008.

2.

On July 9, 2009, AngloGold exercised its right to maintain its 13.2907% equity interest in the Company. AngloGold’s equity interest had been diluted by virtue of the Company’s issuance of shares since January 1, 2009, principally due to the exercise of 7,753,385 warrants, broker options and broker warrants in May. The “top-up” provision, contained in the June 30, 2006 purchase agreement among AngloGold, the Company and Talon Gold Alaska, Inc. pursuant to which the Company acquired AngloGold’s Alaskan assets (including the Company’s flagship Livengood property), gives AngloGold the right, twice a year, to maintain its then current equity ownership percentage in the Company on an ongoing basis thereby avoiding dilution as a result of the issuance of shares by the Company in connection with property payments or warrant or option e xercises. AngloGold also has a separate right to participate in any equity financings by the Company up to its then pre-financing percentage equity interest. As a consequence of AngloGold’s election to exercise its “top-up” right, the Company sold to AngloGold, on a private placement basis, an aggregate of 1,218,283 common shares at a price of CAD 2.68 per share (reflecting the closing price of the Company’s common shares on the TSXV on July 9, 2009 of CAD 3.15 less the maximum discount (15%), as required by the provisions of the “top-up” right) for gross proceeds of CAD 3,264,998. The private placement closed on August 25, 2009.

AngloGold presently holds 7,665,578 Common Shares, representing approximately 13.29%, of the outstanding common shares. The foregoing transactions were both approved by the Company’s Audit Committee, which is composed solely of independent directors, and by the directors of the Company other than AngloGold’s nominee.

APPOINTMENT OF AUDITOR

The Audit Committee has recommended to the Board that the Company propose Messrs. MacKay LLP, Chartered Accountants, the incumbent auditors, to the shareholders for re-election as the Company’s auditors for the financial year ending May 31, 2010. Accordingly, unless such authority is withheld, the persons named in the accompanying proxy intend to vote for the reappointment of MacKay LLP, Chartered Accountants, as auditors of the Company and to authorize the directors to fix their remuneration.

MANAGEMENT CONTRACTS

The management functions of the Company are not, to any substantial degree, performed by a person or persons other than the Company’s directors or senior officers.

PARTICULARS OF MATTERS TO BE ACTED UPON

Annual Re-Approval of Incentive Stock Option Plan

Pursuant to Policy 4.4 of the TSXV, all TSXV listed companies are required to adopt a stock option plan prior to granting incentive stock options. Accordingly, in August 2006, the Board established the Plan. The purpose of the Plan is to attract and motivate directors, senior officers, employees, consultants and others providing services to the Company and its subsidiaries, and thereby advance the Company’s interests, by affording such persons with an opportunity to acquire an equity interest in the Company through the issuance of stock options. The Plan is a “rolling” stock option plan reserving a maximum of 10% of the issued shares of the Company at the time of the stock option grant. The shareholders originally approved the Plan on September 22, 2006 and last re-approved it on October 21, 2008. As a “rolling” stock option plan, the Plan is required to be re approved by the shareholders each year.

The material terms of the Plan are as follows:

1.

Options may be granted to Employees, Senior Officers, Directors, Non-Employee Directors, Management Company Employees, and Consultants (all as defined in the Plan) of the Company and its Affiliates who are, in the opinion of the Compensation Committee, in a position to contribute to the success of the Company or any of its Affiliates.

2.

The aggregate number of shares which may be issued pursuant to options granted under the Plan, unless otherwise approved by shareholders, may not exceed that number which is equal to 10% of the common shares issued and outstanding at the time of the grant.

3.

The number of shares subject to each option will be determined by the Board, or a duly appointed committee of the Board (in the case of the Company, this is the Compensation Committee), provided that the aggregate number of shares reserved for issuance pursuant to options granted to:

(a)

insiders during any 12 month period may not exceed 10% of the issued shares;

(b)

any one individual during any 12 month period may not exceed 5% of the issued shares;

(c)

any one consultant during any 12 month period may not exceed 2% of the issued shares; and

(d)

all persons employed to provide investor relations activities (as a group) may not exceed 2% of the issued shares during any 12 month period; in each case calculated as at the date of grant of the option, including all other shares under option to such person at that time.

4.

The exercise price of an option may not be set at less than the minimum price permitted by the TSXV (currently the closing price of the common shares on the TSXV on the day prior to an option grant less the maximum discount permitted by the TSXV).

5.

Options may be exercisable for a period of up to five years from the date of grant, unless the Company is classified as a Tier 1 issuer by the TSXV (not presently the case), in which case options may be exercisable for a period of ten years from the date of grant.

6.

The Plan does not contain any specific provisions with respect to the causes of cessation of entitlement of any optionee to exercise his option, provided, however, that the directors may, at the time of grant, determine that an option will terminate within a fixed period (which is shorter than the option term) upon the ceasing of the optionee to be an eligible optionee or upon the death of the optionee, provided that, in the case of the death of the optionee, an option will be exercisable only within one year from the date of the optionee’s death.

7.

Options are non-assignable and non-transferable.

8.

The Plan does not provide for any specific vesting periods. The Compensation Committee may determine when any option will become exercisable and any applicable vesting periods, and may determine that an option shall be exercisable in instalments. However, options granted to consultants engaged to perform investor relations activities must be subject to a vesting requirement, whereby such options will vest over a period of not less than 12 months, with a maximum of 25% vesting in any 3 month period.

9.

On the occurrence of a takeover bid, issuer bid or going private transaction, the Board will have the right to accelerate the date on which any option becomes exercisable and may, if permitted by applicable legislation, permit an option to be exercised conditional upon the tendering of the shares thereby issued to such bid and the completion of, and consequent taking up of such shares under, such bid or going private transaction.

10.

The exercise price per optioned share under an option may be reduced, at the discretion of the Compensation Committee, if:

(a)

at least six months has elapsed since the later of the date such option was granted and the date the exercise price for such option was last amended; and

(b)

disinterested shareholder approval is obtained for any reduction in the exercise price under an option held by an insider of the Company.

11.

The Company does not and will not provide any financial assistance to any optionee in connection with the exercise of any option.

If the Plan is not re-approved, options will continue to be granted and amended from time to time, subject to shareholder approval when required.

As at

September 15, 2009, there are incentive stock options outstanding under the Plan to purchase an aggregate of 5,645,000 common shares, representing 9.78% of the issued capital as at that date. As at September 15, 2009, a total of 5,771,362 options (representing 10% of the outstanding capital as at that date) are permitted to be granted under the Plan, and therefore an additional 126,363 options are available for grant under the Plan as at that date.

A copy of the Plan may be inspected at the Company’s head office located at Suite 1920 - 1188 West Georgia Street, Vancouver, B.C. during normal business hours at any time up to the date of the Meeting and at the Meeting. In addition, a copy of the Plan will be mailed, free of charge, to any shareholder who sends a written request therefor to the Company’s Corporate Secretary at Suite 1920 – 1188 West Georgia Street, Vancouver, B.C., CANADA V6E 4A2.

Accordingly, shareholders will be asked at the Meeting to pass an ordinary resolution, the text of which will be in substantially the following form:

“RESOLVED, as an ordinary resolution, that the Company’s 2006 Incentive Stock Option Plan, as described in the Company’s Information Circular dated September 15, 2009, and the grant of options thereunder in accordance therewith, be and is hereby ratified and approved.”

Management considers it desirable and in the best interests of the Company and its shareholders to re-approve the Plan.

Shareholder Rights Plan

General

The Board adopted a shareholder rights plan agreement dated as of August 26, 2009 between the Company and Computershare Investor Services Inc., as rights agent (the “Rights Plan”). The Rights Plan is intended to provide the shareholders of the Company and the Board with adequate time to consider and evaluate any unsolicited bid made for the Company, to provide the Board with adequate time to identify, develop and negotiate value-enhancing alternatives, if considered appropriate, to any such unsolicited bid, to encourage the fair treatment of shareholders in connection with any takeover bid for the Company and to ensure that any proposed transaction is in the best interests of the shareholders.

By letter dated August 21, 2009, the TSXV has indicated that it has no objection to the adoption of the Rights Plan subject to (a) evidence of shareholder approval of the Rights Plan at the Meeting and (b) confirmation that the news release concerning the adoption of the Rights Plan has been disseminated (confirmed). In order for the Rights Plan to continue in effect, the TSXV requires that the Rights Plan be approved by the shareholders within six (6) months of its adoption or it is required to be cancelled. If the Rights Plan is not ratified at the Meeting, it will terminate at the end of the Meeting. To the knowledge of the directors and senior officers of the Company, as of the date hereof, no person is the beneficial owner of 20% or more of the outstanding shares.

The Rights Plan requires that it be ratified by the Independent Shareholders (as defined in the Rights Plan) which excludes various shareholders including Acquiring Persons, Grandfathered Persons, any Offerors and any associates or affiliates of any such shareholder(s) or any person(s) acting jointly and in concert with such shareholder(s). As at the Effective Date, the Company is not aware of any shareholder who is not an Independent Shareholder as defined in the Rights Plan. Accordingly, unless, prior to the Meeting, any non-Independent Shareholders are identified, all shareholders will be entitled to vote on the resolution to ratify and approve the Rights Plan.

Background

In considering whether to adopt the Rights Plan, the Board considered the current legislative framework in Canada governing takeover bids. Under provincial securities legislation, a takeover bid generally means an offer to acquire voting or equity shares of a person or persons, where the shares subject to the offer to acquire, together with shares already owned by the bidder and certain related parties thereto, aggregate 20% or more of the outstanding shares.

The existing legislative framework for takeover bids in Canada raises the following concerns for shareholders:

1.

Time

Current legislation permits a takeover bid to expire 35 days after it is initiated. The Board is of the view that this may not be sufficient time to permit shareholders to consider a takeover bid and to make a reasoned decision about the merits of a takeover bid.

2.

Pressure to Tender

A shareholder may feel compelled to tender to a takeover bid which the shareholder considers to be inadequate out of a concern that in failing to do so, the shareholder may be left with illiquid or minority discounted shares. This is particularly so in the case of a takeover bid for less than all Company’s shares, where the bidder wishes to obtain a control position but does not wish to acquire all of the Company’s shares. The Rights Plan provides a mechanism which is intended to ensure that a shareholder can separate the decision with respect to the bid from the decision to tender, lessening undue pressure to tender.

3.

Full Value

The Board was also concerned that a person seeking such control might attempt, among other things, a gradual accumulation of the Company’s shares in the open market; the accumulation of a large block of shares in a highly compressed period of time from institutional shareholders and professional speculators or arbitrageurs; or an offer for any or all of the Company’s shares at what the Board considers to be less than full and fair value. The Rights Plan is intended to restrict the acquisition of more than 20% of the Company’s outstanding shares in such a manner. The Rights Plan is designed to encourage any bidder to provide shareholders with equal treatment in a takeover and full value for their investment.

The Rights Plan should provide adequate time for shareholders to assess a bid and to permit competing bids to emerge. It also gives the Board sufficient time to explore other options. A potential bidder can avoid the dilutive features of the Rights Plan by making a bid that conforms to the conditions specified in the Rights Plan.

To qualify as a permitted bid under the Rights Plan, a takeover bid must be made to all shareholders other than the “Offeror” and be open for 60 days after the bid is made. If at least 50% of the Company’s common shares subject to the bid that are not held by the bidder are deposited, the bidder may take up and pay for such shares and the bid must remain open for a further period of 10 clear business days on the same terms. See “Permitted Bid and Competing Permitted Bid Requirements” below.

Summary of the Rights Plan

The following is a summary of the principal terms of the Rights Plan which is qualified in its entirety by reference to the text of the Rights Plan. A copy of the Rights Plan is available on SEDAR atwww.sedar.com. Capitalized terms that are not defined herein have the meaning ascribed to them in the Rights Plan.

Effective Date

The effective date of the Rights Plan (the “Effective Date”) is August 26, 2009 subject to the ratification by the shareholders at the Meeting.

Term

If the Rights Plan is ratified and approved at the Meeting, it will remain in force until the earlier of the Expiration Time and the termination of the annual meeting of the shareholders in the year 2012 unless at or prior to such meeting the shareholders ratify the continued existence of the Rights Plan (subject to earlier expiry in the event of (i) the redemption of the Rights (as defined below); or (ii) the exchange of Rights for debt or equity securities or assets (or a combination thereof), all as more particularly set out in the Rights Plan (the “Expiration Time”).

Issue of Rights

On the Effective Date, one right (a “Right”) was issued and attached to each of the Company’s outstanding shares and one Right was issued and will continue to be issued in respect of each share of the Company issued thereafter, prior to the earlier of the Separation Time (as defined below) and the Expiration Time.

Rights Exercise Privilege

The Rights will separate from the shares and become exercisable at the Separation Time (as defined below). After the Separation Time, but prior to the occurrence of a Flip-in Event (as defined below), each Right may be exercised to purchase one share at an exercise price per Right of CAD 64(the “Exercise Price”).

Flip-in Event and Exchange Option

Subject to certain customary exceptions, upon the acquisition by a person of 20% or more of the shares of the Company and that person becoming an Acquiring Person (a “Flip-in Event”) and following the Separation Time, each Right, other than a Right beneficially owned by an Acquiring Person, its affiliates and associates, their respective joint actors and certain transferees, may be exercised to purchase that number of shares which have a market value equal to two times the Exercise Price. Rights Beneficially Owned by an Acquiring Person, its affiliates and associates, their respective joint actors and certain transferees will be void. The Rights Plan provides that a person (a “Grandfathered Person”) who is the Beneficial Owner of 20% or more of the outstanding shares determined as at the Record Time shall not be an Acquiring Person unless, after the Rec ord Time, that person becomes the Beneficial Owner of any additional shares (to the knowledge of the Board, there are no Grandfathered Persons). The Board of Directors is authorized, after a Flip-in Event has occurred, to issue or deliver, in return for the Rights and on payment of the relevant exercise price or without charge, debt, equity or other securities or assets of the Company or a combination thereof.

Certificates and Transferability

Prior to the earlier of the Separation Time (as defined below) and the Expiration Time, the Rights will be evidenced by a legend imprinted on certificates for shares of the Company issued from and after the Effective Date and will not be transferable separately from the shares. From and after the Separation Time (as defined below) and prior to the Expiration Time, the Rights will be evidenced by Rights Certificates which will be transferable and traded separately from the shares of the Company.

Separation Time

“Separation Time” means, subject to Section 5.2 of the Rights Plan, the close of business on the tenth trading day after the earliest of:

(a)

the Stock Acquisition Date, being the first date of public announcement by the Company or a person of facts indicating that a person has become an Acquiring Person;

(b)

the date of commencement of, or first public announcement of the intent of any Person (other than the Company or any Subsidiary of the Company) to commence a takeover bid (other than a Permitted Bid or a Competing Permitted Bid); and

(c)

the date upon which a Permitted Bid or Competing Permitted Bid ceases to be such;

or such later date as may be determined by the Board acting in good faith, provided that if the foregoing results in a Separation Time being prior to Record Time, the Separation Time shall be the Record Time, and provided further that if any takeover bid referred to in clause (b) of this definition expires, is cancelled, terminated or otherwise withdrawn prior to the Separation Time, such takeover bid shall be deemed, for the purposes of this definition, never to have been made.

Permitted Bid and Competing Permitted Bid Requirements

The requirements for a Permitted Bid include the following:

(a)

the takeover bid must be made for all shares of the Company and by way of a takeover bid circular;

(b)

the takeover bid must be made to all shareholders;

(c)

the takeover bid must be outstanding for a minimum period 60 days and shares of the Company tendered pursuant to the takeover bid may not be taken up prior to the expiry of the 60 days period and only if at such time more than 50% of the shares of the Company held by Independent Shareholders have been tendered to the takeover bid and not withdrawn; and

(d)