UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

| | | | | | | | |

| ☒ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | |

For the quarterly period ended September 30, 2021

OR

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from to . |

| | | | | | | | | | | |

| (Exact name of registrant as specified in its charter) | Commission file number | State or other jurisdiction of incorporation or organization | (I.R.S. Employer Identification No.) |

| Crestwood Equity Partners LP | 001-34664 | Delaware | 43-1918951 |

| Crestwood Midstream Partners LP | 001-35377 | Delaware | 20-1647837 |

| | | | | | | | | | | | | | |

| 811 Main Street | Suite 3400 | Houston | Texas | 77002 |

| (Address of principal executive offices) | | | | (Zip code) |

(832) 519-2200

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | |

| Title of each class | Trading Symbol | Name of each exchange on which registered |

| Crestwood Equity Partners LP | Common Units representing limited partnership interests | CEQP | New York Stock Exchange |

| Crestwood Equity Partners LP | Preferred Units representing limited partnership interests | CEQP-P | New York Stock Exchange |

| Crestwood Midstream Partners LP | None | None | None |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| Crestwood Equity Partners LP | | Yes | ☒ | No | ☐ | |

| Crestwood Midstream Partners LP | | Yes | ☒ | No | ☐ | |

(Explanatory Note: Crestwood Midstream Partners LP is currently a voluntary filer and is not subject to the filing requirements of the Securities Exchange Act of 1934. Although not subject to these filing requirements, Crestwood Midstream Partners LP has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months.)

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

| | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| Crestwood Equity Partners LP | | Yes | ☒ | No | ☐ | |

| Crestwood Midstream Partners LP | | Yes | ☒ | No | ☐ | |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | |

| Crestwood Equity Partners LP | Large accelerated filer | ☒ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | ☐ | Emerging growth company | ☐ |

| Crestwood Midstream Partners LP | Large accelerated filer | ☐ | Accelerated filer | ☐ | Non-accelerated filer | ☒ | Smaller reporting company | ☐ | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange act.

| | | | | | | | |

| Crestwood Equity Partners LP | | ☐ |

| Crestwood Midstream Partners LP | | ☐ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| Crestwood Equity Partners LP | | Yes | ☐ | No | ☒ | |

| Crestwood Midstream Partners LP | | Yes | ☐ | No | ☒ | |

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date (October 21, 2021).

| | | | | | | | |

| | |

| Crestwood Equity Partners LP | | 62,899,539 |

| Crestwood Midstream Partners LP | | None |

Crestwood Midstream Partners LP, as a wholly-owned subsidiary of a reporting company, meets the conditions set forth in General Instruction H(1)(a) and (b) of Form 10-Q and is therefore filing this report with the reduced disclosure format as permitted by such instruction.

CRESTWOOD EQUITY PARTNERS LP

CRESTWOOD MIDSTREAM PARTNERS LP

INDEX TO FORM 10-Q

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements

CRESTWOOD EQUITY PARTNERS LP

CONSOLIDATED BALANCE SHEETS

(in millions, except unit information)

| | | | | | | | | | | |

| September 30,

2021 | | December 31,

2020 |

| | (unaudited) | | |

| Assets | | | |

| Current assets: | | | |

| Cash | $ | 14.3 | | | $ | 14.0 | |

| | | |

Accounts receivable, less allowance for doubtful accounts of $1.4 million and $0.9 million at September 30, 2021 and December 31, 2020 | 420.0 | | | 262.2 | |

| Inventory | 175.0 | | | 89.1 | |

| Assets from price risk management activities | 39.1 | | | 27.2 | |

| | | |

| Prepaid expenses and other current assets | 7.1 | | | 13.4 | |

| Total current assets | 655.5 | | | 405.9 | |

| Property, plant and equipment | 3,788.5 | | | 3,759.6 | |

| Less: accumulated depreciation | 962.7 | | | 842.5 | |

| Property, plant and equipment, net | 2,825.8 | | | 2,917.1 | |

| Intangible assets | 1,126.1 | | | 1,126.1 | |

| Less: accumulated amortization | 377.9 | | | 331.8 | |

| Intangible assets, net | 748.2 | | | 794.3 | |

| Goodwill | 138.6 | | | 138.6 | |

| Operating lease right-of-use assets, net | 31.1 | | | 36.8 | |

| Investments in unconsolidated affiliates | 168.0 | | | 943.7 | |

| Other non-current assets | 7.3 | | | 7.3 | |

| Total assets | $ | 4,574.5 | | | $ | 5,243.7 | |

| | | |

| Liabilities and capital | | | |

| Current liabilities: | | | |

| Accounts payable | $ | 358.7 | | | $ | 160.3 | |

| Accrued expenses and other liabilities | 140.5 | | | 122.0 | |

| Liabilities from price risk management activities | 277.3 | | | 76.3 | |

| Contingent consideration, current portion | — | | | 19.0 | |

| Current portion of long-term debt | 0.2 | | | 0.2 | |

| Total current liabilities | 776.7 | | | 377.8 | |

| Long-term debt, less current portion | 2,024.9 | | | 2,483.8 | |

| Contingent consideration | — | | | 38.0 | |

| Other long-term liabilities | 259.8 | | | 253.3 | |

| Deferred income taxes | 2.3 | | | 2.7 | |

| Total liabilities | 3,063.7 | | | 3,155.6 | |

Commitments and contingencies (Note 9) | 0 | | 0 |

Interest of non-controlling partner in subsidiary (Note 11) | 434.5 | | | 432.7 | |

| Crestwood Equity Partners LP partners’ capital (62,897,480 common units issued and outstanding at September 30, 2021 and 73,970,208 common and subordinated units issued and outstanding at December 31, 2020) | 464.3 | | | 1,043.4 | |

| Preferred units (71,257,445 units issued and outstanding at both September 30, 2021 and December 31, 2020) | 612.0 | | | 612.0 | |

| Total partners’ capital | 1,076.3 | | | 1,655.4 | |

| Total liabilities and capital | $ | 4,574.5 | | | $ | 5,243.7 | |

See accompanying notes.

| | | | | | | | | | | | | | | | | | | | | | | |

CRESTWOOD EQUITY PARTNERS LP CONSOLIDATED STATEMENTS OF OPERATIONS (in millions, except per unit data) (unaudited)

|

| Three Months Ended | | Nine Months Ended |

| | September 30, | | September 30, |

| | 2021 | | 2020 | | 2021 | | 2020 |

| Revenues: | | | | | | | |

| Product revenues: | | | | | | | |

| Gathering and processing | $ | 82.0 | | | $ | 54.0 | | | $ | 237.2 | | | $ | 187.2 | |

| | | | | | | |

| Marketing, supply and logistics | 1,038.8 | | | 352.5 | | | 2,634.9 | | | 1,069.5 | |

Related party (Note 15) | 6.5 | | | 10.7 | | | 24.2 | | | 25.4 | |

| 1,127.3 | | | 417.2 | | | 2,896.3 | | | 1,282.1 | |

| Services revenues: | | | | | | | |

| Gathering and processing | 88.8 | | | 91.2 | | | 261.1 | | | 287.4 | |

| Storage and transportation | 2.0 | | | 3.5 | | | 6.0 | | | 10.1 | |

| Marketing, supply and logistics | 7.6 | | | 7.1 | | | 24.2 | | | 19.7 | |

Related party (Note 15) | 0.6 | | | 0.2 | | | 1.0 | | | 0.5 | |

| 99.0 | | | 102.0 | | | 292.3 | | | 317.7 | |

| Total revenues | 1,226.3 | | | 519.2 | | | 3,188.6 | | | 1,599.8 | |

| | | | | | | |

| Costs of product/services sold (exclusive of items shown separately below): | | | | | | | |

| Product costs | 1,060.2 | | | 348.2 | | | 2,595.8 | | | 1,090.2 | |

Product costs - related party (Note 15) | 34.8 | | | 6.1 | | | 101.3 | | | 12.9 | |

| Service costs | 4.3 | | | 4.4 | | | 13.2 | | | 15.7 | |

| Total costs of products/services sold | 1,099.3 | | | 358.7 | | | 2,710.3 | | | 1,118.8 | |

| | | | | | | |

| Operating expenses and other: | | | | | | | |

| Operations and maintenance | 31.6 | | | 31.0 | | | 90.2 | | | 100.2 | |

| General and administrative | 25.9 | | | 19.6 | | | 67.4 | | | 64.0 | |

| Depreciation, amortization and accretion | 64.6 | | | 60.8 | | | 182.6 | | | 177.9 | |

| Loss on long-lived assets, net | 18.5 | | | 21.3 | | | 19.6 | | | 26.1 | |

| Goodwill impairment | — | | | — | | | — | | | 80.3 | |

| | | | | | | |

| 140.6 | | | 132.7 | | | 359.8 | | | 448.5 | |

| Operating income (loss) | (13.6) | | | 27.8 | | | 118.5 | | | 32.5 | |

| Earnings (loss) from unconsolidated affiliates, net | 4.9 | | | 10.5 | | | (125.9) | | | 24.4 | |

| Interest and debt expense, net | (30.9) | | | (33.7) | | | (102.0) | | | (100.3) | |

| Loss on modification/extinguishment of debt | — | | | — | | | (6.7) | | | — | |

| Other income, net | 0.1 | | | — | | | 0.2 | | | 0.2 | |

| Income (loss) before income taxes | (39.5) | | | 4.6 | | | (115.9) | | | (43.2) | |

| (Provision) benefit for income taxes | (0.1) | | | — | | | (0.1) | | | 0.1 | |

| Net income (loss) | (39.6) | | | 4.6 | | | (116.0) | | | (43.1) | |

| Net income attributable to non-controlling partner | 10.3 | | | 10.3 | | | 30.7 | | | 30.4 | |

| | | | | | | |

| | | | | | | |

| Net loss attributable to Crestwood Equity Partners LP | (49.9) | | | (5.7) | | | (146.7) | | | (73.5) | |

| Net income attributable to preferred units | 15.0 | | | 15.0 | | | 45.0 | | | 45.0 | |

| Net loss attributable to partners | $ | (64.9) | | | $ | (20.7) | | | $ | (191.7) | | | $ | (118.5) | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

CRESTWOOD EQUITY PARTNERS LP CONSOLIDATED STATEMENTS OF OPERATIONS (continued) (in millions, except per unit data) (unaudited)

|

| Three Months Ended | | Nine Months Ended |

| September 30, | | September 30, |

| 2021 | | 2020 | | 2021 | | 2020 |

Net loss per limited partner unit: (Note 12) | | | | | | | |

| Basic and Diluted | $ | (1.03) | | | $ | (0.28) | | | $ | (2.88) | | | $ | (1.62) | |

| | | | | | | |

| Weighted-average limited partners’ units outstanding: | | | | | | | |

| Basic and Diluted | 62.9 | | | 73.4 | | | 66.6 | | | 73.1 | |

See accompanying notes.

CRESTWOOD EQUITY PARTNERS LP

CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME

(in millions)

(unaudited)

| | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended | | Nine Months Ended |

| September 30, | | September 30, |

| 2021 | | 2020 | | 2021 | | 2020 |

| Net income (loss) | $ | (39.6) | | | $ | 4.6 | | | $ | (116.0) | | | $ | (43.1) | |

| Change in fair value of Suburban Propane Partners, L.P. units | — | | | 0.3 | | | — | | | (0.8) | |

| Comprehensive income (loss) | (39.6) | | | 4.9 | | | (116.0) | | | (43.9) | |

| Comprehensive income attributable to non-controlling partner | 10.3 | | | 10.3 | | | 30.7 | | | 30.4 | |

| Comprehensive loss attributable to Crestwood Equity Partners LP | $ | (49.9) | | | $ | (5.4) | | | $ | (146.7) | | | $ | (74.3) | |

See accompanying notes.

CRESTWOOD EQUITY PARTNERS LP

CONSOLIDATED STATEMENTS OF PARTNERS’ CAPITAL

(in millions)

(unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Preferred | | Partners | | | | |

| Units | | Capital | | Common Units | | Subordinated Units | | Capital | | | | Total Partners’

Capital |

| Balance at December 31, 2020 | 71.3 | | | $ | 612.0 | | | 73.6 | | | 0.4 | | | $ | 1,043.4 | | | | | $ | 1,655.4 | |

Crestwood Holdings Transactions (Note 11) | — | | | — | | | — | | | — | | | (273.2) | | | | | (273.2) | |

Retirement of units (Note 11) | — | | | — | | | (11.5) | | | (0.4) | | | — | | | | | — | |

| Distributions to partners | — | | | (15.0) | | | — | | | — | | | (46.4) | | | | | (61.4) | |

| Unit-based compensation charges | — | | | — | | | 1.1 | | | — | | | 3.7 | | | | | 3.7 | |

| | | | | | | | | | | | | |

| Taxes paid for unit-based compensation vesting | — | | | — | | | (0.4) | | | — | | | (8.1) | | | | | (8.1) | |

| Other | — | | | — | | | — | | | — | | | (0.4) | | | | | (0.4) | |

| Net income (loss) | — | | | 15.0 | | | — | | | — | | | (63.4) | | | | | (48.4) | |

| Balance at March 31, 2021 | 71.3 | | | 612.0 | | | 62.8 | | | — | | | 655.6 | | | | | 1,267.6 | |

| Distributions to partners | — | | | (15.0) | | | — | | | — | | | (39.3) | | | | | (54.3) | |

| Unit-based compensation charges | — | | | — | | | — | | | — | | | 7.6 | | | | | 7.6 | |

| Taxes paid for unit-based compensation vesting | — | | | — | | | — | | | — | | | (0.1) | | | | | (0.1) | |

| Other | — | | | — | | | — | | | — | | | (0.3) | | | | | (0.3) | |

| Net income (loss) | — | | | 15.0 | | | — | | | — | | | (63.4) | | | | | (48.4) | |

| Balance at June 30, 2021 | 71.3 | | | 612.0 | | | 62.8 | | | — | | | 560.1 | | | | | 1,172.1 | |

| Distributions to partners | — | | | (15.0) | | | — | | | — | | | (39.3) | | | | | (54.3) | |

| Unit-based compensation charges | — | | | — | | | 0.1 | | | — | | | 9.6 | | | | | 9.6 | |

| Taxes paid for unit-based compensation vesting | — | | | — | | | — | | | — | | | (0.1) | | | | | (0.1) | |

| Other | — | | | — | | | — | | | — | | | (1.1) | | | | | (1.1) | |

| Net income (loss) | — | | | 15.0 | | | — | | | — | | | (64.9) | | | | | (49.9) | |

| Balance at September 30, 2021 | 71.3 | | | $ | 612.0 | | | 62.9 | | | — | | | $ | 464.3 | | | | | $ | 1,076.3 | |

CRESTWOOD EQUITY PARTNERS LP

CONSOLIDATED STATEMENTS OF PARTNERS’ CAPITAL (continued)

(in millions)

(unaudited)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Preferred | | Partners | | |

| Units | | Capital | | Common Units | | Subordinated Units | | Capital | | Total Partners’

Capital |

| Balance at December 31, 2019 | 71.3 | | | $ | 612.0 | | | 71.9 | | | 0.4 | | | $ | 1,320.8 | | | $ | 1,932.8 | |

| Distributions to partners | — | | | (15.0) | | | — | | | — | | | (45.3) | | | (60.3) | |

| Unit-based compensation charges | — | | | — | | | 1.7 | | | — | | | 0.2 | | | 0.2 | |

| Taxes paid for unit-based compensation vesting | — | | | — | | | (0.5) | | | — | | | (15.1) | | | (15.1) | |

| Change in fair value of Suburban Propane Partners, L.P. units | — | | | — | | | — | | | — | | | (1.1) | | | (1.1) | |

| Other | — | | | — | | | 0.2 | | | — | | | 3.5 | | | 3.5 | |

| Net income (loss) | — | | | 15.0 | | | — | | | — | | | (48.3) | | | (33.3) | |

| Balance at March 31, 2020 | 71.3 | | | 612.0 | | | 73.3 | | | 0.4 | | | 1,214.7 | | | 1,826.7 | |

| Distributions to partners | — | | | (15.0) | | | — | | | — | | | (45.7) | | | (60.7) | |

| Unit-based compensation charges | — | | | — | | | — | | | — | | | 13.6 | | | 13.6 | |

| Taxes paid for unit-based compensation vesting | — | | | — | | | (0.1) | | | — | | | (0.4) | | | (0.4) | |

| | | | | | | | | | | |

| | | | | | | | | | | |

| Other | — | | | — | | | — | | | — | | | (0.1) | | | (0.1) | |

| Net income (loss) | — | | | 15.0 | | | — | | | — | | | (49.5) | | | (34.5) | |

| Balance at June 30, 2020 | 71.3 | | | 612.0 | | | 73.2 | | | 0.4 | | | 1,132.6 | | | 1,744.6 | |

| Distributions to partners | — | | | (15.0) | | | — | | | — | | | (45.7) | | | (60.7) | |

| Unit-based compensation charges | — | | | — | | | 0.4 | | | — | | | 7.1 | | | 7.1 | |

| Taxes paid for unit-based compensation vesting | — | | | — | | | — | | | — | | | (0.1) | | | (0.1) | |

| Change in fair value of Suburban Propane Partners, L.P. units | — | | | — | | | — | | | — | | | 0.3 | | | 0.3 | |

| Other | — | | | — | | | — | | | — | | | (0.3) | | | (0.3) | |

| Net income (loss) | — | | | 15.0 | | | — | | | — | | | (20.7) | | | (5.7) | |

| Balance at September 30, 2020 | 71.3 | | | $ | 612.0 | | | 73.6 | | | 0.4 | | | $ | 1,073.2 | | | $ | 1,685.2 | |

See accompanying notes.

CRESTWOOD EQUITY PARTNERS LP

CONSOLIDATED STATEMENTS OF CASH FLOWS

(in millions)

(unaudited)

| | | | | | | | | | | |

| Nine Months Ended |

| | September 30, |

| | 2021 | | 2020 |

| Operating activities | | | |

| Net loss | $ | (116.0) | | | $ | (43.1) | |

| Adjustments to reconcile net loss to net cash provided by operating activities: | | | |

| Depreciation, amortization and accretion | 182.6 | | | 177.9 | |

| Amortization of debt-related deferred costs | 5.1 | | | 4.9 | |

| | | |

| Unit-based compensation charges | 22.8 | | | 17.3 | |

| Loss on long-lived assets, net | 19.6 | | | 26.1 | |

| | | |

| Goodwill impairment | — | | | 80.3 | |

| | | |

| Loss on modification/extinguishment of debt | 6.7 | | | — | |

| (Earnings) loss from unconsolidated affiliates, net, adjusted for cash distributions received | 137.5 | | | 5.4 | |

| Deferred income taxes | (0.4) | | | (0.4) | |

| | | |

| Other | 0.2 | | | — | |

| Changes in operating assets and liabilities | 114.8 | | | 26.9 | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Net cash provided by operating activities | 372.9 | | | 295.3 | |

| Investing activities | | | |

Acquisition, net of cash acquired (Note 3) | — | | | (162.3) | |

| Purchases of property, plant and equipment | (55.8) | | | (158.8) | |

| Investments in unconsolidated affiliates | (10.2) | | | (6.0) | |

| Capital distributions from unconsolidated affiliates | 648.4 | | | 27.8 | |

| | | |

| Other | 0.5 | | | 1.6 | |

| Net cash provided by (used in) investing activities | 582.9 | | | (297.7) | |

| Financing activities | | | |

| Proceeds from the issuance of long-term debt | 2,236.4 | | | 947.0 | |

| Payments on long-term debt | (2,695.9) | | | (731.1) | |

| Payments on finance leases | (2.1) | | | (2.4) | |

| Payments for deferred financing costs | (11.1) | | | — | |

| | | |

| | | |

| | | |

| Net proceeds from issuance of non-controlling interest | 1.0 | | | 2.8 | |

| Payments for Crestwood Holdings Transactions | (275.6) | | | — | |

| Distributions to partners | (125.0) | | | (136.7) | |

| Distributions to non-controlling partner | (29.9) | | | (27.8) | |

| | | |

| Distributions to preferred unitholders | (45.0) | | | (45.0) | |

| | | |

| Taxes paid for unit-based compensation vesting | (8.3) | | | (15.6) | |

| | | |

| Net cash used in financing activities | (955.5) | | | (8.8) | |

| Net change in cash | 0.3 | | | (11.2) | |

| Cash at beginning of period | 14.0 | | | 25.7 | |

| Cash at end of period | $ | 14.3 | | | $ | 14.5 | |

| Supplemental schedule of noncash investing activities | | | |

| Net change to property, plant and equipment through accounts payable and accrued expenses | $ | (9.2) | | | $ | 40.0 | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

See accompanying notes.

CRESTWOOD MIDSTREAM PARTNERS LP

CONSOLIDATED BALANCE SHEETS

(in millions)

| | | | | | | | | | | |

| September 30,

2021 | | December 31,

2020 |

| (unaudited) | | |

| Assets | | | |

| Current assets: | | | |

| Cash | $ | 13.9 | | | $ | 13.7 | |

| | | |

Accounts receivable, less allowance for doubtful accounts of $1.4 million and $0.9 million at September 30, 2021 and December 31, 2020 | 420.0 | | | 262.2 | |

| Inventory | 175.0 | | | 89.1 | |

| Assets from price risk management activities | 39.1 | | | 27.2 | |

| | | |

| Prepaid expenses and other current assets | 7.1 | | | 13.4 | |

| Total current assets | 655.1 | | | 405.6 | |

| Property, plant and equipment | 4,118.6 | | | 4,089.6 | |

| Less: accumulated depreciation | 1,159.1 | | | 1,028.3 | |

| Property, plant and equipment, net | 2,959.5 | | | 3,061.3 | |

| Intangible assets | 1,126.1 | | | 1,126.1 | |

| Less: accumulated amortization | 377.9 | | | 331.8 | |

| Intangible assets, net | 748.2 | | | 794.3 | |

| Goodwill | 138.6 | | | 138.6 | |

| Operating lease right-of-use assets, net | 31.1 | | | 36.8 | |

| Investments in unconsolidated affiliates | 168.0 | | | 943.7 | |

| Other non-current assets | 5.1 | | | 5.2 | |

| Total assets | $ | 4,705.6 | | | $ | 5,385.5 | |

| Liabilities and capital | | | |

| Current liabilities: | | | |

| Accounts payable | $ | 358.6 | | | $ | 157.8 | |

| Accrued expenses and other liabilities | 139.3 | | | 120.1 | |

| Liabilities from price risk management activities | 277.3 | | | 76.3 | |

| Contingent consideration, current portion | — | | | 19.0 | |

| Current portion of long-term debt | 0.2 | | | 0.2 | |

| Total current liabilities | 775.4 | | | 373.4 | |

| Long-term debt, less current portion | 2,024.9 | | | 2,483.8 | |

| Contingent consideration | — | | | 38.0 | |

| Other long-term liabilities | 256.6 | | | 251.8 | |

| Deferred income taxes | 0.7 | | | 0.7 | |

| Total liabilities | 3,057.6 | | | 3,147.7 | |

Commitments and contingencies (Note 9) | 0 | | 0 |

Interest of non-controlling partner in subsidiary (Note 11) | 434.5 | | | 432.7 | |

| Partners’ capital | 1,213.5 | | | 1,805.1 | |

| | | |

| | | |

| | | |

| Total liabilities and capital | $ | 4,705.6 | | | $ | 5,385.5 | |

See accompanying notes.

CRESTWOOD MIDSTREAM PARTNERS LP

CONSOLIDATED STATEMENTS OF OPERATIONS

(in millions)

(unaudited)

| | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended | | Nine Months Ended |

| September 30, | | September 30, |

| | 2021 | | 2020 | | 2021 | | 2020 |

| Revenues: | | | | | | | |

| Product revenues: | | | | | | | |

| Gathering and processing | $ | 82.0 | | | $ | 54.0 | | | $ | 237.2 | | | $ | 187.2 | |

| | | | | | | |

| Marketing, supply and logistics | 1,038.8 | | | 352.5 | | | 2,634.9 | | | 1,069.5 | |

Related party (Note 15) | 6.5 | | | 10.7 | | | 24.2 | | | 25.4 | |

| 1,127.3 | | | 417.2 | | | 2,896.3 | | | 1,282.1 | |

| Service revenues: | | | | | | | |

| Gathering and processing | 88.8 | | | 91.2 | | | 261.1 | | | 287.4 | |

| Storage and transportation | 2.0 | | | 3.5 | | | 6.0 | | | 10.1 | |

| Marketing, supply and logistics | 7.6 | | | 7.1 | | | 24.2 | | | 19.7 | |

Related party (Note 15) | 0.6 | | | 0.2 | | | 1.0 | | | 0.5 | |

| 99.0 | | | 102.0 | | | 292.3 | | | 317.7 | |

| Total revenues | 1,226.3 | | | 519.2 | | | 3,188.6 | | | 1,599.8 | |

| | | | | | | |

| Costs of product/services sold (exclusive of items shown separately below): | | | | | | | |

| Product costs | 1,060.2 | | | 348.2 | | | 2,595.8 | | | 1,090.2 | |

Product costs - related party (Note 15) | 34.8 | | | 6.1 | | | 101.3 | | | 12.9 | |

| Service costs | 4.3 | | | 4.4 | | | 13.2 | | | 15.7 | |

| Total costs of product/services sold | 1,099.3 | | | 358.7 | | | 2,710.3 | | | 1,118.8 | |

| | | | | | | |

| Operating expenses and other: | | | | | | | |

| Operations and maintenance | 31.6 | | | 31.0 | | | 90.2 | | | 100.2 | |

| General and administrative | 24.4 | | | 18.5 | | | 61.3 | | | 60.4 | |

| Depreciation, amortization and accretion | 68.2 | | | 64.2 | | | 193.2 | | | 188.4 | |

| Loss on long-lived assets, net | 18.5 | | | 21.3 | | | 19.6 | | | 26.1 | |

| Goodwill impairment | — | | | — | | | — | | | 80.3 | |

| | | | | | | |

| 142.7 | | | 135.0 | | | 364.3 | | | 455.4 | |

| Operating income (loss) | (15.7) | | | 25.5 | | | 114.0 | | | 25.6 | |

| Earnings (loss) from unconsolidated affiliates, net | 4.9 | | | 10.5 | | | (125.9) | | | 24.4 | |

| Interest and debt expense, net | (30.9) | | | (33.7) | | | (102.0) | | | (100.3) | |

| Loss on modification/extinguishment of debt | — | | | — | | | (6.7) | | | — | |

| Income (loss) before income taxes | (41.7) | | | 2.3 | | | (120.6) | | | (50.3) | |

| (Provision) benefit for income taxes | (0.1) | | | — | | | (0.1) | | | 0.2 | |

| Net income (loss) | (41.8) | | | 2.3 | | | (120.7) | | | (50.1) | |

| Net income attributable to non-controlling partner | 10.3 | | | 10.3 | | | 30.7 | | | 30.4 | |

| Net loss attributable to Crestwood Midstream Partners LP | $ | (52.1) | | | $ | (8.0) | | | $ | (151.4) | | | $ | (80.5) | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | | |

| | | | | | |

| | | | | | | |

| | | | | | | |

See accompanying notes.

CRESTWOOD MIDSTREAM PARTNERS LP

CONSOLIDATED STATEMENTS OF PARTNERS’ CAPITAL

(in millions)

(unaudited)

| | | | | | | | | | | |

| | | | | | Total Partners’

Capital |

| Balance at December 31, 2020 | | | | | $ | 1,805.1 | |

| Distributions to partners | | | | | (334.0) | |

| Unit-based compensation charges | | | | | 2.3 | |

| Taxes paid for unit-based compensation vesting | | | | | (8.1) | |

| Other | | | | | (0.1) | |

| Net loss | | | | | (50.5) | |

| Balance at March 31, 2021 | | | | | 1,414.7 | |

| Distributions to partners | | | | | (61.4) | |

| Unit-based compensation charges | | | | | 7.6 | |

| Taxes paid for unit-based compensation vesting | | | | | (0.1) | |

| | | | | |

| Net loss | | | | | (48.8) | |

| Balance at June 30, 2021 | | | | | 1,312.0 | |

| Distributions to partners | | | | | (55.9) | |

| Unit-based compensation charges | | | | | 9.6 | |

| Taxes paid for unit-based compensation vesting | | | | | (0.1) | |

| | | | | |

| Net loss | | | | | (52.1) | |

| Balance at September 30, 2021 | | | | | $ | 1,213.5 | |

| | | | | | | | | | | | |

| | | | | | | Total Partners’

Capital |

| Balance at December 31, 2019 | | | | | | $ | 2,099.3 | |

| Distributions to partners | | | | | | (57.0) | |

| Unit-based compensation charges | | | | | | (4.4) | |

| Taxes paid for unit-based compensation vesting | | | | | | (15.1) | |

| Other | | | | | | (1.1) | |

| Net loss | | | | | | (35.5) | |

| Balance at March 31, 2020 | | | | | | 1,986.2 | |

| Distributions to partners | | | | | | (62.0) | |

| Unit-based compensation charges | | | | | | 13.6 | |

| Taxes paid for unit-based compensation vesting | | | | | | (0.4) | |

| Other | | | | | | 0.1 | |

| Net loss | | | | | | (37.0) | |

| Balance at June 30, 2020 | | | | | | 1,900.5 | |

| Distributions to partners | | | | | | (61.9) | |

| Unit-based compensation charges | | | | | | 7.1 | |

| Taxes paid for unit-based compensation vesting | | | | | | (0.1) | |

| Other | | | | | | (0.1) | |

| Net loss | | | | | | (8.0) | |

| Balance at September 30, 2020 | | | | | | $ | 1,837.5 | |

See accompanying notes.

CRESTWOOD MIDSTREAM PARTNERS LP

CONSOLIDATED STATEMENTS OF CASH FLOWS

(in millions)

(unaudited)

| | | | | | | | | | | |

| Nine Months Ended |

| | September 30, |

| | 2021 | | 2020 |

| Operating activities | | | |

| Net loss | $ | (120.7) | | | $ | (50.1) | |

| Adjustments to reconcile net loss to net cash provided by operating activities: | | | |

| Depreciation, amortization and accretion | 193.2 | | | 188.4 | |

| Amortization of debt-related deferred costs | 5.1 | | | 4.9 | |

| Unit-based compensation charges | 22.8 | | | 17.3 | |

| Loss on long-lived assets, net | 19.6 | | | 26.1 | |

| Goodwill impairment | — | | | 80.3 | |

| | | |

| Loss on modification/extinguishment of debt | 6.7 | | | — | |

| (Earnings) loss from unconsolidated affiliates, net, adjusted for cash distributions received | 137.5 | | | 5.4 | |

| Deferred income taxes | — | | | (0.1) | |

| Other | 0.2 | | | — | |

| Changes in operating assets and liabilities | 114.1 | | | 21.8 | |

| Net cash provided by operating activities | 378.5 | | | 294.0 | |

| Investing activities | | | |

Acquisition, net of cash acquired (Note 3) | — | | | (162.3) | |

| Purchases of property, plant and equipment | (55.8) | | | (158.8) | |

| Investments in unconsolidated affiliates | (10.2) | | | (6.0) | |

| Capital distributions from unconsolidated affiliates | 648.4 | | | 27.8 | |

| | | |

| Other | 0.5 | | | 1.6 | |

| Net cash provided by (used in) investing activities | 582.9 | | | (297.7) | |

| Financing activities | | | |

| Proceeds from the issuance of long-term debt | 2,236.4 | | | 947.0 | |

| Payments on long-term debt | (2,695.9) | | | (731.1) | |

| Payments on finance leases | (2.1) | | | (2.4) | |

| Payments for deferred financing costs | (11.1) | | | — | |

| | | |

| | | |

| Net proceeds from issuance of non-controlling interest | 1.0 | | | 2.8 | |

| Distributions to partners | (451.3) | | | (180.9) | |

| Distributions to non-controlling partner | (29.9) | | | (27.8) | |

| | | |

| | | |

| | | |

| | | |

| Taxes paid for unit-based compensation vesting | (8.3) | | | (15.6) | |

| | | |

| Net cash used in financing activities | (961.2) | | | (8.0) | |

| Net change in cash | 0.2 | | | (11.7) | |

| Cash at beginning of period | 13.7 | | | 25.4 | |

| Cash at end of period | $ | 13.9 | | | $ | 13.7 | |

| Supplemental schedule of noncash investing activities | | | |

| Net change to property, plant and equipment through accounts payable and accrued expenses | $ | (9.2) | | | $ | 40.0 | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

See accompanying notes.

CRESTWOOD EQUITY PARTNERS LP

CRESTWOOD MIDSTREAM PARTNERS LP

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

Note 1 – Organization and Business Description

The accompanying notes to the consolidated financial statements apply to Crestwood Equity Partners LP (Crestwood Equity or CEQP) and Crestwood Midstream Partners LP (Crestwood Midstream or CMLP), unless otherwise indicated.

The accompanying consolidated financial statements and related notes should be read in conjunction with our 2020 Annual Report on Form 10-K filed with the Securities and Exchange Commission (SEC) on February 26, 2021. The financial information as of September 30, 2021, and for the three and nine months ended September 30, 2021 and 2020, is unaudited. The consolidated balance sheets as of December 31, 2020 were derived from the audited balance sheets filed in our 2020 Annual Report on Form 10-K.

References in this report to “we,” “us,” “our,” “ours,” “our company,” the “partnership,” the “Company,” “Crestwood Equity,” “CEQP,” and similar terms refer to either Crestwood Equity Partners LP itself or Crestwood Equity Partners LP and its consolidated subsidiaries, as the context requires. Unless otherwise indicated, references to “Crestwood Midstream” and “CMLP” refer to either Crestwood Midstream Partners LP itself or Crestwood Midstream Partners LP and its consolidated subsidiaries.

Organization

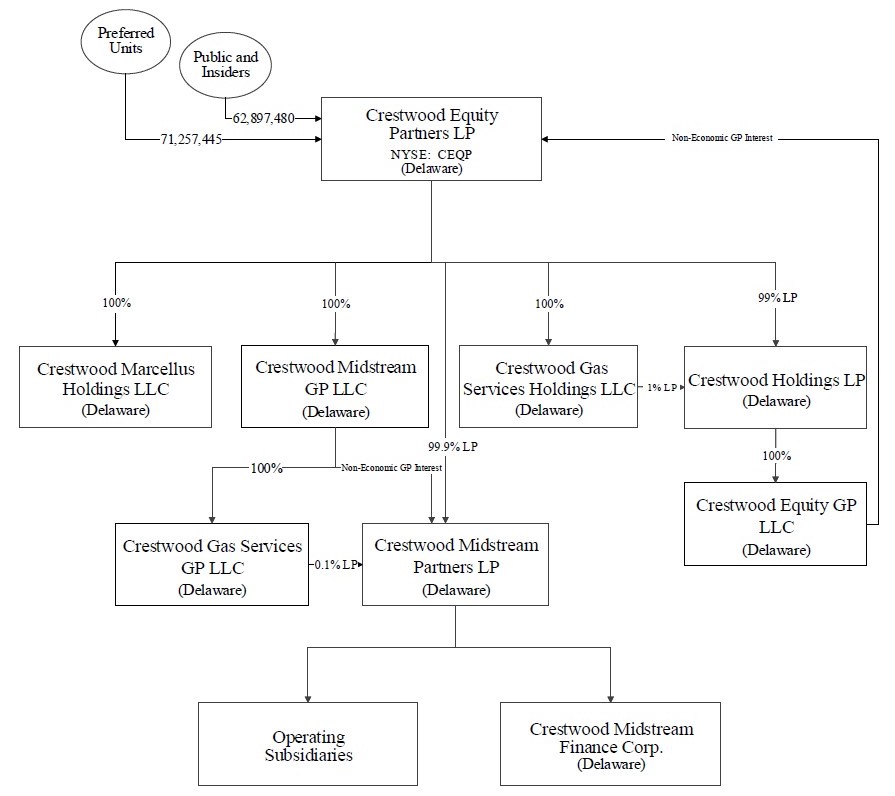

Crestwood Equity Partners LP. CEQP is a publicly-traded (NYSE: CEQP) Delaware limited partnership formed in March 2001. Crestwood Equity GP LLC (Crestwood Equity GP) owns our non-economic general partnership interest. Prior to the Crestwood Holdings Transactions described below, Crestwood Equity was indirectly owned by Crestwood Holdings LLC (Crestwood Holdings), which is substantially owned and controlled by First Reserve Management, L.P. (First Reserve).

Crestwood Midstream Partners LP. Crestwood Equity owns a 99.9% limited partnership interest in Crestwood Midstream and Crestwood Gas Services GP LLC (CGS GP), a wholly-owned subsidiary of Crestwood Equity, owns a 0.1% limited partnership interest in Crestwood Midstream. Crestwood Midstream GP LLC, a wholly-owned subsidiary of Crestwood Equity, owns the non-economic general partnership interest of Crestwood Midstream.

Crestwood Holdings Transactions. In March 2021, CEQP paid Crestwood Holdings approximately $268 million to (i) acquire approximately 11.5 million CEQP common units, 0.4 million subordinated units of CEQP and 100% of the equity interests of Crestwood Marcellus Holdings LLC and Crestwood Gas Services Holdings LLC (whose assets consisted solely of CEQP common and subordinated units and 1% of the limited partner interests in Crestwood Holdings LP) in March 2021; and (ii) acquire the general partner and the remaining 99% limited partner interests of Crestwood Holdings LP (whose assets consist solely of its ownership interest in Crestwood Equity GP, which owns CEQP’s non-economic general partner interest) in August 2021 (collectively, the Crestwood Holdings Transactions). The purchase price was funded through borrowings under the Crestwood Midstream credit facility. CEQP retired the common and subordinated units acquired in the Crestwood Holdings Transactions.

The diagram below reflects a simplified version our ownership structure as of September 30, 2021 following the Crestwood Holdings Transactions.

Business Description

Crestwood Equity develops, acquires, owns or controls, and operates primarily fee-based assets and operations within the energy midstream sector. We provide broad-ranging infrastructure solutions across the value chain to service premier liquids-rich natural gas and crude oil shale plays across the United States. We own and operate a diversified portfolio of natural gas liquids (NGLs), crude oil, natural gas and produced water gathering, processing, storage, disposal and transportation assets that connect fundamental energy supply with energy demand across the United States. Crestwood Equity is a holding company and all of its consolidated operating assets are owned by or through its wholly-owned subsidiary, Crestwood Midstream.

Our financial statements reflect 3 operating and reporting segments described below.

•Gathering and Processing. Our gathering and processing operations provide natural gas, crude oil and produced water gathering, compression, treating, processing and disposal services to producers in multiple unconventional resource plays in some of the largest shale plays in the United States in which we have established footprints in the “core of the core” areas.

•Storage and Transportation. Our storage and transportation operations provide crude oil and natural gas storage and transportation services to producers, utilities and other customers.

•Marketing, Supply and Logistics. Our marketing, supply and logistics operations provide NGLs, crude oil and natural gas marketing, storage, terminal and transportation services to producers, refiners, marketers and other customers.

Note 2 – Basis of Presentation and Summary of Significant Accounting Policies

Basis of Presentation

Our consolidated financial statements are prepared in accordance with Generally Accepted Accounting Principles (GAAP) and include the accounts of all consolidated subsidiaries after the elimination of all intercompany accounts and transactions. Certain amounts and footnote disclosures in the prior periods have been reclassified to conform to the current year presentation, none of which impacted our previously reported net income, earnings per unit or partners’ capital. In management’s opinion, all necessary adjustments to fairly present our results of operations, financial position and cash flows for the periods presented have been made and all such adjustments are of a normal and recurring nature. Certain information and footnote disclosures normally included in annual consolidated financial statements prepared in accordance with GAAP have been omitted pursuant to the rules and regulations of the SEC.

Significant Accounting Policies

There were no material changes in our significant accounting policies from those described in our 2020 Annual Report on Form 10-K. Below is an update of our accounting policies related to Property, Plant and Equipment and Goodwill.

During the three months ended September 30, 2021, we recorded a loss on long-lived assets of approximately $19 million related to the abandonment and dismantlement of certain of our gathering and processing segment’s Marcellus West Union compressor station assets. Our West Union compressor station assets were located in West Virginia and provided compression and dehydration services to our customers. During the three months ended September 30, 2020, we recorded a $19.9 million loss on long-lived assets related to the sale of our Fayetteville assets in October 2020 and during the nine months ended September 30, 2020 we recorded an $80.3 million full impairment of the goodwill associated with our Powder River Basin reporting unit based on events that occurred during 2020 which resulted in a significant decrease in the forecasted cash flows and fair value of the reporting unit. For a further discussion of this goodwill impairment, see our 2020 Annual Report on Form 10-K.

Note 3 – Acquisition

In April 2020, we acquired several NGL storage and rail-to-truck terminals from Plains All American Pipeline, L.P. for approximately $162 million. The acquired assets include 7 MMBbls of NGL storage and 7 terminals. These assets are included in our marketing, supply and logistics segment. The transaction costs related to this acquisition were not material during the three and nine months ended September 30, 2020.

Note 4 – Certain Balance Sheet Information

Accrued Expenses and Other Liabilities

Accrued expenses and other liabilities consisted of the following (in millions):

| | | | | | | | | | | | | | | | | | | | | | | |

| CEQP | | CMLP |

| September 30, | | December 31, | | September 30, | | December 31, |

| 2021 | | 2020 | | 2021 | | 2020 |

| Accrued expenses | $ | 51.1 | | | $ | 48.3 | | | $ | 49.9 | | | $ | 46.4 | |

| Accrued property taxes | 6.9 | | | 8.4 | | | 6.9 | | | 8.4 | |

| Income tax payable | 0.3 | | | 0.2 | | | 0.3 | | | 0.2 | |

| Interest payable | 36.7 | | | 24.9 | | | 36.7 | | | 24.9 | |

| Accrued additions to property, plant and equipment | 18.1 | | | 12.3 | | | 18.1 | | | 12.3 | |

| Operating leases | 14.5 | | | 14.7 | | | 14.5 | | | 14.7 | |

| Finance leases | 2.1 | | | 2.9 | | | 2.1 | | | 2.9 | |

| Deferred revenue | 10.8 | | | 10.3 | | | 10.8 | | | 10.3 | |

| | | | | | | |

| Total accrued expenses and other liabilities | $ | 140.5 | | | $ | 122.0 | | | $ | 139.3 | | | $ | 120.1 | |

Other Long-Term Liabilities

Other long-term liabilities consisted of the following (in millions):

| | | | | | | | | | | | | | | | | | | | | | | |

| CEQP | | CMLP |

| September 30, | | December 31, | | September 30, | | December 31, |

| 2021 | | 2020 | | 2021 | | 2020 |

| Contract liabilities | $ | 183.4 | | | $ | 172.2 | | | $ | 183.4 | | | $ | 172.2 | |

| Operating leases | 22.0 | | | 28.5 | | | 22.0 | | | 28.5 | |

| Asset retirement obligations | 35.6 | | | 34.1 | | | 35.6 | | | 34.1 | |

| Other | 18.8 | | | 18.5 | | | 15.6 | | | 17.0 | |

| Total other long-term liabilities | $ | 259.8 | | | $ | 253.3 | | | $ | 256.6 | | | $ | 251.8 | |

Note 5 - Investments in Unconsolidated Affiliates

Stagecoach Gas Divestiture

In July 2021, Stagecoach Gas sold certain of its wholly-owned subsidiaries to a subsidiary of Kinder Morgan, Inc. (Kinder Morgan) for approximately $1.195 billion plus certain purchase price adjustments (Initial Closing) pursuant to a purchase and sale agreement dated as of May 31, 2021 between our wholly-owned subsidiary, Crestwood Pipeline and Storage Northeast LLC (Crestwood Northeast), Con Edison Gas Pipeline and Storage Northeast, LLC (CEGP), a wholly-owned subsidiary of Consolidated Edison, Inc., Stagecoach Gas and Kinder Morgan. Following the Initial Closing and subject to certain customary closing conditions, Crestwood Northeast and CEGP will sell each of their equity interests in Stagecoach Gas and its wholly-owned subsidiary, Twin Tier Pipeline LLC, (Second Closing) to Kinder Morgan for approximately $30 million, subject to certain closing adjustments.

In conjunction with the Initial Closing, we recorded our share of a loss on long-lived assets (including goodwill) recorded by our Stagecoach Gas equity investment associated with the sale. This eliminated our $51.3 million historical basis difference between our investment balance and the equity in the underlying net assets of Stagecoach Gas, and also resulted in a $155.4 million reduction in our earnings from unconsolidated affiliates during the nine months ended September 30, 2021. In addition, our earnings from unconsolidated affiliates during the nine months ended September 30, 2021 were also reduced by our proportionate share of transaction costs of approximately $3.0 million related to the Initial Closing, which were paid by us in July 2021 on behalf of Stagecoach Gas. Our Stagecoach Gas investment is included in our storage and transportation segment.

Net Investments and Earnings (Loss) of Unconsolidated Affiliates

Our net investments in and earnings (loss) from our unconsolidated affiliates are as follows (in millions):

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Investment | | Earnings (Loss) from

Unconsolidated Affiliates | | Earnings (Loss) from

Unconsolidated Affiliates |

| | | | | | | Three Months Ended | | Nine Months Ended |

| | | September 30, | | December 31, | | September 30, | | September 30, |

| | | 2021 | | 2020 | | 2021 | | 2020 | | 2021 | | 2020 |

Stagecoach Gas Services LLC(1) | | | $ | 15.2 | | | $ | 792.5 | | | $ | 0.9 | | | $ | 9.9 | | | $ | (139.4) | | | $ | 28.3 | |

Tres Palacios Holdings LLC(2) | | | 38.4 | | | 35.5 | | | (0.1) | | | 0.1 | | | 9.1 | | | 0.2 | |

Powder River Basin Industrial Complex, LLC(3) | | | 3.5 | | | 3.6 | | | (0.1) | | | — | | | — | | | (4.4) | |

Crestwood Permian Basin Holdings LLC(4) | | | 110.9 | | | 112.1 | | | 4.2 | | | 0.5 | | | 4.4 | | | 0.3 | |

| Total | | | $ | 168.0 | | | $ | 943.7 | | | $ | 4.9 | | | $ | 10.5 | | | $ | (125.9) | | | $ | 24.4 | |

(1)As of September 30, 2021, our equity in the underlying net assets of Stagecoach Gas approximates the carrying value of our investment.

(2)As of September 30, 2021, our equity in the underlying net assets of Tres Palacios Holdings LLC (Tres Holdings) exceeded the carrying value of our investment balance by approximately $21.8 million. During both the three and nine months ended September 30, 2021 and 2020, we recorded amortization of approximately $0.3 million and $0.9 million, respectively, related to this excess basis, which is reflected as an increase in our earnings from unconsolidated affiliates in our consolidated statements of operations. Our Tres Holdings investment is included in our storage and transportation segment.

(3)As of September 30, 2021, our equity in the underlying net assets of Powder River Basin Industrial Complex, LLC (PRBIC) approximates the carrying value of our investment balance. During the first quarter of 2020, we recorded our share of a long-lived asset impairment recorded by our PRBIC equity investment, which eliminated our $5.5 million historical basis difference between our investment balance and the equity in the underlying net assets of PRBIC, and also resulted in a $4.5 million reduction in our earnings from unconsolidated affiliates during the nine months ended September 30, 2020. Our PRBIC investment is included in our storage and transportation segment.

(4)As of September 30, 2021, our equity in the underlying net assets of Crestwood Permian exceeded our investment balance by $7.5 million, and this excess amount is not subject to amortization. Our Crestwood Permian investment is included in our gathering and processing segment and is no longer considered a variable interest entity.

Summarized Financial Information of Unconsolidated Affiliates

Below is the summarized operating results for our significant unconsolidated affiliates (in millions; amounts represent 100% of unconsolidated affiliate information):

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Nine Months Ended September 30, |

| 2021 | | 2020 |

| Operating Revenues | | Operating Expenses | | Net Income (Loss) | | Operating Revenues | | Operating Expenses | | Net Income (Loss) |

| Stagecoach Gas | $ | 81.4 | | | $ | 456.9 | | | $ | (375.5) | | | $ | 115.3 | | | $ | 58.9 | | | $ | 56.5 | |

| | | | | | | | | | | |

| | | | | | | | | | | |

Other(1) | 232.4 | | | 208.2 | | | 24.9 | | | 91.2 | | | 113.0 | | | (21.0) | |

| Total | $ | 313.8 | | | $ | 665.1 | | | $ | (350.6) | | | $ | 206.5 | | | $ | 171.9 | | | $ | 35.5 | |

(1)Includes our Tres Holdings, PRBIC and Crestwood Permian equity investments.

Distributions and Contributions

The following table summarizes our distributions from and contributions to our unconsolidated affiliates (in millions):

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Distributions(1) | | Contributions | | | | |

| | Nine Months Ended | | Nine Months Ended | | | | |

| | September 30, | | September 30, | | |

| | 2021 | | 2020 | | 2021 | | 2020 | | | | |

| Stagecoach Gas | | $ | 640.9 | | | $ | 44.5 | | | $ | — | | | $ | — | | | | | |

| Tres Holdings | | 13.1 | | | 4.4 | | | 6.9 | | | 6.0 | | | | | |

| PRBIC | | 0.1 | | | 0.2 | | | — | | | — | | | | | |

| Crestwood Permian | | 8.9 | | | 8.5 | | | 3.3 | | | — | | | | | |

| Total | | $ | 663.0 | | | $ | 57.6 | | | $ | 10.2 | | | $ | 6.0 | | | | | |

(1) In July 2021, Stagecoach Gas closed on the sale of certain of its wholly-owned subsidiaries to a subsidiary of Kinder Morgan and distributed to us approximately $613.9 million as our proportionate share of the gross proceeds received from the sale. We utilized approximately $3 million of these proceeds to pay transaction costs related to the sale described above, $40 million of these proceeds to pay our remaining contingent consideration obligation and related accrued interest described below, and the remaining proceeds to repay a portion of the amounts outstanding under the Crestwood Midstream credit facility. In October 2021, we received cash distributions from Tres Holdings and Crestwood Permian of approximately $2.4 million and $7.4 million, respectively.

Other

Contingent Consideration. Pursuant to the Stagecoach Gas limited liability company agreement, we were required to make payments to CEGP because certain performance targets on growth capital projects were not achieved by December 31, 2020. During the nine months ended September 30, 2021, we fully satisfied this obligation by paying $57 million plus accrued interest of $2.1 million to CEGP.

Guarantee. CEQP issued a guarantee under which CEQP would be required to pay up to $10 million if Crestwood Permian fails to honor its obligations to Crestwood Permian Basin LLC, a 50% equity investment of Crestwood Permian, in the event Crestwood Permian Basin LLC fails to satisfy its obligations under its gas gathering agreement with a third party. We do not believe that it is probable that this guarantee will result in future losses based on our assessment of the nature of the guarantee, the financial condition of the guaranteed party and the period of time that the guarantee has been outstanding, and as a result, we have not recorded a liability related to this guarantee on our consolidated balance sheets at September 30, 2021 and December 31, 2020.

Note 6 – Risk Management

We are exposed to certain market risks related to our ongoing business operations. These risks include exposure to changing commodity prices. We utilize derivative instruments to manage our exposure to fluctuations in commodity prices, which is discussed below. Additional information related to our derivatives is discussed in Note 7.

Risk Management Activities

We sell NGLs (such as propane, ethane, butane and heating oil), crude oil and natural gas to energy-related businesses and may use a variety of financial and other instruments including forward contracts involving physical delivery of NGLs, crude oil and natural gas. We periodically enter into offsetting positions to economically hedge against the exposure our customer contracts create. Certain of these contracts and positions are derivative instruments. We do not designate any of our commodity-based derivatives as hedging instruments for accounting purposes. Our commodity-based derivatives are reflected at fair value in our consolidated balance sheets, and changes in the fair value of these derivatives that impact the consolidated statements of operations are reflected in costs of product/services sold. Our commodity-based derivatives that are settled with physical commodities are reflected as an increase to product revenues, and the commodity inventory that is utilized to satisfy those physical obligations is reflected as an increase to product costs in our consolidated statements of operations. The following table summarizes the impact to our consolidated statements of operations related to our commodity-based derivatives during the three and nine months ended September 30, 2021 and 2020 (in millions):

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Three Months Ended | | Nine Months Ended |

| | September 30, | | September 30, |

| | 2021 | | 2020 | | 2021 | | 2020 |

| Product revenues | | $ | 129.4 | | | $ | 32.4 | | | $ | 296.9 | | | $ | 125.4 | |

| Gain (loss) reflected in product costs | | $ | (53.4) | | | $ | (1.8) | | | $ | (94.8) | | | $ | 13.4 | |

We attempt to balance our contractual portfolio in terms of notional amounts and timing of performance and delivery obligations. This balance in the contractual portfolio significantly reduces the volatility in product costs related to these instruments.

Notional Amounts and Terms

The notional amounts of our derivative financial instruments include the following:

| | | | | | | | | | | | | | | | | | | | | | | |

| | September 30, 2021 | | December 31, 2020 |

| | Fixed Price

Payor | | Fixed Price

Receiver | | Fixed Price

Payor | | Fixed Price

Receiver |

| Propane, ethane, butane, heating oil and crude oil (MMBbls) | 73.9 | | | 78.4 | | | 72.7 | | | 76.5 | |

| Natural gas (Bcf) | 32.1 | | | 42.8 | | | 22.6 | | | 28.6 | |

Notional amounts reflect the volume of transactions, but do not represent the amounts exchanged by the parties to the financial instruments. Accordingly, notional amounts do not reflect our monetary exposure to market or credit risks. All contracts subject to price risk had a maturity of 36 months or less; however, 86% of the contracted volumes will be delivered or settled within 12 months.

Credit Risk

Inherent in our contractual portfolio are certain credit risks. Credit risk is the risk of loss from nonperformance by suppliers, customers or financial counterparties to a contract. We take an active role in managing credit risk and have established control procedures, which are reviewed on an ongoing basis. We attempt to minimize credit risk exposure through credit policies and periodic monitoring procedures as well as through customer deposits, letters of credit and entering into netting agreements that allow for offsetting counterparty receivable and payable balances for certain financial transactions, as deemed appropriate. The counterparties associated with our price risk management activities are energy marketers and propane retailers, resellers and dealers.

Certain of our derivative instruments have credit limits that require us to post collateral. The amount of collateral required to be posted is a function of the net liability position of the derivative as well as our established credit limit with the respective counterparty. If our credit rating were to change, the counterparties could require us to post additional collateral. The amount of additional collateral that would be required to be posted would vary depending on the extent of change in our credit rating as well as the requirements of the individual counterparty. In addition, we have margin requirements with a derivative clearing broker and a third party broker related to our net asset or liability position with each respective broker. All collateral amounts have been netted against the asset or liability with the respective counterparty and are reflected in our consolidated balance sheets as assets and liabilities from price risk management activities.

The following table presents the fair value of our commodity derivative instruments with credit-risk related contingent features and their associated collateral (in millions):

| | | | | | | | | | | |

| September 30, 2021 | | December 31, 2020 |

Aggregate fair value liability of derivative instruments with credit-risk-related contingent features(1) | $ | 157.6 | | | $ | 38.5 | |

| Broker-related net derivative asset position | $ | 199.6 | | | $ | 35.9 | |

| Broker-related cash collateral received | $ | 163.9 | | | $ | 18.3 | |

| Cash collateral received, net | $ | 14.3 | | | $ | 12.4 | |

(1)At September 30, 2021 and December 31, 2020, we posted $1.1 million and less than $0.1 million of collateral associated with these derivatives.

Note 7 – Fair Value Measurements

The accounting standard for fair value measurement establishes a three-tier fair value hierarchy, which prioritizes the inputs used in measuring fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurement) and the lowest priority to unobservable inputs (Level 3 measurement). The three levels of the fair value hierarchy are as follows:

•Level 1—Quoted prices are available in active markets for identical assets or liabilities as of the reporting date. Active markets are those in which transactions for the asset or liability occur in sufficient frequency and volume to provide

pricing information on an ongoing basis. Level 1 primarily consists of financial instruments such as exchange-traded derivatives, listed equities and US government treasury securities.

•Level 2—Pricing inputs are other than quoted prices in active markets included in Level 1, which are either directly or indirectly observable as of the reporting date. Level 2 includes those financial instruments that are valued using models or other valuation methodologies. These models are primarily industry-standard models that consider various assumptions, including quoted forward prices for commodities, time value, volatility factors, and current market and contractual prices for the underlying instruments, as well as other relevant economic measures. Substantially all of these assumptions are observable in the marketplace throughout the full term of the instrument, can be derived from observable data or are supported by observable levels at which transactions are executed in the marketplace. Instruments in this category include non-exchange-traded derivatives such as over the counter (OTC) forwards, options and physical exchanges.

•Level 3—Pricing inputs include significant inputs that are generally less observable from objective sources. These inputs may be used with internally developed methodologies that result in management’s best estimate of fair value.

Financial Assets and Liabilities

As of September 30, 2021 and December 31, 2020, we held certain assets and liabilities that are required to be measured at fair value on a recurring basis, which include our derivative instruments related to crude oil, NGLs and natural gas. Our derivative instruments consist of forwards, swaps, futures, physical exchanges and options.

Our derivative instruments that are traded on the New York Mercantile Exchange have been categorized as Level 1.

Our derivative instruments also include OTC contracts, which are not traded on a public exchange. The fair values of these derivative instruments are determined based on inputs that are readily available in public markets or can be derived from information available in publicly quoted markets. These instruments have been categorized as Level 2.

Our OTC options are valued based on the Black Scholes option pricing model that considers time value and volatility of the underlying commodity. The inputs utilized in the model are based on publicly available information as well as broker quotes. These options have been categorized as Level 2.

Our financial assets and liabilities are classified in their entirety based on the lowest level of input that is significant to the fair value measurement. The assessment of the significance of a particular input to the fair value measurement requires judgment, and may affect the valuation of fair value assets and liabilities and their placement within the fair value hierarchy levels.

The following tables set forth by level within the fair value hierarchy, our financial instruments that were accounted for at fair value on a recurring basis at September 30, 2021 and December 31, 2020 (in millions):

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| September 30, 2021 |

| | | | | | |

| Level 1 | | Level 2 | | Level 3 | | Gross Fair Value | | Contract Netting(1) | | Collateral/Margin Received or Paid | | Fair Value |

| Assets | | | | | | | | | | | | | |

| Assets from price risk management | $ | 74.2 | | | $ | 1,469.0 | | | $ | — | | | $ | 1,543.2 | | | $ | (1,339.6) | | | $ | (164.5) | | | $ | 39.1 | |

Suburban Propane Partners, L.P. units(2) | 2.2 | | | — | | | — | | | 2.2 | | | — | | | — | | | 2.2 | |

| Total assets at fair value | $ | 76.4 | | | $ | 1,469.0 | | | $ | — | | | $ | 1,545.4 | | | $ | (1,339.6) | | | $ | (164.5) | | | $ | 41.3 | |

| | | | | | | | | | | | | |

| Liabilities | | | | | | | | | | | | | |

| Liabilities from price risk management | $ | 55.8 | | | $ | 1,547.4 | | | $ | — | | | $ | 1,603.2 | | | $ | (1,339.6) | | | $ | 13.7 | | | $ | 277.3 | |

| Total liabilities at fair value | $ | 55.8 | | | $ | 1,547.4 | | | $ | — | | | $ | 1,603.2 | | | $ | (1,339.6) | | | $ | 13.7 | | | $ | 277.3 | |

| | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| December 31, 2020 |

| | | | | | |

| Level 1 | | Level 2 | | Level 3 | | Gross Fair Value | | Contract Netting(1) | | Collateral/Margin Received or Paid | | Fair Value |

| Assets | | | | | | | | | | | | | |

| Assets from price risk management | $ | 20.2 | | | $ | 480.5 | | | $ | — | | | $ | 500.7 | | | $ | (455.0) | | | $ | (18.5) | | | $ | 27.2 | |

Suburban Propane Partners, L.P. units(2) | 2.1 | | | — | | | — | | | 2.1 | | | — | | | — | | | 2.1 | |

| Total assets at fair value | $ | 22.3 | | | $ | 480.5 | | | $ | — | | | $ | 502.8 | | | $ | (455.0) | | | $ | (18.5) | | | $ | 29.3 | |

| | | | | | | | | | | | | |

| Liabilities | | | | | | | | | | | | | |

| Liabilities from price risk management | $ | 25.1 | | | $ | 494.0 | | | $ | — | | | $ | 519.1 | | | $ | (455.0) | | | $ | 12.2 | | | $ | 76.3 | |

| Total liabilities at fair value | $ | 25.1 | | | $ | 494.0 | | | $ | — | | | $ | 519.1 | | | $ | (455.0) | | | $ | 12.2 | | | $ | 76.3 | |

(1)Amounts represent the impact of legally enforceable master netting agreements that allow us to settle positive and negative positions.

(2)Amount is reflected in other non-current assets on CEQP’s consolidated balance sheets.

Cash, Accounts Receivable and Accounts Payable

As of September 30, 2021 and December 31, 2020, the carrying amounts of cash, accounts receivable and accounts payable approximate fair value based on the short-term nature of these instruments.

Credit Facility

The fair value of the amounts outstanding under our Crestwood Midstream credit facility approximates the carrying amounts as of September 30, 2021 and December 31, 2020, due primarily to the variable nature of the interest rate of the instrument, which is considered a Level 2 fair value measurement.

Senior Notes

We estimate the fair value of our senior notes primarily based on quoted market prices for the same or similar issuances (representing a Level 2 fair value measurement). The following table represents the carrying amount (reduced for deferred financing costs associated with the respective notes) and fair value of our senior notes (in millions):

| | | | | | | | | | | | | | | | | | | | | | | |

| September 30, 2021 | | December 31, 2020 |

| Carrying

Amount | | Fair

Value | | Carrying

Amount | | Fair

Value |

| 2023 Senior Notes | $ | — | | | $ | — | | | $ | 683.8 | | | $ | 691.5 | |

| 2025 Senior Notes | $ | 496.3 | | | $ | 511.9 | | | $ | 495.5 | | | $ | 509.9 | |

| 2027 Senior Notes | $ | 594.0 | | | $ | 618.4 | | | $ | 593.2 | | | $ | 594.1 | |

| 2029 Senior Notes | $ | 690.5 | | | $ | 734.0 | | | $ | — | | | $ | — | |

Note 8 – Long-Term Debt

Long-term debt consisted of the following at September 30, 2021 and December 31, 2020 (in millions):

| | | | | | | | | | | |

| September 30,

2021 | | December 31,

2020 |

| Credit Facility | $ | 250.5 | | | $ | 719.0 | |

| 2023 Senior Notes | — | | | 687.2 | |

| 2025 Senior Notes | 500.0 | | | 500.0 | |

| 2027 Senior Notes | 600.0 | | | 600.0 | |

| 2029 Senior Notes | 700.0 | | | — | |

Other(1) | 0.2 | | | 0.4 | |

| Less: deferred financing costs, net | 25.6 | | | 22.6 | |

| Total debt | 2,025.1 | | | 2,484.0 | |

| Less: current portion | 0.2 | | | 0.2 | |

| Total long-term debt, less current portion | $ | 2,024.9 | | | $ | 2,483.8 | |

(1)Represents non-interest bearing obligations related to certain companies acquired in 2014 with payments due through 2022.

Credit Facility

Crestwood Midstream’s five-year $1.25 billion revolving credit facility (the CMLP Credit Facility) is available to fund acquisitions, working capital and internal growth projects and for general partnership purposes. Contemporaneous with the Crestwood Holdings Transactions described in Note 1, Crestwood Midstream entered into the Third Amendment to its credit agreement in order to, among other things, permit the borrowings under the CMLP Credit Facility to fund the Crestwood Holdings Transactions and revise the definition of Change in Control in the CMLP Credit Agreement as it relates to the control of CEQP’s general partner). The other covenants and restrictive provisions under the amended credit agreement are materially consistent with the covenants that existed at December 31, 2020.

Crestwood Midstream is required under its credit agreement to maintain a net debt to consolidated EBITDA ratio (as defined in its credit agreement) of not more than 5.50 to 1.0, a consolidated EBITDA to consolidated interest expense ratio (as defined in its credit agreement) of not less than 2.50 to 1.0, and a senior secured leverage ratio (as defined in its credit agreement) of not more than 3.75 to 1.0. At September 30, 2021, the net debt to consolidated EBITDA ratio was approximately 3.45 to 1.0, the consolidated EBITDA to consolidated interest expense ratio was approximately 4.98 to 1.0, and the senior secured leverage ratio was 0.42 to 1.0.

At September 30, 2021, Crestwood Midstream had $985.3 million of available capacity under its credit facility considering the most restrictive debt covenants in its credit agreement. At September 30, 2021 and December 31, 2020, Crestwood Midstream’s outstanding standby letters of credit were $14.2 million and $23.9 million. Borrowings under the credit facility accrue interest at prime or Eurodollar based rates plus applicable spreads, which resulted in interest rates between 2.34% and 4.50% at September 30, 2021 and 2.40% and 4.50% at December 31, 2020. The weighted-average interest rate on outstanding borrowings as of September 30, 2021 and December 31, 2020 was 2.41% and 2.45%.

Senior Notes

2029 Senior Notes. In January 2021, Crestwood Midstream issued $700 million of 6.00% unsecured senior notes due 2029 (the 2029 Senior Notes). The 2029 Senior Notes will mature on February 1, 2029, and interest is payable semi-annually in arrears on February 1 and August 1 of each year, beginning on August 1, 2021. The net proceeds from this offering of approximately $691.0 million were used to repay a portion of the 2023 Senior Notes and to repay indebtedness under the CMLP Credit Facility.

2023 Senior Note Repayments. During the nine months ended September 30, 2021, we redeemed $687.2 million of principal outstanding under our 2023 Senior Notes. In conjunction with the repayment of the notes, we recognized a loss on extinguishment of debt of approximately $6.7 million during the nine months ended September 30, 2021, and paid approximately $8.6 million of accrued interest on the 2023 Senior Notes on the dates they were repurchased. We funded the

repayment using a portion of the proceeds from the issuance of the 2029 Senior Notes and borrowings under the CMLP Credit Facility.

Note 9 – Commitments and Contingencies

Legal Proceedings

Linde Lawsuit. On December 23, 2019, Linde Engineering North America Inc. (Linde) filed a lawsuit in the District Court of Harris County, Texas alleging that Arrow Field Services, LLC, our consolidated subsidiary, and Crestwood Midstream breached a contract entered into in March 2018 under which Linde was to provide engineering, procurement and construction services to us related to the completion of the construction of the Bear Den II cryogenic processing plant. During the three months ended September 30, 2021, we paid approximately $19.5 million to Linde related to this matter, and Linde claims remaining unpaid invoices of approximately $36 million, along with other damages. This matter is not an insurable event based on our insurance policies, and we are unable to predict the outcome for this matter.

General. We are periodically involved in litigation proceedings. If we determine that a negative outcome is probable and the amount of loss is reasonably estimable, then we accrue the estimated amount. The results of litigation proceedings cannot be predicted with certainty. We could incur judgments, enter into settlements or revise our expectations regarding the outcome of certain matters, and such developments could have a material adverse effect on our results of operations or cash flows in the period in which the amounts are paid and/or accrued. As of September 30, 2021 and December 31, 2020, we had approximately $16.6 million and $10.4 million accrued for outstanding legal matters. Based on currently available information, we believe it is remote that future costs related to known contingent liability exposures for which we can estimate will exceed current accruals by an amount that would have a material adverse impact on our consolidated financial statements. As we learn new facts concerning contingencies, we reassess our position both with respect to accrued liabilities and other potential exposures.

Any loss estimates are inherently subjective, based on currently available information, and are subject to management’s judgment and various assumptions. Due to the inherently subjective nature of these estimates and the uncertainty and unpredictability surrounding the outcome of legal proceedings, actual results may differ materially from any amounts that have been accrued.

Regulatory Compliance

In the ordinary course of our business, we are subject to various laws and regulations. In the opinion of our management, compliance with current laws and regulations will not have a material effect on our results of operations, cash flows or financial condition.

Environmental Compliance

Our operations are subject to stringent and complex laws and regulations pertaining to worker health, safety, and the environment. We are subject to laws and regulations at the federal, state, regional and local levels that relate to air and water quality, hazardous and solid waste management and disposal, and other environmental matters. The cost of planning, designing, constructing and operating our facilities must incorporate compliance with environmental laws and regulations and safety standards. Failure to comply with these laws and regulations may trigger a variety of administrative, civil and potentially criminal enforcement measures.

During 2019, we experienced produced water releases on our Arrow water gathering system located within the Fort Berthold Indian Reservation in North Dakota. In January 2021, we received a Notice of Violation and Opportunity to Confer from the Environmental Protection Agency (EPA) related to the water releases. In March 2021, we executed a Consent Agreement with the EPA and agreed to pay $0.1 million for penalties related to the water releases. The EPA provided the public a 30-day period to comment on the Consent Agreement and is currently reviewing the comments received. We expect to finalize and settle the Consent Agreement after the EPA completes its review and response, if necessary, to the comments received. We are also substantially complete with all remediation efforts related to the water releases and continue to monitor any remaining impacts. We will continue our remediation efforts to ensure that lands impacted by the produced water releases are fully remediated. In response to the water releases, we removed several miles of gathering pipeline from the system that remained in service and replaced those sections with a pipeline composed of higher capacity material that is more suitable to the environment and climate conditions in the Bakken. The replaced pipeline increased water gathering capacity on the Arrow

system and furthers our commitment to sustainability and environmental stewardship in the areas where we live and operate. We believe these events are insurable under our policies. We have not recorded an insurance receivable as of September 30, 2021.

At September 30, 2021 and December 31, 2020, our accrual of approximately $1.2 million and $1.3 million was based on our undiscounted estimate of amounts we will spend on compliance with environmental and other regulations, and any associated fines or penalties. We estimate that our potential liability for reasonably possible outcomes related to our environmental exposures could range from approximately $1.2 million to $1.9 million at September 30, 2021.

Self-Insurance

We utilize third-party insurance subject to varying retention levels of self-insurance, which management considers prudent. Such self-insurance relates to losses and liabilities primarily associated with medical claims, workers’ compensation claims and general, product, vehicle and environmental liability. Losses are accrued based upon management’s estimates of the aggregate liability for claims incurred using certain assumptions followed in the insurance industry and based on past experience. The primary assumption utilized is actuarially determined loss development factors. The loss development factors are based primarily on historical data. Our self insurance reserves could be affected if future claim developments differ from the historical trends. We believe changes in health care costs, trends in health care claims of our employee base, accident frequency and severity and other factors could materially affect the estimate for these liabilities. We continually monitor changes in employee demographics, incident and claim type and evaluate our insurance accruals and adjust our accruals based on our evaluation of these qualitative data points. We are liable for the development of claims for our previously disposed of retail propane operations, provided they were reported prior to August 1, 2012. The following table summarizes CEQP’s and CMLP’s self-insurance reserves at September 30, 2021 and December 31, 2020 (in millions):

| | | | | | | | | | | | | | | | | | | | | | | |

| | CEQP | | CMLP |

| | September 30,

2021 | | December 31, 2020 | | September 30,

2021 | | December 31, 2020 |

Self-insurance reserves(1) | $ | 6.7 | | | $ | 7.7 | | | $ | 5.8 | | | $ | 6.7 | |

(1)At September 30, 2021, CEQP and CMLP classified approximately $4.8 million and $4.1 million, respectively, of these reserves as other long-term liabilities on their consolidated balance sheets.

Guarantees and Indemnifications

We are involved in various joint ventures that sometimes require financial and performance guarantees. In a financial guarantee, we are obligated to make payments if the guaranteed party fails to make payments under, or violates the terms of, the financial arrangement. In a performance guarantee, we provide assurance that the guaranteed party will execute on the terms of the contract. If they do not, we are required to perform on their behalf. We also periodically provide indemnification arrangements related to assets or businesses we have sold. For a further description of our guarantees associated with our joint ventures, see Note 5.

Our potential exposure under guarantee and indemnification arrangements can range from a specified amount to an unlimited dollar amount, depending on the nature of the claim, specificity as to duration, and the particular transaction. As of September 30, 2021 and December 31, 2020, we have no amounts accrued for these guarantees.

Note 10 - Leases

The following table summarizes the balance sheet information related to our operating and finance leases at September 30, 2021 and December 31, 2020 (in millions):

| | | | | | | | | | | |

| September 30,

2021 | | December 31, 2020 |

| Operating Leases | | | |

| Operating lease right-of-use assets, net | $ | 31.1 | | | $ | 36.8 | |

| | | |

| Accrued expenses and other liabilities | $ | 14.5 | | | $ | 14.7 | |

| Other long-term liabilities | 22.0 | | | 28.5 | |

| Total operating lease liabilities | $ | 36.5 | | | $ | 43.2 | |

| Finance Leases | | | |

| Property, plant and equipment | $ | 12.1 | | | $ | 13.3 | |

| Less: accumulated depreciation | 8.5 | | | 7.9 | |

| Property, plant and equipment, net | $ | 3.6 | | | $ | 5.4 | |

| | | |

| Accrued expenses and other liabilities | $ | 2.1 | | | $ | 2.9 | |

| Other long-term liabilities | 1.2 | | | 1.9 | |

| Total finance lease liabilities | $ | 3.3 | | | $ | 4.8 | |

Lease expense. Our operating lease expense, net totaled $3.7 million and $5.8 million for the three months ended September 30, 2021 and 2020 and $12.8 million and $20.4 million for the nine months ended September 30, 2021 and 2020. Our finance lease expense totaled $0.8 million and $0.9 million for the three months ended September 30, 2021 and 2020 and $2.6 million and $3.1 million for the nine months ended September 30, 2021 and 2020.

Note 11 – Partners’ Capital and Non-Controlling Partner

Common and Subordinated Units