As filed with the Securities and Exchange Commission on April 16, 2004

Registration No. 333 –112714

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

AMENDMENT NO. 1

TO

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

MICHAEL FOODS, INC.

(Exact Name of Registrant as Specified in Its Charter)

| | | | |

| Delaware | | 2015 | | 13-4151741 |

(State or Other Jurisdiction of Incorporation or Organization) | | (Primary Standard Industrial Classification Code Number) | | (I.R.S. Employer Identification No.) |

301 Carlson Parkway, Suite 400

Minnetonka, Minnesota 55305

(952) 258-4000

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

John D. Reedy

Michael Foods, Inc.

301 Carlson Parkway, Suite 400

Minnetonka, Minnesota 55305

(952) 258-4000

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

See Table of Additional Registrants Below

Copies to:

Todd R. Chandler, Esq.

Weil, Gotshal & Manges LLP

767 Fifth Avenue

New York, New York 10153

(212) 310-8000

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after the effective date of this Registration Statement.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

The Registrants hereby amend this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrants shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

ADDITIONAL REGISTRANTS

| | | | | | | | |

Exact Name of Registrant

as Specified in Its Charter

| | State or Other

Jurisdiction of

Incorporation

or Organization

| | Primary

Standard

Industrial

Classification

Code Number

| | I.R.S. Employer

Identification No.

| | Address, Including Zip Code and

Telephone Number, Including Area

Code, of Registrant’s Principal

Executive Offices

|

Casa Trucking, Inc. | | Minnesota | | 4212 | | 22-3493806 | | 301 Carlson Parkway, Suite 400

Minnetonka, Minnesota 55305 |

| | | | |

Crystal Farms Refrigerated Distribution Company | | Minnesota | | 5143 | | 41-1669454 | | 6465 Wayzata Blvd., Suite 200

Minneapolis, Minnesota 55426 |

| | | | |

Farm Fresh Foods, Inc. | | Nevada | | 2033 | | 91-2086470 | | 3840 North Civic Center Dr. “B”

North Las Vegas, Nevada 89030 |

| | | | |

KMS Dairy, Inc. | | Minnesota | | 5143 | | 41-0845810 | | 301 Carlson Parkway, Suite 400

Minnetonka, Minnesota 55305 |

| | | | |

M.G. Waldbaum Company | | Nebraska | | 2015 | | 47-0445304 | | 301 Carlson Parkway, Suite 400

Minnetonka, Minnesota 55305 |

| | | | |

Michael Foods of Delaware, Inc. | | Delaware | | 2015 | | 41-1579532 | | 301 Carlson Parkway, Suite 400

Minnetonka, Minnesota 55305 |

| | | | |

Minnesota Products, Inc. | | Minnesota | | 2033 | | 41-1394918 | | 301 Carlson Parkway, Suite 400

Minnetonka, Minnesota 55305 |

| | | | |

Northern Star Co. | | Minnesota | | 2033 | | 41-1468193 | | 301 Carlson Parkway, Suite 400

Minnetonka, Minnesota 55305 |

| | | | |

Papetti Electroheating Corporation | | New Jersey | | 2015 | | 22-3301353 | | One Papetti Plaza

Elizabeth, New Jersey 07926 |

| | | | |

Papetti’s Hygrade Egg Products, Inc. | | Minnesota | | 2015 | | 22-3493805 | | 301 Carlson Parkway, Suite 400

Minnetonka, Minnesota 55305 |

| | | | |

WFC, Inc. | | Wisconsin | | 5143 | | 41-1698341 | | 450 North CP Avenue

Lake Mills, Wisconsin 53551 |

| | | | |

Wisco Farm Cooperative | | Wisconsin | | 5143 | | 39-1524981 | | 450 North CP Avenue

Lake Mills, Wisconsin 53551 |

The name, address, including zip code and telephone number, including area code, of agent for service for each of the Additional Registrants is:

John D. Reedy

301 Carlson Parkway, Suite 400

Minnetonka, Minnesota 55305

(952) 258-4000

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, Dated April 16, 2004

PROSPECTUS

Offer of $150,000,000 principal amount of

8% Senior Subordinated Notes due 2013

registered under the Securities Act of 1933

in exchange for

$150,000,000 principal amount of outstanding

8% Senior Subordinated Notes due 2013

We are offering the new, registered notes described above in exchange for our outstanding notes described above. In this prospectus we refer to the outstanding notes as the “old notes” and our new notes as the “registered notes,” and we refer to the old notes and the registered notes, together, as the “notes.” The form and terms of the registered notes are identical in all material respects to the form and terms of the old notes, except for transfer restrictions, registration rights and additional interest payment provisions relating only to the old notes. We do not intend to apply to have any notes listed on any securities exchange or automated quotation system and there may be no active trading market for them.

Material Terms of the Exchange Offer

| | • | The exchange offer expires at , New York City time, on , 2004, unless extended. Whether or not the exchange offer is extended, the time at which it ultimately expires is referred to in this prospectus as the time of expiration. |

| | • | The only conditions to completing the exchange offer are that the exchange offer not violate any applicable law, regulation or interpretation of the staff of the Securities and Exchange Commission and that no injunction, order or decree of any court or governmental agency that would prohibit, prevent or otherwise materially impair our ability to proceed with the exchange offer shall be in effect. |

| | • | All old notes that are validly tendered and not validly withdrawn will be exchanged. |

| | • | Tenders of old notes in the exchange offer may be withdrawn at any time prior to the time of expiration. |

| | • | We will not receive any cash proceeds from the exchange offer. |

None of our affiliates, no broker-dealers that acquired old notes directly from us and no persons engaged in a distribution of registered notes may participate in the exchange offer. Any broker-dealer that acquired old notes as a result of market-making or other trading activities and receives registered notes for its own account in exchange for those old notes must acknowledge that it will deliver a prospectus in connection with any resale of those registered notes. The letter of transmittal states that, by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer for that purpose. We have agreed that, for a period ending on the earlier of (a) 180 days after the time of expiration and (b) the date on which broker-dealers are no longer required to deliver a prospectus in connection with market-making or other trading activities, we will make this prospectus available to any broker-dealer for use in connection with any resales by that broker-dealer. See “Plan of Distribution.”

Consider carefully the “Risk Factors” beginning on page 13 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2004

TABLE OF CONTENTS

i

PROSPECTUS SUMMARY

This summary highlights information contained elsewhere in this prospectus. You should read the entire prospectus carefully, including, in particular, the section entitled “Risk Factors” and the financial statements and the related notes to those statements. All references to market share contained in this prospectus are based on sales volumes unless otherwise indicated. Except as otherwise required by the context, in this prospectus (a) “our company,” “we,” “us” or “our” refer to the historical and current business now operated by Michael Foods, Inc. and its subsidiaries, and (b) the “issuer” refers to Michael Foods, Inc. exclusive of its subsidiaries.

About Us

We are a leading producer and distributor of specialty egg products to the foodservice, retail and industrial ingredients markets. We are also a leading producer and distributor of refrigerated potato products to the retail market. In addition, we distribute refrigerated food items, primarily cheese and other dairy products, to the retail grocery market predominantly in the central United States. For the year ended December 31, 2003, we generated net sales of $1,180.5 million on a pro forma basis after giving effect to the sale of our dairy products division, which we sold effective September 30, 2003.

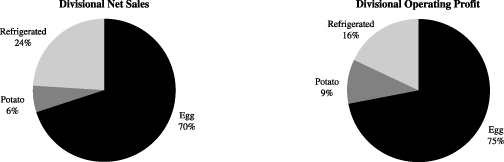

The following charts set forth the net sales and operating profit of our three divisions—egg products, potato products and refrigerated distribution—as a percentage of total net sales and operating profit for these three divisions for the year ended December 31, 2003.

Egg Products.We believe our egg products division is the largest producer of processed egg products and the fourth largest egg producer in the United States. For the year ended December 31, 2003, the egg products division represented approximately 70% and 75% of the net sales and the operating profit of our three divisions, respectively.

Potato Products.We believe our potato products division is the largest processor and distributor in the United States of a wide variety of refrigerated potato products sold to the retail grocery market. Our products which are sold to the retail grocery and foodservice markets, principally include hash browns and diced, sliced, mashed and other specialty potato products. For the year ended December 31, 2003, the potato products division represented approximately 6% and 9% of the net sales and the operating profit of our three divisions, respectively.

Refrigerated Distribution.Our refrigerated distribution division is a distributor of over 400 branded and private label refrigerator case items to retailers and wholesale warehouses predominantly in the central United States. For the year ended December 31, 2003, the refrigerated distribution division represented approximately 24% and 16% of the net sales and operating profit of our three divisions, respectively.

1

Industry Trends

We believe that our specialty egg products are well positioned to continue capitalizing on the growth of the foodservice industry, which is being driven by increasing food consumption away from home. Our business is influenced by the following industry trends:

| | • | Growth in the foodservice industry. |

| | • | Growth in egg consumption. |

| | • | Growth in higher value-added processed egg products. |

| | • | Consolidation in the foodservice distribution channel. |

Our Competitive Strengths

We believe that the following key competitive strengths will contribute to our continued success:

| | • | Extensive portfolio of specialty and branded products with leading regional and national market positions. |

| | • | Long-standing customer relationships. |

| | • | Large scale operator with efficient manufacturing operations. |

| | • | Industry-leading product development capabilities. |

| | • | Strong, proven management team with significant equity interest. |

| | • | Stable free cash flow generation. |

Our Business Strategy

Our strategy has enabled us to capitalize upon key industry trends, specifically the increases in both food prepared away from the home and the consumption of further-processed eggs. The primary components of our business strategy include the following:

| | • | Encouraging customers to purchase our higher-margin products, particularly egg products; |

| | • | Capitalizing on growth opportunities; |

| | • | Continuing strategic sourcing and cost reduction programs; and |

| | • | Pursuing attractive acquisition and joint venture opportunities. |

Risk Factors

Our ability to attain our objectives depends upon our success in addressing risks relating to our business and the industries we serve, including the following:

| | • | Fluctuations in egg, potato and cheese market prices and the prices of other raw materials, such as grain; |

| | • | Susceptibility of food products to microbial contamination; |

| | • | Exposure to product liability claims; |

2

| | • | Declines in egg consumption or in the consumption of processed food products; |

| | • | Intense competition in the markets in which we operate; |

| | • | A limited number of large customers accounting for a significant portion of our net sales volume; |

| | • | Loss or expiration of a patent or trademark which could negatively impact our ability to produce and sell the products associated with such patent or trademark; |

| | • | Government regulation which could increase our production costs and legal and regulatory expenses; |

| | • | Unexpected costs associated with compliance with environmental regulations; |

| | • | Extreme weather conditions, disease and pests; |

| | • | Our failure to attract and retain qualified employees; |

| | • | Strikes, work stoppages and slowdowns; |

| | • | Disruptions of our business operations as a result of loss of members of our management team; and |

| | • | Additional costs associated with pressure from animal rights groups regarding the treatment of animals. |

For further discussion of these and the other risks we face and risks associated with the exchange offer and holding the notes, see “Risk Factors,” beginning on page 13.

The Transactions

On October 10, 2003, we entered into a merger agreement pursuant to which affiliates of Thomas H. Lee Partners, L.P. and certain members of our management acquired us for approximately $1.055 billion in cash, subject to certain adjustments. For a more detailed discussion of management’s participation in the acquisition, see “Management—Management Participation.” See also “The Transactions” and “Certain Relationships and Related Transactions—Certain Agreements Relating to the Acquisition.” The acquisition and related financing transactions, described below, were consummated on November 20, 2003.

Concurrently with the acquisition, the following financing transactions occurred:

| | • | an investment by affiliates of Thomas H. Lee Partners, L.P. totaling $290.0 million in cash; |

| | • | an equity investment of $33.0 million by certain members of our management team, more fully-discussed in the section of this prospectus entitled “Management—Management Participation”; |

| | • | the entering into of a senior secured credit facility providing for $495.0 million in term loans, which were drawn at closing and a revolving credit facility for working capital and general corporate purposes of $100.0 million, with available borrowing capacity at closing of approximately $93.5 million; |

| | • | the entering into of a senior unsecured term loan facility providing for loans of up to $135.0 million, which were drawn at closing; and |

| | • | the offering of $150.0 million in aggregate principal amount of old notes. |

The proceeds from the financing transactions were used to:

| | • | pay approximately $650.0 million to the former equityholders of M-Foods Holdings, the parent of our predecessor, under the terms of the merger agreement; |

| | • | repay approximately $98.0 million of outstanding indebtedness under the then existing credit facility of our predecessor; |

3

| | • | repurchase for approximately $254.0 million the 11 3/4% senior subordinated notes due 2011 of our predecessor pursuant to a tender offer and consent solicitation by THL Food Products Co., or Food Products; and |

| | • | pay approximately $61.0 million in fees and expenses related to the acquisition and the related financing transactions. |

We refer to the acquisition, these financing transactions and the application of the proceeds from the financing transactions as the “transactions.” Our predecessor refers to Michael Foods, Inc., a Minnesota corporation, whose operations were merged into us pursuant to the merger agreement.

Michael Foods, Inc. is a corporation organized under the laws of the State of Delaware. Our principal executive offices are located at 301 Carlson Parkway, Suite 400, Minnetonka, Minnesota 55305, and our telephone number is (952) 258-4000. Our worldwide web address iswww.michaelfoods.com. Our web site and the information contained on our web site is not a part of this prospectus.

4

Summary of the Terms of the Exchange Offer

On November 20, 2003, the issuer issued $150.0 million aggregate principal amount of its 8% senior subordinated notes due 2013 in a transaction exempt from registration under the Securities Act of 1933. We refer to the issuance of the old notes in this prospectus as the “original issuance.”

At the time of the original issuance, we entered into an agreement in which we agreed to register new notes, with substantially the same form and terms of the old notes, and to offer to exchange the registered notes for the old notes. This agreement is referred to in this prospectus as the “registration rights agreement.”

Unless you are a broker-dealer and you satisfy the conditions set forth below under “—Resales of the Registered Notes,” we believe that the registered notes to be issued to you in the exchange offer may be resold by you without compliance with the registration and prospectus delivery provisions of the Securities Act. You should read the discussions under the headings “The Exchange Offer” and “Description of Notes” for further information regarding the registered notes.

| | | | |

Registration Rights Agreement | | Under the registration rights agreement, the issuer is obligated to offer to exchange the old notes for registered notes with terms identical in all material respects to the old notes. The exchange offer is intended to satisfy that obligation. After the exchange offer is complete, except as set forth in the next paragraph, you will no longer be entitled to any exchange or registration rights with respect to your old notes. The registration rights agreement requires the issuer to file a registration statement for a continuous offering in accordance with Rule 415 under the Securities Act for your benefit if you would not receive freely tradeable registered notes in the exchange offer or you are ineligible to participate in the exchange offer and indicate that you wish to have your old notes registered under the Securities Act. See “The Exchange Offer—Procedures for Tendering.” |

| |

The Exchange Offer | | The issuer is offering to exchange $1,000 principal amount of its 8% senior subordinated notes due 2013, which have been registered under the Securities Act, for each $1,000 principal amount of its unregistered 8% senior subordinated notes due 2013 that were issued in the original issuance. In order to be exchanged, an old note must be validly tendered and accepted. All old notes that are validly tendered and not validly withdrawn before the time of expiration will be accepted and exchanged. As of this date, there are $150.0 million aggregate principal amount of old notes outstanding. The issuer will issue the registered notes promptly after the time of expiration. |

5

| | | | |

Resales of the Registered Notes | | Except as described below, we believe that the registered notes to be issued in the exchange offer may be offered for resale, resold and otherwise transferred by you without compliance with the registration and (except with respect to broker-dealers) prospectus delivery provisions of the Securities Act if (but only if) you meet the following conditions: |

| | |

| | | • | | you are not an “affiliate” of the issuer, as that term is defined in Rule 405 under the Securities Act. |

| | |

| | | • | | if you are a broker-dealer, you acquired the old notes which you seek to exchange for registered notes as a result of market making or other trading activities and not directly from us and you comply with the prospectus delivery requirements of the Securities Act; |

| | |

| | | • | | the registered notes are acquired by you in the ordinary course of your business; |

| | |

| | | • | | you are not engaging in and do not intend to engage in a distribution of the registered notes; and |

| | |

| | | • | | you do not have an arrangement or understanding with any person to participate in the distribution of the registered notes. |

| |

| | | Our belief is based on interpretations by the staff of the SEC, as set forth in no-action letters issued to third parties unrelated to us. The staff has not considered the exchange offer in the context of a no-action letter, and we cannot assure you that the staff would make a similar determination with respect to the exchange offer. If you do not meet the above conditions, you may not participate in the exchange offer or sell, transfer or otherwise dispose of any old notes unless (i) they have been registered for resale by you under the Securities Act and you deliver a “resale” prospectus meeting the requirements of the Securities Act or (ii) you sell, transfer or otherwise dispose of the registered notes in accordance with an applicable exemption from the registration requirements of the Securities Act. Any broker-dealer that acquired old notes as a result of market-making activities or other trading activities, and receives registered notes for its own account in exchange for old notes, must acknowledge that it will deliver a prospectus in connection with any resale of the registered notes. See “Plan of Distribution.” A broker-dealer may use this prospectus for an offer to resell or to otherwise transfer those registered notes for a period of 180 days after the time of expiration. |

| |

Time of Expiration | | The exchange offer will expire at , New York City time, on , 2004, unless we decide to extend the exchange offer. We do not intend to extend the exchange offer, although we reserve the right to do so. We will not extend the exchange offer past , 2004. |

6

| | | | |

Conditions to the Exchange Offer | | The only conditions to completing the exchange offer are that the exchange offer not violate any applicable law, regulation or applicable interpretation of the staff of the SEC and that no injunction, order or decree of any court or any governmental agency that would prohibit, prevent or otherwise materially impair our ability to proceed with the exchange offer shall be in effect. Except for the continued effectiveness of the registration statement of which this prospectus forms a part, no federal or state regulatory requirement is required to be complied with nor any federal or state regulatory approval is required to be obtained in connection with the exchange offer. See “The Exchange Offer—Conditions.” |

| |

Procedures for Tendering Old Notes Held in the Form of Book-Entry Interests | | The old notes were issued as global notes in fully registered form without interest coupons. Beneficial interests in the old notes held by direct or indirect participants in The Depository Trust Company, or DTC, are shown on, and transfers of those interests are effected only through, records maintained in book-entry form by DTC with respect to its participants. If you hold old notes in the form of book-entry interests and you wish to tender your old notes for exchange pursuant to the exchange offer, you must transmit to the exchange agent on or prior to the time of expiration of the exchange offer either: |

| | |

| | | • | | a written or facsimile copy of a properly completed and duly executed letter of transmittal, including all other documents required by such letter of transmittal, at the address set forth on the cover page of the letter of transmittal; or |

| | |

| | | • | | a computer-generated message transmitted by means of DTC’s Automated Tender Offer Program system and received by the exchange agent and forming a part of a confirmation of book-entry transfer, in which you acknowledge and agree to be bound by the terms of the letter of transmittal. |

| |

| | | The exchange agent must also receive on or prior to the expiration of the exchange offer either: |

| | |

| | | • | | a timely confirmation of book-entry transfer of your old notes into the exchange agent’s account at DTC pursuant to the procedure for book-entry transfers described in this prospectus under the heading “The Exchange Offer—Book-Entry Transfer;” or |

| | |

| | | • | | the documents necessary for compliance with the guaranteed delivery procedures described below. |

| |

| | | A letter of transmittal for your notes accompanies this prospectus. By executing the letter of transmittal or delivering a computer-generated message through DTC’s Automated Tender Offer Program system, you will represent to us that, among other things: |

| | |

| | | • | | you are not an affiliate of the issuer; |

7

| | | | |

| | | • | | you are not a broker-dealer who acquired the old notes that you are sending to the issuer directly from the issuer; |

| | |

| | | • | | the registered notes to be acquired by you in the exchange offer are being acquired in the ordinary course of your business; |

| | |

| | | • | | you are not engaging in and do not intend to engage in a distribution of the registered notes; and |

| | |

| | | • | | you do not have an arrangement or understanding with any person to participate in the distribution of the registered notes. |

| |

Procedures for Tendering Certificated Old Notes | | If you are a holder of book-entry interests in the old notes, you are entitled to receive, in limited circumstances, in exchange for your book-entry interests, certificated notes which are in equal principal amounts to your book-entry interests. See “Description of Notes—Exchange of Global Notes for Certificated Notes.” If you acquire certificated old notes prior to the expiration of the exchange offer, you must tender your certificated old notes in accordance with the procedures described in this prospectus under the heading “The Exchange Offer—Procedures for Tendering—Certificated Old Notes.” |

| |

Special Procedures for Beneficial Owners | | If you are the beneficial owner of old notes and they are registered in the name of a broker, dealer, commercial bank, trust company or other nominee and you wish to tender your old notes, you should contact the registered holder promptly and instruct the registered holder to tender on your behalf. If you wish to tender on your own behalf, you must, prior to completing and executing the letter of transmittal and delivering your old notes, either make appropriate arrangements to register ownership of the old notes in your name or obtain a properly completed bond power from the registered holder. The transfer of registered ownership may take considerable time. See “The Exchange Offer—Procedures for Tendering—Procedures Applicable to All Holders.” |

| |

Guaranteed Delivery Procedures | | If you wish to tender your old notes in the exchange offer and: |

| | |

| | | (1) | | they are not immediately available; |

| | |

| | | (2) | | time will not permit your old notes or other required documents to reach the exchange agent before the expiration of the exchange offer; or |

| | |

| | | (3) | | you cannot complete the procedure for book-entry transfer on a timely basis, |

| |

| | | you may tender your old notes in accordance with the guaranteed delivery procedures set forth in “The Exchange Offer— Procedures for Tendering—Guaranteed Delivery Procedures.” |

8

| | | | |

Acceptance of Old Notes and Delivery of Registered Notes | | Except under the circumstances described above under “The Exchange Offer—Conditions,” the issuer will accept for exchange any and all old notes which are properly tendered prior to the time of expiration. The registered notes to be issued to you in the exchange offer will be delivered promptly following the time of expiration. See “The Exchange Offer—Terms of the Exchange Offer.” |

| |

Withdrawal | | You may withdraw the tender of your old notes at any time prior to the time of expiration. We will return to you any old notes not accepted for exchange for any reason without expense to you as promptly after withdrawal, rejection of tender or termination of the exchange offer. |

| |

Exchange Agent | | Wells Fargo Bank Minnesota, National Association is serving as the exchange agent in connection with the exchange offer. |

| |

Consequences of Failure to Exchange | | If you do not participate in the exchange offer for your old notes, upon completion of the exchange offer, the liquidity of the market for your old notes could be adversely affected. See “The Exchange Offer—Consequences of Failure to Exchange.” |

| |

United States Federal Income Tax Consequences of the Exchange Offer | | The exchange of old notes for registered notes in the exchange offer will not be a taxable event for United States federal income tax purposes. See “United States Federal Income Tax Consequences.” |

9

Summary of Terms of the Registered Notes

The form and terms of the registered notes are the same as the form and terms of the old notes, except that the registered notes will be registered under the Securities Act. As a result, the registered notes will not bear legends restricting their transfer and will not contain the registration rights and liquidated damages provisions contained in the old notes. The registered notes represent the same debt as the old notes. Both the old notes and the registered notes are governed by the same indenture.

The summary below describes the principal terms of the registered notes. Some of the terms and conditions described below are subject to important limitations and exceptions. The “Description of Notes” section of this prospectus contains a more detailed description of the terms and conditions of the notes.

| | | | |

Issuer | | Michael Foods, Inc., a Delaware corporation. |

| |

Securities | | $150.0 million in principal amount of 8% Senior Subordinated Notes due 2013 registered under the Securities Act. |

| |

Maturity | | November 15, 2013. |

| |

Interest | | Annual rate: 8%. |

| |

| | | Payment frequency: every six months on May 15 and November 15. |

| |

| | | First payment: May 15, 2004. |

| |

Ranking | | The registered notes will be our unsecured senior subordinated debt. Accordingly, they will rank: |

| | |

| | | • | | junior to all of our existing and future senior debt, including borrowings under our senior credit facility and our senior unsecured term loan facility; |

| | |

| | | • | | equally with any of our future unsecured senior subordinated debt; |

| | |

| | | • | | senior to any of our future debt that expressly provides that it is subordinated to the registered notes; and |

| | |

| | | • | | effectively subordinated to any existing or future debt or other liabilities of any of our subsidiaries that do not guarantee the registered notes. |

| |

| | | As of December 31, 2003, the notes were subordinated to approximately $640.1 million of our senior debt, of which $630.0 million consisted of borrowings under our senior credit facility and our senior unsecured term loan facility. |

10

| | | | |

Guarantees | | The registered notes will be unconditionally guaranteed on an unsecured senior subordinated basis by each of our existing and future domestic subsidiaries, other than subsidiaries treated as unrestricted subsidiaries and other than immaterial subsidiaries. We refer to these subsidiaries as subsidiary guarantors and the guarantees that such subsidiary guarantors provide as the guarantees. The guarantees will rank: |

| | |

| | | • | | junior to all existing and future senior debt of the subsidiary guarantors, including the subsidiary guarantors’ guarantees of borrowings under our senior credit facility and our senior unsecured term loan facility; |

| | |

| | | • | | equally with any future unsecured senior subordinated debt of the subsidiary guarantors; and |

| | |

| | | • | | senior to all future debt of the subsidiary guarantors that expressly provides that it is subordinated to the guarantees. |

| |

| | | As of December 31, 2003, the guarantees were subordinated to approximately $640.1 million (excludes guarantees of payment of certain industrial revenue bonds in the amount of $6.4 million) of senior debt of the subsidiary guarantors, of which $630.0 million consisted of guarantees of the issuer’s borrowings under our senior credit facility and our senior unsecured term loan facility. |

| |

Optional Redemption | | We may redeem the registered notes, in whole or in part, at any time on or after November 15, 2008, at the redemption prices described in the section “Description of Notes—Optional Redemption,” plus accrued and unpaid interest. |

| |

| | | In addition, on or before November 15, 2006, we may redeem up to 40% of the registered notes with the net cash proceeds from certain equity offerings at the redemption price listed in “Description of Notes—Optional Redemption.” However, we may only make such redemptions if at least 60% of the aggregate principal amount of registered notes initially issued under the indenture remains outstanding immediately after the occurrence of such redemption. |

| |

Change of Control | | Upon the occurrence of a change in control, we must offer to repurchase the registered notes at 101% of their principal amount, plus accrued and unpaid interest, if any, to the date of repurchase. |

| |

Certain Covenants | | The indenture governing the registered notes, among other things, limits our ability and the ability of our restricted subsidiaries to: |

| | |

| | | • | | borrow money; |

| | |

| | | • | | pay dividends on or redeem or repurchase stock; |

| | |

| | | • | | make certain types of investments and other restricted payments; |

11

| | | | |

| | | • | | create liens; |

| | |

| | | • | | sell certain assets or merge with or into other companies; |

| | |

| | | • | | enter into certain transactions with affiliates; |

| | |

| | | • | | sell stock in our restricted subsidiaries; and |

| | |

| | | • | | restrict dividends or other payments from our subsidiaries. |

| |

| | | These covenants contain important exceptions, limitations and qualifications. For more information, see “Description of Notes.” |

You should refer to “Risk Factors,” beginning on page 13 for an explanation of the material risks of participating in the exchange offer and of investing in the registered notes.

12

RISK FACTORS

Participating in the exchange offer and investing in the registered notes involves a high degree of risk. You should read and consider carefully each of the following factors, as well as the other information contained in this prospectus, before making a decision on whether to participate in the exchange offer. Additional risks and uncertainties not currently known to us or those we currently deem to be immaterial may also materially and adversely affect our business operations. Any of the following risks could materially adversely affect our business, financial condition or results of operations. In such case, you may lose all or part of your original investment.

Risks Associated with the Exchange Offer

Because there is no public market for the registered notes, you may not be able to resell your registered notes.

The registered notes will be registered under the Securities Act, but will constitute a new issue of securities with no established trading market. This may adversely affect:

| | • | the liquidity of any trading market that may develop; |

| | • | the ability of holders to sell their registered notes; or |

| | • | the price at which the holders would be able to sell their registered notes. |

If a trading market were to develop, the registered notes might trade at higher or lower prices than their principal amount or purchase price, depending on many factors, including prevailing interest rates, the market for similar debentures and our financial performance.

We understand that the initial purchasers of the old notes presently intend to make a market in the notes. However, they are not obligated to do so, and any market-making activity with respect to the notes may be discontinued at any time without notice. In addition, any market-making activity will be subject to the limits imposed by the Securities Act and the Exchange Act, and may be limited during the exchange offer or the pendency of an applicable shelf registration statement. Therefore, an active trading market may not exist for the registered notes and any trading market that does develop may not be liquid.

In addition, any holder who tenders in the exchange offer for the purpose of participating in a distribution of the registered notes may be deemed to have received restricted securities, and if so, will be required to comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale transaction. For a description of these requirements, see “The Exchange Offer.”

Your old notes will not be accepted for exchange if you fail to follow the exchange offer procedures and, as a result, your old notes will continue to be subject to existing transfer restrictions and you may not be able to sell your old notes.

We will not accept your old notes for exchange if you do not follow the exchange offer procedures. We will issue registered notes as part of this exchange offer only after a timely receipt of your old notes, a properly completed and duly executed letter of transmittal and all other required documents. Therefore, if you wish to tender your old notes, please allow sufficient time to ensure timely delivery. If we do not receive your old notes, letter of transmittal and other required documents by the time of expiration of the exchange offer, we will not accept your old notes for exchange. We are under no duty to give notification of defects or irregularities with respect to the tenders of outstanding old notes for exchange. If there are defects or irregularities with respect to your tender of old notes, we will not accept your old notes for exchange.

13

If you fail to exchange your old notes, they will continue to be restricted securities and may become less liquid.

Following the exchange offer, old notes that you do not tender or that are not accepted will continue to be restricted securities. Because we anticipate that most holders of old notes will elect to exchange their old notes, we expect that the liquidity of the market for any old notes remaining after the completion of the exchange offer may be substantially limited. If you fail to exchange your old notes and continue to hold old notes, you may not offer or sell these old notes due to their status as restricted securities except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. The issuer will issue registered notes in exchange for the old notes pursuant to the exchange offer only following the satisfaction of the procedures and conditions described elsewhere in this prospectus. These procedures and conditions include timely receipt by the exchange agent of the old notes and of a properly completed and duly executed letter of transmittal.

Risks Relating to the Notes

Our substantial indebtedness could adversely affect our financial health and prevent the issuer from fulfilling the issuer’s obligations under these notes and reduce the cash available to support our business and operations.

As a result of the transactions, we have a significant amount of indebtedness.

Our substantial indebtedness could have important consequences to you. For example, it could:

| | • | make it more difficult for the issuer to satisfy the issuer’s obligations with respect to the notes; |

| | • | increase our vulnerability to general adverse economic and industry conditions; |

| | • | require us to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness, thereby reducing the availability of our cash flow to fund working capital, capital expenditures, acquisitions and investments and other general corporate purposes; |

| | • | limit our flexibility in planning for, or reacting to, changes in our business and the markets in which we operate; |

| | • | increase our vulnerability to interest rate increases as borrowings under our senior credit facility and senior unsecured term loan facility are at variable rates; |

| | • | place us at a competitive disadvantage compared to our competitors that have less debt; and |

| | • | limit, among other things, our ability to borrow additional funds. |

In addition, we may be able to incur substantial additional indebtedness in the future. The terms of the indenture governing the notes, the senior credit facility and the senior unsecured term loan facility would allow us to issue and incur additional debt upon satisfaction of certain conditions. See “Description of Notes—Certain Covenants—Incurrence of Indebtedness and Issuance of Preferred Stock” and “Description of Credit Facilities.” As of December 31, 2003, we had $93.5 million available for additional borrowing under the revolving credit facility under the senior credit facility after taking into account $6.5 million of outstanding letters of credit. If new debt is added to current debt levels, the related risks described above could intensify.

Your right to receive payments on the notes is junior to the issuer’s existing senior indebtedness and possibly all of the issuer’s future borrowings. Further, the guarantees of the notes are junior to all of the guarantors’ existing senior indebtedness and possibly to all their future borrowings.

The notes and the guarantees which are unsecured, rank junior to all of the issuer’s and the subsidiary guarantors’ existing senior indebtedness, including the issuer’s borrowings and the related guarantees by the subsidiary guarantors under the senior credit facility and the senior unsecured term loan facility, and all of the

14

issuer’s and the subsidiary guarantors’ future senior indebtedness. As a result of that subordination, upon any distribution to the issuer’s creditors or the creditors of the subsidiary guarantors in a bankruptcy, liquidation or reorganization or similar proceeding relating to the issuer or the subsidiary guarantors or the issuer’s or the guarantors’ property, the holders of senior debt of the issuer and the subsidiary guarantors will be entitled to be paid in full before any payment may be made with respect to the notes or the subsidiary guarantees. In addition, all payments on the notes and the guarantees will be blocked in the event of a payment default on designated senior debt and may be blocked for up to 179 consecutive days in the event of certain non-payment defaults on designated senior debt. In the event of a bankruptcy, liquidation or reorganization or similar proceeding relating to the issuer or the subsidiary guarantors, the indenture relating to the notes requires that amounts otherwise payable to holders of the notes in a bankruptcy or similar proceeding be paid to holders of senior debt instead until the holders of the senior debt are paid in full. As a result, holders of the notes may not receive all amounts owed to them and may receive less, ratably, than holders of trade payables and other unsubordinated indebtedness in any such proceeding. As of December 31, 2003, the notes were subordinated to approximately $640.1 million of senior debt of the issuer, of which $630.0 million consisted of borrowings under the senior credit facility and senior unsecured term loan facility, and the guarantees were subordinated to approximately $646.5 million of senior debt of the subsidiary guarantors, of which $630.0 million consisted of guarantees of the issuer’s borrowings under the senior credit facility and senior unsecured term loan facility. In addition, approximately $93.5 million were available for borrowing as additional senior debt under the revolving credit facility of the senior credit facility. We will be permitted to borrow substantial additional indebtedness, including senior debt, in the future.

Since the notes are unsecured, your right to collect from our assets may be limited by the right of certain of our commodity suppliers if we default in payment to these commodity suppliers.

Upon default in payment to certain of the issuer’s and the subsidiary guarantors’ commodity suppliers, federal and state laws, including the Perishable Agricultural Commodities Act and the Minnesota Wholesale Produce Distributors Act, may create for these suppliers a floating statutory trust, which in effect grants these unpaid suppliers a claim on all of the issuer’s and the subsidiary guarantors’ inventories and products before the holders of secured or unsecured debt, including the notes.

Since the notes are unsecured, your right to collect from our assets is limited by the rights of holders of secured debt.

If the issuer becomes insolvent or is liquidated, or if payment under the senior credit facility is accelerated, the lenders under the senior credit facility will be entitled to exercise the remedies available to a secured lender under applicable law. The lenders under the senior credit facility will have a claim on all assets securing the senior credit facility before the holders of unsecured debt, including the notes. The issuer’s obligations under the notes are unsecured, while the issuer’s obligations under the senior credit facility are secured by substantially all of the issuer’s assets and those of the issuer’s subsidiaries. In addition, the notes are contractually subordinated to all existing and future senior debt of the issuer. See “Description of Credit Facilities.”

The issuer will require a significant amount of cash to service its indebtedness and the issuer’s ability to generate cash depends on many factors beyond the issuer’s control.

The issuer’s business may not generate sufficient cash flow to make payments on and to refinance its indebtedness, including the notes and amounts borrowed under the senior credit facility and the senior unsecured term loan facility, and to fund planned capital expenditures and expansion efforts and any strategic acquisitions we may make, if any. Our business may not generate sufficient cash flow from operations in the future due to our failure to properly manage our business or due to general economic, financial, competitive and other factors that are beyond our control.

15

In addition, our currently anticipated growth in net sales and cash flow may not be realized on schedule and future borrowings may not be available to us under the senior credit facility in amounts sufficient to enable the repayment of indebtedness, including the notes, or to fund other liquidity needs. We may need to refinance all or a portion of our indebtedness, including the notes, on or before maturity. We may not be able to refinance any of our debt, including the senior credit facility, the senior unsecured term loan facility and the notes, on commercially reasonable terms or at all.

The senior credit facility, the senior unsecured term loan facility and the indenture related to the notes contain various covenants which limit our management’s discretion in the operations of our business.

The senior credit facility, the senior unsecured term loan facility and the indenture related to the notes contain various provisions which limit our management’s discretion in managing our business by, among other things, restricting our ability to:

| | • | pay dividends on stock or repurchase stock; |

| | • | make certain types of investments and other restricted payments; |

| | • | use assets as security in other transactions; |

| | • | sell certain assets or merge with or into other companies; |

| | • | enter into certain transactions with affiliates; |

| | • | sell stock in certain of our subsidiaries; and |

| | • | restrict dividends or other payments to the issuer of the notes. |

In addition, the senior credit facility requires us to meet certain financial ratios. Covenants in the senior credit facility also require us to use a portion of the proceeds we receive in specified debt or equity issuances to repay outstanding borrowings under our senior credit facility.

Any failure to comply with the restrictions of the senior credit facility, the senior unsecured term loan facility, the indenture related to the notes or any other subsequent financing agreements may result in an event of default. Such default may allow the creditors, if the agreements so provide, to accelerate the related debt and may result in the acceleration of any other debt to which a cross-acceleration or cross-default provisions applies. In addition, the lenders may be able to terminate any commitments they had made to provide us with further funds.

The issuer may not have the ability to raise the funds necessary to finance the change of control offer required by the indenture.

Upon the occurrence of certain specific kinds of change of control events, the issuer will be required to offer to repurchase all outstanding notes. However, it is possible that the issuer will not have sufficient funds at the time of the change of control to make the required repurchase of notes or that restrictions in the senior credit facility will not allow such repurchases. The issuer’s ability to repurchase these notes upon certain specific kinds of change of control events may be limited by the terms of the issuer’s senior indebtedness and the subordination provisions of the indenture. For example, the senior credit facility will prohibit the issuer from repurchasing the notes after certain specific kinds of change of control events until the issuer first repays debt under the senior credit facility in full or obtains a waiver from the bank lenders. If the issuer fails to repurchase the notes in that circumstance, it will go into default under the indenture related to the notes and the senior credit facility. The senior unsecured term loan facility also contains similar provisions to those specified in this paragraph. Any future debt which we incur may also contain restrictions on repayment which come into effect upon certain specific kinds of change of control events. If a change of control occurs, we may not have sufficient funds to repay other debt obligations which will be required to be repaid, in addition to the notes. See “Description of Notes—Repurchase at the Option of Holders—Change of Control” and “Description of Credit Facilities.”

16

Federal and state statutes allow courts, under specific circumstances, to void the notes or the guarantees and require noteholders to return payments received from the issuer or the subsidiary guarantors.

If a bankruptcy case or lawsuit is initiated by unpaid creditors of the issuer or any subsidiary guarantor, the debt represented by the notes or the guarantees may be reviewed under the federal bankruptcy law and comparable provisions of state fraudulent transfer laws. Under these laws, the notes or the guarantee could be voided, or claims in respect of the notes or the guarantees could be subordinated to the issuer’s or the applicable subsidiary guarantor’s other debt.

In addition, any payment to holders of the notes by the issuer or a subsidiary guarantor pursuant to the notes or the guarantees, as the case may be, could be voided and required to be returned by holders of the notes to the issuer or such subsidiary guarantor, or to a fund for the benefit of the creditors of the issuer or such subsidiary guarantor.

If a guarantee were voided as a fraudulent conveyance or held unenforceable for any other reason, holders of the notes would be solely creditors of the issuer and creditors of our other subsidiaries that have validly guaranteed the notes. The notes then would be effectively subordinated to all obligations of the subsidiary whose guarantee was voided.

To the extent that the claims of the holders of the notes against the issuer or any subsidiary guarantor were subordinated in favor of other creditors of the issuer or such subsidiary guarantor, such other creditors would be entitled to be paid in full before any payment could be made on the notes or the guarantees. If one or more of the guarantees is voided or subordinated, after providing for all prior claims, there may not be sufficient assets remaining to satisfy the claims of the holders of these notes.

Risks Relating to Our Company and the Industries We Serve

Our operating results are significantly affected by egg, potato and cheese market prices and the prices of other raw materials, such as grain, which can fluctuate widely.

Our operating results are significantly affected by egg, potato and cheese prices and the prices of corn and soybean meal, which are the primary feedstock used in our internal production of eggs. The prices of these raw materials fluctuate widely, which fluctuations may adversely affect our operating results. For example, for the year ended December 31, 2003, costs of eggs purchased from third-party suppliers and corn and soybean meal fed to our internal flocks were approximately $374.0 million, which represented 54% of total cost of sales for the egg products division. A majority of this amount consisted of purchases of eggs from third-party suppliers.

Eggs, corn and soybean meal are each commodities that are subject to significant price fluctuations due to market conditions. For illustrative purposes, our yearly average cost of eggs, corn and soybean meal for the past ten years is set forth below:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 1994

| | 1995

| | 1996

| | 1997

| | 1998

| | 1999

| | 2000

| | 2001

| | 2002

| | 2003

|

| | | (in dollars) |

Liquid whole eggs (per pound) | | $ | 0.35 | | $ | 0.36 | | $ | 0.50 | | $ | 0.43 | | $ | 0.38 | | $ | 0.31 | | $ | 0.30 | | $ | 0.30 | | $ | 0.31 | | $ | 0.50 |

Corn (per bushel) | | | 2.50 | | | 2.81 | | | 3.68 | | | 2.75 | | | 2.38 | | | 2.11 | | | 2.11 | | | 2.10 | | | 2.28 | | | 2.34 |

Soybean meal (per ton) | | | 180 | | | 181 | | | 240 | | | 246 | | | 158 | | | 139 | | | 169 | | | 163 | | | 166 | | | 1.94 |

In general, the pricing of eggs is affected by an inelasticity of supply and demand, in connection with which small increases in production or decreases in demand can have a large effect on prices. Our operating profit has historically been adversely affected when egg and grain prices rise. In addition, our operating profit has historically been negatively impacted during extended periods of low egg prices. For example, during 2000 the operating profits for our lower value-added egg products sold mostly to industrial ingredient customers declined

17

by approximately $14.0 million due, in part, to a decline in egg prices to a fifteen year low in mid-2000. This resulted in a decline in operating profits for the egg products division as a whole, as the growth in sales and earnings of our higher value-added products was insufficient to fully offset this decline. Egg prices have experienced an upward trend since 2002 rising to historical highs in late 2003 and early 2004. Furthermore, grain prices, particularly for soybean meal, began rising sharply in late 2003 and have continued rising in 2004. Therefore, changes in the price of eggs, corn or soybean meal may have a material adverse affect on our business, prospects, results of operations or financial condition. We also can experience similar negative effects on our results of operations because of increases in the price of potatoes and cheese. Although we can take steps to mitigate the effects of changes to our raw material costs, fluctuations in prices are outside of our control. For a description of our risk management strategy designed to reduce the impacts of changes in these commodity prices, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Commodity Risk Management” and “Business—Egg Products Division—Commodity Risk Management.”

We produce and distribute food products that are susceptible to microbial contamination.

Many of our food products, particularly egg products, are vulnerable to contamination by disease producing organisms, or pathogens, contained in food, such asListeria monocytogenes andSalmonella enteritidis, which are generally found in the environment. Shipment of adulterated products, even if inadvertent, is a violation of law and may lead to an increased risk of exposure to product liability claims, as discussed below, product recalls and increased scrutiny by federal and state regulatory agencies and may have a material adverse effect on our reputation, business, prospects, results of operations and financial condition. The risk may be controlled, but may not be eliminated, by adherence to good manufacturing practices and finished product testing. Also, products purchased from others for repacking or distribution may contain contaminants that may be inadvertently redistributed by us. Once contaminated products have been shipped for distribution, illness and death may result if the pathogens are not eliminated by processing at the foodservice or consumer level. In 2000, our refrigerated distribution division recalled certain cheese products manufactured for us by a third party due to a possible listeria contamination. See “Business—Food Safety.”

As a result of selling food products, we face the risk of exposure to product liability claims.

We face the risk of exposure to product liability claims and adverse public relations in the event that our quality control procedures fail and the consumption of our products cause injury or illness. If a product liability claim is successful, our insurance may not be adequate to cover all liabilities we may incur, and we may not be able to continue to maintain such insurance, or obtain comparable insurance at a reasonable cost, if at all. We generally seek contractual indemnification and insurance coverage from parties supplying us products, but this indemnification or insurance coverage is limited by the creditworthiness of the indemnifying party, and their insurance carriers, if any, as well as the insured limits of any insurance provided by suppliers. If we do not have adequate insurance or contractual indemnification available, product liability claims relating to defective products could have a material adverse effect on our business reputation and earnings. In addition, even if a product liability claim is not successful or is not fully pursued, the negative publicity surrounding any assertion that our products caused illness or injury could have a material adverse effect on our reputation with existing and potential customers and on our business, prospects, results of operations and financial condition. See “Business—Food Safety.”

A decline in egg consumption or in the consumption of processed food products would have a material adverse effect on our net sales and results of operations.

Adverse publicity relating to health concerns and the nutritional value of eggs and egg products could adversely affect egg consumption and consequently demand for our processed egg products, which would have a material adverse effect on our business, prospects, results of operations and financial condition. In addition, as almost all of our operations consist of the production and distribution of processed food products, a change in

18

consumer preferences relating to processed food products or in consumer perceptions regarding the nutritional value of processed food products could adversely affect demand, which would have a material adverse effect on our business, prospects, results of operations, liquidity and financial condition.

The categories of the food industry in which we operate are highly competitive, and our inability to compete successfully could adversely affect our business, prospects, results of operations and financial condition.

Competition in each of the categories of the food industry within which we operate is intense. Increased competition against any of our products could result in price reduction, reduced margins and loss of market share, which could negatively affect our business, prospects, results of operations and financial condition. In particular, we compete with major companies such as Cargill Incorporated, Kraft Foods, Inc. and ConAgra Foods. Each of these companies has substantially greater financial resources, name recognition, research and development, marketing and human resources than we have. In addition, our competitors may succeed in developing new or enhanced products which are better than our products. These companies may also prove to be more successful than we are in marketing and selling these products. We may not be able to compete successfully with any or all of these companies.

Our largest customers have historically accounted for a significant portion of our net sales volume. Accordingly, our business may be adversely affected by the loss of, or reduced purchases by, one or more of our large customers.

Our largest customers have historically accounted for a significant portion of the net sales volume of each of our divisions. If, for any reason, one of our key customers were to purchase significantly less of our products in the future or were to terminate its purchases from us, and we are not able to sell our products to new customers at comparable or greater levels, our business, prospects, financial condition and results of operations may be materially adversely effected. For more information, see the “Customers” section for each of our divisions in “Business.”

Our business relies on patents and trademarks. The loss or expiration of a patent, whether licensed or owned, or the loss of any trademark could negatively impact our ability to produce and sell the products associated with such patent or trademark, which could have a material adverse effect on our sales volume and net income.

We rely on patents, trademarks, trade secrets and other intellectual property in our business, the loss or expiration of which could negatively impact our ability to produce and sell the associated products, which could have a material adverse effect on our results of operations. In addition, as a result of infringement or misappropriation by third parties, we have been engaged and may continue to be engaged in extensive legal proceedings, along with the owner of the licensed patents, against some of the parties we believe to be infringing on the licensed patents. See “Business—Legal Proceedings” for a summary of these proceedings. In 1988, we obtained an exclusive license to use patented processes developed and owned by North Carolina State University involving the ultrapasteurization of liquid eggs. Four of the five patents licensed to us under this license expire in 2006 and are used in the production of ESL liquid egg products. Our license to use each of these patents will continue until the expiration of the patents. In addition to some of our competitors already using these patented processes in violation of our rights under the license, we believe additional parties may begin to produce and market processed egg products that are similar to ours when the licensed patents expire. Moreover, our competitors may develop and use technology in the production and development of liquid egg products that does not violate the patents that we license.

We also own several registered and unregistered trademarks that are used in the marketing and sale of our products. We have invested a substantial amount of money in promoting our trademarked brands. However, the degree of protection that these trademarks afford us is unknown.

We may not have the resources necessary to engage in actions to prevent infringement of our trademarks or the patents that we license. The steps we have taken to protect our intellectual property rights may not be

19

adequate to prevent third parties from infringing or misappropriating our intellectual property rights. Any such infringement, misappropriation or termination of the patent license, or the expiration, lapsing, or invalidation of the licensed patents, our trademarks or other intellectual property, could have a material adverse effect on our business, prospects, results of operations and financial condition. For more information, see “Business—Proprietary Technologies and Trademarks.”

Government regulation could increase our costs of production and increase our legal and regulatory expenses.

Our manufacture, processing, packaging, storage, distribution and labeling of food products are subject to extensive federal, state and local regulation, including regulation by the Food and Drug Administration, or the FDA, the United States Department of Agriculture, or the USDA, and various state and local health and agricultural agencies. Public health concerns about animal feed could lead to modified regulations regarding hen feed which could require us to replace ingredients we currently use in feeding our internal flocks with more expensive alternatives, increasing our egg production costs and adversely affecting our results of operations and financial position. In addition, some of our facilities are subject to continuous on-site inspections. Applicable statutes and regulations governing food products include rules for identifying the content of specific types of foods, the nutritional value of that food and its serving size. Many jurisdictions also provide that food manufacturers adhere to good manufacturing practices (the definition of which may vary by jurisdiction) with respect to production processes. In addition, our production and distribution facilities are subject to various federal, state and local environmental and workplace regulations. Failure to comply with all applicable laws and regulations could subject us to civil remedies, including fines, injunctions, recalls or seizures, and criminal sanctions, which could have a material adverse effect on our business, financial condition and results of operations. Furthermore, compliance with current or future laws or regulations could require us to make material expenditures or otherwise adversely affect the way we operate our business, our prospects, results of operations and financial condition.

We may incur unexpected costs associated with compliance with environmental regulations.

We are subject to federal, state, and local environmental requirements, including those governing discharges to air and water, the management of hazardous substances, the disposal of solid and hazardous wastes, and the remediation of contamination. If we do not fully comply with environmental regulations, or if a release of hazardous substances occurs at or from one of our facilities, we may be subject to penalties and/or held liable for the cost of remedying the condition. For example, in 2000, 2002 and 2003, we were required to upgrade the wastewater treatment systems at three of our facilities. We expect that in 2004 our Papetti’s subsidiary will be required to pay a fine of approximately $200,000 in connection with regulatory noncompliance relating to one of the facilities. We may be required to upgrade the systems at other facilities in the future. The operational and financial effects associated with compliance with the variety of environmental regulations we are subject to could require us to make material expenditures or otherwise adversely affect the way we operate our business and our prospects, results of operations and financial condition. See “Business—Environmental Regulation.”

Extreme weather conditions, disease and pests could harm our business.

All of our business activities are subject to a variety of agricultural risks. Unusual weather conditions, disease and pests can materially and adversely affect the quality and quantity of the food products we produce and distribute. These factors could affect a substantial portion of our production facilities in any year and have a material adverse effect on our business, prospects, results of operations or financial condition.

The categories of the food industry in which we compete are labor intensive, and if we cannot attract and retain qualified employees, we may not be able to implement our operating strategies.

The categories of the food industry in which we compete are labor intensive. Labor shortages, the inability to hire or retain qualified employees or increased labor costs could have a material adverse effect on our ability

20

to control expenses and efficiently conduct our operations. Some of our operations have experienced a high rate of employee turnover and could continue to experience high turnover in the future. We may not be able to continue to hire and retain the sufficiently skilled labor force necessary to operate efficiently and to support our operating strategies. In addition, we may not continue to experience favorable labor relations and our labor expenses could increase as a result of a continuing shortage in the supply of personnel.

Strikes, work stoppages and slowdowns could negatively affect our results of operations.

We currently participate in a union contract which extends through December 31, 2007, that covers, as of December 31, 2003, 183 employees of our potato products division, constituting approximately 72.1% of the division’s employees and 4.8% of all our 3,806 employees. Our unionized workforce may initiate a strike, work stoppage or slowdown, in which event our business, prospects, results of operations and financial condition could be adversely affected and we may not be able to adequately meet the needs of our customers utilizing our remaining workforce. In addition, we could have similar actions with our non-unionized workforce. Furthermore, our non-unionized workforce could become unionized in the future.

Our industry and the sales of our products are subject to seasonal variations and, as a result, our quarterly operating results may fluctuate.

Our quarterly operating results are affected by the seasonal fluctuations of our net sales and operating profits. Accordingly, the market price of the notes may fluctuate significantly. Shell eggs prices typically rise seasonally in the first and fourth quarters of the year due to increased demand during holiday periods. Consequently, we generally experience higher net sales from our egg products division in our first and fourth quarters. Operating profits from the potato products division are less seasonal, but tend to be higher in the second half of the year, coinciding with the potato harvest. Our refrigerated distribution division typically experiences higher net sales and operating profits in the fourth quarter as a result of increasing consumer demand during the holiday season. As a result of these seasonal and quarterly fluctuations, we believe that comparisons of our sales and operating results between different quarters within a single fiscal year are not necessarily meaningful and that these comparisons cannot be relied upon as indicators of our future performance.

Our business operations could be significantly disrupted if we lost members of our management team.

Our success depends to a significant degree upon the continued contributions of our executive officers and key employees, both individually and as a group and our future performance will be substantially dependent on our ability to retain and motivate them. In particular, the loss of our president and chief executive officer, Gregg A. Ostrander, our chief operating officer, James D. Clarkson, and our executive vice president and chief financial officer, John D. Reedy, could prevent us from executing our business strategy. We maintain employment agreements with Messrs. Ostrander, Clarkson and Reedy and key man life insurance for each of them other than Mr. Clarkson. See “Management—Directors, Executive Officers and Key Employees.”

Pressure from animal rights groups regarding the treatment of animals may subject us to additional costs to conform our practices to comply with these developing standards or subject us to marketing costs to defend challenges to our current practices and protect our image with our customers.

Many of our customers are facing pressure from animal rights groups, such as People for the Ethical Treatment of Animals, or PETA, to require that any companies that supply them with food products operate their business in a manner that treats animals in conformity with certain standards developed by these animal rights groups. Changing our procedures and infrastructure to conform to these guidelines could add significant additional costs to our internal production of eggs, including cost increases from housing and feeding the increased flock population resulting from the termination of molting practices, and the cost for us to purchase eggs from our third-party suppliers. We may not be able to pass on these costs to customers who require us to meet these standards. Nevertheless, we are facing increasing pressure from some of our largest customers to change our operating procedures with respect to our flock of 13.5 million hens to meet some or all of these

21

developing treatment standards. The treatment standards, among other things, generally require that we provide increased cage space for our hens, stop beak trimming and stop forced molting (the act of putting birds into a regeneration cycle). These increased costs may adversely affect our business and results of operations.

Under a provision of the State of Nebraska’s constitution, we may be required to divest real property we hold in that state, which could subject us to prolonged litigation and have a material adverse effect on our business, prospects, financial condition and results of operations.

In the year ended December 31, 2003, approximately 24% of our total shell egg requirements were met by the Nebraska operations of our egg products division and approximately 70% of our producing hens were located in Nebraska. A provision of the constitution of the State of Nebraska generally prohibits corporations from engaging in farming or ranching in Nebraska and therefore may require us to divest our Nebraska egg production operations. Although the constitutional provision contains an exemption for agricultural land operated by a corporation for the purpose of raising poultry, the Attorney General of Nebraska has, in written opinions, taken the position that facilities devoted primarily to the production of eggs do not fall within such exemption and therefore remain subject to the restrictions contained in the constitutional provision. The constitution empowers the Attorney General of Nebraska, or if the Attorney General fails to act, any citizen of Nebraska, to obtain a court order to, among other things, force a divestiture of land held in violation of this constitutional provision. If land subject to such a court order is not divested within a two-year period, the constitutional provision directs the court to declare the land escheated, or forfeited, to the State of Nebraska. Our current view that our egg production facilities in Nebraska are part of integrated facilities for the production, processing and distribution of egg products, and therefore used for non-farming and non-ranching purposes, may be rejected by a Nebraska court, in which event our operations in Nebraska would be subject to the constitutional provision. In the event we are forced to divest our egg production operations in Nebraska or become involved in prolonged litigation or other proceedings relating to a possible divestiture, our business, prospects, results of operations and financial condition could be materially adversely affected. For more information, see “Business—Government Regulation.”

The interests of the issuer’s controlling stockholder could conflict with those of the holders of the notes.