UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-10407

Master Portfolio Trust

(Exact name of registrant as specified in charter)

620 Eighth Avenue, 47th Floor, New York, NY 10018

(Address of principal executive offices) (Zip code)

Marc A. De Oliveira

Franklin Templeton

100 First Stamford Place

Stamford, CT 06902

(Name and address of agent for service)

Registrant’s telephone number, including area code:

877-6LM-FUND/656-3863

Date of fiscal year end: August 31

Date of reporting period: August 31, 2024

| ITEM 1. | REPORT TO STOCKHOLDERS. |

The Annual Report to Stockholders is filed herewith.

| | |

Liquid Reserves Portfoliotrue | |

| Annual Shareholder Report | August 31, 2024 |

|

This annual shareholder report contains important information about Liquid Reserves Portfolio for the period September 1, 2023, to August 31, 2024.

You can find additional information about the Fund at https://www.franklintempleton.com/regulatory-masterfunds-documents. You can also request this information by contacting us at 877-6LM-FUND/656-3863.

This report describes changes to the Fund that occurred during the reporting period.

WHAT WERE THE FUND COSTS FOR THE LAST YEAR? (based on a hypothetical $10,000 investment)

| | |

Fund Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment* |

| Liquid Reserves Portfolio | $1 | 0.01% |

| * | Reflects fee waivers and/or expense reimbursements, without which expenses would have been higher. Additional amounts may be voluntarily waived and/or reimbursed from time to time. |

KEY FUND STATISTICS (as of August 31, 2024)

| |

Total Net Assets | $8,307,942,958 |

Total Number of Portfolio Holdings | 73 |

Total Management Fee Paid | $0 |

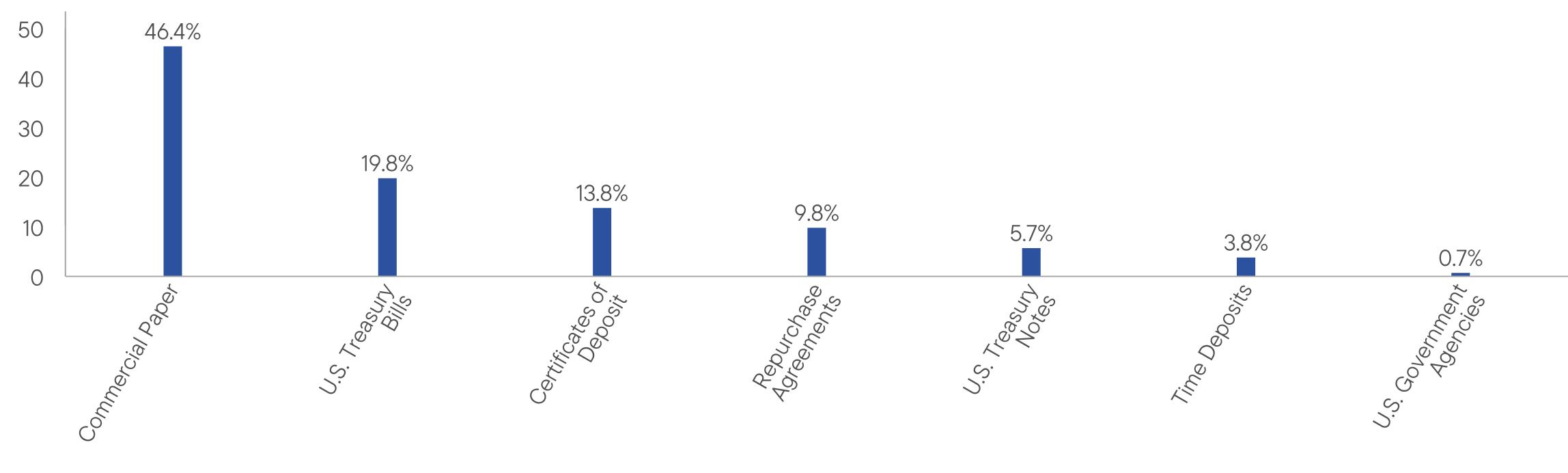

WHAT DID THE FUND INVEST IN? (as of August 31, 2024)

Portfolio Composition (% of Total Investments)

| Liquid Reserves Portfolio | PAGE 1 | 98066-AHTSR-1024 |

HOW HAS THE FUND CHANGED?

Effective October 2, 2023, pursuant to amendments to Rule 2a-7 under the Investment Company Act of 1940, as amended (“Rule 2a-7”), the Portfolio may no longer impose a redemption gate and the application of liquidity fees, if any, is no longer tied to the Portfolio’s weekly liquid assets.

Effective October 2, 2024, pursuant to Rule 2a-7, if Liquid Reserves Portfolio has total daily net redemptions that exceed 5% of the Portfolio’s net assets, or such smaller amount of net redemptions as the Board of Trustees of the Portfolio determines, based on flow information available within a reasonable period after the last computation of the Portfolio’s net asset value on that day, Liquid Reserves Portfolio may be required to apply a liquidity fee to all shares that are redeemed at a price computed on that day.

This is a summary of certain changes to the Portfolio since September 1, 2023.

| |

| WHERE CAN I FIND ADDITIONAL INFORMATION ABOUT THE FUND? |

Additional information is available on https://www.franklintempleton.com/regulatory-masterfunds-documents, including its: |

| • proxy voting information • financial information • holdings • tax information |

| Liquid Reserves Portfolio | PAGE 2 | 98066-AHTSR-1024 |

46.419.813.89.85.73.80.7

The registrant has adopted a code of ethics that applies to the registrant’s principal executive officer, principal financial officer, principal accounting officer or controller.

| ITEM 3. | AUDIT COMMITTEE FINANCIAL EXPERT. |

The Board of Trustees of the registrant has determined that Robert Abeles, Jr., possesses the technical attributes identified in Instruction 2(b) of Item 3 to Form N-CSR to qualify an “Audit Committee’s financial expert,” and has designated Mr. Abeles, Jr. as the Audit Committee’s financial expert. Mr. Abeles, Jr. is an “independent” Trustees pursuant to paragraph (a) (2) of Item 3 to Form N-CSR.

| Item 4. | Principal Accountant Fees and Services. |

a) Audit Fees. The aggregate fees billed in the last two fiscal year ending August 31, 2023 and August 31, 2024 (the “Reporting Periods”) for professional services rendered by the Registrant’s principal accountant (the “Auditor”) for the audit of the Registrant’s annual financial statements, or services that are normally provided by the Auditor in connection with the statutory and regulatory filings or engagements for the Reporting Periods, were $125,406 in August 31, 2023 and $125,406 in August 31, 2024.

b) Audit-Related Fees. The aggregate fees billed in the Reporting Period for assurance and related services by the Auditor that are reasonably related to the performance of the Registrant’s financial statements were $0 in August 31, 2023 and $0 in August 31, 2024.

(c) Tax Fees. The aggregate fees billed in the Reporting Periods for professional services rendered by the Auditor for tax compliance, tax advice and tax planning (“Tax Services”) were $39,000 in August 31, 2023 and $39,000 in August 31, 2024. These services consisted of (i) review or preparation of U.S. federal, state, local and excise tax returns; (ii) U.S. federal, state and local tax planning, advice and assistance regarding statutory, regulatory or administrative developments, and (iii) tax advice regarding tax qualification matters and/or treatment of various financial instruments held or proposed to be acquired or held.

There were no fees billed for tax services by the Auditors to service affiliates during the Reporting Periods that required pre-approval by the Audit Committee.

d) All Other Fees.

There was no other fee billed in the Reporting Periods for products and services provided by the Auditor, other than the services reported in paragraphs (a) through (c) for the Item for the Master Portfolio Trust.

All Other Fees. There were no other non-audit services rendered by the Auditor to Franklin Templeton Fund Adviser, LLC (“FTFA”), and any entity controlling, controlled by or under common control with FTFA that provided ongoing services to Master Portfolio Trust requiring pre-approval by the Audit Committee in the Reporting Period.

(e) Audit Committee’s pre–approval policies and procedures described in paragraph (c) (7) of Rule 2-01 of Regulation S-X.

(1) The Charter for the Audit Committee (the “Committee”) of the Board of each registered investment company (the “Fund”) advised by FTFA or one of their affiliates (each, an “Adviser”)

requires that the Committee shall approve (a) all audit and permissible non-audit services to be provided to the Fund and (b) all permissible non-audit services to be provided by the Fund’s independent auditors to the Adviser and any Covered Service Providers if the engagement relates directly to the operations and financial reporting of the Fund. The Committee may implement policies and procedures by which such services are approved other than by the full Committee.

The Committee shall not approve non-audit services that the Committee believes may impair the independence of the auditors. As of the date of the approval of this Audit Committee Charter, permissible non-audit services include any professional services (including tax services), that are not prohibited services as described below, provided to the Fund by the independent auditors, other than those provided to the Fund in connection with an audit or a review of the financial statements of the Fund. Permissible non-audit services may not include: (i) bookkeeping or other services related to the accounting records or financial statements of the Fund; (ii) financial information systems design and implementation; (iii) appraisal or valuation services, fairness opinions or contribution-in-kind reports; (iv) actuarial services; (v) internal audit outsourcing services; (vi) management functions or human resources; (vii) broker or dealer, investment adviser or investment banking services; (viii) legal services and expert services unrelated to the audit; and (ix) any other service the Public Company Accounting Oversight Board determines, by regulation, is impermissible.

Pre-approval by the Committee of any permissible non-audit services is not required so long as: (i) the aggregate amount of all such permissible non-audit services provided to the Fund, the Adviser and any service providers controlling, controlled by or under common control with the Adviser that provide ongoing services to the Fund (“Covered Service Providers”) constitutes not more than 5% of the total amount of revenues paid to the independent auditors during the fiscal year in which the permissible non-audit services are provided to (a) the Fund, (b) the Adviser and (c) any entity controlling, controlled by or under common control with the Adviser that provides ongoing services to the Fund during the fiscal year in which the services are provided that would have to be approved by the Committee; (ii) the permissible non-audit services were not recognized by the Fund at the time of the engagement to be non-audit services; and (iii) such services are promptly brought to the attention of the Committee and approved by the Committee (or its delegate(s)) prior to the completion of the audit.

(2) None of the services described in paragraphs (b) through (d) of this Item were performed in reliance on paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) Not applicable.

(g) Non-audit fees billed by the Auditor for services rendered to Master Portfolio Trust, FTFA and any entity controlling, controlled by, or under common control with FTFA that provides ongoing services to Master Portfolio Trust during the reporting period were $350,359 in August 31, 2023 and $342,635 in August 31, 2024.

(h) Yes. Master Portfolio Trust’s Audit Committee has considered whether the provision of non-audit services that were rendered to Service Affiliates, which were not pre-approved (not requiring pre-approval), is compatible with maintaining the Accountant’s independence. All services provided by the Auditor to the Master Portfolio Trust or to Service Affiliates, which were required to be pre-approved, were pre-approved as required.

(i) Not applicable.

(j) Not applicable.

| ITEM 5. | AUDIT COMMITTEE OF LISTED REGISTRANTS. |

| a) | The independent board members are acting as the registrant’s audit committee as specified in Section 3(a)(58)(B) of the Exchange Act. The Audit Committee consists of the following Board members: |

Robert Abeles, Jr.

Jane F. Dasher

Anita L. DeFrantz

Susan B. Kerley

Michael Larson

Avedick B. Poladian

William E.B. Siart

Jaynie M. Studenmund

Peter J. Taylor

| ITEM 6. | SCHEDULE OF INVESTMENTS. |

| (a) | Please see schedule of investments contained in the Financial Statements and Financial Highlights included under Item 7 of this Form N-CSR. |

| ITEM 7. | FINANCIAL STATEMENTS AND FINANCIAL HIGLIGHTS FOR OPEN-END MANAGEMENT INVESTMENT COMPANIES. |

Schedule of InvestmentsAugust 31, 2024 Liquid Reserves Portfolio

(Percentages shown based on Portfolio net assets)

| | | | | |

Short-Term Investments — 95.5% |

|

| | | | |

Atlantic Asset Securitization LLC | | | | |

| | | | |

| | | | |

| | | | |

| | | | |

Bedford Row Funding Corp. | | | | |

Bedford Row Funding Corp. | | | | |

| | | | |

| | | | |

BofA Securities Inc. (SOFR + 0.430%) | | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

Great Bear Funding DAC/Great Bear Funding LLC | | | | |

Great Bear Funding DAC/Great Bear Funding LLC | | | | |

ING U.S. Funding LLC (SOFR + 0.230%) | | | | |

| | | | |

| | | | |

| | | | |

Longship Funding DAC/Longship Funding LLC | | | | |

Longship Funding DAC/Longship Funding LLC | | | | |

| | | | |

Oversea-Chinese Banking Corp. Ltd. | | | | |

Oversea-Chinese Banking Corp. Ltd. | | | | |

| | | | |

| | | | |

Skandinaviska Enskilda Banken AB (SOFR + 0.220%) | | | | |

| | | | |

Societe Generale SA (SOFR + 0.330%) | | | | |

| | | | |

See Notes to Financial Statements.

Liquid Reserves Portfolio 2024 Annual Report

Schedule of Investments (cont’d)August 31, 2024 Liquid Reserves Portfolio

(Percentages shown based on Portfolio net assets)

| | | | | |

Commercial Paper — continued |

Starbird Funding Corp. (SOFR + 0.220%) | | | | |

Sumitomo Mitsui Trust Bank Ltd. | | | | |

Sumitomo Mitsui Trust Bank Ltd. | | | | |

Sumitomo Mitsui Trust Bank Ltd. | | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

| | | | |

Victory Receivables Corp. | | | | |

|

| |

U.S. Treasury Bills — 19.0% |

U.S. Cash Management Bill | | | | |

| | | | |

| | | | |

| | | | |

| | | | |

|

Total U.S. Treasury Bills | |

Certificates of Deposit — 13.2% |

| | | | |

| | | | |

Bank of Nova Scotia (SOFR + 0.210%) | | | | |

Credit Agricole Corporate and Investment Bank | | | | |

Credit Agricole Corporate and Investment Bank | | | | |

| | | | |

| | | | |

Natixis SA (SOFR + 0.420%) | | | | |

Oversea-Chinese Banking Corp. Ltd. (SOFR + 0.180%) | | | | |

Sumitomo Mitsui Trust Bank Ltd. | | | | |

| | | | |

|

Total Certificates of Deposit | |

U.S. Treasury Notes — 5.4% |

U.S. Treasury Notes (3 mo. U.S. Treasury Money Market Yield + 0.170%) | | | | |

U.S. Treasury Notes (3 mo. U.S. Treasury Money Market Yield + 0.245%) | | | | |

See Notes to Financial Statements.

Liquid Reserves Portfolio 2024 Annual Report

Liquid Reserves Portfolio

(Percentages shown based on Portfolio net assets)

| | | | | |

U.S. Treasury Notes — continued |

U.S. Treasury Notes (3 mo. U.S. Treasury Money Market Yield + 0.150%) | | | | |

|

Total U.S. Treasury Notes | |

|

| | | | |

| | | | |

|

| |

U.S. Government Agencies — 0.7% |

Federal National Mortgage Association (FNMA) (SOFR + 0.135%) | | | | |

|

Repurchase Agreements — 9.3% |

BNP Paribas SA tri-party repurchase agreement dated 8/30/24; Proceeds at maturity — $101,989,722; (Fully collateralized by corporate bonds and notes, 1.050% to 7.000% due 1/10/25 to 12/31/79; Market value — $105,000,037) | | | | |

BNP Paribas SA tri-party repurchase agreement dated 8/30/24; Proceeds at maturity — $127,491,667; (Fully collateralized by corporate bonds and notes, 0.550% to 9.250% due 11/10/24 to 10/31/82; Market value — $131,250,008) | | | | |

JPMorgan Securities LLC tri-party repurchase agreement dated 6/26/24; Proceeds at maturity — $304,140,000; (Fully collateralized by corporate bonds and notes and money market instruments, 1.776% to 9.500% due 9/1/24 to 11/3/78; Market value — $318,335,595) | | | | |

MUFG Securities Americas Inc. tri-party repurchase agreement dated 7/24/24; Proceeds at maturity — $101,993,333; (Fully collateralized by asset-backed securities, 3.650% to 6.630% due 1/20/27 to 11/15/32; Market value — $106,000,654) | | | | |

See Notes to Financial Statements.

Liquid Reserves Portfolio 2024 Annual Report

Schedule of Investments (cont’d)August 31, 2024 Liquid Reserves Portfolio

(Percentages shown based on Portfolio net assets)

| | | | | |

Repurchase Agreements — continued |

TD Securities LLC tri-party repurchase agreement dated 8/30/24; Proceeds at maturity — $150,089,833; (Fully collateralized by corporate bonds and notes, 3.375% to 14.500% due 11/13/25 to 9/20/31; Market value — $168,000,260) | | | | |

|

Total Repurchase Agreements | |

Total Investments — 95.5% (Cost — $7,935,924,024) | |

Other Assets in Excess of Liabilities — 4.5% | |

Total Net Assets — 100.0% | |

| Commercial paper exempt from registration under Section 4(2) of the Securities Act of 1933. This security may be resold in transactions that are exempt from registration, normally to qualified institutional buyers. This security has been deemed liquid pursuant to guidelines approved by the Board of Trustees. |

| Rate shown represents yield-to-maturity. |

| Variable rate security. Interest rate disclosed is as of the most recent information available. Certain variable rate securities are not based on a published reference rate and spread but are determined by the issuer or agent and are based on current market conditions. These securities do not indicate a reference rate and spread in their description above. |

Abbreviation(s) used in this schedule: |

| | Secured Overnight Financing Rate |

See Notes to Financial Statements.

Liquid Reserves Portfolio 2024 Annual Report

Statement of Assets and LiabilitiesAugust 31, 2024

| |

Investments, at value (Cost — $7,935,924,024) | |

| |

| |

| |

| |

Fund accounting fees payable | |

| |

| |

Audit and tax fees payable | |

| |

| |

| |

| |

| |

| |

See Notes to Financial Statements.

Liquid Reserves Portfolio 2024 Annual Report

Statement of OperationsFor the Year Ended August 31, 2024

| |

| |

| |

Investment management fee (Note 2) | |

| |

| |

| |

| |

| |

| |

| |

| |

Less: Fee waivers and/or expense reimbursements (Note 2) | |

| |

| |

Realized and Unrealized Gain (Loss) on Investments (Notes 1 and 3): |

Net Realized Gain From Investment Transactions | |

Change in Net Unrealized Appreciation (Depreciation) From Investments | |

| |

Increase in Net Assets From Operations | |

See Notes to Financial Statements.

Liquid Reserves Portfolio 2024 Annual Report

Statements of Changes in Net Assets

For the Years Ended August 31, | | |

| | |

| | |

| | |

Change in net unrealized appreciation (depreciation) | | |

Increase in Net Assets From Operations | | |

| | |

Proceeds from contributions | | |

| | |

Decrease in Net Assets From Capital Transactions | | |

| | |

| | |

| | |

| | |

See Notes to Financial Statements.

Liquid Reserves Portfolio 2024 Annual Report

For the years ended August 31: |

| | | | | |

Net assets, end of year (millions) | | | | | |

| | | | | |

Ratios to average net assets: |

| | | | | |

| | | | | |

| | | | | |

| Performance figures may reflect compensating balance arrangements, fee waivers and/or expense reimbursements. In the absence of compensating balance arrangements, fee waivers and/or expense reimbursements, the total return would have been lower. Past performance is no guarantee of future results. |

| The investment manager, pursuant to the terms of the feeder fund’s investment management agreement, has agreed to waive 0.10% of Portfolio expenses, attributable to the Portfolio’s investment management fee. Additional amounts may be voluntarily waived and/or reimbursed from time to time. |

| Reflects fee waivers and/or expense reimbursements. |

| Amount represents less than 0.005% or greater than (0.005)%. |

See Notes to Financial Statements.

Liquid Reserves Portfolio 2024 Annual Report

Notes to Financial Statements

1. Organization and significant accounting policies

Liquid Reserves Portfolio (the “Portfolio”) is a separate diversified investment series of Master Portfolio Trust (the “Trust”). The Trust, a Maryland statutory trust, is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company. The Declaration of Trust permits the Trustees to issue beneficial interests in the Portfolio. At August 31, 2024, all investors in the Portfolio were funds advised or administered by the investment manager of the Portfolio and/or its affiliates.

The Portfolio sells and effects withdrawals of its interests at prices based on the current market value of the securities it holds. Therefore, the price of an interest in the Portfolio fluctuates along with changes in the market-based value of the holdings of the Portfolio. Because the price of an interest in the Portfolio fluctuates, it has what is called a “floating net asset value” or “floating NAV”. Under Rule 2a-7 of the 1940 Act (“Rule 2a-7”), the Portfolio must follow strict rules as to the credit quality, liquidity, diversification and maturity of its investments.

The Portfolio follows the accounting and reporting guidance in Financial Accounting Standards Board (“FASB”) Accounting Standards Codification Topic 946, Financial Services – Investment Companies (“ASC 946”). The following are significant accounting policies consistently followed by the Portfolio and are in conformity with U.S. generally accepted accounting principles (“GAAP”), including, but not limited to, ASC 946. Estimates and assumptions are required to be made regarding assets, liabilities and changes in net assets resulting from operations when financial statements are prepared. Changes in the economic environment, financial markets and any other parameters used in determining these estimates could cause actual results to differ. Subsequent events have been evaluated through the date the financial statements were issued.

(a) Investment valuation. The valuations for fixed income securities (which may include, but are not limited to, corporate, government, municipal, mortgage-backed, collateralized mortgage obligations and asset-backed securities) are typically the prices supplied by independent third party pricing services, which may use market prices or broker/dealer quotations or a variety of valuation techniques and methodologies. The independent third party pricing services typically use inputs that are observable such as issuer details, interest rates, yield curves, prepayment speeds, credit risks/spreads, default rates and quoted prices for similar securities. When the Portfolio holds securities or other assets that are denominated in a foreign currency, the Portfolio will normally use the currency exchange rates as of 4:00 p.m. (Eastern Time). If independent third party pricing services are unable to supply prices for a portfolio investment, or if the prices supplied are deemed by the manager to be unreliable, the market price may be determined by the manager using quotations from one or more broker/dealers or at the transaction price if the security has recently been purchased and no value has yet been obtained from a pricing service or pricing broker. When reliable prices are not readily available, such as when the value of a

Liquid Reserves Portfolio 2024 Annual Report

Notes to Financial Statements (cont’d)

security has been significantly affected by events after the close of the exchange or market on which the security is principally traded, but before the Portfolio calculates its net asset value, the Portfolio values these securities as determined in accordance with procedures approved by the Portfolio’s Board of Trustees.

Pursuant to policies adopted by the Board of Trustees, the Portfolio’s manager has been designated as the valuation designee and is responsible for the oversight of the daily valuation process. The Portfolio’s manager is assisted by the Global Fund Valuation Committee (the “Valuation Committee”). The Valuation Committee is responsible for making fair value determinations, evaluating the effectiveness of the Portfolio’s pricing policies, and reporting to the Portfolio’s manager and the Board of Trustees. When determining the reliability of third party pricing information for investments owned by the Portfolio, the Valuation Committee, among other things, conducts due diligence reviews of pricing vendors, monitors the daily change in prices and reviews transactions among market participants.

The Valuation Committee will consider pricing methodologies it deems relevant and appropriate when making fair value determinations. Examples of possible methodologies include, but are not limited to, multiple of earnings; discount from market of a similar freely traded security; discounted cash-flow analysis; book value or a multiple thereof; risk premium/yield analysis; yield to maturity; and/or fundamental investment analysis. The Valuation Committee will also consider factors it deems relevant and appropriate in light of the facts and circumstances. Examples of possible factors include, but are not limited to, the type of security; the issuer’s financial statements; the purchase price of the security; the discount from market value of unrestricted securities of the same class at the time of purchase; analysts’ research and observations from financial institutions; information regarding any transactions or offers with respect to the security; the existence of merger proposals or tender offers affecting the security; the price and extent of public trading in similar securities of the issuer or comparable companies; and the existence of a shelf registration for restricted securities.

For each portfolio security that has been fair valued pursuant to the policies adopted by the Board of Trustees, the fair value price is compared against the last available and next available market quotations. The Valuation Committee reviews the results of such back testing monthly and fair valuation occurrences are reported to the Board of Trustees quarterly.

The Portfolio uses valuation techniques to measure fair value that are consistent with the market approach and/or income approach, depending on the type of security and the particular circumstance. The market approach uses prices and other relevant information generated by market transactions involving identical or comparable securities. The income approach uses valuation techniques to discount estimated future cash flows to present value.

Liquid Reserves Portfolio 2024 Annual Report

GAAP establishes a disclosure hierarchy that categorizes the inputs to valuation techniques used to value assets and liabilities at measurement date. These inputs are summarized in the three broad levels listed below:

•

Level 1 — unadjusted quoted prices in active markets for identical investments

•

Level 2 — other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, credit risk, etc.)

•

Level 3 — significant unobservable inputs (including the Portfolio’s own assumptions in determining the fair value of investments)

The inputs or methodologies used to value securities are not necessarily an indication of the risk associated with investing in those securities.

The following is a summary of the inputs used in valuing the Portfolio’s assets carried at fair value:

|

| | Other Significant

Observable Inputs

(Level 2) | Significant

Unobservable

Inputs

(Level 3) | |

| | | | |

| See Schedule of Investments for additional detailed categorizations. |

(b) Repurchase agreements. The Portfolio may enter into repurchase agreements with institutions that its subadviser has determined are creditworthy. Each repurchase agreement is recorded at cost. Under the terms of a typical repurchase agreement, the Portfolio acquires a debt security subject to an obligation of the seller to repurchase, and of the Portfolio to resell, the security at an agreed-upon price and time, thereby determining the yield during the Portfolio’s holding period. When entering into repurchase agreements, it is the Portfolio’s policy that its custodian or a third party custodian, acting on the Portfolio’s behalf, take possession of the underlying collateral securities, the market value of which, at all times, at least equals the principal amount of the repurchase transaction, including accrued interest. To the extent that any repurchase transaction maturity exceeds one business day, the value of the collateral is marked-to-market and measured against the value of the agreement in an effort to ensure the adequacy of the collateral. If the counterparty defaults, the Portfolio generally has the right to use the collateral to satisfy the terms of the repurchase transaction. However, if the market value of the collateral declines during the period in which the Portfolio seeks to assert its rights or if bankruptcy proceedings are commenced with respect to the seller of the security, realization of the collateral by the Portfolio may be delayed or limited.

(c) Interest income and expenses. Interest income (including interest income from payment-in-kind securities) consists of interest accrued and discount earned (including both original issue and market discount adjusted for amortization of premium) on the

Liquid Reserves Portfolio 2024 Annual Report

Notes to Financial Statements (cont’d)

investments of the Portfolio. Expenses of the Portfolio are accrued daily. The Portfolio bears all costs of its operations other than expenses specifically assumed by the manager.

(d) Method of allocation. Net investment income and net realized/unrealized gains and/or losses of the Portfolio are allocated pro rata, based on respective ownership interests, among the Fund and other investors in the Portfolio (the “Holders”) at the time of such determination.

(e) Credit and market risk. Investments in securities that are collateralized by real estate mortgages are subject to certain credit and liquidity risks. When market conditions result in an increase in default rates of the underlying mortgages and the foreclosure values of underlying real estate properties are materially below the outstanding amount of these underlying mortgages, collection of the full amount of accrued interest and principal on these investments may be doubtful. Such market conditions may significantly impair the value and liquidity of these investments and may result in a lack of correlation between their credit ratings and values.

(f) Compensating balance arrangements. The Portfolio has an arrangement with its custodian bank whereby a portion of the custodian’s fees is paid indirectly by credits earned on the Portfolio’s cash on deposit with the bank.

(g) Income taxes. The Portfolio is classified as a partnership for federal income tax purposes. As such, each investor in the Portfolio is treated as owner of its proportionate share of the net assets, income, expenses and realized and unrealized gains and losses of the Portfolio. Therefore, no federal income tax provision is required. It is intended that the Portfolio’s assets will be managed so an investor in the Portfolio can satisfy the requirements of Subchapter M of the Internal Revenue Code.

Management has analyzed the Portfolio’s tax positions taken on income tax returns for all open tax years and has concluded that as of August 31, 2024, no provision for income tax is required in the Portfolio’s financial statements. The Portfolio’s federal and state income tax returns for tax years for which the applicable statutes of limitations have not expired are subject to examination by the Internal Revenue Service and state departments of revenue.

(h) Other. Purchases, maturities and sales of money market instruments are accounted for on the date of the transaction. Realized gains and losses are calculated on the identified cost basis.

2. Investment management agreement and other transactions with affiliates

Franklin Templeton Fund Adviser, LLC (“FTFA”) (formerly known as Legg Mason Partners Fund Advisor, LLC prior to November 30, 2023) is the Portfolio’s investment manager and Western Asset Management Company, LLC (“Western Asset”) is the Portfolio’s subadviser. FTFA and Western Asset are indirect, wholly-owned subsidiaries of Franklin Resources, Inc. (“Franklin Resources”).

Liquid Reserves Portfolio 2024 Annual Report

Under the investment management agreement, the Portfolio pays an investment management fee, calculated daily and paid monthly, at an annual rate of 0.10% of the Portfolio’s average daily net assets.

FTFA provides administrative and certain oversight services to the Portfolio. FTFA delegates to the subadviser the day-to-day portfolio management of the Portfolio. For its services, FTFA pays Western Asset a fee monthly, at an annual rate equal to 70% of the net management fee it receives from the Portfolio.

As a result of the investment management agreement between FTFA and the feeder fund, FTFA has agreed to waive 0.10% of Portfolio expenses, attributable to the Portfolio’s investment management fee. Additional amounts may be voluntarily waived and/or reimbursed from time to time.

During the year ended August 31, 2024, fees waived and/or expenses reimbursed amounted to $10,147,377.

FTFA is permitted to recapture amounts waived and/or reimbursed to the Portfolio during the same fiscal year under certain circumstances.

All officers and one Trustee of the Trust are employees of Franklin Resources or its affiliates and do not receive compensation from the Trust.

At August 31, 2024, the aggregate cost of investments and the aggregate gross unrealized appreciation and depreciation of investments for federal income tax purposes were as follows:

| | Gross

Unrealized

Appreciation | Gross

Unrealized

Depreciation | Net

Unrealized

Appreciation |

| | | | |

4. Derivative instruments and hedging activities

During the year ended August 31, 2024, the Portfolio did not invest in derivative instruments.

Liquid Reserves Portfolio 2024 Annual Report

Report of Independent Registered Public Accounting Firm

To the Board of Trustees of Master Portfolio Trust and Investors of Liquid Reserves Portfolio

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities, including the schedule of investments, of Liquid Reserves Portfolio (one of the portfolios constituting Master Portfolio Trust, referred to hereafter as the “Portfolio”) as of August 31, 2024, the related statement of operations for the year ended August 31, 2024, the statement of changes in net assets for each of the two years in the period ended August 31, 2024, including the related notes, and the financial highlights for each of the five years in the period ended August 31, 2024 (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Portfolio as of August 31, 2024, the results of its operations for the year then ended, the changes in its net assets for each of the two years in the period ended August 31, 2024 and the financial highlights for each of the five years in the period ended August 31, 2024 in conformity with accounting principles generally accepted in the United States of America.

These financial statements are the responsibility of the Portfolio’s management. Our responsibility is to express an opinion on the Portfolio’s financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Portfolio in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits of these financial statements in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. Our procedures included confirmation of securities owned as of August 31, 2024 by correspondence with the custodian and brokers. We believe that our audits provide a reasonable basis for our opinion.

/s/PricewaterhouseCoopers LLP

Baltimore, Maryland

October 23, 2024

We have served as the auditor of one or more investment companies in the Franklin Templeton Group of Portfolios since 1948.

Liquid Reserves Portfolio 2024 Annual Report

Changes in and Disagreements with AccountantsFor the period covered by this report

Results of Meeting(s) of ShareholdersFor the period covered by this report

Remuneration Paid to Directors, Officers and OthersFor the period covered by this report

Refer to the financial statements included herein.

Liquid Reserves Portfolio

Board Approval of Management andSubadvisory Agreements (unaudited) The Executive and Contracts Committee of the Board of Trustees (the “Executive and Contracts Committee”) considered the Management Agreement between the Trust and Franklin Templeton Fund Adviser, LLC (“FTFA”) (formerly known as Legg Mason Partners Fund Advisor, LLC) with respect to the Fund and the subadvisory agreement between FTFA and Western Asset Management Company, LLC (“Western Asset” or the “Subadviser”, and together with FTFA, the “Advisers”) with respect to the Fund (collectively, the “Agreements”) at a meeting held on April 30, 2024. At an in-person meeting held on May 16, 2024, the Executive and Contracts Committee reported to the full Board of Trustees their considerations and recommendation with respect to the Agreements, and the Board of Trustees, including a majority of the Independent Trustees, considered and approved renewal of the Agreements.

In arriving at their decision to approve the renewal of the Agreements, the Trustees met with representatives of the Advisers, including relevant investment advisory personnel; considered a variety of information prepared by the Advisers, materials provided by Broadridge and advice and materials provided by counsel to the Independent Trustees; reviewed performance and expense information for peer groups of comparable funds selected by Broadridge (the “Performance Universe”) and certain other comparable products available from Western Asset or affiliates of Western Asset, including separate accounts managed by Western Asset; and requested and reviewed additional information as necessary. These reviews were in addition to information obtained by the Trustees at their regular quarterly meetings (and various committee meetings) with respect to the Fund’s performance and other relevant matters and related discussions with the Advisers’ personnel. The information received and considered by the Board both in conjunction with the May meeting and at prior meetings was both written and oral. With respect to the Broadridge materials, the Board was provided with a description of the methodology used to determine the similarity of the Fund with the funds included in the Performance Universe. It was noted that while the Board found the Broadridge data generally useful they recognized its limitations, including that the data may vary depending on the end date selected and that the results of the performance comparisons may vary depending on the selection of the peer group and its composition over time. The Board noted that the Fund is a “master fund” in a “master-feeder” structure, in which each feeder fund has the same investment objective and policies as the Fund and invests substantially all of its assets in the Fund. The information provided and presentations made to the Board encompassed the Fund and all funds for which the Board has responsibility, including the following feeder funds in the Fund (each, a “Feeder Fund”): Western Asset Institutional Liquid Reserves, a series of Legg Mason Partners Institutional Trust, and Western Asset Premier Institutional Liquid Reserves, a series of Legg Mason Partners Institutional Trust.

As part of their review, the Trustees examined FTFA’s ability to provide high quality oversight and administrative and shareholder support services to the Fund and the

Liquid Reserves Portfolio

Subadvisers’ ability to provide high quality investment management services to the Fund. The Trustees considered the experience of FTFA’s personnel in providing the types of services that FTFA is responsible for providing to the Fund; the ability of FTFA to attract and retain capable personnel; and the capability and integrity of FTFA’s senior management and staff. The Trustees also considered the investment philosophy and research and decision-making processes of the Subadviser; the experience of their key advisory personnel responsible for management of the Fund; the ability of the Subadviser to attract and retain capable research and advisory personnel; the risks to the Advisers associated with sponsoring the Fund (such as entrepreneurial, operational, reputational, litigation and regulatory risk), as well as FTFA’s and the Subadviser’s risk management processes; the capability and integrity of the Advisers’ senior management and staff; and the level of skill required to manage the Fund. In addition, the Trustees reviewed the quality of the Advisers’ services with respect to regulatory compliance and compliance with the investment policies of the Fund, and conditions that might affect the Advisers’ ability to provide high quality services to the Fund in the future, including their business reputations, financial conditions and operational stabilities. The Board also considered the policies and practices of FTFA and the Subadviser regarding the selection of brokers and dealers and the execution of portfolio transactions. Based on the foregoing, the Trustees concluded that the Subadviser’s investment process, research capabilities and philosophy were well suited to the Fund given its investment objectives and policies, and that the Advisers would be able to meet any reasonably foreseeable obligations under the Agreements.

The Board reviewed the qualifications, backgrounds and responsibilities of FTFA’s and Western Asset’s senior personnel and the team of investment professionals primarily responsible for the day-to-day portfolio management of the Fund. The Board also considered, based on its knowledge of FTFA and its affiliates, the financial resources of Franklin Resources, Inc., the parent organization of the Advisers. The Board recognized the importance of having a fund manager with significant resources.

In considering the performance of the Fund, the Board received and considered performance information for each Feeder Fund as well as for the Performance Universe selected by Broadridge. The Board noted that the Feeder Funds’ performance was the same as the performance of the Fund (except for the effect of fees at the Feeder Fund level), and therefore was relevant to the Board’s consideration of the Fund’s performance. The Board was provided with a description of the methodology used to determine the similarity of the Feeder Funds with the funds included in the Performance Universe. It was noted that while the Board found the Broadridge data generally useful they recognized its limitations, including that the data may vary depending on the end date selected and that the results of the performance comparisons may vary depending on the selection of the peer group and its composition over time. The Board also noted that it had received and discussed with management information throughout the year at periodic intervals comparing each Feeder

Liquid Reserves Portfolio

Board Approval of Management andSubadvisory Agreements (unaudited) (cont’d) Fund’s performance against its benchmark and against each Feeder Fund’s peers. In addition, the Board considered each Feeder Fund’s performance in light of overall financial market conditions.

• The information comparing Western Asset Institutional Liquid Reserves’ performance to that of its Performance Universe, consisting of all funds (including the Feeder Fund) classified as institutional money market funds by Broadridge, showed, among other data, that the Feeder Fund’s performance for the 1-, 3-, 5- and 10-year periods ended December 31, 2023 was above the median.

• The information comparing Western Asset Premier Institutional Liquid Reserves’ performance to that of its Performance Universe, consisting of all funds (including the Feeder Fund) classified as institutional money market funds by Broadridge, showed, among other data, that the Feeder Fund’s performance for the 1- and 3-year and since inception periods ended December 31, 2023 was above the median.

The Trustees also considered the management fee payable by the Fund to FTFA, total expenses payable by the Fund and the fee that FTFA pays to the Subadviser. They reviewed information concerning management fees paid to investment advisers of similarly managed funds as well as fees paid by Western Asset’s other clients, including separate accounts managed by Western Asset. The Trustees also noted that the Fund does not pay any management fees directly to the Subadviser because FTFA pays the Subadviser for services provided to the Fund out of the management fee FTFA receives from the Fund.

• The information comparing Western Asset Institutional Liquid Reserves’ Contractual and Actual Management Fees as well as its actual total expense ratio to its peer group, consisting of a group of institutional money market funds (including the Fund) chosen by Broadridge to be comparable to the Feeder Fund, showed that the Feeder Fund’s Contractual Management Fee and Actual Management Fee were above the median. The Board noted that the Feeder Fund’s actual total expense ratio was at the median. The Board also considered that the current limitation on the Feeder Fund’s expenses is expected to continue through December 2024.

• The information comparing Western Asset Premier Institutional Liquid Reserves’ Contractual and Actual Management Fees as well as its actual total expense ratio to its peer group, consisting of a group of institutional money market funds (including the Fund) chosen by Broadridge to be comparable to the Feeder Fund, showed that the Feeder Fund’s Contractual Management Fee was above the median and its Actual Management Fee was below the median. The Board noted that the Feeder Fund’s actual total expense ratio was below the median. The Board also considered that the current limitation on the Feeder Fund’s expenses is expected to continue through December 2024.

Liquid Reserves Portfolio

The Trustees further evaluated the benefits of the advisory relationship to the Advisers, including, among others, the profitability of the relationship to the Advisers; the direct and indirect benefits that the Advisers may receive from their relationships with the Fund, including the “fallout benefits,” such as reputational value derived from serving as investment adviser to the Fund; and the affiliation between the Advisers and certain other service providers for the Fund. In that connection, the Board considered that the ancillary benefits that the Advisers receive were reasonable. The Trustees noted that Western Asset does not have soft dollar arrangements.

Finally, the Trustees considered, in light of the profitability information provided by the Advisers, the extent to which economies of scale would be realized by the Advisers as the assets of the Fund grow. The Trustees considered an analysis of the profitability of FTFA and its affiliates in providing services to the Fund and the Feeder Fund.

• The Board noted that the Western Asset Institutional Liquid Reserves’ Contractual Management Fee and Actual Management Fee were above the median.

• The Board noted that the Western Asset Premier Institutional Liquid Reserves’ Contractual Management Fee was above the median and its Actual Management Fee was below the median of the peer group. The Board also noted the size of the Feeder Fund.

In their deliberations with respect to these matters, the Independent Trustees were advised by their independent counsel, who is independent, within the meaning of the Securities and Exchange Commission rules regarding the independence of counsel, of the Advisers. The Independent Trustees weighed the foregoing matters in light of the advice given to them by their independent counsel as to the law applicable to the review of investment advisory contracts. In arriving at a decision, the Trustees, including the Independent Trustees, did not identify any single matter as all-important or controlling, and each Trustee may have attributed different weight to the various factors in evaluating the Agreements. The foregoing summary does not detail all the matters considered. The Trustees judged the terms and conditions of the Agreements, including the investment advisory fees, in light of all of the surrounding circumstances.

Based upon their review, the Trustees, including all of the Independent Trustees, determined, in the exercise of their business judgment, that they were satisfied with the quality of investment advisory services being provided by the Advisers; that the fees to be paid to the Advisers under the Agreements were fair and reasonable given the scope and quality of the services rendered by the Advisers; and that approval of the Agreements was in the best interest of the Fund and its shareholders.

Liquid Reserves Portfolio

| ITEM 8. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS FOR OPEN-END MANAGEMENT INVESTMENT COMPANIES. |

The information is disclosed as part of the Financial Statements included in Item 7 of this Form N-CSR.

| ITEM 9. | PROXY DISCLOSURES FOR OPEN-END MANAGEMENT INVESTMENT COMPANIES. |

The information is disclosed as part of the Financial Statements included in Item 7 of this Form N-CSR.

| ITEM 10. | REMUNERATION PAID TO DIRECTORS, OFFICERS, AND OTHERS OF OPEN-END MANAGEMENT INVESTMENT COMPANIES. |

The information is disclosed as part of the Financial Statements included in Item 7 of this Form N-CSR.

| ITEM 11. | STATEMENT REGARDING BASIS FOR APPROVAL OF INVESTMENT ADVISORY CONTRACT. |

The information is disclosed as part of the Financial Statements included in Item 7 of this Form N-CSR, as applicable.

| ITEM 12. | DISCLOSURE OF PROXY VOTING POLICIES AND PROCEDURES FOR CLOSED-END MANAGEMENT INVESTMENT COMPANIES. |

Not applicable.

| ITEM 13. | PORTFOLIO MANAGERS OF CLOSED-END MANAGEMENT INVESTMENT COMPANIES. |

Not applicable.

| ITEM 14. | PURCHASES OF EQUITY SECURITIES BY CLOSED-END MANAGEMENT INVESTMENT COMPANY AND AFFILIATED PURCHASERS. |

Not applicable.

| ITEM 15. | SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS. |

Not applicable.

| ITEM 16. | CONTROLS AND PROCEDURES. |

| (a) | The registrant’s principal executive officer and principal financial officer have concluded that the registrant’s disclosure controls and procedures (as defined in Rule 30a- 3(c) under the Investment Company Act of 1940, as amended (the “1940 Act”)) are effective as of a date within 90 days of the filing date of this report that includes the disclosure required by this paragraph, based on their evaluation of the disclosure controls and procedures required by Rule 30a-3(b) under the 1940 Act and 15d-15(b) under the Securities Exchange Act of 1934. |

| (b) | There were no changes in the registrant’s internal control over financial reporting (as defined in Rule 30a-3(d) under the 1940 Act) that occurred during the period covered by this report that have materially affected, or are likely to materially affect the registrant’s internal control over financial reporting. |

| ITEM 17. | DISCLOSURE OF SECURITIES LENDING ACTIVITIES FOR CLOSED-END MANAGEMENT INVESTMENT COMPANIES. |

Not applicable.

| ITEM 18. | RECOVERY OF ERRONEOUSLY AWARDED COMPENSATION. |

(a) (1) Code of Ethics attached hereto.

Exhibit 99.CODE ETH

(a) (2) Certifications pursuant to section 302 of the Sarbanes-Oxley Act of 2002 attached hereto.

Exhibit 99.CERT

(b) Certifications pursuant to Section 906 of the Sarbanes-Oxley Act of 2002 attached hereto.

Exhibit 99.906CERT

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this Report to be signed on its behalf by the undersigned, there unto duly authorized.

| Master Portfolio Trust |

| | | |

| By: | /s/ Jane Trust | |

| | Jane Trust | |

| | Chief Executive Officer | |

| | | |

| Date: | October 24, 2024 | |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| By: | /s/ Jane Trust | |

| | Jane Trust | |

| | Chief Executive Officer | |

| | | |

| Date: | October 24, 2024 | |

| By: | /s/ Christopher Berarducci | |

| | Christopher Berarducci | |

| | Principal Financial Officer | |

| | | |

| Date: | October 24, 2024 | |