Investment Community Meeting MasterCard Incorporated September 15, 2010 Exhibit 99.1 |

8:30 a.m. Welcome Barbara Gasper 8:35 a.m. Opening Remarks Bob Selander 8:45 a.m. Strategic Discussion Ajay Banga 9:05 a.m. Product & Solutions Overview Gary Flood 9:20 a.m. Core Products Tim Murphy 9:40 a.m. Emerging Payments Ed McLaughlin 10:00 a.m. Break 10:20 a.m. U.S. Markets Chris McWilton 10:40 a.m. International Markets Walt Macnee 11:00 a.m. European Opportunities Javier Perez 11:20 a.m. Financial Perspective Martina Hund-Mejean 11:40 a.m. Q&A Session Management 12:25 p.m. MA Labs & Product Demo Intro Garry Lyons 12:35 p.m. Closing Remarks Ajay Banga 12:45 p.m. Lunch, Mingle & Product Demos Management & Staff 3:00 p.m. Event Adjourns Agenda Page 2 Investment Community Meeting September 15, 2010 |

Today’s presentation may contain, in addition to historical information, forward looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are based on our current assumptions, expectations and projections about future events which reflect the best judgment of management and involve a number of risks and uncertainties that could cause actual results to differ materially from those suggested by our comments today. You should review and consider the information contained in our filings with the SEC regarding these risks and uncertainties. MasterCard disclaims any obligation to publicly update or revise any forward-looking statements or information provided during today’s presentations. Forward-Looking Statements Page 3 Investment Community Meeting September 15, 2010 |

Investment Community Meeting Change through Innovation September 15, 2010 Bob Selander Executive Vice Chairman |

MasterCard’s Transformation Over the Last Decade Page 5 September 15, 2010 We faced challenges... ...and responded with innovative & competitive solutions • Strengthened brands and marketing • Launched Priceless Weak Brands • Rewrote core systems • Developed Competitively Advantaged Offerings Dated Technology • Created customer teams • Introduced value-added services & MasterCard Advisors Association Mentality • Merged with Europay • Created single global entity Disparate Structure • Changed ownership and governance structure • Increased level of commercial rigor Lack of Capital and Flexibility Investment Community Meeting |

Learning by Innovating Page 6 September 15, 2010 We made mistakes along the way • Mondex • Debit in the U.S. We learned lessons that made us more successful • Listen to customers • A global, top-down approach doesn’t always work • Importance of planning for different scenarios Investment Community Meeting |

Trends present both challenges & opportunities Evolving Industry and Environment Page 7 September 15, 2010 We continue to deliver innovative solutions • Mobile phone initiatives • MoneySend • inControl • Transformation of payments • New customers • New competition • Nationalism/regulation • Demographic trends • Secular trends Investment Community Meeting |

Summary Page 8 September 15, 2010 Our innovative approach... Whether in the strategic business decisions we’ve made over the last decade or the competitive solutions we’ve introduced in recent months ...will continue to drive momentum across our business. Investment Community Meeting |

Investment Community Meeting Looking to the Future Ajay Banga President and Chief Executive Officer September 15, 2010 |

MasterCard Today Page 10 September 15, 2010 Unified, global presence Increasingly differentiated assets Challenging environment Strong financial performance Significant growth potential Investment Community Meeting |

Key Trends Creating Opportunities in the “War on Cash” Page 11 September 15, 2010 Growing affluent and middle class Ongoing increase in acceptance Growing importance of youth Financial inclusion Continued urbanization 8-10% Market Growth Investment Community Meeting |

Other Trends Presenting Opportunities and Challenges Page 12 September 15, 2010 New Technologies New Entrants into Payments Increasing Role of Governments Investment Community Meeting |

MasterCard Strategy: Looking to the Future Page 13 September 15, 2010 Growth will come through both displacement of cash and checks and increased market share. + = 8-10% Market Growth 3-5% Growth from Strategic Investments Low to Mid-Teens Long-Term Net Revenue Growth Investment Community Meeting |

Strategy Enables Future Growth Page 14 September 15, 2010 Credit Debit Processing • Segmented offerings and product enhancements • New geographies and customers • Reinforce strong position outside U.S. • Increase U.S. market share profitably • Public sector, corporate and consumer reloadable • Grow market share • Domestic processing • Expand processing capabilities Prepaid Investment Community Meeting |

Strategy Enables Future Growth Page 15 September 15, 2010 Geographies Customers • Invest disproportionately in high growth markets • Grow acceptance, channels, processing Relationships with: • Merchants • Telcos • Governments • Transit Operators Investment Community Meeting |

Strategy Enables Future Growth Page 16 September 15, 2010 Information Services MasterCard Labs • Ideate, incubate and test new ideas • Monetize information through diversified channels • Enhance merchant services e-Commerce & Mobile • Drive faster than market growth • Partner and build payments infrastructure in emerging markets • Differentiate the consumer experience in developed markets Investment Community Meeting |

Acquisitions Play a Role in the Strategy Page 17 September 15, 2010 DataCash fits our acquisition criteria well • Drive e-Commerce growth in tandem with acquiring relationships • Expand DataCash and MiGS gateway products beyond Europe and Asia/Pacific • Enhance fraud management expertise • Deliver new products with minimal merchant integration challenges Strategic Rationale • Clear fit with e-Commerce strategy • Complements and enhances existing assets • Attractive returns Deal Criteria Investment Community Meeting |

Striking the right global / local balance Sharpening our competitive edge through: •Innovation •Thoughtful risk taking •Speed to market Driving Strategy Execution Page 18 September 15, 2010 Investment Community Meeting |

Investment Community Meeting Global Products & Solutions Gary Flood President, Global Products & Solutions September 15, 2010 |

Optimizing Solutions for Growth Page 20 September 15, 2010 Advisory Services Advisory Services Processing Processing Core Products Core Products Marketing Marketing MasterCard Labs MasterCard Labs Emerging Payments Emerging Payments Investment Community Meeting |

Global Opportunity to Displace Cash and Checks Page 21 September 15, 2010 85% of the world’s transactions are still done in Cash 1 2.5 billion adults worldwide are unbanked 2 Over $1.7 trillion Commercial 4 opportunity globally by 2015 4.6 billion Mobile Phones 6 globally, with just 10% smart phone penetration Global consumer Check 1 volume equals $9 trillion Prepaid 3 will grow to $850 billion by 2017 More than $1 trillion in e-Commerce 5 sales globally by 2011 Opportunity to displace cash in Transit 7 space is $29 billion globally Sources: 1. MasterCard Advisors; 2. McKinsey; 3. BCG; 4. Packaged Facts; 5. Glenbrook Partners; 6. GSMA; 7. Datamonitor Investment Community Meeting |

Strategic Pillars Page 22 September 15, 2010 8-10% Market Growth 3-5% Strategic Investments Low to Mid-Teens Long-Term Net Revenue Growth Investment Community Meeting |

Sustainable Differentiation Requires Continuous Innovation Page 23 September 15, 2010 Today Differentiated assets provide leverage • Integrated Solutions • Unified Global Entity • Network Response and Flexibility • inControl • Advisory Services • Data Analytics • Smart Data Near-Term Innovation supported by key strategic investments • Prepaid • Information Services • e-Commerce • Mobile / P2P • MasterCard Labs • Open API • Consumer Segmentation • New Customers Longer-Term Fully-integrated continuous innovation • Drive value for: – Customers – Merchants – End Consumers Investment Community Meeting |

Processing Creates Value Page 24 September 15, 2010 MasterCard Worldwide Network Unique •Central & Distributed Network •99.999% Global Availability •Fastest Global Network New Channels •Mobile •Transit Local •Domestic Processing •Currency •Rules Value-Add •inControl •Rewards Investment Community Meeting e-Commerce Real-time Risk Scoring Extended Capabilities •Integrated Processing Solutions •Strategic Payment Services •MiGS and DataCash Global •210 Countries •23,000 Financial Institutions |

Advisory Services Page 25 September 15, 2010 Solving Needs & Driving Growth Investment Community Meeting Leveraging: • Data • Insights • Payments Expertise • Problem-Solving Skills Three lines of business: • Consulting • Information • Managed Services |

Marketing Strategy Corresponds to Market Evolution Page 26 September 15, 2010 Brand Preference Brand Preference Brand Awareness Brand Awareness • Consumer & merchant education and awareness • Acceptance development • Issuance support • Infrastructure/business model • Fully integrated marketing • Product innovation • Consumer benefit driven from functionality • Issuer & merchant strategic marketing alignment • Activation Investment Community Meeting |

Australia: Targeting Gen Y to Drive Debit Page 27 Investment Community Meeting September 15, 2010 Australian debit volume increased 89% 1 Top of wallet behavior more than doubled 2 among the target demographic Note: 1. YOY results as of Q1 2010; 2. Q1 2010 vs. Q1 2008 |

Understanding Debit Page 28 Investment Community Meeting September 15, 2010 <Play Video> |

Global Products & Solutions Page 29 Investment Community Meeting September 15, 2010 Powering MasterCard’s Growth Tremendous opportunities exist Innovation and differentiation are critical A global strategy with market- level insight, alignment and flawless execution drive success |

Investment Community Meeting Driving Growth at the Core: Credit, Debit, Prepaid Tim Murphy Chief Product Officer, Core Products September 15, 2010 |

Credit: Core to Our Growth Page 31 Investment Community Meeting September 15, 2010 Volumes stabilizing in the US; growth in ROW Partnerships / assets for the Affluent Consumer-centric value propositions Commercial payments Focused on: 2Q10 YOY Growth US: -1.5% ROW: 9.8% Leading innovation in product and card design |

The Right Partnerships Relevant Products Innovative Design Credit: Differentiation for the Affluent Page 32 Investment Community Meeting September 15, 2010 Turkish Airlines Aeroflot (Russia) BBVA Black Itau Black Chase Continental OnePass |

Commercial Credit: Substantial Opportunity in Commercial Page 33 Investment Community Meeting September 15, 2010 2Q10 YOY Growth US: 4.3% ROW: 14.1% Fastest growing segment in credit Gaining share in Europe, pursuing greenfield opportunities in APMEA and LAC Leveraging differentiated product assets Lufthansa Miles & More |

• Debit economics • Network exclusivity • Discounts at POS • Credit min / max Recent US Financial Regulation: Impact on Debit Page 34 Investment Community Meeting September 15, 2010 Impacts Opportunities • Brand sales in light of network exclusivity • Prepaid for financial inclusion |

Debit: Driving Growth in Local Markets Page 35 Investment Community Meeting September 15, 2010 Winning profitable deals in key markets Winning domestic switching Accelerating cash conversion Focused on: 2Q10 YOY Growth US * : 0.8% / 21.0% ROW: 28.7% Significant and sustained growth around the world Leveraging country-level strategies, well positioned in many markets * Includes/excludes US deconversions |

Debit: Being Local is Key to Winning Business India State Bank of India Created customized offering to largest bank in India Europe TEB (Turkish Economy Bank) Display Card Next generation debit card Investment Community Meeting Page 36 September 15, 2010 |

Prepaid: Capturing the Global Opportunity Page 37 Investment Community Meeting September 15, 2010 Public Sector Corporate Consumer Reloadable Large & quickly growing global opportunity IPS provides a robust prepaid issuer processing solution across all categories Focused on three verticals: |

Prepaid: Leveraging Value Page 38 Investment Community Meeting September 15, 2010 Public Sector Direct Express ® Debit MasterCard ® Gives recipients faster access to their funds and saves taxpayer dollars Consumer Travelex and Bank of China World’s largest distributor of foreign currency prepaid cards |

Summary Page 39 Investment Community Meeting September 15, 2010 Growth at the core continues... Credit in focus and generating momentum Debit growth continues in US and around the world Prepaid is the next generation opportunity |

Investment Community Meeting Growth through Innovation September 15, 2010 Ed McLaughlin Chief Emerging Payments Officer |

Past, Present & Future State Page 41 Investment Community Meeting September 15, 2010 A strong global network and brand with robust assets / applications Building infrastructures and enhancing consumer experiences around the world Facilitating commerce by driving growth in new markets and segments Who we are What we are working on Where we are going |

Accelerating e-Commerce Page 42 Investment Community Meeting September 15, 2010 Rapid adoption of the Internet continues to bolster online sales Brand loyalty, security and convenience drive growth • Infrastructure: Gateways, payment options, fraud tools • Consumer Engagement: Maestro online, MasterCard MarketPlace, social media Focused on: 3% 18% 45% 32% North America Europe Asia Pacific LAC + Other Source: MasterCard Analysis and ComScore data |

• Infrastructure: Contactless, Mobile Payments Gateway • Consumer Application: PayPass, MoneySend, inControl alerts, API and Apps Focused on: Transitioning to Mobility Source: Arthur D. Little, 2009 Mobile phones… Ubiquitous part of consumers’ daily lives Innovation platform through a partnership approach Investment Community Meeting Page 43 September 15, 2010 |

Mobile Momentum Page 44 Investment Community Meeting September 15, 2010 MasterCard introduces Mobile Payments Gateway, an m-wallet platform linking MasterCard cards First Mobile PayPass Tag pilot in Canada First Market Trial of Personalized NFC-Enabled Mobile Phones 200 phones payment pilot in partnership with ViVOtech Fully-integrated on-demand person-to-person mobile payment service Custom technology trial of Near Field Communication and MTA First trial of PayPass- enabled mobile phones for secure EMV payments Pioneer mobile phone debit payments in the UK, using Maestro PayPass Enable customers to make contactless payments via phones with MasterCard PayPass Turkey’s first mobile phones, enabled with MasterCard PayPass Partnering in the development of a Mobile Payments proposition that focuses specifically on consumer convenience First large scale deployment of PayPass in a mobile phone (60K Customer) First trial in Taiwan to make use of NFC smart posters and m-coupons First Mobile Pilot in India (Bangalore) using Mobile PayPass First Commercial mobile NFC Deployment Turkey’s first mobile phones, enabled with MasterCard PayPass Partnership will pursue mobile commerce opportunities |

Enabling Transit Payments Page 45 Investment Community Meeting September 15, 2010 High volume, faster than cash but current systems are cumbersome and inconvenient Transit is an anchor for everyday spend • Infrastructure: Transit gateway, open loop network • Consumer Experience: PayPass, prepaid, mobile integration Focused on: |

Summary Page 46 Investment Community Meeting September 15, 2010 Driving growth in emerging markets, devices and segments Leveraging and expanding our infrastructure Enhancing consumer experience through mobility, access and personalization |

US Markets Chris McWilton President, US Markets Investment Community Meeting September 15, 2010 |

US Markets Page 48 Investment Community Meeting September 15, 2010 Winning deals in the fast-growing Debit space has created excellent momentum for US Debit Well positioned for the impact of the financial reform legislation Engaging with non-traditional customers: governments, merchants, telcos, others to grow revenue |

Significant Momentum – “Game On!” Page 49 Investment Community Meeting September 15, 2010 |

Strategy to Address Recent US Legislation Page 50 Investment Community Meeting September 15, 2010 Ensure Fed has a well-informed view Leverage advantages of MasterCard signature and PIN debit offerings Provide financial institutions with new solutions Merchant focused innovation |

Non-Traditional Customers Page 51 Investment Community Meeting September 15, 2010 Engaging with merchants, governments, telcos and other players New U.S. Business Development function devoted to non-traditional players |

Current Customer Priorities Page 52 Investment Community Meeting September 15, 2010 Seeking to replace or enhance revenue streams Optimizing portfolio economics Complying with regulation and managing uncertainty |

Opportunity • More than half of the market is still using paper • Economic downturn causing consumer shift to Debit • Regulation driving change in competitive landscape Strategic Imperatives • Leverage strong momentum • Drive product innovation and demonstrate differentiated value • Maximize processing US Strategic Priorities Page 53 Investment Community Meeting September 15, 2010 Source: Euromonitor Debit Debit Checks 26% Cash 26% Cards 32% EFT 16% 2009 PCE $10T |

US Strategic Priorities Page 54 Investment Community Meeting September 15, 2010 Opportunity •Will represent a $442B market by 2017E •Regulation driving the unbanked to Prepaid •Adjunct to our Debit business Strategic Imperatives •Build already strong presence in corporate, public sector and consumer reloadable verticals Source: Boston Consulting Group Prepaid Prepaid |

US Strategic Priorities Page 55 Investment Community Meeting September 15, 2010 Opportunity • Favorably positioned with secular trends • Credit cards accounted for one-fifth of PCE in 2009 • Regulation will drive product innovation Strategic Imperatives • Protect and grow core Credit • Leverage consumer insights to drive product innovation • Capitalize on commercial growth as corporate travel rebounds Source: Economic Intelligence Unit Credit Credit |

US Strategic Priorities Page 56 Investment Community Meeting September 15, 2010 Opportunity • Double-digit growth in online sales despite tepid overall retail sales growth • US accounts for more than 30% of all global e-Commerce volume Strategic Imperatives • Grow share of online card spend ahead of the market • Partner with targeted online players • Leverage MasterCard Marketplace e-Commerce e-Commerce |

US Strategic Priorities Page 57 Investment Community Meeting September 15, 2010 Opportunity • Significant competitive differentiator • Regulation driving changes in Issuer business models • Economy driving changes in consumer trends Strategic Imperatives • Improve profitability of Issuer portfolios • Demonstrate predictive capabilities and insights Advisory Services Advisory Services |

Page 58 Investment Community Meeting September 15, 2010 Leveraging significant deal activity and momentum Exercising prudence in financial negotiations Investing in innovative products and solutions Focusing on both traditional and non-traditional customers Building, Growing and Diversifying revenue streams US Poised for Growth |

Investment Community Meeting International Markets Walt Macnee President, International Markets September 15, 2010 |

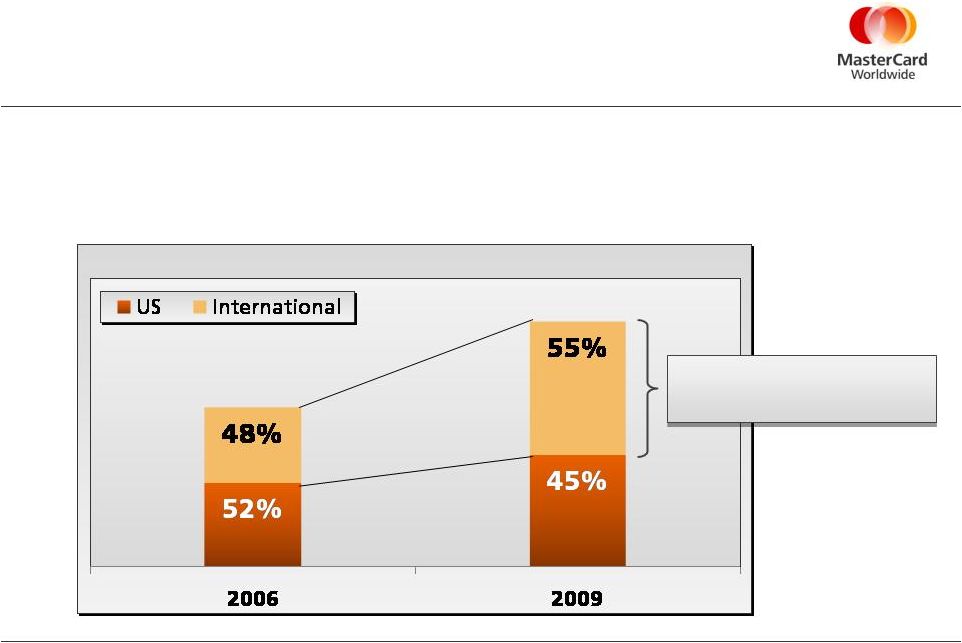

Our Objective... Sustained double digit revenue growth through Global resources embedded in local execution. International Markets: Large and Growing Page 60 Investment Community Meeting September 15, 2010 210 Countries with $2.8B Net Revenue MasterCard Net Revenue $5.1B $3.3B CAGR 21% CAGR 10% |

Strategic Framework for Capturing Opportunities and Addressing Challenges Page 61 Investment Community Meeting September 15, 2010 Prioritization of markets based on size of opportunity and potential returns for MasterCard Segmentation of markets to identify common themes and approach Country-level strategies around MasterCard strategic pillars of: |

Global Drivers Translate into Market-level Opportunities and Challenges Page 62 Investment Community Meeting September 15, 2010 Secular Trends Demographic Trends Transformation of Payments Evolving Role of Governments |

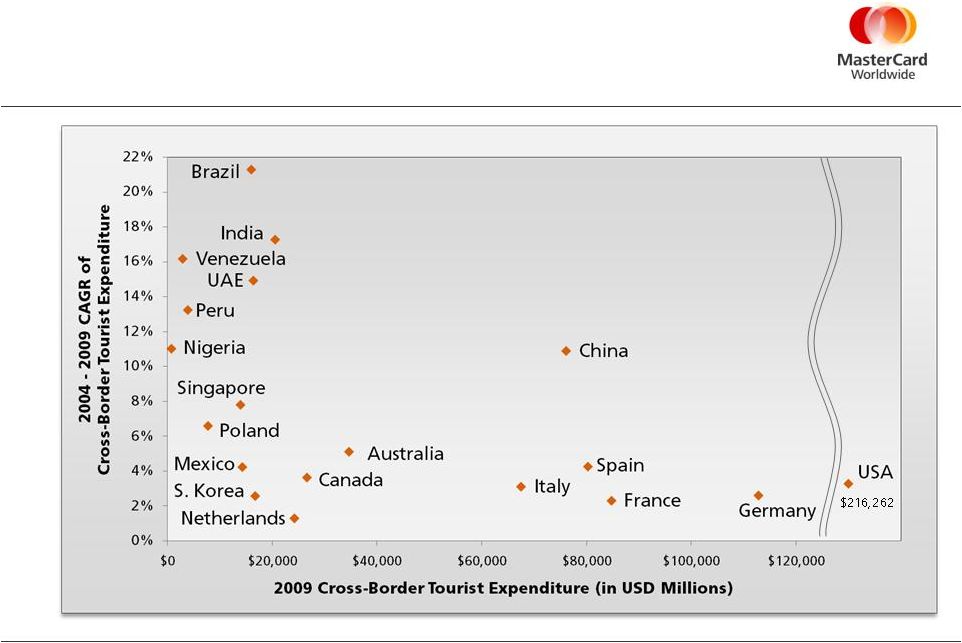

Source: Euromonitor International Secular Trends: Growth of Cross-Border Travel Page 63 Investment Community Meeting September 15, 2010 |

Capturing Growth in Cross-Border Page 64 Investment Community Meeting September 15, 2010 Germany Leveraging domestic position to capture outbound travel China Won all 9 recent co-brands to capture growing cross-border in China |

Demographic Trends: Reaching the Un/Under-banked Page 65 Investment Community Meeting September 15, 2010 Source: Euromonitor International Developed Countries Emerging Countries Emerging Countries Developed Countries Developed Countries Emerging Countries Banked Population (as % of 15+ Population) Broadband Penetration (Subscribers per Household) Mobile Penetration (Subscribers per Capita) |

Mobile Payments: Reaching the Banked and Un/Under-banked Page 66 Investment Community Meeting September 15, 2010 MasterCard introduces Mobile Payments Gateway, an m-wallet platform linking MasterCard cards First Mobile PayPass Tag pilot in Canada First Market Trial of Personalized NFC-Enabled Mobile Phones 200 phones payment pilot in partnership with ViVOtech Fully-integrated on-demand person-to-person mobile payment service Custom technology trial of Near Field Communication and MTA First trial of PayPass- enabled mobile phones for secure EMV payments Pioneer mobile phone debit payments in the UK, using Maestro PayPass Enable customers to make contactless payments via phones with MasterCard PayPass Turkey’s first mobile phones, enabled with MasterCard PayPass Partnering in the development of a Mobile Payments proposition that focuses specifically on consumer convenience First large scale deployment of PayPass in a mobile phone (60K Customer) First trial in Taiwan to make use of NFC smart posters and m-coupons First Mobile Pilot in India (Bangalore) using Mobile PayPass First Commercial mobile NFC Deployment Turkey’s first mobile phones, enabled with MasterCard PayPass Partnership will pursue mobile commerce opportunities |

Transformation of Payments Trend Page 67 Investment Community Meeting September 15, 2010 New Types of Customers New Technologies and Products The changing payments landscape provides new opportunities with non-traditional customers and innovative products but also introduces new challenges |

Expanding Our Customer Base Page 68 Investment Community Meeting September 15, 2010 Strategic Global Prepaid Alliance with Travelex Co-Brand Partnership Spanning 11 Countries in Latin America |

Evolving Role of Governments Trend Page 69 Investment Community Meeting September 15, 2010 MasterCard is actively partnering with governments Working with regulatory bodies to drive positive change Supporting financial inclusion in emerging markets Driving electronic payments infrastructure development |

Russia Supporting Government’s Payments Agenda Page 70 Investment Community Meeting September 15, 2010 MasterCard partners with Sberbank, Russia’s largest retail bank, to offer customers Maestro Debit Cards instead of traditional savings passbooks. |

Page 71 Investment Community Meeting September 15, 2010 Focusing on market trends Tailoring country-level strategies Leveraging global resources Adapting innovation for local execution The Growth Engine for MasterCard International Markets |

Investment Community Meeting Europe: Opportunities for Growth Javier Perez President, MasterCard Europe September 15, 2010 |

Europe: Largest PCE in the World Page 73 Investment Community Meeting September 15, 2010 Source: Economist Intelligence Unit (EIU) 2009 Global PCE US$ 34T |

Spend on Cards MasterCard Market Share MasterCard Switching Ratio United States 31% 27% 90% Europe’s Card Payments Business is Far from Being Mature and Saturated Page 74 Investment Community Meeting September 15, 2010 Continental Europe has substantial potential to grow Sources: PCE – EIU, Spend on Cards – Euromonitor, Market Share – Nilson, RBR, Processing data - Internal data 2009 Continental Europe PCE $10T 23% 50% 19% |

MasterCard is Well Positioned to Capture the Opportunity Page 75 Investment Community Meeting September 15, 2010 A starting position of strength Building for the future with products and partnerships An active force in shaping the industry Global and independent Giulio Tremonti, Italy's Minister of Welfare, presents the new Maestro social card to the press. |

Leveraging the Single Euro Payments Area Page 76 Investment Community Meeting September 15, 2010 We are now switching domestic debit in every SEPA country 2006 2009 Domestic Debit Switching No Domestic Debit Switching Percent of MasterCard Domestic Debit Transactions Switched 3.4% 6.9% SEPA opens competition for 97% of domestic transactions |

Then Challenges Now • 90% of Dutch Debit cards converted to EMV Maestro • Additional security and features for consumers • MasterCard begins processing Dutch domestic Debit transactions Domestic scheme: 100% of Debit cards and domestic volume • Nationalist sentiment • Cost of migrating merchants to EMV • Deliver a positive consumer experience Processing all Dutch domestic transactions would increase MasterCard Europe’s processed transactions by 40% Unlocking Opportunity in The Netherlands Page 77 Investment Community Meeting September 15, 2010 Enhancing the consumer experience |

Then Challenges Now Unlocking Opportunity in France Page 78 Investment Community Meeting September 15, 2010 Sparking innovation and choice • Strong domestic schemes controlled by banks • Difficult for non-traditional players to enter market • “Breaking the market” • Legacy of co-branding restrictions • Carrefour: First major MasterCard-only Issuer in France • Auchan and others follow; unique card propositions emerge • 2.5 million PayPass cards within 18 months • MasterCard begins processing French domestic Debit transactions |

2006 2009 2015 E Well Positioned to Seize the Opportunity Page 79 Investment Community Meeting September 15, 2010 Sources: PCE – EIU, Spend on Cards – Euromonitor, Market share – RBR, Processing data – Internal data Spend on Cards MasterCard Market Share MasterCard Switching Ratio $8T 20% 46% 15% $10T 23% 50% 19% $12T + + + Continental Europe PCE |

Investment Community Meeting Financial Perspective Martina Hund-Mejean Chief Financial Officer September 15, 2010 |

Topics for Today 2010 Outlook Rebates & Incentives Capital Structure Considerations Long-Term Growth Opportunity Updated Long-Term Performance Targets Investment Community Meeting Page 81 September 15, 2010 |

Worldwide Gross Dollar Volume (GDV) Growth 0.6 5.6 8.3 8.5 4.6 0.3 2.5 3.4 5.2 0.6 5.9 10.8 11.9 9.8 0% 5% 10% 15% Q3'09 Q4'09 Q1'10 Q2'10 Jul/Aug Reported Processed 5.6 Processed Investment Community Meeting Page 82 September 15, 2010 As Reported Impact of Deconversions |

US Credit Gross Dollar Volume Growth Reported 1.2 Processed Investment Community Meeting Page 83 September 15, 2010 0% -5% -10% -15% -20% |

US Debit Gross Dollar Volume Growth 5.2 10.5 7.0 0.8 -5.0 0.4 2.3 15.3 20.2 25.8 5.6 12.8 22.3 21.0 20.8 -10% 0% 10% 20% 30% Q3'09 Q4'09 Q1'10 Q2'10 Jul/Aug Reported Processed 0.7 Processed Investment Community Meeting Page 84 September 15, 2010 As Reported Impact of Deconversions |

Rest of World Gross Dollar Volume Growth 7.4 11.6 14.8 14.5 14.0 0% 4% 8% 12% 16% Q3'09 Q4'09 Q1'10 Q2'10 Jul/Aug Reported Processed 12.5 Processed Investment Community Meeting Page 85 September 15, 2010 |

Worldwide Processed Transactions 7.6 6.6 4.6 0.1 0.1 1.6 4.8 9.8 12.0 8.2 9.4 9.9 12.1 0% 5% 10% 15% Q3'09 Q4'09 Q1'10 Q2'10 Jul/Aug Investment Community Meeting Page 86 September 15, 2010 As Reported Impact of Deconversions |

Worldwide Cross-Border Volume Growth Investment Community Meeting Page 87 September 15, 2010 |

• Raised Acquirer Cross-Border Assessment Fee in Q4 2009, with corresponding rebates • Will simplify structure starting Q4 2010 – All rebates will be collapsed into gross revenue with no impact on net revenue • As-reported Acquirer Cross-Border Rebates were: – Q1 2010 = $65 million – Q2 2010 = $62 million Acquirer Cross-Border Rebates Investment Community Meeting Page 88 September 15, 2010 |

2010 Financial Outlook: Constant Currency • 1-2 ppt headwind from Euro/Real FX • Debit Portfolio losses • Rebates & Incentives trajectory Net Revenue Operating Expenses Net Income Growth • Modest decline • 1-2 ppt tailwind from Euro/Real FX • Reinvestment in the business in Q3 / Q4 • A&M spend higher in second half of year • Achieve at least 20% Investment Community Meeting Page 89 September 15, 2010 |

Rebates & Incentives Mix* % of Rebates & Incentives * Excludes Acquirer Cross-Border Rebates Volume / Transaction Based ~ 70 % New / Renewed Deals and Customer Marketing ~ 30 % Investment Community Meeting Page 90 September 15, 2010 |

Capital Structure Considerations Guiding Principles • Preserve strong balance sheet, liquidity and credit ratings • $3.5 billion net cash with remaining litigation payable of $0.6 billion as of June 30, 2010 • Available debt capacity, though to be used sparingly until clarity around outstanding litigation • Bias towards share repurchase over dividend increases • Will target regular cadence depending on use of cash in the business • $1.0 billion share repurchase program recently authorized by the Board of Directors • Investments in organic opportunities and M&A transactions • Primary focus in technology, processing, prepaid, e-Commerce and mobile Strong Balance Sheet Long-Term Business Growth Return Excess Cash Investment Community Meeting Page 91 September 15, 2010 |

Liquidity Investment Community Meeting Page 92 September 15, 2010 |

2010 – 2015E (CAGR) Global PCE 6% Card Purchase Vol. 10% Secular Growth 4% PCE Growth and Secular Trend Provide for Tremendous Opportunity Source: EIU, Euromonitor and MasterCard internal estimates Personal Consumption Expenditure (PCE) 65% 56% 46% 12% 15% 18% 23% 29% 36% 2005 2010E 2015E Cash & Check EFT Credit / Debit $27 Trillion $36 Trillion $48 Trillion Investment Community Meeting Page 93 September 15, 2010 |

Long-Term Revenue Growth Source: EIU, Euromonitor and MasterCard internal estimates Estimated 2010-2015 CAGR MasterCard Long-Term Revenue Global PCE Secular Growth +4% 6% ~10% Low – Mid Teens ~9% Industry Purchase Volume Adjusted Industry Purchase Volume MA Mix Strategic Investments (1%) Investment Community Meeting Page 94 September 15, 2010 |

Updated Longer-Term 2011 – 2013 Performance Objectives On a constant currency basis: Net Revenue Growth Rate Operating Margin Earnings Per Share Growth Rate 20% + CAGR minimum 50% annually 12-14% CAGR Investment Community Meeting Page 95 September 15, 2010 |

APPENDIX Cross-Border Pricing Change ($ in millions) Page 96 Investment Community Meeting September 15, 2010 Note 1: Adjusted view of Q1 and Q2 2010 illustrates impact if cross-border acquiring rebate pricing change had occurred on 1/1/2010. Pricing change will not be retroactive. Simplified structure with no Net Revenue impact As Reported Adjusted View 1 B/(W) B/(W) Q1 2010 $ % growth $ % growth Gross Revenue 1,683 12.7 1,748 17.1 Rebates & Incentives (375) (11.3) (440) (30.7) Net Revenue 1,308 13.1 1,308 13.1 Rebates & Incentives % of Gross Revenue 22.3% 25.2% Q2 2010 Gross Revenue 1,766 8.7 1,828 12.6 Rebates & Incentives (401) (16.6) (463) (34.7) Net Revenue 1,365 6.6 1,365 6.7 Rebates & Incentives % of Gross Revenue 22.7% 25.3% |

Investment Community Meeting Innovation Experience Garry Lyons Group Executive, Research & Development September 15, 2010 |

MasterCard Drives Growth through Innovation Page 98 Investment Community Meeting September 15, 2010 MasterCard has always been a payments innovator. And will continue to be a key contributor Change is happening fast. Needs of merchants and cardholders evolving faster than ever We must leverage our preeminence in payments. To stay ahead or react quickly as opportunities emerge |

Make MasterCard better & faster at innovation, and facilitate the creation of disruptive breakthrough solutions for the next phase in MasterCard’s growth. Breakthrough Innovations Page 99 Investment Community Meeting September 15, 2010 Preserving the strength of our brand, reputation and quality of our network. “The temptation of business is always to feed yesterday and to starve tomorrow.” – Peter Drucker |

Be open and diverse Guiding Principles Page 100 Investment Community Meeting September 15, 2010 Share everything Dare to dream Labs is a stepping stone Good ideas can come from anywhere Fail smart Define success metrics early Timeliness trumps perfection |

Access to new ideas, creating even better experiences MasterCard Open API: The New Frontier Page 101 Investment Community Meeting September 15, 2010 Companies revolutionized by opening up… proven impact This is just the beginning… Developer portal is on track to launch later this year. |

Product Demonstrations Page 102 Investment Community Meeting September 15, 2010 inControl Providing personalized spending control and peace of mind. MasterCard MarketPlace A smarter way to shop online. Prepaid Solutions Leading the conversion from cash and checks to electronic payments. MoneySend Greater speed, convenience and security in person-to-person payments. Integrated Processing Solutions The globally integrated processing platform for debit and prepaid. Smart Data Spend management to help companies work smarter. |

Investment Community Meeting Closing Remarks Ajay Banga President and Chief Executive Officer September 15, 2010 |

Looking to the Future Page 104 Investment Community Meeting September 15, 2010 Striking the right global / local balance Investing in innovative products and solutions Capturing opportunities while addressing challenges Delivering strong financial performance |

|