Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934 (Amendment No. )

Filed by the Registrant x

Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| x | Definitive Proxy Statement |

| ¨ | Definitive Additional Materials |

| ¨ | Soliciting Material Under §240.14a-12 |

COOPER INDUSTRIES PLC

(Name of Registrant as Specified in its Charter)

N/A

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. |

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

Table of Contents

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

| ¨ | Fee paid previously with preliminary materials. |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) | Amount previously paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

Table of Contents

COOPER INDUSTRIES PLC

Unit F10, Maynooth Business Campus,

Maynooth, Ireland

To Our Shareholders:

You are cordially invited to attend two special meetings of the shareholders of Cooper Industries plc, which is referred to as Cooper. The first, the special court-ordered meeting, is to be held on October 26, 2012 at 11:00 a.m. local time, at the Chase Tower in the 54th Floor conference room, located at 600 Travis Street, Houston, Texas 77002, and the second, the extraordinary general meeting, referred to as the EGM, is to be held on October 26, 2012 at 11:10 a.m. local time, at the same location, or, if later, as soon as possible after the conclusion or adjournment of the special court-ordered meeting.

As previously announced, on May 21, 2012, Cooper entered into a transaction agreement with Eaton Corporation, which is referred to as Eaton, pursuant to which Eaton will acquire Cooper through the formation of a new holding company incorporated in Ireland, which is referred to as New Eaton. The acquisition of Cooper will be effected by means of a “scheme of arrangement” under Irish law.

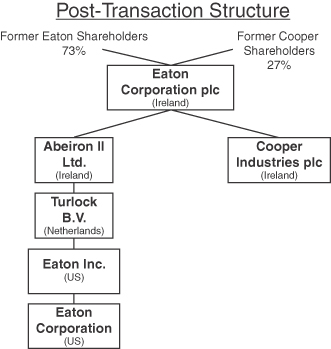

As consideration for the acquisition, Cooper shareholders will receive $39.15 in cash and 0.77479 of a New Eaton ordinary share for each Cooper share. In connection with the acquisition, Eaton will merge with a wholly owned subsidiary of New Eaton. Each Eaton common share then issued and outstanding will be cancelled and automatically converted into the right to receive one New Eaton ordinary share. Upon completion of the merger and acquisition, based on the number of Eaton and Cooper shares outstanding as of the record date, the former shareholders of Eaton are expected to own approximately 73%, and the former shareholders of Cooper are expected to own approximately 27%, of the outstanding voting shares of New Eaton. The receipt of New Eaton shares and cash for Cooper ordinary shares will be a taxable transaction to Cooper shareholders.

You are being asked to vote on a proposal to approve the scheme at both special meetings, as well as three additional proposals being presented at the EGM that shareholders must approve in order to properly implement the scheme. You are also being asked to vote at the EGM on proposals relating to the creation of “distributable reserves,” which are required under Irish law in order for New Eaton to, among other things, be able to pay dividends in the future, as well as the non-binding advisory approval of specified compensatory arrangements between Cooper and its named executive officers relating to the transaction; however, the acquisition is not conditioned on approval of these proposals. The scheme also is subject to approval by the Irish High Court. More information about the transaction and the proposals is contained in the accompanying joint proxy statement/prospectus.We urge allCooper shareholders to read the accompanyingjointproxy statement/prospectus,includingthe Annexes and the documents incorporatedby referencetherein,carefullyand in their entirety.In particular,we urge you to read carefully“Risk Factors” beginning on page 28 of the accompanyingjointproxy statement/prospectus.

Your proxy is being solicited by the board of directors of Cooper. After careful consideration, the board of directors of Cooper has unanimously determined that the transaction agreement and the transactions contemplated by the transaction agreement, including the scheme, are fair to and in the best interests of Cooper and its shareholders and that the terms of the scheme are fair and reasonable.The Cooper board recommendsunanimouslythatyou vote“FOR” all proposals.In considering the recommendation of the Cooper board, you should be aware that certain directors and executive officers of Cooper will have interests in the proposed transaction in addition to the interests they might have as shareholders.Your voteisvery important.Pleasevote as soon as possible,whether or not you plan to attendthe specialmeetings,by followingthe instructionsin the accompanyingjointproxy statement/prospectus.

On behalf of the Cooper board of directors, thank you for your consideration and continued support.

Very truly yours,

Kirk Hachigian

Chairman, President and Chief Executive Officer

Neitherthe Securitiesand Exchange Commissionnor any statesecuritiescommissionhas approved or disapproved of the securitiesto be issuedin connectionwith the transactionor determinedifthe accompanyingjointproxy statement/prospectusisaccurateor complete.Anyrepresentationto the contraryisa criminaloffense.

For the avoidance of doubt, the accompanying joint proxy statement/prospectus is not intended to be and is not a prospectus for the purposes of the Investment Funds, Companies and Miscellaneous Provisions Act of 2005 of Ireland (the “2005 Act”), the Prospectus (Directive 2003/71/EC) Regulations 2005 of Ireland or the Prospectus Rules issued under the 2005 Act, and the Central Bank of Ireland has not approved this document.

The accompanying joint proxy statement/prospectus is dated September 14, 2012, and is first being mailed to shareholders of Cooper on or about September 19, 2012.

Table of Contents

ADDITIONAL INFORMATION

The accompanying joint proxy statement/prospectus incorporates by reference important business and financial information about Cooper from documents that are not included in or delivered with the joint proxy statement/prospectus. This information is available to you without charge upon your written or oral request. You can obtain the documents incorporated by reference in the joint proxy statement/prospectus by requesting them in writing or by telephone from Cooper at the following address and telephone number:

Cooper

c/o Cooper US, Inc.

600 Travis Street, Suite 5600

Houston, Texas 77002

(713) 209-8400

www.cooperindustries.com “Investors” tab

In addition, if you have questions about the transaction or the special meetings, or if you need to obtain copies of the accompanying joint proxy statement/prospectus, proxy cards, election forms or other documents incorporated by reference in the joint proxy statement/prospectus, you may contact the contact listed below. You will not be charged for any of the documents you request.

D.F. King and Co. Inc.

48 Wall Street, 22nd Floor

New York, NY 10005

(800) 859-8508 (toll free)

(212) 269-5550 (banks and brokers collect)

If you would like to request documents, please do so by October 19, 2012, in order to receive them before the special meetings.

For a more detailed description of the information incorporated by reference in the accompanying joint proxy statement/prospectus and how you may obtain it, see “Where You Can Find More Information” beginning on page 208 of the accompanying joint proxy statement/prospectus.

Table of Contents

COOPER INDUSTRIES PLC

Unit F10, Maynooth Business Campus

Maynooth, Ireland

NOTICE OF COURT MEETING OF SHAREHOLDERS

NOTICE OF COURT MEETING

IN THE HIGH COURT No. 2012/497 COS

IN THE MATTER OF COOPER INDUSTRIES PLC

– and –

IN THE MATTER OF THE COMPANIES ACTS 1963 to 2012

NOTICE IS HEREBY GIVEN that by an Order dated September 12, 2012 made in the above matters, the Irish High Court has directed a meeting (the “Court Meeting”) to be convened of the holders of the Scheme Shares (as defined in the proposed scheme of arrangement) of Cooper Industries plc (“Cooper”) for the purpose of considering and, if thought fit, approving (with or without modification) a scheme of arrangement pursuant to Section 201 of the Companies Act 1963 proposed to be made between Cooper and the holders of the Scheme Shares (and that such meeting will be held at the Chase Tower in the 54th Floor conference room, located at 600 Travis Street, Houston, Texas 77002, on October 26, 2012, at 11:00 a.m. (local time)), at which place and time all holders of the Scheme Shares entitled to vote thereat are invited to attend.

A copy of the scheme of arrangement and a copy of the explanatory statement required to be furnished pursuant to Section 202 of the Companies Act 1963 are included in the document of which this Notice forms part.

Scheme Shareholders may vote in person at the Court Meeting or they may appoint another person, whether a Member of Cooper or not, as their proxy to attend, speak and vote in their stead. A Form of Proxy for use at the Court Meeting is enclosed with this Notice. Completion and return of a Form of Proxy will not preclude a Scheme Shareholder from attending and voting in person at the Court Meeting, or any adjournment thereof, if that shareholder wishes to do so. Any alteration to the Form of Proxy must be initialed by the person who signs it.

It is requested that Forms of Proxy duly completed and signed, together with any power of attorney, if any, under which it is signed, be lodged with Cooper’s inspector of election, Broadridge Financial Solutions, 51 Mercedes Way, Edgewood, New York 11717, no later than 11:59 p.m. (Eastern Time in the U.S.) on the day before the Court Meeting but, if forms are not so lodged, they may be handed to the Chairman of the Court Meeting before the start of the Court Meeting and will still be valid.

Scheme Shareholders may also submit a proxy or proxies via the Internet by accessing the inspector of election’s website (www.proxyvote.com) or vote by telephone (+1-800-690-6903) anytime up to 11:59 p.m. (Eastern Time in the U.S.) on the day immediately preceding the Court Meeting.

In the case of joint holders, the vote of the senior who tenders a vote, whether in person or by proxy, will be accepted to the exclusion of the vote(s) of the other joint holder(s) and, for this purpose, seniority will be determined by the order in which the names stand in the register of Members of Cooper in respect of the joint holding.

Table of Contents

Entitlement to attend and vote at the meeting, or any adjournment thereof, and the number of votes which may be cast thereat, will be determined by reference to the register of Members of Cooper as of 11:59 p.m. (Eastern Time in the U.S.) on September 13, 2012, which is referred to as the “Voting Record Time.” In each case, changes to the register of Members of Cooper after such time shall be disregarded for the purposes of being entitled to vote.

If the Form of Proxy is properly executed and returned to Cooper’s inspector of election, it will be voted in the manner directed by the shareholder executing it, or if no directions are given, will be voted at the discretion of the Chairman of the Court Meeting or any other person duly appointed as proxy by the shareholder.

In the case of a corporation, the Form of Proxy must be either under its Common Seal or under the hand of an officer or attorney, duly authorized.

By the said Order, the Irish High Court has appointed Kirk S. Hachigian, Chairman, President and Chief Executive Officer, or, failing him, Bruce M. Taten, Senior Vice President, General Counsel and Chief Compliance Officer, or, failing him, such director or officer of Cooper as the Board of Directors of Cooper may determine, to act as Chairman of the said meeting and has directed the Chairman to report the result thereof to the Irish High Court.

Subject to the approval of the resolution proposed at the meeting convened by this notice and the requisite resolutions to be proposed at the extraordinary general meeting of Cooper convened for October 26, 2012, it is anticipated that the Irish High Court will order that the hearing of the petition to sanction the said scheme of arrangement will take place in the second half of 2012.

Terms shall have the same meaning in this Notice as they have in the joint proxy statement/prospectus accompanying this Notice.

The said scheme of arrangement will be subject to the subsequent sanction of the Irish High Court.

Issued shares and total voting rights

The total number of issued Scheme Shares held by Scheme Shareholders as of the Voting Record Time entitled to vote at the Court Meeting is 161,489,215. The resolution at the Court Meeting shall be decided on a poll. Every holder of a Cooper ordinary share as of the Voting Record Time will have one vote for every Cooper ordinary share carrying voting rights of which he, she or it is the holder. A holder of a Cooper ordinary share as of the Voting Record Time (whether present in person or by proxy) who is entitled to more than one vote need not use all his, her or its votes or cast all his, her or its votes in the same way. To be passed, the resolution requires the approval of a majority in number of the shareholders of record of Cooper ordinary shares as of the Voting Record Time voting on the proposal representing at least 75 percent in value of the Scheme Shares held by such holders voting in person or by proxy.

YOUR VOTE IS IMPORTANT

IT IS IMPORTANT THAT AS MANY VOTES AS POSSIBLE ARE CAST AT THE COURT MEETING (WHETHER IN PERSON OR BY PROXY) SO THAT THE IRISH HIGH COURT CAN BE SATISFIED THAT THERE IS A FAIR AND REASONABLE REPRESENTATION OF COOPER SHAREHOLDER OPINION. TO ENSURE YOUR REPRESENTATION AT THE MEETING, YOU ARE REQUESTED TO COMPLETE, SIGN AND DATE THE ENCLOSED PROXY FORM AS PROMPTLY AS POSSIBLE AND RETURN IT IN THE POSTAGE PREPAID ENVELOPE ENCLOSED FOR THAT PURPOSE OR BY INTERNET OR TELEPHONE IN THE MANNER PROVIDED ABOVE. IF YOU ATTEND THE MEETING, YOU MAY VOTE IN PERSON EVEN IF YOU HAVE RETURNED A PROXY.

Dated September 14, 2012

Arthur Cox

Earlsfort Centre

Earlsfort Terrace

Dublin 2

Ireland

Solicitors for Cooper

Table of Contents

COOPER INDUSTRIES PLC

Unit F10, Maynooth Business Campus

Maynooth, Ireland

NOTICE OF EXTRAORDINARY GENERAL MEETING OF SHAREHOLDERS

NOTICE OF EXTRAORDINARY GENERAL MEETING

OF COOPER INDUSTRIES PLC

NOTICE IS HEREBY GIVEN that an EXTRAORDINARY GENERAL MEETING (“EGM”) of Cooper Industries Plc (the “Company”) will be held at the Chase Tower in the 54th Floor conference room, located at 600 Travis Street, Houston, Texas 77002, on October 26, 2012 at 11:10 a.m. (local time) (or, if later, as soon as possible after the conclusion or adjournment of the Court Meeting (as defined in the scheme of arrangement which is included in the document of which this Notice forms part)) for the purpose of considering and, if thought fit, passing the following resolutions of which Resolutions 1, 3, 5, 6 and 7 will be proposed as ordinary resolutions and Resolutions 2 and 4 as special resolutions:

| 1. | Ordinary Resolution: To approve the Scheme of Arrangement |

That, subject to the approval by the requisite majorities of the Scheme of Arrangement (as defined in the document of which this Notice forms part) at the Court Meeting, the Scheme of Arrangement (a copy of which has been produced to this meeting and for the purposes of identification signed by the Chairman thereof) in its original form or with or subject to any modification, addition or condition approved or imposed by the Irish High Court be approved and the directors of Cooper be authorised to take all such action as they consider necessary or appropriate for carrying the Scheme of Arrangement into effect.

| 2. | Special Resolution: Cancellation of Cooper Shares pursuant to the Scheme of Arrangement |

That, subject to the passing of Resolution 1 (above) and to the confirmation of the Irish High Court pursuant to Section 72 of the Companies Act 1963, the issued capital of Cooper be reduced by cancelling and extinguishing all the Cancellation Shares (as defined in the Scheme of Arrangement) but without thereby reducing the authorised share capital of Cooper.

| 3. | Ordinary Resolution: Directors’ authority to allot securities and application of reserves |

That, subject to the passing of Resolutions 1 and 2 and in this notice of meeting:

| (i) | the directors of Cooper be and are hereby generally authorised pursuant to and in accordance with Section 20 of the Companies (Amendment) Act 1983 to give effect to this resolution and accordingly to effect the allotment of the New Cooper Shares (as defined in the Scheme of Arrangement) referred to in paragraph (ii) below provided that (i) this authority shall expire on 31 December 2013, (ii) the maximum aggregate nominal amount of shares which may be allotted hereunder shall be an amount equal to nominal value of the Cancellation Shares and (iii) this authority shall be without prejudice to any other authority under the said Section 20 previously granted before the date on which this resolution is passed; and |

| (ii) | forthwith upon the reduction of capital referred to in Resolution 2 above taking effect, the reserve credit arising in the books of account of Cooper as a result of the cancellation of the Cancellation Shares be applied in paying up in full at par such number of New Cooper Shares as shall be equal to the |

Table of Contents

| aggregate of the number of Cancellation Shares cancelled pursuant to Resolution 2 above, such new Cooper Shares to be allotted and issued to Eaton Corporation Limited and/or its nominee(s) credited as fully paid up and free from all liens, charges, encumbrances, rights of pre-emption and any other third party rights of any nature whatsoever. |

| 4. | Special Resolution: Amendment to Articles |

That, subject to the Scheme becoming effective, the Articles of Association of Cooper be amended by adding the following new Article 108:

108. Scheme of Arrangement

| (a) | In these Articles, the “Scheme” means the scheme of arrangement dated September 14, 2012 between the Company and the holders of the Scheme Shares under Section 201 of the Companies Act 1963 in its original form or with or subject to any modification, addition or condition approved or imposed by the Irish High Court and expressions defined in the Scheme and (if not so defined) in the document containing the explanatory statement circulated with the Scheme under Section 202 of the Companies Act 1963 shall have the same meanings in this Article. |

| (b) | Notwithstanding any other provision of these Articles, if the Company allots and issues any Ordinary Shares (other than to Eaton Corporation public limited company incorporated in Ireland, (company number 512978 (“New Eaton”) or its nominee(s) (holding on bare trust for New Eaton)) on or after the Voting Record Time and prior to 10:00 p.m. (Irish time) on the day before the date on which the Scheme becomes effective (the “Scheme Record Time”), such shares shall be allotted and issued subject to the terms of the Scheme and the holder or holders of those shares shall be bound by the Scheme accordingly. |

| (c) | Notwithstanding any other provision of these Articles, if any new Ordinary Shares are allotted or issued to any person (a “new member”) (other than under the Scheme or to New Eaton or any subsidiary undertaking of New Eaton or anyone acting on behalf of New Eaton (holding on bare trust for New Eaton) at or after the Scheme Record Time, New Eaton will, provided the Scheme has become effective, have such shares transferred immediately, free of all encumbrances, to New Eaton and/or its nominee(s) (holding on bare trust for New Eaton) in consideration of and conditional on the payment by New Eaton to the new member of the consideration to which the new member would have been entitled under the terms of the Scheme had such shares transferred to New Eaton hereunder been a Scheme Share, such new Cooper Shares to rankpari passu in all respects with all other Cooper Shares for the time being in issue and ranking for any dividends or distributions made, paid or declared thereon following the date on which the transfer of such new Cooper Shares is executed. |

| (d) | In order to give effect to any such transfer required by this Article 108, the Company may appoint any person to execute and deliver a form of transfer on behalf of, or as attorney for, the new member in favour of New Eaton and/or its nominee(s) (holding on bare trust for New Eaton). Pending the registration of New Eaton as a holder of any share to be transferred under this Article 108, the new member shall not be entitled to exercise any rights attaching to any such share unless so agreed by New Eaton and New Eaton shall be irrevocably empowered to appoint a person nominated by the Directors of New Eaton to act as attorney on behalf of any holder of that share in accordance with any directions New Eaton gives in relation to any dealings with or disposal of that share (or any interest in it), exercising any rights attached to it or receiving any distribution or other benefit accruing or payable in respect of it and any holders of that share must exercise all rights attaching to it in accordance with the directions of New Eaton. The Company shall not be obliged to issue a certificate to the new member for any such share. |

Table of Contents

| 5. | Ordinary Resolution: Creation of Distributable Reserves of New Eaton |

That the reduction of all of the share premium of New Eaton resulting from the issuance of New Eaton Shares (as defined in the Scheme of Arrangement) pursuant to (i) the Scheme of Arrangement and (ii) a subscription for New Eaton Shares by Eaton Inc. prior to the merger, in order to create distributable reserves of New Eaton be approved.

| 6. | Ordinary Resolution (non-binding, advisory): Approval of specified compensatory arrangement between Cooper and its named executive officers |

That, on a non-binding advisory basis, specified compensatory arrangements between Cooper and its named executive officers relating to the transaction (as more particularly described in the section of the accompanying joint proxy statement/prospectus captioned “Interests of Certain Persons in the Transaction—Cooper”) be approved.

| 7. | Ordinary Resolution: Adjournment of the EGM |

That any motion by the Chairman to adjourn the EGM, or any adjournments thereof, to another time and place if necessary or appropriate to solicit additional proxies if there are insufficient votes at the time of the EGM to approve the Scheme, or the other resolutions set out at 2 through 6 above, be approved.

By order of the Board

Company Secretary

Terrance V. Helz

Dated: September 14, 2012 | Cooper Industries plc Unit F10, Maynooth Business Campus Straffan Road Maynooth Co. Kildare |

Notes:

| 1. | A shareholder of Cooper entitled to attend and vote is entitled to appoint a proxy to attend, speak and vote on his or her behalf and may appoint more than one proxy to attend on the same occasion. A proxy need not be a shareholder of Cooper. Appointment of a proxy will not preclude a Cooper shareholder from attending and voting at the meeting should the shareholder subsequently wish to do so. To be effective, the form of proxy, duly completed and signed together with any power of attorney, if any, under which it is signed must be deposited with Cooper’s inspector of election, Broadridge Financial Solutions, 51 Mercedes Way, Edgewood, New York 11717, no later than 11:59 p.m. (Eastern Time in the U.S.) on the day before the EGM. Alternatively, shareholders may also submit a proxy or proxies via the Internet by accessing the inspector of election’s website (www.proxyvote.com) or to vote by telephone (+1-800-690-6903) anytime up to 11:59 p.m. (Eastern Time in the U.S.) on the day immediately preceding the EGM. |

| 2. | If the Form of Proxy is properly executed and returned to Cooper’s inspector of election, it will be voted in the manner directed by the shareholder executing it or, if no directions are given, will be voted at the discretion of the Chairman of the EGM or any other person duly appointed as proxy by the shareholder. |

| 3. | In the case of a corporation, the Form of Proxy must be either under its Common Seal or under the hand of an officer or attorney, duly authorised. |

| 4. | In the case of joint holders, the vote of the senior holder who tenders a vote, whether in person or by proxy, shall be accepted to the exclusion of the vote(s) of the other joint holder(s) and for this purpose seniority shall be determined by the order in which the names stand in the Register of Members of Cooper in respect of the joint holding. |

| 5. | The completion and return of the Form of Proxy will not preclude a member from attending and voting at the meeting in person. |

Table of Contents

| 6. | In accordance with article 17 of Cooper’s articles of association, the board of directors of Cooper has determined that only holders of record of Ordinary Shares of Cooper as of 11:59 p.m. (Eastern Time in the U.S.) on September 13, 2012 may vote at the EGM or any adjournment thereof. Changes to the register of Members of Cooper after such time shall be disregarded for the purposes of being entitled to vote. |

| 7. | Terms shall have the same meaning in this Notice as they have in the scheme of arrangement included in the joint proxy statement/prospectus accompanying this Notice. |

| 8. | Any alteration to the Form of Proxy must be initialled by the person who signs it. |

| 9. | Only holders of record of Ordinary Shares of Cooper as of the Voting Record Time are entitled to notice of and to vote at the EGM or any adjournments of the EGM. A person who holds shares “beneficially” will not be the holder of record. Instead, the depository (for example, Cede & Co., as nominee for DTC) or other nominee will be the holder of record of such shares. Where persons hold shares beneficially through a bank, broker or other nominee, the nominee may generally vote the shares it holds in accordance with instructions received. Therefore, beneficial holders should follow the instructions provided by their nominee when voting their shares. Persons holding shares beneficially through a nominee who plan to attend the EGM should bring photo identification and proof of ownership, such as a bank or brokerage firm account statement or a letter from the broker holding their shares, confirming their beneficial ownership of such shares as of the Voting Record Time for the EGM. Persons holding shares beneficially through a nominee who plan to vote at the meeting must obtain a legal proxy from the nominee, and should contact their nominee for instructions on how to obtain such a legal proxy. See “The Special Meetings of Cooper’s Shareholders” of the accompanying joint proxy statement/prospectus. |

| 10. | The Scheme is subject to the approval of the Scheme by the requisite shareholder majorities at the Court Meeting, the passing of resolutions 1 through 4 at the EGM and the subsequent sanction by the Irish High Court. The Scheme is not subject to the passing of resolutions 5 through 7 at the EGM. |

| 11. | Cooper shareholders should also refer to the section of the accompanying joint proxy statement/prospectus captioned “The Special Meetings of Cooper’s Shareholders,” which further describes the matters being voted on at the EGM and the ultimate effect of each resolution. |

Table of Contents

To Our Shareholders:

You are cordially invited to attend a special meeting of the shareholders of Eaton Corporation to be held on October 26, 2012 at 3 p.m. local time, at Eaton Center, located at 1111 Superior Avenue, Cleveland, Ohio 44114.

As previously announced, on May 21, 2012, Eaton entered into a transaction agreement with Cooper Industries plc to acquire Cooper through the formation of a new holding company incorporated in Ireland that will be renamed Eaton Corporation plc, which is referred to as New Eaton. The acquisition of Cooper will be effected by means of a “scheme of arrangement” under Irish law, subject to the approval of the Irish High Court. As consideration for the acquisition, Cooper shareholders will receive $39.15 in cash and 0.77479 of a New Eaton ordinary share for each Cooper share.

In connection with the acquisition, Eaton will merge with Turlock Corporation, a wholly owned subsidiary of New Eaton. Each Eaton common share then issued and outstanding will be cancelled and automatically converted into the right to receive one ordinary share of New Eaton. After giving effect to the acquisition and the merger, Eaton shareholders are expected to own approximately 73% of New Eaton ordinary shares and Cooper shareholders are expected to own approximately 27% of New Eaton ordinary shares. The exchange of Eaton shares for New Eaton ordinary shares and cash in lieu of New Eaton fractional shares will be a taxable transaction to Eaton shareholders. The New Eaton ordinary shares are expected to be listed on the New York Stock Exchange under the symbol “ETN.” Based on the number of Eaton and Cooper shares outstanding as of the record date, the total number of New Eaton ordinary shares that is expected to be issued in connection with the acquisition and the merger is approximately 463,053,528.

We urge all Eaton shareholders to read the accompanying joint proxy statement/prospectus, including the Annexes and the documents incorporated by reference in the accompanying joint proxy statement/prospectus, carefully and in their entirety. In particular, we urge you to read carefully “Risk Factors” beginning on page 28 of the accompanying joint proxy statement/prospectus.

Eaton is holding a special meeting of our shareholders to seek your approval to adopt the transaction agreement and approve the merger and certain related proposals. Your proxy is being solicited by the board of directors of Eaton. After careful consideration, our board of directors has unanimously approved the transaction agreement and determined that the terms of the acquisition will further the strategies and goals of Eaton.Our board of directors recommends unanimously that you vote “FOR” the proposal to adopt the transaction agreement and approve the merger and “FOR” the other proposals described in the accompanying joint proxy statement/prospectus. In considering the recommendation of the board of directors of Eaton, you should be aware that certain directors and executive officers of Eaton will have interests in the proposed transaction in addition to interests they might have as shareholders of Eaton. See “The Transaction—Interests of Certain Persons in the Transaction—Eaton.”Your vote is very important.Please vote as soon as possible whether or not you plan to attend the special meeting by following the instructions in the accompanying joint proxy statement/prospectus.

On behalf of the Eaton board of directors, thank you for your consideration and continued support.

| Very truly yours, |

|

Alexander M. Cutler Chairman and Chief Executive Officer Eaton Corporation |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued in connection with the transaction or determined if the accompanying joint proxy statement/prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

For the avoidance of doubt, the accompanying joint proxy statement/prospectus is not intended to be and is not a prospectus for the purposes of the Investment Funds, Companies and Miscellaneous Provisions Act of 2005 of Ireland (the “2005 Act”), the Prospectus (Directive 2003/71/EC) Regulations 2005 of Ireland or the Prospectus Rules issued under the 2005 Act, and the Central Bank of Ireland has not approved this document.

The accompanying joint proxy statement/prospectus is dated September 14, 2012, and is first being mailed to shareholders of Eaton on or about September 19, 2012.

Table of Contents

ADDITIONAL INFORMATION

The accompanying joint proxy statement/prospectus incorporates by reference important business and financial information about Eaton from documents that are not included in or delivered with the joint proxy statement/prospectus. This information is available to you without charge upon your written or oral request. You can obtain the documents incorporated by reference in the joint proxy statement/prospectus by requesting them in writing or by telephone from Eaton at the following address and telephone number:

Eaton

1111 Superior Avenue

Cleveland, Ohio 44114

Attention: Investor Relations

(216) 523-4205

www.eaton.com “Investor Relations” tab

In addition, if you have questions about the transaction or the special meeting, or if you need to obtain copies of the accompanying joint proxy statement/prospectus, proxy cards, election forms or other documents incorporated by reference in the joint proxy statement/prospectus, you may contact the contacts listed below. You will not be charged for any of the documents you request.

The Proxy Advisory Group, LLC

18 East 41st Street, Suite 2000

New York, NY 10017

(888) 55 PROXY (toll free)

(212) 616-2180 (banks and brokers collect)

MacKenzie Partners Inc.

105 Madison Avenue

New York, NY 10016

proxy@mackenziepartners.com

(212) 929-5500 (call collect)

or

Toll-Free (800) 322-2885

If you would like to request documents, please do so by October 19, 2012, in order to receive them before the special meeting.

For a more detailed description of the information incorporated by reference in the accompanying joint proxy statement/prospectus and how you may obtain it, see “Where You Can Find More Information” beginning on page 208 of the accompanying joint proxy statement/prospectus.

Table of Contents

EATON CORPORATION

Eaton Center

Cleveland, Ohio 44114

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

| Time: | 3 p.m. local time

| |

| Date: | October 26, 2012

| |

| Place: | Eaton Center, located at 1111 Superior Avenue, Cleveland, Ohio 44114.

| |

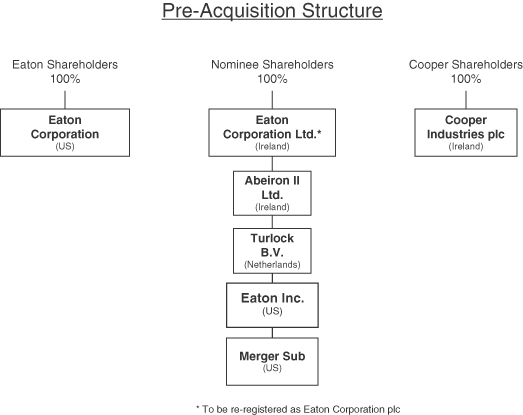

| Purpose: | (1) To adopt the transaction agreement, dated May 21, 2012, as amended by amendment no. 1 to the transaction agreement, dated June 22, 2012, among Eaton Corporation, Cooper Industries plc, Eaton Corporation Limited (formerly known as Abeiron Limited) (referred to in the accompanying joint proxy statement/prospectus as “New Eaton”), Abeiron II Limited (formerly known as Comdell Limited), Turlock B.V., Eaton Inc. and Turlock Corporation, approve the merger and approve the revised articles of association of New Eaton;

| |

(2) To approve the reduction of capital of New Eaton to allow the creation of distributable reserves of New Eaton which are required under Irish law in order to allow New Eaton to make distributions and to pay dividends and repurchase or redeem shares following completion of the transaction;

| ||

(3) To consider and vote upon, on a non-binding advisory basis, specified compensatory arrangements between Eaton and its named executive officers relating to the transaction agreement; and

| ||

(4) To approve any motion to adjourn the Eaton special meeting, or any adjournments thereof, to another time or place if necessary or appropriate (i) to solicit additional proxies if there are insufficient votes at the time of the Eaton special meeting to adopt the transaction agreement and approve the merger, (ii) to provide to Eaton shareholders in advance of the special meeting any supplement or amendment to the joint proxy statement/prospectus or (iii) to disseminate any other information which is material to the Eaton shareholders voting at the special meeting.

| ||

The enclosed joint proxy statement/prospectus describes the purpose and business of the special meeting, contains a detailed description of the merger and the transaction agreement and includes a copy of the transaction agreement, as amended, as Annex A and the conditions of the acquisition and the scheme as Annex B. Please read these documents carefully before deciding how to vote.

| ||

Record Date: | The record date for the Eaton special meeting has been fixed by the board of directors as the close of business on September 13, 2012. Eaton shareholders of record at that time are entitled to vote at the Eaton special meeting. |

More information about the transaction and the proposals is contained in the accompanying joint proxy statement/prospectus.We urge all Eaton shareholders to read the accompanying joint proxy statement/prospectus, including the Annexes and the documents incorporated by reference in the accompanying joint proxy statement/prospectus, carefully and in their entirety. In particular, we urge you to read carefully “Risk Factors” beginning on page 28 of the accompanying joint proxy statement/prospectus.

Table of Contents

The Eaton board of directors recommends unanimously that Eaton shareholders vote “FOR” the proposal to adopt the transaction agreement and approve the merger, “FOR” the proposal to reduce the capital of New Eaton to allow the creation of distributable reserves, “FOR” the proposal to approve, on a non-binding advisory basis, specified compensatory arrangements between Eaton and its named executive officers and “FOR” the Eaton adjournment proposal.

By order of the Board of Directors

Thomas E. Moran

Senior Vice President and Secretary

September 14, 2012

YOUR VOTE IS IMPORTANT

You may vote your shares by using a toll-free telephone number or electronically over the Internet as described on the proxy form. We encourage you to file your proxy using either of these options if they are available to you. Alternatively, you may mark, sign, date and mail your proxy form in the postage-paid envelope provided. The method by which you vote does not limit your right to vote in person at the special meeting. We strongly encourage you to vote.

Table of Contents

i

Table of Contents

| Page | ||||

| 43 | ||||

| 43 | ||||

| 43 | ||||

| 43 | ||||

| 43 | ||||

| 43 | ||||

| 43 | ||||

| 44 | ||||

| 44 | ||||

Share Ownership and Voting by Eaton’s Officers and Directors | 45 | |||

| 45 | ||||

| 46 | ||||

| 46 | ||||

| 46 | ||||

| 47 | ||||

| 47 | ||||

| 48 | ||||

| 48 | ||||

| 48 | ||||

| 48 | ||||

| 48 | ||||

Record Date; Outstanding Ordinary Shares; Ordinary Shares Entitled to Vote | 49 | |||

| 49 | ||||

Ordinary Share Ownership and Voting by Cooper’s Officers and Directors | 49 | |||

Vote Required; Recommendation of Cooper’s Board of Directors | 50 | |||

| 51 | ||||

| 52 | ||||

| 52 | ||||

| 52 | ||||

| 53 | ||||

| 53 | ||||

| 53 | ||||

| 54 | ||||

| 54 | ||||

| 54 | ||||

Recommendation of the Eaton Board of Directors and Eaton’s Reasons for the Transaction | 62 | |||

Recommendation of the Cooper Board of Directors and Cooper’s Reasons for the Transaction | 65 | |||

| 68 | ||||

| 81 | ||||

ii

Table of Contents

| Page | ||||

| 91 | ||||

| 92 | ||||

| 98 | ||||

| 99 | ||||

| 99 | ||||

| 100 | ||||

| 100 | ||||

| 101 | ||||

| 101 | ||||

| 102 | ||||

| 103 | ||||

| 104 | ||||

| 104 | ||||

| 105 | ||||

Tax Consequences of the Transaction to U.S. Holders of Eaton Common Shares | 107 | |||

Tax Consequences of the Transaction to U.S. Holders of Cooper Ordinary Shares | 107 | |||

Tax Consequences to U.S. Holders of Holding Shares in New Eaton | 108 | |||

| 110 | ||||

| 116 | ||||

DELISTING AND DEREGISTRATION OF SHARES OF EATON COMMON SHARES | 116 | |||

| 116 | ||||

| 116 | ||||

| 117 | ||||

| 117 | ||||

| 117 | ||||

| 117 | ||||

| 117 | ||||

| 118 | ||||

| 118 | ||||

| 118 | ||||

UNAUDITED PRO FORMA CONDENSED CONSOLIDATED FINANCIAL STATEMENTS | 119 | |||

| 132 | ||||

| 132 | ||||

| 132 | ||||

| 132 | ||||

| 132 | ||||

Treatment of Cooper Stock Options and other Cooper Equity-Based Awards | 133 | |||

Treatment of Eaton Stock Options and other Eaton Equity-Based Awards | 134 | |||

| 134 | ||||

| 134 | ||||

| 135 | ||||

iii

Table of Contents

| Page | ||||

| 137 | ||||

Conditions to the Completion of the Acquisition and the Merger | 143 | |||

| 144 | ||||

| 144 | ||||

| 145 | ||||

| 145 | ||||

| 146 | ||||

| 146 | ||||

| 147 | ||||

| 149 | ||||

| 150 | ||||

EATON SHAREHOLDER VOTE ON SPECIFIED COMPENSATORY ARRANGEMENTS | 151 | |||

| 151 | ||||

| 151 | ||||

| 151 | ||||

COOPER SHAREHOLDER VOTE ON SPECIFIED COMPENSATORY ARRANGEMENTS | 152 | |||

| 152 | ||||

| 152 | ||||

| 152 | ||||

| 153 | ||||

COMPARATIVE PER SHARE MARKET PRICE DATA AND DIVIDEND INFORMATION | 155 | |||

| 156 | ||||

| 156 | ||||

| 157 | ||||

| 158 | ||||

| 159 | ||||

| 160 | ||||

| 160 | ||||

| 160 | ||||

| 160 | ||||

| 161 | ||||

| 161 | ||||

| 161 | ||||

Variation of Rights Attaching to a Class or Series of Shares | 162 | |||

| 163 | ||||

| 163 | ||||

| 164 | ||||

| 164 | ||||

iv

Table of Contents

| Page | ||||

| 165 | ||||

| 167 | ||||

| 167 | ||||

| 167 | ||||

| 168 | ||||

| 168 | ||||

| 168 | ||||

| 168 | ||||

| 169 | ||||

| 169 | ||||

| 169 | ||||

COMPARISON OF THE RIGHTS OF HOLDERS OF EATON COMMON SHARES AND NEW EATON ORDINARY SHARES | 171 | |||

COMPARISON OF THE RIGHTS OF HOLDERS OF COOPER ORDINARY SHARES AND NEW EATON ORDINARY SHARES | 195 | |||

| 206 | ||||

| 206 | ||||

| 206 | ||||

| 206 | ||||

| 208 | ||||

| 211 | ||||

| 211 | ||||

| 211 | ||||

| 212 | ||||

| 213 | ||||

| 216 | ||||

| 217 | ||||

| 217 | ||||

| 218 | ||||

The Cooper Directors and Executive Officers and the Effect of the Scheme on Their Interests | 219 | |||

| 223 | ||||

| 223 | ||||

| 224 | ||||

| 224 | ||||

| 224 | ||||

| 225 | ||||

| 231 | ||||

| 231 | ||||

v

Table of Contents

| Page | ||||

| 231 | ||||

| 232 | ||||

| 233 | ||||

| 233 | ||||

| 272 | ||||

| 274 | ||||

| 274 | ||||

| 274 | ||||

| 275 | ||||

| 277 | ||||

| 278 | ||||

| 279 | ||||

| 280 | ||||

| 283 | ||||

| 283 | ||||

| 284 | ||||

| 286 | ||||

| 288 | ||||

| F-1 | ||||

| F-2 | ||||

EATON CORPORATION LIMITED NOTES TO CONSOLIDATED BALANCE SHEET | F-3 | |||

ANNEX A Transaction Agreement and Amendment No. 1 to the Transaction Agreement | A-1 | |||

| B-1 | ||||

| C-1 | ||||

| D-1 | ||||

| E-1 | ||||

| F-1 | ||||

| G-1 | ||||

| H-1 | ||||

vi

Table of Contents

QUESTIONS AND ANSWERS ABOUT THE TRANSACTION AND THE SPECIAL MEETINGS

The following questions and answers are intended to address briefly some commonly asked questions regarding the transaction and the special meetings. These questions and answers only highlight some of the information contained in this joint proxy statement/prospectus. They may not contain all the information that is important to you. You should read carefully this entire joint proxy statement/prospectus, including the Annexes and the documents incorporated by reference into this joint proxy statement/prospectus, to understand fully the proposed transactions and the voting procedures for the special meetings. See “Where You Can Find More Information” beginning on page 208. Unless otherwise specified, all references in this joint proxy statement/prospectus to “Eaton” refer to Eaton Corporation, an Ohio corporation; all references in this joint proxy statement/prospectus to “Cooper” refer to Cooper Industries plc, a public limited company incorporated in Ireland; all references in this joint proxy statement/prospectus to “New Eaton” refer to Eaton Corporation Limited (formerly known as Abeiron Limited), a private limited company incorporated in Ireland that will be re-registered as a public limited company and renamed Eaton Corporation plc at or prior to the completion of the transaction; as described in this joint proxy statement/prospectus; all references in this joint proxy statement/prospectus to “Abeiron II” refer to Abeiron II Limited (formerly known as Comdell Limited), a private limited company incorporated in Ireland; all references in this joint proxy statement/prospectus to “Turlock” refer to Turlock B.V., a private limited liability company incorporated in the Netherlands; all references in this joint proxy statement/prospectus to “Eaton Sub” refer to Eaton Inc., an Ohio corporation; all references in this joint proxy statement/prospectus to “Merger Sub” refer to Turlock Corporation, an Ohio corporation; unless otherwise indicated or the context requires, all references in this joint proxy statement/prospectus to “we” refer to Eaton and Cooper; all references to the “transaction agreement” refer to the Transaction Agreement, dated May 21, 2012, as amended by Amendment No. 1 to the Transaction Agreement, dated June 22, 2012, by and among Eaton, Cooper, New Eaton, Abeiron II, Turlock, Eaton Sub and Merger Sub, a copy of which is included as Annex A to this joint proxy statement/prospectus; all references to the “conditions appendix” refer to Annex B to this joint proxy statement/prospectus; and all references to the “expenses reimbursement agreement” refer to the Expenses Reimbursement Agreement, dated May 21, 2012, by and between Eaton and Cooper, which is included as Annex C to this joint proxy statement/prospectus. Unless otherwise indicated, all references to “dollars” or “$” in this joint proxy statement/prospectus are references to U.S. dollars. If you are in any doubt about this transaction you should consult an independent financial advisor who, if you are taking advice in Ireland, is authorized or exempted by the Investment Intermediaries Act 1995, or the European Communities (Markets in Financial Instruments) Regulations (No’s 1 to 3) 2007 (as amended).

| Q: | Why am I receiving this joint proxy statement/prospectus? |

| A: | Eaton, Cooper, New Eaton, Abeiron II, Turlock, Eaton Sub and Merger Sub have entered into the transaction agreement, pursuant to which New Eaton will acquire Cooper by means of a “scheme of arrangement,” or “scheme,” which we refer to in this joint proxy statement/prospectus as the “acquisition,” and, simultaneously with and conditioned on the concurrent consummation of the acquisition, Merger Sub will be merged with and into Eaton, which we refer to in this joint proxy statement/prospectus as the “merger,” with Eaton surviving the merger as a wholly owned subsidiary of New Eaton. |

Eaton is holding a special meeting of shareholders in order to obtain the shareholder approval necessary to adopt the transaction agreement and approve the merger, as described in this joint proxy statement/prospectus.

Cooper is convening a special court-ordered meeting of its shareholders in order to obtain shareholder approval of the scheme of arrangement. If Cooper obtains the necessary shareholder approval of the scheme of arrangement, at 11:10 a.m. local time on October 26, 2012, or, if later, as soon as possible after the conclusion or adjournment of the special court-ordered meeting, Cooper will convene an extraordinary general meeting, or the “EGM,” in order to obtain shareholder approval of the resolutions necessary to implement the scheme of arrangement and related resolutions. The Cooper special court-ordered meeting and the EGM are referred to herein collectively as the Cooper “special meetings.”

1

Table of Contents

We will be unable to complete the merger and the acquisition unless the requisite Eaton and Cooper shareholder approvals are obtained at the respective special meetings. However, as described below, the merger and the acquisition are not conditioned on approval of certain of the matters being presented at the Eaton special meeting and the Cooper EGM.

The acquisition, the merger and the other transactions contemplated to occur at the completion by the transaction agreement are referred to collectively in this joint proxy statement/prospectus as the “transaction.”

We have included in this joint proxy statement/prospectus important information about the merger, the acquisition, the transaction agreement (a copy of which is attached as Annex A), the conditions appendix (a copy of which is attached as Annex B), the expenses reimbursement agreement (a copy of which is attached as Annex C), the Eaton special meeting and the Cooper special meetings. You should read this information carefully and in its entirety. The enclosed voting materials allow you to vote your shares without attending the applicable special meeting by granting a proxy or voting your shares by mail, telephone or over the Internet.

| Q: | When and where will the Eaton and Cooper special meetings be held? |

| A: | The Eaton special meeting will be held at Eaton Center, 1111 Superior Avenue, Cleveland, Ohio 44114, on October 26, 2012, at 3:00 p.m., local time. |

The Cooper special court-ordered meeting will be convened at the Chase Tower in the 54th Floor conference room, located at 600 Travis Street, Houston, Texas 77002, on October 26, 2012, at 11:00 a.m., local time.

The Cooper EGM will be convened at the Chase Tower in the 54th Floor conference room, located at 600 Travis Street, Houston, Texas 77002, on October 26, 2012, at 11:10 a.m., local time or, if later, as soon as possible after the conclusion or adjournment of the Cooper special court-ordered meeting.

| Q: | What will the Eaton shareholders receive as consideration in the transaction? |

| A: | Upon the effective time of the merger, each Eaton common share issued and outstanding immediately prior to the merger will be cancelled and will automatically be converted into the right to receive one New Eaton ordinary share. The one-for-one exchange ratio is fixed, and, as a result, the number of New Eaton ordinary shares received by the Eaton shareholders in the transaction will not fluctuate up or down based on the market price of the Eaton common shares or the Cooper ordinary shares prior to the transaction. It is expected that the New Eaton ordinary shares will be listed on the NYSE under the symbol “ETN.” Following the consummation of the transaction, the Eaton common shares will be delisted from the NYSE and the Chicago Stock Exchange. |

Since Irish law does not recognize fractional shares held of record, New Eaton will not issue any fractions of New Eaton ordinary shares to Eaton shareholders in the transaction. Instead, the total number of New Eaton ordinary shares that any Eaton shareholder would have been entitled to receive will be rounded down to the nearest whole number and all entitlements to fractional New Eaton ordinary shares will be aggregated and sold by the exchange agent, with any sale proceeds being distributed in cash pro rata to the Eaton shareholders whose fractional entitlements have been sold.

| Q: | What will the Cooper shareholders receive as consideration in the transaction? |

| A: | Upon the completion of the transaction, the holder of each Cooper ordinary share issued and outstanding immediately prior to completion of the acquisition (other than Eaton or any Eaton affiliate) will obtain the right to receive from New Eaton (i) $39.15 in cash and (ii) 0.77479 of a New Eaton ordinary share, which, collectively, is referred to in this joint proxy statement/prospectus as the “scheme consideration.” |

Since Irish law does not recognize fractional shares held of record, New Eaton will not issue any fractions of New Eaton ordinary shares to Cooper shareholders in the transaction. Instead, the total number of New Eaton ordinary shares that any Cooper shareholder would have been entitled to receive will be rounded down to the nearest whole number and all entitlements to fractional New Eaton ordinary shares will be aggregated and sold by the exchange agent, with any sale proceeds being distributed in cash pro rata to the Cooper shareholders whose fractional entitlements have been sold.

2

Table of Contents

Following the consummation of the transaction, Cooper ordinary shares will be delisted from the NYSE.

All Cooper treasury shares will be cancelled immediately prior to the scheme becoming effective, and no scheme consideration will be received in respect of such shares.

| Q: | What proposals are being voted on at the Eaton special meeting and what shareholder vote is required to adopt those proposals? |

| A: | (1)Proposal to adopt the transaction agreement and approve the merger: The affirmative vote of holders of two-thirds (2/3) of the Eaton common shares outstanding on the record date. |

(2) Proposal to reduce the share premium of New Eaton to allow the creation of distributable reserves: The affirmative vote of holders of a majority of Eaton common shares outstanding on the record date.

(3) Proposal to consider and vote upon, on a non-binding advisory basis, specified compensatory arrangements between Eaton and its named executive officers: The affirmative vote of holders of a majority of Eaton common shares outstanding on the record date. This proposal is advisory and therefore not binding on the Eaton board of directors.

Abstentions, failures to vote and broker non-votes will have the same effect as a vote against proposals 1, 2 and 3.

(4) Proposal to adjourn the Eaton special meeting, or any adjournments thereof, (i) to solicit additional proxies if there are insufficient votes at the time of the special meeting to adopt the transaction agreement and approve the merger, (ii) to provide to the Eaton shareholders in advance of the special meeting any supplement or amendment to the joint proxy statement/prospectus or (iii) to disseminate any other information which is material to the Eaton shareholders voting at the special meeting, referred to as the “Eaton adjournment proposal”: The affirmative vote of holders of a majority of the Eaton voting shares represented, in person or by proxy, at the special meeting, is required for the approval of the Eaton adjournment proposal.

Abstentions and shares held in “street name” by brokers that are voted on proposals 1, 2 or 3, but not on proposal 4, will have the same effect as a vote against proposal 4.

The merger and the acquisition are not conditioned on approval of proposals 2, 3 or 4 described above.

As of the record date, directors and executive officers of Eaton and their affiliates owned and were entitled to vote 1,645,018 Eaton common shares, representing approximately 0.49% percent of the Eaton common shares outstanding on that date.

| Q: | What proposals are being voted on at the Cooper special meetings and what shareholder vote is required to adopt those proposals? |

| A: | Cooper Special Court-Ordered Meeting |

Cooper shareholders are being asked to vote on a proposal to approve the scheme at both the Cooper special court-ordered meeting and at the Cooper EGM. The vote required for such proposal is different at each of the meetings, however. As set out in full under the section entitled “Part 2—Explanatory Statement—Consents and Meetings,” the approval required at the special court-ordered meeting is a majority in number of the Cooper shareholders of record casting votes on the proposal representing three-fourths (75 percent) or more in value of the Cooper ordinary shares held by such holders, present and voting either in person or by proxy.

Because the vote required to approve the proposal at the Cooper special court-ordered meeting is based on votes properly cast at the meeting, and because abstentions and broker non-votes are not considered votes properly cast, abstentions and broker non-votes, along with failures to vote, will have no effect on such proposal.

The merger and the acquisition are conditioned on approval of the scheme at the Cooper special court-ordered meeting.

3

Table of Contents

Cooper Extraordinary General Meeting

Set forth below is a table summarizing certain information with respect to the EGM Resolutions:

EGM | Resolution | Ordinary | Transaction | |||

| 1 | Approve the scheme of arrangement and authorize the directors of Cooper to take all such actions as they consider necessary or appropriate for carrying the scheme of arrangement into effect. | Ordinary | Yes | |||

| 2 | Approve the cancellation of any Cooper ordinary shares in issue before 10:00 p.m., Irish time, on the day before the Irish High Court hearing to sanction the scheme. | Special | Yes | |||

| 3 | Authorize the directors of Cooper to allot and issue new Cooper shares, fully paid up, to New Eaton in connection with effecting the scheme. | Ordinary | Yes | |||

| 4 | Amend the articles of association of Cooper so that any ordinary shares of Cooper that are issued at or after 10:00 p.m., Irish time, on the last business day before the scheme becomes effective are acquired by New Eaton for the scheme consideration. | Special | Yes | |||

| 5 | Approve the reduction of the share premium of New Eaton resulting from (i) the issuance of New Eaton shares pursuant to the scheme and (ii) a subscription for New Eaton shares by Eaton Sub prior to the merger, in order to create distributable reserves of New Eaton. | Ordinary | No | |||

| 6 | Approve, on a non-binding advisory basis, specified compensatory arrangements between Cooper and its named executive officers relating to the transaction. | Ordinary | No | |||

| 7 | Adjourn the Cooper EGM, or any adjournments thereof, to solicit additional proxies if there are insufficient proxies at the time of the EGM to approve the scheme of arrangement or resolutions 2 through 6. This resolution is referred to as the “Cooper EGM adjournment proposal.” | Ordinary | No | |||

At the Cooper EGM, the requisite approval of each of the EGM resolutions depends on whether it is an “ordinary resolution” (EGM resolutions 1, 3, 5, 6 and 7), which requires the approval of the holders of at least a majority of the votes cast by the holders of Cooper ordinary shares present and voting, either in person or by proxy, or a “special resolution” (EGM resolutions 2 and 4), which requires the approval of the holders of at least 75 percent of the votes cast by the holders of Cooper ordinary shares present and voting, either in person or by proxy.

For all the EGM resolutions, because the votes required to approve such resolutions are based on votes properly cast at the meeting, and because abstentions and broker non-votes are not considered votes properly cast, abstentions and broker non-votes, along with failures to vote, will have no effect on the EGM resolutions.

As of the Cooper record date, the Cooper directors and executive officers had the right to vote approximately 0.35% of the Cooper ordinary shares then outstanding and entitled to vote at the special court-ordered meeting and the EGM. It is expected that Cooper’s directors and executive officers will vote “FOR” each of the proposals at the special court-ordered meeting and at the EGM.

4

Table of Contents

| Q: | Why are there two Cooper special meetings? |

| A: | Irish law requires that two separate shareholder meetings be held, the special court-ordered meeting and the EGM. Both meetings are necessary to cause the scheme of arrangement to become effective. At the special court-ordered meeting, Cooper shareholders (other than Eaton or any of its affiliates) will be asked to approve the scheme. At the EGM, Cooper shareholders will also be asked to approve related matters. For more detail on these matters, see “The Special Meetings of Cooper’s Shareholders.” |

| Q: | What constitutes a quorum? |

| A: | Eaton: The shareholders present in person or by proxy at any meeting of shareholders will constitute a quorum for a meeting, but no action required by law or the Eaton articles of incorporation or regulations to be authorized or taken by the holders of a designated proportion of the shares of a class may be authorized or taken by a lesser proportion. Eaton’s inspector of election intends to treat as “present” for these purposes shareholders who have submitted properly executed or transmitted proxies that are marked “abstain.” The inspector will also treat as “present” shares held in “street name” by brokers that are voted on at least one proposal to come before the meeting. |

Cooper: The holders of Cooper ordinary shares outstanding entitling them to exercise a majority of the voting power of Cooper on the Cooper record date will constitute a quorum for a meeting. Cooper’s inspector of election intends to treat as “present” for these purposes shareholders who have submitted properly executed or transmitted proxies that are marked “abstain.” The inspector will also treat as “present” shares held in “street name” by brokers that are voted on at least one proposal to come before the meeting.

| Q: | Why am I being asked to approve the distributable reserves proposal? |

| A: | Under Irish law, dividends may only be paid (and share repurchases and redemptions must generally be funded) out of “distributable reserves,” which New Eaton will not have immediately following the completion of the transaction. Please see “Creation of Distributable Reserves of New Eaton” beginning on page 150. Shareholders of Eaton and Cooper are also being asked at their respective special meetings to approve the creation of distributable reserves of New Eaton (through the reduction of the share premium account of New Eaton), in order to permit New Eaton to be able to pay dividends (and repurchase or redeem shares) after the transaction. |

The approval of the distributable reserves proposal is not a condition to the consummation of the transaction. Accordingly, if shareholders of Eaton approve the transaction agreement, and shareholders of Cooper approve the scheme and resolutions 1, 2, 3 and 4 to be proposed at the EGM, but shareholders of Eaton and/or Cooper do not approve the distributable reserves proposal, and the transaction is consummated, New Eaton may not have sufficient distributable reserves to pay dividends (or to repurchase or redeem shares) following the transaction. In addition, the creation of distributable reserves of New Eaton requires the approval of the Irish High Court. Although New Eaton is not aware of any reason why the Irish High Court would not approve the creation of distributable reserves, the issuance of the required order is a matter for the discretion of the Irish High Court. Please see “Risk Factors” beginning on page 28 and “Creation of Distributable Reserves of New Eaton” beginning on page 150.

| Q: | What are the recommendations of the Eaton and Cooper boards of directors regarding the proposals being put to a vote at their respective special meetings? |

| A: | The Eaton board of directors has unanimously approved the transaction agreement and determined that the terms of the acquisition will further the strategies and goals of Eaton. |

The Eaton board of directors unanimously recommends that Eaton shareholders vote:

| • | “FOR” the proposal to adopt the transaction agreement and approve the merger; |

| • | “FOR” the proposal to reduce the capital of New Eaton to allow the creation of distributable reserves; |

5

Table of Contents

| • | “FOR” the proposal to approve, on a non-binding, advisory basis, specified compensatory arrangements between Eaton and its named executive officers; and |

| • | “FOR” the Eaton adjournment proposal. |

See “The Transaction—Recommendation of the Eaton Board of Directors and Eaton’s Reasons for the Transaction” beginning on page 62.

In considering the recommendation of the board of directors of Eaton, you should be aware that certain directors and executive officers of Eaton will have interests in the proposed transaction in addition to interests they might have as shareholders. See “The Transaction—Interests of Certain Persons in the Transaction—Eaton” beginning on page 92.

The Cooper board of directors has unanimously approved the transaction agreement and determined that the transaction agreement and the transactions contemplated by the transaction agreement, including the scheme, are fair to and in the best interests of Cooper and its shareholders and that the terms of the scheme are fair and reasonable.

The Cooper board of directors unanimously recommends that Cooper shareholders vote:

| • | “FOR” the scheme of arrangement at the special court-ordered meeting; |

| • | “FOR” the scheme of arrangement at the EGM; |

| • | “FOR” the cancellation of any Cooper ordinary shares in issue before 10:00 p.m., Irish time, on the day before the Irish High Court hearing to sanction the scheme; |

| • | “FOR” the authorization of the directors of Cooper to allot and issue new Cooper shares, fully paid up, to New Eaton in connection with effecting the scheme; |

| • | “FOR” amendment of the articles of association of Cooper so that any ordinary shares of Cooper that are issued at or after 10:00 p.m., Irish time on the last business day before the scheme becomes effective are acquired by New Eaton for the scheme consideration; |

| • | “FOR” the reduction of the share premium of New Eaton resulting from (i) the issuance of New Eaton shares pursuant to the scheme and (ii) a subscription for New Eaton shares by Eaton Sub prior to the merger, in order to create distributable reserves of New Eaton; |

| • | “FOR” the approval, on a non-binding, advisory basis of specified compensatory arrangements between Cooper and its named executive officers; and |

| • | “FOR” the Cooper EGM adjournment proposal. |

See “The Transaction—Recommendation of the Cooper Board of Directors and Cooper’s Reasons for the Transaction” beginning on page 65.

In considering the recommendation of the board of directors of Cooper, you should be aware that certain directors and executive officers of Cooper will have interests in the proposed transaction in addition to interests they might have as shareholders. See “The Transaction—Interests of Certain Persons in the Transaction—Cooper” beginning on page 94.

| Q: | When is the transaction expected to be completed? |

| A: | As of the date of this joint proxy statement/prospectus, the transaction is expected to be completed in the second half of 2012. However, no assurance can be provided as to when or if the transaction will be completed. The required vote of Eaton and Cooper shareholders to adopt the required shareholder proposals at their respective special meetings, as well as the necessary regulatory consents and approvals, must first be obtained and other conditions specified in the conditions appendix must be satisfied or, to the extent applicable, waived. |

6

Table of Contents

| Q: | Why will the place of incorporation of New Eaton be Ireland? |

| A: | Eaton decided that New Eaton would be incorporated in Ireland, given: |

| • | The transaction was not economically feasible without incorporation outside the United States because of material competitive advantages currently enjoyed by Cooper as a result of its non-United States incorporation. Amongst these advantages are greater flexibility and lower cost of cash management, an enhanced ability to grow faster through organic growth and acquisitions, as well as a lower worldwide effective tax rate. Loss of these existing Cooper competitive advantages would have caused a large dis-synergy that would have prevented the acquisition from occurring; |

| • | Cooper is incorporated in Ireland and, as such, the simplest transaction was to also incorporate New Eaton in Ireland; |

| • | Incorporating New Eaton in Ireland will result in significantly enhanced global cash management and flexibility and associated financial benefits to the combined enterprise. These benefits include increased global liquidity and free global cash flow among the various entities of the combined enterprise without negative tax effects. In addition, the Irish rules surrounding the taxation of controlled foreign corporations are much more typical of the rules found in most developed countries compared to the rules found in the United States that are competitively adverse. As an example, the Irish rules surrounding controlled foreign corporations allow a number of active inter-company business operations to occur without negative tax effect. Because of these benefits, we expect that New Eaton will be able to operate its businesses more easily and at lower cost, and also will have a lower worldwide effective tax rate than it would have otherwise; |

| • | Ireland is a beneficial location considering Eaton’s and Cooper’s presence in markets outside the United States, particularly in Europe; and |

| • | Ireland enjoys strong relationships as a member of the European Union, and has a long history of international investment and a good network of commercial, tax, and other treaties with the United States, the European Union and many other countries where both Cooper and Eaton have major operations. |

| Q: | Who is entitled to vote? |

| A: | Eaton: The board of directors of Eaton has fixed a record date of September 13, 2012 as the Eaton record date. If you were an Eaton shareholder of record as of the close of business on the Eaton record date, you are entitled to receive notice of and to vote at the Eaton special meeting and any adjournments thereof. |

Cooper: The board of directors of Cooper has fixed a record date of September 13, 2012 as the Cooper record date. If you were a Cooper shareholder of record as of 11:59 p.m. (Eastern Time in the U.S.) on the Cooper record date, you are entitled to receive notice of and to vote at the Cooper special meetings and any adjournments thereof.

| Q: | What if I sell my Eaton common shares before the Eaton special meeting or my Cooper ordinary shares before the Cooper special meetings? |

Eaton:The Eaton record date is earlier than the date of the Eaton special meeting and the date that the transaction is expected to be completed. If you transfer your shares after the Eaton record date but before the Eaton special meeting, you will retain your right to vote at the Eaton special meeting, but will have transferred the right to receive New Eaton ordinary shares pursuant to the transaction. In order to receive the New Eaton ordinary shares, you must hold your shares through completion of the transaction.

Cooper:The Cooper record date is also earlier than the date of the Cooper special meetings and the date that the transaction is expected to be completed. If you transfer your shares after the Cooper record date but before the Cooper special meetings, you will retain your right to vote at the Cooper special meetings, but will have transferred the right to receive the scheme consideration. In order to receive the scheme consideration, you must hold your shares through completion of the transaction.

7

Table of Contents

| Q: | How do I vote? |

| A: | Eaton: If you are an Eaton shareholder of record, you may vote your shares at the Eaton special meeting in one of the following ways: |

| • | by mailing your completed and signed proxy card in the enclosed return envelope; |

| • | by voting by telephone or over the Internet as instructed on the enclosed proxy card; or |

| • | by attending the Eaton special meeting and voting in person. |

If you hold your shares through a bank, broker or other nominee, you should follow the instructions provided by your bank, broker or other nominee in order to instruct them on how to vote such shares.

Cooper: If you are a Cooper shareholder of record, you may vote your shares at the Cooper special meetings in one of the following ways:

| • | by mailing your applicable completed and signed proxy card in the enclosed return envelope; |

| • | by voting by telephone or over the Internet as instructed on the applicable enclosed proxy card; or |

| • | by attending the applicable Cooper special meeting and voting in person. |

If you are a Cooper shareholder of record, the shares listed on your proxy card will include the following shares, if applicable:

| • | shares held in the Cooper Dividend Reinvestment and Stock Purchase Plan; |

| • | shares held in custody for your account by State Street Bank, as Trustee of the Cooper Industries Retirement Savings and Stock Ownership Plan (“CO-SAV”); |

| • | shares held in custody for your account by Fidelity Management Trust Company, as Trustee of the Apex Tool 401(k) Savings Plan (“Apex Savings Plan”); and |

| • | shares held in a book-entry account at Computershare Trust Company, N.A., Cooper’s transfer agent. |

If you hold your shares through a bank, broker or other nominee, you should follow the instructions provided by your bank, broker or other nominee in order to instruct them on how to vote such shares.

| Q: | If I hold Cooper shares through CO-SAV, will the trustee vote my shares for me? |

| A: | Yes. If you hold Cooper shares through CO-SAV, you should instruct State Street Bank, as trustee of CO-SAV, how to vote your shares by marking the appropriate boxes on the relevant proxy card. Even if you do not provide proper instructions to the trustee of CO-SAV, however, the trustee will still vote your shares held through CO-SAV. If you do not provide proper instructions, then the trustee will vote your shares in your CO-SAV account in proportion to the way the other CO-SAV participants voted their shares. The trustee will also vote Cooper ordinary shares not yet allocated to participants’ accounts in proportion to the way that CO-SAV participants voted their shares. Therefore, whether or not you provide instructions to the trustee, your Cooper shares in your CO-SAV account will be treated as “present” at the Cooper special meetings for purposes of determining a quorum. |

| Q: | If my shares are held in “street name” by my bank, broker or other nominee will my bank, broker or other nominee automatically vote my shares for me? |

| A: | No. Your bank, broker or other nominee will not vote your shares if you do not provide your bank, broker or other nominee with a signed voting instruction form with respect to your shares, such failure to vote being referred to as a “broker non-vote.” Therefore, you should instruct your bank, broker or other nominee to vote your shares by following the directions your bank, broker or other nominee provides. |

8

Table of Contents

Brokers do not have discretionary authority to vote on any of the Eaton proposals or on any of the Cooper proposals.

Please see “The Special Meeting of Eaton’s Shareholders—Voting Shares Held in Street Name” beginning on page 46 and “The Special Meetings of Cooper’s Shareholders—Voting Ordinary Shares Held in Street Name” beginning on page 52.

| Q: | How many votes do I have? |

| A: | Eaton: You are entitled to one vote for each Eaton common share that you owned as of the close of business on the Eaton record date. As of the close of business on the Eaton record date, 337,933,300 Eaton common shares were outstanding and entitled to vote at the special meeting. |

Cooper: You are entitled to one vote for each Cooper ordinary share that you owned as of the close of business on the Cooper record date. As of 11:59 p.m. (Eastern Time in the U.S.) on the Cooper record date, 161,489,215 Cooper ordinary shares were outstanding and entitled to vote at the special court-ordered meeting and at the EGM.

| Q: | What if I hold shares in both Eaton and Cooper? |

| A: | If you are a shareholder of both Eaton and Cooper, you will receive two separate packages of proxy materials. A vote as an Eaton shareholder for the proposal to adopt the transaction agreement will not constitute a vote as a Cooper shareholder for the proposal to approve the scheme of arrangement, or vice versa.THEREFORE, PLEASE MARK, SIGN, DATE AND RETURN ALL PROXY CARDS THAT YOU RECEIVE, WHETHER FROM EATON OR COOPER, OR SUBMIT A SEPARATE PROXY AS BOTH AN EATON AND A COOPER SHAREHOLDER FOR EACH SPECIAL MEETING, OVER THE INTERNET OR BY TELEPHONE. |

| Q: | Should I send in my stock certificates now? |