UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

__________________________________

FORM 10-K

__________________________________

(Mark One)

|

| |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2015

OR

|

| |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File No. 001-32594

______________________________________________

HEARTLAND PAYMENT SYSTEMS, INC.

(Exact name of registrant as specified in its charter)

|

| | |

| Delaware | | 22-3755714 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification Number) |

90 Nassau Street, Princeton, New Jersey 08542

(Address of principal executive offices) (Zip Code)

(609) 683-3831

(Registrant’s telephone number, including area code)

____________________________________________________________

Securities registered pursuant to 12(b) of the Act:

|

| | |

| Title of each class | | Name of each exchange on which registered |

| Common Stock, $0.001 par value | | New York Stock Exchange |

| Securities registered pursuant to 12(g) of the Act: |

| | (NONE) | |

| | (title of Class) | |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. x YES o NO

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. o YES x NO

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x YES o NO

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). x YES o NO

Indicate by check mark if disclosure of delinquent filer pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one): |

| | | | | | |

| Large accelerated filer | | x | | Accelerated filer | | o |

| | | | | | | |

| Non-accelerated filer | | o (Do not check if a smaller reporting company) | | Smaller reporting company | | o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). o YES x NO

The aggregate market value of the voting and non-voting common stock held by non-affiliates computed by reference to the price at which the common stock was last sold on the New York Stock Exchange on June 30, 2015 was approximately $1.5 billion.

As of February 24, 2016, there were 36,996,676 shares of the registrant’s Common Stock, $0.001 par value, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Specifically identified portions of the registrant's definitive proxy statement to be filed with the Securities and Exchange Commission pursuant to Regulation 14A in connection with the 2016 annual meeting of shareholders are incorporated by reference into Part III of this Annual Report on Form 10-K for fiscal year ended December 31, 2015.

Heartland Payment Systems, Inc.

Annual Report on Form 10-K

For the Year Ended December 31, 2015

TABLE OF CONTENTS

|

| | |

| | | Page |

| | | |

| Item 1. | | |

| Item 1A. | | |

| Item 1B. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | MINE SAFETY DISCLOSURES | |

| | | |

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| Item 9. | | |

| Item 9A. | | |

| Item 9B. | | |

| | | |

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

| | | |

| Item 15. | | |

| | | |

| |

FORWARD LOOKING STATEMENTS

Unless the context requires otherwise, references in this Annual Report on Form 10-K to “the Company,” “we,” “us,” and “our” refer to Heartland Payment Systems, Inc. and its subsidiaries.

Some of the information in this report may contain forward-looking statements that are based on our management's beliefs and assumptions and on information currently available to our management. Forward-looking statements include the information concerning our possible or assumed future results of operations, financial condition and prospects, business strategies, financing plans, competitive position, industry environment, potential growth opportunities, the effects of future regulation and the effects of competition. Forward-looking statements include all statements that are not historical facts and can be identified by the use of forward-looking terminology such as the words “anticipate,” “believe,” "estimate," “expect,” “intend,” “plan,” "predict," "will be," "will continue" or similar expressions.

Forward-looking statements involve risks, uncertainties and assumptions. Actual results may differ materially from those expressed in the forward-looking statements. You should understand that many important factors, in addition to those discussed elsewhere in this report, could cause our results to differ materially from those expressed in the forward-looking statements. Certain of these factors are described in Item 1A. Risk Factors in this Annual Report on Form 10-K and include, without limitation, the risk that our proposed merger with Global Payments Inc. may not be consummated, on a timely basis and on the expected terms or at all, changes in the price of Global Payments common stock prior to the consummation of the merger, the ability to realize the anticipated benefits of the proposed merger, on the expected timeline or at all, the effect of the pending merger on our business, financial results, operations, and relationships with customers, vendors, and employees, unauthorized disclosure of user data through breaches of our computer systems or otherwise, our failure to comply with the applicable requirements of the Visa and MasterCard bankcard networks, our competitive environment, the business cycles and credit risks of our merchants, chargeback liability, merchant attrition, reliance on and problems with our sponsor banks, our relationships with third-party bankcard payment processors, our inability to pass increased interchange fees, assessments, and transaction fees along to our merchants, economic conditions, systems failures and government regulation.

PART I.

ITEM 1. BUSINESS

Overview of Our Company

Heartland Payment Systems, Inc.

90 Nassau Street, Princeton, NJ 08542

(609) 683-3831

Our primary business is to provide Payment Processing services to merchants throughout the United States. This involves providing end-to-end electronic payment processing services to merchants by facilitating the exchange of information and funds between them and cardholders' financial institutions. To accomplish this, we undertake merchant set-up and training, transaction authorization and electronic draft capture, clearing and settlement, merchant accounting, merchant assistance and support, and risk management. We also sell and rent point-of-sale ("POS") devices. Our card-accepting customers primarily fall into two categories: small and mid-sized merchants (referred to as "Small and Midsized Enterprises," or “SME merchants”) and Network Services merchants, which are predominantly petroleum industry merchants of all sizes (referred to as “Network Services merchants”).

We provide additional services in our other business segments such as:

| |

| • | Integrated commerce solutions, payment processing, higher education loan services and open and closed-loop payment solutions to higher-education institutions through Campus Solutions, |

| |

| • | School nutrition, POS solutions, and associated payment solutions, including online prepayment solutions, to kindergarten through 12th grade ("K-12") schools through Heartland School Solutions, |

| |

| • | Full-service payroll processing and related tax filing services throughout the United States provided by Heartland Payroll Solutions, and |

| |

| • | Other, including (1) integrated payments solutions for small ticket merchants throughout the United States and Canada provided by Micropayments, (2) POS solutions and other adjacent business service applications provided by Heartland Commerce, and (3) marketing solutions including loyalty and gift cards which we provide through Heartland Marketing Solutions. |

We were incorporated in June 2000, in the state of Delaware. As of December 31, 2015, we employed 4,272 full- and part-time personnel, including 1,460 sales professionals, 730 customer service, risk management, financial and operations support and underwriting employees, 431 systems and technology employees, 457 Heartland Payroll Solutions employees, 230 Heartland School Solutions employees, 434 Campus Solutions employees, 39 Micropayments employees, 229 accounting and administration employees, and 262 Heartland Commerce employees. Our sales professionals include 1,069 Relationship Managers and Territory Managers and 171 Senior Product Advisors, primarily payroll specialists. None of our employees were represented by a labor union, and we have experienced no work stoppages. We consider our employee relations to be good.

Agreement and Plan of Merger

On December 15, 2015, we entered into an Agreement and Plan of Merger (the “Merger Agreement”) with Global Payments Inc., a Georgia corporation (“Global”), Data Merger Sub One, Inc., a Delaware corporation and wholly owned subsidiary of Global (“Merger Sub One”) and Data Merger Sub Two, LLC, a Delaware limited liability company and wholly owned subsidiary of Global (“Merger Sub Two”, and together with Merger Sub One, the “Merger Subs”).

Pursuant to the terms and subject to the conditions set forth in the Merger Agreement, Global will acquire the Company in a two-step transaction. First, Merger Sub One will merge with and into the Company, with the Company continuing as a wholly owned subsidiary of Global. Second, the Company will merge with and into Merger Sub Two immediately following the initial merger, with Merger Sub Two surviving the second merger as a wholly owned subsidiary of Global.

As a result of the merger, subject to the terms and conditions of the Merger Agreement, each outstanding share of our common stock (other than certain shares owned by the parties to the Merger Agreement or by stockholders who have validly exercised their appraisal rights) will be converted into the right to receive (subject to adjustment as set forth in the next sentence) $53.28 in cash, without interest, and 0.6687 shares of Global common stock. Under the terms of the Merger Agreement, in the event that the number of shares of Global common stock issuable as a result of the merger would exceed 19.9% of the issued and outstanding shares of Global common stock immediately prior to the closing of the merger, the stock consideration will be reduced so that no more than 19.9% of the outstanding shares of Global common stock will be issuable in

the merger and the cash consideration will be increased by a corresponding amount, so that the value of the per share merger consideration will remain the same.

Consummation of the merger is subject to customary conditions, including without limitation, (1) approval by the holders of at least a majority of the outstanding shares of the Company’s common stock, (2) the absence of any law or order of any governmental entity which prohibits the consummation of the merger, (3) the effectiveness under the Securities Act of 1933 (as amended) of the Registration Statement on Form S-4 filed by Global with respect to the merger, and (4) subject to certain materiality exceptions, the accuracy of the representations and warranties made by the parties and compliance by the parties with their respective obligations under the Merger Agreement.

Each of the Company and Global has made customary representations and warranties in the Merger Agreement. The Merger Agreement also contains customary covenants, including, without limitation, (1) covenants providing for the parties to use reasonable best efforts to cause the closing of the merger to be consummated, and (2) the Company’s agreement to not solicit proposals relating to alternative transactions to the merger or engage in discussions or negotiations with respect thereto, subject to certain exceptions. Additionally, the parties have agreed to select two Company nominees for appointment to Global’s board of directors in connection with the closing of the merger.

The Merger Agreement contains certain termination rights for Global and the Company, including a mutual termination right in the event the merger is not consummated by June 15, 2016 (subject to extension under certain circumstances). Upon termination of the Merger Agreement under specified circumstances described in the Merger Agreement, including (1) if Global terminates the Merger Agreement following a change of recommendation of the Company’s board of directors, (2) if the Company terminates the Merger Agreement to enter into a definitive agreement with a third party with respect to a superior acquisition proposal, or (3) if the Merger Agreement is terminated under certain circumstances and the Company subsequently enters into, or consummates, an alternative acquisition proposal within 12 months, the Company will be required to pay Global a termination fee of $153,000,000.

Certain terms of the Merger Agreement are summarized in, and the Merger Agreement has been filed as an exhibit to the Current Report on Form 8-K filed by the Company on December 17, 2015.

General Business Developments

Acquisitions

Campus Solutions

On September 4, 2014, we completed the acquisition of TouchNet Information Systems, Inc. (“TouchNet”), an integrated commerce solutions provider to higher-education institutions for a cash payment of $375 million, less a net working capital deficit, for all outstanding common shares. The purchase was funded primarily with a new five year, $375 million secured term loan. See “Management's Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources — Credit Facilities,” for further discussion. TouchNet added over 600 higher education institutions serving more than 6 million students, nearly one-third of the higher education enrollment in the United States, to our Campus Solutions business.

Heartland School Solutions

On April 1, 2014, we purchased the net assets of MCS Software Corporation ("MCS Software") for a $17.3 million cash payment. The purchase price was funded from a combination of operating cash and financing under our revolving credit facility. This acquisition further expanded our market-leading position in the K-12 school nutrition and POS technology industry.

Heartland Payroll Solutions

On February 27, 2015, we purchased the stock of Payroll 1, Inc. ("Payroll 1") for a $30.0 million cash payment, plus net working capital. The purchase price was financed under our 2014 Revolving Credit Facility. The acquisition of Payroll 1 expanded our existing payroll processing business and customer base by adding 6,573 customers at acquisition.

Heartland Commerce

Heartland Commerce provides a comprehensive suite of POS solutions and is comprised primarily of the following businesses acquired since February 2014:

On October 30, 2015, we acquired the stock of Menusoft Systems Corporation (a.k.a. “Digital Dining”) for a cash payment of $18.7 million. The purchase was funded from a combination of operating cash and financing under the 2014 Revolving Credit Facility. Digital Dining offers restaurants the convenience of a handheld POS on an iPhone, iPod and iPad in a hybrid environment with conventional fixed terminals, and is also used by restaurateurs for table management, delivery, reservations, labor scheduling, inventory and loyalty programs.

On February 11, 2015, we acquired the stock of Dinerware, Inc. ("Dinerware") for a cash payment of $15.0 million. The purchase was funded from a combination of operating cash and financing under the 2014 Revolving Credit Facility. Dinerware provides restaurant POS software solutions to the hospitality industry and POS systems to enhance the operations of a wide range of food service establishments.

On January 30, 2015, we acquired the net assets of Automation Inc. ("pcAmerica") for a cash payment of $15.0 million. The purchase was funded from a combination of operating cash and financing under the 2014 Revolving Credit Facility. PcAmerica delivers POS systems to streamline daily operations, including customer transactions, inventory tracking, employee labor, and marketing reports to meet the evolving needs of retail stores and restaurants.

On October 31, 2014, we acquired the net assets of Xpient Solutions, LLC (“Xpient”) for a cash payment of $30.0 million, plus net working capital. The purchase price was funded from a combination of operating cash and financing under our revolving credit facility. Xpient provides POS software solutions to customers primarily in the food service industry.

On February 15, 2014, we purchased the net assets of Merchant Software Corporation ("Liquor POS") for a $3.3 million cash payment. The purchase price was funded from operating cash flows. Liquor POS is a leading provider of POS systems to the liquor retail vertical serving more than 3,400 merchants.

Business Segment Overview

Payment Processing

Performance Update

At December 31, 2015, we provided our card payment processing services to 182,526 active SME merchants located across the United States. This compares to 169,831 active SME merchants at December 31, 2014. At December 31, 2015, we provided card payment processing services to approximately 3,194 Network Services merchants with approximately 43,987 locations, compared to 2,181 Network Services merchants with 42,397 locations at December 31, 2014.

Our total card processing volume for the year ended December 31, 2015 was $117.4 billion, a 6.8% increase from the $109.9 billion processed during the year ended December 31, 2014. Our SME card processing volume for the year ended December 31, 2015 was $93.1 billion, a 14.8% increase over $81.1 billion in 2014. Total card processing volume for 2015 also included $24.3 billion of settled volume for Network Services merchants, compared to $28.8 billion for 2014.

In addition to settling card transactions, Network Services processes a wide range of payment transactions for its predominantly petroleum customer base, including providing 2.4 billion transaction authorizations (primarily for Visa and MasterCard) through its front-end card processing systems in 2015.

According to The Nilson Report, in 2014 we were the 5th largest merchant acquirer in the United States ranked by transaction count and the 9th largest merchant acquirer by processed dollar volume, which consisted of Visa and MasterCard credit and debit cards, as well as other credit cards such as American Express, Discover, Diners Club, Carte Blanche, UnionPay, etc. These rankings represented 3.8 billion transactions and 2.9% of the total U.S. bankcard processed dollar volume.

The following table summarizes revenue, net revenue (which we define as total revenue less interchange fees and dues, assessments and fees) and operating income for our Payment Processing segment for the years ended December 31, 2015, 2014 and 2013:

|

| | | | | | | | | | | | |

| | | Year Ended December 31, |

| | | 2015 | | 2014 | | 2013 |

| | | (In thousands) |

| Revenue | | $ | 2,371,878 |

| | $ | 2,111,487 |

| | $ | 1,979,579 |

|

| Net revenue | | 518,313 |

| | 472,731 |

| | 443,189 |

|

| Operating income | | 119,312 |

| | 127,553 |

| | 138,226 |

|

Business Structure

Our Payment Processing revenue from SME merchants and Network Services merchants is recurring in nature. We typically enter into three-year service contracts with our SME merchants and three-to-five-year agreements with Network Services merchants.

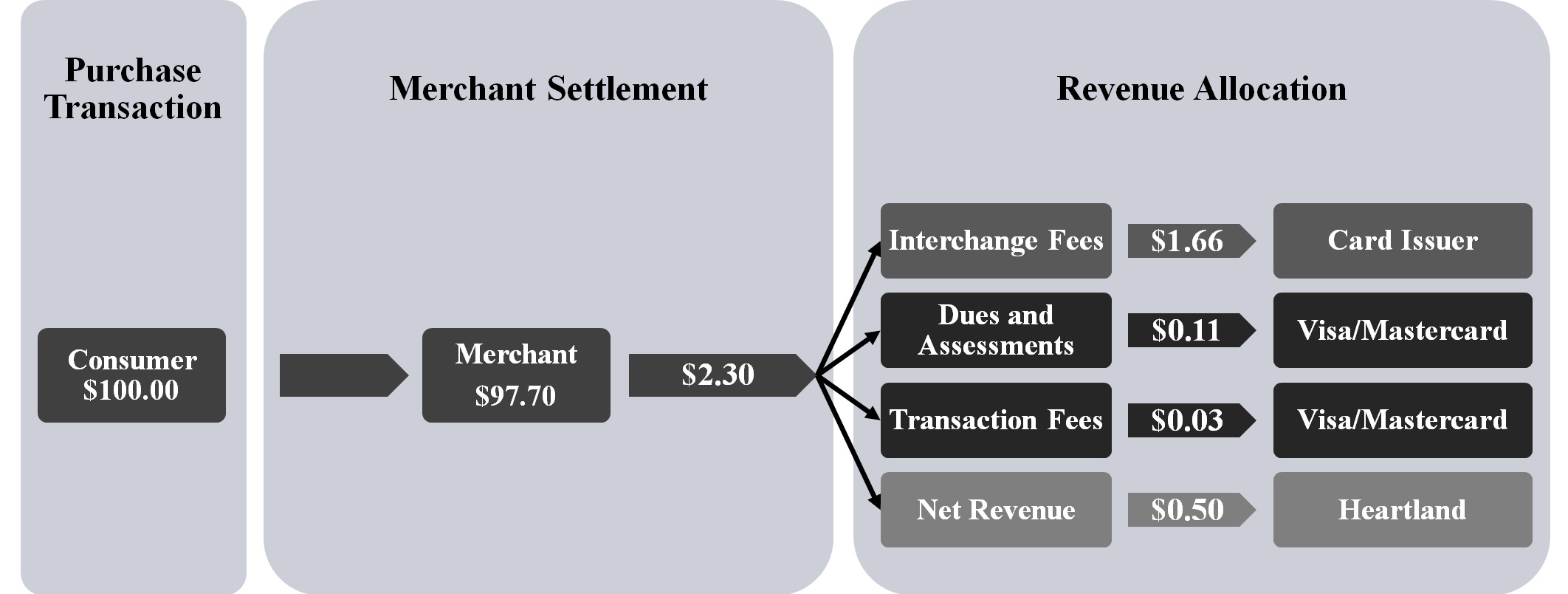

Most of our SME revenue is from fees for processing transactions, which are primarily a combination of a percentage of the dollar amount of each card transaction we process, a flat fee per transaction and monthly fees for services. We make mandatory payments of interchange fees to card issuing banks through card networks and dues, assessments and transaction authorization fees to Visa, MasterCard and Discover, and we retain the remainder as net revenue. For example, in a transaction using a Visa or MasterCard card, the allocation of funds resulting from a $100 transaction follows.

In contrast, our processing revenues from Network Services merchants generally consist of a flat fee per transaction, thus revenues are driven primarily by the number of transactions we process (whether settled or only authorized), not card processing volume.

Our Merchant Base

We have developed significant expertise in industries that we believe present relatively low risks as the consumers are generally present and the products or services are generally delivered at the time the transaction is processed. These include:

| |

| • | Brick-and-mortar retailers |

| |

| • | Automotive sales and repair shops |

| |

| • | Convenience and liquor stores |

| |

| • | Professional service providers |

Generally, we define SME merchants as generating annual Visa and MasterCard card processing volume between $50,000 and $5,000,000. However, with the added functionality and cost benefits that our in-house processing platforms afford us, we also market to merchants with annual processing volume above $5,000,000.

The following table summarizes our SME processing volume by merchant category for the month of December 2015, compared to the months of December 2014 and December 2013.

|

| | | | | |

| | Month of December |

| | 2015 | | 2014 | | 2013 |

| Restaurants | 35.1% | | 35.1% | | 35.2% |

| Retail | 17.2% | | 17.9% | | 17.8% |

| Convenience, Fast Food & Liquor | 11.8% | | 11.4% | | 11.0% |

| Professional Services | 7.4% | | 7.3% | | 7.4% |

| Automotive | 6.6% | | 6.7% | | 6.8% |

| Lodging | 4.1% | | 4.5% | | 4.6% |

| Petroleum | 1.3% | | 1.6% | | 1.9% |

| Other | 16.5% | | 15.5% | | 15.3% |

Total SME processing volume $7.6 billion $6.6 billion $5.9 billion

No single SME merchant accounted for more than 0.42% of our total SME Visa and MasterCard card processing volume in 2015, and during 2015, our top 25 SME merchants represented only 3.69% of our SME Visa and MasterCard card processing volume and 3.31% of our SME Visa and MasterCard gross processing revenue. In 2015, approximately 93% of our SME card processing volume came from merchants we installed in 2014 and earlier.

In December 2015, SME merchants located in the following states represented the following percentages of our SME card processing volume: California represented 13.0%, Texas represented 6.2%, Florida represented 5.8%, New York represented 5.1% and Pennsylvania represented 3.5%, respectively. No other state represented more than 3.3% of our total SME card processing volume. Our geographic concentration tends to reflect the states with the highest economic activity, as well as certain states where we have historically maintained a stronger sales force. This merchant and geographic diversification makes us less sensitive to changing economic conditions in any particular industry or region. We believe that the loss of any single SME merchant would not have a material adverse effect on our financial condition or results of operations.

Payment Processing Platforms

We have developed a number of proprietary payment processing systems to increase our operating efficiencies and customize our product offerings. These include:

| |

| • | HPS Exchange, VAPS and NWS, our internal front-end authorization systems, provide authorization and data capture services that distribute processing and merchant data to card networks, merchants, and our sales force and customer service staff. These systems provide us greater control of the electronic transaction process, allow us to offer our merchants a differentiated product offering, and offer economies of scale that we expect will increase our long-term profitability. |

HPS Exchange, VAPS and NWS enable us to provide more customized solutions to merchants that demand customized front-end solutions and take advantage of new terminal hardware platforms and technology like our end-to-end encryption solution (included in our Heartland Secure solutions), as well as near field communication ("NFC") and Europay, MasterCard and Visa (“EMV”) processing. HPS Exchange, VAPS and NWS offer our merchants authorization and capture services in multiple industry verticals to a variety of POS systems including legacy terminals, petroleum pumps, middleware technologies, PC-integrated POS systems and web-based virtual terminals. In addition, HPS Exchange, VAPS and NWS offer third-party POS developers multiple protocols to meet their needs for integration.

During 2015, approximately 97% of the transactions of our SME merchants were processed on HPS Exchange, and 97% of all SME merchant accounts established in 2015 were placed on the system. During 2015, 100% of the transactions for our Network Services merchants were processed on VAPS or NWS.

| |

| • | Passport, our internally developed back-end processing system, provides one settlement platform for SME merchants and Network Services merchants, providing value-added features such as optimized funding, multi-bank next day Funding, automated dispute resolution, advanced interchange management and single portal integration via |

InfoCentral. In addition, Passport generates significant cost savings and allows us greater economies of scale, by replacing third-party processors' per-transaction charges with more of a fixed-cost structure. This structure allows per-transaction savings as increasing numbers of transactions are processed on Passport. In addition, Passport provides us the opportunity to offer our merchants significantly greater amounts of information regarding their processing characteristics, in more usable formats, and to offer our services to larger merchants. At both December 31, 2015 and 2014, substantially all of our SME merchants were processing on Passport, and all of our Network Services settled transactions were processing on Passport.

Security, Disaster Recovery and Back-up Systems

In the course of our operations, we compile and maintain a large database of information relating to our merchants and their transactions, and large amounts of card information cross our network as we authorize transactions. We have placed significant emphasis on maintaining a high level of security in order to attempt to protect the information of our merchants and their customers. We maintain current updates of network and operating system security releases and virus definitions, and have engaged a third party to regularly test our systems for vulnerability to unauthorized access. Further, we encrypt the cardholder numbers and merchant data that are stored in our databases using what we believe are the strongest commercially available encryption methods.

Our internal network configuration provides multiple layers of security to isolate our databases from unauthorized access and implements detailed security rules to limit access to all critical systems.

Visa, STAR, NYCE and other debit card networks have established security guidelines for PIN-based debit transaction processing that is based upon ANSI standards that are published as the “ASC X9 TG-3 Retail Financial Services Compliance Guideline; Part 1: PIN Security and Key Management.” We have a regularly scheduled Security Review of our Key Management Procedures against this standard that is performed by an external auditor.

We also have engaged external auditors to perform an annual Statement on Standards for Attestation Engagements No. 16 ("SSAE 16") review and make available the “Report on Heartland's Description of Transaction Processing System and on the Suitability on the Design and Operating Effectiveness of its Controls."

We operate our front-end processing, back-end processing, and other product platforms in two geographically dispersed outsourced data centers located in Texas and California. We establish system service level operational thresholds based on our large national merchants' requirements, and regularly exceed those levels, with system availability of greater than 99.9%. To achieve this standard, transactions are mirrored between the two data centers, and each center has the capacity to handle our full merchant transaction load. This duplicate processing capability ensures uninterrupted transaction processing during maintenance windows and other times processing may be interrupted in one data center. We regularly process through both data centers.

Sponsor Banks

Because we are not a ''member bank'' as defined by Visa and MasterCard, in order to process and settle these bankcard transactions for our merchants, we have entered into sponsorship agreements with member banks. Visa and MasterCard rules restrict us from performing funds settlement or accessing merchant settlement funds and require that these funds be in the possession of the member bank until the merchant is funded.

A sponsorship agreement permits us to route Visa and MasterCard bankcard transactions under the member bank's control and identification numbers to clear credit and signature debit bankcard transactions through Visa and MasterCard. A sponsorship agreement also enables us to settle funds between cardholders and merchants by delivering funding files to the member bank, which in turn transfers settlement funds to the merchants' bank accounts. These restrictions place the settlement assets and liabilities under the control of the member bank.

The sponsorship agreements with the member banks require, among other things, that we abide by the bylaws and regulations of the Visa and MasterCard networks. If we were to breach a sponsorship agreement, the sponsor banks can terminate the agreement and, under the terms of the agreement, we would have 180 days to identify an alternative sponsor bank. As of December 31, 2015, we have not been notified of any such issues by our sponsor banks, Visa or MasterCard.

At December 31, 2015, we were party to three bank sponsorship agreements.

| |

| • | Processing for the majority of our small and mid-sized merchants (referred to as "Small and Midsized Enterprises," or “SME merchants”) is performed under a February 8, 2012, sponsorship agreement with Wells |

Fargo Bank, N.A. ("WFB"). The WFB sponsorship agreement was in effect until February 8, 2016 and would have automatically renewed for three years unless either party provided written notice of non-renewal to the other party. On November 5, 2015, we provided written notice of non-renewal to WFB. Under the terms of the WFB sponsorship agreement, we have up to six months beyond February 8, 2016 to complete a conversion of its SME merchants to another sponsorship arrangement.

On November 5, 2015, we entered into a sponsorship agreement with Deutsche Bank Trust Company Americas ("Deutsche Bank") for our SME merchants. We are highly confident we will complete the conversion of our SME merchants to the Deutsche Bank sponsorship arrangement within the six-month conversion period beginning February 8, 2016. The sponsorship agreement with Deutsche Bank involves substantially the same terms as applied in the February 8, 2012 agreement with WFB. The agreement with Deutsche Bank is for a five-year term expiring on November 5, 2020 and will automatically renew for successive one-year periods unless either party provides six months written notice of non-renewal to the other party.

| |

| • | On November 23, 2009, we entered into a sponsorship agreement with The Bancorp Bank ("TBB") to sponsor processing for our Network Services merchants, which are predominantly petroleum industry merchants of all sizes (referred to as "Network Services Merchants"), and since October 2013, certain of our SME merchants. In August 2015, the agreement with TBB automatically renewed until February 2017, with subsequent one-year auto-renewal periods, unless either party provides six months written notice of non-renewal to the other party. |

| |

| • | On March 24, 2011, we entered into a sponsorship agreement with Barclays Bank Delaware to sponsor processing for certain of our large national merchants. The original agreement with Barclays Bank Delaware would have expired in March 2016; however, in September 2015, the agreement with Barclays Bank Delaware automatically renewed until March 2017. In January 2016, we signed an extension of this agreement, which will now expire in March 2021. The agreement will continue to automatically renew for successive one-year periods thereafter, unless either party provides six months written notice of non-renewal to the other party. |

The following is a breakout of our total Visa and MasterCard settled card processing volume for the month of December 2015 by percentage processed under our individual bank sponsorship agreements:

|

| | |

| | % of | December 2015 |

| Sponsor Bank | Bankcard Processing

Volume |

| Wells Fargo Bank, N.A. | 75% |

| The Bancorp Bank | 18% |

| Barclays Bank Delaware | 7% |

Customer Acquisition

Unlike many of our competitors who rely on Independent Sales Organizations ("ISOs") or salaried salespeople and telemarketers, we have built a direct, primarily commission-based, sales force. Our sales model divides the United States into nine primary markets overseen by Senior Vice Presidents and Vice Presidents of Sales. These Senior Vice Presidents and Vice Presidents are responsible for hiring Relationship Managers and increasing the sales of our products in their markets.

We measure the overall production of our sales force by new gross margin installed, which reflects the expected annual gross profit from a merchant contract after deducting processing and servicing costs associated with that revenue. We measure installed margin primarily for our SME card processing, payroll processing and loyalty and gift card marketing businesses. In 2015, our newly installed gross margin for the year increased 21.4% from the gross margin we installed during the year ended December 31, 2014 an increase from 17.3% growth achieved in 2014. We attribute this increase in newly installed gross margin to higher volumes and margins at newly installed merchants and improved individual productivity achieved by our salespersons, as well as growth in our sales force. Our SME sales force included Relationship Managers, Territory Managers, and Senior Product Advisors ("SPAs"), amounted to 1,240 and 985 at December 31, 2015 and 2014, respectively. We expect to drive increases in year-over-year installed margin in future periods primarily by increasing the number of SPAs and Relationship and Territory Managers.

We designed our sales force compensation structure to motivate our Relationship Managers to establish profitable long-term relationships with low-risk merchants and create a predictable and recurring revenue stream. Compensation for Relationship Managers is entirely commission-based, with commissions paid as a percentage of the financial value of new merchant accounts installed, which is measured in terms of the annual gross margin we estimate we will receive from the

merchant accounts installed. This is calculated by deducting the cost of processing (on a per-transaction basis) and servicing (measured in dollars per month) from the expected first-year net revenue the account is expected to generate.

The Relationship Manager and SPA generally will be paid a signing bonus equal to 50% of the first 12 months' estimated gross margin. The Relationship Manager and SPA will also receive, beginning the month installed, 15% and 20%, respectively, of the gross margin generated from the merchant each month as residual commissions for as long as the merchant remains our customer.

In addition, the Division Manager will receive an amount equal to 25% of the amount paid to the Relationship Manager and SPA (split with a Territory Manager, if one exists for the account). The Senior Vice Presidents and Vice Presidents will receive an amount equal to 25% of the amount paid to the Division Manager. For example, if an SME merchant account has $1,000 of estimated annual gross margin for the first 12 months and estimated monthly gross margin of $83.33, our sales force would be compensated as follows:

|

| | | | | | |

| Signing Bonus: | | | |

| Estimated gross margin for first 12 months | | $ | 1,000 |

| |

| Signing bonus paid to: | | | |

| Relationship Manager | | $ | 500 |

| 50.0 | % |

| Division Manager (plus Territory Manager) | | $ | 125 |

| 12.5 | % |

| SVP/VP | | $ | 31 |

| 3.13 | % |

| | | | |

| Residual Commission: | | | |

| Estimated monthly gross margin | | $ | 83.33 |

| |

| Monthly residual commission paid to: | | | |

| Relationship Manager | | $ | 12.50 |

| 15.0 | % |

| Division Manager (plus Territory Manager) | | $ | 3.12 |

| 3.75 | % |

| SVP/VP | | $ | 0.78 |

| 0.94 | % |

Marketing

Our marketing efforts have historically focused on industry verticals and marketing partnerships. We focus our marketing efforts on industries in which we believe our direct sales model is most effective and on merchants with certain key attributes. These attributes include owners who are typically on location, interact with customers, value a local sales presence, and consult with trade associations and other civic groups to make purchasing decisions.

We also determine which additional markets to enter into based on the following criteria:

•Average potential customer revenue;

•Number of locations to be serviced;

•Underwriting risk; and

•Required technological upgrades.

We have focused significantly on the hospitality industry and, in particular, independent restaurants. The number of restaurants to which we provide our payment processing services was approximately 43,800 as of December 31, 2015.

We have also historically had success in marketing our products and services through relationships with key trade associations, agent banks and value-added resellers.

As of December 31, 2015, we had preferred partner agreements with more than 250 trade associations. Of these partnerships, 48 are restaurant associations, including 46 state restaurant associations, the National Restaurant Association and the Counsel of State Restaurant Associations and another 20 are state lodging associations.

In exchange for an association's endorsements and recommendation of our products and services to their members, and upon the installation of a new merchant that is a member of the association, we pay to the trade association a signing bonus and residual commission.

We offer programs to banks across the United States that allow them access to leverage our extensive sales and support teams and other resources. The program provides our partner banks a source to refer their customers for merchant services as well as payroll processing and other electronic payment processing services. We offer on-site sales, training, installation, and ongoing service and support to the referred merchants. In exchange for a bank's endorsement of our products

and services, we typically pay the bank a monthly residual fee based on the referred merchant's processing volumes or margin. As of December 31, 2015, we provide these services to more than 1,500 banking locations in the United States.

In order to further market our products and services, we enter into arrangements with value-added resellers and third-party software developers. Value-added resellers typically sell complementary products and services such as hardware and software applications and POS hardware, software and communication network services to merchants in markets similar to ours. Our agreements with value-added resellers provide that, in exchange for their endorsement of our products and services and upon the installation of a new merchant referred by them, we will pay the value-added reseller a portion of the sales commission from the Relationship Manager responsible for that merchant and/or a transaction fee.

As we continue to expand our product offerings, we intend to introduce capabilities that will allow our systems to be compatible with third-party software developers while working to reduce merchants' third-party up-front costs for processing with us. We are committed to passing along our cost efficiencies to our merchants and their POS providers to encourage joint technology partnerships.

Merchant and Transaction Risk Management

We focus our sales efforts on low-risk bankcard merchants and have developed systems and procedures designed to minimize our exposure to potential merchant losses.

We have developed significant expertise in industries that we believe present relatively low risks as the customers are generally present and the products or services are generally delivered at the time the transaction is processed. These industries include restaurants, brick-and-mortar retailers, professional service providers, convenience and liquor stores, automotive sales and repair shops, gas stations, lodging establishments and others. The following table summarizes our SME merchants by industry as of December 31, 2015.

|

| |

| | As of |

| Industry | December 31, 2015 |

| Restaurants | 24.0% |

| Retail | 18.2% |

| Professional Services | 12.8% |

| Convenience, Fast Food & Liquor | 11.5% |

| Automotive | 7.8% |

| Lodging | 2.9% |

| Petroleum | 1.7% |

| Other | 21.1% |

Effective risk management helps us minimize merchant losses relating to chargebacks, reject losses and merchant fraud for the mutual benefit of our merchants and ourselves. We believe our knowledge and experience in dealing with attempted fraud has resulted in our development and implementation of effective risk management and fraud prevention systems and procedures for the types of fraud discussed in this section. In 2015, 2014 and 2013, we experienced merchant losses of $2.9 million, $7.3 million and $3.1 million, respectively, or 0.31 basis points, 0.90 basis points and 0.41 basis points, respectively, of our SME card processing volume. In 2014, our losses included $4.6 million resulting from chargebacks from a single merchant who entered bankruptcy in the fourth quarter.

We employ the following systems and procedures to minimize our exposure to merchant and transaction fraud:

Underwriting. Our sales force sends new applications to their regional service team for scoring and account set up. Higher-risk applications are routed to our credit underwriting department for review and screening. Our underwriting department's review of these applications serves as the basis for our decision whether to accept or reject a merchant account. The review also provides the criteria for establishing cash deposit or letter of credit requirements, processing limits, average transaction amounts and pricing, which assists us in monitoring merchant transactions for those accounts that exceed those pre-determined thresholds. The criteria set by our underwriting department also assist our risk management staff in advising merchants with respect to identifying and avoiding fraudulent transactions. Depending upon their experience level, our underwriting staff has the authority to render judgment on new applications or to take additional actions such as adjusting processing limits supported by prior processing history, analyzing average charge per transaction information or establishing cash deposits/letters of credit, reserves, and delayed funding requirements for new and existing merchants. Our underwriting department prepares accounts that are risk-sensitive for our Credit Committee review. The Credit Committee consists of a Manager of Underwriting, Manager of Risk Review, Director of Underwriting and Vice President of HSC Operations. Merchant accounts that exceed certain committee thresholds are reviewed by our CEO, Vice Chairman, Group President, or Chief of Operations. Our sponsor

banks also review and approve our merchant underwriting policies and procedures to ensure compliance with Visa and MasterCard operating rules and regulations.

Merchant Monitoring. We employ several levels of merchant account monitoring to help us identify suspicious transactions and trends. Daily merchant activity is sorted into a number of customized reports by our systems. Our risk management team reviews any unusual activity highlighted by these reports, such as larger than normal transactions or credits, and monitors other parameters that are helpful in identifying suspicious activity. We have daily windows to decide if any transactions should be held for further review, which provides us time to interview a merchant or issuing bank to determine the validity of suspicious transactions. We have also developed a fraud management system for HPS Exchange that is fully integrated with our internal customer relationship management software and has detailed review capabilities to further streamline our monitoring of those transactions. We also place merchants who require special monitoring on alert status and have engaged a web crawling solution that scans all merchant websites for content and integrity.

Investigation and Loss Prevention. If a merchant exceeds any parameters established by our underwriting and/or risk management staff or violates regulations established by the applicable bankcard network or the terms of our merchant agreement, one of our investigators will identify the incident and take appropriate action to reduce our exposure to loss and the exposure of our merchant. This action may include requesting additional transaction information, withholding or diverting funds, verifying delivery of merchandise or even deactivating the merchant account. Additionally, Relationship Managers may be instructed to retrieve equipment owned by us.

Collateral. We require some of our merchants to establish cash deposits or letters of credit that we use to offset against liabilities we may incur. We hold such cash deposits or letters of credit for as long as we are exposed to a loss resulting from a merchant's payment processing activity. In addition, we maintain a five-day delayed deposit policy on transactions processed by our Internet merchants and newly established merchants who have not previously processed bankcards to allow for additional risk monitoring. We also place a “hold” on batches containing questionable transactions, diverting the funds to a separate account pending review. As of December 31, 2015, these cash deposits and delayed and “held” batches totaled approximately $6.6 million.

Industry Overview

The payment processing industry provides merchants with credit, debit, gift and loyalty card and other payment processing services, along with related information services. The industry continues to grow as a result of wider merchant acceptance, increased consumer use of bankcards and advances in payment processing and telecommunications technology. According to The Nilson Report, total expenditures for all card type transactions by U.S. consumers are expected to grow to $6.6 trillion by 2019, representing a compound annual growth rate of 8.3%. The proliferation of bankcards has made the acceptance of bankcard payments a virtual necessity for many businesses, regardless of size, in order to remain competitive. This increased use of bankcards and prepaid cards, payment processing via smart phones, enhanced technology initiatives, efficiencies derived from economies of scale and the availability of more sophisticated products and services to all market segments has resulted in a highly competitive and specialized industry.

The payment processing industry is dominated by a small number of large, fully integrated payment processors that sell directly to, and handle the processing needs of, the nation's largest merchants. These integrated processors serve a broad market spectrum from large to small merchants and some provide banking, ATM and other payment-related services and systems in addition to card payment processing. Large national merchants with multiple locations and high volumes of bankcard transactions typically demand and receive the full range of payment processing services at low per-transaction costs.

SME merchants' payment processing needs generally are served by a large number of smaller payment processors, including banks and ISOs, that generally procure most of the payment processing services they offer from large payment processors. It is difficult, however, for banks and ISOs to customize payment processing services for the SME merchant on a cost-effective basis or to provide sophisticated value-added services.

Accordingly, services to the SME merchant market segment historically have been characterized by basic payment processing without the availability of the more customized and sophisticated processing, information-based services or customer service that are offered to large merchants. The continued growth in bankcard transactions is expected to cause SME merchants to increasingly value sophisticated payment processing and information services similar to those provided to large merchants. Heartland employees handle all aspects of the merchant’s payments needs, including sales, underwriting and risk management and servicing, as well as ancillary services like equipment deployment and repair and transaction tokenization and encryption services.

We compete with other providers of payment processing services on the basis of the following factors:

• Sales force size and effectiveness

• Range of product offering

• Quality of service

• Reliability of service

• Professional association endorsements

• Ability to evaluate, undertake and manage risk

• Speed in approving merchant applications

• Price

• Brand name

Some of our large competitors have substantially greater capital resources than we have. Others operate as subsidiaries of financial institutions or bank holding companies, which could allow them to own and conduct depository and other banking activities that we do not have the regulatory authority to own or conduct. Further, since they are affiliated with financial institutions or banks, these competitors may not incur the costs associated with being sponsored by a bank for registration with card networks and they can settle transactions quickly for the merchants with a deposit account at the bank. In addition, large, global technology companies are emerging in the card payment space.

Competitive Advantage

We believe our competitive strengths related to card payment processing, particularly for SME merchants, include the following:

| |

| • | Large, Experienced, Efficient, Direct Sales Force |

We sell and market our SME card payment processing services through a nationwide direct sales force of 1,069 Relationship Managers and Territory Managers, and 171 Senior Product Advisors, as of December 31, 2015, who work exclusively for us. Our sales professionals have local merchant relationships and industry-specific knowledge that allow them to effectively compete for merchants. These relationships are also supported by our customer service and support teams located in our service center. We believe our control of sales, underwriting and servicing both enhances our SME merchant retention and reduces our risks. We also believe that internally generated SME merchant contracts generally are of a higher quality and are more predictable than contracts acquired from third parties and the costs associated with such contracts generally are lower than the costs associated with contracts acquired from third parties.

Many of our competitors rely on third party distribution channels, including ISO's and Value-Added Resellers (“VARs”) that often generate merchant accounts for multiple payment processing companies, maintain ownership of the merchant relationships and may demand, over time, an increasing level of compensation from their processors.

We grow our SME payment processing business exclusively through internal expansion by generating new SME merchant contracts submitted by our own direct sales force.

| |

| • | Strong Position and Substantial Experience in Our Target Markets |

As of December 31, 2015, we were providing card payment processing services to 182,526 active SME merchants located across the United States. We believe our understanding of the needs of SME merchants and the risks inherent in doing business with them, combined with our efficient direct sales force, provides us with a competitive advantage over larger service providers that access this market segment through third-party sales channels. We also believe that we have a competitive advantage over service providers of a similar or smaller size that may lack our extensive experience and resources, and so do not benefit from the economies of scale that we have achieved.

At December 31, 2015, we also provided card payment processing services to approximately 3,194 Network Services merchants with approximately 43,987 locations. These Network Services merchants are predominantly in the petroleum industry. We believe that our understanding of the processing needs of petroleum merchants and the products we offer them provides us with a competitive advantage.

Historically, we have focused our sales efforts on SME merchants who have certain key attributes and on industries in which we believe our direct sales model is most effective and the risks associated with card processing are relatively low. These attributes include owners who are typically on location, interact with customers in person, value a local sales and servicing presence and often consult with trade associations and other civic groups to help make purchasing decisions.

To further promote our products and services, we have entered into referral arrangements with various trade associations, with an emphasis on restaurant and hospitality groups. We believe that these partnerships have enabled us to gain exposure and credibility within the restaurant and hospitality industries and have provided us with opportunities to market our products to new merchants.

Our historical focus on SME merchants has diversified our merchant portfolio and we believe has reduced the risks associated with revenue concentration. In 2015, no single SME merchant represented more than 0.42% of our total SME Visa and MasterCard processing volume, consistent with prior years.

Our Network Services business has further diversified our total merchant portfolio, adding a substantial base of large national merchants, predominantly in the petroleum industry.

| |

| • | Merchant-Centric Culture |

We have built a corporate culture and established practices that we believe improve the quality of services and products we provide to our merchants. We developed and endorsed the Merchant Bill of Rights, an advocacy initiative that details ten principles we believe should characterize all merchants' processing relationships. The Merchant Bill of Rights allows our sales team to differentiate our approach to bankcard processing and we believe that a focus on these principles will enhance our merchant relationships, and so reduce merchant attrition. We believe that our culture and practices allow us to maintain strong merchant relationships and differentiate ourselves from our competitors in obtaining new merchants.

Our merchant-centric culture spans from our sales force, which maintains a local market presence to provide rapid, personalized customer service, through our service center, which is segmented into regional teams to optimize responsiveness, and to our technology organization, which has developed a customer management interface and information system that alerts our Relationship Managers to any problems a merchant has reported and provides them with detailed information on the merchants in their portfolio. Additionally, we believe that we are one of the few companies that fully disclose our pricing to merchants. We think this approach contributes substantially to building long-term merchant relationships.

| |

| • | Scalable Operating Structure |

Our scalable operating structure generally allows us to expand our operations without proportionally increasing our fixed and semi-fixed support costs. In addition, our front-end and back-end card processing platforms were designed with the flexibility to support significant growth and drive economies of scale with low incremental transaction costs. Most of our operating costs are tied to the number of individuals we employ. We have in the past used, and expect in the future to use, technology to leverage our personnel, which should cause our personnel costs to increase at a lower rate than our card processing volume.

We employ information technology systems, which use the Internet to improve management reporting, enrollment processes, customer service, sales management, productivity, merchant reporting and problem resolution. We believe that these systems help attract both new merchants and Relationship Managers and provide us with a competitive advantage over many of our competitors who rely on less flexible legacy systems. We also offer a full suite of data security solutions, including encryption, tokenization and EMV, all wrapped with a data breach warranty that responds to an increasingly security-focused SME merchant.

We actively leverage the latest advances in technology to provide the best payments experience for merchants within liability levels that we believe exceed industry norms.

Campus Solutions

Campus Solutions provides integrated commerce solutions, payment processing, higher education loan services and open and closed-loop payment solutions to higher-education institutions.

TouchNet provides integrated commerce solutions to more than 700 higher education institutions serving over 7 million students, which is nearly one-third the higher education enrollment in the United States. Our offering of an end-to-end integrated commerce and payments solution to the higher education market is unmatched in the industry. Since 1989, TouchNet has been a pioneer in delivering innovative payment solutions. Colleges and universities have relied on TouchNet to unify and secure payment and related business transactions throughout the campus enterprise. TouchNet enables institutions of higher education to process and manage the myriad of campus payments—from student tuition to parking to alumni donations to campus events—on one platform and through one service provider.

Educational Computer Systems, Inc. ("ECSI") provides a suite of solutions to support administrative services for higher education including student loan payment processing, delinquency and default services, refund management, tuition payment plans, electronic billing and payment, tax document services, and business outsourcing. ECSI's core services support the management, payment and collection of student loans including Perkins and institutional financing. Since its founding in 1972, ECSI has printed and mailed 500 million billing statements, processed over 400 million tuition and loan payments and managed accounts for approximately 7 million students and borrowers. ECSI also processes nearly 5 million tax documents every year.

Campus Solutions also provides open- and closed-loop payment solutions for college or university campuses to efficiently process small-value electronic transactions. Campus Solutions currently serves more than 3,400 colleges and universities across multiple higher education sectors including nonprofit, for-profit, private, and community colleges.

Besides payment processing, our OneCard product which enables personal identification, door access, cashless vending transactions, cashless laundry, meal plans and cashless printing at campus facilities. In addition, our RefundSelect program, which we introduced in 2010, addresses the major operational needs of campuses by providing an open-loop debit card platform onto which schools load financial aid refunds. At December 31, 2015, we had 61 colleges enrolled in the RefundSelect program. We issued approximately 586,000 refunds totaling approximately $1.2 billion in 2015. We currently have 247 OneCard and RefundSelect college and university accounts.

The Campus Solutions industry is competitive with no single competitor providing the complete set of solutions that we provide. However, companies such as Higher One, Nelnet and Tuition Management Systems are larger competitors that compete with some of the solutions provided by us. Competition is primarily based on the products and services offered, innovation, customer service, reputation and price. Products must be compliant with various government regulations, which impede new, smaller entrants. We believe our Campus Solutions business is well positioned to gain customers and generate additional revenue by selling additional products to our existing base of customers.

The following table summarizes revenue and operating income for Campus Solutions for the years ended December 31, 2015, 2014 and 2013:

|

| | | | | | | | | | | | |

| | | Year Ended December 31, |

| | | 2015 | | 2014 | | 2013 |

| | | (In thousands) |

| Revenue | | $ | 117,208 |

| | $ | 61,538 |

| | $ | 36,186 |

|

| Operating income | | 36,293 |

| | 12,653 |

| | 3,930 |

|

Heartland School Solutions

Heartland School Solutions provides cafeteria POS solutions to more than 34,000 schools, making us the largest provider of kindergarten through 12th grade (K-12) food-service technology in the nation. In conjunction with this core POS business, approximately 80% of our customer schools actively use Heartland's online prepayment solutions to allow parents to fund accounts for school lunches or other on-campus activities. Parents can opt to establish recurring payments with customized low balance thresholds, make one-time payments, or simply see what their students ate for lunch that day. With a consistently high annual renewal rate for its POS customers, those platforms serve as a reliable base on which to offer additional value-added products and services. We offer back-office management software, hardware, annual technical support, and training to our customer school districts.

Heartland School Solutions has been built through a series of six acquisitions in 2010, 2011, 2012, and 2014. On April 1, 2014, Heartland completed its most recent acquisition in this market, MCS Software. Following the acquisitions, we focused on merging the management and operational structures of the six acquired businesses that make up the School Solutions segment. The more than 200 combined School Solutions professionals now operate under a single management structure and go-to-market strategy. While continuing to maintain certain legacy POS platforms for the foreseeable future, we combined all online prepayment activity into our MySchoolBucks platform, which has more than five and half million registered users. During 2015, we made a significant investment in our consumer-focused marketing strategy in order to encourage more widespread adoption of our online payment products, which, along with our acquisition of MCS Software, resulted in total growth in processing volume of 22% in 2015. As of December 31, 2015, we have over 1.5 million parents who are actively using our online payment products.

The K-12 food service technology industry is competitive, with our largest competitor being Horizon Software International and other smaller, privately held companies. Competition in the K-12 food-service technology industry is primarily based on the products and services offered, innovation, customer service, ease of use, reputation and price. Products must be in compliance with government regulations for schools in the districts we serve. Payment processing is becoming an increasingly important element of the overall offering for schools, which provides us with a competitive advantage, as we are the only payment processor in the K-12 industry. We believe we are well positioned to gain new school customers and generate additional revenue with our existing customers primarily through greater adoption of payment processing services.

The following table summarizes revenue and operating income for Heartland School Solutions for the years ended December 31, 2015, 2014 and 2013:

|

| | | | | | | | | | | | |

| | | Year Ended December 31, |

| | | 2015 | | 2014 | | 2013 |

| | | (In thousands) |

| Revenue | | $ | 60,870 |

| | $ | 57,570 |

| | $ | 50,541 |

|

| Operating income (a) | | 23,451 |

| | 10,874 |

| | 16,348 |

|

(a) See Note 1 Organization and Operations in the Notes to the Consolidated Financial Statements

for a discussion of an Out-of-Period Adjustment recorded in the year ended December 31, 2014.

Heartland Payroll Solutions

We operate a full-service nationwide payroll processing service. Our payroll services include check printing, direct deposit, related federal, state and local tax deposits, time clock sales and integrations, accounting documentation, Affordable Care Act ("ACA") reporting and human resources information. In order to improve operating efficiencies and ease of use for our customers and to decrease our own processing costs, we offer electronic and paperless payroll processing that allows an employer to submit its periodic payroll information to us via the Internet. If a customer chooses the online option, all reports and interactions between the employer and Heartland Payroll Solutions can be managed electronically, eliminating the need for cumbersome paperwork. Approximately half of our payroll customers currently submit their information electronically. However, if a customer chooses not to submit their payroll data online, they may submit such information via phone or facsimile. Regardless of input method, clients can choose to have Heartland Payroll Solutions print and ship their payroll package or to receive this information electronically.

On December 31, 2012, we acquired Ovation Payroll, Inc. ("Ovation"), adding more than 10,000 customers to our payroll business. On February 27, 2015, we purchased the stock of Payroll 1 for a $30.0 million cash payment, plus net working capital. The purchase price was financed from the 2014 Revolving Credit Facility. The acquisition of Payroll 1 expanded our existing payroll processing business and customer base by adding 6,573 customers at acquisition. As of December 31, 2015, 2014 and 2013, we provided payroll processing services to 33,937, 25,764 and 24,088 customers, respectively. In 2015, 2014 and 2013, we added 7,302, 5,821 and 5,797 new payroll processing customers, respectively.

We operate a comprehensive payroll management platform, which streamlines all aspects of the payroll process to enable time and cost savings. We consider our payroll platform to be state of the art, enabling us to process payroll on a large scale and provide customizable, cost-effective solutions for businesses of all sizes. It enables faster processing and continuous updates to help businesses remain compliant with payroll, tax, ACA and human resources regulations. The platform features web-hosted access, enabling businesses and their accountants to securely access all payroll data from virtually anywhere with SSL-encryption protection. It also provides robust, easy-to-use reporting for better business analysis. The Heartland Payroll platform is equipped to interface with certain leading providers of accounting services and time and attendance applications, as well as restaurant and retail POS systems. Our platform also includes an Employee Self-Serve web portal that allows employees to review copies of their paychecks, vouchers and payroll detail.

The payroll processing services industry is highly competitive, with services provided by outsourced providers like Heartland Payroll Solutions, but also accounting firms and self-service options. Overall the industry is comprised of two major segments: large national full-service payroll providers, and numerous much smaller national, regional, local and online providers. While large national payroll service firms such as ADP, Paychex, Ceridian, and Intuit are highly recognized, the full service payroll industry market is very fragmented. We compete with both segments.

Competition in the payroll processing industry is primarily based on service responsiveness, payroll accuracy, quality, reputation, range of product offering and price. Continual changes in tax laws and regulations are inherent to the payroll industry. When combined with the market demand for the latest in technology, third party integration and platform development, smaller competitors may lack the technical and financial resources to meet these needs. We believe Heartland Payroll Solutions is well positioned to continue to gain market share from those challenged providers. Additionally, we believe our competitive position is enhanced through our ability to offer payment processing services to payroll customers, and vice versa, and thus offer an integrated services suite, which will provide our customers with efficient and convenient options.

The following table summarizes revenue and operating income for Heartland Payroll Solutions for the years ended December 31, 2015, 2014 and 2013:

|

| | | | | | | | | | | | |

| | | Year Ended December 31, |

| | | 2015 | | 2014 | | 2013 |

| | | (In thousands) |

| Revenue | | $ | 69,037 |

| | $ | 50,394 |

| | $ | 44,565 |

|

| Operating income | | 9,465 |

| | 9,076 |

| | 3,404 |

|

Heartland Commerce

We provide the hospitality and retail industry with leading-edge POS solutions, payments processing capabilities and other adjacent business service applications through our Heartland Commerce business. Heartland Commerce is comprised of Xpient Solutions, LLC (“Xpient” acquired in October 2014); Merchant Software Corporation (referred to as "Liquor POS" which was acquired in February 2014); Automation, Inc. (d/b/a “pcAmerica” acquired in January 2015); Dinerware, Inc. (“Dinerware” acquired in February 2015) and Menusoft Systems Corporation (a.k.a. “Digital Dining” acquired in October 2015) to the Heartland Commerce business. Heartland Commerce is in the process of developing cloud-based POS systems that complement our well-established on-premise POS solutions. Digital Dining offers restaurants the convenience of a handheld POS on an iPhone, iPod and iPad in a hybrid environment with conventional fixed terminals, and is also used by restaurateurs for table management, delivery, reservations, labor scheduling, inventory and loyalty programs. Heartland Commerce net revenue was $34.4 million in 2015 which includes $15.0 million in net revenue from the 2015 acquisitions described above. Heartland Commerce had a net operating loss of $2.1 million for 2015.

The POS solutions industry has become increasingly competitive, and integrated with payments, with some of the large POS companies forging key partnerships with payments companies, and other merchant acquirers selling their services through POS VARS. As a way to surpass the competition, Heartland’s strategy is to not only establish partnerships with POS dealers but to also own select best of breed POS technologies. This enables us to offer a truly integrated POS platform that becomes the focal point for many of Heartland's value added applications including payment processing, table management, payroll, security, and online ordering.

Micropayments

We provide services to the small-value transaction market through our Micropayments business. We manufacture and sell solutions comprising unattended online wireless credit card-based payment systems, and unattended value top-up systems for off-line closed-loop smart (chip) card based payment systems. Our electronic cash systems provide small-value transaction processing for commercial laundry machines and vending machines, which are located in apartment laundries, cruise ships, corporate and university campuses, and penitentiaries. These systems offer consumers convenient ways to use their debit and credit cards to purchase and reload electronic cash cards, and to spend the value on the card for small-value purchases in both attended and unattended POS locations. In addition, we provide merchants financial settlement between the electronic cash card issuer and the vendor/merchant who accepts the card as payment. Our WaveRider system allows laundry patrons to use their debit or credit card to pay directly for their laundry right at the washer or dryer, simply by swiping their card. We believe there is increasing consumer demand for, and merchant interest in, card-based solutions for small denomination transactions, and expect to make additional investments in the future in developing solutions in this area.

The unattended payments industry is competitive with the largest competitor being USA Technologies. Other competitors include vending machine manufacturers and privately held companies focusing on specific vertical markets. Competition is primarily based on the products and services offered, ease of installation and setup, innovation and price. As payment processing is a core component of the services offered, we believe that we have a distinct advantage over many of our competitors. As unattended payments become more commonplace and expected, we believe that we will continue to add new customers.

The following table summarizes revenue and operating income for Micropayments for the years ended December 31, 2015, 2014 and 2013:

|

| | | | | | | | | | | | |

| | | Year Ended December 31, |

| | | 2015 | | 2014 | | 2013 |

| | | (In thousands) |

| Revenue | | $ | 18,638 |

| | $ | 16,950 |

| | $ | 12,634 |

|

| Operating income | | 4,333 |

| | 3,568 |

| | 1,336 |

|

Heartland Marketing Solutions

Heartland Marketing Solutions ("HMS") delivers a full suite of consumer engagement solutions for merchants. These include mobile and card-based gift and rewards marketing services to merchant locations through real-time communications with the merchant POS, enabling us to leverage existing installations across our merchant base and enhancing our overall value proposition to the merchant community. In addition to gift and rewards, HMS also delivers vertical use case driven mobile applications, such as the Heartland ToGo product, a mobile and online ordering solution that is integrated with gift and rewards. In addition to servicing the SME merchant market, HMS also provides these solutions to regional and national brands.

The Marketing Solutions space continues to evolve and become even more relevant as merchants are looking for deeper engagement with their customers. In 2015, HMS launched several enhancements such as a suite of Application Programming Interfaces ("APIs"), integration into several mobile application providers, a full suite of digital card distribution to the SME space and has developed the groundwork for a robust data and analytics solution. As of December 31, 2015, Heartland Marketing Solutions has 12,954 active merchant locations and loaded $458 million on approximately 12.5 million consumer gift cards, compared to 11,669 active merchant locations and $340 million loaded on approximately 9.6 million cards as of December 31, 2014.

In addition, there has been prolific emergence of mobile application providers to enable merchants to create a branded mobile application to compete with other large brands. HMS has reacted by developing a robust set of APIs to enable integration in the fast-moving market to allow for quick integration into multiple third-party solutions. This option enables merchants to partner with any application developer to integrate gift and rewards into the application of their choosing. HMS continues to see traction in vertical use case driven integrations, including the continued sales and growth of Heartland ToGo, a mobile and online ordering solution with embedded gift and rewards. As of December 31, 2015, Heartland has boarded more than 175 merchants on the Heartland ToGo solution.