Exhibit 99.1

Managed Services, Managed Better

Special Note about Forward-Looking Statements

This presentation includes “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995 that reflect our current views as to future events and financial performance with respect to our operations. These statements can be identified by the fact that they do not relate strictly to historical or current facts. They use words such as “aim,” “anticipate,” “estimate,” “expect,” “will be,” “will continue,” “will likely result,” “project,” “intend,” “plan,” “believe” and other words and terms of similar meaning in conjunction with a discussion of future operating or financial performance. These statements are subject to risks and uncertainties that could cause actual results to differ materially from those expressed or implied in the forward-looking statements.

Factors that might cause such a difference include: unfavorable economic conditions; ramifications of any future terrorist attacks or increased security alert levels; increased operating costs, including labor-related and energy costs; shortages of qualified personnel or increases in labor costs; costs and possible effects of union organizing activities; currency risks and other risks associated with international markets; risks associated with acquisitions, including acquisition integration costs; our ability to integrate and derive the expected benefits from our recent acquisitions; competition; decline in attendance at client facilities; unpredictability of sales and expenses due to contract terms and terminations; the contract intensive nature of our business, which may lead to client disputes; high leverage; claims relating to the provision of food services; costs of compliance with governmental regulations and government investigations; liability associated with noncompliance with governmental regulations, including regulations pertaining to food services, the environment, Federal and state employment laws and wage and hour laws and import and export controls and customs laws; dram shop litigation; inability to retain current clients and renew existing client contracts; determination by customers to reduce their outsourcing and use of preferred vendors; seasonality; and other risks that are set forth in the “Risk Factors” sections of ARAMARK’s SEC filings.

For further information regarding risks and uncertainties associated with ARAMARK’s business, please refer to the “Management’s Discussion and Analysis of Results of Operations and Financial Condition” and “Risk Factors” and other sections of ARAMARK’s SEC filings, including, but not limited to, our annual report on Form 10-K and quarterly reports on Form 10-Q, copies of which may be obtained by contacting ARAMARK’s investor relations department via its web site www.aramark.com.

Forward-looking statements speak only as of the date made. We undertake no obligation to update any forward-looking statements to reflect the events or circumstances arising after the date as of which they are made. As a result of these risks and uncertainties, readers are cautioned not to place undue reliance on the forward-looking statements included herein or that may be made elsewhere from time to time by, or on behalf of, us.

Important Disclosure

In this presentation, we mention certain financial measures that are considered non-GAAP. Generally, a non-GAAP financial measure is a numerical measure of a company’s performance, financial position, or cash flows that either excludes or includes items different than those prepared or presented in accordance with generally accepted accounting principles. We have prepared disclosures and reconciliations of non-GAAP financial measures that were used in this presentation and may be used periodically by management when discussing the Company’s financial results with investors and analysts, which are available on our website www.aramark.com.

2

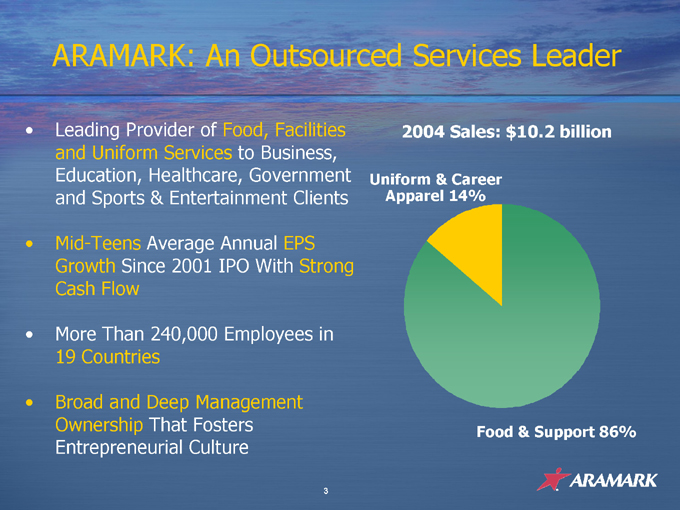

ARAMARK: An Outsourced Services Leader

Leading Provider of Food, Facilities and Uniform Services to Business, Education, Healthcare, Government and Sports & Entertainment Clients

Mid-Teens Average Annual EPS Growth Since 2001 IPO With Strong Cash Flow

More Than 240,000 Employees in 19 Countries

Broad and Deep Management Ownership That Fosters Entrepreneurial Culture

2004 Sales: $10.2 billion

Uniform & Career Apparel 14%

Food & Support 86%

3

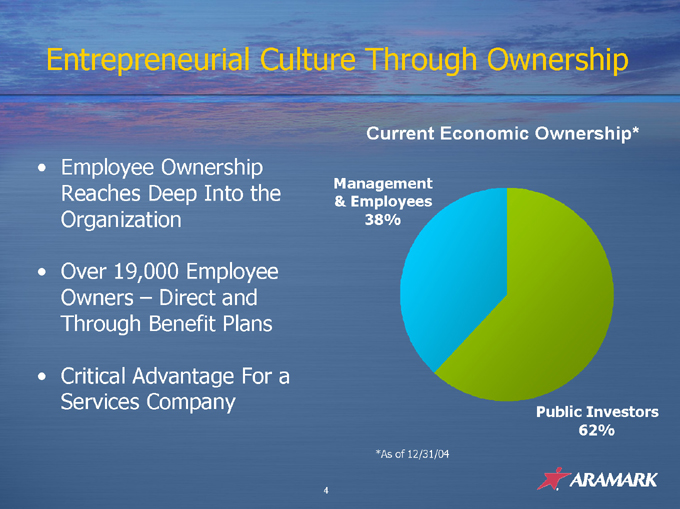

Entrepreneurial Culture Through Ownership

Employee Ownership Reaches Deep Into the Organization

Over 19,000 Employee Owners – Direct and Through Benefit Plans

Critical Advantage For a Services Company

Current Economic Ownership*

Management & Employees 38%

*As of 12/31/04

Public Investors 62%

4

Drivers of Outsourcing

Client Focus on Core Business

“Customer” (End-User) Satisfaction is Critical to Client

Improved Effectiveness Often Important to Client’s Success

Client Cost Reduction

About 40% of New ARAMARK Business in 2003-2004 Came From Previously Self-Operated Clients

5

Services Provided

Food & Support Services

Cafés, Executive Dining Rooms

Catering Retail and C-Stores Conference Center Management Refreshment Services Concessions Event Planning On-site Restaurants Lodging

Energy Management Groundskeeping Laundry & Linen Services Plant Operations Central Transportation Building Commissioning Clinical Equipment Services Environmental Services

Uniform Services

Uniform Rental / Lease

Nationwide Service National Account Programs Clean Rooms

WearGuard & Crest Brands

Direct Sale Offerings Managed & National Account Programs QSR / Healthcare Leader

Galls Brand

Public Safety Catalog Business

6

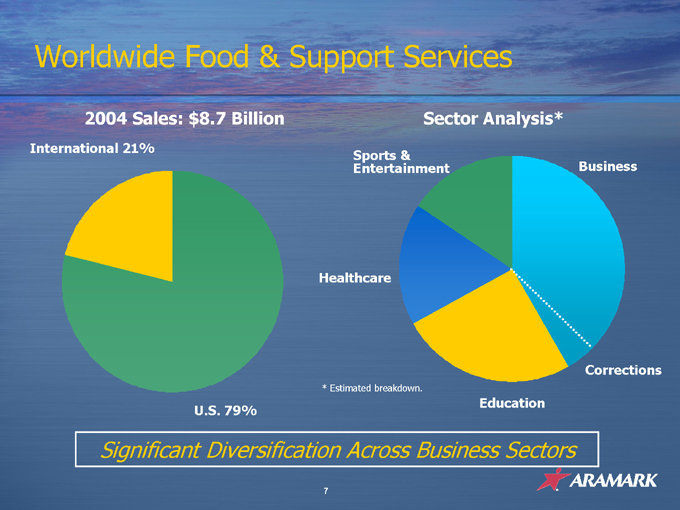

Worldwide Food & Support Services

2004 Sales: $8.7 Billion

International 21%

U.S. 79%

Sector Analysis*

Sports & Entertainment

Healthcare

* Estimated breakdown.

Education

Corrections

Business

Significant Diversification Across Business Sectors

7

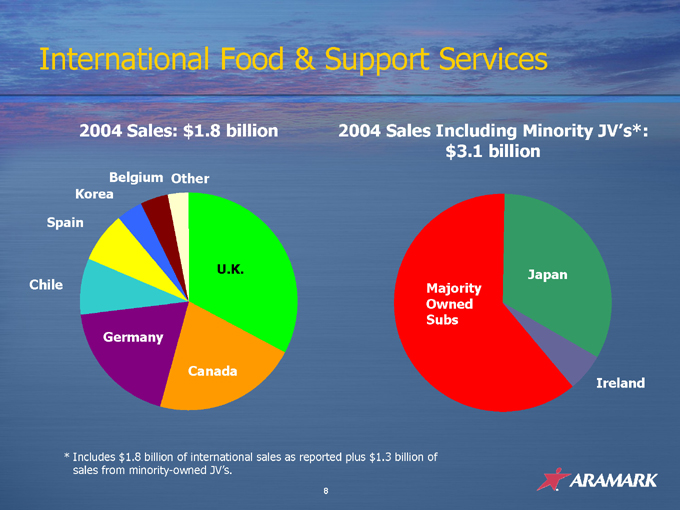

International Food & Support Services

2004 Sales: $1.8 billion

Belgium Other

Korea

Spain

Chile

U.K.

Germany

Canada

2004 Sales Including Minority JV’s*: $3.1 billion

Majority Owned Subs

Japan

Ireland

* Includes $1.8 billion of international sales as reported plus $1.3 billion of sales from minority-owned JV’s.

8

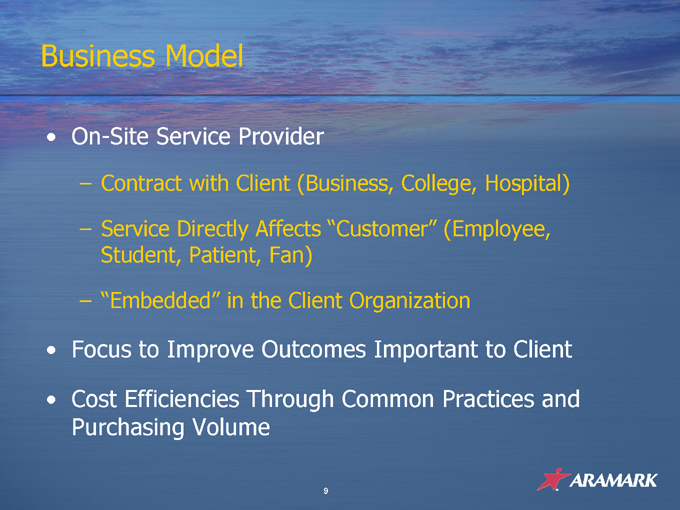

Business Model

On-Site Service Provider

Contract with Client (Business, College,

Hospital) Service Directly Affects “Customer” (Employee, Student, Patient, Fan) “Embedded” in the Client Organization

Focus to Improve Outcomes Important to Client Cost Efficiencies Through Common Practices and Purchasing Volume

9

How We Add Value

Customer Knowledge

Understand Preferences Through Research and Operational Experience

Tailor Service Offerings to Increase Customer Satisfaction

Broad, Retail-Oriented Food Service Offerings

Improved Environment Through Facilities Management

Improve Economics to Client Through:

Increased Customer Spend and Participation

Higher Quality / Efficiency to Support Client’s Mission

Standardized Operation and Volume to Drive Cost Efficiencies

Value is More Than Just Low Cost

10

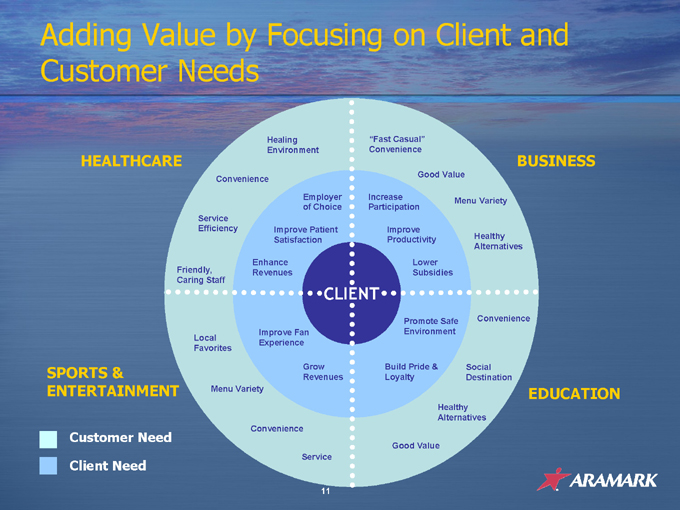

Adding Value by Focusing on Client and Customer Needs

HEALTHCARE

SPORTS & ENTERTAINMENT

BUSINESS

EDUCATION

Healing Environment

Convenience

Service Efficiency

Friendly, Caring Staff

Local Favorites

Menu Variety

Convenience

Service

Good Value

Healthy Alternatives

Social Destination

Convenience

Healthy Alternatives

Menu Variety

Good Value

“Fast Casual” Convenience

Employer of Choice

Improve Patient Satisfaction

Enhance Revenues

Improve Fan Experience

Grow Revenues

Build Pride & Loyalty

Promote Safe Environment

Lower Subsidies

Improve Productivity

Increase Participation

Customer Need

Client Need

11

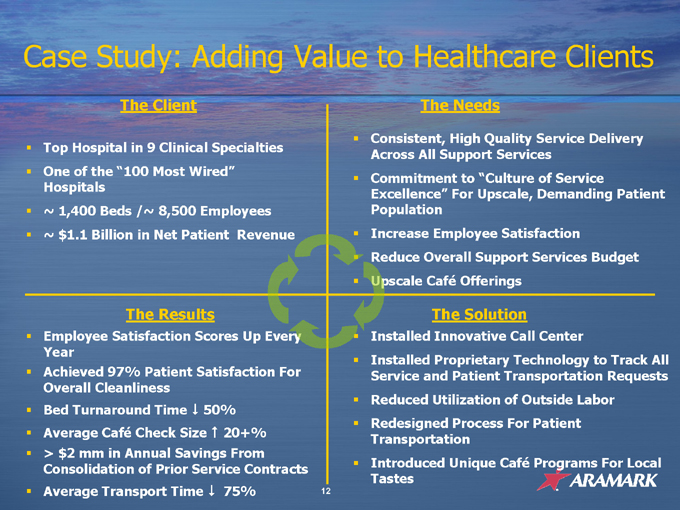

Case Study: Adding Value to Healthcare Clients

The Client

Top Hospital in 9 Clinical Specialties

One of the “100 Most Wired” Hospitals

~ 1,400 Beds /~ 8,500 Employees

~ $1.1 Billion in Net Patient Revenue

The Results

Employee Satisfaction Scores Up Every Year

Achieved 97% Patient Satisfaction For Overall Cleanliness

Bed Turnaround Time 50%

Average Café Check Size 20+%

> $2 mm in Annual Savings From Consolidation of Prior Service Contracts

Average Transport Time 75%

The Needs

Consistent, High Quality Service Delivery Across All Support Services

Commitment to “Culture of Service Excellence” For Upscale, Demanding Patient Population

Increase Employee Satisfaction

Reduce Overall Support Services Budget

Upscale Café Offerings

The Solution

Installed Innovative Call Center

Installed Proprietary Technology to Track All Service and Patient Transportation Requests

Reduced Utilization of Outside Labor

Redesigned Process For Patient Transportation

Introduced Unique Café Programs For Local Tastes

12

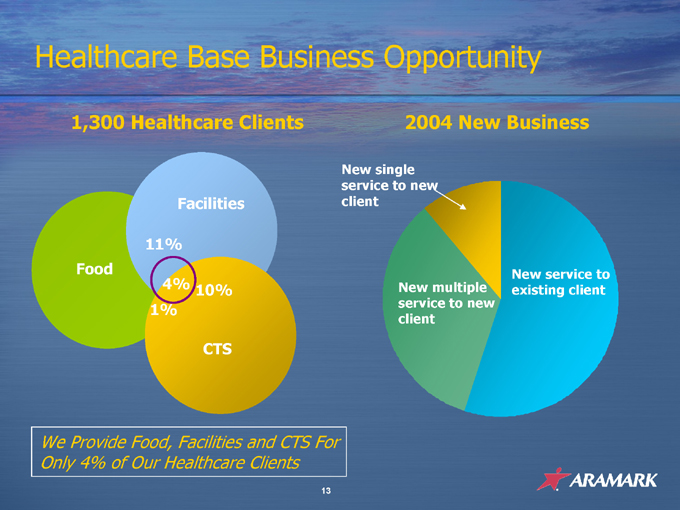

Healthcare Base Business Opportunity

1,300 Healthcare Clients

Food

Facilities

11%

4%

1%

10%

CTS

2004 New Business

New single service to new client

New multiple service to new client

New service to existing client

We Provide Food, Facilities and CTS For Only 4% of Our Healthcare Clients

13

Growth Opportunities

Additional Penetration Into Self-Operated Clients

Healthcare, Education are Underpenetrated

Higher Usage at Existing Clients

Improved Service Offerings Attract More Customers From On-Site Population

Additional Services

Cross-Selling Food and Facilities Services

International Expansion

Grow From Current 19 Country Base

14

ARAMARK: Uniform & Career Apparel

A leading U.S. provider with approximately $1.5 billion in sales in fiscal 2004

Rental:

A nationwide network servicing 1.5 million wearers in 90% of the top 200 markets

Direct Marketing:

Direct sales of a broad career apparel line through WearGuard/Crest and Galls to quick service restaurant, healthcare and public safety sectors

Uniform Services

Uniform Rental/Lease

Dust Control

Clean Room

WearGuard/ Crest

Direct Purchase Products

Mass Personalization

Workwear

QSR/Healthcare Design

Galls

Public Safety (Law, Fire, EMT)

Apparel and Equipment

Sourcing, Manufacturing, Distribution

15

Business Model

Broad Line of Rental and Direct Sale Career Apparel Covering Nearly All Job Categories

A Nationwide Network of Uniform Rental Service Facilities Covering 90% of the Top 200 Markets

Broad, Direct Distribution Through Catalog, Outbound Telemarketing, Sales Force and Internet

Best-in-Class Global Uniform Manufacturing / Sourcing to Reduce Costs and Control Quality

16

How We Add Value

Important Component of Employer Branding

Particularly Service Companies Significant Customizing Capability

Consistent Employee Image

Increased Employee Satisfaction

Improved Employee Protection

17

Growth Opportunities

Penetration of “Non-User” Population

26 Million Potential “First-Time” Users

Currently About 50% of New Sales

Ancillary Sales to Existing Customers

Cross-Sell Allied, Sanitation Products

Nationwide Clients

Ability to Standardize Products, Services and Cost

18

Mission One Helps Us Achieve Our Goals

Retention

Base Business Grrowth

One Best Team

New Business

Through Mission One, ARAMARK is Striving to be Number One in Profitable Organic Growth by Providing a Full Portfolio of Unmatched Services to Our Clients

19

Operating & Financial Discipline

Organic Sales Growth

Margin Improvement

Cash Flow

Return on Invested Capital Acquisition Strategy

20

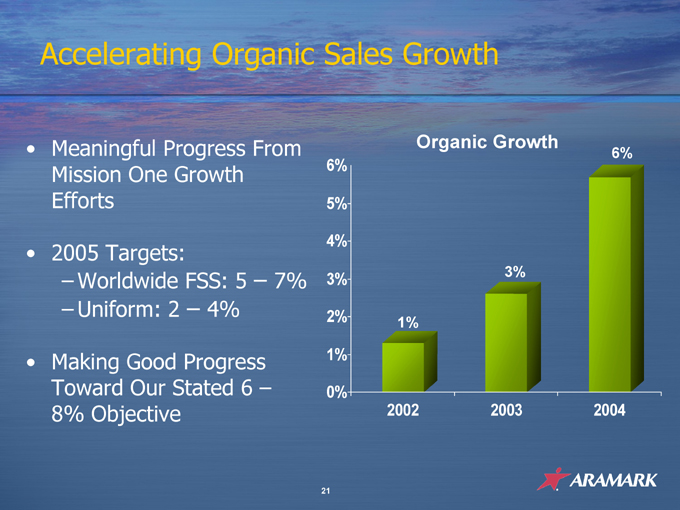

Accelerating Organic Sales Growth

Meaningful Progress From Mission One Growth Efforts

2005 Targets:

Worldwide FSS: 5 – 7%

Uniform: 2 – 4%

Making Good Progress Toward Our Stated 6 –8% Objective

6% 5% 4% 3% 2% 1% 0%

Organic Growth

1%

3%

6%

2002 2003 2004

21

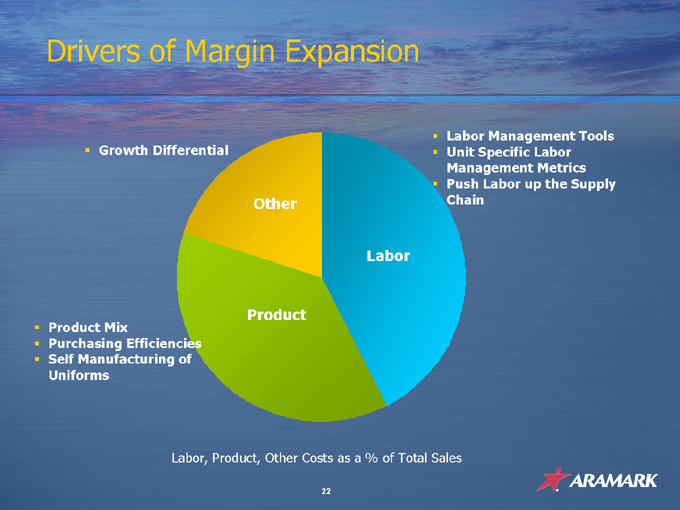

Drivers of Margin Expansion

Growth Differential

Product Mix

Purchasing Efficiencies

Self Manufacturing of Uniforms

Other

Product

Labor

Labor Management Tools

Unit Specific Labor Management Metrics

Push Labor up the Supply Chain

Labor, Product, Other Costs as a % of Total Sales

22

Strong Cash Flow and Return on Invested Capital

Low Capital Intensity ~ 3% of Sales

Focused on Adding Value Through Optimal Capital Structure

Strong Cash Flow

Generation Supports Debt Service

Objective to Retain Investment Grade Rating

Strong Low-Teens ROIC

ROIC Significantly Exceeds Cost of Capital

23

Acquisition Strategy

Disciplined and Return-Focused

Target: 15% After-Tax IRR EPS Accretive in 1-2 years

Strategies

Strengthen Existing Services and Client Portfolio

Fine Host, Harrison, CTS

Add or Strengthen Key Services

ServiceMaster

Expand International Reach

AIM Services (Japan), Campbell Catering (Ireland),

Central Restaurantes (Chile), Travers (Canada), Restauracion

Colectiva & Rescot (Spain), Catering Alliance (UK), Bright

China Service Industries (China)

24

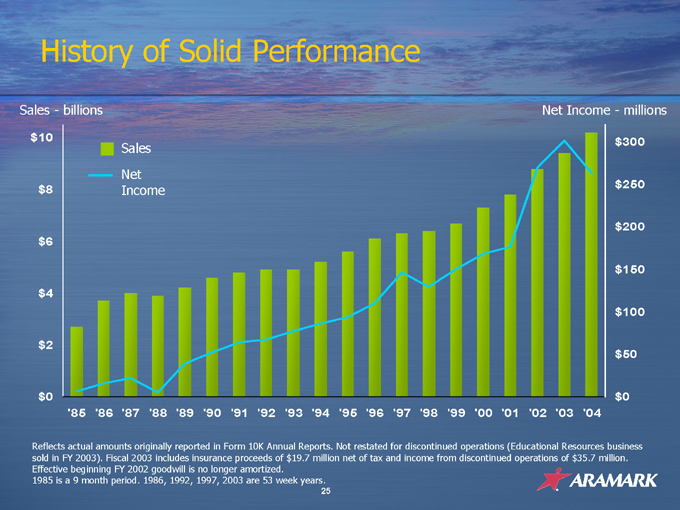

History of Solid Performance

Sales—billions $10 $8 $6 $4 $2 $0

Sales Net Income

Net Income—millions

‘85 ‘86 ‘87 ‘88 ‘89 ‘90 ‘91 ‘92 ‘93 ‘94 ‘95 ‘96 ‘97 ‘98 ‘99 ‘00 ‘01 ‘02 ‘03 ‘04 $300 $250 $200 $150 $100 $50 $0

Reflects actual amounts originally reported in Form 10K Annual Reports. Not restated for discontinued operations (Educational Resources business sold in FY 2003). Fiscal 2003 includes insurance proceeds of $19.7 million net of tax and income from discontinued operations of $35.7 million.

Effective beginning FY 2002 goodwill is no longer amortized.

1985 is a 9 month period. 1986, 1992, 1997, 2003 are 53 week years.

25

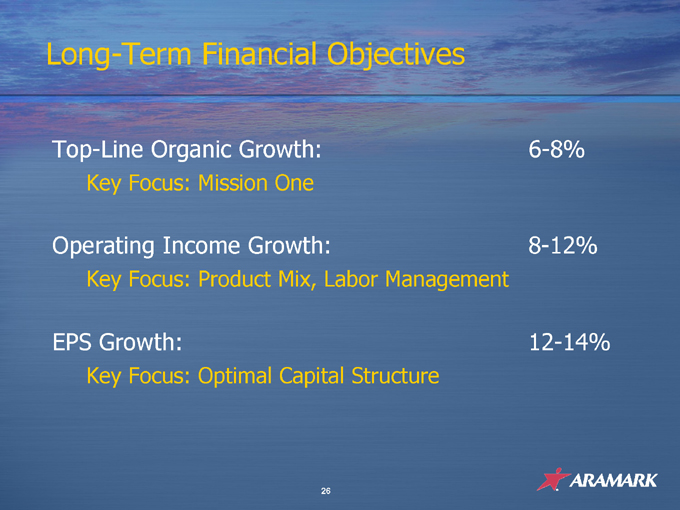

Long-Term Financial Objectives

Top-Line Organic Growth:

Key Focus: Mission One

6-8%

Operating Income Growth:

Key Focus: Product Mix, Labor Management

8-12%

EPS Growth:

Key Focus: Optimal Capital Structure

12-14%

26

Key Strengths

Ability to Add Value to Customer

Tangible Benefits to Our Clients

Operational Excellence and Economies of Scale

Shared With Our Clients

High Client Retention

Mid 90% Range

Diversification Across Business Sectors

Business, Education, Government, Healthcare, Sports & Entertainment

27

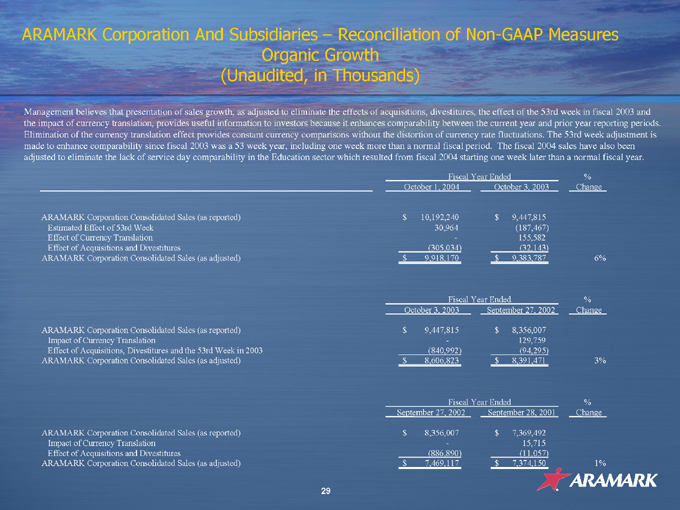

Managed Services, Managed Better

ARAMARK Corporation And Subsidiaries – Reconciliation of Non-GAAP Measures Organic Growth (Unaudited, in Thousands)

Management believes that presentation of sales growth, as adjusted to eliminate the effects of acquisitions, divestitures, the effect of the 53rd week in fiscal 2003 and the impact of currency translation, provides useful information to investors because it enhances comparability between the current year and prior year reporting periods. Elimination of the currency translation effect provides constant currency comparisons without the distortion of currency rate fluctuations. The 53rd week adjustment is made to enhance comparability since fiscal 2003 was a 53 week year, including one week more than a normal fiscal period. The fiscal 2004 sales have also been adjusted to eliminate the lack of service day comparability in the Education sector which resulted from fiscal 2004 starting one week later than a normal fiscal year.

October 1, 2004 Fiscal Year Ended October 3, 2003 % Change

ARAMARK Corporation Consolidated Sales (as reported) $10,192,240 $9,447,815

Estimated Effect of 53rd Week 30,964 (187,467)

Effect of Currency Translation - 155,582

Effect of Acquisitions and Divestitures (305,034) (32,143)

ARAMARK Corporation Consolidated Sales (as adjusted) $9,918,170 $9,383,787 6%

October 3, 2003 Fiscal Year Ended September 27, 2002 % Change

ARAMARK Corporation Consolidated Sales (as reported) $9,447,815 $8,356,007

Impact of Currency Translation - 129,759

Effect of Acquisitions, Divestitures and the 53rd Week in 2003 (840,992) (94,295)

ARAMARK Corporation Consolidated Sales (as adjusted) $8,606,823 $8,391,471 3%

September 27, 2002 Fiscal Year Ended September 28, 2001 % Change

ARAMARK Corporation Consolidated Sales (as reported) $8,356,007 $7,369,492

Impact of Currency Translation - 15,715

Effect of Acquisitions and Divestitures (886,890) (11,057)

ARAMARK Corporation Consolidated Sales (as adjusted) $7,469,117 $7,374,150 1%

29