EXHIBIT 99.1

EXCERPTS FROM PRELIMINARY OFFERING MEMORANDUM,

DATED JANUARY 5, 2007

Unless otherwise indicated or the context otherwise requires, references to “ARAMARK,” “we,” “our,” “us” and “the Company” and similar terms refer to ARAMARK Corporation and its subsidiaries on a consolidated basis, which are being acquired pursuant to the Transactions (as described below) by RMK Acquisition Corporation, a Delaware corporation (“MergerCo”) formed by investment funds (the “Sponsor Funds”) managed by GS Capital Partners, CCMP Capital Advisers, J.P. Morgan Partners, Thomas H. Lee Partners and Warburg Pincus LLC (the “Sponsors,” and together with the management participants who invest in Aramark Holdings Corporation, a Delaware corporation (“Holdings”) which will be the indirect parent of ARAMARK following the consummation of the Transactions (as defined below), the “Investors”), prior to the merger (the “Merger”) of MergerCo with and into ARAMARK Corporation, and ARAMARK, as the surviving company following the Merger. The offering of senior fixed rate notes, senior floating rate notes and senior subordinated notes (collectively, the “notes”), the initial borrowings under our new senior secured credit facilities, the funding under our amended receivables facility, the equity investment and participation by the Investors in Holdings or our parent companies, the Merger, the repayment of certain other existing outstanding indebtedness described below and other related transactions in connection with the Merger are collectively referred to as the “Transactions.”

Unaudited pro forma condensed consolidated financial information

The following unaudited pro forma condensed consolidated financial statements have been developed by applying pro forma adjustments to the historical audited consolidated financial statements of ARAMARK in relation to the acquisition of ARAMARK by an investor group led by Joseph Neubauer and the Sponsor Funds. The unaudited pro forma consolidated statement of income gives effect to the Transactions as if they had occurred on October 1, 2005. The unaudited pro forma condensed consolidated balance sheet gives effect to the Transactions as if they had occurred on September 29, 2006. Assumptions underlying the pro forma adjustments are described in the accompanying notes, which should be read in conjunction with these unaudited pro forma condensed consolidated financial statements. The presentation assumes that the equity and cost basis of Holdings’ investment in ARAMARK will be “pushed down” in the ARAMARK consolidated financial statements.

The unaudited pro forma adjustments are based upon available information and certain assumptions that we believe are reasonable under the circumstances. The unaudited pro forma condensed consolidated financial information is presented for informational purposes only. The unaudited pro forma condensed consolidated financial information does not purport to represent what our results of operations or financial condition would have been had the Transactions actually occurred on the dates indicated and they do not purport to project our results of operations or financial condition for any future period or as of any future date. The unaudited pro forma condensed consolidated financial statements should be read in conjunction with the information contained in “The Transactions” below and “Selected historical consolidated financial data” and “Management’s discussion and analysis of results of operations and financial condition” and the consolidated financial statements and related notes thereto appearing in our Annual Report on Form 10-K for the year ended September 29, 2006. All pro forma adjustments and their underlying assumptions are described more fully in the notes to our unaudited pro forma condensed consolidated financial statements.

The Merger will be accounted for using purchase accounting. The pro forma information presented, including allocations of purchase price, is based on preliminary estimates of the fair values of assets acquired and liabilities assumed, currently available information and assumptions and will be revised as additional information becomes available. The actual adjustments to our consolidated financial statements upon the closing of the Transactions will depend on a number of factors, including additional information available and our net assets on the closing date of the Transactions. Therefore, the actual adjustments will differ from the pro forma adjustments, and the differences may be material.

The final purchase price allocation is dependent on, among other things, the finalization of asset and liability valuations. As of the date hereof, we have not completed the valuation studies necessary to estimate the fair values of the assets we have acquired and liabilities we have assumed and the related allocation of purchase price. We have allocated the total estimated purchase price, calculated as described in note (b) under “—Notes to unaudited pro forma condensed consolidated balance sheet,” to the assets acquired and liabilities assumed based on preliminary estimates of their fair values. A final determination of these fair values will reflect our consideration of a final valuation prepared by third-party appraisers. This final valuation will be based on the actual net tangible and intangible assets that existed as of the closing date of the Transactions. Any final adjustment will change the allocations of purchase price, which could affect the fair value assigned to the assets and liabilities and could result in a change to the unaudited pro forma condensed consolidated financial statements, including a change to goodwill.

1

Unaudited pro forma condensed consolidated balance sheet

as of September 29, 2006

| (in millions) | ARAMARK historical | Pro forma adjustments | Pro forma ARAMARK | |||||||||

Assets | ||||||||||||

Current assets: | ||||||||||||

Cash and cash equivalents | $ | 47.7 | $ | 55.5 | (a) | $ | 103.2 | |||||

Receivables | 870.9 | — | 870.9 | |||||||||

Inventories | 494.2 | — | 494.2 | |||||||||

Prepayments and other current assets | 114.1 | — | 114.1 | |||||||||

Total current assets | 1,526.9 | 55.5 | 1,582.4 | |||||||||

Property and equipment, net | 1,196.8 | — | 1,196.8 | |||||||||

Goodwill | 1,747.1 | 3,483.5 | (b) | 5,230.6 | ||||||||

Other intangible assets | 298.0 | 1,346.7 | (b) | 1,644.7 | ||||||||

Other assets | 494.5 | 315.6 | (b),(c) | 810.1 | ||||||||

| $ | 5,263.3 | $ | 5,201.3 | $ | 10,464.6 | |||||||

Liabilities and shareholders’ equity | ||||||||||||

Current liabilities: | ||||||||||||

Current maturities of long-term borrowings | $ | 40.2 | $ | — | $ | 40.2 | ||||||

Accounts payable | 642.8 | — | 642.8 | |||||||||

Accrued expenses and other current liabilities | 903.7 | (51.6 | )(b) | 852.1 | ||||||||

Total current liabilities | 1,586.7 | (51.6 | ) | 1,535.1 | ||||||||

Long-term borrowings | 1,763.1 | 4,458.9 | (a),(b) | 6,222.0 | ||||||||

Deferred income taxes and other noncurrent liabilities | 391.9 | 689.6 | (b),(d) | 1,081.5 | ||||||||

Shareholders’ equity | 1,521.6 | 104.4 | (d) | 1,626.0 | ||||||||

| $ | 5,263.3 | $ | 5,201.3 | $ | 10,464.6 | |||||||

See accompanying notes to unaudited pro forma condensed consolidated balance sheet

2

Notes to unaudited pro forma condensed consolidated balance sheet

| a) | Reflects the estimated sources and uses of funds for the Transactions as follows: |

(in millions) | |||

| Sources | |||

Senior secured term loan facility(1) | $ | 3,660.0 | |

Senior notes | 1,700.0 | ||

Senior subordinated notes | 570.0 | ||

Receivables facility | 211.0 | ||

Equity contribution(2) | 2,095.0 | ||

Total sources | $ | 8,236.0 | |

| Uses | |||

Estimated purchase price for shares and share equivalents(3) | $ | 6,244.2 | |

Repayment of existing indebtedness | 1,425.3 | ||

Receivables facility | 211.0 | ||

Estimated fees and expenses(4) | 300.0 | ||

Total uses | $ | 8,180.5 | |

Pro forma net adjustment to cash | $ | 55.5 | |

(1) Upon the closing of the Transactions, we will enter into a $3,660.0 million term loan facility, comprised of a $3,110.0 million facility with ARAMARK as the borrower (which includes $50.0 million U.S. dollar-equivalent denominated in Japanese Yen) and additional tranches of $175.0 million, $55.0 million, $225.0 million and $95.0 million with our Canadian, Irish, U.K. and German subsidiaries each as a borrower, respectively. The term loans have a seven-year maturity.

(2) Represents an estimated $2,095.0 million to be invested in equity securities of Holdings by investment funds associated with or designated by the Sponsors and the management participants, including, Mr. Neubauer. See “The Transactions” below.

(3) Assumes approximately 180.3 million shares outstanding as of September 29, 2006 at $33.80, plus net option value of approximately $104.4 million which is calculated based on approximately 10.7 million options outstanding with an average exercise price of $24.02 per share, and 1.4 million restricted stock units at $33.80 per share.

(4) Consists of $147.4 million of estimated financing fees ($134.6 million of which will be capitalized and amortized over the related terms of the financings and $12.8 million related to bridge loan commitment fees which will be expensed immediately upon completion of the Transactions), $27.8 million of direct transaction costs, which will be expensed prior to or upon consummation of the Transactions and reflected as an adjustment to historical equity and $124.9 million of direct acquisition costs.

3

b) The following table sets forth the calculation related to the preliminary allocation of purchase price with respect to the Transactions:

| (in millions) | ||||||

Total purchase price(1) | $ | 5,795.2 | ||||

Fees/expenses directly related to the Transactions | 124.9 | |||||

Total | 5,920.1 | |||||

Net assets acquired before adjustments | 1,521.6 | |||||

ARAMARK transaction costs(2) | (19.0 | ) | ||||

Impact of acceleration of vesting of options outstanding and restricted stock units(3) | 34.7 | |||||

Net assets acquired | 1,537.3 | |||||

Estimated purchase price in excess of net assets acquired | 4,382.8 | |||||

Allocations to assets/liabilities acquired: | ||||||

Equity method investees and other investments(4) | 188.1 | |||||

Contract rights and other customer related intangibles, net(5) | 1,346.7 | |||||

Long-term debt(6) | 45.7 | |||||

Other assets | (3.8 | ) | ||||

Other noncurrent liabilities(7) | (110.7 | ) | ||||

| 1,466.0 | ||||||

Deferred income taxes(8) | (566.7 | ) | ||||

Preliminary adjustments to net assets acquired | 899.3 | |||||

Pro forma adjustment to goodwill | $ | 3,483.5 | ||||

(1) Represents the investment to purchase all outstanding shares, restricted stock units, and stock options (see note (a)), less carryover basis adjustment of $449.0 million (see note (d)).

(2) ARAMARK will record charges totaling $31.0 million prior to the Transactions, primarily related to change in control payments to certain executives ($22.7 million) and the settlement of certain shareholder litigation matters ($5.0 million). Of the $31.0 million, $3.3 million is reflected as an adjustment to other assets. The net after tax impact of these transactions is $19.0 million. The tax benefits associated with these charges are reflected as adjustments to accrued expenses and other current liabilities.

(3) Immediately prior to the consummation of the Transactions, 5.9 million unvested options outstanding and 0.9 million unvested restricted stock units outstanding will become fully vested. The resulting net increase in shareholders’ equity of $34.7 million will be recorded as an adjustment prior to the Transactions. The tax benefits associated with these shareholders’ equity transactions are reflected as adjustments to accrued expenses and other current liabilities.

(4) Represents the estimated adjustment to fair value of ARAMARK’s investment in two equity method investees, and the adjustment to estimated fair value of a cost method investment, reflected in adjustments to other assets.

4

(5) For purposes of these pro forma condensed consolidated financial statements, preliminary fair values and useful lives of contract rights and other customer related intangibles have been estimated based on our specific experience with acquired businesses in prior years. These estimates follow:

| (in millions) | Estimated average useful life | Estimated fair value | Historical cost | Purchase accounting adjustment | |||||||

Contract rights and other customer related intangibles | 10 years | $ | 1,644.7 | $ | 298.0 | $ | 1,346.7 | ||||

Goodwill is not amortized and will be evaluated for impairment on an annual basis. The value related to our trade name is not yet estimable and is currently included in goodwill. No adjustment to fair value has been made with respect to tangible property. Any required purchase price allocation adjustments would be recorded upon completion of appraisals subsequent to the completion of the Transactions. In addition, there may be other fair value adjustments that we have not yet estimated.

(6) Reflects fair value adjustment to assumed long-term debt not repaid, specifically the existing senior notes due 2012.

(7) Represents the estimated adjustment to recognize the unfunded projected benefit obligation of several defined benefit pension plans ($14.0 million) and the assumption of the liability of a non-qualified defined contribution plan previously funded with deferred stock units ($96.7 million).

(8) Reflects the estimated deferred taxes related to the purchase accounting adjustments calculated at a 38.6% effective tax rate.

c) Reflects the capitalization of $134.6 million of estimated financing costs that we will incur in connection with the senior secured credit facilities and the notes.

d) Adjustment to shareholders’ equity consists of the following:

| (in millions) | ||||

Sponsor and management participants equity contribution | $ | 2,095.0 | ||

Less: estimated carryover basis adjustment(1) | (449.0 | ) | ||

Less: impact on shareholders’ equity due to assumption of MergerCo swap(2) | (12.1 | ) | ||

Less: MergerCo bridge loan commitment fee expense | (7.9 | ) | ||

Less: historical equity | (1,521.6 | ) | ||

Net increase in shareholders’ equity | $ | 104.4 | ||

It is anticipated that a portion of the management participant equity contribution will have certain put rights which, upon finalizing the Transactions, will likely result in some portion or all (up to $95.0 million) of such contribution being classified outside of shareholders’ equity in the ARAMARK consolidated financial statements.

5

(1) ARAMARK’s Chairman and Chief Executive Officer held an equity investment in the Company prior to the Transactions and will continue to hold an equity interest in Holdings subsequent to the Transactions. In accordance with Emerging Issues Task Force Issue No. 88-16, Basis in Leveraged Buyout Transactions, an adjustment is recorded to reflect the deemed dividend and the estimated predecessor basis.

(2) In connection with the Transactions, MergerCo entered into an interest rate swap transaction fixing the rate on $1.5 billion of variable rate debt to be incurred in connection with the Transactions. The swap was designated as a cash flow hedge. The Company will assume the swap as part of the Merger. This adjustment records the fair value of the swap arrangement at the date on which the Transactions are completed, estimated to be $19.8 million at September 29, 2006, net of deferred taxes of $7.7 million. The fair value of the swap is reflected as adjustments to deferred income taxes and other non-current liabilities.

6

Unaudited pro forma condensed consolidated statement of income

for the year ended September 29, 2006

| (in millions) | ARAMARK historical | Pro forma adjustments | Pro forma ARAMARK | ||||||||

Sales | $ | 11,621.2 | $ | — | $ | 11,621.2 | |||||

Costs and expenses: | |||||||||||

Cost of services provided | 10,572.5 | 3.8 | (a) | 10,576.3 | |||||||

Depreciation and amortization | 339.3 | 134.7 | (a) | 474.0 | |||||||

Selling and general corporate expense | 178.9 | (6.4 | )(b) | 172.5 | |||||||

Operating income | 530.5 | (132.1 | ) | 398.4 | |||||||

Interest and other financing costs, net | 139.9 | 451.0 | 590.9 | (c) | |||||||

Income/(loss) before income taxes | 390.6 | (583.1 | ) | (192.5 | ) | ||||||

Provision/(benefit) for income taxes | 129.2 | (225.3 | )(d) | (96.1 | ) | ||||||

Income/(loss) from continuing operations(e) | $ | 261.4 | $ | (357.8 | ) | $ | (96.4 | ) | |||

See accompanying notes to unaudited pro forma condensed consolidated statement of income

7

Notes to unaudited pro forma condensed consolidated statement of income

a) Represents change in amortization based upon preliminary estimates of fair value and useful lives of client contract rights and other customer based intangible assets (see note (b) under “—Notes to unaudited pro forma condensed consolidated balance sheet”).

b) Reflects adjustment to eliminate Transaction-related costs incurred during fiscal 2006.

c) Reflects pro forma interest expense resulting from our new capital structure, as follows:

(in millions)

Existing indebtedness | $ | 27.7 | |

Receivables facility(1) | 13.1 | ||

Senior secured revolving credit facility(2) | 11.6 | ||

Senior secured term loan facility(3) | 286.2 | ||

Senior secured synthetic letter of credit facility(4) | 6.3 | ||

Notes | 213.3 | ||

Other(5) | 32.7 | ||

| $ | 590.9 | ||

(1) Reflects estimated costs on the $211.0 million receivables facility.

(2) Reflects interest on the historical revolving borrowings adjusted to reflect the anticipated interest rate of LIBOR plus 2.00% and the commitment fee on the portion of the revolving credit facility that is expected to be undrawn.

(3) Reflects interest on the $3,660.0 million term loan facility that is expected to be at a rate of LIBOR plus 2.50%.

(4) Marginal interest rate on the $250.0 million synthetic letter of credit facility that is expected to be at a rate of 2.50%.

(5) Includes amortization of estimated financing costs ($19.2 million), amortization of the fair value adjustment to assumed existing senior notes due 2012 ($8.0 million), additional interest expense related to the liability assumed of a non-qualified defined contribution plan previously funded with deferred stock units ($5.5 million).

A 0.125% change in interest rates on our total pro forma debt would change the total amount of pro forma annual interest expense by approximately $8.8 million.

d) Represents the income tax effect of the pro forma adjustments, calculated at an effective tax rate of 38.6%.

e) The pro forma condensed consolidated statement of income does not include the effects of the following non-recurring items:

The Company expects to grant stock options to management participants in connection with the Transactions. The terms and amounts of the options have not been finally determined and therefore the related compensation expense cannot be estimated at this time. The fiscal 2006 historical share-based compensation of $22.0 million is included in the above pro forma condensed consolidated statement of income. Share-based compensation expense may vary materially from the historical fiscal 2006 amounts as a result of the management participant option grants discussed above.

8

In connection with the Transactions, the Company will issue restricted stock units with an estimated fair value of approximately $11.0 million to certain of our senior management in consideration for such senior managers waiving the right to receive certain change of control payments and benefits existing in their current employment contracts. These restricted stock units will vest on the one year anniversary of the Transactions and will be recorded as compensation expense in the post-acquisition period. This amount has not been reflected in the pro forma condensed consolidated financial statements.

9

The Transactions

On August 8, 2006, MergerCo, FinanceCo and ARAMARK entered into the Merger Agreement, pursuant to which the parties agreed to the Merger, subject to the terms and conditions therein. At the effective time of the Merger, each outstanding share of our Class A Common Stock, par value $0.01 per share (“Class A common stock”), and Class B Common Stock, par value $0.01 per share (the “Class B common stock,” and together with the Class A common stock, the “common stock”) (other than shares held in treasury, shares held by MergerCo, RMK Finance LLC (“FinanceCo”), our “parent companies” (as defined below) or any direct or indirect wholly-owned subsidiary of MergerCo, FinanceCo, our parent companies or the Company and other than shares as to which a stockholder has properly exercised appraisal rights) will be converted into the right to receive $33.80 in cash. On December 20, 2006, at a special meeting of our stockholders, holders of shares representing approximately 86% of our outstanding voting power voted in favor of the Merger Agreement. Accordingly, upon the closing of the Transactions, ARAMARK stockholders will receive $33.80 in cash for each share of ARAMARK common stock held.

Investment funds associated with or designated by the Sponsors will invest approximately $1,800.0 million in equity securities of Holdings as part of the Transactions. In addition, Mr. Neubauer has agreed to contribute up to approximately 8.5 million shares of Class A common stock (having an aggregate value of up to $250.0 million) to Holdings. As described below approximately 250 members of the Company’s management are being offered the opportunity to invest in the equity of Holdings in connection with the Transactions. These other members of our management who invest in Holdings, along with Mr. Neubauer, are referred to as the “management participants.” Mr. Neubauer’s investment will be reduced by up to $50.0 million to the extent that the other management participants invest more than $50.0 million in the equity of Holdings. We currently expect that Mr. Neubauer and the other management participants will contribute equity of approximately $295.0 million.

In addition to the equity investments described above, the purchase of the company by the Investors will be financed by borrowings under our new senior secured credit facilities, the funding under our amended receivables facility and the issuance of the notes .

In addition, in May 2005, our subsidiary, ARAMARK Services, Inc. (“ARAMARK Services”), issued to the public $250.0 million aggregate principal amount of unsecured 5.00% senior notes due 2012. The entire principal amount of these senior notes will remain outstanding and unsecured after completion of the merger. The existing senior notes due 2012 are not, and as a result of the Transactions will not become, guaranteed by any of our subsidiaries or secured by any of our assets. Substantially all of the Company’s other existing senior notes will be redeemed or otherwise refinanced in connection with the merger and related transactions.

10

The following table illustrates the currently expected estimated sources and uses of the funds for the Transactions as if the closing had occurred on September 29, 2006 (our fiscal year end). Actual amounts will vary from estimated amounts depending on several factors, including differences between the balances of our outstanding indebtedness that we are redeeming as of September 29, 2006 and at the closing of the Transactions, differences from our estimate of fees, expenses and other costs related to the Transactions, differences between the cash balance at September 29, 2006 and at the closing of the Transactions, differences from our estimate of funding on our receivables facility due to a difference in the amount of eligible receivables at the closing of the Transactions and any changes made to the sources of the contemplated debt financing.

| (in millions) | |||

Sources of funds: | |||

Senior secured credit facilities: | |||

Revolving credit facility(1) | $ | — | |

Term loan facility(2) | 3,660.0 | ||

Receivables facility(3) | 211.0 | ||

Senior notes | 1,700.0 | ||

Senior subordinated notes | 570.0 | ||

Other retained indebtedness(4) | 353.0 | ||

Equity contribution(5) | 2,095.0 | ||

Total sources | $ | 8,589.0 | |

Uses of funds: | |||

Purchase price(6) | $ | 6,244.2 | |

Refinance of existing indebtedness(1)(7) | 1,636.3 | ||

Other retained indebtedness(4) | 353.0 | ||

Cash to balance sheet | 55.5 | ||

Estimated fees and expenses(8) | 300.0 | ||

Total uses | $ | 8,589.0 | |

| (1) | Upon the closing of the Transactions, we will enter into a $600.0 million senior secured revolving credit facility with a six-year maturity. As of September 29, 2006, on a pro forma basis after giving effect to the Transactions and the redemption of certain of our existing indebtedness, we would have had no borrowings outstanding under our revolving credit facility. As a result of our seasonal working capital requirements, however, we anticipate that we will borrow approximately $150.0 million under such revolving credit facility at closing. This balance is expected to be paid down during the course of fiscal 2007 in accordance with our seasonal working capital fluctuations. |

| (2) | Upon the closing of the Transactions, we will enter into a new $3,660.0 million senior secured term loan facility with a seven-year maturity, the full amount of which will be borrowed on the closing date. We will also enter into a $250.0 million synthetic letter of credit facility. On the closing date of the Transactions, we plan to issue approximately $200.0 million in letters of credit under this facility. |

11

| (3) | As of September 29, 2006, on a pro forma basis after giving effect to the Transactions, we would have had $211.0 million outstanding under our receivables facility ($186.0 million of which is off-balance sheet). As a result of our estimate of additional eligible receivables, we anticipate that approximately $225.0 million of the receivables facility will be outstanding on the closing of the Transactions ($200.0 million of which is expected to be off-balance sheet). Because sales of receivables under the receivables facility depend, in part, on the amount of eligible receivables, the amount of available funding under this facility may fluctuate from our estimated amount to be funded at closing and over time. |

| (4) | Consists of $250.0 million aggregate principal amount of ARAMARK Services’ existing senior notes due 2012, $54.3 million of capital lease obligations and $48.7 million of senior unsecured borrowings by certain of our foreign subsidiaries which shall remain outstanding after the consummation of the Transactions. The existing senior notes due 2012 are guaranteed only by ARAMARK Corporation and will remain unsecured after the consummation of the Transactions. This guarantee will rank equal in right of payment to all of the notes. |

| (5) | Represents the sum of (a) cash equity investments of approximately $1,800.0 million to be made in Holdings by the Sponsor Funds and (b) approximately $295.0 million of equity that we expect the management participants, including Mr. Neubauer, to invest. |

| (6) | The holders of our outstanding shares of common stock will receive $33.80 in cash per share in connection with the Transactions, except for certain senior managers of the Company who will be permitted to rollover their current equity interests in the Company. In addition, Mr. Neubauer has agreed to contribute to Holdings up to approximately 8.5 million shares of the Company’s common stock having an aggregate value of up to $250.0 million. Holders of outstanding stock options will receive in cash the excess of $33.80 over the applicable per share exercise price for each stock option held, whether vested or unvested. Holders of restricted stock units and director deferred stock units will receive $33.80 in cash for each share subject to the restricted stock units or deferred stock units held, whether vested or unvested. As of December 29, 2006, we had: |

| • | 180.8 million shares of our common stock outstanding; |

| • | 9.9 million shares subject to outstanding stock options, with a range of exercise prices from $9.35 to $33.45; and |

| • | 1.5 million shares in the aggregate subject to outstanding restricted stock units and director deferred stock units. |

| (7) | We will redeem on the date that is 30 days after the closing of the Transactions the following series of notes. On the closing date of the Transactions, irrevocable notice of the redemption will be provided to the holders of each series, and the outstanding aggregate principal amount of each series (together with any redemption premium and accrued and unpaid interest up to but not including the scheduled redemption date) will be set aside for the redemption. See also note (8) below. |

| (in millions) | |||

6.375% notes due February 2008 | $ | 300.0 | |

7.00% notes due May 2007 | 300.0 | ||

7.25% notes and debentures due August 2007 | 30.7 | ||

Total | $ | 630.7 | |

| Other indebtedness to be repaid includes $326.1 million under our existing U.S. and Canadian senior credit facility, $262.9 million under our existing European/Multicurrency senior credit facility, $65.9 million of bank term loans, $211.0 million ($186.0 million of which is off-balance sheet) under our existing receivables facility and $17.4 million of other obligations. |

| Also includes repayment of the $125.0 million aggregate principal amount of the 7.10% notes due December 2006 prior to the closing date. Does not include approximately $80.0 million borrowed on December 1, 2006 to consummate the acquisition of Overall Laundry Services, Inc. |

| (8) | Reflects our estimate of fees, expenses and other costs associated with the Transactions. Such fees and expenses include placement and other financing fees as well as advisory fees, transaction fees paid to affiliates of the Sponsors, and other transaction costs and professional fees, including a premium of approximately $5.9 million relating to the redemption of the notes discussed in note (7) above. |

12

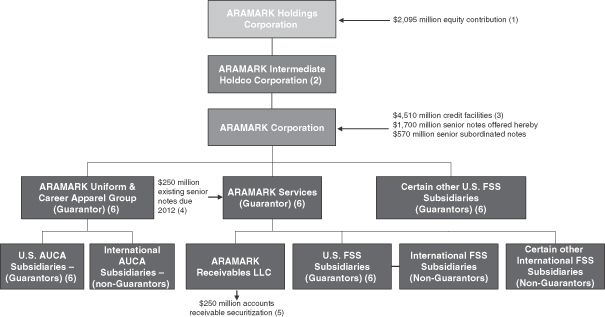

Ownership structure

As set forth in the diagram below, following consummation of the Transactions, all of our issued and outstanding capital stock will be held by ARAMARK Intermediate Holdco Corporation, a wholly-owned subsidiary of Holdings. We expect the Sponsor Funds will own approximately 86.0% of the outstanding capital stock of Holdings as of the closing date. The remainder of the capital stock of Holdings will be held by the Company’s management. See “The Transactions.” This structure will be achieved through a series of equity contributions expected to occur in connection with the Merger. Holdings and ARAMARK Intermediate Holdco Corporation, which we refer to collectively as our “parent companies,” have been formed for the purpose of consummating the Transactions. We will continue to own the same operating assets after the Transactions.

| (1) | Represents the sum of (i) cash equity investments of approximately $1,800.0 million to be made in Holdings by the Sponsor Funds and (ii) approximately $295.0 million of equity of the management participants, including Mr. Neubauer. |

| (2) | ARAMARK Intermediate Holdco Corporation will guarantee the credit facilities, but not the notes. |

| (3) | Upon the closing of the Transactions, we will enter into (i) a new $3,660.0 million term loan facility with a seven-year maturity, the full amount of which will be borrowed on the closing date; (ii) a $250.0 million synthetic letter of credit facility (of which we plan to issue approximately $200.0 million in letters of credit on the closing date); and (iii) a $600.0 million revolving credit facility with a six-year maturity. As of September 29, 2006, on a pro forma basis after giving effect to the Transactions and the redemption of certain of our existing indebtedness, we would have had no borrowings outstanding under our synthetic letter of credit facility and our revolving credit facility. As a result of our seasonal working capital requirements, however, we anticipate that we will utilize approximately $150.0 million of borrowing capacity under such credit facility at closing. The balance is expected to be paid down during the course of fiscal 2007 in accordance with our seasonal working capital fluctuations. |

| (4) | Consists of $250.0 million aggregate principal amount of ARAMARK Services’ existing senior notes due 2012. The entire principal amount of these senior notes will remain outstanding and unsecured after completion of the Transactions. These notes are guaranteed only by ARAMARK. This guarantee will rank equal in right of payment to both the senior notes and the senior subordinated notes. |

| (5) | Our amended receivables facility will provide for up to $250.0 million of funding, based, in part, on the amount of eligible receivables. We estimate that approximately $225.0 million of the receivables facility will be funded at the closing of the Transactions. Because sales of receivables under the receivables facility depend, in part, on the amount of eligible receivables, the amount of available funding under this facility may fluctuate from our estimated amount to be funded at closing and over time. |

| (6) | Only existing or subsequently acquired domestic subsidiaries of the Company that guarantee the senior secured credit facilities will guarantee the notes, subject to certain limited exceptions. |

13

Certain Non-GAAP Financial Measures

EBITDA is defined as income from continuing operations before cumulative effect of change in accounting principle plus provision for income taxes, interest and other financing costs, net, and depreciation and amortization. Adjusted EBITDA is defined as EBITDA further adjusted to give effect to adjustments required in calculating covenant ratios and compliance under the indentures governing the notes and our new senior secured credit facilities. EBITDA and Adjusted EBITDA are not presentations made in accordance with GAAP, are not measures of financial performance or condition, liquidity or profitability, and should not be considered as an alternative to (1) net income, operating income or any other performance measures determined in accordance with GAAP or (2) operating cash flows determined in accordance with GAAP. Additionally, EBITDA and Adjusted EBITDA are not intended to be measures of free cash flow for management’s discretionary use, as they do not consider certain cash requirements such as interest payments, tax payments and debt service requirements.

Our presentation of EBITDA has limitations as an analytical tool, and you should not consider it in isolation or as a substitute for analysis of our results as reported under GAAP. We believe that the presentation of EBITDA and Adjusted EBITDA is appropriate to provide additional information about the calculation of certain financial covenants in the indentures governing the notes and our new senior secured credit facilities. Adjusted EBITDA is a material component of these covenants. For instance, both the indentures governing the notes and our new senior secured credit facilities contain financial ratios that are calculated by reference to Adjusted EBITDA. Non-compliance with the financial ratio maintenance covenants contained in our new senior secured credit facilities could result in the requirement to immediately repay all amounts outstanding under such facilities, while non-compliance with the debt incurrence ratio contained in our new senior secured credit facilities and the indentures governing the notes would prohibit us from being able to incur additional indebtedness other than pursuant to specified exceptions.

Because not all companies use identical calculations, these presentations of EBITDA and Adjusted EBITDA may not be comparable to other similarly titled measures of other companies.

The following table sets forth a reconciliation of net income from continuing operations before cumulative effect of change in accounting principle to EBITDA and EBITDA to Adjusted EBITDA for the periods indicated:

| Fiscal year(a) | |||||||||||||||||||||

| (in millions) | 2002 | 2003 | 2004 | 2005 | 2006 | Pro Forma 2006 | |||||||||||||||

| (unaudited) | |||||||||||||||||||||

Income/(loss) from continuing operations before cumulative effect of change in accounting principle | $ | 251.3 | $ | 265.4 | $ | 263.1 | $ | 288.5 | $ | 261.4 | $ | (96.4 | ) | ||||||||

Interest and other financing costs, net | 136.4 | 142.5 | 122.4 | 127.0 | 139.9 | 590.9 | |||||||||||||||

Provision/(benefit) for income taxes | 141.9 | 144.1 | 152.1 | 164.7 | 129.2 | (96.1 | ) | ||||||||||||||

Depreciation and amortization | 229.6 | 263.0 | 298.0 | 320.1 | 339.3 | 474.0 | |||||||||||||||

EBITDA | $ | 759.2 | $ | 815.0 | $ | 835.6 | $ | 900.3 | $ | 869.8 | $ | 872.4 | |||||||||

| �� | |||||||||||||||||||||

Non-cash options and restricted stock unit expense(b) | 3.5 | 22.8 | 22.8 | ||||||||||||||||||

Pro forma EBITDA for equity method investees(c) | 20.0 | 20.0 | 23.8 | ||||||||||||||||||

Pro forma EBITDA for certain acquisitions(d) | 1.6 | 6.8 | 6.8 | ||||||||||||||||||

Asset impairment and related charges in AUCA—Direct Marketing(e) | — | 46.3 | 46.3 | ||||||||||||||||||

Costs related to the Transactions | — | 6.4 | — | ||||||||||||||||||

Equity investee gain on real estate sale | (9.7 | ) | — | — | |||||||||||||||||

Costs to exit our West Africa offshore oil services business and U.K. severance cost | 7.4 | — | — | ||||||||||||||||||

Contract termination and related costs | — | 4.7 | 4.7 | ||||||||||||||||||

Senior management severance and reorganization costs | — | 3.8 | 3.8 | ||||||||||||||||||

New Orleans Convention Center delayed re-start adjustment(f) | — | (2.6 | ) | (2.6 | ) | ||||||||||||||||

Unusual receivables write-off(g) | — | 3.1 | 3.1 | ||||||||||||||||||

Other miscellaneous items | — | 2.2 | 2.2 | ||||||||||||||||||

Adjusted EBITDA | $ | 923.1 | $ | 983.3 | $ | 983.3 | |||||||||||||||

| (a) | Fiscal years 2002, 2003, 2004, 2005 and 2006 refer to the fiscal years ended September 27, 2002, October 3, 2003, October 1, 2004, September 30, 2005, and September 29, 2006, respectively. Fiscal 2003 is a 53-week year. All other periods presented are 52-week years. |

| (b) | Represents compensation expense for stock option and restricted stock unit awards. |

| (c) | Represents our share of EBITDA from AIM Services Co., Ltd. ($13.0 million) and SMG ($7.0 million) equity method investments not already reflected in our EBITDA. EBITDA for these equity method investees is calculated in a manner consistent with our EBITDA on a consolidated basis but does not necessarily represent cash distributions received from these investees. Pro forma 2006 includes additional amortization of $3.8 million related to purchase accounting. |

14

| (d) | Represents the annualizing of EBITDA from acquisitions made during the respective periods. For fiscal 2006 and pro forma 2006 this adjustment includes EBITDA for the twelve months ended September 29, 2006 relating to the acquisition of Overall Laundry Services, Inc. on December 1, 2006 for a purchase price of $80.3 million. Overall Laundry Services, a uniform rental services provider based in Everett, Washington, generated revenues of $38.8 million and operating income of $1.0 million during the year ended December 31, 2005. We are implementing certain cost savings measures with respect to this acquisition. |

| (e) | Represents charges for goodwill impairment ($35.0 million) and for asset/liability adjustments ($11.3 million) related to our decision to exit the healthcare uniform business. |

| (f) | Reflects estimated impact of delayed re-start of operations at the New Orleans Convention Center post Hurricane Katrina ($5.0 million) net of related insurance proceeds related to Hurricane Katrina received in fiscal 2006 ($7.6 million). |

| (g) | Reflects unusual write-offs associated with various contract renegotiations and client bankruptcies. |

(in millions) | |||

Pro forma credit statistics: | |||

Ratio of total debt (including receivables facility) to Adjusted EBITDA(a) | 6.6x | ||

Cash interest expense(b) | $ | 554.2 | |

Ratio of Adjusted EBITDA to cash interest expense | 1.8x | ||

Ratio of Adjusted EBITDA less capital expenditures, net of disposals to cash interest expense | 1.3x | ||

| (a) | Total debt for purposes of this ratio represents total pro forma debt plus off-balance sheet financing under our receivables facility and the full face value amount of our existing senior notes due 2012. |

| (b) | Cash interest expense consists of pro forma interest on our new senior secured credit facilities, senior notes, senior subordinated notes and our existing debt. |

15

Legal proceedings

In connection with our acquisition of certain assets of Fine Host Corporation, we received and have cooperated with document requests from the United States Attorney’s Office for the Southern District of New York and the United States Department of Agriculture’s Office of Inspector General regarding certain billing practices that Fine Host Corporation put in place prior to our acquisition of the assets of Fine Host Corporation. On September 30, 2005, we signed a settlement agreement with Fine Host Corporation in connection with certain claims for indemnification we had made under our acquisition agreement with Fine Host Corporation.

Our business is subject to various federal, state and local laws and regulations governing, among other things, the generation, handling, storage, transportation, treatment and disposal of water wastes and other substances. We engage in informal settlement discussions with federal, state and local authorities regarding allegations of violations of environmental laws at operations relating to primarily our uniform rental segment or to businesses conducted by our predecessors, the aggregate amount of which and related remediation costs we do not believe should have a material adverse effect on our financial condition or results of operations.

From time to time, we are a party to various legal actions involving claims incidental to the conduct of our business, including actions by clients, customers, employees and third parties, including under federal and state employment laws, wage and hour laws, customs, import and export control laws and dram shop laws. Based on information currently available, advice of counsel, available insurance coverage, established reserves and other resources, we do not believe that any such current actions are likely to be, individually or in the aggregate, material to our business, financial condition, results of operations or cash flows. However, in the event of unexpected further developments, it is possible that the ultimate resolution of these matters, or other similar matters, if unfavorable, may be materially adverse to our business, financial condition, results of operations or cash flows.

In July 2004, the Company learned that it was under investigation by the United States Department of Commerce, among others, relating to Galls, a division of the Company, in connection with record keeping and documentation of certain export sales. The Government obtained and received numerous records from the Company, which is cooperating in the investigation.

In March 2000, Antonia Verni, by guardian ad litem, and Fazila Verni sued the Company and certain affiliates, along with Ronald Verni, David Lanzaro, the New Jersey Sports & Exposition Authority, the N.Y. Giants, Harry M. Stevens, Inc. of New Jersey, Shakers, The Gallery, Toyota Motors of North America, Inc. and the National Football League, for monetary damages for injuries they suffered. On January 18 and 19, 2005, a New Jersey jury found ARAMARK Corporation and certain affiliates liable for approximately $30 million in compensatory damages and $75 million in punitive damages in connection with an automobile accident caused by an intoxicated driver who attended a professional football game at which certain affiliates of the Company provided food and beverage service. The Company and its affiliates appealed the judgment to the Appellate Division of Superior Court of New Jersey on April 13, 2005. On August 3, 2006, the Appellate Division of the Superior Court issued its decision reversing the entire verdict of the trial court. The Appellate Division cited multiple errors by the trial court and reversed the finding of liability against the Company and its affiliates. The Appellate Division reversed both the compensatory and punitive damage awards and remanded the matter back to the trial court for a new trial. On September 6, 2006, the plaintiffs filed a petition for certification concerning the Appellate Division decision with the New Jersey Supreme Court and the New Jersey Supreme Court has not yet ruled on the petition. The Company and its affiliates intend to defend themselves vigorously in this matter.

16

On May 1, 2006, two cases were filed in the Court of Chancery of the State of Delaware in New Castle County against the Company and each of the Company’s directors. The two cases are putative class actions brought by stockholders alleging that the Company’s directors breached their fiduciary duties to the Company in connection with the proposal from a group of investors led by Mr. Neubauer to acquire all of the outstanding shares of the Company. On May 22, 2006, two additional cases making substantially identical allegations were brought against the Company and certain of its directors, one in the Court of Common Pleas in Philadelphia, Pennsylvania (in which only the Company and Mr. Neubauer were named as defendants) and another in the Court of Chancery of the State of Delaware in New Castle County (in which the Company and all directors were named as defendants). All of the cases make claims for monetary damages, injunctive relief and attorneys’ fees and expenses. On June 7, 2006, the Court of Chancery of the State of Delaware consolidated the three pending Delaware actions as In re: ARAMARK Corporation Shareholders Litigation.

On or around August 11, 2006, a fourth punitive class action complaint was filed in the Court of Chancery of the State of Delaware in New Castle County by the City of Southfield Police and Fire Retirement System purportedly on behalf of the Company’s stockholders. The complaint names the Company and each of the Company’s directors as defendants and alleges that the defendants breached their fiduciary duties to the stockholders in connection with the proposed acquisition of the Company’s outstanding shares and making claims for monetary damages, injunctive relief and attorneys’ fees and expenses. On August 25, 2006, the Court of Chancery of the State of Delaware consolidated this action with In re: ARAMARK Corporation Shareholders Litigation. The parties have entered into agreements in principle to settle the Delaware consolidated actions and the action pending in the Pennsylvania Court of Common Pleas. The agreements in principle remain subject to court approval. As part of the agreements in principle, each share of Class A common stock beneficially owned by members of ARAMARK’s management committee (Joseph Neubauer, L. Frederick Sutherland, Bart J. Colli, Timothy P. Cost, Andrew C. Kerin, Lynn B. McKee, Ravi K. Saligram and Thomas J. Vozzo) was counted as one vote for purposes of the additional vote to approve the adoption of the merger agreement. In connection with settling the Delaware action in principle, counsel for the plaintiffs has agreed to seek court approval of no more than $2.1 million in attorneys’ fees and expenses, which amount the Company has agreed not to oppose. In connection with settling the Pennsylvania action in principle, we expect counsel for the plaintiffs to make a demand for a reasonable amount of attorneys’ fees and expenses, which amount has not yet been determined.

In June 2006, the Bermuda Monetary Authority (BMA) presented a winding up petition to the Supreme Court of Bermuda as to Hatteras Re, a Bermuda reinsurance company which participates in a portion of ARAMARK’s casualty insurance program, to place it into provisional liquidation. A Joint Provisional Liquidator (JPL) was appointed and authorized to assume control of Hatteras Re’s business. At an official meeting of creditors on November 9, 2006, the creditors elected to keep the JPL as a Permanent Liquidator (PL) and ARAMARK was elected to the creditor’s committee. The activities of the PL are currently underway and ARAMARK’s insurance claims are being paid by Hatteras Re under the direction of the PL. A preliminary analysis by ARAMARK and its insurance advisors indicates Hatteras Re has access to funds sufficient to pay ARAMARK’s estimated insurance claims for the relevant program periods. ARAMARK has reached an agreement in principle with the PL that will allow ARAMARK to pursue with other insurance carriers an alternative insurance solution for the covered periods, however, the terms and conditions of such an arrangement have not yet been finally determined. While the ultimate outcome of this matter is uncertain, and dependent in part on future developments, based on the information currently available, ARAMARK does not expect the final resolution will have a material adverse effect on the consolidated financial statements.

17