Exhibit 99.1

|

| TRANSALTA CORPORATION NEWS RELEASE |

TransAlta Reports Fourth Quarter and Full Year 2013 Results, 2014 Outlook, Asset Sale, and Revised Dividend

CALGARY, Alberta (February 20, 2014) — TransAlta Corporation (“TransAlta”) (TSX: TA; NYSE: TAC) today reported its fourth quarter 2013 and full year 2013 financial results, its outlook for 2014 and two significant initiatives to enhance the Corporation’s financial strength to grow, provide a solid and sustainable dividend, and to ensure a strong balance sheet throughout the commodity cycle.

Comparable EBITDA(1) for the full year ending Dec. 31, 2013 was $1,023 million, an increase of $8 million from 2012. Strong performance in gas, renewables, and trading, more than offset the lower pricing in the Pacific Northwest and higher unplanned outages at Canadian Coal. Free Cash Flow(1) for the full year ending Dec. 31, 2013 increased by $37 million to $295 million, or $1.12 per share. Comparable EBITDA for the fourth quarter 2013 was $242 million compared to $312 million during the same period last year. Results were lower than last year due to lower prices in Alberta and the Pacific Northwest, icing events in Eastern Canada that impacted our wind results, and higher unplanned outages in Canadian Coal.

Comparable net earnings for the full year ending Dec. 31, 2013 were $81 million, or $0.31 per share. A reported net loss of $71 million ($0.27 per share) was recorded for the full year ending Dec. 31, 2013 due to a number of one-time items and the impact of certain de-designated and ineffective hedges. Comparable net earnings and reported net loss for the three months ending Dec. 31, 2013 were $1 million and $66 million, respectively.

Over the past five years, TransAlta has invested a large amount of capital in growth projects in our core markets which is a key part of our strategy. To enhance our ability to continue to execute on our growth strategy and be competitive, TransAlta also announced today two key initiatives; the sale of our 50 per cent interest in CE Generation, Blackrock development and Wailuku to our partner in these holdings, MidAmerican Renewables for U.S.$193.5 million and the resizing of our dividend to an annualized amount of $0.72 per common share to align with our growth and financial objectives. These initiatives, combined with actions we have taken since late 2012, will enhance the Corporation’s ability to execute its growth strategy, maintain a strong balance sheet and create shareholder value. Specifically, these two initiatives deliver a number of key benefits to security holders, including:

· Increasing cash flow per share

· Providing an attractive, sustainable dividend

· Improving the Corporation’s credit metrics and balance sheet

· Generating an additional $120 million per year in free cash flow

· Creating a stronger financial base for growing TransAlta and maintaining a strong balance sheet throughout the commodity cycle

(1) Comparable EBITDA refers to Earnings before interest, taxes, depreciation and amortization including finance lease income and adjusted for certain other items. Free Cash Flow refers to Funds from Operations less sustaining capital less preferred dividends less non-controlling interest payments. Comparable EBITDA, comparable net earnings attributable to common shareholders, funds from operations, free cash flow, comparable earnings per share, funds from operations per share, and free cash flow per share are not defined under International Financial Reporting Standards (“IFRS”). Presenting these measures from period to period provides supplemental information to help management and shareholders evaluate earnings’ and cash flow trends in comparison with prior periods’ results. Refer to the Non-IFRS Measures section of our Management’s Discussion and Analysis (“MD&A”) for further discussion of these items.

“Our growth strategy is unchanged and our ability to execute is enhanced through these two additional initiatives” said Dawn Farrell, President and CEO. “An attractive, sustainable dividend continues to be an important part of our approach to delivering value to shareholders. In addition, a strong investment grade balance sheet is critical for enhancing our ability to compete for growth opportunities.”

2014 Outlook

TransAlta expects comparable EBITDA for 2014 to be in the range of $1,015 and $1,065 million based on the current outlook for power prices in Alberta and the Pacific Northwest. Free Cash Flow is expected to be in the range of $293 to $343 million, or $1.07 and $1.26 per share, based on sustaining capital expenditures of approximately $350 million. With the revised dividend, our expected dividend is 57 per cent to 67 per cent of Free Cash Flow.

Recent Strategic Accomplishments

· Announced sale of CE Generation, Blackrock development, and Wailuku to MidAmerican Renewables

· The TAMA Transmission partnership between TransAlta and MidAmerican Transmission successfully qualified to compete in the next phase of the competitive bid process within Alberta for the Fort McMurray West 500 kV Transmission Project.

· Established the Fortescue River Gas Pipeline joint venture to build and own a $178 million natural gas pipeline in Western Australia to better serve our customers within that region. TransAlta’s interest in the joint venture is 43 per cent.

· Concluded a long-term contract extension with BHP Billiton’s Nickel West operations in Western Australia for 245 MW.

· Completed the acquisition of TransAlta’s first wind project in the United States. An economic interest in the 144 MW wind farm in Wyoming was purchased by TransAlta’s majority owned subsidiary, TransAlta Renewables Inc. (“TransAlta Renewables”).

· Formation of TransAlta Renewables, a sponsored vehicle by TransAlta. The 29 facilities within TransAlta Renewables are fully operational and 100 per cent contracted.

· Executed 24-year contract with the City of Riverside in California for 86 MW at CalEnergy LLC.

· Executed 24-year contract with Salt River Project in Arizona for 50 MW at CalEnergy LLC.

· Executed a 20-year contract with the Ontario Power Authority for 74 MW from the Ottawa Gas Facility.

Q4 2013 compared to Q4 2012

· Comparable EBITDA of $242 million down from $312 million for the same period last year

· Funds from Operations of $179 million down from $214 million for the same period last year

· Free Cash Flow of $61 million down from $74 million in 2012

· Availability of 91.8 per cent

Full year 2013 compared to full year 2012

· Comparable EBITDA of $1,023 million up from $1,015 million in 2012

· Funds from operations of $729 million down from $788 million in 2012

· Free cash flow of $295 million, an increase of $37 million from 2012

· Adjusted availability(1) of 87.8 per cent as compared to our annual target of 89 to 90 per cent. Lower availability is primarily attributed to the force majeure at Keephills Unit 1

(1) Adjusted for economic dispatching at Centralia Thermal, but not for Keephills Unit 1 force majeure.

Full Year Business Line Review by Segment

Generation

· Canadian Coal: Comparable EBITDA decreased $64 million to $309 million compared to $373 million in 2012. The main impact to the business in 2013 was increased unplanned outages compared to 2012 that could not be offset by lower planned outages. We also took over the Highvale Mine in 2013 and expanded the mine to be able to deliver coal to all six Sundance units and all three Keephills units. Planned major maintenance for this business sector has returned to normal levels after a large capital program in 2012 was completed.

· U.S. Coal: Comparable EBITDA decreased $82 million to $66 million in 2013 compared to $148 million in 2012. The decline in comparable EBITDA was primarily due to weak merchant pricing and the expiry of contracts. Fuel costs were lower in 2013 reflecting re-negotiated coal and rail costs. Capital was reduced significantly due to the long period of economic curtailment of these units under low prices.

· Gas: Comparable EBITDA increased $15 million to $327 million in 2013 compared to $312 million in 2012 primarily due to a full year of income from the Solomon power plant that was acquired in late 2012 and stronger merchant pricing in our Alberta business. Capital expenditures in this business were up $9 million to $58 million compared to 2012.

· Wind: Comparable EBITDA increased $29 million to $180 million in 2013 compared to $151 million in 2012 primarily due to higher prices in the Alberta market and the commencement of operations at the New Richmond facility in Québec.

· Hydro: Comparable EBITDA increased $20 million to $147 million in 2013 compared to $127 million in 2012 primarily due to favourable pricing in the Alberta market.

Energy Trading

· Comparable EBITDA increased $74 million to $61 million in 2013 compared to a loss of $13 million in 2012 due to strong trading performance across all markets and prudent management of risk.

Corporate

· OM&A expense decreased $16 million to $66 million in 2013 compared to $82 million in 2012 primarily due to lower compensation costs as a result of restructuring in the fourth quarter of 2012 and a continued focus on managing costs.

Full Year Consolidated Financial Review

Comparable EBITDA increased $8 million to $1,023 million in 2013 from $1,015 million for 2012, reflecting the higher gross margins in Gas, Wind, Hydro, and Energy Trading, which more than offset higher unplanned outages in Canadian Coal and lower pricing within our U.S. Coal business.

Despite higher comparable EBITDA, Funds from Operations for the year decreased $59 million to $729 million from $788 million for the same period last year primarily due to higher interest expenses and cash taxes, and differences in timing of cash proceeds associated with power hedges and coal inventories.

Free Cash Flow increased $37 million to $295 million in 2013 from $258 million in 2012 primarily due to lower sustaining capital expenditures associated with fewer planned outages in 2013 relative to 2012.

Comparable earnings for the year were $81 million ($0.31 per share) down from $117 million ($0.50 per share) in 2012. The decrease in comparable earnings is primarily due to an increase in depreciation and amortization, income taxes, and net interest, partially offset by an increase in comparable EBITDA.

A reported net loss of $71 million ($0.27 per share) was recorded for the year compared to a net loss of $615 million ($2.62 per share) last year. This year over year change is primarily driven by a decrease in asset impairment charges of $342 million, a decrease in costs associated with the return of Sundance Units 1 and 2 to service of $170 million, a decrease in the impact of write off of deferred income tax assets of $141 million partially offset by a provision of $42 million associated with a potential settlement related to California power markets during the 2000 - 2001 period.

Full Year Operating Review

· Fleet availability, including finance leases and equity investments, was 85.5 per cent compared to 88.4 per cent last year. Adjusting for economic dispatching at Centralia Thermal in our U.S. Coal business, availability was 87.8 per cent compared to 90.0 per cent in 2012. The decrease is mainly due to higher unplanned outages in our Canadian Coal business at the Alberta coal PPA facilities and the Keephills Unit 1 force majeure outage, partially offset by lower planned outages at the Alberta coal facilities.

· We completed the four major outages scheduled for 2013.

· Total sustaining expenditures were $341 million for the year compared to $439 million last year. Sustaining expenditures fell within our target range of $295-$345 million for 2013.

Significant Events

Sale of CE Generation

On Feb. 20, 2014, we announced the sale of our 50 per cent interest in CE Generation, Blackrock development and Wailuku to our partner in these holdings, MidAmerican Renewables for a price of U.S.$193.5 million.

Revised Dividend

On Feb. 20, 2014, our Board of Directors declared a quarterly dividend of $0.18 per common share (or $0.72 per common share on an annualized basis).

Sundance Unit 6 Agreement

On Feb. 19, 2014, we reached an agreement with the PPA Buyer related to the dispute on Sundance Unit 6. We don’t expect any material impact to the financial statements as a result of the agreement.

Wyoming Wind Acquisition

On Dec. 20, 2013, we completed the acquisition, through one of our wholly owned subsidiaries, of a 144 MW wind farm in Wyoming for approximately U.S.$102 million from an affiliate of NextEra Energy Resources, LLC. The wind farm is fully operational and contracted under a long-term PPA until 2028 with an investment grade counterparty. An economic interest in the wind farm was acquired by TransAlta Renewables from TransAlta in consideration for a payment equal to the original purchase price of the acquisition.

Western Australia Contract Extension

On Oct. 30, 2013, we announced a long-term contract extension to supply power to the BHP Billiton Nickel West operations in Western Australia from our Southern Cross Energy facilities (“Southern Cross”). The extension is effective immediately and replaces the previous contract which was set to expire at the beginning of 2014.

Operating since 1996, Southern Cross has a total installed capacity of 245 MW from the Kambalda, Mt. Keith, Leinster, and Kalgoorlie power stations.

Ottawa Facility’s Long-term Contract with Ontario Power Authority

On Aug. 30, 2013, we announced the execution of an agreement for a 20-year power supply term with the Ontario Power Authority for our Ottawa gas facility, effective January 2014. Under the new deal, the plant has become dispatchable. This will assist in reducing the incidents of surplus baseload generation in the market, while maintaining the ability of the system to reliably produce energy when it is needed.

This new contract will benefit our shareholders by providing long-term stable earnings from this facility and is also expected to benefit ratepayers of Ontario by securing attractively priced capacity from this existing facility, reducing the need for new capacity to be built in the future and allowing hospitals in the area to continue to be served with the steam they need for heat and other energy processes, in an environmentally friendly manner.

TransAlta Renewables

On Aug. 9, 2013, we transferred 28 indirectly owned wind and hydroelectric generating assets to TransAlta Renewables through the sale of all the issued and outstanding shares of two subsidiaries: Canadian Hydro Developers, Inc. and Western Sustainable Power Inc. The initial public offering resulted in an aggregate of 22.1 million common shares being issued for gross proceeds to TransAlta Renewables of $221 million. TransAlta, directly and indirectly, holds 92.6 million common shares, representing approximately 80.7 per cent of the common shares in TransAlta Renewables.

Sundance Units 1 and 2 Return to Service

In December 2010, Units 1 and 2 of our Sundance facility were shut down due to conditions observed in the boilers at both units. On July 20, 2012, an arbitration panel concluded that Unit 1 and Unit 2 were not economically destroyed and required TransAlta to return these units to service. Unit 1 returned to service on Sept. 2, 2013 and Unit 2 returned to service on Oct. 4, 2013.

The following table depicts key financial results and statistical operating data:

Fourth Quarter and 12 Months Ended Dec. 31 2013 Highlights

In $CAD millions, unless otherwise stated |

| 3 months |

| 3 months |

| 12 months |

| 12 months |

|

Adjusted availability (%)(1) |

| 91.8 |

| 89.4 |

| 87.8 |

| 90.0 |

|

Production (GWh) |

| 12,640 |

| 10,880 |

| 42,482 |

| 38,750 |

|

Revenue |

| 587 |

| 646 |

| 2,292 |

| 2,210 |

|

Comparable EBITDA(2) |

| 242 |

| 312 |

| 1,023 |

| 1,015 |

|

Reported Net Earnings (loss) attributable to common shareholders |

| (66 | ) | 39 |

| (71 | ) | (615 | ) |

Comparable Net Earnings attributable to common shareholders(2) |

| 1 |

| 55 |

| 81 |

| 117 |

|

Funds from Operations(2) |

| 179 |

| 214 |

| 729 |

| 788 |

|

Cash Flow from Operating Activities |

| 165 |

| 245 |

| 765 |

| 520 |

|

Free Cash Flow(2) |

| 61 |

| 74 |

| 295 |

| 258 |

|

|

|

|

|

|

|

|

|

|

|

Basic and Diluted Earnings (loss) per common share |

| (0.25 | ) | 0.15 |

| (0.27 | ) | (2.62 | ) |

Comparable Earnings per share(2) |

| 0.00 |

| 0.22 |

| 0.31 |

| 0.50 |

|

Funds from Operations per share(2) |

| 0.67 |

| 0.84 |

| 2.76 |

| 3.35 |

|

Free Cash Flow per share(2) |

| 0.23 |

| 0.29 |

| 1.12 |

| 1.10 |

|

Dividends paid per common share |

| 0.29 |

| 0.29 |

| 1.16 |

| 1.16 |

|

The complete report for the quarter, including MD&A and unaudited interim financial statements, as well as our quarterly presentation, will be available on the Investors section of our website: www.transalta.com.

Dividend Declarations

The Board of Directors of TransAlta today declared a quarterly dividend of $0.18 per share on common shares payable on April 1, 2014 to shareholders of record at the close of business March 4, 2014.

The Board of Directors of TransAlta also declared a quarterly dividend of $0.2875 per share on TransAlta’s issued and outstanding Cumulative Redeemable Rate Reset First Preferred Shares, Series A, payable on March 31, 2014 to shareholders of record at the close of business on March 4, 2014.

The Board of Directors of TransAlta also declared a quarterly dividend of $0.2875 per share on TransAlta’s issued and outstanding Cumulative Redeemable Rate Reset First Preferred Shares, Series C, payable on March 31, 2014 to shareholders of record at the close of business on March 4, 2014.

(1) Adjusted for economic dispatching at Centralia Thermal, but not for Keephills Unit 1 force majeure.

(2) Comparable EBITDA refers to Earnings before interest, taxes, depreciation and amortization including finance lease income and adjusted for certain other items. Free Cash Flow refers to Funds from Operations less sustaining capital less preferred dividends less non-controlling interest payments. Comparable EBITDA, comparable net earnings attributable to common shareholders, funds from operations, free cash flow, comparable earnings per share, funds from operations per share, and free cash flow per share are not defined under International Financial Reporting Standards (“IFRS”). Presenting these measures from period to period provides supplemental information to help management and shareholders evaluate earnings’ and cash flow trends in comparison with prior periods’ results. Refer to the Non-IFRS Measures section of our Management’s Discussion and Analysis (“MD&A”) for further discussion of these items.

The Board of Directors of TransAlta also declared a quarterly dividend of $0.3125 per share on TransAlta’s issued and outstanding Cumulative Redeemable Rate Reset First Preferred Shares, Series E, payable on March 31, 2014 to shareholders of record at the close of business on March 4, 2014.

TransAlta files year end disclosure documents

TransAlta also announced today it has filed its Annual Information Form, Audited Consolidated Financial Statements and accompanying notes, as well as its MD&A. These documents will be available through TransAlta’s website at www.transalta.com or through Sedar at www.sedar.com.

TransAlta has also filed its 40-F with the U.S. Securities and Exchange Commission. The form is available through their website at www.sec.gov. Paper copies of all documents are available to shareholders free of charge upon request.

Conference call

We will hold a conference call and web cast at 7:00 a.m. MT (9:00 a.m. ET) today to discuss fourth quarter, full year 2013 results and 2014 Outlook, as well as the asset sale and revised dividend. The call will begin with formal remarks by Dawn Farrell, President and CEO, and Brett Gellner, Chief Financial Officer and Chief Investment Officer, followed by a question and answer period for investment analysts, investors and other interested parties. A question and answer period for the media will immediately follow. Please contact the conference operator five minutes prior to the call, noting “TransAlta Corporation” as the company and “Brent Ward” as moderator.

Dial-in numbers:

Toll-free North American participants call: 1-800-319-4610

Outside of Canada & USA call: 1-604-638-5340

A link to the live webcast will be available on the Investor Centre section of TransAlta’s website at http://www.transalta.com/investor-centre/events-presentations/webcasts-conference-calls. If you are unable to participate in the call, the instant replay is accessible at 1-800-319-6413 (Canada and USA toll free) or 1-604-638-9010 (Outside of Canada) with TransAlta pass code 2231 followed by the # sign. A complete copy of TransAlta’s fourth quarter extended news release is available in the Investor Centre section of our website: www.transalta.com. A transcript of the broadcast will be posted on the website once it becomes available. Note: If using a hands-free phone, lift the handset and press one to ask a question.

TransAlta is a power generation and wholesale marketing company focused on creating long-term shareholder value. TransAlta maintains a low-to-moderate risk profile by operating a highly contracted portfolio of assets in Canada, the United States and Australia. TransAlta’s focus is to efficiently operate wind, hydro, natural gas and coal facilities in order to provide customers with a reliable, low-cost source of power. For over 100 years, TransAlta has been a responsible operator and a proud contributor to the communities in which it works and lives. TransAlta has been selected by Sustainalytics as one of Canada’s Top 50 Socially Responsible Companies since 2009 and is recognized globally for its leadership on sustainability and corporate responsibility standards by FTSE4Good.

This news release contains forward looking statements, including statements regarding the business and anticipated financial performance of TransAlta Corporation. In particular, this news release contains forward-looking statements pertaining to the sale of the Corporation’s interest in CE Generation, Blackrock development and Wailuku to the MidAmerican Renewables, a potential settlement related to California power markets as well as the Corporation’s expectations for its 2014 comparable EBITDA. Free Cash Flow, sustaining capital expenditures and dividend payout. These statements are based on TransAlta Corporation’s belief and assumptions based on information available at the time the assumptions were made. These statements are subject to a number of risks and uncertainties that may cause actual results to differ materially from those contemplated by the forward-looking statements. Some of the factors that could cause such differences include: operational risks involving our facilities, market prices where we operate, unplanned outages at generating facilities and the capital investments required, equipment failure and our ability to carry out repairs in a cost effective manner or timely manner, the effects of weather, disruptions in the source of fuels, water, or wind required to operate our facilities, energy trading risks, failure to obtain necessary regulatory approvals in a timely fashion, legislative or regulatory developments, competition, global capital markets activity, changes in prevailing interest rates, currency exchange rates, inflation levels, commodity, prices general economic conditions in geographic areas where TransAlta Corporation operates and successful completion of the conditions applicable to the sale of CE Generation, Blackrock development and Wailuku.

Note: All financial figures are in Canadian dollars unless noted otherwise.

For more information: |

|

|

|

Investor inquiries: | Media inquiries: |

|

|

Brent Ward | Stacey Hatcher |

Director, Corporate Finance and Investor Relations | Senior Corporate Relations Advisor |

Phone: 1-800-387-3598 in Canada and U.S. | Cell: 587-216-2242 |

Email: investor_relations@transalta.com | Toll-free media number: 1-855-255-9184 |

| Alternate local number: 403-267-2540 |

BASIS OF PRESENTATION

This news release should be read in conjunction with our 2013 audited consolidated financial statements and our 2013 Annual Management’s Discussion and Analysis (“MD&A”). In this news release, unless the context otherwise requires, ‘we’, ‘our’, ‘us’, the ‘Corporation’, and ‘TransAlta’ refers to TransAlta Corporation and its subsidiaries. The consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”). All tabular amounts in the following discussion are in millions of Canadian dollars unless otherwise noted. Certain financial measures included in this news release do not have a standardized meaning as prescribed by IFRS. These measures may not be comparable to similar measures presented by other issuers and should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS. See the Non-IFRS Measures section of this news release for additional information. This news release is dated Feb. 20, 2014. Additional information respecting TransAlta, including its Annual Information Form, is available on SEDAR at www.sedar.com.

RESULTS OF OPERATIONS

The results of operations are presented on a consolidated basis and by business segment. We have three business segments: Generation, Energy Trading, and Corporate. For this news release, we have further split what is reported as our Generation business segment into the various fuel types to provide additional information to our readers. In this news release, the impact of foreign exchange fluctuations on foreign currency denominated transactions and balances is discussed with the relevant Consolidated Statements of Earnings (Loss) and Consolidated Statements of Financial Position items. While individual line items in the Consolidated Statements of Financial Position may be impacted by foreign exchange fluctuations, the net impact of the translation of these items relating to foreign operations to our presentation currency is reflected in accumulated other comprehensive income (loss) (“AOCI”) in the equity section of the Consolidated Statements of Financial Position.

HIGHLIGHTS

Fourth Quarter Highlights

Strategic Highlights

· Announced plans to build and own (TransAlta ownership 48 per cent) a $178 million natural gas pipeline to our Solomon power station.

· Acquired 144 megawatt (“MW”) wind farm in Wyoming.

· TAMA Transmission LP (“TAMA transmission”) successfully qualified to participate as a proponent in the Fort McMurray West 500 kilovolt Transmission Project.

Operational Financial Results

· Consolidated: Comparable earnings before interest, taxes, depreciation, and amortization (“EBITDA”) for 2013 decreased $70 million to $242 million. The decline in comparable EBITDA from our Canadian and United States (“U.S.”) coal operations, gas, and hydro could not be offset by the improvements in wind and trading. Higher unplanned outages at our Alberta coal Power Purchase Arrangement (“PPA”) facilities, and lower pricing at Centralia Thermal contributed to the bulk of the decline in the coal business in 2013.

· Canadian Coal: In 2013, comparable EBITDA was $68 million compared to $102 million in 2012. The decrease in comparable EBITDA resulted from higher coal costs, unfavourable market pricing, and higher unplanned outages at the Alberta coal PPA facilities, partially offset by lower planned outages at the Alberta coal PPA facilities and Genesee Unit 3.

· U.S. Coal: Comparable EBITDA decreased to $14 million in 2013 compared to $37 million in 2012. The decline in comparable EBITDA is due to lower pricing, including margins on purchased power, partially offset by favourable coal pricing.

· Gas: Comparable EBITDA decreased by $17 million to $82 million primarily due to lower pricing and higher OM&A due to higher routine maintenance.

· Wind: Comparable EBITDA for wind improved by $4 million in 2013 to $58 million primarily due to the commencement of commercial operations at New Richmond.

· Hydro: Comparable EBITDA decreased by $11 million to $21 million primarily due to lower prices and lower water resources.

· Equity Investments: The geothermal business, which is recorded within equity investments, lost $5 million in 2013 compared to a loss of $10 million in 2012. The reduction of the loss is primarily due to favourable pricing and favourable changes in foreign exchange rates, partially offset by higher planned and unplanned outages.

· Energy Trading Segment: Our Energy Trading business showed an improvement in comparable EBITDA of $12 million in 2013 as a result of increased value from trading around power and gas assets, prudent management of risk, increased customer margins, and favourable market conditions driven largely by extreme weather events during the quarter.

· Corporate Segment: The Corporate Segment was comparable to 2012.

· Overall availability, including finance leases and equity investments, was 91.8 per cent compared to 89.4 per cent in 2012. The increase is primarily due to lower planned outages at the Alberta coal PPA facilities, Genesee Unit 3, and Sarnia, partially offset by higher unplanned outages at the Alberta coal PPA facilities.

· Overall production increased 1,760 gigawatt hours (“GWh”) to 12,640 GWh compared to 2012.

Consolidated Highlights

· Funds from operations (“FFO”) decreased $35 million to $179 million compared to the prior year due to primarily due to higher cash interest and cash taxes as well as differences in timing of cash proceeds associated with power hedges.

· Comparable net earnings were $1 million ($0.00 net earnings per share), down from $55 million ($0.22 net earnings per share) in 2012. The decrease is primarily due to a decrease in comparable EBITDA and an increase depreciation and amortization, partially offset by a decrease in income tax expense.

· Reported net loss attributable to common shareholders was $66 million ($0.25 net loss per share), down from net earnings of $39 million ($0.15 net earnings per share) in 2012. The change is driven by a decrease in comparable EBITDA of $70 million and the following non-comparable amounts, net of tax:

· Increase in impact of the California claim of $42 million

· Increase in loss on de-designated hedges of $19 million

· Increase in impact of Sundance Units 1 and 2 return to service of $8 million

· Increase in impact of writeoff of deferred income tax assets of $12 million

· We have accrued for a potential settlement with San Diego Gas & Electric Company, the California Attorney General, and other government agencies with a pre-tax impact of U.S.$52 million.

The following table depicts key financial results and statistical operating data:

|

| 3 months ended Dec. 31 |

| Year ended Dec. 31 |

| ||||

|

| 2013 |

| 2012 |

| 2013 |

| 2012 |

|

Availability (%)(1) |

| 91.8 |

| 89.4 |

| 85.5 |

| 88.4 |

|

Adjusted availability (%)(1),(2) |

| 91.8 |

| 89.4 |

| 87.8 |

| 90.0 |

|

Production (GWh)(1) |

| 12,640 |

| 10,880 |

| 42,482 |

| 38,750 |

|

Revenues |

| 587 |

| 646 |

| 2,292 |

| 2,210 |

|

Comparable EBITDA(3) |

| 242 |

| 312 |

| 1,023 |

| 1,015 |

|

Net earnings (loss) attributable to common shareholders |

| (66 | ) | 39 |

| (71 | ) | (615 | ) |

Comparable net earnings attributable to common shareholders(3) |

| 1 |

| 55 |

| 81 |

| 117 |

|

Funds from operations(3) |

| 179 |

| 214 |

| 729 |

| 788 |

|

Cash flow from operating activities |

| 165 |

| 245 |

| 765 |

| 520 |

|

Free cash flow(4) |

| 61 |

| 74 |

| 295 |

| 258 |

|

|

|

|

|

|

|

|

|

|

|

Net earnings (loss) per share attributable to common shareholders, basic and diluted |

| (0.25 | ) | 0.15 |

| (0.27 | ) | (2.62 | ) |

Comparable net earnings (loss) per share(3) |

| 0.00 |

| 0.22 |

| 0.31 |

| 0.50 |

|

Funds from operations per share(3) |

| 0.67 |

| 0.84 |

| 2.76 |

| 3.35 |

|

Free cash flow per share(3) |

| 0.23 |

| 0.29 |

| 1.12 |

| 1.10 |

|

Dividends paid per common share |

| 0.29 |

| 0.29 |

| 1.16 |

| 1.16 |

|

As at |

| Dec. 31, 2013 |

| Dec. 31, 2012 |

|

Total assets |

| 9,783 |

| 9,503 |

|

Total long-term liabilities |

| 5,508 |

| 4,769 |

|

Comparable EBITDA is as follows:

|

| 3 months ended Dec. 31 |

| Year ended Dec. 31 |

| ||||

Comparable EBITDA |

| 2013 |

| 2012 |

| 2013 |

| 2012 |

|

Generation Segment |

|

|

|

|

|

|

|

|

|

Canadian Coal |

| 68 |

| 102 |

| 309 |

| 373 |

|

U.S. Coal |

| 14 |

| 37 |

| 66 |

| 148 |

|

Gas |

| 82 |

| 99 |

| 327 |

| 312 |

|

Wind |

| 58 |

| 54 |

| 180 |

| 151 |

|

Hydro |

| 21 |

| 32 |

| 147 |

| 127 |

|

Total Generation Segment |

| 243 |

| 324 |

| 1,029 |

| 1,111 |

|

Energy Trading Segment |

| 20 |

| 8 |

| 61 |

| (13 | ) |

Corporate Segment |

| (21 | ) | (20 | ) | (67 | ) | (83 | ) |

Total comparable EBITDA |

| 242 |

| 312 |

| 1,023 |

| 1,015 |

|

(1) Availability and production includes all generating assets (generation operations, finance leases, and equity investments).

(2) Adjusted for economic dispatching at Centralia Thermal.

(3) These items are not defined under IFRS. Presenting these items from period to period provides management and investors with the ability to evaluate earnings trends more readily in comparison with prior periods’ results. Refer to the Non-IFRS Measures section of this news release for further discussion of these items, including, where applicable, reconciliations to measures calculated in accordance with IFRS.

AVAILABILITY & PRODUCTION

Availability for the three months ended Dec. 31, 2013 increased compared to the same period in 2012, primarily due to lower planned outages at the Alberta coal PPA facilities, partially offset by higher unplanned outages at the Alberta coal PPA facilities.

Availability for the year ended Dec. 31, 2013 decreased compared to 2012, mainly due to higher unplanned outages at the Alberta coal PPA facilities, primarily driven by the Keephills Unit 1 force majeure outage, partially offset by lower planned outages at the Alberta coal PPA facilities.

Production for the three months ended Dec. 31, 2013 increased 1,760 GWh compared to the same period in 2012, primarily due to Sundance Units 1 and 2 returning to service, lower economic dispatching at Centralia Thermal, and lower planned outages at the Alberta coal PPA facilities, partially offset by higher unplanned outages at the Alberta coal PPA facilities and higher contract curtailments at our Ottawa facility.

For the year ended Dec. 31, 2013, production increased 3,732 GWh compared to 2012, primarily due to lower economic dispatching at Centralia Thermal, Sundance Units 1 and 2 returning to service, lower planned outages at the Alberta coal PPA facilities, higher PPA customer demand, and lower market curtailments, partially offset by higher unplanned outages at the Alberta coal PPA facilities, primarily driven by the Keephills Unit 1 force majeure outage, and higher planned and unplanned outages at Centralia Thermal.

FUNDS FROM OPERATIONS AND FREE CASH FLOW

FFO for the three months and year ended Dec. 31, 2013 decreased $35 million and $59 million, respectively, compared to the same periods in 2012 to $179 million and $729 million, respectively, primarily due to higher cash interest and cash taxes as well as differences in timing of cash proceeds associated with power hedges.

Free cash flow for the three months ended Dec. 31, 2013 decreased $13 million compared to the same period in 2012 to $61 million due to lower comparable net earnings, partially offset by lower sustaining capital expenditures.

For the year ended Dec. 31, 2013, free cash flow increased $37 million compared to 2012 to $295 million due to lower sustaining capital expenditures, partially offset by lower comparable net earnings.

SUBSEQUENT EVENTS

Sale of CE Generation LLC, Blackrock Development Project, and Wailuku Holding Company, LLC

On Feb. 20, 2014 we announced an agreement to sell our 50 per cent ownership of CE Generation LLC (“CE Gen”), the Blackrock development project (“Blackrock”), and Wailuku Holding Company, LLC (“Wailuku”) to MidAmerican Renewables for proceeds of U.S.$193.5 million. MidAmerican Renewables holds the other 50 per cent interest in CE Gen, Blackrock, and Wailuku.

Dividend

On Feb. 20, 2014, we announced the resizing of our dividend to a quarterly dividend of $0.18 per common share (or $0.72 per common share on an annualized basis) to align with our growth and financial objectives.

Sundance Unit 6 Agreement

On Feb. 19, 2014, we reached an agreement with the PPA Buyer related to the dispute on Sundance Unit 6. We don’t expect any material impact to the financial statements as a result of the agreement.

California Claim

In response to complaints filed by San Diego Gas & Electric Company, the California Attorney General, and other government agencies, the Federal Energy Regulatory Commission (“FERC”) ordered us to refund approximately U.S.$47 million for sales we made in the organized markets of the California Power Exchange, the California Independent System Operator, and the California Department of Water Resources during the 2000 - 2001 period. In addition, the California parties have sought additional refunds that to date have been rejected by FERC. We have established a U.S.$47 million provision to cover any potential refunds. Final rulings are not expected in the near future.

For the year ended Dec. 31, 2013, we accrued for a potential settlement of all outstanding disputes with the California parties, which resulted in a pre-tax charge to earnings of approximately U.S.$52 million.

Keephills Unit 2

On Jan. 31, 2014, an outage commenced at Unit 2 of our Keephills facility to perform a rewind of the generator stator as a result of the generator event in 2013 at Keephills Unit 1. We gave notice of a High Impact Low Probability event and claimed force majeure relief under the PPA.

Fort McMurray Transmission Project

On Jan. 17, 2014, we announced that our strategic partnership with MidAmerican Transmission, TAMA Transmission, which was formed on May 9, 2013, successfully qualified to participate as a proponent in the Fort McMurray West 500 kilovolt Transmission Project. The Alberta Electric System Operator announced its selection of a short-list of companies, identifying that TAMA Transmission will participate in the next stage of its competitive process for the project.

Australia Natural Gas Pipeline

On Jan. 15, 2014, we announced that, through a wholly owned subsidiary, an unincorporated joint venture named Fortescue River Gas Pipeline was formed, of which we have a 43 per cent interest. The first project of the new joint venture will be to build, own, and operate a $178 million natural gas pipeline from the Dampier to Bunbury Natural Gas Pipeline to our Solomon power station.

BUSINESS ENVIRONMENT

We operate in a variety of business environments to generate electricity, find buyers for the power we generate, and arrange for its transmission. The major markets we operate in are Western Canada, the Western U.S., and Eastern Canada. For a further description of the regions in which we operate as well as the impact of prices of electricity and natural gas upon our financial results, refer to our 2013 Annual MD&A.

Electricity Prices

Please refer to the Business Environment section of our 2013 Annual MD&A for a full discussion of the spot electricity market and the impact of electricity prices on our business, as well as our strategy to hedge our risks associated with changes in these prices.

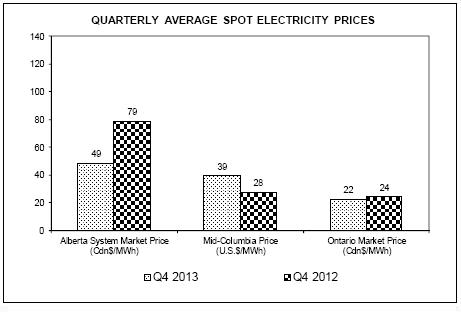

The average spot electricity prices for the three months and ended Dec. 31, 2013 and 2012 in our three major markets are shown in the following graphs.

For the three months ended Dec. 31, 2013, average spot prices in Alberta decreased compared to the same period in 2012, primarily due to an increase in supply as a result of Sundance Units 1 and 2 returning to service. In the Pacific Northwest, average spot prices increased due to higher natural gas prices, lower hydro generation, and strong demand, particularly in December. Average spot prices in Ontario for the three months ended Dec. 31, 2013 decreased compared to the same period in 2012 due to an increase in supply as a result of increased nuclear, hydro, and wind generation.

For the year ended Dec. 31, 2013, average spot prices in Alberta increased compared to 2012, primarily due to tighter supply and demand conditions. In the Pacific Northwest, average spot prices increased due to higher natural gas prices and lower hydro generation. Average spot prices in Ontario for the year ended Dec. 31, 2013 increased compared to 2012 due to higher natural gas prices, which was partially offset by an increase in supply as a result of nuclear generating plants returning to service.

In 2014, power prices in Alberta are expected to be lower than 2013 as a result of more baseload generation and fewer planned maintenance outages across the market. However, prices can vary based on supply and weather conditions. In the Pacific Northwest, we expect prices to settle higher than in 2013 due to marginally higher natural gas prices and an outlook for lower hydro generation compared to 2013.

Spark Spreads

Please refer to the Business Environment section of our 2013 Annual MD&A for a full discussion of spark spreads and the impact of spark spreads on our business.

The average spark spreads for the three months and year ended Dec. 31, 2013 and 2012 in our three major markets are shown in the following graphs.

(1) For a 7,000 British Thermal Units per kilowatt hour heat rate plant.

For the three months ended Dec. 31, 2013, average spark spreads decreased in Alberta compared to the same period in 2012 due to an increase in supply as a result of Sundance Units 1 and 2 returning to service. In the Pacific Northwest, average spark spreads increased due to higher power prices driven by lower hydro generation and high demand associated with colder weather in 2013. For the three months ended Dec. 31, 2013, average spark spreads decreased in Ontario compared to the same period in 2012 due to lower power prices driven by an increase in supply as a result of increased nuclear, hydro, and wind generation.

(1) For a 7,000 British Thermal Units per kilowatt hour heat rate plant.

For the year ended Dec. 31, 2013, average spark spreads increased in Alberta compared to 2012 due to higher power prices driven by tighter supply and demand conditions. In the Pacific Northwest, average spark spreads increased due to higher power prices driven by lower hydro generation. Average spark spreads in Ontario decreased for the year ended Dec. 31, 2013 compared to 2012 as power prices did not rise as rapidly as natural gas prices, largely due to nuclear generating plants returning to service and increased renewables generation.

DISCUSSION OF SEGMENTED RESULTS

3 months ended Dec. 31, 2013 |

| Generation |

| Energy |

| Corporate |

| Total |

|

Revenues |

| 561 |

| 26 |

| — |

| 587 |

|

Fuel and purchased power |

| 278 |

| — |

| — |

| 278 |

|

Gross margin |

| 283 |

| 26 |

| — |

| 309 |

|

Operations, maintenance, and administration |

| 110 |

| 9 |

| 21 |

| 140 |

|

Depreciation and amortization |

| 137 |

| — |

| 6 |

| 143 |

|

Inventory writedown |

| 1 |

| — |

| — |

| 1 |

|

Taxes, other than income taxes |

| 5 |

| — |

| — |

| 5 |

|

Intersegment cost allocation |

| 3 |

| (3 | ) | — |

| — |

|

Operating income (loss) |

| 27 |

| 20 |

| (27 | ) | 20 |

|

Finance lease income |

| 12 |

| — |

| — |

| 12 |

|

Equity loss |

| (5 | ) | — |

| — |

| (5 | ) |

California claim |

| — |

| (56 | ) | — |

| (56 | ) |

Sundance Units 1 and 2 return to service |

| (10 | ) | — |

| — |

| (10 | ) |

Gain on sale of assets |

| — |

| — |

| 2 |

| 2 |

|

Insurance recovery |

| 8 |

| — |

| — |

| 8 |

|

Foreign exchange gain |

|

|

|

|

|

|

| 3 |

|

Net interest expense |

|

|

|

|

|

|

| (66 | ) |

Loss before income taxes |

|

|

|

|

|

|

| (92 | ) |

3 months ended Dec. 31, 2012 (Restated)* |

| Generation |

| Energy |

| Corporate |

| Total |

|

Revenues |

| 633 |

| 13 |

| — |

| 646 |

|

Fuel and purchased power |

| 245 |

| — |

| — |

| 245 |

|

Gross margin |

| 388 |

| 13 |

| — |

| 401 |

|

Operations, maintenance, and administration |

| 93 |

| 8 |

| 19 |

| 120 |

|

Depreciation and amortization |

| 114 |

| — |

| 5 |

| 119 |

|

Inventory writedown |

| 10 |

| — |

| — |

| 10 |

|

Restructuring provision |

| 5 |

| — |

| 8 |

| 13 |

|

Taxes, other than income taxes |

| 5 |

| — |

| 1 |

| 6 |

|

Intersegment cost allocation |

| 3 |

| (3 | ) | — |

| — |

|

Operating income (loss) |

| 158 |

| 8 |

| (33 | ) | 133 |

|

Finance lease income |

| 11 |

| — |

| — |

| 11 |

|

Equity loss |

| (10 | ) | — |

| — |

| (10 | ) |

Foreign exchange loss |

|

|

|

|

|

|

| (2 | ) |

Net interest expense |

|

|

|

|

|

|

| (60 | ) |

Earnings before income taxes |

|

|

|

|

|

|

| 72 |

|

* Please refer to Note 3 of our audited consolidated financial statements within our 2013 Annual Report for additional information regarding the restatements.

Year ended Dec. 31, 2013 |

| Generation |

| Energy |

| Corporate |

| Total |

|

Revenues |

| 2,213 |

| 79 |

| — |

| 2,292 |

|

Fuel and purchased power |

| 926 |

| — |

| — |

| 926 |

|

Gross margin |

| 1,287 |

| 79 |

| — |

| 1,366 |

|

Operations, maintenance, and administration |

| 418 |

| 32 |

| 66 |

| 516 |

|

Depreciation and amortization |

| 501 |

| 1 |

| 23 |

| 525 |

|

Asset impairment charges (reversals) |

| (18 | ) | — |

| — |

| (18 | ) |

Inventory writedown |

| 22 |

| — |

| — |

| 22 |

|

Restructuring provision |

| (2 | ) | — |

| (1 | ) | (3 | ) |

Taxes, other than income taxes |

| 26 |

| — |

| 1 |

| 27 |

|

Intersegment cost allocation |

| 14 |

| (14 | ) | — |

| — |

|

Operating income (loss) |

| 326 |

| 60 |

| (89 | ) | 297 |

|

Finance lease income |

| 46 |

| — |

| — |

| 46 |

|

Equity loss |

| (10 | ) | — |

| — |

| (10 | ) |

California claim |

| — |

| (56 | ) | — |

| (56 | ) |

Sundance Units 1 and 2 return to service |

| (25 | ) | — |

| — |

| (25 | ) |

Gain on sale of assets |

| — |

| — |

| 12 |

| 12 |

|

Insurance recovery |

| 8 |

| — |

| — |

| 8 |

|

Foreign exchange gain |

|

|

|

|

|

|

| 1 |

|

Loss on assumption of pension obligations |

|

|

|

|

|

|

| (29 | ) |

Net interest expense |

|

|

|

|

|

|

| (256 | ) |

Loss before income taxes |

|

|

|

|

|

|

| (12 | ) |

Year ended Dec. 31, 2012 (Restated)* |

| Generation |

| Energy |

| Corporate |

| Total |

|

Revenues |

| 2,207 |

| 3 |

| — |

| 2,210 |

|

Fuel and purchased power |

| 753 |

| — |

| — |

| 753 |

|

Gross margin |

| 1,454 |

| 3 |

| — |

| 1,457 |

|

Operations, maintenance, and administration |

| 388 |

| 29 |

| 82 |

| 499 |

|

Depreciation and amortization |

| 489 |

| — |

| 20 |

| 509 |

|

Asset impairment charges |

| 324 |

| — |

| — |

| 324 |

|

Inventory writedown |

| 44 |

| — |

| — |

| 44 |

|

Restructuring provision |

| 5 |

| — |

| 8 |

| 13 |

|

Taxes, other than income taxes |

| 27 |

| — |

| 1 |

| 28 |

|

Intersegment cost allocation |

| 13 |

| (13 | ) | — |

| — |

|

Operating income (loss) |

| 164 |

| (13 | ) | (111 | ) | 40 |

|

Finance lease income |

| 16 |

| — |

| — |

| 16 |

|

Equity loss |

| (15 | ) | — |

| — |

| (15 | ) |

Sundance Units 1 and 2 return to service |

| (254 | ) | — |

| — |

| (254 | ) |

Gain on sale of assets |

| 3 |

| — |

| — |

| 3 |

|

Gain on sale of collateral |

| — |

| 15 |

| — |

| 15 |

|

Other income |

|

|

|

|

|

|

| 1 |

|

Foreign exchange loss |

|

|

|

|

|

|

| (9 | ) |

Net interest expense |

|

|

|

|

|

|

| (242 | ) |

Loss before income taxes |

|

|

|

|

|

|

| (445 | ) |

* Please refer to Note 3 of our audited consolidated financial statements within our 2013 Annual Report for additional information regarding the restatements.

Coal: TransAlta owns and operates coal-fired facilities and related mining operations in Canada and the U.S. Coal revenues and overall profitability are derived from the availability and production of electricity. For a full listing of all of our generating assets and the regions in which they operate, refer to the Plant Summary section of our 2013 Annual MD&A.

Canadian Coal

During 2013, we completed the restoration of Sundance Units 1 and 2. For further information please refer to the Significant Events section of our 2013 Annual MD&A.

|

| 3 months ended Dec. 31 |

| Year ended Dec. 31 |

| ||||

|

| 2013 |

| 2012 |

| 2013 |

| 2012 |

|

Production (GWh) |

| 6,643 |

| 5,285 |

| 21,568 |

| 20,265 |

|

Installed capacity (MW) |

| 3,576 |

| 3,012 |

| 3,576 |

| 3,012 |

|

|

|

|

|

|

|

|

|

|

|

Revenues |

| 251 |

| 239 |

| 916 |

| 913 |

|

Fuel and purchased power |

| 144 |

| 110 |

| 451 |

| 383 |

|

Comparable gross margin(1) |

| 107 |

| 129 |

| 465 |

| 530 |

|

Operations, maintenance, and administration |

| 53 |

| 47 |

| 201 |

| 195 |

|

Taxes, other than income taxes |

| 2 |

| 1 |

| 11 |

| 10 |

|

Intersegment cost allocation |

| 1 |

| 1 |

| 4 |

| 3 |

|

Gain on sale of property, plant, and equipment |

| (1 | ) | (7 | ) | (2 | ) | (10 | ) |

Mine depreciation |

| (16 | ) | (15 | ) | (58 | ) | (41 | ) |

Comparable EBITDA(1) |

| 68 |

| 102 |

| 309 |

| 373 |

|

Depreciation and amortization |

| 82 |

| 73 |

| 292 |

| 268 |

|

Other(2) |

| — |

| — |

| — |

| (20 | ) |

Comparable operating income (loss)(1) |

| (14 | ) | 29 |

| 17 |

| 125 |

|

|

|

|

|

|

|

|

|

|

|

Sustaining expenditures: |

|

|

|

|

|

|

|

|

|

Routine capital |

| 26 |

| 14 |

| 69 |

| 59 |

|

Mining equipment and land purchases |

| 15 |

| 9 |

| 65 |

| 38 |

|

Finance leases |

| 2 |

| — |

| 9 |

| — |

|

Planned major maintenance(3) |

| 7 |

| 45 |

| 94 |

| 219 |

|

Total sustaining expenditures |

| 50 |

| 68 |

| 237 |

| 316 |

|

Production for the three months ended Dec. 31, 2013 increased 1,358 GWh compared to the same period in 2012 due to Sundance Units 1 and 2 returning to service, lower planned outages at the Alberta coal PPA facilities and Genesee Unit 3, partially offset by higher unplanned outages at the Alberta coal PPA facilities, primarily driven by the Keephills Unit 1 force majeure outage.

For the three months ended Dec. 31, 2013, comparable EBITDA decreased by $34 million compared to the same period in 2012 due to higher coal costs, unfavourable market pricing, higher unplanned outages at the Alberta coal PPA facilities, and an increase in OM&A, partially offset by lower planned outages at the Alberta coal PPA facilities and Genesee Unit 3. Coal costs increased as a result of an increased asset base from the mine transition and the normal advancement of the mine. OM&A increased as a result of Sundance Units 1 and 2 returning to service and higher routine maintenance costs.

(1) Comparable figures are not defined under IFRS. Refer to the Non-IFRS Measures section of this MD&A for further discussion of these items, including, where applicable, reconciliations to net earnings attributable to common shareholders and cash flow from operating activities.

(2) Impacts to revenue associated with Sundance Units 1 and 2 to provide period over period comparability.

(3) Consists of no planned outages in the fourth quarter of 2013, two planned outages in the fourth quarter of 2012, three planned outages in 2013, and six planned outages in 2012.

Depreciation and amortization for the three months ended Dec. 31, 2013 increased by $9 million compared to the same period in 2012 due to an increased asset base.

For the three months ended Dec. 31, 2013, the decrease in sustaining capital expenditures compared to 2012 is mainly due to the lower number of planned outages.

Production for the year ended Dec. 31, 2013 increased 1,303 GWh compared to 2012 due to Sundance Units 1 and 2 returning to service, lower planned outages at the Alberta coal PPA facilities, lower market curtailments, and higher PPA customer demand, partially offset by higher unplanned outages at the Alberta coal PPA facilities, primarily driven by the Keephills Unit 1 force majeure outage.

For the year ended Dec. 31, 2013, comparable EBITDA decreased by $64 million compared to 2012 due to lower realized prices, higher penalties, higher coal costs, and higher unplanned outages at the Alberta coal PPA facilities, partially offset by lower planned outages at the Alberta coal PPA facilities and lower market curtailments. Coal costs increased as a result of an increased asset base from the mine transition and the normal advancement of the mine.

Depreciation and amortization for the year ended Dec. 31, 2013 increased by $24 million compared to 2012 due to an increased asset base and an increase in mine depreciation, partially offset by a decrease in asset retirements and the effect of the change of the economic useful lives of certain plants during 2012.

For the year ended Dec. 31, 2013, the decrease in sustaining capital expenditures compared to 2012 is mainly due to the lower number of planned outages, offset by higher mining equipment purchases.

U.S. Coal

|

| 3 months ended Dec. 31 |

| Year ended Dec. 31 |

| ||||

|

| 2013 |

| 2012 |

| 2013 |

| 2012 |

|

Production (GWh) |

| 2,480 |

| 2,090 |

| 6,711 |

| 3,736 |

|

Installed capacity (MW) |

| 1,340 |

| 1,340 |

| 1,340 |

| 1,340 |

|

|

|

|

|

|

|

|

|

|

|

Revenues |

| 113 |

| 128 |

| 346 |

| 368 |

|

Fuel and purchased power |

| 84 |

| 67 |

| 205 |

| 150 |

|

Comparable gross margin |

| 29 |

| 61 |

| 141 |

| 218 |

|

Operations, maintenance, and administration |

| 12 |

| 11 |

| 43 |

| 39 |

|

Inventory writedown |

| 1 |

| 10 |

| 22 |

| 19 |

|

Taxes, other than income taxes |

| 1 |

| 2 |

| 4 |

| 6 |

|

Intersegment cost allocation |

| 1 |

| 2 |

| 6 |

| 7 |

|

Gain on sale of property, plant, and equipment |

| — |

| (1 | ) | — |

| (1 | ) |

Comparable EBITDA |

| 14 |

| 37 |

| 66 |

| 148 |

|

Depreciation and amortization |

| 15 |

| 12 |

| 56 |

| 66 |

|

Comparable operating income (loss) |

| (1 | ) | 25 |

| 10 |

| 82 |

|

|

|

|

|

|

|

|

|

|

|

Sustaining expenditures: |

|

|

|

|

|

|

|

|

|

Routine capital |

| 1 |

| 2 |

| 6 |

| 10 |

|

Planned major maintenance |

| 2 |

| 4 |

| 10 |

| 22 |

|

Total sustaining expenditures |

| 3 |

| 6 |

| 16 |

| 32 |

|

Production for the three months ended Dec. 31, 2013 increased 390 GWh compared to the same period in 2012 due to lower economic dispatching at Centralia Thermal and lower unplanned outages at Centralia Thermal.

For the three months ended Dec. 31, 2013, comparable EBITDA decreased by $23 million compared to the same period in 2012, primarily due to lower pricing, including margins on purchased power, partially offset by favourable coal pricing.

Depreciation and amortization for the three months ended Dec. 31, 2013 increased by $3 million compared to the same period in 2012 due to an increased asset base.

Production for the year ended Dec. 31, 2013 increased 2,975 GWh compared to 2012 due to lower economic dispatching at Centralia Thermal, driven by improving market conditions, partially offset by higher planned outages at Centralia Thermal.

For the year ended Dec. 31, 2013, comparable EBITDA decreased by $82 million compared to 2012 due to contracts expiring and lower spot prices, partially offset by favourable coal pricing.

Depreciation and amortization for the year ended Dec. 31, 2013 decreased by $10 million compared to 2012 due to the impact of a lower asset base as a result of asset impairments.

For the year ended Dec. 31, 2013, the decrease in sustaining capital expenditures compared to 2012 is mainly due to the lower expenditures on planned outages.

Gas: TransAlta owns and operates natural gas-fired facilities in Canada and Australia. Gas revenues and overall profitability are derived from the availability and production of electricity and steam. For a full listing of all of our generating assets and the regions in which they operate, refer to the Plant Summary section of our 2013 Annual MD&A.

|

| 3 months ended Dec. 31 |

| Year ended Dec. 31 |

| ||||

|

| 2013 |

| 2012 |

| 2013 |

| 2012 |

|

Production (GWh)(1) |

| 1,886 |

| 1,989 |

| 7,854 |

| 8,230 |

|

Installed capacity (MW)(1) |

| 1,567 |

| 1,567 |

| 1,567 |

| 1,567 |

|

|

|

|

|

|

|

|

|

|

|

Revenues |

| 144 |

| 173 |

| 636 |

| 607 |

|

Fuel and purchased power |

| 48 |

| 68 |

| 252 |

| 226 |

|

Comparable gross margin |

| 96 |

| 105 |

| 384 |

| 381 |

|

Operations, maintenance, and administration |

| 26 |

| 20 |

| 100 |

| 86 |

|

Taxes, other than income taxes |

| — |

| 1 |

| 3 |

| 4 |

|

Intersegment cost allocation |

| 1 |

| — |

| 2 |

| 1 |

|

Finance lease income |

| (12 | ) | (12 | ) | (47 | ) | (19 | ) |

Gain on sale of property, plant, and equipment |

| — |

| (3 | ) | — |

| (3 | ) |

Insurance recovery |

| (1 | ) | — |

| (1 | ) | — |

|

Comparable EBITDA |

| 82 |

| 99 |

| 327 |

| 312 |

|

Depreciation and amortization |

| 28 |

| 30 |

| 107 |

| 109 |

|

Other |

| — |

| 1 |

| 1 |

| 3 |

|

Comparable operating income |

| 54 |

| 68 |

| 219 |

| 200 |

|

|

|

|

|

|

|

|

|

|

|

Sustaining expenditures: |

|

|

|

|

|

|

|

|

|

Routine capital |

| 7 |

| 5 |

| 17 |

| 13 |

|

Planned major maintenance |

| 17 |

| 15 |

| 41 |

| 36 |

|

Total sustaining expenditures |

| 24 |

| 20 |

| 58 |

| 49 |

|

(1) Includes production and net ownership capacity for Fort Saskatchewan, a natural gas-fired facility that has been accounted for as a finance lease.

Production for the three months ended Dec. 31, 2013 decreased 103 GWh compared to the same period in 2012 due to higher contract curtailments at our Ottawa facility, partially offset by lower customer demand and lower planned outages at our Sarnia facility.

For the three months ended Dec. 31, 2013, comparable EBITDA decreased by $17 million compared to the same period in 2012 due to lower pricing and higher OM&A due to higher routine maintenance.

Depreciation and amortization for the three months ended Dec. 31, 2013 decreased by $2 million compared to the same period in 2012 due to an increase in asset retirements.

Production for the year ended Dec. 31, 2013 decreased 376 GWh compared to 2012 due to higher contract and market curtailments at our Ottawa and Sarnia facilities, partially offset by lower unplanned outages at our Sarnia facility.

For the year ended Dec. 31, 2013, comparable EBITDA increased by $15 million compared to 2012 due to a full year of income from the Solomon power station that was acquired in August 2012, partially offset by higher OM&A costs resulting from higher routine maintenance.

Depreciation and amortization for the year ended Dec. 31, 2013 decreased by $2 million compared to 2012 due to a decrease in asset retirements and favourable changes in foreign exchange rates.

Renewables: TransAlta owns and operates hydro and wind facilities in Canada and the U.S. Renewable revenues and overall profitability are derived from the availability of water and wind resources and the production of electricity, as well as ancillary services such as system support. For a full listing of all of our generating assets and the regions in which they operate, refer to the Plant Summary section of our 2013 Annual MD&A.

Wind

During 2013, we began commercial operations at New Richmond, a 68 MW wind farm in Québec. We also completed the acquisition of a 144 MW wind farm in Wyoming through one of our wholly owned subsidiaries. For further information please refer to the Significant Events section of our 2013 Annual MD&A.

|

| 3 months ended Dec. 31 |

| Year ended Dec. 31 |

| ||||

|

| 2013 |

| 2012 |

| 2013 |

| 2012 |

|

Production (GWh) |

| 872 |

| 750 |

| 2,709 |

| 2,583 |

|

Installed capacity (MW) |

| 1,077 |

| 1,061 |

| 1,077 |

| 1,061 |

|

|

|

|

|

|

|

|

|

|

|

Revenues |

| 73 |

| 67 |

| 237 |

| 207 |

|

Fuel and purchased power |

| 4 |

| 3 |

| 13 |

| 12 |

|

Comparable gross margin |

| 69 |

| 64 |

| 224 |

| 195 |

|

Operations, maintenance, and administration |

| 10 |

| 9 |

| 38 |

| 38 |

|

Taxes, other than income taxes |

| 1 |

| 1 |

| 5 |

| 5 |

|

Intersegment cost allocation |

| — |

| — |

| 1 |

| 1 |

|

Comparable EBITDA |

| 58 |

| 54 |

| 180 |

| 151 |

|

Depreciation and amortization |

| 21 |

| 18 |

| 79 |

| 72 |

|

Comparable operating income |

| 37 |

| 36 |

| 101 |

| 79 |

|

|

|

|

|

|

|

|

|

|

|

Sustaining expenditures: |

|

|

|

|

|

|

|

|

|

Routine capital |

| 2 |

| 1 |

| 3 |

| 2 |

|

Planned major maintenance |

| 3 |

| 1 |

| 6 |

| 2 |

|

Total sustaining expenditures |

| 5 |

| 2 |

| 9 |

| 4 |

|

Production for the three months ended Dec. 31, 2013 increased 122 GWh compared to the same period in 2012 due to higher wind resources and the commencement of commercial operations at New Richmond, partially offset by higher unplanned outages.

For the three months ended Dec. 31, 2013, comparable EBITDA increased by $4 million compared to the same period in 2012 due to the commencement of commercial operations at New Richmond and higher wind volumes, partially offset by a decrease in prices in Alberta.

Depreciation and amortization for the three months ended Dec. 31, 2013 increased by $3 million compared to the same period in 2012 due to the commencement of operations at New Richmond.

Production for the year ended Dec. 31, 2013 increased 126 GWh compared to 2012 due to the commencement of commercial operations at New Richmond.

For the year ended Dec. 31, 2013, comparable EBITDA increased by $29 million compared to 2012 due to the commencement of commercial operations at New Richmond and higher Alberta merchant prices.

Depreciation and amortization for the year ended Dec. 31, 2013 increased by $7 million compared to 2012 due to the commencement of operations at New Richmond.

Hydro

|

| 3 months ended Dec. 31 |

| Year ended Dec. 31 |

| ||||

|

| 2013 |

| 2012 |

| 2013 |

| 2012 |

|

Production (GWh) |

| 368 |

| 397 |

| 2,085 |

| 2,356 |

|

Installed capacity (MW) |

| 893 |

| 913 |

| 893 |

| 913 |

|

|

|

|

|

|

|

|

|

|

|

Revenues |

| 23 |

| 40 |

| 181 |

| 164 |

|

Fuel and purchased power |

| (2 | ) | 2 |

| 5 |

| 7 |

|

Comparable gross margin |

| 25 |

| 38 |

| 176 |

| 157 |

|

Operations, maintenance, and administration |

| 9 |

| 6 |

| 31 |

| 27 |

|

Taxes, other than income taxes |

| 1 |

| — |

| 3 |

| 2 |

|

Intersegment cost allocation |

| — |

| — |

| 1 |

| 1 |

|

Insurance recovery |

| (6 | ) | — |

| (6 | ) | — |

|

Comparable EBITDA |

| 21 |

| 32 |

| 147 |

| 127 |

|

Depreciation and amortization |

| 6 |

| 7 |

| 25 |

| 29 |

|

Comparable operating income |

| 15 |

| 25 |

| 122 |

| 98 |

|

|

|

|

|

|

|

|

|

|

|

Sustaining expenditures: |

|

|

|

|

|

|

|

|

|

Routine capital |

| 5 |

| 2 |

| 9 |

| 7 |

|

Planned major maintenance |

| 4 |

| 4 |

| 5 |

| 7 |

|

Total sustaining expenditures |

| 9 |

| 6 |

| 14 |

| 14 |

|

Production for the three months ended Dec. 31, 2013 decreased by 29 GWh compared to the same period in 2012 due to lower water resources.

For the three months ended Dec. 31, 2013, comparable EBITDA decreased by $11 million compared to the same period in 2012 due to lower prices and lower water resources.

Depreciation and amortization for the three months ended Dec. 31, 2013 was comparable to the same period in 2012.

Production for the year ended Dec. 31, 2013 decreased by 271 GWh compared to 2012 due to lower water resources.

For the year ended Dec. 31, 2013, comparable EBITDA increased by $20 million compared to 2012 due to favourable prices, partially offset by lower water resources.

Depreciation and amortization for the year ended Dec. 31, 2013 decreased by $4 million compared to 2012 due to a change in the useful lives of the hydro assets during 2013.

Asset Impairment Charges and Reversals

Renewables

During 2013, we recognized a total pre-tax impairment charge of $4 million related to three contracted hydro assets within the renewables fleet. The assets were impaired primarily due to an increase in future capital and operating expenses that resulted from the completion of condition assessments. The annual impairment assessments are based on estimates of fair value less costs to sell derived from long range forecasts. The impairment losses are included in the Generation Segment.

Alberta Merchant

As part of the annual impairment review and assessment process in 2013, it was determined that our Alberta plants with significant merchant capacity, should be considered one cash-generating unit (the “Alberta Merchant CGU”). Previously, each plant was assessed for impairment individually. The reasons for this change include consideration of the Final Regulations published by the Canadian federal government in September 2012 governing Greenhouse Gas (“GHG”) emissions and the 50-year total life for Canadian coal-fired power plants; and the refinement of our risk management approach and practices regarding our Alberta wholesale market price exposure. The Final Regulations confirmed additional operating time and increased flexibility for our Alberta coal plants and led, in part, to a broadening of our view on the management of our Alberta wholesale market price exposure. While no impairment losses were recognized in 2013 for the Alberta Merchant CGU, total pre-tax impairment losses of $23 million that were recognized previously on renewables plants that now form part of the Alberta Merchant CGU were reversed. The Alberta Merchant CGU’s recoverable amount was based on an estimate of fair value less costs to sell using a discounted cash flow methodology, based on our long range forecasts and prices evidenced in the marketplace.

The pre-tax reversal is recognized in the Generation Segment.

Centralia Thermal

The TransAlta Energy Bill and a Memorandum of Agreement that was signed on Dec. 23, 2011 provided a framework for the orderly transition from coal-fired energy produced at Centralia Thermal and the shutdown of the units in 2020 and 2025. On July 25, 2012, we announced that we entered into a long-term power agreement to provide electricity from the Centralia Thermal plant to Puget Sound Energy from December 2014 until the facility is fully retired in 2025. As a result of these agreements, we recognized a pre-tax impairment charge of nil and $347 million included in the Generation Segment during the three months and year ended Dec. 31, 2012, respectively. The impairment assessment was based on whether the carrying amount of the Centralia Thermal plant was recoverable based on an estimate of fair value less costs to sell.

In 2013 and 2012, $28 million and $169 million, respectively, of deferred income tax assets were written off related to the tax benefits of losses associated with our U.S. operations. We wrote these assets off as it was no longer considered probable that sufficient taxable income would be available from our existing U.S. operations to utilize the underlying tax losses. An increase in future U.S. income will allow us to write up our deferred income tax assets in future periods.

Reversals

Impairment charges can be reversed in future periods if the forecasted cash flows to be generated by the impacted plants improve.

Equity Investments

Our investments in joint ventures are accounted for using the equity method and consist of our investments in CE Gen, Wailuku, TAMA Transmission, and CalEnergy, LLC (“CalEnergy”).

Our interests in the CE Gen and Wailuku joint ventures are comprised of geothermal, natural gas, and hydro facilities in various locations throughout the U.S., with 852 MW of gross generating capacity (396 MW net ownership interest). The table below summarizes key operational information adjusted to reflect our interest in these investments:

|

| 3 months ended Dec. 31 |

| Year ended Dec. 31 |

| ||||

|

| 2013 |

| 2012 |

| 2013 |

| 2012 |

|

Availability (%) |

| 94.3 |

| 93.8 |

| 91.2 |

| 94.2 |

|

Production (GWh): |

|

|

|

|

|

|

|

|

|

Gas |

| 84 |

| 90 |

| 385 |

| 380 |

|

Renewables |

| 307 |

| 279 |

| 1,170 |

| 1,200 |

|

Total production |

| 391 |

| 369 |

| 1,555 |

| 1,580 |

|

Availability for the three months ended Dec. 31, 2013 increased compared to the same period in 2012 due to lower unplanned outages.

Production for the three months ended Dec. 31, 2013 increased by 22 GWh compared to the same period in 2012 due to an increase in customer demand and lower unplanned outages.

Equity loss for the three months ended Dec. 31, 2013 was $5 million compared to $10 million for the same period in 2012. The reduction of the loss is primarily due to lower unplanned outages and favourable pricing.

Availability for the year ended Dec. 31, 2013 decreased compared to 2012 due to higher planned and unplanned outages.

Production for the year ended Dec. 31, 2013 decreased by 25 GWh compared to 2012 due to higher planned and unplanned outages, partially offset by an increase in customer demand.

Equity loss for the year ended Dec. 31, 2013 was $10 million compared to $15 million for 2012. The reduction of the loss is primarily due to favourable pricing and favourable changes in foreign exchange rates, partially offset by higher planned and unplanned outages.