Exhibit 99.1

| MANAGEMENT’S DISCUSSION AND ANALYSIS | | 2 |

Table of Contents

| 1 | Overview and highlights | 4 |

| 2 | Segmented results | 12 |

| 3 | Liquidity and capital resources | 19 |

| 4 | Contingent liabilities | 21 |

| 5 | Summary of quarterly results | 22 |

| 6 | Non-GAAP measures | 22 |

| 7 | Critical accounting policies and estimates | 25 |

| 8 | Changes in accounting policies | 26 |

| 9 | Impact of accounting pronouncements affecting future periods | 26 |

| 10 | Risks and uncertainties | 26 |

| 11 | Sensitivity analysis | 28 |

| 12 | Outlook | 29 |

| 13 | Disclosure controls and internal control over financial reporting | 30 |

| CONSOLIDATED FINANCIAL STATEMENTS | 31 |

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 1 |

MANAGEMENT’S DISCUSSION AND ANALYSIS

The following management’s discussion and analysis (MD&A) of Catalyst Paper Corporation (the company, we, us, and our) should be read in conjunction with our interim consolidated financial statements for the three month and nine month periods ended September 30, 2011 and September 30, 2010, and our audited annual consolidated financial statements for the year ended December 31, 2010 and the notes thereto, which have been prepared in accordance with generally accepted accounting principles (GAAP) in the United States (U.S.). Additional information about the company, including our most recent Annual Information Form is available on our website at www.catalystpaper.com, or the Canadian Securities Administrator’s electronic filing website at www.sedar.com.

Throughout this discussion, references are made to certain measures that are not measures of performance under U.S. GAAP, including operating earnings, EBITDA, EBITDA before restructuring costs, average delivered cash costs per tonne before specific items, net earnings (loss) attributable to the company before specific items, net earnings (loss) per share attributable to the company’s common shareholders before specific items, and free cash flow. We believe that these non-GAAP measures are useful in evaluating our performance. These non-GAAP measures are defined and reconciled to their nearest GAAP measure in section 6, Non-GAAP measures.

In this MD&A, unless otherwise indicated, all dollar amounts are expressed in Canadian dollars. The term “dollars” and the symbols “$” and “CDN$” refer to Canadian dollars and the term “U.S. dollars” and the symbol “US$” refer to United States dollars.

In this MD&A, the term “tonne” and the symbol “MT” refer to a metric tonne and the term “ton” or the symbol “ST” refer to a short ton, a measure of weight equal to 0.9072 metric tonne. Use of these symbols is in accordance with industry practice.

The information in this report is as of November 14, 2011, which is the date of filing in conjunction with our press release announcing our results for the third quarter of 2011. Disclosure contained in this document is current to November 14, 2011, unless otherwise stated.

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 2 |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Certain statements and information in this MD&A are not based on historical facts and constitute forward-looking statements or forward-looking information within the meaning of Canadian securities laws and the U.S. Private Securities Litigation Reform Act of 1995 (forward-looking statements), including but not limited to, statements about our strategy, plans, future operating performance, contingent liabilities and outlook.

Forward-looking statements:

| • | Are statements that address or discuss activities, events or developments that we expect or anticipate may occur in the future; |

| • | Can be identified by the use of words such as “believe”, “expect”, “anticipate”, “intend”, “plan”, “likely”, “predicts”, “estimates”, “forecasts”, and similar words or phrases or the negative of such words or phrases; |

| • | Reflect our current beliefs, intentions or expectations based on certain assumptions and estimates, including those identified below, which could prove to be significantly incorrect: |

| | • | Our ability to develop, manufacture and sell new products and services that meet the needs of our customers and gain commercial acceptance; |

| | • | Our ability to continue to sell our products and services in the expected quantities at the expected prices and expected times; |

| | • | Our ability to successfully obtain cost savings from our cost reduction initiatives; |

| | • | Our ability to implement business strategies and pursue opportunities; |

| | • | Expected cost of goods sold; |

| | • | Expected component supply costs and constraints; |

| | • | Expected foreign exchange and tax rates. |

| • | While considered reasonable by management, are inherently subject to known and unknown risks and uncertainties and other factors that could cause actual results or events to differ from historical or anticipated results or events. These risk factors and others are discussed in the MD&A. Certain of these risks are: |

| | • | The impact of general economic conditions in the countries in which we do business; |

| | • | Conditions in the capital markets and our ability to obtain financing and refinance existing debt; |

| | • | Market conditions and demand for our products (including declines in advertising and circulation); |

| | • | The implementation of trade restrictions in jurisdictions where our products are marketed; |

| | • | Fluctuations in foreign exchange or interest rates; |

| | • | Raw material prices (including wood fibre, chemicals and energy); |

| | • | The effect of, or change in, environmental and other governmental regulations; |

| | • | Uncertainty relating to labour relations; |

| | • | The availability of qualified personnel; |

| | • | The effects of competition from domestic and foreign producers; |

| | • | The risk of natural disaster and other factors many of which are beyond our control. |

As a result, no assurance can be given that any of the events or results anticipated by such forward-looking statements will occur or, if they do occur, what benefit they will have on our operations or financial condition. Readers are cautioned not to place undue reliance on these forward-looking statements. We disclaim any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 3 |

1.OVERVIEW AND HIGHLIGHTS

BUSINESS OVERVIEW

We are the largest producer of mechanical printing papers in western North America. We also produce NBSK pulp which is marketed primarily in Asia. Our business is comprised of three business segments: specialty printing papers, newsprint, and pulp. Specialty printing papers include coated mechanical, uncoated mechanical, and directory paper. We are the only producer of coated mechanical paper and soft calender (SC) paper in western North America. We operate four paper mills, three of which are located in British Columbia (B.C.) in Crofton, Port Alberni, and Powell River, and one in Snowflake, Arizona, which produces 100% recycled-content paper. Our Crofton mill includes a two-line kraft pulp operation.

More information about our business segments, product profile and our geographic sales distribution is provided on pages 7 to 9 of our 2010 Annual Report. Our production capacity by mill and product line is summarized in the following chart:

2011 Capacity by Mill Location and Product Line 1 | | |

| | | | Specialty printing papers 1 | | | Newsprint 1 | | | Pulp 2 | | | | | |

| Mill location | | Number of paper machines | | | Uncoated mechanical | | | Coated mechanical | | | Directory | | | Newsprint | | | NBSK pulp | | | Total | | |

Crofton, B.C. 3 | | | 3 | | | | - | | | | - | | | | 145,000 | | | | 291,000 | | | | 310,000 | 4 | | | 746,000 | |

| Port Alberni, B.C. | | | 2 | | | | - | | | | 223,000 | | | | 115,000 | | | | - | | | | - | | | | 338,000 | |

| Powell River, B.C. | | | 3 | | | | 449,000 | | | | - | | | | - | | | | 30,000 | | | | - | | | | 479,000 | |

| Snowflake, Arizona | | | 2 | | | | 48,000 | | | | - | | | | - | | | | 289,000 | | | | - | | | | 337,000 | |

| Total capacity (tonnes) | | | 10 | | | | 497,000 | | | | 223,000 | | | | 260,000 | | | | 610,000 | | | | 310,000 | | | | 1,900,000 | |

| % of total capacity | | | | | | | 26 | % | | | 12 | % | | | 14 | % | | | 32 | % | | | 16 | % | | | 100 | % |

| 1 | Capacities expressed in the above table can vary as we are able to switch production between products, particularly newsprint, directory and machine-finished uncoated grades. |

| 2 | A plan was approved to expand total pulp capacity by approximately 25,000 tonnes by 2012. This projected capacity expansion has not been reflected in the table above. |

| 3 | We have indefinitely curtailed the No. 1 paper machine at Crofton, removing the equivalent of 140,000 tonnes of newsprint production on an annualized basis. The capacity and number of machines noted in the above table have not been adjusted to reflect this indefinite curtailment. |

| 4 | Total pulp capacity at Crofton is 370,000 tonnes, of which 310,000 tonnes are designated as market pulp with the remainder of 60,000 tonnes being consumed internally. |

THIRD QUARTER OVERVIEW

Our results for the third quarter were negatively impacted by an impairment charge of $151.0 million related to our Snowflake mill. Excluding this impairment charge, our operating results improved from the previous quarter due to increased sales volumes, higher paper prices, the positive foreign exchange impact of a weakening Canadian dollar and productivity gains. The previous quarter’s results were heavily impacted by fires and extended maintenance outages at our Snowflake and Powell River mills.

Demand for mechanical paper products increased in the third quarter compared to the second quarter. Transaction prices were higher for coated and uncoated mechanical paper grades while newsprint and directory transaction prices were similar to the previous quarter. The Canadian dollar weakened in Q3 and ended the quarter below par. The market for NBSK pulp softened in the current quarter as inventories increased in part due to weakening paper demand which resulted in lower pulp prices.

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 4 |

Financial Performance

We recorded a net loss attributable to the company of $205.7 million and a net loss attributable to the company before specific items of $14.1 million in Q3. This compared to a net loss of $47.4 million and $46.9 million, respectively, in Q2. Significant specific items in Q3 included an impairment charge on certain assets of our Snowflake mill and a foreign exchange loss on the translation of U.S. dollar denominated debt. Significant specific items in the prior quarter included a foreign exchange gain on the translation of U.S. dollar denominated debt and losses sustained from fires at our Snowflake and Powell River mills.

EBITDA was $26.8 million in Q3 compared to negative $3.9 million in Q2. Refer to section 6, Non-GAAP measures, for additional information on specific items in the reported financial results.

SELECTED FINANCIAL INFORMATION

| | 2011 | | | 2010 | |

(In millions of Canadian dollars, except where otherwise stated) | YTD | | | | Q3 | | | | Q2 | | | | Q1 | | | YTD | | | | Q3 | | | | Q2 | | | | Q1 | |

Sales | | $ | 941.7 | | | $ | 340.3 | | | $ | 297.8 | | | $ | 303.6 | | | $ | 895.0 | | | $ | 322.3 | | | $ | 299.4 | | | $ | 273.3 | |

Operating earnings (loss) | | | (193.1 | ) | | | (151.6 | ) | | | (30.6 | ) | | | (10.9 | ) | | | (367.7 | ) | | | 5.1 | | | | (323.9 | ) | | | (48.9 | ) |

| Depreciation and amortization | | | 81.6 | | | | 27.8 | | | | 27.0 | | | | 26.8 | | | | 92.1 | | | | 28.2 | | | | 31.2 | | | | 32.7 | |

EBITDA 1 | | | 38.8 | | | | 26.8 | | | | (3.9 | ) | | | 15.9 | | | | 17.6 | | | | 34.2 | | | | (0.4 | ) | | | (16.2 | ) |

- before restructuring costs 1 | | | 38.8 | | | | 26.8 | | | | (3.9 | ) | | | 15.9 | | | | 42.9 | | | | 34.5 | | | | 10.5 | | | | (2.1 | ) |

Net earnings (loss) attributable to the company | | | (266.0 | ) | | | (205.7 | ) | | | (47.4 | ) | | | (12.9 | ) | | | (406.5 | ) | | | 6.0 | | | | (368.4 | ) | | | (44.1 | ) |

- before specific items 1 | | | (84.6 | ) | | | (14.1 | ) | | | (46.9 | ) | | | (23.6 | ) | | | (91.1 | ) | | | (9.6 | ) | | | (43.9 | ) | | | (37.6 | ) |

EBITDA margin 1 | | | 4.1 | % | | | 7.9 | % | | | (1.3 | %) | | | 5.2 | % | | | 2.0 | % | | | 10.6 | % | | | (0.1 | %) | | | (5.9 | %) |

- before restructuring costs 1 | | | 4.1 | % | | | 7.9 | % | | | (1.3 | %) | | | 5.2 | % | | | 4.8 | % | | | 10.7 | % | | | 3.5 | % | | | (0.8 | %) |

| Net earnings (loss) per share attributable to the company’s common shareholders (in dollars) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| - basic and diluted | | $ | (0.70 | ) | | $ | (0.54 | ) | | $ | (0.13 | ) | | $ | (0.03 | ) | | $ | (1.06 | ) | | $ | 0.02 | | | $ | (0.96 | ) | | $ | (0.12 | ) |

- before specific items 1 | | | (0.22 | ) | | | (0.04 | ) | | | (0.12 | ) | | | (0.06 | ) | | | (0.24 | ) | | | (0.03 | ) | | | (0.11 | ) | | | (0.10 | ) |

| (In thousands of tonnes) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | | 1,232.2 | | | | 439.8 | | | | 393.0 | | | | 399.4 | | | | 1,200.8 | | | | 412.1 | | | | 404.5 | | | | 384.2 | |

| Production | | | 1,234.8 | | | | 428.3 | | | | 396.1 | | | | 410.4 | | | | 1,195.9 | | | | 417.7 | | | | 403.0 | | | | 375.2 | |

| 1 | Refer to section 6, Non-GAAP measures. |

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 5 |

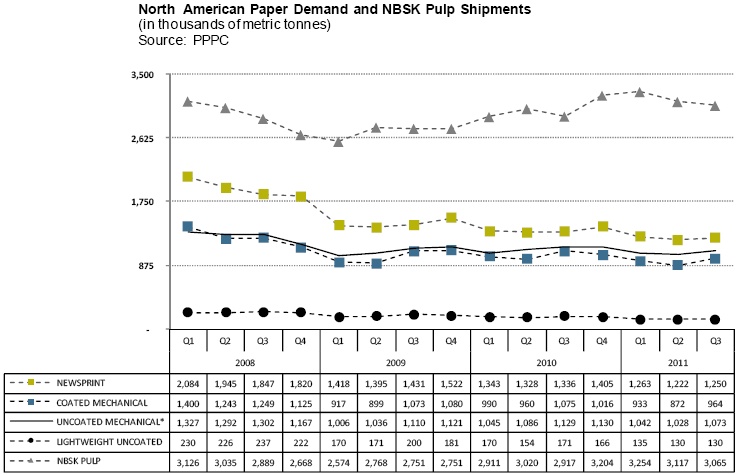

Market Overview

| * | Uncoated mechanical is comprised of high-gloss and standard grades. |

Overall, market conditions remained challenging in the quarter compared to the same quarter last year. North American demand for all paper grades decreased and inventory levels for most paper grades increased. Operating rates for most paper grades remained at similar levels as recent mill curtailments and closures helped to offset lower demand. North American demand for uncoated mechanical grades was down slightly compared to levels of a year ago while demand decreases for coated mechanical, directory paper and newsprint were more substantial. Directory, coated and uncoated mechanical benchmark prices increased during the quarter while the benchmark price for newsprint was down slightly.

Global pulp shipments increased for the quarter compared to last year as pulp shipments to China increased during the quarter offsetting lower shipments to Europe and North America. NBSK pulp shipments increased 5.1% year over year led by very strong shipments to China. NBSK pulp benchmark prices for China decreased during the quarter due to heavy shipments and rising inventory levels.

British Columbia Harmonized Sales Tax Extinguished

Elections B.C. announced on August 26, 2011 that British Columbia voters, via a mail-in ballot, defeated the Harmonized Sales Tax (HST) in a binding British Columbia sales tax referendum conducted in June and July of 2011. The elimination of the HST will have a significant negative impact on our future results. The HST had replaced the separate Provincial Sales Tax (PST) and federal Goods and Services Tax (GST) on July 1, 2010. The Province will revert back to the previous PST regime on a future date that will be no earlier than April 1, 2013. If the previous PST regime is implemented the cost impact will be approximately $10.5 million annually, based on actual 2011

annualized expenditures.

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 6 |

Impairment of Snowflake Assets

We recorded an impairment charge of $151.0 million (US$145.3 million) on certain assets of our Snowflake mill in the current quarter. The charge was comprised of a full write-down of the net book value of building, machinery and equipment of US$135.6 million and maintenance supplies and spare parts inventory of US$9.7 million. The impairment includes the assets of The Apache Railway Company, a subsidiary of Catalyst Paper (Snowflake) Inc.

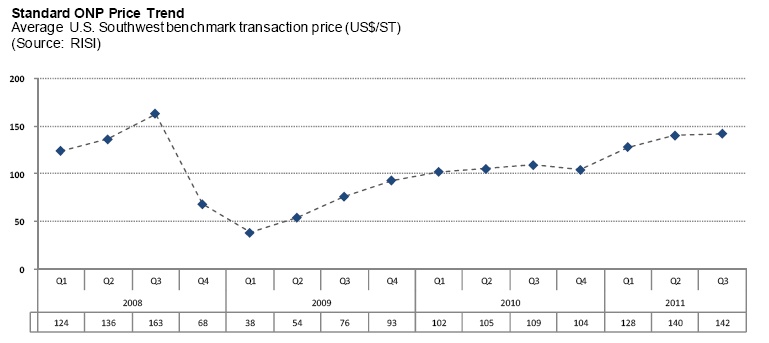

Significant changes to the economic and market environment in which the Snowflake mill operates have had an adverse effect on the mill’s operating results. The profitability of the Snowflake mill’s recycled newsprint operation has been, and will continue to be, negatively impacted by reduced North American demand for newsprint due to declining circulation, ongoing conservation and migration to electronic media. This reduction in demand has resulted in excess newsprint capacity and very competitive conditions in the marketplace that continue to limit our ability to successfully implement price increases to reflect increases to our cost structure.

Recycled newsprint is derived from recovered old newsprint (ONP), and continued demand from China for recycled paper has resulted in increased input costs and therefore deteriorating operating margins. Although there has been a recent decline in the price of ONP the global market is forecasted to remain strong, and this will continue to place significant supply and price pressure on ONP in the future.

Given these deteriorating conditions of depressed newsprint demand and pricing as well as continued upward pressure on our input costs, full impairment of the specified assets in the quarter has become appropriate in accordance with United States generally accepted accounting principles (U.S. GAAP). The assets continue to be owned by the company and are still in use.

Capital Structure Review

On June 20, 2011, the company announced that it is reviewing alternatives to address its capital structure with the goal of improving its balance sheet. In particular, the company has identified reduction of the company’s indebtedness as a priority given current business and economic conditions and is accordingly reviewing alternatives regarding both its 7.375% unsecured senior notes due 2014 and its 11.0% senior secured notes due 2016. The company recently engaged Perella Weinberg Partners as its financial advisor to assist in this process and discussions are ongoing with certain holders of these notes and/or their representatives.

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 7 |

STRATEGY UPDATE

Our objective is to return to profitability and maximize cash flows by focusing on reducing manufacturing costs and optimizing our brands and customer base. Additional information related to our corporate strategy, including key performance drivers and indicators, can be found on pages 16 to 21 of our 2010 Annual Report.

2011 Key Objectives

The following is an update on our third quarter progress towards our 2011 key objectives:

Social:

| • | Significantly improve safety performance |

| | • | Our lost-time injury frequency in Q3 of 0.71 was an improvement from Q2 levels of 1.37 and was below our target of 1.60. As well, our medical incident rate improved from 4.10 in Q2 to 3.79 in Q3 but was above our target of 3.20. |

| • | Enhance employee communication |

| | • | A multi-faceted safety awareness program began in February and a semi-annual employee engagement tracking survey has been introduced. |

| • | Continue to seek competitive business conditions in B.C., including joint municipal infrastructure agreements |

| | • | Discussions continued with B.C. municipalities and the provincial government. |

| | • | In September 2011, the City of Powell River adopted the Revitalization Tax Exemption Program Bylaw, extending the tax exemption for a further four years provided the annual application requirements are met. This will maintain the annual major industry property taxes we pay to the City of Powell River. The services arrangements under which we would use our effluent system to treat the City’s liquid waste and dispose of the City’s bio-solids in the mill’s wood waste boiler will be decided by a referendum. |

Financial:

| • | Continue to focus on cash flows, liquidity and cost reductions |

| | • | Free cash flow for the quarter was $1.4 million and total liquidity decreased by $10.5 million from Q2. This was due to a reduction in cash on hand primarily due to the annual payment of property taxes for 2011 of $18.1 million, the payment of outstanding property taxes for a prior year of $4.1 million, a one-time pension contribution of US$5.1 million to wind-up a US defined benefit pension plan and a general increase in working capital requirements. |

| | • | Capital expenditures in the current quarter of $5.6 million were primarily invested in maintenance of business. |

| | • | On track to realize annual fixed cost savings of approximately $13 million in 2011 in connection with the permanent closure of the Elk Falls mill and the Coquitlam paper recycling facility. |

| • | Improve capital structure |

| | • | As discussed in the Overview, we are presently reviewing alternatives for our US$250 million of 7.375% senior unsecured notes which mature March 1, 2014 and our US$390 million of 11.0% senior secured notes which mature December 15, 2016. |

| • | Continue to innovate and diversify product line |

| | • | Completed the development of our uncoated book grades to provide a full range of caliper-controlled paper for book publishers, including initial trials of recycled book paper from our Snowflake mill. |

| | • | Increased our capability to supply uncoated high bright grades to the retail insert market by expanding the production of our lightest weight grades at Crofton and Snowflake. |

| | • | Despite a declining demand for our grades, Catalyst continues to gain market share in all grade categories. New products such as Pacificote, our coated four grade, and Electrabrite Book Sage have contributed to this growth. |

| | • | Renewed annual contracts with all our largest telephone directory customers at higher prices. |

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 8 |

Environmental:

| • | Capital upgrade of $5 million at Port Alberni mill to improve combustion efficiency and environmental performance of its biomass boiler and a $13 million upgrade at Powell River mill to increase the electrical generation from the existing generator and biomass boiler |

| | • | Each of these projects is in process and scheduled to complete in advance of the March 31, 2012 spending deadline for the Pulp and Paper Green Transformation Program. Completion of these projects is expected to result in annual EBITDA improvement of $5.0 million. |

| • | Completed close to $2 million worth of improvements to Robertson Creek dam at Port Alberni. |

| | • | The new dam meets all current provincial safety guidelines and protects the federal fish hatchery and properties downstream. |

| • | Implement Forest Stewardship Council chain of custody certification at all Canadian mills |

| | • | With the Forest Stewardship Council (FSC) chain of custody system implemented at the company’s B.C. coastal mills, sourcing of FSC fibre from coastal, interior and ONP suppliers continues to support targeted sales and marketing campaigns. |

| • | Achieve conservation targets in water and energy |

| | • | Water audits completed at our Port Alberni and Crofton mills to verify usage, associated energy costs, and identify conservation opportunities through improved processes. |

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 9 |

CONSOLIDATED RESULTS OF OPERATIONS

Sales

Q3 2011 vs. Q2 2011

Sales revenues increased by 14.3% as a result of higher sales volumes achieved for pulp and paper as well as higher transaction prices for uncoated and coated mechanical papers. This was partially offset by a reduction in transaction prices for pulp in the third quarter. Prior quarter sales volumes were adversely impacted by fires and extended maintenance outages at our Snowflake and Powell River mills.

Q3 2011 vs. Q3 2010

Sales revenues increased by 5.6% due to higher sales volumes, both for pulp and paper, as well as higher transaction prices in the current quarter for all paper grades and pulp. These factors were partially offset by the negative impact of a stronger Canadian dollar in the current quarter.

2011 YTD vs. 2010 YTD

Sales revenues increased by 5.2% due to higher transaction prices for our paper and pulp products, and higher overall sales volumes as increased pulp and specialty sales volumes more than offset lower newsprint sales. This was partially offset by the negative impact of the stronger Canadian dollar.

EBITDA and EBITDA before Restructuring Costs

The following table provides variances between periods for EBITDA and EBITDA before restructuring costs:

| (In millions of Canadian dollars) | | | Q2 2011 | | | | Q3 2010 | | | 2010 YTD | |

EBITDA in comparative period 1 | | $ | (3.9 | ) | | $ | 34.2 | | | $ | 17.6 | |

| Restructuring costs | | | - | | | | 0.3 | | | | 25.3 | |

EBITDA before restructuring costs in comparative period 1 | | | (3.9 | ) | | | 34.5 | | | | 42.9 | |

| Paper prices | | | 4.6 | | | | 15.6 | | | | 66.9 | |

| Pulp prices | | | (2.3 | ) | | | 0.5 | | | | 15.4 | |

| Impact of Canadian dollar | | | 3.2 | | | | (14.4 | ) | | | (44.1 | ) |

| Volume and mix | | | 9.2 | | | | 7.5 | | | | 23.0 | |

| Furnish mix and costs | | | (1.8 | ) | | | (12.4 | ) | | | (32.8 | ) |

| Power and fuel costs | | | 1.9 | | | | (1.7 | ) | | | 3.2 | |

| Maintenance costs | | | 5.9 | | | | (0.6 | ) | | | (18.0 | ) |

| Labour costs | | | 3.5 | | | | (0.8 | ) | | | (7.7 | ) |

| Selling, general and administrative | | | (0.1 | ) | | | 1.3 | | | | 2.3 | |

| Lower of cost or market impact on inventory, net of inventory change | | | 6.9 | | | | 1.1 | | | | (5.6 | ) |

| Other, net | | | (0.3 | ) | | | (3.8 | ) | | | (6.7 | ) |

EBITDA before restructuring costs in the current period 1 | | | 26.8 | | | | 26.8 | | | | 38.8 | |

| Restructuring costs | | | - | | | | - | | | | - | |

EBITDA in the current period 1 | | $ | 26.8 | | | $ | 26.8 | | | $ | 38.8 | |

| 1 | Refer to section 6, Non-GAAP measures. |

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 10 |

Operating Earnings (Loss)

Q3 2011 vs. Q2 2011

Operating earnings decreased by $121.0 million primarily due to a $151.0 million impairment charge related to our Snowflake mill and an increase to depreciation and amortization expense of $0.8 million, partially offset by higher EBITDA in the current quarter of $30.7 million.

Q3 2011 vs. Q3 2010

Operating earnings deteriorated by $156.7 million due to increased impairment and closure costs of $149.7 million and a reduction in EBITDA of $7.4 million, partially offset by a reduction in depreciation and amortization expense of $0.4 million. The $149.7 million increase in impairment and other closure costs consists of the Snowflake impairment charge of $151.0 million, offset by a $0.4 million credit adjustment related to the permanent closure of the Coquitlam paper recycling facility and $0.9 million recognized as impairment expense in Q3 2010.

2011 YTD vs. 2010 YTD

Operating earnings improved by $174.6 million due to a reduction in impairment and other closure costs of $142.9 million, higher EBITDA of $21.2 million and lower depreciation and amortization expense of $10.5 million. Impairment and other closure costs of $293.2 million were recognized in 2010 related to the closure of the Elk Falls mill and Coquitlam paper recycling facility.

Net Earnings (Loss) Attributable to the Company

Q3 2011 vs. Q2 2011

Net earnings attributable to the company decreased by $158.3 million. This was primarily due to lower after-tax operating earnings of $121.0 million and an after-tax foreign exchange loss on translation of U.S. dollar denominated debt of $41.0 million compared to an after-tax foreign exchange gain of $4.5 million in the second quarter. This was partially offset by after-tax losses incurred in Q2 on fires at our Snowflake mill of $4.1 million and our Powell River mill of $1.2 million.

Q3 2011 vs. Q3 2010

Net earnings attributable to the company decreased by $211.7 million primarily due to reduced after-tax operating earnings of $156.7 million and an after-tax foreign exchange loss on the translation of U.S. dollar denominated debt of $41.0 million compared to an after-tax foreign exchange gain of $16.3 million in Q3 2010.

2011 YTD vs. 2010 YTD

Net earnings attributable to the company improved by $140.5 million primarily due to increased after-tax operating earnings of $161.3 million and increased other income of $16.2 million. This was partially offset by an after-tax foreign exchange loss on the translation of U.S. dollar denominated debt of $25.8 million compared to an after-tax foreign exchange gain of $6.7 million in 2010 YTD.

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 11 |

2.SEGMENTED RESULTS

SPECIALTY PRINTING PAPERS

| | | Three months ended September 30 | | | Nine months ended September 30 |

(In millions of Canadian dollars, except where otherwise stated) | | 2011 | | | 2010 | | | Change | | | 2011 | | | 2010 | | | Change |

| Sales | | $ | 187.9 | | | $ | 181.8 | | | $ | 6.1 | | | $ | 515.9 | | | $ | 511.0 | | | $ | 4.9 | |

| Operating earnings (loss) | | | (26.7 | ) | | | (1.8 | ) | | | (24.9 | ) | | | (63.2 | ) | | | (142.2 | ) | | | 79.0 | |

| Depreciation and amortization | | | 19.6 | | | | 20.8 | | | | (1.2 | ) | | | 56.9 | | | | 61.1 | | | | (4.2 | ) |

EBITDA 1 | | | 12.6 | | | | 19.5 | | | | (6.9 | ) | | | 13.3 | | | | 22.7 | | | | (9.4 | ) |

- before restructuring costs 1 | | | 12.6 | | | | 19.6 | | | | (7.0 | ) | | | 13.3 | | | | 30.9 | | | | (17.6 | ) |

EBITDA margin 1 | | | 6.7 | % | | | 10.7 | % | | | (4.0 | %) | | | 2.6 | % | | | 4.4 | % | | | (1.8 | %) |

- before restructuring costs 1 | | | 6.7 | % | | | 10.8 | % | | | (4.1 | %) | | | 2.6 | % | | | 6.0 | % | | | (3.4 | %) |

(In thousands of tonnes) | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | | 229.8 | | | | 220.6 | | | | 9.2 | | | | 639.3 | | | | 635.7 | | | | 3.6 | |

| Production | | | 230.0 | | | | 226.6 | | | | 3.4 | | | | 645.2 | | | | 647.9 | | | | (2.7 | ) |

| 1 | Refer to section 6, Non-GAAP measures. |

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 12 |

Segment Overview

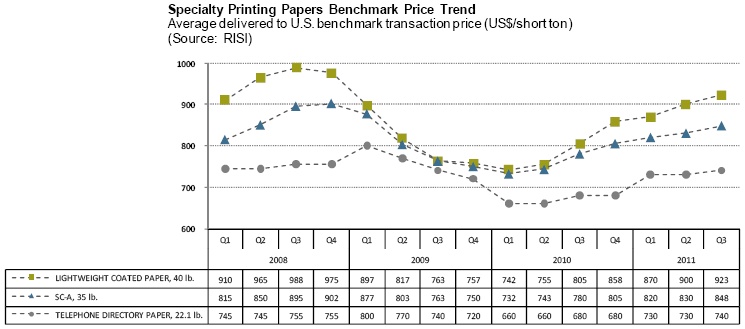

North American demand for coated mechanical and uncoated mechanical (high-gloss and standard grades) decreased 10.3% and 4.9% respectively, from the same quarter last year due to continued weakness in print advertising. Coated mechanical inventories increased while uncoated mechanical inventories were lower year over year. Adjusted operating rates continued to remain steady as mill and machine closures and curtailment offset lower demand. Our sales volumes rebounded in the third quarter after the second quarter extended maintenance outage and fire at Powell River. During the quarter, we partially implemented the July 1, 2011 US$30 per short ton price increase for our coated mechanical and SC grades and the June 1, 2011 US$40 per short ton price increase on our high bright and super bright paper grades. In addition, we announced a US$30 per short ton price increase for our high bright grades effective October 1, 2011. During the quarter the benchmark prices for these grades improved modestly from Q2. The average lightweight coated benchmark price increased 2.6% to US$923 per ton while the average soft-calendered A grade (SC-A) increased 2.2% to US$848 per ton compared to the previous quarter.

North American directory demand fell 24.0% in Q3 compared to the prior year due to ongoing pressure to reduce or eliminate white pages, smaller books, lower circulation, and the continued migration from printed books to the Internet. Market conditions improved during the quarter compared to the previous quarter as operating rates increased due to the closure of a competitor’s mill. During the quarter we implemented the July 1, 2011 US$70 per ton increase on our non-contract customers. The majority of our directory pricing is largely fixed for the year based on 2011 contract pricing.

Operational Performance

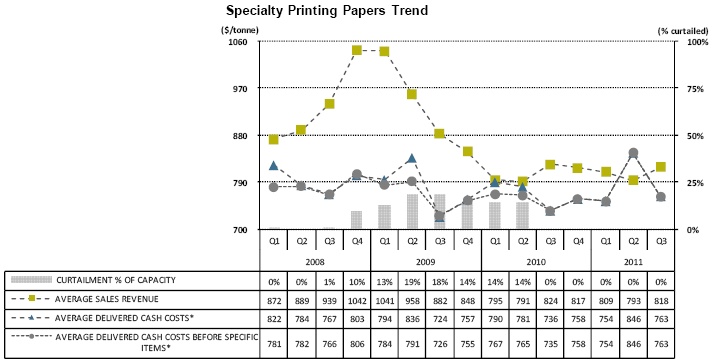

The following chart summarizes the operating performance of our specialty printing papers segment:

| * | Average delivered cash costs per tonne consist of cost of sales, excluding depreciation and amortization, and including the impact of SG&A and restructuring costs. Average delivered cash costs per tonne before specific items consist of cost of sales, excluding depreciation and amortization, and including the impact of SG&A, but excluding the impact of restructuring costs. |

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 13 |

| | • | Sales volume increased by 9,200 tonnes due to higher sales volumes in uncoated mechanical and coated mechanical, partially offset by lower sales volumes in directory. |

| | • | Average sales revenue decreased $6 per tonne due to the negative impact of the stronger Canadian dollar, partially offset by higher average transaction prices for directory, uncoated and lightweight coated papers. |

| | • | Average delivered cash costs increased $27 per tonne primarily due to increased maintenance, labour, and furnish as well as increases to the cost of electric power, chemicals and operating supplies. |

2011 YTD vs. 2010 YTD

| | • | Sales volume increased by 3,600 tonnes due to higher sales volumes in coated mechanical, partially offset by lower sales of directory paper and uncoated mechanical paper. The reduction in sales of uncoated paper was due primarily to the extended maintenance outage and fire at our Powell River mill in the second quarter of 2011. |

| | • | Average sales revenue increased $3 per tonne due to higher average transaction prices, mostly offset by the negative impact of the stronger Canadian dollar. |

| | • | Average delivered cash costs increased $18 per tonne due to increased maintenance, labour, and furnish costs, partially offset by the absence of restructuring costs in the current year. |

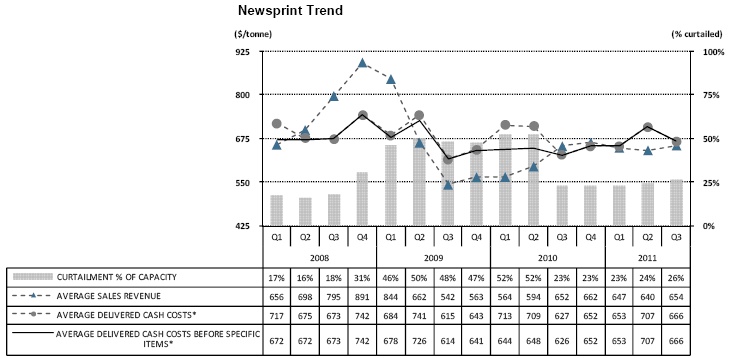

NEWSPRINT

| | | Three months ended September 30 | | | Nine months ended September 30 | |

(In millions of Canadian dollars, except where otherwise stated) | | 2011 | | | 2010 | | | Change | | | 2011 | | | 2010 | | | Change | |

| Sales | | $ | 77.0 | | | $ | 79.7 | | | $ | (2.7 | ) | | $ | 223.9 | | | $ | 222.3 | | | $ | 1.6 | |

| Operating earnings (loss) | | | (136.4 | ) | | | (1.1 | ) | | | (135.3 | ) | | | (153.6 | ) | | | (239.2 | ) | | | 85.6 | |

| Depreciation and amortization | | | 4.1 | | | | 3.7 | | | | 0.4 | | | | 13.3 | | | | 20.4 | | | | (7.1 | ) |

EBITDA 1 | | | (1.4 | ) | | | 3.0 | | | | (4.4 | ) | | | (9.6 | ) | | | (29.4 | ) | | | 19.8 | |

- before restructuring costs 1 | | | (1.4 | ) | | | 3.1 | | | | (4.5 | ) | | | (9.6 | ) | | | (13.3 | ) | | | 3.7 | |

EBITDA margin 1 | | | (1.8 | %) | | | 3.8 | % | | | (5.6 | %) | | | (4.3 | %) | | | (13.2 | %) | | | 8.9 | % |

- before restructuring costs 1 | | | (1.8 | %) | | | 3.9 | % | | | (5.7 | %) | | | (4.3 | %) | | | (6.0 | %) | | | 1.7 | % |

| (In thousands of tonnes) | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | | 117.8 | | | | 122.3 | | | | (4.5 | ) | | | 346.0 | | | | 368.5 | | | | (22.5 | ) |

| Production | | | 111.6 | | | | 120.1 | | | | (8.5 | ) | | | 348.1 | | | | 358.3 | | | | (10.2 | ) |

| 1 | Refer to section 6, Non-GAAP measures. |

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 14 |

Segment Overview

Total North American demand for newsprint was down 6.4% in Q3, year over year in part due to lower newspaper print advertising. In Q3, year over year, North American shipments were down 3.3% as a 2.5% increase in exports partially offset weak North American demand during the quarter. Operating rates were similar to the previous year. The average Q3 North American Newsprint benchmark price decreased slightly by 0.3% to US$620 per tonne compared to the previous quarter. Our sales volume increased 6,000 tonnes from the previous quarter as increased sales from Snowflake after the second quarter outage were offset by lower sales volumes in our B.C. operations in large part due to higher specialty volumes. The Crofton No. 1 paper machine remained indefinitely curtailed throughout the quarter, resulting in a reduction of 35,300 tonnes, or 23% of newsprint production capacity in Q3, based on our 2011 annualized production capacity.

Strong demand from China has fueled an upward trend in ONP prices since the start of 2009. This price pressure has had a significant impact on the profitability of the Snowflake mill’s recycled newsprint operation. For the nine months ended September 2011, the Snowflake mill produced approximately 54% of all newsprint produced during that period.

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 15 |

Operational Performance

The following chart summarizes the operating performance of our newsprint segment:

| * | Average delivered cash costs per tonne consist of cost of sales, excluding depreciation and amortization, and including the impact of SG&A and restructuring costs. Average delivered cash costs per tonne before specific items consist of cost of sales, excluding depreciation and amortization, and including the impact of SG&A, but excluding the impact of restructuring costs. |

Q3 2011 vs. Q3 2010

| | • | Sales volume decreased by 4,500 tonnes primarily due to a shift to more specialty volume and a four-day planned maintenance outage at our Snowflake mill in September. |

| | • | Average sales revenue increased $2 per tonne due to the higher average transaction prices, partially offset by negative impact of the stronger Canadian dollar. |

| | • | Average delivered cash costs increased $39 per tonne, due primarily to higher ONP prices. |

2011 YTD vs. 2010 YTD

| | • | Sales volume decreased by 22,500 tonnes due to lower production largely resulting from the extended maintenance outage at our Snowflake mill during the second quarter of 2011 as well as a shift to more specialty volume. |

| | • | Average sales revenue increased $44 per tonne due to higher average transaction prices, offset in part by the negative impact of the stronger Canadian dollar. |

| | • | Average delivered cash costs decreased $8 per tonne due to the absence of restructuring costs in the current year, partially offset by higher ONP prices and increased maintenance costs due to the extended maintenance outage at Snowflake during the second quarter of 2011. |

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 16 |

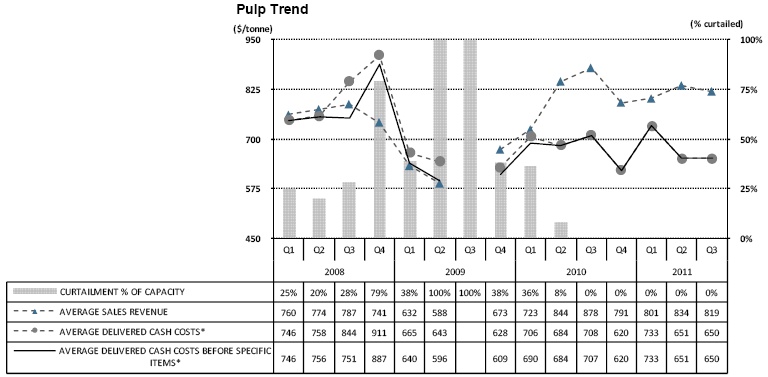

PULP

| | | Three months ended September 30 | | | Nine months ended September 30 | |

(In millions of Canadian dollars, except where otherwise stated) | | 2011 | | | 2010 | | | Change | | | 2011 | | | 2010 | | | Change | |

| Sales | | $ | 75.4 | | | $ | 60.8 | | | $ | 14.6 | | | $ | 201.9 | | | $ | 161.7 | | | $ | 40.2 | |

| Operating earnings (loss) | | | 11.5 | | | | 8.0 | | | | 3.5 | | | | 23.7 | | | | 13.7 | | | | 10.0 | |

| Depreciation and amortization | | | 4.1 | | | | 3.7 | | | | 0.4 | | | | 11.4 | | | | 10.6 | | | | 0.8 | |

EBITDA 1 | | | 15.6 | | | | 11.7 | | | | 3.9 | | | | 35.1 | | | | 24.3 | | | | 10.8 | |

- before restructuring costs 1 | | | 15.6 | | | | 11.8 | | | | 3.8 | | | | 35.1 | | | | 25.3 | | | | 9.8 | |

EBITDA margin 1 | | | 20.7 | % | | | 19.2 | % | | | 1.5 | % | | | 17.4 | % | | | 15.0 | % | | | 2.4 | % |

- before restructuring costs 1 | | | 20.7 | % | | | 19.4 | % | | | 1.3 | % | | | 17.4 | % | | | 15.6 | % | | | 1.8 | % |

| (In thousands of tonnes) | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | | 92.2 | | | | 69.2 | | | | 23.0 | | | | 246.9 | | | | 196.6 | | | | 50.3 | |

| Production | | | 86.7 | | | | 71.0 | | | | 15.7 | | | | 241.5 | | | | 189.7 | | | | 51.8 | |

| 1 | Refer to section 6, Non-GAAP measures. |

Segment Overview

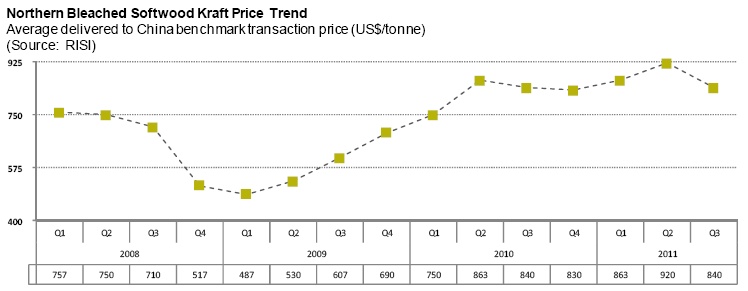

NBSK pulp markets weakened in Q3 as global paper demand weakened and pulp inventories rose. Global NBSK shipments increased 5.1% from the same quarter last year due to increased shipments to China which was up 83.2%. The average NBSK benchmark pulp price for China decreased 8.7% to US$840 per tonne compared to the previous quarter.

A plan was approved earlier this year to expand our total pulp capacity by 25,000 tonnes. We are on track to increase our total capacity to 1,120 tonnes per day (tpd) by the end of 2011.

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 17 |

Operational Performance

The following chart summarizes the operating performance of our pulp segment:

| * | Average delivered cash costs per tonne consist of cost of sales, excluding depreciation and amortization, and including the impact of SG&A and restructuring costs. Average delivered cash costs per tonne before specific items consist of cost of sales, excluding depreciation and amortization, and including the impact of SG&A, but excluding the impact of restructuring costs. |

Q3 2011 vs. Q3 2010

| | • | Sales volume increased by 23,000 tonnes compared to the same quarter last year due to improved production and strong demand for NBSK pulp from China. |

| | • | Average sales revenue decreased $59 per tonne due to the negative impact of the stronger Canadian dollar, partially offset by higher average transaction prices in the current quarter. |

| | • | Average delivered cash costs decreased by $58 per tonne due to lower fuel, maintenance and labour costs in the current quarter. |

2011 YTD vs. 2010 YTD

| | • | Sales volume increased by 50,300 tonnes due to strong demand from China as well as the fact that pulp production was fully operational throughout the first nine months of 2011, compared to being partially curtailed throughout the same period of 2010. |

| | • | Average sales revenue decreased $4 per tonne due to the negative impact of the stronger Canadian dollar, partially offset by higher average transaction prices. |

| | • | Average delivered cash costs decreased by $23 per tonne due to the absence of restructuring costs in the current year, lower fuel costs and lower maintenance costs, offset in part by increases in the cost of chips and chemicals. |

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 18 |

3.LIQUIDITY AND CAPITAL RESOURCES

SELECTED FINANCIAL INFORMATION

| | | Three months ended September 30 | | | Nine months ended September 30 | |

(In millions of Canadian dollars, except where otherwise stated) | | 2011 | | | 2010 | | | Change | | | 2011 | | | 2010 | | | Change | |

Cash flows provided (used) by operations before changes in non-cash working capital | | $ | 5.7 | | | $ | 11.3 | | | $ | (5.6 | ) | | $ | (30.2 | ) | | $ | (43.7 | ) | | $ | 13.5 | |

| Changes in non-cash working capital | | | (44.5 | ) | | | (16.7 | ) | | | (27.8 | ) | | | (37.3 | ) | | | (16.4 | ) | | | (20.9 | ) |

| Cash flows provided (used) by | | | | | | | | | | | | | | | | | | | | | | | | |

| Operations | | | (38.8 | ) | | | (5.4 | ) | | | (33.4 | ) | | | (67.5 | ) | | | (60.1 | ) | | | (7.4 | ) |

| Investing activities | | | (4.9 | ) | | | (3.4 | ) | | | (1.5 | ) | | | (12.7 | ) | | | (1.8 | ) | | | (10.9 | ) |

| Financing activities | | | 31.3 | | | | (9.7 | ) | | | 41.0 | | | | 2.6 | | | | 61.1 | | | | (58.5 | ) |

| Capital spending | | | 5.6 | | | | 2.4 | | | | 3.2 | | | | 13.5 | | | | 8.4 | | | | 5.1 | |

| Depreciation and amortization | | | 27.8 | | | | 28.2 | | | | (0.4 | ) | | | 81.6 | | | | 92.1 | | | | (10.5 | ) |

| Impairment (recovery) and other closure costs | | | 150.6 | | | | 0.9 | | | | 149.7 | | | | 150.3 | | | | 293.2 | | | | (142.9 | ) |

Capital spending as % of depreciation and amortization | | | 20 | % | | | 9 | % | | | 11 | % | | | 17 | % | | | 9 | % | | | 8 | % |

Net debt to net capitalization at September 301 | | | 84 | % | | | 64 | % | | | 20 | % | | | 84 | % | | | 64 | % | | | 20 | % |

| 1 | Net debt ratio equals net debt (total debt less cash) divided by net capitalization (shareholder’s equity attributable to the company and total debt less cash). |

Refer to page 38 of our 2010 Annual Report for a discussion of the nature and sources of funding for our principal cash requirements.

OPERATING ACTIVITIES

Cash flows from operating activities decreased by $33.4 million in Q3 from the same quarter in the previous year, primarily due to an unfavourable change in non-cash working capital of negative $44.5 million compared to negative $16.7 million during the third quarter of 2010 as well as a reduction in EBITDA of $7.4 million. The increase in working capital in Q3 2011 was primarily due to an increase in trade accounts receivable of $37.5 million and a decrease in accounts payable and accrued liabilities of $8.4 million.

INVESTING ACTIVITIES

Cash used by investing activities was $4.9 million in Q3 compared to cash used of $3.4 million in the same quarter last year. This increase was largely due to higher fixed asset additions in the current quarter. Capital spending in the current period related primarily to maintenance of business projects.

FINANCING ACTIVITIES

Cash provided by financing activities in Q3 was $31.3 million compared to cash used of $9.7 million in the same quarter last year. This was primarily due to a net draw on our asset based loan facility (ABL facility) of $31.5 million in the current quarter compared to the purchase of US$9.5 million of our 8.625% senior notes for US$8.9 million in Q3 2010.

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 19 |

CAPITAL RESOURCES

Availability on the ABL Facility and total liquidity is summarized in the following table:

| | | 2011 | | | 2010 | |

| (In millions of Canadian dollars) | | | Q3 | | | | Q2 | | | | Q1 | | | | Q4 | | | | Q3 | | | | Q2 | | | | Q1 | |

Borrowing base 1 | | $ | 167.3 | | | $ | 134.3 | | | $ | 174.1 | | | $ | 152.4 | | | $ | 161.7 | | | $ | 167.8 | | | $ | 144.8 | |

| Letters of credit | | | (27.7 | ) | | | (28.1 | ) | | | (25.5 | ) | | | (23.4 | ) | | | (25.1 | ) | | | (25.3 | ) | | | (24.0 | ) |

| Amount drawn, net | | | (31.5 | ) | | | - | | | | - | | | | - | | | | - | | | | - | | | | (25.0 | ) |

| Minimum excess availability | | | - | | | | - | | | | (35.0 | ) | | | (35.0 | ) | | | (35.0 | ) | | | (35.0 | ) | | | (35.0 | ) |

Availability 2 | | | 108.1 | | | | 106.2 | | | | 113.6 | | | | 94.0 | | | | 101.6 | | | | 107.5 | | | | 60.8 | |

| Cash on hand | | | 17.8 | | | | 30.2 | | | | 53.8 | | | | 95.4 | | | | 82.3 | | | | 100.8 | | | | 58.7 | |

| Total liquidity | | $ | 125.9 | | | $ | 136.4 | | | $ | 167.4 | | | $ | 189.4 | | | $ | 183.9 | | | $ | 208.3 | | | $ | 119.5 | |

| 1 | The borrowing base at September 30, 2011 includes a reserve of $0.4 million for unpaid property taxes and associated penalties (Q2 2011 - $4.5 million, Q1 2011 - $4.4 million). |

| 2 | Our ABL Facility is subject to certain financial covenants as disclosed in our interim consolidated financial statements for the three and nine months ended September 30, 2011 in note 11, Long-term debt. |

Our total liquidity decreased by $58.0 million from the same quarter last year primarily due to a decrease in cash on hand, partially offset by an increase in availability under the amended ABL facility. Liquidity decreased by $10.5 million compared to the previous quarter largely due to a decrease in cash on hand resulting from the annual payment of property taxes for 2011 of $18.1 million, the payment of outstanding property taxes for a prior year of $4.1 million, a one-time pension contribution of US$5.1 million to wind-up a U.S. defined benefit pension plan and a general increase in working capital requirements. This was partially offset by a higher borrowing base in the current quarter of $33.0 million.

At November 14, 2011, the company had 381,900,450 common shares issued and outstanding and 2,159,691 stock options for 2,159,691 common shares that, at November 14, 2011, were exercisable.

FINANCIAL INSTRUMENTS

Our financial instruments consist primarily of cash and cash equivalents, accounts receivable, accounts payable and accrued liabilities, long-term debt, and derivatives. Derivatives are used primarily to reduce exposure to currency risk on revenues, or occasionally debt, as well as price risk associated with revenue and energy costs.

For a description of the nature and extent of risk to the company from our financial instruments, as well as our respective accounting treatment of financial instruments, refer to our annual consolidated financial statements for the year ended December 31, 2010, note 26, Financial instruments. For the methods and assumptions we use to determine the fair value of financial instruments, refer to note 25, Fair value measurement, of those statements. Our methods and assumptions for determining the fair value of financial instruments have not changed materially since those used in the preparation of our consolidated financial statements for the year ended December 31, 2010.

At September 30, 2011, we had foreign currency options and forward contracts with a notional principal of US$191.4 million with major financial institutions. At September 30, 2011 period-end exchange rates, these instruments were reported at their fair value of $3.2 million.

The following table reconciles the average spot exchange rate to our effective exchange rate and provides the impact to EBITDA related to the cash flow hedges that were in place as at June 30, 2010 and were designated as hedging instruments at that time:

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 20 |

US$/CDN$ FOREIGN EXCHANGE

| | | 2011 | | | 2010 | |

| | | | Q3 | | | | Q2 | | | | Q1 | | | | Q4 | | | | Q3 | | | | Q2 | | | | Q1 | |

| Average Bank of Canada noon spot rate | | | 1.020 | | | | 1.033 | | | | 1.015 | | | | 0.987 | | | | 0.962 | | | | 0.973 | | | | 0.961 | |

(Favourable)/unfavourable impact of derivatives designated as effective hedges for accounting purposes1 | | | - | | | | (0.001 | ) | | | (0.004 | ) | | | (0.005 | ) | | | (0.014 | ) | | | (0.024 | ) | | | (0.023 | ) |

| Average effective rate included in EBITDA | | | 1.020 | | | | 1.032 | | | | 1.011 | | | | 0.982 | | | | 0.948 | | | | 0.949 | | | | 0.938 | |

(Favourable)/unfavourable impact of derivatives, other than those designated as effective hedges for accounting purposes, included in other expenses2 | | | 0.023 | | | | (0.002 | ) | | | (0.011 | ) | | | (0.016 | ) | | | (0.019 | ) | | | 0.051 | | | | 0.004 | |

Foreign exchange (gain)/loss, on working capital balances, included in other expenses3 | | | (0.043 | ) | | | 0.006 | | | | 0.007 | | | | 0.010 | | | | 0.008 | | | | (0.029 | ) | | | 0.000 | |

Average effective rate in net earnings/(loss) before income taxes4 | | | 1.000 | | | | 1.036 | | | | 1.007 | | | | 0.976 | | | | 0.937 | | | | 0.971 | | | | 0.942 | |

| (In millions of dollars) | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 1Favourable/(unfavourable) impact of derivatives designated as effective hedges for accounting purposes included in EBITDA | | $ | 0.2 | | | $ | 0.3 | | | $ | 0.9 | | | $ | 1.3 | | | $ | 3.8 | | | $ | 5.2 | | | $ | 4.9 | |

| 2Favourable/(unfavourable) impact of derivatives other than those designated as effective hedges for accounting purposes included in other expenses | | | (5.8 | ) | | | 0.3 | | | | 2.5 | | | | 4.2 | | | | 4.9 | | | | (11.3 | ) | | | (0.8 | ) |

| 3Foreign exchange gain/(loss) on working capital balances included in other expenses | | | 10.9 | | | | (1.2 | ) | | | (1.6 | ) | | | (2.5 | ) | | | (2.1 | ) | | | 6.2 | | | | (0.1 | ) |

| 4Excludes foreign exchange gain/(loss) on long term debt and $US interest expense | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

4.CONTINGENT LIABILITIES

The company’s contingent liabilities at December 31, 2010 are described on page 43 of our 2010 Annual Report. For additional and updated information regarding the company’s contingent liabilities, refer to our interim consolidated financial statements for the three and nine months ended September 30, 2011 note 20, Contingent liabilities. An update to these contingencies is noted below:

In September, 2011, we settled the claim by Quebecor World (USA)’s (Quebecor) litigation trustee against us under the U.S. Bankruptcy Code seeking the return of approximately $18.8 million of alleged preferential payments made to us by Quebecor in the ordinary course of our trade relationship during the 90-day period preceding Quebecor’s Chapter 11 filing in 2007. The net amount payable by the Company in respect of the settlement was not material and is covered by our allowance for doubtful accounts.

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 21 |

5.SUMMARY OF QUARTERLY RESULTS

The following table highlights selected financial information for the eight consecutive quarters ending September 30, 2011:

| | | 2011 | | | 2010 | | | | 2009 | 1 |

(In millions of Canadian dollars, except per share amounts) | | | Q3 | | | | Q2 | | | | Q1 | | | | Q4 | | | | Q3 | | | | Q2 | | | | Q1 | | | | Q4 | |

| Sales | | $ | 340.3 | | | $ | 297.8 | | | $ | 303.6 | | | $ | 333.6 | | | $ | 322.3 | | | $ | 299.4 | | | $ | 273.3 | | | $ | 295.0 | |

EBITDA 2 | | | 26.8 | | | | (3.9 | ) | | | 15.9 | | | | 28.7 | | | | 34.2 | | | | (0.4 | ) | | | (16.2 | ) | | | 14.1 | |

| Net earnings (loss) attributable to the company | | | (205.7 | ) | | | (47.4 | ) | | | (12.9 | ) | | | 9.6 | | | | 6.0 | | | | (368.4 | ) | | | (44.1 | ) | | | (35.8 | ) |

| Net earnings (loss) per share attributable to the company’s common shareholders | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| - basic and diluted | | $ | (0.54 | ) | | $ | (0.13 | ) | | $ | (0.03 | ) | | $ | 0.02 | | | $ | 0.02 | | | $ | (0.96 | ) | | $ | (0.12 | ) | | $ | (0.09 | ) |

| 1 | Refer to section 8, Changes in accounting policies, for a discussion of the change in our policy with respect to classification of gains and losses on certain of our derivative financial instruments and translation of foreign currency-denominated working capital balances effective January 1, 2010. Prior period comparative information has been restated. |

| 2 | Refer to section 6, Non-GAAP measures. |

Refer to section 1, Overview and highlights, and the discussion on Consolidated results of operations, for details of Q3 results compared to Q2 2011.

For summary financial information about Powell River Energy Inc., a variable interest entity for which we are the primary beneficiary, refer to note 4, Variable interest entities, of our interim consolidated financial statements for the three and nine months ended September 30, 2011.

6.NON-GAAP MEASURES

Management uses certain measures that are not defined by U.S. GAAP to evaluate our performance and, as a result, the measures as employed by management may not be comparable to similarly titled measures reported by other entities. These non-GAAP measures should not be considered by an investor as an alternative to their nearest respective GAAP measure. Our non-GAAP measures include operating earnings (loss), EBITDA (earnings before interest, taxes, depreciation and amortization, impairment and other closure costs, and before other non-operating income and expenses), EBITDA before restructuring costs, EBITDA margin, EBITDA margin before restructuring costs, average delivered cash costs per tonne before specific items, net earnings (loss) attributable to the company before specific items, net earnings (loss) per share attributable to the company’s common shareholders before specific items, and free cash flow.

Specific items are items of an unusual or non-recurring nature, or items that are subject to material volatility based on factors outside of management’s control. Specific items include: foreign exchange gain or loss on long-term debt, gain or loss on cancellation of long-term debt, asset-impairment and other closure costs, restructuring costs, unusual non-recurring items, and certain income tax adjustments.

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 22 |

EBITDA AND EBITDA BEFORE RESTRUCTURING COSTS

EBITDA as defined equates to operating earnings (loss) plus depreciation and amortization and impairment and other closure costs. EBITDA margin and EBITDA margin before restructuring costs are defined as EBITDA and EBITDA before restructuring costs as a percentage of sales. These measures enable comparison of consolidated and segment operating results between periods without regard to debt service, income taxes, capital expenditure requirements, and specific items.

Reconciliation to Net Earnings (Loss) Attributable to the Company:

| | 2011 | | | 2010 | |

| (In millions of Canadian dollars) | YTD | | | | Q3 | | | | Q2 | | | | Q1 | | | Total | | | | Q4 | | | | Q3 | | | | Q2 | | | | Q1 | |

Net earnings (loss) attributable to the company | | $ | (266.0 | ) | | $ | (205.7 | ) | | $ | (47.4 | ) | | $ | (12.9 | ) | | $ | (396.9 | ) | | $ | 9.6 | | | $ | 6.0 | | | $ | (368.4 | ) | | $ | (44.1 | ) |

Net earnings (loss) attributable to non-controlling interest | | | (0.3 | ) | | | - | | | | (0.3 | ) | | | - | | | | (1.3 | ) | | | (0.6 | ) | | | (0.4 | ) | | | 0.3 | | | | (0.6 | ) |

Net earnings (loss) | | | (266.3 | ) | | | (205.7 | ) | | | (47.7 | ) | | | (12.9 | ) | | | (398.2 | ) | | | 9.0 | | | | 5.6 | | | | (368.1 | ) | | | (44.7 | ) |

Depreciation and amortization | | | 81.6 | | | | 27.8 | | | | 27.0 | | | | 26.8 | | | | 119.3 | | | | 27.2 | | | | 28.2 | | | | 31.2 | | | | 32.7 | |

Impairment (recovery) and other closure costs | | | 150.3 | | | | 150.6 | | | | (0.3 | ) | | | - | | | | 294.5 | | | | 1.3 | | | | 0.9 | | | | 292.3 | | | | - | |

Gain on cancellation of long-term debt | | | - | | | | - | | | | - | | | | - | | | | (0.6 | ) | | | - | | | | (0.6 | ) | | | - | | | | - | |

Foreign exchange (gain) loss on long-term debt | | | 23.7 | | | | 41.0 | | | | (5.1 | ) | | | (12.2 | ) | | | (27.6 | ) | | | (19.0 | ) | | | (16.3 | ) | | | 21.3 | | | | (13.6 | ) |

Loss on Snowflake fire | | | 4.1 | | | | - | | | | 4.1 | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | |

Loss on Powell River fire | | | 1.6 | | | | - | | | | 1.6 | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | |

Other (income) expense | | | (4.4 | ) | | | (5.6 | ) | | | 0.7 | | | | 0.5 | | | | 3.2 | | | | (2.4 | ) | | | (2.8 | ) | | | 4.9 | | | | 3.5 | |

Interest expense, net | | | 55.0 | | | | 19.0 | | | | 18.7 | | | | 17.3 | | | | 72.0 | | | | 18.2 | | | | 19.0 | | | | 18.0 | | | | 16.8 | |

Income tax expense (recovery) | | | (6.8 | ) | | | (0.3 | ) | | | (2.9 | ) | | | (3.6 | ) | | | (16.3 | ) | | | (5.6 | ) | | | 0.2 | | | | - | | | | (10.9 | ) |

EBITDA | | $ | 38.8 | | | $ | 26.8 | | | $ | (3.9 | ) | | $ | 15.9 | | | $ | 46.3 | | | $ | 28.7 | | | $ | 34.2 | | | $ | (0.4 | ) | | $ | (16.2 | ) |

Restructuring costs | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Specialty printing papers | | | - | | | | - | | | | - | | | | - | | | | 8.2 | | | | - | | | | 0.1 | | | | 3.3 | | | | 4.8 | |

Newsprint | | | - | | | | - | | | | - | | | | - | | | | 16.1 | | | | - | | | | 0.1 | | | | 7.5 | | | | 8.5 | |

Pulp | | | - | | | | - | | | | - | | | | - | | | | 1.0 | | | | - | | | | 0.1 | | | | 0.1 | | | | 0.8 | |

Total restructuring costs | | | - | | | | - | | | | - | | | | - | | | | 25.3 | | | | - | | | | 0.3 | | | | 10.9 | | | | 14.1 | |

EBITDA before restructuring costs | | $ | 38.8 | | | $ | 26.8 | | | $ | (3.9 | ) | | $ | 15.9 | | | $ | 71.6 | | | $ | 28.7 | | | $ | 34.5 | | | $ | 10.5 | | | $ | (2.1 | ) |

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 23 |

NET EARNINGS (LOSS) ATTRIBUTABLE TO THE COMPANY BEFORE SPECIFIC ITEMS

Specific items are defined previously, and the exclusion of such items from net earnings (loss) attributable to the company facilitates the comparison of financial results between periods.

Reconciliation to Net Earnings (Loss) Attributable to the Company:

| (In millions of Canadian dollars and after-taxes, except where otherwise stated) | 2011 | | 2010 |

| YTD | | | Q3 | | | Q2 | | | Q1 | | | Total | | | Q4 | | | Q3 | | | Q2 | | | Q1 | |

| Net earnings (loss) attributable | | | | | | | | | | | | | | | | | | | | | | | | | |

| to the company | | $ | (266.0 | ) | | $ | (205.7 | ) | | $ | (47.4 | ) | | $ | (12.9 | ) | | $ | (396.9 | ) | | $ | 9.6 | | | $ | 6.0 | | | $ | (368.4 | ) | | $ | (44.1 | ) |

Specific items: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Gain on cancellation of long-term debt | | | - | | | | - | | | | - | | | | - | | | | (0.5 | ) | | | - | | | | (0.5 | ) | | | - | | | | - | |

Foreign exchange loss (gain) on long-term debt | | | 25.8 | | | | 41.0 | | | | (4.5 | ) | | | (10.7 | ) | | | (24.2 | ) | | | (17.5 | ) | | | (16.3 | ) | | | 21.3 | | | | (11.7 | ) |

Loss on Snowflake fire | | | 4.1 | | | | - | | | | 4.1 | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | |

Loss on Powell River fire | | | 1.2 | | | | - | | | | 1.2 | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | |

Impairment (recovery) and other closure costs | | | 150.3 | | | | 150.6 | | | | (0.3 | ) | | | - | | | | 291.4 | | | | (1.8 | ) | | | 0.9 | | | | 292.3 | | | | - | |

Restructuring costs | | | - | | | | - | | | | - | | | | - | | | | 21.3 | | | | - | | | | 0.3 | | | | 10.9 | | | | 10.1 | |

Notes exchange costs | | | - | | | | - | | | | - | | | | - | | | | 5.9 | | | | - | | | | - | | | | - | | | | 5.9 | |

Income tax adjustments | | | - | | | | - | | | | - | | | | - | | | | 16.0 | | | | 13.8 | | | | - | | | | - | | | | 2.2 | |

Net earnings (loss) attributable to the company before |

specific items | | $ | (84.6 | ) | | $ | (14.1 | ) | | $ | (46.9 | ) | | $ | (23.6 | ) | | $ | (87.0 | ) | | $ | 4.1 | | | $ | (9.6 | ) | | $ | (43.9 | ) | | $ | (37.6 | ) |

Net earnings (loss) per share attributable to the company’s common shareholders in dollars: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| As reported | | $ | (0.70 | ) | | $ | (0.54 | ) | | $ | (0.13 | ) | | $ | (0.03 | ) | | $ | (1.04 | ) | | $ | 0.02 | | | $ | 0.02 | | | $ | (0.96 | ) | | $ | (0.12 | ) |

| Before specific items | | | (0.22 | ) | | | (0.04 | ) | | | (0.12 | ) | | | (0.06 | ) | | | (0.23 | ) | | | 0.01 | | | | (0.03 | ) | | | (0.11 | ) | | | (0.10 | ) |

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 24 |

FREE CASH FLOW

Free cash flow excludes working capital and certain other sources and uses of cash, which are disclosed in the consolidated statements of cash flows. This measure allows us to assess our ability to generate funds to repay debt and assists in cash flow forecasting.

Reconciliation to Cash Provided by Operating Activities less Cash Used by Investing Activities:

| | | 2011 | | | 2010 | |

| (In millions of Canadian dollars) | | YTD | | | | Q3 | | | | Q2 | | | | Q1 | | | Total | | | | Q4 | | | | Q3 | | | | Q2 | | | | Q1 | |

| Cash provided (used) by operating activities | | $ | (67.5 | ) | | $ | (38.8 | ) | | $ | (15.7 | ) | | $ | (13.0 | ) | | $ | (44.1 | ) | | $ | 16.0 | | | $ | (5.4 | ) | | $ | (24.9 | ) | | $ | (29.8 | ) |

| Cash provided (used) by investing activities | | | (12.7 | ) | | | (4.9 | ) | | | (5.2 | ) | | | (2.6 | ) | | | (4.5 | ) | | | (2.7 | ) | | | (3.4 | ) | | | (1.8 | ) | | | 3.4 | |

| Proceeds from the sale of property, plant and equipment and other assets | | | (0.8 | ) | | | (0.7 | ) | | | (0.1 | ) | | | - | | | | (7.9 | ) | | | (0.7 | ) | | | (0.2 | ) | | | (0.2 | ) | | | (6.8 | ) |

| Other investing activities | | | - | | | | - | | | | (0.3 | ) | | | 0.3 | | | | 1.2 | | | | 0.6 | | | | 1.2 | | | | (0.8 | ) | | | 0.2 | |

| Non-cash working capital changes except change in taxes and interest | | | 43.1 | | | | 50.2 | | | | (18.7 | ) | | | 11.6 | | | | 12.9 | | | | (9.5 | ) | | | 21.8 | | | | 10.1 | | | | (9.5 | ) |

| Other | | | 5.5 | | | | (4.4 | ) | | | 11.7 | | | | (1.8 | ) | | | 2.0 | | | | 3.4 | | | | (3.0 | ) | | | (4.3 | ) | | | 5.9 | |

| Free cash flow | | $ | (32.4 | ) | | $ | 1.4 | | | $ | (28.3 | ) | | $ | (5.5 | ) | | $ | (40.4 | ) | | $ | 7.1 | | | $ | 11.0 | | | $ | (21.9 | ) | | $ | (36.6 | ) |

Management’s Calculation of Free Cash Flow:

| | | 2011 | | | 2010 | |

| (In millions of Canadian dollars) | | YTD | | | | Q3 | | | | Q2 | | | | Q1 | | | Total | | | | Q4 | | | | Q3 | | | | Q2 | | | | Q1 | |

| EBITDA | | $ | 38.8 | | | $ | 26.8 | | | $ | (3.9 | ) | | $ | 15.9 | | | $ | 46.3 | | | $ | 28.7 | | | $ | 34.2 | | | $ | (0.4 | ) | | $ | (16.2 | ) |

| Interest expense, excluding amortization | | | (54.2 | ) | | | (19.0 | ) | | | (17.6 | ) | | | (17.6 | ) | | | (72.7 | ) | | | (18.5 | ) | | | (19.2 | ) | | | (18.5 | ) | | | (16.5 | ) |

| Capital expenditures | | | (13.5 | ) | | | (5.6 | ) | | | (5.6 | ) | | | (2.3 | ) | | | (11.2 | ) | | | (2.8 | ) | | | (2.4 | ) | | | (2.8 | ) | | | (3.2 | ) |

| Income taxes received (paid) | | | 0.1 | | | | 0.5 | | | | (0.1 | ) | | | (0.3 | ) | | | (0.4 | ) | | | (0.2 | ) | | | (0.4 | ) | | | 0.1 | | | | 0.1 | |

Employee future benefits, expense over (under) cash contributions 1 | | | (3.6 | ) | | | (1.3 | ) | | | (1.1 | ) | | | (1.2 | ) | | | (2.4 | ) | | | (0.1 | ) | | | (1.2 | ) | | | (0.3 | ) | | | (0.8 | ) |

| Free cash flow | | $ | (32.4 | ) | | $ | 1.4 | | | $ | (28.3 | ) | | $ | (5.5 | ) | | $ | (40.4 | ) | | $ | 7.1 | | | $ | 11.0 | | | $ | (21.9 | ) | | $ | (36.6 | ) |

| 1 | Free cash flow is adjusted to reflect the cash impact of employee future benefits rather than the accounting expense which is included in EBITDA. |

7.CRITICAL ACCOUNTING POLICIES AND ESTIMATES

The preparation of financial statements in conformity with U.S. GAAP requires companies to establish accounting policies and to make estimates that affect both the amount and timing of recording of assets, liabilities, revenues and expenses. Some of these estimates require judgments about matters that are inherently uncertain and actual results could differ from estimates.

On an ongoing basis, we review our estimates based upon currently available information. The discussion on the accounting policies that require management's most difficult, subjective and complex judgments, and which are subject to a fair degree of measurement uncertainty can be found on pages 51 to 54 of the company's 2010 Annual Report. There were no significant changes in Q3 2011.

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 25 |

8.CHANGES IN ACCOUNTING POLICIES

There were no new pronouncements issued by the Financial Accounting Standards Board (FASB) that impacted our consolidated financial statements in Q3 2011.

Effective January 1, 2010, we changed our policy on the classification of foreign exchange gains and losses on the ineffective portion of our derivative financial instruments, on the portion that is excluded from the assessment of hedge effectiveness, and on translation of monetary assets and liabilities denominated in foreign currencies. The respective foreign exchange gains and losses previously recognized in Sales are now recognized in Other income (expense). We continue to classify the effective portion of gains or losses on our currently designated U.S. dollar revenue risk management instruments in Sales, the same income statement line item in which the hedged item is classified.

In addition, we changed our policy on the classification of changes in the fair value of all derivative commodity swap agreements not designated as hedges for accounting purposes that were previously recognized in Sales and Cost of sales, excluding depreciation and amortization. The changes in the fair value related to these instruments are now recognized in Other income (expense).

| 9. | | IMPACT OF ACCOUNTING PRONOUNCEMENTS AFFECTING FUTURE PERIODS |

There were no new pronouncements issued by the FASB that may impact our consolidated financial statements for future periods.

10.RISKS AND UNCERTAINTIES

We face risks and uncertainties which fall into the general business areas of markets, international commodity prices, currency exchange rates, environmental issues, fibre supply, government regulation and policy, and for Canadian companies, trade barriers and potential impacts of aboriginal rights, including unresolved aboriginal land claims in B.C.

In order to address these risks and effectively manage them, we have developed a process for managing risk and the interrelationship between risks and our strategic plan. We provide regular updates to the Audit Committee, work with corporate and operational management to identify, measure, and prioritize the critical risks facing the company, and manage these risks by ensuring that they are adequately addressed through mitigating procedures where appropriate. The objectives of the risk-management function include developing a common framework for understanding what constitutes principal business risks, ensuring that risk management activities are aligned with business strategies, and providing an effective mechanism for governance in the area of risk management.

A description of our risks and uncertainties can be found on pages 55 to 61 of our 2010 Annual Report. Our update as of November 14, 2011 can be found below:

Long-term debt

The company’s debt of $840.1 million at September 30, 2011 as compared to $783.9 million at December 31, 2010 is summarized in note 11, Long-term debt, of our interim consolidated financial statements for the three and nine months ended September 30, 2011. A description of our risks and uncertainties at December 31, 2010 referenced our total debt or our individual debt instruments as of that date and are summarized in our consolidated financial statements for the year ended December 31, 2010 in note 14, Long-term debt. These risks and uncertainties also apply to the total debt and the individual debt instruments outstanding at September 30, 2011. These risks and uncertainties include those under the following headings in our 2010 Annual Report: Our substantial debt may impair our financial and operating flexibility; We are subject to exchange rate fluctuations; and, A change in our legal control could be materially adverse.

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 26 |

The company has withheld payment of a portion of the assessed property taxes

With the payment of all of our outstanding 2010 property taxes and applicable penalties and interest to North Cowichan, the risk and uncertainties associated with the non-payment of the 2010 property taxes to North Cowichan identified under this heading in the Risks and Uncertainties section of our 2010 Annual Report are no longer applicable.

We do however owe $0.4 million, including the 10% penalty for late payment, for unpaid 2011 property taxes in dispute related to North Cowichan as at November 14, 2011. Therefore the risks and uncertainties associated with non-payment of 2011 property taxes are the same as those identified in the Risk and Uncertainties section of our 2010 Annual Report with respect to the non-payment of 2010 property taxes. If any 2011 taxes remain unpaid on September 26, 2013, the municipality must proceed to a tax sale but, in that event, we would have until September 26, 2014 to redeem the property by paying all outstanding taxes, penalties, and interest to the date of redemption.

On October 18, 2011, the Supreme Court of Canada heard our appeal on the 2009 property taxes of North Cowichan. A decision is anticipated in six to twelve months.

Our substantial debt may impair our financial and operating flexibility

As of September 30, 2011, we had $727.3 million of outstanding recourse debt on a consolidated basis, excluding non-recourse debt of $113.8 million owed by PREI.

Our ABL facility, which had excess availability of $108.1 million and a withdrawn credit balance of $31.5 million on September 30, 2011, is subject to a financial covenant to maintain a minimum fixed charge coverage ratio of 1.1/1.0, which comes into effect if excess availability under the ABL Facility falls below $22 million.

As discussed in the Overview, the company is reviewing alternatives regarding both its 7.375% unsecured senior notes due 2014 and its 11.0% senior secured notes due 2016. Should we be unable to implement appropriate alternatives to reduce our indebtedness, our level of debt, substantial debt service requirements, and the terms and conditions of our debt agreements could negatively impact our financial condition, operating results and business.

Labour disruptions could have a negative impact on our business

The collective agreement with the United Transportation Union covering 3 hourly employees at Apache Railway expires at the end of 2011. The collective agreement with the Christian Labour Association of Canada covering our hourly employees at our Surrey Distribution Center expires March 31, 2012. The collective agreements with the Communications, Energy and Paperworkers Union (CEP) and the Pulp and Paper Workers of Canada at our Crofton and Powell River mills expire on April 30, 2012. Agreements with the CEP at Port Alberni expire April 30 2013. We do not anticipate labour disruptions in our operations in 2011.

The company is subject to significant environmental regulation

It was expected that the Province of B.C. would issue regulations in Q2, 2011 for its previously announced cap and trade program for greenhouse gases (GHGs). These regulations were not issued in Q2, 2011 and it is now expected that implementation of cap and trade will be delayed until 2012 or 2013. It is too early to determine the impact on the company under a cap and trade program. Under a worst case scenario, the increased costs to the company could be approximately $2 million per year beginning in 2012 and increasing to $9 million per year in 2020.

The U.S. Environmental Protection Agency (EPA) published the Maximum Achievable Control Technology (MACT) rules for industrial boilers on March 20, 2011. This is a program that sets emission limits for stationary industrial boilers and process heaters. The standards address numerous pollutants and have suggested considerable reductions in emission limits. The EPA has asked the Federal Courts for additional time to further evaluate the standards which are required in order to meet legal obligations under the Clean Air Act. The current timetable allows for comments to be submitted by October 31, 2011 and the final standards to be issued by April 2012. A preliminary impact assessment of these rules and potential future changes to Snowflake’s emission control requirements has been completed with estimated costs in the $8 million to $10 million range.

| CATALYST PAPER 2011 THIRD QUARTER REPORT │ MANAGEMENT’S DISCUSSION AND ANALYSIS | | 27 |

Elimination of British Columbia Harmonized Sales Tax will negatively impact our future financial results

Elections B.C. confirmed the elimination of the British Columbia Harmonized Sales Tax. The Province will revert back to the previous provincial sales tax regime on a date no earlier than April 1, 2013, and we estimate that the additional annualized cost to our business from that date onward will be approximately $10.5 million, based on actual 2011 annualized expenditures.

11.SENSITIVITY ANALYSIS

Our earnings are sensitive to fluctuations in product prices, foreign exchange, energy and fibre costs as described on pages 62 to 63 of our 2010 Annual Report and summarized in the following table:

| (In millions of Canadian dollars, except per share amounts) | EBITDA1 | Net Earnings2 | Earnings per Share |

Product prices 3 | | | |

| A US$10 per tonne change in the sales price of: | | | |

| Specialty printing papers | | $ | 9 | | | $ | 7 | | | $ | 0.02 | |

| Newsprint | | | 5 | | | | 4 | | | | 0.01 | |

| Pulp | | | 4 | | | | 3 | | | | 0.01 | |

Foreign exchange 4 | | | | | | | | | | | | |

| A US$0.01 change in the U.S. dollar relative to the Canadian dollar | | | 7 | | | | 5 | | | | 0.01 | |

Energy cost sensitivity 5 | | | | | | | | | | | | |

| A 5% change in the price of: | | | | | | | | | | | | |

| Natural gas and oil - direct purchases | | | 1 | | | | 1 | | | | 0.00 | |

| Electricity - direct purchases | | | 6 | | | | 5 | | | | 0.01 | |

| Coal | | | 1 | | | | 1 | | | | 0.00 | |

| Freight cost sensitivity | | | | | | | | | | | | |

| A US$5/bbl change in the price of West Texas Int. (WTI) Oil | | | 3 | | | | 2 | | | | 0.01 | |

Fibre sensitivity 5 | | | | | | | | | | | | |

| A US$5 per unit change in the price of: | | | | | | | | | | | | |

| Wood chips (Bdt) | | | 8 | | | | 6 | | | | 0.02 | |

| ONP (ST) | | | 2 | | | | 1 | | | | 0.00 | |

| 1 | Refer to section 6, Non-GAAP measures. |

| 2 | Based on an expected tax rate of 25%. |