catalyst paper corporation

MANAGEMENT’S DISCUSSION AND ANALYSIS

Management’s Discussion and Analysis

The following management’s discussion and analysis (MD&A) of Catalyst Paper Corporation (the company, we, us, and our) should be read in conjunction with our consolidated financial statements for the years ended December 31, 2011, 2010 and 2009, and the notes thereto, which have been prepared in accordance with generally accepted accounting principles (GAAP) in the United States (U.S.). Additional information about the company, including our most recent Annual Information Form is available on our website atwww.catalystpaper.com, or the Canadian Securities Administrators’ electronic filing website atwww.sedar.com.

Throughout this discussion, references are made to certain measures that are not measures of performance under U.S. GAAP, including operating earnings, EBITDA, EBITDA before restructuring costs, average delivered cash costs per tonne before specific items, net earnings (loss) attributable to the company before specific items, net earnings (loss) per share attributable to the company’s common shareholders before specific items, and free cash flow. We believe that these non-GAAP measures are useful in evaluating our performance. These non-GAAP measures are defined and reconciled to their nearest GAAP measure in section 13, Non-GAAP Measures.

In this MD&A, unless otherwise indicated, all dollar amounts are expressed in Canadian dollars. The term “dollars” and the symbols “$” and “CDN$” refer to Canadian dollars and the term “U.S. dollars” and the symbol “US$” refer to United States dollars.

In this MD&A, the term “tonne” and the symbol “MT” refer to a metric tonne and the term “ton” or the symbol “ST” refer to a short ton, a measure of weight equal to 0.9072 metric tonne. Use of these symbols is in accordance with industry practice.

The information in this report is as at February 29, 2012, which is the date of filing in conjunction with our press release announcing our results for the fourth quarter of 2011 and 12 months ended December 31, 2011. Disclosure contained in this document is current to February 29, 2012, unless otherwise stated.

| 2 Management’s Discussion and Analysis - February 29, 2012 |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Certain statements and information in this MD&A are not based on historical facts and constitute forward-looking statements or forward-looking information within the meaning of Canadian securities laws and the U.S. Private Securities Litigation Reform Act of 1995 (forward-looking statements), including but not limited to, statements about our strategy, plans, future operating performance, contingent liabilities and outlook as well as statements about our creditor protection proceedings, debtor in possession financing, reorganization process and debt restructuring.

Forward-looking statements:

| · | Are statements that address or discuss activities, events or developments that we expect or anticipate may occur in the future; |

| · | Can be identified by the use of words such as “believe”, “expect”, “anticipate”, “intend”, “plan”, “likely”, “predicts”, “estimates”, “forecasts”, and similar words or phrases or the negative of such words or phrases; |

| · | Reflect our current beliefs, intentions or expectations based on certain assumptions and estimates, including those identified below, which could prove to be significantly incorrect: |

| | | |

| o | Our ability to develop, manufacture and sell new products and services that meet the needs of our customers and gain commercial acceptance; |

| o | Our ability to continue to sell our products and services in the expected quantities at the expected prices and expected times; |

| o | Our ability to successfully obtain cost savings from our cost reduction initiatives; |

| o | Our ability to implement business strategies and pursue opportunities; |

| o | Expected cost of goods sold; |

| o | Expected component supply costs and constraints; |

| o | Expected foreign exchange and tax rates. |

| · | While considered reasonable by management, are inherently subject to known and unknown risks and uncertainties and other factors that could cause actual results or events to differ from historical or anticipated results or events. These risk factors and others are discussed in this MD&A. Certain of these risks are: |

| | | |

| o | The impact of general economic conditions in the countries in which we do business; |

| o | Conditions in the capital markets and our ability to obtain financing and refinance existing debt; |

| o | Market conditions and demand for our products (including declines in advertising and circulation); |

| o | The implementation of trade restrictions in jurisdictions where our products are marketed; |

| o | Fluctuations in foreign exchange or interest rates; |

| o | Raw material prices (including wood fibre, chemicals and energy); |

| o | The effect of, or change in, environmental and other governmental regulations; |

| o | Uncertainty relating to labour relations; |

| o | The availability of qualified personnel; |

| o | The effects of competition from domestic and foreign producers; |

| o | The risk of natural disaster and other factors many of which are beyond our control. |

| o | Risks and uncertainties relating to our creditor protection proceedings, including our ability to continue as a going concern and ability to implement a debt restructuring. |

As a result, no assurance can be given that any of the events or results anticipated by such forward-looking statements will occur or, if they do occur, what benefit they will have on our operations or financial condition. Readers are cautioned not to place undue reliance on these forward-looking statements. We disclaim any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law.

| 3 Management’s Discussion and Analysis - February 29, 2012 |

Table of Contents

| 1 | | Company profile | | 5 |

| 2 | | Annual overview - 2011 | | 7 |

| 3 | | Strategy | | 15 |

| 4 | | Consolidated results - annual | | 24 |

| 5 | | Segmented results - annual | | 25 |

| 6 | | Consolidated and segmented results - quarterly | | 34 |

| 7 | | Financial condition | | 40 |

| 8 | | Liquidity and capital resources | | 41 |

| 9 | | Related party transactions | | 45 |

| 10 | | Contingent liabilities | | 46 |

| 11 | | Off-balance sheet arrangements | | 47 |

| 12 | | Summary of quarterly results | | 48 |

| 13 | | Non-GAAP measures | | 49 |

| 14 | | Critical accounting policies and estimates | | 53 |

| 15 | | Changes in accounting policies | | 57 |

| 16 | | Impact of accounting pronouncements affecting future periods | | 58 |

| 17 | | Risks and uncertainties | | 59 |

| 18 | | Governance and management systems | | 70 |

| 19 | | Sensitivity analysis | | 72 |

| 20 | | Outlook | | 73 |

| 21 | | Disclosure controls and internal control over financial reporting | | 76 |

| 4 Management’s Discussion and Analysis - February 29, 2012 |  |

We are the largest producer of mechanical printing papers in western North America. We also produce NBSK pulp which is marketed primarily in Asia. Our business is comprised of three business segments: specialty printing papers, newsprint, and pulp. Specialty printing papers include coated mechanical, uncoated mechanical and directory paper. We are the only producer of coated mechanical paper and soft-calender (SC) paper in western North America. We operate four paper mills, three of which are located in British Columbia (B.C.) in Crofton, Port Alberni and Powell River, and one in Snowflake, Arizona, which produces 100% recycled-content paper. Our Crofton mill includes a two-line kraft pulp operation.

Our products are sold by our sales and marketing personnel in North America and through distributors and agents in other geographic markets. These products are shipped by a combination of rail, truck, and barge for customers located in North America and by break-bulk and deep-sea container vessels for customers located overseas.

Specialty printing papers

Our largest business segment is specialty printing papers, which generated 57% of 2011 consolidated sales revenue; our papers are sold to a diversified customer base consisting of retailers, magazine and catalogue publishers, commercial printers and telephone directory publishers. In 2011, 89% of specialty printing papers sales volume was sold to customers in North America.

Newsprint

Newsprint sales generated 23% of 2011 consolidated sales revenue. The newsprint customer base consists primarily of newspaper publishers located in western and central North America, Asia and Latin America. In 2011, 71% of newsprint sales volume was sold to customers in North America.

Pulp

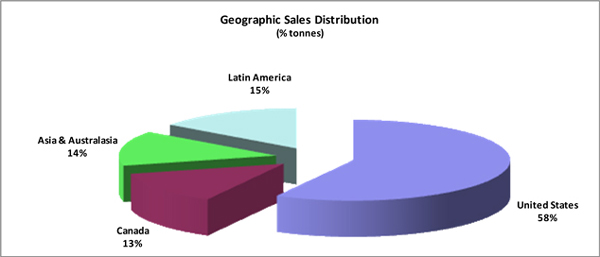

Pulp sales generated 20% of 2011 consolidated sales revenue. The pulp customer base is located primarily in Asia and includes producers of tissue, magazine papers, wood-free printing and writing papers, and certain specialty printing paper products. In 2011, 98% of pulp sales volume was sold to customers in Asia. The Crofton pulp mill is located on tidewater and has a deep-sea vessel loading facility, which enables direct-from-mill shipments to international buyers.

| 5 Management’s Discussion and Analysis - February 29, 2012 | |

| 2012PRODUCT APPLICATIONS |

| Segment | Specialty printing papers | Newsprint | Market pulp |

| Category | Uncoated mechanical | Coated

mechanical | Directory | Newsprint | NBSK pulp |

| Soft-calendered | Machine-finished |

| Brand names | Electracal

Electraprime | Electrabrite

Electrabrite Lite Electrastar

Electrastar Max | Electracote

Electracote Brite

Pacificote | Catalyst | Marathon | Crofton Kraft

|

| Basis weight (g/m2) | 45 – 52 | 45 – 74 | 47.3-74 | 29 – 40 | 43 – 48.8 | n/a |

| Applications | retail inserts,

magazines,

catalogues,

flyers, direct mail, directories | retail inserts,

magazines,

supplements, flyers, direct mail, books, corporate communication

books/manuals | retail inserts,

magazines,

catalogues,

direct mail

| telephone books,

catalogues | newspapers,

retail inserts, flyers,

supplements,

directories

| tissue,

printing and writing papers,

specialty paper products,

containerboard |

| Total capacity (tonnes) | 540,0001 | 223,000 | 226,0001 | 471,0001 | 335,0002 |

| % of total capacity | 30% | 12% | 13% | 26% | 19% |

| 2012 CAPACITY BY MILL LOCATION AND PRODUCT LINE1 |

| | | Specialty printing papers1 | Newsprint1 | Market

pulp | Total |

| Mill location | Number of

paper machines | Uncoated

mechanical | Coated

mechanical | Directory | Newsprint | NBSK

pulp | |

| Crofton, B.C. 3 | 2 | - | - | 111,000 | 194,000 | 335,0002 | 640,000 |

| Port Alberni, B.C. | 2 | - | 223,000 | 115,000 | - | - | 338,000 |

| Powell River, B.C. | 3 | 480,000 | - | - | - | - | 480,000 |

| Snowflake, Arizona | 2 | 60,000 | - | - | 277,000 | - | 337,000 |

| Total capacity (tonnes) | 9 | 540,000 | 223,000 | 226,000 | 471,000 | 335,000 | 1,795,000 |

| % of total capacity | | 30% | 12% | 13% | 26% | 19% | 100% |

| 1 | Capacities expressed in the above tables can vary as we are able to switch production between products, particularly newsprint, directory and machine-finished uncoated grades. |

| 2 | Total pulp capacity at Crofton is 395,000 tonnes, of which 335,000 tonnes are designated as market pulp with the remainder 60,000 tonnes being consumed internally. A plan was approved to expand total pulp capacity by approximately 25,000 tonnes by 2012. |

| 3 | No. 1 paper machine at Crofton remains indefinitely curtailed. If this machine were to be restarted we do not expect it would produce newsprint. |

| 6 Management’s Discussion and Analysis - February 29, 2012 | |

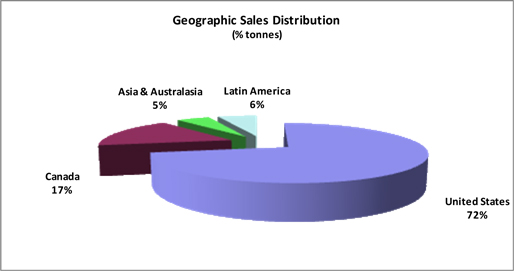

Geographic sales distribution

Our products are sold globally. North America continues to be our principal market, comprising 68% of consolidated sales volume for 2011.

Creditor Protection and Restructuring Process

Following extensive discussions and negotiations in 2011 and early 2012 with certain holders of our 7.375% senior unsecured notes due 2014 (2014 Notes) and our 11.0% senior secured notes due 2016 (2016 Notes) in an effort to implement a recapitalization transaction that would reduce our indebtedness and improve the company’s capital structure, the Board of directors and management determined it was necessary to pursue a restructuring under court supervision.

On January 31, 2012 we obtained an initial order from the Supreme Court of British Columbia under the Companies’ Creditors Arrangement Act (CCAA) staying creditor proceedings during our restructuring process under the CCAA and on February 3, 2012 obtained an amended order from the Court approving debtor-in possession (DIP) financing (as described below) that the DIP lender has agreed to provide to Catalyst during the restructuring process. The Canadian court order under the CCAA has been recognized under chapter 15 of title 11 of the US Bankruptcy Code. A further order confirming the initial order was obtained from the Canadian court on February 14, 2012. PricewaterhouseCoopers Inc. was appointed by the court as the monitor under the CCAA process.

The company arranged for a $175 million debtor-in possession facility (DIP Facility) as part of the CCAA proceedings. The DIP Facility has an 18-month maturity and is expected to provide for ongoing working capital, capital expenditure requirements as well as for general corporate purposes during the restructuring process under the CCAA. Collateral consists of a super-priority charge over accounts receivable, inventories, cash and certain other property of the company. For further details on the DIP Facility, refer to the Terms of DIP Financing section described in note 30,Subsequent event, in our annual consolidated financial statements for the year ended December 31, 2011.

| 7 Management’s Discussion and Analysis - February 29, 2012 | |

The company believes that restructuring under the CCAA will best facilitate the completion of a restructuring transaction that will deliver the improvements to our liquidity and capital structure necessary to place the company on a more firm financial and competitive footing. The company’s operating revenue combined with the DIP Credit Facility are expected to provide sufficient liquidity to meet ongoing obligations to employees and suppliers and ensure that normal operations continue during the restructuring process.

We had previously announced in June 2011that we would be reviewing alternatives to address our capital structure with the goal of improving our balance sheet. We identified the reduction of our indebtedness as a priority given current business and economic conditions. We commenced discussions on recapitalization alternatives in respect of both our 2014 Notes and 2016 Notes and engaged Perella Weinberg Partners as our financial advisor to assist in this process in October, 2011. For 2011, we incurred restructuring costs of $5.9 million on this recapitalization initiative, consisting of legal and consulting fees.

On December 15, 2011, we withheld an interest payment of approximately US$21 million due on December 15, 2011 on our 2016 Notes, electing to take advantage of a 30 day grace period that applied to that interest payment. The decision to withhold this interest payment was driven by our debt restructuring discussions with various holders of our 2014 Notes and 2016 Notes.

On January 14, 2012 we entered into a restructuring and support agreement with holders of our 2016 Notes holding approximately 53% of the total outstanding 2016 Notes and holders of our 2014 Notes holding approximately 25% of the total outstanding 2014 Notes to proceed with a proposed recapitalization transaction under theCanada Business Corporations Act(CBCA). Waivers of the December 15, 2011 interest payment by the holders of the 2016 Notes were included in this agreement and an order was obtained from the Supreme Court of British Columbia under the CBCA staying any proceedings in respect of that interest payment. An order was also obtained from the United States court recognizing the Canadian CBCA order under Chapter 15 in the United States.

The recapitalization transaction under the CBCA was subject to two conditions being met by January 31, 2012: (a) a new labour agreement ratified by all six union locals at the company’s BC mills and (b) two-thirds support of both the holders of the 2014 Notes and holders of the 2016 Notes. Neither of these conditions was met. The failure to meet those conditions coupled with declining liquidity led to the CCAA filing.

Listing and trading of our common shares

On February 1, 2012 we received notice from the Toronto Stock Exchange (TSX) that it had determined to immediately suspend the trading of our common shares on the TSX. The TSX advised that its decision was based on the commencement of our proceedings under the CCAA. The last day that our shares traded on the TSX was January 31, 2012. In addition, the TSX has advised that it intends to delist our common shares effective March 8, 2012. We do not intend to take any action to appeal this decision and therefore we expect that our common shares will be delisted on March 8, 2012.

Third Avenue Management LLC (TAM) advised us in February 2012 that, as at February 16, 2012, all common shares of the company owned by client accounts managed by TAM were disposed of. The disposition was over-the-counter sales transactions implemented after our CCAA filing.

| 8 Management’s Discussion and Analysis - February 29, 2012 | |

Repudiation of operating lease at paper recycling operation

On February 22, 2012, we gave notice that we no longer intend to meet our contractual obligations as lessee under an operating leaseat the paper recycling operation we shut down in 2010 (refer to note 5,Measurement uncertainty – impairment of long-lived assets, in our annual consolidated financial statements for the year ended December 31, 2011). The operating lease was scheduled to expire on November 30, 2023. Per the terms of the 30 day notice, a final lease payment will be made on March 1, 2012 for the 23 day period ending March 23, 2012. Any future claims arising from this operating lease are automatically stayed while the CCAA Order is in effect.

Business overview

2011 was a challenging year for our company and the pulp and paper industry in general. The global economic recovery lost most of its momentum, resulting in reduced North American demand, lower export shipments and higher inventory levels for most paper grades. Operating earnings were negatively impacted by a strong Canadian dollar for most of the year, increased recovered old newsprint (ONP) cost and general inflationary pressure.

Fires and extended maintenance outages at our Snowflake and Powell River mills during the second quarter resulted in significant production losses and higher maintenance spending. Declining demand in our newsprint and directory markets, lower pulp prices in the fourth quarter and significantly reduced long-term pulp and paper price estimates resulted in a $660.2 million impairment charge to our Canadian operations. Our Snowflake mill’s disappointing historical performance and challenging future outlook resulted in an impairment charge of $161.8 million. After giving effect to these impairment changes, the company’s liabilities exceeded the book value of its assets by $617.3 million as at December 31, 2011.

The NBSK pulp market remained solid in 2011 due to strong demand from China, with shipments and benchmark prices increasing for most of the year. By the fourth quarter inventory levels in China were very high, resulting in reduced demand and a significant decline in benchmark prices.

Financial performance

We recorded a net loss attributable to the company of $974.0 million and a net loss attributable to the company before specific items of $126.3 million in 2011. This compared to losses of $396.9 million and $87.0 million, respectively, in 2010. Significant specific items in 2011 included an impairment charge on the pulp and paper assets of our Canadian operations, an impairment charge on certain assets of our Snowflake mill, losses sustained due to fires at our Snowflake and Powell River mills, restructuring costs incurred on capital structure negotiations and a foreign exchange loss on the translation of U.S. dollar denominated debt. Significant specific items in the prior year included impairment and other closure costs related to the Elk Falls and paper recycling operations, restructuring costs, a foreign exchange gain on the translation of U.S. dollar denominated debt, note exchange costs, and an unfavourable tax adjustment.

| 9 Management’s Discussion and Analysis - February 29, 2012 | |

Selected annual financial information

| (In millions of dollars, except where otherwise stated) |

| | | 2011 | | | 2010 | | | 20091 | |

| | | | | | | | | | |

| Sales | | $ | 1,261.5 | | | $ | 1,228.6 | | | $ | 1,223.5 | |

| Operating earnings (loss) | | | (894.4 | ) | | | (367.5 | ) | | | (40.8 | ) |

| Depreciation and amortization | | | 112.4 | | | | 119.3 | | | | 146.6 | |

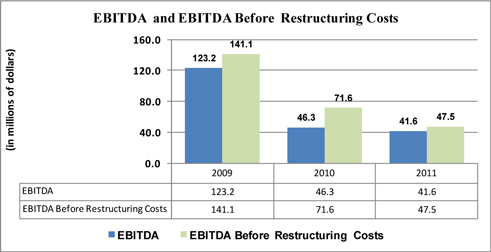

| EBITDA2 | | | 41.6 | | | | 46.3 | | | | 123.2 | |

| – before restructuring costs2 | | | 47.5 | | | | 71.6 | | | | 141.1 | |

| Net earnings (loss) attributable to the company | | | (974.0 | ) | | | (396.9 | ) | | | (4.4 | ) |

| – before specific items2 | | | (126.3 | ) | | | (87.0 | ) | | | (58.8 | ) |

| Total assets | | | 737.6 | | | | 1,696.2 | | | | 2,090.8 | |

| Total long-term liabilities | | | 713.6 | | | | 1,094.2 | | | | 1,120.9 | |

| | | | | | | | | | | | | |

| EBITDA margin2 | | | 3.3 | % | | | 3.8 | % | | | 10.1 | % |

| – before restructuring costs2 | | | 3.8 | % | | | 5.8 | % | | | 11.5 | % |

| Net earnings (loss) per share attributable to the company’s common shareholders (in dollars) | | | | | | | | | | | | |

| – basic and diluted | | $ | (2.55 | ) | | $ | (1.04 | ) | | $ | (0.01 | ) |

| – before specific items | | | (0.33 | ) | | | (0.23 | ) | | | (0.15 | ) |

| | | | | | | | | | | | | |

| (In thousands of tonnes) | | | | | | | | | | | | |

| Sales | | | 1,638.8 | | | | 1,634.9 | | | | 1,494.9 | |

| Production | | | 1,655.8 | | | | 1,625.7 | | | | 1,475.4 | |

| | | | | | | | | | | | | |

| Common shares (millions) | | | | | | | | | | | | |

| At period-end | | | 381.9 | | | | 381.8 | | | | 381.8 | |

| Weighted average | | | 381.9 | | | | 381.8 | | | | 381.8 | |

| 1 | Refer to section 15,Changes in accounting policies, for a discussion of the change in our policy with respect to classification of gains and losses on certain of our derivative financial instruments and translation of foreign currency-denominated working capital balances effective January 1, 2010. Prior period comparative information has been restated. |

| 2 | Refer to section 13, Non-GAAP measures. |

Market Overview

* Uncoated mechanical is comprised of high-gloss and standard grades.

| 10 Management’s Discussion and Analysis - February 29, 2012 | |

North American demand for all paper grades decreased in 2011 and inventory levels for most paper grades increased. Recent mill curtailments and closures helped to offset lower demand and support price momentum. North American demand for uncoated mechanical grades declined slightly in the year while demand reductions for coated mechanical, directory paper and newsprint were more significant. Benchmark prices for directory, coated, uncoated mechanical and newsprint increased for the year.

The global market for NBSK pulp increased due to very strong demand from China which more than offset declining demand in Europe and North America. NBSK pulp benchmark prices increased for most of the year due to the strong Asian market. Shipments slipped and prices declined significantly in the fourth quarter due to excess pulp inventory and reduced demand in China.

Impairment of Canadian Operations

We recorded an impairment charge of $660.2 million on the buildings, plant and equipment of our Canadian operations. Continuing declines in demand for newsprint and directory, economic slowdown in the United States and globally and the strengthening of the Canadian dollar for most of the year were all indications of possible impairment. A reduction in pulp prices in the fourth quarter of 2011 was a further indication of possible impairment of our pulp assets. In February 2012, a leading information provider for the global pulp and paper industry released their latest 5-year forecast for pulp and paper prices and future exchange rates. This new forecast reflected significantly lower future price estimates for pulp and paper than what had been previously forecasted. These indicators triggered a comprehensive impairment analysis of the company’s Canadian operations. The impairment reduced the carrying value of our pulp assets by $83.5 million and our paper assets by $576.7 million. Refer to note 5,Measurement uncertainty – impairment of long-lived assets, in our annual consolidated financial statements for the year ended December 31, 2011 for a description of the assumptions and estimates used to calculate this impairment charge. The table below illustrates the reduction in future price estimates for pulp and paper:

| RISI 5-Year Forecast - September 2011 | | | | | | | | | | | | | | | |

| RISI Benchmark Price (US$/MT) | | | 2012 | | | | 2013 | | | | 2014 | | | | 2015 | | | | Trend | |

| Newsprint | | | 677 | | | | 714 | | | | 765 | | | | 796 | | | | 738 | |

| Directory | | | 860 | | | | 882 | | | | 934 | | | | 971 | | | | 912 | |

| Uncoated | | | 976 | | | | 1,011 | | | | 1,039 | | | | 1,073 | | | | 1,025 | |

| LWC | | | 1,025 | | | | 1,074 | | | | 1,120 | | | | 1,156 | | | | 1,094 | |

| Pulp | | | 810 | | | | 783 | | | | 778 | | | | 926 | | | | 824 | |

| | | | | | | | | | | | | | | | | | | | | |

| RISI 5-Year Forecast - February 2012 | | | | | | | | | | | | | | | | | | | | |

| RISI Benchmark Price (US$/MT) | | | 2012 | | | | 2013 | | | | 2014 | | | | 2015 | | | | Trend | |

| Newsprint | | | 639 | | | | 669 | | | | 700 | | | | 714 | | | | 681 | |

| Directory | | | 849 | | | | 860 | | | | 899 | | | | 918 | | | | 882 | |

| Uncoated | | | 920 | | | | 969 | | | | 1,028 | | | | 1,045 | | | | 991 | |

| LWC | | | 962 | | | | 1,025 | | | | 1,096 | | | | 1,114 | | | | 1,049 | |

| Pulp | | | 717 | | | | 800 | | | | 852 | | | | 829 | | | | 799 | |

| | | | | | | | | | | | | | | | | | | | | |

| Variance (US$/MT) | | | 2012 | | | | 2013 | | | | 2014 | | | | 2015 | | | | Trend | |

| Newsprint | | | (38 | ) | | | (45 | ) | | | (65 | ) | | | (82 | ) | | | (58 | ) |

| Directory | | | (11 | ) | | | (22 | ) | | | (35 | ) | | | (53 | ) | | | (30 | ) |

| Uncoated | | | (56 | ) | | | (42 | ) | | | (11 | ) | | | (28 | ) | | | (34 | ) |

| LWC | | | (63 | ) | | | (49 | ) | | | (24 | ) | | | (42 | ) | | | (44 | ) |

| Pulp | | | (93 | ) | | | 17 | | | | 74 | | | | (97 | ) | | | (25 | ) |

| 11 Management’s Discussion and Analysis - February 29, 2012 | |

After giving effect to these charges and the impairment charges relating to the Snowflake assets described below, the company’s liabilities exceeded the book value of its assets by $617.3 million as at December 31, 2011.

Impairment of Snowflake Assets

We impaired the assets of our Snowflake mill by $161.8 million (US$155.9 million). In the third quarter, the net book value of building, machinery and equipment of US$135.6 million and maintenance supplies and spare parts inventory of US$9.7 million were written off. In the fourth quarter, land was impaired by US$10.6 million. These impairment charges included the assets of The Apache Railway Company, a subsidiary of Catalyst Paper (Snowflake) Inc.

The third quarter impairment was triggered by poor operating results and cash flow losses at our Snowflake mill that management projects will continue in the future. These losses are due primarily to deteriorating newsprint pricing and demand as well as tight market conditions for ONP resulting in higher input costs. We continue to own and use the impaired assets in our operations.

The fourth quarter impairment of land was based on an appraisal obtained from an independent third party real estate appraiser, dated January 3, 2012, that valued the Snowflake land at US$6.6 million. Refer to note 5,Measurement uncertainty – impairment of long-lives assets,in our annual consolidated financial statements for the year ended December 31, 2011 for a description of the assumptions and estimates used to calculate this impairment charge.

British Columbia Harmonized Sales Tax Extinguished

Elections B.C. announced on August 26, 2011 that provincial voters, via a mail-in ballot, defeated the Harmonized Sales Tax (HST) in a binding British Columbia sales tax referendum conducted in June and July of 2011. The elimination of the HST will have a significant negative impact on our future results. The HST had replaced the separate Provincial Sales Tax (PST) and federal Goods and Services Tax (GST) on July 1, 2010. The Province will revert back to a PST regime on April 1, 2013. Although we are not aware at this time of the details of the new PST regime, the cost impact would be approximately $11 million annually, based on actual 2011 expenditures if the previous PST regime is implemented.

Maintenance Outages and Fires

Our results were negatively impacted by fires and extended maintenance outages in the second quarter. At the Snowflake mill, a recovered paper storage yard fire, a market curtailment, and a five-day extension to a planned annual mill maintenance outage resulted in production downtime of 15 days or 8,400 tonnes of lost production. The fire at Snowflake destroyed approximately 11,000 tonnes of recovered ONP and resulted in losses of $4.4 million. At the Powell River mill, a five-day planned mill maintenance outage was extended to 10 days to address unexpected findings in the mill’s steam supply system, resulting in 14,000 tonnes of lost production. Also in the quarter at Powell River, an electrical cable equipment fire idled the mill’s No. 9 paper machine for five days and the No. 10 paper machine for 14 days and resulted in losses of $2.4 million and 8,700 tonnes of lost production.

| 12 Management’s Discussion and Analysis - February 29, 2012 | |

The losses incurred on the fires were not covered by insurance as the losses were below our policy deductible of $2 million per occurrence and our annual aggregate of $6 million with a per occurrence contribution not to exceed $3 million.

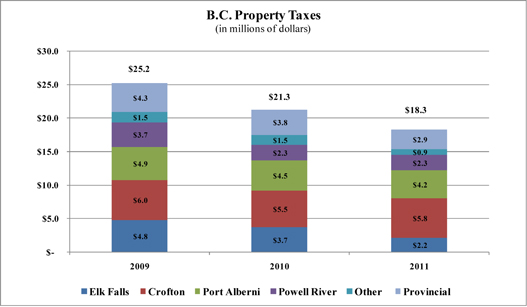

Property Tax Dispute

We paid $22.2 million of property taxes in 2011. This payment included $18.1 million municipal and provincial property taxes levied by our B.C. municipalities for 2011 as well as $4.1 million to North Cowichan for 2010 property taxes and interest. Pursuant to statutory requirements, the payment to North Cowichan was applied firstly to pay outstanding 2010 property taxes, penalties and interest in full and secondly to 2011 property taxes. As a result there are unpaid property taxes owing to North Cowichan for 2011, together with the 10% penalty for late payment, of $0.4 million at December 31, 2011. Our property tax expense and liability has been recorded based on the full amount of property taxes levied for 2011.

Our appeal to the Supreme Court of Canada regarding North Cowichan’s 2009 property taxes was dismissed on January 20, 2012. Shortly after that ruling we discontinued our proceedings disputing the 2010 and 2011 property taxes assessed by North Cowichan and as at February 29, 2012 have paid all of our unpaid property taxes and penalties owing to North Cowichan for 2011. We also discontinued our appeal in respect of the Strathcona Regional District portion of the property taxes levied by the City of Campbell River for 2010. We continue to press for a fair and sustainable level of municipal property taxes for major industry in the B.C. communities in which we operate.

Amendment and Extension of Asset Based Loan (ABL) Facility

On May 31, 2011 we amended our $330.0 million revolving asset based loan facility (ABL Facility), by reducing the amount of the facility to $175.0 million, extending the maturity date from August 13, 2013 to May 31, 2016 and removing the fixed assets of the Snowflake mill from the borrowing base under the ABL Facility. For further details on the ABL Facility amendment, refer to note 13,Long-term debt, in our annual consolidated financial statements for the year ended December 31, 2011. The ABL Facility was replaced by the DIP Facility as part of our CCAA proceedings.

| 13 Management’s Discussion and Analysis - February 29, 2012 | |

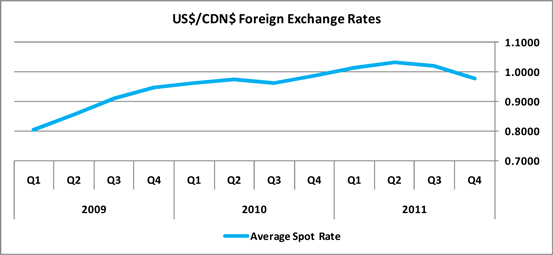

Canadian dollar

The chart below illustrates the movement of the US$/CDN$ average spot rate over the past three years:

| US$/CDN$ Exchange |

| | 2009 | 2010 | 2011 |

| | Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4 | Q1 | Q2 | Q3 | Q4 |

| Average spot rate | 0.803 | 0.857 | 0.911 | 0.947 | 0.961 | 0.973 | 0.962 | 0.987 | 1.015 | 1.033 | 1.020 | 0.977 |

| Average effective rate | 0.832 | 0.860 | 0.906 | 0.934 | 0.938 | 0.949 | 0.948 | 0.982 | 1.011 | 1.032 | 1.020 | 0.977 |

| Period-end spot rate | 0.794 | 0.860 | 0.933 | 0.956 | 0.985 | 0.943 | 0.971 | 1.005 | 1.029 | 1.037 | 0.963 | 0.983 |

The majority of our sales are denominated in U.S. dollars. During 2011, the Canadian dollar strengthened significantly against the U.S. dollar for most of the year. The unfavourable movement in the average year-over-year spot rate was slightly offset by the favourable impact of our hedge positions, which helped lower our average effective exchange rate in 2011. Overall the US$/CDN$ exchange rate movements had a negative impact of $63.1 million on revenue and a negative impact of $40.5 million on EBITDA. The increase in the year-end spot rate resulted in an after-tax foreign exchange loss of $11.8 million on the translation of U.S. dollar denominated debt in 2011, compared to an after-tax foreign exchange gain of $24.2 million in 2010. We have a program in place to hedge a portion of our anticipated U.S. dollar sales, although, effective April 1, 2010, we no longer designate the positions as hedges for accounting purposes. At December 31, 2011, the notional principal of the foreign currency options and forward contracts was US$148.0 million. Refer to our annual consolidated financial statements for the year ended December 31, 2011, note 25,Financial instruments, for additional details.

| 14 Management’s Discussion and Analysis - February 29, 2012 | |

Our goal is to return to profitability and maximize cash flows through capital restructuring, reducing manufacturing costs and optimizing our brands and customer base.

PERFORMANCE METRICS

The following performance drivers are key to achieving our strategic goals and creating value for our investors:

| 1) | Financial performance and flexibility |

Our success depends on adequate liquidity and an appropriate capital structure. The ability to generate sufficient cash to maintain our operations, finance growth and service our debt and other obligations is critical.

Cash flows, liquidity and capital structure

| – | Continue to focus on cash flows, liquidity and cost reductions |

| – | Improve capital structure |

| Ø | Key performance indicators |

Key metrics to measure our ability to generate operating income and free cash flow include:

| – | EBITDA and EBITDA before restructuring costs |

| – | Average delivered cash costs per tonne and average delivered cash costs per tonne before specific items. |

Refer to section 13,Non-GAAP measures, for definitions of these measures.

| – | EBITDA declined in 2011 mostly due to a strong Canadian dollar for most of the year, rising ONP prices, production losses due to fires and extended maintenance outages and increased maintenance spending. |

| 15 Management’s Discussion and Analysis - February 29, 2012 | |

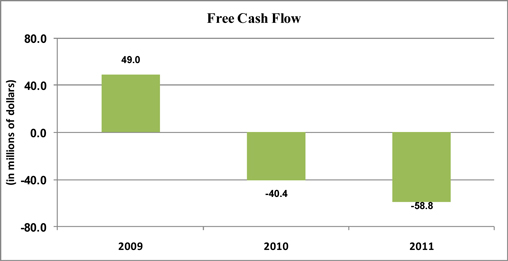

| – | Free cash flow for the year was negative $58.8 million. EBITDA of $41.6 million was more than offset by interest expense (excluding non-cash amortization) of $72.6 million, capital expenditures of $19.7 million and cash contributions to pensions and other post employment benefits in excess of the recorded expense of $8.0 million. |

| – | In February 2011 we redeemed the 8.625% senior notes that were due June 2011 for US$26.0 million. |

| – | We successfully renegotiated our ABL Facility, thereby extending the maturity date from 2013 to 2016 and reducing the amount of the Facility from $330.0 million to $175.0 million. |

| – | Inflationary pressure resulted in increases to our cost structure. The cost of chips, coating and chemicals increased significantly in 2011. |

| – | Realized annual fixed cost savings of approximately $13 million in 2011 in connection with the permanent closure of the Elk Falls mill and the Coquitlam paper recycling facility. |

| 16 Management’s Discussion and Analysis - February 29, 2012 | |

| – | Capital spending for the year was $19.7 million which included $12.9 million for maintenance of business. Prior year capital spending of $11.2 million included $6.7 million for maintenance of business. |

| 2) | Product mix and positioning |

Shifting our production mix to higher value grades, capturing a bigger share of the market, penetrating new markets and diversifying our product mix to manage fluctuations in demand to ensure that we remain competitive in a challenging marketplace.

Product mix

Continue to innovate and diversify product lines

| Ø | Key performance indicators |

Key metrics include average sales revenue per tonne. Further details on 2011 results are provided in section 4,Consolidated results – annual,section 5,Segmented results – annual,and section 6,Consolidated and segmented results – quarterly.

| 1 | Refer to section 15,Changes in accounting policies, for a discussion of the change in our policy with respect to classification of gains and losses on certain of our derivative financial instruments and translation of foreign currency-denominated working capital balances effective January 1, 2010. Prior period comparative information has been restated. |

| – | Produced uncoated freesheet paper under trial conditions achieving generally positive results. |

| – | Completed the development of our uncoated book grades to provide a full range of caliper-controlled paper for book publishers, including initial trials of recycled book paper from our Snowflake mill. |

| – | Increased our capability to supply uncoated high bright grades to the retail insert market by expanding the production of our lightest weight grades at Crofton and Snowflake. |

| 17 Management’s Discussion and Analysis - February 29, 2012 | |

| – | Expanded capability of Snowflake to include the production of directory paper. Catalyst is now able to produce 100% recycled, FSC certified directory paper to better satisfy the demands of the largest directory publishers. |

Market position

Grow market share.

| Ø | Key performance indicators |

Key metrics include total sales tonnes. Further details on 2011 results are provided in section 4,Consolidated results – annual,section 5,Segmented results – annual,and section 6,Consolidated and segmented results – quarterly.

| – | Despite declining demand for most paper grades, Catalyst continued to gain market share in all of our pulp and specialty papers grade categories. New products such as Pacificote, our coated mechanical four grade, and Electrabrite Book Sage have contributed to this growth. |

| – | Renewed annual contracts with all our largest telephone directory customers at higher prices. Consolidated our position as the largest, most reliable directory producer in North America. |

| 3) | Corporate Social Responsibility |

Corporate social responsibility is a core value. We are focused on improving workplace safety, promoting better communication with employees and following conservation practices that reduce our environmental impact.

| 18 Management’s Discussion and Analysis - February 29, 2012 | |

Safety

Significantly improve safety performance. Safety is our first operating priority and was an area of renewed focus in 2011.

| Ø | Key performance indicators |

Key metrics include the medical incident rate (MIR) which is the number of incidents requiring medical attention per 200,000 hours worked, and the lost-time injury frequency (LTI) which is the number of lost-time injuries per 200,000 hours worked.

| – | Compared to historical results, there was a significant improvement in safety in 2011 though targets for the year were narrowly missed. |

| – | Safety initiatives were implemented through the year including a field hazard assessment process, a company-wide safety improvement team, and a high-impact employee safety awareness program. |

Employee communication

Enhance employee communication to promote a productive, safe and customer-focused operating environment and effective internal controls.

| Ø | Key performance indicators |

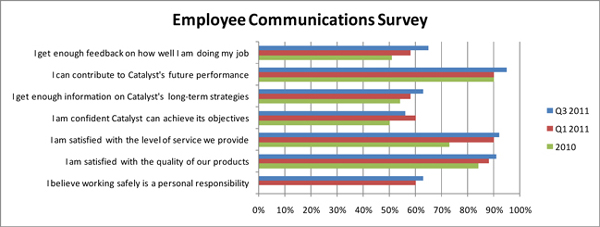

A key metric to evaluate the results of our internal communication programs is our bi-annual employee communications survey.

| 19 Management’s Discussion and Analysis - February 29, 2012 | |

| – | A number of programs were initiated in 2011 to strengthen employee communication and engagement. |

| – | Employee communications survey results showed improvements in all but one indicator as uncertainly over the future of the pulp-and-paper industry and the company’s capital structure took a toll on employee confidence in the business. |

Competitive Business Conditions

Continue to seek competitive business conditions in B.C., including joint municipal infrastructure agreements.

| Ø | Key performance indicators |

A key measure to evaluate our success in establishing more favourable business conditions is the level of municipal and provincial property taxes levied in respect of our operations in British Columbia.

| 20 Management’s Discussion and Analysis - February 29, 2012 | |

| – | Reduction in total property tax is due primarily to facility closures in 2010. Our agreement with the City of Powell River also yielded reduced property taxes. Property tax rates levied on our other B.C. facilities have not changed significantly since 2009. |

| – | Continued to implement the agreement in principle with the City of Powell River including settling service arrangements under which the City’s municipal waste would be treated using the mill’s effluent system and disposed of in the mill’s wood waste boiler. |

| – | In September 2011, the City of Powell River adopted the Revitalization Tax Exemption Program Bylaw, maintaining the mill’s annual tax payment at the agreed level for a further four years provided the annual application requirements are met. |

Capital upgrades to reduce environmental impact

Capital upgrade of $5 million at Port Alberni mill to improve combustion efficiency and environmental performance of its biomass boiler and a $13 million upgrade at Powell River mill to increase the electrical generation of the existing generator.

| Ø | Key performance indicators |

We track the progress of these upgrades based on capital and other costs incurred, the portion of these costs we get reimbursed for, environmental impact, EBITDA savings to date and anticipated EBITDA savings.

| – | We received the Green Transformation Program funding approval for these projects in February 2011. |

| – | Each of these projects is in process and scheduled to complete in advance of the March 31, 2012 spending deadline for the Pulp and Paper Green Transformation Program. Completion of these projects is expected to result in annual EBITDA improvement of $5.0 million. |

| 21 Management’s Discussion and Analysis - February 29, 2012 | |

| – | Completed close to $2 million worth of improvements to Robertson Creek dam at Port Alberni. The new dam meets all current provincial safety guidelines and protects the federal fish hatchery and properties downstream. |

Conservation practices and processes

| – | Achieve conservation targets in water and energy. |

| – | Implement Forest Stewardship Council chain of custody certification at all Canadian mills. |

| Ø | Key performance indicators |

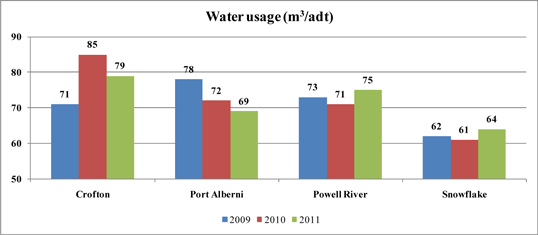

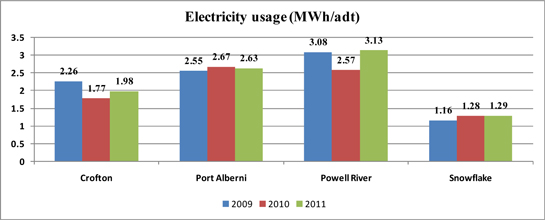

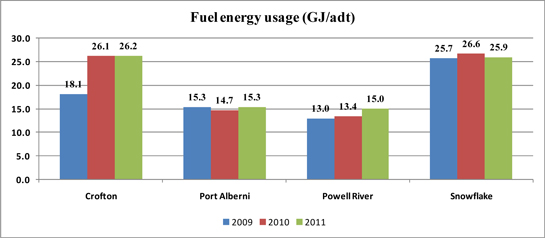

Key performance metrics include water, electricity and fuel usage. Water usage is measured as cubic meter per air-dried tonne (m3/adt). Electricity usage is measured in megawatt-hours per air-dried tonne (MWh/adt) and includes all purchased and self-generated electricity. Fuel energy usage is measured in gigajoules per air-dried tonne (GJ/adt) and includes all purchased fuels and self-generated biomass (black liquor).

| – | Water audits completed at our Port Alberni and Crofton mills to verify usage, associated energy costs, and identify conservation opportunities through improved processes. |

| 22 Management’s Discussion and Analysis - February 29, 2012 | |

| – | Usage of both fuel energy and electricity per tonne of production were up modestly in 2011. Intensity of energy use was impacted in recent years by production curtailments and product mix. Reduced pulp production in 2009, for example, resulted in relatively low fuel-energy intensity and increased electricity intensity. |

| – | A new Energy Improvement Team is streamlining the process of moving from conservation ideas to implementation, and developing usage benchmarks and analysis based on current mill configurations. |

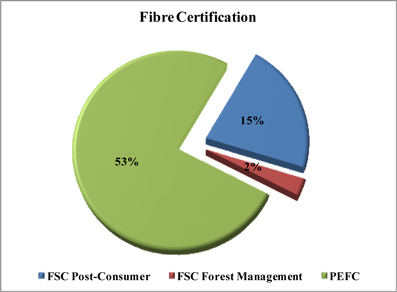

| – | 70% of our overall fibre supply is certified to a recognized standard. In addition to the Programme for the Endorsement of Forest Certification (PEFC) chain of custody, the company implemented the Forest Stewardship Council (FSC) chain of custody system at its B.C. mills to support targeted sales and marketing campaigns. The Snowflake recycled paper mill is also FSC chain of custody certified. |

See section 20,Outlook, for details of our key priorities for 2012.

| 23 Management’s Discussion and Analysis - February 29, 2012 | |

| 4 | CONSOLIDATED RESULTS - ANNUAL |

| | Consolidated results of operations |

Year ended December 31, 2011 compared to year ended December 31, 2010

Sales

Sales increased by $32.9 million in 2011 as the favourable impact of higher transaction prices for pulp and paper and increased sales volumes for pulp were partially offset by lower paper sales and the unfavourable impact of the stronger Canadian dollar.

| | The following table highlights the factors that affected our sales by segment: |

| (In millions of dollars) |

| | | Year ended December 31, | | | | | | Increase (decrease) from 2010 as a result of | |

| Sales | | 2011 | | | 2010 | | | Total

change | | | Volume | | | Price1 | | | Foreign

exchange | |

| Specialty printing papers | | $ | 718.7 | | | $ | 700.1 | | | $ | 18.6 | | | $ | 9.2 | | | $ | 44.2 | | | $ | (34.8 | ) |

| Newsprint | | | 294.8 | | | | 303.5 | | | | (8.7 | ) | | | (24.4 | ) | �� | | 28.7 | | | | (13.0 | ) |

| Total paper | | | 1,013.5 | | | | 1,003.6 | | | | 9.9 | | | | (15.2 | ) | | | 72.9 | | | | (47.8 | ) |

| Pulp | | | 248.0 | | | | 225.0 | | | | 23.0 | | | | 26.0 | | | | 12.3 | | | | (15.3 | ) |

| Total | | $ | 1,261.5 | | | $ | 1,228.6 | | | $ | 32.9 | | | $ | 10.8 | | | $ | 85.2 | | | $ | (63.1 | ) |

| 1 | Price is inclusive of sales mix. |

EBITDA and EBITDA before restructuring costs

The following table provides variances between periods for EBITDA and EBITDA before restructuring costs:

| (In millions of dollars) | | EBITDA 1 | | | EBITDA before restructuring costs1 | |

| 2010 | | $ | 46.3 | | | $ | 71.6 | |

| Paper prices | | | 72.9 | | | | 72.9 | |

| Pulp prices | | | 12.3 | | | | 12.3 | |

| Impact of Canadian dollar | | | (40.5 | ) | | | (40.5 | ) |

| Volume and mix | | | 20.5 | | | | 20.5 | |

| Furnish mix and costs | | | (41.4 | ) | | | (41.4 | ) |

| Power and fuel costs | | | (0.5 | ) | | | (0.5 | ) |

| Labour costs | | | (6.7 | ) | | | (6.7 | ) |

| Maintenance costs | | | (21.1 | ) | | | (21.1 | ) |

| Lower of cost or market impact on inventory, net of inventory change | | | (10.6 | ) | | | (10.6 | ) |

| Selling, general and administrative costs | | | 2.6 | | | | 2.6 | |

| Restructuring costs | | | 19.4 | | | | – | |

| Other, net | | | (11.6 | ) | | | (11.6 | ) |

| 2011 | | $ | 41.6 | | | $ | 47.5 | |

| 1 | Refer to section 13, Non-GAAP measures, for further details. |

Operating earnings (loss)

Operating earnings dropped by $526.9 million due to an increase in impairment and other closure costs of $529.1 and lower EBITDA of $4.7 million, partially offset by a reduction in depreciation and amortization expense of $6.9 million. Impairment and other closure costs totalled $823.6 million for 2011, consisting mostly of the impairment of the pulp and paper assets of our Canadian operations as well as the impairment of Snowflake’s assets, while $294.5 million was recognized in 2010 on the closure of the Elk Falls mill and Coquitlam paper recycling facility.

| 24 Management’s Discussion and Analysis - February 29, 2012 | |

Net earnings (loss) attributable to the company

Net loss attributable to the company increased by $577.1 million. This was primarily due to lower after-tax operating earnings driven by a $532.2 million after-tax increase in impairment and other closure costs, $6.4 million in after-tax losses we incurred on the fires at our Snowflake and Powell River mills and an after-tax foreign exchange loss on the translation of our U.S. dollar denominated debt of $11.8 million compared to an after-tax gain of $24.2 million in the previous year.

The following table reconciles 2011 net earnings (loss) attributable to the company to 2010:

| (In millions of dollars) | | Pre-tax | | | After-tax | |

| 2010 net earnings (loss) attributable to the company | | $ | (413.2 | ) | | $ | (396.9 | ) |

| Lower EBITDA before restructuring costs | | | (24.1 | ) | | | (5.6 | ) |

| Lower restructuring costs | | | 19.4 | | | | 15.4 | |

| Lower depreciation and amortization expense | | | 6.9 | | | | (22.9 | ) |

| Higher impairment charge in 2011 | | | (529.1 | ) | | | (532.2 | ) |

| Change in foreign exchange gain (loss) on long-term debt | | | (37.3 | ) | | | (36.0 | ) |

| Gain on cancellation of long-term debt in 2010 | | | (0.6 | ) | | | (0.5 | ) |

| Loss on Snowflake fire in 2011 | | | (4.4 | ) | | | (4.4 | ) |

| Loss on Powell River fire in 2011 | | | (2.4 | ) | | | (2.0 | ) |

| Lower other expense, net | | | 3.5 | | | | 3.0 | |

| Higher interest expense | | | (1.4 | ) | | | (9.2 | ) |

| Lower income tax recovery | | | – | | | | 16.0 | |

| Change in net earnings (loss) attributable to non-controlling interest | | | 1.3 | | | | 1.3 | |

| 2011 net earnings (loss) attributable to the company | | $ | (981.4 | ) | | $ | (974.0 | ) |

| 5 | SEGMENTED RESULTS - ANNUAL |

Specialty printing papers

| (In millions of dollars, except where otherwise stated) |

| | | 2011 | | | 2010 | | | 20091 | |

| Sales | | $ | 718.7 | | | $ | 700.1 | | | $ | 832.3 | |

| Operating earnings (loss) | | | (585.7 | ) | | | (147.5 | ) | | | 41.1 | |

| Depreciation and amortization | | | 81.9 | | | | 79.6 | | | | 93.8 | |

| EBITDA2 | | | 24.1 | | | | 36.5 | | | | 134.9 | |

| – before restructuring costs2 | | | 27.6 | | | | 44.7 | | | | 146.6 | |

| EBITDA margin2 | | | 3.4 | % | | | 5.2 | % | | | 16.2 | % |

| – before restructuring costs2 | | | 3.8 | % | | | 6.4 | % | | | 17.6 | % |

| | | | | | | | | | | | | |

| (In thousands of tonnes) | | | | | | | | | | | | |

| Sales | | | 878.6 | | | | 867.0 | | | | 896.5 | |

| Production | | | 883.4 | | | | 873.3 | | | | 890.6 | |

| | | | | | | | | | | | | |

| 1 | Refer to section 15,Changes in accounting policies, for a discussion of the change in our policy with respect to classification of gains and losses on certain of our derivative financial instruments and translation of foreign currency-denominated working capital balances effective January 1, 2010. Prior period comparative information has been restated. |

| 2 | Refer to section 13,Non-GAAP measures. |

| 25 Management’s Discussion and Analysis - February 29, 2012 | |

Segment Overview

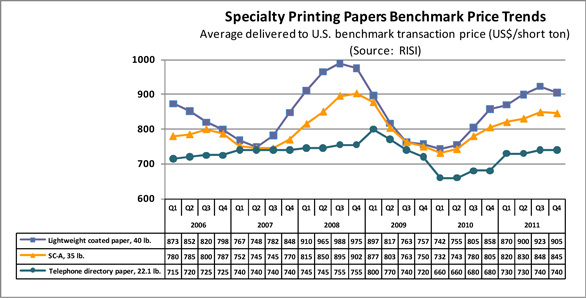

| | North American demand for coated mechanical decreased 8.6% for the year due to a slowdown in the economic recovery in 2011 that resulted in reduced advertising pages in magazines and a decrease in catalogues being mailed out. While inventories increased for the year, adjusted operating rates continued to remain steady due to mill closures and other capacity shuts. The average benchmark price for lightweight coated paper (LWC) increased to US$900 per short ton from US$790 per short ton in 2010. The LWC benchmark price peaked in the third quarter of 2011 and has been dropping since that time. |

| | North American uncoated mechanical demand (high-gloss and standard grades) decreased 5.8% due to declines in print advertising and lower circulation and page counts for retail inserts. Our sales volumes rebounded in the second half of the year after the second quarter extended maintenance outage and fire at Powell River. Average benchmark prices for super-calendered A grade (SC-A) delivered to the U.S. of US$836 per short ton in 2011 increased by9.3% compared to the previous year. A series of machine closuresin the USA and Europe kept the uncoated mechanical market tight despite weak demand. |

| | We partially implemented a number of announced price increases for the year, including increases of US$40 per short ton effective April 1, 2011 and US$30 per short ton effective July 1, 2011 on all coated and high gloss grades. Additionally, we successfully implemented the majority of the June 1 US$40 per short ton and partially implemented the October 1 US$30 per short ton increase for standard uncoated mechanical grades. |

| | North American directory demand decreased 20.8% in 2011 from the prior year. Factors contributing to the precipitous decline include a reduction in the publication of white pages, smaller book sizes, lower circulation, and the continued migration from printed directory books to the Internet. Market conditions improved in the second half of the year due to the closure of significant competitive capacity in North America. At US$735 per short ton, the average directory benchmark price for the current year increased by9.7% compared to the prior year reflecting higher 2011 contract prices. We implemented a July 1, 2011 US$70 per ton price increase on our non-contract customers. The majority of our directory pricing was largely fixed for the year based on 2011 contract pricing. |

| 26 Management’s Discussion and Analysis - February 29, 2012 | |

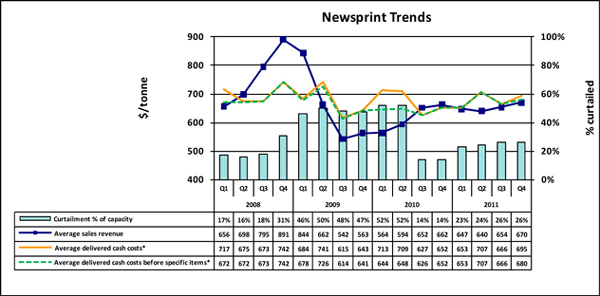

Operational performance

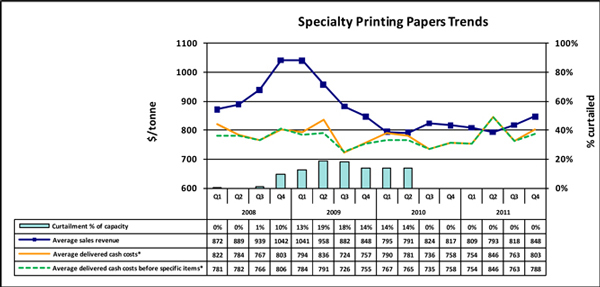

The following chart summarizes the operating performance of our specialty printing papers segment:

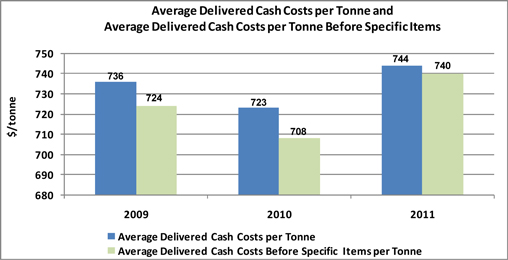

| * | Average delivered cash costs per tonne consist of cost of sales, excluding depreciation and amortization, and including the impact of SG&A and restructuring costs. Average delivered cash costs per tonne before specific items consist of cost of sales, excluding depreciation and amortization, and including the impact of SG&A, but excluding the impact of restructuring costs. |

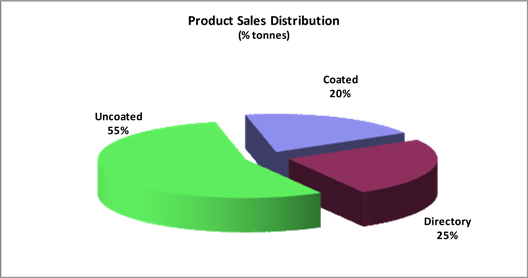

| | The 2011 specialty printing papers product-grade distribution, based on sales volume, is depicted in the chart below: |

| 27 Management’s Discussion and Analysis - February 29, 2012 | |

The 2011 specialty printing papers geographic sales distribution, based on sales volume, is depicted in the chart below.

| · | Sales volume increased by 11,600 tonnes due to higher coated and uncoated sales volumes, partially offset by slightly lower directory sales volumes for the year. |

| · | Average sales revenue increased $11 per tonne, reflecting higher average transaction prices that were partially offset by the negative impact of a stronger Canadian dollar. |

| · | Average delivered cash costs increased $26 per tonne due to increased maintenance, labour, chemicals and electric power costs as well as higher furnish cost mostly due to increased cost of chips and coating. This was partially offset by a reduction in restructuring costs. |

Newsprint

| | (In millions of dollars, except where otherwise stated) |

| | | | 2011 | | | 2010 | | | 20091 | |

| | Sales | | $ | 294.8 | | | $ | 303.5 | | | $ | 320.6 | |

| | Operating earnings (loss) | | | (239.9 | ) | | | (243.7 | ) | | | (70.3 | ) |

| | Depreciation and amortization | | | 15.5 | | | | 25.4 | | | | 44.5 | |

| | EBITDA2 | | | (12.2 | ) | | | (28.2 | ) | | | (8.4 | ) |

| | – before restructuring costs2 | | | (10.7 | ) | | | (12.1 | ) | | | (5.4 | ) |

| | EBITDA margin2 | | | (4.1 | %) | | | (9.3 | %) | | | (2.6 | %) |

| | – before restructuring costs2 | | | (3.6 | %) | | | (4.0 | %) | | | (1.7 | %) |

| | | | | | | | | | | | | | |

| | (In thousands of tonnes) | | | | | | | | | | | | |

| | Sales | | | 451.7 | | | | 491.3 | | | | 488.2 | |

| | Production | | | 457.4 | | | | 479.0 | | | | 497.3 | |

| | | | | | | | | | | | | | |

| 1 | Refer to section 15,Changes in accounting policies, for a discussion of the change in our policy with respect to classification of gains and losses on certain of our derivative financial instruments and translation of foreign currency-denominated working capital balances effective January 1, 2010. Prior period comparative information has been restated. |

| 2 | Refer to section 13,Non-GAAP Measures. |

| 28 Management’s Discussion and Analysis - February 29, 2012 | |

Segment Overview

| | North American newsprint shipments were down by 6.4% in 2011. Exports fell by 5.5% as demand for newsprint around the world cooled off. North American demand declined 7.4% due to weak advertising and declining circulation. Operating rates remained similar to the prior year as North American newsprint capacity was shut at a rate to compensate for declining demand. |

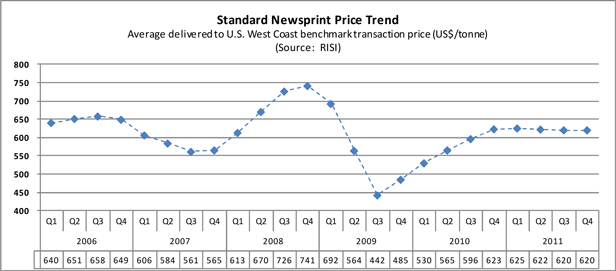

| | The average North American Newsprint benchmark price increased to US$622 per metric tonne or 7.6% compared to the previous year. No price increases were announced for 2011. |

| | The Crofton No. 1 paper machine, originally curtailed in January 2010, remained indefinitely curtailed throughout 2011, resulting in 140,000 tonnes of curtailment on an annualized basis or 23% of our 2011 newsprint capacity. |

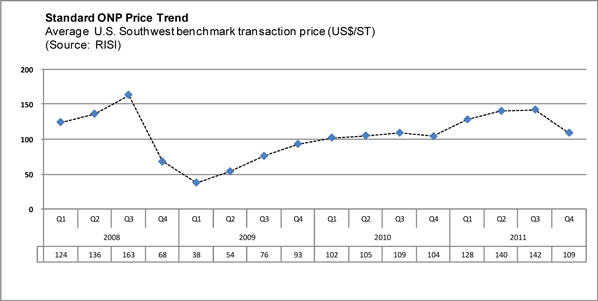

| | Strong demand from China has fuelled an upward trend in ONP prices since 2009. This price pressure has had a significant impact on the profitability of the Snowflake mill’s recycled newsprint operation. Snowflake accounted for approximately 54% of the company’s newsprint output in 2011. ONP prices peaked in the third quarter and the average Southwest benchmark price has decreased to US$109 per short ton for Q4 compared to US$142 per short ton for Q3. The recent weakening in ONP prices is primarily due to excess inventories and reduced demand from China. |

| 29 Management’s Discussion and Analysis - February 29, 2012 | |

Operational performance

The following chart summarizes the operating performance of our newsprint segment:

| * | Average delivered cash costs per tonne consist of cost of sales, excluding depreciation and amortization, and including the impact of SG&A and restructuring costs. Average delivered cash costs per tonne before specific items consist of cost of sales, excluding depreciation and amortization, and including the impact of SG&A, but excluding the impact of restructuring costs. |

| 30 Management’s Discussion and Analysis - February 29, 2012 | |

The 2011 newsprint geographic sales distribution, based on sales volume, is depicted in the chart below:

| · | Sales volume decreased by 39,600 tonnes due to declining newsprint demand, lower production resulting from the extended maintenance outage at our Snowflake mill during the second quarter of 2011 and our conversion to produce more specialty printing papers. |

| · | Average sales revenue increased $35 per tonne due to higher transaction prices, partially offset by the negative impact of the stronger Canadian dollar. |

| · | Average delivered cash costs increased $5 per tonne due to higher ONP prices and increased maintenance costs due in part to the extended maintenance outage at Snowflake, partially offset by reduced restructuring costs in the current year. |

Pulp

| | (In millions of dollars, except where otherwise stated) |

| | | | 2011 | | | 2010 | | | 20091 | |

| | Sales | | $ | 248.0 | | | $ | 225.0 | | | $ | 70.6 | |

| | Operating earnings (loss) | | | (68.8 | ) | | | 23.7 | | | | (11.6 | ) |

| | Depreciation and amortization | | | 15.0 | | | | 14.3 | | | | 8.3 | |

| | EBITDA2 | | | 29.7 | | | | 38.0 | | | | (3.3 | ) |

| | – before restructuring costs2 | | | 30.6 | | | | 39.0 | | | | (0.1 | ) |

| | EBITDA margin2 | | | 12.0 | % | | | 16.9 | % | | | (4.7 | %) |

| | – before restructuring costs2 | | | 12.3 | % | | | 17.3 | % | | | (0.1 | %) |

| | | | | | | | | | | | | | |

| | (In thousands of tonnes) | | | | | | | | | | | | |

| | Sales | | | 308.5 | | | | 276.6 | | | | 110.2 | |

| | Production | | | 315.0 | | | | 273.4 | | | | 87.5 | |

| | | | | | | | | | | | | | |

| 1 | Refer to section 15,Changes in accounting policies, for a discussion of the change in our policy with respect to classification of gains and losses on certain of our derivative financial instruments and translation of foreign currency-denominated working capital balances effective January 1, 2010. Prior period comparative information has been restated. |

| 2 | Refer to section 13,Non-GAAP measures. |

| 31 Management’s Discussion and Analysis - February 29, 2012 | |

Segment Overview

| | Global shipments of NBSK pulp grew 4.8% in 2011 compared to the previous year, driven primarily by increased demand from China which increased its demand by 30.5%. NBSK pulp markets weakened in the second half of the year as global inventories rose and demand from China weakened. The rapid increase in pulp prices seen in recent years continued in the first half of 2011 with the average NBSK benchmark price for China peaking in the second quarter at US$920 per tonne. This price declined to US$713 per tonne in Q4 due to the slowdown in Chinese buying and increase in global pulp inventories. The average benchmark price for the year of US$834 per tonne was 1.6% higher than 2010. |

| | We expanded Crofton’s pulp capacity by 25,000 tonnes to 1,120 tonnes per day (tpd) based on a plan that was approved in May. |

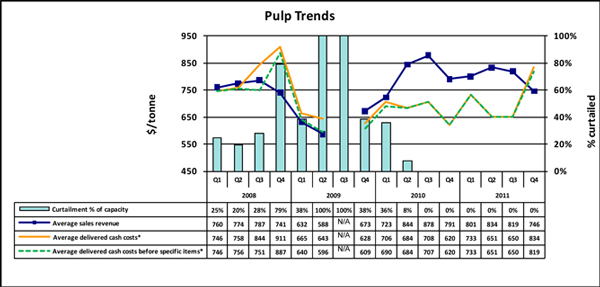

Operational performance

The following chart summarizes the operating performance of our pulp segment:

| 32 Management’s Discussion and Analysis - February 29, 2012 | |

| * | Average delivered cash costs per tonne consist of cost of sales, excluding depreciation and amortization, and including the impact of SG&A and restructuring costs. Average delivered cash costs per tonne before specific items consist of cost of sales, excluding depreciation and amortization, and including the impact of SG&A, but excluding the impact of restructuring costs. |

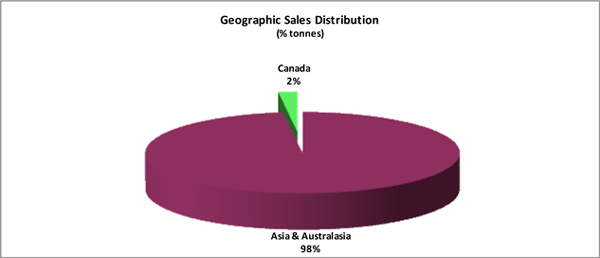

| | The primary market for our market pulp is Asia. The 2011 pulp geographic sales distribution, based on sales volume, is depicted in the chart below: |

| · | Sales volume increased by 31,900 tonnes due to increased shipments to China for most of the year as well as the fact that pulp production was fully operational throughout the current year while being partially curtailed in 2010. |

| · | Average sales revenue decreased by $9 per tonne due to the negative impact of the stronger Canadian dollar that more than offset higher average transaction prices for the year. |

| · | Average delivered cash costs increased by $31 per tonne due to a write-down on pulp inventories to net realizable value as well as cost increases to freight, chips, chemicals and operating supplies. |

| 33 Management’s Discussion and Analysis - February 29, 2012 | |

| 6 | CONSOLIDATED AND SEGMENTED RESULTS - QUARTERLY |

Selected quarterly financial information

| | (In millions of dollars, except where otherwise stated) |

| | | | 2011 | | | 2010 | |

| | | | TOTAL | | | Q4 | | | Q3 | | | Q2 | | | Q1 | | | TOTAL | | | Q4 | | | Q3 | | | Q2 | | | Q1 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Sales | | $ | 1,261.5 | | | $ | 319.8 | | | $ | 340.3 | | | $ | 297.8 | | | $ | 303.6 | | | $ | 1,228.6 | | | $ | 333.6 | | | $ | 322.3 | | | $ | 299.4 | | | $ | 273.3 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Operating earnings (loss) | | | (894.4 | ) | | | (701.3 | ) | | | (151.6 | ) | | | (30.6 | ) | | | (10.9 | ) | | | (367.5 | ) | | | 0.2 | | | | 5.1 | | | | (323.9 | ) | | | (48.9 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Depreciation and amortization | | | 112.4 | | | | 30.8 | | | | 27.8 | | | | 27.0 | | | | 26.8 | | | | 119.3 | | | | 27.2 | | | | 28.2 | | | | 31.2 | | | | 32.7 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | EBITDA1 | | | 41.6 | | | | 2.8 | | | | 26.8 | | | | (3.9 | ) | | | 15.9 | | | | 46.3 | | | | 28.7 | | | | 34.2 | | | | (0.4 | ) | | | (16.2 | ) |

| | – before restructuring costs1 | | | 47.5 | | | | 8.7 | | | | 26.8 | | | | (3.9 | ) | | | 15.9 | | | | 71.6 | | | | 28.7 | | | | 34.5 | | | | 10.5 | | | | (2.1 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Net earnings (loss) attributable to the company | | | (974.0 | ) | | | (708.0 | ) | | | (205.7 | ) | | | (47.4 | ) | | | (12.9 | ) | | | (396.9 | ) | | | 9.6 | | | | 6.0 | | | | (368.4 | ) | | | (44.1 | ) |

| | – before specific items1 | | | (126.3 | ) | | | (41.7 | ) | | | (14.1 | ) | | | (46.9 | ) | | | (23.6 | ) | | | (87.0 | ) | | | 4.1 | | | | (9.6 | ) | | | (43.9 | ) | | | (37.6 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | EBITDA margin1 | | | 3.3 | % | | | 0.9 | % | | | 7.9 | % | | | (1.3 | %) | | | 5.2 | % | | | 3.8 | % | | | 8.6 | % | | | 10.6 | % | | | (0.1 | %) | | | (5.9 | %) |

| | – before restructuring costs1 | | | 3.8 | % | | | 2.7 | % | | | 7.9 | % | | | (1.3 | %) | | | 5.2 | % | | | 5.8 | % | | | 8.6 | % | | | 10.7 | % | | | 3.5 | % | | | (0.8 | %) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Net earnings (loss) per share attributable to the company’s common shareholders (in dollars)

– basic and diluted | | $ | (2.55 | ) | | $ | (1.85 | ) | | $ | (0.54 | ) | | $ | (0.13 | ) | | $ | (0.03 | ) | | $ | (1.04 | ) | | $ | 0.02 | | | $ | 0.02 | | | $ | (0.96 | ) | | $ | (0.12 | ) |

| | – before specific items1 | | | (0.33 | ) | | | (0.11 | ) | | | (0.04 | ) | | | (0.12 | ) | | | (0.06 | ) | | | (0.23 | ) | | | 0.01 | | | | (0.03 | ) | | | (0.11 | ) | | | (0.10 | ) |

| | (In thousands of tonnes) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Sales (000 tonnes) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Specialty printing papers | | | 878.6 | | | | 239.3 | | | | 229.8 | | | | 202.8 | | | | 206.7 | | | | 867.0 | | | | 231.3 | | | | 220.6 | | | | 208.9 | | | | 206.2 | |

| | Newsprint | | | 451.7 | | | | 105.7 | | | | 117.8 | | | | 111.8 | | | | 116.4 | | | | 491.3 | | | | 122.8 | | | | 122.3 | | | | 123.1 | | | | 123.1 | |

| | Total paper | | | 1,330.3 | | | | 345.0 | | | | 347.6 | | | | 314.6 | | | | 323.1 | | | | 1,358.3 | | | | 354.1 | | | | 342.9 | | | | 332.0 | | | | 329.3 | |

| | Pulp | | | 308.5 | | | | 61.6 | | | | 92.2 | | | | 78.4 | | | | 76.3 | | | | 276.6 | | | | 80.0 | | | | 69.2 | | | | 72.5 | | | | 54.9 | |

| | Total sales | | | 1,638.8 | | | | 406.6 | | | | 439.8 | | | | 393.0 | | | | 399.4 | | | | 1,634.9 | | | | 434.1 | | | | 412.1 | | | | 404.5 | | | | 384.2 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Production (000 tonnes) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Specialty printing papers | | | 883.4 | | | | 238.2 | | | | 230.0 | | | | 200.9 | | | | 214.3 | | | | 873.3 | | | | 225.4 | | | | 226.6 | | | | 209.1 | | | | 212.2 | |

| | Newsprint | | | 457.4 | | | | 109.3 | | | | 111.6 | | | | 111.7 | | | | 124.8 | | | | 479.0 | | | | 120.7 | | | | 120.1 | | | | 124.5 | | | | 113.7 | |

| | Total paper | | | 1,340.8 | | | | 347.5 | | | | 341.6 | | | | 312.6 | | | | 339.1 | | | | 1,352.3 | | | | 346.1 | | | | 346.7 | | | | 333.6 | | | | 325.9 | |

| | Pulp | | | 315.0 | | | | 73.5 | | | | 86.7 | | | | 83.5 | | | | 71.3 | | | | 273.4 | | | | 83.7 | | | | 71.0 | | | | 69.4 | | | | 49.3 | |

| | Total production | | | 1,655.8 | | | | 421.0 | | | | 428.3 | | | | 396.1 | | | | 410.4 | | | | 1,625.7 | | | | 429.8 | | | | 417.7 | | | | 403.0 | | | | 375.2 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Common shares (millions) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | At period-end | | | 381.9 | | | | 381.9 | | | | 381.9 | | | | 381.8 | | | | 381.8 | | | | 381.8 | | | | 381.8 | | | | 381.8 | | | | 381.8 | | | | 381.8 | |

| | Weighted average | | | 381.9 | | | | 381.9 | | | | 381.9 | | | | 381.8 | | | | 381.8 | | | | 381.8 | | | | 381.8 | | | | 381.8 | | | | 381.8 | | | | 381.8 | |

| 1 | Refer to section 13, Non-GAAP measures. |

| 34 Management’s Discussion and Analysis - February 29, 2012 | |

Summary of selected segmented quarterly financial information

| | (In millions of dollars, except where otherwise stated) |

| | | | 2011 | | | 2010 | |

| | Specialty printing papers | | TOTAL | | | Q4 | | | Q3 | | | Q2 | | | Q1 | | | TOTAL | | | Q4 | | | Q3 | | | Q2 | | | Q1 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Sales | | $ | 718.7 | | | $ | 202.8 | | | $ | 187.9 | | | $ | 160.9 | | | $ | 167.1 | | | $ | 700.1 | | | $ | 189.1 | | | $ | 181.8 | | | $ | 165.1 | | | $ | 164.1 | |

| | Operating earnings (loss) | | | (585.7 | ) | | | (522.5 | ) | | | (26.7 | ) | | | (29.3 | ) | | | (7.2 | ) | | | (147.5 | ) | | | (5.3 | ) | | | (1.8 | ) | | | (120.1 | ) | | | (20.3 | ) |

| | Depreciation and amortization | | | 81.9 | | | | 25.0 | | | | 19.6 | | | | 18.8 | | | | 18.5 | | | | 79.6 | | | | 18.5 | | | | 20.8 | | | | 19.0 | | | | 21.3 | |

| | EBITDA1 | | | 24.1 | | | | 10.8 | | | | 12.6 | | | | (10.6 | ) | | | 11.3 | | | | 36.5 | | | | 13.8 | | | | 19.5 | | | | 2.2 | | | | 1.0 | |

| | – before restructuring costs1 | | | 27.6 | | | | 14.3 | | | | 12.6 | | | | (10.6 | ) | | | 11.3 | | | | 44.7 | | | | 13.8 | | | | 19.6 | | | | 5.5 | | | | 5.8 | |

| | EBITDA margin1 | | | 3.4 | % | | | 5.3 | % | | | 6.7 | % | | | (6.6 | %) | | | 6.8 | % | | | 5.2 | % | | | 7.3 | % | | | 10.7 | % | | | 1.3 | % | | | 0.6 | % |

| | – before restructuring costs1 | | | 3.8 | % | | | 7.1 | % | | | 6.7 | % | | | (6.6 | %) | | | 6.8 | % | | | 6.4 | % | | | 7.3 | % | | | 10.8 | % | | | 3.3 | % | | | 3.5 | % |

| | Sales (000 tonnes) | | | 878.6 | | | | 239.3 | | | | 229.8 | | | | 202.8 | | | | 206.7 | | | | 867.0 | | | | 231.3 | | | | 220.6 | | | | 208.9 | | | | 206.2 | |

| | Production (000 tonnes) | | | 883.4 | | | | 238.2 | | | | 230.0 | | | | 200.9 | | | | 214.3 | | | | 873.3 | | | | 225.4 | | | | 226.6 | | | | 209.1 | | | | 212.2 | |

| | Curtailment (000 tonnes)2 | | | – | | | | – | | | | – | | | | – | | | | – | | | | 76.7 | | | | – | | | | – | | | | 38.0 | | | | 38.7 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Newsprint | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Sales | | $ | 294.8 | | | $ | 70.9 | | | $ | 77.0 | | | $ | 71.5 | | | $ | 75.4 | | | $ | 303.5 | | | $ | 81.2 | | | $ | 79.7 | | | $ | 73.1 | | | $ | 69.5 | |

| | Operating earnings (loss) | | | (239.9 | ) | | | (86.3 | ) | | | (136.4 | ) | | | (11.9 | ) | | | (5.3 | ) | | | (243.7 | ) | | | (4.5 | ) | | | (1.1 | ) | | | (211.8 | ) | | | (26.3 | ) |

| | Depreciation and amortization | | | 15.5 | | | | 2.2 | | | | 4.1 | | | | 4.5 | | | | 4.7 | | | | 25.4 | | | | 5.0 | | | | 3.7 | | | | 8.6 | | | | 8.1 | |

| | EBITDA1 | | | (12.2 | ) | | | (2.6 | ) | | | (1.4 | ) | | | (7.6 | ) | | | (0.6 | ) | | | (28.2 | ) | | | 1.2 | | | | 3.0 | | | | (14.2 | ) | | | (18.2 | ) |

| | – before restructuring costs1 | | | (10.7 | ) | | | (1.1 | ) | | | (1.4 | ) | | | (7.6 | ) | | | (0.6 | ) | | | (12.1 | ) | | | 1.2 | | | | 3.1 | | | | (6.7 | ) | | | (9.7 | ) |

| | EBITDA margin1 | | | (4.1 | %) | | | (3.7 | %) | | | (1.8 | %) | | | (10.6 | %) | | | (0.8 | %) | | | (9.3 | %) | | | 1.5 | % | | | 3.8 | % | | | (19.4 | %) | | | (26.2 | %) |

| | – before restructuring costs1 | | | (3.6 | %) | | | (1.6 | %) | | | (1.8 | %) | | | (10.6 | %) | | | (0.8 | %) | | | (4.0 | %) | | | 1.5 | % | | | 3.9 | % | | | (9.2 | %) | | | (14.0 | %) |

| | Sales (000 tonnes) | | | 451.7 | | | | 105.7 | | | | 117.8 | | | | 111.8 | | | | 116.4 | | | | 491.3 | | | | 122.8 | | | | 122.3 | | | | 123.1 | | | | 123.1 | |

| | Production (000 tonnes) | | | 457.4 | | | | 109.3 | | | | 111.6 | | | | 111.7 | | | | 124.8 | | | | 479.0 | | | | 120.7 | | | | 120.1 | | | | 124.5 | | | | 113.7 | |

| | Curtailment (000 tonnes)2 | | | 150.3 | | | | 39.7 | | | | 39.8 | | | | 36.3 | | | | 34.5 | | | | 327.5 | | | | 35.3 | | | | 35.3 | | | | 128.0 | | | | 128.9 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Pulp | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Sales | | $ | 248.0 | | | $ | 46.1 | | | $ | 75.4 | | | $ | 65.4 | | | $ | 61.1 | | | $ | 225.0 | | | $ | 63.3 | | | $ | 60.8 | | | $ | 61.2 | | | $ | 39.7 | |

| | Operating earnings (loss) | | | (68.8 | ) | | | (92.5 | ) | | | 11.5 | | | | 10.6 | | | | 1.6 | | | | 23.7 | | | | 10.0 | | | | 8.0 | | | | 8.0 | | | | (2.3 | ) |

| | Depreciation and amortization | | | 15.0 | | | | 3.6 | | | | 4.1 | | | | 3.7 | | | | 3.6 | | | | 14.3 | | | | 3.7 | | | | 3.7 | | | | 3.6 | | | | 3.3 | |

| | EBITDA1 | | | 29.7 | | | | (5.4 | ) | | | 15.6 | | | | 14.3 | | | | 5.2 | | | | 38.0 | | | | 13.7 | | | | 11.7 | | | | 11.6 | | | | 1.0 | |

| | – before restructuring costs1 | | | 30.6 | | | | (4.5 | ) | | | 15.6 | | | | 14.3 | | | | 5.2 | | | | 39.0 | | | | 13.7 | | | | 11.8 | | | | 11.7 | | | | 1.8 | |

| | EBITDA margin1 | | | 12.0 | % | | | (11.7 | %) | | | 20.7 | % | | | 21.9 | % | | | 8.5 | % | | | 16.9 | % | | | 21.6 | % | | | 19.2 | % | | | 19.0 | % | | | 2.5 | % |

| | – before restructuring costs1 | | | 12.3 | % | | | (9.8 | %) | | | 20.7 | % | | | 21.9 | % | | | 8.5 | % | | | 17.3 | % | | | 21.6 | % | | | 19.4 | % | | | 19.1 | % | | | 4.5 | % |

| | Sales (000 tonnes) | | | 308.5 | | | | 61.6 | | | | 92.2 | | | | 78.4 | | | | 76.3 | | | | 276.6 | | | | 80.0 | | | | 69.2 | | | | 72.5 | | | | 54.9 | |

| | Production (000 tonnes) | | | 315.0 | | | | 73.5 | | | | 86.7 | | | | 83.5 | | | | 71.3 | | | | 273.4 | | | | 83.7 | | | | 71.0 | | | | 69.4 | | | | 49.3 | |

| | Curtailment (000 tonnes)2 | | | – | | | | – | | | | – | | | | – | | | | – | | | | 37.9 | | | | – | | | | – | | | | 7.2 | | | | 30.7 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| 1 | Refer to section 13,Non-GAAP measures. |

| 2 | Curtailment consists of downtime related to market demand. |

| 35 Management’s Discussion and Analysis - February 29, 2012 | |

Fourth quarter overview

| | Demand for the quarter was down year-over-year for most paper grades but seasonal strength, low inventories, and high operating rates resulted in similar pricing compared to Q3. Directory and newsprint benchmark prices remained stable quarter-over-quarter while benchmark prices declined for coated and uncoated mechanical. Market conditions for pulp deteriorated significantly in the fourth quarter due to excess inventory and declining demand from China, with benchmark prices decreasing 15% to US$713 per tonne from US$840 per tonne in Q3. |

| | The positive impact of a weakening Canadian dollar was more than offset by a significant decline in pulp transaction prices, and lower pulp and paper shipments quarter-over-quarter. The weaker Canadian dollar resulted in a foreign exchange loss on the translation of our U.S. dollar denominated debt which negatively impacted our net earnings compared to the preceding quarter. |