UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-10467

Causeway Capital Management Trust

(Exact name of registrant as specified in charter)

11111 Santa Monica Boulevard, 15th Floor

Los Angeles, CA 90025

(Address of principal executive offices) (Zip code)

SEI Investments Global Funds Services

One Freedom Valley Drive

Oaks, PA 19456

(Name and address of agent for service)

Registrant’s telephone number, including area code: 1-866-947-7000

Date of fiscal year end: September 30, 2011

Date of reporting period: September 30, 2011

| Item 1. | Reports to Stockholders. |

LETTER TO SHAREHOLDERS

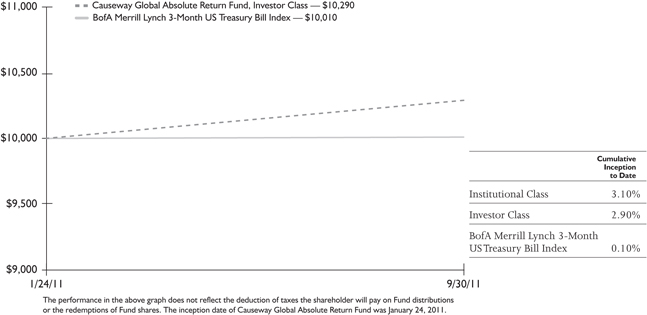

Since inception on January 24, 2011, through the fiscal year ended September 30, 2011, the Causeway Global Absolute Return Fund’s (“Fund’s”) Institutional Class returned (on a cumulative basis) +3.10% and Investor Class returned +2.90%, compared to +0.10% for the BofA Merrill Lynch 3-Month U.S. Treasury Bill Index. During the same period, the MSCI World Index (“World Index”) fell 14.04%. At fiscal year-end, the Fund had net assets of approximately $14.3 million.

Performance Review

The Fund’s global long portfolio takes long positions in securities under swap agreements, and the Fund’s global short portfolio takes short positions in securities under swap agreements. The global long portfolio underperformed the World Index, which detracted from overall performance, while the global short portfolio benefited the Fund by underperforming the World Index.

Global equity markets continued their ascent through early 2011. The effects of monetary stimulus in the United States spilled into real assets prices and propelled markets. Energy and other raw materials prices spiked dramatically, pressuring developing markets policy makers to continue tightening monetary policy to thwart inflation. Quality cyclicals (stocks exposed to global economic recovery) performed especially well in this climate, extending their recovery from the market troughs of early 2009. Market volatility subsided and reached fiscal year lows in the spring of 2011. The Chicago Board Options Exchange Market Volatility Index (VIX) dropped below 15 in April 2011. Analysis from our quantitative team showed growing investor complacency. By April 2011, our annualized two-year expected return of the stocks on the long side of the Fund’s portfolio had diminished to low double digits from the robust forecasts of late-2008/early-2009.

In May 2011, investor sentiment suddenly reversed and markets performed poorly through the end of the 2011 fiscal year. Global equities declined each of the last five months, with the most significant sell-offs occurring in August and September. The lack of resolution to the euro sovereign debt crisis and the increasing prospect of a double-dip recession caused investor confidence to plunge. During this period, every industry group and every developed stock market was in the red. A “risk-off” mentality permeated markets globally: correlations rose dramatically, as evidenced by VIX climbing into the mid-40s; emerging markets substantially underperforming developed markets; high yield bond spreads widening; and commodity prices plunging. The flight-to-safety trade was on, sending yields on 10-year US Treasury bonds to the lowest level ever recorded. Economically defensive sectors (consumer staples, health care, and telecommunication services) significantly outperformed the most economically cyclical sectors (materials, financials, and industrials). In this environment, the quantitatively managed short-side of the Fund was critical in protecting shareholders’ capital from broad market declines.

| | |

2 | | Causeway Global Absolute Return Fund |

Exposures to our global long positions are determined by our fundamental, bottom-up stock selection process. Global long positions in the transportation and consumer services industry groups as well as an overweight to the capital goods industry group detracted the most from relative performance versus the World Index, while long exposures in the food beverage & tobacco and consumer services industry groups as well as an underweight to the diversified financials industry group contributed to relative performance. The largest single detractor to return in the global long portfolio this period was an exposure to mail & parcel delivery company, PostNL (Netherlands). Other notable top detractors to return included exposures to shipbuilder, Sembcorp Marine (Singapore), engineering & construction company, Tecnicas Reunidas (Spain), Unicredit (Italy’s largest bank - which was sold during the period) and shipbuilder & heavy equipment manufacturer, Hyundai Heavy Industries (South Korea). The largest single positive contributor to the return in the long portfolio this period was an exposure to tobacco company, Lorillard (US). Additional top contributors to the return included exposures to healthcare providers, Centene Corp. (US) and UnitedHealth Group (US), oil services firm, National Oilwell Varco (US), and toy company, Mattel (US).

We use a quantitative approach for security selection for the global short portfolio of the Fund. Our quantitative model identifies short positions in stocks which we believe are overvalued and have deteriorating earnings growth dynamics, poor technical price movements, and insolvency risk and/or inferior quality of earnings. Since inception of the Fund through fiscal year end, three out of four of these categories of characteristics succeeded in identifying poor performers. The strongest predictive power came from our price-sensitive technical factors followed by our earnings growth metrics and insolvency/earnings quality metrics. Only our valuation metrics negatively impacted performance, meaning expensive stocks outperformed cheap stocks during the period (we tend to short expensive stocks).

The global short portfolio’s relative added-value since inception can primarily be attributed to successful stock selection; we had particular success in identifying downside candidates in the US, UK, and Euro region. We also benefited by taking more short exposure in the Euro region, and less in the US (compared to the World Index). From an industry group perspective, added value through stock selection was concentrated in diversified financials, energy, automobiles & components, and pharmaceuticals and biotechnology. Allocation decisions also added value through increased short exposure to the diversified financials industry group, and less short exposure to the pharmaceuticals and biotechnology industry group. From a stock perspective, short positions in Essar Energy PLC (UK), Citigroup (US), Alstom (France), Deutsche Bank (Germany), and Cree (US) were effective as all of these stocks fell substantially compared to the World Index. Detractors from short-side performance were concentrated in Hong Kong and Japan, and within the transportation, insurance, and materials industry groups. At the stock level, Odakyu Electric Railway (Japan), Amazon.com (US), China Unicom (Hong Kong), Keikyu Corp. (Japan), and Tobu Railway (Japan) all appreciated substantially during the periods that we took short positions in them, negatively impacting performance.

| | |

| Causeway Global Absolute Return Fund | | 3 |

Significant Portfolio Changes

On the long side of the portfolio, exposures to currencies, sectors, and countries are entirely a by-product of our bottom-up portfolio construction process. With that said, the Fund’s exposures in the health care, telecommunication services, and materials sectors decreased the most compared to the beginning of the period, while exposures in the consumer discretionary, energy, and industrials sectors increased the most. From a regional perspective, the most notable weight changes included increased exposure to companies listed in Singapore, the United States, and Korea. The most significantly reduced country exposures were France, Greece, and Japan.

On the short-side of the portfolio, portfolio turnover was higher compared to the global long portfolio, which is consistent with the shorter time horizon of our quantitative investment process. Notable names in which we increased short exposure during the period include Procter & Gamble (US), Peugeot (France), Royal Bank of Canada (Canada), Genting (Singapore), and Sony Corp. (Japan). Notable names in which we reduced or covered short exposure included Kraft Foods (US), Boston Scientific (US), SAP AG (Germany), Berkshire Hathaway (US), and China Resources Land (Hong Kong).

We define net exposure in a region or sector as long exposure minus short exposure. From a geographical perspective, during the fiscal period we increased net exposure from significantly short to marginally short exposure in the US; increased net exposure from marginally short to neutral in Singapore; reduced net exposure from marginally long to marginally short exposure in Japan; and reduced net exposure from significantly long to long exposure in the Euro region. From an economic sector perspective, we increased net exposure from significantly short to less short exposure in the financials sector; increased net exposure from long to significantly long exposure in the consumer discretionary sector; reduced net exposure from significantly long to less long exposure in the health care sector; and reduced net exposure from short to significantly short in the telecommunication services sector.

Investment Outlook – Global Long Portfolio

As we experienced most recently in 2008, negative sentiment can be self-fulfilling. Fear and lack of confidence causes individuals and businesses to postpone both consumption and investment. Without decisive government policy action, concerns of contagion have taken hold, tainting the outlook by investors for risk-bearing assets, including equities. Panic selling, while discomforting, has a silver lining. Indiscriminate selling fills our weekly value screens with well-managed companies generating enviable levels of free cash flow. We find bargains in bear markets. Not just bargains, but high-quality, leading franchise companies whose share prices have suffered with the market declines. The euro zone crisis, the US debt downgrade, Middle East political tensions, and some severe natural disasters have not changed the underlying long-term revenue growth profile for the vast majority of companies we follow closely. We have used this opportunity to take long positions in a company that dominates the global market for

| | |

4 | | Causeway Global Absolute Return Fund |

corporate information technology, Oracle (US), a highly-efficient retailer such as Tesco (UK), and a shipbuilder, SembCorp Marine (Singapore), each able to expand in the more dynamic emerging countries while becoming even more efficient in the developed world. Our fundamental analysts are scouring the output of quantitative screens, looking for opportunities to upgrade the quality of the global long portfolio in genuinely mispriced securities. European banking and insurance stocks are significantly undervalued, but the risks (political, regulatory, and economic) remain elevated. We retain an exposure to European financials, but keep that exposure well diversified. We continue to prefer the highest quality defensive and industrial companies with strong balance sheets that can deliver reasonably good earnings, even in a recessionary environment. We also prefer companies that pay generous dividends and make well-timed share repurchases that pay equity shareholders to wait for their stock prices to appreciate.

Investment Outlook – Global Short Portfolio

In times of market duress, the quantitatively managed global short portfolio of the Fund is critical in dampening overall portfolio volatility and providing an additional source of return in environments where positive returns are difficult to achieve. Recent market gyrations created opportunities, both long and short, for the Fund. On the short side, we continue to monitor over 3,000 stocks for overvaluation, earnings downgrades, financial stress or accounting gimmickry, and/or unusual price movements. We believe the present environment is fertile for our quantitative approach, and we are identifying many opportunities to hedge the long side of the Fund with attractive downside (short) candidates.

Portfolio Characteristics

On an aggregate long/short portfolio basis, we continue to maintain a near market-neutral posture with only +2.3% net exposure overall (absolute value of long exposures minus short exposures) as of September 30, 2011. At the sector level, our net biases are towards industrials and consumer discretionary, where we have significant positive net exposure, and against consumer staples and financials where we have meaningful negative net exposure. From a region/currency perspective, we are net biased towards Europe and Korea and biased against Canada, Australia, and the US. Total gross exposure (leverage) is at 289% (2.89x) as of September 30, 2011. We believe this remains consistent with our risk management goal of delivering volatility below equity market volatility, and low or no correlation to the World Index.

| | |

| Causeway Global Absolute Return Fund | | 5 |

We thank you for your continued confidence in Causeway Global Absolute Return Fund.

The above commentary expresses the portfolio managers’ views as of the date shown and should not be relied upon by the reader as research or investment advice regarding any stock. These views and the portfolio holdings are subject to change. There is no guarantee that any forecasts made will come to pass.

| | |

6 | | Causeway Global Absolute Return Fund |

Comparison of Change in the Value of a $10,000 Investment in Causeway Global Absolute Return Fund, Investor Class shares versus the BofA Merrill Lynch 3-Month US Treasury Bill Index

The performance data represents past performance and is not an indication of future results. Investment return and the principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth less than their original cost and current performance may be higher or lower than the performance quoted. For performance data current to the most recent month end, please call 1-866-947-7000 or visit www.causewayfunds.com. Investment performance reflects fee waivers in effect. In the absence of such fee waivers, total return would be reduced. Total returns assume reinvestment of dividends and capital gains distributions at net asset value when paid. Investor Class shares pay a shareholder service fee of up to 0.25% per annum of average daily net assets. Institutional Class shares pay no shareholder service fee. The Fund imposes a 2% redemption fee on the value of shares redeemed less than 60 days after purchase. If your account incurred a redemption fee, your performance will be lower than the performance shown here. For more information, please see the prospectus.

The BofA Merrill Lynch US 3-Month Treasury Bill Index is comprised of a single issue purchased at the beginning of the month and held for a full month. Each month the index is rebalanced and the issue selected is the outstanding Treasury Bill that matures closest to, but not beyond 3 months from, the rebalancing date. The Treasury Bills comprising the Index are guaranteed by the U.S. government as to the timely payment of interest and principal. The Index is gross of withholding taxes and assumes reinvestment of dividends and capital gains. The Index does not reflect the payment of transaction costs, fees and expenses associated with an investment in the Fund. It is not possible to invest directly in an index. While the Fund may invest a portion of its assets in Treasury Bills, it will primarily be exposed to notional positions in securities that will not be similarly guaranteed by the U.S. government. An investment in the Fund involves special risks (please see Note 5 in the Notes to Financial Statements).

| | |

| Causeway Global Absolute Return Fund | | 7 |

SCHEDULE OF INVESTMENTS (000)*

September 30, 2011

| | | | | | | | |

Causeway Global Absolute Return Fund | | Number of Shares | | | Value | |

SHORT-TERM INVESTMENT | | | | | | | | |

Dreyfus Cash Management, Institutional Class, 0.050% **,1 | | | 14,241,098 | | | $ | 14,241 | |

| | | | | | | | |

Total Short-Term Investment

(Cost $14,241) — 99.6% | | | | | | | 14,241 | |

| | | | | | | | |

Total Investments — 99.6%

(Cost $14,241) | | | | | | | 14,241 | |

| | | | | | | | |

Other Assets in Excess of Liabilities — 0.4% | | | | | | | 58 | |

| | | | | | | | |

Net Assets — 100.0 % | | | | | | $ | 14,299 | |

| | | | | | | | |

A summary of outstanding total return swap agreements held by the Fund at September 30, 2011, is as follows:

| | | | | | | | | | | | | | | | |

Counterparty | | Reference Entity/ Obligation | | Fixed payments paid | | Total Return received or paid | | Termination

Date | | Net

Notional

Amount2 | | | Net

Unrealized

Appreciation

(Depreciation) | |

Long Positions | | | | | | | | | | | | | | | | |

| | | | | | |

| Morgan Stanley | | South Korea Custom Basket of Securities | | Long: Fed Funds-1 day + 0.65% | | Total Return of the basket of securities | | 1/25/2013 | | $ | 843 | | | $ | — | |

| | | | | | |

| Morgan Stanley | | United States Custom Basket of Long Securities | | Long: Fed Funds-1 day + 0.50% | | Total Return of the basket of securities | | 1/25/2013 | | | 7,904 | | | | 13 | |

| | | | | | |

| Short Positions | | | | | | | | | | | | | | | | |

| | | | | | |

| Morgan Stanley | | Australia Custom Basket of Securities | | Short: Fed Funds-1 day – 0.50% to Fed Funds-1 day – 1.00% | | Total Return of the basket of securities | | 1/25/2013 | | | (792 | ) | | | (5 | ) |

| | | | | | |

| Morgan Stanley | | Canada Custom Basket of Securities | | Short: Fed Funds-1 day – 0.35% to Fed Funds-1 day – 0.36% | | Total Return of the basket of securities | | 1/25/2013 | | | (1,078 | ) | | | (1 | ) |

| | | | | | |

| Morgan Stanley | | United States Custom Basket of Short Securities | | Short: Fed Funds-1 day – 0.35% to Fed Funds-1 day – 1.09% | | Total Return of the basket of securities | | 1/25/2013 | | | (8,350 | ) | | | (13 | ) |

| | |

| | The accompanying notes are an integral part of the financial statements. |

| 8 | | Causeway Global Absolute Return Fund |

SCHEDULE OF INVESTMENTS (000)* (concluded)

September 30, 2011

| | | | | | | | | | | | | | | | |

Counterparty | | Reference Entity/ Obligation | | Fixed payments paid | | Total Return received or paid | | Termination

Date | | Net

Notional

Amount2 | | | Net

Unrealized

Appreciation

(Depreciation) | |

Contracts for Differences | |

| | | | | | |

| Morgan Stanley | | Europe Custom Basket of Securities | | Long: Fed Funds-1 day + 0.55% Short: Fed Funds-1 day – 0.40% to Fed Funds-1 day – 1.00% | | Total Return of the basket of securities | | 1/25/2013 | | $ | 1,131 | | | $ | — | |

| | | | | | |

| Morgan Stanley | | Germany Custom Basket of Securities | | Long: Fed Funds-1 day + 0.55% Short: Fed Funds-1 day – 0.40% | | Total Return of the basket of securities | | 1/25/2013 | | | 426 | | | | — | |

| | | | | | |

| Morgan Stanley | | Hong Kong Custom Basket of Securities | | Long: Fed Funds-1 day + 0.55% Short: Fed Funds-1 day – 0.50% | | Total Return of the basket of securities | | 1/25/2013 | | | 66 | | | | — | |

| | | | | | |

| Morgan Stanley | | Japan Custom Basket of Securities | | Long: Fed Funds-1 day + 0.55% Short: Fed Funds-1 day – 0.40% | | Total Return of the basket of securities | | 1/25/2013 | | | (184 | ) | | | (9 | ) |

| | | | | | |

| Morgan Stanley | | Singapore Custom Basket of Securities | | Long: Fed Funds-1 day + 0.55% Short: Fed Funds-1 day – 0.50% to Fed Funds-1 day – 0.92% | | Total Return of the basket of securities | | 1/25/2013 | | | 9 | | | | (1 | ) |

| | | | | | |

| Morgan Stanley | | United Kingdom Custom Basket of Securities | | Long: Fed Funds-1 day + 0.55% Short: Fed Funds-1 day – 0.35% | | Total Return of the basket of securities | | 1/25/2013 | | | 329 | | | | (1 | ) |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | $ | (17 | ) |

| | | | | | | | | | | | | | | | |

| ** | The rate reported is the 7-day effective yield as of September 30, 2011. |

| 1 | Of this investment $9,900 was pledged and segregated with the custodian as collateral for outstanding total return equity swap agreements. |

| 2 | The net notional amount is the sum of long and short positions. The gross notional amount of long positions and short positions at September 30, 2011 is $10,708 and $(10,404), respectively. The gross notional amounts are representative of the volume of activity during the period ended September 30, 2011. |

| | |

| The accompanying notes are an integral part of the financial statements. | | |

| Causeway Global Absolute Return Fund | | 9 |

SECTOR DIVERSIFICATION

As of September 30, 2011, the sector diversification was as follows (Unaudited):

| | | | |

Causeway Global Absolute Return Fund | | % of Net Assets | |

Short-Term Investment | | | 99.6 | % |

| | | | |

Other Assets in Excess of Liabilities | | | 0.4 | |

| | | | |

Net Assets | | | 100.0 | % |

| | | | |

| | |

| | The accompanying notes are an integral part of the financial statements. |

| 10 | | Causeway Global Absolute Return Fund |

STATEMENT OF ASSETS AND LIABILITIES (000)*

| | | | |

| | | CAUSEWAY GLOBAL ABSOLUTE RETURN FUND | |

| | | 9/30/11 | |

ASSETS: | | | | |

Investment at Value (Cost $14,241) | | $ | 14,241 | |

Receivable Due from Swap Counterparty | | | 1,420 | |

Unrealized Appreciation on Total Return Swaps | | | 13 | |

Receivable Due from Adviser | | | 21 | |

| | | | |

Total Assets | | | 15,695 | |

| | | | |

LIABILITIES: | | | | |

Payable Due from Swap Counterparty | | | 1,287 | |

Unrealized Depreciation on Total Return Swaps | | | 30 | |

Payable to Adviser | | | 18 | |

Payable to Administrator | | | 3 | |

Trustees’ Fees | | | 1 | |

Shareholder Services Fees — Investor Class | | | 1 | |

Other Accrued Expenses | | | 56 | |

| | | | |

Total Liabilities | | | 1,396 | |

| | | | |

Net Assets | | $ | 14,299 | |

| | | | |

NET ASSETS: | | | | |

Paid-in Capital (unlimited authorization — no par value) | | $ | 14,313 | |

Accumulated Net Realized Gain on Swap Contracts | | | 3 | |

Net Unrealized Depreciation on Swap Contracts | | | (17 | ) |

| | | | |

Net Assets | | $ | 14,299 | |

| | | | |

Net Asset Value Per Share (based on net assets of $11,444,341 ÷ 1,109,949 shares)

— Institutional Class | | $ | 10.31 | |

| | | | |

Net Asset Value Per Share (based on net assets of $2,855,151 ÷ 277,442 shares) — Investor Class | | $ | 10.29 | |

| | | | |

| * | Except for Net Asset Value data. |

| | |

| The accompanying notes are an integral part of the financial statements. | | |

| Causeway Global Absolute Return Fund | | 11 |

STATEMENT OF OPERATIONS (000)

| | | | |

| | | CAUSEWAY GLOBAL

ABSOLUTE RETURN

FUND | |

| | | 1/24/11* TO

9/30/11 | |

INVESTMENT INCOME: | | | | |

Interest | | $ | 5 | |

| | | | |

Total Investment Income | | | 5 | |

| | | | |

EXPENSES: | | | | |

Investment Advisory Fees | | | 100 | |

Transfer Agent Fees | | | 39 | |

Professional Fees | | | 38 | |

Administration Fees | | | 27 | |

Printing Fees | | | 15 | |

Shareholder Services Fees — Investor Class | | | 2 | |

Registration Fees | | | 2 | |

Custodian Fees | | | 2 | |

Trustees’ Fees | | | 2 | |

Other Fees | | | 6 | |

| | | | |

Total Expenses | | | 233 | |

| | | | |

LESS: | | | | |

Waiver of Investment Advisory Fee | | | (100 | ) |

Reimbursement of Other Expenses by Adviser | | | (7 | ) |

| | | | |

Total Waiver and Reimbursement | | | 107 | |

| | | | |

Net Expenses | | | 126 | |

| | | | |

Net Investment Loss | | | (121 | ) |

| | | | |

Net Realized and Unrealized Gain (Loss) on Swap Contracts: | | | | |

Net Realized Gain from Swap Contracts | | | 124 | |

Net Change in Unrealized Depreciation on Swap Contracts | | | (17 | ) |

| | | | |

Net Realized and Unrealized Gain on Swap Contracts | | | 107 | |

| | | | |

Net Decrease in Net Assets Resulting from Operations | | $ | (14 | ) |

| | | | |

| * | Commencement of operations. |

| | |

| | The accompanying notes are an integral part of the financial statements. |

| 12 | | Causeway Global Absolute Return Fund |

STATEMENT OF CHANGES IN NET ASSETS (000)

| | | | |

| | | CAUSEWAY GLOBAL

ABSOLUTE RETURN FUND | |

| | | 1/24/11* to

9/30/11 | |

OPERATIONS: | | | | |

Net Investment Loss | | $ | (121 | ) |

Net Realized Gain from Swap Contracts | | | 124 | |

Net Change in Unrealized Depreciation on Swap Contracts | | | (17 | ) |

| | | | |

Net Decrease in Net Assets Resulting from Operations | | | (14 | ) |

| | | | |

Net Increase in Net Assets Derived from Capital Share Transactions(1) | | | 14,313 | |

| | | | |

Total Increase in Net Assets | | | 14,299 | |

| | | | |

NET ASSETS: | | | | |

Beginning of Period | | | — | |

| | | | |

End of Period | | $ | 14,299 | |

| | | | |

| (1) | See Note 7 in the Notes to Financial Statements. |

| * | Commencement of operations. |

| | |

| The accompanying notes are an integral part of the financial statements. | | |

| Causeway Global Absolute Return Fund | | 13 |

FINANCIAL HIGHLIGHTS

For the period ended September 30

For a Share Outstanding Throughout the Period

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Net Asset

Value,

Beginning

of Period ($) | | | Net

Investment

Loss ($) | | | Net Realized

and

Unrealized

Gain on

Investments

($) | | | Total from

Operations

($) | | | Dividends

from Net

Investment

Income ($) | | | Net Asset

Value, End

of Period

($ ) | | | Total

Return

(%) | | | Net Assets

End of

Period

($000) | | | Ratio of

Expenses to

Average Net

Assets (% ) | | | Ratio of

Expenses

to Average

Net Assets

(Excluding

Waivers and

Reimburse-

ments) (%) | | | Ratio

of Net

Investment

Loss to

Average Net

Assets (%) | | | Portfolio

Turnover

Rate (%) | |

CAUSEWAY GLOBAL ABSOLUTE RETURN FUND† | |

Institutional Class | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

2011(1) | | | 10.00 | | | | (0.12 | ) | | | 0.43 | | | | 0.31 | | | | — | | | | 10.31 | | | | 3.10 | | | | 11,444 | | | | 1.85 | | | | 3.51 | | | | (1.77 | ) | | | — | |

Investor Class | | | | | | | | | | | | | | | | | | | | | | | | | |

2011(1) | | | 10.00 | | | | (0.15 | ) | | | 0.44 | | | | 0.29 | | | | — | | | | 10.29 | | | | 2.90 | | | | 2,855 | | | | 2.10 | | | | 3.33 | | | | (2.06 | ) | | | — | |

| (1) | Commenced operations on January 24, 2011. All ratios for the period are annualized. Total returns and portfolio turnover rate are for the period indicated and have not been annualized. |

| † | Per share amounts calculated using average shares method. |

| Amounts | designated as “—” are $0 or 0% or have been rounded to $0 or 0%. |

| | |

| | The accompanying notes are an integral part of the financial statements. |

| 14 | | Causeway Global Absolute Return Fund |

NOTES TO FINANCIAL STATEMENTS

Causeway Global Absolute Return Fund (the “Fund”) is a series of Causeway Capital Management Trust (the “Trust”).The Trust is an open-end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act” ) and is a Delaware statutory trust that was established on August 10, 2001.The Fund commenced operations on January 24, 2011.The Fund is authorized to offer two classes of shares, the Institutional Class and the Investor Class. The Declaration of Trust authorizes the issuance of an unlimited number of shares of beneficial interest of the Fund. The Fund is diversified. The Fund’s prospectus provides a description of the Fund’s investment objectives, policies and strategies. The Trust has four additional series, the financial statements of which are presented separately.

| 2. | Significant Accounting Policies |

The following is a summary of the significant accounting policies consistently followed by the Fund.

Use of Estimates in the Preparation of Financial Statements –The preparation of financial statements in conformity with generally accepted accounting principles (“GAAP”) in the United States of America requires management to make estimates and assumptions that affect the reported amount of net assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

Security and Derivative Contract Valuations – Over-the-counter financial derivative instruments, such as swap agreements, derive their value from underlying asset prices, indices, reference rates, and other inputs, or a

combination of these factors. These contracts are normally valued on the basis of broker dealer quotations.

Except as described below, securities listed on a securities exchange (except the NASDAQ Stock Market (“NASDAQ”)), or Over-the-Counter (“OTC”) for which market quotations are available are valued at the last reported sale price as of the close of trading on each business day, or, if there is no such reported sale, at the last reported bid price for long positions. For securities traded on NASDAQ, the NASDAQ Official Closing Price will be used. Securities listed on multiple exchanges or OTC markets are valued on the exchange or OTC market considered by the Fund to be the primary market. The prices for foreign securities are reported in local currency and converted to U.S. dollars using currency exchange rates. If a security price cannot be obtained from an independent pricing agent, the Fund seeks to obtain a bid price from at least one independent broker. Investments in the Dreyfus Cash Management money market fund are valued daily at the net asset value per share.

Securities and derivative contracts for which market prices are not “readily available” are valued in accordance with fair value pricing procedures approved by the Fund’s Board of Trustees (the “Board”). The Fund’s fair value pricing procedures are implemented through a Fair Value Commitee (the “Committee”) designated by the Board. Some of the more common reasons that may necessitate that a security be valued using fair value pricing procedures include: the security’s trading has been halted or suspended; the security has been delisted from a national exchange; the security’s primary trading market is temporarily closed at a time when under normal conditions it would be open; the security’s primary pricing source is not able or willing to provide a price; or the security is a swap agreement that is not publicly traded. When the Committee values

| | |

| Causeway Global Absolute Return Fund | | 15 |

NOTES TO FINANCIAL STATEMENTS

(continued)

a security in accordance with the fair value pricing procedures, the Committee will determine the value after taking into consideration relevant information reasonably available to the Committee.

In accordance with the authoritative guidance on fair value measurements and disclosure under GAAP, the Fund discloses fair value of its investments in a hierarchy that prioritizes the inputs to valuation techniques used to measure the fair value. The objective of a fair value measurement is to determine the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date (an exit price). Accordingly, the fair value hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets or liabilities (Level 1) and the lowest priority to unobservable inputs (Level 3).The guidance establishes three levels of fair value hierarchy as follows:

| | • | | Level 1 — Unadjusted quoted prices in active markets for identical, unrestricted assets or liabilities that the Fund has the ability to access at the measurement date; |

| | • | | Level 2 — Quoted prices which are not active, or inputs that are observable (either directly or indirectly) for substantially the full term of the asset or liability; and |

| | • | | Level 3 — Prices, inputs or exotic modeling techniques which are both significant to the fair value measurement and unobservable (supported by little or no market activity). |

Investments are classified within the level of the lowest significant input considered in determining fair value. Investments classified within Level 3 whose fair value measurement considers several inputs may include

Level 1 or Level 2 in puts as components of the overall fair value measurement.

The table below sets forth information about the level with in the fair value hierarchy at which the Fund’s investments are measured at September 30, 2011:

| | | | | | | | | | | | | | | | |

Investments in Securities | | Level 1

(000) | | | Level 2

(000) | | | Level 3

(000) | | | Total

(000) | |

Short-Term

Investment | | $ | 14,241 | | | $ | — | | | $ | — | | | $ | 14,241 | |

| | | | | | | | | | | | | | | | |

Total Investments in Securities | | $ | 14,241 | | | $ | — | | | $ | — | | | $ | 14,241 | |

| | | | | | | | | | | | | | | | |

| | | | |

Other Financial Instruments – Assets | | Level 1

(000) | | | Level 2

(000) | | | Level 3

(000) | | | Total

(000) | |

Total Return Swaps | | $ | — | | | $ | 13 | | | $ | — | | | $ | 13 | |

| | | | | | | | | | | | | | | | |

Total Other Financials Instruments – Assets | | $ | — | | | $ | 13 | | | $ | — | | | $ | 13 | |

| | | | | | | | | | | | | | | | |

| | | | |

Other Financial Instruments – Liabilities | | Level 1

(000) | | | Level 2

(000) | | | Level 3

(000) | | | Total

(000) | |

Total Return Swaps | | $ | — | | | $ | (30 | ) | | $ | — | | | $ | (30 | ) |

| | | | | | | | | | | | | | | | |

Total Other Financials Instruments – Liabilities | | $ | — | | | $ | (30 | ) | | $ | — | | | $ | (30 | ) |

| | | | | | | | | | | | | | | | |

Please refer to the Schedule of Investments for additional information regarding the composition of the amounts listed above.

Changes in valuation techniques may result in transfers in or out of an investment’s assigned level within the hierarchy during the reporting period. For the Fund there were no transfers between Level 1 and Level 2 during the reporting period, based on the in put level assigned under the hierarchy at the beginning and end of the reporting period.

For the period ended September 30, 2011, there were no significant changes to the Fund’s fair value methodologies.

| | |

| 16 | | Causeway Global Absolute Return Fund |

NOTES TO FINANCIAL STATEMENTS

(continued)

Federal Income Taxes — It is the Fund’s intention to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code and to distribute all of its taxable income Accordingly, no provision for Federal in come taxes has been made in the financial statements.

The Fund evaluates tax positions taken or expected to be taken in the course of preparing the Fund’s tax returns to determine whether it is “more-likely-than-not” (i.e., greater than 50- percent) that each tax position will be sustained upon examination by a taxing authority based on the technical merits of the position. Tax positions not deemed to meet the more likely-than-not threshold are recorded as a tax benefit or expense in the current year. The Fund did not record any tax provision in the current period. However, management’s conclusions regarding tax positions taken may be subject to review and adjustment at a later date based on factors including, but not limited to , examination by tax authorities (i.e., the last 3 tax year ends, as applicable ), on-going analysis of and changes to tax laws, regulations and interpretations thereof.

As of and during the period September 30, 2011, the Fund did not have a liability for any unrecognized tax benefits. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the period the Fund did not incur any significant interest or penalties.

Security Transactions and Related Income – Security transactions are accounted for on the date the security is purchased or sold (trade date). Dividend income is recognized on the ex-dividend date, if any, and interest income is recognized using the accrual basis of accounting. Costs used in determining realized gains and losses on the sales of investment securities are those of the specific securities sold.

Swap Agreements – Under a swap agreement, the Fund pays the other party to the agreement (a “swap counterparty”) fees plus an amount equal to any negative total returns from stipulated underlying investments identified by the Fund’s portfolio managers. In exchange, the counterparty pays the Fund an amount equal to any positive total returns from the stipulated underlying investments. The returns to be “swapped” between the Fund and the swap counterparty will be calculated with reference to a “notional” amount, i.e., the dollar amount hypothetically invested, long or short, in a particular security or group of securities. The Fund’s returns will generally depend on the net amount to be paid or received under the swap agreement, which will depend on the market movements of the stipulated underlying securities. The Fund’s net asset value will reflect any amounts owed to the Fund by the swap counterparty (when the Fund’s position under a swap agreement is, on a net basis, “in the money”) or amounts owed by the Fund to the counterparty (when the Fund’s position under a swap agreement is, on a net basis, “out of the money”).

Swap Agreements and Leverage – Normally, the Fund’s assets (other than the swap agreements) will be directly invested primarily in money market instruments and U.S. Treasury securities that will be used to support and cover the Fund’s obligations under its swap agreements. However, the use of a swap agreement allows the Fund to obtain investment exposures greater than it could otherwise obtain with direct investments, allowing it to effectively increase, or leverage, its total long and short investment exposures.

Expense/Classes– Expenses that are directly related to one Fund of the Trust are charged directly to that Fund. Other operating expenses of the Trust are prorated to the Fund and the other series of the Trust on the basis of relative daily net assets. Class specific expenses are

| | |

| Causeway Global Absolute Return Fund | | 17 |

NOTES TO FINANCIAL STATEMENTS

(continued)

borne by that class of shares. Income, realized and unrealized gains/losses and non-class specific expenses are allocated to the respective classes on the basis of relative daily net assets.

Dividends and Distributions – Dividends from net investment income, if any, are declared and paid on an annual basis. Any net realized capital gains on sales of securities are distributed to shareholders at least annually.

Redemption Fee – The Fund imposes a redemption fee of 2% on the value of capital shares redeemed by shareholders less than 60 days after purchase. The redemption fee does not apply to shares purchased through reinvested distributions or shares redeemed through designated systematic withdrawal plans. The redemption fee does not normally apply to omnibus account arrangements through financial intermediaries where the purchase and sale orders of a number of persons are aggregated before being communicated to the Fund. However, the Fund seeks agreements with these intermediaries to impose the Fund’s redemption fee or a different redemption fee on their customers if feasible, or to impose other appropriate restrictions on excessive short-term trading. The officers of the Fund may waive the redemption fee for shareholders in asset allocation and similar investment programs reasonably believed not to be engaged in short-term market timing, including for holders of shares purchased by Causeway Capital Management LLC (the “Adviser”) for its clients to rebalance their portfolios. For the period ended September 30, 2011, the Institutional Class and Investor Class retained $226 and $313 in redemption fees, respectively.

| 3. | Investment Advisory, Administration, Shareholder Service and Distribution Agreements |

The Trust, on behalf of the Fund, has entered into an Investment Advisory Agreement (the “Advisory Agreement”) with the Adviser. Under the Advisory Agreement, the Adviser is entitled to a monthly fee equal to an annual rate of 1.5 0% of the Fund’s average daily net assets. The Adviser contractually agreed through January 31, 2012 to waive its fee and, to the extent necessary, reimburse the Fund to keep total annual fund operating expenses (excluding swap agreement financing charges and transaction costs, borrowing expenses, dividend expenses on securities sold short, brokerage fees and commissions, interest, taxes, shareholder service fees, fees and expenses of other funds in which the Fund invests, and extraordinary expenses) from exceeding 1.85% of Institutional Class and Investor Class average daily net assets. For the period ended September 30, 2011, the Adviser waived $100,267 and reimbursed $6,773.

The Trust and SEI Investments Global Funds Services (the “Administrator”) have entered into an Administration Agreement. Under the terms of the Administration Agreement, the Administrator is entitled to an annual fee which is calculated daily and paid monthly based on the aggregate average daily net assets of the Trust as follows: 0.0 6% up to $1 billion; 0.05% of the assets exceeding $1 billion up to $2 billion; 0.04% of the assets exceeding $2 billion up to $3 billion; 0.03% of the assets exceeding $3 billion up to $4 billion; and 0.02% of the assets exceeding $4 billion. The Fund is subject to a minimum annual fee of $40,000. If the Fund has three or more share classes, it shall be subject to an additional minimum fee of $20,000 per additional share class (over two).

| | |

| 18 | | Causeway Global Absolute Return Fund |

NOTES TO FINANCIAL STATEMENTS

(continued)

The Trust has adopted a Shareholder Service Plan and Agreement for Investor Class shares that allows the Trust to pay broker-dealers and other financial intermediaries a fee of up to 0.25% per annum of average daily net assets for services provided to Investor Class shareholders. For the period ended September 30, 2011, the Investor Class paid 0.25% of average daily net assets under this plan.

The Trust and SEI Investments Distribution Co. (the “Distributor”) have entered into a Distribution Agreement. The Distributor receives no fees for its distribution services under this agreement.

The officers of the Trust are also officers or employees of the Administrator or Adviser. They receive no fees for serving as officers of the Trust.

As of September 30, 2011, approximately $5.630 million of net assets were held by affiliated investors.

| 4. | Investment Transactions |

During the period ended September 30, 2011, there were no security purchases or sales, other than short-term investments.

| 5. | Derivatives and Risks of Investing |

A swap agreement is a form of derivative that includes leverage, allowing the Fund to obtain the right to a return on a stipulated capital base that exceeds the amount the Fund has invested. The use of swap agreements could cause the Fund to be more volatile, resulting in larger gains or losses in response to changes in the values of the securities underlying the swap agreements than if the Fund had made direct investments. Use of leverage involves special risks and is speculative. If the Adviser is incorrect in evaluating long and short exposures, leverage will magnify any

losses, and such losses may be significant. By using swap agreements, the Fund is exposed to liquidity risks since it may not be able to close out a swap agreement immediately, particularly during times of market turmoil. It may also be difficult to value a swap agreement if the Fund has difficulty in closing the position.

The use of derivative contracts exposes an investor to various market risks. The Fund’s investment in total return equity swap agreements exposed the Fund to equity risk for the period ended September 30, 2011. Equity risk is the risk that the value of a particular stock or stock market to which the Fund has long exposure is falling, or to which the Fund has short exposure is rising. The fair value, if any, of the total return equity swap agreements as of September 30, 2011 is reported on the Statement of Assets and Liabilities. The related change in unrealized and realized gains or losses for the reporting period is reported on the Statement of Operations.

The Fund expects to enter into, change, and exit from notional securities positions from time to time, which will cause the Fund to recognize short term capital gains or losses, and to close out swap agreements at least monthly, which will cause the Fund to realize ordinary income or loss throughout the year that, when distributed to shareholders, will generally be taxable to them as short term capital gains or losses or ordinary income rather than at lower long-term capital gains rates.

By using swap agreements, the Fund is exposed to additional risks concerning the counterparty. For example, the Fund bears the risk of loss of the amount expected to be received under a swap agreement in the event of the default or bankruptcy of the counterparty, or if the counterparty fails to honor its obligations. The Fund intends initially to enter into swap agreements with a single counterparty, focusing its exposure to the

| | |

| Causeway Global Absolute Return Fund | | 19 |

NOTES TO FINANCIAL STATEMENTS

(continued)

counterparty credit risk of that single counterparty. Further, the swap counterparty’s obligations to the Fund likely will not be collateralized. The Fund intends, however, to close out swap agreements at least monthly, and may do so more frequently, so that net gains under swap agreements with a single counterparty do not exceed 5% of the Fund’s total assets at any given time.

There is the risk that the counterparty refuses to continue to enter into swap agreements with the Fund in the future, or requires increased fees, which could impair the Fund’s ability to achieve its investment objective. A swap counterparty may also increase its collateral requirements, which may limit the Fund’s ability to use leverage and reduce investment returns. In addition, if the Fund cannot locate a counterparty willing to enter into transactions with the Fund, it will not be able to implement its investment strategy. As of September 30, 2011 the Fund’s swap agreements were with one counterparty.

| 6. | Federal Tax Information |

The Fund is classified as a separate taxable entity for Federal income tax purposes. The Fund intends to qualify as a separate “regulated investment company” under Subchapter M of the Internal Revenue Code and make the requisite distributions to shareholders that will be sufficient to relieve it from Federal income tax and Federal excise tax. Therefore, no Federal tax provision is required. To the extent that dividends from net investment income and distributions from net realized capital gains exceed amounts reported in the financial statements, such amounts are reported separately.

The Fund may be subject to taxes imposed by countries in which it invests in issuers existing or operating in such countries. Such taxes are generally based on income earned. The Fund accrues such taxes when the related income is earned. Dividend and interest income is recorded net of non-U.S. taxes paid.

The amounts of distributions from net investment income and net realized capital gains are determined in accordance with Federal income tax regulations, which may differ from those amounts determined under generally accepted accounting principles in the United States of America. These book/tax differences are either temporary or permanent in nature. The character of distributions made during the year from net investment income or net realized gains, and the timing of distributions made during the year may differ from the year that the income or realized gains (losses) were recorded by the Fund. To the extent these differences are permanent, adjustments are made to the appropriate equity accounts in the period that the differences arise.

Accordingly, the following permanent differences, which are primarily due to swap agreement reclasses and net investment losses reclassified to /(from) the following accounts as of September 30, 2011 (000):

| | | | | | |

Undistributed

Net Investment

Income (loss) | | | Accumulated

Net Realized

Gain/Loss | |

| $ | 121 | | | $ | (121) | |

These reclassifications had no impact on net assets or net asset value per share.

For the period ended September 30, 2011, the Fund did not pay any dividends or distributions.

| | |

| 20 | | Causeway Global Absolute Return Fund |

NOTES TO FINANCIAL STATEMENTS

(continued)

As of September 30, 2011, the components of accumulated losses on a tax basis were as follows (000):

| | | | |

Undistributed Ordinary Income | | $ | 3 | |

Unrealized Depreciation | | | (17 | ) |

| | | | |

Total Accumulated Losses | | $ | (14 | ) |

| | | | |

Post October Capital and Currency Losses represent losses realized on securities and currency transactions from November 1, 2010 through September 30, 2011 that, in accordance with Federal income tax regulations, the Fund may elect to defer and treat as having arisen in the following fiscal year.

Under the recently enacted Regulated Investment Company Modernization Act of 2010, the Fund will be permitted to carry forward capital losses incurred in taxable years beginning after December 22, 2010 for an unlimited period. Post-enactment capital losses that are carried forward will retain their character as either short-term or long-term capital losses rather than being considered all short-term as under previous law.

At September 30, 2011, the total cost of securities for Federal income tax purposes and the aggregate gross unrealized appreciation and depreciation on investment securities for the Fund were as follows (000):

| | | | | | | | | | | | |

Federal Tax Cost | | Appreciated

Securities | | | Depreciated

Securities | | | Net

Unrealized

Appreciation | |

| $14,241 | | $ | — | | | $ | — | | | $ | — | |

| | | | | | | | | | | | |

| 7. | Capital Shares Issued and Redeemed (000) |

| | | | | | | | |

| | | Period Ended

September 30, 2011 | |

| | | Shares | | | Value | |

Institutional Class: | | | | | | | | |

Shares Sold | | | 1,111 | | | $ | 11,406 | |

Shares Redeemed | | | (1 | ) | | | (11 | ) |

| | | | | | | | |

Increase in Shares Outstanding Derived from Institutional Class Transactions | | | 1,110 | | | | 11,395 | |

| | | | | | | | |

Investor Class: | | | | | | | | |

Shares Sold | | | 296 | | | | 3,109 | |

Shares Redeemed | | | (19 | ) | | | (191 | ) |

| | | | | | | | |

Increase in Shares Outstanding Derived from Investor Class Transactions | | | 277 | | | | 2,918 | |

| | | | | | | | |

Increase in Shares Outstanding from Capital Share Transactions | | | 1,387 | | | $ | 14,313 | |

| | | | | | | | |

| 8. | Significant Shareholder Concentration |

As of September 30, 2011, one shareholder of the Fund owned 45% of net assets of the Institutional Class and one shareholder of the Fund owned 17% of the net assets of the Investor Class.

| 9. | New Accounting Pronouncement |

In May 2011, the Financial Accounting Standards Board is sued ASU No. 2011-04 “Amendments to Achieve Common Fair Value Measurement and Disclosure Requirements in U.S. GAAP and International Financial Reporting Standards (“IFRS”).”

| | |

| Causeway Global Absolute Return Fund | | 21 |

NOTES TO FINANCIAL STATEMENTS

(continued)

ASU 2011-04 includes common requirements for measurement of and disclosure about fair value between U.S. GAAP and IFRS.ASU 2011-04 will require reporting entities to disclose the following information for fair value measurements categorized within Level 3 of the fair value hierarchy: quantitative information about the unobservable inputs used in the fair value measurement, the valuation processes used by the reporting entity, and a narrative description of the sensitivity of the fair value measurement to changes in unobservable inputs and the interrelation-ships between those unobservable inputs. In addition, ASU 2011-04 will require reporting entities to make disclosures about amounts and reasons for all transfers in and out of Level 1 and Level 2 fair value measurements. The new and revised disclosures are effective for interim and annual reporting periods beginning after December 15, 2011.At this time, management is evaluating the implications of ASU 2011-04 and its impact on the financial statements.

The Fund has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date the financial statements were issued. Based on this evaluation, no adjustments were required to the financial statements.

| | |

| | |

| 22 | | Causeway Global Absolute Return Fund |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Trustees and Shareholders of Causeway Global Absolute Return Fund

In our opinion, the accompanying statement of assets and liabilities, including the schedule of investments, and the related statements of operations and of changes in net assets and the financial highlights present fairly, in all material respects, the financial position of Causeway Global Absolute Return Fund (the “Fund”) at September 30, 2011, and the results of its operations, the changes in its net assets and the financial highlights for the period January 24, 2011 (commencement of operations) through September 30, 2011, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements based on our audit. We conducted our audit of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities at September 30, 2011 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Los Angeles, California

November 28, 2011

| | |

| Causeway Global Absolute Return Fund | | 23 |

TRUSTEES AND OFFICERS INFORMATION (Unaudited)

Information pertaining to the Trustees and officers of the Trust is set forth below. Trustees who are not deemed to be “interested persons” of the Trust as defined in the 1940 Act are referred to as “Independent Trustees.” The Trustee who is deemed to be an “interested person” of the Trust is referred to as an “Interested Trustee.” The Trust’s Statement of Additional Information (“SAI”) includes additional information about the Trustees and officers. The SAI may be obtained without charge by calling 1-866-947-7000.

| | | | | | | | | | |

Name Address, Age1 | | Position(s) Held with the Company | | Term of Office and Length of Time Served2 | | Principal Occupation(s) During Past Five Years | | Number of Portfolios in Trust Complex Overseen by Trustee3 | | Other Directorships Held by Trustee4 |

INDEPENDENT TRUSTEES5 | | | | | | | | | | |

| | | | | |

John A. G. Gavin Age: 80 | | Trustee; Chairman of the Board | | Trustee since 9/01; Chairman | | Chairman, Gamma Holdings | | | | Director, TCW Funds, Inc. and TCW Strategic Income Fund, Inc.; Trustee, Hotchkis and Wiley Funds |

| | | | | |

John R, Graham Age: 50 | | Trustee | | Since 10/08 | | Film Composer (since 2005); Senior Vice President, Corporate Financial Development and Communications, The Walt Disney Company (2004-2005); Senior Vice President, Mergers and Acquisitions, Lehman Brothers Inc. (2000-2004). | | 5 | | None |

| | | | | |

Lawry J. Meister Age: 49 | | Trustee | | Since 10/08 | | President, Steaven Jones Development Company, Inc. (real estate firm) (since 1995). | | 5 | | None |

| | | | | |

Eric H. Sussman Age: 45 | | Trustee Chairman of the Audit Committee | | Trustee since 9/01; Chairman since 10/04 | | Tenured Lecturer, Anderson Graduate School of Management, University of California, Los Angeles (since 1995); President, Amber Capital, Inc. (real estate investment and financial planning firm) (since 1993). | | 5 | | Trustee, Presidio Funds (until 2010) |

| | | | | |

INTERESTED TRUSTEE5 | | | | | | | | | | |

Mark D. Cone Age: 43 | | Trustee | | Since 10/08 | | Executive Vice President and Chief Marketing Officer of the Adviser (since 2001). | | 5 | | None |

| | |

24 | | Causeway Global Absolute Return Fund |

TRUSTEES AND OFFICERS INFORMATION (Unaudited)

(continued)

| | | | | | | | | | |

Name Address, Age1 | | Position(s) Held with the Company | | Term of Office and Length of Time Served2 | | Principal Occupation(s) During Past Five Years | | Number of Portfolios in Trust Complex Overseen by Trustee3 | | Other

Directorships

Held by

Trustee4 |

OFFICERS | | | | | | | | | | |

| | | | | |

Turner Swan 11111 Santa Monica Blvd., 15th Floor Los Angeles, CA 90025 Age: 49 | | President | | Since 8/01 | | General Counsel, Secretary , and Member of the Adviser (since 2001); Compliance Officer of the Adviser (since 2010). | | N/A | | N/A |

| | | | | |

| Gracie V. Fermelia 11111 Santa Monica Blvd., 15th Floor Los Angeles, CA 90025 Age: 49 | | Chief Compliance Officer and Assistant Secretary | | CCO since 7/05; Asst. Sect. since 8/01 | | Chief Compliance Officer of the Adviser (since July 2005); Chief Operating Officer and Member of the Adviser (since 2001). | | N/A | | N/A |

| | | | | |

Michael Lawson6 One Freedom Valey Drive Oaks, PA 19456 Age: 50 | | Treasurer | | Since 7/05 | | Director of the Administrator’s Fund Accounting department (since July 2005); Manager in the Administrator’s Fund Accounting department (November 1998 to July 2005). | | N/A | | N/A |

| | | | | |

| Gretchen W. Corbell 11111 Santa Monica Blvd., 15th Floor Los Angeles, CA 90025 Age: 40 | | Secretary | | Since 10/11 | | Associate Attorney of the Adviser (since 2004). | | N/A | | N/A |

| | | | | |

Dianne Sulzbach6 One Freedom Valley Drive Oaks, PA 19456 Age: 34 | | Vice President and Assistant Secretary | | Since 8/11 | | Corporate Counsel of the Administrator (since 2011); Associate Counsel, Morgan Lewis & Bockius (2006-2010). | | N/A | | N/A |

| | | | | |

Carolyn F. Mead6 One Freedom Valley Drive Oaks, PA 19456 Age: 54 | | Vice President and Assistant Secretary | | Since 7/08 | | Corporate Counsel of the Administrator (since 2007); Associate Counsel, Stradley, Ronan, Stevens & Young LLP (2004-2007). | | N/A | | N/A |

| | |

| Causeway Global Absolute Return Fund | | 25 |

TRUSTEES AND OFFICERS INFORMATION (Unaudited)

(continued)

| | | | | | | | | | |

Name Address, Age1 | | Position(s) Held with the

Company | | Term of Office and Length of Time Served2 | | Principal Occupation(s) During Past Five Years | | Number of

Portfolios

in Trust

Complex

Overseen by

Trustee3 | | Other

Directorships

Held by

Trustee4 |

Bernadette Sparling6 One Freedom Valley Drive Oaks, PA 19456 Age: 34 | | Vice President and Assistant Secretary | | Since 7/08 | | Corporate Counsel of the Administrator (since 2005); Associate Counsel, Blank Rome LLP (2001-2005). | | N/A | | N/A |

| 1 | Each Trustee may be contacted by writing to the Trustee c/o Causeway Capital Management Trust, One Freedom Valley Drive, Oaks, PA 19456. |

| 2 | Each Trustee holds office during the life time of the Trust or until his or her sooner resignation, retirement, removal, death or incapacity in accordance with the Trust’s Declaration of Trust. The president, treasurer and secretary each holds office at the pleasure of the Board of Trustees or until he or she sooner resigns in accordance with the Trust’s Bylaws. |

| 3 | The “Trust Complex” consists of all registered investment companies for which Causeway Capital Management LLC serves as investment adviser. As of September 30, 2011, the Trust Complex consisted of one investment company with five portfolios — International Value Fund, Emerging Markets Fund, Global Value Fund, International Opportunities Fund, and Global Absolute Return Fund. |

| 4 | Directorships of companies required to report to the Securities and Exchange Commission under the Securities Exchange Act of 1934 (i.e., “public companies”) or other investment companies registered under the 1940 Act. |

| 5 | Mr. Cone is considered an “interested person” of the Trust as defined in the 1940 Act because he is an employee of the Adviser. |

| 6 | These officers of the Trust also serve as officers of one or more mutual funds for which SEI Investments Company or an affiliate acts as investment manager, administrator or distributor. |

| | |

26 | | Causeway Global Absolute Return Fund |

DISCLOSURE OF FUND EXPENSES (Unaudited)

As a shareholder of the Fund, you incur two types of costs: (1) transaction costs, including redemption fees, and (2) ongoing costs, including management fees, shareholder service fees, and other Fund expenses. It is important for you to understand the impact of these costs on your investment returns.

Ongoing operating expenses are deducted from a mutual fund’s gross income and directly reduce its final investment return. These expenses are expressed as a percentage of a mutual fund’s average net assets; this percentage is known as a mutual fund’s expense ratio.

The following examples use the expense ratio and are intended to help you understand the ongoing costs (in dollars) of investing in the Fund and to compare these costs with those of other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period.

The table on the next page illustrates the Fund’s costs in two ways:

Actual Fund Return. This section helps you to estimate the actual expenses after fee waivers that the Fund incurred over the period. The “Expenses Paid During Period” column shows the actual dollar expense cost incurred by a $1,000 investment in the Fund, and the “Ending Account Value” number is derived from deducting that expense cost from the Fund’s gross investment return.

You can use this information, together with the actual amount you invested in the Fund, to estimate the expenses you paid over that period. Simply divide your actual account value by $1,000 to arrive at a ratio (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply that ratio by the number shown under “Expenses Paid During Period.”

Hypothetical 5% Return. This section helps you compare the Fund’s costs with those of other mutual funds. It assumes that the Fund had an annual 5% return before expenses during the year, but that the expense ratio (Column 3) for the period is unchanged. This example is useful in making comparisons because the Securities and Exchange Commission requires all mutual funds to make this 5% calculation. You can assess the Fund’s comparative cost by comparing the hypothetical result for the Fund in the “Expenses Paid During Period” column with those that appear in the same charts in the shareholder reports for other mutual funds.

NOTE: Because the return is set at 5% for comparison purposes — NOT the Fund’s actual return — the account values shown may not apply to your specific investment.

| | |

| Causeway Global Absolute Return Fund | | 27 |

DISCLOSURE OF FUND EXPENSES (Unaudited)

(concluded)

| | | | | | | | | | | | | | | | |

| | | Beginning

Account

Value

4/01/11 | | | Ending

Account

Value

9/30/11 | | | Annualized

Expense

Ratios | | | Expenses

Paid

During

Period* | |

Causeway Global Absolute Return Fund | | | | | | | | | | | | | | | | |

Actual Fund Return | | | | | | | | | | | | | | | | |

Institutional Class | | $ | 1,000.00 | | | $ | 1,001.90 | | | | 1.85 | % | | $ | 9.26 | |

Hypothetical 5% Return | | | | | | | | | | | | | | | | |

Institutional Class | | $ | 1,000.00 | | | $ | 1,015.81 | | | | 1.85 | % | | $ | 9.33 | |

Causeway Global Absolute Return Fund | | | | | | | | | | | | | | | | |

Actual Fund Return | | | | | | | | | | | | | | | | |

Investor Class | | $ | 1,000.00 | | | $ | 1,001.00 | | | | 2.10 | % | | $ | 10.55 | |

Hypothetical 5% Return | | | | | | | | | | | | | | | | |

Investor Class | | $ | 1,000.00 | | | $ | 1,014.52 | | | | 2.10 | % | | $ | 10.63 | |

| * | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by 183/365 (to reflect the one-half year period). |

| | |

28 | | Causeway Global Absolute Return Fund |

INVESTMENT ADVISER

Causeway Capital Management LLC

11111 Santa Monica Blvd.

15th Floor

Los Angeles, CA 90025

DISTRIBUTOR

SEI Investments Distribution Co.

One Freedom Valley Drive

Oaks, Pennsylvania 19456

TO OBTAIN MORE INFORMATION

Call 1-866-947-7000 or visit us online at

www.causewayfunds.com

This material must be preceded or accompanied by a current prospectus.

The Fund files its complete schedule of portfolio holdings with the Securities and Exchange Commission (“Commission”) for the first and third quarters of each fiscal year on Form N-Q within sixty days after the end of the period. The Fund’s Forms N-Q are available on the Commission’s website at http://www.sec.gov, and may be reviewed and copied at the Commission’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to portfolio securities, as well as information relating to how the Trust voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available (i) without charge, upon request, by calling 1-866-947-7000; and (ii) on the Commission’s website at http://www.sec.gov.

CCM-AR-101-0100

The registrant has adopted a code of ethics that applies to the registrant’s principal executive officer, principal financial officer and principal accounting officer. During the fiscal year ended September 30, 2011, there were no material changes or waivers to the code of ethics.

| Item 3. | Audit Committee Financial Expert. |

(a)(1) The registrant’s board of trustees has determined that the registrant has at least one audit committee financial expert serving on the audit committee.

(a)(2) The audit committee financial expert is Eric Sussman. Mr. Sussman is independent as defined in Form N-CSR Item 3(a)(2).

| Item 4. | Principal Accountant Fees and Services. |

Aggregate fees billed to the registrant for professional services rendered by the registrant’s principal accountant for the fiscal years ended September 30, 2011 and 2010 were as follows:

| | | | | | | | | | |

| | | 2011 | | | 2010 | |

| (a) | | Audit Fees | | $ | 166,895 | | | $ | 131,900 | |

| (b) | | Audit-Related Fees | | | None | | | | None | |

| (c) | | Tax Fees(1) | | $ | 42,700 | | | $ | 27,700 | |

| (d) | | All Other Fees | | | None | | | | None | |

Note:

| (1) | Tax fees include amounts related to tax return and excise tax calculation reviews and foreign tax reclaim analysis. |

(e)(1) The registrant’s audit committee has adopted a charter that requires it to pre-approve the engagement of auditors to (i) audit the registrant’s financial statements, (ii) provide other audit or non-audit services to the registrant, or (iii) provide non-audit services to the registrant’s investment adviser if the engagement relates directly to the operations and financial reporting of the registrant.

(e)(2) No services included in paragraphs (b) through (d) of this Item were approved by the audit committee pursuant to paragraph (c)(7)(i)(C) of Rule 2-01 of Regulation S-X.

(f) Not applicable.

(g) For the fiscal year ended September 30, 2011, the aggregate non-audit fees billed by the registrant’s accountant for services rendered to the registrant and the registrant’s investment adviser were $42,700 and $178,492, respectively. For the fiscal year ended September 30, 2010, the aggregate non-audit fees billed by the registrant’s accountant for services rendered to the registrant and the registrant’s investment adviser were $27,700 and $168,975, respectively.

(h) The audit committee considered whether the provision of non-audit services rendered to the registrant’s investment adviser by the registrant’s principal accountant that were not pre-approved pursuant to paragraph (c)(7)(ii) of Rule 2-01 of Regulation S-X was compatible with maintaining the principal accountant’s independence.

| Item 5. | Audit Committee of Listed Registrants. |

Not applicable to open-end management investment companies.

| Item 6. | Schedule of Investments |

See Item 1.

| Item 7. | Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies. |

Not applicable to open-end management investment companies.

| Item 8. | Portfolio Managers of Closed-End Management Investment Companies |

Not applicable to open-end management investment companies.

| Item 9. | Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers. |

Not applicable to open-end management investment companies.

| Item 10. | Submission of Matters to a Vote of Security Holders. |

There have been no material changes to the registrant’s procedures by which shareholders may recommend nominees to the registrant’s board of trustees since the registrant’s last filing on Form N-CSR.

| Item 11. | Controls and Procedures. |

(a) The certifying officers, whose certifications are included herewith, have evaluated the registrant’s disclosure controls and procedures within 90 days of the filing date of this report. In their opinion, based on their evaluation, the registrant’s disclosure controls and procedures are adequately designed, and are operating effectively to ensure, that information required to be disclosed by the registrant in the reports it files or submits under the Securities Exchange Act of 1934 is recorded, processed, summarized and reported within the time periods specified in the Securities and Exchange Commission’s rules and forms.

(b) There were no changes in the registrant’s internal control over financial reporting that occurred during the registrant’s second fiscal quarter of the period covered by this report that have materially affected, or are reasonably likely to materially affect, the registrant’s internal control over financial reporting.

(a)(1) Code of Ethics attached hereto.

(a)(2) Separate certifications for the principal executive officer and the principal financial officer of the registrant as required by Rule 30a-2(a) under the Investment Company Act of 1940 (17 CFR 270.30a-2(a)) are filed herewith.

(b) Officer certifications as required by Rule 30a-2(b) under the Investment Company Act of 1940 (17 CFR 270.30a-2(b)) also accompany this filing as an exhibit.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| | | | | | |

(Registrant) | | | | Causeway Capital Management Trust | | |

| | | |

By (Signature and Title)* | | | | /s/ Turner Swan | | |

| | | | Turner Swan, President | | |

| | | |

Date: December 2, 2011 | | | | | | |

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| | | | | | |

By (Signature and Title)* | | | | /s/ Turner Swan | | |

| | | | Turner Swan, President | | |

| | | |

| Date: December 2, 2011 | | | | | | |

| | | |

| By (Signature and Title)* | | | | /s/ Michael Lawson | | |

| | | | Michael Lawson, Treasurer | | |

| | | |

| Date: December 2, 2011 | | | | | | |

| * | Print the name and title of each signing officer under his or her signature. |