Westfield Financial, Inc. 8-K

Exhibit 99.1

W ESTFIELD F INANCIAL , I NC . NASDAQ: WFD FIG PARTNER’S 10 TH ANNUAL BANK CEO FORUM SEPTEMBER 15 – 16, 2014

F ORWARD – LOOKING STATEMENTS Today’s presentation may contain forward - looking statements, which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated” and “potential . ” Examples of forward - looking statements include, but are not limited to, estimates with respect to our financial condition and results of operation and business that are subject to various factors which could cause actual results to differ materially from these estimates . These factors include, but are not limited to : • changes in the interest rate environment that reduce margins; • changes in the regulatory environment; • the highly competitive industry and market area in which we operate; • general economic conditions, either nationally or regionally, resulting in, among other things, a deterioration in credit quality; • changes in business conditions and inflation; • changes in credit market conditions; • changes in the securities markets which affect investment management revenues; • increases in Federal Deposit Insurance Corporation deposit insurance premiums and assessments ; • changes in technology used in the banking business; • the soundness of other financial services institutions; • certain of our intangible assets may become impaired in the future; • our controls and procedures may fail or be circumvented; • new lines of business or new products and services, including the additions of the Westfield Wealth Management and Insurance Group; • changes in key management personnel ; • r ecent or proposed legislative and regulatory initiatives; and • other factors set forth in our Annual Report on Form 10 - K for the year ended December 31, 2013, and other reports filed by us with the Securities and Exchange Commission (“SEC ”). Any or all of our forward - looking statements in today’s presentation or in any other public statements we make may turn out to be wrong . They can be affected by inaccurate assumptions we might make or known or unknown risks and uncertainties . Consequently, no forward - looking statements can be guaranteed . We disclaim any obligation to subsequently revise any forward - looking statements to reflect events or circumstances after the date of such statements, or to reflect the occurrence of anticipated or unanticipated events . 2

W ESTFIELD F INANCIAL O VERVIEW – W HO W E A RE ▪ A bank holding company headquartered in Westfield, MA with $ 1 . 3 billion in assets and 12 branches throughout western Massachusetts and northern Connecticut with one additional branch scheduled to open in October in Enfield, Connecticut . ▪ Successfully transitioned to a commercial bank model from a legacy mutual thrift . ▪ 63 % commercial loans to total loans with 47 % in C & I and non - owner occupied CRE to total loans . ▪ Strong credit quality always essential – NPA/Assets of 0 . 25 % as of June 30 , 2014 . ▪ Target small to mid - sized businesses , which the larger banks are not focused on . ▪ Ranked # 4 in deposit market share in cities where we have branches (# 5 in Hampden County, Massachusetts)* . ▪ Extremely strong regulatory capital ratios . Capital rationalization remains a priority . ▪ Strong and seasoned management team with long tenure at WFD . Top 5 senior officers have a combined 118 years banking experience, 87 years with Westfield Bank . * Does not include the Granby Banking Center deposit total which opened June 2013 3

W ESTFIELD F INANCIAL O VERVIEW – W HO W E A RE C ORPORATE S UMMARY Westfield Financial, Inc. – NASDAQ (WFD) Corporate Headquarters – Westfield, MA Third quarter 2014, established a commercial lending hub for our middle market and commercial real estate lending teams located in downtown Springfield, along the I - 91 “Knowledge Corridor ”, extending our reach into the Hartford metro area 12 Branches; with one branch in Enfield, CT scheduled to open in October 12 Stand alone ATMS/Cash Machines Financial Overview – As of June 30, 2014 Total Assets $1.3 billion Total Loans $686 million Total Deposits $819 million Total Common Equity $147 million EPS $0.34 2013 vs. $0.26 in 2012 $0.16 YTD 2014 vs. $0.16 YTD 2013 4

C OMMERCIAL L ENDING T EAM WITH R EGIONAL B ANK E XPERIENCE Years Lending Years with Westfield Bank Prior Experience James Hagan President and CEO 30 20 Fleet Bank, Bank of New England Allen Miles EVP and Senior Lender 26 16 Westbank, Bank of New England Commercial Lenders: Dennis Keefe 35 3 Berkshire Bank, Fleet Bank Ted Horan 31 New hire 4Q 2013 Liberty Bank, Connecticut Richard Hanchett 28 7 New Alliance Bank, Westbank Bernard Donnelly 26 5 Peoples United Bank, Bank of Boston Thomas Cebula 18 3 Fleet Bank, Bank of New England Michael Harrington 16 7 New Alliance Bank, Westbank Sharon Czarnecki 7 22 Credit Analyst, Westfield Bank Brittany Kelleher 5 7 Credit Analyst, Westfield Bank 5

M ARKET O VERVIEW 6 Source: 1 Knowledge Corridor website; 2 Masslive website Big Concentrated Market 1 Nation’s 20 th largest metro region, with 2.77 million people, ranks ahead of Denver and St. Louis. Robust Business Sectors 1 Key areas of excellence, focus and investment include: • Financial Services • Health Care • Precision Manufacturing • Insurance • Education Academic Powerhouse 1 High academic concentration with 41 colleges and universities and approximately 215,000 students. Exceptional Achievement 1 Consistently among the nation’s top 10 in percentage of population with advanced degrees, science - engineering doctorates and new patents registered. $2.48 Billion in Springfield Economic Development Projects 2 Springfield’s chief development officer announced in March 2014 it has planned or in - progress projects totaling $2.48 billion. WFD Branch Footprint K NOWLEDGE C ORRIDOR An interstate partnership of regional economic development, planning, business, tourism and educational institutions that work together to advance the region’s economic progress.

M ARKET Overview 7 Source: 1 United States Census Bureau; 2 United States Department of Labor • Third quarter 2014 - relocated middle market commercial lending team to Springfield, MA to provide better access to key markets and centers of influence. This will create better synergies for business development in northern Connecticut. • Third quarter 2014 - announced new banking center in Enfield, CT. o Positioned to take advantage of market disruption created by M&A . o Attractive market demographics : Massachusetts Connecticut Hampden County Hartford County 2008 - 2012 Median Income 1 $ 49,729 $64,752 2013 estimate Population 1 626,915 1,215,211 2012 Businesses 1 (private non - farm) 9,683 22,477 June 2014 Workforce 2 323,000 555,800 • Bradley Airport Development Zone - This zone establishes tax incentives for manufacturers and certain related businesses that build or substantially renovate facilities in the area and create new jobs; which we have the lending expertise. • Our markets lagged the national economy in experiencing recovery; however, more recently the unemployment rate in our markets has improved at a faster pace than the national average : Unemployment Rate June 2014 June 2013 Difference Hampden County 2 6.6% 8.6% (2.0%) Hartford County 2 6.5% 8.2% (1.7%) United States 2 6.1% 7.5% (1.4%) Recent Actions to Position WFD for Continued Growth Opportunities

W E A RE E XECUTING O UR S TRATEGY • Favorable shift in interest earning assets by way of loan growth with less reliance on investment portfolio. o For the twelve months ended June 30, 2014, loans grew by $ 79.5 million, or 13.0 %, while investments have decreased by $ 110.7 million, or 18.3 %. • Target small and mid - sized businesses, which the large banks are not focused on. For the twelve months ended June 30, 2014: o C&I and CRE loans growth of $61.5 million or 16.5%. o Opened business transactional deposit accounts with an aggregate YTD average balance of $ 2.1 million. o In 4Q 2013, hired a dedicated commercial lender for the northern Connecticut market; hired two seasoned commercial lenders in 2012. o Efficient pipeline: Loan Committee meets on a weekly basis regarding decision making on large loans. Credit scoring used for small business loan originations under $350,000. • Grow residential real estate lending to diversify risk and deepen customer relationships. o Residential loans grew $18.2 million for the twelve months ended June 30, 2014, with emphasis on hybrid ARMs . • 1Q 2014 introduced Westfield Wealth Management, a new s ource of fee income. o Formed a strategic alliance with Charter Oak Insurance Agency, a general agency of Massachusetts Mutual Insurance Co. Charter Oak and Mass Mutual are located within the Westfield Bank footprint. o Provides for an ongoing revenue stream to Westfield Bank through referral based activity – the Bank does not have any significant operating expenses. 8

W E A RE E XECUTING O UR S TRATEGY • Try to effectively balance capital deployment to earn a return on our shareholders’ investment versus returning the capital dollar - for - dollar in repurchases and dividends. o TCE/TA of 11.4% as of June 30, 2014 down from 29.0% at December 31, 2006. o 1.5 million shares repurchased below TBV and dividends of $0.24 per share for the twelve months ended June 30, 2014 . • Use technology to provide solutions desired by our customers and create operational efficiencies for bank workflow . o Examples include mobile banking, bill payment, cash management and remote check capture for customers. o Cash recyclers and imaging technology for bank operational efficiency. • Reduce and manage operating expenses. o Non - interest expense declined 1.68%, or $444,000, for the twelve months ending June 30, 2014 over the previous twelve month period. 9 Quarterly non interest expense (in thousands) 6,300 6,400 6,500 6,600 6,700 6,800 6,900 Q2 13 Q3 13 Q4 13 Q1 14 Q2 14 6,789 6,851 6,488 6,534 6,531

I MPROVED MIX OF INTEREST EARNING ASSETS I NCREASING LOANS AND REDUCING SECURITIES 10 $ in millions 595 596 607 620 637 648 686 636 631 607 558 554 542 496 $450 $500 $550 $600 $650 $700 Q4 2012 Q1 2013 Q2 2013 Q3 2013 Q4 2013 Q1 2014 Q2 2014 Loans Securities

L OAN P ORTFOLIO C OMPOSITION $ in millions As of June 30, 2014 11 Owner Occupied $111.1 16% Non Owner Occupied $174.9 26% Consumer Loans $1.5 1% Home Equity $37.2 5% Residential Real Estate $213.7 31% Commercial & Industrial $147.7 21%

C OMMERCIAL L OAN P ORTFOLIO 12 $ in millions As of June 30, 2014 Manufacturing $61.3 14% Wholesale Trade $34.5 8% Retail Trade $31.6 7% Real Estate, Rental & Leasing $151.3 35% Professional, Scientific & Technical $20.0 5% Educational & Health Care $33.4 8% Arts, Entertainment & Recreation $30.2 7% Other $71.0 16% Diversified amongst a variety of segments Granularity of commercial loan relationships >$5 Million & < $10 million $121.8 28% Over $10 million $119.2 28% Under $5 Million $192.3 44%

O UR C URRENT D EPOSIT M ARKET C ITIES & T OWNS WHERE WE HAVE BRANCHES * $ in thousands Source: SNL Financial *Does not include the Granby Banking Center deposit total which opened June 2013 13 Deposits Market Bank Name Branches 06/30/2013 Share 1 TD Bank National Association 14 1,216,805 19.63% 2 United Bank 10 866,413 13.98% 3 PeoplesBank 10 796,691 12.85% 4 Westfield Bank 11 783,224 12.64% 5 Bank of America, NA 11 755,930 12.20% 6 Berkshire Bank 7 447,600 7.22% 7 Hampden Bank 6 334,174 5.39% 8 Peoples United Bank 4 235,782 3.80% 9 First Niagra Bank NA 9 221,103 3.57% 10 RBS Citizens NA 11 155,921 2.52% 11 Nuvo Bank & Trust Co 1 104,986 1.69% 12 Soveriegn Bank NA 3 94,261 1.52% 13 Easthampton Savings Bank 2 65,993 1.06% 14 Webster Bank, NA 4 62,519 1.01% 15 Chicopee Savings Bank 1 56,549 0.91%

(1) As of 06/30/2014 or the most recent quarter for which regulatory filings are available ; excludes NBN which has unique business plan Source: SNL Financial C OMMERCIAL B USINESS L ENDING C&I Loans as % of Total Loans All public banks in New England between $500 million and $5 billion in total assets (1) 14 0.00 5.00 10.00 15.00 20.00 25.00 30.00 CXBT KTHN WFD EBTC CBNK MBVT SIFI FBNK CMTV NWYF UBNK SAL FNLC Median CAC HBNK PNBK NVSL BHB NHTB WASH CNBKA UNB CATC EBSB PEOP BLMT HIFS

C ONSISTENTLY S TRONG C REDIT Q UALITY Q2 2014 Q1 2014 Q4 2013 Q3 2013 Q2 2013 Allowance for loan losses as a percentage of loans 1.17% 1.17% 1.17% 1.18% 1.23% Nonperforming loans as a percentage of total loans 0.47% 0.48% 0.41% 0.47% 0.54% Nonperforming assets as a percentage of total assets 0.25% 0.24% 0.20% 0.23% 0.25% 15

F OCUS ON C ORE D EPOSITS O VER FIVE YEAR PERIOD , TOTAL DEPOSITS GREW $187 MILLION (29.43%), WHILE N ON - MATURITY DEPOSITS GREW $182 MILLION (61.47%) June 30, 2014 June 30, 2009 16 Noninterest checking 17% Interest - bearing checking 5% Savings and MMDA 37% Time 41% Noninterest checking 13% Interest - bearing checking, 12% Savings and MMDA, 22% Time 53%

S TABLE AND C ONSISTENT N ET I NTEREST M ARGIN T AX E QUIVALENT B ASIS 17 As of June 30, 2014 1.00% 1.50% 2.00% 2.50% 3.00% 1Q 13 2Q 13 3Q 13 4Q 13 1Q 14 2Q 14 2.59% 2.55% 2.62% 2.57% 2.63% 2.61%

P RICE TO T ANGIBLE B OOK V ALUE (1) As of 06/30/2014 or the most recent quarter for which regulatory filings are available; excludes NBN which has unique bu sin ess plan Source: Company SEC filings and call reports; stock prices as of 06/30/2014. . . . B UT OUR VALUATION DOES NOT REFLECT OUR STRONG COMMERCIAL PLATFORM AND FOCUS All public banks and thrifts in New England between $500 million and $5 billion in total assets (1) 18 0.0 50.0 100.0 150.0 200.0 250.0 EBSB UNB CMTV WASH CXBT PNBK NHTB CATC HIFS CAC MBVT FNLC EBTC BHB Median BLMT PEOP UBNK BWFG HBNK CNBKA FBNK SAL SIFI KTHN NWYF CBNK NVSL WFD

W HY I NVEST IN W ESTFIELD F INANCIAL • Stock trading below tangible book . • Experienced, disciplined regional leadership team. • Continued opportunities for organic growth. • Expansion into demographically attractive markets. • Improving mix of interest earning assets. • High credit quality. • Balance sheet mix well positioned for rising rates. • Noninterest income opportunities from new wealth management services. 19

APPENDIX 20

▪ Balanced maturity and repricing schedule of loan portfolio: o 26.5% of loan portfolio due within one year; o 39.9% of loan portfolio due within three years; and o 55.2% of loan portfolio due within five years. ▪ $ 155.0 million notional of float - to - fixed interest rate swaps executed in 2013: o Includes $135.0 million notional of forward - starting. o Maturities through September 2022 . ▪ Thoughtful rebalancing of the mix in the securities and loan portfolios: o Steady cash flow generated by the securities portfolio is a reliable source of liquidity. 21 A CTIVE INTEREST RATE RISK MANAGEMENT

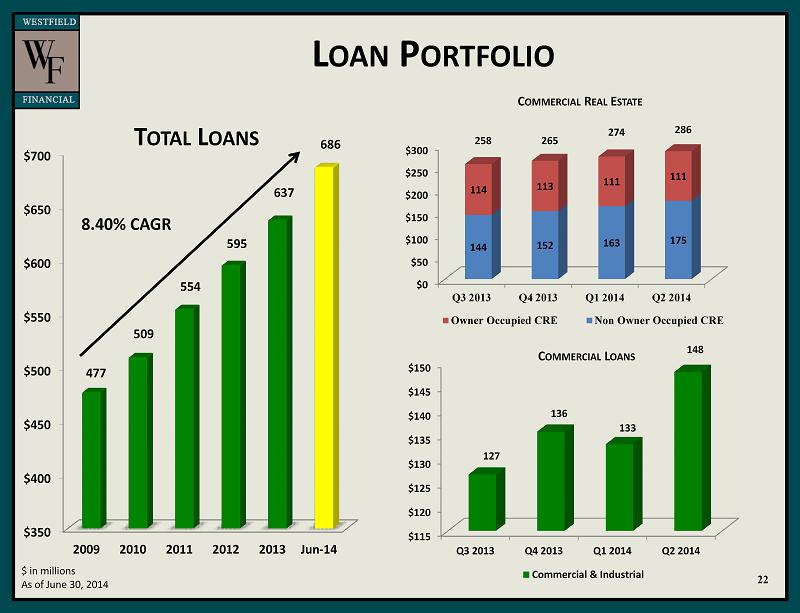

L OAN P ORTFOLIO 22 $ in millions As of June 30, 2014 $350 $400 $450 $500 $550 $600 $650 $700 2009 2010 2011 2012 2013 Jun-14 477 509 554 595 637 686 $0 $50 $100 $150 $200 $250 $300 Q3 2013 Q4 2013 Q1 2014 Q2 2014 144 152 163 175 114 113 111 111 Owner Occupied CRE Non Owner Occupied CRE $115 $120 $125 $130 $135 $140 $145 $150 Q3 2013 Q4 2013 Q1 2014 Q2 2014 127 136 133 148 Commercial & Industrial 258 265 274 286 C OMMERCIAL R EAL E STATE C OMMERCIAL L OANS T OTAL L OANS 8.40% CAGR

T OTAL D EPOSITS 23 $ in millions As of June 30, 2014 4.74% CAGR $450 $500 $550 $600 $650 $700 $750 $800 $850 2009 2010 2011 2012 2013 Jun-14 648 700 733 753 817 819

S ECURITIES P ORTFOLIO B REAKDOWN 24 As of June 30, 2014 GSE Mortgage Backed Securities 70.3% New England Municpal Bonds 5.1% Government Sponsored Enterprise Debt 11.2% Equity Securities 1.6% Corporate Bonds 11.8% Treasury/Agency 81.6 % AAA 0.3 % AA & A 9.5 % Less than A 3.7 % Split Ratings 3.3 % Not Rated 1.6 % S TRONG U NDERLYING C REDIT IN S ECURITIES P ORTFOLIO C ONSERVATIVE S ECURITIES P ORTFOLIO

E FFECTIVELY L EVERAGING C APITAL S HAREHOLDERS ’ EQUITY TO ASSETS 25 As of June 30, 2014 0.00% 5.00% 10.00% 15.00% 20.00% 25.00% 2009 2010 2011 2012 2013 Jun-14 20.76% 17.85% 17.34% 14.54% 12.07% 11.43%

C APITAL M ANAGEMENT C UMULATIVE R ETURN OF C APITAL S INCE S ECOND S TEP C ONVERSION On March 13, 2014, the Board of Directors authorized a stock repurchase program under which the Company may purchase up to 1,970,000 shares, or 10% of its outstanding common stock. 26 56,713 33.0% 87,135 50.7% Percentages at top of bars represent cumulative return of capital via dividends and repurchases as a percentage of net proceeds from second step conversion. 111,511 64.9% 153,963 89.7% 180,227 105.0% 184,001 107.2% As of June 30, 2014 193,311 112.6% - 75,000 150,000 225,000 2009 2010 2011 2012 2013 1Q 2014 2Q 2014 32,540 46,835 61,140 71,861 77,733 78,862 81,087 24,173 40,300 50,371 82,102 102,494 105,139 112,224 Dividends Repurchases

E FFECTIVE P RICE E XECUTION OF R EPURCHASES S HARES R EPURCHASED BY Q UARTER AND P/TBV OF R EPURCHASES The lower the price, the more active WFD has been in its repurchase activity. By repurchasing significant numbers of shares below TBV, WFD has BOTH right - sized its capital level while ALSO increasing tangible book value. Shares Repurch (000) P/TBV of repurch 27 70% 80% 90% 100% 110% 120% 0 500 1,000 1,500 2,000 2,500 1Q 10 2Q 10 3Q 10 4Q 10 1Q 11 2Q 11 3Q 11 4Q 11 1Q 12 2Q 12 3Q 12 4Q 12 1Q 13 2Q 13 3Q 13 4Q 13 1Q 14 2Q 14 Shares Repurchased (000) Repurch Price / Last Quarter TBV

D IVIDEND H ISTORY 28 $0.00 $0.15 $0.30 $0.45 $0.60 $0.75 2008 2009 2010 2011 2012 2013 2Q 2013 2Q 2014 $0.20 $0.20 $0.22 $0.24 $0.24 $0.24 $0.12 $0.12 $0.40 $0.30 $0.30 $0.30 $0.20 $0.05 $0.05 Regular dividends Special dividends 2008 2009 2010 2011 2012 2013 2Q 2013 2Q 2014 Regular dividends $0.20 $0.20 $0.22 $0.24 $0.24 $0.24 $0.12 $0.12 Dividend payout 71.4% 90.9% 122.2% 218.2% 109.1% 70.6% 75.0% 75.0% Dividend yield 2.1% 1.9% 2.7% 2.6% 3.3% 3.3% 1.7% 1.6% Total dividends $0.60 $0.50 $0.52 $0.54 $0.44 $0.29 $0.17 $0.12 Dividend payout 214.3% 227.3% 288.9% 490.9% 200.0% 85.3% 106.3% 75.0% Dividend yield 6.2% 4.8% 6.3% 5.8% 6.0% 8.0% 4.7% 3.2%

D ILUTED E ARNINGS P ER S HARE 29 As of June 30, 2014 17.23% CAGR $0.00 $0.05 $0.10 $0.15 $0.20 $0.25 $0.30 $0.35 2009 2010 2011 2012 2013 Jan - June 2013 Jan - June 2014 $0.18 $0.11 $0.22 $0.26 $0.34 $0.16 $0.16

WESTFIELD FINANCIAL, INC. AND SUBSIDIARIES Consolidated Statements of Income and Other Data (Dollars in thousands, except share and per share data) (Unaudited) 30 Three Months Ended Six Months Ended June 30, March 31, December 31, September 30, June 30, June 30, 2014 2014 2013 2013 2013 2014 2013 INTEREST AND DIVIDEND INCOME: Loans $ 6,821 $ 6,557 $ 6,458 $ 6,371 $ 6,307 $ 13,378 $ 12,578 Securities 3,256 3,406 3,594 3,954 3,917 6,662 7,974 Other investments - at cost 63 65 33 20 21 128 40 Federal funds sold, interest - bearing deposits and other short - term investments 3 6 4 3 1 9 3 Total interest and dividend income 10,143 10,034 10,089 10,348 10,246 20,177 20,595 INTEREST EXPENSE: Deposits 1,288 1,291 1,358 1,390 1,390 2,580 2,777 Long - term debt 1,071 1,011 1,051 1,094 1,188 2,081 2,446 Short - term borrowings 83 77 73 36 31 160 65 Total interest expense 2,442 2,379 2,482 2,520 2,609 4,821 5,288 Net interest and dividend income 7,701 7,655 7,607 7,828 7,637 15,356 15,307 PROVISION (CREDIT) FOR LOAN LOSSES 450 100 120 (71) (70) 550 (305) Net interest and dividend income after provision for loan losses 7,251 7,555 7,487 7,899 7,707 14,806 15,612 NONINTEREST INCOME: Service charges and fees 632 670 625 615 594 1,303 1,164 Income from bank - owned life insurance 386 379 388 388 387 765 773 Gain on bank - owned life insurance death benefit - - - - 563 - 563 Loss on prepayment of borrowings - - - (540) (1,404) - (2,830) Gain on sales of securities, net 21 29 330 546 823 50 2,250 Total noninterest income 1,039 1,078 1,343 1,009 963 2,118 1,920 NONINTEREST EXPENSE: Salaries and employees benefits 3,665 3,778 3,774 4,059 3,817 7,444 7,625 Occupancy 751 761 731 733 730 1,512 1,434 Data processing 610 515 586 602 602 1,125 1,152 Professional fees 483 512 497 499 527 994 1,037 OREO expense - - - - - - 22 FDIC insurance 177 165 162 169 163 342 324 Other 845 803 738 789 950 1,649 1,709 Total noninterest expense 6,531 6,534 6,488 6,851 6,789 13,066 13,303 INCOME BEFORE INCOME TAXES 1,759 2,099 2,342 2,057 1,881 3,858 4,229 INCOME TAX PROVISION 417 451 533 476 297 868 863 NET INCOME $ 1,342 $ 1,648 $ 1,809 $ 1,581 $ 1,584 $ 2,990 $ 3,366 Basic earnings per share $ 0.07 $ 0.09 $ 0.09 $ 0.08 $ 0.08 $ 0.16 $ 0.16 Weighted average shares outstanding 18,308,828 18,812,795 19,379,466 19,583,632 20,276,261 18,559,419 20,686,860 Diluted earnings per share $ 0.07 $ 0.09 $ 0.09 $ 0.08 $ 0.08 $ 0.16 $ 0.16 Weighted average diluted shares outstanding 18,308,828 18,812,795 19,379,466 19,583,632 20,276,261 18,559,419 20,686,887

WESTFIELD FINANCIAL, INC. AND SUBSIDIARIES Consolidated Balance Sheets and Other Data (Dollars in thousands, except per share data) ( Unaudited) 31 June 30, March 31, December 31, September 30, June 30, 2014 2014 2013 2013 2013 Cash and cash equivalents $ 39,362 $ 21,370 $ 19,742 $ 28,418 $ 15,706 Securities available for sale, at fair value 192,754 233,899 243,204 242,957 417,053 Securities held to maturity, at cost 288,199 292,019 295,013 298,988 173,982 Federal Home Loan Bank of Boston and other restricted stock - at cost 15,056 15,631 15,631 15,631 15,629 Loans 686,068 648,240 637,427 620,154 606,605 Allowance for loan losses 8,017 7,567 7,459 7,311 7,473 Net loans 678,051 640,673 629,968 612,843 599,132 Bank - owned life insurance 47,945 47,558 47,179 46,791 46,403 Other assets 24,951 23,866 26,104 25,703 25,730 TOTAL ASSETS $ 1,286,318 $ 1,275,016 $ 1,276,841 $ 1,271,331 $ 1,293,635 Total deposits $ 818,590 $ 806,695 $ 817,112 $ 793,510 $ 782,682 Short - term borrowings 59,751 58,460 48,197 61,784 69,972 Long - term debt 248,760 248,568 248,377 248,184 269,991 Securities pending settlement 67 195 299 - - Other liabilities 12,185 9,512 8,712 10,954 10,573 TOTAL LIABILITIES 1,139,353 1,123,430 1,122,697 1,114,432 1,133,218 TOTAL SHAREHOLDERS' EQUITY 146,965 151,586 154,144 156,899 160,417 TOTAL LIABILITIES AND SHAREHOLDERS' EQUITY $ 1,286,318 $ 1,275,016 $ 1,276,841 $ 1,271,331 $ 1,293,635 Book value per share $ 7.67 $ 7.66 $ 7.65 $ 7.57 $ 7.73

O THER D ATA 32 ( 1) Three and six months results have been annualized. ( 2) The efficiency ratio represents the ratio of operating expenses divided by the sum of net interest and dividend income and noninterest income, excluding gain and loss of the sale of securities, gain on bank - owned life insurance death benefit and loss on prepayment of borrowings. Three Months Ended Six Months Ended June 30, March 31, December 31, September 30, June 30, June 30, 2014 2014 2013 2013 2013 2014 2013 Return on average assets (1) 0.42% 0.52% 0.57% 0.49% 0.49% 0.47% 0.52% Return on average equity (1) 3.64% 4.38% 4.61% 3.96% 3.66% 4.01% 3.82% Efficiency ratio (2) 74.91 75.07 75.27 77.58 78.78 74.99 77.15 Net interest margin 2.61% 2.63% 2.57% 2.62% 2.55% 2.62% 2.57% June 30, March 31, December 31, September 30, June 30, 2014 2014 2013 2013 2013 30 - 89 day delinquent loans $ 5,539 $ 5,382 $ 3,459 $ 1,860 $ 1,438 Nonperforming loans 3,225 3,095 2,586 2,933 3,272 Nonperforming loans as a percentage of total loans 0.47% 0.48% 0.41% 0.47% 0.54% Nonperforming assets as a percentage of total assets 0.25% 0.24% 0.20% 0.23% 0.25% Allowance for loan losses as a percentage of nonperforming loans 248.59% 244.49% 288.44% 249.27% 228.39% Allowance for loan losses as a percentage of total loans 1.17% 1.17% 1.17% 1.18% 1.23%

T OTAL R ETURN P ERFORMANCE * T HREE Y EAR T OTAL R ETURN V ERSUS SNL T HRIFT I NDEX * Source: SNL Financial, data as of close of business September 2, 2014 . 33 (30.00) (20.00) (10.00) 0.00 10.00 20.00 30.00 40.00 50.00 60.00 70.00 80.00 09/02/2011 12/02/2011 03/02/2012 06/02/2012 09/02/2012 12/02/2012 03/02/2013 06/02/2013 09/02/2013 12/02/2013 03/02/2014 06/02/2014 09/02/2014 WFD SNL U.S. Thrift