UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant ☐

Filed by a Party other than the Registrant ☒

Check the appropriate box:

☐ | Preliminary Proxy Statement | |

☐ | Confidential, For Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

☐ | Definitive Proxy Statement | |

☐ | Definitive Additional Materials | |

☒ | Soliciting Material Pursuant to § 240.14a-12 | |

Spirit Airlines, Inc.

(Name of Registrant as Specified In Its Charter)

JetBlue Airways Corporation

Sundown Acquisition Corp.

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

☒ | No fee required. | |

☐ | Fee paid previously with preliminary materials. | |

☐ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(1) and 0-11. | |

Filed by JetBlue Airways Corporation

Pursuant to Rule 14a-12 under the

Securities Exchange Act of 1934, as amended

Subject Company: Spirit Airlines, Inc.

Commission File No.: 001-35186

Date: July 28, 2022

This filing contains the following communications:

| 1. | A transcript of a video featuring antitrust expert Glenn Pomerantz, published on www.LowFaresGreatService.com on July 28, 2022. |

| 2. | Regulatory Fact Sheets published by JetBlue Airways Corporation (“JetBlue”) on www.LowFaresGreatService.com on July 28, 2022. |

| 3. | A transcript of a video featuring JetBlue Chief Executive Officer, Robin Hayes, published on JetBlue’s HelloJetBlue intranet on July 28, 2022. |

| 4. | Information published by JetBlue on its HelloJetBlue intranet on July 28, 2022. |

| 5. | An investor presentation published by JetBlue on the Investor Relations page of JetBlue’s website (accessible at https://blueir.investproductions.com/investor-relations) and on www.LowFaresGreatService.com on July 28, 2022. |

| 6. | Information posted by JetBlue to various social media platforms on July 28, 2022. |

| 7. | A “Transaction Fact Sheet” published by JetBlue on www.LowFaresGreatService.com on July 28, 2022. |

| 8. | Screenshots of information published by JetBlue and Spirit Airlines, Inc. on www.LowFaresGreatService.com on July 28, 2022. |

| 1. | The following is a transcript of a video featuring antitrust expert Glenn Pomerantz, published on www.LowFaresGreatService.com on July 28, 2022: |

Hi. I’m Glenn Pomerantz. I’ve been practicing law for almost 40 years with a primary focus on antitrust matters, including the litigation of various mergers. I’ve been retained by the Department of Justice and by State Attorneys Generals to examine and lead them at trial in connection with other mergers, such as the attempted merger of AT&T and T-Mobile. I’ve been retained by JetBlue to work with their experienced antitrust counsel to examine the regulatory environment and how the Department of Justice and courts will review the merger of JetBlue and Spirit Airlines.

What do you view as the biggest challenge the JetBlue-Spirit combination is going to have with regulators?

I think the biggest challenge with the regulators is the current Administration’s stated position that any airline merger is likely to face a challenge in court. Here, with JetBlue acquiring Spirit, you have a low-cost airline acquiring an ultra-low-cost airline and that’s going to cause the DOJ to look into how such a merger would affect passengers. Now, JetBlue has a very strong response – the “JetBlue Effect.” And what the JetBlue effect means is that when JetBlue enters a market with its low fares and great service, it causes the legacy airlines to lower their fares to the benefit of passengers. And here, it’s not just JetBlue that says there’s such a thing as the “JetBlue Effect.” The DOJ itself acknowledges that effect in the Northeast Alliance litigation. In fact, the DOJ calls the “JetBlue Effect” uniquely disruptive and beneficial to passengers. So when JetBlue acquires Spirit, it’s going to be able to take that “JetBlue Effect” and expand it to many more passengers on many more routes.

Do you think the DOJ would prefer a Frontier-Spirit combination?

JetBlue is known for offering high-quality service. They offer that service to business travelers, and they offer it to vacationers. Spirit and Frontier are known for offering basic service, and that difference in service is something that the Department of Justice and any court will consider in assessing this merger.

Why do you think JetBlue-Spirit would create a stronger competitor to the legacy airlines?

There, you have the acknowledged “JetBlue Effect.” What that means is that the legacy airlines are going to face competition from JetBlue with their low fares and their great service in on more routes, benefiting more passengers.

What do you say to those who are concerned that the JetBlue transaction cannot get done?

I think if anyone were to carefully look at the competitive effects of combining JetBlue with Spirit, they’re going to find two things. First, the “JetBlue Effect” is real. What that means is that passengers on JetBlue and passengers on the legacy airlines are going to enjoy the benefits of lower fares and good service — in fact, great service. And if instead you’re worried about the passengers who really want an ultra-low-cost alternative, those alternatives will be there. There are plenty of other ultra-low-cost carriers, who will enter and take over a route of Spirit’s if that route is profitable. Frontier is out there. In fact, Frontier is looking to expand. They have a lot of aircraft already on order. And there’s Allegiant and Sun Country and some recent entrants as well. So, everyone’s going to win if JetBlue and Spirit merge.

| 2. | The following are Regulatory Fact Sheets published by JetBlue on www.LowFaresGreatService.com on July 28, 2022: |

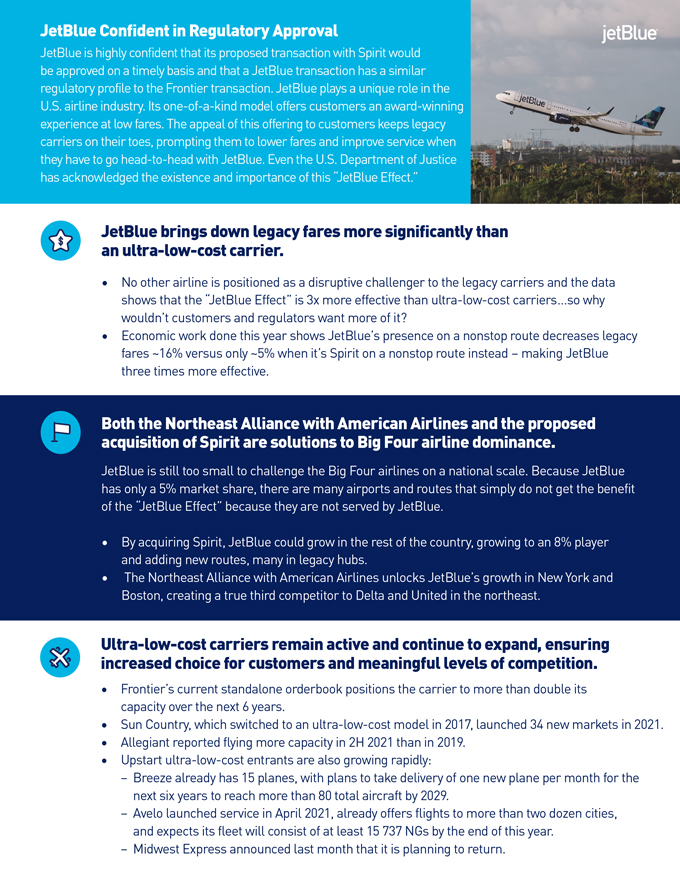

JetBlue Confident in Regulatory Approval JetBlue is highly confident that its proposed transaction with Spirit would be approved on a timely basis and that a JetBlue transaction has a similar regulatory profile to the Frontier transaction. JetBlue plays a unique role in the U.S. airline industry. Its one-of-a-kind model offers customers an award-winning experience at low fares. The appeal of this offering to customers keeps legacy carriers on their toes, prompting them to lower fares and improve service when they have to go head-to-head with JetBlue. Even the U.S. Department of Justice has acknowledged the existence and importance of this “JetBlue Effect.” JetBlue an ultra-low-cost brings down carrier. legacy fares more significantly than • No other airline is positioned as a disruptive challenger to the legacy carriers and the data shows that the “JetBlue Effect” is 3x more effective than ultra-low-cost carriers…so why wouldn’t customers and regulators want more of it? • Economic work done this year shows JetBlue’s presence on a nonstop route decreases legacy fares ~16% versus only ~5% when it’s Spirit on a nonstop route instead – making JetBlue three times more effective. acquisition Both the Northeast of Spirit Alliance are solutions with American to Big Four Airlines airline and dominance. the proposed JetBlue is still too small to challenge the Big Four airlines on a national scale. Because JetBlue has only a 5% market share, there are many airports and routes that simply do not get the benefit of the “JetBlue Effect” because they are not served by JetBlue. • By acquiring Spirit, JetBlue could grow in the rest of the country, growing to an 8% player and adding new routes, many in legacy hubs. • The Northeast Alliance with American Airlines unlocks JetBlue’s growth in New York and Boston, creating a true third competitor to Delta and United in the northeast. Ultra-low-cost increased choice carriers for customers remain active and meaningful and continue levels to expand, of competition. ensuring • Frontier’s current standalone orderbook positions the carrier to more than double its capacity over the next 6 years. • Sun Country, which switched to an ultra-low-cost model in 2017, launched 34 new markets in 2021. • Allegiant reported flying more capacity in 2H 2021 than in 2019. • Upstart ultra-low-cost entrants are also growing rapidly: - Breeze already has 15 planes, with plans to take delivery of one new plane per month for the next six years to reach more than 80 total aircraft by 2029. - Avelo launched service in April 2021, already offers flights to more than two dozen cities, and expects its fleet will consist of at least 15 737 NGs by the end of this year. - Midwest Express announced last month that it is planning to return.

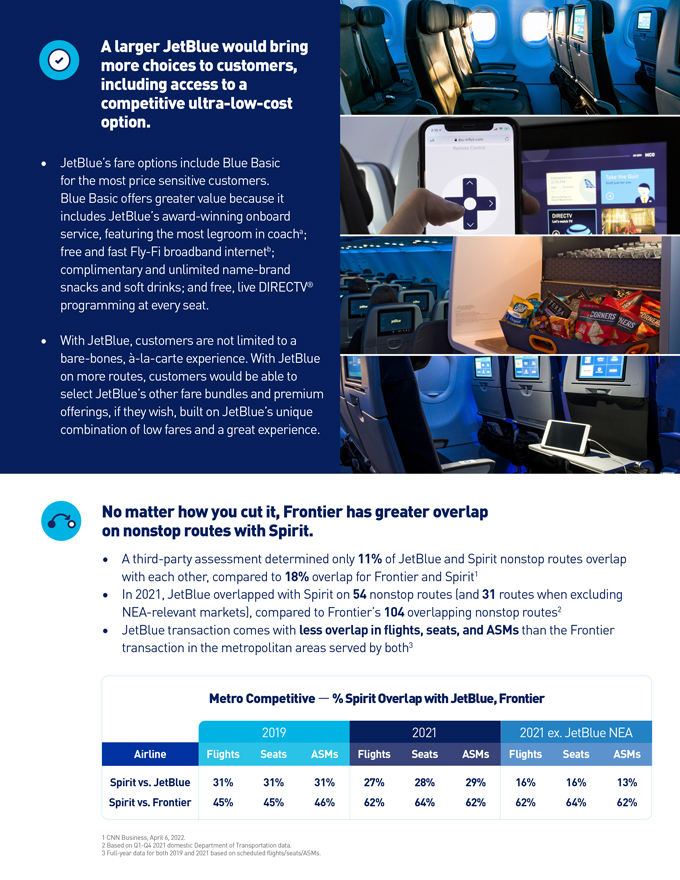

more A larger choices JetBlue to customers, would bring including competitive access ultra-low-cost to a option. • JetBlue’s fare options include Blue Basic for the most price sensitive customers. Blue Basic offers greater value because it includes JetBlue’s award-winning onboard service, featuring the most legroom in coacha; free and fast Fly-Fi broadband internetb; complimentary and unlimited name-brand snacks and soft drinks; and free, live DIRECTV® programming at every seat. • With JetBlue, customers are not limited to a bare-bones, à-la-carte experience. With JetBlue on more routes, customers would be able to select JetBlue’s other fare bundles and premium offerings, if they wish, built on JetBlue’s unique combination of low fares and a great experience. on No nonstop matter how routes you with cut it, Spirit. Frontier has greater overlap • A third-party assessment determined only 11% of JetBlue and Spirit nonstop routes overlap with each other, compared to 18% overlap for Frontier and Spirit1 • In 2021, JetBlue overlapped with Spirit on 54 nonstop routes (and 31 routes when excluding NEA-relevant markets), compared to Frontier’s 104 overlapping nonstop routes2 • JetBlue transaction comes with less overlap in flights, seats, and ASMs than the Frontier transaction in the metropolitan areas served by both3 Metro Competitive — % Spirit Overlap with JetBlue, Frontier 2019 2021 2021 ex. JetBlue NEA Airline Flights Seats ASMs Flights Seats ASMs Flights Seats ASMs Spirit vs. JetBlue 31% 31% 31% 27% 28% 29% 16% 16% 13% Spirit vs. Frontier 45% 45% 46% 62% 64% 62% 62% 64% 62% 1 2 Based CNN Business, on Q1-Q4 April 2021 6, domestic 2022. Department of Transportation data. 3 Full-year data for both 2019 and 2021 based on scheduled flights/seats/ASMs.

Footnotes

| a | JetBlue offers the most legroom in coach based on average fleet-wide seat pitch for U.S. airlines. |

| b | Fly-Fi and live television are available on all JetBlue-operated flights. On ViaSat-2 equipped aircraft, Fly-Fi will not be available on portions of some routes, and live television will not be available while operating outside of the contiguous U.S., or until the aircraft returns to the coverage area. On all other aircraft, Fly-Fi and live television will not be available while operating outside of the contiguous U.S., or until the aircraft returns to the coverage area. |

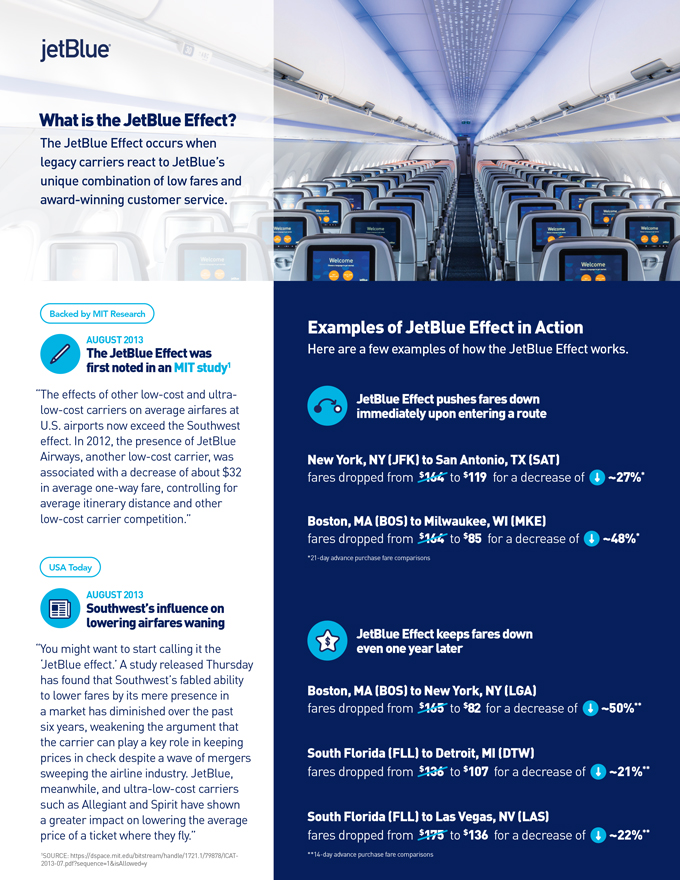

What is the JetBlue Effect? The JetBlue Effect occurs when legacy carriers react to JetBlue’s unique combination of low fares and award-winning customer service. Backed by MIT Research AUGUST 2013 The JetBlue Effect was first noted in an MIT study1 “The effects of other low-cost and ultra-low-cost carriers on average airfares at U.S. airports now exceed the Southwest effect. In 2012, the presence of JetBlue Airways, another low-cost carrier, was associated with a decrease of about $32 in average one-way fare, controlling for average itinerary distance and other low-cost carrier competition.” USA Today AUGUST 2013 Southwest’s influence on lowering airfares waning “You might want to start calling it the ‘JetBlue effect.’ A study released Thursday has found that Southwest’s fabled ability to lower fares by its mere presence in a market has diminished over the past six years, weakening the argument that the carrier can play a key role in keeping prices in check despite a wave of mergers sweeping the airline industry. JetBlue, meanwhile, and ultra-low-cost carriers such as Allegiant and Spirit have shown a greater impact on lowering the average price of a ticket where they fly.” 1SOURCE: https://dspace.mit.edu/bitstream/handle/1721.1/79878/ICAT-2013-07.pdf?sequence=1&isAllowed=y Examples of JetBlue Effect in Action Here are a few examples of how the JetBlue Effect works. JetBlue Effect pushes fares down immediately upon entering a route New York, NY (JFK) to San Antonio, TX (SAT) fares dropped from $164 to $119 for a decrease of ~27%* Boston, MA (BOS) to Milwaukee, WI (MKE) fares dropped from $164 to $85 for a decrease of ~48%* *21-day advance purchase fare comparisons JetBlue Effect keeps fares down even one year later Boston, MA (BOS) to New York, NY (LGA) fares dropped from $165 to $82 for a decrease of ~50%** South Florida (FLL) to Detroit, MI (DTW) fares dropped from $136 to $107 for a decrease of ~21%** South Florida (FLL) to Las Vegas, NV (LAS) fares dropped from $175 to $136 for a decrease of ~22%** **14-day advance purchase fare comparisons

The Department of Justice on the JetBlue Effect CASE 1:21-CV-115582 In the Department of Justice’s court filing regarding JetBlue’s Northeast Alliance with American Airlines, the DOJ told the court: “JetBlue’s reputation for lowering fares is so well known in the airline industry that it has earned a name: the ‘JetBlue Effect.’ JetBlue’s record in Boston and New York City illustrates why. Since launching service at Boston Logan in 2004, JetBlue has challenged the major airlines—including American—by offering lower fares and better service. Consumers voted with their feet. JetBlue became Boston’s leading airline, offering more flights out of Boston than any other airline. What’s more, JetBlue forced American and other airlines that serve Boston to lower their fares as well. This competition has resulted in substantial savings for consumers. In 2019, JetBlue estimated that it had saved consumers flying to and from Boston more than $3 billion since it started serving the airport in 2004. JetBlue has had a similar effect in New York City. In a presentation titled ‘16 Years of Disrupting the Industry,’ JetBlue explained that ‘there’s no question we are a disruptor. There’s no better example of how we’ve influenced change than at our home at JFK Airport.’” 2SOURCE: https://www.justice.gov/opa/press-release/file/1434621/download APRIL 6, 2022 JetBlue CEO Robin Hayes appears on CNBC “When JetBlue flies into a market and competes with a legacy airline, the overall fares come down more than when an ultra-low-cost carrier flies against the legacy airlines and they do that because JetBlue is not ignored [by the legacy airlines].”

Footnotes

| a | JetBlue offers the most legroom in coach based on average fleet-wide seat pitch for U.S. airlines. |

| b | Fly-Fi and live television are available on all JetBlue-operated flights. On ViaSat-2 equipped aircraft, Fly-Fi will not be available on portions of some routes, and live television will not be available while operating outside of the contiguous U.S., or until the aircraft returns to the coverage area. On all other aircraft, Fly-Fi and live television will not be available while operating outside of the contiguous U.S., or until the aircraft returns to the coverage area. |

| 3. | The following is a transcript of a “BlueNote” video featuring JetBlue Chief Executive Officer, Robin Hayes, published on JetBlue’s HelloJetBlue intranet on July 28, 2022: |

BlueNote

[VIDEO]

Dear Crewmembers,

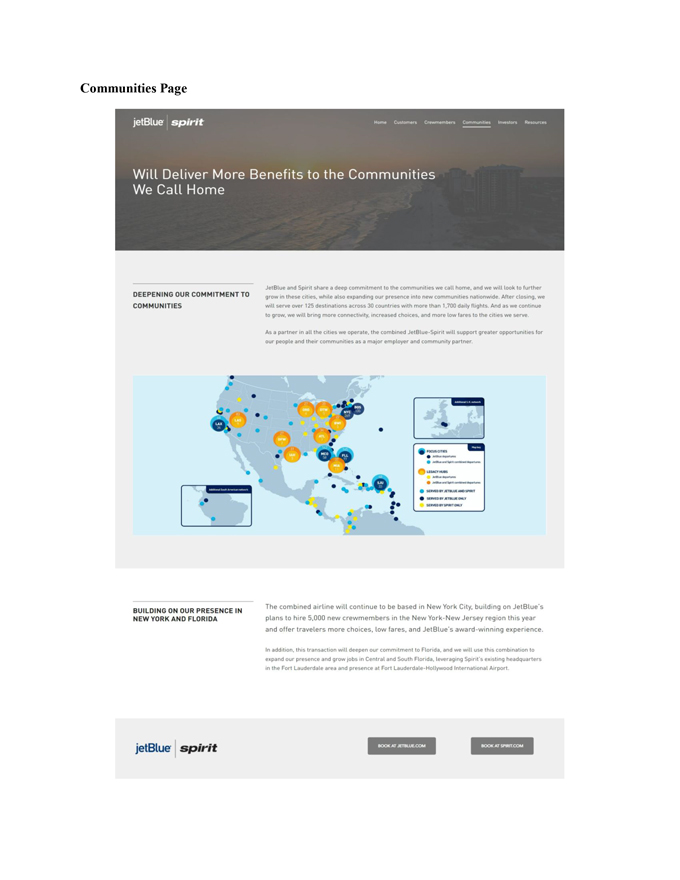

I have great news to share. We have reached an agreement to buy Spirit Airlines to create a low-fare, customer-centric competitor to the Big Four airlines. This is exciting news, including for the many Crewmembers who have wanted us to accelerate our growth, especially in the focus cities outside of the Northeast and in legacy carrier hubs across the U.S.

Spirit’s Airbus fleet and network fit perfectly with ours, and together with their 10,000 team members, we will fly more routes in more cities faster than we could on our own. Once Spirit is integrated into JetBlue we’ll be the nation’s fifth largest airline, with about 9% market share. We’ll still be smaller than the Big Four airlines, but with more than 1,700 daily flights we’ll have more opportunities to challenge those legacy carriers to lower their fares and step up their game — just as we’ve been doing for 22 years.

A bigger JetBlue is good for Crewmembers, too. Whether you work on the front line or in the support center, a larger airline will provide more career and flying opportunities, as well as more investment in programs like JetBlue Scholars, our Gateways program and Support Center pathways.

The combined airline will be based in New York, but we will use this combination to expand our presence and grow jobs in Central and South Florida as well. We’re looking forward to welcoming Spirit’s team members into JetBlue once the deal closes. We’ve now had a chance to meet with Spirit’s team face to face and have come to a very friendly place with them. I’m confident we will work very well together after closing. And we want all of Spirit’s team members to feel welcome here at JetBlue. If you happen to talk to Spirit’s team members on the line or while you are traveling, please share a little of that blue juice with them and let them know how excited we are that they will be joining us.

I know many of you will have your own questions about how we are going to integrate JetBlue and Spirit. It’s important, though, we don’t get ahead of ourselves. It will take quite some time before we are one airline. In fact, until Spirit’s shareholders and the government approve our deal, we remain two separate companies with independent operations. And once we have gotten the green light to move forward, there will still be a lot of work to do to function as one, including sunsetting the Spirit brand, retrofitting their fleet and bringing together our operating and ticketing systems. We are also looking forward to learning from the Spirit team and bringing the best of the airline into JetBlue.

Now, while it’s a long way off; when the time comes to consider incorporating our teams, especially combining unionized and non-union groups and groups with different unions, we’re committed to working with our respective people and labor leaders to ensure a larger JetBlue is a winning proposition for all Crewmembers. And we will, of course, follow the law that governs seniority integration for our industry. All of this will not happen overnight though. Between JetBlue and Spirit, we’ll put a great team in place to get the job done and we’ll keep you posted in the months ahead.

Today is a day to celebrate though, I know there’s a lot to manage in our day-to-day business right now, but we can’t let that stop us from making game-changing moves that set us up for our future. By acquiring Spirit, we are making an important investment that will benefit us for the long term. In five or ten years we will look back on this as another defining moment for JetBlue, one that gave our one-of-a-kind airline with a brand that people love, award-winning service and everyday low fares, the opportunity to reach more people in more places than we ever have before. Thanks for all you are doing and we’ll talk much more about this in the weeks and months ahead.

Robin

| 4. | The following information was published by JetBlue on its HelloJetBlue intranet on July 28, 2022: |

Your Top JetBlue-Spirit Questions Answered

How long will it take before Spirit is integrated into JetBlue?

It will take two or more years before JetBlue and Spirit operate as one airline. Our preliminary timeline anticipates that the transaction will close in the first half of 2024, and after that, it could take another year to receive a single operating certificate. It will take several years to unify all the branding as JetBlue, integrate our IT systems, and retrofit the Spirit fleet with the JetBlue experience.

What happens next?

Spirit shareholders will need to have a meeting to vote on our deal, and that should happen this fall. We also will be working to get government approval on our transaction. Until we close, we remain two separate companies and it’s business as usual at JetBlue.

Will we retain anything from the Spirit’s offering or operational processes?

The combined airline will be called JetBlue, and we will sunset the Spirit brand. Although Spirit’s onboard experience is very different than ours, they’ve been very successful and we can learn from them too. As part of our integration, we will take a closer look to see what things they do better than JetBlue and decide if we want to incorporate any of those things into our business.

Where will the combined airline be based?

The combined airline will be based in New York City, and we plan use Spirit’s new headquarters building in Fort Lauderdale as a JetBlue support center and training center.

How can we afford to buy another airline right now?

We were able to borrow money to pay for Spirit from several banks. Since Spirit will generate additional revenue for JetBlue, we’ll be able to take that incoming money to help pay off the debt.

How will frontline workgroup seniority lists be integrated?

There’s a federal law called McCaskill-Bond that lays out how seniority lists should be integrated so everyone receives fair treatment. Our non-union workgroups will receive a fund for legal representation to ensure they have a neutral party supporting the process. It’s still a long way off however, as we need to secure government approval first.

Do you expect the government will approve the transaction?

While we’ve all heard that the current administration is concerned about consolidation, we know the U.S. Department of Justice and the U.S. Department of Transportation want to see more competition in the airline industry. If they will allow us to get bigger by buying Spirit, we can bring more low fares and great service to benefit Customers. Nothing keeps the legacy carriers on their toes like when they have to go head-to-head with JetBlue, and we will make a strong case to DOJ and DOT that we should be allowed to do that.

Would we walk away from the Northeast Alliance with American Airlines to secure approval?

We will present our case on the Northeast Alliance to the court in September. Both the NEA and our acquisition of Spirit enhance competition, and so we firmly believe Customers win if we can keep both.

Approval and Integration Will Take Several Years

Our preliminary timeline anticipates that the transaction will close in the first half of 2024, with integration work beginning after that. A four to five year integration process with full fleet retrofitting would follow, with the expectation that we would be operating with one single operating certificate by first quarter 2025.

Integration: How Two Airlines Will Become One

The airline industry has been full of mergers for the past 30 years, and we can learn a lot from what they did right and what they did wrong.

It takes quite a bit of work to integrate two companies into one. To fold Spirit into JetBlue, we’ll need to look at a how we integrate our culture, teams, fleet, IT systems, real estate and operations.

This will all be done by an integration team that will include people from both JetBlue and Spirit. The planning will begin right away, with teams from both airlines starting to look at all the work that needs to be done. Once we have government approval and the deal closes, then we can start the actual integration work.

Brand, Experience and Fleet

The new company will be called JetBlue and we will sunset the Spirit brand. That means we’ll need to change all the places where the Spirit brand is displayed. Spirit’s fleet will be retrofitted to the JetBlue Experience and repainted with our livery designs.

People and Culture

The new airline will be double the size of JetBlue today. That means we don’t expect any involuntary job reductions – in fact, we expect to grow! But with so many new people starting to work together, we’ll create a plan that reinforces a “one team” culture among the people who work for both airlines and look at the talent we have across support functions to build one great team that can work together.

The Best of Both Airlines

While the combined company will be JetBlue and we’ll offer the JetBlue Experience across the full fleet, we also will be open to ideas from Spirit. If there’s something they’re doing really well with systems, technology, operations, or product offerings, we’ll take a close look to see if it might be worth keeping as part of the new company.

Seniority List Integration

A big focus for our frontline Crewmembers will be seniority list integration. The McCaskill-Bond Statue, which is a federal law, lays out how exactly how this will be done fairly. We’ll share more information with the workgroups on what the law looks at. Our workgroups under the direct relationship will receive a legal fund from JetBlue so that they have legal representation during this process.

“Headquarters” and Support Center Locations

While we don’t typically use the word “headquarters,” everyone will want to know where the HQ of the combined company will be. The answer: New York City. We are most definitely New York’s Hometown Airline and that won’t change.

The exciting news is that we will also be able to boost our presence in Fort Lauderdale by turning Spirit’s new headquarters building into a JetBlue support center and training campus. Of course, with 34,000 people part of the new company, having additional training space and simulators outside of Orlando will be essential to meet our growing needs. We’ll also be adding jobs in Orlando in the year ahead, so we are set to be a growing employer in Florida.

IT Systems

JetBlue runs on many different systems, from ticketing, to operations, to website/app, to backbone corporate infrastructure. We’ll create a roadmap that brings all these systems together and lays out what our long-term IT infrastructure will be. This will be a complicated process, but the goal will be to finish this project with better systems that set up JetBlue for the future and help our Crewmembers succeed in their jobs.

Loyalty Programs

When two companies merge, Customers always want to know how it will affect them. In this case, we’ll eventually bring together the two loyalty programs so that Customers get even more value and options. That’s a ways off though, and right now nothing changes.

The integration team will help us prioritize all of our projects to make sure we have enough people and resources to get all of our work done and transparent communication will be key.

The most important thing is while we have a good idea of what the combined company will look like, we will learn a lot in the integration process that will guide our specific plans for these areas.

How are we going to pay for Spirit?

Today, we shared the news that we’ve reached an agreement to buy Spirit. The announcement comes nearly four months after our initial offer, and follows a number of improved offers we have made since April. All of that anteing does raise the question: how we can afford to lay out so much money, especially as we are still working through our pandemic recovery?

We talked to our CFO Ursula Hurley to get a better understanding of how this acquisition is doable for JetBlue. As Ursula explained, our cash offer to buy Spirit is not the same as using money that we have just “laying around.” Rather, it’s a loan that we will have to repay. As we integrate Spirit into JetBlue, we will have more money coming in and higher profits than we do today, which we will then use to pay down our debt with the bank.

WHY IS WORTH IT TO BORROW THE MONEY?

Taking a loan like this is “worth it” because it’s an investment in our future. A great example is a home mortgage. If you own your home, at different points in your life, you might borrow money to invest in a new kitchen, a home renovation, or even to buy a newer house. You do that because even though you’ll be in more debt, the value of your home will be higher in the long run. It’s an investment that pays off.

Similarly, now that we have bought Spirit, we’ll take on more debt. But a larger JetBlue with more planes and Customers will improve our value in the long run, help us make more profit, and make the loan worth its expense.

WHY GET A LOAN FOR THIS AND NOT FOR OTHER INVESTMENTS AT JETBLUE?

In buying Spirit, we’re acquiring an asset—one that has planes, a network and technology, just to mention a few. It’s an asset that a bank can confidently loan us money for, because the bank knows it will eventually improve our value.

Could we borrow money for other investments at JetBlue? It depends. Typically, companies take on debt to finance capital expenditures (such as equipment purchases) and, as we’re doing, to acquire other companies. If the investment adds value to JetBlue, a bank is much more likely to back it with a loan.

Want to read more of Ursula’s explanation of how we’re able to pay for Spirit? Click here.

| 5. | The following is an investor presentation published by JetBlue on the Investor Relations page of JetBlue’s website (accessible at https://blueir.investproductions.com/investor-relations) and on www.LowFaresGreatService.com on July 28, 2022: |

Bringing Low Fares and Great Service to More Customers A JetBlue and Spirit Combination Will Provide a Compelling Alternative to the ‘Big Four’ Carriers

Important Information for Investors and Stockholders Forward Looking Statements Certain statements in this communication, including statements concerning JetBlue, Spirit, the proposed transaction and other matters, contain various forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, which represent JetBlue management’s beliefs and assumptions concerning future events. These statements are intended to qualify for the “safe harbor” from liability established by the Private Securities Litigation Reform Act of 1995. When used in the communication, the words “expects,” “plans,” “intends,” “anticipates,” “indicates,” “remains,” “believes,” “estimates,” “forecast,” “guidance,” “outlook,” “may,” “will,” “should,” “seeks,” “goals,” “targets” and similar expressions are intended to identify forward-looking statements. Additionally, forward-looking statements include statements that do not relate solely to historical facts, such as statements which identify uncertainties or trends, discuss the possible future effects of current known trends or uncertainties, or which indicate that the future effects of known trends or uncertainties cannot be predicted, guaranteed, or assured. Forward-looking statements involve risks, uncertainties and assumptions, and are based on information currently available to JetBlue and Spirit. Actual results may differ materially from those expressed in the forward-looking statements due to many factors, including, without limitation, those listed in JetBlue’s and Spirit’s U.S. Securities and Exchange Commission (“SEC”) filings, matters of which JetBlue or Spirit may not be aware, the coronavirus pandemic including new and existing variants, the outbreak of any other disease or similar public health threat that affects travel demand or behavior, the occurrence of any event, change or other circumstances that could give rise to the right of JetBlue or Spirit or both of them to terminate the merger agreement; failure to obtain applicable regulatory or Spirit stockholder approval in a timely manner or otherwise and the potential financial consequences thereof; failure to satisfy other closing conditions to the proposed transactions; failure of the parties to consummate the proposed transaction; JetBlue’s ability to finance the proposed transaction and the indebtedness JetBlue expects to incur in connection with the proposed transaction; the possibility that JetBlue may be unable to achieve expected synergies and operating efficiencies within the expected timeframes or at all and to successfully integrate Spirit’s operations with those of JetBlue, and the possibility that such integration may be more difficult, time-consuming or costly than expected or that operating costs and business disruption (including, without limitation, disruptions in relationships with employees, customers or suppliers) may be greater than expected in connection with the proposed transaction; failure to realize anticipated benefits of the combined operations; demand for the combined company’s services; the growth, change and competitive landscape of the markets in which the combined company participates; expected seasonality trends; diversion of managements’ attention from ongoing business operations and opportunities; potential adverse reactions or changes to business or employee relationships, including those resulting from the announcement or completion of the transaction; risks related to investor and rating agency perceptions of each of the parties and their respective business, operations, financial condition and the industry in which they operate; risks related to the potential impact of general economic, political and market factors on the companies or the proposed transaction; ongoing and increase in costs related to IT network security. Given the risks and uncertainties surrounding forward-looking statements, you should not place undue reliance on these statements. Further information concerning these and other factors is contained in JetBlue’s and Spirit’s SEC filings, including but not limited to, JetBlue’s and Spirit’s 2021 Annual Reports on Form 10-K and their Quarterly Reports on Form 10-Q. In light of these risks and uncertainties, the forward-looking events discussed in this communication might not occur. JetBlue’s and Spirit’s forward-looking statements included in this communication speak only as of the date the statements were written or recorded. JetBlue and Spirit undertake no obligation to update or revise forward-looking statements, whether as a result of new information, future events, changed circumstances, or otherwise. Additional Important Information and Where to Find It This communication is being made in respect to the proposed transaction involving JetBlue, Sundown Acquisition Corp., and Spirit. A meeting of the stockholders of Spirit will be announced as promptly as practicable to seek stockholder approval in connection with the proposed transaction. Spirit expects to file with the SEC a proxy statement and other relevant documents in connection with the proposed transaction. The definitive proxy statement will be sent or given to the stockholders of Spirit and will contain important information about the proposed transaction and related matters. STOCKHOLDERS ARE URGED TO READ THE PROXY STATEMENT (INCLUDING ANY AMENDMENTS OR SUPPLEMENTS THERETO) AND ALL OTHER RELEVANT DOCUMENTS FILED WITH THE SEC IN THEIR ENTIRETY CAREFULLY WHEN THEY BECOME AVAILABLE, INCLUDING ALL PROXY MATERIALS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Any definitive proxy statement (if and when available) will be mailed to stockholders of Spirit. Investors and stockholders may obtain a free copy of any proxy statement and (when available) other documents filed by JetBlue and Spirit at the SEC’s web site at https://www.sec.gov. In addition, investors and stockholders will be able to obtain free copies of any proxy statement (when available) and other documents filed by JetBlue and Spirit with the SEC on JetBlue’s Investor Relations website at http://investor.jetblue.com and on Spirit’s Investor Relations website at https://ir.spirit.com. Participants in the Solicitation JetBlue and Spirit, and certain of their respective directors and executive officers, may be deemed to be participants in the solicitation of proxies from the holders of Spirit common stock. Information regarding JetBlue’s directors and executive officers is contained in JetBlue’s Definitive Proxy Statement for its 2022 Annual Meeting of Stockholders filed with the SEC on April 7, 2022, and in JetBlue’s Annual Report on Form 10-K for the fiscal year ended December 31, 2021, filed with the SEC on February 22, 2022. Information regarding Spirit’s directors and executive officers is contained in Spirit’s Definitive Proxy Statement for its 2022 Annual Meeting of Stockholders filed with the SEC on March 30, 2022. Investors may obtain additional information regarding the interests of such participants by reading the proxy statement and other relevant materials regarding the proposed transaction when they become available. These documents can be obtained free of charge as described in the preceding paragraph. No Offer Or Solicitation This communication shall not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction.

Strategic Rationale and Financial Impact

Will Create Long-Term Value for All Stakeholders Will Provide Significant Value for JetBlue and Spirit Shareholders Exhibits Strong Strategic Rationale Will Create a Compelling National Low-fare Challenger Will Accelerate Existing Growth Plan while Complementing JetBlue’s Northeast Alliance (NEA) Strategy Will Significantly Enhance JetBlue’s Long-term Financial Returns

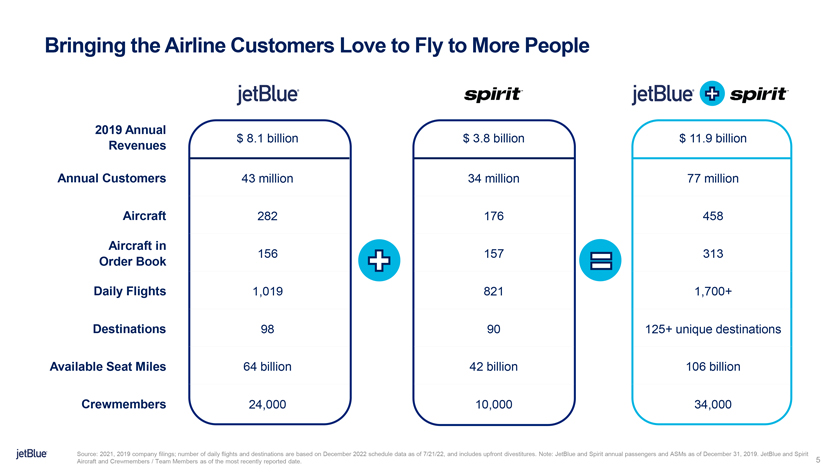

Bringing the Airline Customers Love to Fly to More People 2019 Annual $ 8.1 billion $ 3.8 billion $ 11.9 billion Revenues Annual Customers 43 million 34 million 77 million Aircraft 282 176 458 Aircraft in 156 157 313 Order Book v v v Daily Flights 1,019 821 1,700+ Destinations 98 90 125+ unique destinations Available Seat Miles 64 billion 42 billion 106 billion Crewmembers 24,000 10,000 34,000 Source: 2021, 2019 company filings; number of daily flights and destinations are based on December 2022 schedule data as of 7/21/22, and includes upfront divestitures. Note: JetBlue and Spirit annual passengers and ASMs as of December 31, 2019. JetBlue and Spirit Aircraft and Crewmembers / Team Members as of the most recently reported date.

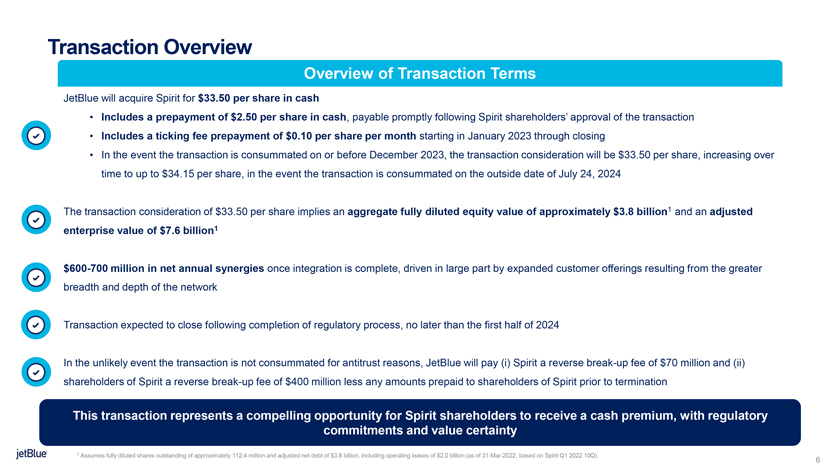

Transaction Overview Overview of Transaction Terms JetBlue will acquire Spirit for $33.50 per share in cash • Includes a prepayment of $2.50 per share in cash, payable promptly following Spirit shareholders’ approval of the transaction • Includes a ticking fee prepayment of $0.10 per share per month starting in January 2023 through closing • In the event the transaction is consummated on or before December 2023, the transaction consideration will be $33.50 per share, increasing over time to up to $34.15 per share, in the event the transaction is consummated on the outside date of July 24, 2024 The transaction consideration of $33.50 per share implies an aggregate fully diluted equity value of approximately $3.8 billion1 and an adjusted enterprise value of $7.6 billion1 $600-700 million in net annual synergies once integration is complete, driven in large part by expanded customer offerings resulting from the greater breadth and depth of the network Transaction expected to close following completion of regulatory process, no later than the first half of 2024 In the unlikely event the transaction is not consummated for antitrust reasons, JetBlue will pay (i) Spirit a reverse break-up fee of $70 million and (ii) shareholders of Spirit a reverse break-up fee of $400 million less any amounts prepaid to shareholders of Spirit prior to termination This transaction represents a compelling opportunity for Spirit shareholders to receive a cash premium, with regulatory commitments and value certainty 1 Assumes fully diluted shares outstanding of approximately 112.4 million and adjusted net debt of $3.8 billion, including operating leases of $2.0 billion (as of 31-Mar-2022, based on Spirit Q1 2022 10Q). 6

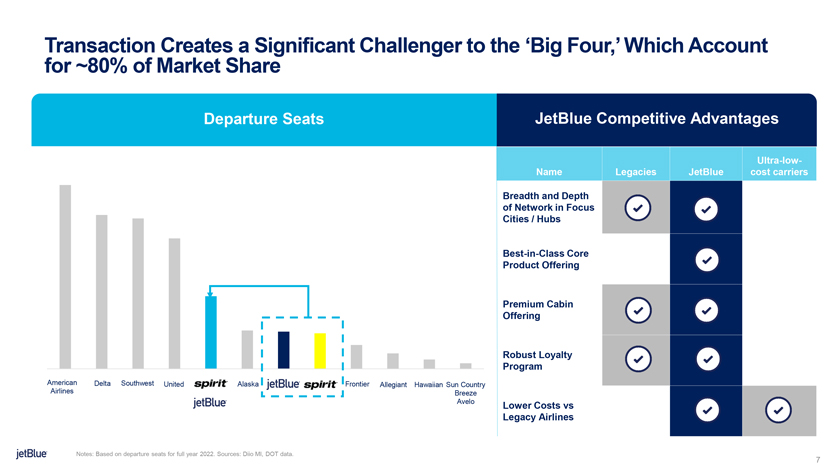

Transaction Creates a Significant Challenger to the ‘Big Four,’ Which Account for ~80% of Market Share Departure Seats JetBlue Competitive Advantages Ultra-low-Name Legacies JetBlue cost carriers Breadth and Depth of Network in Focus Cities / Hubs Best-in-Class Core Product Offering Premium Cabin Offering Robust Loyalty Program American Delta Southwest United Alaska Frontier Allegiant Hawaiian Sun Country Airlines Breeze Avelo Lower Costs vs Legacy Airlines Notes: Based on departure seats for full year 2022. Sources: Diio MI, DOT data. 7

Spirit Assets Will Enhance JetBlue’s Relevance in Legacy Hubs, Bringing the JetBlue Effect to Significantly More Customers Paying High Fares JetBlue’s contemplated combined network plan includes: • ~140 new domestic non-stop routes, bringing more than $500 million of annual consumer savings to customers on those routes via the JetBlue Effect • Enhances JetBlue’s unique ability to drive market relevance in key legacy hubs like South Florida and Los Angeles • Strong divestiture commitment to provide ULCC(s) access to Spirit’s NYC and Boston infrastructure and Fort Lauderdale growth • A unique product offering aimed at serving a wider array of customer demographics (e.g., leisure, VFR, premium, small and large businesses, etc.) Note: Based on average departures/day per respective schedule for December 2022 for JetBlue and Spirit. Includes upfront divestitures. Sources: Diio MI, DOT data. 8

Bringing Award-Winning Service and Lower Fares to More Customers Enhancing a unique customer offering • More customers get low fares and award-winning service across more destinations • JetBlue has won hundreds of awards since its inception – and continues to do so o Top publications and readers’ choice surveys including best domestic U.S. airline • Increase in flight schedules to a combined 127 destinations to / from some of the largest U.S. cities Magnifying the “JetBlue Effect” • Increased scale will drive heightened competition with legacy carriers, resulting in lower fares for more customers and communities o “JetBlue Effect” leads to lower legacy fares on routes JetBlue enters • Combination would introduce JetBlue for the first time to new destinations, including St. Louis, Memphis, Louisville, Atlantic City, Myrtle Beach, and four additional destinations in Colombia • Even more airport access in valuable cities such as Los Angeles, Las Vegas, Chicago, Detroit, and Atlanta where further JetBlue growth would benefit travelers 9

Significant Benefits to Spirit Team Members and JetBlue Crewmembers Greater career opportunities for Team Members and Crewmembers Commitment to maintain Fort Lauderdale support center 24-month job / income commitment to all Spirit Team Members, measured from signing of merger agreement Strong combined team with complementary expertise Leverage best practices and learnings from both companies to enhance our culture

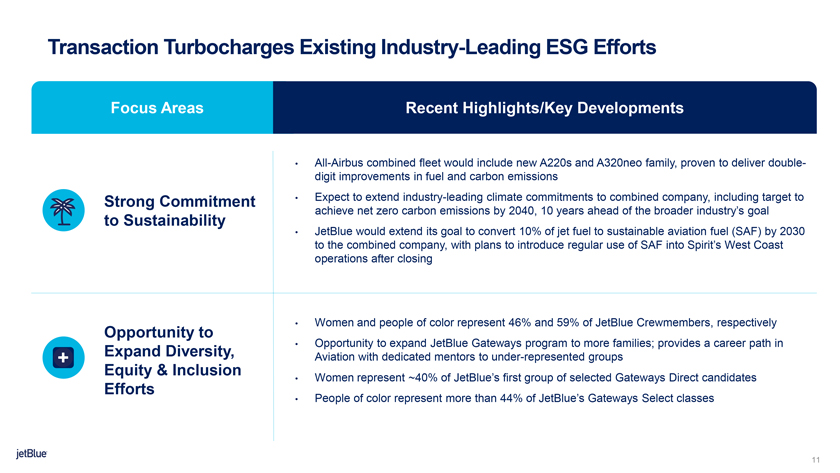

Transaction Turbocharges Existing Industry-Leading ESG Efforts Focus Areas Recent Highlights/Key Developments • All-Airbus combined fleet would include new A220s and A320neo family, proven to deliver double-digit improvements in fuel and carbon emissions Strong Commitment • Expect to extend industry-leading climate commitments to combined company, including target to achieve net zero carbon emissions by 2040, 10 years ahead of the broader industry’s goal to Sustainability • JetBlue would extend its goal to convert 10% of jet fuel to sustainable aviation fuel (SAF) by 2030 to the combined company, with plans to introduce regular use of SAF into Spirit’s West Coast operations after closing • Women and people of color represent 46% and 59% of JetBlue Crewmembers, respectively Opportunity to Expand Diversity, • Opportunity to expand JetBlue Gateways program to more families; provides a career path in Aviation with dedicated mentors to under-represented groups Equity & Inclusion • Women represent ~40% of JetBlue’s first group of selected Gateways Direct candidates Efforts • People of color represent more than 44% of JetBlue’s Gateways Select classes

Platform for Efficient and Sustainable Growth Built on a Common Airbus Family Fleet The combined order book will create natural synergies, with the potential to double current JetBlue growth rate • Provides platform for growth when OEM order books allow limited options • Retain significant flexibility to adjust growth via: o Accelerating retirement of existing E190 and A320ceo fleet o Exercising options to increase A220 and A320neo deliveries JetBlue Pre-Transaction Net Fleet Count Post-Transaction Net Fleet Count 675 A320 family A220 E190 A320 family A220 E190 100 +7% CAGR 455 60 346 8 +3% CAGR 282 100 575 60 8 387 214 246 2021 2027 2021 2027 Source: Latest company filings, investor presentations. Note: Does not include any anticipated retirements / lease returns for Spirit. 12

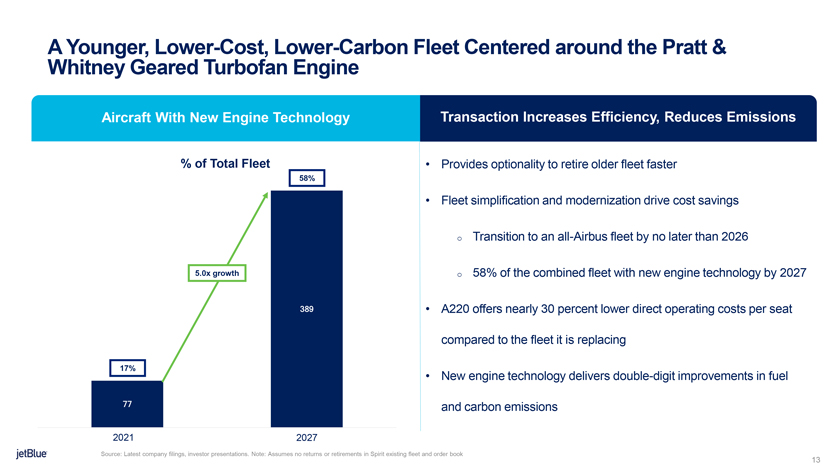

A Younger, Lower-Cost, Lower-Carbon Fleet Centered around the Pratt & Whitney Geared Turbofan Engine Aircraft With New Engine Technology Transaction Increases Efficiency, Reduces Emissions % of Total Fleet • Provides optionality to retire older fleet faster 58% • Fleet simplification and modernization drive cost savings o Transition to an all-Airbus fleet by no later than 2026 5.0x growth o 58% of the combined fleet with new engine technology by 2027 389 • A220 offers nearly 30 percent lower direct operating costs per seat compared to the fleet it is replacing 17% • New engine technology delivers double-digit improvements in fuel 77 and carbon emissions 2021 2027 Source: Latest company filings, investor presentations. Note: Assumes no returns or retirements in Spirit existing fleet and order book 13

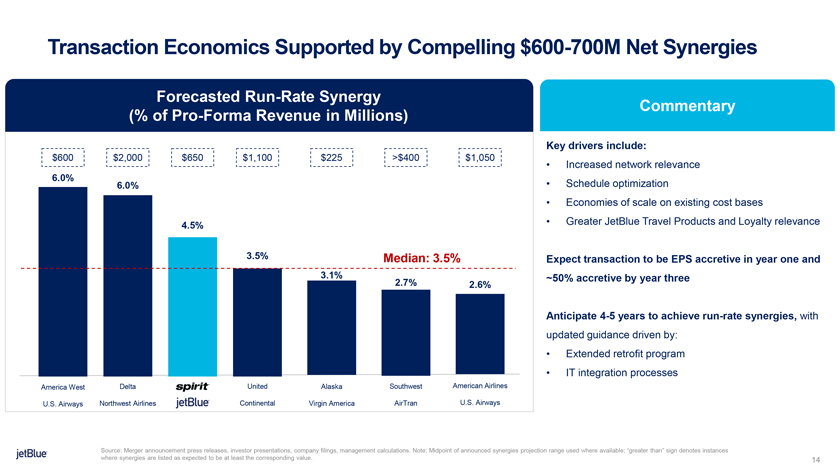

Transaction Economics Supported by Compelling $600-700M Net Synergies Forecasted Run-Rate Synergy Commentary (% of Pro-Forma Revenue in Millions) Key drivers include: $600 $2,000 $650 $1,100 $225 >$400 $1,050 • Increased network relevance 6.0% • Schedule optimization 6.0% • Economies of scale on existing cost bases 4.5% • Greater JetBlue Travel Products and Loyalty relevance 3.5% Median: 3.5% Expect transaction to be EPS accretive in year one and 3.1% ~50% accretive by year three 2.7% 2.6% Anticipate 4-5 years to achieve run-rate synergies, with updated guidance driven by: • Extended retrofit program • IT integration processes America West Delta United Alaska Southwest American Airlines U.S. Airways Northwest Airlines Continental Virgin America AirTran U.S. Airways Source: Merger announcement press releases, investor presentations, company filings, management calculations. Note: Midpoint of announced synergies projection range used where available; “greater than” sign denotes instances where synergies are listed as expected to be at least the corresponding value. 14

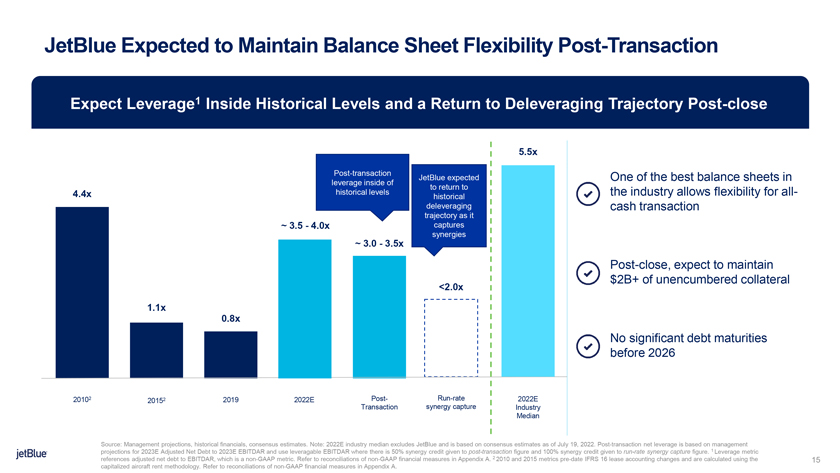

JetBlue Expected to Maintain Balance Sheet Flexibility Post-Transaction Expect Leverage1 Inside Historical Levels and a Return to Deleveraging Trajectory Post-close 5.5x Post-transaction JetBlue expected One of the best balance sheets in leverage inside of to return to 4.4x historical levels he industry allows flexibility for all- historical deleveraging ash transaction trajectory as it ~ 3.5—4.0x captures synergies ~ 3.0—3.5x Post-close, expect to maintain 2B+ of unencumbered collateral <2.0x 1.1x 0.8x No significant debt maturities efore 2026 20102 20152 2019 2022E Post- Run-rate 2022E Transaction synergy capture Industry Median Source: Management projections, historical financials, consensus estimates. Note: 2022E industry median excludes JetBlue and is based on consensus estimates as of July 19, 2022. Post-transaction net leverage is based on management projections for 2023E Adjusted Net Debt to 2023E EBITDAR and use leveragable EBITDAR where there is 50% synergy credit given to post-transaction figure and 100% synergy credit given to run-rate synergy capture figure. 1 Leverage metric references adjusted net debt to EBITDAR, which is a non-GAAP metric. Refer to reconciliations of non-GAAP financial measures in Appendix A. 2 2010 and 2015 metrics pre-date IFRS 16 lease accounting changes and are calculated using the 15 capitalized aircraft rent methodology. Refer to reconciliations of non-GAAP financial measures in Appendix A.

Conviction in Regulatory Approval

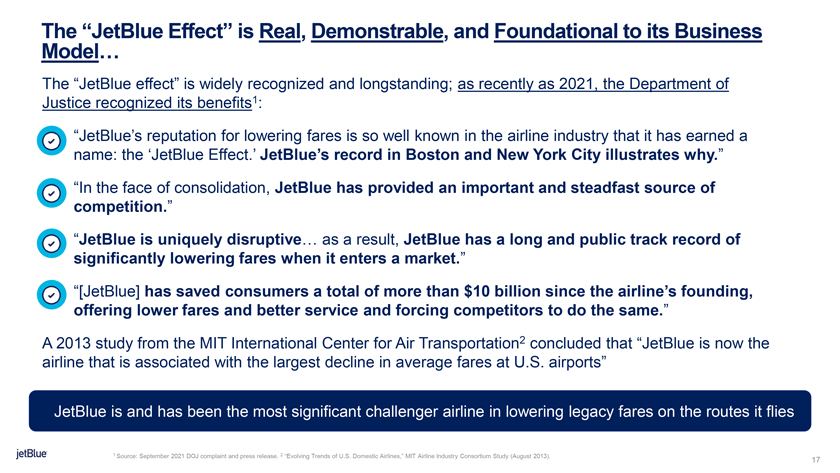

The “JetBlue Effect” is Real, Demonstrable, and Foundational to its Business Model… The “JetBlue effect” is widely recognized and longstanding; as recently as 2021, the Department of Justice recognized its benefits1: “JetBlue’s reputation for lowering fares is so well known in the airline industry that it has earned a name: the ‘JetBlue Effect.’ JetBlue’s record in Boston and New York City illustrates why.” “In the face of consolidation, JetBlue has provided an important and steadfast source of competition.” “JetBlue is uniquely disruptive… as a result, JetBlue has a long and public track record of significantly lowering fares when it enters a market.” “[JetBlue] has saved consumers a total of more than $10 billion since the airline’s founding, offering lower fares and better service and forcing competitors to do the same.” A 2013 study from the MIT International Center for Air Transportation2 concluded that “JetBlue is now the airline that is associated with the largest decline in average fares at U.S. airports” JetBlue is and has been the most significant challenger airline in lowering legacy fares on the routes it flies 1 Source: September 2021 DOJ complaint and press release. 2 “Evolving Trends of U.S. Domestic Airlines,” MIT Airline Industry Consortium Study (August 2013).

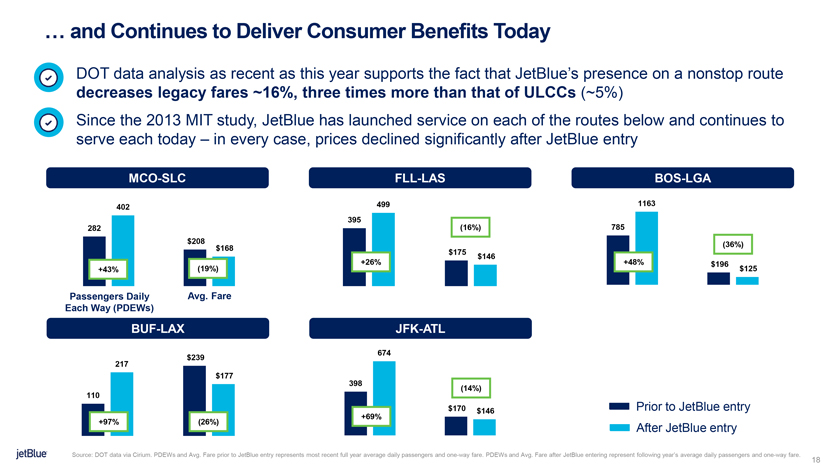

… and Continues to Deliver Consumer Benefits Today DOT data analysis as recent as this year supports the fact that JetBlue’s presence on a nonstop route decreases legacy fares ~16%, three times more than that of ULCCs (~5%) Since the 2013 MIT study, JetBlue has launched service on each of the routes below and continues to serve each today – in every case, prices declined significantly after JetBlue entry MCO-SLC FLL-LAS BOS-LGA 402 499 1163 395 282 (16%) 785 $208 (36%) $168 $175 $146 +26% +48% $196 +43% (19%) $125 Passengers Daily Avg. Fare Each Way (PDEWs) BUF-LAX JFK-ATL 674 $239 217 $177 398 (14%) 110 Prior to JetBlue entry +69% $170 $146 +97% (26%) After JetBlue entry Source: DOT data via Cirium. PDEWs and Avg. Fare prior to JetBlue entry represents most recent full year average daily passengers and one-way fare. PDEWs and Avg. Fare after JetBlue entering represent following year’s average daily passengers and one-way fare. 18

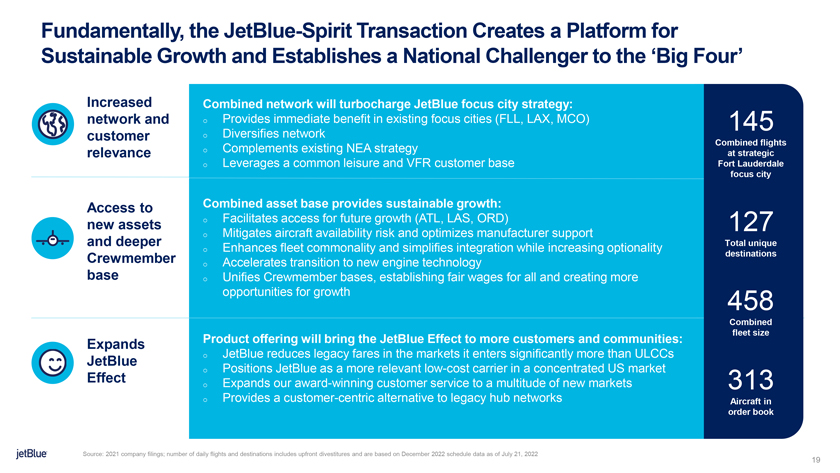

Fundamentally, the JetBlue-Spirit Transaction Creates a Platform for Sustainable Growth and Establishes a National Challenger to the ‘Big Four’ Increased Combined network will turbocharge JetBlue focus city strategy: network and o Provides immediate benefit in existing focus cities (FLL, LAX, MCO) 145 customer o Diversifies network NEA Combined flights relevance o Complements existing strategy at strategic o Leverages a common leisure and VFR customer base Fort Lauderdale focus city Access to Combined asset base provides sustainable growth: new assets o Facilitates access for future growth (ATL, LAS, ORD) 127 o Mitigates aircraft availability risk and optimizes manufacturer support Total unique and deeper Enhances fleet commonality and o simplifies integration while increasing optionality destinations Crewmember o Accelerates transition to new engine technology base o Unifies Crewmember bases, establishing fair wages for all and creating more opportunities for growth 458 Combined Product offering will bring the JetBlue Effect to more customers and communities: fleet size Expands JetBlue o JetBlue reduces legacy fares in the markets it enters significantly more than ULCCs o Positions JetBlue as a more relevant low-cost carrier in a concentrated US market Effect to a multitude of new markets o Expands our award-winning customer service 313 o Provides a customer-centric alternative to legacy hub networks Aircraft in order book Source: 2021 company filings; number of daily flights and destinations includes upfront divestitures and are based on December 2022 schedule data as of July 21, 2022 19

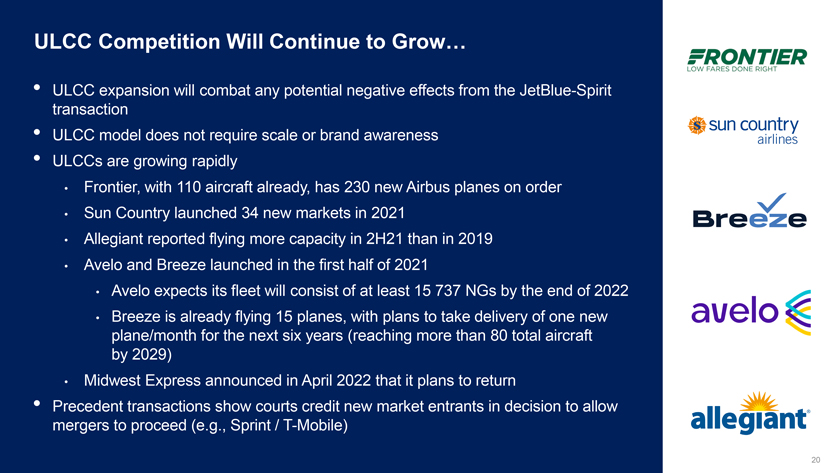

ULCC Competition Will Continue to Grow… • ULCC expansion will combat any potential negative effects from the JetBlue-Spirit transaction • ULCC model does not require scale or brand awareness • ULCCs are growing rapidly • Frontier, with 110 aircraft already, has 230 new Airbus planes on order • Sun Country launched 34 new markets in 2021 • Allegiant reported flying more capacity in 2H21 than in 2019 • Avelo and Breeze launched in the first half of 2021 • Avelo expects its fleet will consist of at least 15 737 NGs by the end of 2022 • Breeze is already flying 15 planes, with plans to take delivery of one new plane/month for the next six years (reaching more than 80 total aircraft by 2029) • Midwest Express announced in April 2022 that it plans to return • Precedent transactions show courts credit new market entrants in decision to allow mergers to proceed (e.g., Sprint / T-Mobile) 20

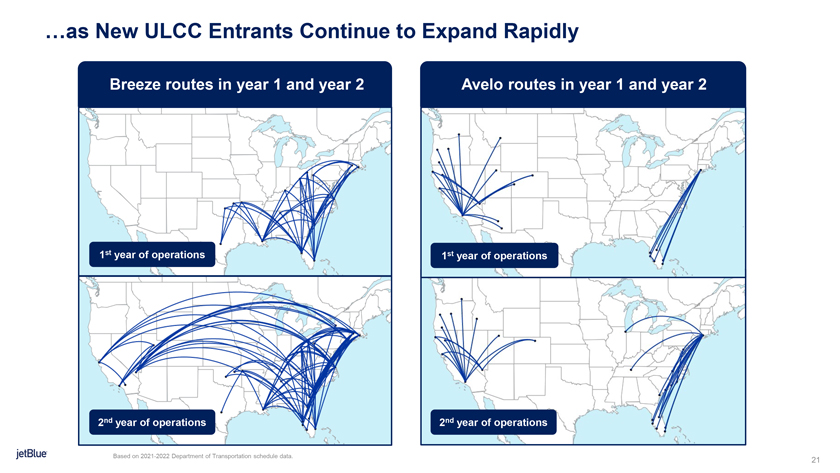

…as New ULCC Entrants Continue to Expand Rapidly Breeze routes in year 1 and year 2 Avelo routes in year 1 and year 2 1st year of operations 1st year of operations 2nd year of operations 2nd year of operations Based on 2021-2022 Department of Transportation schedule data.

Summary and Preliminary Transaction Timeline

Transaction Will Create a Compelling National Low-fare Challenger, Benefitting All Stakeholders Will accelerate JetBlue’s strategic plan, creating more value for all stakeholders of combined airline Combined airline would fly under the JetBlue brand, bringing its unique combination of lower fares and great experience to more customers Will provide combined Crewmember base enhanced career opportunities Pro-competitive combination as “JetBlue Effect” is more effective in lowering legacy fares

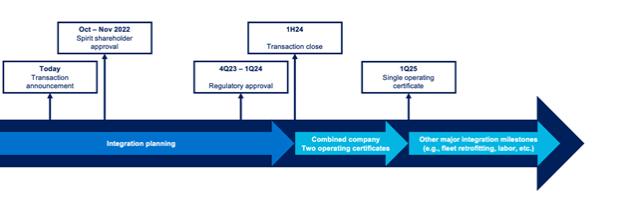

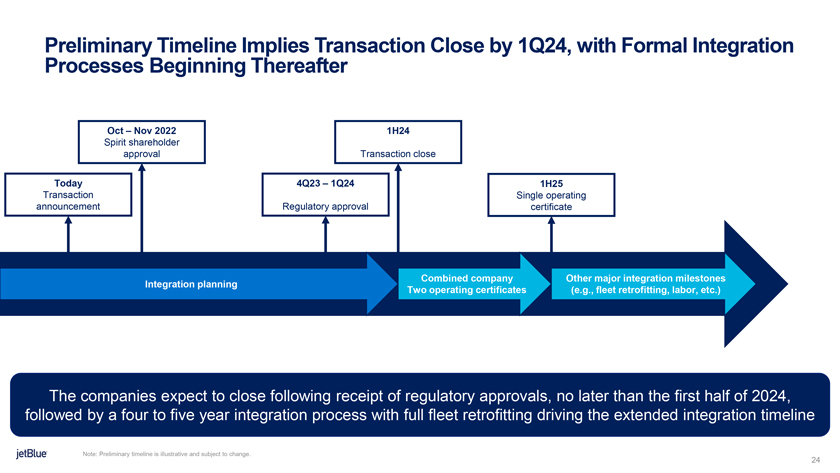

Preliminary Timeline Implies Transaction Close by 1Q24, with Formal Integration Processes Beginning Thereafter Oct – Nov 2022 1H24 Spirit shareholder approval Transaction close Today 4Q23 – 1Q24 1H25 Transaction Single operating announcement Regulatory approval certificate Combined company Other major integration milestones Integration planning Two operating certificates (e.g., fleet retrofitting, labor, etc.) The companies expect to close following receipt of regulatory approvals, no later than the first half of 2024, followed by a four to five year integration process with full fleet retrofitting driving the extended integration timeline Note: Preliminary timeline is illustrative and subject to change.

Appendix

Appendix A Non-GAAP Financial Measures JetBlue presents the ratio of Adjusted Net Debt to EBITDAR, which is a non-GAAP financial measures, in this presentation. This non-GAAP financial measure, and the non-GAAP financial measures used to calculate it, are derived from our consolidated financial statements, but are not presented in accordance with generally accepted accounting principles in the United States, or GAAP. The most comparable GAAP measure is total debt to net income (loss). We believe these non-GAAP financial measures provide a meaningful comparison of our results to others in the airline industry and our prior year results. Investors should consider these non-GAAP financial measures in addition to, and not as a substitute for, our financial performance measures prepared in accordance with GAAP. Further, our non-GAAP information may be different from the non-GAAP information provided by other companies. In the following pages, we provide an explanation of each non-GAAP financial measure and provide a reconciliation of non-GAAP financial measures used in this presentation to the most directly comparable GAAP financial measures. Please note that we present an estimated ratio of Adjusted Net Debt to EBITDAR on a prospective basis. We are not able to provide, without unreasonable effort, a reconciliation of these estimated non-GAAP financial measures to the most directly comparable GAAP measure because we do not currently have sufficient data to accurately estimate the individual adjustments included in the most directly comparable GAAP measure that would be necessary for such reconciliations. As these adjustments are inherently variable and uncertain and depend on various factors that are beyond our control, we are also unable to predict their probable significance.

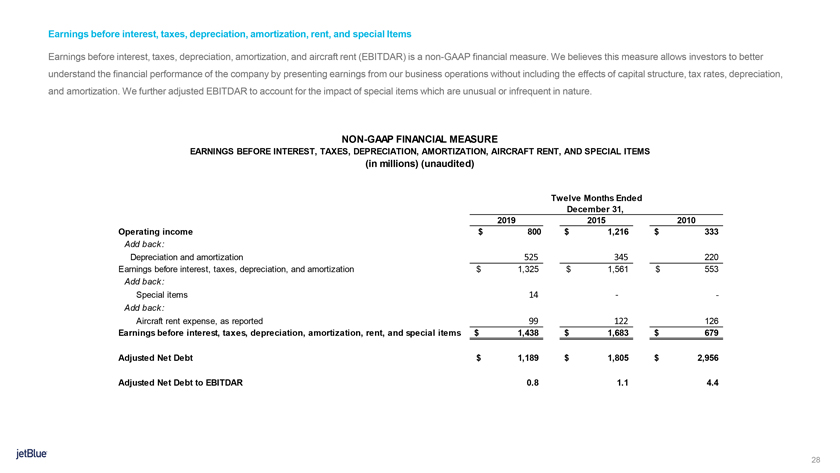

Adjusted Net Debt Adjusted net debt is a non-GAAP financial measure which we believe is helpful to investors in assessing our overall debt profile. We reduce our adjusted debt by cash, cash equivalents, and short-term investments resulting in adjusted net debt, to present the amount of assets needed to satisfy our debt obligations. NON-GAAP FINANCIAL MEASURE ADJUSTED NET DEBT (in millions) (unaudited) December 31, 2015 December 31, 2010 Long-term debt and finance leases $ 1,379 $ 2,850 Current maturities of long-term debt and finance leases 448 183 Capitalized aircraft rent (7 * aircraft rent) 854 883 Adjusted Debt $ 2,681 $ 3,916 Cash and cash equivalents $ 318 $ 465 Short-term investments 558 495 Total Liquidity $ 876 $ 960 Adjusted Net Debt $ 1,805 $ 2,956 December 31, 2019 Long-term debt and finance leases $ 1,990 Current maturities of long-term debt and finance leases 344 Operating lease liabilities—aircraft 183 Adjusted debt $ 2,517 Cash and Cash Equivalents $ 959 STI + LTMS 369 Total Liquidity $ 1,328 Adjusted net debt $ 1,189

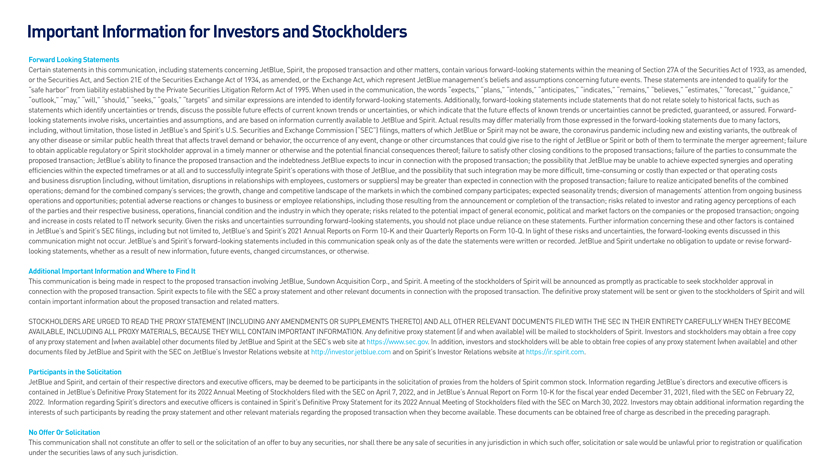

Earnings before interest, taxes, depreciation, amortization, rent, and special Items Earnings before interest, taxes, depreciation, amortization, and aircraft rent (EBITDAR) is a non-GAAP financial measure. We believes this measure allows investors to better understand the financial performance of the company by presenting earnings from our business operations without including the effects of capital structure, tax rates, depreciation, and amortization. We further adjusted EBITDAR to account for the impact of special items which are unusual or infrequent in nature. NON-GAAP FINANCIAL MEASURE EARNINGS BEFORE INTEREST, TAXES, DEPRECIATION, AMORTIZATION, AIRCRAFT RENT, AND SPECIAL ITEMS (in millions) (unaudited) Twelve Months Ended December 31, 2019 2015 2010 Operating income $ 800 $ 1,216 $ 333 Add back: Depreciation and amortization 525 345 220 Earnings before interest, taxes, depreciation, and amortization $ 1,325 $ 1,561 $ 553 Add back: Special items 14 — Add back: Aircraft rent expense, as reported 99 122 126 Earnings before interest, taxes, depreciation, amortization, rent, and special items $ 1,438 $ 1,683 $ 679 Adjusted Net Debt $ 1,189 $ 1,805 $ 2,956 Adjusted Net Debt to EBITDAR 0.8 1.1 4.4

| 6. | The following are posts made by JetBlue to various social media platforms on July 28, 2022: |

JetBlue Homepage

Taking off together.

We’re proud to announce JetBlue & Spirit Airlines will come together to create a bigger, better JetBlue. After closing, the combined network will offer 1700+ daily flights to 125+ destinations—and the low fares and award-winning service you know and love.

Learn more >

We’re proud to announce @JetBlue & @SpiritAirlines will come together to create a bigger, better JetBlue. After closing, the combined network will offer 1700+ daily flights to 125+ destinations—and the low fares and award-winning service you know and love. Learn more at www.lowfaresgreatservice.com

We’re proud to announce @JetBlue & @SpiritAirlines will come together to create a bigger, better JetBlue. After closing, the combined network will offer 1700+ daily flights to 125+ destinations—and the low fares and award-winning service you know and love.

Don’t worry–for now we remain two independent airlines, and tickets you’ve purchased on either JetBlue or Spirit, and points or benefits you’ve earned, are still valid.

We still have a lot of work to do before we close and we’re committed to keeping you informed. In the meantime, learn more about what this exciting combination means for you at the link in our bio.

We are proud to announce @JetBlue & [@SpiritAirlines] will come together to create a bigger, better JetBlue. After closing, the combined network will offer 1700+ daily flights to 125+ destinations—and the low fares and award-winning service you know and love.

Don’t worry–for now we remain two independent airlines, and tickets you’ve purchased on either JetBlue or Spirit, and points or benefits you’ve earned, are still valid.

We still have a lot of work to do before we close and we’re committed to keeping you informed. In the meantime, learn more about what this exciting combination means for you at www.lowfaresgreatservice.com.

We are proud to announce @JetBlue & [@SpiritAirlines] will come together to create a bigger, better JetBlue. After closing, the combined network will offer 1700+ daily flights to 125+ destinations—and the low fares and award-winning service you know and love.

Don’t worry–for now we remain two independent airlines, and tickets you’ve purchased on either JetBlue or Spirit, and points or benefits you’ve earned, are still valid.

We still have a lot of work to do below we close and we’re committed to keeping you informed. In the meantime, learn more about what this exciting combination means for you at www.lowfaresgreatservice.com.

| 7. | The following is a “Transaction Fact Sheet” published by JetBlue on www.LowFaresGreatService.com on July 28, 2022: |

An Airline that Customers Will Love to Fly • Brings more customers more choices, without having to choose between a low fare Deal Terms and a great experience • Expands reach of the “JetBlue Effect,” resulting in JetBlue + Spirit: All cash transaction of $33.50 per share in cash, increasing over time up to $34.15, lower fares for more customers and communities depending on timing of closing. • Plans to rebrand and retrofit Spirit’s fleet The National Low-Fare as JetBlue, introducing a superior onboard experience to Spirit customers Challenger to the Headquarters Corporate Identity “Big Four” Airlines Will be based in New York City with Will maintain the much-loved Will Provide More Opportunities and a significant presence in Florida JetBlue brand Benefits to Crewmembers Today, the four largest U.S. carriers • Combined team of 34,000 crewmembers with plans to hire more as the airline grows control more than 80% of the domestic Footprint Fleet • Opportunity to be a part of a company with market, leaving consumers eager for Will increase connectivity and presence Complementary Airbus fleet and a history of leading in customer service and more low-fare alternatives. in all of JetBlue’s focus cities, including order book will simplify integration innovation 140+ daily flights in FLL • Greater career growth opportunities, travel benefits, and ability to make a bigger difference At closing, a combined JetBlue-Spirit in our communities will be the fifth largest domestic airline, bringing JetBlue’s unique combination Will Deliver Superior Value and High of low fares and award-winning Degree of Certainty to All Shareholders customer service to more fliers. • Expected to double annual revenue growth Together, JetBlue and Spirit will have: through the middle of the decade, and improve profitability by approximately 200 basis points • $11.9B annual revenue • Net run rate projected operational synergies of $600-700 million • 77M annual customers • High conviction around likelihood of obtaining • 1,700+ daily flights antitrust approvals and closing the transaction • 127 unique destinations • 458 aircraft, 300+ order book Will Bring Industry-Leading ESG Efforts • 106B available seat miles (ASM) to a Larger Combined Company • Will form one of the youngest and most fuel efficient fleets in the industry • Will expand JetBlue’s goal to achieve net zero jetblue co . m carbon emissions by 2040 – 10 years ahead of the broader industry – including three key targets for 2030 Notes: Based on average departures/day per respective schedules with committed upfront

Important Information for Investors and Stockholders Forward Looking Statements Certain statements in this communication, including statements concerning JetBlue, Spirit, the proposed transaction and other matters, contain various forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, which represent JetBlue management’s beliefs and assumptions concerning future events. These statements are intended to qualify for the “safe harbor” from liability established by the Private Securities Litigation Reform Act of 1995. When used in the communication, the words “expects,” “plans,” “intends,” “anticipates,” “indicates,” “remains,” “believes,” “estimates,” “forecast,” “guidance,” “outlook,” “may,” “will,” “should,” “seeks,” “goals,” “targets” and similar expressions are intended to identify forward-looking statements. Additionally, forward-looking statements include statements that do not relate solely to historical facts, such as statements which identify uncertainties or trends, discuss the possible future effects of current known trends or uncertainties, or which indicate that the future effects of known trends or uncertainties cannot be predicted, guaranteed, or assured. Forward-looking statements involve risks, uncertainties and assumptions, and are based on information currently available to JetBlue and Spirit. Actual results may differ materially from those expressed in the forward-looking statements due to many factors, including, without limitation, those listed in JetBlue’s and Spirit’s U.S. Securities and Exchange Commission (“SEC”) filings, matters of which JetBlue or Spirit may not be aware, the coronavirus pandemic including new and existing variants, the outbreak of any other disease or similar public health threat that affects travel demand or behavior, the occurrence of any event, change or other circumstances that could give rise to the right of JetBlue or Spirit or both of them to terminate the merger agreement; failure to obtain applicable regulatory or Spirit stockholder approval in a timely manner or otherwise and the potential financial consequences thereof; failure to satisfy other closing conditions to the proposed transactions; failure of the parties to consummate the proposed transaction; JetBlue’s ability to finance the proposed transaction and the indebtedness JetBlue expects to incur in connection with the proposed transaction; the possibility that JetBlue may be unable to achieve expected synergies and operating efficiencies within the expected timeframes or at all and to successfully integrate Spirit’s operations with those of JetBlue, and the possibility that such integration may be more difficult, time-consuming or costly than expected or that operating costs and business disruption (including, without limitation, disruptions in relationships with employees, customers or suppliers) may be greater than expected in connection with the proposed transaction; failure to realize anticipated benefits of the combined operations; demand for the combined company’s services; the growth, change and competitive landscape of the markets in which the combined company participates; expected seasonality trends; diversion of managements’ attention from ongoing business operations and opportunities; potential adverse reactions or changes to business or employee relationships, including those resulting from the announcement or completion of the transaction; risks related to investor and rating agency perceptions of each of the parties and their respective business, operations, financial condition and the industry in which they operate; risks related to the potential impact of general economic, political and market factors on the companies or the proposed transaction; ongoing and increase in costs related to IT network security. Given the risks and uncertainties surrounding forward-looking statements, you should not place undue reliance on these statements. Further information concerning these and other factors is contained in JetBlue’s and Spirit’s SEC filings, including but not limited to, JetBlue’s and Spirit’s 2021 Annual Reports on Form 10-K and their Quarterly Reports on Form 10-Q. In light of these risks and uncertainties, the forward-looking events discussed in this communication might not occur. JetBlue’s and Spirit’s forward-looking statements included in this communication speak only as of the date the statements were written or recorded. JetBlue and Spirit undertake no obligation to update or revise forward-looking statements, whether as a result of new information, future events, changed circumstances, or otherwise. Additional Important Information and Where to Find It This communication is being made in respect to the proposed transaction involving JetBlue, Sundown Acquisition Corp., and Spirit. A meeting of the stockholders of Spirit will be announced as promptly as practicable to seek stockholder approval in connection with the proposed transaction. Spirit expects to file with the SEC a proxy statement and other relevant documents in connection with the proposed transaction. The definitive proxy statement will be sent or given to the stockholders of Spirit and will contain important information about the proposed transaction and related matters. STOCKHOLDERS ARE URGED TO READ THE PROXY STATEMENT (INCLUDING ANY AMENDMENTS OR SUPPLEMENTS THERETO) AND ALL OTHER RELEVANT DOCUMENTS FILED WITH THE SEC IN THEIR ENTIRETY CAREFULLY WHEN THEY BECOME AVAILABLE, INCLUDING ALL PROXY MATERIALS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Any definitive proxy statement (if and when available) will be mailed to stockholders of Spirit. Investors and stockholders may obtain a free copy of any proxy statement and (when available) other documents filed by JetBlue and Spirit at the SEC’s web site at https://www.sec.gov. In addition, investors and stockholders will be able to obtain free copies of any proxy statement (when available) and other documents filed by JetBlue and Spirit with the SEC on JetBlue’s Investor Relations website at http://investor.jetblue.com and on Spirit’s Investor Relations website at https://ir.spirit.com. Participants in the Solicitation JetBlue and Spirit, and certain of their respective directors and executive officers, may be deemed to be participants in the solicitation of proxies from the holders of Spirit common stock. Information regarding JetBlue’s directors and executive officers is contained in JetBlue’s Definitive Proxy Statement for its 2022 Annual Meeting of Stockholders filed with the SEC on April 7, 2022, and in JetBlue’s Annual Report on Form 10-K for the fiscal year ended December 31, 2021, filed with the SEC on February 22, 2022. Information regarding Spirit’s directors and executive officers is contained in Spirit’s Definitive Proxy Statement for its 2022 Annual Meeting of Stockholders filed with the SEC on March 30, 2022. Investors may obtain additional information regarding the interests of such participants by reading the proxy statement and other relevant materials regarding the proposed transaction when they become available. These documents can be obtained free of charge as described in the preceding paragraph. No Offer Or Solicitation This communication shall not constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction.

| 8. | The following screenshot images are taken from www.LowFaresGreatService.com on July 28, 2022: |

Forward Looking Statements

Certain statements in this Schedule 14A Information, including statements concerning JetBlue, Spirit, the proposed transaction and other matters, contain various forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or the Exchange Act, which represent JetBlue management’s beliefs and assumptions concerning future events. These statements are intended to qualify for the “safe harbor” from liability established by the Private Securities Litigation Reform Act of 1995. When used in this Schedule 14A Information, the words “expects,” “plans,” “intends,” “anticipates,” “indicates,” “remains,” “believes,” “estimates,” “forecast,” “guidance,” “outlook,” “may,” “will,” “should,” “seeks,” “goals,” “targets” and similar expressions are intended to identify forward-looking statements. Additionally, forward-looking statements include statements that do not relate solely to historical facts, such as statements which identify uncertainties or trends, discuss the possible future effects of current known trends or uncertainties, or which indicate that the future effects of known trends or uncertainties cannot be predicted, guaranteed, or assured. Forward-looking statements involve risks, uncertainties and assumptions, and are based on information currently available to JetBlue and Spirit. Actual results may differ materially from those expressed in the forward-looking statements due to many factors, including, without limitation, those listed in JetBlue’s and Spirit’s U.S. Securities and Exchange Commission (“SEC”) filings, matters of which JetBlue or Spirit may not be aware, the coronavirus pandemic including new and existing variants, the outbreak of any other disease or similar public health threat that affects travel demand or behavior, the occurrence of any event, change or other circumstances that could give rise to the right of JetBlue or Spirit or both of them to terminate the merger agreement; failure to obtain applicable regulatory or Spirit stockholder approval in a timely manner or otherwise and the potential financial consequences thereof; failure to satisfy other closing conditions to the proposed transactions; failure of the parties to consummate the proposed transaction; JetBlue’s ability to finance the proposed transaction and the indebtedness JetBlue expects to incur in connection with the proposed transaction; the possibility that JetBlue may be unable to achieve expected synergies and operating efficiencies within the expected timeframes or at all and to successfully integrate Spirit’s operations with those of JetBlue, and the possibility that such integration may be more difficult, time-consuming or costly than expected or that operating costs and business disruption (including, without limitation, disruptions in relationships with employees, customers or suppliers) may be greater than expected in connection with the proposed transaction; failure to realize anticipated benefits of the combined operations; demand for the combined company’s services; the growth, change and competitive landscape of the markets in which the combined company participates; expected seasonality trends; diversion of managements’ attention from ongoing business operations and opportunities; potential adverse reactions or changes to business or employee relationships, including those resulting from the announcement or completion of the transaction; risks related to investor and rating agency perceptions of each of the parties and their respective business, operations, financial condition and the industry in which they operate; risks related to the potential impact of general economic, political and market factors on the companies or the proposed transaction; ongoing and increase in costs related to IT network security. Given the risks and uncertainties surrounding forward-looking statements, you should not place undue reliance on these statements. Further information concerning these and other factors is contained in JetBlue’s and Spirit’s SEC filings, including but not limited to, JetBlue’s and Spirit’s 2021 Annual Reports on Form 10-K and their Quarterly Reports on Form 10-Q. In light of these risks and uncertainties, the forward-looking events discussed in this Schedule 14A Information might not occur. JetBlue’s and Spirit’s forward-looking statements included in this Schedule 14A Information speak only as of the date the statements were written or recorded. JetBlue and Spirit undertake no obligation to update or revise forward-looking statements, whether as a result of new information, future events, changed circumstances, or otherwise.

Additional Important Information and Where to Find It

This communication is being made in respect to the proposed transaction involving JetBlue, Sundown Acquisition Corp., and Spirit. A meeting of the stockholders of Spirit will be announced as promptly as practicable to seek stockholder approval in connection with the proposed transaction. Spirit expects to file with the SEC a proxy statement and other relevant documents in connection with the proposed transaction. The definitive proxy statement will be sent or given to the stockholders of Spirit and will contain important information about the proposed transaction and related matters.

STOCKHOLDERS ARE URGED TO READ THE PROXY STATEMENT (INCLUDING ANY AMENDMENTS OR SUPPLEMENTS THERETO) AND ALL OTHER RELEVANT DOCUMENTS FILED WITH THE SEC IN THEIR ENTIRETY CAREFULLY WHEN THEY BECOME AVAILABLE, INCLUDING ALL PROXY MATERIALS, BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION. Any definitive proxy statement (if and when available) will be

mailed to stockholders of Spirit. Investors and stockholders may obtain a free copy of any proxy statement and (when available) other documents filed by JetBlue and Spirit at the SEC’s web site at https://www.sec.gov. In addition, investors and stockholders will be able to obtain free copies of any proxy statement (when available) and other documents filed by JetBlue and Spirit with the SEC on JetBlue’s Investor Relations website at http://investor.jetblue.com and on Spirit’s Investor Relations website at https://ir.spirit.com.

Participants in the Solicitation