Public Service Enterprise Group

NJ Utility Shareholder Group Meeting

Hasbrouck Heights, NJ

December 9, 2008

Forward-Looking Statement

Readers are cautioned that statements contained in this presentation about our and our subsidiaries’ future performance, including future

revenues, earnings, strategies, prospects and all other statements that are not purely historical, are forward-looking statements for purposes of the

safe harbor provisions under The Private Securities Litigation Reform Act of 1995. Although we believe that our expectations are based on

reasonable assumptions, we can give no assurance they will be achieved. The results or events predicted in these statements may differ

materially from actual results or events. Factors which could cause results or events to differ from current expectations include, but are not limited

to:

Adverse changes in energy industry, policies and regulation, including market rules that may adversely affect our operating results.

Any inability of our energy transmission and distribution businesses to obtain adequate and timely rate relief and/or regulatory approvals from

federal and/or state regulators.

Changes in federal and/or state environmental regulations that could increase our costs or limit operations of our generating units.

Changes in nuclear regulation and/or developments in the nuclear power industry generally, that could limit operations of our nuclear generating

units.

Actions or activities at one of our nuclear units that might adversely affect our ability to continue to operate that unit or other units at the same site.

Any inability to balance successfully our energy obligations, available supply and trading risks.

Any deterioration in our credit quality.

Availability of capital and credit markets at reasonable pricing terms and ability to meet cash needs.

Any inability to realize anticipated tax benefits or retain tax credits.

Increases in the cost of or interruption in the supply of fuel and other commodities necessary to the operation of our generating units.

Delays or cost escalations in our construction and development activities.

Adverse capital market performance of our decommissioning and defined benefit plan trust funds.

Changes in technology and/or increased customer conservation.

For further information, please refer to our Annual Report on Form 10-K, including Item 1A. Risk Factors, and subsequent reports on Form 10-Q

and Form 8-K filed with the Securities and Exchange Commission. These documents address in further detail our business, industry issues and

other factors that could cause actual results to differ materially from those indicated in this presentation. In addition, any forward-looking

statements included herein represent our estimates only as of today and should not be relied upon as representing our estimates as of any

subsequent date. While we may elect to update forward-looking statements from time to time, we specifically disclaim any obligation to do so,

even if our estimates change, unless otherwise required by applicable securities laws.

2

GAAP Disclaimer

PSEG presents Operating Earnings in addition to its Net Income reported

in accordance with accounting principles generally accepted in the United

States (GAAP). Operating Earnings is a non-GAAP financial measure that

differs from Net Income because it excludes the impact of the sale of

certain non-core domestic and international assets and material

impairments and lease-transaction-related charges. PSEG presents

Operating Earnings because management believes that it is appropriate

for investors to consider results excluding these items in addition to the

results reported in accordance with GAAP. PSEG believes that the non-

GAAP financial measure of Operating Earnings provides a consistent and

comparable measure of performance of its businesses to help

shareholders understand performance trends. This information is

not intended to be viewed as an alternative to GAAP information. The last

slide in this presentation includes a list of items excluded from Net Income

to reconcile to Operating Earnings, with a reference to that slide included

on each of the slides where the non-GAAP information appears.

3

PSEG Strategic Overview

Tom O’Flynn

Executive Vice President and Chief Financial Officer

PSEG’s diverse asset mix, operational excellence and strong

balance sheet …

… position it to provide value and benefit from multiple growth

opportunities.

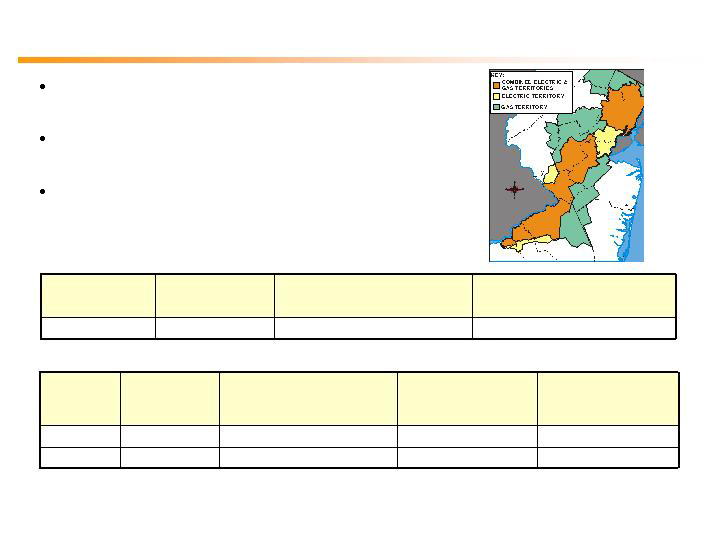

Stable electric and gas

distribution and electric

transmission company

rated top quartile for

reliability, providing

service in mature

service territory in New

Jersey.

Major merchant

generation company with

13,487 MW* of base-

load, intermediate and

load-following capability

operating in attractive

Northeast markets with

operating control of

additional 2,000 MW of

capacity in Texas.

Redeployment of capital

through the sale of

international assets.

Focused on managing

Texas assets, lease

portfolio, modest

domestic PPA capacity

and potential investment

in renewable energy

development.

2007 Operating

Earnings:

$949M**

$115M**

$376M**

2008 Guidance:

$1,010M - $1,110M

$75M – $90M

$350M – $370M

** See page 19 for Items excluded from Net Income to reconcile to Operating Earnings

* Includes recent uprates at Hope Creek (150MW) and Salem 2 (23MW)

5

PSEG is well-positioned …

Regulatory contract for new peaking capacity in CT (in-service date 2012)

Potential to leverage existing brownfield sites

Compressed Air Energy Storage (CAES)

Garden State Offshore Energy exploring development of 350MW offshore wind farm (could be fully operational in 2013)

Capacity

Needs

Significant new transmission capital program to improve reliability

FERC approved request for cost of service formula rates for existing and future transmission investments effective October 1, 2008

Capital investment in coal fleet to meet environmental requirements

maintains critical infrastructure and expands capability

Infrastructure

Requirements

PSEG Power’s base-load nuclear assets well situated in carbon

constrained environment

RGGI auction provides guide for eventual Federal action

NJ releases Energy Master Plan (EMP)

PSE&G pursuing investments in energy efficiency and renewables

Climate

Change

… to capitalize on the challenges of the current business environment.

6

PSEG – 2008 Highlights

$3.35 billion of available liquidity; capital needs funded from internal

cash

Responding to challenging credit markets – capital expenditures for

2009 reduced by $275 - $325 million

Strong balance

sheet

SAESA and Bioenergie sale closed; reserve established for

potential lease liability

Ratings outlook for PSEG, PSE&G, and Holdings moved from

Negative to Stable

Improved risk

profile

NJ releases Energy Master Plan

FERC Transmission rate order effective October 1, 2008

FERC endorses Reliability Pricing Model

RGGI auction in September 2008 – price for carbon at $3.07/ton

Supportive

regulatory

environment

PSE&G honored as America’s Most Reliable Electric Utility

PSEG Power – Nuclear capacity factor at 93% YTD September 30

– Nuclear uprates yield 173MW of new capacity

Strong operating

performance

maintained

Maintaining 2008 guidance of $2.80 - $3.05 per share

Supporting lower half of 2009 earnings of $3.05 - $3.35 per share

Solid earnings

performance

7

Low-cost portfolio

Strong cash generator

Regional focus in competitive,

liquid markets

Assets favorably located

Many units east of PJM constraints

Southern NEPOOL/Connecticut

Near customers/load centers

80% of fossil capacity has dual-fuel

capabilities

Integrated generation and portfolio

management optimizes asset-

based revenues

… with numerous competitive advantages over the long-term.

PSEG Power - right set of assets in right markets …

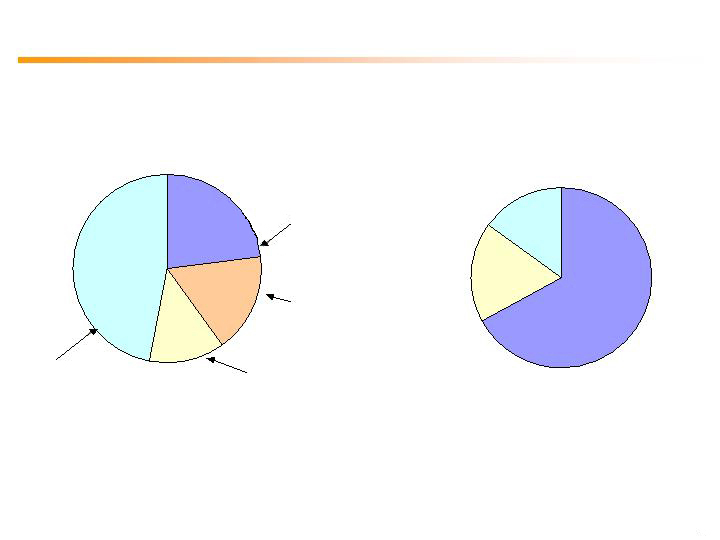

18%

46 %

8 %

27 %

Fuel Diversity – 2008

Coal

Gas

Oil

Nuclear

Pumped

Storage

1%

Energy Produced - 2007

54%

25%

19%

Oil 1%

Pumped

Storage

1%

Nuclear

Coal

Gas

Total GWh: 53,200**

Total MW: 13,487*

* Includes recent uprates at Hope Creek (150MW) and Salem 2 (23MW)

** Excludes 2,000MW of combined cycle generation in Texas under PSEG Power’s operating control.

8

Through its highly skilled workforce and disciplined capital

investments …

2008 National ReliabilityOne Award winner

– Winner in three of the last four years

Solid regulatory relationships on traditional

utility matters

NJ is ranked 2nd nationally in personal

income per capita

(0.2%)

1.6%

Historical Annual

Sales Growth

2003 - 2007

3,397M Therms

44,354 GWh

Electric Sales and Gas Sold

and Transported

LTM 9/30/08

0.2%

1.7 Million

Gas

0.5%

2.1 Million

Electric

Projected Annual

Sales Growth

2008 - 2012

Customers

1.3%

Historical Annual Peak Growth

2003-2007

10,654

Billing Peak (MW)

1,429

Network Circuit

Miles

1.4%*

Projected Annual Peak Growth

2008 - 2012

Electric and Gas Distribution Statistics (9/30/08)

Transmission Statistics (9/30/08)

… PSE&G has become a nationally recognized leader in delivering

safe and reliable service.

* to be updated in December, preliminary estimate of update is ~1.0%

9

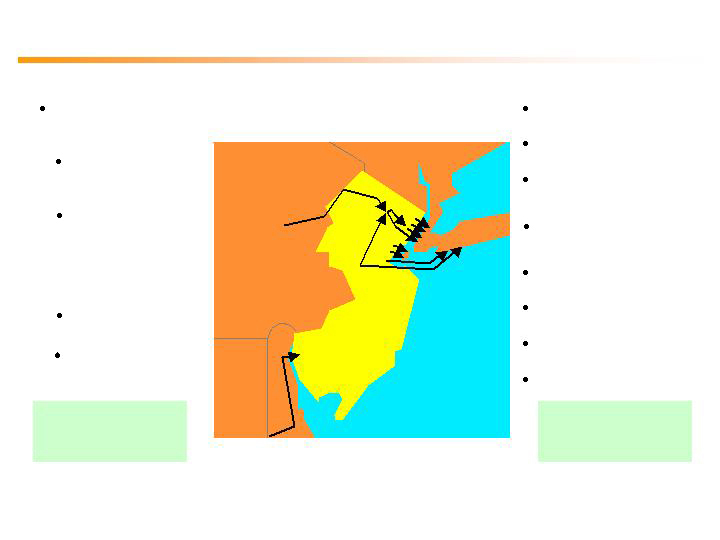

By 2018, NJ’s load is expected to grow by 4,000MW while net import

capability decrease by 1,300MW …

Projects to NY

The Neptune HVDC project (685 MW)

connecting Sayreville to Long Island

The Linden VFT project (330 MW)

connecting Linden to Staten Island

The Bergen O66 project (670 MW)

connecting Bergen to ConEd’s West

49th Street substation

The Bergen Q75 project (1,000 MW)

connecting Bergen to ConEd’s West

49th Street substation

U2-046 project (660MW) originating at

Roseland 500kV

U2-047 project (672) connecting Deans

500kV with Long Island

U2-077 project (300MW) originating at

Linden 230kV

U2-100 project (1,000MW) originating

at Bergen 230kV

Projects to NJ

PSEG’s evaluation of the

proposed backbone

transmission projects:

Northern 500kV route

into Jefferson and

Roseland

Southern 500kV route

into Salem

… indicating the need for additional generation, DSM or transmission

investments.

Total Import

Capability

~ 4,000 MW

Total Export

Capability

~ 5,317 MW

2008-2018 NJ Summer Peak

Annual Growth Rate = 1.8%

Sources: Imports: PSE&G Estimates; Exports: PJM 2008 Regional Transmission Expansion Plan; and Load Growth: PJM 2008 Load Forecast Report

Projects within NJ

Branchburg to

Roseland

Roseland to Hudson

10

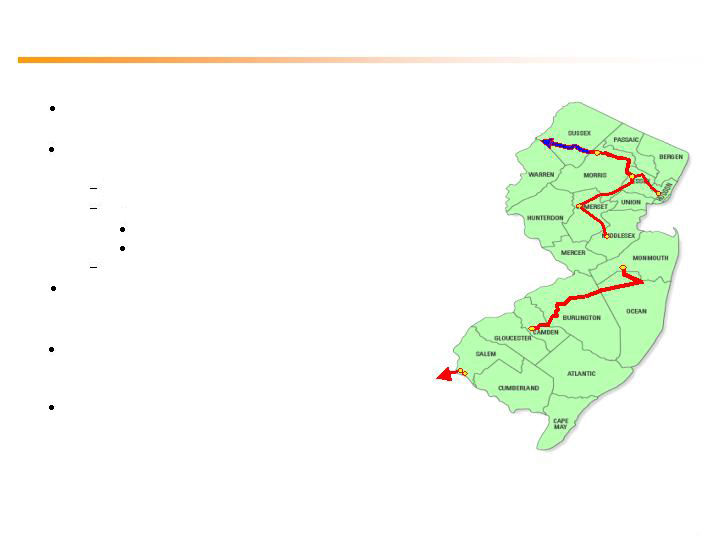

FERC’s recent transmission formula rate order grants an 11.68%

ROE and fully-forecasted cost of service …

… creating an attractive investment environment for PSE&G’s

Transmission Capital Program.

Branchburg

Roseland

Jefferson

New Freedom

Smithburg

Deans

MAPP

Hope Creek

Salem

Project

Transmission Growth

Effective October 1, 2008, PSE&G is operating under

fully forecasted transmission formula rates

PJM approval was received for the Susquehanna to

Roseland line in October 2007

Siting and permitting process underway

FERC approved Incentive rate filing:

125 BPS adder to ROE

100% CWIP in Rate Base

Current cost estimate $750 million

FERC approval of Sub-Transmission to Transmission

system reliability investments represents about $375

million through 2012, post-2012 ~$60 million/year

Other approved RTEP projects ~$250 million also

contribute meaningfully to improved reliability and

earnings growth

Backbone projects are in various stages of

consideration/approval, but present real opportunity to

improve reliability throughout the state, with the

potential investment of ~ $1.5B through 2015

Hudson

11

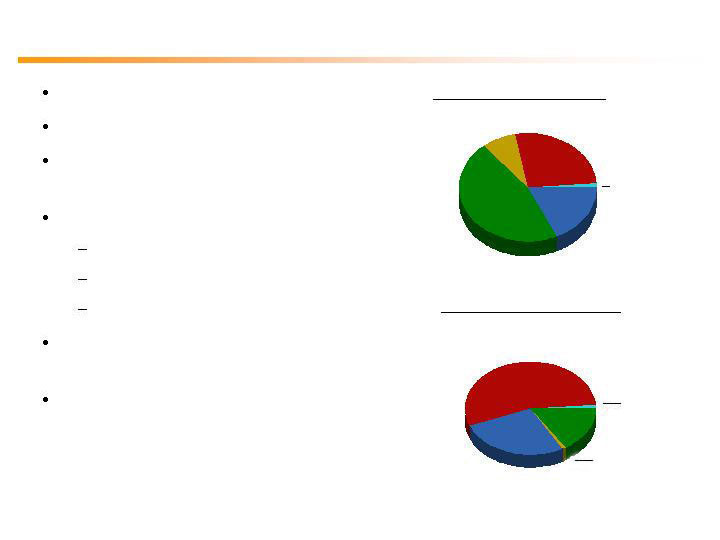

With the sale of international assets, Holdings is now focused …

… on its domestic generation assets, leveraged lease portfolio and

potential renewables development.

PSEG

Resources

47%

Chile & Peru

Distribution

Texas

Merchant

Generation

Other US

Generation

2007 Operating Earnings*

86% of the portfolio is

in energy-related

leveraged leases

2008 Guidance - Operating Earnings

13%

23%

17%

Texas

Merchant

Generation

67%

PSEG

Resources

15%

Other US

Generation

18%

~390MW owned in

CA, HI, NH

fully contracted

$ 115M

$ 75M - $90M

Two companies sold

and SAESA in Disc

Ops. in 2007

Two 1,000 MW CCGTs

1 in Central Texas (South Zone)

1 in West Texas

* See page 19 for Items excluded from Net Income to reconcile to Operating Earnings

12

-40

-20

0

20

40

60

80

2007

2008E

2009E

2010E

2011E

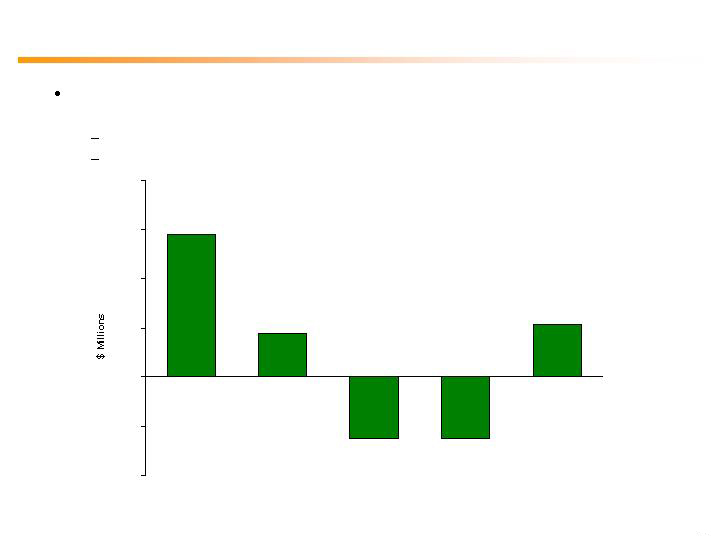

PSEG Resources is managing its current investment portfolio …

… and earnings reflect potential resolution of tax matters.

PSEG Resources - Earnings Profile

Most of exposure related to cross border leases dealt with in 2nd quarter

2008.

$355 million charge to reflect potential changes to timing of tax cash flow.

$135 million increase to interest reserve.

$58

$15 -$20

($20) –

($30)

$15 - $25

(Net Income)

($20) –

($30)

13

2007 Operating Earnings*

2008 Guidance

2009 Guidance

$2.71

$2.80 - $3.05

On track to meet 2008 earnings guidance …

* See page 19 for Items excluded from Net Income to reconcile to Operating Earnings

9 Months YTD

Operating

Earnings:

$2.43*

$3.05 - $3.35

… but, potential increases in coal prices and pension / financing

costs may limit growth in 2009 to lower half of forecast range.

14

PSEG Liquidity as of October 31, 2008

Expiration

Total

Primary

Usage at

Available

Company

Facility

Date

Facility

Purpose

10/31/2008

10/31/2008

PSEG

5-year Credit Facility

Dec-12

$1,000

1

CP Support/Funding/LCs

$13

$987

Bilateral Credit Facility

Jun-09

$100

CP Support/Funding

$0

$100

Uncommitted Bilateral Agreement

N/A

N/A

Funding

0

N/A

PSE&G

5-year Credit Facility

Jun-12

600

2

CP Support/Funding/LCs

116

484

Uncommitted Bilateral Agreement

N/A

N/A

Funding

0

N/A

Energy

5-year Credit Facility

Jun-10

136

Funding/LCs

21

115

Holdings

Power

5-Year Credit Facility

Dec-12

1,600

3

Funding/LCs

205

1,395

Bilateral Credit Facility

Jun-09

100

Funding/LCs

0

100

Bilateral Credit Facility

Mar-09

150

Funding/LCs

48

102

Bilateral Credit Facility

Sep-09

50

Funding

50

0

Bilateral Credit Facility

Mar-10

100

Funding/LCs

24

76

Total

$3,836

$3,359

1

PSEG Facility reduces by $47 million in 2012

2

PSE&G Facility reduces by $28 million in 2012

3

Power Facility reduces by $75 million in 2012

($ millions)

15

$1.12

$1.14

$1.29

$1.17

2005

2006

2007

2008

2009E

Our recent 10% dividend increase continues 100-year history of

paying common dividends.

A payout objective of 40 – 50% provides opportunity for growth

with earnings.

* Indicated annual dividend rate

*

44%

Payout

Ratio

40 – 50%

43%

66%

63%

?

Dividends per Share

16

Creating shareholder value for the long-term …

PSEG

S&P

Utilities

S&P 500

12.6%

10.1%

-1.4%

PSEG

S&P

Utilities

S&P 500

9.6%

3.2%

-0.9%

5-year Total Return*

10-year Total Return*

*Average monthly returns ending November 30, 2008

… has been and will continue to be our focus.

17

PSEG Value Proposition

PSEG is well-positioned in current business environment

Operational excellence efforts support:

Asset mix provides opportunities in attractive markets

Strengthened balance sheet supports capital investment

$3.35 billion available liquidity to support business

Return of cash to shareholders through dividends and share

repurchase provides discipline to investment process

maintaining reliability

controlling costs

providing value to the customer

18

Items Excluded from Net Income to Reconcile to Operating Earnings

Please see Slide 3 for an explanation of PSEG’s use of Operating Earnings as a non-GAAP financial measure and how

it differs from Net Income.

Nine Months

Nine Months

Ended

Year Ended

Ended

Year Ended

September 30,

September 30,

2008*

2007**

2008*

2007**

Lease Transaction Reserves:

(490)

$

-

$

(0.96)

$

-

$

Impact of Asset Sales:

Chilquinta & Luz Del Sur

(23)

-

(0.05)

Write down of Turboven

(7)

-

(0.01)

Premium on bond redemption

(1)

(28)

-

(0.06)

Total Impact of Asset Sales

(1)

$

(58)

$

-

$

(0.12)

$

Discontinued Operations:

208

$

16

$

0.41

$

0.03

$

*

As stated in Form 10-Q for the quarterly period ended September 30, 2008.

**

As stated in 2007 Form 10-K.

December 31,

December 31,

($ millions)

(EPS)

19