UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-10501

Name of Fund: BlackRock Municipal 2018 Term Trust (BPK)

Fund Address: 100 Bellevue Parkway, Wilmington, DE 19809

Name and address of agent for service: John M. Perlowski, Chief Executive Officer, BlackRock Municipal 2018 Term Trust, 55 East 52nd Street, New York, NY 10055

Registrant’s telephone number, including area code: (800) 882-0052, Option 4

Date of fiscal year end: 12/31/2016

Date of reporting period: 06/30/2016

Item 1 – Report to Stockholders

JUNE 30, 2016

| | | | |

SEMI-ANNUAL REPORT (UNAUDITED) | | | |  |

BlackRock California Municipal 2018 Term Trust (BJZ)

BlackRock Municipal 2018 Term Trust (BPK)

BlackRock New York Municipal 2018 Term Trust (BLH)

|

| Not FDIC Insured • May Lose Value • No Bank Guarantee |

| | | | | | |

| | | | | | | |

| 2 | | SEMI-ANNUAL REPORT | | JUNE 30, 2016 | | |

Dear Shareholder,

Uneven economic outlooks and divergence of monetary policies across regions have been the overarching themes driving financial markets over the past couple of years. In the latter half of 2015, as U.S. growth outpaced other developed markets, investors were focused largely on the timing of the Federal Reserve’s (the “Fed”) decision to end its near-zero interest rate policy. The Fed ultimately hiked rates in December, whereas the European Central Bank and the Bank of Japan took additional steps to stimulate growth, even introducing negative interest rates. The U.S. dollar had strengthened considerably ahead of these developments, causing profit challenges for U.S. companies that generate revenues overseas, and pressuring emerging market currencies and commodities prices.

Also during this time period, oil prices collapsed due to excess global supply. China, one of the world’s largest consumers of oil, was another notable source of stress for financial markets as the country showed signs of slowing economic growth and took measures to devalue its currency. Declining confidence in the country’s policymakers stoked investors’ worries about the potential impact of China’s weakness on the global economy. Global market volatility increased and risk assets (such as equities and high yield bonds) suffered in this environment.

The elevated market volatility spilled over into 2016, but as the first quarter wore on, fears of a global recession began to fade, allowing markets to calm and risk assets to rebound. Central bank stimulus in Europe and Japan, combined with a more tempered outlook for rate hikes in the United States, helped bolster financial markets. A softening in U.S. dollar strength brought relief to U.S. exporters and emerging market economies. Oil prices rebounded as the world’s largest producers agreed to reduce supply.

Volatility spiked again in late June when the United Kingdom shocked investors with its vote to leave the European Union. Uncertainty around how the British exit might affect the global economy and political landscape long term drove investors to high quality assets, pushing already-low global yields to even lower levels.

At BlackRock, we believe investors need to think globally, extend their scope across a broad array of asset classes and be prepared to adjust accordingly as market conditions change over time. We encourage you to talk with your financial advisor and visit blackrock.com for further insight about investing in today’s markets.

Sincerely,

Rob Kapito

President, BlackRock Advisors, LLC

Rob Kapito

President, BlackRock Advisors, LLC

| | | | | | | | |

| Total Returns as of June 30, 2016 | |

| | | 6-month | | | 12-month | |

U.S. large cap equities

(S&P 500® Index) | | | 3.84 | % | | | 3.99 | % |

U.S. small cap equities

(Russell 2000® Index) | | | 2.22 | | | | (6.73 | ) |

International equities

(MSCI Europe, Australasia,

Far East Index) | | | (4.42 | ) | | | (10.16 | ) |

Emerging market equities

(MSCI Emerging

Markets Index) | | | 6.41 | | | | (12.05 | ) |

3-month Treasury bills

(BofA Merrill Lynch 3-Month

U.S. Treasury Bill Index) | | | 0.15 | | | | 0.19 | |

U.S. Treasury securities

(BofA Merrill Lynch 10-Year

U.S. Treasury Index) | | | 7.95 | | | | 9.49 | |

U.S. investment grade

bonds (Barclays

U.S. Aggregate Bond Index) | | | 5.31 | | | | 6.00 | |

Tax-exempt municipal

bonds (S&P Municipal

Bond Index) | | | 4.35 | | | | 7.80 | |

U.S. high yield bonds

(Barclays U.S.

Corporate High Yield 2%

Issuer Capped Index) | | | 9.06 | | | | 1.65 | |

| Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. You cannot invest directly in an index. | |

| | | | | | |

| | | | | | | |

| | THIS PAGE NOT PART OF YOUR FUND REPORT | | | | 3 |

| | |

| Municipal Market Overview | | |

|

| For the Reporting Period Ended June 30, 2016 |

Municipal Market Conditions

Municipal bonds generated positive performance for the period, due to falling interest rates and a favorable supply-and-demand environment. Interest rates were volatile in 2015 (bond prices rise as rates fall) leading up to a long-awaited rate hike from the U.S. Federal Reserve (the “Fed”) that ultimately came in December. However, ongoing reassurance from the Fed that rates would be increased gradually and would likely remain low overall resulted in strong demand for fixed income investments, with municipal bonds being one of the strongest-performing sectors for the 12-month period. Investors favored the relative yield and stability of municipal bonds amid bouts of volatility resulting from uneven U.S. economic data, volatile oil prices, global growth concerns, geopolitical risks (particularly the United Kingdom’s decision to leave the European Union), and widening central bank divergence — i.e., policy easing outside the United States while the Fed was posturing to commence policy tightening. During the 12 months ended June 30, 2016, municipal bond funds garnered net inflows of approximately $42 billion (based on data from the Investment Company Institute).

For the same 12-month period, total new issuance remained relatively strong from a historical perspective at $390 billion (though lower than the $410 billion issued in the prior 12-month period). A noteworthy portion of new supply during this period was attributable to refinancing activity (roughly 59%) as issuers continued to take advantage of low interest rates and a flatter yield curve to reduce their borrowing costs.

|

S&P Municipal Bond Index |

Total Returns as of June 30, 2016 |

6 months: 4.35% |

12 months: 7.80% |

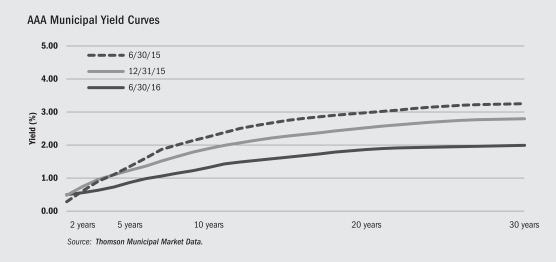

A Closer Look at Yields

From June 30, 2015 to June 30, 2016, yields on AAA-rated 30-year municipal bonds decreased by 126 basis points (“bps”) from 3.28% to 2.02%, while 10-year rates fell by 93 bps from 2.28% to 1.35% and 5-year rates decreased 49 bps from 1.38% to 0.89% (as measured by Thomson Municipal Market Data). The municipal yield curve experienced significant flattening over the 12-month period with the spread between 2- and 30-year maturities flattening by 121 bps and the spread between 2- and 10-year maturities flattening by 88 bps.

During the same time period, on a relative basis, tax-exempt municipal bonds broadly outperformed U.S. Treasuries with the greatest outperformance experienced in longer-term issues. In absolute terms, the positive performance of municipal bonds was driven largely by falling interest rates as well as a supply/demand imbalance within the municipal market as investors sought income and incremental yield in an environment where opportunities became increasingly scarce. More broadly, municipal bonds benefited from the greater appeal of tax-exempt investing in light of the higher tax rates implemented in 2014. The asset class is known for its lower relative volatility and preservation of principal with an emphasis on income as tax rates rise.

Financial Conditions of Municipal Issuers

The majority of municipal credits remain strong, despite well-publicized distress among a few issuers. Four of the five states with the largest amount of debt outstanding — California, New York, Texas and Florida — have exhibited markedly improved credit fundamentals during the slow national recovery. However, several states with the largest unfunded pension liabilities have seen their bond prices decline noticeably and remain vulnerable to additional price deterioration. On the local level, Chicago’s credit quality downgrade is an outlier relative to other cities due to its larger pension liability and inadequate funding remedies. BlackRock maintains the view that municipal bond defaults will remain minimal and in the periphery while the overall market is fundamentally sound. We continue to advocate careful credit research and believe that a thoughtful approach to structure and security selection remains imperative amid uncertainty in a modestly improving economic environment.

The opinions expressed are those of BlackRock as of June 30, 2016, and are subject to change at any time due to changes in market or economic conditions. The comments should not be construed as a recommendation of any individual holdings or market sectors. Investing involves risk including loss of principal. Bond values fluctuate in price so the value of your investment can go down depending on market conditions. Fixed income risks include interest-rate and credit risk. Typically, when interest rates rise, there is a corresponding decline in bond values. Credit risk refers to the possibility that the bond issuer will not be able to make principal and interest payments. There may be less information on the financial condition of municipal issuers than for public corporations. The market for municipal bonds may be less liquid than for taxable bonds. Some investors may be subject to Alternative Minimum Tax (AMT). Capital gains distributions, if any, are taxable.

The Standard & Poor’s Municipal Bond Index, a broad, market value-weighted index, seeks to measure the performance of the U.S. municipal bond market. All bonds in the index are exempt from U.S. federal income taxes or subject to the AMT. Past performance is no guarantee of future results. Index performance is shown for illustrative purposes only. It is not possible to invest directly in an index.

| | | | | | |

| | | | | | | |

| 4 | | SEMI-ANNUAL REPORT | | JUNE 30, 2016 | | |

| | |

| The Benefits and Risks of Leveraging | | |

The Trusts may utilize leverage to seek to enhance the distribution rate on, and net asset value (“NAV”) of, their common shares (“Common Shares”). However, these objectives cannot be achieved in all interest rate environments.

In general, the concept of leveraging is based on the premise that the financing cost of leverage, which is based on short-term interest rates, is normally lower than the income earned by a Trust on its longer-term portfolio investments purchased with the proceeds from leverage. To the extent that the total assets of the Trusts (including the assets obtained from leverage) are invested in higher-yielding portfolio investments, the Trusts’ shareholders benefit from the incremental net income. The interest earned on securities purchased with the proceeds from leverage is paid to shareholders in the form of dividends, and the value of these portfolio holdings is reflected in the per share NAV.

To illustrate these concepts, assume a Trust’s capitalization is $100 million and it utilizes leverage for an additional $30 million, creating a total value of $130 million available for investment in longer-term income securities. If prevailing short-term interest rates are 3% and longer-term interest rates are 6%, the yield curve has a strongly positive slope. In this case, a Trust’s financing costs on the $30 million of proceeds obtained from leverage are based on the lower short-term interest rates. At the same time, the securities purchased by a Trust with the proceeds from leverage earn income based on longer-term interest rates. In this case, a Trust’s financing cost of leverage is significantly lower than the income earned on a Trust’s longer-term investments acquired from such leverage proceeds, and therefore the holders of Common Shares (“Common Shareholders”) are the beneficiaries of the incremental net income.

However, in order to benefit shareholders, the return on assets purchased with leverage proceeds must exceed the ongoing costs associated with the leverage. If interest and other costs of leverage exceed the Trusts’ return on assets purchased with leverage proceeds, income to shareholders is lower than if the Trusts had not used leverage. Furthermore, the value of the Trusts’ portfolio investments generally varies inversely with the direction of long-term interest rates, although other factors can influence the value of portfolio investments. In contrast,

the value of the Trusts’ obligations under their respective leverage arrangements generally does not fluctuate in relation to interest rates. As a result, changes in interest rates can influence the Trusts’ NAVs positively or negatively. Changes in the future direction of interest rates are very difficult to predict accurately, and there is no assurance that the Trusts’ intended leveraging strategy will be successful.

The use of leverage also generally causes greater changes in each Trust’s NAV, market price and dividend rates than comparable portfolios without leverage. In a declining market, leverage is likely to cause a greater decline in the NAV and market price of a Trust’s shares than if the Trust were not leveraged. In addition, each Trust may be required to sell portfolio securities at inopportune times or at distressed values in order to comply with regulatory requirements applicable to the use of leverage or as required by the terms of leverage instruments, which may cause the Trusts to incur losses. The use of leverage may limit a Trust’s ability to invest in certain types of securities or use certain types of hedging strategies. Each Trust incurs expenses in connection with the use of leverage, all of which are borne by shareholders and may reduce income to the shareholders. Moreover, to the extent the calculation of the Trusts’ investment advisory fees includes assets purchased with the proceeds of leverage, the investment advisory fees payable to the Trusts’ investment adviser will be higher than if the Trusts did not use leverage.

Each Trust may utilize leverage through TOB Trusts as described in the Notes to Financial Statements.

Under the Investment Company Act of 1940, as amended (the “1940 Act”), the Trusts are permitted to issue debt up to 33 1/3% of their total managed assets. A Trust may voluntarily elect to limit its leverage to less than the maximum amount permitted under the 1940 Act.

If a Trust segregates or designates on its books and records cash or liquid assets having values not less than the value of a Trust’s obligations under the TOB Trust (including accrued interest), then such transaction is not considered a senior security and is not subject to the foregoing limitations and requirements under the 1940 Act.

| | | | | | |

| | | | | | | |

| | SEMI-ANNUAL REPORT | | JUNE 30, 2016 | | 5 |

| | | | |

| Trust Summary as of June 30, 2016 | | BlackRock California Municipal 2018 Term Trust |

BlackRock California Municipal 2018 Term Trust’s (BJZ) (the “Trust”) investment objectives seek to provide current income exempt from regular federal and California income taxes and to return $15 per common share to holders of common shares on or about December 31, 2018. The Trust seeks to achieve its investment objectives by investing, under normal market conditions, at least 80% of its total assets in municipal bonds that at the time of investment are investment grade quality.

There is no assurance that the Trust will achieve its investment objective of returning $15 per share.

| | |

Symbol on New York Stock Exchange (“NYSE”) | | BJZ |

Initial Offering Date | | October 26, 2001 |

Termination Date (on or about) | | December 31, 2018 |

Yield on Closing Market Price as of June 30, 2016 ($15.17)1 | | 2.19% |

Tax Equivalent Yield2 | | 4.46% |

Current Monthly Distribution per Common Share3 | | $0.0277 |

Current Annualized Distribution per Common Share3 | | $0.3324 |

Economic Leverage as of June 30, 2016 | | — |

| | 1 | | Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. Past performance does not guarantee future results. |

| | 2 | | Tax equivalent yield assumes the maximum marginal federal and state tax rate of 50.93%, which includes the 3.8% Medicare tax. Actual tax rates will vary based on income, exemptions and deductions. Lower taxes will result in lower tax equivalent yields. |

| | 3 | | The distribution rate is not constant and is subject to change. |

Returns for the six months ended June 30, 2016 were as follows:

| | | | | | | | |

| | | Returns Based On | |

| | | Market Price | | | NAV | |

BJZ1,2 | | | 1.91 | % | | | 1.17 | % |

Lipper California Municipal Debt Funds3 | | | 11.26 | % | | | 6.80 | % |

| | 1 | | All returns reflect reinvestment of dividends and/or distributions. |

| | 2 | | The Trust moved from a discount to NAV to a small premium during the period, which accounts for the difference between performance based on price and performance based on NAV. |

The following discussion relates to the Trust’s absolute performance based on NAV:

| • | | The Trust is scheduled to terminate on or about December 31, 2018, and it therefore holds securities that will mature close to that date. As rates declined more on the long end of the yield curve, the Trust’s shorter maturity profile was a disadvantage in comparison to its Lipper category peers, which typically hold longer-dated securities. |

| • | | California’s municipal bond market generated strong performance in the first half of 2016, reflecting both the sharp decline in U.S. Treasury yields and the continued improvement in fiscal conditions at both the state and local levels. (Bond prices rise as yields fall.) The gains were largely concentrated among intermediate- and longer-term bonds, while shorter-term issues produced much smaller returns. |

| • | | The Trust’s NAV was generally stable during the period, with a significant portion of total return coming from income. At the sector level, California tax-backed state, utility and transportation issues provided the largest positive contribution to performance. The Trust’s positions in lower-rated investment grade and below investment grade bonds also contributed, as lower-quality issues generally outpaced their higher-quality counterparts. The Trust maintained a fully invested portfolio, which helped maximize the income component of total return. |

| • | | The majority of the Trust’s investments delivered positive price performance, as all components of the S&P Muni Main Index gained ground during the period. However, the Trust’s low duration — which is a function of its termination date on or about December 31, 2018 — prevented it from fully participating in the gains of the broader market. (Duration is a measure of interest rate sensitivity.) Reinvestment risk also detracted from Trust performance. As higher yielding bonds mature or are called, the subsequent purchases need to be made at materially lower yields. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | | | | | |

| | | | | | | |

| 6 | | SEMI-ANNUAL REPORT | | JUNE 30, 2016 | | |

| | |

| | | BlackRock California Municipal 2018 Term Trust |

|

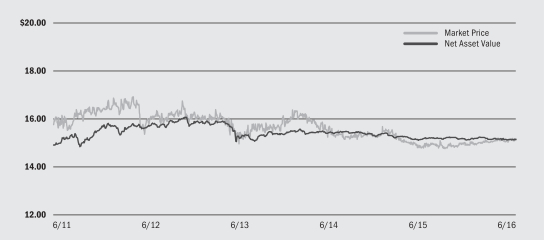

| Market Price and Net Asset Value Per Share Summary |

| | | | | | | | | | | | | | | | | | | | |

| | | 6/30/16 | | | 12/31/15 | | | Change | | | High | | | Low | |

Market Price | | $ | 15.17 | | | $ | 15.05 | | | | 0.80 | % | | $ | 15.24 | | | $ | 14.91 | |

Net Asset Value | | $ | 15.16 | | | $ | 15.15 | | | | 0.07 | % | | $ | 15.25 | | | $ | 15.13 | |

|

| Market Price and Net Asset Value History For the Past Five Years |

|

| Overview of the Trust’s Total Investments* |

| | | | | | | | |

| Sector Allocation | | 6/30/16 | | | 12/31/15 | |

Utilities | | | 28 | % | | | 28 | % |

County/City/Special District/School District | | | 24 | | | | 21 | |

Health | | | 12 | | | | 12 | |

Education | | | 11 | | | | 10 | |

State | | | 11 | | | | 17 | |

Transportation | | | 9 | | | | 7 | |

Corporate | | | 4 | | | | 4 | |

Housing | | | 1 | | | | 1 | |

| | | | |

| | |

| Call/Maturity Schedule3 | | | |

Calendar Year Ended December 31, | | | | |

2016 | | | 11 | % |

2017 | | | 7 | |

2018 | | | 55 | |

2019 | | | 17 | |

2020 | | | — | |

| | 3 | | Scheduled maturity dates and/or bonds that are subject to potential calls by issuers over the next five years. |

| | * | | Excludes short-term securities. |

| | | | | | | | |

| Credit Quality Allocation1 | | 6/30/16 | | | 12/31/15 | |

AAA/Aaa | | | 2 | % | | | 2 | % |

AA/Aa | | | 68 | | | | 67 | |

A | | | 15 | | | | 18 | |

BBB/Baa | | | 6 | | | | 7 | |

N/R2 | | | 9 | | | | 6 | |

| | 1 | | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either Standard & Poor’s (“S&P”) or Moody’s Investors Service (“Moody’s”) if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| | 2 | | The investment adviser evaluates the credit quality of unrated investments based upon certain factors including, but not limited to, credit ratings for similar investments and financial analysis of sectors and individual investments. Using this approach, the investment adviser has deemed certain of these unrated securities as investment grade quality. As of June 30, 2016 and December 31, 2015, the market value of unrated securities deemed by the investment adviser to be investment grade represents 5% and 4%, respectively, of the Trust’s total investments. |

| | | | | | |

| | | | | | | |

| | SEMI-ANNUAL REPORT | | JUNE 30, 2016 | | 7 |

| | | | |

| Trust Summary as of June 30, 2016 | | BlackRock Municipal 2018 Term Trust |

BlackRock Municipal 2018 Term Trust’s (BPK) (the “Trust”) investment objectives seek to provide current income exempt from regular federal income tax and to return $15 per common share (the initial offering price per common share) to holders of common shares on or about December 31, 2018. The Trust seeks to achieve its investment objectives by investing, under normal market conditions, its assets in municipal bonds exempt from federal income taxes (except that the interest may be subject to the federal AMT). The Trust invests at least 80% of its assets in municipal bonds that are investment grade quality at the time of investment.

There is no assurance that the Trust will achieve its investment objective of returning $15 per share.

| | |

Symbol on NYSE | | BPK |

Initial Offering Date | | October 26, 2001 |

Termination Date (on or about) | | December 31, 2018 |

Yield on Closing Market Price as of June 30, 2016 ($15.25)1 | | 2.19% |

Tax Equivalent Yield2 | | 3.87% |

Current Monthly Distribution per Common Share3 | | $0.0278 |

Current Annualized Distribution per Common Share3 | | $0.3336 |

Economic Leverage as of June 30, 20164 | | 2% |

| | 1 | | Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. Past performance does not guarantee future results. |

| | 2 | | Tax equivalent yield assumes the maximum marginal federal tax rate of 43.4%, which includes the 3.8% Medicare tax. Actual tax rates will vary based on income, exemptions and deductions. Lower taxes will result in lower tax equivalent yields. |

| | 3 | | The distribution rate is not constant and is subject to change. |

| | 4 | | Represents TOB Trusts as a percentage of total managed assets, which is the total assets of the Trust, including any assets attributable to TOB Trusts, minus the sum of accrued liabilities. For a discussion of leveraging techniques utilized by the Trust, please see The Benefits and Risks of Leveraging on page 5. |

Returns for the six months ended June 30, 2016 were as follows:

| | | | | | | | |

| | | Returns Based On | |

| | | Market Price | | | NAV | |

BPK1,2 | | | (0.30 | )% | | | 1.40 | % |

Lipper Intermediate Municipal Debt Funds3 | | | 7.02 | % | | | 5.41 | % |

| | 1 | | All returns reflect reinvestment of dividends and/or distributions. |

| | 2 | | The Trust moved from a premium to NAV to a discount during the period, which accounts for the difference between performance based on price and performance based on NAV. |

The following discussion relates to the Trust’s absolute performance based on NAV:

| • | | The Trust is scheduled to terminate on or about December 31, 2018, and it therefore holds securities that will mature close to that date. As rates declined more on the long end of the yield curve, the Trust’s shorter maturity profile was a disadvantage in comparison to its Lipper category peers, which typically hold longer-dated securities. |

| • | | Municipal bonds generated strong performance in the first half of 2016, reflecting both the sharp decline in U.S. Treasury yields and the continued health of state and local finances. (Bond prices rise as yields fall.) The gains were largely concentrated among intermediate- and longer-term bonds, while shorter-term issues produced much smaller returns. |

| • | | The Trust’s NAV was generally stable during the period, with a significant portion of total return coming from income. At the sector level, health and transportation issues provided the largest positive contribution to performance. The Trust’s positions in lower-rated investment grade and below investment grade bonds also contributed, as lower-quality issues generally outpaced their higher-quality counterparts. The Trust maintained a fully invested portfolio, which helped maximize the income component of total return. The Trust also employed leverage through the use of tender option bonds, which modestly enhanced returns for the period. |

| • | | The majority of the Trust’s investments delivered positive price performance, as all components of the S&P Muni Main Index gained ground during the period. However, the Trust’s low duration — which is a function of its termination date on or about December 31, 2018 — prevented it from fully participating in the gains of the broader market. (Duration is a measure of interest rate sensitivity.) Reinvestment risk also detracted from performance. As higher yielding bonds mature or are called, the subsequent purchases need to be made at materially lower yields. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | | | | | |

| | | | | | | |

| 8 | | SEMI-ANNUAL REPORT | | JUNE 30, 2016 | | |

| | |

| | | BlackRock Municipal 2018 Term Trust |

|

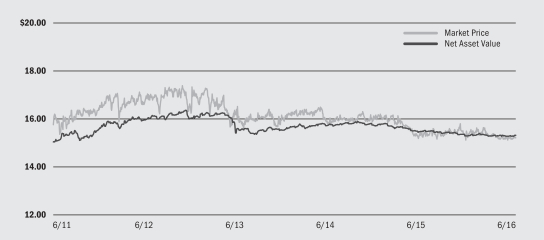

| Market Price and Net Asset Value Per Share Summary |

| | | | | | | | | | | | | | | | | | | | |

| | | 6/30/16 | | | 12/31/15 | | | Change | | | High | | | Low | |

Market Price | | $ | 15.25 | | | $ | 15.50 | | | | (1.61 | )% | | $ | 15.80 | | | $ | 15.14 | |

Net Asset Value | | $ | 15.35 | | | $ | 15.34 | | | | 0.07 | % | | $ | 15.42 | | | $ | 15.31 | |

|

| Market Price and Net Asset Value History For the Past Five Years |

|

| Overview of the Trust’s Total Investments* |

| | | | | | | | |

| Sector Allocation | | 6/30/16 | | | 12/31/15 | |

County/City/Special District/School District | | | 25 | % | | | 23 | % |

Transportation | | | 19 | | | | 16 | |

Health | | | 15 | | | | 14 | |

State | | | 12 | | | | 11 | |

Corporate | | | 10 | | | | 12 | |

Utilities | | | 8 | | | | 11 | |

Education | | | 6 | | | | 8 | |

Housing | | | 4 | | | | 5 | |

Tobacco | | | 1 | | | | — | |

| | | | |

| | |

| Call/Maturity Schedule3 | | | |

Calendar Year Ended December 31, | | | | |

2016 | | | 1 | % |

2017 | | | 10 | |

2018 | | | 69 | |

2019 | | | 12 | |

2020 | | | 1 | |

| | 3 | | Scheduled maturity dates and/or bonds that are subject to potential calls by issuers over the next five years. |

| | * | | Excludes short-term securities. |

| | | | | | | | |

| Credit Quality Allocation1 | | 6/30/16 | | | 12/31/15 | |

AAA/Aaa | | | 6 | % | | | 6 | % |

AA/Aa | | | 28 | | | | 27 | |

A | | | 37 | | | | 37 | |

BBB/Baa | | | 16 | | | | 15 | |

BB/Ba | | | 1 | | | | 1 | |

B | | | 1 | | | | — | |

N/R2 | | | 11 | | | | 14 | |

| | 1 | | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either S&P or Moody’s if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| | 2 | | The investment adviser evaluates the credit quality of unrated investments based upon certain factors including, but not limited to, credit ratings for similar investments and financial analysis of sectors and individual investments. Using this approach, the investment adviser has deemed certain of these unrated securities as investment grade quality. As of June 30, 2016 and December 31, 2015, the market value of unrated securities deemed by the investment adviser to be investment grade represents 6% and 8%, respectively, of the Trust’s total investments. |

| | | | | | |

| | | | | | | |

| | SEMI-ANNUAL REPORT | | JUNE 30, 2016 | | 9 |

| | | | |

| Trust Summary as of June 30, 2016 | | BlackRock New York Municipal 2018 Term Trust |

BlackRock New York Municipal 2018 Term Trust’s (BLH) (the “Trust”) investment objectives seek to provide current income exempt from regular federal income tax and New York State and New York City personal income taxes and to return $15 per common share (the initial offering price per common share) to holders of common shares on or about December 31, 2018. The Trust seeks to achieve its investment objectives by investing at least 80% of its total assets in municipal bonds that at the time of investment are investment grade quality.

There is no assurance that the Trust will achieve its investment objective of returning $15 per share.

| | |

Symbol on NYSE | | BLH |

Initial Offering Date | | October 26, 2001 |

Termination Date (on or about) | | December 31, 2018 |

Yield on Closing Market Price as of June 30, 2016 ($15.03)1 | | 1.41% |

Tax Equivalent Yield2 | | 2.85% |

Current Monthly Distribution per Common Share3 | | $0.0177 |

Current Annualized Distribution per Common Share3 | | $0.2124 |

Economic Leverage as of June 30, 2016 | | — |

| | 1 | | Yield on closing market price is calculated by dividing the current annualized distribution per share by the closing market price. Past performance does not guarantee future results. |

| | 2 | | Tax equivalent yield assumes the maximum marginal federal and state tax rate of 50.59%, which includes the 3.8% Medicare tax. Actual tax rates will vary based on income, exemptions and deductions. Lower taxes will result in lower tax equivalent yields. |

| | 3 | | The distribution rate is not constant and is subject to change. |

Returns for the six months ended June 30, 2016 were as follows:

| | | | | | | | |

| | | Returns Based On | |

| | | Market Price | | | NAV | |

BLH1,2 | | | 1.42 | % | | | 1.21 | % |

Lipper New York Municipal Debt Funds3 | | | 11.97 | % | | | 6.56 | % |

| | 1 | | All returns reflect reinvestment of dividends and/or distributions. |

| | 2 | | The Trust’s discount to NAV, which narrowed slightly during the period, accounts for the difference between performance based on price and performance based on NAV. |

The following discussion relates to the Trust’s absolute performance based on NAV:

| • | | The Trust is scheduled to terminate on or about December 31, 2018, and it therefore holds securities that will mature close to that date. As rates declined more on the long end of the yield curve, the Trust’s shorter maturity profile was a disadvantage in comparison to its Lipper category peers, which typically hold longer-dated securities. |

| • | | New York’s municipal bond market generated strong performance in the first half of 2016, reflecting both the sharp decline in U.S. Treasury yields and the continued improvement in fiscal conditions at both the state and local levels. (Bond prices rise as yields fall.) The gains were largely concentrated among intermediate- and longer-term bonds, while shorter-term issues produced much smaller returns. |

| • | | The Trust’s NAV was generally stable during the period, with a significant portion of total return coming from income. At the sector level, New York state and local tax-backed bonds provided the largest positive contribution to performance, followed by transportation issues. The Trust’s positions in lower-rated investment grade and below investment grade bonds also contributed, as lower-quality issues generally outpaced their higher-quality counterparts. The Trust maintained a fully invested portfolio, which helped maximize the income component of total return. |

| • | | The majority of the Trust’s investments delivered positive price performance, as all components of the S&P Muni Main Index gained ground during the period. However, the Trust’s low duration — which is a function of its termination date on or about December 31, 2018 — prevented it from fully participating in the gains of the broader market. (Duration is a measure of interest rate sensitivity.) Reinvestment risk also detracted from performance. As higher yielding bonds mature or are called, the subsequent purchases need to be made at materially lower yields. |

The views expressed reflect the opinions of BlackRock as of the date of this report and are subject to change based on changes in market, economic or other conditions. These views are not intended to be a forecast of future events and are no guarantee of future results.

| | | | | | |

| | | | | | | |

| 10 | | SEMI-ANNUAL REPORT | | JUNE 30, 2016 | | |

| | |

| | | BlackRock New York Municipal 2018 Term Trust |

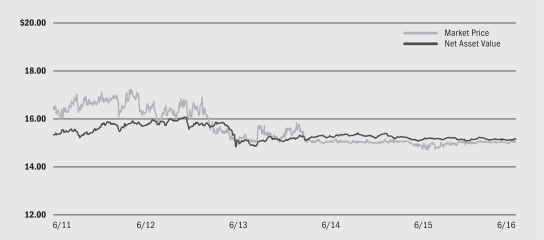

|

| Market Price and Net Asset Value Per Share Summary |

| | | | | | | | | | | | | | | | | | | | |

| | | 6/30/16 | | | 12/31/15 | | | Change | | | High | | | Low | |

Market Price | | $ | 15.03 | | | $ | 14.94 | | | | 0.60 | % | | $ | 15.13 | | | $ | 14.90 | |

Net Asset Value | | $ | 15.14 | | | $ | 15.08 | | | | 0.40 | % | | $ | 15.21 | | | $ | 15.08 | |

|

| Market Price and Net Asset Value History For the Past Five Years |

|

| Overview of the Trust’s Total Investments* |

| | | | | | | | |

| Sector Allocation | | 6/30/16 | | | 12/31/15 | |

County/City/Special District/School District | | | 40 | % | | | 38 | % |

Transportation | | | 18 | | | | 19 | |

Education | | | 13 | | | | 11 | |

State | | | 10 | | | | 11 | |

Utilities | | | 7 | | | | 7 | |

Health | | | 7 | | | | 7 | |

Housing | | | 3 | | | | 3 | |

Tobacco | | | 1 | | | | 1 | |

Corporate | | | 1 | | | | 3 | |

| | | | |

| | |

| Call/Maturity Schedule3 | | | |

Calendar Year Ended December 31, | | | | |

2016 | | | 1 | % |

2017 | | | 1 | |

2018 | | | 63 | |

2019 | | | 11 | |

2020 | | | 21 | |

| | 3 | | Scheduled maturity dates and/or bonds that are subject to potential calls by issuers over the next five years. |

| | * | | Excludes short-term securities. |

| | | | | | | | |

| Credit Quality Allocation1 | | 6/30/16 | | | 12/31/15 | |

AAA/Aaa | | | 15 | % | | | 15 | % |

AA/Aa | | | 61 | | | | 62 | |

A | | | 12 | | | | 10 | |

BBB/Baa | | | 4 | | | | 5 | |

BB/Ba | | | 1 | | | | — | |

N/R2 | | | 7 | | | | 8 | |

| | 1 | | For financial reporting purposes, credit quality ratings shown above reflect the highest rating assigned by either S&P or Moody’s if ratings differ. These rating agencies are independent, nationally recognized statistical rating organizations and are widely used. Investment grade ratings are credit ratings of BBB/Baa or higher. Below investment grade ratings are credit ratings of BB/Ba or lower. Investments designated N/R are not rated by either rating agency. Unrated investments do not necessarily indicate low credit quality. Credit quality ratings are subject to change. |

| | 2 | | The investment adviser evaluates the credit quality of unrated investments based upon certain factors including, but not limited to, credit ratings for similar investments and financial analysis of sectors and individual investments. Using this approach, the investment adviser has deemed certain of these unrated securities as investment grade quality. As of June 30, 2016 and December 31, 2015 the market value of unrated securities deemed by the investment adviser to be investment grade represents 5% and 1%, respectively, of the Trust’s total investments. |

| | | | | | |

| | | | | | | |

| | SEMI-ANNUAL REPORT | | JUNE 30, 2016 | | 11 |

| | |

Schedule of Investments June 30, 2016 (Unaudited) | | BlackRock California Municipal 2018 Term Trust (BJZ) (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Municipal Bonds | | Par (000) | | | Value | |

California — 96.5% | | | | | | | | |

Corporate — 4.4% | |

California Pollution Control Financing Authority, RB, Mandatory Put Bonds, Republic Services, Inc. Project, Series B, AMT, 5.25%, 6/01/23 (a) | | $ | 2,020 | | | $ | 2,137,423 | |

California Pollution Control Financing Authority, Refunding RB, Mandatory Put Bonds, Republic Services, Inc. Project, Series C, AMT,

5.25%, 6/01/23 (a) | | | 2,030 | | | | 2,148,004 | |

| | | | | | | | |

| | | | | | | | 4,285,427 | |

County/City/Special District/School District — 23.2% | | | | | | | | |

City & County of San Francisco California, GO, Refunding, Series R-1, 5.00%, 6/15/18 | | | 1,640 | | | | 1,782,352 | |

City of Vista California, COP, Refunding, Community Projects (NPFGC) (b): | | | | | | | | |

4.75%, 5/01/17 | | | 1,115 | | | | 1,154,137 | |

5.00%, 5/01/17 | | | 1,000 | | | | 1,037,180 | |

Fontana Public Finance Authority California, Refunding, Tax Allocation Bonds, North Fontana Redevelopment Project, Series A (AGM), 5.25%, 9/01/18 | | | 3,395 | | | | 3,409,021 | |

Golden Empire Schools Financing Authority, Refunding RB, Kern High School District Projects,

0.91%, 5/01/17 (a) | | | 3,000 | | | | 2,999,100 | |

Irvine Unified School District California, Refunding, Special Tax Bonds, Community Facilities District No. 86-1 (AGM), 5.25%, 9/01/18 | | | 5,000 | | | | 5,451,800 | |

Jurupa Public Financing Authority, Refunding, Special Tax Bonds, Series A, 4.00%, 9/01/18 | | | 380 | | | | 404,172 | |

Lathrop Financing Authority, RB, Water Supply Project, 5.80%, 6/01/21 | | | 470 | | | | 480,664 | |

Lodi Unified School District California, GO, Refunding (AGM), 4.00%, 8/01/18 | | | 1,000 | | | | 1,068,760 | |

Los Angeles Community College District California, GO, Election of 2001, Series E-1, 4.00%, 8/01/18 | | | 200 | | | | 214,054 | |

Los Angeles Unified School District California, GO, Election of 2004, Series H (AGM),

5.00%, 7/01/17 (b) | | | 300 | | | | 313,362 | |

Los Banos Unified School District California, GO, Election of 2008 (AGM), 5.00%, 8/01/17 (b) | | | 475 | | | | 502,845 | |

Oakland Unified School District/Alameda County, GO, Refunding, 5.00%, 8/01/18 | | | 900 | | | | 970,308 | |

Placentia-Yorba Linda Unified School District, COP, Refunding Series A (AGM), 4.00%, 10/01/18 | | | 160 | | | | 171,779 | |

San Marcos Unified School District California, GO, CAB (c): | |

0.00%, 8/01/17 | | | 385 | | | | 380,565 | |

0.00%, 8/01/18 | | | 500 | | | | 487,220 | |

Santa Clara Unified School District California, GO, Election of 2004, Series A, 5.00%, 7/01/18 | | | 1,690 | | | | 1,837,807 | |

| | | | | | | | |

| | | | | | | | 22,665,126 | |

| | | | | | | | |

| Municipal Bonds | | Par (000) | | | Value | |

California (continued) | | | | | | | | |

Education — 10.6% | | | | | | | | |

California Municipal Finance Authority, Refunding RB, Series A: | | | | | | | | |

3.00%, 1/01/17 | | $ | 425 | | | $ | 427,541 | |

3.00%, 1/01/18 | | | 440 | | | | 446,873 | |

University of California, Refunding RB: | | | | | | | | |

General, Series AB, 5.00%, 5/15/19 | | | 2,500 | | | | 2,807,350 | |

Series A, 4.00%, 11/01/18 | | | 3,000 | | | | 3,233,070 | |

Series A, 5.00%, 11/01/18 | | | 900 | | | | 990,756 | |

Series AR, 3.00%, 5/15/18 | | | 230 | | | | 240,387 | |

Series S, 5.00%, 5/15/18 (d) | | | 5 | | | | 5,412 | |

Series S, 5.00%, 5/15/18 | | | 1,995 | | | | 2,160,166 | |

| | | | | | | | |

| | | | | | | | 10,311,555 | |

Health — 11.9% | | | | | | | | |

California Health Facilities Financing Authority, RB, Scripps Health, Series A, 5.00%, 10/01/18 | | | 750 | | | | 822,038 | |

California Health Facilities Financing Authority, Refunding RB: | | | | | | | | |

Adventist Health System/West, Series A, 4.00%, 3/01/18 | | | 1,000 | | | | 1,052,220 | |

Sutter Health, Series D, 5.00%, 8/15/18 | | | 515 | | | | 563,034 | |

California Statewide Communities Development Authority, RB, Kaiser Permanente, Series E-1, 5.00%, 4/01/44 (a) | | | 4,700 | | | | 4,867,226 | |

California Statewide Communities Development Authority, Refunding RB: | | | | | | | | |

CHF Irvine LLC, 5.00%, 5/15/18 | | | 1,000 | | | | 1,077,620 | |

Episcopal Communities & Services, 5.00%, 5/15/18 | | | 300 | | | | 322,161 | |

Huntington Memorial Hospital, Series B, 5.00%, 7/01/18 | | | 500 | | | | 542,370 | |

Rady Children’s Hospital, Series A, 4.00%, 8/15/18 | | | 1,000 | | | | 1,068,880 | |

County of Los Angeles California Redevelopment Authority, Refunding, Tax Allocation Bonds, South Gate Redevelopment Project No. 1 and Claremont Consolidated Redevelopment Project, Series A, 4.00%, 9/01/18 | | | 850 | | | | 910,086 | |

Union City Community Redevelopment Agency, Refunding, Tax Allocation Bonds, Series A, 4.00%, 10/01/18 | | | 350 | | | | 376,135 | |

| | | | | | | | |

| | | | | | | | 11,601,770 | |

Housing — 1.2% | |

California HFA, RB, Series A (Fannie Mae): | | | | | | | | |

3.20%, 8/01/18 | | | 390 | | | | 407,378 | |

3.50%, 2/01/19 | | | 750 | | | | 795,435 | |

| | | | | | | | |

| | | | | | | | 1,202,813 | |

| | | | | | | | | | |

| AGC | | Assured Guarantee Corp. | | COP | | Certificates of Participation | | ISD | | Independent School District |

| AGM | | Assured Guaranty Municipal Corp. | | EDA | | Economic Development Authority | | LRB | | Lease Revenue Bonds |

| AMBAC | | American Municipal Bond Assurance Corp. | | GAN | | Grant Anticipation Notes | | NPFGC | | National Public Finance Guarantee Corp. |

| AMT | | Alternative Minimum Tax (subject to) | | GO | | General Obligation Bonds | | PSF-GTD | | Permanent School Fund Guaranteed |

| ARB | | Airport Revenue Bonds | | HFA | | Housing Finance Agency | | RB | | Revenue Bonds |

| CAB | | Capital Appreciation Bonds | | IDA | | Industrial Development Authority | | S/F | | Single-Family |

See Notes to Financial Statements.

| | | | | | |

| | | | | | | |

| 12 | | SEMI-ANNUAL REPORT | | JUNE 30, 2016 | | |

| | |

Schedule of Investments (continued) | | BlackRock California Municipal 2018 Term Trust (BJZ) |

| | | | | | | | |

| Municipal Bonds | | Par (000) | | | Value | |

California (continued) | | | | | | | | |

State — 9.6% | |

State of California, GO, Refunding: | | | | | | | | |

5.00%, 9/01/18 | | $ | 5,900 | | | $ | 6,451,001 | |

5.00%, 11/01/20 | | | 20 | | | | 20,080 | |

Series A, 5.00%, 7/01/18 (d) | | | 720 | | | | 783,274 | |

Veterans, Series BZ, AMT (NPFGC),

5.35%, 12/01/21 | | | 10 | | | | 10,031 | |

State of California Public Works Board, Refunding RB, California Community Colleges, Series A,

5.00%, 12/01/17 | | | 2,020 | | | | 2,051,673 | |

| | | | | | | | |

| | | | | | | | 9,316,059 | |

Transportation — 8.7% | |

City of Long Beach California, RB, Series A,

5.00%, 5/15/18 | | | 500 | | | | 541,200 | |

Port of Oakland California, Refunding RB, Series O, AMT: | | | | | | | | |

5.00%, 5/01/18 | | | 4,280 | | | | 4,607,762 | |

5.00%, 5/01/19 | | | 3,000 | | | | 3,344,820 | |

| | | | | | | | |

| | | | | | | | 8,493,782 | |

Utilities — 26.9% | | | | | | | | |

California State Department of Water Resources, Refunding RB: | | | | | | | | |

Series H, 5.00%, 5/01/18 (b) | | | 2,500 | | | | 2,702,150 | |

Series H, 5.00%, 5/01/22 | | | 1,000 | | | | 1,078,810 | |

Series L, 5.00%, 5/01/19 | | | 2,000 | | | | 2,243,680 | |

Series N, 5.00%, 5/01/19 | | | 3,500 | | | | 3,926,440 | |

City of Riverside California Sewer Revenue, Refunding RB, Series A, 4.00%, 8/01/18 | | | 1,000 | | | | 1,068,320 | |

City of San Francisco California Public Utilities Commission Water Revenue, Refunding RB, Series D, 3.00%, 11/01/18 | | | 2,000 | | | | 2,108,600 | |

City of Tulare California Sewer Revenue, Refunding RB (AGM), 4.00%, 11/15/18 | | | 315 | | | | 339,110 | |

County of Los Angeles California Sanitation Districts Financing Authority, Refunding RB, Series A,

3.00%, 10/01/18 | | | 3,000 | | | | 3,162,210 | |

Cucamonga Valley California Water District, Refunding RB, Series A (AGM): | | | | | | | | |

4.00%, 9/01/18 | | | 325 | | | | 348,338 | |

4.00%, 9/01/19 | | | 325 | | | | 358,088 | |

| | | | | | | | |

| Municipal Bonds | | Par (000) | | | Value | |

California (continued) | | | | | | | | |

Utilities (continued) | | | | | | | | |

Los Angeles California Department of Water & Power, RB, Series B, 5.00%, 7/01/18 | | $ | 955 | | | $ | 1,039,327 | |

Los Angeles California Department of Water & Power, Refunding RB, Power System, Series A,

5.00%, 7/01/19 | | | 2,500 | | | | 2,820,475 | |

Sacramento California Municipal Utility District, Refunding RB, Series X, 5.00%, 8/15/18 | | | 400 | | | | 437,040 | |

Southern California Public Power Authority, Refunding RB, Canyon Power, Series A, 4.00%, 7/01/18 | | | 685 | | | | 732,149 | |

Stockton East Water District California, COP, Refunding, Series B (NPFGC), 0.00%, 4/01/19 (c) | | | 4,590 | | | | 3,915,040 | |

| | | | | | | | |

| | | | | | | | 26,279,777 | |

| Total Municipal Bonds in California | | | | | | | 94,156,309 | |

| | | | | | | | |

Guam — 0.3% | | | | | | | | |

Utilities — 0.3% | |

Guam Power Authority, Refunding RB, Series A (AGM), 5.00%, 10/01/19 | | | 240 | | | | 270,890 | |

| | | | | | | | |

U.S. Virgin Islands — 0.9% | | | | | | | | |

State — 0.9% | | | | | | | | |

Virgin Islands Public Finance Authority, RB, Series A, 5.00%, 10/01/16 | | | 930 | | | | 939,077 | |

Total Long-Term Investments (Cost — 92,520,380) — 97.7% | | | | 95,366,276 | |

| | | | | | | | |

| | | | | | | | | |

| | |

| Short-Term Securities | | Shares | | | | |

BlackRock Liquidity Funds, MuniCash, Institutional Class, 0.26%, (e)(f) | | | 1,439,683 | | | | 1,439,683 | |

Total Short-Term Securities (Cost — $1,439,683) — 1.5% | | | | 1,439,683 | |

| Total Investments (Cost — $93,960,063) — 99.2% | | | | 96,805,959 | |

| Other Assets Less Liabilities — 0.8% | | | | 741,465 | |

| | | | | | | | |

Net Assets — 100.0% | | | $ | 97,547,424 | |

| | | | | | | | |

|

| Notes to Schedule of Investments |

| (a) | | Variable rate security. Rate as of period end. |

| (b) | | U.S. Government securities, held in escrow, are used to pay interest on this security, as well as to retire the bond in full at the date indicated, typically at a premium to par. |

| (d) | | Security is collateralized by municipal bonds or U.S. Treasury obligations. |

| (e) | | During the six months ended June 30, 2016, investments in issuers considered to be affiliates of the Trust for purposes of Section 2(a)(3) of the Investment Company Act of 1940, as amended, were as follows: |

| | | | | | | | | | | | | | | | | | | | |

| Affiliate | | Shares Held

at December 31,

2015 | | | Net

Activity | | | Shares Held

at June 30,

2016 | | | Value at

June 30,

2016 | | | Income | |

BlackRock Liquidity Funds, MuniCash, Institutional Class | | | — | | | | 1,439,683 | | | | 1,439,683 | | | $ | 1,439,683 | | | $ | 352 | |

BIF California Municipal Money Fund | | | 1,076,590 | | | | (1,076,590 | ) | | | — | | | | — | | | | 2 | |

| |

Total | | | | | | | | | | | | | | $ | 1,439,683 | | | $ | 354 | |

| | | | | | | | | | | | | | | | |

See Notes to Financial Statements.

| | | | | | |

| | | | | | | |

| | SEMI-ANNUAL REPORT | | JUNE 30, 2016 | | 13 |

| | |

Schedule of Investments (concluded) | | BlackRock California Municipal 2018 Term Trust (BJZ) |

| (f) | | Current yield as of period end. |

For Trust compliance purposes, the Trust’s sector classifications refer to any one or more of the sector sub-classifications used by one or more widely recognized market indexes or rating group indexes, and/or as defined by the investment adviser. These definitions may not apply for purposes of this report, which may combine such sector sub-classifications for reporting ease.

|

| Fair Value Hierarchy as of Period End |

Various inputs are used in determining the fair value of investments. For information about the Trust’s policy regarding valuation of investments, refer to the Notes to Financial Statements.

The following table summarizes the Trust’s investments categorized in the disclosure hierarchy:

| | | | | | | | | | | | | | | | |

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

Assets: | | | | | | | | | | | | | | | | |

| Investments: | | | | | | | | | | | | | | | | |

Long-Term Investments1 | | | — | | | $ | 95,366,276 | | | | — | | | $ | 95,366,276 | |

Short-Term Securities | | $ | 1,439,683 | | | | — | | | | — | | | | 1,439,683 | |

| | | | |

Total | | $ | 1,439,683 | | | $ | 95,366,276 | | | | — | | | $ | 96,805,959 | |

| | | | |

1 See above Schedule of Investments for values in each sector. | |

During the six months ended June 30, 2016, there were no transfers between levels.

See Notes to Financial Statements.

| | | | | | |

| | | | | | | |

| 14 | | SEMI-ANNUAL REPORT | | JUNE 30, 2016 | | |

| | |

Schedule of Investments June 30, 2016 (Unaudited) | | BlackRock Municipal 2018 Term Trust (BPK) (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Municipal Bonds | | Par

(000) | | | Value | |

Alabama — 2.9% | | | | | | | | |

Alabama 21st Century Authority, Refunding RB, Series A, 5.00%, 6/01/18 | | $ | 500 | | | $ | 538,205 | |

Alabama Federal Aid Highway Finance Authority, RB, GAN, Garvee, 5.00%, 9/01/18 | | | 6,000 | | | | 6,545,340 | |

| | | | | | | | |

| | | | | | | | 7,083,545 | |

Alaska — 2.6% | | | | | | | | |

City of Valdez Alaska, Refunding RB,

5.00%, 1/01/18 | | | 6,000 | | | | 6,337,620 | |

California — 6.4% | | | | | | | | |

California Health Facilities Financing Authority, RB, Sutter Health, Series B, 5.00%, 8/15/19 | | | 2,500 | | | | 2,835,875 | |

California Pollution Control Financing Authority, Refunding RB, Mandatory Put Bonds, Republic Services, Inc. Project, Series C, AMT,

5.25%, 6/01/23 (a) | | | 4,055 | | | | 4,290,717 | |

Golden Empire Schools Financing Authority, Refunding RB, Kern High School District Projects,

0.91%, 5/01/17 (a) | | | 1,710 | | | | 1,709,487 | |

Los Angeles Regional Airports Improvement Corp., Refunding RB, Facilities Lease, LAXFuel Corp., AMT: | | | | | | | | |

5.00%, 1/01/17 | | | 450 | | | | 459,878 | |

5.00%, 1/01/18 | | | 930 | | | | 988,376 | |

Los Angeles Unified School District California, GO, Series I, 5.00%, 7/01/20 | | | 3,750 | | | | 4,227,150 | |

Oakland Unified School District/Alameda County, GO, Refunding, 5.00%, 8/01/18 | | | 1,000 | | | | 1,078,120 | |

| | | | | | | | |

| | | | | | | | 15,589,603 | |

Colorado — 1.0% | | | | | | | | |

Colorado Educational & Cultural Facilities Authority, Refunding RB, Peak to Peak Charter School,

4.00%, 8/15/18 | | | 175 | | | | 185,391 | |

Colorado Health Facilities Authority, Refunding RB, Evangelical Lutheran Good Samaritan Society Project: | | | | | | | | |

4.00%, 12/01/17 | | | 515 | | | | 532,309 | |

4.00%, 12/01/18 | | | 540 | | | | 569,533 | |

Park Creek Metropolitan District Colorado, Refunding RB, Senior Limited Property Tax, 4.00%, 12/01/18 | | | 1,000 | | | | 1,067,930 | |

| | | | | | | | |

| | | | | | | | 2,355,163 | |

Delaware — 0.3% | | | | | | | | |

Delaware State Economic Development Authority, RB, State University Project, 5.00%, 10/01/18 | | | 735 | | | | 801,091 | |

Florida — 5.4% | | | | | | | | |

City of Miami Beach Florida, RB, 5.00%, 9/01/18 | | | 875 | | | | 954,266 | |

County of Broward Florida Airport System Revenue, Refunding RB, Series P-1, AMT, 5.00%, 10/01/18 | | | 3,930 | | | | 4,283,857 | |

County of Broward Florida School Board, COP, Series A (AGM), 5.25%, 7/01/18 (b) | | | 1,250 | | | | 1,363,437 | |

County of Indian River Florida School Board, COP, Refunding, Series A, 5.00%, 7/01/18 | | | 600 | | | | 650,472 | |

County of Miami-Dade Florida, Refunding RB, Series A, AMT, 5.00%, 10/01/18 | | | 2,000 | | | | 2,183,140 | |

Miami Beach Health Facilities Authority, Refunding RB, Mount Sinai Medical Center, 4.00%, 11/15/18 | | | 250 | | | | 266,598 | |

Miami-Dade County School Board Foundation, Inc, COP, Refunding Series A, 5.00%, 5/01/18 | | | 1,500 | | | | 1,615,740 | |

| | | | | | | | |

| Municipal Bonds | | Par

(000) | | | Value | |

Florida (continued) | | | | | | | | |

Pine Island Community Development District, RB,

5.30%, 11/01/10 (c)(d) | | $ | 400 | | | $ | 224,292 | |

Stevens Plantation Community Development District, Special Assessment Bonds, Series B,

6.38%, 5/01/13 (c)(d) | | | 2,270 | | | | 1,588,410 | |

| | | | | | | | |

| | | | | | | | 13,130,212 | |

Guam — 0.3% | | | | | | | | |

Guam Power Authority, Refunding RB, Series A (AGM), 5.00%, 10/01/19 | | | 620 | | | | 699,800 | |

Hawaii — 0.2% | | | | | | | | |

Hawaii State Department of Budget & Finance, Refunding RB, Special Purpose Senior Living Revenue, 5.00%, 11/15/18 | | | 370 | | | | 396,326 | |

Illinois — 6.7% | | | | | | | | |

Chicago Transit Authority, Refunding RB,

5.00%, 6/01/18 | | | 1,000 | | | | 1,069,020 | |

Counties of Du Page & Will Illinois Community School District No. 204 Indian Prairie, GO, Refunding Series B, 3.00%, 12/30/18 | | | 1,935 | | | | 2,029,854 | |

Fox Valley Park District, GO, Series A,

5.00%, 12/15/18 | | | 1,725 | | | | 1,903,348 | |

Illinois Finance Authority, Refunding RB: | | | | | | | | |

University Medical Center Rush, Series A,

5.00%, 11/15/18 | | | 1,000 | | | | 1,093,640 | |

Central DuPage Health, Series B, 5.00%, 11/01/18 | | | 2,290 | | | | 2,499,283 | |

Peoples Gas Light and Coke Co. Project, Series B, 1.88%, 2/01/33 (a) | | | 1,000 | | | | 1,024,410 | |

Railsplitter Tobacco Settlement Authority, RB,

5.00%, 6/01/18 | | | 1,290 | | | | 1,386,737 | |

State of Illinois, GO (AGM), 5.00%, 4/01/18 | | | 465 | | | | 486,423 | |

State of Illinois, RB, Build Illinois, Series B: | | | | | | | | |

5.00%, 6/15/18 (e) | | | 355 | | | | 384,958 | |

Unrefunded Balance, 5.00%, 6/15/18 | | | 1,645 | | | | 1,777,422 | |

State of Illinois, GO, Refunding, 5.00%, 8/01/18 | �� | | 2,500 | | | | 2,672,050 | |

| | | | | | | | |

| | | | | | | | 16,327,145 | |

Indiana — 2.2% | | | | | | | | |

Indiana Finance Authority, RB, Ohio River Bridges East End Crossing Project, Series B, AMT,

5.00%, 1/01/19 | | | 1,715 | | | | 1,750,672 | |

Indiana State Municipal Power Agency, Refunding RB, Series A, 5.00%, 1/01/19 | | | 875 | | | | 968,415 | |

Indianapolis Airport Authority, Refunding RB, Special Facilities, FedEx Corp. Project, AMT,

5.10%, 1/15/17 (e) | | | 2,500 | | | | 2,557,975 | |

| | | | | | | | |

| | | | | | | | 5,277,062 | |

Iowa — 1.1% | | | | | | | | |

Iowa Finance Authority, Refunding RB, Midwestern Disaster Area, Iowa Fertilizer Co. Project,

5.00%, 12/01/19 | | | 1,850 | | | | 1,924,721 | |

University of Iowa, Refunding RB, Series S,

5.00%, 11/01/18 | | | 655 | | | | 720,035 | |

| | | | | | | | |

| | | | | | | | 2,644,756 | |

Kansas — 1.1% | | | | | | | | |

Kansas Development Finance Authority, Refunding RB, Adventist Health, 5.00%, 11/15/18 | | | 2,500 | | | | 2,745,100 | |

See Notes to Financial Statements.

| | | | | | |

| | | | | | | |

| | SEMI-ANNUAL REPORT | | JUNE 30, 2016 | | 15 |

| | |

Schedule of Investments (continued) | | BlackRock Municipal 2018 Term Trust (BPK) |

| | | | | | | | |

| Municipal Bonds | | Par

(000) | | | Value | |

Kentucky — 3.4% | | | | | | | | |

County of Kenton Kentucky School District Finance Corp., Refunding RB, 2.50%, 6/01/18 | | $ | 3,210 | | | $ | 3,306,172 | |

County of Louisville & Jefferson Kentucky Metropolitan Government, Refunding RB, Catholic Health Initiatives, Series A, 5.00%, 12/01/18 | | | 1,755 | | | | 1,924,006 | |

Kentucky Housing Corp., RB, S/F Housing, Series C, AMT, 4.63%, 7/01/22 | | | 3,195 | | | | 3,205,448 | |

| | | | | | | | |

| | | | | | | | 8,435,626 | |

Maryland — 3.6% | | | | | | | | |

Maryland Health & Higher Educational Facilities Authority, Refunding RB: | | | | | | | | |

Charlestown Community, 5.00%, 1/01/19 | | | 1,685 | | | | 1,851,192 | |

Meritas Medical Center, 5.00%, 7/01/18 | | | 400 | | | | 431,896 | |

University of Maryland Medical System,

5.00%, 7/01/18 | | | 1,000 | | | | 1,078,700 | |

Maryland State Transportation Authority, Refunding RB, Baltimore/Washington Thurgood Marshall Airport Project, Series B, AMT, 5.00%, 3/01/19 | | | 5,000 | | | | 5,529,250 | |

| | | | | | | | |

| | | | | | | | 8,891,038 | |

Michigan — 3.9% | | | | | | | | |

Kalamazoo Hospital Finance Authority, Refunding RB, Bronson Methodist Hospital (AGM),

5.00%, 5/15/18 | | | 2,025 | | | | 2,170,759 | |

Michigan State Finance Authority, Refunding RB, AMT: | | | | | | | | |

5.00%, 11/01/17 | | | 2,275 | | | | 2,375,032 | |

5.00%, 11/01/18 | | | 2,100 | | | | 2,257,332 | |

Michigan State Hospital Finance Authority, Refunding RB, Oakwood Obligation Group, Series A,

5.00%, 7/15/17 (b) | | | 1,000 | | | | 1,046,050 | |

Michigan State Housing Development Authority, Refunding RB, Series B, 4.15%, 4/01/18 | | | 1,000 | | | | 1,050,110 | |

Saginaw Valley State University, RB, Series A,

5.00%, 7/01/18 | | | 600 | | | | 649,092 | |

| | | | | | | | |

| | | | | | | | 9,548,375 | |

Mississippi — 0.4% | | | | | | | | |

Mississippi Development Bank, Refunding RB,

5.00%, 3/01/18 | | | 1,000 | | | | 1,063,930 | |

Missouri — 0.8% | | | | | | | | |

City of Kansas City Missouri, Refunding ARB, AMT, Series A, 5.00%, 9/01/18 | | | 1,750 | | | | 1,897,857 | |

Nebraska — 1.6% | | | | | | | | |

Central Plains Energy Project, RB, Gas Project

(Project No. 3), 5.00%, 9/01/17 | | | 2,330 | | | | 2,431,355 | |

Public Power Generation Agency, RB, Whelan Energy Center, Series 2-A (AGC), 5.00%, 1/01/17 (b) | | | 1,500 | | | | 1,533,000 | |

| | | | | | | | |

| | | | | | | | 3,964,355 | |

Nevada — 4.0% | | | | | | | | |

City of Las Vegas Nevada, Special Assessment Bonds, Summerlin Area, 5.35%, 6/01/17 | | | 450 | | | | 456,291 | |

County of Clark Nevada, Refunding, Special Assessment Bonds, Improvement District No. 142, Mountain’s Edge, 4.00%, 8/01/18 | | | 3,715 | | | | 3,845,954 | |

Director of the State of Nevada Department of Business & Industry, RB, Mandatory Put Bonds, Republic Services, Inc. Project, AMT,

5.63%, 12/01/26 (a) | | | 5,120 | | | | 5,481,830 | |

| | | | | | | | |

| | | | | | | | 9,784,075 | |

| | | | | | | | |

| Municipal Bonds | | Par

(000) | | | Value | |

New Hampshire — 2.1% | | | | | | | | |

New Hampshire State Turnpike System, RB, Series A, 5.00%, 10/01/18 | | $ | 4,740 | | | $ | 5,191,912 | |

New Jersey — 13.9% | | | | | | | | |

County of Atlantic New Jersey, Refunding,

3.00%, 10/01/18 (f) | | | 1,855 | | | | 1,934,876 | |

New Jersey EDA, Refunding RB: | | | | | | | | |

Cigarette Tax Revenue, 5.00%, 6/15/18 | | | 5,000 | | | | 5,294,100 | |

Lions Gate Project, 3.25%, 1/01/18 | | | 250 | | | | 253,600 | |

New Jersey Educational Facilities Authority, RB, Seton Hall University, Series D, 5.00%, 7/01/18 | | | 320 | | | | 344,589 | |

New Jersey Educational Facilities Authority, Refunding RB, University of Medicine & Dentistry, Series B,

6.25%, 12/01/18 (e) | | | 2,500 | | | | 2,826,025 | |

New Jersey Health Care Facilities Financing Authority, Refunding RB: | | | | | | | | |

AHS Hospital Corp., 5.00%, 7/01/18 | | | 850 | | | | 919,725 | |

AtlantiCare Regional Medical Center,

5.00%, 7/01/17 (b) | | | 1,500 | | | | 1,564,965 | |

Barnabas Health, Series A, 5.00%, 7/01/18 | | | 2,000 | | | | 2,153,260 | |

Princeton HealthCare System, 5.00%, 7/01/18 | | | 1,620 | | | | 1,748,174 | |

New Jersey Higher Education Student Assistance Authority, RB, Series 1A, AMT: | | | | | | | | |

5.00%, 12/01/17 | | | 460 | | | | 484,178 | |

5.00%, 12/01/18 | | | 2,000 | | | | 2,168,000 | |

New Jersey State Housing & Mortgage Finance Agency, Refunding RB, S/F Housing, Series T, AMT,

4.55%, 10/01/22 | | | 1,705 | | | | 1,737,054 | |

New Jersey State Turnpike Authority, Refunding RB, Series G, 5.00%, 1/01/18 | | | 1,350 | | | | 1,436,211 | |

New Jersey Transportation Trust Fund Authority, RB: | | | | | | | | |

Series B, 5.00%, 6/15/18 | | | 2,000 | | | | 2,126,440 | |

Transportation Program, Series AA, 5.00%, 6/15/18 | | | 2,000 | | | | 2,126,440 | |

Transportation System, Series A, 5.75%, 6/15/18 | | | 1,320 | | | | 1,422,445 | |

Transportation System, Series A (AMBAC),

5.75%, 6/15/18 | | | 2,070 | | | | 2,230,653 | |

Newark Housing Authority, RB, South Ward Police Facility (AGC), 4.50%, 12/01/18 | | | 2,785 | | | | 2,904,226 | |

South Jersey Transportation Authority LLC, Refunding RB, Series A, 5.00%, 11/01/20 | | | 200 | | | | 225,118 | |

| | | | | | | | |

| | | | | | | | 33,900,079 | |

New York — 5.9% | | | | | | | | |

City of New York New York Industrial Development Agency, ARB, American Airlines, Inc., JFK International Airport Project, AMT, Series B,

2.00%, 8/01/28 (a) | | | 1,530 | | | | 1,528,440 | |

Metropolitan Transportation Authority, Refunding RB: | | | | | | | | |

Series A, 5.00%, 11/15/18 | | | 1,000 | | | | 1,102,540 | |

Series F, 4.00%, 11/15/18 | | | 200 | | | | 215,506 | |

New York State Dormitory Authority, RB, General Purpose, Series A, 5.00%, 3/15/18 | | | 6,500 | | | | 6,984,575 | |

New York State Dormitory Authority, Refunding RB, Series A, 3.00%, 7/01/18 | | | 440 | | | | 460,451 | |

New York Transportation Development Corp., Refunding RB, American Airlines, Inc., AMT,

5.00%, 8/01/18 | | | 1,500 | | | | 1,594,320 | |

Port Authority of New York & New Jersey, ARB, JFK International Air Terminal LLC Project,

5.00%, 12/01/20 | | | 1,200 | | | | 1,375,884 | |

See Notes to Financial Statements.

| | | | | | |

| | | | | | | |

| 16 | | SEMI-ANNUAL REPORT | | JUNE 30, 2016 | | |

| | |

Schedule of Investments (continued) | | BlackRock Municipal 2018 Term Trust (BPK) |

| | | | | | | | |

| Municipal Bonds | | Par

(000) | | | Value | |

New York (continued) | | | | | | | | |

State of New York Dormitory Authority, Refunding RB, Original Regional Medical Center,

5.00%, 12/01/17 (g) | | $ | 1,000 | | | $ | 1,055,640 | |

| | | | | | | | |

| | | | | | | | 14,317,356 | |

North Carolina — 0.9% | | | | | | | | |

North Carolina HFA, Refunding RB, Series 28-A, AMT, 4.65%, 7/01/23 | | | 2,170 | | | | 2,196,778 | |

Pennsylvania — 11.6% | | | | | | | | |

Altoona City Authority, Refunding RB,

5.25%, 11/01/18 | | | 2,500 | | | | 2,741,025 | |

Chester County Health & Education Facilities Authority, Refunding RB: | | | | | | | | |

3.00%, 12/01/17 | | | 585 | | | | 595,203 | |

4.00%, 12/01/18 | | | 805 | | | | 840,307 | |

Cumberland County Municipal Authority, Refunding RB: | | | | | | | | |

4.00%, 1/01/18 | | | 1,380 | | | | 1,439,906 | |

5.75%, 1/01/19 (e) | | | 2,135 | | | | 2,398,054 | |

5.75%, 1/01/19 | | | 240 | | | | 267,475 | |

Lancaster Industrial Development Authority, Refunding RB, Garden Spot Village Project, 5.00%, 5/01/17 | | | 1,175 | | | | 1,201,872 | |

Montgomery County Industrial Development Authority, Refunding RB, 5.00%, 1/15/18 | | | 1,000 | | | | 1,053,570 | |

Pennsylvania Economic Development Financing Authority, RB: | | | | | | | | |

PA Bridges Finco LP, AMT, 5.00%, 12/31/18 | | | 2,100 | | | | 2,301,411 | |

University of Pennsylvania Medical Center,

5.00%, 3/15/18 | | | 750 | | | | 804,765 | |

Waste Management, Inc. Project,

1.55%, 12/01/33 (a) | | | 5,000 | | | | 5,050,650 | |

Pennsylvania Economic Development Financing Authority, Refunding RB, Amtrak Project, Series A, AMT, 3.00%, 11/01/18 | | | 1,000 | | | | 1,035,300 | |

Pennsylvania Higher Educational Facilities Authority, RB, Shippensburg University Student Services, Inc., Student Housing Project: | | | | | | | | |

4.00%, 10/01/17 | | | 275 | | | | 282,282 | |

4.00%, 10/01/18 | | | 560 | | | | 584,035 | |

Pennsylvania Higher Educational Facilities Authority, Refunding RB, Drexel University, Series A,

5.00%, 5/01/18 | | | 1,000 | | | | 1,073,470 | |

Pennsylvania IDA, Refunding RB, Economic Development, 5.00%, 7/01/18 | | | 1,500 | | | | 1,621,485 | |

Pennsylvania Turnpike Commission, RB, Sub-Series A (AGC), 5.00%, 6/01/19 (b) | | | 1,000 | | | | 1,122,130 | |

Philadelphia Gas Works Co., Refunding RB,

4.00%, 8/01/18 | | | 1,790 | | | | 1,905,437 | |

State Public School Building Authority, RB, Community College of Allegheny County Project (AGM),

5.00%, 7/15/18 | | | 900 | | | | 970,245 | |

West Chester Area School District, GO, Refunding, Series AA, 5.00%, 5/15/18 | | | 1,000 | | | | 1,082,110 | |

| | | | | | | | |

| | | | | | | | 28,370,732 | |

Tennessee — 1.2% | | | | | | | | |

Metropolitan Government Nashville & Davidson County Health & Educational Facilities Board, Refunding RB, Lipscomb University Project, Series A, 4.00%, 10/01/18 | | | 260 | | | | 276,637 | |

| | | | | | | | |

| Municipal Bonds | | Par

(000) | | | Value | |

Tennessee (continued) | | | | | | | | |

Tennessee Energy Acquisition Corp., RB: | | | | | | | | |

Series A, 5.25%, 9/01/18 | | $ | 1,040 | | | $ | 1,128,983 | |

Series C, 5.00%, 2/01/18 | | | 1,500 | | | | 1,592,700 | |

| | | | | | | | |

| | | | | | | | 2,998,320 | |

Texas — 12.1% | | | | | | | | |

Birdville ISD Texas, GO, Refunding, CAB (PSF-GTD), 0.00%, 2/15/18 (h) | | | 1,615 | | | | 1,596,250 | |

Central Texas Regional Mobility Authority, Refunding RB, Senior Lien, 5.75%, 1/01/18 (e) | | | 750 | | | | 807,345 | |

City of Dallas Texas, GO, Refunding, 5.00%, 2/15/18 | | | 2,500 | | | | 2,675,700 | |

City of Dallas Texas, Refunding RB, Civic Center Convention Complex (AGC), 5.00%, 8/15/21 | | | 2,500 | | | | 2,783,675 | |

City of Houston Texas, Refunding RB, Sub Lien, Series B, 5.00%, 7/01/18 | | | 1,000 | | | | 1,080,570 | |

Eagle Mountain & Saginaw ISD, GO, Refunding,

5.00%, 8/15/18 | | | 150 | | | | 163,689 | |

Houston ISD Public Facilities Authority, RB,

5.00%, 9/15/18 | | | 5,000 | | | | 5,465,350 | |

Lower Colorado River Authority, Refunding RB, LCRA Transmission, Series B, 5.00%, 5/15/18 | | | 5,000 | | | | 5,399,800 | |

New Hope Cultural Education Facilities Corp., RB, Stephenville LLC Tarleton State University Project, Series A: | | | | | | | | |

4.00%, 4/01/17 | | | 160 | | | | 163,016 | |

4.00%, 4/01/18 | | | 685 | | | | 713,168 | |

4.00%, 4/01/20 | | | 165 | | | | 179,805 | |

North Texas Tollway Authority, Refunding RB, Series C, 5.00%, 1/01/19 | | | 2,215 | | | | 2,445,648 | |

Tarrant County Cultural Education Facilities Finance Corp., Refunding RB, 5.00%, 11/15/18 | | | 1,195 | | | | 1,267,990 | |

Texas Municipal Gas Acquisition & Supply Corp. III, RB, 5.00%, 12/15/18 | | | 4,360 | | | | 4,750,133 | |

| | | | | | | | |

| | | | | | | | 29,492,139 | |

Virginia — 0.9% | | | | | | | | |

City of Norfolk Virginia, Refunding RB, Water Revenue, 5.00%, 11/01/18 | | | 1,230 | | | | 1,352,213 | |

Virginia College Building Authority, Refunding RB, Series A, 5.00%, 7/01/18 (g) | | | 785 | | | | 833,081 | |

| | | | | | | | |

| | | | | | | | 2,185,294 | |

Washington — 1.5% | | | | | | | | |

Energy Northwest, Refunding RB, Wind Project Revenue, 5.00%, 7/01/18 | | | 2,865 | | | | 3,101,219 | |

Washington Health Care Facilities Authority, Refunding RB, Providence Health & Services, Series B,

5.00%, 10/01/18 | | | 500 | | | | 548,025 | |

| | | | | | | | |

| | | | | | | | 3,649,244 | |

Wisconsin — 1.0% | | | | | | | | |

State of Wisconsin, Refunding RB, Series A,

5.00%, 5/01/18 | | | 1,000 | | | | 1,079,200 | |

Wisconsin Health & Educational Facilities Authority, Refunding RB, Froedtert & Community Health, Inc., 5.00%, 4/01/19 | | | 1,265 | | | | 1,408,628 | |

| | | | | | | | |

| | | | | | | | 2,487,828 | |

| Total Municipal Bonds – 99.0% | | | | | | | 241,762,361 | |

See Notes to Financial Statements.

| | | | | | |

| | | | | | | |

| | SEMI-ANNUAL REPORT | | JUNE 30, 2016 | | 17 |

| | |

Schedule of Investments (continued) | | BlackRock Municipal 2018 Term Trust (BPK) |

| | | | | | | | |

Municipal Bonds Transferred to

Tender Option Bond Trusts (i) — 2.2% | | Par

(000) | | | Value | |

Illinois — 2.2% | | | | | | | | |

City of Chicago Illinois Waterworks Revenue, Refunding RB, 2nd Lien (AGM),

5.00%, 11/01/20 (a) | | $ | 5,000 | | | $ | 5,394,950 | |

Total Long-Term Investments

(Cost — $241,430,194) — 101.2% | | | | | | | 247,157,311 | |

| | | | | | | | |

| Short-Term Securities | |

Shares | | | Value | |

BlackRock Liquidity Funds, MuniCash, Institutional Class, 0.26% (j)(k) | | | 502,055 | | | $ | 502,055 | |

Total Short-Term Securities

(Cost — $502,055) — 0.2% | | | | | | | 502,055 | |

| Total Investments (Cost — $241,932,249) — 101.4% | | | | 247,659,366 | |

| Other Assets Less Liabilities — 0.1% | | | | 265,077 | |

Liability for TOB Trust Certificates, Including Interest

Expense and Fees Payable — (1.5)% | | | | (3,754,069 | ) |

| | | | | | | | |

| Net Assets —100.0% | | | | | | $ | 244,170,374 | |

| | | | | | | | |

|

| Notes to Schedule of Investments |

| (a) | | Variable rate security. Rate as of period end. |

| (b) | | U.S. Government securities, held in escrow, are used to pay interest on this security, as well as to retire the bond in full at the date indicated, typically at a premium to par. |

| (c) | | Non-income producing security. |

| (d) | | Issuer filed for bankruptcy and/or is in default of interest payments. |

| (e) | | Security is collateralized by municipal bonds or U.S. Treasury obligations. |

| (f) | | When-issued security. |

| (g) | | Security exempt from registration pursuant to Rule 144A under the Securities Act of 1933, as amended. These securities may be resold in transactions exempt from registration to qualified institutional investors. |

| (i) | | Represent bonds transferred to a TOB Trust in exchange of cash and residual certificates received by the Trust. These bonds serve as collateral in a secured borrowing. See Note 4 of the Notes to Financial Statements for details. |

| (j) | | During the six months ended June 30, 2016, investments in issuers considered to be affiliates of the Trust for purposes of Section 2(a)(3) of the Investment Company Act of 1940, as amended, were as follows: |

| | | | | | | | | | | | | | | | | | | | |

| Affiliate | | Shares Held

at December 31,

2015 | | | Net

Activity | | | Shares Held

at June 30,

2016 | | | Value at

June 30,

2016 | | | Income | |

BlackRock Liquidity Funds, MuniCash, Institutional Class | | | — | | | | 502,055 | | | | 502,055 | | | $ | 502,055 | | | $ | 862 | |

FFI Institutional Tax-Exempt Fund | | | 69 | | | | (69 | ) | | | — | | | | — | | | | 132 | |

Total | | | | | | | | | | | | | | $ | 502,055 | | | $ | 994 | |

| | | | | | | | | | | | | | | | |

| (k) | | Current yield as of period end. |

|

| Fair Value Hierarchy as of Period End |

Various inputs are used in determining the fair value of investments. For information about the Trust’s policy regarding valuation of investments, refer to the Notes to Financial Statements.

The following table summarizes the Trust’s investments categorized in the disclosure hierarchy:

| | | | | | | | | | | | | | | | |

| | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

Assets: | | | | | | | | | | | | | | | | |

| Investments: | | | | | | | | | | | | | | | | |

Long Term Investments1 | | | — | | | $ | 247,157,311 | | | | — | | | $ | 247,157,311 | |

Short-Term Securities | | $ | 502,055 | | | | — | | | | — | | | | 502,055 | |

| | | | |

Total | | $ | 502,055 | | | $ | 247,157,311 | | | | — | | | $ | 247,659,366 | |

| | | | |

1 See above Schedule of Investments for values in each state or political subdivision. | |

The Trust may hold assets and/or liabilities in which the fair value approximates the carrying amount for financial statement purposes. As of period end, TOB Trust Certificates of $3,750,000 are categorized as Level 2 within the disclosure hierarchy.

During the six months ended June 30, 2016, there were no transfers between levels.

See Notes to Financial Statements.

| | | | | | |

| | | | | | | |

| 18 | | SEMI-ANNUAL REPORT | | JUNE 30, 2016 | | |

| | |

Schedule of Investments June 30, 2016 (Unaudited) | | BlackRock New York Municipal 2018 Term Trust (BLH) (Percentages shown are based on Net Assets) |

| | | | | | | | |

| Municipal Bonds | | Par (000) | | | Value | |

New York — 97.7% | | | | | | | | |

Corporate — 1.0% | |

New York Transportation Development Corp., Refunding RB, American Airlines, Inc., AMT, 5.00%, 8/01/18 | | $ | 500 | | | $ | 531,440 | |

County/City/Special District/School District — 40.1% | |

City of New York New York, GO, Refunding, Series A, 5.00%, 8/01/18 | | | 500 | | | | 544,790 | |

City of New York New York, GO: | | | | | | | | |

Sub-Series G-1, 5.00%, 4/01/18 (a) | | | 5,000 | | | | 5,383,450 | |

Sub-Series H-2, 5.00%, 6/01/20 | | | 3,470 | | | | 4,016,664 | |

City of New York New York Industrial Development Agency, ARB, American Airlines, Inc., JFK International Airport Project, AMT, Series B,

2.00%, 8/01/28 (b) | | | 1,530 | | | | 1,528,439 | |

City of New York New York Transitional Finance Authority, RB, Fiscal 2008, Series S-1,

5.00%, 1/15/23 | | | 1,400 | | | | 1,495,018 | |

City of Rochester New York, GO, Refunding,

Series I, 4.00%, 8/15/18 | | | 2,000 | | | | 2,138,200 | |

County of Erie New York Industrial Development Agency, GO: | | | | | | | | |