Effective Use of Structured Products In an Uncertain World February 2009 Erick Goralski Director Structured Investments Deutsche Bank Securities, Inc. |  |

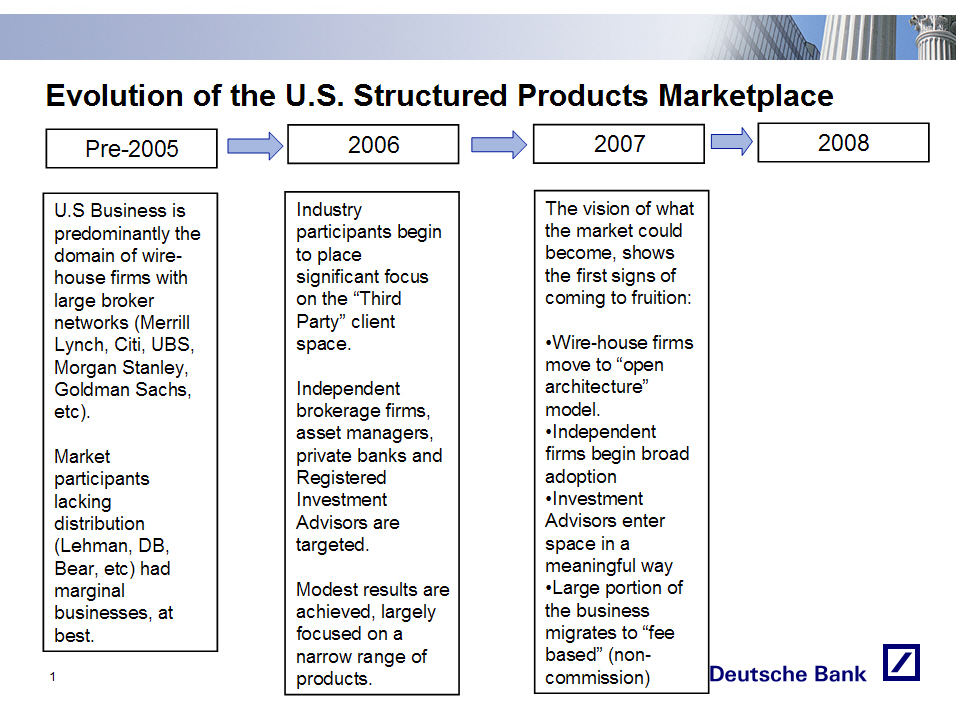

Evolution of the U.S. Structured Products Marketplace

Pre-2005 2006 2007 2008

- -------- ---- ---- ----

U.S Business is Industry The vision of what

predominantly participants begin the market could

the domain of to place become, shows

wire-house significant focus the first signs of

firms with large on the "Third coming to fruition:

broker networks Party" client

(Merrill Lynch, space. o Wire-house firms

Citi, UBS, Morgan move to "open

Stanley, Goldman Independent architecture"

Sachs, etc). brokerage firms, model.

asset managers, o Independent

Market participants private banks and firms begin broad

lacking distribution Registered adoption

(Lehman, DB, Bear, etc) Investment o Investment

had marginal Advisors are Advisors enter

businesses, at best. targeted. space in a

meaningful way

Modest results are o Large portion of

achieved, largely the business

focused on a migrates to "fee

narrow range of based" (non-

products. commission)

|  |

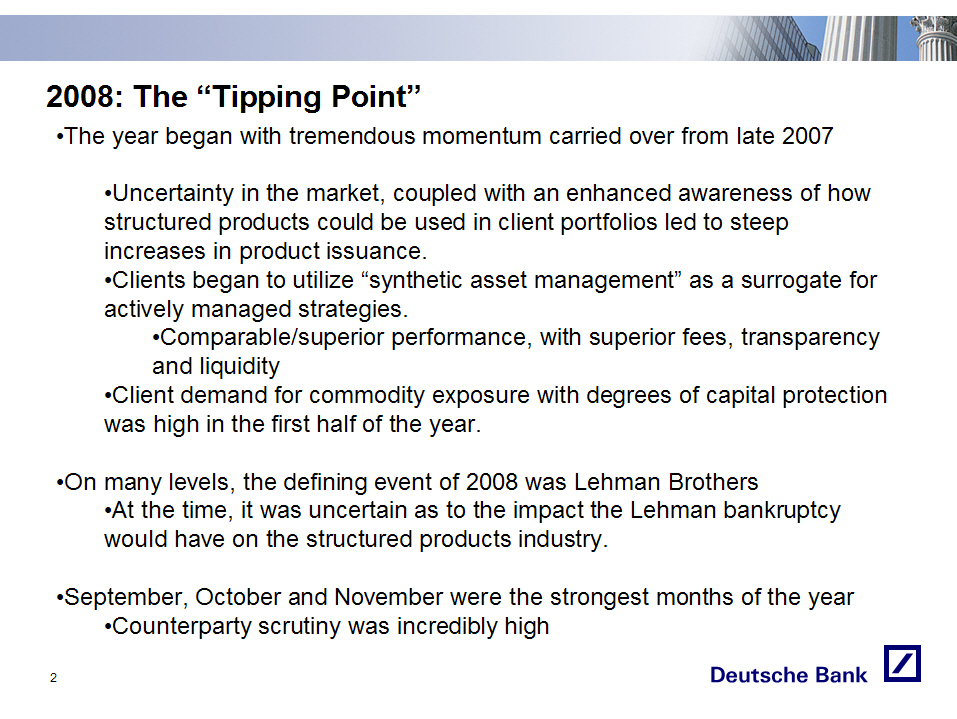

2008: The "Tipping Point"

o The year began with tremendous momentum carried over from late 2007

oUncertainty in the market, coupled with an enhanced awareness of how

structured products could be used in client portfolios led to steep

increases in product issuance.

o Clients began to utilize "synthetic asset management" as a surrogate for

actively managed strategies.

o Comparable/superior performance, with superior fees, transparency

and liquidity

o Client demand for commodity exposure with degrees of capital protection

was high in the first half of the year.

o On many levels, the defining event of 2008 was Lehman Brothers

o At the time, it was uncertain as to the impact the Lehman bankruptcy

would have on the structured products industry.

o September, October and November were the strongest months of the year

o Counterparty scrutiny was incredibly high

|  |

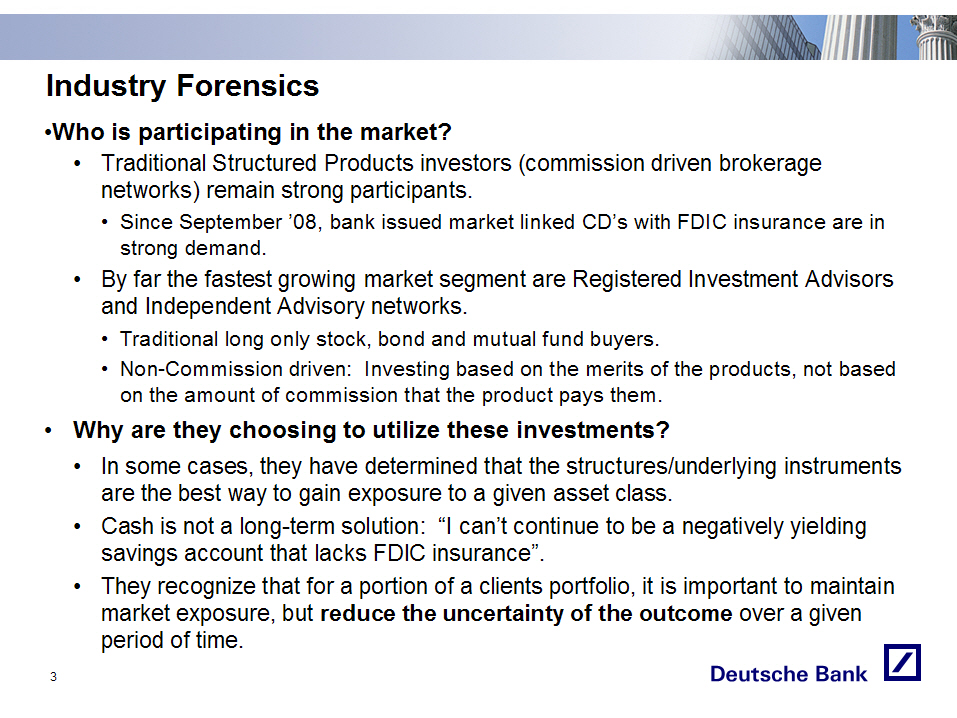

Industry Forensics

o Who is participating in the market?

o Traditional Structured Products investors (commission driven brokerage

networks) remain strong participants.

o Since September 08, bank issued market linked CDs with FDIC insurance

are in strong demand.

o By far the fastest growing market segment are Registered Investment Advisors

and Independent Advisory networks.

o Traditional long only stock, bond and mutual fund buyers.

o Non-Commission driven: Investing based on the merits of the products,

not based on the amount of commission that the product pays them.

o Why are they choosing to utilize these investments?

o In some cases, they have determined that the structures/underlying

instruments are the best way to gain exposure to a given asset class.

o Cash is not a long-term solution: "I can't continue to be a negatively

yielding savings account that lacks FDIC insurance".

o They recognize that for a portion of a clients portfolio, it is

important to maintain market exposure, but reduce the uncertainty of the

outcome over a given period of time.

|  |

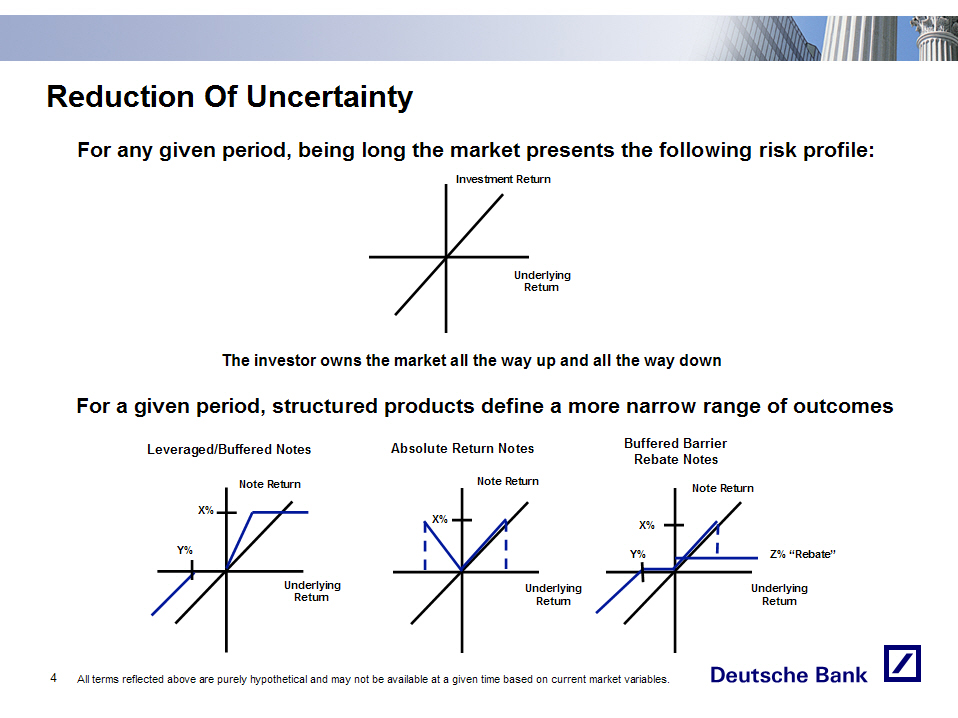

Reduction Of Uncertainty

For any given period, being long the market presents the following risk profile:

Investment Return

Underlying

Return

The investor owns the market all the way up and all the way down

For a given period, structured products define a more narrow range of outcomes

Leveraged/Buffered Notes Absolute Return Notes Buffered Barrier

Rebate Notes

Note Return Note Return Note Return

Underlying Underlying Underlying

Return Return Return

All terms reflected above are purely hypothetical and may not be available at a given time based on current

market variables.

|  |

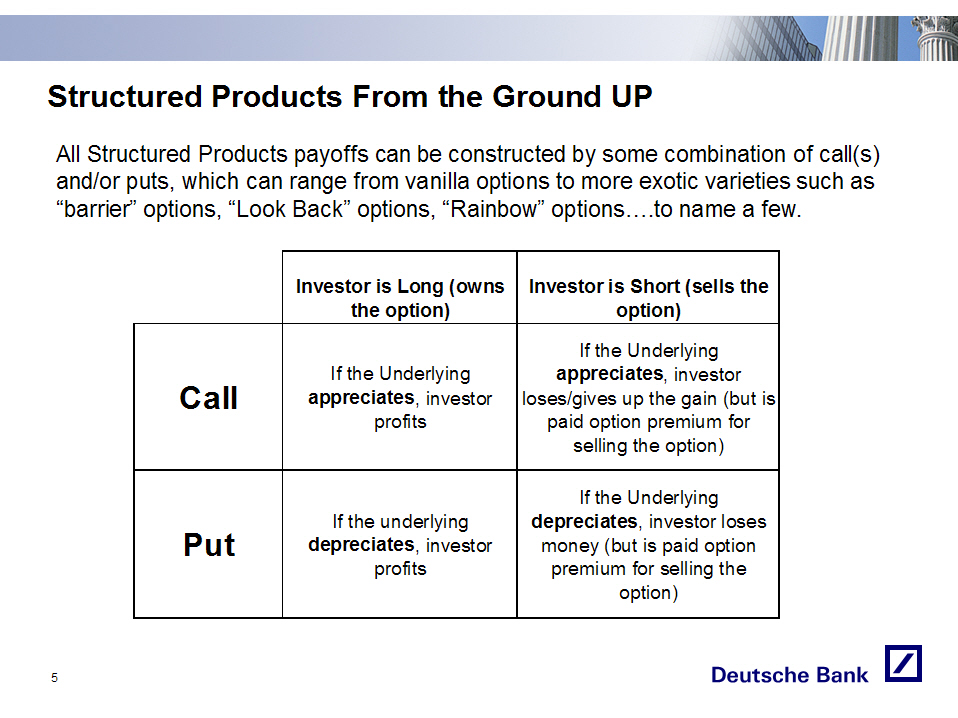

Structured Products From the Ground UP All Structured Products payoffs can be constructed by some combination of call(s) and/or puts, which can range from vanilla options to more exotic varieties such as "barrier" options, "Look Back" options, "Rainbow" options.to name a few. |  |

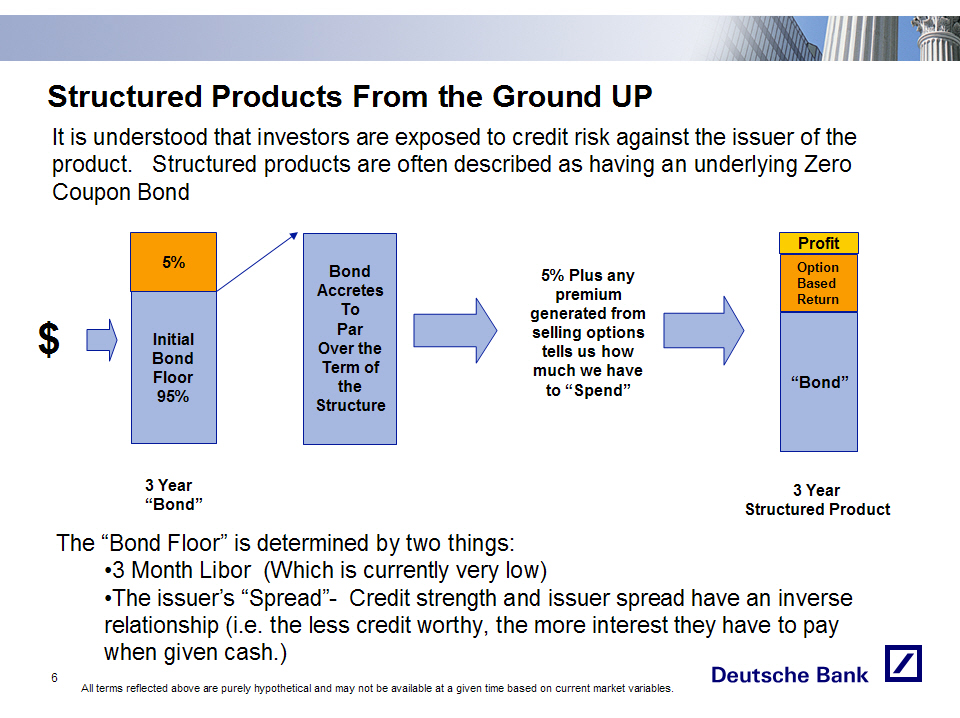

Structured Products From the Ground UP

It is understood that investors are exposed to credit risk against the issuer of the product. Structured

products are often described as having an underlying Zero Coupon Bond

5% Bond 5% Plus any Profit

Accretes premium

Initial To generated from Option

$ Bond Par selling options Based

Floor Over the tells us how Return

95% Term of much we have

the to "Spend" "Bond"

Structure

3 Year 3 Year

"Bond" Structured Product

The "Bond Floor" is determined by two things:

o 3 Month Libor (Which is currently very low)

o The issuer's "Spread"- Credit strength and issuer spread have an inverse

relationship (i.e. the less credit worthy, the more interest they have to

pay when given cash.)

All terms reflected above are purely hypothetical and may not be available

at a given time based on current market variables.

|  |

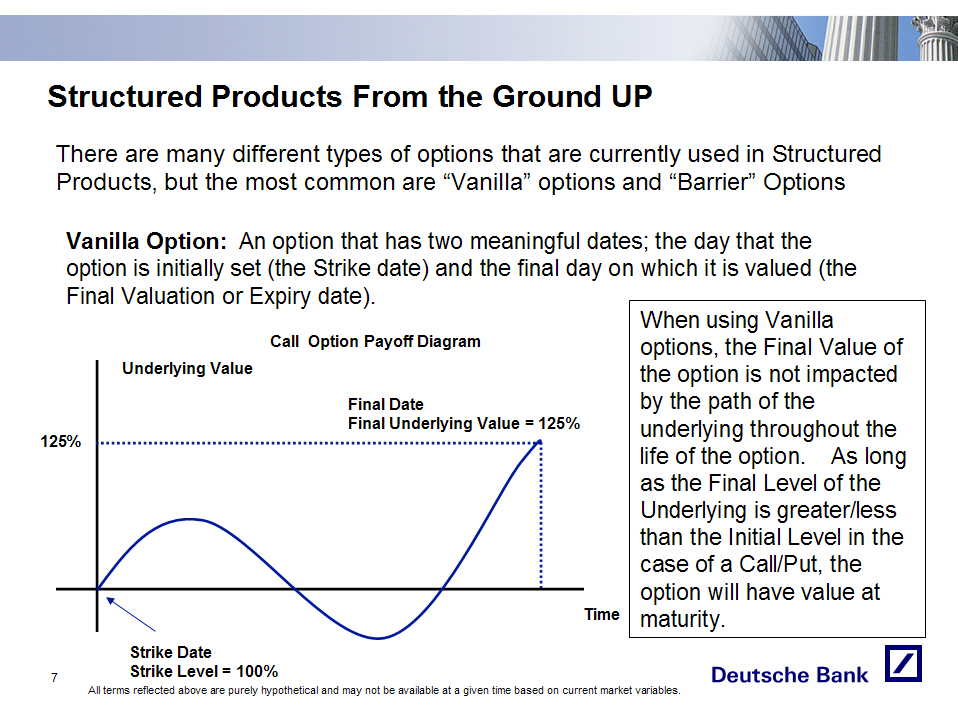

Structured Products From the Ground UP There are many different types of options that are currently used in Structured Products, but the most common are "Vanilla" options and "Barrier" Options Vanilla Option: An option that has two meaningful dates; the day that the option is initially set (the Strike date) and the final day on which it is valued (the Final Valuation or Expiry date). Call Option Payoff Diagram Underlying Value Final Date Final Underlying Value = 125% Strike Date Strike Level = 100% Time When using Vanilla options, the Final Value of the option is not impacted by the path of the underlying throughout the life of the option. As long as the Final Level of the Underlying is greater/less than the Initial Level in the case of a Call/Put, the option will have value at maturity. All terms reflected above are purely hypothetical and may not be available at a given time based on current market variables. |  |

Structured Products From the Ground UP

Barrier Option: Barrier Options introduce the concept of "Path Dependency" of

the underlying. They function in a similar way to Vanilla Options (at maturity),

unless the underlying has moved through a pre-defined point at some point during

the life of the option. If the "barrier crossing" occurs, the option value is

zero at maturity.

Scenario 1 Scenario 2

Underlying Value Underlying Value

Barrier =125% Scenario 1, the barrier Barrier =125%

is never crossed. Barrier

Strike option and Vanilla

=100% option have equal value Barrier is

at maturity. Broken

Time Option Expires

Scenario 2, the barrier is Worthless

broken. At maturity,

Vanilla option captures

the upside of the

market, Barrier option

expires worthless.

All terms reflected above are purely hypothetical and may not be available at a

given time based on current market variables.

|  |

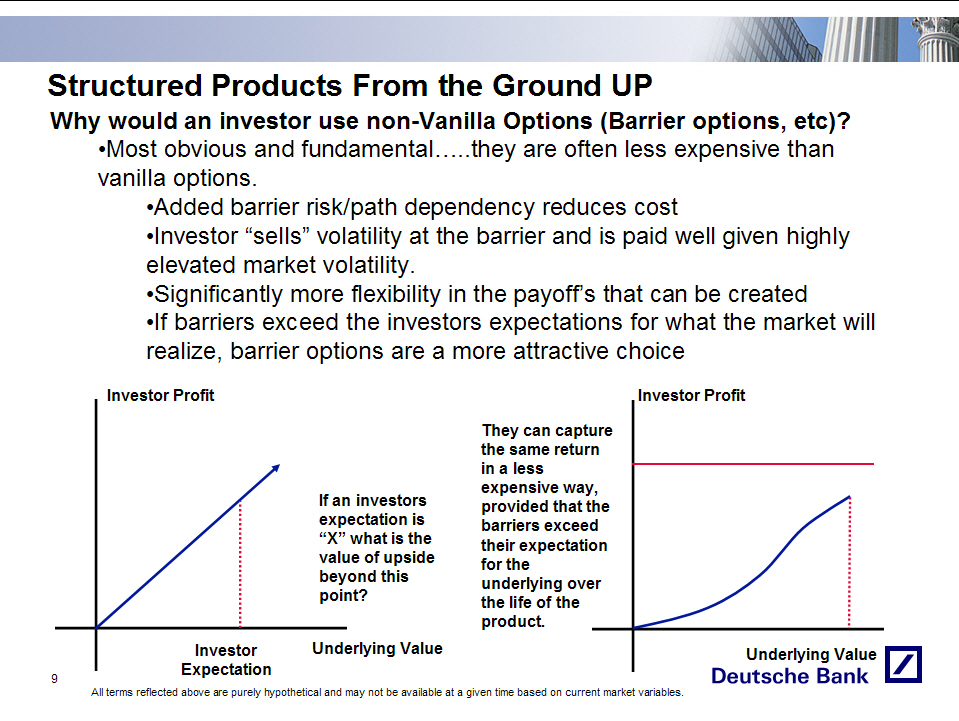

Structured Products From the Ground UP

Why would an investor use non-Vanilla Options (Barrier options, etc)?

o Most obvious and fundamental they are often less expensive than vanilla

options.

o Added barrier risk/path dependency reduces cost

o Investor "sells" volatility at the barrier and is paid well given

highly elevated market volatility.

o Significantly more flexibility in the payoff's that can be created

o If barriers exceed the investors expectations for what the market

will realize, barrier options are a more attractive choice

Investor Profit Investor Profit

If an investors They can capture

expectation is the same return

"X" what is the in a less

value of upside expensive way,

beyond this provided that the

point? barriers exceed

their expectation

Investor for the

Expectation underlying over

the life of the

Underlying Value product. Underlying Value

All terms reflected above are purely hypothetical and may not be available at a

given time based on current market variables.

|  |

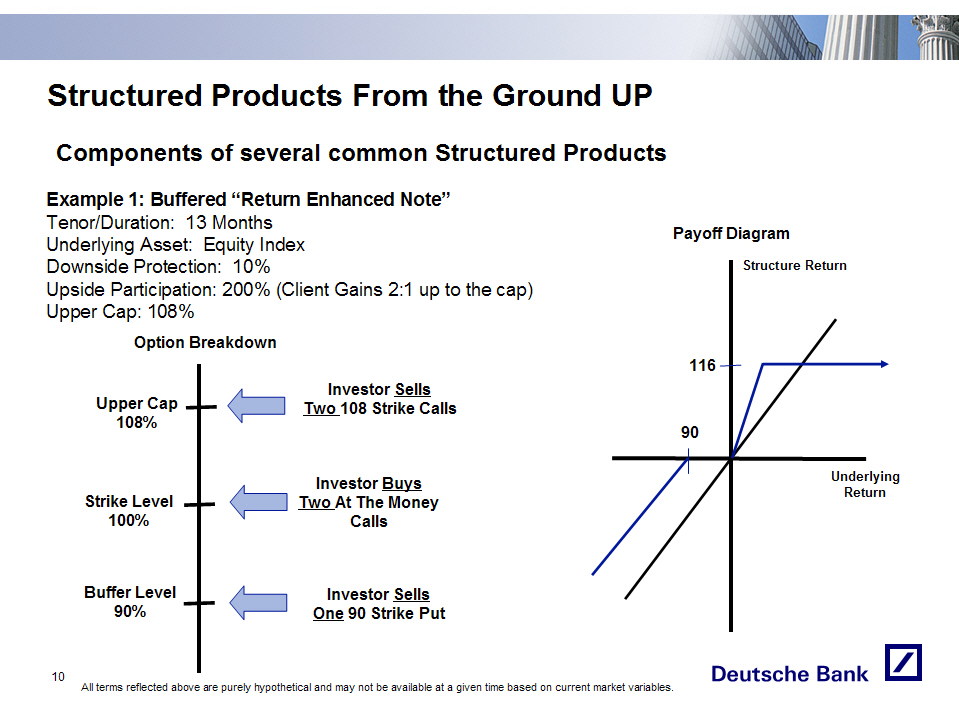

Structured Products From the Ground UP

Components of several common Structured Products

Example 1: Buffered "Return Enhanced Note"

Tenor/Duration: 13 Months

Underlying Asset: Equity Index

Downside Protection: 10%

Upside Participation: 200% (Client Gains 2:1 up to the cap)

Upper Cap: 108%

Option Breakdown

Upper Cap Investor Sells

108% Two 108 Strike Calls

Strike Level Investor Buys

100% Two At The

Money Calls

Buffer Level Investor Sells

90% One 90 Strike Put

All terms reflected above are purely hypothetical and may not be available at a

given time based on current market variables.

|  |

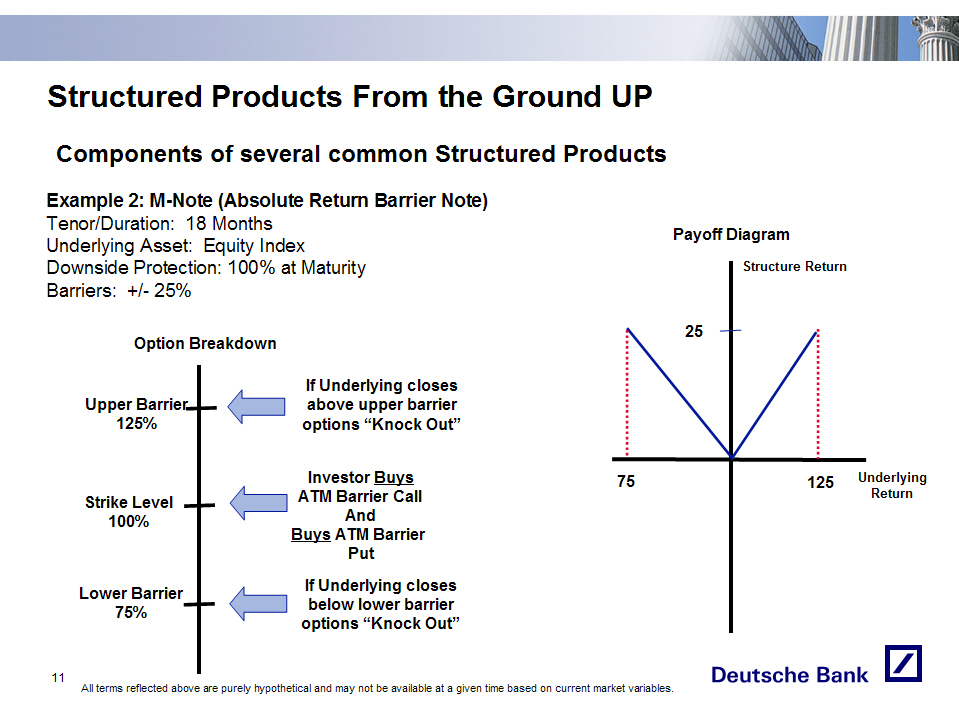

Structured Products From the Ground UP

Components of several common Structured Products

Example 2: M-Note (Absolute Return Barrier Note)

Tenor/Duration: 18 Months

Underlying Asset: Equity Index

Downside Protection: 100% at Maturity

Barriers: +/- 25%

Option Breakdown

Upper Cap If Underlying closes

125% above upper barrier

options "Knock Out"

Strike Level Investor Buys

100% ATM Barrier Call

And Buys ATM

Barrier Put

Buffer Level If Underlying closes

75% below lower barrier

options "Knock Out"

All terms reflected above are purely hypothetical and may not be available at a

given time based on current market variables.

|  |

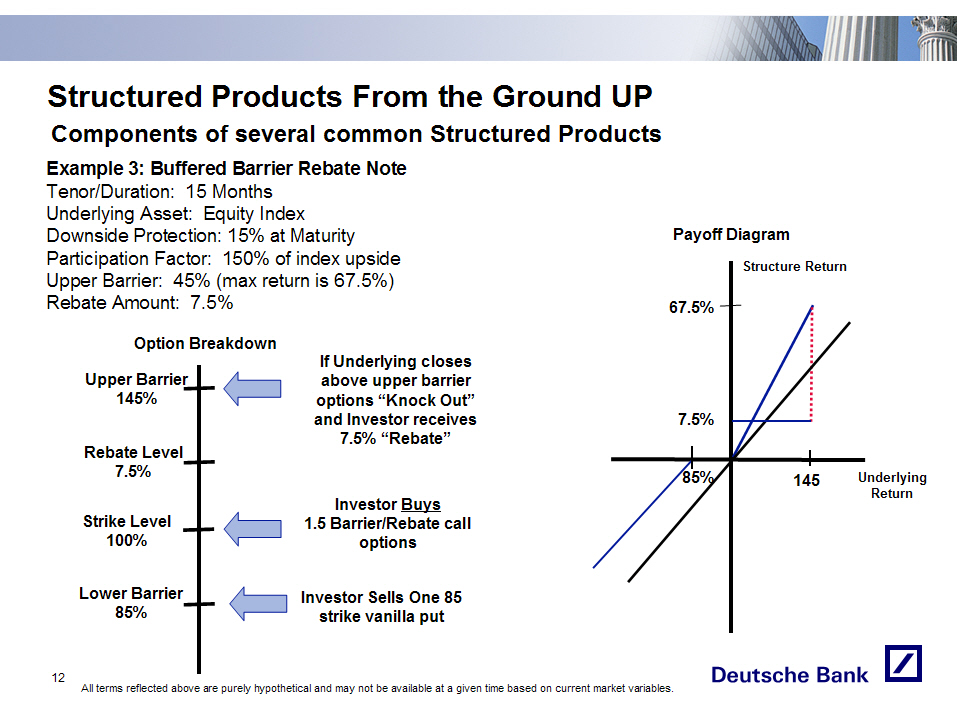

Structured Products From the Ground UP

Components of several common Structured Products

Example 3: Buffered Barrier Rebate Note

Tenor/Duration: 15 Months

Underlying Asset: Equity Index

Downside Protection: 15% at Maturity

Participation Factor: 150% of index upside

Upper Barrier: 45% (max return is 67.5%)

Rebate Amount: 7.5%

Option Breakdown

If Underlying closes

above upper barrier

Upper Barrier options "Knock Out"

145% and Investor receives

7.5% "Rebate"

Rebate Level

7.5%

Investor Buys

Strike Level 1.5 Barrier/Rebate

100% call options

Lower Level Investor Sells One 85

85% strike vanilla put

All terms reflected above are purely hypothetical and may not be available at a

given time based on current market variables.

|  |

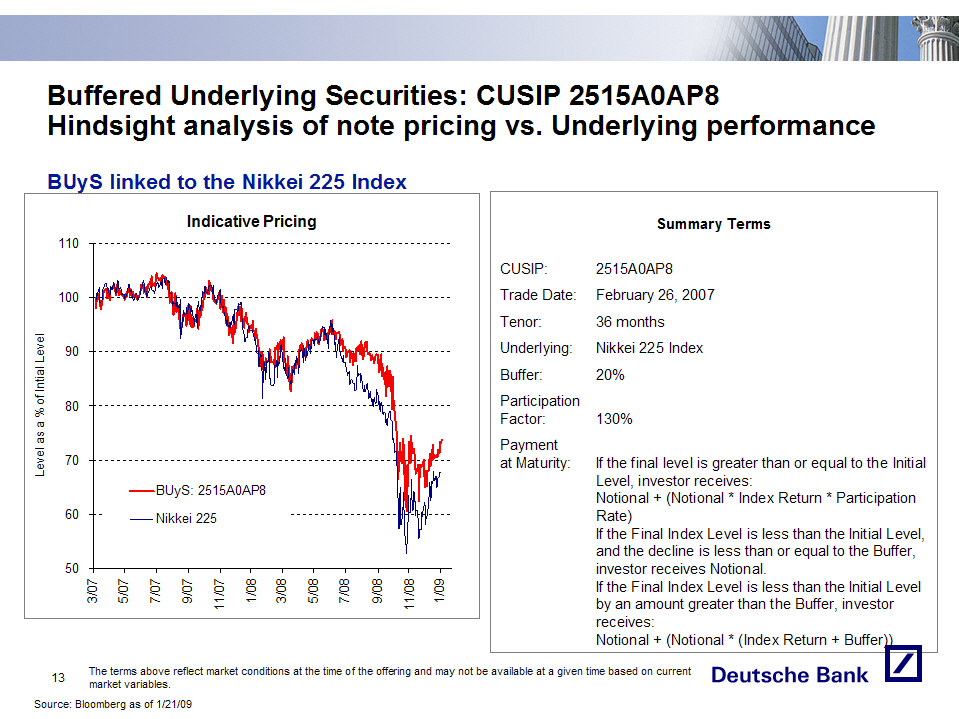

Buffered Underlying Securities: CUSIP 2515A0AP8

Hindsight analysis of note pricing vs. Underlying performance

BUyS linked to the Nikkei 225 Index

Summary Terms

CUSIP: 2515A0AP8

Trade Date: February 26, 2007

Tenor: 36 months

Underlying: Nikkei 225 Index

Buffer: 20%

Participation

Factor: 130%

Payment

at Maturity: If the final level is greater than or equal to the Initial Level,

investor receives:

Notional + (Notional * Index Return * Participation Rate) If the

Final Index Level is less than the Initial Level, and the decline

is less than or equal to the Buffer, investor receives Notional.

If the Final Index Level is less than the Initial Level by an

amount greater than the Buffer, investor receives:

Notional + (Notional * (Index Return + Buffer))

The terms above reflect market conditions at the time of the offering and may

not be available at a given time based on current market variables.

Source: Bloomberg as of 1/21/09

|  |

Absolute Return Barrier Note: CUSIP 25152C643

M-Note linked to the S&P 500 Index

Summary Terms

CUSIP: 25152C643

Trade Date: March 26, 2007

Tenor : 18 months

Underlying: S&P 500 Index

Barrier: +/- 21%

Payment at If Underlying ever trades outside Barriers,

Maturity: 00%

If Underlying never trades outside Barriers, 100% + Absolute

Return

Payment

Made: 117.34% @ maturity

The terms above reflect market conditions at the time of the offering and may

not be available at a given time based on current market variables.

Source: Bloomberg as of 09/23/08

|  |

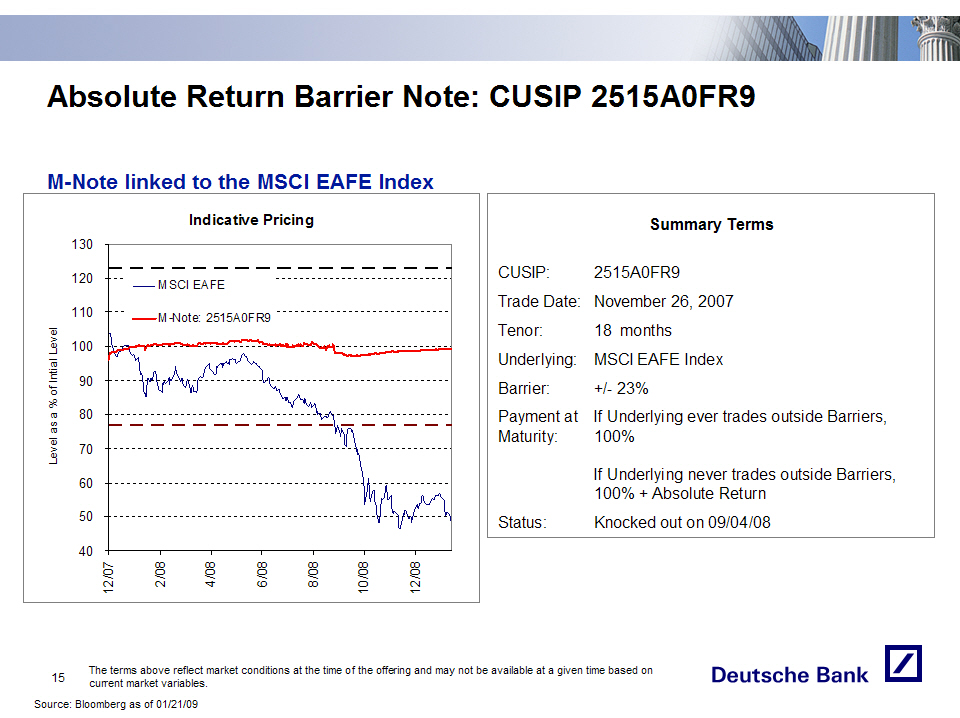

Absolute Return Barrier Note: CUSIP 2515A0FR9

M-Note linked to the MSCI EAFE Index

Summary Terms

CUSIP: 2515A0FR9

Trade Date: November 26, 2007

Tenor: 18 months

Underlying: MSCI EAFE Index

Barrier: +/- 23%

Payment at If Underlying ever trades outside Barriers,

Maturity: 100%

If Underlying never trades outside Barriers, 100% + Absolute

Return

Status: Knocked out on 09/04/08

The terms above reflect market conditions at the time of the offering and may

not be available at a given time based on current market variables.

Source: Bloomberg as of 01/21/09

|  |

Indicative Performance Calculations o Indicative Pricing for all Deutsche Bank Structured Equity Notes are based off of bid levels posted by Deutsche Bank on Bloomberg that reflect indicative unwind levels for a limited notional amount of a given note (generally up to $1,000,000). The indicative bid levels posted on Bloomberg include accrued interest, if any, for a given security. o Actual unwind levels may vary from the indicative bid levels posted on Bloomberg depending on many factors that include actual unwind notional amount, current volatility of the underlier, liquidity in the market, Deutsche Bank's creditworthiness, and Deutsche Bank's profit and loss amortization assumptions. o Deutsche Bank's upfront fees (if any) are amortized over a portion of the life of the trade. Indicative bid levels posted on Bloomberg may not reflect the true fair value of a given security. o Indicative Note Performance is calculated using the underlying stock performance and accrued interest (if any) during the given time frame o Stock total return is calculated using stock price and dividends (if any) paid out to investors during the given timeframe |  |

Risk Factors oAn investment in the securities described herein may result in a loss, and any payment is subject to our creditworthiness o Certain built-in costs are likely to adversely affect the value of the securities prior to maturity o You have no periodic coupon or dividend payments or voting rights o The securities will not be listed and there will likely be limited liquidity o Our research, opinions or recommendations could affect the level of the underlyings or the market value of the securities o Our actions as calculation agent of the securities and our hedging activity may adversely affect the value of the securities o Many economic and market factors will affect the value of the securities |  |

Disclaimer Copyright 2009 Deutsche Bank Securities Inc. All rights reserved. "Deutsche Bank" means Deutsche Bank AG and its affiliated companies, as the context requires. The distribution of this document and the availability of some of the products and services referred to herein may be restricted by law in certain jurisdictions. Some products and services referred to herein are not eligible for sale in all countries and in any event may only be sold to qualified investors. Deutsche Bank will not offer or sell any products or services to any persons prohibited by the law in their country of origin or in any other relevant country from engaging in any such transactions. Deutsche Bank or persons associated with Deutsche Bank an their affiliates may maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, trade instruments economically related to or have investment banking or other relationships with the issuers of or engage in any other transaction involving such securities, and earn brokerage or other compensation. Any transaction that may involve the products, services and strategies referred to in this presentation will involve risks. You could lose your entire investment or incur substantial loss. The products, services and strategies referred to herein may not be suitable for all investors. The information contained in this presentation is being provided on the basis that you have such knowledge and experience in financial and business matters to be capable of evaluating the merits and risks associated with such information. In contemplating any transaction, you should consult with your own investment advisors. In any discussion of a proposed transaction, Deutsche Bank would act at arms length and not in any advisory or fiduciary capacity. The information contained in this presentation does not represent the rendering of accounting, tax, legal or regulatory advice. It cannot be used or relied upon for purposes of avoiding compliance with any accounting, tax, legal or regulatory obligations or avoiding satisfaction of any U.S. federal income tax penalties. You should consult with independent accounting, tax, legal and regulatory counsel regarding such matters as they may apply to your particular circumstances. Foreign currency rates of exchange may adversely affect the value, price or income of any security or investment. Past performance is no guarantee of future results. Backtested, hypothetical or simulated performance results discussed herein have inherent limitations. Unlike an actual performance record based on trading actual client portfolios, simulated results are achieved by means of the retroactive application of a backtested model itself designed with the benefit of hindsight. Taking into account historical events the backtesting of performance also differs from actual account performance because an actual investment strategy may be adjusted any time, for any reason, including a response to material, economic or market factors. The backtested performance includes hypothetical results that do not reflect the reinvestment of dividends and other earnings or the deduction of advisory fees, brokerage or other commissions, and any other expenses that a client would have paid or actually paid. No representation is made that any trading strategy or account will or is likely to achieve profits or losses similar to those shown. Alternative modeling techniques or assumptions might produce significantly different results and prove to be more appropriate. Past hypothetical backtest results are neither an indicator nor guarantee of future returns. Actual results will vary, perhaps materially, from the analysis. Results represent the performance of each basket on a back tested basis, tied to a structure whose economics are determined by current economic factors such as current volatilities and interest rates. There is no guarantee that a similar structure would have been available at any point in the past and that such results could have been achieved. Options, structured securities and illiquid investments, such as private investments, are complex instruments and are not be suitable for all investors. Prior to buying or selling an option investors must review the Characteristics and Risks of Standardized Options: http://onn.theocc.com/publications/risks/riskstoc.pdf If you are unable to access the website please contact Deutsche Bank AG at +1 (212) 250-6248 for a copy of this important document. These investments typically involve a high degree of risk, are not transferable and typically will not be listed or traded on any exchange and are intended for sale only to sophisticated investors who are capable of understanding and assuming the risks involved. The market value of any structured security may be affected by changes in economic, financial and political factors (including, but not limited to, spot and forward interest and exchange rates), time to maturity, market conditions and volatility and the equity prices and credit quality of any issuer or reference issuer. Any investor should conduct his/her own investigation and analysis of the product and consult with its own professional advisers as to the risks involved in making such a purchase; since, it may be difficult to realize the investment prior to maturity, obtain reliable information about the market value of such investments or the extent of the risks to which they are exposed, including the risk of total loss of capital. |  |

Disclaimer (con't) Calculations of returns on instruments referred to herein may be linked to a referenced index or interest rate. In such cases, the investments may not be suitable for persons unfamiliar with such index or interest rate, or unwilling or unable to bear the risks associated with the transaction. Products denominated in a currency, other than the investor's home currency, will be subject to changes in exchange rates, which may have an adverse effect on the value, price or income return of the products. These products may not be readily realizable investments and are not traded on any regulated market. The securities referred to herein involve risk, which may include interest rate, index, currency, credit, political, liquidity, time value, commodity and market risk and is not suitable for all investors. These instruments are not bank deposits and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency. These instruments are not guaranteed under the Federal Deposit Insurance Corporation's Temporary Liquidity Guarantee Program. These instruments are not insured by any statutory scheme or governmental agency of the United Kingdom. The distribution of this document and availability of these products and services in certain jurisdictions may be restricted by law. Deutsche Bank AG has filed a registration statement (including a prospectus) with the Securities and Exchange Commission, or SEC, for offerings to which this communication relates. Before you invest, you should read the prospectus in that registration statement and the other documents relating to such offering that Deutsche Bank AG has filed with the SEC for more complete information about Deutsche Bank AG and the offering. You may obtain these documents without cost by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, Deutsche Bank AG, any agent or any dealer participating in the offering will arrange to send you the prospectus if you so request by calling toll-free 1-800-311-4409. |  |