|

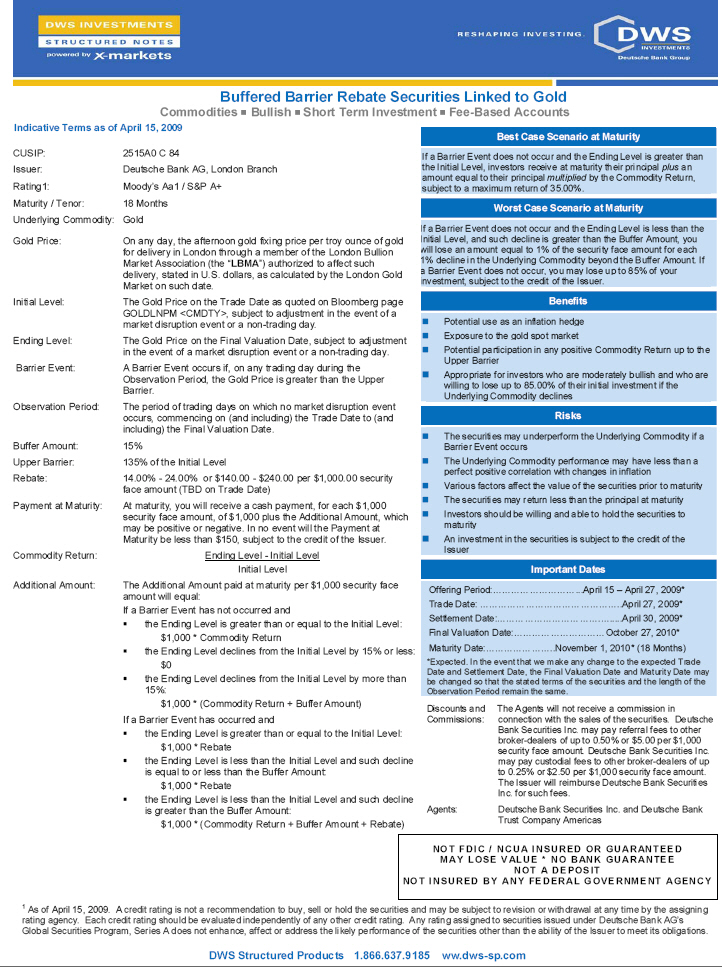

Buffered Barrier Rebate Securities Linked to Gold

Commodities |X| Bullish |X| Short Term Investment |X| Fee-Based Accounts

Indicative Terms as of April 15, 2009

CUSIP: 2515A0 C 84

Issuer: Deutsche Bank AG, London Branch

Rating1: Moody's Aa1 / S&P A+

Maturity / Tenor: 18 Months

Underlying Commodity: Gold

Gold Price: On any day, the afternoon gold fixing price per troy

ounce of gold for delivery in London through a member of

the London Bullion Market Association (the "LBMA")

authorized to affect such delivery, stated in U.S.

dollars, as calculated by the London Gold Market on such

date.

Initial Level: The Gold Price on the Trade Date as quoted on Bloomberg

page GOLDLNPM CMDTY, subject to adjustment in the event

of a market disruption event or a non-trading day.

Ending Level: The Gold Price on the Final Valuation Date, subject to

adjustment in the event of a market disruption event or a

non-trading day.

Barrier Event: A Barrier Event occurs if, on any trading day during

the Observation Period, the Gold Price is greater

than the Upper Barrier.

Observation Period: The period of trading days on which no market disruption

event occurs, commencing on (and including) the Trade

Date to (and including) the Final Valuation Date.

Buffer Amount: 15%

Upper Barrier: 135% of the Initial Level

Rebate: 14.00% - 24.00% or $140.00 - $240.00 per $1,000.00

security face amount (TBD on Trade Date)

Payment at Maturity: At maturity, you will receive a cash payment, for each

$1,000 security face amount, of $1,000 plus the

Additional Amount, which may be positive or negative. In

no event will the Payment at Maturity be less than $150,

subject to the credit of the Issuer.

Commodity Return: Ending Level - Initial Level

Initial Level

Additional Amount: The Additional Amount paid at maturity per $1,000

security face amount will equal:

If a Barrier Event has not occurred and

|X| the Ending Level is greater than or equal to the

Initial Level:

$1,000 * Commodity Return

|X| the Ending Level declines from the Initial Level

by 15% or less:

$0

|X| the Ending Level declines from the Initial Level

by more than 15%:

$1,000 * (Commodity Return + Buffer Amount)

If a Barrier Event has occurred and

|X| the Ending Level is greater than or equal to the

Initial Level:

$1,000 * Rebate

|X| the Ending Level is less than the Initial Level

and such decline is equal to or less than the

Buffer Amount:

$1,000 * Rebate

|X| the Ending Level is less than the Initial Level

and such decline is greater than the Buffer Amount:

$1,000 * (Commodity Return + Buffer Amount + Rebate)

- -------------------------------------------------------------

Best Case Scenario at Maturity

- -------------------------------------------------------------

If a Barrier Event does not occur and the Ending Level is

greater than the Initial Level, investors receive at

maturity their principal plus an amount equal to their

principal multiplied by the Commodity Return, subject to a

maximum return of 35.00%.

- -------------------------------------------------------------

Worst Case Scenario at Maturity

- -------------------------------------------------------------

If a Barrier Event does not occur and the Ending Level is

less than the Initial Level, and such decline is greater

than the Buffer Amount, you will lose an amount equal to 1%

of the security face amount for each 1% decline in the

Underlying Commodity beyond the Buffer Amount. If a Barrier

Event does not occur, you may lose up to 85% of your

investment, subject to the credit of the Issuer.

|X|

- -------------------------------------------------------------

Benefits

- -------------------------------------------------------------

|X| Potential use as an inflation hedge

|X| Exposure to the gold spot market

|X| Potential participation in any positive Commodity

Return up to the Upper Barrier

|X| Appropriate for investors who are moderately

bullish and who are willing to lose up to 85.00% of

their initial investment if the Underlying Commodity

declines

- -------------------------------------------------------------

Risks

- -------------------------------------------------------------

|X| The securities may underperform the Underlying

Commodity if a Barrier Event occurs

|X| The Underlying Commodity performance may have less

than a perfect positive correlation with changes in

inflation

|X| Various factors affect the value of the securities

prior to maturity

|X| The securities may return less than the principal

at maturity

|X| Investors should be willing and able to hold the

securities to maturity

|X| An investment in the securities is subject to the

credit of the Issuer

- -------------------------------------------------------------

Important Dates

- -------------------------------------------------------------

Offering Period:.....................April 15 - April 27, 2009*

Trade Date: .........................April 27, 2009*

Settlement Date:.....................April 30, 2009*

Final Valuation Date:................October 27, 2010*

Maturity Date:.......................November 1, 2010* (18 Months)

*Expected. In the event that we make any change to the

expected Trade Date and Settlement Date, the Final

Valuation Date and Maturity Date may be changed so that the

stated terms of the securities and the length of the

Observation Period remain the same.

- -------------------------------------------------------------

Discounts and The Agents will not receive a commission in

Commissions: connection with the sales of the securities. Deutsche Bank

Securities Inc. may pay referral fees to other broker-dealers of

up to 0.50% or $5.00 per $1,000 security face amount. Deutsche

Bank Securities Inc. may pay custodial fees to other broker-

dealers of up to 0.25% or $2.50 per $1,000 security face amount.

The Issuer will reimburse Deutsche Bank Securities Inc. for such

fees.

Agents: Deutsche Bank Securities Inc. and Deutsche Bank Trust Company

Americas

NOT FDIC / NCUA INSURED OR GUARANTEED

MAY LOSE VALUE * NO BANK GUARANTEE

NOT A DEPOSIT

NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY

As of April 15, 2009. A credit rating is not a recommendation to buy, sell or

hold the securities and may be subject to revision or withdrawal at any time by

the assigning rating agency. Each credit rating should be evaluated

independently of any other credit rating. Any rating assigned to securities

issued under Deutsche Bank AG's Global Securities Program, Series A does not

enhance, affect or address the likely performance of the securities other than

the ability of the Issuer to meet its obligations.

DWS Structured Products 1.866.637.9185 ww.dws-sp.com

|

Buffered Barrier Rebate Fact Sheet

DWS Structured Products

| Return Scenarios at Maturity (Assumes an Upper Barrier of 135% and a Rebate of 19.00%) | |||||

| If a Barrier Event Does Not Occur | A Barrier Event Does Occur | ||||

| Underlying Commodity Return | Barrier Security Return | Payment at Maturity (per $1,000 invested) | Commodity Return | Barrier Security Return | Payment at Maturity (per $1,000 invested) |

| -35.00% | -20.00% | $800.00 | -35.00% | -1.00% | $990.00 |

| -30.00% | -15.00% | $850.00 | -30.00% | 4.00% | $1,040.00 |

| -20.00% | -5.00% | $950.00 | -20.00% | 14.00% | $1,140.00 |

| -10.00% | 0.00% | $1,000.00 | -10.00% | 19.00% | $1,190.00 |

| 0.00% | 0.00% | $1,000.00 | 0.00% | 19.00% | $1,190.00 |

| 10.00% | 10.00% | $1,100.00 | 10.00% | 19.00% | $1,190.00 |

| 20.00% | 20.00% | $1,200.00 | 20.00% | 19.00% | $1,190.00 |

| 30.00% | 30.00% | $1,300.00 | 30.00% | 19.00% | $1,190.00 |

| 35.00% | 35.00% | $1,350.00 | 35.00% | 19.00% | $1,190.00 |

This hypothetical scenario analysis does not reflect advisory fees, brokerage or other commissions, or any other expenses that an investor may incur in connection with the securities. No representation is made that any trading strategy or account will, or is likely to, achieve similar returns to those shown above. Hypothetical results are neither an indicator nor guarantee of future returns. Actual results will vary, perhaps materially, from this analysis. The numbers appearing in the above table have been rounded for ease of analysis.

Selected Risk Factors |

MARKET RISK - The return on the securities at maturity, if any, is linked to the performance of the Underlying Commodity and will depend on whether the Underlying Commodity ever exceeds the Upper Barrier on any trading day during the Observation Period, the magnitude of the Commodity Return, and if any decline in the Underlying Commodity exceeds the Buffer Amount. THE SECURITIES MAY PAY LESS THAN THE PRINCIPAL AMOUNT - You may receive a lower payment at maturity than you would have received if you had invested in the Underlying Commodity. If the Underlying Commodity Level exceeds the Upper Barrier on any trading day during the Observation Period and at maturity, the Ending Level is less than the Initial Level, and such decline is greater than Buffer Amount, the securities will not guarantee any return in excess of a payment of between $290.00 and $390.00 (to be determined on Trade Date) per $1,000 security face amount. If the Gold Price does not exceed the Upper Barrier on any trading day during the Observation Period and at maturity, the Ending Level is less than the Initial Level, and such decline is greater than the Buffer Amount, the securities will not guarantee any return in excess of $150.00 per $1,000 security face amount, subject to the credit of the Issuer. THE BARRIER FEATURE WILL LIMIT YOUR RETURN ON THE SECURITIES AND MAY AFFECT YOUR PAYMENT AT MATURITY - Your investment in the securities may not perform as well as an investment in a security with an uncapped return based solely on the performance of the Underlying Commodity. CERTAIN BUILT-IN COSTS ARE LIKELY TO ADVERSELY AFFECT THE VALUE OF THE SECURITIES PRIOR TO MATURITY - Certain built-in costs, such as our estimated cost of hedging, are likely to adversely affect the value of the securities prior to maturity. You should be willing and able to hold your securities to maturity. OUR ACTIONS AS CALCULATION AGENT AND OUR HEDGING ACTIVITY MAY ADVERSELY AFFECT THE VALUE OF THE SECURITIES - We and our affiliates and agents may publish research, express opinions or provide recommendations that are inconsistent with investing in or holding the securities, any such research, opinions or recommendations could affect the level of the Underlying Commodity or the market value of the securities. THE RISKS OF INVESTING IN COMMODITIES CAN BE SUBSTANTIAL - The price of the Underlying Commodity may be affected by numerous market factors, including events in the equity markets, the bond market and the foreign exchange market, fluctuations in interest rates, and world economic, political, and regulatory events. MANY ECONOMIC AND MARKET FACTORS WILL IMPACT THE VALUE OF THE SECURITIES - In addition to the Gold Price on any day, the value of the securities will be affected by a number of complex and interrelated economic and market factors that may either offset or magnify each other. COUNTERPARTY RISK - The payment of amounts owed to you under the securities is subject to the Issuer’s ability to pay. Consequently, you are subject to counterparty risk and are susceptible to risks relating to the creditworthiness of Deutsche Bank AG. | POTENTIAL CONFLICTS - We and our affiliates play a variety of roles in connection with the issuance of the securities, including acting as calculation agent and hedging our obligations under the securities. In performing duties, the economic interests of the calculation agent and other affiliates of ours are potentially adverse to your interests as an investor in the securities. LACK OF LIQUIDITY – There may be little or no secondary market for the securities. The securities will not be listed on any securities exchange. SIINGLE COMMODITY PRICES TEND TO BE MORE VOLATLE AND MAY NOT CORRELATE WITH THE PRICES OF COMMODITIES GENERALLY - The payment at maturity on the securities is linked exclusively to the Underlying Commodity and not to a diverse basket of commodities or a broad-based commodity index. The Underlying Commodity may not correlate to the price of commodities generally and may diverge significantly from the price of commodities generally. Because the securities are linked to the price of a single Underlying Commodity, they carry greater risk and may be more volatile than a security linked to the prices of multiple commodities or a broad-based commodity index THE U.S. TAX CONSEQUENCES OF AN INVESTMENT IN THE SECURITIES ARE UNCLEAR - Significant aspects of the U.S. federal income tax treatment of the securities are uncertain, and no assurance can be given that the Internal Revenue Service will accept, or a court will uphold, the tax consequences described in the accompanying term sheet. See “Selected Risk Considerations” in the accompanying term sheet and “Risk Factors” in the accompanying product supplement for additional information. Deutsche Bank AG has filed a registration statement (including a prospectus) with the Securities and Exchange Commission, or SEC, for the offering to which this fact sheet relates. Before you invest, you should read the prospectus in that registration statement and the other documents including term sheet No. 642AX and the product supplement relating to this offering that Deutsche Bank AG has filed with the SEC for more complete information about Deutsche Bank AG and this offering. You may obtain these documents without cost by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, Deutsche Bank AG, any agent or any dealer participating in this offering will arrange to send you the prospectus, prospectus supplement, product supplement, term sheet No. 642AX and this fact sheet if you so request by calling toll-free 1-800-311-4409. You may revoke your offer to purchase the securities at any time prior to the time at which we accept such offer by notifying the applicable agent. We reserve the right to change the terms of, or reject any offer to purchase, the securities prior to their issuance. We will notify you in the event of any changes to the terms of the securities, and you will be asked to accept such changes in connection with your purchase of any securities. You may also choose to reject such changes, in which case we may reject your offer to purchase the securities. |

ISSUER FREE WRITING PROSPECTUS

Filed Pursuant to Rule 433

Registration Statement No. 333-137902

Dated April 15, 2009 R-9899-1 (02/09)

DWS Structured Products 1.866.637.9185 ww.dws-sp.com