| Deutsche Bank Commodity Indices June 2009 Registration Statement No. 333-137902 Dated June 5, 2009; Filed pursuant to Rule 433 Deutsche Bank AG has filed a registration statement (including a prospectus) with the Securities and Exchange Commission, or SEC, for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents that Deutsche Bank AG has filed with the SEC for more complete information about Deutsche Bank AG and this offering. You may obtain these documents without cost by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, Deutsche Bank AG, any agent or any dealer participating in the offering will arrange to send you the prospectus if you so request by calling toll-free 1-800-311-4409. |

| Contents 1 Executive Summary 2 Beta Commodity Indices 3 Enhanced Beta Commodity Indices 4 Alpha Commodity Indices 5 Commodity Index Comparative Performance 2 |

|

Executive Summary

The Evolution of Commodity Markets

- - Commodities have been accepted by investors as an asset class in its own

right, suitable for absolute returns and portfolio diversification. Optimal

use of commodities can not only enhance returns, but also reduce overall

volatility in an investment portfolio

- - The primary way most investors have been accessing the asset class is

through commodity indices. They provide a diversified, easy, and quick way

to get an exposure to the asset class

- - However, commodities represent a unique asset class with some

characteristics that need to be considered. As the market has evolved,

Deutsche Bank has created new indices to try to capture the special

features of the asset class

- - Deutsche Bank is a provider of non-benchmark commodity indices and provides

a comprehensive suite of commodity index products aimed at enhancing beta

returns and extracting market-neutral alpha returns in the commodity space

3

|

|

Executive Summary

Commodity Index FAQ

- - Why use Commodity Indices?

- Simple Asset Allocation Solution -- Investment in a broad based

commodity index provides exposure to multiple sectors through one

convenient vehicle

- "Rule Based" Index Returns -- formula- driven commodity indices help

to eliminate active manager risks such as style drift and key-man

concerns that may be associated with investments in partnerships and

managed accounts

- Pure Commodity Exposure to Eliminate Corporate Risk -- Equity

ownership through commodity-producing firms carries corporate

performance risk / reward factor unrelated to the price of the

commodity itself

- Greater Liquidity -- Commodity Index based investments, such as

structured notes, may provide greater liquidity than other investments

such as investment partnerships or ownership of physical assets

- - How does a Commodity Index Work? What are the features of Commodity

Indices?

- Commodity indices include different underlying commodities in

different proportions. For example, the S&PGSCI is heavily weighted

towards the energy sector

- Most commodity indices are long only, but there are some which allow

for short positions. For example, the DB Commodity Harvest has both

long and short positions for each underlying commodity

- Commodity indices are made up of futures contracts, and the method in

which these contracts are bought and sold as contracts approach expiry

is called "Rolling".

Depending on the prices in the futures market, there may be gains and

losses associated with this rolling process, known as Roll Yield

- All commodity Indices have a Roll Yield because they are constructed

from futures contracts. But different Commodity Indices have different

Roll Yields because of the mix of underlying commodities they hold and

the different index rules for rolling futures contracts

4

|

|

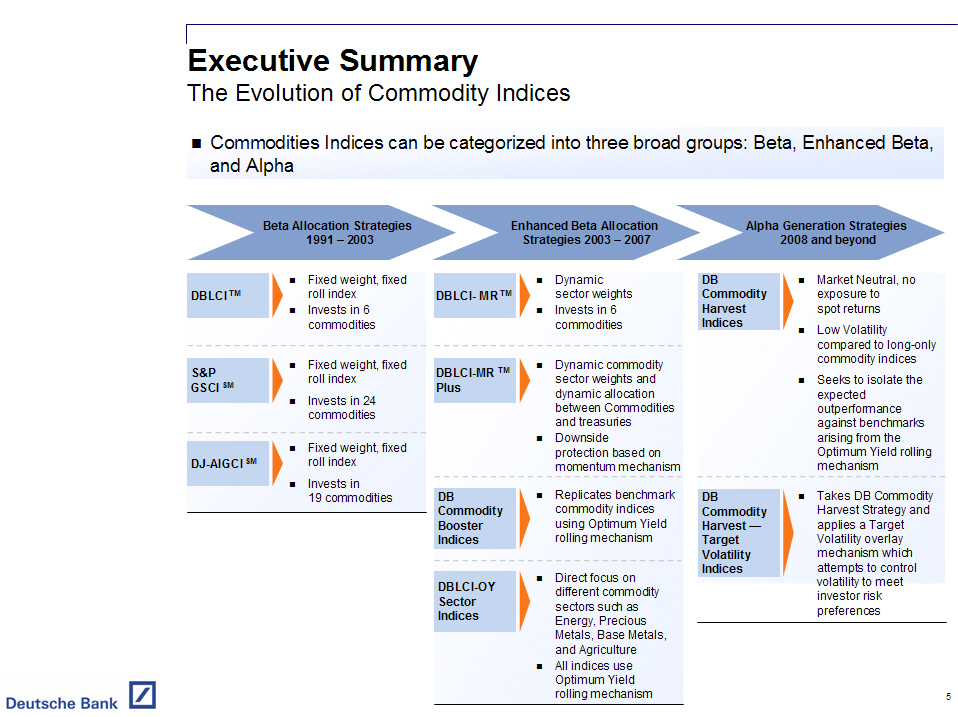

Executive Summary

The Evolution of Commodity Indices

- - Commodities Indices can be categorized into three broad groups: Beta,

Enhanced Beta, and Alpha

[GRAPHIC OMITTED]

5

|

|

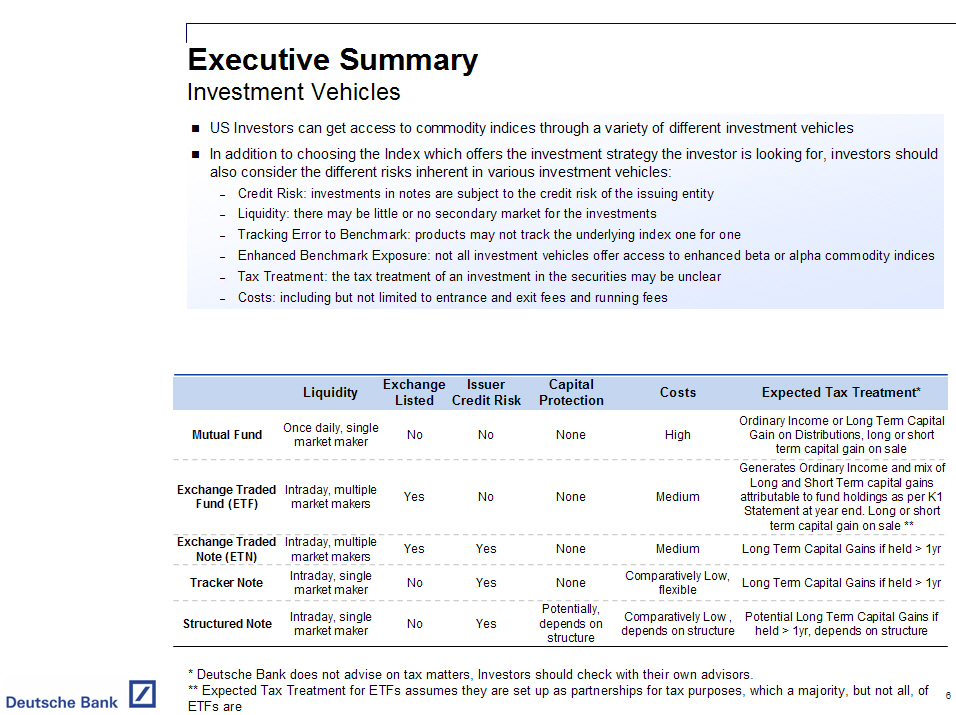

Executive Summary

Investment Vehicles

- - US Investors can get access to commodity indices through a variety of

different investment vehicles

- - In addition to choosing the Index which offers the investment strategy the

investor is looking for, investors should also consider the different risks

inherent in various investment vehicles:

- Credit Risk: investments in notes are subject to the credit risk of

the issuing entity - Liquidity: there may be little or no secondary

market for the investments

- Tracking Error to Benchmark: products may not track the underlying

index one for one

- Enhanced Benchmark Exposure: not all investment vehicles offer access

to enhanced beta or alpha commodity indices - Tax Treatment: the tax

treatment of an investment in the securities may be unclear

- Costs: including but not limited to entrance and exit fees and running

fees

- -----------------------------------------------------------------------------------------------------------------------------------------

Exchange Issuer Capital

Liquidity Listed Credit Risk Protection Costs Expected Tax Treatment*

- -----------------------------------------------------------------------------------------------------------------------------------------

Ordinary Income or Long Term Capital

Mutual Fund Once daily, single No No None High Gain on Distributions, long or short

market maker term capital gain on sale

- -----------------------------------------------------------------------------------------------------------------------------------------

Exchange Traded Intraday, multiple Yes No None Medium Generates Ordinary Income and mix

Fund (ETF) market makers of Long and Short Term capital gains

attributable to fund holdings as per

K1 Statement at year end. Long or short

term capital gain on sale **

- -----------------------------------------------------------------------------------------------------------------------------------------

Exchange Traded Intraday, multiple Yes Yes None Medium Long Term Capital Gains if held > 1yr

Note (ETN) market makers

- -----------------------------------------------------------------------------------------------------------------------------------------

Tracker Note Intraday, single No Yes None Comparatively Low, Long Term Capital Gains if held > 1yr

market maker flexible

- -----------------------------------------------------------------------------------------------------------------------------------------

Structured Note Intraday, single No Yes Potentially, Comparatively Low, Potential Long Term Capital Gains if

market maker depends on depends on held > 1yr, depends on structure

structure structure

- -----------------------------------------------------------------------------------------------------------------------------------------

* Deutsche Bank does not advise on tax matters, Investors should check with

their own advisors.

** Expected Tax Treatment for ETFs assumes they are set up as partnerships for

tax purposes, which a majority, but not all, of 6 ETFs are

6

|

|

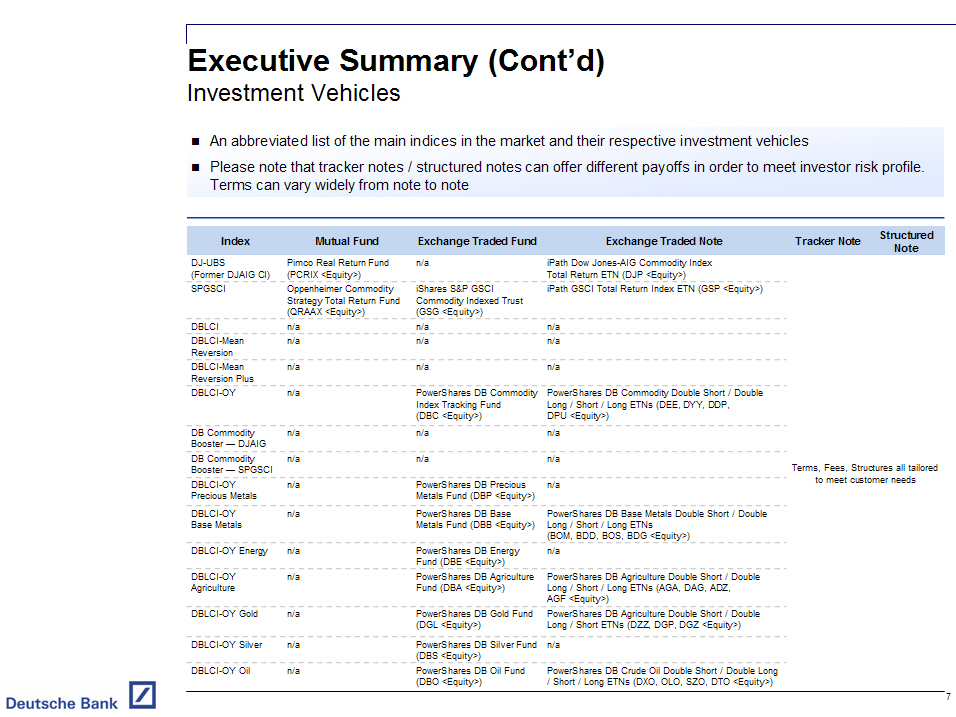

Executive Summary (Cont'd)

Investment Vehicles

- - An abbreviated list of the main indices in the market and their respective

investment vehicles

- - Please note that tracker notes / structured notes can offer different

payoffs in order to meet investor risk profile. Terms can vary widely from

note to note

- ------------------------------------------------------------------------------------------------------------------------------------

Index Mutual Fund Exchange Traded Fund Exchange Traded Note Tracker Note Structured Note

- ------------------------------------------------------------------------------------------------------------------------------------

DJ-UBS Pimco Real Return Fund n/a iPath Dow Jones-AIG

(Former DJAIG CI) (PCRIX (Equity)) Commodity Index Total

Return ETN (DJP

(Equity))

- ----------------------------------------------------------------------------------------------------

SPGSCI Oppenheimer Commodity iShares S&P GSCI iPath GSCI Total Return

Strategy Total Return Fund Commodity Indexed Trust Index ETN (GSP (Equity))

(QRAAX (Equity)) (GSG (Equity))

- ----------------------------------------------------------------------------------------------------

DBLCI n/a n/a n/a

- ----------------------------------------------------------------------------------------------------

DBLCI-Mean n/a n/a n/a

Reversion

- ----------------------------------------------------------------------------------------------------

DBLCI-Mean n/a n/a n/a

Reversion Plus

- ----------------------------------------------------------------------------------------------------

DBLCI-OY n/a PowerShares DB Commodity PowerShares DB Commodity

Index Tracking Fund Double Short / Double

(DBC (Equity)) Long / Short / Long ETNs

(DEE, DYY, DDP, DPU

(Equity))

- ----------------------------------------------------------------------------------------------------

DB Commodity n/a n/a n/a

Booster -- DJAIG

- ----------------------------------------------------------------------------------------------------

DB Commodity n/a n/a n/a

Booster -- SPGSCI

- ----------------------------------------------------------------------------------------------------

DBLCI-OY n/a PowerShares DB Precious n/a

Precious Metals Metals Fund (DBP (Equity))

- ----------------------------------------------------------------------------------------------------

DBLCI-OY n/a PowerShares DB Base PowerShares DB Base Terms, Fees, Structures

Base Metals Metals Fund (DBB (Equity)) Metals Double Short / all tailored to meet

Double Long / Short / customer needs

Long ETNs (BOM, BDD,

BOS, BDG (Equity))

- ----------------------------------------------------------------------------------------------------

DBLCI-OY Energy n/a PowerShares DB Energy n/a

Fund (DBE (Equity))

- ----------------------------------------------------------------------------------------------------

DBLCI-OY n/a PowerShares DB Agriculture PowerShares DB

Agriculture Fund (DBA (Equity)) Agriculture Double Short

/ Double Long / Short /

Long ETNs (AGA, DAG,

ADZ, AGF (Equity))

- ----------------------------------------------------------------------------------------------------

DBLCI-OY Gold n/a PowerShares DB Gold Fund PowerShares DB

(DGL (Equity)) Agriculture Double Short

/ Double Long / Short

ETNs (DZZ, DGP, DGZ

(Equity))

- ----------------------------------------------------------------------------------------------------

DBLCI-OY Silver n/a PowerShares DB Silver Fund n/a

(DBS (Equity))

- ----------------------------------------------------------------------------------------------------

DBLCI-OY Oil n/a PowerShares DB Oil Fund PowerShares DB Crude Oil

(DBO (Equity)) Double Short / Double

Long/ Short / Long ETNs

(DXO, OLO, SZO, DTO

(Equity))

- ------------------------------------------------------------------------------------------------------------------------------------

7

|

|

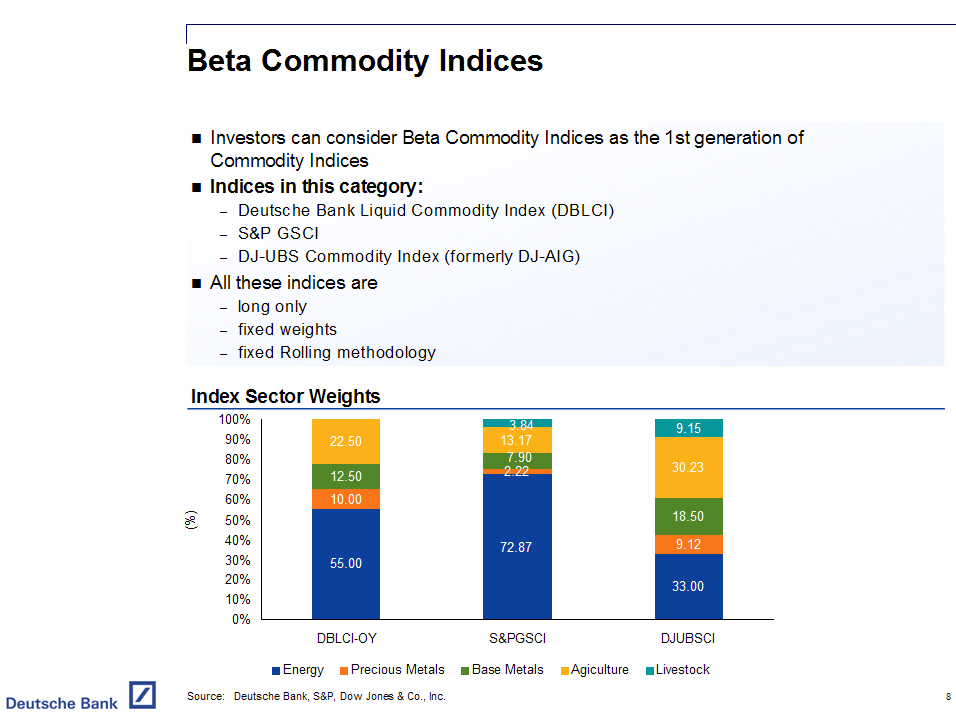

Beta Commodity Indices

- - Investors can consider Beta Commodity Indices as the 1st generation of

Commodity Indices

- - Indices in this category:

- Deutsche Bank Liquid Commodity Index (DBLCI)

- S&P GSCI

- DJ-UBS Commodity Index (formerly DJ-AIG)

- - All these indices are

- long only

- fixed weights

- fixed Rolling methodology

Index Sector Weights

- --------------------

[GRAPHIC OMITTED]

Source: Deutsche Bank, S&P, Dow Jones & Co., Inc.

8

|

|

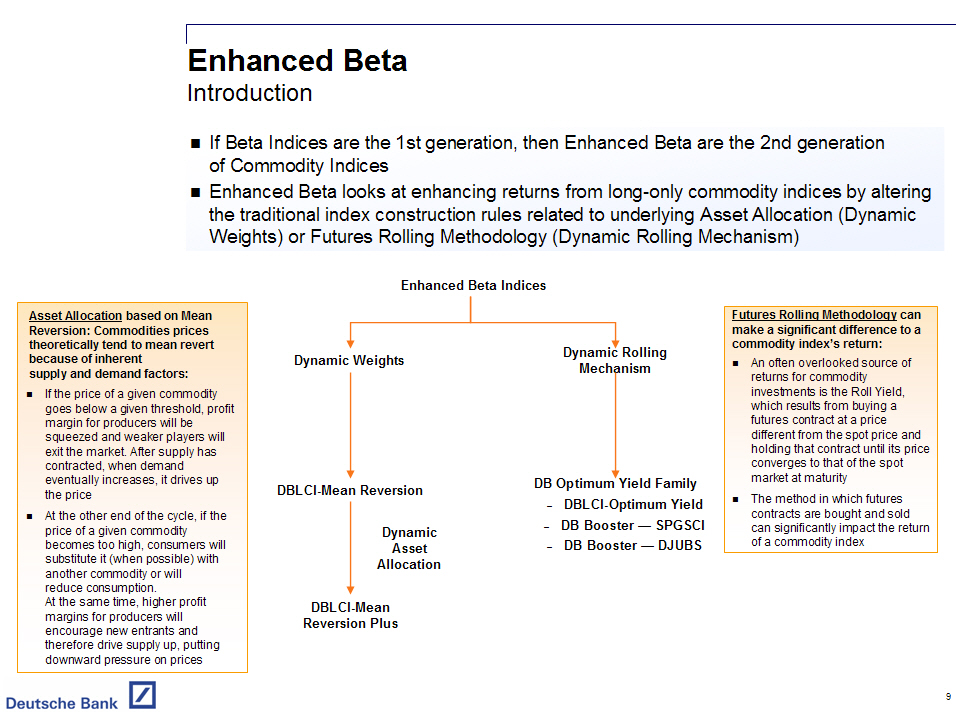

Enhanced Beta

Introduction

- - If Beta Indices are the 1st generation, then Enhanced Beta are the 2nd

generation of Commodity Indices

- - Enhanced Beta looks at enhancing returns from long-only commodity indices

by altering the traditional index construction rules related to underlying

Asset Allocation (Dynamic Weights) or Futures Rolling Methodology (Dynamic

Rolling Mechanism)

[GRAPHIC OMITTED]

Asset Allocation based on Mean Reversion: Commodities prices theoretically tend

to mean revert because of inherent supply and demand factors:

- - If the price of a given commodity goes below a given threshold, profit

margin for producers will be squeezed and weaker players will exit the

market. After supply has contracted, when demand eventually increases, it

drives up the price

- - At the other end of the cycle, if the price of a given commodity becomes

too high, consumers will substitute it (when possible) with another

commodity or will reduce consumption.

At the same time, higher profit margins for producers will encourage new

entrants and therefore drive supply up, putting downward pressure on

prices

Futures Rolling Methodology can make a significant difference to a commodity

index's return:

- - An often overlooked source of returns for commodity investments is the

Roll Yield, which results from buying a futures contract at a price

different from the spot price and holding that contract until its price

converges to that of the spot market at maturity

- - The method in which futures contracts are bought and sold can

significantly impact the return of a commodity index

9

|

|

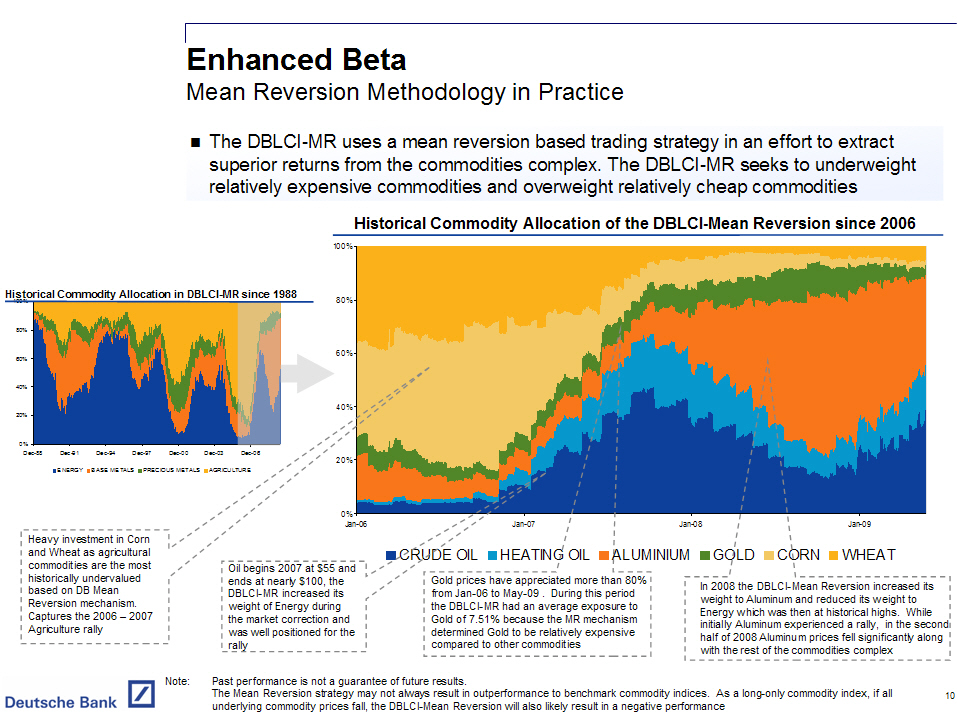

Enhanced Beta

Mean Reversion Methodology in Practice

- - The DBLCI-MR uses a mean reversion based trading strategy in an effort to

extract superior returns from the commodities complex. The DBLCI-MR seeks

to underweight relatively expensive commodities and overweight relatively

cheap commodities

Historical Commodity Allocation of the DBLCI-Mean Reversion since 2006

[GRAPHIC OMITTED]

Heavy investment in Corn and Wheat as agricultural commodities are the most

historically undervalued based on DB Mean Reversion mechanism. Captures the

2006 - 2007 Agriculture rally

Oil begins 2007 at $55 and ends at nearly $100, the DBLCI-MR increased its

weight of Energy during the market correction and was well positioned for the

rally

Gold prices have appreciated more than 80% from Jan-06 to May-09 . During this

period the DBLCI-MR had an average exposure to Gold of 7.51% because the MR

mechanism determined Gold to be relatively expensive compared to other

commodities

In 2008 the DBLCI-Mean Reversion increased its weight to Aluminum and reduced

its weight to Energy which was then at historical highs. While initially

Aluminum experienced a rally, in the second half of 2008 Aluminum prices fell

significantly along with the rest of the commodities complex

Note: Past performance is not a guarantee of future results.

The Mean Reversion strategy may not always result in outperformance

to benchmark commodity indices. As a long-only commodity index, if

all 10 underlying commodity prices fall, the DBLCI-Mean Reversion

will also likely result in a negative performance

10

|

|

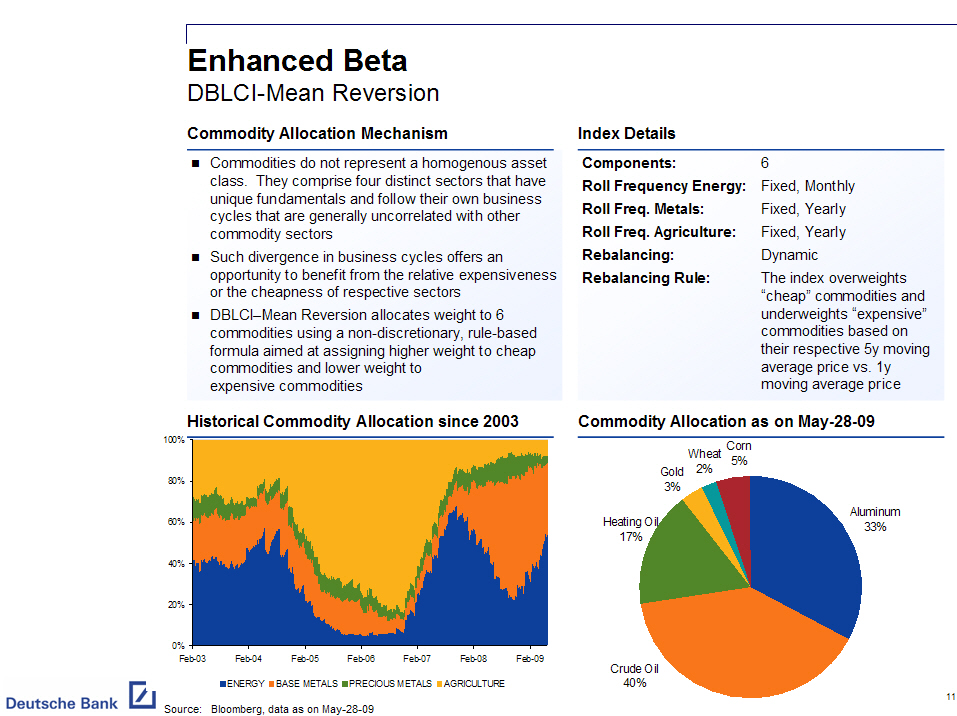

Enhanced Beta

DBLCI-Mean Reversion

Commodity Allocation Mechanism

- ------------------------------

- - Commodities do not represent a homogenous asset class. They comprise four

distinct sectors that have unique fundamentals and follow their own

business cycles that are generally uncorrelated with other commodity

sectors

- - Such divergence in business cycles offers an opportunity to benefit from

the relative expensiveness or the cheapness of respective sectors

- - DBLCI-Mean Reversion allocates weight to 6 commodities using a

non-discretionary, rule-based formula aimed at assigning higher weight to

cheap commodities and lower weight to expensive commodities

Index Details

- -------------

Components: 6

Roll Frequency Energy: Fixed, Monthly

Roll Freq. Metals: Fixed, Yearly

Roll Freq. Agriculture: Fixed, Yearly

Rebalancing: Dynamic

Rebalancing Rule: The index overweights "cheap" commodities and

underweights "expensive" commodities based on their

respective 5y moving average price vs. 1y moving

average price

Historical Commodity Allocation since 2003 Commodity Allocation as on May-28-09

[GRAPHIC OMITTED] [GRAPHIC OMITTED]

Source: Bloomberg, data as on May-28-09

11

|

|

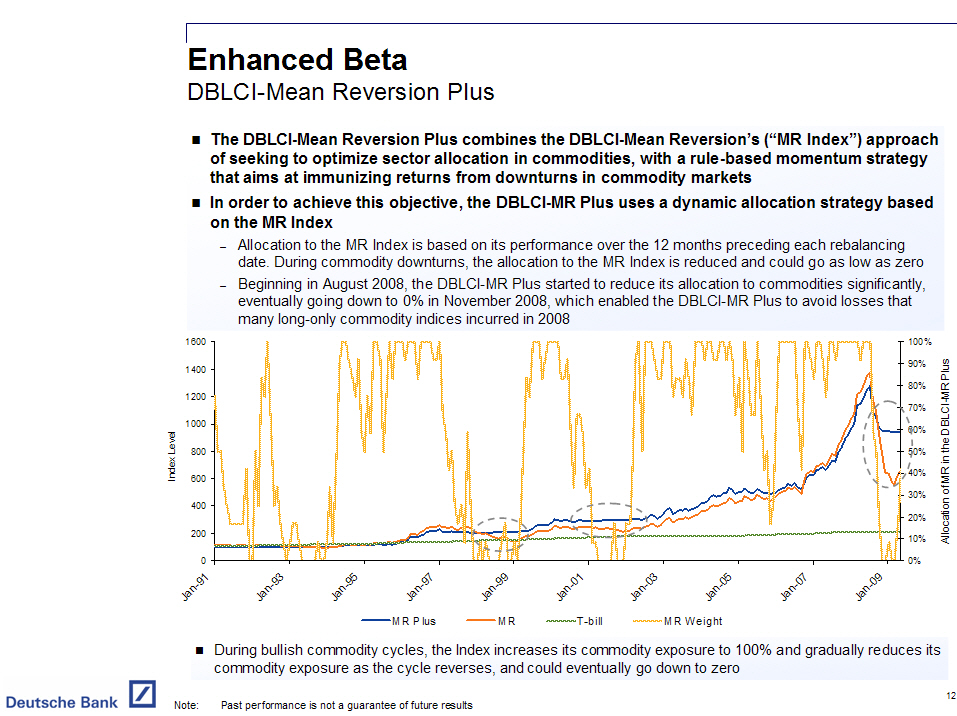

Enhanced Beta

DBLCI-Mean Reversion Plus

- - The DBLCI-Mean Reversion Plus combines the DBLCI-Mean Reversion's ("MR

Index") approach of seeking to optimize sector allocation in commodities,

with a rule-based momentum strategy that aims at immunizing returns from

downturns in commodity markets

- - In order to achieve this objective, the DBLCI-MR Plus uses a dynamic

allocation strategy based on the MR Index

- Allocation to the MR Index is based on its performance over the 12

months preceding each rebalancing date. During commodity downturns,

the allocation to the MR Index is reduced and could go as low as zero

- Beginning in August 2008, the DBLCI-MR Plus started to reduce its

allocation to commodities significantly, eventually going down to 0%

in November 2008, which enabled the DBLCI-MR Plus to avoid losses that

many long-only commodity indices incurred in 2008

[GRAPHIC OMITTED]

- - During bullish commodity cycles, the Index increases its commodity exposure

to 100% and gradually reduces its commodity exposure as the cycle reverses,

and could eventually go down to zero

Note: Past performance is not a guarantee of future results

12

|

|

Enhanced Beta

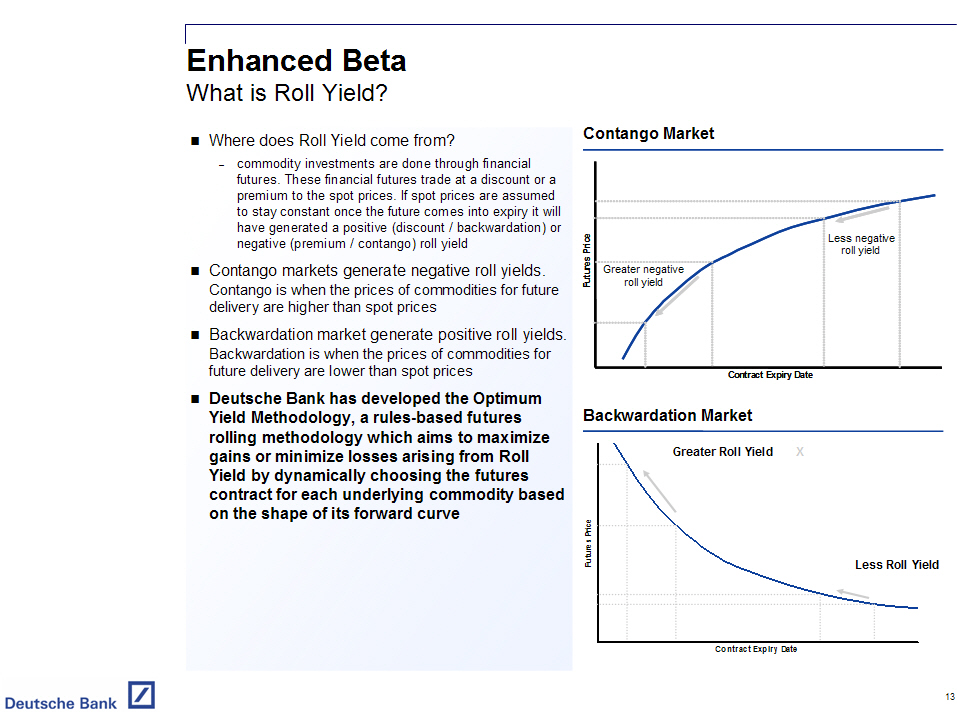

What is Roll Yield?

- - Where does Roll Yield come from?

- commodity investments are done through financial futures. These

financial futures trade at a discount or a premium to the spot prices.

If spot prices are assumed to stay constant once the future comes into

expiry it will have generated a positive (discount / backwardation) or

negative (premium / contango) roll yield

- - Contango markets generate negative roll yields.

- - Contango is when the prices of commodities for future delivery are higher

than spot prices

- - Backwardation market generate positive roll yields.

Backwardation is when the prices of commodities for future delivery are

lower than spot prices

- - Deutsche Bank has developed the Optimum

Yield Methodology, a rules-based futures rolling methodology which aims to

maximize gains or minimize losses arising from Roll Yield by dynamically

choosing the futures contract for each underlying commodity based on the

shape of its forward curve

[GRAPHIC OMITTED]

13

|

|

Enhanced Beta

Optimum Yield Family of Indices

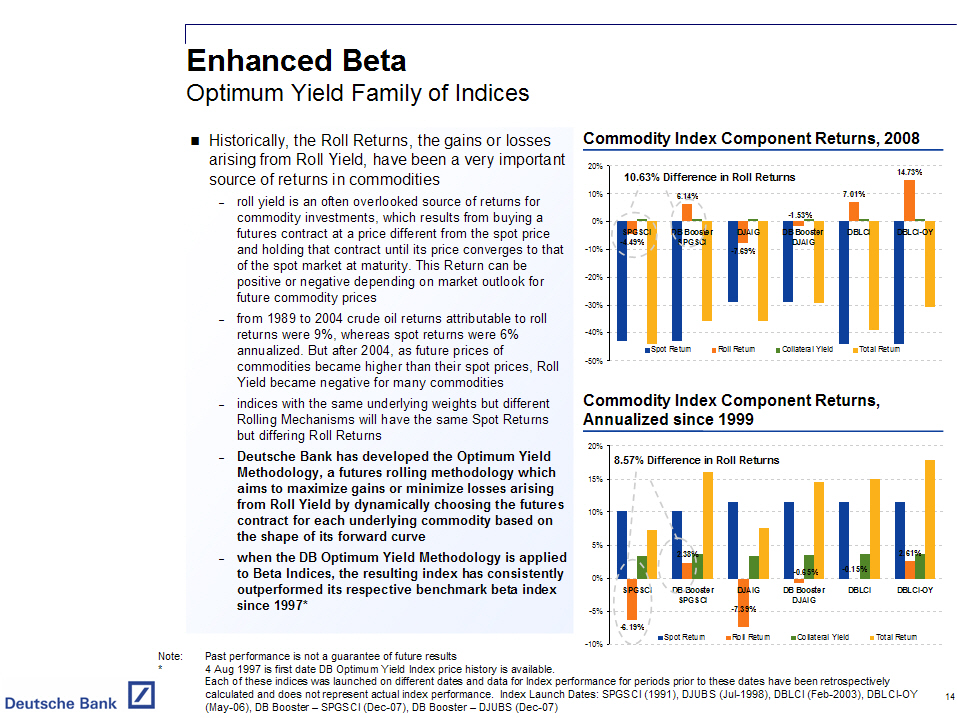

- - Historically, the Roll Returns, the gains or losses arising from Roll

Yield, have been a very important source of returns in commodities

- roll yield is an often overlooked source of returns for commodity

investments, which results from buying a futures contract at a price

different from the spot price and holding that contract until its

price converges to that of the spot market at maturity. This Return

can be positive or negative depending on market outlook for future

commodity prices

- from 1989 to 2004 crude oil returns attributable to roll returns were

9%, whereas spot returns were 6% annualized. But after 2004, as future

prices of commodities became higher than their spot prices, Roll Yield

became negative for many commodities

- indices with the same underlying weights but different Rolling

Mechanisms will have the same Spot Returns but differing Roll Returns

- Deutsche Bank has developed the Optimum Yield

Methodology, a futures rolling methodology which aims to maximize

gains or minimize losses arising from Roll Yield by dynamically

choosing the futures contract for each underlying commodity based on

the shape of its forward curve

- when the DB Optimum Yield Methodology is applied to Beta Indices, the

resulting index has consistently outperformed its respective benchmark

beta index since 1997*

Commodity Index Component Returns, 2008

- ---------------------------------------

[GRAPHIC OMITTED]

Commodity Index Component Returns,

Annualized since 1999

- ---------------------

[GRAPHIC OMITTED]

Note: Past performance is not a guarantee of future results

* 4 Aug 1997 is first date DB Optimum Yield Index price history is

available. Each of these indices was launched on different dates and

data for Index performance for periods prior to these dates have been

retrospectively calculated and does not represent actual index

performance. Index Launch Dates: SPGSCI (1991), DJUBS (Jul-1998),

DBLCI (Feb-2003), DBLCI-OY 14 (May-06), DB Booster - SPGSCI (Dec-07),

DB Booster - DJUBS (Dec-07)

14

|

|

Enhanced Beta

Optimum Yield Family of Indices

- ---------------------------------------------------------------------------------------------------

Beta Benchmark Enhanced Beta Counterpart Annualized Outperformance

- ---------------------------------------------------------------------------------------------------

SPGSCI DB Commodity Booster -- SPGSCI 9.00%

SPGSCI Light Energy DB Commodity Booster -- SPGSCI Light Energy 5.83%

DJUBS DB Commodity Booster -- DJUBS 6.45%

DBLCI DBLCI -- Optimum Yield 3.59%

- ---------------------------------------------------------------------------------------------------

Optimum Yield Index Performance vs Benchmarks

[GRAPHIC OMITTED]

Note: Past performance is not a guarantee of future results

* 4 Aug 1997 is first date DB Optimum Yield Index price history is

available. Data from 4 August 1997 to 29 May 2009 Each of these

indices was launched on different dates and data for Index performance

for periods prior to these dates have been retrospectively calculated

and does not represent actual index performance. Index Launch Dates:

SPGSCI (Jan-91), SPGSCI Light Energy (Jan-91), DJUBS (Jul-98), DBLCI

(Feb-03), 15 DBLCI-OY (May-06), DB Booster - SPGSCI (Dec-07), DB

Booster - DJUBS (Dec-07), DB Booster - SPGSCI Light Energy (Dec-07 )

15

|

|

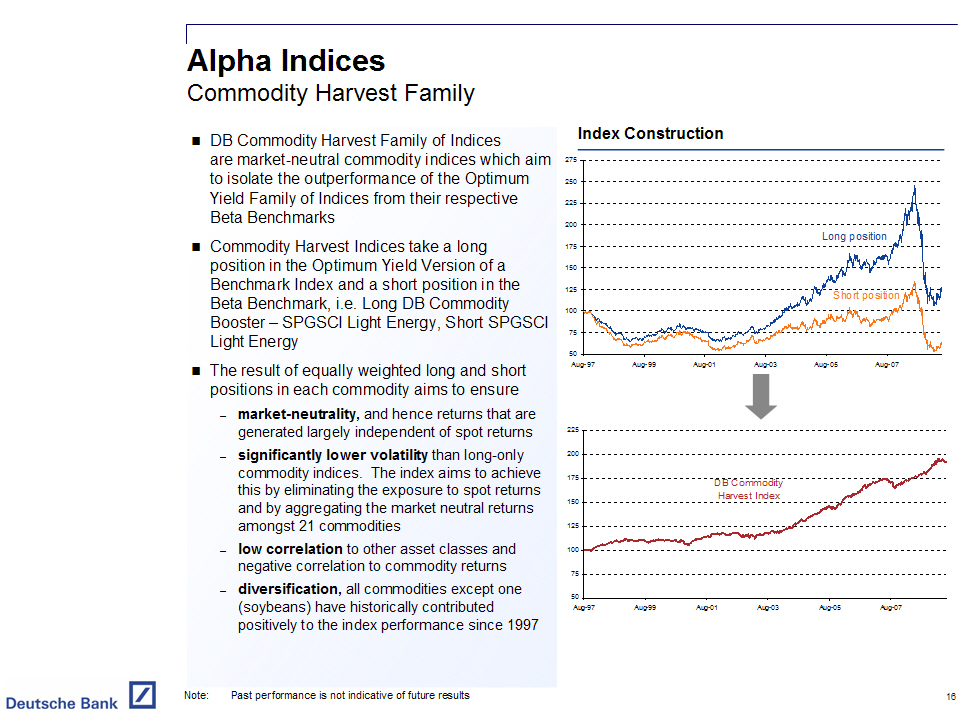

Alpha Indices

Commodity Harvest Family

- - DB Commodity Harvest Family of Indices are market-neutral commodity indices

which aim to isolate the outperformance of the Optimum Yield Family of

Indices from their respective Beta Benchmarks

- - Commodity Harvest Indices take a long position in the Optimum Yield Version

of a Benchmark Index and a short position in the Beta Benchmark, i.e. Long

DB Commodity Booster - SPGSCI Light Energy, Short SPGSCI Light Energy

- - The result of equally weighted long and short positions in each commodity

aims to ensure

- market-neutrality, and hence returns that are generated largely

independent of spot returns

- significantly lower volatility than long-only commodity indices. The

index aims to achieve this by eliminating the exposure to spot returns

and by aggregating the market neutral returns amongst 21 commodities

- low correlation to other asset classes and negative correlation to

commodity returns

- diversification, all commodities except one (soybeans) have

historically contributed positively to the index performance since

1997

Index Construction

[GRAPHIC OMITTED]

Note: Past performance is not indicative of future results

16

|

|

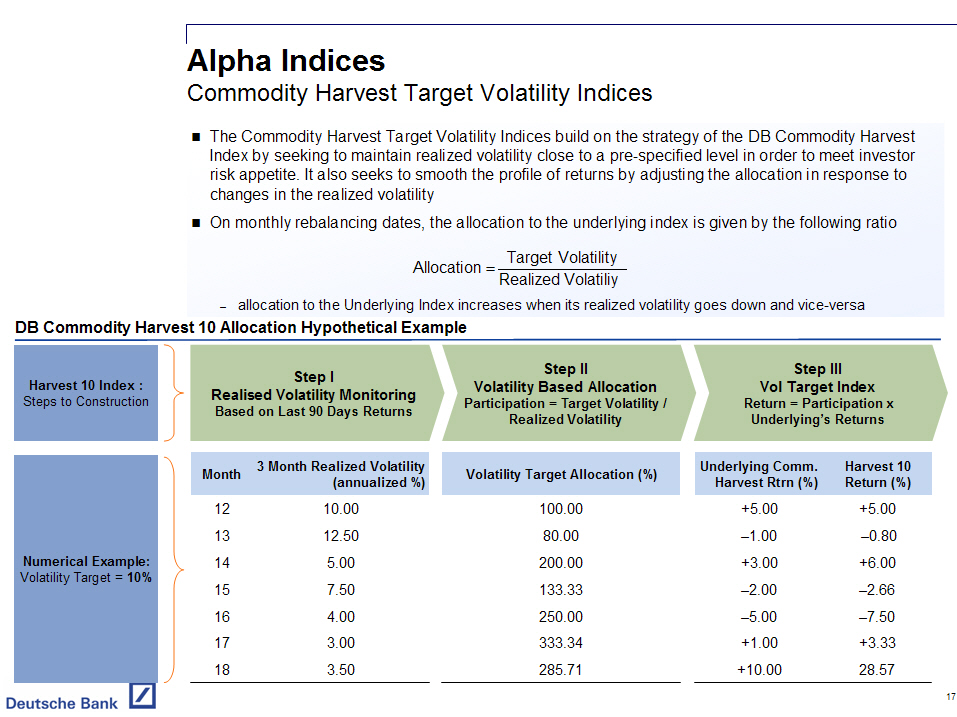

Alpha Indices

Commodity Harvest Target Volatility Indices

- - The Commodity Harvest Target Volatility Indices build on the strategy of

the DB Commodity Harvest Index by seeking to maintain realized volatility

close to a pre-specified level in order to meet investor risk appetite. It

also seeks to smooth the profile of returns by adjusting the allocation in

response to changes in the realized volatility

- - On monthly rebalancing dates, the allocation to the underlying index is

given by the following ratio

Allocation = Target Volatility

----------------------------------------

Realized Volatiliy

- allocation to the Underlying Index increases when its

realized volatility goes down and vice-versa

DB Commodity Harvest 10 Allocation Hypothetical Example

- -------------------------------------------------------

Harvest 10 Index :

Steps to Construction

- ---------------------

Step I Step II Step III

Realised Volatility Monitoring Volatility Based Allocation Vol Target Index

Based on Last 90 Days Returns Participation = Target Volatility / Return = Participation x

Realized Volatility Underlying's Returns

Numerical Example:

Volatility Target = 10%

3 Month Realized

Volatility Volatility Underlying Comm. Harvest 10

Month (annualized %) Target Allocation (%) Harvest Rtrn (%) Return (%)

- ----------------------------------------------------------------------------------

12 10.00 100.00 +5.00 +5.00

13 12.50 80.00 -1.00 -0.80

14 5.00 200.00 +3.00 +6.00

15 7.50 133.33 -2.00 -2.66

16 4.00 250.00 -5.00 -7.50

17 3.00 333.34 +1.00 +3.33

18 3.50 285.71 +10.00 28.57

17

|

|

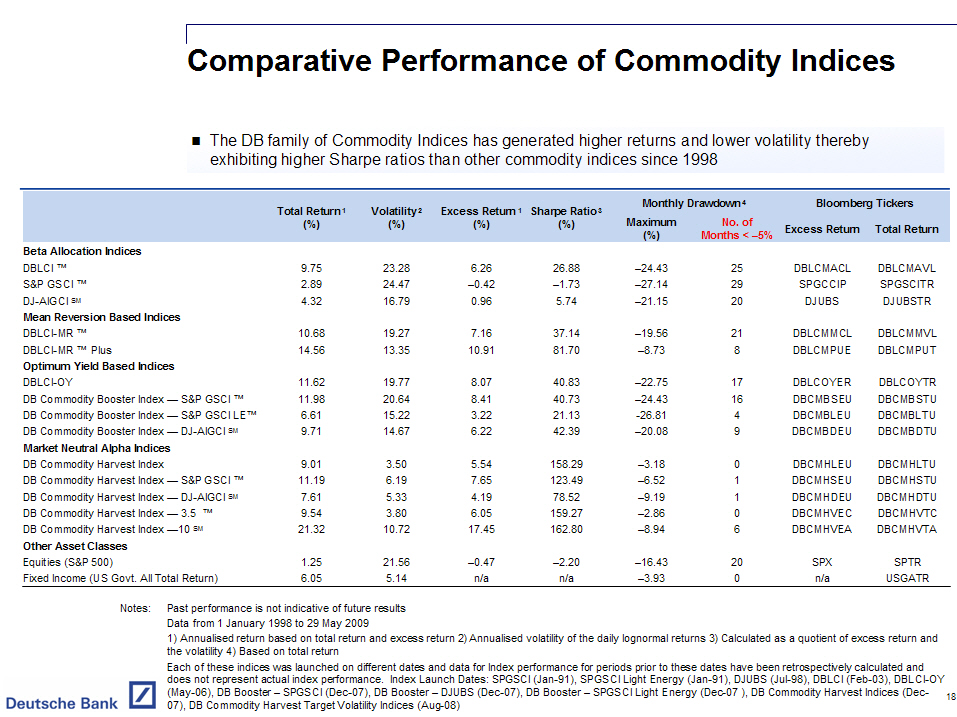

Comparative Performance of Commodity Indices

- - The DB family of Commodity Indices has generated higher returns and lower

volatility thereby exhibiting higher Sharpe ratios than other commodity

indices since 1998

Total Volatility(2) Excess Sharpe Monthly Bloomberg

Return (1) Return (1) Ratio (3) Drawdown (4) Tickers

Maximum No. of Excess Total

(%) (%) (%) (%) (%) Months < -5% Return Return

- -----------------------------------------------------------------------------------------------------------------------------------------------

Beta Allocation Indices

DBLCI (TM) 9.75 23.28 6.26 26.88 -24.43 25 DBLCMACL DBLCMAVL

S&P GSCI (TM) 2.89 24.47 -0.42 -1.73 -27.14 29 SPGCCIP SPGSCITR

DJ-AIGCI SM 4.32 16.79 0.96 5.74 -21.15 20 DJUBS DJUBSTR

Mean Reversion Based Indices

DBLCI-MR (TM) 10.68 19.27 7.16 37.14 -19.56 21 DBLCMMCL DBLCMMVL

DBLCI-MR (TM) Plus 14.56 13.35 10.91 81.70 -8.73 8 DBLCMPUE DBLCMPUT

Optimum Yield Based Indices

DBLCI-OY 11.62 19.77 8.07 40.83 -22.75 17 DBLCOYER DBLCOYTR

DB Commodity Booster Index -- S&P GSCI (TM) 11.98 20.64 8.41 40.73 -24.43 16 DBCMBSEU DBCMBSTU

DB Commodity Booster Index -- S&P GSCI LE(TM) 6.61 15.22 3.22 21.13 -26.81 4 DBCMBLEU DBCMBLTU

DB Commodity Booster Index -- DJ-AIGCI SM 9.71 14.67 6.22 42.39 -20.08 9 DBCMBDEU DBCMBDTU

Market Neutral Alpha Indices

DB Commodity Harvest Index 9.01 3.50 5.54 1 58.29 -3.18 0 DBCMHLEU DBCMHLTU

DB Commodity Harvest Index -- S&P GSCI (TM) 11.19 6.19 7.65 1 23.49 -6.52 1 DBCMHSEU DBCMHSTU

DB Commodity Harvest Index -- DJ-AIGCI SM 7.61 5.33 4.19 78.52 -9.19 1 DBCMHDEU DBCMHDTU

DB Commodity Harvest Index -- 3.5 (TM) 9.54 3.80 6.05 1 59.27 -2.86 0 DBCMHVEC DBCMHVTC

DB Commodity Harvest Index --10 SM 21.32 10.72 17.45 1 62.80 -8.94 6 DBCMHVEA DBCMHVTA

Other Asset Classes

Equities (S&P 500) 1.25 21.56 -0.47 -2.20 -16.43 20 SPX SPTR

Fixed Income (US Govt. All Total Return) 6.05 5.14 n/a n/a -3.93 0 n/a USGATR

Notes: Past performance is not indicative of future results

Data from 1 January 1998 to 29 May 2009

1) Annualised return based on total return and excess return 2)

Annualised volatility of the daily lognormal returns 3) Calculated as

a quotient of excess return and the volatility 4) Based on total

return

Each of these indices was launched on different dates and data for

Index performance for periods prior to these dates have been

retrospectively calculated and does not represent actual index

performance. Index Launch Dates: SPGSCI (Jan-91), SPGSCI Light Energy

(Jan-91), DJUBS (Jul-98), DBLCI (Feb-03), DBLCI-OY (May-06), DB

Booster - SPGSCI (Dec-07), DB Booster - DJUBS (Dec-07), DB Booster -

SPGSCI Light Energy (Dec-07 ), DB Commodity Harvest Indices (Dec- 18

07), DB Commodity Harvest Target Volatility Indices (Aug-08)

18

|

| Important Considerations For further details on the DB Commodity Index Suite refer to Underlying Supplement dated December 16, 2008: http://www.sec.gov/Archives/edgar/data/1159508/000119312508254080/d424b21.pdf Commodities are speculative and highly volatile and the risk of loss of trading in commodities can be substantial. An investment linked to a commodity index involves a number of risks, including the risk that the index's strategy may not be successful, and its return, if any, will be dependent on, among other things, the performance of the relevant index during the term of the investment and the terms and conditions of that investment. The absence of backwardation or presence of contango in the markets for futures contracts included in a long-only commodity index will adversely affect the level of that index. An index's performance is unpredictable, and past performance is not indicative of future performance. We give no representation or warranty on the future performance of any index or investment. Deutsche Bank AG and its affiliates do not provide legal, tax, or accounting advice, and we are not acting in any way as an advisory or in a fiduciary capacity. Prospective investors should consider an investment linked to a DB commodity index only after careful consideration of the risks, consultation with their legal, tax, accounting, and other advisors as to the suitability of the investment in light of their own particular financial, tax and other circumstances, and review and consideration of any documents that we provide to you in connection with any offering We are not acting and do not purport to act in any way as an advisor or in a fiduciary capacity. We therefore strongly suggest that recipients seek their own independent advice in relation to any investment, financial, legal, tax, accounting or regulatory issues discussed herein. Analyses and opinions contained herein may be based on assumptions that if altered can change the analyses or opinions expressed. Nothing contained herein shall constitute any representation or warranty as to future performance of any financial instrument, credit, index, currency rate or other market or economic measure. Furthermore, past performance is not necessarily indicative of future results. Securities and investment banking activities in the United States are performed by Deutsche Bank Securities Inc., member NYSE, NASD and SIPC, and its broker-dealer affiliates. Lending and other commercial banking activities in the United States are performed by Deutsche Bank AG, and its banking affiliates. (C) 2009 Deutsche Bank AG 19 |

|

Disclaimer

S&P GSCI SM Disclaimer

Any securities Deutsche Bank AG may issue from time to time and this

presentation are not sponsored, endorsed, sold or promoted by Standard & Poor's,

a division of The McGraw-Hill Companies, Inc. ("S&P"). Standard & Poor's does

not make any representation or warranty, express or implied, to the owners of

the securities or any member of the public regarding the advisability of

investing in securities generally or in these securities, particularly or the

ability of S&P GSCI Index to track general commodity market performance. S&P's

only relationship to Deutsche Bank AG is the licensing of certain trademarks and

trade names of S&P and of S&P GSCI Index, which indices are determined, composed

and calculated by S&P without regard to Deutsche Bank AG or the securities. S&P

has no obligation to take the needs of Deutsche Bank AG or the owners of the

Bonds into consideration in determining, composing or calculating S&P GSCI

Index. S&P is not responsible for and have not participated in the determination

of the timing of, prices at, or quantities of the securities to be issued or in

the determination or calculation of the equation by which the S&P GSCI Index are

to be converted into cash. S&P has no obligation or liability in connection with

the administration, marketing or trading of the Bonds.

S&P DOES NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF S&P GSCI INDEX OR

ANY DATA INCLUDED THEREIN AND S&P SHALL HAVE NO LIABILITY FOR ANY ERRORS,

OMISSIONS, OR INTERRUPTIONS THEREIN. S&P MAKES NO WARRANTY, EXPRESS OR IMPLIED,

AS TO RESULTS TO BE OBTAINED BY DEUTSCHE BANK AG, OWNERS OF SECURITIES OR ANY

OTHER PERSON OR ENTITY FROM THE USE OF S&P GSCI INDEX OR ANY DATA INCLUDED

THEREIN. S&P MAKES NO EXPRESS OR IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIMS ALL

WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE WITH

RESPECT TO THE S&P INDICES OR DEUTSCHE BANK'S VARIATIONS OF S&P INDICES OR ANY

DATA INCLUDED THEREIN. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT SHALL

S&P HAVE ANY LIABILITY FOR ANY SPECIAL, PUNITIVE, INDIRECT, OR CONSEQUENTIAL

DAMAGES (INCLUDING LOST PROFITS), EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH

DAMAGES.

S&P GSCI Index is a trademark of The McGraw-Hill Companies, Inc. and has been

licensed for use by Deutsche Bank AG.

DJ-UBSCISM Disclaimer

"Dow Jones(R)", "DJ", "UBS," "DJ-UBSCISM" are service marks of Dow Jones &

Company, Inc. ("Dow Jones") and UBS AG ("UBS AG"), as the case may be, and have

been licensed for use for certain purposes by Deutsche Bank AG

The securities which Deutsche Bank AG may offer from time to time are not

sponsored, endorsed, sold or promoted by Dow Jones, UBS AG, UBS Securities LLC

("UBS Securities") or any of their subsidiaries or affiliates. None of Dow

Jones, UBS AG, UBS Securities or any of their subsidiaries or affiliates makes

any representation or warranty, express or implied, to the owners of or

counterparts to the securities or any member of the public regarding the

advisability of investing in securities or commodities generally or in the

securities particularly. The only relationship of Dow Jones, UBS AG, UBS

Securities or any of their subsidiaries or affiliates to the Licensee is the

licensing of certain trademarks, trade names and service marks and of the

DJ-UBSCISM, which is determined, composed and calculated by Dow Jones in

conjunction with UBS Securities without regard to Deutsche Bank AG or the

securities. Dow Jones and UBS Securities have no obligation to take the needs of

Deutsche Bank AG or the owners of the securities into consideration in

determining, composing or calculating DJ-UBSCISM. None of Dow Jones, UBS AG, UBS

Securities or any of their respective subsidiaries or affiliates is responsible

for or has participated in the determination of the timing of, prices at, or

quantities of the securities to be issued or in the determination or calculation

of the equation by which the securities are to be converted into cash. None of

Dow Jones, UBS AG, UBS Securities or any of their subsidiaries or affiliates

shall have any obligation or liability, including, without limitation, to

securities' customers, in connection with the administration, marketing or

trading of the securities. Notwithstanding the foregoing, UBS AG, UBS Securities

and their respective subsidiaries and affiliates may independently issue and/or

sponsor financial products unrelated to the securities currently being issued by

Licensee, but which may be similar to and competitive with such securities. In

addition, UBS AG, UBS Securities and their subsidiaries and affiliates actively

trade commodities, commodity indexes and commodity futures (including the Dow

Jones-UBS Commodity IndexSM and Dow Jones-UBS Commodity Index Total ReturnSM),

as well as swaps, options and derivatives which are linked to the performance of

such commodities, commodity indexes and commodity futures. It is possible that

this trading activity will affect the value of the Dow Jones-UBS Commodity

IndexSM and any securities Deutsche Bank AG may issue from time to time.

NONE OF DOW JONES, UBS AG, UBS SECURITIES OR ANY OF THEIR SUBSIDIARIES OR

AFFILIATES GUARANTEES THE ACCURACY AND/OR THE COMPLETENESS OF THE DOW JONES-UBS

COMMODITY INDEXSM OR ANY DATA RELATED THERETO AND NONE OF DOW JONES, UBS AG, UBS

SECURITIES OR ANY OF THEIR SUBSIDIARIES OR AFFILIATES SHALL HAVE ANY LIABILITY

FOR ANY ERRORS, OMISSIONS OR INTERRUPTIONS THEREIN. NONE OF DOW JONES, UBS AG,

UBS SECURITIES OR ANY OF THEIR SUBSIDIARIES OR AFFILIATES MAKES ANY WARRANTY,

EXPRESS OR IMPLIED, AS TO RESULTS TO BE OBTAINED BY DEUTSCHE BANK AG, OWNERS OF

THE SECURITIES OR ANY OTHER PERSON OR ENTITY FROM THE USE OF THE DOW JONES-UBS

COMMODITY INDEXSM OR ANY DATA RELATED THERETO. NONE OF DOW JONES, UBS AG, UBS

SECURITIES OR ANY OF THEIR SUBSIDIARIES OR AFFILIATES MAKES ANY EXPRESS OR

IMPLIED WARRANTIES AND EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANTABILITY OR

FITNESS FOR A PARTICULAR PURPOSE OR USE WITH RESPECT TO THE DOW JONES-UBS

COMMODITY INDEXSM OR ANY DATA RELATED THERETO. WITHOUT LIMITING ANY OF THE

FOREGOING, IN NO EVENT SHALL DOW JONES, UBS AG, UBS SECURITIES OR ANY OF THEIR

SUBSIDIARIES OR AFFILIATES HAVE ANY LIABILITY FOR ANY LOST PROFITS OR INDIRECT,

PUNITIVE, SPECIAL OR CONSEQUENTIAL DAMAGES OR LOSSES, EVEN IF NOTIFIED OF THE

POSSIBILITY THEREOF. THERE ARE NO THIRD PARTY BENEFICIARIES OF ANY AGREEMENTS OR

ARRANGEMENTS AMONG DOW JONES, UBS SECURITIES AND DEUTSCHE BANK AG, OTHER THAN

UBS AG.

"Dow Jones(R)", "DJ", "UBS(R)" "Dow Jones-UBS Commodity IndexSM" are service

marks of Dow Jones & Company, Inc. and UBS AG, as the case may be, and have been

licensed for use for certain purposes by Deutsche Bank. The DB Commodity Harvest

- - DJUBS and DB Commodity Booster - DJUBS, which is based in part on the Dow

Jones-UBS Commodity Index, is not sponsored or endorsed by Dow Jones & Company,

Inc. or UBS Securities LLC, but is published with their consent.

20

|