Term Sheet No. 726J To prospectus dated October 10, 2006, prospectus supplement dated November 13, 2006 and product supplement J dated June 27, 2008 | Registration Statement No. 333-137902 Dated August 31, 2009; Rule 433 |

Deutsche Bank AG, London Branch

Capped Buffered Underlying Securities (BUyS) Linked to the S&P GSCITM Natural Gas Index Excess Return due September 10*, 2012

General

| • | Capped Buffered Underlying Securities (BUyS) Linked to the S&P GSCITM Natural Gas Index Excess Return due September 10*, 2012 (the “BUyS”) are designed for investors who seek a return of 150.00% of the appreciation, if any, of the S&P GSCITM Natural Gas Index Excess Return (the “Index”) at maturity, up to an Index Return Cap (as defined below) of between 41.00% and 47.00% (to be determined on the Trade Date). Investors should be willing to forgo coupon and dividend payments during the term of the BUyS and to lose up to 80.00% of their initial investment, subject to the credit of the Issuer, if the Index declines. |

| • | Senior unsecured obligations of Deutsche Bank AG due on or about September 10*, 2012. |

| • | Denominations of $1,000 (the “Face Amount”) and multiples thereof, and minimum initial investments of $1,000. |

| • | The BUyS are expected to price on or about September 4*, 2009 and are expected to settle three business days later on or about September 10*, 2009 (the “Settlement Date”). |

| • | After the Trade Date but prior to Settlement Date, we may accept additional orders for the BUyS and increase the Face Amount. |

Key Terms

| Issuer: | Deutsche Bank AG, London Branch. |

| Index: | S&P GSCITM Natural Gas Index Excess Return (Bloomberg: “SPGCNGP <Index>”) |

| Issue Price: | 100% of the Face Amount. |

| Payment at Maturity: | · If the Final Level is greater than or equal to the Initial Level, you will receive a cash payment per $1,000 Face Amount of BUyS that provides you with a return on your investment equal to the Index Return, subject to the Index Return Cap, multiplied by the Participation Rate, subject to the Maximum Return. Accordingly, subject to the Maximum Return, your payment at maturity per $1,000 Face Amount will be calculated as follows: |

| $1,000 + ($1,000 x Index Return x Participation Rate) | |

· If the Final Level declines from the Initial Level, and such decline is equal to or less than the Buffer Level, you will receive a cash payment of $1,000 per $1,000 Face Amount. | |

· If the Final Level declines from the Initial Level, and such decline is greater than the Buffer Level, you will lose 1% of the Face Amount of your BUyS for every 1% that the Final Level declines from the Initial Level beyond the Buffer Level. Accordingly, if the Final Level declines from the Initial Level beyond the Buffer Level, your payment at maturity per $1,000 Face Amount will be calculated as follows: $1,000 + [$1,000 × (Index Return + Buffer Level)] | |

| If the Final Level declines from the Initial Level by more than the Buffer Level, you could lose up to $800.00 per $1,000 Face Amount of BUyS. |

| Index Return: | Subject to the Index Return Cap, the Index Return, expressed as a percentage, will equal: Final Level – Initial Level Initial Level |

| Initial Level: | The Index closing level on the Trade Date, subject to postponement as described under “Description of Securities – Adjustment to Valuation Dates and Payment Dates” in the accompanying product supplement and “Additional Terms of the BUyS – Commodity Hedging Disruption Events” in this term sheet. |

| Final Level: | The Index closing level on the Final Valuation Date, subject to postponement as described under “Description of Securities – Adjustment to Valuation Dates and Payment Dates” in the accompanying product supplement and “Additional Terms of the BUyS – Commodity Hedging Disruption Events” in this term sheet. |

| Buffer Level: | 20.00% |

| Participation Rate: | 150.00% upside participation |

| Index Return Cap: | 41.00% – 47.00% (to be determined on the Trade Date) |

| Maximum Return: | 61.50% – 70.50% (equal to the Participation Rate multiplied by the Index Return Cap, which will be determined on the Trade Date) |

| Trade Date: | September 4*, 2009 |

| Final Valuation Date: | September 5*, 2012, subject to postponement as described under “Description of Securities – Adjustment to Valuation Dates and Payment Dates” in the accompanying product supplement and “Additional Terms of the BUyS – Commodity Hedging Disruption Events” in this term sheet. |

| Maturity Date: | September 10*, 2012, subject to postponement as described under “Description of Securities – Adjustment to Valuation Dates and Payment Dates” in the accompanying product supplement and “Additional Terms of the BUyS – Commodity Hedging Disruption Events” in this term sheet. |

| Listing: | The BUyS will not be listed on any securities exchange. |

| CUSIP: | 2515A0 R2 1 |

| ISIN: | US2515A0R213 |

* Expected. In the event that we make any change to the expected Trade Date and Settlement Date, the Final Valuation Date and Maturity Date may be changed so that the stated term of the BUyS remains the same.

Investing in the BUyS involves a number of risks. See “Risk Factors” beginning on page 6 of the accompanying product supplement and “Selected Risk Considerations” beginning on page TS-4 of this term sheet.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the BUyS or passed upon the accuracy or the adequacy of this term sheet or the accompanying product supplement, prospectus supplement and prospectus. Any representation to the contrary is a criminal offense.

Price to Public | Max. Total Discounts, Commissions and Fees(1) | Min. Proceeds to Us | |

| Per Security | $1,000.00 | $7.50 | $992.50 |

| Total | $ | $ | $ |

| (1) | For more detailed information about discounts and commissions, please see “Supplemental Underwriting Information” on the last page of this term sheet. The BUyS will be sold with varying underwriting discounts and commissions in an amount not to exceed $7.50 per $1,000.00 BUyS. |

The BUyS are not bank deposits and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency. The BUyS are not guaranteed under the Federal Deposit Insurance Corporation's Temporary Liquidity Guarantee Program.

| Deutsche Bank Securities | Deutsche Bank Trust Company Americas |

ADDITIONAL TERMS SPECIFIC TO THE BUYS

| • | You should read this term sheet together with the prospectus dated October 10, 2006, as supplemented by the prospectus supplement dated November 13, 2006 relating to our Series A global notes of which these BUyS are a part, and the more detailed information contained in product supplement J dated June 27, 2008. You may access these documents on the SEC website at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website): |

| • | Product supplement J dated June 27, 2008: |

| • | Prospectus supplement dated November 13, 2006: |

| • | Prospectus dated October 10, 2006: |

| • | Our Central Index Key, or CIK, on the SEC website is 0001159508. As used in this term sheet, “we,” “us” or “our” refers to Deutsche Bank AG, including, as the context requires, acting through one of its branches. |

| • | This term sheet, together with the documents listed above, contains the terms of the BUyS and supersedes all other prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth in “Risk Factors” in the accompanying product supplement, as the BUyS involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisers before deciding to invest in the BUyS. |

| • | Deutsche Bank AG has filed a registration statement (including a prospectus) with the Securities and Exchange Commission, or SEC, for the offering to which this term sheet relates. Before you invest, you should read the prospectus in that registration statement and the other documents relating to this offering that Deutsche Bank AG has filed with the SEC for more complete information about Deutsche Bank AG and this offering. You may obtain these documents without cost by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, Deutsche Bank AG, any agent or any dealer participating in this offering will arrange to send you the prospectus, prospectus supplement, product supplement and this term sheet if you so request by calling toll-free 1-800-311-4409. |

| • | You may revoke your offer to purchase the BUyS at any time prior to the time at which we accept such offer by notifying the applicable agent. We reserve the right to change the terms of, or reject any offer to purchase, the BUyS prior to their issuance. We will notify you in the event of any changes to the terms of the BUyS, and you will be asked to accept such changes in connection with your purchase of any BUyS. You may also choose to reject such changes, in which case we may reject your offer to purchase the BUyS. |

TS-1

What is the Payment Amount on the BUyS at Maturity Assuming a Range of Performance for the Index?

The table below illustrates the payment at maturity per BUyS Face Amount for a hypothetical range of performance for the Index from -100.00% to +100.00% and assumes a Participation Rate of 150.00%, a Buffer Level of 20.00%, an Index Return Cap of 44.00%, a Maximum Return of 66.00% and an Initial Level of 1.318 (the actual Index Return Cap, Maximum Return and Initial Level will be determined on the Trade Date). The following results are based solely on the hypothetical example cited. You should consider carefully whether the BUyS are suitable to your investment goals. The numbers appearing in the table below have been rounded for ease of analysis.

| Final Level | Percentage Change in Index | Index Return (%) | Payment at Maturity ($) | Return on BUyS (%) |

| 2.636 | 100.00% | 44.00% | $1,660.00 | 66.00% |

| 2.307 | 75.00% | 44.00% | $1,660.00 | 66.00% |

| 1.977 | 50.00% | 44.00% | $1,660.00 | 66.00% |

| 1.898 | 44.00% | 44.00% | $1,660.00 | 66.00% |

| 1.845 | 40.00% | 40.00% | $1,600.00 | 60.00% |

| 1.648 | 25.00% | 25.00% | $1,375.00 | 37.50% |

| 1.450 | 10.00% | 10.00% | $1,150.00 | 15.00% |

| 1.344 | 2.00% | 2.00% | $1,030.00 | 3.00% |

| 1.331 | 1.00% | 1.00% | $1,015.00 | 1.50% |

| 1.318 | 0.00% | 0.00% | $1,000.00 | 0.00% |

| 1.305 | -1.00% | -1.00% | $1,000.00 | 0.00% |

| 1.292 | -2.00% | -2.00% | $1,000.00 | 0.00% |

| 1.186 | -10.00% | -10.00% | $1,000.00 | 0.00% |

| 1.120 | -15.00% | -15.00% | $1,000.00 | 0.00% |

| 1.054 | -20.00% | -20.00% | $1,000.00 | 0.00% |

| 0.923 | -30.00% | -30.00% | $900.00 | -10.00% |

| 0.659 | -50.00% | -50.00% | $700.00 | -30.00% |

| 0.330 | -75.00% | -75.00% | $450.00 | -55.00% |

| 0.000 | -100.00% | -100.00% | $200.00 | -80.00% |

Hypothetical Examples of Amounts Payable at Maturity

The following hypothetical examples illustrate how the payments at maturity set forth in the table above are calculated.

Example 1: The level of the Index increases from the Initial Level of 1.318 to the Final Level of 1.450. Because the Index percentage change of 10% is less than the Index Return Cap of 44.00%, the investor receives a payment at maturity of $1,150.00 per BUyS Face Amount calculated as follows:

Payment at maturity = $1,000.00 + ($1,000.00 x 10.00% x 150.00%) = $1,150.00

Example 2: The level of the Index increases from the Initial Level of 1.318 to the Final Level of 1.977. Because the Index percentage change of 50% is greater than the Index Return Cap of 44.00%, the investor receives a payment at maturity of $1,660.00 per BUyS Face Amount, the maximum payment on the BUyS.

Payment at maturity = $1,000.00 + ($1,000.00 x 44.00% x 150.00%) = $1,660.00

Example 3: The level of the Index declines from the Initial Level of 1.318 to the Final Level of 1.292. Because the 2% decline in the Index from the Initial Level of 1.318 to the Final Level of 1.292 does not exceed the Buffer Level of 20.00%, the investor receives a payment at maturity of $1,000.00 per BUyS Face Amount.

Payment at maturity = $1,000.00

TS-2

Example 4: The level of the Index declines from the Initial Level of 1.318 to the Final Level of 0.923. Because the 30% decline in the Index from the Initial Level of 1.318 to the Final Level of 0.923 exceeds the Buffer Level of 20.00%, the investor receives a payment at maturity of $900.00 per BUyS Face Amount calculated as follows:

Payment at maturity = $1,000.00 + [$1,000.00 x (-30.00% + 20.00%)] = $900.00

Example 5: The level of the Index declines from the Initial Level of 1.318 to the Final Level of 0.000. Because the decline in the Index from the Initial Level of 1.318 to the Final Level of 0.000 exceeds the Buffer Level of 20.00%, the investor receives a payment at maturity of $200.00 per BUyS Face Amount calculated as follows:

Payment at maturity = $1,000.00 + [$1,000.00 x (-100.00% + 20.00%)] = $200.00

Selected Purchase Considerations

| • | THE APPRECIATION POTENTIAL OF THE BUYS IS LIMITED — You will not benefit from any appreciation of the Index beyond the Index Return Cap of between 41.00% and 47.00% (to be determined on the Trade Date), and therefore the maximum payment you can receive is between $1,615.00 and $1,705.00 (to be determined on the Trade Date) for each $1,000 Face Amount of BUyS. Because the BUyS are our senior obligations, payment of any amount at maturity is subject to our ability to pay our obligations as they become due. |

| • | LIMITED PROTECTION AGAINST LOSS — Payment at maturity of the Face Amount of your BUyS is protected against a decline in the Final Level, as compared to the Initial Level, of up to the Buffer Level, subject to our ability to pay our obligations as they become due. If such decline is more than the Buffer Level of 20.00%, for every 1% decline beyond the Buffer Level, you will lose an amount equal to 1% of the Face Amount of your BUyS. For example, an Index Return of -30.00% will result in a 10% loss of your initial investment. |

| • | RETURN LINKED TO PERFORMANCE OF THE S&P GSCI™ NATURAL GAS INDEX EXCESS RETURN — The return on the BUyS is linked to the S&P GSCI™ Natural Gas Index Excess Return, a sub-index of the S&P GSCI™, a world production-weighted index that is designed to reflect the relative significance of principal non-financial commodities (i.e., physical commodities) in the world economy, which is calculated, maintained and published daily by Standard & Poor’s, a division of McGraw-Hill Companies. The S&P GSCI™ Natural Gas Index Excess Return is intended to provide investors with a publicly available benchmark for investment performance in the natural gas commodity markets. As presently constituted, the only contracts used to calculate the Index are the natural gas futures contracts traded on the New York Mercantile Exchange (“NYMEX”). For purposes of calculating the total dollar value traded, the Index also takes into account the trading volume of the Intercontinental Exchange (“ICE”) Henry Hub Natural Gas Cleared Swap. For more information on the Index, including its calculation methodology, see “The S&P GSCI™ Natural Gas Index Excess Return” in this term sheet. |

| • | A COMMODITY HEDGING DISRUPTION EVENT MAY RESULT IN ACCELERATION OF THE BUYS — If a commodity hedging disruption event (as defined under “Additional Terms of the BUyS — Commodity Hedging Disruption Events”) occurs, we will have the right, but not the obligation, to accelerate the payment on the BUyS. The amount due and payable per $1,000 BUyS Face Amount of securities upon such early acceleration will be determined by the calculation agent in good faith in a commercially reasonable manner on the date on which we deliver notice of such acceleration and will be payable on the fifth business day following the day on which the calculation agent delivers notice of such acceleration. |

Please see the risk factor entitled “Commodity Futures Contracts are Subject to Uncertain Legal and Regulatory Regimes, Which May Result in a Hedging Disruption Event and a Loss on Your Investment” for more information.

| • | CERTAIN TAX CONSEQUENCES — You should review carefully the section of the accompanying product supplement entitled “Certain U.S. Federal Income Tax Consequences.” Although the tax consequences of an investment in the BUyS are uncertain, we believe it is reasonable to treat the BUyS as prepaid financial contracts for U.S. federal income tax purposes. Based on current law, under this treatment you should not be required to recognize taxable income prior to the maturity of your BUyS, other than pursuant to a sale or exchange, and your gain or loss on the BUyS should be long-term capital gain or loss if you hold the BUyS for more than one year. If, however, the Internal Revenue Service (the “IRS”) were successful in asserting an |

TS-3

| alternative treatment for the BUyS, the timing and/or character of income on the BUyS might differ materially and adversely from the description herein. We do not plan to request a ruling from the IRS, and no assurance can be given that the IRS or a court will agree with the tax treatment described in this term sheet and the accompanying product supplement. |

In December 2007, the Department of the Treasury (“Treasury”) and the IRS released a notice requesting comments on various issues regarding the U.S. federal income tax treatment of “prepaid forward contracts” and similar instruments, such as the BUyS. The notice focuses in particular on whether to require holders of these instruments to accrue income over the term of their investment. It also asks for comments on a number of related topics, including the character of income or loss with respect to these instruments; the relevance of factors such as the nature of the underlying property to which the instruments are linked; the degree, if any, to which income (including any mandated accruals) realized by non-U.S. holders should be subject to withholding tax; and whether these instruments are or should be subject to the “constructive ownership” regime, which very generally can operate to recharacterize certain long-term capital gain as ordinary income that is subject to an interest charge. While the notice requests comments on appropriate transition rules and effective dates, any Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the BUyS, possibly with retroactive effect.

Under current law, the United Kingdom will not impose withholding tax on payments made with respect to the BUyS.

For a discussion of certain German tax considerations relating to the BUyS, you should refer to the section in the accompanying prospectus supplement entitled “Taxation by Germany of Non-Resident Holders.”

| We do not provide any advice on tax matters. Both U.S. and non-U.S. holders should consult their tax advisers regarding all aspects of the U.S. federal tax consequences of investing in the BUyS (including possible alternative treatments and the issues presented by the December 2007 notice), as well as any tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction. |

An investment in the BUyS involves significant risks. Investing in the BUyS is not equivalent to investing directly in the Index or in any of the components of the Index. These risks are explained in more detail in the “Risk Factors” section of the accompanying product supplement.

| • | YOUR INVESTMENT IN THE BUYS IS PROTECTED ONLY TO THE EXTENT OF THE BUFFER LEVEL, SUBJECT TO OUR CREDITWORTHINESS — The BUyS do not guarantee any return of your initial investment in excess of $200.00 per $1,000 BUyS Face Amount. The return on the BUyS at maturity is linked to the performance of the Index and will depend on whether, and the extent to which, the Index Return is positive or negative. Your investment will be exposed to any decline in the Final Level, as compared to the Initial Level, beyond the Buffer Level. Accordingly, you could lose up to $800.00 for each $1,000 that you invest. Payment of any amount at maturity is subject to our ability to meet our obligations as they become due. |

| • | THE RETURN ON YOUR BUYS IS LIMITED BY THE MAXIMUM RETURN — As a holder of the BUyS, you will not benefit from any appreciation of the Index beyond the Index Return Cap of between 41.00% and 47.00% (to be determined on the Trade Date). Consequently, the BUyS are subject to a Maximum Return of between 61.50% and 70.50% (to be determined on the Trade Date) and your payment at maturity will be limited to a maximum payment of between $1,615.00 and $1,705.00 for each $1,000 Face Amount of BUyS you hold, regardless of any further appreciation of the Index, which may be significant. |

| • | ASSUMING NO CHANGES IN MARKET CONDITIONS OR ANY OTHER RELEVANT FACTORS, THE MARKET VALUE OF THE BUYS ON THE SETTLEMENT DATE (AS DETERMINED BY DEUTSCHE BANK AG) WILL BE LESS THAN THE ORIGINAL ISSUE PRICE — While the payment at maturity described in this term sheet is based on the full Face Amount of your BUyS, the original Issue Price of the BUyS includes the agents’ commission and the cost of hedging our obligations under the BUyS through one or more of our affiliates. Therefore, the market value of the BUyS on the Settlement Date, assuming no changes in market conditions or other relevant factors, will be less than the original Issue Price. The inclusion of commissions and hedging costs in the original Issue Price will also decrease the price, if any, at which we will be willing to |

TS-4

| purchase the BUyS after the Settlement Date, and any sale on the secondary market could result in a substantial loss to you. Our hedging costs include the projected profit that we or our affiliates are expected to realize in consideration for assuming the risks inherent in managing the hedging transactions. The BUyS are not designed to be short-term trading instruments. Accordingly, you should be willing and able to hold your BUyS to maturity. |

| • | THE BUYS WILL NOT BE LISTED AND THERE WILL LIKELY BE LIMITED LIQUIDITY — The BUyS will not be listed on any securities exchange. Deutsche Bank AG or its affiliates may offer to purchase the BUyS in the secondary market but are not required to do so and may cease such market-making activities at any time. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the BUyS easily. Because other dealers are not likely to make a secondary market for the BUyS, the price at which you may be able to trade your BUyS is likely to depend on the price, if any, at which Deutsche Bank AG or its affiliates are willing to buy the BUyS. |

| • | THE BUYS ARE SUBJECT TO OUR CREDITWORTHINESS — An actual or anticipated downgrade in our credit rating will likely have an adverse effect on the market value of the BUyS. The payment at maturity on the BUyS is subject to our creditworthiness. |

| • | WE AND OUR AFFILIATES AND AGENTS MAY PUBLISH RESEARCH, EXPRESS OPINIONS OR PROVIDE RECOMMENDATIONS THAT ARE INCONSISTENT WITH INVESTING IN OR HOLDING THE BUYS. ANY SUCH RESEARCH, OPINIONS OR RECOMMENDATIONS COULD AFFECT THE LEVEL OF THE INDEX TO WHICH THE BUYS ARE LINKED OR THE MARKET VALUE OF THE BUYS — Deutsche Bank AG, its affiliates and agents publish research from time to time on financial markets and other matters that may influence the value of the BUyS, or express opinions or provide recommendations that are inconsistent with purchasing or holding the BUyS. Deutsche Bank AG, its affiliates and agents may have published research or other opinions that are inconsistent with the investment view implicit in the BUyS. Any research, opinions or recommendations expressed by Deutsche Bank AG, its affiliates or agents may not be consistent with each other and may be modified from time to time without notice. Investors should make their own independent investigation of the merits of investing in the BUyS and the Index to which the BUyS are linked. |

| • | THE VALUE OF THE BUYS WILL BE AFFECTED BY A NUMBER OF UNPREDICTABLE FACTORS — The value of the BUyS will be affected by the supply of and demand for the BUyS and other factors, many of which are independent of our financial condition and results of operations, including: |

| • | the value of the Index; |

| • | geopolitical conditions and economic, financial, political, regulatory and judicial events that affect natural gas or commodities markets generally; |

| • | the interest rates then prevailing in the market; |

| • | the time remaining to maturity of the BUyS; |

| • | the volatility of natural gas; |

| • | the combined volatility of natural gas as reflected in the volatility and expected volatility of the Index; and |

| • | our creditworthiness, including actual or anticipated downgrades in our credit ratings. |

| • | HIGHER FUTURES PRICES OF THE COMMODITY FUTURES CONTRACTS COMPRISING THE INDEX RELATIVE TO THE CURRENT PRICES OF SUCH CONTRACTS MAY AFFECT THE VALUE OF THE INDEX AND THE VALUE OF THE BUYS — The Index is composed of futures contracts on physical commodities. Unlike equities, which typically entitle the holder to a continuing stake in a corporation, commodity futures contracts normally specify a certain date for delivery of the underlying physical commodity. As the exchange-traded futures contracts that compose the Index approach expiration, they are replaced by contracts that have a later expiration. Thus, for example, a contract purchased and held in October may specify an end-of-the-month October expiration. As time passes, the contract expiring in October is replaced with a contract for delivery in November. This process is referred to as “rolling.” If the market for these contracts is (putting aside other considerations) in “backwardation,” where the prices are lower in the distant delivery months than in the nearer delivery months, the sale of the October contract would take place at a price that is higher than the price of the November contract, thereby creating a positive “roll yield.” While many of the contracts included in the Index have historically exhibited periods of backwardation, backwardation will most likely not exist at all times, and there can be no assurance that backwardation will |

TS-5

| exist at times that are advantageous, with respect to your interests as a holder of the BUyS, to the valuation of the Index. The presence of contango in the commodity markets (i.e., where the prices for the relevant futures contracts are higher in the distant delivery months than in nearby delivery months) could result in negative “roll yields,” which could adversely affect the value of the Index and thus the value of BUyS linked to the Index. The natural gas curve is currently in contango, so if the shape of this curve stays the same throughout the life of the trade and spot prices do not increase enough in order to offset the negative roll yield, the value of the Index and the BUyS may be adversely affected. |

| • | COMMODITY PRICES ARE CHARACTERIZED BY HIGH AND UNPREDICTABLE VOLATILITY, WHICH COULD LEAD TO A HIGH AND UNPREDICTABLE VOLATILITY IN THE INDEX — Market prices of the commodity futures contracts comprising the Index tend to be highly volatile. Commodity market prices are not related to the value of a future income or earnings stream, as tends to be the case with fixed-income and equity investments, but are subject to rapid fluctuations based on numerous factors, including changes in supply and demand relationships, governmental programs and policies, national and international monetary, trade, political and economic events, changes in interest and exchange rates, speculation and trading activities in commodities and related contracts, weather, and agricultural, trade, fiscal and exchange control policies. Many commodities are also highly cyclical. These factors may have a larger impact on commodity prices and commodity-linked instruments than on traditional fixed-income and equity securities. These variables may create additional investment risks that cause the value of the BUyS to be more volatile than the values of traditional securities. These and other factors may affect the level of the Index, and thus the value of your BUyS, in unpredictable or unanticipated ways. The high volatility and cyclical nature of commodity markets may render such an investment inappropriate as the focus of an investment portfolio. |

| • | GLOBAL ENERGY COMMODITY PRICES ARE PRIMARILY AFFECTED BY THE GLOBAL DEMAND FOR AND SUPPLY OF THESE COMMODITIES, BUT ARE ALSO SIGNIFICANTLY INFLUENCED BY SPECULATIVE ACTIONS AND BY CURRENCY EXCHANGE RATES — Prices for energy commodities, which includes natural gas, are affected by governmental programs and policies, national and international political and economic events, changes in interest and exchange rates, trading activities in commodities and related contracts, trade, fiscal, monetary and exchange control policies and with respect to natural gas specifically, drought, floods, weather, government intervention, environmental policies, embargoes and tariffs. Demand for energy products by consumers, as well as the agricultural, manufacturing and transportation industries, affects the price of energy commodities. Sudden disruptions in the supplies of energy commodities, such as those caused by war, natural events, accidents or acts of terrorism, may cause prices of energy commodities futures contracts to become extremely volatile and unpredictable. Also, sudden and dramatic changes in the futures market may occur, for example, upon a cessation of hostilities that may exist in countries producing energy commodities, the introduction of new or previously withheld supplies into the market or the introduction of substitute products or commodities. Demand for energy commodities such as natural gas is generally linked to economic activity, and will tend to reflect general economic conditions. |

| • | COMMODITY FUTURES CONTRACTS ARE SUBJECT TO UNCERTAIN LEGAL AND REGULATORY REGIMES, WHICH MAY RESULT IN A HEDGING DISRUPTION EVENT AND A LOSS ON YOUR INVESTMENT — The commodity futures contracts that comprise the Index are subject to legal and regulatory regimes in the United States and, in some cases, in other countries that may change in ways that could adversely affect our ability to hedge our obligations under the BUyS. The Commodity Futures Trading Commission (the “CFTC”) has recently announced that it is considering imposing position limits on certain commodities (such as energy commodities) and the manner in which current exemptions for bona fide hedging transactions or positions are implemented. Such restrictions may cause us or our affiliates to be unable to effect transactions necessary to hedge our obligations under the BUyS, in which case we may, in our sole and absolute discretion, accelerate the payment on the BUyS early and pay you an amount determined in good faith and in a commercially reasonable manner by the calculation agent. If the payment on the BUyS is accelerated, your investment may result in a loss and you may not be able to reinvest your money in a comparable investment. Please see “Additional Terms of the BUyS — Commodity Hedging Disruption Events” in this term sheet. |

| • | OWNING THE BUYS IS NOT THE SAME AS OWNING ANY COMMODITY FUTURES CONTRACTS — The return on your BUyS will not reflect the return you would realize if you actually held the commodity contracts comprising the Index. The Index is a hypothetical construct that does not hold any underlying assets of any kind. As a result, a holder of the BUyS will not have any direct or indirect rights to any commodity contracts. |

TS-6

| • | SUSPENSION OR DISRUPTIONS OF MARKET TRADING IN THE COMMODITY AND RELATED FUTURES MARKETS MAY ADVERSELY AFFECT THE LEVEL OF THE INDEX, AND THEREFORE THE VALUE OF THE BUYS — The commodity markets are subject to temporary distortions or other disruptions due to various factors, including the lack of liquidity in the markets, the participation of speculators and government regulation and intervention. In addition, U.S. futures exchanges and some foreign exchanges have regulations that limit the amount of fluctuation in options futures contract prices that may occur during a trading day. These limits are generally referred to as “daily price fluctuation limits” and the maximum or minimum price of a contract on any given day as a result of these limits is referred to as a “limit price.” Once the limit price has been reached in a particular contract, no trades may be made at a different price. Limit prices have the effect of precluding trading in a particular contract or forcing the liquidation of contracts at disadvantageous times or prices. These circumstances could adversely affect the level of the Index and, therefore, the value of your BUyS. |

| • | THE INDEX MAY BE MORE VOLATILE AND SUSCEPTIBLE TO PRICE FLUCTUATIONS OF COMMODITIES THAN A BROADER COMMODITIES INDEX — The Index may be more volatile and susceptible to price fluctuations than a broader commodities index, such as the S&P GSCI™. In contrast to the S&P GSCI™, which includes contracts on natural gas and other energy commodities, the Index is comprised of contracts on only natural gas. As a result, price volatility in the contracts included in the Index will likely have a greater impact on the Index than it would on the broader S&P GSCI™. In addition, because the Index omits principal market sectors comprising the S&P GSCI™, it will be less representative of the economy and commodity markets as a whole and will therefore not serve as a reliable benchmark for commodity market performance generally. |

| • | THE BUYS ARE LINKED TO AN EXCESS RETURN INDEX AND NOT A TOTAL RETURN INDEX — The BUyS are linked to an excess return index and not a total return index. An excess return index reflects the returns that are potentially available through an unleveraged investment in the contracts composing such index. By contrast, a “total return” index, in addition to reflecting those returns, also reflects interest that could be earned on funds committed to the trading of the underlying futures contracts. |

| • | TRADING BY US OR OUR AFFILIATES IN THE COMMODITIES MARKETS MAY IMPAIR THE VALUE OF THE BUYS — We and our affiliates are active participants in the commodities markets as dealers, proprietary traders and agents for our customers, and therefore at any given time we may be a party to one or more commodities transactions. In addition, we or one or more of our affiliates may hedge our commodity exposure from the BUyS by entering into various transactions. We may adjust these hedges at any time and from time to time. Our trading and hedging activities may have a material adverse effect on the commodities prices and consequently have a negative impact on the performance of the Index including on the Final Valuation Date, which would affect your payment at maturity. It is possible that we or our affiliates could receive significant returns from these hedging activities while the value of or amounts payable under the BUyS may decline. |

| • | THE U.S. FEDERAL INCOME TAX CONSEQUENCES OF AN INVESTMENT IN A BUYS ARE UNCLEAR — There is no direct legal authority regarding the proper U.S. federal income tax treatment of the BUyS, and we do not plan to request a ruling from the IRS. Consequently, significant aspects of the tax treatment of the BUyS are uncertain, and no assurance can be given that the IRS or a court will agree with the treatment of the BUyS as prepaid financial contracts. If the IRS were successful in asserting an alternative treatment for the BUyS, the timing and/or character of income thereon might differ materially and adversely from the description herein. As described above under “Certain Tax Consequences,” in December 2007, Treasury and the IRS released a notice requesting comments on various issues regarding the U.S. federal income tax treatment of “prepaid forward contracts” and similar instruments, such as the BUyS. Any Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the BUyS, possibly with retroactive effect. Both U.S. and non-U.S. holders should review carefully the section of the accompanying product supplement entitled “Certain U.S. Federal Income Tax Consequences,” and consult their tax advisers regarding the U.S. federal income tax consequences of an investment in the BUyS (including possible alternative treatments and the issues presented by the December 2007 notice), as well as any tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction. |

The BUyS may be suitable for you if:

| • | You seek an investment with a return linked to the performance of the Index; |

TS-7

| • | You are willing to invest in the BUyS based on the Participation Rate, indicated Index Return Cap (the actual Index Return Cap will be set on the Trade Date) and Buffer Level; |

| • | You are willing to lose up to 80.00% of your initial investment, subject to our creditworthiness; |

| • | You are willing and able to hold the BUyS to maturity; |

| • | You are willing to accept our credit risk; and |

| • | You do not seek current income from this investment. |

The BUyS may not be suitable for you if:

| • | You do not seek an investment with exposure to the Index; |

| • | You are unwilling or unable to hold the BUyS to maturity; |

| • | You seek an investment that is protected against the loss of your initial investment beyond the Buffer Level; |

| • | You are not willing to be exposed to our credit risk; |

| • | You seek current income from your investments; or |

| • | You seek an investment for which there will be an active secondary market. |

The S&P GSCI™ Natural Gas Index Excess Return

We have derived all information regarding the S&P GSCI™ Natural Gas Index Excess Return and S&P GSCI™ contained in this term sheet, including, without limitation, their make-up, method of calculation, and changes in their components, from publicly available information, and we have not participated in the preparation of, or verified, such publicly available information. Such information reflects the policies of, and is subject to change by, Standard & Poor’s, a division of The McGraw-Hill Companies (“S&P”). The Index is calculated, maintained and published by S&P. The value of the S&P GSCI™ Natural Gas Index Excess Return is published each trading day under the Bloomberg ticker symbol “SPGSNGP”.

The Index is intended to provide investors with a publicly available benchmark for investment performance in the natural gas commodity markets and is a sub-index of the S&P GSCI™, a composite index of commodity sector returns. S&P acquired the rights to the S&P GSCI™ from Goldman, Sachs & Co. in February 2007. Goldman, Sachs & Co. established and began calculating the S&P GSCI™ in May 1991. The former name of the S&P GSCI™ was the Goldman Sachs Commodity Index, or GSCI®.

The S&P GSCI™ is an index on a world production-weighted basket of principal non-financial commodities (i.e., physical commodities) that satisfy specified criteria. The S&P GSCI™ is designed to be a measure of the performance over time of the markets for these commodities. The only commodities represented in the S&P GSCI™ are those physical commodities on which active and liquid contracts are traded on trading facilities in major industrialized countries. The commodities included in the S&P GSCI™ are weighted, on a production basis, to reflect the relative significance (in the view of S&P, in consultation with its Index Advisory Panel, as described below) of such commodities to the world economy. The fluctuations in the value of the S&P GSCI™ are intended generally to correlate with changes in the prices of such physical commodities in global markets. The S&P GSCI™ has been normalized such that its hypothetical level on January 2, 1970 was 100. Futures contracts on the S&P GSCI™, and options on such futures contracts, are currently listed for trading on the Chicago Mercantile Exchange.

The Index reflects the excess return that is potentially available through an unleveraged investment in the natural gas futures contracts included in the S&P GSCI™. Since the S&P GSCI™ is the parent index of the Index, the methodology for the S&P GSCI™ relates as well to the methodology of the Index.

The Index provides investors with a publicly available benchmark for investment performance in the natural gas commodity markets. As presently constituted, the only contracts used to calculate the Index are the natural gas futures contracts (the “Index Component”) traded on the New York Mercantile Exchange. For purposes of calculating the total dollar value traded, the Index also takes into account the trading volume of the ICE Henry Hub Natural Gas Cleared Swap. The natural gas futures contracts included in the Index change on a monthly basis because the futures contracts included in the Index at any given time are currently required to be the natural gas futures contracts traded on the NYMEX with the closest expiration date (the “front-month contract”). The front-month contract expires each month two business days prior to the last business day of such month. The Index incorporates a methodology for rolling the current futures contract into the futures contract with the next closest

TS-8

expiration date (the “next-month contract”) each month. Assuming that markets are not disrupted or the limitations that regulate the amount of fluctuation in options futures contract prices that may occur during a trading day have not been reached, the Index gradually reduces the weighting of the front-month contract and increases the weighting of the next-month contract over a five business day period commencing on the fifth business day of the month, so that on the first day of the roll-over the front-month contract represents 80% and the next-month contract represents 20% of the Index, and on the fifth day of the roll-over period (i.e., the ninth business day of the month) the next-month contract represents 100% of the Index.

The value of the Index on any given day reflects:

| · | the price levels of the contracts included in the Index (which represents the value of the Index), and |

| · | the “contract daily return,” which is the percentage change in the total dollar weight of the Index from the previous day to the current day. |

Set forth below is a summary of the composition of and the methodology used to calculate the S&P GSCI™ and the Index. The methodology for determining the composition and weighting of the Index and the S&P GSCI™ and for calculating their values is subject to modification in a manner consistent with the purposes of the Index and the S&P GSCI™, as described below. S&P makes the official calculations of the S&P GSCI™ and the Index.

The Index Committee and the Index Advisory Panel

S&P has established an Index Committee to oversee the daily management and operations of the S&P GSCI™, and is responsible for all analytical methods and calculation of the indices. The Committee is comprised of three full-time professional members of S&P’s staff and two members of Goldman Sachs Group, Inc. At each meeting, the Committee reviews any issues that may affect index constituents, statistics comparing the composition of the indices to the market, commodities that are being considered as candidates for an addition to an index, and any significant market events. In addition, the Index Committee may revise index policy covering rules for selecting commodities or other matters.

S&P considers information about changes to its indices and related matters to be potentially market- moving and material. Therefore, all Index Committee discussions are confidential.

S&P has established an Index Advisory Panel (the “Advisory Panel”) to assist it in connection with the operation of the S&P GSCI™. The Advisory Panel meets on an annual basis and at other times at the request of the Index Committee. The principal purpose of the Advisory Panel is to advise the Index Committee and S&P with respect to, among other things, the calculation of the S&P GSCI™, the effectiveness of the S&P GSCI™ as a measure of commodity futures market performance and the need for changes in the composition or in the methodology of the S&P GSCI™. The Advisory Panel acts solely in an advisory and consultative capacity; all decisions with respect to the composition, calculation and operation of the S&P GSCI™ are made by the Index Committee and S&P.

Composition of the S&P GSCI™

In order to be included in the S&P GSCI™, a contract must satisfy the following general eligibility criteria:

| · | The contract must be in respect of a physical commodity and not a financial commodity. |

| · | In addition, the contract must: |

| · | have a specified expiration or term or provide in some other manner for delivery or settlement at a specified time, or within a specified period, in the future; and |

| · | at any given point in time, be available for trading at least five months prior to its expiration or such other date or time period specified for delivery or settlement. |

Beginning in January 2007, the trading facility (as defined below) on which the contract trades must allow market participants to execute spread transactions, through a single order entry, between the pairs of contract expirations (defined below) included in the S&P GSCI™ that, at any given point in time, will be involved in the rolls to be effected in the next three roll periods (defined below).

The commodity must be the subject of a contract that:

| · | is denominated in U.S. dollars; and |

| · | is traded on or through an exchange, facility or other platform (referred to as a “trading facility”) that has its principal place of business or operations in a country that is a member of the Organization for Economic Cooperation and Development during the relevant annual calculation period or interim calculation period and that: |

TS-9

| · | makes price quotations generally available to its members or participants (and to S&P) in a manner and with a frequency that is sufficient to provide reasonably reliable indications of the level of the relevant market at any given point in time; |

| · | makes reliable trading volume information available to S&P with at least the frequency required by S&P to make the monthly determinations; |

| · | accepts bids and offers from multiple participants or price providers; and |

| · | is accessible by a sufficiently broad range of participants. |

With respect to inclusion on each sub-index of the S&P GSCI™, a contract must be in respect to the physical commodity that is described by that specific index.

The price of the relevant contract that is used as a reference or benchmark by market participants (referred to as the “daily contract reference price”) generally must have been available on a continuous basis for at least two years prior to the proposed date of inclusion in the S&P GSCI™. In appropriate circumstances, however, S&P, in consultation with the Advisory Panel, may determine that a shorter time period is sufficient or that historical daily contract reference prices for such contract may be derived from daily contract reference prices for a similar or related contract. The daily contract reference price may be (but is not required to be) the settlement price or other similar price published by the relevant trading facility for purposes of margining transactions or for other purposes.

At and after the time a contract is included in the S&P GSCI™, the daily contract reference price for such contract must be published between 10:00 a.m. and 4:00 p.m., New York City time, on each business day relating to such contract by the trading facility on or through which it is traded and must generally be available to all members of, or participants in, such facility (and to S&P) on the same day from the trading facility or through a recognized third-party data vendor. Such publication must include, at all times, daily contract reference prices for at least one expiration or settlement date that is five months or more from the date the determination is made, as well as for all expiration or settlement dates during such five-month period.

For a contract to be eligible for inclusion in the S&P GSCI™, volume data with respect to such contract must be available for at least the three months immediately preceding the date on which the determination is made. The following eligibility criteria apply:

| · | A contract that is not included in the S&P GSCI™ at the time of determination and that is based on a commodity that is not represented in the S&P GSCI™ at such time must, in order to be added to the S&P GSCI™ at such time, have a total dollar value traded, over the relevant period, as the case may be and annualized, of at least U.S. $15 billion. The total dollar value traded equals (i) the dollar value of the total quantity of the commodity underlying transactions in the relevant contract over the period for which the calculation is made, multiplied by (ii) the average of the daily contract reference prices on the last day of each month during such period. |

| · | A contract that is already included in the S&P GSCI™ at the time of determination and that is the only contract on the relevant commodity included in the S&P GSCI™ must, in order to continue to be included in the S&P GSCI™ after such time, have a total dollar value traded, over the relevant period, as the case may be and annualized, of at least U.S. $5 billion and at least U.S. $10 billion during at least one of the three most recent annual periods used in making the determination. |

| · | A contract that is not included in the S&P GSCI™ at the time of determination and that is based on a commodity on which there are one or more contracts already included in the S&P GSCI™ at such time must, in order to be added to the S&P GSCI™ at such time, have a total dollar value traded, over the relevant period, as the case may be and annualized of at least U.S. $30 billion. |

| · | A contract that is already included in the S&P GSCI™ at the time of determination and that is based on a commodity on which there are one or more contracts already included in the S&P GSCI™ at such time must, in order to continue to be included in the S&P GSCI™ after such time, have a total dollar value traded, over the relevant period, as the case may be and annualized, of at least U.S. $10 billion and at least U.S. $20 billion during at least one of the three most recent annual periods used in making the determination. |

In addition:

TS-10

| · | A contract that is already included in the S&P GSCI™ at the time of determination must, in order to continue to be included after such time, have a reference percentage dollar weight of at least 0.10%. The reference percentage dollar weight is determined by dividing the reference dollar weight of such contract by the sum of the reference dollar weights of all designated contracts. The reference dollar weight of a contract is determined by multiplying the CPW (defined below) of a contract by the average of its daily contract reference prices on the last day of each month during the relevant period. These reference percentage dollar weight amounts are summed for all contracts included in the S&P GSCI™ and each contract’s percentage of the total is then determined. |

| · | A contract that is not included in the S&P GSCI™ at the time of determination must, in order to be added to the S&P GSCI™ at such time, have a reference percentage dollar weight of at least 1.0%. |

| · | In the event that two or more contracts on the same commodity satisfy the eligibility criteria, such contracts will be included in the S&P GSCI™ in the order of their respective total quantity traded during the relevant period (determined as the total quantity of the commodity underlying transactions in the relevant contract), with the contract having the highest total quantity traded being included first, provided that no further contracts will be included if such inclusion would result in the portion of the S&P GSCI™ attributable to such commodity exceeding a particular level. |

| · | If additional contracts could be included with respect to several commodities at the same time, that procedure is first applied with respect to the commodity that has the smallest portion of the S&P GSCI™ attributable to it at the time of determination. Subject to the other eligibility criteria relating to the composition of the S&P GSCI™ the contract with the highest total quantity traded on such commodity will be included. Before any additional contracts on the same commodity or on any other commodity are included, the portion of the S&P GSCI™ attributable to all commodities is recalculated. The selection procedure described above is then repeated with respect to the contracts on the commodity that then has the smallest portion of the S&P GSCI™ attributable to it. |

The contracts currently included in the S&P GSCI™ are all futures contracts traded on the NYMEX, the ICE Futures, the Chicago Mercantile Exchange (“CME”), the CBOT, the Coffee, Sugar & Cocoa Exchange, Inc. (“CSC”), the New York Cotton Exchange (“NYC”), the Kansas City Board of Trade (“KBT”), the Commodities Exchange Inc. (“CMX”) and the London Metal Exchange (“LME”).

The quantity of each of the contracts included in the S&P GSCI™ is determined on the basis of a five-year average (referred to as the “world production average”) of the production quantity of the underlying commodity as published by the United Nations Statistical Yearbook, the Industrial Commodity Statistics Yearbook and other official sources. However, if a commodity is primarily a regional commodity, based on its production, use, pricing, transportation, or other factors, S&P, in consultation with its advisory committee may calculate the weight of such commodity based on regional, rather than world, production data. At present, natural gas is the only commodity the weight of which is calculated on the basis of regional production data, with the relevant region being North America.

The five-year moving average is updated annually for each commodity included in the S&P GSCI™, based on the most recent five-year period (ending approximately two years prior to the date of calculation and moving backwards) for which complete data for all commodities is available. The contract production weights, or CPWs, used in calculating the S&P GSCI™ are derived from world or regional production averages, as applicable, of the relevant commodities, and are calculated based on the total quantity traded for the relevant contract and the world or regional production average, as applicable, of the underlying commodity. However, if the volume of trading in the relevant contract, as a multiple of the production levels of the commodity, is below specified thresholds, the CPW of the contract is reduced until the threshold is satisfied. This is designed to ensure that trading in each such contract is sufficiently liquid relative to the production of the commodity.

In addition, S&P performs this calculation on a monthly basis and, if the multiple of any contract is below the prescribed threshold, the composition of the S&P GSCI™ is reevaluated, based on the criteria and weighting procedure described above. This procedure is undertaken to allow the S&P GSCI™ to shift from contracts that have lost substantial liquidity into more liquid contracts, during the course of a given year. As a result, it is possible that the composition or weighting of the S&P GSCI™ will change on one or more of these monthly evaluation dates. In addition, regardless of whether any changes have occurred during the year, S&P reevaluates the composition of the S&P GSCI™, in consultation with the Advisory Panel, at the conclusion of each year, based on the above criteria. Other commodities that satisfy such criteria, if any, will be added to the S&P GSCI™. Commodities included in the S&P GSCI™ which no longer satisfy such criteria, if any, will be deleted.

TS-11

S&P, in consultation with the Advisory Panel, also determines whether modifications in the selection criteria or the methodology for determining the composition and weights of and for calculating the S&P GSCI™ are necessary or appropriate in order to assure that the S&P GSCI™ represents a measure of commodity market performance. S&P has the discretion to make any such modifications, in consultation with the Advisory Panel.

Contract Expirations

Because the S&P GSCI™ comprises actively traded contracts with scheduled expirations, it can only be calculated by reference to the prices of contracts for specified expiration, delivery or settlement periods, referred to as “contract expirations.” The contract expirations included in the S&P GSCI™ for each commodity during a given year are designated by S&P, in consultation with the Advisory Panel, provided that each such contract must be an “active contract.” An “active contract” for this purpose is a liquid, actively traded contract expiration, as defined or identified by the relevant trading facility or, if no such definition or identification is provided by the relevant trading facility, as defined by standard custom and practice in the industry.

If a trading facility deletes one or more contract expirations, the S&P GSCI™ will be calculated during the remainder of the year in which such deletion occurs on the basis of the remaining contract expirations designated by S&P. If a trading facility ceases trading in all contract expirations relating to a particular contract, S&P may designate a replacement contract on the commodity. The replacement contract must satisfy the eligibility criteria for inclusion in the S&P GSCI™. To the extent practicable, the replacement will be effected during the next monthly review of the composition of the S&P GSCI™. If that timing is not practicable, S&P will determine the date of the replacement and will consider a number of factors, including the differences between the existing contract and the replacement contract with respect to contractual specifications and contract expirations.

Value of the S&P GSCI™

The value of the S&P GSCI™ on any given day is equal to the total dollar weight of the S&P GSCI™ divided by a normalizing constant that assures the continuity of the S&P GSCI™ over time. The total dollar weight of the S&P GSCI™ is the sum of the dollar weight of each of the underlying commodities.

The dollar weight of each such commodity on any given day is equal to:

| · | the daily contract reference price, |

| · | multiplied by the appropriate CPWs, and |

| · | during a roll period, the appropriate “roll weights” (discussed below). |

The daily contract reference price used in calculating the dollar weight of each commodity on any given day is the most recent daily contract reference price made available by the relevant trading facility, except that the daily contract reference price for the most recent prior day will be used if the exchange is closed or otherwise fails to publish a daily contract reference price on that day. In addition, if the trading facility fails to make a daily contract reference price available or publishes a daily contract reference price that, in the reasonable judgment of S&P, reflects manifest error, the relevant calculation will be delayed until the price is made available or corrected; provided, that, if the price is not made available or corrected by 4:00 p.m., New York City time, S&P may, if it deems such action to be appropriate under the circumstances, determine the appropriate daily contract reference price for the applicable futures contract in its reasonable judgment for purposes of the relevant S&P GSCI™ calculation.

Contract Daily Return

The contract daily return on any given day is equal to the sum, for each of the commodities included in the S&P GSCI™ of the applicable daily contract reference price on the relevant contract multiplied by the appropriate CPW and the appropriate “roll weight,” divided by the total dollar weight of the S&P GSCI™ on the preceding day, minus one.

The “roll weight” of each commodity reflects the fact that the positions in contracts must be liquidated or rolled forward into more distant contract expirations as they approach expiration. If actual positions in the relevant markets were rolled forward, the roll would likely need to take place over a period of days. Since the S&P GSCI™ is designed to replicate the performance of actual investments in the underlying contracts, the rolling process incorporated in the S&P GSCI™ also takes place over a period of days at the beginning of each month (referred to as the “roll period”). On each day of the roll period, the “roll weights” of the first nearby contract expiration on a particular commodity and the more distant contract expiration into which it is rolled are adjusted, so that the hypothetical position in the contract on the commodity that is included in the S&P GSCI™ is gradually shifted from the first nearby contract expiration to the more distant contract expiration.

TS-12

If on any day during a roll period any of the following conditions exists, the portion of the roll that would have taken place on that day is deferred until the next day on which such conditions do not exist:

| · | no daily contract reference price is available for a given contract expiration; |

| · | any such price represents the maximum or minimum price for such contract month, based on exchange price limits (referred to as a “Limit Price”); |

| · | the daily contract reference price published by the relevant trading facility reflects manifest error, or such price is not published by 4:00 p.m., New York City time. In that event, S&P may, but is not required to, determine a daily contract reference price and complete the relevant portion of the roll based on such price; provided, that, if the trading facility publishes a price before the opening of trading on the next day, S&P will revise the portion of the roll accordingly; or |

| · | trading in the relevant contract terminates prior to its scheduled closing time. |

If any of these conditions exist throughout the roll period, the roll with respect to the affected contract, will be effected in its entirety on the next day on which such conditions no longer exist.

Calculation of the Index

The value of the Index on any S&P GSCI™ business day is equal to the product of (1) the value of the underlying futures contracts on the immediately preceding S&P GSCI™ business day multiplied by (2) one plus the contract daily return of the applicable Index on the S&P GSCI™ business day on which the calculation is made.

License Agreement with Standard & Poor’s

The S&P GSCI™ and the Index are licensed by S&P for use in connection with an issuance of the BUyS.

The BUyS are not sponsored, endorsed, sold or promoted by S&P. S&P does not make any representations or warranties, express or implied, to the owners of the BUyS or any member of the public regarding the advisability of investing in securities generally or in the BUyS particularly or the ability of the S&P indices to track general stock market performance or any economic factors. S&P’s only relationship to Deutsche Bank AG (the “Licensee”) and its affiliates is the licensing of certain trademarks and trade names of S&P and/or of the S&P GSCI™ which is determined, composed and calculated by S&P without regard to the Licensee or the BUyS. S&P has no obligation to take the needs of the Licensee, its affiliates or the owners of the BUyS into consideration in determining, composing or calculating the S&P GSCI™. S&P is not responsible for and have not participated in the determination of, the timing of, prices at, or quantities of the BUyS to be issued or in the determination or calculation of the equation by which the BUyS are to be converted into cash. S&P has no obligation or liability in connection with the administration, marketing or trading of the BUyS.

S&P DOES NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF THE S&P GSCI™ OR ANY DATA INCLUDED THEREIN, AND S&P SHALL HAVE NO LIABILITY FOR ANY ERRORS, OMISSIONS, OR INTERRUPTIONS THEREIN. S&P MAKES NO WARRANTIES, EXPRESS OR IMPLIED, CONDITIONS OR REPRESENTATIONS AS TO RESULTS TO BE OBTAINED BY LICENSEE, ITS AFFILIATES, OWNERS OF THE BUyS OR ANY OTHER PERSON OR ENTITY FROM THE USE OF THE S&P GSCI™ OR ANY DATA INCLUDED THEREIN. S&P MAKES NO EXPRESS OR IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIM ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE WITH RESPECT TO THE S&P GSCI™ OR ANY DATA INCLUDED THEREIN. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT SHALL S&P HAVE ANY LIABILITY FOR ANY SPECIAL, PUNITIVE, INDIRECT, OR CONSEQUENTIAL DAMAGES (INCLUDING LOST PROFITS), EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.

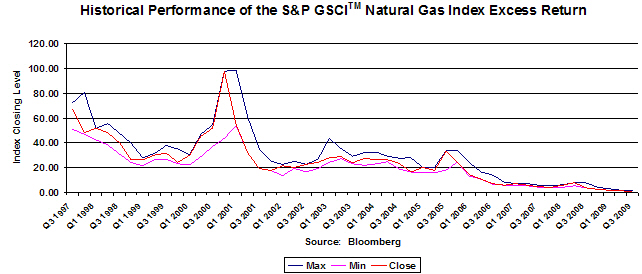

Historical Information

The following graph sets forth the historical performance of the Index based on the daily Index closing levels from August 1, 2007 through August 27, 2009. The Index closing level on August 27, 2009 was 1.31755. We obtained the Index closing levels below from Bloomberg, and we have not participated in the preparation of, or verified, such information. The historical levels of the Index should not be taken as an indication of future performance, and no assurance can be given as to the Final Level of the Index. We cannot give you assurance that the performance of the Index will result in the return of your initial investment in excess of the Buffer Level.

TS-13

Additional Terms of the BUyS

Commodity Hedging Disruption Events

If a commodity hedging disruption event (as defined below) occurs, we will have the right, but not the obligation, to accelerate the payment on the BUyS by providing, or causing the calculation agent to provide, written notice of our election to exercise such right to the trustee at its New York office, on which notice the trustee may conclusively rely, as promptly as possible and in no event later than the business day immediately following the day on which such commodity hedging disruption event occurred.. The amount due and payable per $1,000 Face Amount of securities upon such early acceleration will be determined by the calculation agent in good faith in a commercially reasonable manner on the date on which we deliver notice of such acceleration and will be payable on the fifth business day following the day on which the calculation agent delivers notice of such acceleration. We will provide, or will cause the calculation agent to provide, written notice to the trustee at its New York office, on which notice the trustee may conclusively rely, and to DTC of the cash amount due with respect to the BUyS as promptly as possible and in no event later than two business days prior to the date on which such payment is due. For the avoidance of doubt, the determination set forth above is only applicable to the amount due with respect to acceleration as a result of a commodity hedging disruption event.

A “commodity hedging disruption event” means that:

| (a) | due to (i) the adoption of, or any change in, any applicable law, regulation or rule or (ii) the promulgation of, or any change in, the interpretation by any court, tribunal or regulatory authority with competent jurisdiction of any applicable law, rule, regulation or order (including, without limitation, as implemented by the CFTC or any exchange or trading facility), in each case occurring on or after the pricing date, the calculation agent determines in good faith that it is contrary to such law, rule, regulation or order to purchase, sell, enter into, maintain, hold, acquire or dispose of our or our affiliates’ (A) positions or contracts in securities, options, futures, derivatives or foreign exchange or (B) other instruments or arrangements, in each case, in order to hedge individually or in the aggregate on a portfolio basis our obligations under the BUyS (“hedge positions”), including, without limitation, if such hedge positions are (or, but for the consequent disposal thereof, would otherwise be) in excess of any allowable position limit(s) in relation to any commodity traded on any exchange(s) or other trading facility (it being within the sole and absolute discretion of the calculation agent to determine which of the hedge positions are counted towards such limit); or |

| (b) | for any reason, we or our affiliates are unable, after using commercially reasonable efforts, to (i) acquire, establish, re-establish, substitute, maintain, unwind or dispose of any transaction(s) or asset(s) the calculation agent deems necessary to hedge the risk of entering into and performing our commodity-related obligations with respect to the BUyS, or (ii) realize, recover or remit the proceeds of any such transaction(s) or asset(s). |

TS-14

Supplemental Underwriting Information

Deutsche Bank Securities Inc. (“DBSI”) and Deutsche Bank Trust Company Americas, acting as agents for Deutsche Bank AG, will receive or allow as a concession to other dealers discounts and commissions that will depend on market conditions on the Trade Date. In no event will such discounts and commissions exceed 0.50% or $5.00 per $1,000 BUyS Face Amount. DBSI may pay custodial fees to other broker-dealers of up to 0.25% or $2.50 per $1,000 BUyS Face Amount. Deutsche Bank AG will reimburse DBSI for such fees. See “Underwriting” in the accompanying product supplement.

We expect to deliver the BUyS against payment for the BUyS on the Settlement Date indicated above, which may be a date that is greater than three business days following the Trade Date. Under Rule 15c6-1 of the Securities Exchange Act of 1934, as amended, trades in the secondary market generally are required to settle in three business days, unless the parties to a trade expressly agree otherwise. Accordingly, if the Settlement Date is more than three business days after the Trade Date, purchasers who wish to transact in the BUyS more than three business days prior to the Settlement Date will be required to specify alternative settlement arrangements to prevent a failed settlement.

TS-15