| buffered underlying securities (BUys) AN OUT-PERFORMANCE alternative |

|

World Class Financial Engineering

+

Industry Leading Education and Marketing

=

Innovative Simplicity(SM)

|

|

buys

buffered underlying securities (buys)

1. buffered underlying securities (BUyS):

a flexible, OUT-PERFORMANCE investment tool for investors

o We believe that Structured Products are playing an ever-growing role in

generating returns, as well as in assisting investors with managing portfolio

risk and volatility

o BUyS are a Structured Product that provides investors with limited

protection of their investment at maturity subject to the credit of the

issuer, while still providing for participation in the appreciation of an

underlying

o BUyS may be structured to provide investors with exposure to a wide variety of

assets including equity, equity indices, commodities, commodity indices,

currencies and currency indices

2. DWS Investments + Deutsche Bank = Innovative SimplicitysM

o DWS Investments and Deutsche Bank combine world class asset management,

structuring and risk management expertise in a coordinated manner

o DWS Investments, the US retail brand name of Deutsche Asset Management (DeAM),

strives to deliver superior performance and innovative investment solutions

o Deutsche Bank, 2008 Global Derivatives House of the Year,(1) is a global

leader in derivatives and structuring across all asset classes

3. Structured Products are one of the fastest growing Investments

in the US

o Financial professionals have identified Structured Products as an increasingly

important investment tool(2)

o Investors increasingly look to Structured Products to meet specific stages of

investor life cycles, as well as to provide innovative, solutions-oriented

investments

1 Derivatives Week, October 13, 2008.

2 Tomorrow's Product for Tomorrow's Client: Innovation imperatives in global asset

management, Professor Amin Rajan, Barbara Martin and Janette Shaw, Creative Limited

2006.

|

| buys STRUCTURED Products Structured Products are financially engineered, packaged investments comprised of multiple components, typically a performance component and a principal component. The definition of Structured Products is sufficiently broad to include many traditional investments as well as those typically associated with the term. Currently, the most popular Structured Products in the US are structured notes. Structured Products, including structured notes, offer investors an innovative financial tool kit complementary to more traditional investments such as equities, bonds, commodities and currencies. They provide individual investors and their advisors broad flexibility to manage investment needs. Structured notes complement a well diversified portfolio by giving investors: o Access to asset classes that may be difficult or uneconomic to invest in directly o Features, such as leverage or principal protection, that investors often do not have the ability to replicate in a cost effective manner o Potential to optimize the risk/return profile of a given asset class through the use of financial engineering o Potential to decrease overall portfolio volatility ?? Greater flexibility to design an outcome-based investment portfolio Structured notes may be classified into three broad categories: Principal Protected, Yield Enhancement and Out-Performance: o Principal protected notes generally provide for full or substantially full principal protection at maturity, subject to the credit risk of the issuer o Yield enhancement notes typically give investors the opportunity to earn enhanced periodic, contingent coupon payments o Out-Performance notes generally provide for the potential to participate in enhanced returns, typically with limited or no principal protection and subject to an issuer call or other features such as a return cap Financial advisors and individual investors may select structured notes that fit a specific investor's individual risk/return profile, create a more efficient portfolio and/ or provide for a desired payout-be it greater current income, principal protection or enhanced exposure to a particular asset or assets. 2 |

|

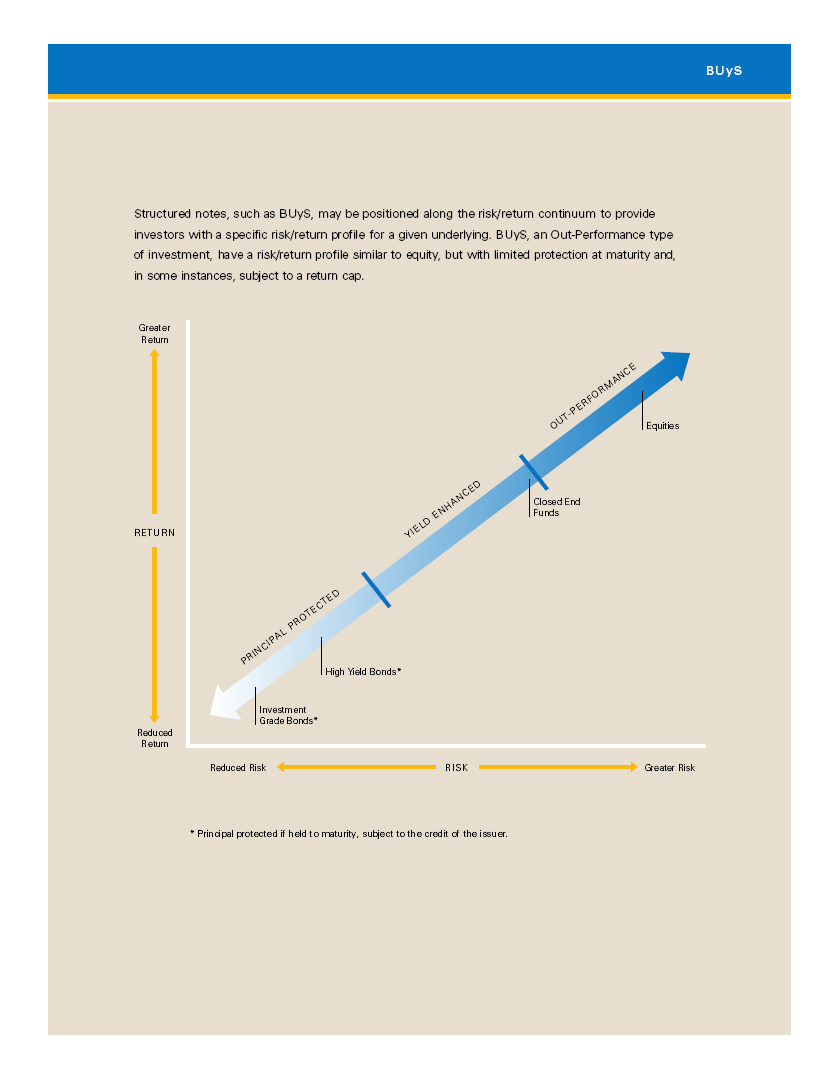

buys

Structured notes, such as BUyS, may be positioned along the risk/return continuum to provide

investors with a specific risk/return profile for a given underlying. BUyS, an Out-Performance type

of investment, have a risk/return profile similar to equity, but with limited protection at

maturity and, in some instances, subject to a return cap.

Greater Return

RETURN

YIELD ENHANCED

-PERFORMANCE

OUT Equities

Closed End

Funds

PRINCIPAL

PROTECTED

High Yield Bonds*

Reduced

Return

Investment

Grade Bonds*

Reduced Risk RISK

Greater Risk

* Principal protected if held to maturity, subject to the credit of the issuer.

|

| STRATEGY STRATEGY As retail and institutional investors seek more intelligent asset allocation, high absolute returns, capital protection and decreased- volatility, Structured Products have been identified by financial professionals as an increasingly important investment tool to meet these complex demands.(1) Buffered Underlying Securities (BUyS) are an Out-Performance type investment that provide investors with limited protection while still providing for participation in the appreciation of the underlying. BUyS are short dated investments that do not pay coupons. Instead, BUyS provide for a one-time payment at maturity based upon the performance of the underlying. The payment at maturity is dependent upon the performance of an underlying, a Buffer Level and, in some instances, a return cap. The Buffer Level is a predetermined percentage set on or prior to the date the securities are priced. It is typically between 10% and 30%, depending upon the specific structure. The Buffer Level provides limited protection against a decline in the underlying during the term of the BUyS. Generally, if the value of the underlying has increased during the term of the BUyS, investors will receive their original investment plus the same percentage increase as that of the underlying. Some BUyS also provide for upside Out-Performance if the value of the underlying has increased-for example, 125% of any such appreciation. Additionally, some BUyS may have a return cap, thereby creating a cap on the maximum return an investor may receive. In cases where the value of the underlying has decreased, if the underlying has declined by less than the Buffer Level, investors will receive their original investment amount at maturity. If, however, the underlying has declined by more than the Buffer Level, the Buffer Level will offset a portion of any such loss and also represents the minimum return at maturity. 1 Tomorrow's Product for Tomorrow's Client: Innovation imperatives in global asset management, Professor Amin Rajan, Barbara Martin and Janette Shaw, Creative Limited 2006. 4 |

| strategy Investment BUyS are SEC registered, corporate debt securities that have a fixed maturity date. Investors in BUyS assume the issuer's credit risk and any payments due on the securities, including any return of principal at maturity, are subject to the credit of the issuer. BUyS are not individually rated, but instead rely on credit ratings of the issuer. Such ratings do not address or enhance the performance of the BUyS other than with respect to the issuer's ability to pay amounts due at maturity. Underlying BUyS may be structured to provide investors with exposure to a variety of assets or sectors. The underlying may consist of single or multiple stocks, indices or other assets. The underlying may provide exposure across varying company sizes, stock exchanges, currencies, geographic regions or industry sectors. Benefits o Buffer Level provides for limited protection at maturity o Generally shorter maturities than principal protected structures o Some structures provide for upside Out-Performance if the value of the underlying has increased, which in some instances may be subject to a return cap Tax Considerations o Generally reasonable to treat as "capital" instruments rather than debt (which would produce ordinary income and "phantom" income accruals); however, US tax consequences of an investment in BUyS are unclear Risks o Investors have credit exposure to the issuer for all amounts due on the BUyS o Investment in BUyS does not have full principal protection, so investors may lose some or substantially all of their investment o Investors in BUyS do not receive or participate in dividends or other distributions on the underlying o If the BUyS is offered with a return cap, the return to investors will be capped and they will not participate in any performance of the underlying above the cap o Returns, including any Out-Performance if applicable, are only realized at maturity o BUyS may trade at a discount and there may be little or no secondary market for the BUyS; BUyS will not be listed on any securities exchange Components BUyS provide for a one-time payment at maturity based upon three components: a Performance Component-which is the performance of the underlying; a Principal Component-which is the amount of principal returned to investors at maturity and the Buffer Level-which is a predetermined percentage amount that provides limited protection at maturity. Some BUyS also have a return cap that limits the return an investor may receive. At maturity, investors will receive the Performance Component plus the Principal Component, subject to the Buffer Level and a return cap, if applicable. 5 |

|

performance component

PERFORMANCE COMPONENT

The Performance Component tracks the performance of the underlying during the term of the BUyS. The

Performance Component is equivalent to the price return of the underlying and is determined by comparing the

value of the underlying on the determination date, typically three trading days prior to maturity of the

securities, to the value of the underlying on the date the BUyS were priced for initial sale.

If the Performance Component is equal to zero or negative-that is, if the value of the

underlying on the determination date is equal to the value of the underlying on the date

the BUyS were priced-or is negative-that is, if the value of the underlying on the

determination date is less than the value of the underlying on the date the BUyS were

priced-the Performance Component will be 0%.

6

|

| performance component If the Performance Component is positive-that is, if the value of the underlying on the determination date is greater than the value of the underlying on the date the BUyS were priced-the Performance Component will be an amount equal to the same percentage as the percentage increase in the value of the underlying. For example, if the underlying has increased by 8%, the Performance Component will be the same such percentage (i.e., 8%). Some BUyS provide for Out-Performance if the value of the underlying has increased. The participation rate for such a BUyS will be greater than 100%, for example 125%. In such a case, the Performance Component will be an amount equal to the percentage increase in the value of the underlying multiplied by the participation rate. For example, if the underlying has increased by 8% and the participation rate is 125%, the amount of the Performance Component will be 10% (i.e., 8% times the participation rate of 125% = 10%). Therefore,- the Performance Component would be 10% of the original principal amount. If the Performance Component is positive and there is a return cap-that is, if the performance of the underlying for purposes of calculating the return of the BUys is subject to a cap-the Performance Component, and the return to investors, will also have a cap. For example, if the underlying has increased by 8%, the participation rate is 125% and there is a return cap of 7.5%, the amount of the Performance Component will be 9.375% (i.e., 7.5%, the return cap because the underlying has increased by 8% which is more than the return cap, times the participation rate of 125% = 9.375%). Therefore the Performance Component would be 9.375% of the original principal amount because the return cap has created and limited the amount of the Performance Component. This is lower than the Performance Component of 10% that would have been calculated without the return cap. 7 |

| principal COMPONENT AND BUFFER LEVEL principal component and buffer level The Principal Component works in tandem with the Buffer Level and is the amount of principal that is returned at maturity. It is determined by comparing the Performance Component, which is the return of the underlying, with the Buffer Level. If the Performance Component is positive, the Principal Component will be an amount equal to 100% of the original principal amount. If the Performance Component is negative but has decreased by less than or equal to the Buffer Level, the Principal Component will still be equal to 100% of the original principal amount. For example, if the Buffer Level is 20% and the underlying has decreased by 15%, the amount of the Principal Component will be 100% of the original principal amount because the decrease is less than the Buffer Level. The Buffer Level provides limited protection against a decrease in the underlying. If the Performance Component is negative and has decreased by more than the Buffer Level, the amount of principal returned at maturity will be reduced by the same percentage reduction in the value of the underlying plus the Buffer Level-that is, the Buffer Level will offset a portion of the decrease in value of the underlying. For example, if the underlying has decreased by 30% and the Buffer Level is 20%, the amount of the Principal Component will be the original principal amount decreased by the same percentage, plus the Buffer Level. Therefore, the Principal Component would be 90% (i.e., 100% - 30% + 20%) of the original principal amount. Consequently the Buffer Level offsets a portion of the decrease of the underlying. 8 |

|

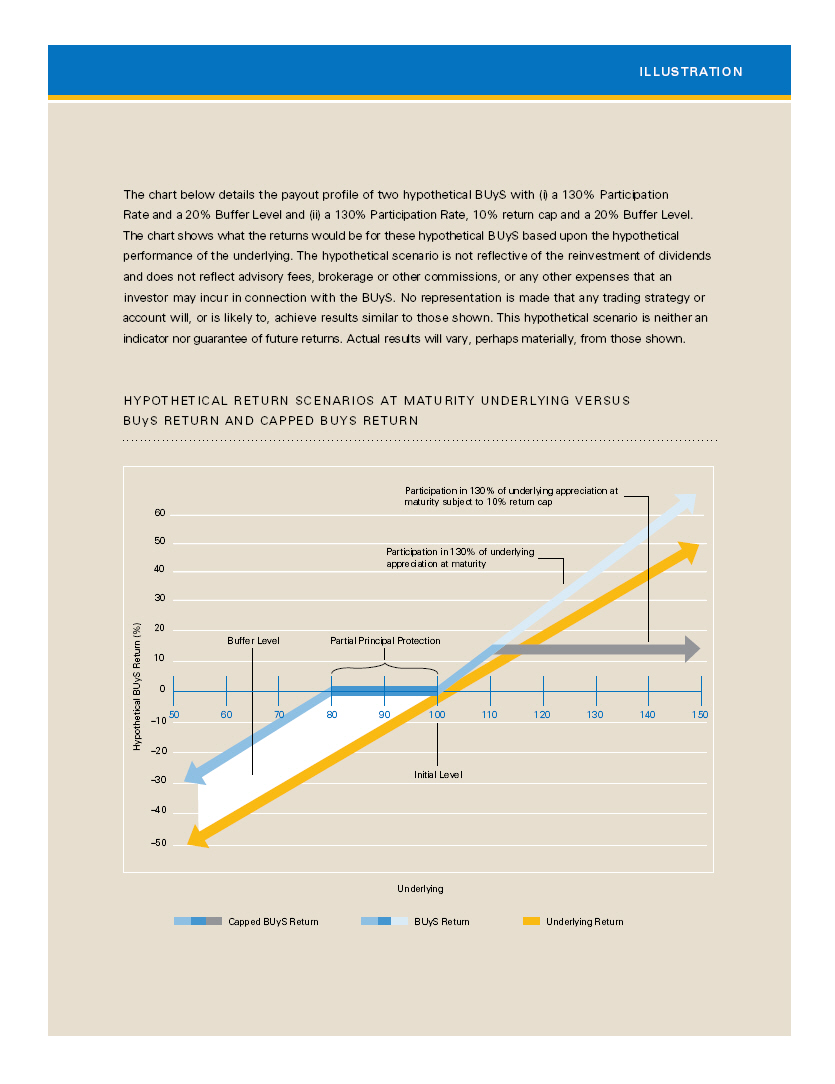

ILLUSTRATION

The chart below details the payout profile of two hypothetical BUyS with (i) a 130% Participation Rate

and a 20% Buffer Level and (ii) a 130% Participation Rate, 10% return cap and a 20% Buffer Level. The

chart shows what the returns would be for these hypothetical BUyS based upon the hypothetical performance

of the underlying. The hypothetical scenario is not reflective of the reinvestment of dividends and does

not reflect advisory fees, brokerage or other commissions, or any other expenses that an investor may

incur in connection with the BUyS. No representation is made that any trading strategy or account will,

or is likely to, achieve results similar to those shown. This hypothetical scenario is neither an

indicator nor guarantee of future returns. Actual results will vary, perhaps materially, from those shown.

HYPOTHETICAL RETURN SCENARIOS AT MATURITY UNDERLYING VERSUS BUyS RETURN AND CAPPED BUyS

RETURN

Participation in 130% of underlying

appreciation at

maturity subject to 10% return

60 cap

50

Participation in 130% of

underlying

40 appreciation at maturity

30

20 Buffer Level Partial Principal

(%) Protection

Return 10

BUyS 0

Hyp-10e(50)l 60 70 80 90 100 110 120 130 140 150

-20

-30 Initial Level

-40

-50

Underlying

Capped BUyS Return BUyS Return Underlying Return

|

|

payment at maturity

How is the Payment at Maturity Calculated on BUyS?

At maturity, holders of BUyS will receive a one time payment based upon the

price performance of the underlying. The return at maturity is equal to the

Performance Component plus the Principal Component, subject to the Buffer Level

and, in certain instances, a return cap.

o The return at maturity of an investment in BUyS is equal to the Performance

Component plus the Principal Component, subject to the Buffer Level and, in

certain instances, a return cap

o If, at maturity, the underlying has depreciated below its value on the date

the BUyS were priced, but by less than the Buffer Level, investors will

receive their original investment amount at maturity

o If, at maturity, the underlying has depreciated below its value on the date

the BUyS were priced by more than the Buffer Level, investors will

participate one-for-one in any such depreciation below the Buffer Level

o Subject to the credit of the issuer, the minimum payment at maturity on BUyS

is equal to the Buffer Level (i.e., at maturity an investor in BUyS will

receive at least the Buffer Level)

|

|

payment at maturity

Step 1

Determine the percentage price return of the underlying, which is equal to:

(Value of the underlying on the determination date - the value of the underlying on the date the securities

were priced)

.

-

.

Value of the underlying on the date the securities were priced

Step 2

Determine the Performance Component. If the percentage return of the underlying (from Step 1) is: (i) zero

or negative, the Performance Component will be 0%; or (ii) positive, the Performance Component will be the

same such percentage (from Step 1). If the BUyS provides for Out-Performance and the percentage return of

the underlying (from Step 1) is positive, the Performance Component will be equal to the percentage return

of the underlying multiplied by the participation rate. If the BUyS provides for a return cap and the

percentage return of the underlying (from Step 1) is positive, the Performance Component will be equal to

the percentage return of the underlying, subject to the return cap, multiplied by the participation rate.

Step 3

Determine the Principal Component. If the percentage return of the underlying (from Step 1) is: (i)

positive, the Principal Component will be 100%; (ii) negative, but has decreased less than or equal to the

Buffer Level, the Principal Component will be 100% or (iii) negative and has decreased by more than the

Buffer Level, the Principal Component will be 100% minus the percentage decrease in the underlying (from

Step 1) plus the Buffer Level.

Step 4

Determine the total percentage return of the BUyS, which is equal to the Performance Component plus

the Principal Component.

Step 5

Determine the total dollar payment at maturity, which is equal to the total percentage

return of the securities times the original principal amount.

(Principal Component + Performance Component) x Denomination

=

Total Dollar Payment at Maturity

|

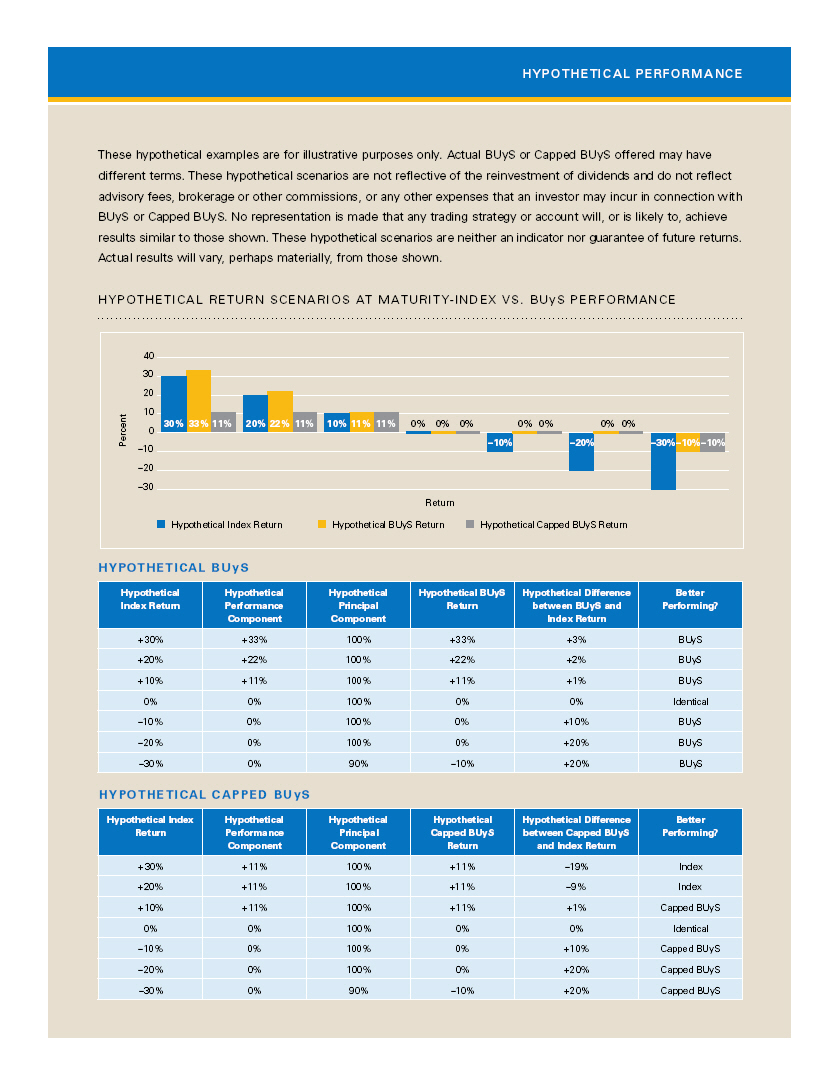

| HYPOTHETICAL PERFORMANCE HYPOTHETICAL PERFORMANCE As with any investment, BUyS should be evaluated based upon many factors including, but not limited to, the potential return of the investment as well as both the risks and benefits of any such investment. Certain benefits and risks of BUyS will result in such an investment performing better in certain markets and worse in others. In a bearish market, BUyS will generally outperform a direct investment in the underlying due to the limited protection at maturity. In a bullish market, BUyS will generally perform as well as a direct investment in the underlying. A BUyS with Out-Performance will generally outperform a direct investment in the underlying in a bullish market. A BUyS with a return cap will outperform a direct investment in the underlying in a bullish market up to the return cap. The chart and table on the following page illustrate the potential benefits and risks of (i) a hypothetical BUyS linked to an equity index with a maturity of three years, a 110% Participation Rate and a Buffer Level of 20%; and (ii) a hypothetical BUyS with a return cap (a "Capped BUyS") linked to an equity index with a maturity of three years, a 110% Participation Rate, a return cap of 10% and a Buffer Level of 20%. The chart and table compare the performance of the hypothetical BUyS and a hypothetical Capped BUyS to the performance of the underlying index over a hypothetical range of potential scenarios. 12 |

|

HYPOTHETICAL PERFORMANCE

These hypothetical examples are for illustrative purposes only. Actual BUyS or Capped BUyS offered may have

different terms. These hypothetical scenarios are not reflective of the reinvestment of dividends and do not

reflect advisory fees, brokerage or other commissions, or any other expenses that an investor may incur in

connection with BUyS or Capped BUyS. No representation is made that any trading strategy or account will, or

is likely to, achieve results similar to those shown. These hypothetical scenarios are neither an indicator

nor guarantee of future returns. Actual results will vary, perhaps materially, from those shown.

HYPOTHETICAL return SCENARIOS AT MATURITY-INDEX VS. BUyS PERFORMANCE

40

30

20

Percent 10

0 30% 33% 11% 20% 22% 11% 10% 11% 11% 0% 0% 0%-10% 0% 0%-20% 0% 0% -30% -10% -10%

-10

-20

-30

Return

Hypothetical BUyS ReturnHypothetical Capped BUyS

Hypothetical Index Return Return

Hypothetical BUyS

Hypothetical Hypothetical Hypothetical Hypothetical BUyS Hypothetical Difference Better

Index Return Performance Principal Return between BUyS and Performing?

Component Component Index Return

+30% +33% 100% +33% +3% BUyS

+20% +22% 100% +22% +2% BUyS

+10% +11% 100% +11% +1% BUyS

0% 0% 100% 0% 0% Identical

-10% 0% 100% 0% +10% BUyS

-20% 0% 100% 0% +20% BUyS

-30% 0% 90% 10% +20% BUyS

Hypothetical CAPPED BUyS

Hypothetical Index Hypothetical Hypothetical Hypothetical Hypothetical Difference Better

Return Performance Principal Capped BUyS between Capped BUyS Performing?

Component Component Return and Index Return

+30% +11% 100% +11% -19% Index

+20% +11% 100% +11% -9% Index

+10% +11% 100% +11% +1% Capped BUyS

0% 0% 100% 0% 0% Identical

-10% 0% 100% 0% +10% Capped BUyS

-20% 0% 100% 0% +20% Capped BUyS

-30% 0% 90% -10% +20% Capped BUyS

|

| one story: dws Investments DWS Investments and DEUTSCHE BANK DWS Investments is the US retail brand name of Deutsche Asset Management (DeAM)-the global asset management division of Deutsche Bank with more than $816 billion in assets under management globally (as of December 31, 2007). DWS Investments can trace its roots as a respected US asset manager back to 1919. With a strong commitment to superior performance, innovation and leadership in intellectual capital, DWS Investments offers a comprehensive and diverse family of products available through financial intermediaries, retirement plans and wrap programs. Through DWS Investments, investors can tap into DeAM's far-reaching global research organization of more than 750 investment professionals (as of December 31, 2007), who manage equity, fixed- income, balanced, cash, real estate and hedge fund investments around the world. Deutsche Bank is a leading global investment bank with a strong and profitable private clients franchise. A leader in Germany and Europe, the bank is growing in North America, Asia and key emerging markets. With $2.027 trillion in assets and 78,291 employees in 76 countries, Deutsche Bank offers innovative financial services throughout the world. The bank competes to be the leading global provider of financial solutions for demanding clients and aims to create exceptional value for its shareholders and people. The partnership between DWS Investments and Deutsche Bank's Global Markets gives financial professionals and investors access to world class asset management, structuring and risk management capabilities in a coordinated manner. 14 |

|

Dws Investments

+

Deutsche Bank

=

Innovative SimplicitySM

|

| Risk Factors Your investment in buys may result in a loss of your initial investment other than the Buffer Level BUyS do not guarantee any return of your initial investment in excess of the Buffer Level. The return on the BUyS at maturity is linked to the performance of the underlying and will depend on whether, and the extent to which, the underlying performance is positive or negative. The return on your Capped buys may be limited by a return cap-For Capped BUyS the underlying return cannot exceed the specified return cap and your payment at maturity is limited to a maximum payment created by the specified return cap, regardless of any increase in the underlying beyond the return cap. Certain built-in costs are likely to adversely affect the value of the buys prior to maturity-Certain built-in costs, such as the agent's commission and the Issuer's estimated cost of hedging, are likely to adversely affect the value of the BUyS prior to maturity. You should be willing and able to hold your BUyS to maturity. No coupon or dividend payments or voting rights- You will not receive coupon payments on the BUyS or have voting rights or rights to receive cash dividends or other distributions on the BUyS or the underlying. Lack of liquidity-There may be little or no secondary market for the BUyS. The BUyS will not be listed on any securities exchange. The issuer's research, opinions or recommendations could affect the level of the underlying or the market value of the buys-The Issuer and its affiliates and agents may publish research, express opinions or provide recommendations that are inconsistent with investing in or holding the BUyS, which could affect the level or price of the underlying or the value of the BUyS. Potential conflicts-Because the Issuer and its affiliates play a variety of roles in connection with the issuance of the BUyS, including acting as calculation agent and hedging its obligations under the BUyS, the economic interests of the calculation agent and other affiliates of the Issuer are potentially adverse to your interests as an investor in the BUyS. Many economic and market factors will affect the value of the buys-In addition to the level of the underlying on any day, the value of the BUyS will be affected by a number of complex and interrelated economic and market factors that may either offset or magnify each other. The u.s. tax consequences of an investment in the buys are unclear-Significant aspects of the U.S. federal income tax treatment of the BUyS are uncertain, and no assurance can be given that the Internal Revenue Service will accept, or a court will uphold, the tax consequences described in the pricing supplement relating to the offering of any particular BUyS. Additional Considerations-Other risks may apply to a particular BUyS. You should read the risk factors in the offering document for a particular BUyS prior to making any investment. 16 |

| [GRAPHIC OMITTED] |

| Before purchasing a structured product, investors should carefully consider the risks associated with an investment in the structured product and whether the structured product is a suitable investment for them. Before investing, prospective investors should read the prospectus relating to the particular structured product. In addition, investors are encouraged to consult with their investment, legal, accounting, tax and other advisers in connection with any investment in a structured product. The issuer has filed a registration statement (including a prospectus) with the SEC for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents the issuer has filed with the SEC for more complete information about the issuer and this offering. You may get these documents for free by visiting EDGAR on the SEC web site at www.sec.gov. Alternatively, the issuer, any underwriter or any dealer participating in the offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-311-4409. X-markets is the Deutsche Bank worldwide platform for structured notes. DWS Investments is the US retail brand name of Deutsche Asset Management (DeAM), the global asset management division of Deutsche Bank AG. issuer free writing prospectus File Pursuant to Rule 433 Registration Statement No. 333-162195 Dated: September 29, 2009 NOT FDIC/NCUA INSURED OR GUARANTEED M A Y L O S E V A L U E N O B A N K G U A R A N T E E NOT A DEPOSIT NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY DWS Investments is part of Deutsche Bank's Asset Management division and, within the US, represents the retail asset management activities of Deutsche Bank AG, Deutsche Bank Trust Company Americas, Deutsche Investment Management Americas Inc. and DWS Trust Company. DWS Investments Distributors, Inc. 222 South Riverside Plaza, Chicago, IL 60606-5808 rep@dws.com Tel (800) 621-1148 DWS Structured Products dws-sp@db.com Tel (866) 637-9185 www.dws-sp.com @ 2009 DWS Investments Distributors, Inc. All rights reserved. R-7605-1 (01/09) BUyS-601 |