| Understanding Structured Notes & CDs DWS Structured Products Americas Understanding Structured Notes & CDs Presentation v 1.0 |

|

What we will cover

* About Deutsche Bank

* Bermuda Triangle of Diminished Expectations

* Structural Diversification(SM)

* Evolution of Investing

* Structured Notes Marketplace

* What is a Structured Note or CD?

* Features & Types of Structured Notes and CDs

* Risk versus Return

* Shaped Returns

* ReCap

Understanding Structured Notes & CDs Presentation v 1.0

2

|

|

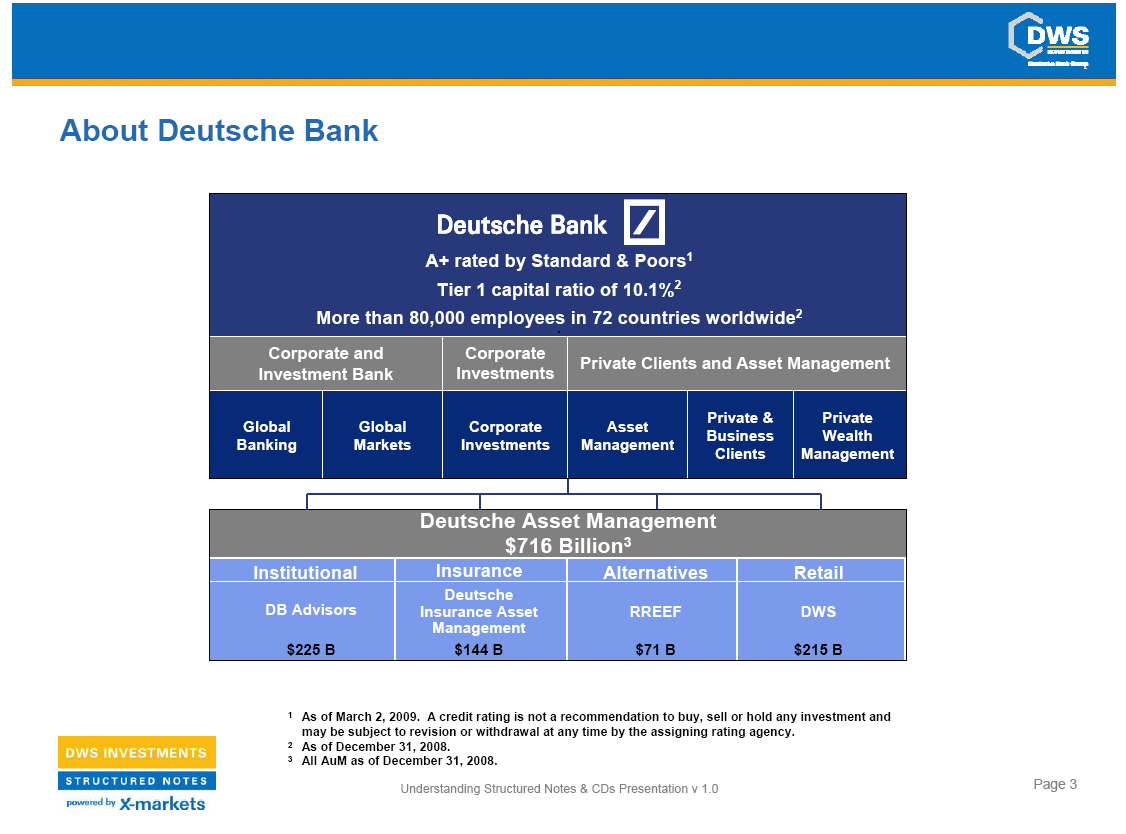

About Deutsche Bank

A+ rated by Standard & Poors(1) Tier 1 capital ratio of 10.1% 2

More than 80,000 employees in 72 countries worldwide 2

(1) As of March 2, 2009. A credit rating is not a recommendation to buy, sell

or hold any investment and may be subject to revision or withdrawal at any time

by the assigning rating agency.

(2) As of December 31, 2008.

(3) All AuM as of December 31, 2008.

Understanding Structured Notes & CDs Presentation v 1.0

3

|

|

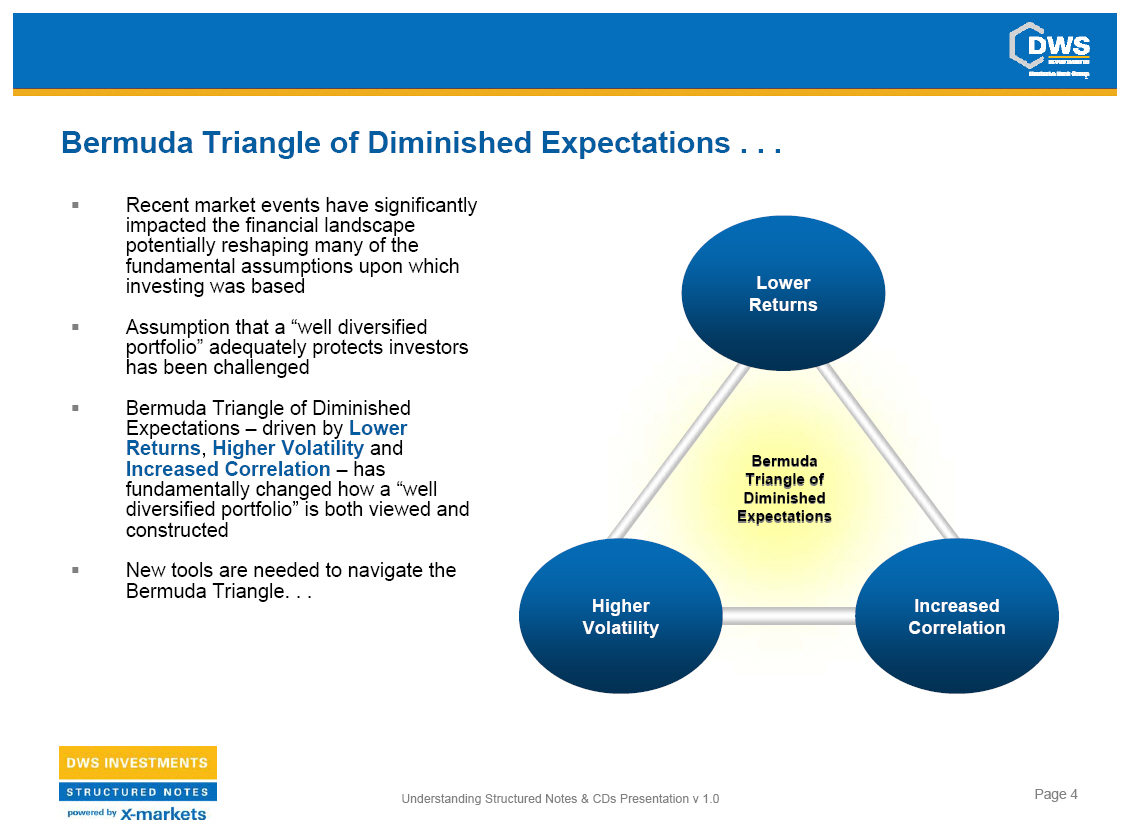

Bermuda Triangle of Diminished Expectations . . .

* Recent market events have significantly impacted the financial landscape

potentially reshaping many of the fundamental assumptions upon which investing

was based

* Assumption that a "well diversified portfolio" adequately protects investors

has been challenged

* Bermuda Triangle of Diminished Expectations -- driven by Lower Returns,

Higher Volatility and Increased Correlation -- has fundamentally changed how a

"well diversified portfolio" is both viewed and constructed

* New tools are needed to navigate the Bermuda Triangle. . .

Understanding Structured Notes & CDs Presentation v 1.0

4

|

|

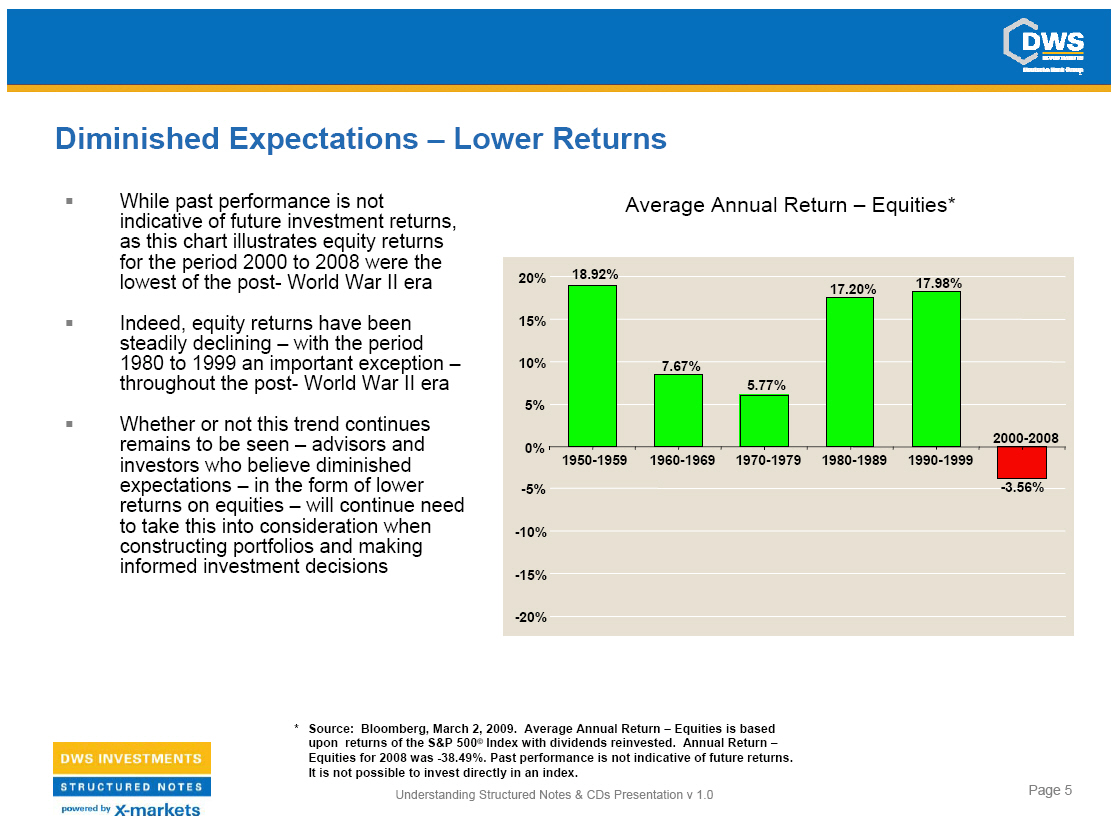

Diminished Expectations -- Lower Returns

* While past performance is not indicative of future investment returns, as

this chart illustrates equity returns for the period 2000 to 2008 were the

lowest of the post- World War II era

* Indeed, equity returns have been steadily declining -- with the period 1980

to 1999 an important exception -- throughout the post- World War II era

* Whether or not this trend continues remains to be seen -- advisors and

investors who believe diminished expectations -- in the form of lower returns

on equities -- will continue need to take this into consideration when

constructing portfolios and making informed investment decisions

Average Annual Return -- Equities*

* Source: Bloomberg, March 2, 2009. Average Annual Return -- Equities is based

upon returns of the S&P 500([C]) Index with dividends reinvested. Annual Return

- --Equities for 2008 was -38.49% . Past performance is not indicative of future

returns. It is not possible to invest directly in an index.

Understanding Structured Notes & CDs Presentation v 1.0

5

|

|

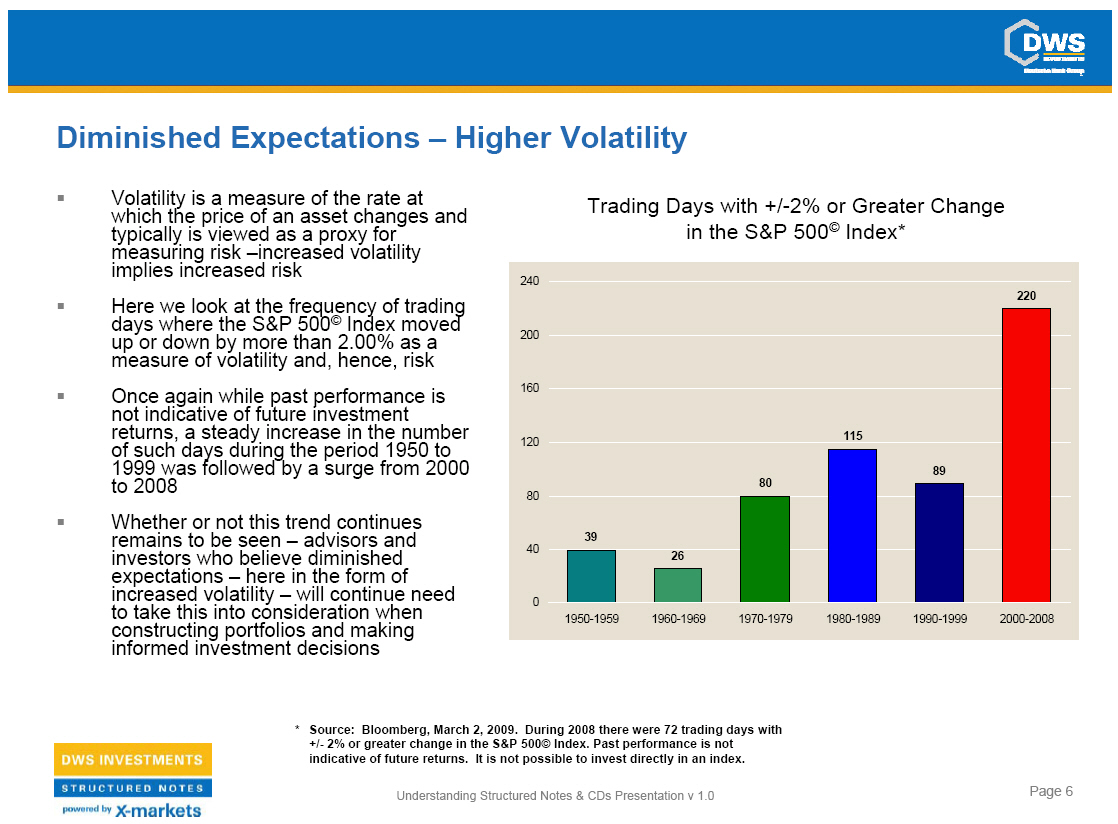

Diminished Expectations -- Higher Volatility

* Volatility is a measure of the rate at which the price of an asset changes

and typically is viewed as a proxy for measuring risk --increased volatility

implies increased risk

* Here we look at the frequency of trading days where the S&P 500([C]) Index

moved up or down by more than 2.00% as a measure of volatility and, hence,

risk

* Once again while past performance is not indicative of future investment

returns, a steady increase in the number of such days during the period 1950 to

1999 was followed by a surge from 2000 to 2008

* Whether or not this trend continues remains to be seen -- advisors and

investors who believe diminished expectations -- here in the form of increased

volatility -- will continue need to take this into consideration when

constructing portfolios and making informed investment decisions

Trading Days with +/-2% or Greater Change in the S&P 500([C]) Index*

* Source: Bloomberg, March 2, 2009. During 2008 there were 72 trading days with

+/- 2% or greater change in the S&P 500[C] Index. Past performance is not

indicative of future returns. It is not possible to invest directly in an

index.

Understanding Structured Notes & CDs Presentation v 1.0

6

|

|

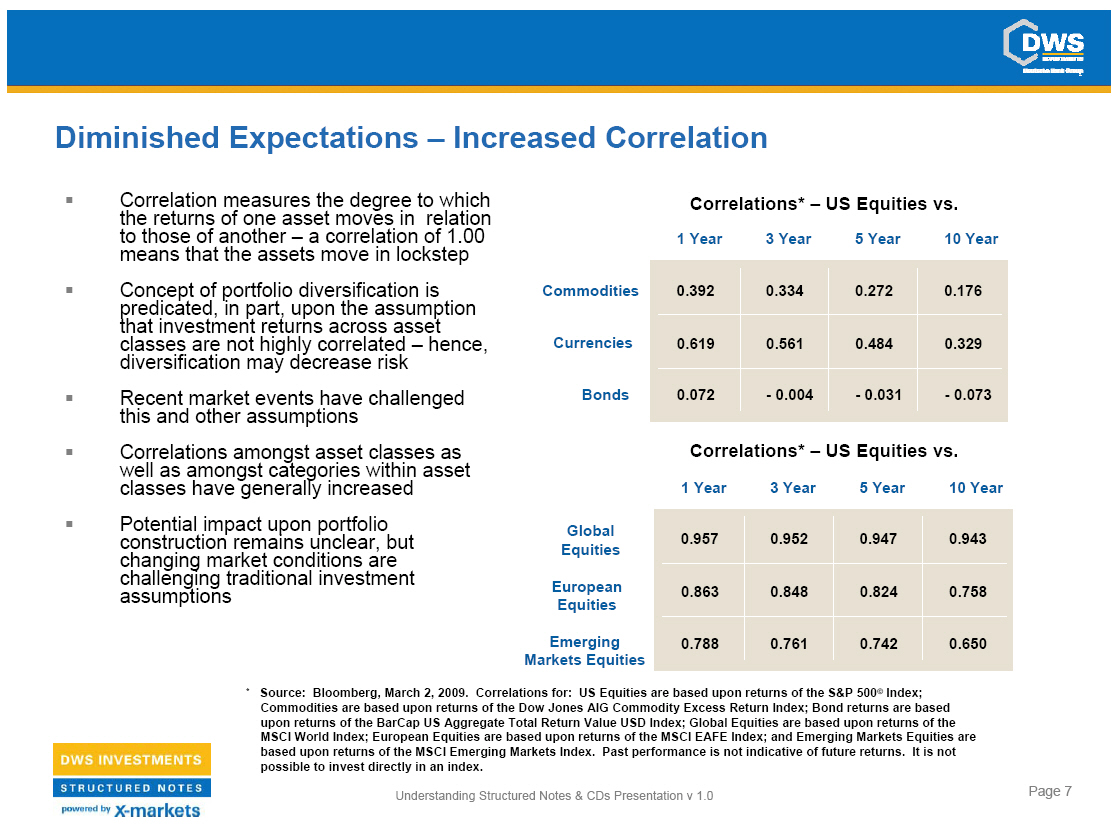

Diminished Expectations -- Increased Correlation

* Correlation measures the degree to which the returns of one asset moves in

relation to those of another -- a correlation of 1.00 means that the assets

move in lockstep

* Concept of portfolio diversification is predicated, in part, upon the

assumption that investment returns across asset classes are not highly

correlated -- hence, diversification may decrease risk

* Recent market events have challenged this and other assumptions

* Correlations amongst asset classes as well as amongst categories within asset

classes have generally increased

* Potential impact upon portfolio construction remains unclear, but changing

market conditions are challenging traditional investment assumptions

Correlations* -- US Equities vs.

Correlations* -- US Equities vs.

(*) Source: Bloomberg, March 2, 2009. Correlations for: US Equities are based

upon returns of the S&P 500([C]) Index; Commodities are based upon returns of

the Dow Jones AIG Commodity Excess Return Index; Bond returns are based upon

returns of the BarCap US Aggregate Total Return Value USD Index; Global

Equities are based upon returns of the MSCI World Index; European Equities are

based upon returns of the MSCI EAFE Index; and Emerging Markets Equities are

based upon returns of the MSCI Emerging Markets Index. Past performance is not

indicative of future returns. It is not possible to invest directly in an

index.

Understanding Structured Notes & CDs Presentation v 1.0

7

|

|

Structural Diversification SM

* For advisors and investors who believe that Diminished Expectations will

continue new tools are needed to navigate the Bermuda Triangle of Lower

Returns, Higher Volatility and Increased Correlation -- one such new tool is

Structural Diversification

* Structural Diversification is best viewed as a complement to traditional

asset allocation investing -- i.e., diversifying a portfolio across asset

classes or amongst categories within asset classes

* It involves integrating outcome oriented investment products -- such as

structured notes and CDs -- into an investment portfolio to provide Structural

Diversification

* Goal of Structural Diversification is to address the Bermuda Triangle of

Lower Returns, Higher Volatility and Increased Correlation with new investment

options such as structured notes & CDs

Understanding Structured Notes & CDs Presentation v 1.0

8

|

|

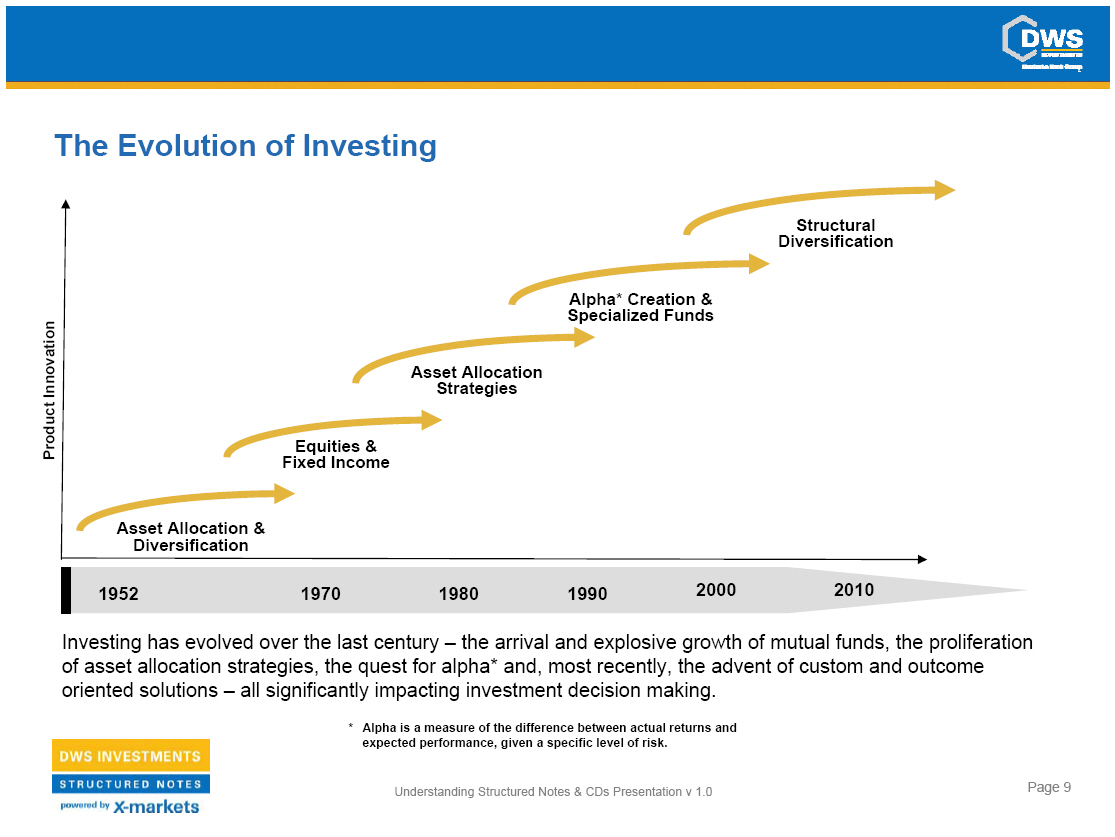

The Evolution of Investing

Investing has evolved over the last century -- the arrival and explosive growth

of mutual funds, the proliferation of asset allocation strategies, the quest

for alpha* and, most recently, the advent of custom and outcome oriented

solutions -- all significantly impacting investment decision making.

* Alpha is a measure of the difference between actual returns and expected

performance, given a specific level of risk.

Understanding Structured Notes & CDs Presentation v 1.0

9

|

|

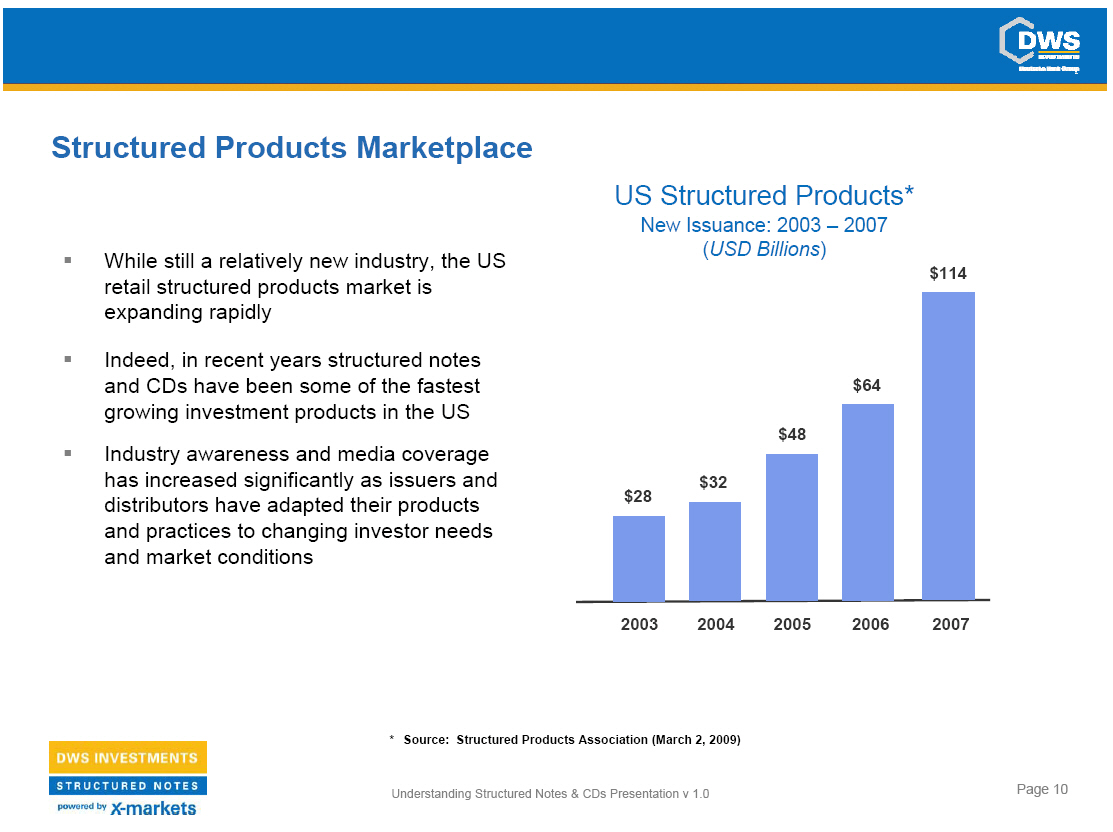

Structured Products Marketplace

* While still a relatively new industry, the US retail structured products

market is expanding rapidly

* Indeed, in recent years structured notes and CDs have been some of the

fastest growing investment products in the US

* Industry awareness and media coverage has increased significantly as issuers

and distributors have adapted their products and practices to changing investor

needs and market conditions

US Structured Products*

New Issuance: 2003 -- 2007 (USD Billions)

* Source: Structured Products Association (March 2, 2009)

Understanding Structured Notes & CDs Presentation v 1.0

10

|

|

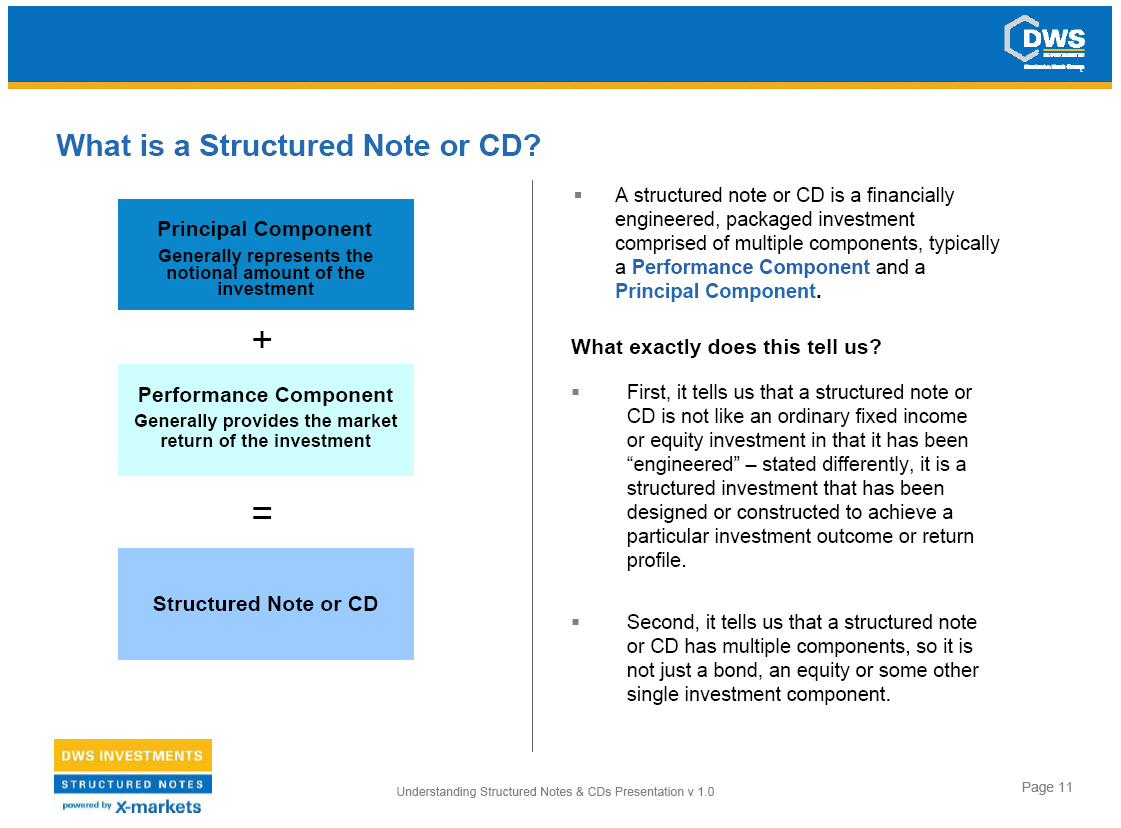

What is a Structured Note or CD?

Principal Component Generally represents the notional amount of the investment

+

Performance Component Generally provides the market return of the investment

Structured Note or CD

* A structured note or CD is a financially engineered, packaged investment

comprised of multiple components, typically

a Performance Component and a

Principal Component.

What exactly does this tell us?

* First, it tells us that a structured note or CD is not like an ordinary fixed

income or equity investment in that it has been "engineered" -- stated

differently, it is a structured investment that has been designed or

constructed to achieve a particular investment outcome or return profile.

* Second, it tells us that a structured note or CD has multiple components, so

it is not just a bond, an equity or some other single investment component.

Understanding Structured Notes & CDs Presentation v 1.0

11

|

|

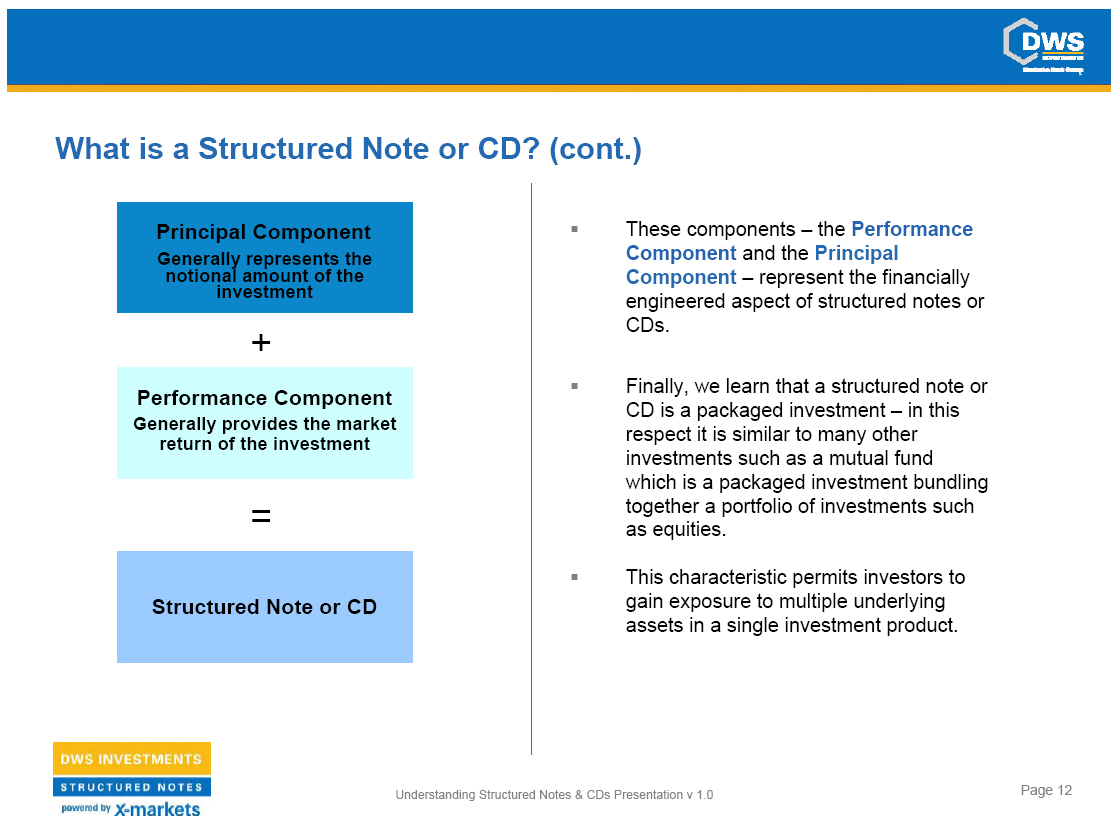

What is a Structured Note or CD? (cont.)

Principal Component Generally represents the notional amount of the investment

+

Performance Component Generally provides the market return of the investment

=

Structured Note or C

* These components -- the Performance Component and the Principal Component --

represent the financially engineered aspect of structured notes or CDs.

* Finally, we learn that a structured note or CD is a packaged investment -- in

this respect it is similar to many other investments such as a mutual fund

which is a packaged investment bundling together a portfolio of investments

such as equities.

* This characteristic permits investors to gain exposure to multiple underlying

assets in a single investment product.

Understanding Structured Notes & CDs Presentation v 1.0

12

|

|

What is a Structured Note or CD? (cont.)

* The return of structured notes and CDs is typically paid at maturity although

some products may feature periodic coupons or be callable by the issuer prior

to maturity.

* May be packaged as registered medium term notes or as FDIC insured

certificates of deposit (subject to applicable FDIC insurance limits)

* The performance of structured notes and CDs prior to maturity is subject to

market conditions and they may trade at a discount in the secondary market, if

any.

Consequently they should be viewed as buy and hold type investments.

* Investors in structured notes and CDs have credit exposure to the issuer for

all amounts due on the notes and CDs including the return of principal at

maturity, if applicable. CDs also have the feature of FDIC insurance up to

applicable limits.

Understanding Structured Notes & CDs Presentation v 1.0

13

|

|

Features of Structured Notes and CDs

Structured Notes and CDs have features often unavailable with traditional

investments such as:

* Enhanced Returns -- Potential to enhance returns across asset classes though

the use of leverage or limited principal protection*.

* Access -- Ability to access asset classes that may be difficult or uneconomic

to invest in directly such as commodities or currencies.

* Shaped Returns -- Investment returns or profiles -- such as full or limited

principal protection*

-- not typically accessible through traditional investment products such as

mutual funds or

ETFs.

* Outcome Oriented -- Investment returns at maturity on most structured notes

and CDs are specified by predetermined rules that are known on trade date --

therefore the range of potential investment outcomes generally is known in

advance.

* Principal protected if held to maturity, subject to the credit of the

issuer.

Understanding Structured Notes & CDs Presentation v 1.0

14

|

|

Types of Structured Notes and CDs

Principal Protected*

Yield Enhancement

Out-Performance

Structured notes and CDs may be classified into three broad categories:

Principal Protected* , Yield Enhancement and Out-Performance.

Financial advisors may select structured notes and CDs that fit a specific

investor's individual risk/return profile, create an Outcome Oriented

portfolio, provide Access to specific asset or asset classes and/or that

provide

Enhanced Returns.

* Principal protected if held to maturity, subject to the credit of the

issuer.

Understanding Structured Notes & CDs Presentation v 1.0

15

|

|

Types of Structured Notes and CDs

Principal Protected*

* Full or substantially full principal protection at maturity, subject to the

credit of the issuer

* May be issued as either a structured note or CD

* Subject to applicable FDIC insurance limits if issued as a CD

* Typically have longer maturities due to the principal protection feature

* Credit exposure to the issuer for all amounts due including the return of

principal at maturity

* Principal protected if held to maturity, subject to the credit of the

issuer.

Understanding Structured Notes & CDs Presentation v 1.0

16

|

|

Types of Structured Notes and CDs

Yield Enhancement

* Typically provide an opportunity to earn enhanced periodic, contingent coupon

payments

* Issued as either a structured note or CD

* If issued as a CD, subject to applicable FDIC insurance limits

* Typically have longer maturities due to the principal protection* as well as

other features

* Principal protected if held to maturity, subject to the credit of the

issuer.

Understanding Structured Notes & CDs Presentation v 1.0

17

|

|

Types of Structured Notes and CDs

Out-Performance

* Generally have limited or no principal protection*

* Typically provide for the potential to participate in

Enhanced Returns

* Issued as a structured note (structured CDs generally provide for full

principal protection*)

* Maturities are generally shorter

* Principal protected if held to maturity, subject to the credit of the

issuer.

Understanding Structured Notes & CDs Presentation v 1.0

18

|

|

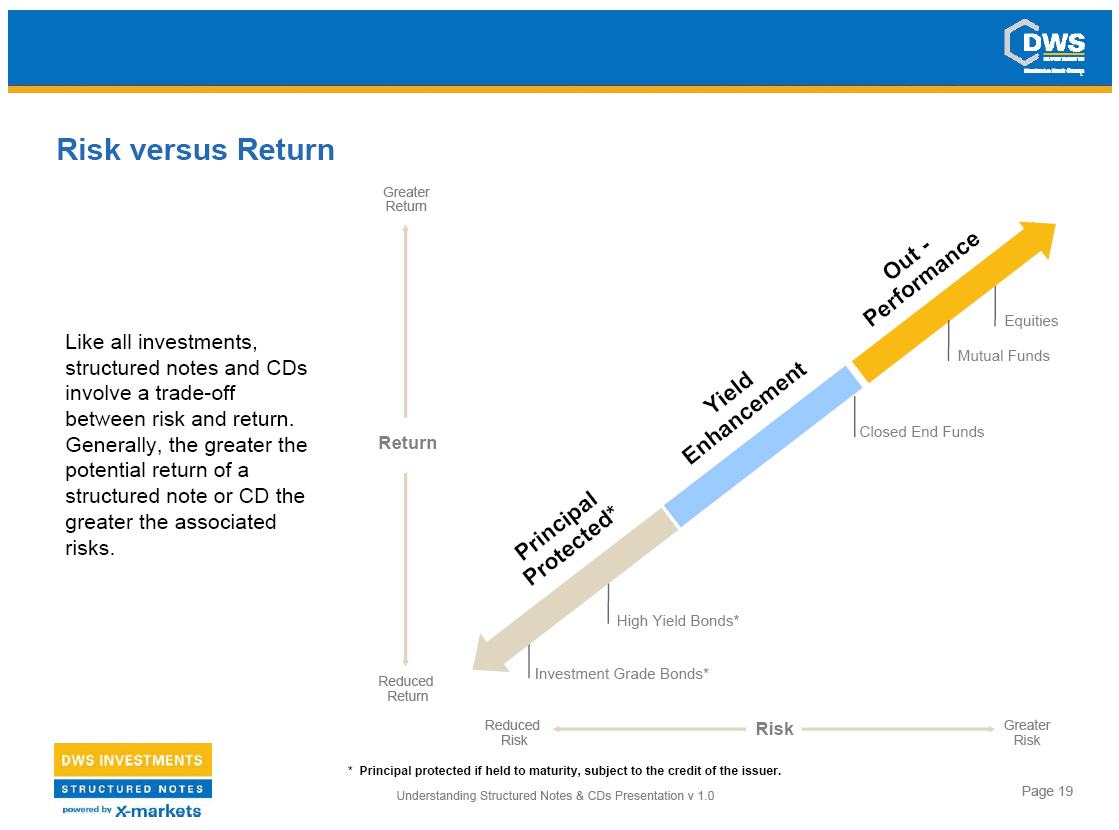

Risk versus Return

Like all investments, structured notes and CDs involve a trade-off between risk

and return. Generally, the greater the potential return of a structured note or

CD the greater the associated risks.

* Principal protected if held to maturity, subject to the credit of the

issuer.

Understanding Structured Notes & CDs Presentation v 1.0

19

|

|

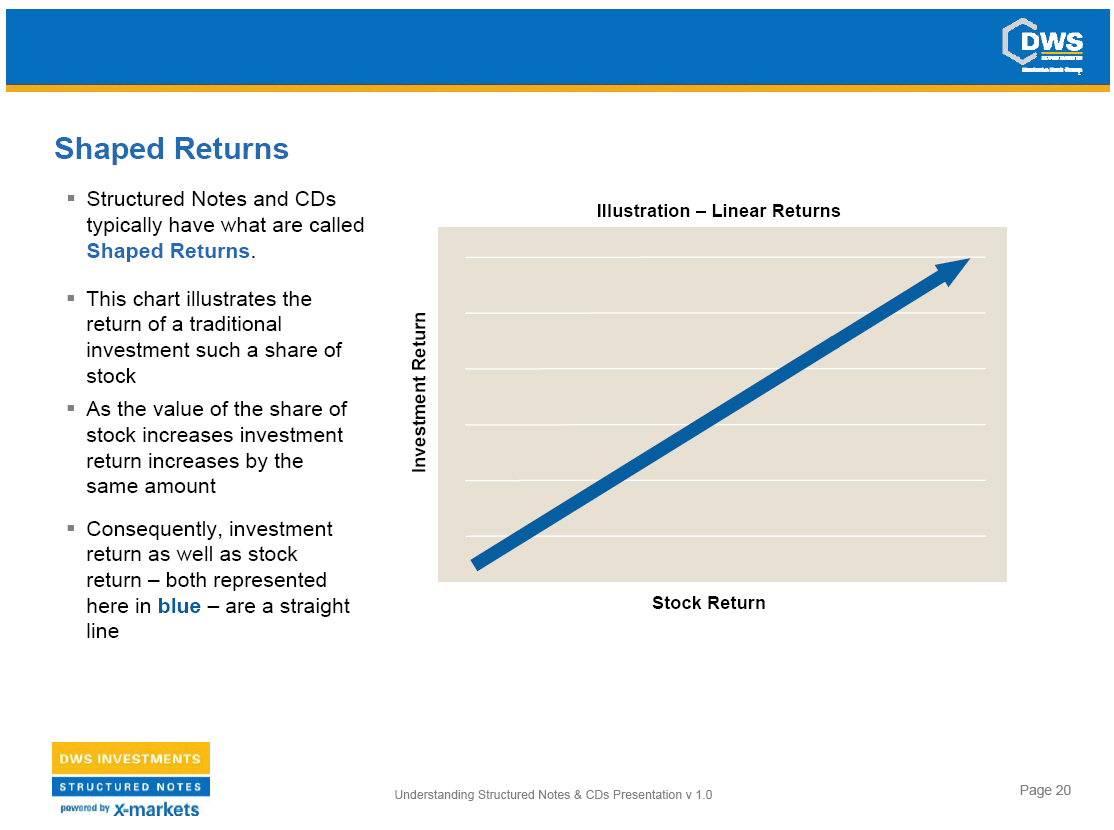

Shaped Returns

* Structured Notes and CDs typically have what are called

Shaped Returns.

* This chart illustrates the return of a traditional investment such a share of

stock

* As the value of the share of stock increases investment return increases by

the same amount

* Consequently, investment return as well as stock return -- both represented

here in blue -- are a straight line

Illustration -- Linear Returns

Understanding Structured Notes & CDs Presentation v 1.0

20

|

|

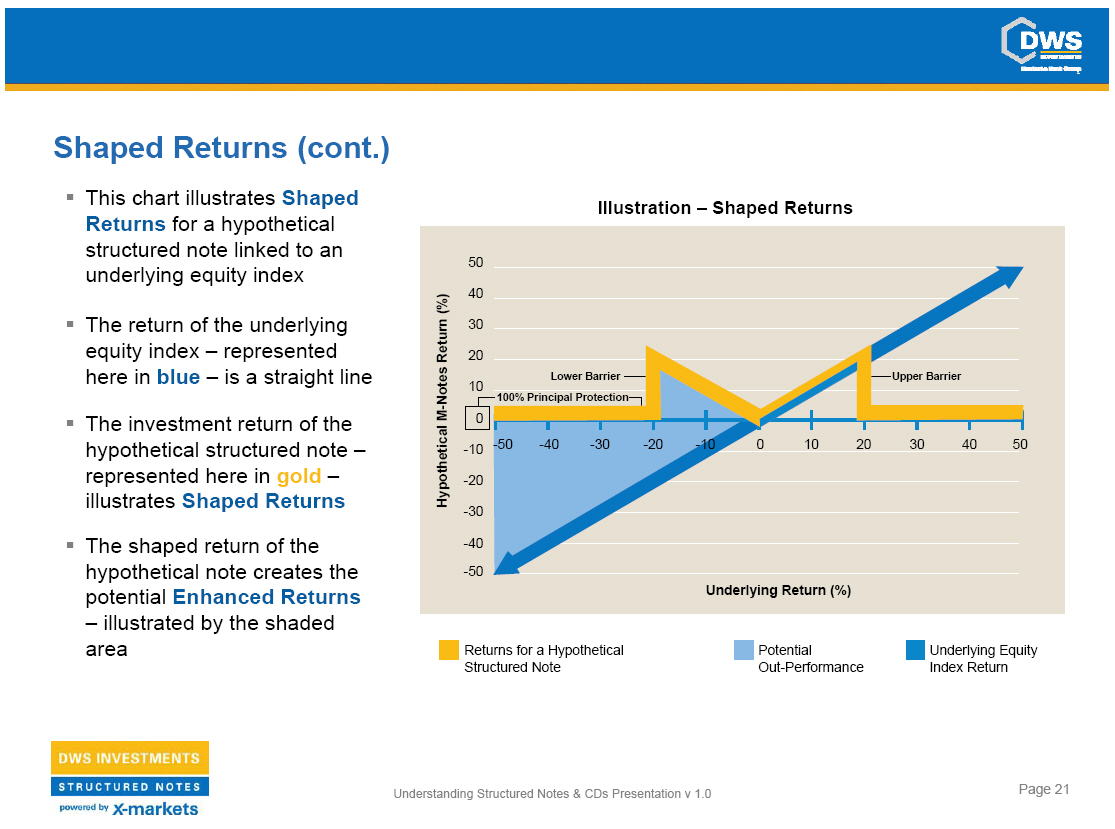

Shaped Returns (cont.)

* This chart illustrates Shaped Returns for a hypothetical structured note

linked to an underlying equity index

* The return of the underlying equity index -- represented here in blue -- is a

straight line

* The investment return of the hypothetical structured note -- represented here

in gold -- illustrates Shaped Returns

* The shaped return of the hypothetical note creates the potential Enhanced

Returns

-- illustrated by the shaded

area

Illustration -- Shaped Returns

Understanding Structured Notes & CDs Presentation v 1.0

21

|

|

ReCap

* Bermuda Triangle of Diminished Expectations -- driven by Lower Returns,

Higher Volatility and Increased Correlation -- has fundamentally changed how a

"well diversified portfolio" is both viewed and constructed

* A structured note or CD is a financially engineered, packaged investment

comprised of multiple components, typically a Performance Component and a

Principal Component.

* Investors in structured notes and CDs have credit exposure to the issuer for

all amounts due on the notes and CDs including the return of principal at

maturity, if applicable.

* Structured notes and CDs may be classified into three broad categories:

Principal Protected*, Yield Enhancement and Out-Performance.

* Structured notes and CDs may be selected to fit a specific investor's

individual risk/return profile, create an Outcome Oriented portfolio, provide

Access to specific asset or asset classes and/or provide Enhanced Returns.

* Like all investments, structured notes and CDs involve a trade-off between

risk and return. Generally, the greater the potential return of a structured

note or CD the greater the associated risks.

* Structured Notes and CDs typically have what are called Shaped Returns and

potentially help provide Structural Diversification.

* Principal protected if held to maturity, subject to the credit of the

issuer.

Understanding Structured Notes & CDs Presentation v 1.0

22

|

|

Important Information

Before purchasing a structured note or CD, investors should carefully consider

the risks associated with an investment in the structured note or CD and

whether the structured note or CD is a suitable investment for them. Before

investing, prospective investors should read the prospectus or disclosure

statement, as applicable, relating to the particular structured note or CD. In

addition, investors are encouraged to consult with their investment, legal,

accounting, tax and other advisers in connection with any investment in a

structured note or CD.

The content of this DWS Investments presentation is intended for informational

and educational purposes only. Before committing to any investment, investors

should seek the advice of an independent financial advisor.

Understanding Structured Notes & CDs Presentation v 1.0

23

|

|

DWS Structured Products Americas Contacts

Christopher Warren

Managing Director - Head of Structured Products Americas

DWS Investments

Distributors, Inc.

345 Park Avenue, 27th Floor

Office 212 454 2123

Fax 212 454 7171

Email chris.warren@db. com

Jason Hubschman

Director - Head of Structuring & Product Development

DWS Investments

Distributors, Inc.

345 Park Avenue, 25th Floor

Office 212 454 7194

Fax 212 454 7171

Email jason.hubschman@db. com

Matt Streeter

Assistant Vice President, Structuring & Product Development

DWS Investments

Distributors, Inc.

345 Park Avenue, 25th Floor

Office 212 454 2774

Fax 212 454 7171 Email

matt.streeter@db. com

Jeff Goldstein

Vice President, Structured Products Marketing

DWS Investments Distributors,

Inc. 345 Park Avenue, 25th Floor

Office 212 454 4372

Fax 212 454 7171

Email jeffrey.goldstein@db. com

Christopher Ferreira

Assistant Vice President, Structured Products Marketing

DWS Investments

Distributors, Inc.

345 Park Avenue, 25th Floor

Office 212 454 2207 Fax 212 454 7171

Email christopher. ferreira@db. com

Rupert Watts

Associate, Structured Products Marketing DWS Investments Distributors, Inc. 345

Park Avenue, 25th Floor

Office 212 454 1553

Fax 212 454 7171

Email rupert.watts@db. com

Emily Agress

Associate, Structured Products Marketing

DWS Investments Distributors, Inc.

345 Park Avenue, 25th Floor

Office 212 454 3977

Fax 212 454 7171

Email emily.agress@db. com

Understanding Structured Notes & CDs Presentation v 1.0

24

|

|

Important Information

Before purchasing a structured product, investors should carefully consider the

risks associated with an investment in the structured product and whether the

structured product is suitable for them. Before investing, prospective

investors should read the prospectus relating to the particular structured

product. In addition, investors are encouraged to consult with their

investment, legal, accounting, tax and other advisors in connection with any

investment in a structured product.

The issuer has filed a registration statement (including a prospectus) with the

SEC for the offering to which this communication relates. Before you invest,

you should read the prospectus in that registration statement and other

documents the issuer has filed with the SEC for more complete information about

the issuer and this offering. You may get these documents for free by visiting

EDGAR on the SEC web site at www.sec.gov. Alternatively, the issuer, any

underwriter or any dealer participating in the offering will arrange to send

you the prospectus if you request it by calling 1-800-311-4409.

DWS Investments is the US retail brand name of Deutsche Asset Management

(DeAM), the global asset management division of Deutsche Bank AG. X-markets is

the Deutsche Bank worldwide platform for structured notes.

ISSUER FREE WRITING PROSPECTUS File Pursuant to Rule 433 Registration Statement

No. 333-162195 Dated: October 9, 2009

NOT FDIC/NCUA INSURED OR GUARANTEED MAY LOSE VALUE / NO BANK GUARANTEE

NOT A DEPOSIT

NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY

DWS Investments is part of Deutsche Asset Management, which is the marketing

name in the US for the asset management activities of Deutsche Bank AG,

Deutsche Bank Trust Company Americas, Deutsche Investment Management Americas

Inc. and DWS Trust Company.

DWS Investments Distributors, Inc.

222 South Riverside Plaza Chicago, IL 60606-5808 rep@dws. com Tel (800)

621-1148

DWS Structured Products dws-sp@db. com Tel (866) 637-9185 www.dws-sp.com

(03/09) R-10297-2

Understanding Structured Notes & CDs Presentation v 1.0

25

|

|

Frequently Asked Questions

Understanding Structured Notes & CDs Presentation v 1.0

26

|