DWS INVESTMENTS

STRUCTURED NOTES

POWERED BY X-MARKETS

RESHAPING INVESTING.

DEUTSCHE BANK GROUP

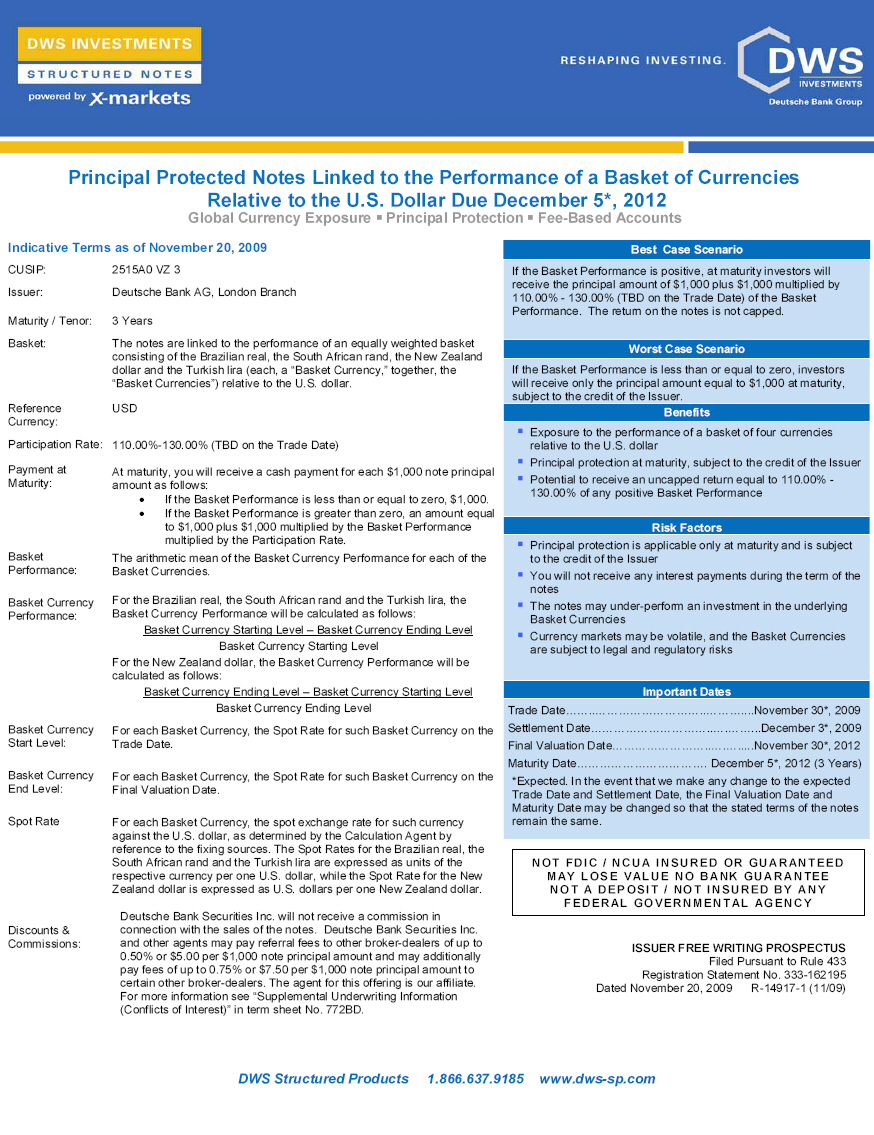

Principal Protected Notes Linked to the Performance of a Basket of Currencies

Relative to the U.S. Dollar Due December 5*, 2012

Global Currency Exposure |X| Principal Protection |X| Fee-Based Accounts

Indicative Terms as of November 20, 2009

CUSIP: 2515A0 VZ 3

Issuer: Deutsche Bank AG, London Branch

Maturity / Tenor: 3 Years

Basket: The notes are linked to the performance of an

equally weighted basket consisting of the

Brazilian real, the South African rand, the New

Zealand dollar and the Turkish lira (each, a

"Basket Currency," together, the "Basket

Currencies") relative to the U.S. dollar.

Reference Currency: USD

Participation Rate: 110.00%-130.00% (TBD on the Trade Date)

Payment at

Maturity: At maturity, you will receive a cash payment for

each $1,000 note principal amount as follows:

o If the Basket Performance is less than or

equal to zero, $1,000.

o If the Basket Performance is greater than

zero, an amount equal to $1,000 plus $1,000

multiplied by the Basket Performance

multiplied by the Participation Rate.

Basket Performance: The arithmetic mean of the Basket Currency

Performance for each of the Basket Currencies.

Basket Currency

Performance: For the Brazilian real, the South African rand and

the Turkish lira, the Basket Currency Performance

will be calculated as follows:

Basket Currency Starting Level - Basket Currency Ending Level

-------------------------------------------------------------

Basket Currency Starting Level

For the New Zealand dollar, the Basket Currency

Performance will be calculated as follows:

Basket Currency Ending Level - Basket Currency Starting Level

-------------------------------------------------------------

Basket Currency Ending Level

Basket Currency

Start Level: For each Basket Currency, the Spot Rate for such

Basket Currency on the Trade Date.

Basket Currency For each Basket Currency, the Spot Rate for such

End Level: Basket Currency on the Final Valuation Date.

Spot Rate For each Basket Currency, the spot exchange rate

for such currency against the U.S. dollar, as

determined by the Calculation Agent by reference

to the fixing sources. The Spot Rates for the

Brazilian real, the South African rand and the

Turkish lira are expressed as units of the

respective currency per one U.S. dollar, while the

Spot Rate for the New Zealand dollar is expressed

as U.S. dollars per one New Zealand dollar.

Discounts &

Commissions: Deutsche Bank Securities Inc. will not receive a

commission in connection with the sales of the

notes. Deutsche Bank Securities Inc. and other

agents may pay referral fees to other

broker-dealers of up to 0.50% or $5.00 per $1,000

note principal amount and may additionally pay

fees of up to 0.75% or $7.50 per $1,000 note

principal amount to certain other broker-dealers.

The agent for this offering is our affiliate. For

more information see "Supplemental Underwriting

Information (Conflicts of Interest)" in term sheet

No. 772BD.

- --------------------------------------------------------------------------------

Best Case Scenario

- --------------------------------------------------------------------------------

If the Basket Performance is positive, at maturity investors will receive the

principal amount of $1,000 plus $1,000 multiplied by 110.00% - 130.00% (TBD on

the Trade Date) of the Basket Performance. The return on the notes is not

capped.

- --------------------------------------------------------------------------------

Worst Case Scenario

- --------------------------------------------------------------------------------

If the Basket Performance is less than or equal to zero, investors will receive

only the principal amount equal to $1,000 at maturity, subject to the credit of

the Issuer.

- --------------------------------------------------------------------------------

Benefits

- --------------------------------------------------------------------------------

|X| Exposure to the performance of a basket of four currencies relative to the

U.S. dollar.

|X| Principal protection at maturity, subject to the credit of the Issuer.

|X| Potential to receive an uncapped return equal to 110.00% -130.00% of any

positive Basket Performance.

- --------------------------------------------------------------------------------

Risk Factors

- --------------------------------------------------------------------------------

|X| Principal protection is applicable only at maturity and is subject to the

credit of the Issuer.

|X| You will not receive any interest payments during the term of the notes.

|X| The notes may under-perform an investment in the underlying Basket

Currencies.

|X| Currency markets may be volatile, and the Basket Currencies are subject to

legal and regulatory risks.

- --------------------------------------------------------------------------------

Important Dates

- --------------------------------------------------------------------------------

Trade Date..................................................November 30*, 2009

Settlement Date..............................................December 3*, 2009

Final Valuation Date........................................November 30*, 2012

Maturity Date..................................... December 5*, 2012 (3 Years)

*Expected. In the event that we make any change to the expected Trade Date and

Settlement Date, the Final Valuation Date and Maturity Date may be changed so

that the stated terms of the notes remain the same.

- --------------------------------------------------------------------------------

NOT FDIC / NCUA INSURED OR GUARANTEED

MAY LOSE VALUE / NO BANK GUARANTEE

NOT A DEPOSIT /NOT INSURED BY ANY

FEDERAL GOVERNMENTAL AGENCY

- --------------------------------------------------------------------------------

ISSUER FREE WRITING PROSPECTUS

Filed Pursuant to Rule 433

Registration Statement No. 333-162195

Dated November 20, 2009 [R-147917-1 (11/09)]

- --------------------------------------------------------------------------------

|  |

Principal Protected Notes Fact Sheet

DWS Structured Products

| Basket Currency | Fixing Source | Fixing Time | Basket Weighting |

Brazilian real (“BRL”) | BRL PTAX at Reuters Page BRFR | 6:00 p.m. Sao Paulo | 1/4 |

South African rand (“ZAR”) | Reuters Page: WMRSPOT15 | 4:00 p.m. London | 1/4 |

New Zealand dollar (“NZD”) | Reuters Page: WMRSPOT12 | 4:00 p.m. London | 1/4 |

Turkish lira (“TRY”) | Reuters Page: WMRSPOT05 | 4:00 p.m. London | 1/4 |

Return Scenarios at Maturity Hypothetical Examples (Assumes a Participation Rate of 120%) | ||

| Change in Basket Level (%) | Payment at Maturity (per $1,000 invested) | Note Return (%) |

| 100.00% | $2,200.00 | 120.00% |

| 80.00% | $1,840.00 | 84.00% |

| 60.00% | $1,720.00 | 72.00% |

| 40.00% | $1,480.00 | 48.00% |

| 20.00% | $1,240.00 | 24.00% |

| 0.00% | $1,000.00 | 0.00% |

| -20.00% | $1,000.00 | 0.00% |

| -40.00% | $1,000.00 | 0.00% |

| -60.00% | $1,000.00 | 0.00% |

| -80.00% | $1,000.00 | 0.00% |

| -100.00% | $1,000.00 | 0.00% |

This hypothetical scenario analysis does not reflect advisory fees, brokerage or other commissions, or any other expenses that an investor may incur in connection with the notes. No representation is made that any trading strategy or account will, or is likely to, achieve similar returns to those shown above. Hypothetical results are neither an indicator nor guarantee of future returns. Actual results will vary, perhaps materially, from this analysis. The numbers appearing in the above table have been rounded for ease of analysis. | ||

| Risk Factors | ||

THE RETURN ON THE NOTES IS SUBJECT TO MARKET RISK– The return on the notes at maturity is linked to the performance of the Basket Currencies relative to the U.S. dollar and will depend on whether, and the extent to which, the Basket Performance is positive. Any positive Basket Performance will depend on the aggregate performance of each Basket Currency relative to the U.S. dollar. Historical performance of the Basket Currencies should not be taken as an indication of the future performance of the Basket Currencies during the term of the notes. THE NOTES DO NOT PAY INTEREST – You will not receive any interest payments during the term of the notes. If the Basket Performance is equal to or less than zero, you will receive only the principal amount of the notes at maturity, which may not be enough to compensate you for any loss in value due to inflation and other factors relating to the value of your investment over time. PAYMENT AT MATURITY OF THE NOTES IS SUBJECT TO OUR CREDITWORTHINESS – Payment at maturity of the notes, including any principal protection is subject to our creditworthiness. An actual or anticipated downgrade in our credit rating will likely have an adverse effect on the market value of the notes. INVESTING IN THE NOTES IS NOT EQUIVALENT TO INVESTING DIRECTLY IN THE BASKET CURRENCIES – You may receive a lower payment at maturity than you would have received if you had invested directly in the Basket Currencies. In addition, the Basket Performance is based on the Basket Currency Performance for each Basket Currency, which is dependent solely on the stated formula set forth above and not on any other formula that could be used for calculating currency performances. POSITIVE PERFORMANCE OF ONE OR MORE BASKET CURRENCIES MAY BE OFFSET BY LOSSES IN THE PERFORMANCE OF OTHER BASKET CURRENCIES – The notes are linked to the performance of an equally weighted basket composed of four currencies. The performance of the Basket will be based on the appreciation or depreciation of the Basket as a whole. Therefore, positive performances of one or more Basket Currencies may be offset, in whole or in part, by negative performances of one or more other Basket Currencies of equal or greater magnitude, which may result in an aggregate Basket Performance equal to or less than zero. LACK OF LIQUIDITY – The notes will not be listed on any securities exchange. CERTAIN BUILT-IN COSTS ARE LIKELY TO ADVERSELY AFFECT THE VALUE OF THE NOTES PRIOR TO MATURITY – Certain built-in costs, such as the agent’s commission and our estimated cost of hedging, are likely to adversely affect the value of the notes prior to maturity. You should be willing and able to hold your notes to maturity. | CURRENCY MARKETS MAY BE VOLATILE AND THE BASKET CURRENCIES ARE SUBJECT TO EMERGING MARKETS’ POLITICAL AND ECONOMIC RISKS – Currency markets may be highly volatile, particularly in relation to emerging or developing nations’ currencies. Foreign currency rate risks include, but are not limited to, convertibility risk and market volatility and potential interference by foreign governments through regulation of local markets, foreign investment or particular transactions in foreign currency. Some of the Basket Currencies are the currencies of emerging market countries and emerging market countries are more exposed to the risk of swift political change and economic downturns than their industrialized counterparts. Currency exchange risk and political or economic instability of the emerging markets are likely to have an adverse effect on the performance of the Basket Currencies, and, consequently, the return on the notes and your payment at maturity. POTENTIAL CONFLICTS – We and our affiliates play a variety of roles in connection with the issuance of the notes, including acting as Calculation Agent and hedging our obligations under the notes. In performing duties, the economic interests of the Calculation Agent and other affiliates of ours are potentially adverse to your interests as an investor in the notes. See “Selected Risk Considerations” in the accompanying term sheet and “Risk Factors” in the accompanying product supplement for additional information. TAX TREATMENT– The notes will be treated as contingent payment debt instruments for U.S. federal income tax purposes. For additional information, see “Selected Purchase Considerations – Taxed as Contingent Payment Debt Instruments” in the accompanying term sheet. Deutsche Bank AG has filed a registration statement (including a prospectus) with the Securities and Exchange Commission, or SEC, for the offering to which this fact sheet relates. Before you invest, you should read the prospectus in that registration statement and the other documents including term sheet No. 772BD and the product supplement relating to this offering that Deutsche Bank AG has filed with the SEC for more complete information about Deutsche Bank AG and this offering. You may obtain these documents without cost by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, Deutsche Bank AG, any agent or any dealer participating in this offering will arrange to send you the prospectus, prospectus supplement, product supplement, underlying supplement, term sheet No. 772BD and this fact sheet if you so request by calling toll-free 1-800-311-4409. | |

DWS Structured Products 1.866.637.9185 www.dws-sp.com