|

Free Writing Prospectus

Filed Pursuant to Rule 433

Registration Statement No.333-162195

Dated December 18, 2009

Deutsche Bank Liquid Commodity Index

Suite of Mean Reversion Indices

December 2009

[GRAPHIC OMITTED]

Deutsche Bank

1

|

|

Mean Reversion Indices

Executive Summary

DBLCI - Mean Reversion (MR) Index

DBLCI - Mean Reversion Enhanced (MRE) Index

DBLCI - Mean Reversion Enhanced 15 (MRE15) Index

DBLCI - Mean Reversion "Plus" (MR+) Index

Appendix

Types of Returns in a Commodity Index

Mean Reversion

Momentum

Optimized Yield

Target Volatility

Comparative Statistics

Market Data Sources

Important Considerations

2

|

|

Mean Reversion Indices

3

|

|

Executive Summary

The Evolution of Commodity Markets

o Commodities are an asset class in their own right and exhibit unique

characteristics such as historically low correlation with traditional asset

classes and a positive correlation with inflation

o Deutsche Bank is one of the largest providers of non-benchmark commodity

indices with a comprehensive suite of commodity index products aimed at

enhancing beta returns and extracting market neutral alpha returns in the

commodity space

o An investment in a commodity index is a simple way for investors to gain

exposure to the asset class while insulating them from the mechanics of

rolling future contracts and posting collateral

o As the commodity market has evolved, Deutsche Bank has created new indices

that may benefit from the special features of the asset class

4

|

|

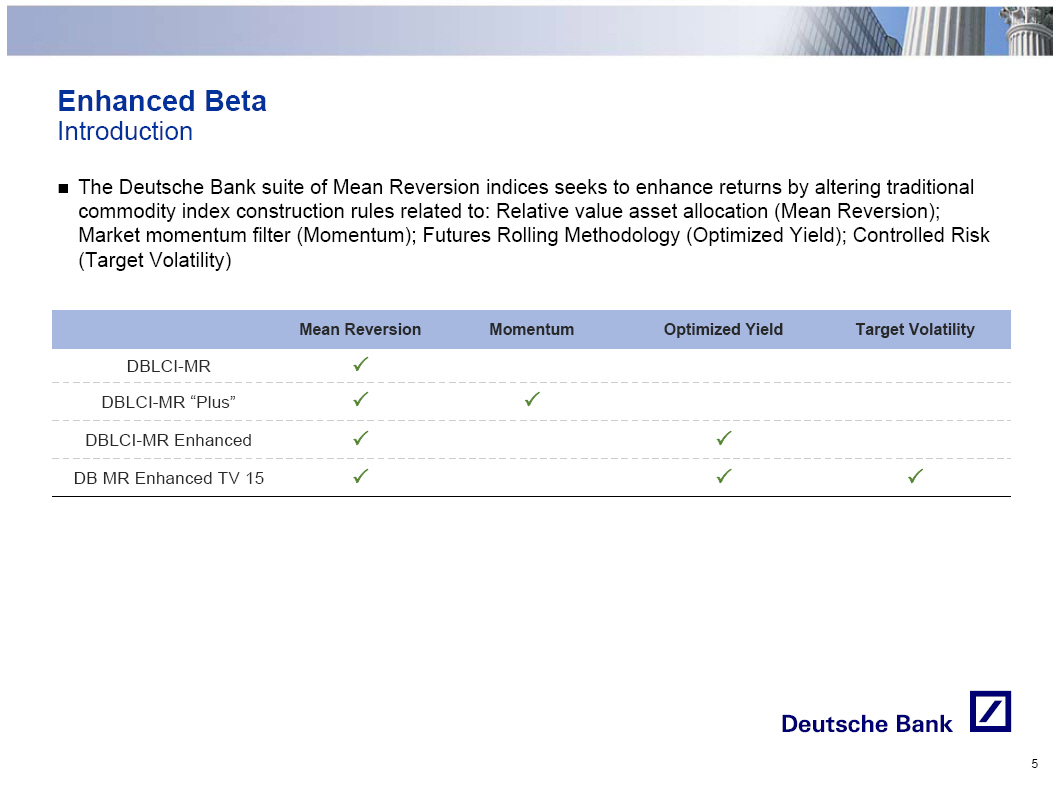

Enhanced Beta

Introduction

o The Deutsche Bank suite of Mean Reversion indices seeks to enhance returns

by altering traditional commodity index construction rules related to:

Relative value asset allocation (Mean Reversion); Market momentum filter

(Momentum); Futures Rolling Methodology (Optimized Yield); Controlled Risk

(Target Volatility)

Mean Reversion Momentum Optimized Yield Target Volatility

DBLCI-MR o

DBLCI-MR "Plus" o o

DBLCI-MR Enhanced o o

DB MR Enhanced TV 15 o o o

5

|

|

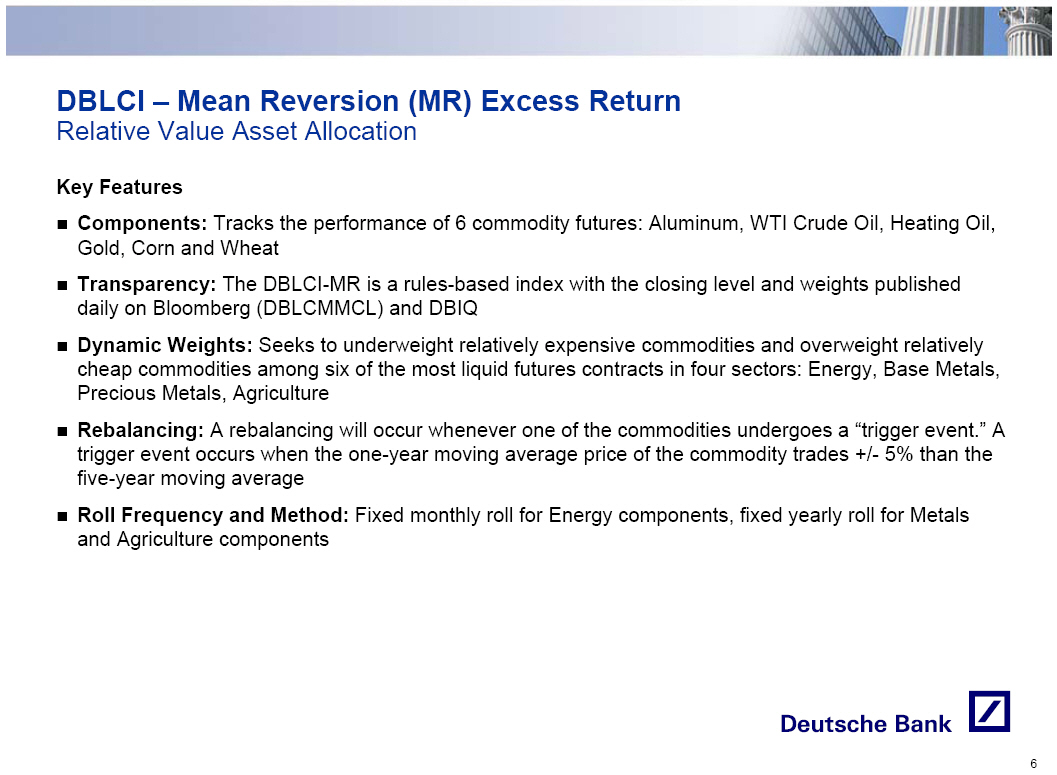

DBLCI - Mean Reversion (MR) Excess Return

Relative Value Asset Allocation

Key Features

o Components: Tracks the performance of 6 commodity futures: Aluminum, WTI

Crude Oil, Heating Oil, Gold, Corn and Wheat

o Transparency: The DBLCI-MR is a rules-based index with the closing level

and weights published daily on Bloomberg (DBLCMMCL) and DBIQ

o Dynamic Weights: Seeks to underweight relatively expensive commodities and

overweight relatively cheap commodities among six of the most liquid

futures contracts in four sectors: Energy, Base Metals, Precious Metals,

Agriculture

o Rebalancing: A rebalancing will occur whenever one of the commodities

undergoes a "trigger event." A trigger event occurs when the one-year

moving average price of the commodity trades +/- 5% than the five-year

moving average

o Roll Frequency and Method: Fixed monthly roll for Energy components, fixed

yearly roll for Metals and Agriculture components

6

|

|

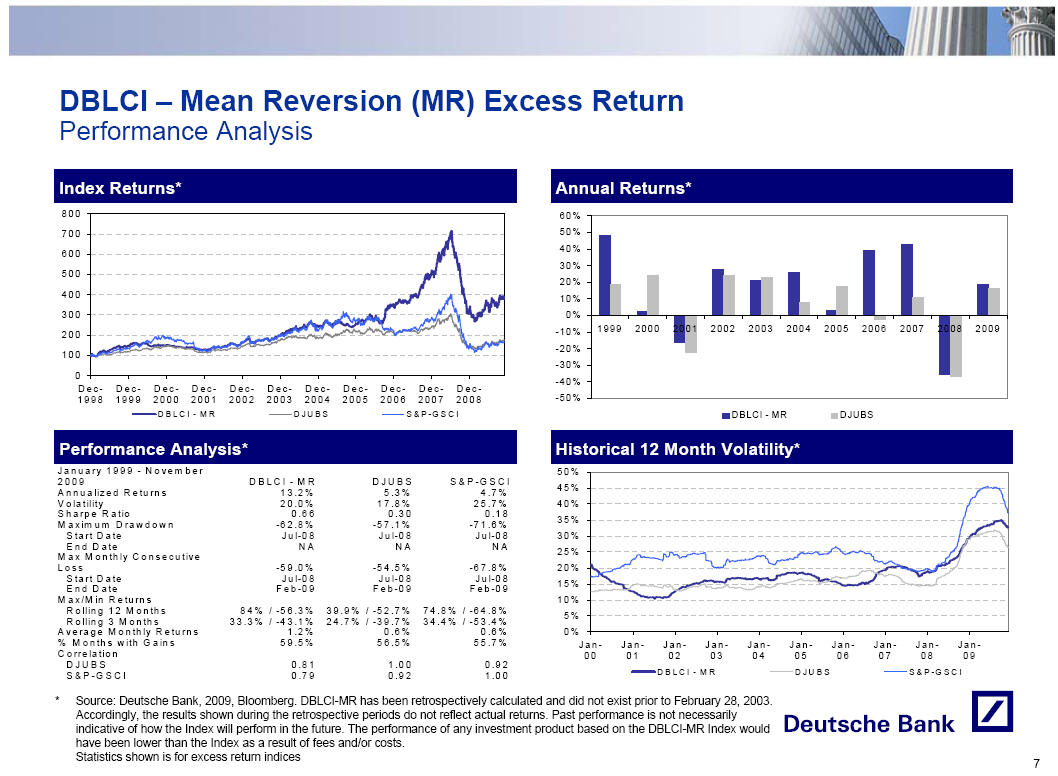

DBLCI - Mean Reversion (MR) Excess Return

Performance Analysis

Index Returns*

[GRAPHIC OMITTED]

Performance Analysis*

January 1999 - November 2009

D B L C I - M R D J U B SS & P -G S C I

Annualized Returns 13.2% 5.3% 4.7%

Volatility 20.0% 17.8% 25.7%

SharpeRatio 0.66 0.30 0.18

MaximumDrawdown -62.8% -57.1% -71.6%

StartDate Jul-08 Jul-08 Jul-08

EndDate NA NA NA

Max Monthly Consecutive Loss -59.0% -54.5% -67.8%

StartDate Jul-08 Jul-08 Jul-08

EndDate Feb-09 Feb-09 Feb-09

Max/Min Returns

Rolling 12 Months 84%/-56.3% 39.9%/-52.7% 74.8%/-64.8%

Rolling 3 Months 33.3%/-43.1% 24.7%/-39.7% 34.4%/-53.4%

Average Monthly Returns 1.2% 0.6% 0.6%

%MonthswithGains 59.5% 56.5% 55.7%

Correlation

DJUBS 0.81 1.00 0.92

S&P-GSCI 0.79 0.92 1.00

Annual Returns*

[GRAPHIC OMITTED]

Historical 12 Month Volatility*

[GRAPHIC OMITTED]

* Source: Deutsche Bank, 2009, Bloomberg. DBLCI-MR has been retrospectively

calculated and did not exist prior to February 28, 2003. Accordingly, the

results shown during the retrospective periods do not reflect actual

returns. Past performance is not necessarily indicative of how the Index

will perform in the future. The performance of any investment product based

on the DBLCI-MR Index would have been lower than the Index as a result of

fees and/or costs. Statistics shown is for excess return indices

7

|

|

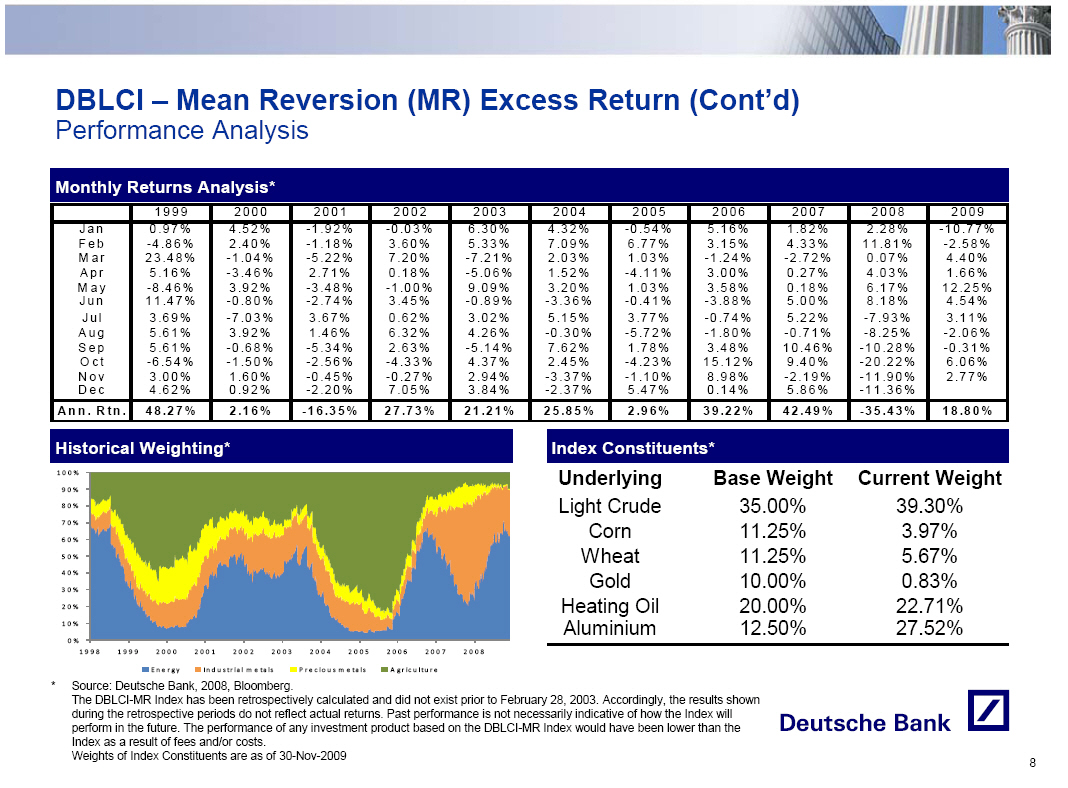

DBLCI - Mean Reversion (MR) Excess Return (Cont'd)

Performance Analysis

Monthly Returns Analysis*

1999 2000 2001 2002 2003

Jan 0.97% 4.52% -1.92% -0.03% 6.30%

Feb -4.86% 2.40% -1.18% 3.60% 5.33%

Mar 23.48% -1.04% -5.22% 7.20% -7.21%

Apr 5.16% -3.46% 2.71% 0.18% -5.06%

May -8.46% 3.92% -3.48% -1.00% 9.09%

Jun 11.47% -0.80% -2.74% 3.45% -0.89%

Jul 3.69% -7.03% 3.67% 0.62% 3.02%

Aug 5.61% 3.92% 1.46% 6.32% 4.26%

Sep 5.61% -0.68% -5.34% 2.63% -5.14%

Oct -6.54% -1.50% -2.56% -4.33% 4.37%

Nov 3.00% 1.60% -0.45% -0.27% 2.94%

Dec 4.62% 0.92% -2.20% 7.05% 3.84%

Ann.Rtn. 48.27% 2.16% -16.35% 27.73% 21.21%

2004 2005 2006 2007 2008 2009

4.32% -0.54% 5.16% 1.82% 2.28% -10.77%

7.09% 6.77% 3.15% 4.33% 11.81% -2.58%

2.03% 1.03% -1.24% -2.72% 0.07% 4.40%

1.52% -4.11% 3.00% 0.27% 4.03% 1.66%

3.20% 1.03% 3.58% 0.18% 6.17% 12.25%

-3.36% -0.41% -3.88% 5.00% 8.18% 4.54%

5.15% 3.77% -0.74% 5.22% -7.93% 3.11%

-0.30% -5.72% -1.80% -0.71% -8.25% -2.06%

7.62% 1.78% 3.48% 10.46% -10.28% -0.31%

2.45% -4.23% 15.12% 9.40% -20.22% 6.06%

-3.37% -1.10% 8.98% -2.19% -11.90% 2.77%

-2.37% 5.47% 0.14% 5.86% -11.36%

25.85% 2.96% 39.22% 42.49% -35.43% 18.80%

Historical Weighting*

[GRAPHIC OMITTED]

Index Constituents*

Underlying Base Weight Current Weight

Light Crude 35.00% 39.30%

Corn 11.25% 3.97%

Wheat 11.25% 5.67%

Gold 10.00% 0.83%

Heating Oil 20.00% 22.71%

Aluminium 12.50% 27.52%

* Source: Deutsche Bank, 2008, Bloomberg.

The DBLCI-MR Index has been retrospectively calculated and did not exist

prior to February 28, 2003. Accordingly, the results shown during the

retrospective periods do not reflect actual returns. Past performance is

not necessarily indicative of how the Index will perform in the future. The

performance of any investment product based on the DBLCI-MR Index would

have been lower than the Index as a result of fees and/or costs.

Weights of Index Constituents are as of 30-Nov-2009

8

|

|

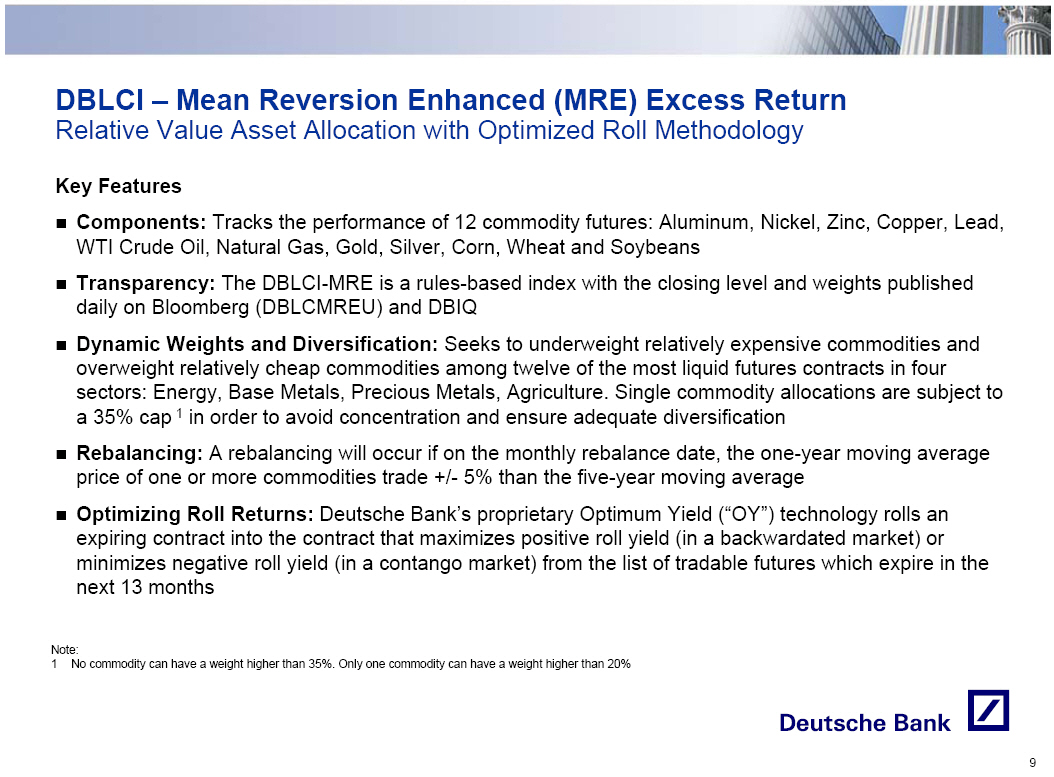

DBLCI - Mean Reversion Enhanced (MRE) Excess Return

Relative Value Asset Allocation with Optimized Roll Methodology

Key Features

o Components: Tracks the performance of 12 commodity futures: Aluminum,

Nickel, Zinc, Copper, Lead, WTI Crude Oil, Natural Gas, Gold, Silver, Corn,

Wheat and Soybeans

o Transparency: The DBLCI-MRE is a rules-based index with the closing level

and weights published daily on Bloomberg (DBLCMREU) and DBIQ

o Dynamic Weights and Diversification: Seeks to underweight relatively

expensive commodities and overweight relatively cheap commodities among

twelve of the most liquid futures contracts in four sectors: Energy, Base

Metals, Precious Metals, Agriculture. Single commodity allocations are

subject to a 35% cap (1) in order to avoid concentration and ensure

adequate diversification

o Rebalancing: A rebalancing will occur if on the monthly rebalance date, the

one-year moving average price of one or more commodities trade +/- 5% than

the five-year moving average

o Optimizing Roll Returns: Deutsche Bank's proprietary Optimum Yield ("OY")

technology rolls an expiring contract into the contract that maximizes

positive roll yield (in a backwardated market) or minimizes negative roll

yield (in a contango market) from the list of tradable futures which expire

in the next 13 months

Note:

1 No commodity can have a weight higher than 35%. Only one commodity can have

a weight higher than 20%

9

|

|

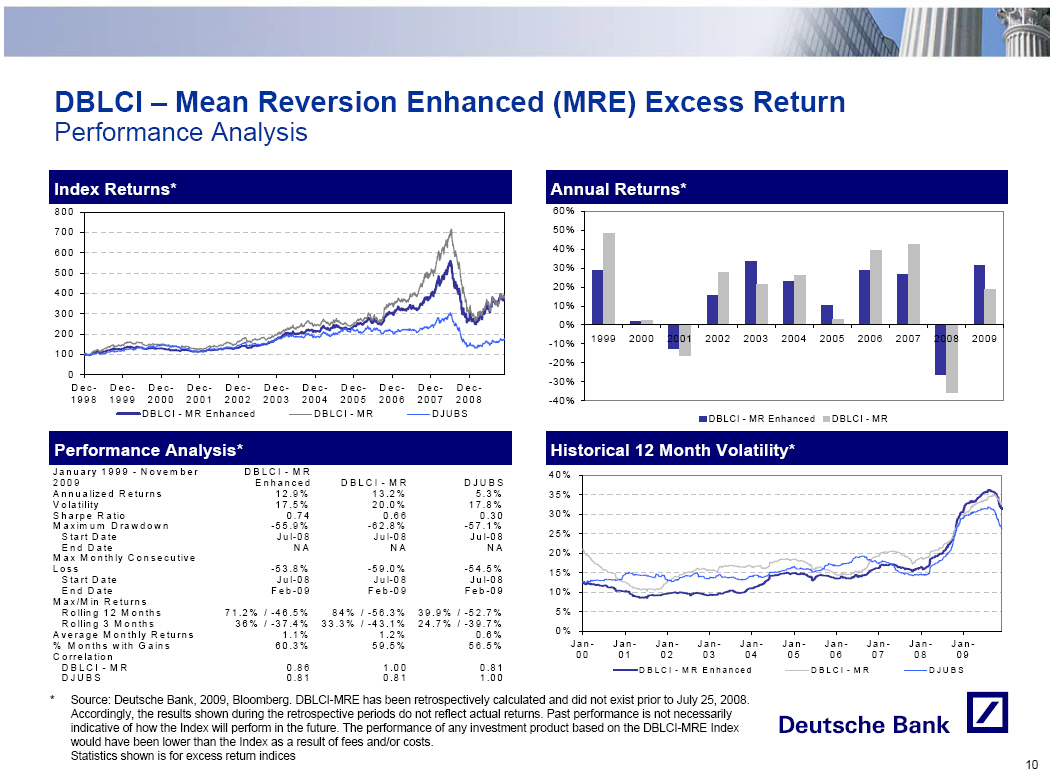

DBLCI - Mean Reversion Enhanced (MRE) Excess Return

Performance Analysis

Index Returns*

[GRAPHIC OMITTED]

Performance Analysis*

January 1999 - November DBLCI-MR

2009 Enhanced DBLCI-MR DJUBS

Annualized Returns 12.9% 13.2% 5.3%

Volatility 17.5% 20.0% 17.8%

Sharpe Ratio 0.74 0.66 0.30

Maximum Drawdown -55.9% -62.8% -57.1%

Start Date Jul-08 Jul-08 Jul-08

End Date NA NA NA

Max MonthlyConsecutive

Loss -53.8% -59.0% -54.5%

Start Date Jul-08 Jul-08 Jul-08

End Date Feb-09 Feb-09 Feb-09

Max/Min Returns

Rolling 12 Months 71.2%/-46.5% 84%/-56.3% 39.9%/-52.7%

Rolling 3 Months 36%/-37.4% 33.3%/-43.1% 24.7%/-39.7%

Average Monthly Returns 1.1% 1.2% 0.6%

% Months with Gains 60.3% 59.5% 56.5%

Correlation

DBLCI-MR 0.86 1.00 0.81

DJUBS 0.81 0.81 1.00

Annual Returns*

[GRAPHIC OMITTED]

Historical 12 Month Volatility*

[GRAPHIC OMITTED]

* Source: Deutsche Bank, 2009, Bloomberg. DBLCI-MRE has been retrospectively

calculated and did not exist prior to July 25, 2008. Accordingly, the

results shown during the retrospective periods do not reflect actual

returns. Past performance is not necessarily indicative of how the Index

will perform in the future. The performance of any investment product based

on the DBLCI-MRE Index would have been lower than the Index as a result of

fees and/or costs.

Statistics shown is for excess return indices

10

|

|

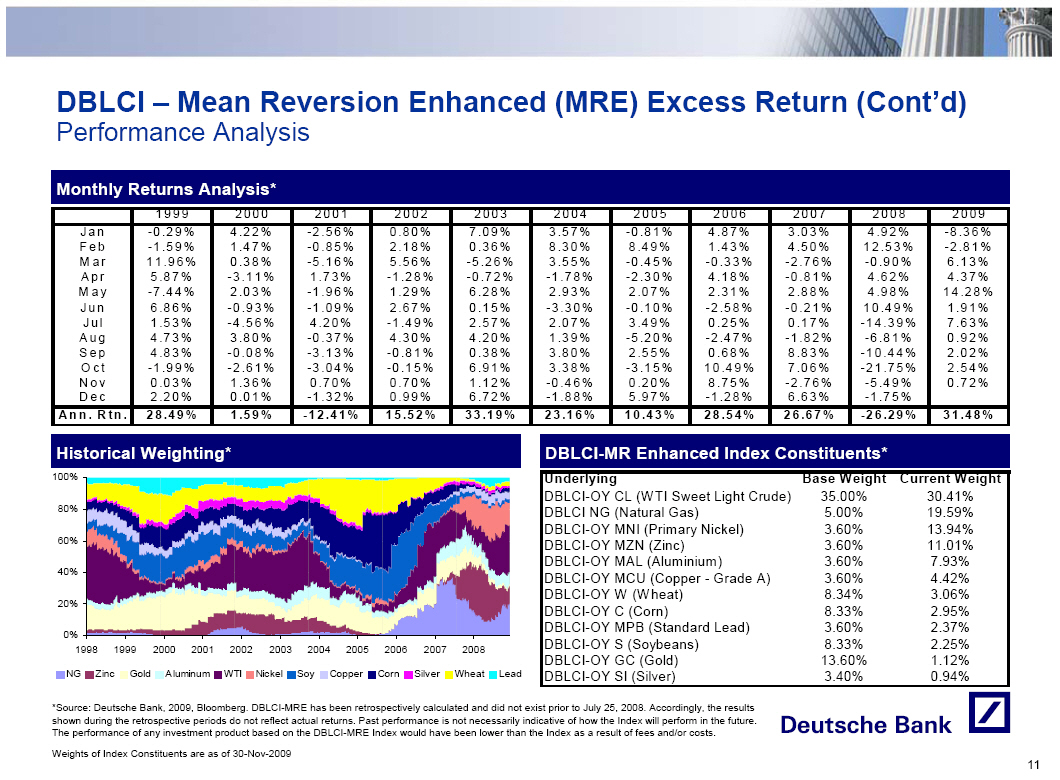

DBLCI - Mean Reversion Enhanced (MRE) Excess Return (Cont'd)

Performance Analysis

Monthly Returns Analysis*

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Jan -0.29% 4.22% -2.56% 0.80% 7.09% 3.57% -0.81% 4.87% 3.03% 4.92% -8.36%

Feb -1.59% 1.47% -0.85% 2.18% 0.36% 8.30% 8.49% 1.43% 4.50% 12.53% -2.81%

Mar 11.96% 0.38% -5.16% 5.56% -5.26% 3.55% -0.45% -0.33% -2.76% -0.90% 6.13%

Apr 5.87% -3.11% 1.73% -1.28% -0.72% -1.78% -2.30% 4.18% -0.81% 4.62% 4.37%

May -7.44% 2.03% -1.96% 1.29% 6.28% 2.93% 2.07% 2.31% 2.88% 4.98% 14.28%

Jun 6.86% -0.93% -1.09% 2.67% 0.15% -3.30% -0.10% -2.58% -0.21% 10.49% 1.91%

Jul 1.53% -4.56% 4.20% -1.49% 2.57% 2.07% 3.49% 0.25% 0.17% -14.39% 7.63%

Aug 4.73% 3.80% -0.37% 4.30% 4.20% 1.39% -5.20% -2.47% -1.82% -6.81% 0.92%

Sep 4.83% -0.08% -3.13% -0.81% 0.38% 3.80% 2.55% 0.68% 8.83% -10.44% 2.02%

Oct -1.99% -2.61% -3.04% -0.15% 6.91% 3.38% -3.15% 10.49% 7.06% -21.75% 2.54%

Nov 0.03% 1.36% 0.70% 0.70% 1.12% -0.46% 0.20% 8.75% -2.76% -5.49% 0.72%

Dec 2.20% 0.01% -1.32% 0.99% 6.72% -1.88% 5.97% -1.28% 6.63% -1.75%

Ann.Rtn. 28.49% 1.59% -12.41% 15.52% 33.19% 23.16% 10.43% 28.54% 26.67% -26.29% 31.48%

Historical Weighting*

[GRAPHIC OMITTED]

DBLCI-MR Enhanced Index Constituents*

- --------------------------------------------------------------------------------

Underlying Base Weight Current Weight

DBLCI-OY CL (WTI Sweet Light Crude) 35.00% 30.41%

DBLCI NG (Natural Gas) 5.00% 19.59%

DBLCI-OY MNI (Primary Nickel) 3.60% 13.94%

DBLCI-OY MZN (Zinc) 3.60% 11.01%

DBLCI-OY MAL (Aluminium) 3.60% 7.93%

DBLCI-OY MCU (Copper - Grade A) 3.60% 4.42%

DBLCI-OY W (Wheat) 8.34% 3.06%

DBLCI-OY C (Corn) 8.33% 2.95%

DBLCI-OY MPB (Standard Lead) 3.60% 2.37%

DBLCI-OY S (Soybeans) 8.33% 2.25%

DBLCI-OY GC (Gold) 13.60% 1.12%

DBLCI-OY SI (Silver) 3.40% 0.94%

- -------------------------------------------------------------------------------

*Source: Deutsche Bank, 2009, Bloomberg. DBLCI-MRE has been retrospectively

calculated and did not exist prior to July 25, 2008. Accordingly, the results

shown during the retrospective periods do not reflect actual returns. Past

performance is not necessarily indicative of how the Index will perform in the

future. The performance of any investment product based on the DBLCI-MRE Index

would have been lower than the Index as a result of fees and/or costs.

Weights of Index Constituents are as of 30-Nov-2009

11

|

|

DBLCI - Mean Reversion Enhanced TV15 (MRE15) Excess Return

Relative Value Asset Allocation with Optimized Roll Methodology and Target Volatility

Key Features

o Components: Tracks the performance of 12 commodity futures: Aluminum,

Nickel, Zinc, Copper, Lead, WTI Crude Oil, Natural Gas, Gold, Silver, Corn,

Wheat and Soybeans

o Transparency: The DBLCI-MRE15 is a rules-based index with the closing level

and weights published daily on Bloomberg (DBLCMTEU) and DBIQ

o Dynamic Weights and Diversification: Seeks to underweight relatively

expensive commodities and overweight relatively cheap commodities among

twelve of the most liquid futures contracts in four sectors: Energy, Base

Metals, Precious Metals, Agriculture. Single commodity allocations are

subject to a 35% cap (1) in order to avoid concentration problem and ensure

adequate diversification

o Rebalancing: A rebalancing will occur if on the monthly rebalance date, the

one-year moving average price of one or more commodities trade +/- 5% than

the five-year moving average

o Optimizing Roll Returns: Deutsche Bank's proprietary optimum yield ("OY")

technology rolls an expiring contract into the contract that maximizes

positive roll yield (in a backwardated market) or minimizes negative roll

yield (in a contango market) from the list of tradable futures which expire

in the next 13 months

o Target Volatility: Exposure to the DBLCI-MRE is reset monthly in order to

target a realized volatility close to 15%. Exposure = Max (300%, 15% target

volatility / 90 day realized volatility)

Note:

1 No commodity can have a weight higher than 35%. Only one commodity can have

a weight higher than 20%

12

|

|

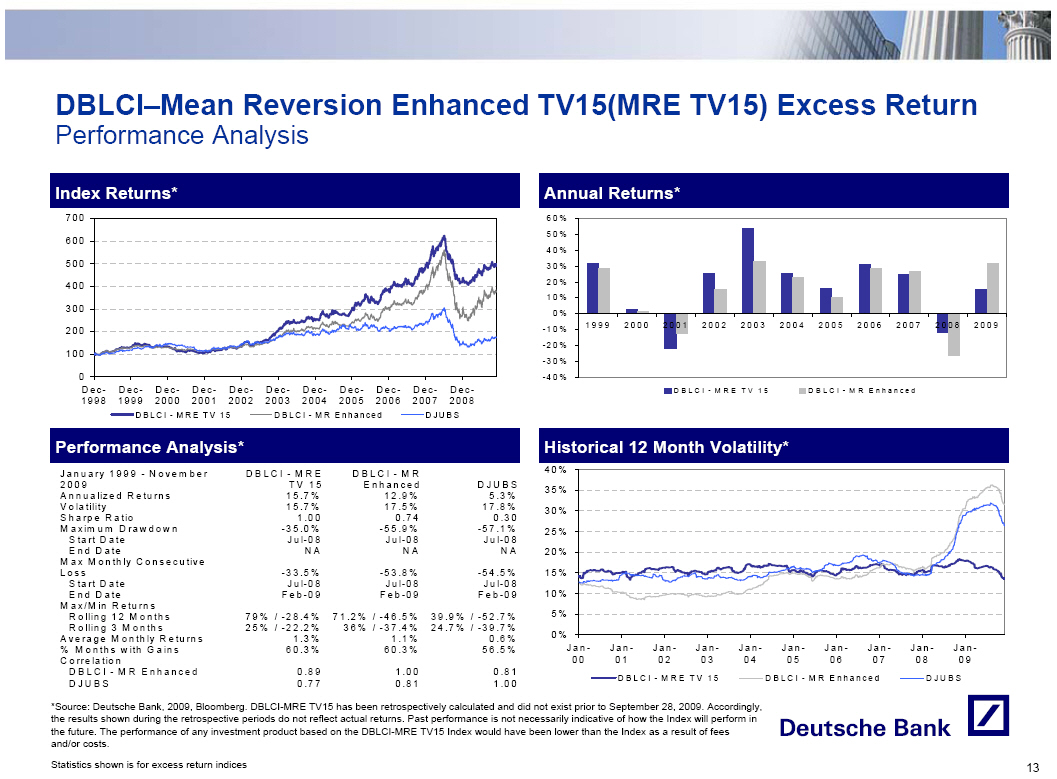

DBLCI-Mean Reversion Enhanced TV15(MRE TV15) Excess Return

Performance Analysis

Index Returns*

[GRAPHIC OMITTED]

Annual Returns*

[GRAPHIC OMITTED]

Performance Analysis*

January 1999 - November DBLCI-MRE DBLCI-MR

2009 TV15 Enhanced DJUBS

Annualized Returns 15.7% 12.9% 5.3%

Volatility 15.7% 17.5% 17.8%

Sharpe Ratio 1.00 0.74 0.30

Maximum Drawdown -35.0% -55.9% -57.1%

Start Date Jul-08 Jul-08 Jul-08

End Date NA NA NA

Max Monthly Consecutive

Loss -33.5% -53.8% -54.5%

Start Date Jul-08 Jul-08 Jul-08

End Date Feb-09 Feb-09 Feb-09

Max/Min Returns

Rolling 12 Months 79%/-28.4% 71.2%/-46.5% 39.9%/-52.7%

Rolling 3 Months 25%/-22.2% 36%/-37.4% 24.7%/-39.7%

Average Monthly Returns 1.3% 1.1% 0.6%

% Months with Gains 60.3% 60.3% 56.5%

Correlation

DBLCI-MREnhanced 0.89 1.00 0.81

DJUBS 0.77 0.81 1.00

Historical 12 Month Volatility*

[GRAPHIC OMITTED]

*Source: Deutsche Bank, 2009, Bloomberg. DBLCI-MRE TV15 has been retrospectively

calculated and did not exist prior to September 28, 2009. Accordingly, the

results shown during the retrospective periods do not reflect actual returns.

Past performance is not necessarily indicative of how the Index will perform in

the future. The performance of any investment product based on the DBLCI-MRE

TV15 Index would have been lower than the Index as a result of fees and/or

costs.

Statistics shown is for excess return indices

13

|

|

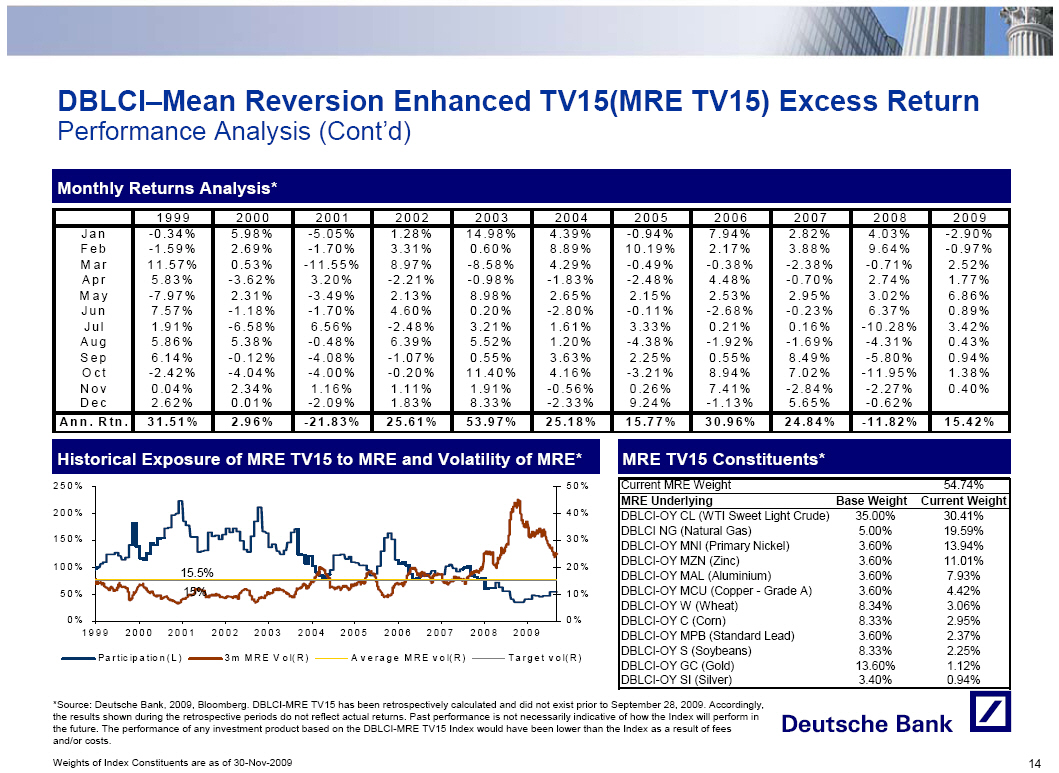

DBLCI-Mean Reversion Enhanced TV15(MRE TV15) Excess Return

Performance Analysis (Cont'd)

Monthly Returns Analysis*

1999 2000 2001 2002 2003

Jan -0.34% 5.98% -5.05% 1.28% 14.98%

Feb -1.59% 2.69% -1.70% 3.31% 0.60%

Mar 11.57% 0.53% -11.55% 8.97% -8.58%

Apr 5.83% -3.62% 3.20% -2.21% -0.98%

May -7.97% 2.31% -3.49% 2.13% 8.98%

Jun 7.57% -1.18% -1.70% 4.60% 0.20%

Jul 1.91% -6.58% 6.56% -2.48% 3.21%

Aug 5.86% 5.38% -0.48% 6.39% 5.52%

Sep 6.14% -0.12% -4.08% -1.07% 0.55%

Oct -2.42% -4.04% -4.00% -0.20% 11.40%

Nov 0.04% 2.34% 1.16% 1.11% 1.91%

Dec 2.62% 0.01% -2.09% 1.83% 8.33%

Ann.Rtn. 31.51% 2.96% -21.83% 25.61% 53.97%

2004 2005 2006 2007 2008 2009

4.39% -0.94% 7.94% 2.82% 4.03% -2.90%

8.89% 10.19% 2.17% 3.88% 9.64% -0.97%

4.29% -0.49% -0.38% -2.38% -0.71% 2.52%

-1.83% -2.48% 4.48% -0.70% 2.74% 1.77%

2.65% 2.15% 2.53% 2.95% 3.02% 6.86%

-2.80% -0.11% -2.68% -0.23% 6.37% 0.89%

1.61% 3.33% 0.21% 0.16% -10.28% 3.42%

1.20% -4.38% -1.92% -1.69% -4.31% 0.43%

3.63% 2.25% 0.55% 8.49% -5.80% 0.94%

4.16% -3.21% 8.94% 7.02% -11.95% 1.38%

-0.56% 0.26% 7.41% -2.84% -2.27% 0.40%

-2.33% 9.24% -1.13% 5.65% -0.62%

25.18% 15.77% 30.96% 24.84% -11.82% 15.42%

Historical Exposure of MRE TV15 to MRE and Volatility of MRE*

[GRAPHIC OMITTED]

MRE TV15 Constituents*

- -------------------------------------------------------------------

Current MRE Weight 54.74%

- -------------------------------------------------------------------

MRE Underlying Base Weight Current Weight

- -------------------------------------------------------------------

DBLCI-OY CL (WTI Sweet Light Crude) 35.00% 30.41%

DBLCI NG (Natural Gas) 5.00% 19.59%

DBLCI-OY MNI (Primary Nickel) 3.60% 13.94%

DBLCI-OY MZN (Zinc) 3.60% 11.01%

DBLCI-OY MAL (Aluminium) 3.60% 7.93%

DBLCI-OY MCU (Copper - Grade A) 3.60% 4.42%

DBLCI-OY W (Wheat) 8.34% 3.06%

DBLCI-OY C (Corn) 8.33% 2.95%

DBLCI-OY MPB (Standard Lead) 3.60% 2.37%

DBLCI-OY S (Soybeans) 8.33% 2.25%

DBLCI-OY GC (Gold) 13.60% 1.12%

DBLCI-OY SI (Silver) 3.40% 0.94%

- -------------------------------------------------------------------

*Source: Deutsche Bank, 2009, Bloomberg. DBLCI-MRE TV15 has been retrospectively

calculated and did not exist prior to September 28, 2009. Accordingly, the

results shown during the retrospective periods do not reflect actual returns.

Past performance is not necessarily indicative of how the Index will perform in

the future. The performance of any investment product based on the DBLCI-MRE

TV15 Index would have been lower than the Index as a result of fees and/or

costs.

Weights of Index Constituents are as of 30-Nov-2009

14

|

|

DBLCI - Mean Reversion "Plus" (MR+) Excess Return

Relative Value Asset Allocation with a Market Momentum Filter

Key Features

o Components: Tracks the performance of 6 commodity futures: Aluminum, WTI

Crude Oil, Heating Oil, Gold, Corn and Wheat

o Transparency: The DBLCI-MR+ is a rules-based index with the closing level,

weights and exposure published daily on Bloomberg (DBLCMPUE) and DBIQ

o Dynamic Weights: Seeks to underweight relatively expensive commodities and

overweight relatively cheap commodities among six of the most liquid

futures contracts in four sectors: Energy, Base Metals, Precious Metals,

Agriculture

o Dynamic Allocation: The "Plus" strategy aims to preserve excess returns

generated by the DBLCI-MR by adjusting its exposure monthly to reflect

upward and downward momentum cycles

o Rebalancing: A rebalancing will occur whenever one of the commodities

undergoes a "trigger event." A trigger event occurs when the one-year

moving average price of the commodity trades +/- 5% than the five- year

moving average

o Roll Frequency and Method: Fixed monthly roll for Energy components, fixed

yearly roll for Metals and Agriculture components

15

|

|

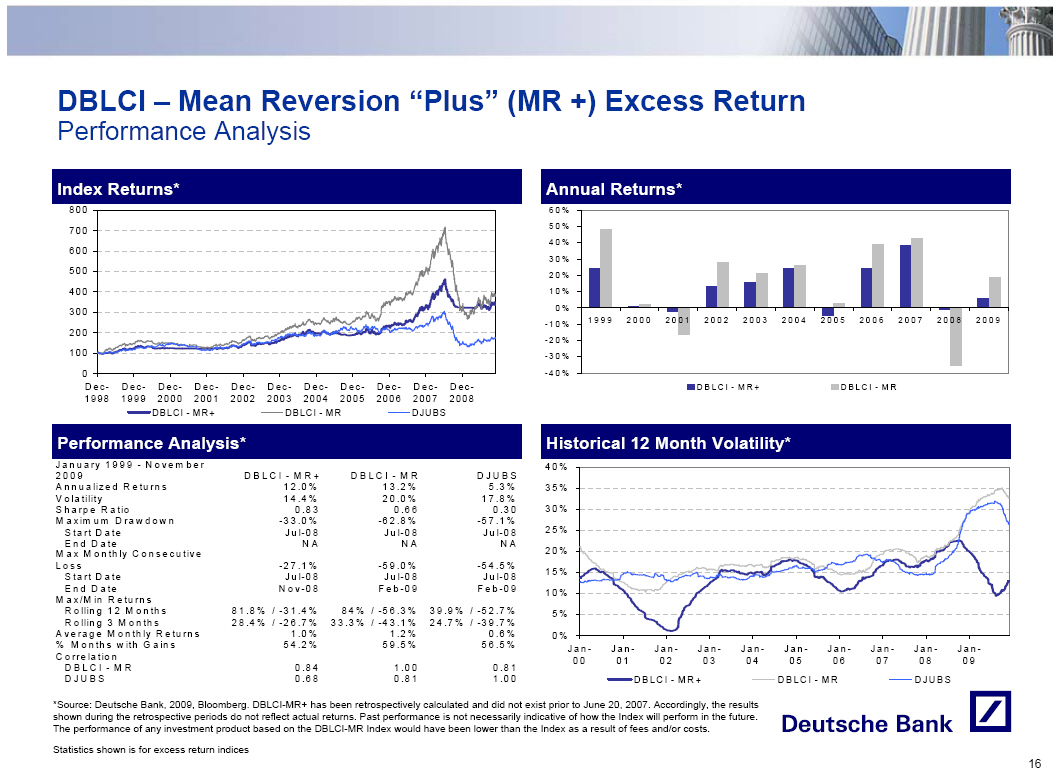

DBLCI - Mean Reversion "Plus" (MR +) Excess Return

Performance Analysis

Index Returns*

[GRAPHIC OMITTED]

Annual Returns*

[GRAPHIC OMITTED]

Performance Analysis*

J a n u a ry 1 9 9 9 -

N o v e m b e r

D B L C I - M R

2 0 0 9 +D B L C I - M R D J U B S

A n n u a liz e d R e turn s 1 2 .0 % 1 3 .2 % 5 .3 %

V o latility 1 4 .4 % 2 0 .0 % 1 7 .8 %

S h a rp e R a tio 0 .8 3 0 .6 6 0 .3 0

M a x im u m D ra w d o w n -3 3 .0 % -6 2 .8 % -5 7 .1 %

S ta rt D a te J u l-0 8 J u l-0 8 J u l-0 8

E n d D a te N A N A N A

M a x M o n th ly C o n s e c u tiv e

L o s s -2 7 .1 % -5 9 .0 % -5 4 .5 %

S ta rt D a te J u l-0 8 J u l-0 8 J u l-0 8

E n d D a te N o v -0 8 F e b -0 9 F e b -0 9

M a x /M in R e tu rn s

R o llin 8 1 .8 % / -3 -5 6 3 9 .9 % / -5

g 1 2 M o n th s 1 .4 % 8 4 %/ .3 % 2 .7 %

R o llin 2 8 .4 % / -2 3 3 .3 % / -4 2 4 .7 % / -3

g 3 M o n th s 6 .7 % 3 .1 % 9 .7 %

Average Monthly Returns 1 .0 % 1 .2 % 0 .6 %

% M o n th s w ith G ain s 5 4 .2 % 5 9 .5 % 5 6 .5 %

C o rre la tio n

D B L C I - M R 0 .8 4 1 .0 0 0 .8 1

D J U B S 0 .6 8 0 .8 1 1 .0 0

Historical 12 Month Volatility*

[GRAPHIC OMITTED]

*Source: Deutsche Bank, 2009, Bloomberg. DBLCI-MR+ has been retrospectively

calculated and did not exist prior to June 20, 2007. Accordingly, the results

shown during the retrospective periods do not reflect actual returns. Past

performance is not necessarily indicative of how the Index will perform in the

future. The performance of any investment product based on the DBLCI-MR Index

would have been lower than the Index as a result of fees and/or costs.

Statistics shown is for excess return indices

16

|

|

DBLCI - Mean Reversion "Plus" (MR +) Excess Return (Cont'd)

Performance Analysis

Monthly Returns Analysis*

1999 2000 2001 2002 2003

Jan 0.03% 4.52% -0.82% -0.37% 6.00%

Feb -0.47% 2.40% -0.54% 0.59% 5.33%

Mar 1.48% -1.04% -0.43% 1.82% -7.21%

Apr 3.46% -3.25% 0.19% 0.56% -4.81%

May -6.05% 3.26% 0.00% -1.06% 7.06%

Jun 8.94% -0.72% 0.00% 0.96% -0.72%

Jul 3.15% -5.41% 0.00% 0.46% 2.41%

Aug 5.61% 1.14% 0.00% 6.32% 3.38%

Sep 5.61% 0.12% -0.71% 2.63% -4.70%

Oct -6.02% -0.96% -0.11% -4.22% 3.50%

Nov 2.40% 1.02% 0.00% -0.63% 1.68%

Dec 4.67% 0.22% 0.00% 5.88% 3.84%

Ann.Rtn. 23.97% 0.90% -2.40% 13.21% 15.56%

2004 2005 2006 2007 2008 2009

4.32% -0.37% 3.00% 1.18% 2.24% -0.59%

6.67% 3.29% 2.93% 4.41% 11.81% -0.09%

2.24% 0.00% -1.24% -2.72% 0.07% 0.00%

1.52% -3.91% 3.00% 0.32% 4.17% -0.38%

3.16% 0.30% 3.58% -0.39% 5.70% 2.83%

-3.08% -0.28% -3.88% 4.11% 8.18% 1.72%

4.96% 1.94% -0.74% 5.22% -7.93% -1.69%

-0.30% -4.54% -1.50% -0.99% -8.32% -2.17%

7.12% 0.69% 0.30% 9.93% -5.79% -0.17%

2.31% -2.10% 8.63% 9.40% -7.37% 4.19%

-3.34% -0.54% 8.98% -2.19% -1.04% 2.37%

-3.07% 1.17% -0.11% 5.76% 0.00%

24.07% -4.53% 24.53% 38.57% -0.67% 6.00%

Historical Exposure of MR+ to MR*

[GRAPHIC OMITTED]

MR+ Constituents*

- --------------------------------------------------------------------

Current MR W eight 91.67%

-------------------------------------------------------------------

M R Underlying Base Weight Current Weight

-------------------------------------------------------------------

Light Crude 35.00% 39.30%

Corn 11.25% 3.97%

W heat 11.25% 5.67%

Gold 10.00% 0.83%

Heating Oil 20.00% 22.71%

Alum inium 12.50% 27.52%

-------------------------------------------------------------------

*Source: Deutsche Bank, 2009, Bloomberg. DBLCI-MR+ has been retrospectively

calculated and did not exist prior to June 20, 2007. Accordingly, the results

shown during the retrospective periods do not reflect actual returns. Past

performance is not necessarily indicative of how the Index will perform in the

future. The performance of any investment product based on the DBLCI-MR Index

would have been lower than the Index as a result of fees and/or costs.

Weights of Index Constituents are as of 30-Nov-2009

17

|

|

Appendix

18

|

|

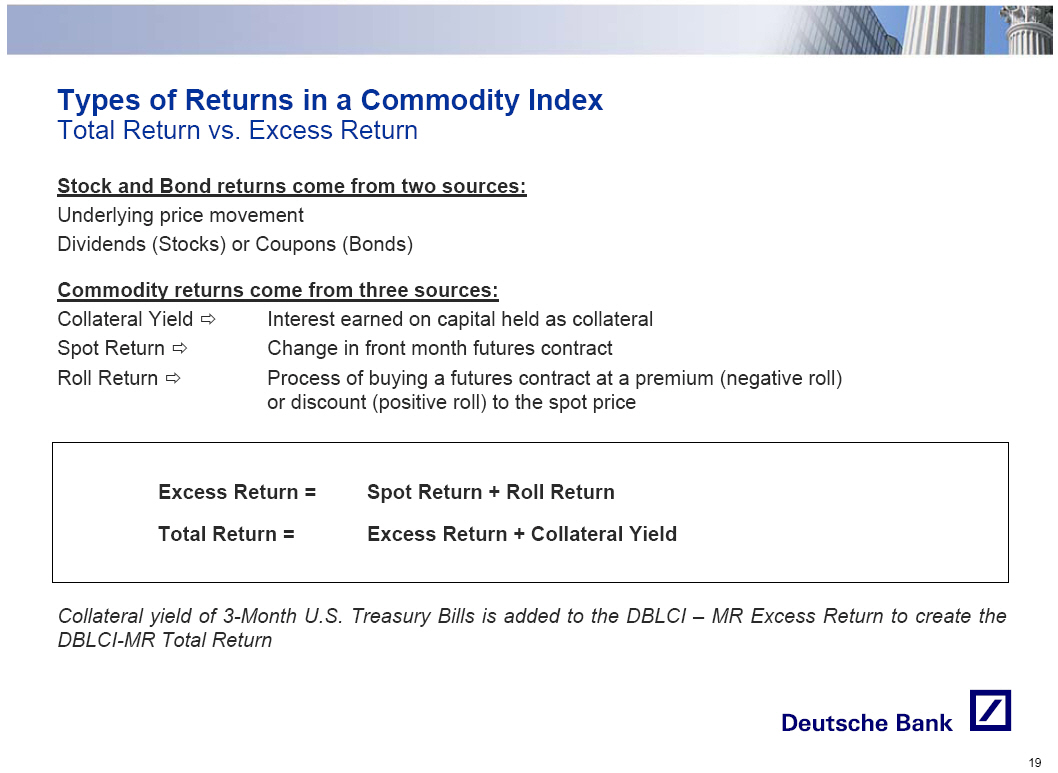

Types of Returns in a Commodity Index

Total Return vs. Excess Return

Stock and Bond returns come from two sources:

Underlying price movement

Dividends (Stocks) or Coupons

(Bonds)

Commodity returns come from three sources:

Collateral Yield > Interest earned on capital held as collateral

Spot Return > Change in front month futures contract

Roll Return > Process of buying a futures contract at a premium (negative roll)

or discount (positive roll) to the spot price

Excess Return = Spot Return + Roll Return

Total Return = Excess Return + Collateral Yield

Collateral yield of 3-Month U.S. Treasury Bills is added to the DBLCI - MR

Excess Return to create the DBLCI-MR Total Return

19

|

|

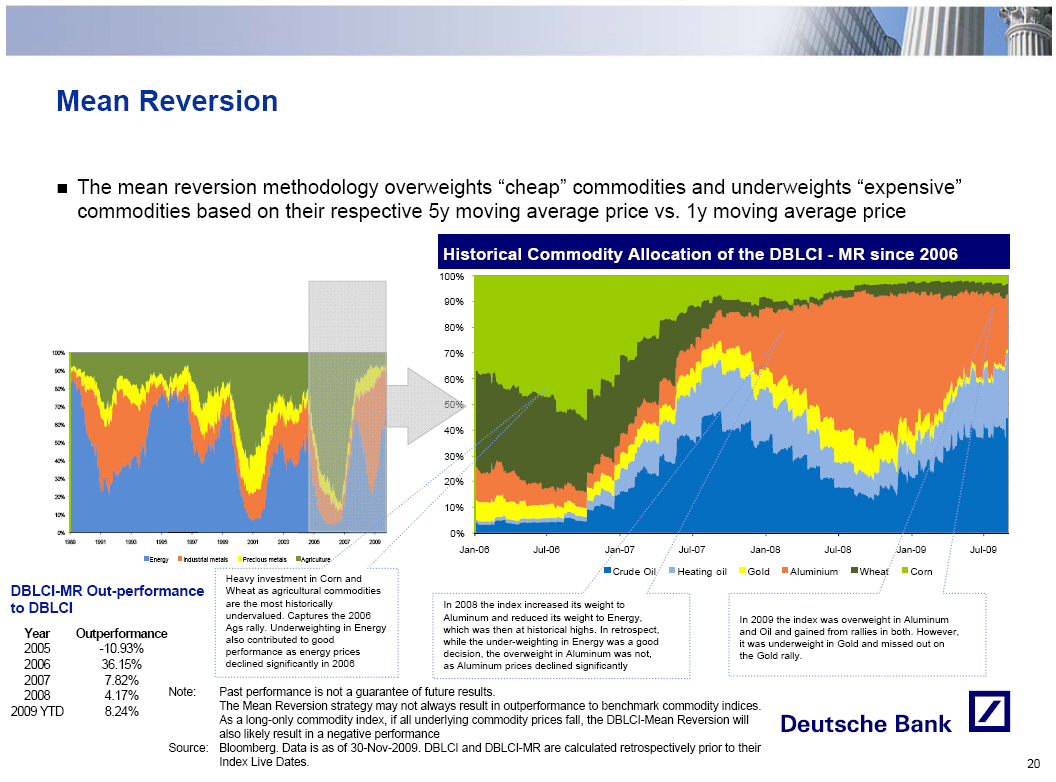

Mean Reversion

o The mean reversion methodology overweights "cheap" commodities and

underweights "expensive" commodities based on their respective 5y moving

average price vs. 1y moving average price

[GRAPHIC OMITTED]

Historical Commodity Allocation of the DBLCI - MR since 2006

[GRAPHIC OMITTED]

DBLCI-MR Out-performance

to DBLCI

Year Outperformance

2005 -10.93%

2006 36.15%

2007 7.82%

Heavy investment in Corn and Wheat as agricultural commodities are the most

historically undervalued. Captures the 2006 Ags rally. Underweighting in Energy

also contributed to good performance as energy prices declined significantly in

2006

In 2008 the index increased its weight to Aluminum and reduced its weight to

Energy, which was then at historical highs. In retrospect, while the

under-weighting in Energy was a good decision, the overweight in Aluminum was

not, as Aluminum prices declined significantly

In 2009 the index was overweight in Aluminum and Oil and gained from rallies in

both. However, it was underweight in Gold and missed out on the Gold rally.

Note:

Past performance is not a guarantee of future results. The Mean Reversion

strategy may not always result in outperformance to benchmark commodity indices.

As a long-only commodity index, if all underlying commodity prices fall, the

DBLCI-Mean Reversion will also likely result in a negative performance

Source:

Bloomberg. Data is as of 30-Nov-2009. DBLCI and DBLCI-MR are calculated

retrospectively prior to their Index Live Dates.

20

|

|

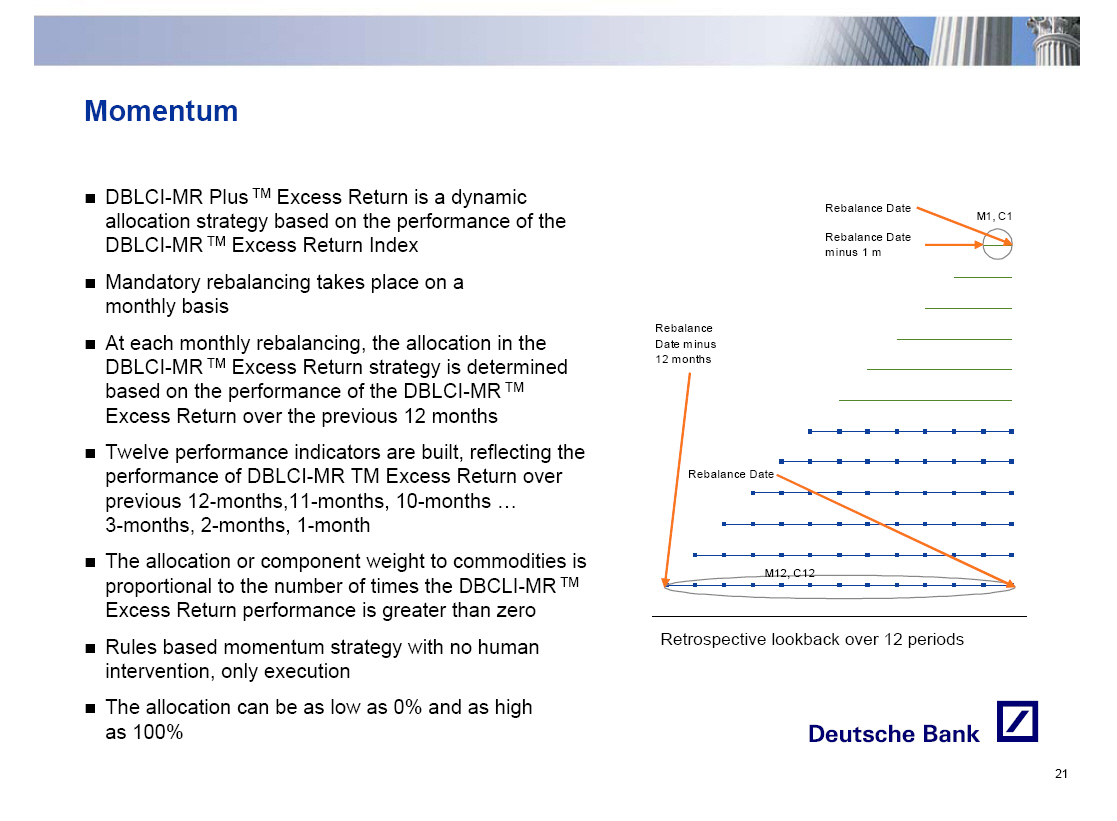

Momentum

o DBLCI-MR Plus TM Excess Return is a dynamic allocation strategy based on

the performance of the DBLCI-MR TM Excess Return Index

o Mandatory rebalancing takes place on a monthly basis

o At each monthly rebalancing, the allocation in the DBLCI-MR TM Excess

Return strategy is determined based on the performance of the DBLCI-MR TM

Excess Return over the previous 12 months

o Twelve performance indicators are built, reflecting the performance of

DBLCI-MR TM Excess Return over previous 12-months,11-months, 10-months ...

3-months, 2-months, 1-month

o The allocation or component weight to commodities is proportional to the

number of times the DBCLI-MR TM Excess Return performance is greater than

zero

o Rules based momentum strategy with no human intervention, only execution

o The allocation can be as low as 0% and as high as 100%

[GRAPHIC OMITTED]

21

|

|

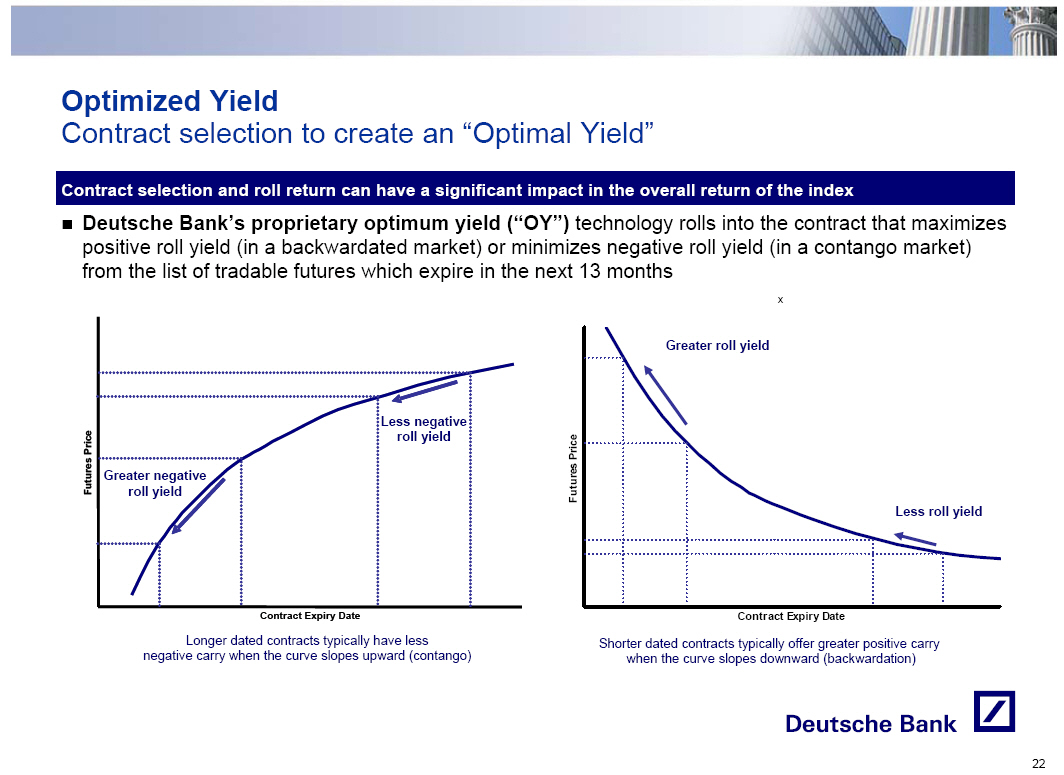

Optimized Yield

Contract selection to create an "Optimum Yield"

Contract selection and roll return can have a significant impact in the overall

return of the index

o Deutsche Bank's proprietary optimum yield ("OY") technology rolls into the

contract that maximizes positive roll yield (in a backwardated market) or

minimizes negative roll yield (in a contango market) from the list of

tradable futures which expire in the next 13 months

[GRAPHIC OMITTED]

Longer dated contracts typically have less negative carry when the curve slopes

upward (contango)

[GRAPHIC OMITTED]

Shorter dated contracts typically offer greater positive carry when the curve

slopes downward (backwardation)

22

|

|

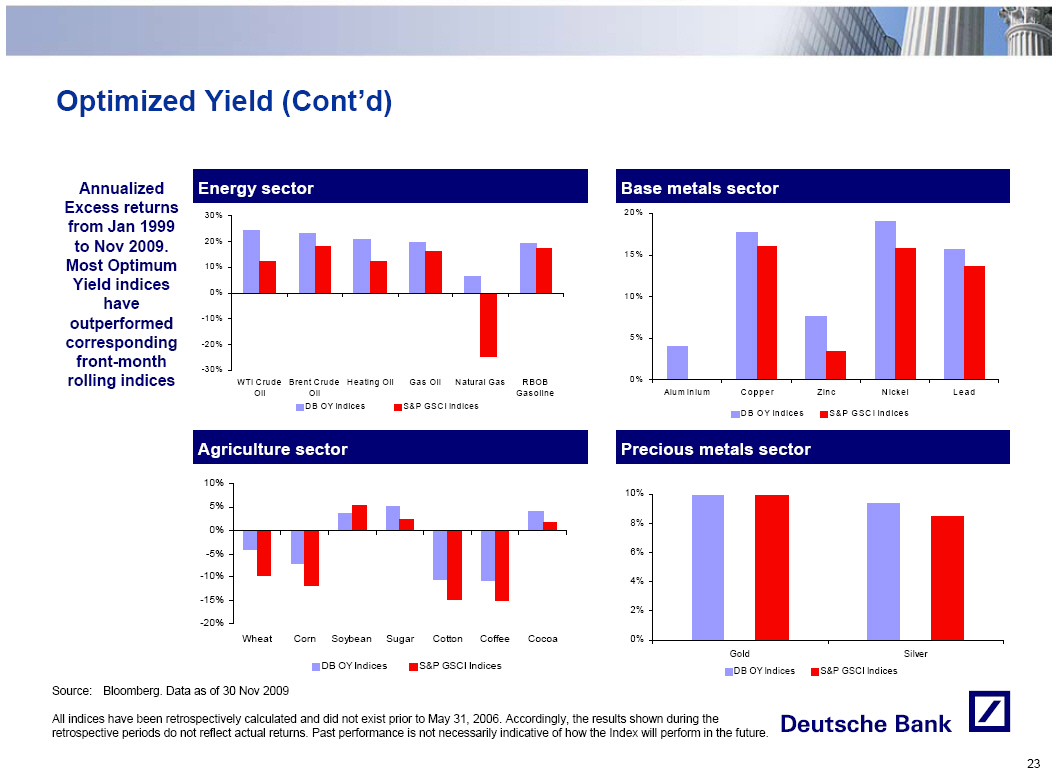

Optimized Yield (Cont'd)

Annualized Excess returns from Jan 1999 to Nov 2009. Most Optimum Yield indices

have outperformed corresponding front-month rolling indices

Energy sector

[GRAPHIC OMITTED]

Base metals sector

[GRAPHIC OMITTED]

Agriculture sector

[GRAPHIC OMITTED]

Precious metals sector

[GRAPHIC OMITTED]

Source: Bloomberg. Data as of 30 Nov 2009

All indices have been retrospectively calculated and did not exist prior to May

31, 2006. Accordingly, the results shown during the retrospective periods do not

reflect actual returns. Past performance is not necessarily indicative of how

the Index will perform in the future.

23

|

|

Optimized Yield

Available Indices

Commodity Contract Expiry Date Bloomberg Ticker

Energy

WTI crude oil 22-Jun-10 DBLCOCLE Index

Brent crude oil 15-Sep-10 DBLCYECO Index

Heating oil 28-May-10 DBLCOHOE Index

RBOB gasoline 29-Oct-10 DBLCYERB Index

Gasoil 12-Jul-10 DBLCYEGO Index

Natural gas 27-Aug-10 DBLCYENG Index

Base Metals

Aluminum 17-Nov-10 DBLCOALE Index

Copper 17-Mar-10 DBLCYECU Index

Zinc 19-May-10 DBLCYEZN Index

Nickel 18-Aug-10 DBLCYENI Index

Lead 18-Aug-10 DBLCYEPB Index

Precious Metals

Gold 28-Apr-10 DBLCOGCE Index

Silver 28-Dec-10 DBLCYESI Index

Agriculture

Wheat 14-Jul-10 DBLCOWTE Index

Kansas Wheat 14-Jul-10 DBLCYEKW Index

Corn 14-Dec-10 DBLCOCNE Index

Soybean 12-Nov-10 DBLCYESS Index

Cotton 7-Oct-10 DBLCYECE Index

Sugar 30-Jun-10 DBLCYESB Index

Coffee 19-Mar-10 DBLCYEKC Index

Cocoa 16-Mar-10 DBLCYECC Index

Source: DBIQ, Data as of 30-Nov-2009

Bloomberg Tickers shown are for Excess Return version of the indices

24

|

|

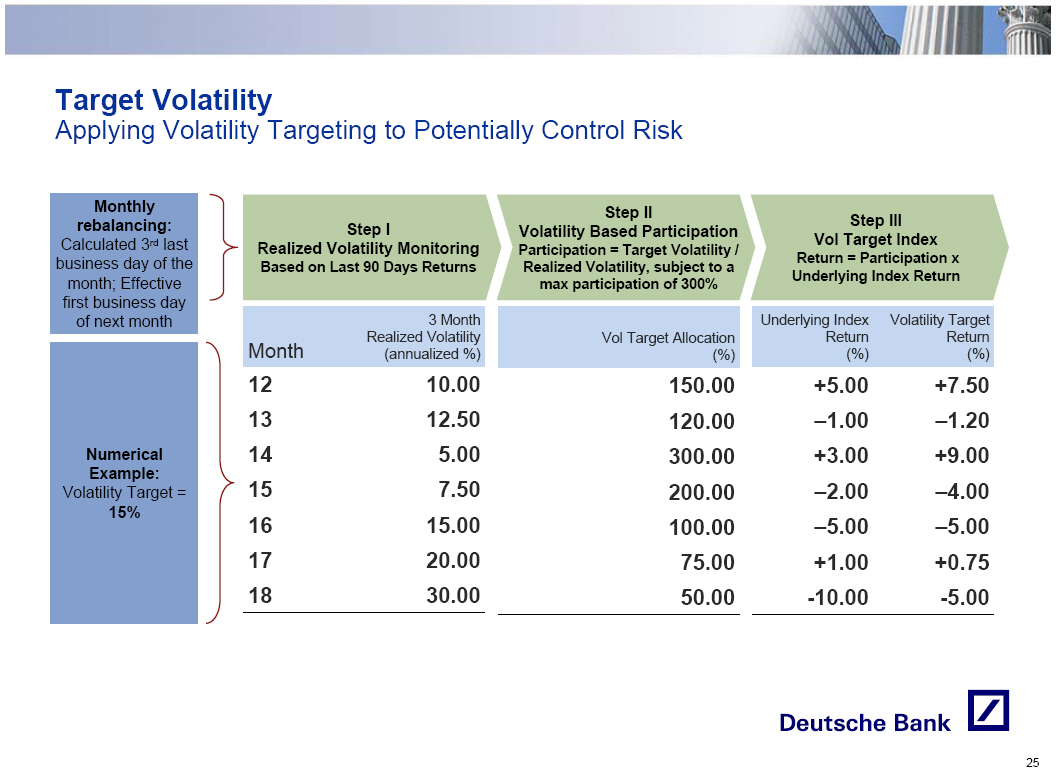

Target Volatility

Applying Volatility Targeting to Potentially Control Risk

Monthly

rebalancing: Step I

Calculated 3rd last Realized Volatility Monitoring

business day of the Based on Last 90 Days Returns

month; Effective

first business day 3 Month

of next month Month Realized Volatility

(annualized %)

12 10.00

13 12.50

Numerical 14 5.00

Example: 15 7.50

Volatility Target = 15% 16 15.00

17 20.00

18 30.00

------------------------------------------

Step II Step III

Volatility Based Participation Vol Target Index

Participation = Target Volatility / Return = Participation x

Realized Volatility, subject to a Underlying Index Return

max participation of 300% Underlying Index Volatility Target

Vol Target Allocation Return Return

(%) (%) (%)

150.00 +5.00 +7.50

120.00 -1.00 -1.20

300.00 +3.00 +9.00

200.00 -2.00 -4.00

100.00 -5.00 -5.00

75.00 +1.00 +0.75

50.00 -10.00 -5.00

- ---------------------------------- ------------------------------------------

25

|

|

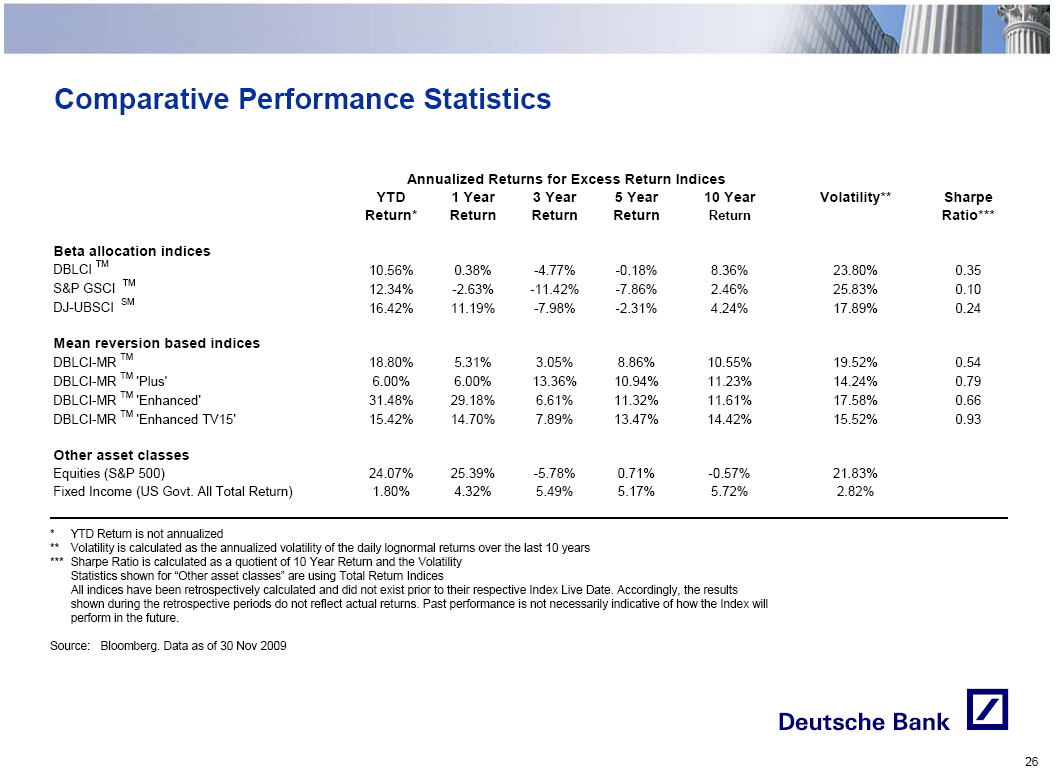

Comparative Performance Statistics

Annualized Returns for Excess Return Indices

YTD 1 Year 3 Year 5 Year 10 Year Volatility** Sharpe

Return* Return Return Return Return Ratio***

Beta allocation indices

DBLCI TM TM 10.56% 0.38% -4.77% -0.18% 8.36% 23.80% 0.35

S&P GSCI 12.34% -2.63% -11.42% -7.86% 2.46% 25.83% 0.10

SM

DJ-UBSCI 16.42% 11.19% -7.98% -2.31% 4.24% 17.89% 0.24

Mean reversion based indices

DBLCI-MR TM 18.80% 5.31% 3.05% 8.86% 10.55% 19.52% 0.54

DBLCI-MR TM 'Plus' 6.00% 6.00% 13.36% 10.94% 11.23% 14.24% 0.79

DBLCI-MR TM 'Enhanced' 31.48% 29.18% 6.61% 11.32% 11.61% 17.58% 0.66

DBLCI-MR TM 'Enhanced TV15' 15.42% 14.70% 7.89% 13.47% 14.42% 15.52% 0.93

Other asset classes

Equities (S&P 500) 24.07% 25.39% -5.78% 0.71% -0.57% 21.83%

Fixed Income (US Govt. All Total Return) 1.80% 4.32% 5.49% 5.17% 5.72% 2.82%

* YTD Return is not annualized

** Volatility is calculated as the annualized volatility of the daily

lognormal returns over the last 10 years

*** Sharpe Ratio is calculated as a quotient of 10 Year Return and the

Volatility Statistics shown for "Other asset classes" are using Total

Return Indices

All indices have been retrospectively calculated and did not exist prior to

their respective Index Live Date. Accordingly, the results shown during the

retrospective periods do not reflect actual returns. Past performance is

not necessarily indicative of how the Index will perform in the future.

Source: Bloomberg. Data as of 30 Nov 2009

26

|

|

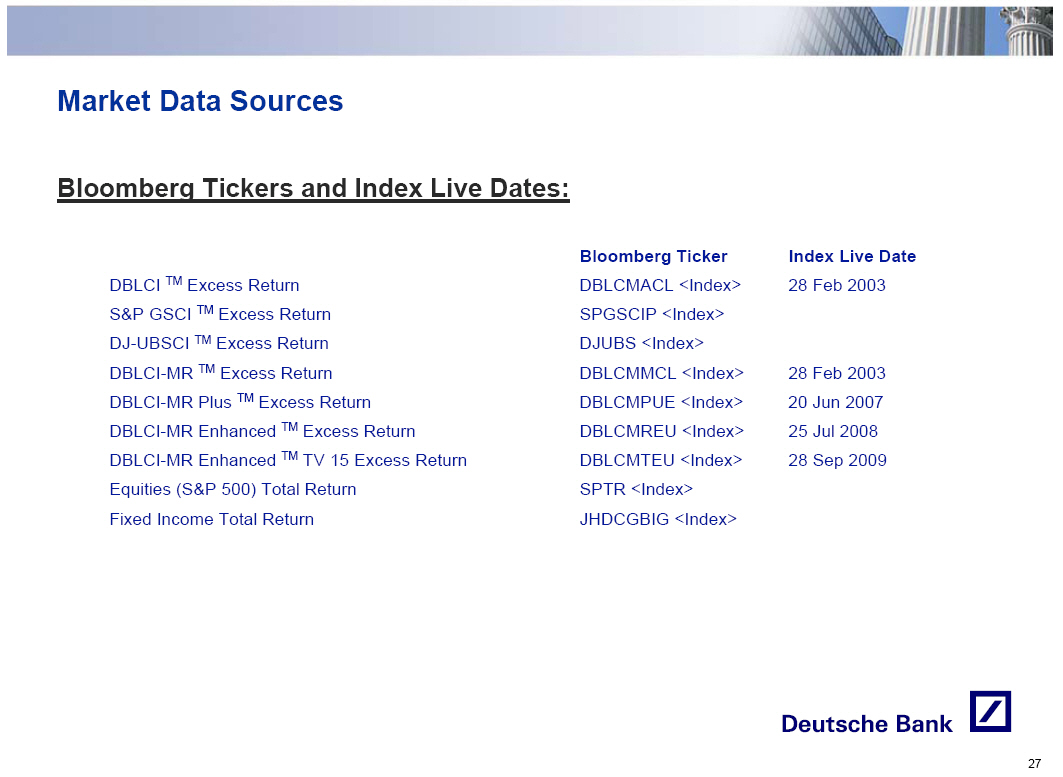

[GRAPHIC OMITTED]

Market Data Sources

Bloomberg Tickers and Index Live Dates:

Bloomberg Ticker Index Live Date

DBLCI TM Excess Return DBLCMACL (Index) 28 Feb 2003

S&P GSCI TM Excess Return SPGSCIP (Index)

DJ-UBSCI TM Excess Return DJUBS (Index)

DBLCI-MR TM Excess Return DBLCMMCL (Index) 28 Feb 2003

DBLCI-MR Plus TM Excess Return DBLCMPUE (Index) 20 Jun 2007

DBLCI-MR Enhanced TM Excess Return DBLCMREU (Index) 25 Jul 2008

DBLCI-MR Enhanced TM TV 15 Excess Return DBLCMTEU (Index) 28 Sep 2009

Equities (S&P 500) Total Return SPTR (Index)

Fixed Income Total Return JHDCGBIG (Index)

27

|

|

Important Considerations

The information contained in this presentation does not provide personal

investment advice. You should consult with independent accounting, tax, legal

and regulatory counsel regarding such matters as they may apply to your

particular circumstances.

Strategy Risk

The Mean Reversion strategy described herein aims to underweight relatively

expensive commodities and overweight relatively inexpensive commodities based on

historical commodity prices. However, indices employing the Mean Reversion

strategy may not be successful in achieving this desired objective.

The Optimal Roll Yield strategy described herein aims to maximize the potential

roll benefits in backwardated markets and minimize potential roll losses in

contango markets by purchasing the relevant new futures contracts that would

generate the maximum implied roll yield. However, indices employing the Optimal

Roll Yield strategy may not be successful in achieving this desired objective.

The Target Volatility strategy described herein aims to achieve a specified

realized volatility in the base index by adjusting the level of participation

based on the historical realized volatility of the base index. However, indices

employing the Target

Volatility strategy may not be successful in achieving this desired objective.

Commodities are speculative and highly volatile, and the risk of loss from

investing in financial instruments linked to commodities or commodity indices

can be substantial.

Past Performance

An index's performance is unpredictable, and past performance is not indicative

of future performance. We give no representation or warranty as to the future

performance of any index or investment.

Some of the indices described herein have very limited performance history.

28

|

|

Important Considerations (Cont'd)

Backtesting

Backtested, hypothetical or simulated performance results discussed herein have

inherent limitations. Unlike an actual historical performances, simulated

results are achieved by means of the retroactive application of a backtested

model itself designed with the benefit of hindsight. Taking into account

historical events, the backtesting of performance also differs from actual

account performance because an actual investment strategy may be adjusted any

time, for any reason, including a response to material, economic or market

factors. The backtested performance includes hypothetical results that do not

reflect the deduction of advisory fees, brokerage or other commissions, and any

other expenses that a client would have paid or actually paid. Past

hypothetical backtest results are neither an indicator nor guarantee of future

returns. Actual results will vary, perhaps materially, from the analysis

contained herein.

Free Writing Prospectus

Deutsche Bank AG has filed a registration statement (including a prospectus)

with the Securities and Exchange Commission, or SEC, for the offering to which

this communication relates. Before you invest, you should read the prospectus in

that registration statement and other documents that Deutsche Bank AG has filed

with the SEC for more complete information about Deutsche Bank AG and only such

offering. You may obtain these documents without cost by visiting EDGAR on the

SEC website at www.sec.gov. Alternatively, Deutsche Bank AG, any agent or any

dealer participating in the offering will arrange to send you the prospectus if

you so request by calling toll-free 1-800-311-4409.

29

|