|

Strictly Private and Confidential

December 2009

Free Writing

Prospectus Filed

Pursuant to Rule 433

Registration

Statement No.

333-162195 Dated

December 18, 2009

Deutsche Bank Commodity Index Enhanced Beta and Alpha Indices

December 2009

|

|

Commodity Indices

Executive Summary

o DB Commodity Booster DJUBS 14 TV Index Excess Return (the "DJUBS Booster TV

14") DB Commodity Harvest

o 10 Index USD Total Return (the "DB Commodity Harvest TV 10")

Appendix

o Types of Returns in a Commodity Index

o Optimized Yield

o Target Volatility

o Comparative Statistics

o Market Data Sources

o Available Optimized Yield Indices

o Important Considerations

2

|

|

Executive Summary

The Evolution of Commodity Markets

o Commodities are an asset class in their own right and exhibit unique

characteristics such as historically low correlation with traditional asset

classes and a positive correlation with inflation

o An investment in a commodity index is a simple way for investors to gain

exposure to the asset class while insulating them from the mechanics of

rolling futures and posting collateral. This transparent, rule-based roll

mechanism eliminates human intervention

o Deutsche Bank is one of the largest providers of non-benchmark commodity

indices with a comprehensive suite of commodity index products aimed at

enhancing beta returns and extracting market neutral alpha returns in the

commodity space

o As the commodity market has evolved, Deutsche Bank has created new indices

that may benefit from the special features of the asset class

3

|

|

Enhanced Beta and Alpha Indices

OPTIMUM YIELD BASED INDEX

o Since 2003, investors have been drawn to enhanced beta allocation and alpha

strategies using commodity indices. The need for these strategies arises due

to several properties that are unique to the commodities asset class.

o Managing Roll Returns: Unlike other asset classes, roll returns form a

significant part of the overall returns in the commodity complex. Most

commodity indices do not react to the changing nature of the commodity term

structure.

- DJUBS Booster TV 14 Index enables investors to replicate the performance

of their commodity benchmark index using Deutsche Bank's proprietary

optimum yield ("OY") indices(1).

ALPHA GENERATING INDEX

o Market Neutral Alpha Returns: The OY methodology enables Deutsche Bank to

create non directional, market neutral exposure to commodities. This is done

by combining the short exposure to a benchmark commodity index with an

equivalent long exposure through replication of that index using the OY

methodology.

- The DB Commodity Harvest TV 10 Index is designed to provide market

neutral stable returns at a controlled volatility level.

Note:

1 Please see Appendix for a brief explanation of the roll return.

4

|

|

DB Commodity Booster DJUBS 14 TV Index

Excess Return (ER)

Index Summary

Key Features

o Composition of DJUBS Booster Index: The DJUBS Booster Index has the same

base weights as the DJUBS Index.

o Optimizing Roll Returns: The DJUBS Booster Index employs Deutsche Bank's

proprietary optimum yield ("OY") technology, which rolls an expiring

contract into the contract that maximizes positive roll yield (in a

backwardated market) or minimizes negative roll yield (in a contango market)

from the list of tradable futures which expire in the next 13 months.

o Target Volatility: The DJUBS Booster TV 14 Index varies its participation in

the DJUBS Booster Index with a view to target a volatility of 14%.

o Transparency: The DJUBS Booster TV 14 is a rules-based index with the

closing level and weights published daily on Bloomberg (DBCMBTVE) and DBIQ.

5

|

|

DB COMMODITY BOOSTER DJUBS 14 TV INDEX EXCESS RETURN

INDEX CONSTRUCTION

Index replicates the DJUBS Index by using DBLCI-OY sub-indices, thereby

providing similar commodity exposure with the benefit of managing roll returns

more effectively

DJUBS Booster TV 14

Apply Target Volatility Technology

o Volatility is targeted at 14% by providing variable exposure to the DJUBS

Booster Index

DJUBS Booster

Apply Optimum Yield Technology

o Optimize roll returns by attempting to invest in contracts with the

highest implied roll yield

DJUBS

Precious Industrial Agriculture &

Livestock

Energy (33%) Metals (10.75%) Metals (20.33%) (35.92%)

6

|

|

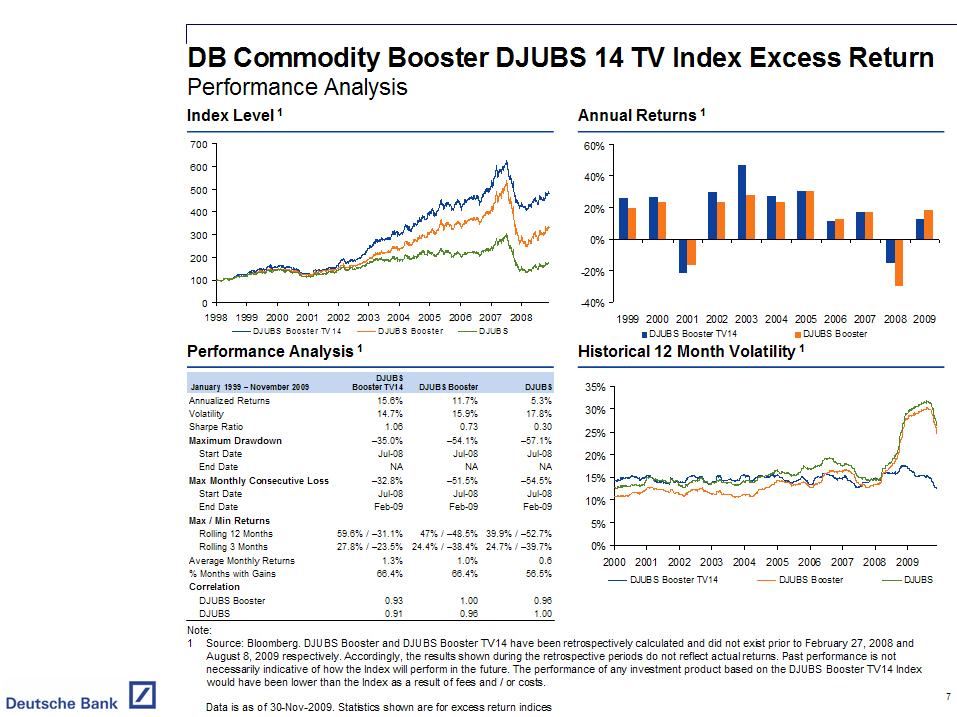

DB Commodity Booster DJUBS 14 TV Index Excess Return

Performance Analysis

Index Level (1) Annual Returns (1)

700 60%

600 40%

500

400 20%

300 0%

200

20%

100

0 40%

1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

DJUBS Booster TV14 DJUBS BoosterDJUBS DJUBS Booster TV14DJUBS Booster

Performance Analysis (1) Historical 12 Month Volatility (1)

DJUBS 35%

January 1999 - November Booster

2009 TV14DJUBS Booster DJUBS

Annualized Returns 15.6% 11.7% 5.3% 30%

Volatility 14.7% 15.9% 17.8%

Sharpe Ratio 1.06 0.73 0.30 25%

Maximum Drawdown -35.0% -54.1% -57.1%

Start Date Jul-08 Jul-08 Jul-08 20%

End Date NA NA NA 15%

Max Monthly Consecutive

Loss -32.8% -51.5% -54.5%

Start Date Jul-08 Jul-08 Jul-08 10%

End Date Feb-09 Feb-09 Feb-09

Max / Min Returns 5%

Rolling 12 Months 59.6% / -31.1% 47% / -48.5% 39.9% / -52.7% 0%

7.8% / -23.5% 24.4% /

Rolling 3 Months 2 -38.4% 24.7% / -39.7%

Average Monthly Returns 1.3% 1.0% 0.6 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

% Months with Gains 66.4% 66.4% 56.5% DJUBS Booster TV14DJUBS Booster DJUBS

Correlation

DJUBS Booster 0.93 1.00 0.96

DJUBS 0.91 0.96 1.00

Note:

1 Source: Bloomberg. DJUBS Booster and DJUBS Booster TV14 have been retrospectively calculated and did

not exist prior to February 27, 2008 and August 8, 2009 respectively. Accordingly, the results shown during

the retrospective periods do not reflect actual returns. Past performance is not necessarily indicative of how

the Index will perform in the future. The performance of any investment product based on the DJUBS Booster

TV14 Index would have been lower than the Index as a result of fees and / or costs.

7

Data is as of 30-Nov-2009. Statistics shown are for excess return indices

|

|

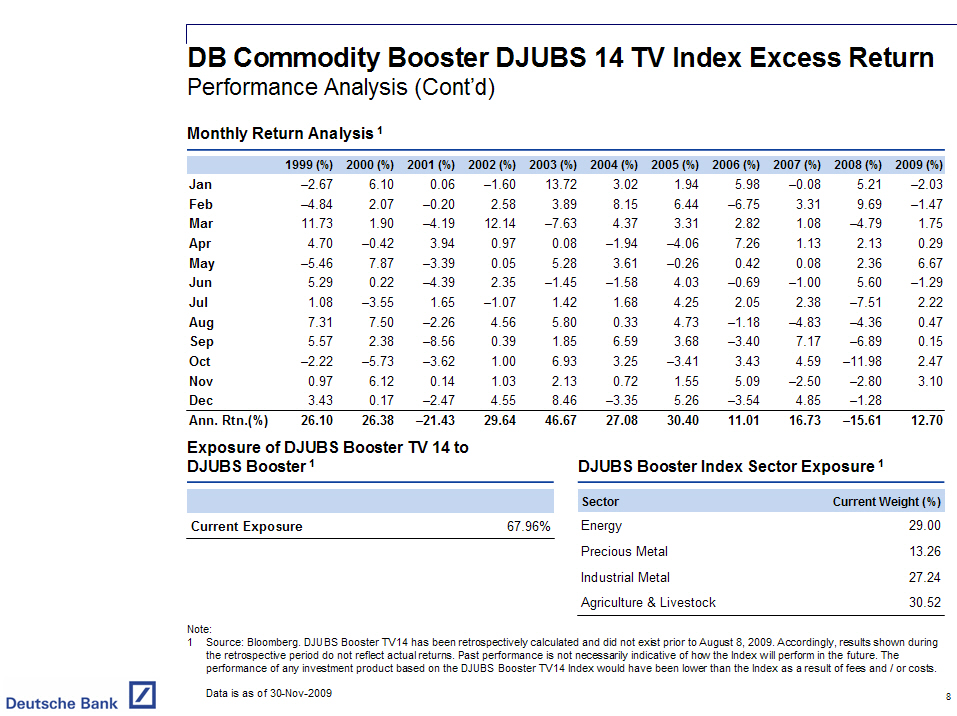

DB Commodity Booster DJUBS 14 TV Index Excess Return

Performance Analysis (Cont'd)

Monthly Return Analysis (1)

1999 (%) 2000 (%) 2001 (%) 2002 (%) 2003 (%) 2004 (%) 2005 (%) 2006 (%) 2007 (%) 2008 (%) 2009 (%)

Jan -2.67 6.10 0.06 -1.60 13.72 3.02 1.94 5.98 -0.08 5.21 -2.03

Feb -4.84 2.07 -0.20 2.58 3.89 8.15 6.44 -6.75 3.31 9.69 -1.47

Mar 11.73 1.90 -4.19 12.14 -7.63 4.37 3.31 2.82 1.08 -4.79 1.75

Apr 4.70 -0.42 3.94 0.97 0.08 -1.94 -4.06 7.26 1.13 2.13 0.29

May -5.46 7.87 -3.39 0.05 5.28 3.61 -0.26 0.42 0.08 2.36 6.67

Jun 5.29 0.22 -4.39 2.35 -1.45 -1.58 4.03 -0.69 -1.00 5.60 -1.29

Jul 1.08 -3.55 1.65 -1.07 1.42 1.68 4.25 2.05 2.38 -7.51 2.22

Aug 7.31 7.50 -2.26 4.56 5.80 0.33 4.73 -1.18 -4.83 -4.36 0.47

Sep 5.57 2.38 -8.56 0.39 1.85 6.59 3.68 -3.40 7.17 -6.89 0.15

Oct -2.22 -5.73 -3.62 1.00 6.93 3.25 -3.41 3.43 4.59 -11.98 2.47

Nov 0.97 6.12 0.14 1.03 2.13 0.72 1.55 5.09 -2.50 -2.80 3.10

Dec 3.43 0.17 -2.47 4.55 8.46 -3.35 5.26 -3.54 4.85 -1.28

- -----------------------------------------------------------------------------------------------------------------------------------

Ann. Rtn.(%) 26.10 26.38 -21.43 29.64 46.67 27.08 30.40 11.01 16.73 -15.61 12.70

Exposure of DJUBS Booster TV 14 to

DJUBS Booster (1) DJUBS Booster Index Sector Exposure (1)

- --------------------------------------------------------------------- -----------------------------------------------

Sector Current Weight (%)

Current Exposure 67.96% Energy 29.00

- --------------------------------------------------------------------- Precious Metal 13.26

Industrial Metal 27.24

Agriculture & Livestock 30.52

Note:

1 Source: Bloomberg. DJUBS Booster TV14 has been retrospectively calculated and did not exist prior to

August 8, 2009. Accordingly, results shown during the retrospective period do not reflect actual returns. Past

performance is not necessarily indicative of how the Index will perform in the future. The performance of any

investment product based on the DJUBS Booster TV14 Index would have been lower than the Index as a result of

fees and / or costs.

Data is as of 30-Nov-2009

8

|

|

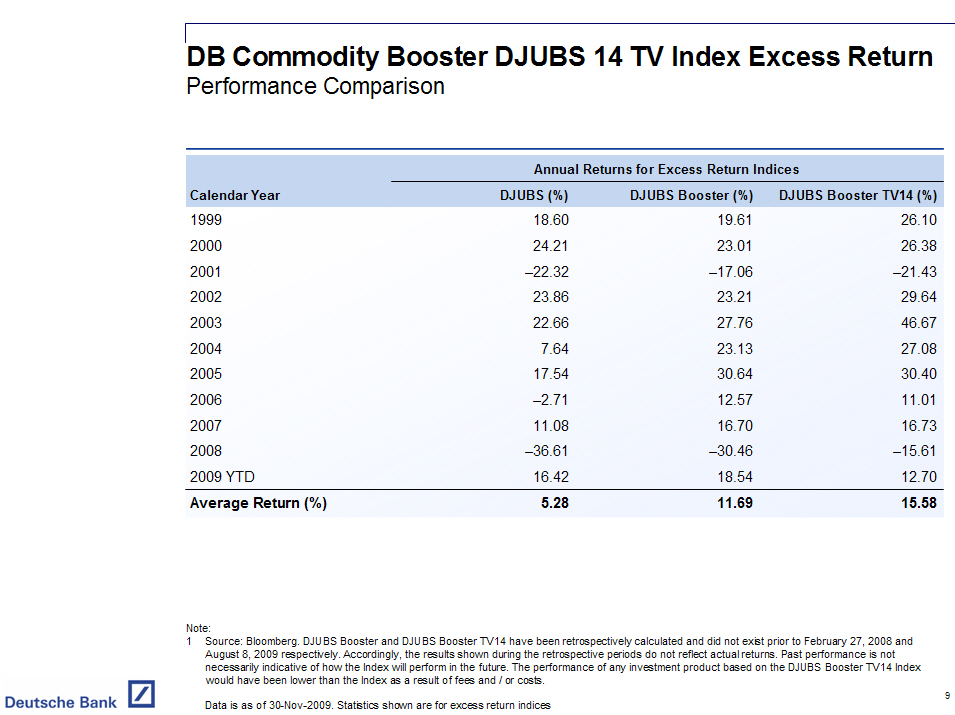

DB Commodity Booster DJUBS 14 TV Index Excess Return

Performance Comparison

Annual Returns for Excess Return Indices

---------------------------------------------------------------------------------

Calendar Year DJUBS (%) DJUBS Booster (%) DJUBS Booster TV14 (%)

1999 18.60 19.61 26.10

2000 24.21 23.01 26.38

2001 -22.32 -17.06 -21.43

2002 23.86 23.21 29.64

2003 22.66 27.76 46.67

2004 7.64 23.13 27.08

2005 17.54 30.64 30.40

2006 -2.71 12.57 11.01

2007 11.08 16.70 16.73

2008 -36.61 -30.46 -15.61

2009 YTD 16.42 18.54 12.70

- ------------------------------------------------------------------------------------------------------------------

Average Return (%) 5.28 11.69 15.58

Note:

1 Source: Bloomberg. DJUBS Booster and DJUBS Booster TV14 have been retrospectively calculated and did

not exist prior to February 27, 2008 and August 8, 2009 respectively. Accordingly, the results shown during

the retrospective periods do not reflect actual returns. Past performance is not necessarily indicative of how

the Index will perform in the future. The performance of any investment product based on the DJUBS Booster

TV14 Index would have been lower than the Index as a result of fees and / or costs.

Data is as of 30-Nov-2009. Statistics shown are for excess return indices

9

|

|

Excess Return vs. Total Return Indices

o The DB Commodity Booster DJUBS 14 TV Index Excess Return is an "Excess

Return" Index. An Excess Return Index has two sources of return:

- Movements in Spot Prices, and

- Roll Returns: Commodity indices are made up of futures contracts, and

the method in which these contracts are bought and sold as contracts

approach expiry is called "Rolling". Depending on the prices in the

futures market, there may be gains and losses associated with this

rolling process, known as "roll returns."

o The DB Commodity Harvest - 10 Index USD Total Return is a "Total Return"

Index. A Total Return Index has three sources of return:

- Movements in Spot Prices: while it is true in general that a Total

Return commodity index would have exposure to movements in commodity

prices, since the DB Commodity Harvest - 10 Index USD Total return is a

long-short index, it is not affected by movements in spot prices. The

gain on the long leg due to movements in spot prices is offset by the

loss on the short leg and vice versa.

- Roll Returns, and

- Collateral Return: 3-month T-bill return earned on notional tied to the

index

10

|

|

DB Commodity Harvest - 10 Index USD Total Return (TR)

Index Summary

Key Features

o Market Neutral Strategy: The DB Commodity Harvest Index goes short the

S&P-GSCI Light Energy Index and long the DB Commodity Booster - Benchmark

Light Energy Index, an Optimum Yield version of the S&P - GSCI Light Energy

Index, in an attempt to provide market-neutral exposure, and to generate

returns from DB's optimum yield technology.

o Optimizing Roll Returns: Deutsche Bank's proprietary optimum yield ("OY")

technology rolls an expiring contract into the contract that maximizes

positive roll yield (in a backwardated market) or minimizes negative roll

yield (in a contango market) from the list of tradable futures which expire

in the next 13 months.

o Target Volatility: The DB Commodity Harvest TV 10 Index varies its

participation in the DB Commodity Harvest Index with a view to target a

volatility of 10%.

o Transparency: The DB Commodity Harvest TV 10 is a rule based index with the

closing level and weights published daily on Bloomberg (DBCMHVEE) and DBIQ.

11

|

|

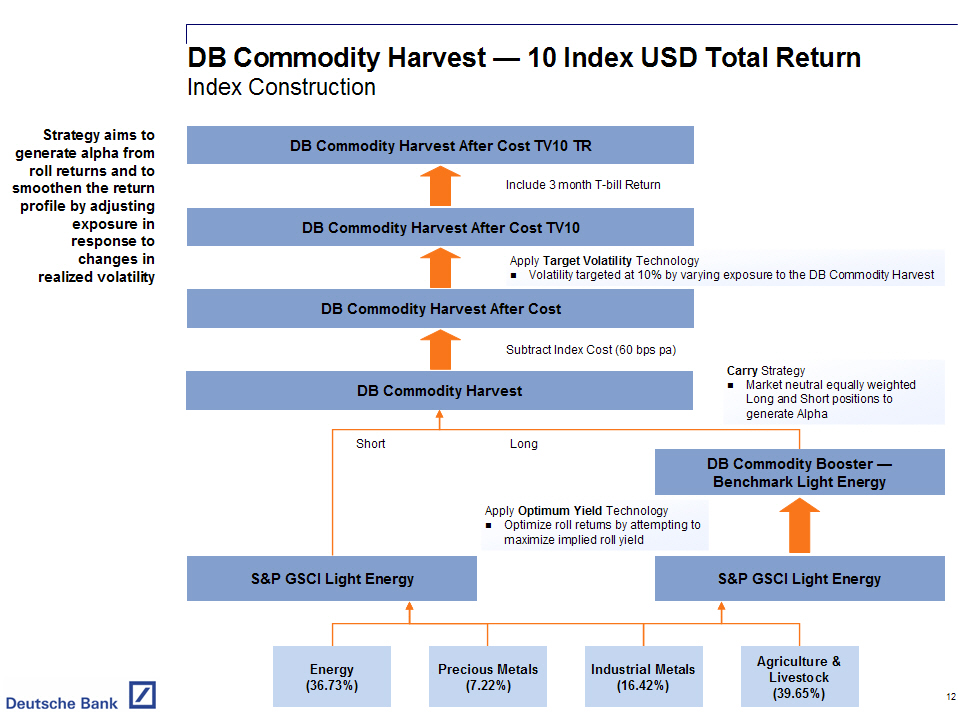

DB Commodity Harvest - 10 Index USD Total Return

Index Construction

Strategy aims to generate alpha from roll returns and to smoothen the return

profile by adjusting exposure in response to changes in realized volatility

DB Commodity Harvest After Cost TV10 TR

Include 3 month T-bill Return

DB Commodity Harvest After Cost TV10

Apply Target Volatility Technology

o Volatility targeted at 10% by varying exposure to the DB Commodity Harvest

DB Commodity Harvest After Cost

Subtract Index Cost (60 bps pa)

DB Commodity Harvest

Short Long

Carry Strategy

o Market neutral equally weighted Long and Short positions to generate Alpha

DB Commodity Booster -

Benchmark Light Energy

Apply Optimum Yield Technology

o Optimize roll returns by attempting to maximize implied roll yield

S&P GSCI Light Energy S&P GSCI Light Energy

Energy Precious Metals Industrial Metals Agriculture &

Livestock

(36.73%) (7.22%) (16.42%) (39.65%)

12

|

|

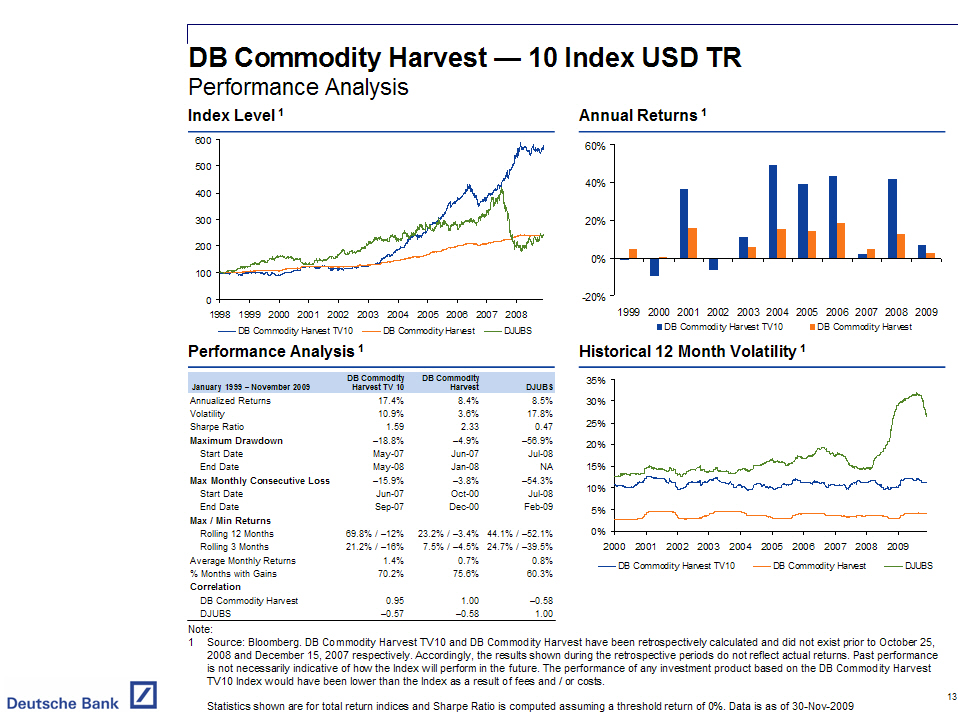

DB Commodity Harvest - 10 Index USD TR

Performance Analysis

Index Level (1)

600

500

400

300

200

100

0

[GRAPHIC OMITTED]

1998 1999 2000 2001 2005 2006

2002 2003 2004 2007 2008

DB Commodity Harvest DB Commodity

TV10 Harvest DJUBS

----- ----- ----

Performance Analysis (1)

- ---------------------------------------------------------------------

DB Commodity DB Commodity

January 1999 - November 2009 Harvest TV 10 Harvest DJUBS

Annualized Returns 17.4% 8.4% 8.5%

Volatility 10.9% 3.6% 17.8%

Sharpe Ratio 1.59 2.33 0.47

Maximum Drawdown -18.8% -4.9% -56.9%

Start Date May-07 Jun-07 Jul-08

End Date May-08 Jan-08 NA

Max Monthly Consecutive Loss -15.9% -3.8% -54.3%

Start Date Jun-07 Oct-00 Jul-08

End Date Sep-07 Dec-00 Feb-09

Max / Min Returns

3.2% / -3.4% 44.1% /

Rolling 12 Months 69.8% / -12%2 -52.1%

24.7% /

Rolling 3 Months 21.2% / -16% 7.5% / -4.5% -39.5%

Average Monthly Returns 1.4% 0.7% 0.8%

% Months with Gains 70.2% 75.6% 60.3%

Correlation

DB Commodity Harvest 0.95 1.00 -0.58

DJUBS -0.57 -0.58 1.00

- ---------------------------------------------------------------------

Note:

Annual Returns (1)

60%

40%

20%

0%

-20%

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

DB Commodity Harvest TV10DB Commodity Harvest

Historical 12 Month Volatility (1)

35%

30%

25%

20%

15%

10%

5%

0%

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

DB Commodity Harvest B Commodity Harvest JUBS

TV10 D D

----- ----- -----

1 Source: Bloomberg. DB Commodity Harvest TV10 and DB Commodity Harvest have been retrospectively

calculated and did not exist prior to October 25, 2008 and December 15, 2007 respectively. Accordingly, the

results shown during the retrospective periods do not reflect actual returns. Past performance is not

necessarily indicative of how the Index will perform in the future. The performance of any investment product

based on the DB Commodity Harvest TV10 Index would have been lower than the Index as a result of fees and / or

costs.

13

Statistics shown are for total return indices and Sharpe Ratio is computed assuming a threshold return of 0%.

Data is as of 30-Nov-2009

|

|

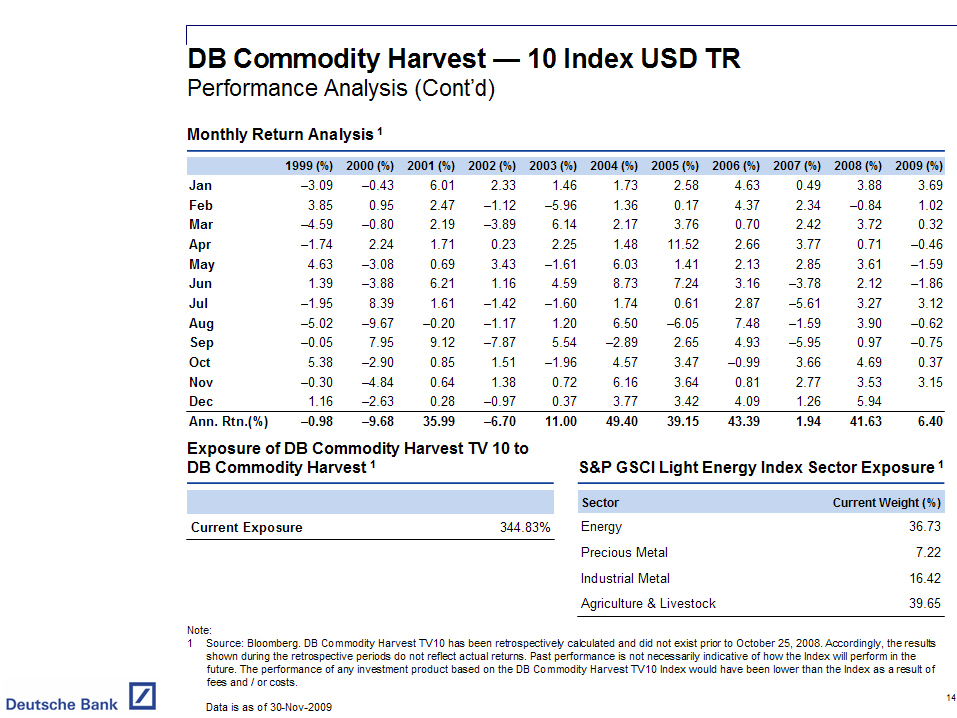

DB Commodity Harvest - 10 Index USD TR

Performance Analysis (Cont'd)

Monthly Return Analysis (1)

[GRAPHIC OMITTED]

999 (%) 2000 (%) 2001 (%) 2002 (%) 2003 (%) 2004 (%) 2005 (%) 2006 (%) 2007 (%) 2008 (%) 2009 (%)

Jan -3.09 -0.43 6.01 2.33 1.46 1.73 2.58 4.63 0.49 3.88 3.69

Feb 3.85 0.95 2.47 -1.12 -5.96 1.36 0.17 4.37 2.34 -0.84 1.02

Mar -4.59 -0.80 2.19 -3.89 6.14 2.17 3.76 0.70 2.42 3.72 0.32

Apr -1.74 2.24 1.71 0.23 2.25 1.48 11.52 2.66 3.77 0.71 -0.46

May 4.63 -3.08 0.69 3.43 -1.61 6.03 1.41 2.13 2.85 3.61 -1.59

Jun 1.39 -3.88 6.21 1.16 4.59 8.73 7.24 3.16 -3.78 2.12 -1.86

Jul -1.95 8.39 1.61 -1.42 -1.60 1.74 0.61 2.87 -5.61 3.27 3.12

Aug -5.02 -9.67 -0.20 -1.17 1.20 6.50 -6.05 7.48 -1.59 3.90 -0.62

Sep -0.05 7.95 9.12 -7.87 5.54 -2.89 2.65 4.93 -5.95 0.97 -0.75

Oct 5.38 -2.90 0.85 1.51 -1.96 4.57 3.47 -0.99 3.66 4.69 0.37

Nov -0.30 -4.84 0.64 1.38 0.72 6.16 3.64 0.81 2.77 3.53 3.15

Dec 1.16 -2.63 0.28 -0.97 0.37 3.77 3.42 4.09 1.26 5.94

- ------------------------------------------------------------------------------------------------------------------------------

Ann. Rtn.(%) -0.98 -9.68 35.99 -6.70 11.00 49.40 39.15 43.39 1.94 41.63 6.40

Exposure of DB Commodity Harvest TV 10 to

DB Commodity Harvest (1) S&P GSCI Light Energy Index Sector Exposure (1)

- --------------------------------------------------------------------- ----------------------------------------------------------

Sector Current Weight (%)

Current Exposure 344.83% Energy 36.73

Precious Metal 7.22

- ---------------------------------------------------------------------

Industrial Metal 16.42

Agriculture & Livestock 39.65

Note:

1 Source: Bloomberg. DB Commodity Harvest TV10 has been retrospectively calculated and did not exist

prior to October 25, 2008. Accordingly, the results shown during the retrospective periods do not reflect

actual returns. Past performance is not necessarily indicative of how the Index will perform in the future.

The performance of any investment product based on the DB Commodity Harvest TV10 Index would have been lower

than the Index as a result of fees and / or costs.

14

Data is as of 30-Nov-2009

|

|

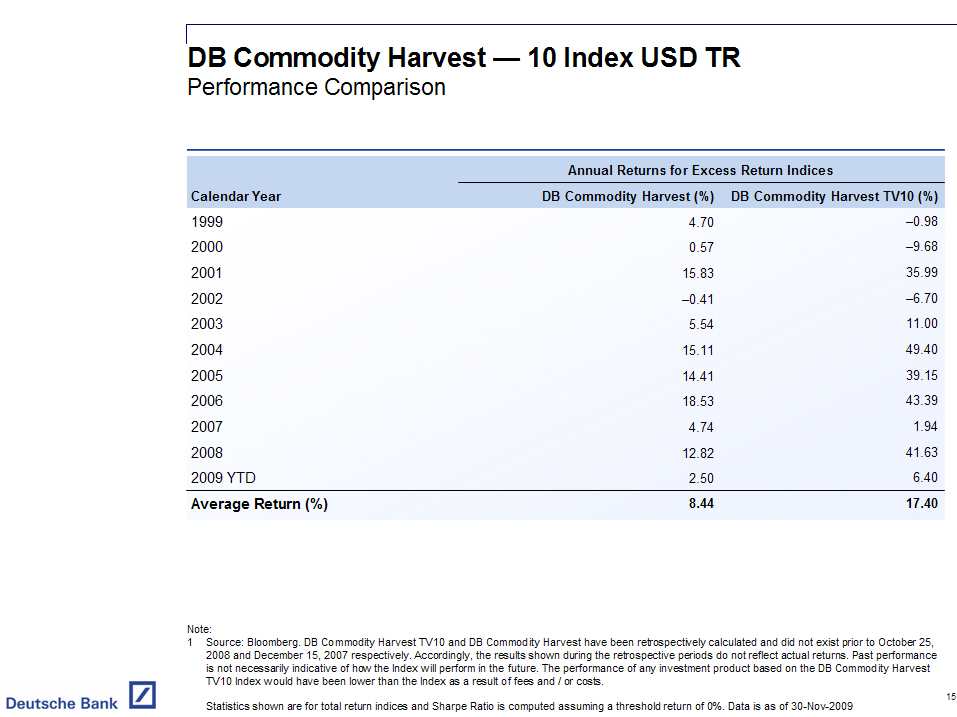

DB Commodity Harvest - 10 Index USD TR

Performance Comparison

Annual Returns for Excess Return Indices

------------------------------------------------------------------------------

------------------------------------------------------------------------------

Calendar Year DB Commodity Harvest (%) DB Commodity Harvest TV10 (%)

1999 4.70 -0.98

2000 0.57 -9.68

2001 15.83 35.99

2002 -0.41 -6.70

2003 5.54 11.00

2004 15.11 49.40

2005 14.41 39.15

2006 18.53 43.39

2007 4.74 1.94

2008 12.82 41.63

2009 YTD 2.50 6.40

- -------------------------------------------------------------------------------------------------------------

Average Return (%) 8.44 17.40

Note:

1 Source: Bloomberg. DB Commodity Harvest TV10 and DB Commodity Harvest have been retrospectively

calculated and did not exist prior to October 25, 2008 and December 15, 2007 respectively. Accordingly, the

results shown during the retrospective periods do not reflect actual returns. Past performance is not

necessarily indicative of how the Index will perform in the future. The performance of any investment product

based on the DB Commodity Harvest TV10 Index would have been lower than the Index as a result of fees and / or

costs.

15

Statistics shown are for total return indices and Sharpe Ratio is computed assuming a threshold return of 0%.

Data is as of 30-Nov-2009

|

| Appendix |

|

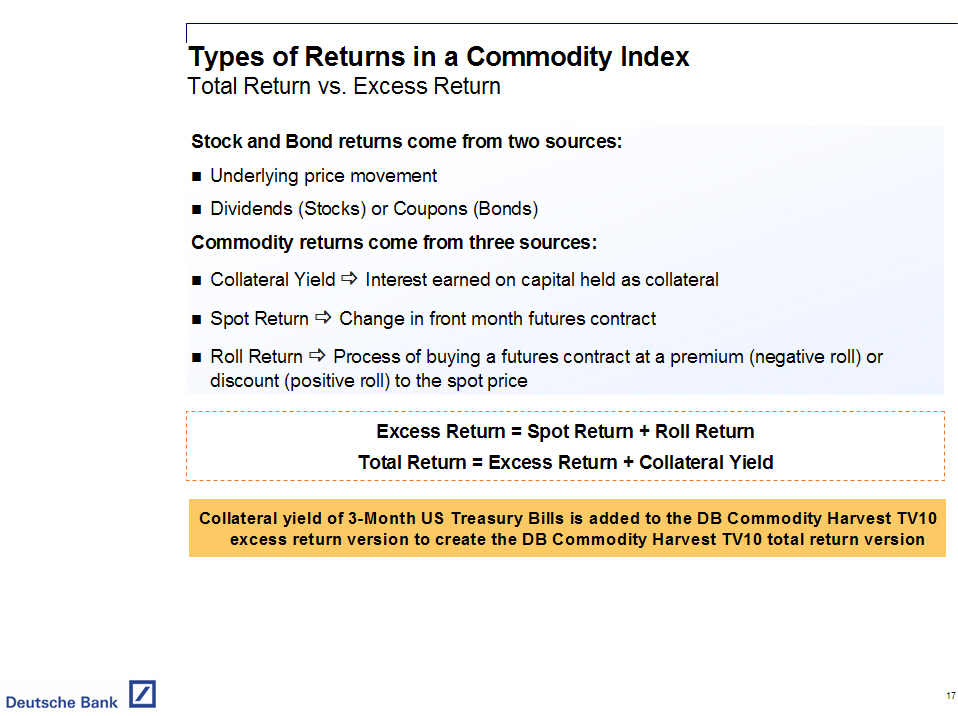

Types of Returns in a Commodity Index

Total Return vs. Excess Return

Stock and Bond returns come from two sources:

o Underlying price movement

o Dividends (Stocks) or Coupons (Bonds)

Commodity returns come from three sources:

o Collateral Yield |X> Interest earned on capital held as collateral

o Spot Return |X> Change in front month futures contract

o Roll Return |X> Process of buying a futures contract at a premium (negative

roll) or discount (positive roll) to the spot price

Excess Return = Spot Return + Roll Return

Total Return = Excess Return + Collateral Yield

Collateral yield of 3-Month US Treasury Bills is added to the DB Commodity Harvest TV10 excess return version

to create the DB Commodity Harvest TV10 total return version

17

|

|

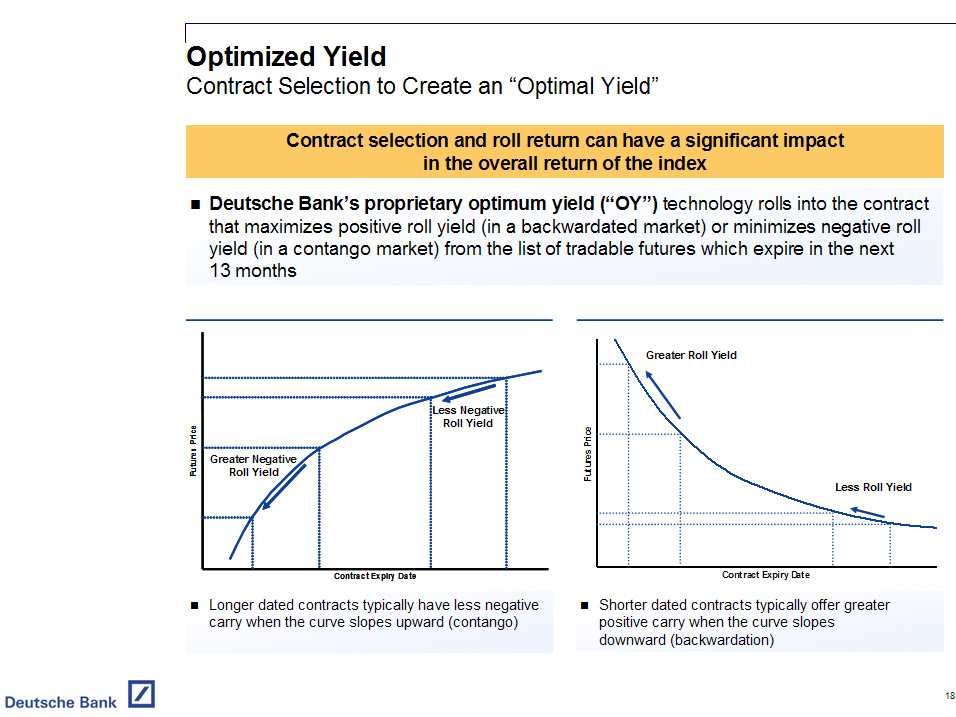

Optimized Yield

Contract Selection to Create an "Optimal Yield"

Contract selection and roll return can have a significant impact in the

overall return of the index

o Deutsche Bank's proprietary optimum yield ("OY") technology rolls into the

contract that maximizes positive roll yield (in a backwardated market) or

minimizes negative roll yield (in a contango market) from the list of

tradable futures which expire in the next 13 months

Greater Roll Yield

Less Negative

Price Roll Yield

Futures Greater Negative

Roll Yield

Futures

Price

Less Roll Yield

Contract Expiry Date

o Longer dated contracts typically have less negative carry when the curve

slopes upward (contango)

Contract Expiry Date

o Shorter dated contracts typically offer greater positive carry when the

curve slopes downward (backwardation)

18

|

|

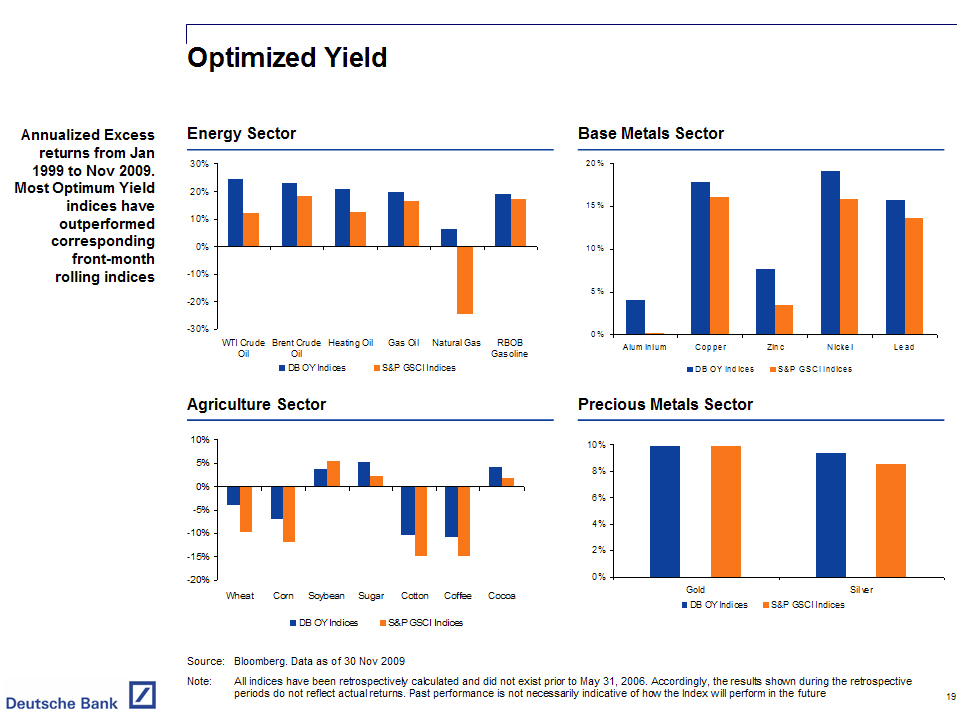

Optimized Yield

Annualized Excess

returns from Jan

Energy Sector Base Metals Sector

1999 to Nov 2009. Most Optimum Yield indices have outperformed corresponding front-month rolling indices

30%

20%

10%

0%

-10%

- -20%

- -30%

rent Heating atural Gas

WTI Crude B Crude Oil Gas Oil N RBOB

Oil Oil Gasoline

DB OY Indices S&P GSCI Indices

Agriculture Sector

- ---------------------------------------------------------------------

10%

5%

0%

-5%

-10%

-15%

-20%

Wheat Corn Soybean Sugar Cotton Coffee Cocoa

20%

15%

10%

5%

0%

Alum inium CopperZinc NickelLead

DB OY Indices S&P GSCI Indices

Precious Metals Sector

- ---------------------------------------------------------------------

10%

8%

6%

4%

2%

0%

--------------------------------------------------------------

Gold Silver

DB OY Indices S&P GSCI Indices

DB OYIndices S&P GSCI Indices

Source: Bloomberg. Data as of 30 Nov 2009

Note: All indices have been retrospectively calculated and did not exist prior to May 31, 2006. Accordingly, the results shown during

the retrospective

periods do not reflect actual returns. Past performance is not necessarily indicative of how the Index will perform in the

future

19

|

|

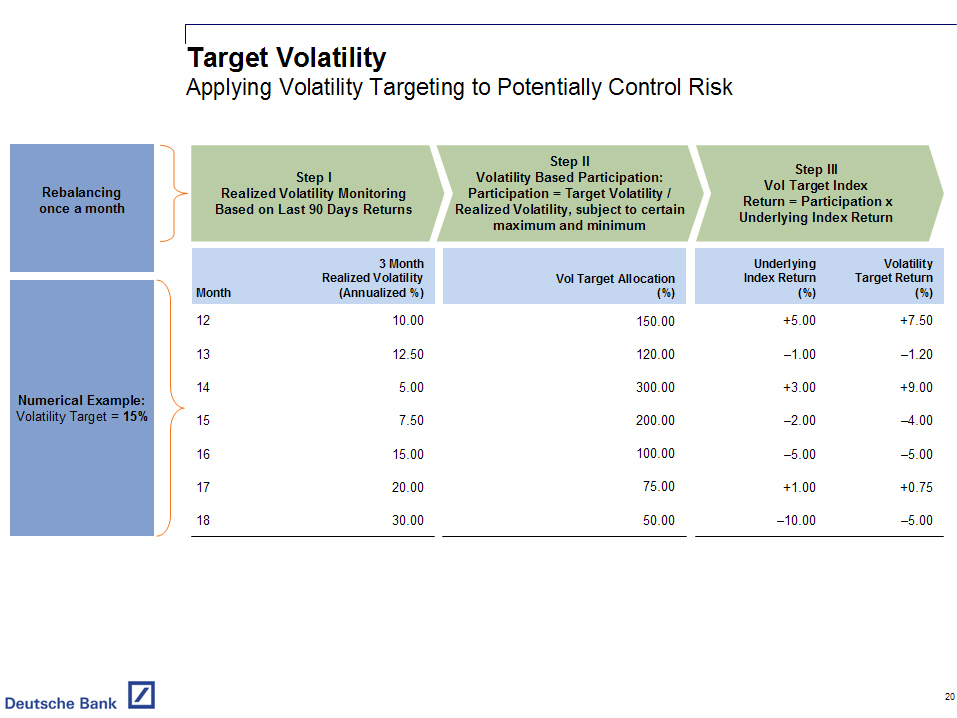

Target Volatility

Applying Volatility Targeting to Potentially Control Risk

Step I Step II Step III

Volatility Based Participation: Vol Target Index

Rebalancing Realized Volatility Monitoring Participation = Target Volatility / Return = Participation x

once a month Based on Last 90 Days Returns Realized Volatility, subject to certain Underlying Index Return

maximum and minimum

3 Month Underlying Volatility

Realized Volatility Vol Target Allocation Index Return Target Return

Month (Annualized %) (%) (%) (%)

12 10.00 150.00 +5.00 +7.50

13 12.50 120.00 -1.00 -1.20

Numerical Example: 14 5.00 300.00 +3.00 +9.00

Volatility Target = 15% 15 7.50 200.00 -2.00 -4.00

16 15.00 100.00 -5.00 -5.00

17 20.00 75.00 +1.00 +0.75

18 30.00 50.00 -10.00 -5.00

20

|

|

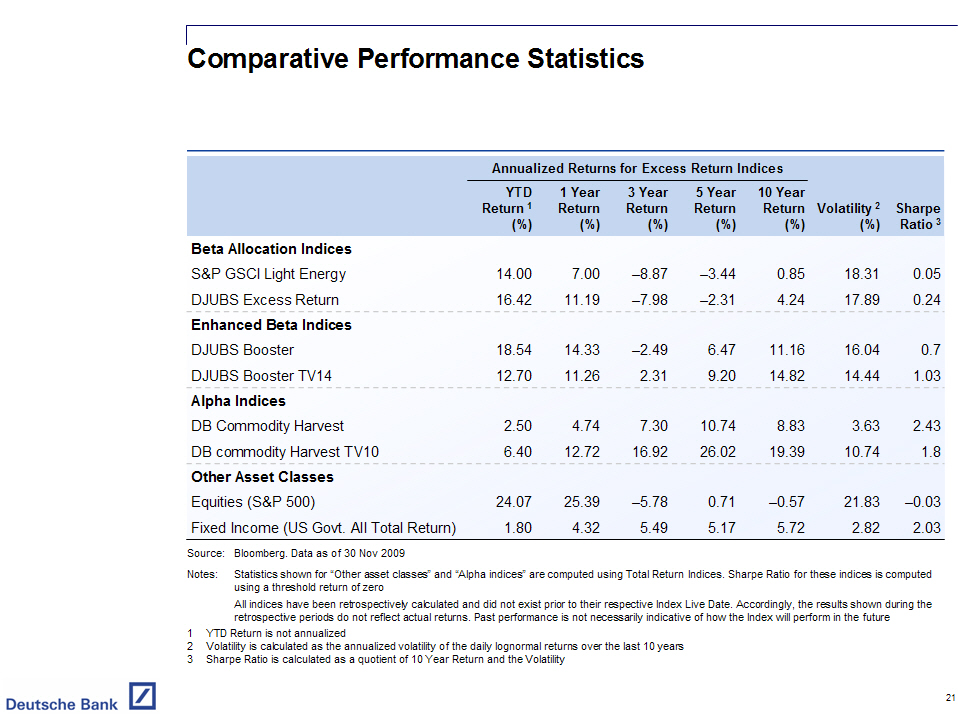

Comparative Performance Statistics

Annualized Returns for Excess Return Indices

-------------------------------------------------------------

YTD 1 Year 3 Year 5 Year 10 Year

Return (1) Return Return Return ReturnVolatility (2) Sharpe

(%) (%) (%) (%) (%) (%) Ratio (3)

Beta Allocation Indices

S&P GSCI Light Energy 14.00 7.00 -8.87 -3.44 0.85 18.31 0.05

DJUBS Excess Return 16.42 11.19 -7.98 -2.31 4.24 17.89 0.24

Enhanced Beta Indices

DJUBS Booster 18.54 14.33 -2.49 6.47 11.16 16.04 0.7

DJUBS Booster TV14 12.70 11.26 2.31 9.20 14.82 14.44 1.03

Alpha Indices

DB Commodity Harvest 2.50 4.74 7.30 10.74 8.83 3.63 2.43

DB commodity Harvest TV10 6.40 12.72 16.92 26.02 19.39 10.74 1.8

Other Asset Classes

Equities (S&P 500) 24.07 25.39 -5.78 0.71 -0.57 21.83 -0.03

Fixed Income (US Govt. All Total Return) 1.80 4.32 5.49 5.17 5.72 2.82 2.03

- ---------------------------------------------------------------------------------------------------------------------------------

Source: Bloomberg. Data as of 30 Nov 2009

Notes: Statistics shown for "Other asset classes" and "Alpha indices" are computed using Total Return

Indices. Sharpe Ratio for these indices is computed using a threshold return of zero

All indices have been retrospectively calculated and did not exist prior to their respective Index

Live Date. Accordingly, the results shown during the retrospective periods do not reflect actual

returns. Past performance is not necessarily indicative of how the Index will perform in the future

1 YTD Return is not annualized

2 Volatility is calculated as the annualized volatility of the daily lognormal returns over the last 10

years

3 Sharpe Ratio is calculated as a quotient of 10 Year Return and the Volatility

21

|

|

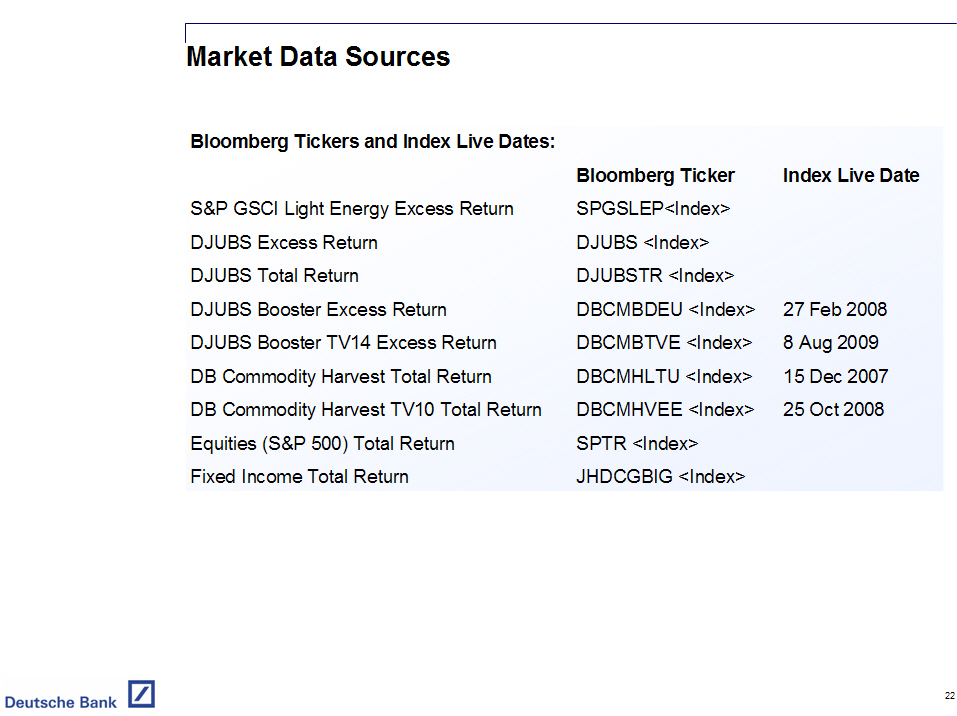

Market Data Sources

Bloomberg Tickers and Index Live Dates:

Bloomberg Ticker Index Live Date

S&P GSCI Light Energy Excess Return SPGSLEP[Index]

DJUBS Excess Return DJUBS [Index]

DJUBS Total Return DJUBSTR [Index]

DJUBS Booster Excess Return DBCMBDEU [Index] 27 Feb 2008

DJUBS Booster TV14 Excess Return DBCMBTVE [Index] 8 Aug 2009

DB Commodity Harvest Total Return DBCMHLTU [Index] 15 Dec 2007

DB Commodity Harvest TV10 Total Return DBCMHVEE [Index] 25 Oct 2008

Equities (S&P 500) Total Return SPTR [Index]

Fixed Income Total Return JHDCGBIG [Index]

22

|

|

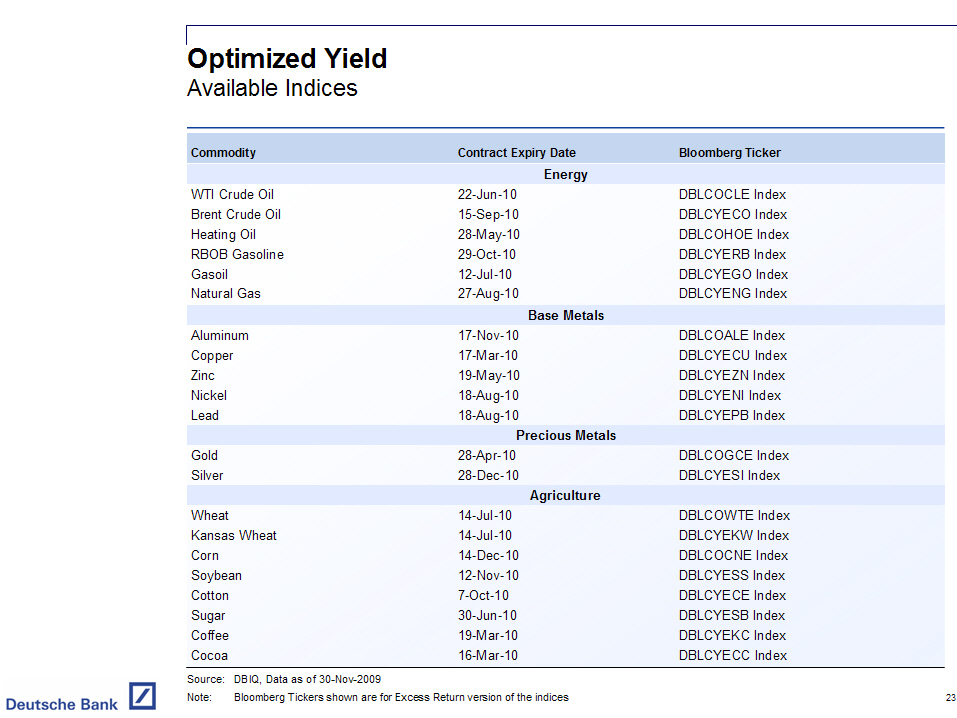

Optimized Yield

Available Indices

Commodity Contract Expiry Date Bloomberg Ticker

Energy

WTI Crude Oil 22-Jun-10 DBLCOCLE Index

Brent Crude Oil 15-Sep-10 DBLCYECO Index

Heating Oil 28-May-10 DBLCOHOE Index

RBOB Gasoline 29-Oct-10 DBLCYERB Index

Gasoil 12-Jul-10 DBLCYEGO Index

Natural Gas 27-Aug-10 DBLCYENG Index

Base Metals

Aluminum 17-Nov-10 DBLCOALE Index

Copper 17-Mar-10 DBLCYECU Index

Zinc 19-May-10 DBLCYEZN Index

Nickel 18-Aug-10 DBLCYENI Index

Lead 18-Aug-10 DBLCYEPB Index

Precious Metals

Gold 28-Apr-10 DBLCOGCE Index

Silver 28-Dec-10 DBLCYESI Index

Agriculture

Wheat 14-Jul-10 DBLCOWTE Index

Kansas Wheat 14-Jul-10 DBLCYEKW Index

Corn 14-Dec-10 DBLCOCNE Index

Soybean 12-Nov-10 DBLCYESS Index

Cotton 7-Oct-10 DBLCYECE Index

Sugar 30-Jun-10 DBLCYESB Index

Coffee 19-Mar-10 DBLCYEKC Index

Cocoa 16-Mar-10 DBLCYECC Index

- ---------------------------------------------------------------------------------------------------

Source: DBIQ, Data as of 30-Nov-2009

Note: Bloomberg Tickers shown are for Excess Return version of the indices

23

|

| Important Considerations The information contained in this presentation does not provide personal investment advice. You should consult with independent accounting, tax, legal and regulatory counsel regarding such matters as they may apply to your particular circumstances. Strategy Risk The DB Commodity Harvest Indices adopt a market neutral strategy by taking a long position in a specified booster index and a short position in a specified benchmark index. However, this market neutral strategy may not be successful, and each index may not be able to achieve its desired objective. The Optimal Roll Yield strategy described herein aims to maximize the potential roll benefits in backwardated markets and minimize potential roll losses in contango markets by purchasing the relevant new futures contracts that would generate the maximum implied roll yield. However, indices employing the Optimal Roll Yield strategy may not be successful in achieving the desired objective. The Target Volatility strategy described herein aims to achieve a specified realized volatility in the base index by adjusting the level of participation based on the historical realized volatility of the base index. However, indices employing the Target Volatility strategy may not be successful in achieving the desired objective. Commodities are speculative and highly volatile and the risk of loss from investing in financial instruments linked to commodities or commodity indices can be substantial. Past Performance An index's performance is unpredictable, and past performance is not indicative of future performance. We give no representation or warranty as to the future performance of any index or investment. Some of the indices described herein have very limited performance history. 24 |

| Important Considerations Backtesting Backtested, hypothetical or simulated performance results discussed herein have inherent limitations. Unlike an actual historical performances, simulated results are achieved by means of the retroactive application of a backtested model itself designed with the benefit of hindsight. Taking into account historical events, the backtesting of performance also differs from actual account performance because an actual investment strategy may be adjusted any time, for any reason, including a response to material, economic or market factors. The backtested performance includes hypothetical results that do not reflect the deduction of advisory fees, brokerage or other commissions, and any other expenses that a client would have paid or actually paid. Past hypothetical backtest results are neither an indicator nor guarantee of future returns. Actual results will vary, perhaps materially, from the analysis contained herein. Free Writing Prospectus Deutsche Bank AG has filed a registration statement (including a prospectus) with the Securities and Exchange Commission, or SEC, for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents that Deutsche Bank AG has filed with the SEC for more complete information about Deutsche Bank AG and any such offering. You may obtain these documents without cost by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, Deutsche Bank AG, any agent or any dealer participating in the offering will arrange to send you the prospectus if you so request by calling toll-free 1-800-311-4409. 25 |

|

Disclaimer

S&P GSCI SM Disclaimer

Any securities Deutsche Bank AG may issue from time to time and this presentation are not sponsored,

endorsed, sold or promoted by Standard & Poor's, a division of The McGraw-Hill Companies, Inc. ("S&P").

Standard & Poor's does not make any representation or warranty, express or implied, to the owners of any

securities or any member of the public regarding the advisability of investing in any securities or the

ability of S&P GSCI Index to track general commodity market performance. S&P's only relationship to

Deutsche Bank AG is the licensing of certain trademarks and trade names of S&P and of S&P GSCI Index,

which indices are determined, composed and calculated by S&P without regard to Deutsche Bank AG or any

securities. S&P has no obligation to take the needs of Deutsche Bank AG or the owners of any securities

into consideration in determining, composing or calculating S&P GSCI Index. S&P is not responsible for and

have not participated in the determination of the timing of, prices at, or quantities of any securities to

be issued or in the determination or calculation of the equation by which the S&P GSCI Index is to be

converted into cash. S&P has no obligation or liability in connection with the administration, marketing

or trading of any securities.

S&P DOES NOT GUARANTEE THE ACCURACY AND / OR THE COMPLETENESS OF S&P GSCI INDEX OR ANY DATA INCLUDED

THEREIN AND S&P SHALL HAVE NO LIABILITY FOR ANY ERRORS, OMISSIONS, OR INTERRUPTIONS THEREIN. S&P MAKES NO

WARRANTY, EXPRESS OR IMPLIED, AS TO RESULTS TO BE OBTAINED BY DEUTSCHE BANK AG, OWNERS OF SECURITIES OR

ANY OTHER PERSON OR ENTITY FROM THE USE OF S&P GSCI INDEX OR ANY DATA INCLUDED THEREIN. S&P MAKES NO

EXPRESS OR IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A

PARTICULAR PURPOSE OR USE WITH RESPECT TO THE S&P INDICES OR DEUTSCHE BANK'S VARIATIONS OF S&P INDICES OR

ANY DATA INCLUDED THEREIN. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT SHALL S&P HAVE ANY

LIABILITY FOR ANY SPECIAL, PUNITIVE, INDIRECT, OR CONSEQUENTIAL DAMAGES (INCLUDING LOST PROFITS), EVEN IF

NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.

S&P GSCI Index is a trademark of The McGraw-Hill Companies, Inc. and has been licensed for use by Deutsche

Bank AG.

DJ-UBSCISM Disclaimer

"Dow Jones(R)", "DJ", "UBS," "DJ-UBSCISM" are service marks of Dow Jones & Company, Inc. ("Dow Jones") and

UBS AG ("UBS AG"), as the case may be, and have been licensed for use for certain purposes by Deutsche Bank

AG

Any securities which Deutsche Bank AG may offer from time to time are not sponsored, endorsed, sold or

promoted by Dow Jones, UBS AG, UBS Securities LLC ("UBS Securities") or any of their subsidiaries or

affiliates. None of Dow Jones, UBS AG, UBS Securities or any of their subsidiaries or affiliates makes any

representation or warranty, express or implied, to the owners of or counterparts to any securities or any

member of the public regarding the advisability of investing in any securities or commodities. The only

relationship of Dow Jones, UBS AG, UBS Securities or any of their subsidiaries or affiliates to the

Licensee is the licensing of certain trademarks, trade names and service marks and of the DJ- UBSCISM,

which is determined, composed and calculated by Dow Jones in conjunction with UBS Securities without regard

to Deutsche Bank AG or any securities. Dow Jones and UBS Securities have no obligation to take the needs of

Deutsche Bank AG or the owners of any securities into consideration in determining, composing or

calculating DJ-UBSCISM. None of Dow Jones, UBS AG, UBS Securities or any of their respective subsidiaries

or affiliates is responsible for or has participated in the determination of the timing of, prices at, or

quantities of any securities to be issued or in the determination or calculation of the equation by which

any securities are to be converted into cash. None of Dow Jones, UBS AG, UBS Securities or any of their

subsidiaries or affiliates shall have any obligation or liability, including, without limitation, to

securities' customers, in connection with the administration, marketing or trading of any securities.

Notwithstanding the foregoing, UBS AG, UBS Securities and their respective subsidiaries and affiliates may

independently issue and/or sponsor financial products unrelated to any securities issued by Licensee, but

which may be similar to and competitive with such securities. In addition, UBS AG, UBS Securities and their

subsidiaries and affiliates actively trade commodities, commodity indexes and commodity futures (including

the Dow Jones-UBS Commodity IndexSM and Dow Jones-UBS Commodity Index Total ReturnSM), as well as swaps,

options and derivatives which are linked to the performance of such commodities, commodity indexes and

commodity futures. It is possible that this trading activity will affect the value of the Dow Jones-UBS

Commodity IndexSM and any securities Deutsche Bank AG may issue from time to time.

NONE OF DOW JONES, UBS AG, UBS SECURITIES OR ANY OF THEIR SUBSIDIARIES OR AFFILIATES GUARANTEES THE

ACCURACY AND/OR THE COMPLETENESS OF THE DOW JONES-UBS COMMODITY INDEXSM OR ANY DATA RELATED THERETO, AND

NONE OF DOW JONES, UBS AG, UBS SECURITIES OR ANY OF THEIR SUBSIDIARIES OR AFFILIATES SHALL HAVE ANY

LIABILITY FOR ANY ERRORS, OMISSIONS OR INTERRUPTIONS THEREIN. NONE OF DOW JONES, UBS AG, UBS SECURITIES OR

ANY OF THEIR SUBSIDIARIES OR AFFILIATES MAKES ANY WARRANTY, EXPRESS OR IMPLIED, AS TO RESULTS TO BE

OBTAINED BY DEUTSCHE BANK AG, OWNERS OF ANY SECURITIES OR ANY OTHER PERSON OR ENTITY FROM THE USE OF THE

DOW JONES-UBS COMMODITY INDEXSM OR ANY DATA RELATED THERETO. NONE OF DOW JONES, UBS AG, UBS SECURITIES OR

ANY OF THEIR SUBSIDIARIES OR AFFILIATES MAKES ANY EXPRESS OR IMPLIED WARRANTIES AND EXPRESSLY DISCLAIMS

ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE WITH RESPECT TO THE DOW

JONES-UBS COMMODITY INDEXSM OR ANY DATA RELATED THERETO. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO

EVENT SHALL DOW JONES, UBS AG, UBS SECURITIES OR ANY OF THEIR SUBSIDIARIES OR AFFILIATES HAVE ANY

LIABILITY FOR ANY LOST PROFITS OR INDIRECT, PUNITIVE, SPECIAL OR CONSEQUENTIAL DAMAGES OR LOSSES, EVEN IF

NOTIFIED OF THE POSSIBILITY THEREOF. THERE ARE NO THIRD PARTY BENEFICIARIES OF ANY AGREEMENTS OR

ARRANGEMENTS AMONG DOW JONES, UBS SECURITIES AND DEUTSCHE BANK AG, OTHER THAN UBS AG.

"Dow Jones(R)", "DJ", "UBS(R)" "Dow Jones-UBS Commodity Index(SM)" are service

marks of Dow Jones & Company, Inc. and UBS AG, as the case may be, and have

been licensed for use for certain purposes by Deutsche Bank. The DB Commodity

Harvest - DJUBS and DB Commodity Booster - DJUBS, which is based in part on the

Dow Jones-UBS Commodity Index, is not sponsored or endorsed by Dow Jones &

Company, Inc. or UBS Securities LLC, but is published with their consent.

26

|