|

Issuer Free Writing Prospectus

Filed pursuant to Rule 433

Registration Statement No. 333-162195

Dated: January 7, 2010

X - Alpha

Alpha from investment style in a market-independent, non-

directional and low-volatility framework

December 31, 2009

Deutsche Bank's X-Alpha USD Excess Return & Total Return Indices have

existed since October 3, 2006. Accordingly, the Index performance from

October 22, 1996 to September 29, 2006 shown in this presentation does

not reflect the performance of the actual Indices or any investable

product, but has been back-calculated on a retrospective basis. The

Indices did not exist during the period of retrospective calculation,

and past performance is not necessarily indicative of how the Indices

will perform in the future. On July 17, 2007, DB made a technical

change to the X-Alpha Index calculation methodology. X-Alpha Index

levels prior to July 17, 2007 were not restated. Further information

is available in the X-Alpha Index Description.

|

|

DB X-Alpha Indices

Portable alpha with a competitive advantage

O X-Alpha seeks to offer uncorrelated absolute return by extracting excess

return from existing DB Regional Style Indices versus their market

Benchmarks

O An attractive alternative to hedge funds

- Low fees

- Daily liquidity

- Transparency

- No performance fees

O An attractive alternative to excess cash

O X-Alpha serves a variety of investment strategies

page 2

|

|

DB Regional Style Indices

Live since October 2002

O DB launched 6 regional style indices in 2002

- US Value, US Growth, Euro Value, Euro Growth, Japan Value, UK Value

- US and Euro style funds were launched in Europe

- Morningstar Fund Ratings for the Euro and US DB Style Funds averaged 4

stars in 2005 and 5 stars in 2006 and 2007

O Indices to provide relative outperformance versus equity market benchmarks

- Excess returns (positive and negative) were not highly correlated across

regions and styles

O Because of uncorrelated excess returns, it made sense to combine indices to

diversify risk and try to stabilise returns

O As there was no UK or Japan Growth Index launched in 2002, these were

created in order to offer consistent diversification across styles/regions

O By extracting the relative performance between the DB Style Index and the

Benchmark in each market (an Index Pair), uncorrelated alpha can be created

page 3

|

|

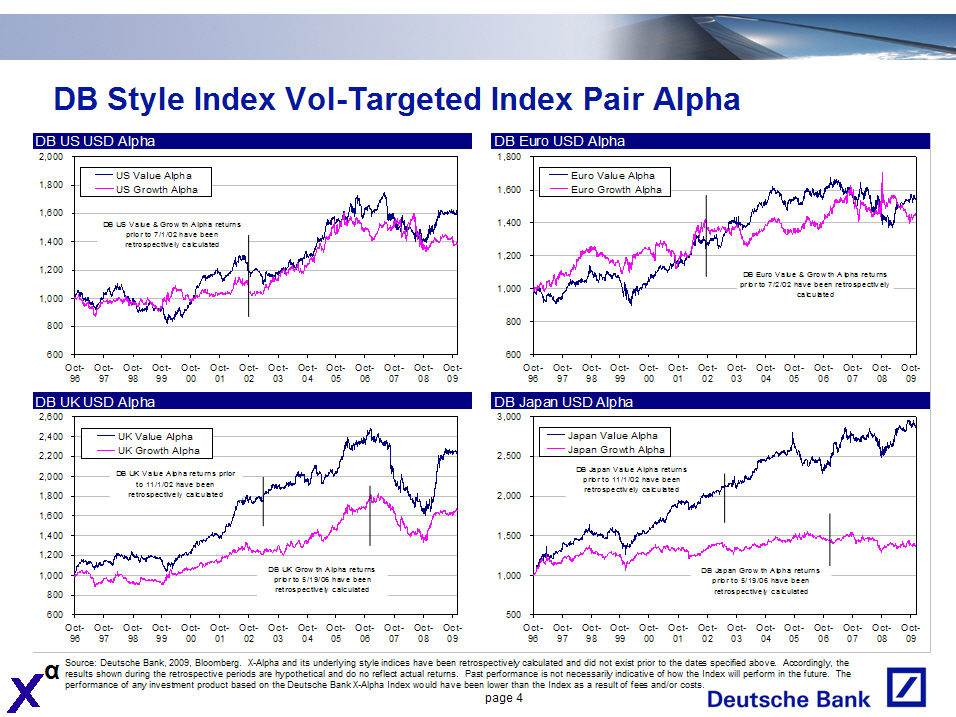

DB Style Index Vol-Targeted Index Pair Alpha

DB US USD Alpha

2,000

1,800 US Value Alpha

US Growth Alpha

1,600

DB US Value & Grow th Alpha

returns

prior to 7/1/02 have

1,400 been

retrospectively

calculated

1,200

1,000

800

600

Oct-Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct-

96 97 98 99 00 01 02 03 04 05 06 07 08 09

DB UK USD Alpha

DB Euro USD Alpha

1,800

Euro Value Alpha

1,600 Euro Growth Alpha

1,400

1,200

DB Euro Value & Grow th Alpha

returns

prior to 7/2/02 have been

1,000 retrospectively

calculated

800

600

Oct-Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct-

96 97 98 99 00 01 02 03 04 05 06 07 08 09

DB Japan USD Alpha

2,600

2,400UK Value Alpha

2,200UK Growth Alpha

3,000

2,500

Japan Value Alpha

Japan Growth Alpha

B UK Value Alpha returns

2,000D prior

to 11/1/02 have been

1,800 retrospectively calculated

2,000

DB Japan Value Alpha returns prior to 11/1/02 have been retrospectively calculated

1,600

1,400

1,200

DB UK Grow th Alpha

1,000 returns

prior to 5/19/06 have

been

retrospectively

800 calculated

600

Oct-Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct-

96 97 98 99 00 01 0203 04 05 06 07 08 09

1,500

DB Japan Grow th Alpha

1,000 returns

rior to 5/19/06 have

p been

retrospectively

calculated

00

Oct-Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct-

96 97 98 99 00 01 02 03 04 05 06 07 08 09

Source: Deutsche Bank, 2009, Bloomberg. X-Alpha and its underlying style indices have been

retrospectively calculated and did not exist prior to the dates specified above. Accordingly, the results

shown during the retrospective periods are hypothetical and do no reflect actual returns. Past performance is

not necessarily indicative of how the Index will perform in the future. The performance of any investment

product based on the Deutsche Bank X-Alpha Index would have been lower than the Index as a result of fees

and/or costs.

page 4

|

|

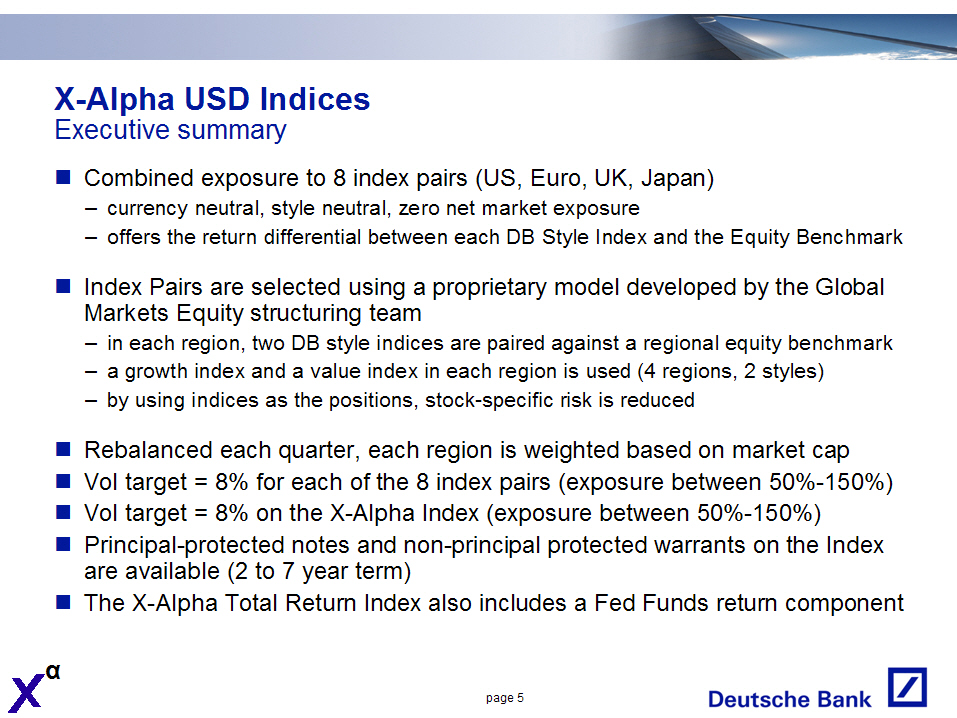

X-Alpha USD Indices

Executive summary

O Combined exposure to 8 index pairs (US, Euro, UK, Japan)

- currency neutral, style neutral, zero net market exposure

- offers the return differential between each DB Style Index and the

Equity Benchmark

O Index Pairs are selected using a proprietary model developed by the Global

Markets Equity structuring team

- in each region, two DB style indices are paired against a regional

equity benchmark

- a growth index and a value index in each region is used (4 regions, 2

styles)

- by using indices as the positions, stock-specific risk is reduced

O Rebalanced each quarter, each region is weighted based on market cap

O Vol target = 8% for each of the 8 index pairs (exposure between 50%-150%)

O Vol target = 8% on the X-Alpha Index (exposure between 50%-150%)

O Principal-protected notes and non-principal protected warrants on the Index

are available (2 to 7 year term)

O The X-Alpha Total Return Index also includes a Fed Funds return component

page 5

|

|

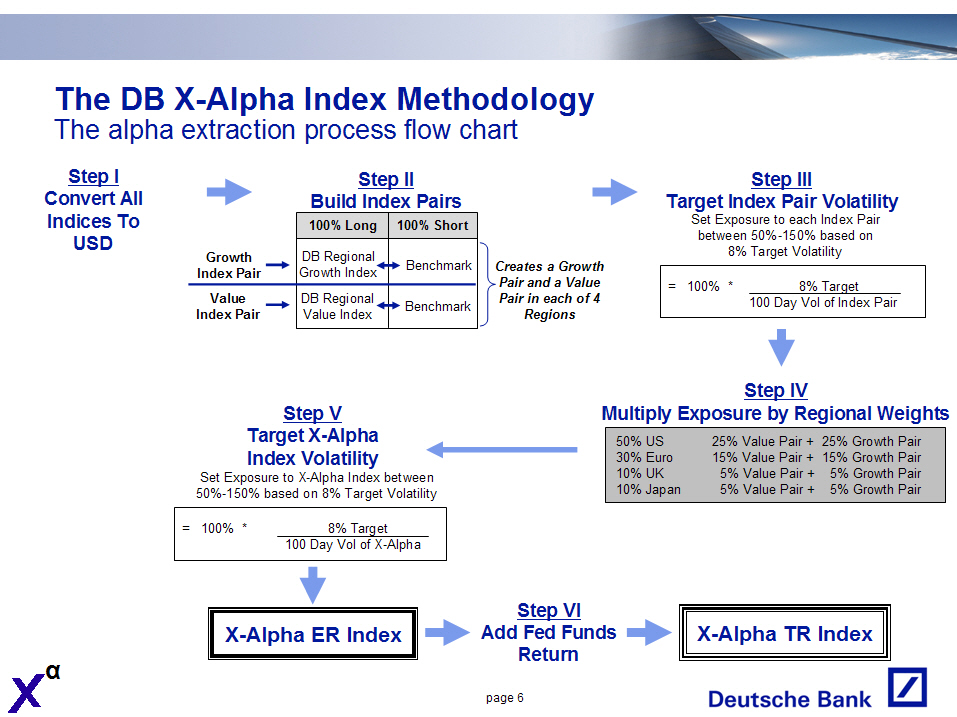

The DB X-Alpha Index Methodology

The alpha extraction process flow chart

Step I Step III

Convert All Step II Target Index Pair Volatility

Indices To Build Index Pairs Set Exposure to each Index Pair

USD ---------------------------------- between 50%-150% based on

100% Long 100% Short 8% Target Volatility

----------------------------------

Growth DB Regional Benchmark Creates a Growth

Index Pair Growth Index Pair and a Value

DB Regional Benchmark Pair in each of 4

Value Value Index Regions

Index Pair

-------------------------------

= 100% * 8% Target

--------------------------

100 Day Vol of Index Pair

Step IV

-------------

Step V Multiply Exposure by Regional Weights

---------------------------------------------------------------

Target X-Alpha 50% US 25% Value Pair + 25% Growth Pair

Index Volatility 30% Euro 15% Value Pair + 15% Growth Pair

Set Exposure to X-Alpha Index between 10% UK 5% Value Pair + 5% Growth Pair

50%-150% based on 8% Target Volatility 10% Japan 5% Value Pair + 5% Growth Pair

---------------------------------------------------------------

-------------------------------

= 100% * 8% Target

--------------------------

100 Day Vol of Index Pair

page 6

|

|

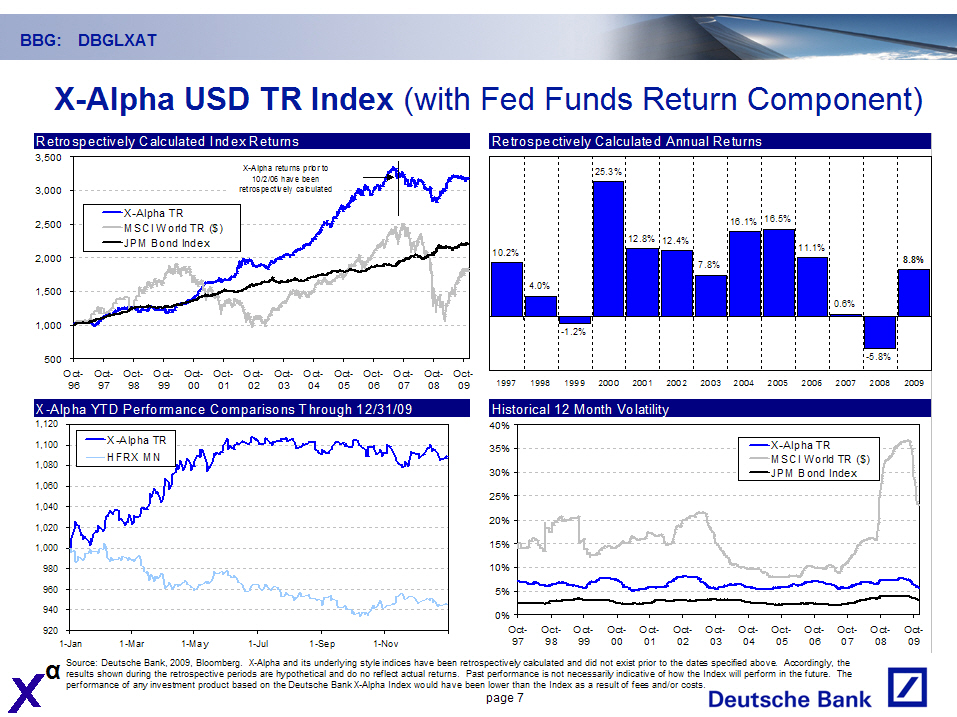

BBG: DBGLXAT

X-Alpha USD TR Index (with Fed Funds Return Component)

Retrospectively Calculated Index Returns

3,500 X-Alpha returns prior to

10/2/06 have been

3,000 retrospectively calculated

2,500 X-Alpha TR

MSCI World TR ($)

JPM Bond Index

2,000

1,500

1,000

500

Oct-Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct-

96 97 98 99 00 01 02 03 04 05 06 07 08 09

X-Alpha YTD Performance Comparisons Through 12/31/09

1,120

1,100 X-Alpha TR

Retrospectively Calculated Annual Returns

25.3%

16.1% 16.5%

12.8% 12.4%

11.1%

10.2% 8.8%

7.8%

4.0%

0.6%

-1.2%

-5.8%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

Historical 12 Month Volatility

X-Alpha TR

1,080

1,060

1,040

1,020

1,000

980

960

940

920

Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct-

97 98 99 00 01 02 03 04 05 06 07 08 09

HFRX MN

MSCI World TR ($)

40% JPM Bond Index

35%

30%

25%

20%

15%

10%

5%

0%

Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct-

1-Jan 1-Mar 1-May 1-Jul 1-Sep 1-Nov

Source: Deutsche Bank, 2009, Bloomberg. X-Alpha and its underlying style indices

have been retrospectively calculated and did not exist prior to the dates

specified above. Accordingly, the results shown during the retrospective periods

are hypothetical and do no reflect actual returns. Past performance is not

necessarily indicative of how the Index will perform in the future. The

performance of any investment product based on the Deutsche Bank X-Alpha Index

would have been lower than the Index as a result of fees and/or costs.

page 7

|

|

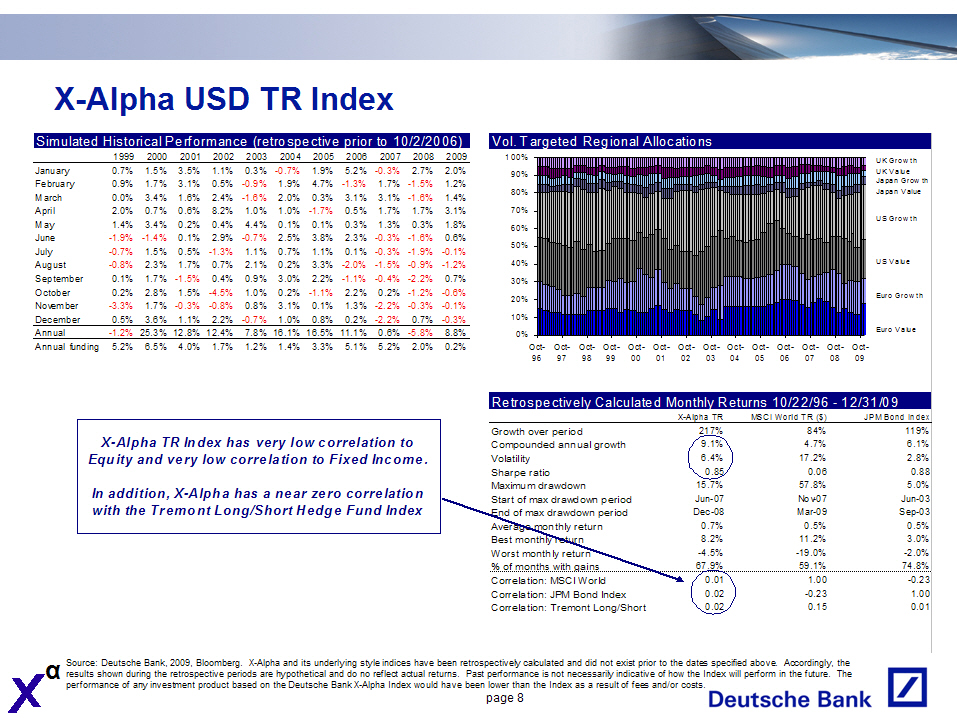

X-Alpha USD TR Index

Simulated Historical Performance (retrospective prior to 10/2/2006)

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

- ---------------------------------------------------------------------------------

January 0.7% 1.5% 3.5% 1.1% 0.3% -0.7% 1.9% 5.2% -0.3% 2.7% 2.0%

February 0.9% 1.7% 3.1% 0.5% -0.9% 1.9% 4.7% -1.3% 1.7% -1.5% 1.2%

March 0.0% 3.4% 1.6% 2.4% -1.6% 2.0% 0.3% 3.1% 3.1% -1.6% 1.4%

April 2.0% 0.7% 0.6% 8.2% 1.0% 1.0% -1.7% 0.5% 1.7% 1.7% 3.1%

May 1.4% 3.4% 0.2% 0.4% 4.4% 0.1% 0.1% 0.3% 1.3% 0.3% 1.8%

June -1.9% -1.4% 0.1% 2.9% -0.7% 2.5% 3.8% 2.3% -0.3% -1.6% 0.6%

July -0.7% 1.5% 0.5% -1.3% 1.1% 0.7% 1.1% 0.1% -0.3% -1.9%-0.1%

August -0.8% 2.3% 1.7% 0.7% 2.1% 0.2% 3.3% -2.0% -1.5% -0.9%-1.2%

September 0.1% 1.7% -1.5% 0.4% 0.9% 3.0% 2.2% -1.1% -0.4% -2.2% 0.7%

October 0.2% 2.8% 1.5% -4.5% 1.0% 0.2% -1.1% 2.2% 0.2% -1.2%-0.6%

November -3.3% 1.7% -0.3% -0.8% 0.8% 3.1% 0.1% 1.3% -2.2% -0.3%-0.1%

December 0.5% 3.6% 1.1% 2.2% -0.7% 1.0% 0.8% 0.2% -2.2% 0.7%-0.3%

- ---------------------------------------------------------------------------------

Annual -1.2% 25.3% 12.8% 12.4% 7.8% 16.1% 16.5% 11.1% 0.6% -5.8% 8.8%

- ---------------------------------------------------------------------------------

Annual funding 5.2% 6.5% 4.0% 1.7% 1.2% 1.4% 3.3% 5.1% 5.2% 2.0% 0.2%

Vol. Targeted Regional Allocations

100% UK Growth

90% UK Value

80% Japan Growth

70% Japan Value

60%

50% US Growth

40%

30% US Value

20%

10% Euro Growth

0%

Euro Value

Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct-

96 97 98 99 00 01 02 03 04 05 06 07 08 09

X-Alpha TR Index has very low correlation to Equity and very low correlation to

Fixed Income.

In addition, X-Alpha has a near zero correlation with the Trem ont Long/Short

Hedge Fund Index

Retrospectively Calculated Monthly Returns 10/22/96 - 12/31/09

X-Alpha TR MSCI World TR ($) JPM Bond Index

- ----------------------------------------------------------------------------------

Growth over period 217% 84% 119%

Compounded annual growth 9.1% 4.7% 6.1%

Volatility 6.4% 17.2% 2.8%

Sharpe ratio 0.85 0.06 0.88

Maximum drawdown 15.7% 57.8% 5.0%

Start of max drawdown period Jun-07 Nov-07 Jun-03

End of max drawdown period Dec-08 Mar-09 Sep-03

Average monthly return 0.7% 0.5% 0.5%

Best monthly return 8.2% 11.2% 3.0%

Worst monthly return -4.5% -19.0% -2.0%

% of months with gains 67.9% 59.1% 74.8%

- ----------------------------------------------------------------------------------

Correlation: MSCI World 0.01 1.00 -0.23

Correlation: JPM Bond Index 0.02 -0.23 1.00

Correlation: Tremont Long/Short 0.02 0.15 0.01

Source: Deutsche Bank, 2009, Bloomberg. X-Alpha and its underlying style indices

have been retrospectively calculated and did not exist prior to the dates

specified above. Accordingly, the results shown during the retrospective periods

are hypothetical and do no reflect actual returns. Past performance is not

necessarily indicative of how the Index will perform in the future. The

performance of any investment product based on the Deutsche Bank X-Alpha Index

would have been lower than the Index as a result of fees and/or costs.

page 8

|

|

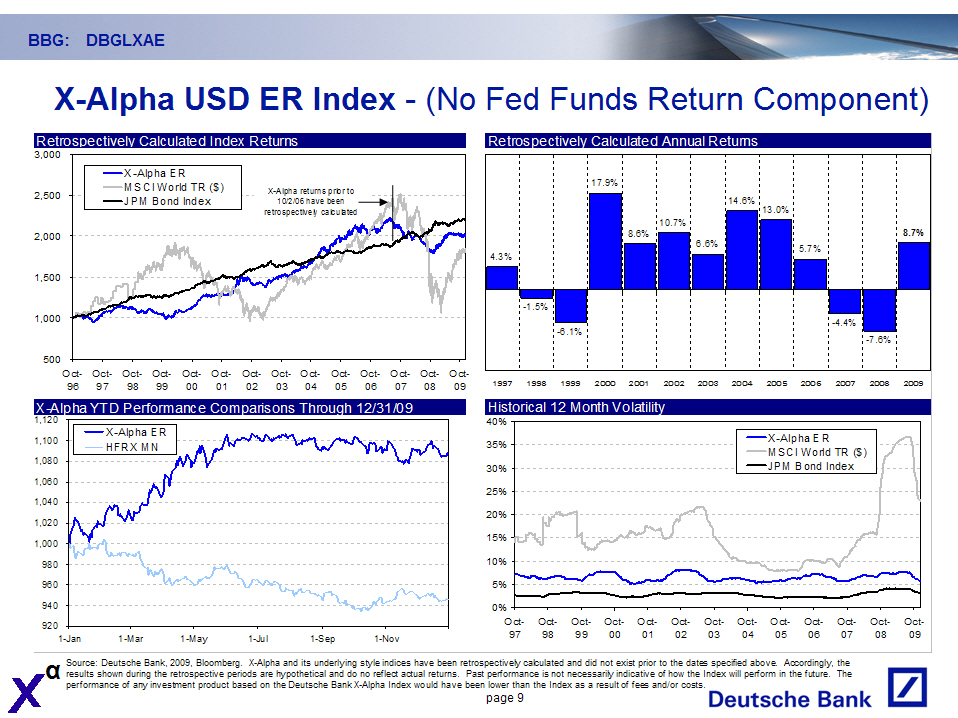

BBG: DBGLXAE

X-Alpha USD ER Index - (No Fed Funds Return Component)

Retrospectively Calculated Index Returns

3,000

X-Alpha ER

SCI World TR ($) -Alpha returns

2,500 M X prior to

JPM Bond Index

10/2/06 have

been

retrospectively

calculated

2,000

1,500

1,000

500

Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct-

96 97 98 99 00 01 02 03 04 05 06 07 08

Retrospectively Calculated Annual Returns

17.9%

14.6%

13.0%

10.7%

8.6% 8.7%

6.6%

4.3% 5.7%

-1.5%

-6.1% -4.4%

-7.6%

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

X-Alpha YTD Performance Comparisons Through 12/31/09

1,120 X-Alpha ER

1,100

HFRX MN

1,080

1,060

1,040

1,020

1,000

980

960

940

920

1-Jan 1-Mar 1-May 1-Jul 1-Sep1-Nov

Historical 12 Month Volatility

40%

X-Alpha ER

35%

MSCI World TR ($)

30% JPM Bond Index

25%

20%

15%

10%

5%

0%

Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct- Oct-Oct- Oct- Oct-

97 98 99 00 01 02 03 04 05 06 07 08 09

Source: Deutsche Bank, 2009, Bloomberg. X-Alpha and its underlying style indices

have been retrospectively calculated and did not exist prior to the dates

specified above. Accordingly, the results shown during the retrospective periods

are hypothetical and do no reflect actual returns. Past performance is not

necessarily indicative of how the Index will perform in the future. The

performance of any investment product based on the Deutsche Bank X-Alpha Index

would have been lower than the Index as a result of fees and/or costs.

page 9

|

|

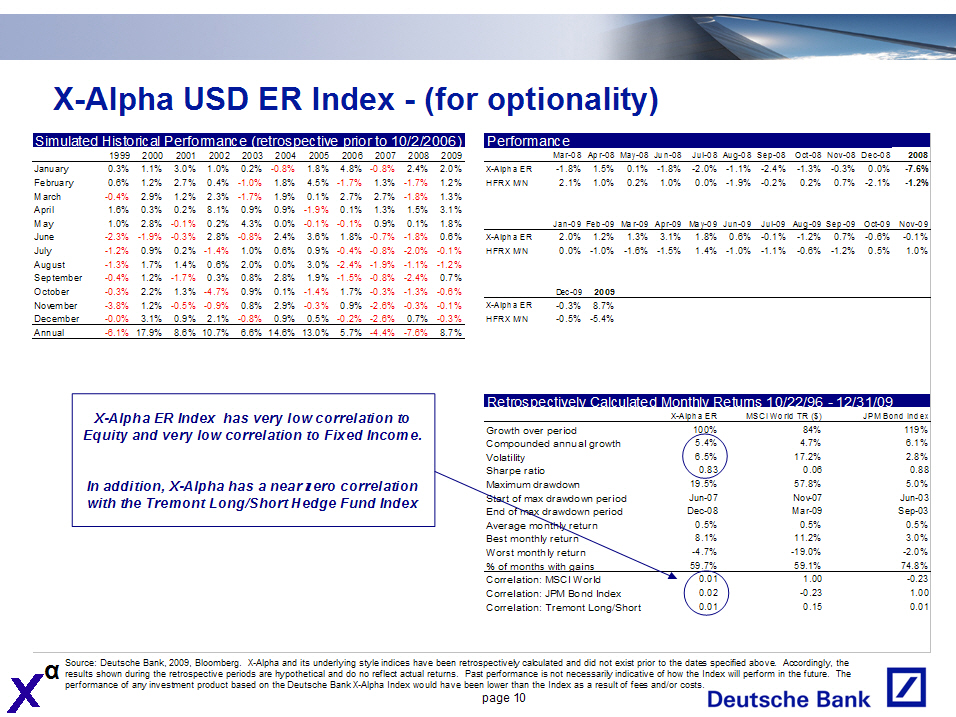

X-Alpha USD ER Index - (for optionality)

Simulated Historical Performance (retrospective prior to 10/2/2006)

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009

- ---------------------------------------------------------------------------------

January 0.3% 1.1% 3.0% 1.0% 0.2% -0.8% 1.8% 4.8% -0.8% 2.4% 2.0%

February 0.6% 1.2% 2.7% 0.4%-1.0% 1.8% 4.5% -1.7% 1.3% -1.7% 1.2%

March -0.4% 2.9% 1.2% 2.3%-1.7% 1.9% 0.1% 2.7% 2.7% -1.8% 1.3%

April 1.6% 0.3% 0.2% 8.1% 0.9% 0.9% -1.9% 0.1% 1.3% 1.5% 3.1%

May 1.0% 2.8% -0.1% 0.2% 4.3% 0.0% -0.1% -0.1% 0.9% 0.1% 1.8%

June -2.3% -1.9% -0.3% 2.8%-0.8% 2.4% 3.6% 1.8% -0.7% -1.8% 0.6%

July -1.2% 0.9% 0.2% -1.4% 1.0% 0.6% 0.9% -0.4% -0.8% -2.0% -0.1%

August -1.3% 1.7% 1.4% 0.6% 2.0% 0.0% 3.0% -2.4% -1.9% -1.1% -1.2%

September -0.4% 1.2% -1.7% 0.3% 0.8% 2.8% 1.9% -1.5% -0.8% -2.4% 0.7%

October -0.3% 2.2% 1.3% -4.7% 0.9% 0.1% -1.4% 1.7% -0.3% -1.3% -0.6%

November -3.8% 1.2% -0.5% -0.9% 0.8% 2.9% -0.3% 0.9% -2.6% -0.3% -0.1%

December -0.0% 3.1% 0.9% 2.1%-0.8% 0.9% 0.5% -0.2% -2.6% 0.7% -0.3%

- ---------------------------------------------------------------------------------

Annual -6.1% 17.9% 8.6% 10.7% 6.6% 14.6% 13.0% 5.7% -4.4% -7.6% 8.7%

- ---------------------------------------------------------------------------------

Performance

Mar-08 Apr-08 May-08 Jun-08 Jul-08 Aug-08 Sep-08 Oct-08 Nov-08 Dec-08 2008

- ----------------------------------------------------------------------------------------------

X-Alpha ER -1.8% 1.5% 0.1% -1.8% -2.0% -1.1% -2.4% -1.3% -0.3% 0.0% -7.6%

HFRX M/N 2.1% 1.0% 0.2% 1.0% 0.0% -1.9% -0.2% 0.2% 0.7% -2.1% -1.2%

Jan-09 Feb-09 Mar-09 Apr-09 May-09 Jun-09 Jul-09 Aug-09 Sep-09 Oct-09 Nov-09

- ----------------------------------------------------------------------------------------------

X-Alpha ER 2.0% 1.2% 1.3% 3.1% 1.8% 0.6% -0.1% -1.2% 0.7% -0.6% -0.1%

-1.0%

HFRX M/N 0.0% -1.6% -1.5% 1.4% -1.0% -1.1% -0.6% -1.2% 0.5% 1.0%

Dec-09 2009

- -----------------------------------------------------------------------------------

X-Alpha ER -0.3% 8.7%

HFRX M/N -0.5% -5.4%

X-Alpha ER Index has very low correlation to Equity and very low correlation to

Fixed Income.

In addition, X-Alpha has a near zero correlation with the Tremont Long/Short

Hedge Fund Index

Retrospectively Calculated Monthly Returns 10/22/96 - 12/31/09

X-Alpha ER MSCI World TR ($) JPM Bond Index

- -----------------------------------------------------------------------------------

Growth over period 100% 84% 119%

Compounded annual growth 5.4% 4.7% 6.1%

Volatility 6.5% 17.2% 2.8%

Sharpe ratio 0.83 0.06 0.88

Maximum drawdown 19.5% 57.8% 5.0%

Start of max drawdown period Jun-07 Nov-07 Jun-03

End of max drawdown period Dec-08 Mar-09 Sep-03

Average monthly return 0.5% 0.5% 0.5%

Best monthly return 8.1% 11.2% 3.0%

Worst monthly return -4.7% -19.0% -2.0%

% of months with gains 59.7% 59.1% 74.8%

- -----------------------------------------------------------------------------------

Correlation: MSCI World 0.01 1.00 -0.23

Correlation: JPM Bond Index 0.02 -0.23 1.00

Correlation: Tremont Long/Short 0.01 0.15 0.01

Source: Deutsche Bank, 2009, Bloomberg. X-Alpha and its underlying style indices

have been retrospectively calculated and did not exist prior to the dates

specified above. Accordingly, the results shown during the retrospective periods

are hypothetical and do no reflect actual returns. Past performance is not

necessarily indicative of how the Index will perform in the future. The

performance of any investment product based on the Deutsche Bank X-Alpha Index

would have been lower than the Index as a result of fees and/or costs.

page 10

|

|

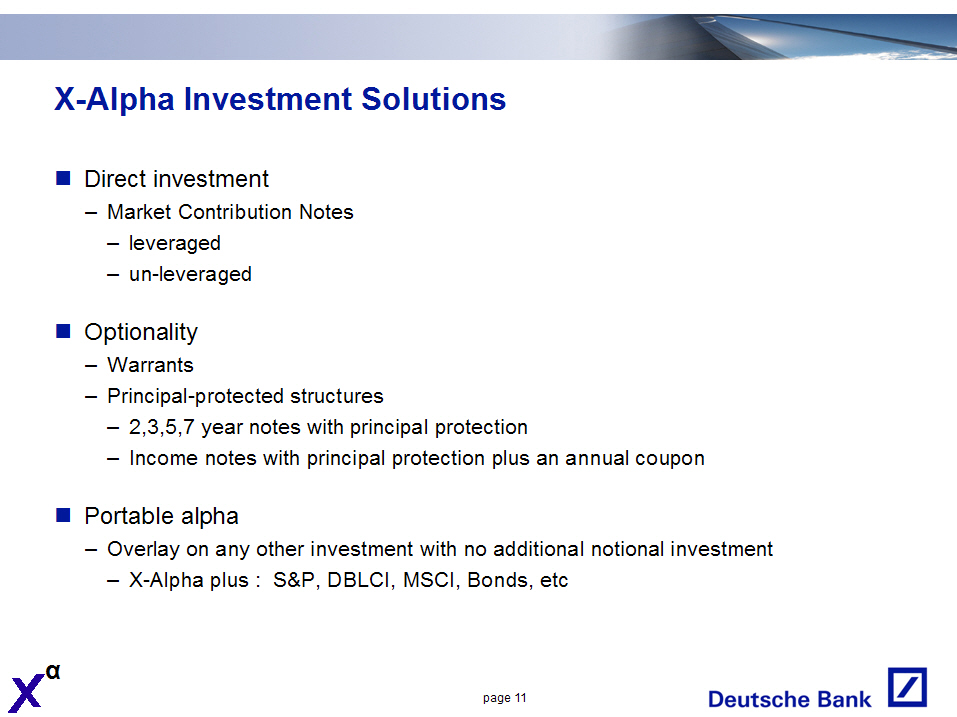

X-Alpha Investment Solutions

o Direct investment

- Market Contribution Notes - leveraged

- un-leveraged

o Optionality

- Warrants

- Principal-protected structures

- 2,3,5,7 year notes with principal protection

- Income notes with principal protection plus an annual coupon

o Portable alpha

- Overlay on any other investment with no additional notional investment

- X-Alpha plus : S & P, DBLCI, MSCI, Bonds, etc

page 11

|

| X - Alpha DB Style Indices Methodology and Historical Performance |

|

Style Investing

Value vs. Growth

O Value Shares

- Mature, established companies with lower earnings volatility

- Sell at lower multiples

- Expected to offer a steady stream of cash flows to shareholders

(dividends)

O Growth Shares

- Relatively young companies with higher earnings volatility

- Sell at higher multiples

- Offer little or no stream of cash flows to shareholders (dividends)

- Expected to offer above average earnings growth

- Companies with higher earnings growth are not always limited to typical

"growth" sectors (Technology, Pharmaceuticals)

O Growth and Value are not necessarily mutually exclusive

- Each style has consistent periods of outperformance versus the market

but at varying amounts and difficult to predict when one style will

dominate

- Some stocks may be growth AND value (low PE and high EPS growth)

page 13

|

|

DB Regional Value Indices

Selection strategy

O Deutsche Bank Value Index Methodology for UK, Japan, US

- Stocks selected from the large cap benchmark (FTSE 100, EURO STOXX(R)

Large, TOPIX 100 or S & P 500 top 251 by market cap)

- Selected according to lowest trailing twelve-month reported P/E ratios

- The price-earnings ratios (P/E) have historically identified undervalued

companies that provided superior performance

O Deutsche Bank Value Index Methodology for Eurozone

- 20 stocks selected from the Dow Jones EURO STOXX(R) Large Index

- Stocks selected according to highest current dividend yield (no more

than five companies from one country)

- In the Eurozone, determining value has been more dependant on dividend

yield

- Yield is believed to be an assessment of shareholder value in three

different ways

- Confidence of management to provide future performance

- Commitment of management to provide earnings stability

- Providing an additional component of return to shareholders

page 14

|

|

DB Regional Growth Indices

Selection strategy

O Deutsche Bank Growth Index Methodology

- Stocks selected from the large cap benchmark (FTSE 100, EURO STOXX(R)

Large, TOPIX 100 or S & P 500 top 251 by market cap)

- The index consists of stocks that show the highest growth in reported

earnings over the past twelve months

- Typically, growth stocks are thought to be from technology or

pharmaceutical industries

- However, the market rewards those companies that demonstrate above

average earnings growth, irrespective of which industry group they may

belong to

- This reflects the possibility that investors may focus more on

demonstrated earnings growth rather than promised earnings growth

O A maximum of five companies per Eurozone country is permitted, no limits for

US, UK and Japan Growth Indices

page 15

|

|

DB Regional Style Indices

Methodology summary

- -------------------------------------------------------------------------------------------------------------------------

Number of

Deutsche Bank Index Selection Pool Stocks Selection Criteria Benchmark

- -------------------------------------------------------------------------------------------------------------------------

US Value Index Top 251 of S & P 500 30 Low Trailing 12 mos. PE S & P 500

- -------------------------------------------------------------------------------------------------------------------------

US Growth Index Top 251 of S & P 500 30 High Trailing 12 mo EPS Growth S & P 500

- -------------------------------------------------------------------------------------------------------------------------

Euro Value Index Dow Jones EuroSTOXX Large 20 High Trailing 12 mo Dividend Yield EuroSTOXX 50

- -------------------------------------------------------------------------------------------------------------------------

Euro Growth Index Dow Jones EuroSTOXX Large 20 High Trailing 12 mo EPS Growth EuroSTOXX 50

- -------------------------------------------------------------------------------------------------------------------------

UK Value Index FTSE 100 20 Low Trailing 12 mos. PE FTSE 100

- -------------------------------------------------------------------------------------------------------------------------

UK Growth Index FTSE 100 20 High Trailing 12 mo EPS Growth FTSE 100

- -------------------------------------------------------------------------------------------------------------------------

Japan Value Index TOPIX 100 20 Low Trailing 12 mos. PE TOPIX 100

- -------------------------------------------------------------------------------------------------------------------------

Japan Growth Index TOPIX 100 20 High Trailing 12 mo EPS Growth TOPIX 100

- -------------------------------------------------------------------------------------------------------------------------

Source: Deutsche Bank, 2008

O Common characteristics of DB Growth and Value Indices

- Companies with negative earnings over the past 12 months are excluded

- Indices are rebalanced quarterly

- Indices are equal-weighted

- All but two indices have been live since October, 2002 (UK & Japan

Growth Indices are live since August, 2006)

- Rules-based investment strategy

page 16

|

|

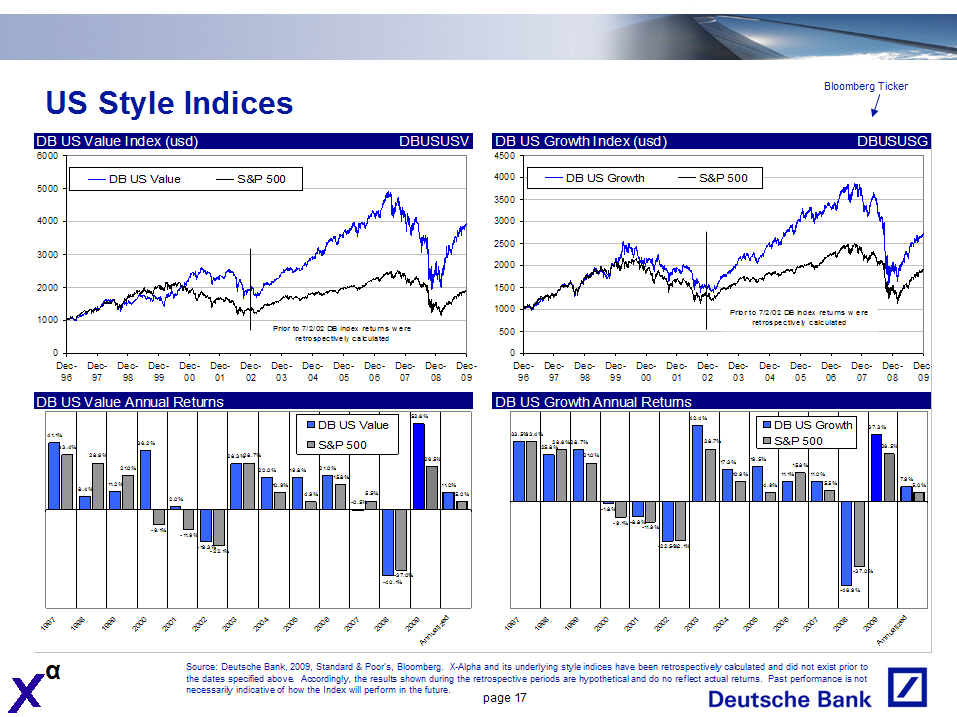

US Style Indices

Bloomberg Ticker

DB US Value Index (usd) DBUSUSV

6000

5000 DB US Value S & P 500

4000

3000

2000

1000

Prior to 7/2/02 DB Index returns were

retrospectively

calculated

0

Dec- Dec- Dec- Dec- Dec- Dec- Dec-Dec- Dec- Dec- Dec- Dec- Dec-

96 97 98 99 00 01 02 03 04 05 06 07 08

DB US Growth Index (usd) DBUSUSG

4500

4000 DB US Growth S & P 500

3500

3000

2500

2000

1500

Prior to 7/2/02 DB Index

1000 returns w ere

retrospectively

500 calculated

Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec-

09 96 97 98 99 00 01 02 03 04 05 06 07 08 09

DB US Value Annual Returns

DB US Value 52.6%

41.1% S & P 500

33.4% 36.2%

28.6% 28.3%28.7% 26.5%

21.0% 20.0% 19.8% 21.0%

15.8%

11.2% 10.9% 11.0%

8.4% 4.9% 5.5% 5.0%

2.0%

-0.5%

-9.1%-11.9%

-19.3%

-22.1%

-37.0%

-40.1%

1997 1998 1999 2000 2001 2002 2003 2004 20052006 2007 2008 2009 Annualized

DB US Growth Annual Returns

42.4% DB US Growth

33.5%33.4% 37.3%

28.7% S & P 500

28.6%28.7% 26.5%

25.8%

21.0% 19.5%

17.3% 15.8%

10.9% 11.1% 11.0%

7.9%

4.9% 5.5% 5.0%

-1.8%

-9.1%-8.8%

-11.9%

-22.5%-22.1%

-37.0%

-46.9%

1997 199819992000 2001 2002 20032004 20052006 2007 2008 2009 Annualized

Source: Deutsche Bank, 2009, Standard & Poor's, Bloomberg. X-Alpha and its

underlying style indices have been retrospectively calculated and did not exist

prior to the dates specified above. Accordingly, the results shown during the

retrospective periods are hypothetical and do no reflect actual returns. Past

performance is not necessarily indicative of how the Index will perform in the

future.

page 17

|

|

Eurozone Style Indices

Bloomberg Ticker

DB Euro Value Index (euro) DBEEEUVA

7000

6000 DB Euro Value Euro STOXX 50

5000

Prior to 7/1/02 DB Index

returns w ere

retrospectively

4000 calculated

3000

2000

1000

0

Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec-

96 97 98 99 00 01 02 03 04 05 06 07 08 09

DB Euro Growth Index (euro) DBEEEUGR

6000

5000 DB Euro Growth Euro STOXX 50

4000

3000

2000

Prior to 7/1/02 DB Index

1000 returns w ere

retrospectively

calculated

0

Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec-

96 97 98 99 00 01 02 03 04 05 06 07 08 09

Source: Deutsche Bank, 2009, Standard & Poor's, Bloomberg. X-Alpha and its

underlying style indices have been retrospectively calculated and did not exist

prior to the dates specified above. Accordingly, the results shown during the

retrospective periods are hypothetical and do no reflect actual returns. Past

performance is not necessarily indicative of how the Index will perform in the

future.

page 18

|

|

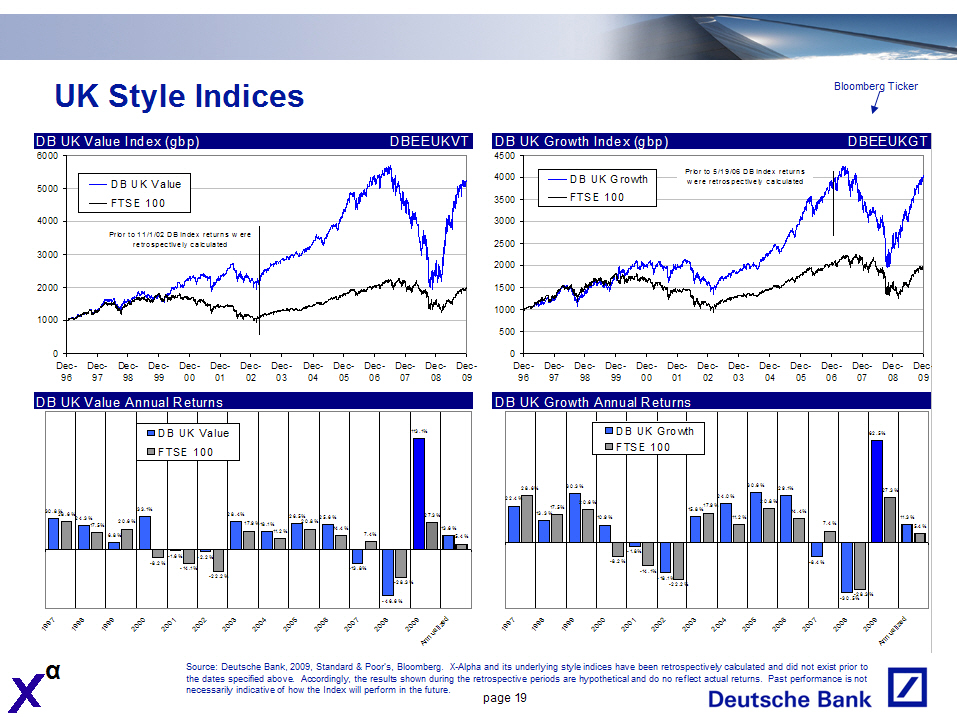

UK Style Indices

DB UK Value Index (gbp) DBEEUKVT

6000

5000 DB UK Value

FTSE 100

4000

Prior to 11/1/02 DB Index returns w ere

retrospectively calculated

3000

2000

1000

0

Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec-Dec- Dec-

96 97 98 99 00 01 02 03 04 05 06 07 08 09

Bloomberg Ticker

DB UK Growth Index (gbp) DBEEUKGT

4500

4000 DB UK Growth Prior to 5/19/06 DB Index returns

were retrospectively calculated

3500 FTSE 100

3000

2500

2000

1500

1000

500

0

Dec-Dec- Dec-Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec- Dec-Dec- Dec-

96 97 98 99 00 01 02 03 04 05 06 07 08 09

Source: Deutsche Bank, 2009, Standard & Poor's, Bloomberg. X-Alpha and its

underlying style indices have been retrospectively calculated and did not exist

prior to the dates specified above. Accordingly, the results shown during the

retrospective periods are hypothetical and do no reflect actual returns. Past

performance is not necessarily indicative of how the Index will perform in the

future.

page 19

|

|

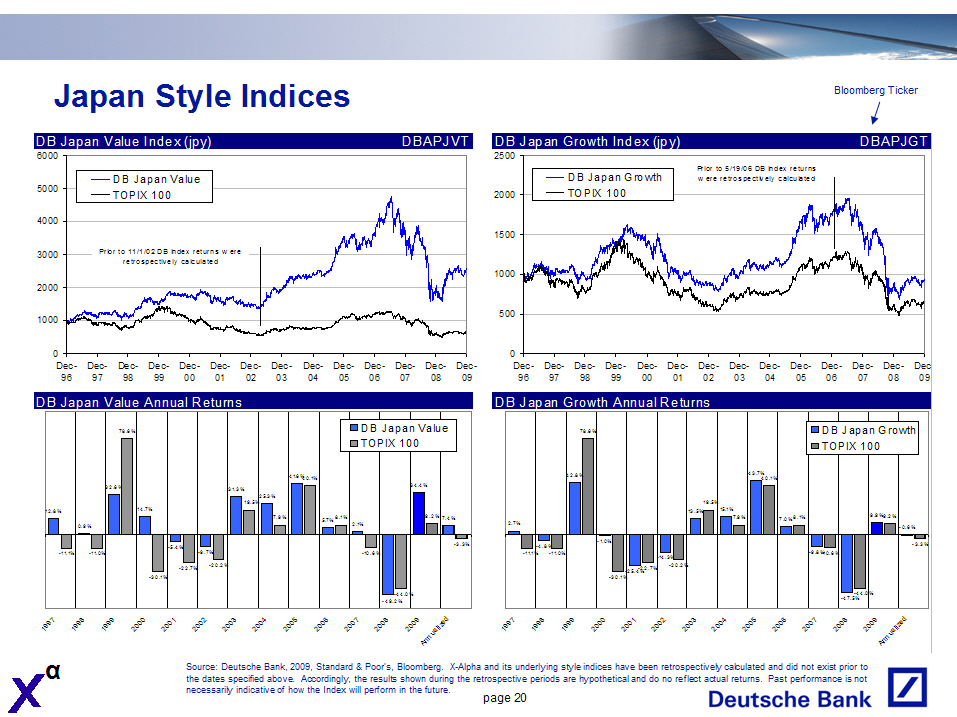

Japan Style Indices

Bloomberg Ticker

Source: Deutsche Bank, 2009, Standard & Poor's, Bloomberg. X-Alpha and its

underlying style indices have been retrospectively calculated and did not exist

prior to the dates specified above. Accordingly, the results shown during the

retrospective periods are hypothetical and do no reflect actual returns. Past

performance is not necessarily indicative of how the Index will perform in the

future.

page 20

|

|

Risk Factors

LIMITED HISTORY OF THE X-ALPHA INDICES - Publication of each X-Alpha Index began on October 3, 2006.

Therefore, the X-Alpha Indices have very limited performance history, and no actual investments which allowed

a tracking of the performance of the X-Alpha Indices was possible before that date. In addition, effective

July 17, 2007, the methodology for the calculation of the X-Alpha Indices was changed by the Index Sponsor.

For this reason, the actual performance history of the X-Alpha Indices for the dates between October 3, 2006

and July 17, 2007 does not reflect the methodology currently in use for the calculation of the X-Alpha

Indices.

AN INVESTMENT LINKED OR RELATED TO AN X-ALPHA INDEX WILL NOT NECESSARILY BE THE SAME AS AN INVESTMENT IN ANY

DB REGIONAL STYLE INDEX, THE BENCHMARK INDEX WITH WHICH IT IS PAIRED OR IN ANY OF THEIR UNDERLYING COMPONENTS

- The X-Alpha Index closing level on any trading day will depend on the performance, in relation to each

pair of Index Constituents which consists of a DB Regional Style Index and a Benchmark Index (each, an

"Index Constituent Pair"), of each DB Regional Style Index compared to the Benchmark Index with which it is

paired. If the overall performance of the DB Regional Style Indices compared to the Benchmark Indices, when

measured by reference to each Index Constituent Pair, is positive, the X-Alpha Index closing level will

rise. Conversely, if the overall performance of the DB Regional Style Indices compared to the Benchmark

Indices, when measured by reference to each Index Constituent Pair, is negative, the X-Alpha Index closing

level will fall. Therefore, whether or not the X-Alpha Index closing level rises or falls depends not only

on whether or not the levels of any of the DB Regional Style Indices and/or the Benchmark Indices rise or

fall but rather on the overall comparative performance of the DB Regional Style Indices to the relevant

Benchmark Indices when measured by reference to each Index Constituent Pair. You should, therefore,

carefully consider the composition and calculation of each DB Regional Style Index and each Benchmark Index

which together form each Index Constituent Pair.

THE VALUE OF EACH X-ALPHA INDEX IS BASED UPON THE RETURN OF EACH INDEX CONSTITUENT PAIR. IF THE RETURN OF A

DB REGIONAL STYLE INDEX IS POSITIVE BUT IS LESS THAN THE RETURN OF A BENCHMARK INDEX WITH WHICH IT IS

PAIRED, THE OVERALL RETURN OF THE RELEVANT INDEX CONSTITUENT PAIR WILL BE NEGATIVE - The value of the

X-Alpha Index is based upon the performance of each DB Regional Style Index relative to that of the

Benchmark Index with which it is paired. Even if a DB Regional Style Index achieves a positive return, the

Index Constituent Pair of which it is a member could achieve a negative return if the Benchmark Index

included in such Index Constituent Pair achieves a greater positive return.

THE INDEX CONSTITUENT PAIRS ARE NOT EQUALLY WEIGHTED IN THE X-ALPHA MODEL - The Index Constituent Pairs

are assigned different geographical weightings in the X-Alpha Model as described in "The Deutsche Bank

X-Alpha USD Excess Return(R) Index - Index Constituent Pairs" in Underlying Supplement No. 14A filed by

Deutsche Bank AG with the SEC on February 28, 2008. One consequence of the unequal weighting of the Index

Constituent Pairs is that the same return generated by two Index Constituent Pairs, whether positive or

negative, may have a different effect on the performance of the Index.

page 21

|

|

Risk Factors

RETURNS GENERATED BY THE INDEX CONSTITUENT PAIRS MAY OFFSET EACH OTHER - At a time when some of the Index

Constituent Pairs generate positive returns, other Index Constituent Pairs may generate positive returns that

are smaller or they may generate returns that are negative. As a result, positive returns generated by one or

more Index Constituent Pairs may be moderated or more than offset by smaller positive returns or negative

returns generated by the other Index Constituent Pairs, particularly if the Index Constituent Pairs that

generate positive returns are assigned relatively low weightings in the X-Alpha Model.

THE RETURNS OF THE INDEX CONSTITUENT PAIRS WILL BE EXPOSED TO FLUCTUATIONS IN EXCHANGE RATES - For the

purposes of determining the returns of the Index Constituent Pairs, the currency in which any DB Regional

Style Index or Benchmark Index is expressed (if such currency is not U.S. dollars) will be converted into

U.S. dollars at the relevant spot exchange rate on each trading day. As a result, any positive or negative

return that is generated as a result of the performance of a DB Regional Style Index compared to that of a

Benchmark Index with which it is paired is exposed to fluctuations in the exchange rate between the U.S.

dollar and the currency in which such DB Regional Style Index and such Benchmark Index are publicly quoted.

In addition, appreciation of the U.S. dollar against the currencies of such indices would have the effect of

reducing the impact of positive excess returns from the relevant Index Constituent Pairs.

THE ACTUAL EXPERIENCED VOLATILITY OF EACH INDEX CONSTITUENT PAIR AND THE X-ALPHA MODEL MAY NOT EQUAL TARGET

VOLATILITY, WHICH MAY HAVE A NEGATIVE IMPACT ON THE PERFORMANCE OF THE INDEX - As described in "The Deutsche

Bank X- Alpha USD Excess Return(R) Index - Calculation and Reconstitution of the Index" in Underlying

Supplement No. 14A filed by Deutsche Bank AG with the SEC on February 28, 2008, the weighting of each Index

Constituent Pair in the X-Alpha Model is adjusted to target a volatility level of 8%. Because this

adjustment is based on recently experienced volatility and is subject to a minimum of 50% and a maximum of

150%, the actual volatility realized on the Index Constituent Pairs and the X-Alpha Model will not

necessarily equal the volatility target. If returns on the Index Constituent Pairs or the X-Alpha Model

coincide with volatility higher than the target, the Index would be exposed less to such returns than if the

volatility targeting had not been done. If returns on Index Constituent Pairs or the X-Alpha Model coincide

with volatility lower than the target, the Index would be exposed more to such returns than if the

volatility targeting had not been done. Such adjustments may have a negative impact on the performance of

the Index.

THE CALCULATION OF THE INDEX CLOSING LEVEL WILL INCLUDE A DEDUCTION OF THE BORROW FEE - On each trading day,

the calculation of the Index closing level will include a deduction of the Borrow Fee to defray transaction

costs incurred in relation to the Index on such day, as described in "The Deutsche Bank X-Alpha USD Excess

Return(R) Index - Index Costs" in Underlying Supplement No. 14A filed by Deutsche Bank AG with the SEC on

February 28, 2008.

page 22

|

|

Risk Factors

WE ARE ONE OF THE COMPANIES THAT MAKE UP THE DOW JONES EURO STOXX 50 TOTAL RETURN INDEX(TM), AND OUR COMMON

STOCK MAY BE INCLUDED IN TWO OF THE DB REGIONAL STYLE INDICES, BUT WE ARE NOT AFFILIATED WITH ANY OTHER

COMPANY INCLUDED IN THE DOW JONES EURO STOXX 50 TOTAL RETURN INDEX(TM), ANY OTHER BENCHMARK INDEX OR ANY DB

REGIONAL STYLE INDEX - We are one of the companies that make up the Dow Jones EURO STOXX 50 Total Return

Index(TM), and our common stock may be included in two of the DB Regional Style Indices, but we are not

affiliated with any of the other companies whose stocks are included in the Dow Jones EURO STOXX 50 Total

Return Index(TM), any of the other Benchmark Indices or any of the DB Regional Style Indices. As a result, we

will have no ability to control the actions of such other companies, including actions that could affect the

value of the stocks underlying any of the Benchmark Indices, the DB Regional Style Indices or the securities

or options linked to the X-Alpha Indices. None of the money you pay us will go to the respective sponsors of

the Benchmark Indices (the "Benchmark Index Sponsors") or to any of the other companies included in the

Benchmark Indices or the DB Regional Style Indices, and none of those companies will be involved in the

offering of the securities or options linked to an X-Alpha Index in any way. Neither those companies nor the

Benchmark Index Sponsors will have any obligation to consider your interests as a holder of securities or

options linked to an X-Alpha Index in taking any corporate actions that might affect the value of such

securities or options.

DEUTSCHE BANK AG, LONDON BRANCH, AS THE SPONSOR OF EACH DB REGIONAL STYLE INDEX, AND EACH BENCHMARK INDEX

SPONSOR MAY ADJUST THE RELEVANT INDEX IN A WAY THAT AFFECTS ITS LEVEL - Deutsche Bank AG, London Branch, as

the sponsor of each DB Regional Style Index (the "DB Regional Style Index Sponsor") and each Benchmark Index

Sponsor are responsible for calculating and maintaining the DB Regional Style Indices and the Benchmark

Indices, respectively. The DB Regional Style Index Sponsor and any Benchmark Index Sponsor can add, delete

or substitute a component stock of a DB Regional Style Index or a Benchmark Index, as the case may be, or

make methodological changes that could affect the level of the relevant index. You should realize that any

changes in the DB Regional Style Index components or the Benchmark Index components may affect the relevant

DB Regional Style Index or Benchmark Index, as the case may be, and may therefore affect the X-Alpha Index,

as any newly added component stock may perform significantly better or worse than the component stock it

replaces. Additionally, the DB Regional Style Index Sponsor and any Benchmark Index Sponsor may alter,

discontinue or suspend calculation or dissemination of the relevant index. Any of these actions could

adversely affect the value of your securities or options linked to an X-Alpha Index. The DB Regional Style

Index Sponsor and the Benchmark Index Sponsors have no obligation to consider your interests in calculating

or revising the relevant indices.

page 23

|

|

Risk Factors

POTENTIAL CONFLICTS OF INTEREST EXIST BECAUSE THE ISSUER OF SECURITIES LINKED TO AN X-ALPHA INDEX, THE

CALCULATION AGENT FOR THE SECURITIES LINKED TO AN X-ALPHA INDEX, THE X-ALPHA INDEX SPONSOR AND THE DB

REGIONAL STYLE INDEX SPONSOR ARE THE SAME LEGAL ENTITY - Deutsche Bank AG is the Issuer of securities linked

to the X-Alpha indices, the calculation agent for securities linked to the X-Alpha indices, the X-Alpha Index

Sponsor and the DB Regional Style Index Sponsor. As the X-Alpha Index Sponsor and the DB Regional Style Index

Sponsor, Deutsche Bank AG carries out calculations necessary to promulgate each X-Alpha Index and each of the

DB Regional Style Indices and maintains some discretion as to how such calculations are made. In particular,

the X-Alpha Index Sponsor and the DB Regional Style Index Sponsor have discretion in selecting among methods

for calculating each X-Alpha Index and each of the DB Regional Style Indices, respectively, in the event that

the regular means of determining the values of the components of each X-Alpha Index or any of the DB Regional

Style Indices, as the case may be, are unavailable at the time such determinations are scheduled to take

place. The X-Alpha Index Sponsor also has discretion to make changes in the reconstitution periods for each

X-Alpha Index, and the DB Regional Style Index Sponsor has discretion under certain circumstances in

selecting the component stocks of each DB Regional Style Index. There can be no assurance that any

determinations made by Deutsche Bank AG in these various capacities will not affect the levels of each

X-Alpha Index or any DB Regional Style Indices or the value of securities or options linked to an X-Alpha

Index. Because determinations made by Deutsche Bank AG in these roles may affect the payments made on options

and securities linked to the X-Alpha Indices, potential conflicts of interest may exist between Deutsche Bank

AG and you.

page 24

|

|

Important notes

Prospective investors should understand and discuss with their professional tax, legal, accounting and other

advisors the effect of a transaction they may enter into. Before entering into any transaction you should take

steps to ensure that you understand and have assessed with your financial advisor, or made an independent

assessment of, the appropriateness of the transaction in the light of your own objectives and circumstances,

including the possible risks and benefits of entering into such a transaction.

Structured notes are not suitable for all investors due to illiquidity, optionality, time to redemption, and

payoff nature of the strategy.

We or our affiliates or persons associated with us or such affiliates ("Associated Persons") may: make a

market in, trade in instruments economically related to, or have an investment banking or other relationship

with one or more of the issuers of the component securities of the underlying index. We or our affiliates

may: maintain a long or short position in securities referenced herein or in related futures or options;

purchase, sell, or maintain inventory; engage in any other transaction involving such securities; and earn

brokerage or other compensation.

Any payout information, scenario analysis, and hypothetical calculations should in no case be construed

as an indication of expected payout on an actual investment and/or expected behavior of an actual

structured product.

Calculations of returns on the instruments may be linked to a referenced index or interest rate. As such,

the investments may not be suitable for persons unfamiliar with such index or interest rate, or unwilling or

unable to bear the risks associated with the transaction. Products denominated in a currency, other than the

investor's home currency, will be subject to changes in exchange rates, which may have an adverse effect on

the value, price or income return of the products. These products may not be readily realizable investments

and are not traded on any regulated market. The securities referred to herein involve risk, which may

include interest rate, index, currency, credit, political, liquidity, time value, commodity and market risk

and are not suitable for all investors.

The past performance of an index, securities or other instruments does not guarantee or predict future

performance. The distribution of this document and availability of these products and services in certain

jurisdictions may be restricted by law.

Deutsche Bank does not provide accounting, tax or legal advice.

BEFORE ENTERING INTO ANY TRANSACTION YOU SHOULD TAKE STEPS TO ENSURE THAT YOU UNDERSTAND AND HAVE MADE AN

INDEPENDENT ASSESSMENT OF THE APPROPRIATENESS OF THE TRANSACTION IN LIGHT OF YOUR OWN OBJECTIVES AND

CIRCUMSTANCES, INCLUDING THE POSSIBLE RISKS AND BENEFITS OF ENTERING INTO SUCH TRANSACTION. YOU SHOULD ALSO

CONSIDER MAKING SUCH INDEPENDENT INVESTIGATIONS AS YOU CONSIDER NECESSARY OR APPROPRIATE FOR SUCH PURPOSE.

"Deutsche Bank" means Deutsche Bank AG and its affiliated companies, as the context requires. Deutsche Bank

Private Wealth Management refers to Deutsche Bank's wealth management activities for high-net- worth clients

around the world. Deutsche Bank Alex Brown is a division of Deutsche Bank Securities Inc.

Deutsche Bank AG has filed a registration statement (including a prospectus) with the SEC for the offerings to

which this communication relates. Before you invest, you should read the prospectus in that registration

statement and other documents the issuer has filed with the SEC for more complete information about the issuer

and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov.

Alternatively, the issuer, any underwriter or any dealer participating in the offering will arrange to send

you the prospectus if you request it by calling toll-free 1-800-311-4409.

Backtested, hypothetical or simulated performance results presented herein have inherent limitations. Unlike

an actual performance record based on trading actual client portfolios, simulated results are achieved by

means of the retroactive application of a backtested model itself designed with the benefit of hindsight.

Taking into account historical events the backtesting of performance also differs from actual account

performance because an actual investment strategy may be adjusted any time, for any reason, including a

response to material, economic or market factors. The backtested performance includes hypothetical results

that do not reflect the reinvestment of dividends and other earnings or the deduction of advisory fees,

brokerage or other commissions, and any other expenses that a client would have paid or actually paid. No

representation is made that any trading strategy or account will or is likely to achieve profits or losses

similar to those shown. Alternative modeling techniques or assumptions might produce significantly different

results and prove to be more appropriate. Past hypothetical backtest results are neither an indicator nor

guarantee of future returns. Actual results will vary, perhaps materially, from the analysis.

Instruments relating to the indices discussed herein are not insured by the Federal Deposit Insurance

Corporation (FDIC) or any other US governmental agency. These instruments are not insured by any

statutory scheme or governmental agency of the United Kingdom.

These investments typically involve a high degree of risk, are not readily transferable and typically will

not be listed or traded on any exchange and are intended for sale only to investors who are capable of

understanding and assuming the risks involved. The market value of any structured security may be affected

by changes in economic, financial and political factors (including, but not limited to, spot and forward

interest and exchange rates), time to maturity, market conditions and volatility and the equity prices and

credit quality of any issuer or reference issuer.

Additional information may be available upon request. Any results shown do not reflect the impact of

commission and/or fees, unless stated.

page 25

|

|

Disclaimers

Dow Jones EURO STOXX 50 IndexTM

Any securities which may be linked to DB Euro USD Alpha (the "securities") are not sponsored, endorsed, sold

or promoted by STOXX Limited, including its affiliates. We refer to STOXX Limited and its affiliates

collectively as STOXX Limited. STOXX Limited has not passed on the legality or suitability of, or the accuracy

or adequacy of descriptions and disclosures relating to the securities. STOXX Limited makes no representation

or warranty, express or implied to the owners of the securities or any member of the public regarding the

advisability of investing in securities generally or in the securities particularly, or the ability of the Dow

Jones EURO STOXX 50 IndexTM to track general stock market performance. The Dow Jones EURO STOXX 50 IndexTM is

determined, composed and calculated by STOXX Limited without regard to Deutsche Bank AG or the securities.

STOXX Limited and Dow Jones have no obligation to take the needs of Deutsche Bank AG or the holders of the

securities into consideration in determining, composing or calculating the Dow Jones EURO STOXX 50 IndexTM.

STOXX Limited and Dow Jones are not responsible for and have not participated in the determination of the

timing of, prices at, or quantities of the securities to be issued or in the determination or calculation of

the equation by which the securities are to be converted into cash. STOXX Limited and Dow Jones have no

liability in connection with the administration, marketing or trading of the securities.

STOXX LIMITED AND DOW JONES DO NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF THE DOW JONES EURO STOXX

50 INDEXTM OR ANY DATA INCLUDED THEREIN AND STOXX LIMITED AND DOW JONES SHALL HAVE NO LIABILITY FOR ANY

ERRORS, OMISSIONS OR INTERRUPTIONS THEREIN. STOXX LIMITED AND DOW JONES MAKE NO WARRANTY, EXPRESS OR IMPLIED,

AS TO RESULTS TO BE OBTAINED BY DEUTSCHE BANK AG, HOLDERS OF THE SECURITIES, OR ANY OTHER PERSON OR ENTITY IN

CONNECTION WITH THE USE OF THE DOW JONES EURO STOXX 50 INDEXTM OR ANY DATA INCLUDED THEREIN. STOXX LIMITED AND

DOW JONES MAKE NO EXPRESS OR IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIM ALL WARRANTIES OF MERCHANTABILITY OR

FITNESS FOR A PARTICULAR PURPOSE OR USE WITH RESPECT TO THE DOW JONES EURO STOXX 50 INDEXTM OR ANY DATA

INCLUDED THEREIN. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT SHALL STOXX LIMITED OR DOW JONES HAVE ANY

LIABILITY FOR ANY LOST PROFITS OR SPECIAL, INCIDENTAL, PUNITIVE, INDIRECT, OR CONSEQUENTIAL DAMAGES, EVEN IF

NOTIFIED OF THE POSSIBILITY THEREOF. THE LICENSING AGREEMENT BETWEEN DEUTSCHE BANK AG AND STOXX LIMITED AND

DOW JONES ARE SOLELY FOR THEIR BENEFIT AND NOT FOR THE BENEFIT OF THE OWNERS OF THE SECURITIES OR ANY THIRD

PARTIES.

"DOW JONES EURO STOXX 50" AND "STOXX" ARE THE INTELLECTUAL PROPERTY OF STOXX LIMITED AND DOW JONES AND HAVE

BEEN LICENSED FOR CERTAIN PURPOSES BY DEUTSCHE BANK AG. THE SECURITIES ARE NOT SPONSORED, ENDORSED, SOLD OR

PROMOTED BY STOXX LIMITED AND DOW JONES, AND STOXX LIMITED AND DOW JONES MAKES NO REPRESENTATION REGARDING THE

ADVISABILITY OF INVESTING IN THE SECURITIES.

Any securities which may be linked to DB US USD Alpha (the "securities") are not sponsored, endorsed, sold or

promoted by Standard & Poor's, a division of the McGraw-Hill Companies, Inc., which we refer to as S & P. S & P

makes no representation or warranty, express or implied, to the owners of the securities or any member of the

public regarding the advisability of investing in securities generally or in the securities particularly, or

the ability of the S & P 500(R) Index to track general stock market performance. S & P has no obligation to take the

needs of Deutsche Bank AG or the holders of the securities into consideration in determining, composing or

calculating the S & P 500(R) Index. S & P is not responsible for and has not participated in the determination of

the timing, price or quantity of the securities to be issued or in the determination or calculation of the

amount due at maturity of the securities. S & P has no obligation or liability in connection with the

administration, marketing or trading of the securities.

S & P DOES NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF THE S & P 500(R) INDEX OR ANY DATA INCLUDED THEREIN

AND S & P SHALL HAVE NO LIABILITY FOR ANY ERRORS, OMISSIONS OR INTERRUPTIONS THEREIN. S & P MAKES NO WARRANTY,

EXPRESS OR IMPLIED, AS TO RESULTS TO BE OBTAINED BY DEUTSCHE BANK AG, HOLDERS OF THE SECURITIES OR ANY OTHER

PERSON OR ENTITY FROM THE USE OF THE S & P 500(R) INDEX OR ANY DATA INCLUDED THEREIN. S & P MAKES NO EXPRESS OR

IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR

PURPOSE OR USE WITH RESPECT TO THE S & P 500(R) INDEX OR ANY DATA INCLUDED THEREIN. WITHOUT LIMITING ANY OF THE

FOREGOING, IN NO EVENT SHALL S & P HAVE ANY LIABILITY FOR ANY SPECIAL, PUNITIVE, INDIRECT OR CONSEQUENTIAL

DAMAGES (INCLUDING LOST PROFITS), EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.

"STANDARD & POOR'S", "S & P", "S & P 500" AND "500" ARE THE INTELLECTUAL PROPERTY OF THE MCGRAW-HILL COMPANIES,

INC. AND HAVE BEEN LICENSED FOR USE BY DEUTSCHE BANK AG. THE SECURITIES ARE NOT SPONSORED, ENDORSED, SOLD OR

PROMOTED BY S & P AND S & P MAKES NO REPRESENTATION REGARDING THE ADVISABILITY OF PURCHASING ANY OF THE SECURITIES.

page 26

|

|

Disclaimers

Any securities which may be linked to DB Japan USD Alpha (the "securities") are not sponsored, endorsed, sold

or promoted by the Tokyo Stock Exchange, Inc., which we refer to as the TSE. The TSE makes no representation

or warranty, express or implied, to the owners of the securities or any member of the public regarding the

advisability of investing in securities generally or in the securities particularly, or the ability of the

TOPIX Index to track general stock market performance. The TSE has no obligation to take the needs of Deutsche

Bank AG or the holders of the securities into consideration in determining, composing or calculating the TOPIX

Index. The TSE is not responsible for and has not participated in the determination of the timing, price or

quantity of the securities to be issued or in the determination or calculation of the amount due at maturity

of the securities. The TSE has no obligation or liability in connection with the administration, marketing or

trading of the securities.

THE TSE DOES NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF THE TOPIX INDEX OR ANY DATA INCLUDED

THEREIN AND THE TSE SHALL HAVE NO LIABILITY FOR ANY ERRORS, OMISSIONS OR INTERRUPTIONS THEREIN. THE TSE MAKES

NO WARRANTY, EXPRESS OR IMPLIED, AS TO RESULTS TO BE OBTAINED BY DEUTSCHE BANK AG, HOLDERS OF THE SECURITIES

OR ANY OTHER PERSON OR ENTITY FROM THE USE OF THE TOPIX INDEX OR ANY DATA INCLUDED THEREIN. THE TSE MAKES NO

EXPRESS OR IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIMS ALL WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A

PARTICULAR PURPOSE OR USE WITH RESPECT TO THE TOPIX INDEX OR ANY DATA INCLUDED THEREIN. WITHOUT LIMITING ANY

OF THE FOREGOING, IN NO EVENT SHALL THE TSE HAVE ANY LIABILITY FOR ANY SPECIAL, PUNITIVE, INDIRECT OR

CONSEQUENTIAL DAMAGES (INCLUDING LOST PROFITS), EVEN IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.

"TOPIX", "TOPIX 100" AND "TOPIX CORE 30" ARE THE INTELLECTUAL PROPERTY OF THE TSE AND HAVE BEEN LICENSED FOR

USE BY DEUTSCHE BANK AG. THE SECURITIES ARE NOT SPONSORED, ENDORSED, SOLD OR PROMOTED BY THE TSE AND THE TSE

MAKES NO REPRESENTATION REGARDING THE ADVISABILITY OF PURCHASING ANY OF THE SECURITIES.

Any securities which may be linked to DB UK USD Alpha (the "securities") are not sponsored, endorsed, sold or

promoted by FTSE International Limited, which we refer to as FTSE, a company owned equally by the London Stock

Exchange and The Financial Times Limited, which we refer to as the LSE and FT, respectively. FTSE, the LSE and

FT make no representation or warranty, express or implied, to the owners of the securities or any member of

the public regarding the advisability of investing in securities generally or in the securities particularly,

or the ability of the FTSE 100(R) Index to track general stock market performance. FTSE, the LSE and FT have no

obligation to take the needs of Deutsche Bank AG or the holders of the securities into consideration in

determining, composing or calculating the FTSE 100(R) Index. FTSE, the LSE and FT are not responsible for and

have not participated in the determination of the timing, price or quantity of the securities to be issued or

in the determination or calculation of the amount due at maturity of the securities. FTSE, the LSE and FT have

no obligation or liability in connection with the administration, marketing or trading of the securities.

FTSE, THE LSE AND FT DO NOT GUARANTEE THE ACCURACY AND/OR THE COMPLETENESS OF THE FTSE 100(R) INDEX OR ANY DATA

INCLUDED THEREIN AND FTSE, THE LSE AND FT SHALL HAVE NO LIABILITY FOR ANY ERRORS, OMISSIONS OR INTERRUPTIONS

THEREIN. FTSE, THE LSE AND FT MAKE NO WARRANTY, EXPRESS OR IMPLIED, AS TO RESULTS TO BE OBTAINED BY DEUTSCHE

BANK AG, HOLDERS OF THE SECURITIES OR ANY OTHER PERSON OR ENTITY FROM THE USE OF THE FTSE 100(R) INDEX OR ANY

DATA INCLUDED THEREIN. FTSE, THE LSE AND FT MAKE NO EXPRESS OR IMPLIED WARRANTIES, AND EXPRESSLY DISCLAIM ALL

WARRANTIES OF MERCHANTABILITY OR FITNESS FOR A PARTICULAR PURPOSE OR USE WITH RESPECT TO THE FTSE 100(R) INDEX

OR ANY DATA INCLUDED THEREIN. WITHOUT LIMITING ANY OF THE FOREGOING, IN NO EVENT SHALL FTSE, THE LSE AND FT

HAVE ANY LIABILITY FOR ANY SPECIAL, PUNITIVE, INDIRECT OR CONSEQUENTIAL DAMAGES (INCLUDING LOST PROFITS), EVEN

IF NOTIFIED OF THE POSSIBILITY OF SUCH DAMAGES.

"FTSE" AND "FTSE 100 INDEX" ARE THE INTELLECTUAL PROPERTY OF FTSE AND HAVE BEEN LICENSED FOR USE BY DEUTSCHE

BANK AG. THE SECURITIES ARE NOT SPONSORED, ENDORSED, SOLD OR PROMOTED BY FTSE, THE LSE OR FT AND FTSE, THE LSE

AND FT MAKE NO REPRESENTATION REGARDING THE ADVISABILITY OF PURCHASING ANY OF THE SECURITIES.

page 27

|