| Free Writing Prospectus Filed pursuant to Rule 433 Registration No. 333-162195 Dated: February 23, 2010 Understanding Structured Notes & CDs DWS Structured Products Americas [GRAPHIC OMITTED] |

|

[GRAPHIC OMITTED]

What we will cover

[] About DWS Investments & Deutsche Bank

[] The Asset Allocation Challenge

[] Structured Products Overview

[] Types of Structured Notes & CDs

[] Considerations

Page 2

|

|

[GRAPHIC OMITTED]

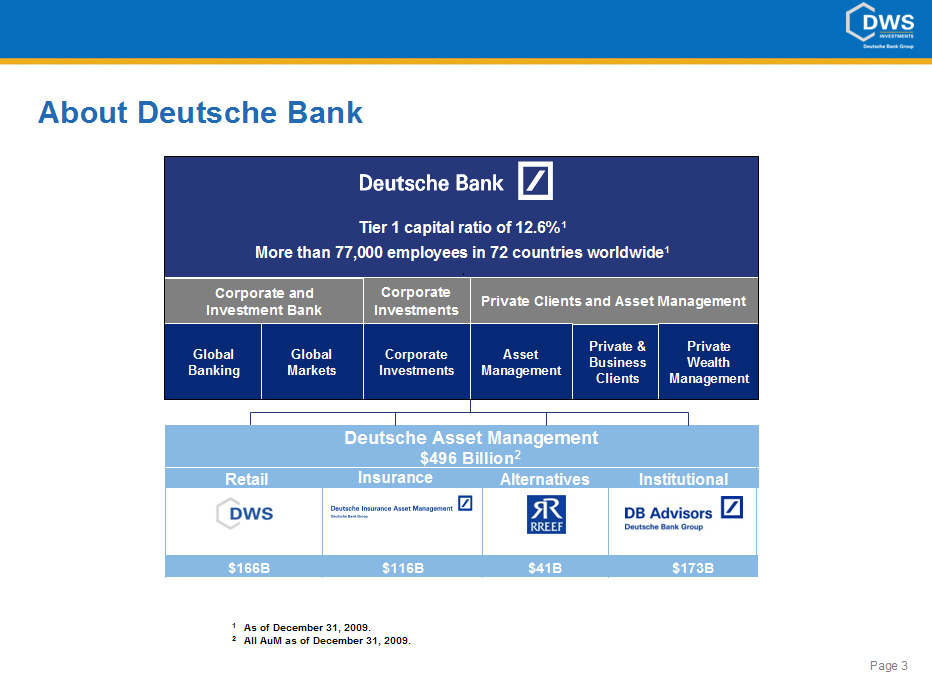

About Deutsche Bank

[GRAPHIC OMITTED]

Tier 1 capital ratio of 12.6%(1)

More than 77,000 employees in 72 countries worldwide(1)

Corporate and Corporate

Investment Bank Investments Private Clients and Asset Management

Private & Private

Global Global Corporate Asset Business Wealth

Banking Markets Investments Management Clients Management

Deutsche Asset Management

$496 Billion(2)

Retail Insurance Alternatives Institutional

[GRAPHIC OMITTED]

(1) As of December 31, 2009.

(2) All AuM as of December 31, 2009.

Page 3

|

|

[GRAPHIC OMITTED]

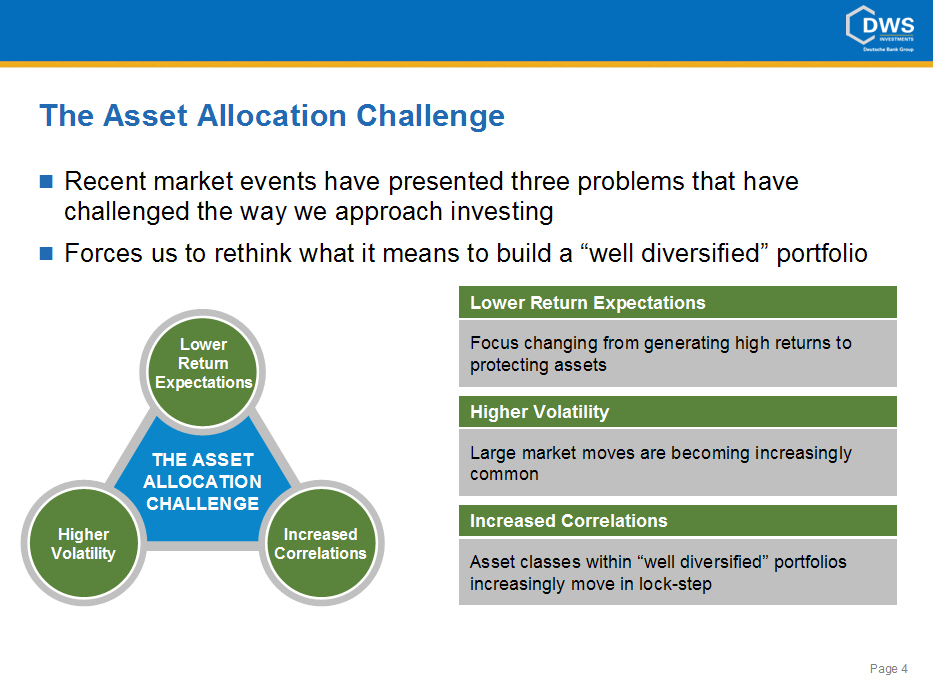

The Asset Allocation Challenge

[] Recent market events have presented three problems that have challenged the

way we approach investing

[] Forces us to rethink what it means to build a "well diversified" portfolio

[GRAPHIC OMITTED]

Page 4

|

|

[GRAPHIC OMITTED]

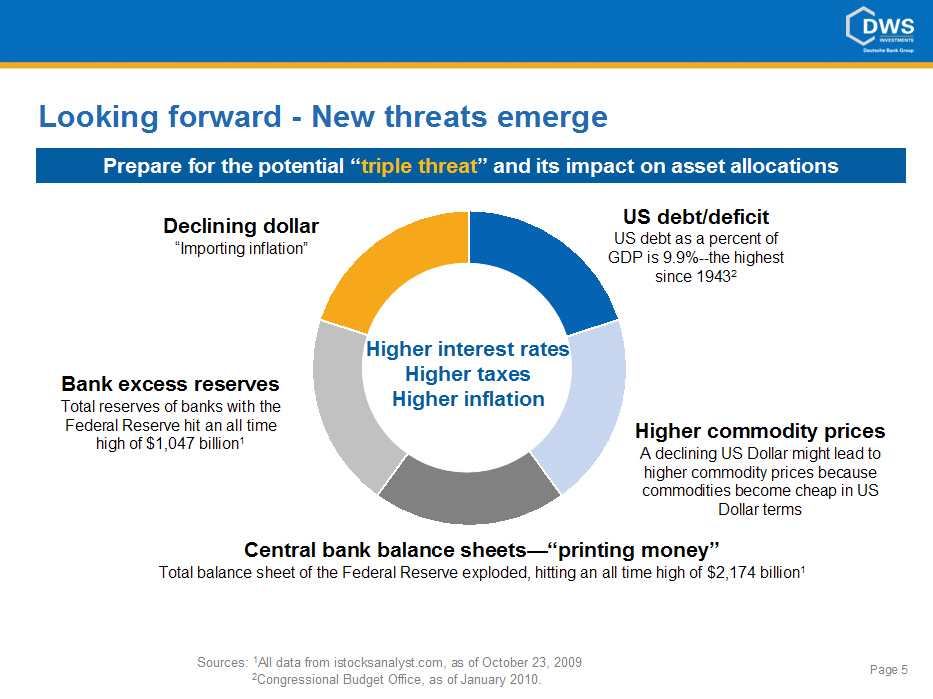

Looking forward - New threats emerge

Prepare for the potential "triple threat" and its impact on asset allocations

Declining dollar US debt/deficit

US debt as a percent of

"Importing inflation" GDP is 9.9%--the highest

since 1943(2)

[GRAPHIC OMITTED]

Central bank balance sheets --"printing money"

Total balance sheet of the Federal Reserve exploded, hitting an all time high

of $2,174 billion(1)

Sources: (1)All data from istocksanalyst.com, as of October 23, 2009

(2)Congressional Budget Office, as of January 2010.

Page 5

|

|

[GRAPHIC OMITTED]

Structured Products Overview

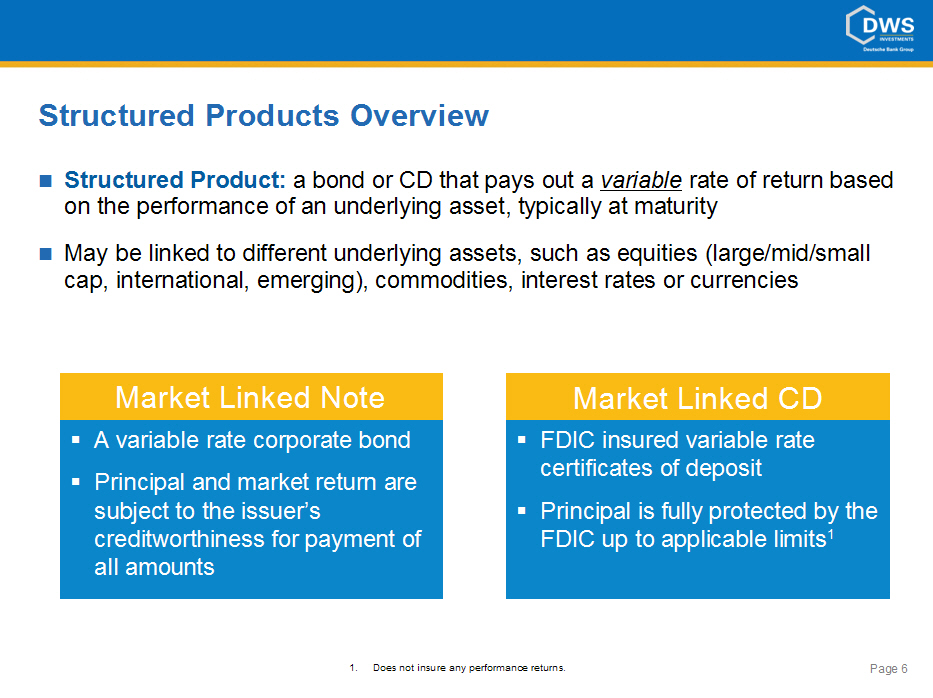

[] Structured Product: a bond or CD that pays out a variable rate of return

based on the performance of an underlying asset, typically at maturity[] May be

linked to different underlying assets, such as equities (large/mid/small cap,

international, emerging), commodities, interest rates or currencies

Market Linked Note

* A variable rate corporate bond

* Principal and market return are subject to the issuer's creditworthiness for

payment of all amounts

Market Linked CD

* FDIC insured variable rate certificates of deposit

* Principal is fully protected by the FDIC up to applicable limits(1)

1. Does not insure any performance returns.

Page 6

|

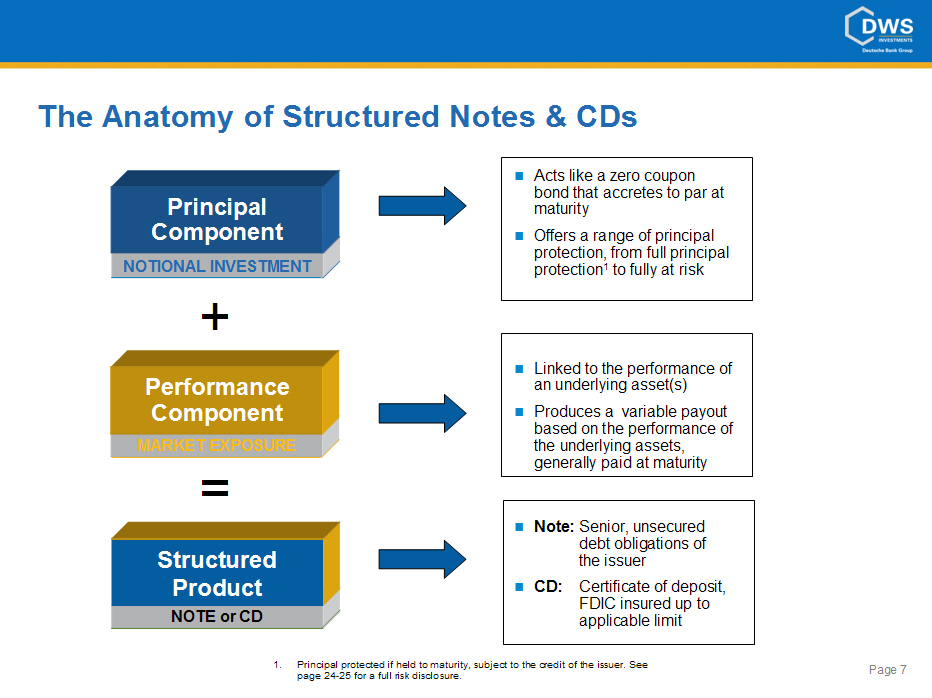

| [GRAPHIC OMITTED] The Anatomy of Structured Notes & CDs [GRAPHIC OMITTED] |

|

[GRAPHIC OMITTED]

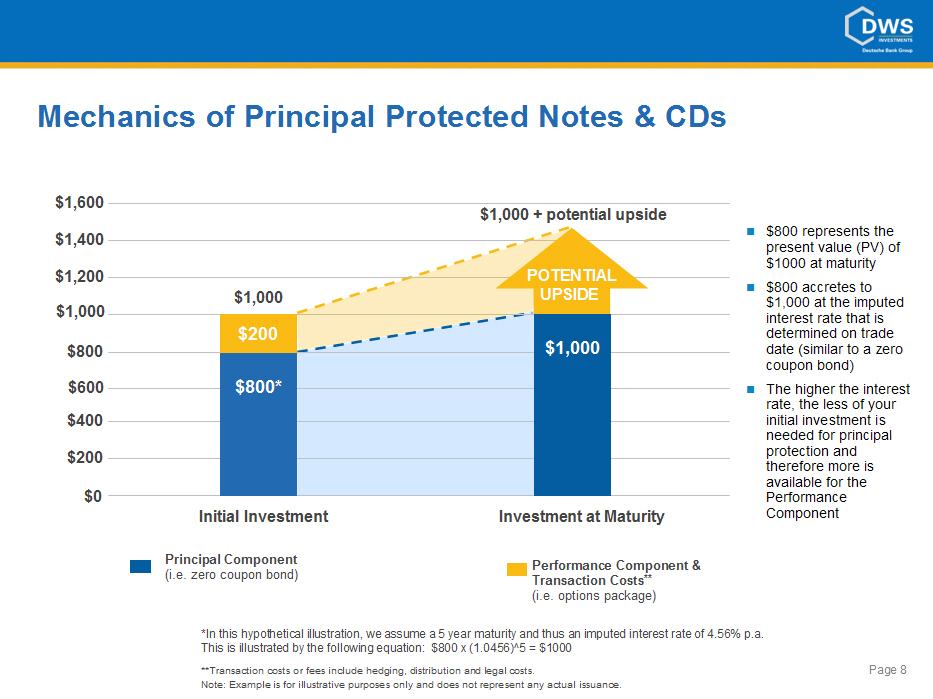

Mechanics of Principal Protected Notes & CDs

[GRAPHIC OMITTED]

[] $800 represents the present value (PV) of $1000 at maturity[] $800

accretes to $1,000 at the imputed interest rate that is determined on trade

date (similar to a zero coupon bond)[] The higher the interest rate, the less

of your initial investment is needed for principal protection and therefore

more is available for the Performance Component

Principal Component Performance Component &

(i.e. zero coupon bond) Transaction Costs(**)

(i.e. options package)

*In this hypothetical illustration, we assume a 5 year maturity and thus an

imputed interest rate of 4.56% p.a. This is illustrated by the following

equation: $800 x (1.0456)^5 = $1000 **Transaction costs or fees include

hedging, distribution and legal costs.

Page 8

Note: Example is for illustrative purposes only and does not represent any

actual issuance.

|

|

[GRAPHIC OMITTED]

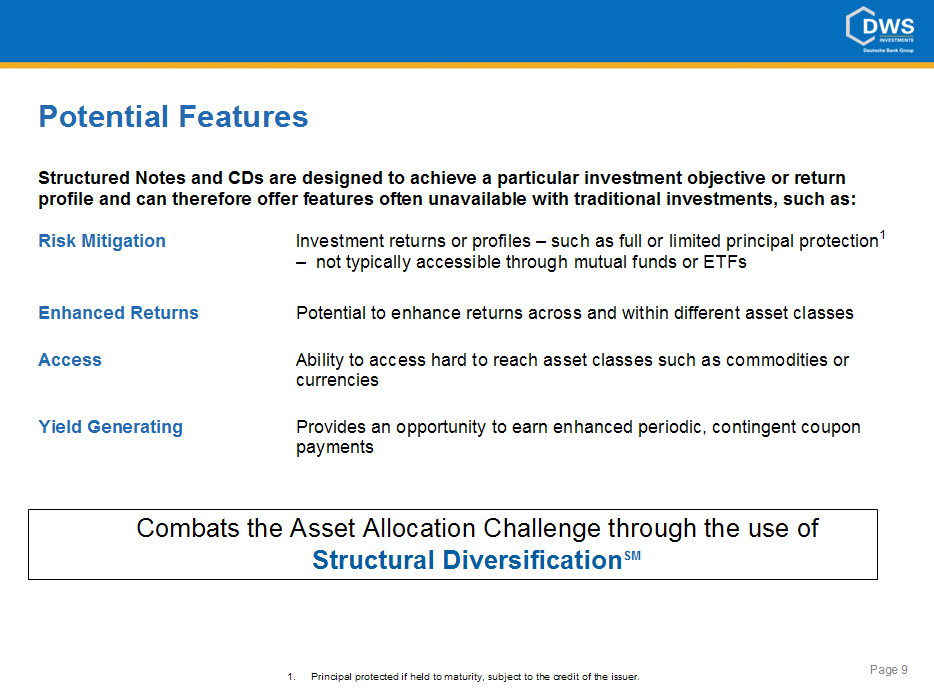

Structured Notes and CDs are designed to achieve a particular investment

objective or return profile and can therefore offer features often unavailable

with traditional investments, such as:

Risk Mitigation Investment returns or profiles -- such as full or limited

principal protection(1)

-- not typically accessible through mutual funds or ETFs

Enhanced Returns Potential to enhance returns across and within different asset

classes

Access Ability to access hard to reach asset classes such as

commodities or

currencies

Yield Generating Provides an opportunity to earn enhanced periodic, contingent

coupon

payments

Combats the Asset Allocation Challenge through the use of

Structural Diversification SM

1. Principal protected if held to maturity, subject to the credit of the

issuer.

Page 9

|

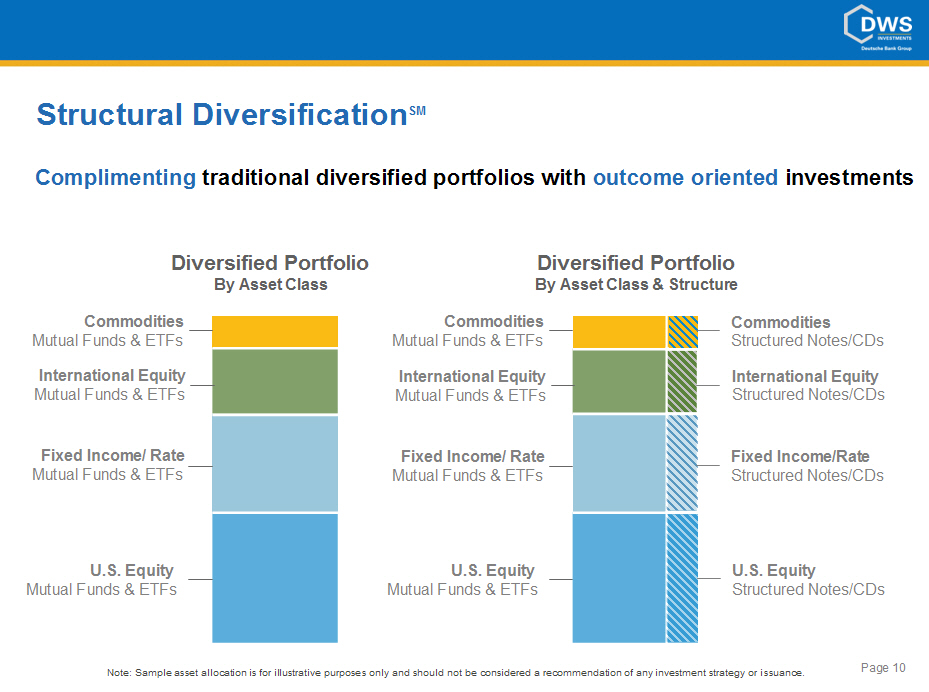

| [GRAPHIC OMITTED] Structural Diversification SM Complimenting traditional diversified portfolios with outcome oriented investments Diversified Portfolio Diversified Portfolio By Asset Class By Asset Class & Structure Commodities Mutual Funds & ETFs International Equity Mutual Funds & ETFs Fixed Income/ Rate Mutual Funds & ETFs Commodities Mutual Funds & ETFs International Equity Mutual Funds & ETFs Fixed Income/ Rate Mutual Funds & ETFs U.S. Equity Mutual Funds & ETFs [GRAPHIC OMITTED] U.S. Equity Mutual Funds & ETFs [GRAPHIC OMITTED] Note: Sample asset allocation is for illustrative purposes only and should not be considered a recommendation of any investment strategy or issuance. Page 10 |

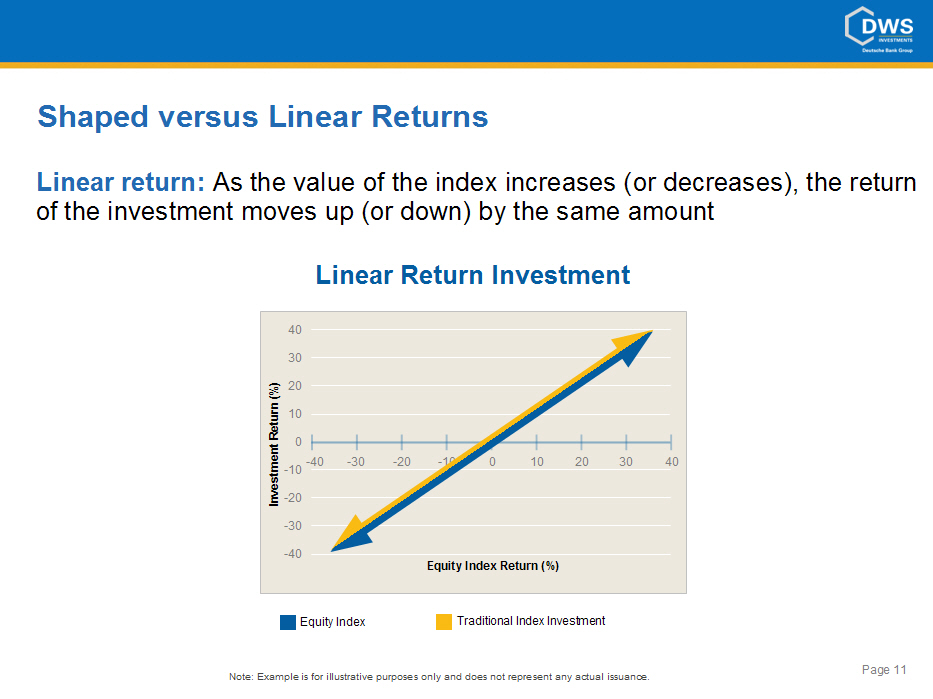

| [GRAPHIC OMITTED] Shaped versus Linear Returns Linear return: As the value of the index increases (or decreases), the return of the investment moves up (or down) by the same amount Linear Return Investment [GRAPHIC OMITTED] Equity Index Traditional Index Investment Note: Example is for illustrative purposes only and does not represent any actual issuance. Page 11 |

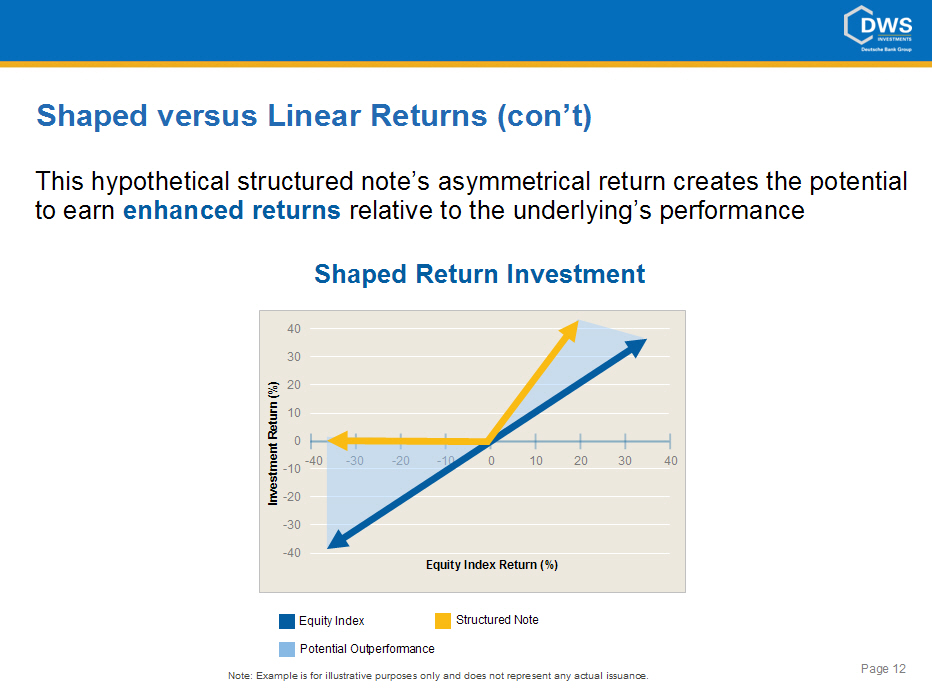

| [GRAPHIC OMITTED] Shaped versus Linear Returns (con't) This hypothetical structured note's asymmetrical return creates the potential to earn enhanced returns relative to the underlying's performance Shaped Return Investment [GRAPHIC OMITTED] Equity Index Structured Note Potential Outperformance Note: Example is for illustrative purposes only and does not represent any actual issuance. Page 12 |

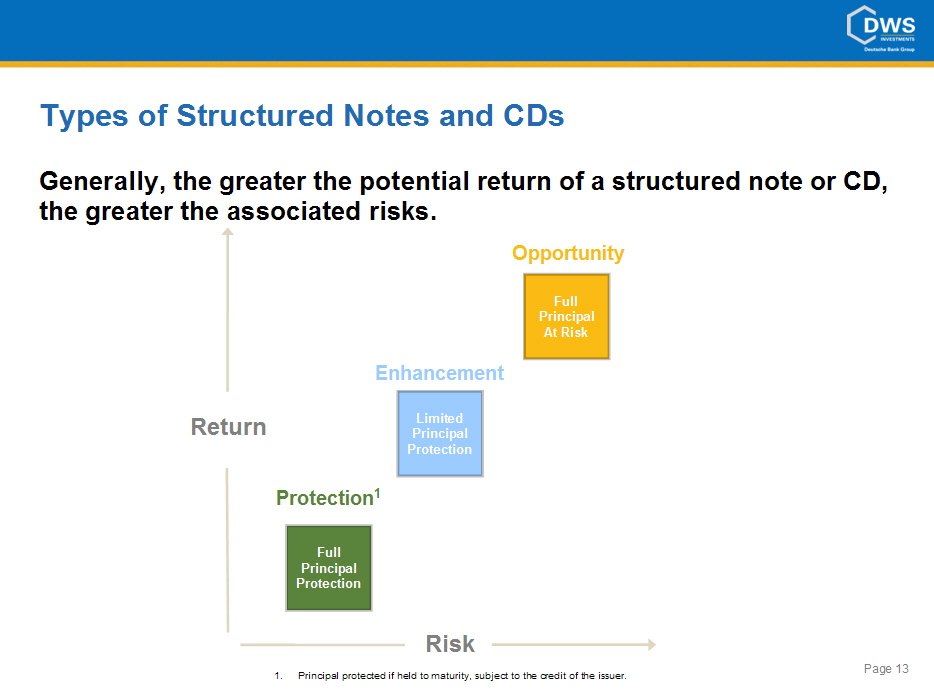

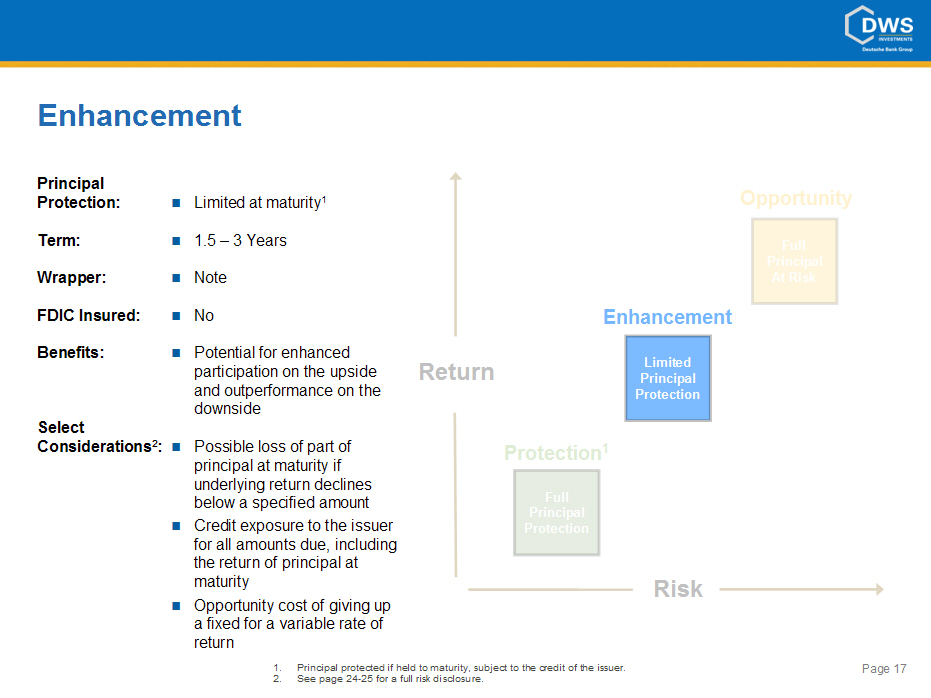

| [GRAPHIC OMITTED] Types of Structured Notes and CDs Generally, the greater the potential return of a structured note or CD, the greater the associated risks. Opportunity [GRAPHIC OMITTED] 1. Principal protected if held to maturity, subject to the credit of the issuer. Page 13 |

| [GRAPHIC OMITTED] |

|

[GRAPHIC OMITTED]

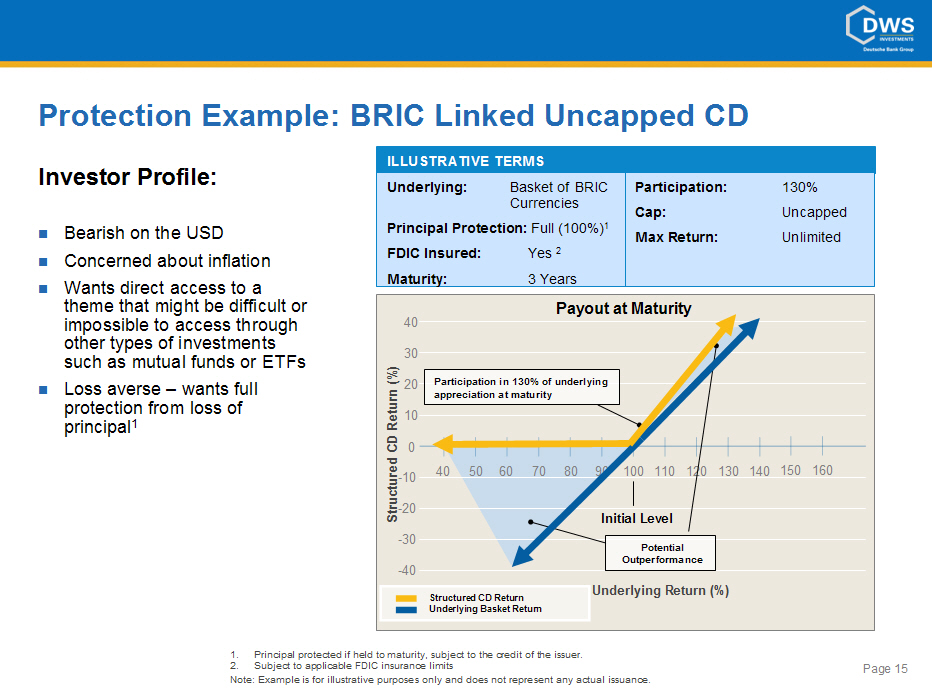

Protection Example: BRIC Linked Uncapped CD

Investor Profile:

[] Bearish on the USD[] Concerned about inflation[] Wants direct access to a

theme that might be difficult or impossible to access through other types of

investments such as mutual funds or ETFs

[] Loss averse -- wants full protection from loss of principal (1)

ILLUSTRATIVE TERMS

Underlying: Basket of BRIC Participation: 130%

Currencies Cap: Uncapped

Principal Protection: Full (100%)(1)

Max Return: Unlimited

FDIC Insured: Yes (2)

Maturity: 3 Years

Payout at Maturity

[GRAPHIC OMITTED]

1. Principal protected if held to maturity, subject to the credit of the

issuer.

2. Subject to applicable FDIC insurance limits

Page 15

Note: Example is for illustrative purposes only and does not represent any

actual issuance.

|

|

[GRAPHIC OMITTED]

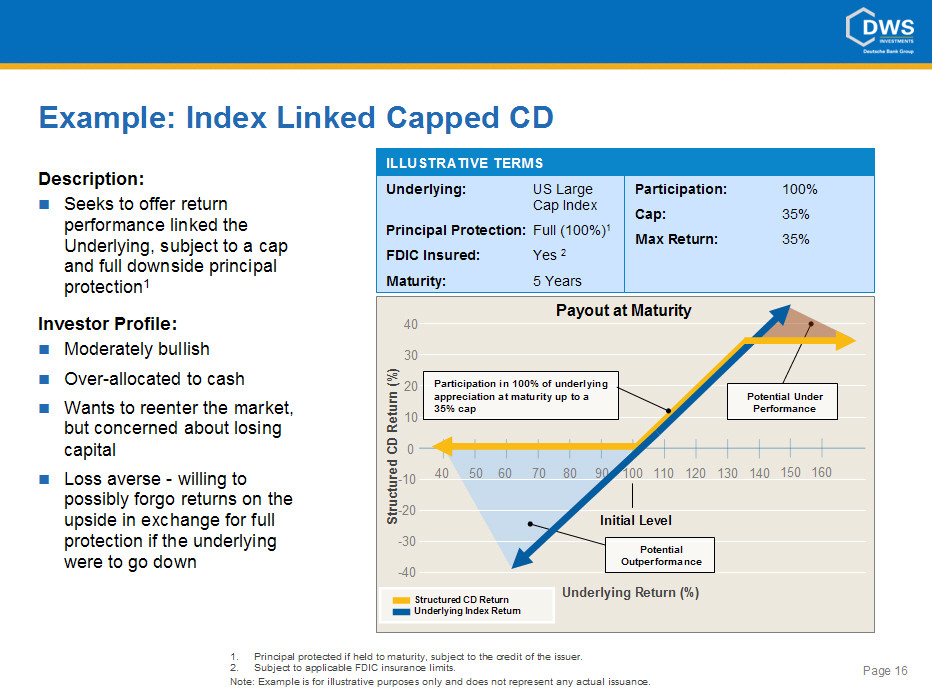

Example: Index Linked Capped CD

ILLUSTRATIVE TERMS

Description: Underlying: US Large Participation:

100%

[] Seeks to offer return Cap Index Cap:

35%

performance linked the Principal Protection: Full (100%)(1)

Underlying, subject to a cap Max Return:

35%

FDIC Insured: Yes (2)

and full downside principal

protection(1) Maturity: 5 Years

Payout at Maturity

Investor Profile: 40

[] Moderately bullish[] Over-allocated to cash [] Wants to reenter the

market, but concerned about losing capital[] Loss averse - willing to possibly

forgo returns on the upside in exchange for full protection if the underlying

were to go down

[GRAPHIC OMITTED]

[GRAPHIC OMITTED]

1. Principal protected if held to maturity, subject to the credit of the

issuer.

2. Subject to applicable FDIC insurance limits.

Page 16

Note: Example is for illustrative purposes only and does not represent any

actual issuance.

|

| [GRAPHIC OMITTED] |

|

[GRAPHIC OMITTED]

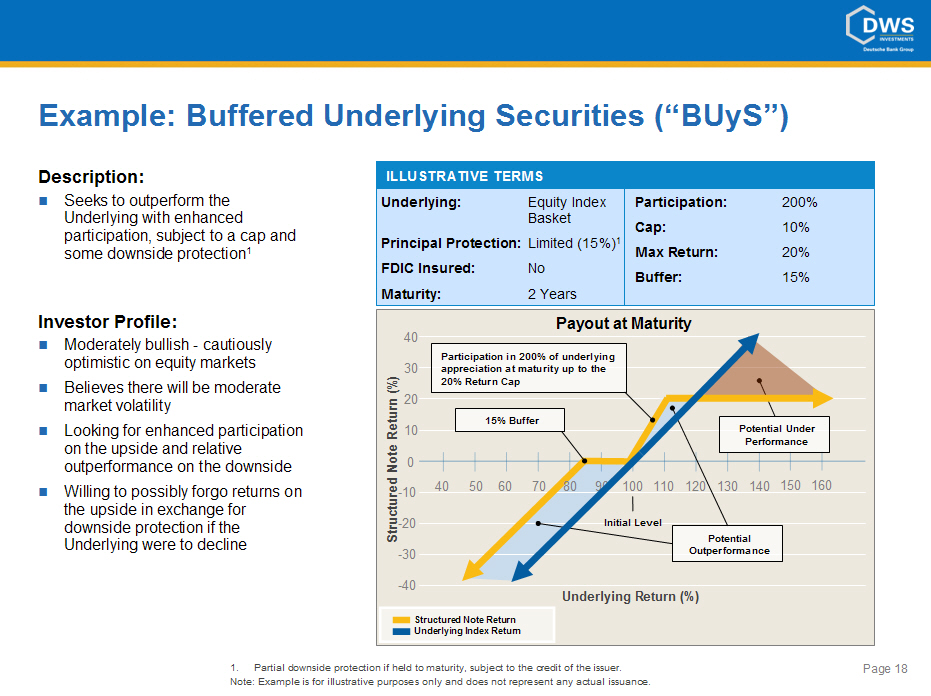

Example: Buffered Underlying Securities ("BUyS")

Description:

[] Seeks to outperform the Underlying with enhanced participation, subject to a

cap and some downside protection (1)

Investor Profile:

[] Moderately bullish - cautiously optimistic on equity markets [] Believes

there will be moderate market volatility[] Looking for enhanced participation

on the upside and relative outperformance on the downside[] Willing to possibly

forgo returns on the upside in exchange for downside protection if the

Underlying were to decline

ILLUSTRATIVE TERMS

Underlying: Equity Index Participation: 200%

Basket Cap: 10%

Principal Protection: Limited (15%)(1)

Max Return: 20%

FDIC Insured: No Buffer: 15%

Maturity: 2 Years

Payout at Maturity

[GRAPHIC OMITTED]

- -40

Underlying Return (%)

Structured Note Return

Underlying Index Return

1. Partial downside protection if held to maturity, subject to the credit of

the issuer.

Page 18

Note: Example is for illustrative purposes only and does not represent any

actual issuance.

|

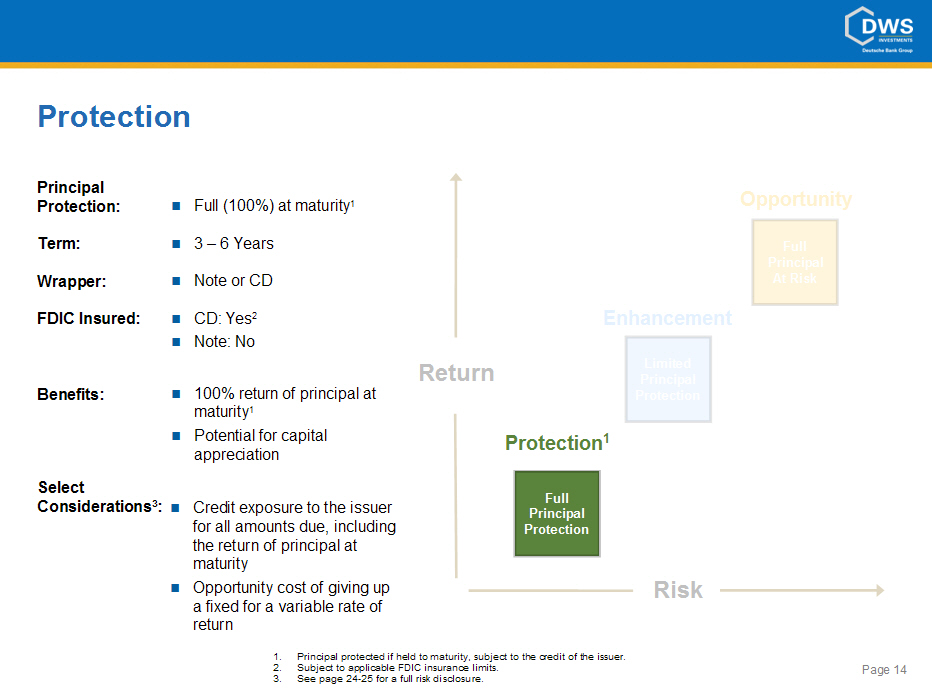

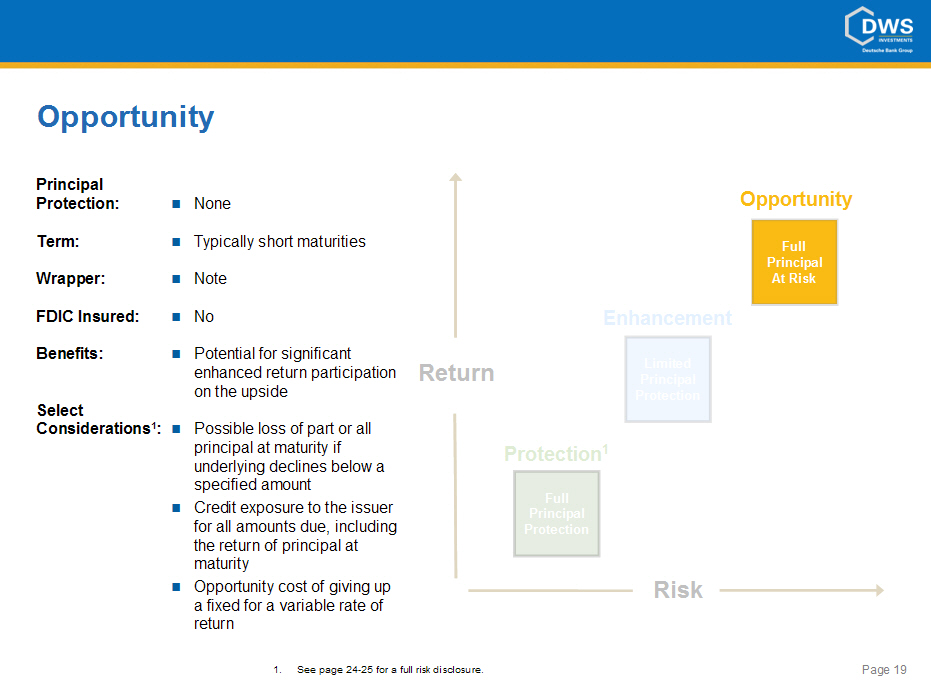

| [GRAPHIC OMITTED] Principal Protection: [] Term: [] Wrapper: [] FDIC Insured: [] Benefits: [] Select Considerations (1):[] [] [] None Typically short maturities Note No Potential for significant enhanced return participation on the upside Possible loss of part or all principal at maturity if underlying declines below a specified amount Credit exposure to the issuer for all amounts due, including the return of principal at maturity Opportunity cost of giving up a fixed for a variable rate of return [GRAPHIC OMITTED] 1. See page 24-25 for a full risk disclosure. Page 19 |

|

[GRAPHIC OMITTED]

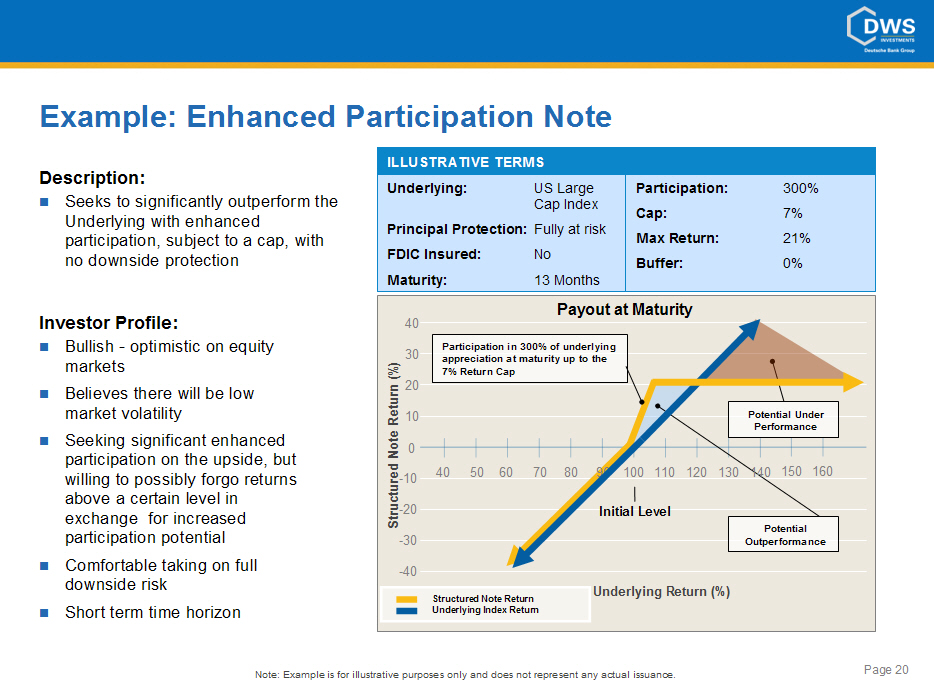

Example: Enhanced Participation Note

Description:

[] Seeks to significantly outperform the Underlying with enhanced

participation, subject to a cap, with no downside protection

Investor Profile:

[] Bullish - optimistic on equity markets [] Believes there will be low market

volatility[] Seeking significant enhanced participation on the upside, but

willing to possibly forgo returns above a certain level in exchange for

increased participation potential[] Comfortable taking on full downside risk[]

Short term time horizon

ILLUSTRATIVE TERMS

Underlying: US Large Participation: 300%

Cap Index Cap: 7%

Principal Protection: Fully at risk Max Return: 21%

FDIC Insured: No Buffer: 0%

Maturity: 13 Months

Payout at Maturity

[GRAPHIC OMITTED]

Structured Note Return

Underlying Index Return

Underlying Return (%)

Note: Example is for illustrative purposes only and does not represent any

actual issuance.

Page 20

|

|

[GRAPHIC OMITTED]

Opportunity Costs: Forgo fixed rate of return for variable returns

FDIC Insurance: Does not insure performance returns

Distributions: Investor forgoes all dividends on the underlying

Issuer Creditworthiness: All payments are subject to the creditworthiness of the

issuer

Secondary Market: Issuer may provide a secondary market in the event

requested

by an investor to liquidate the investment, but is not

obligated to

do so

If provided, the investment may trade at a discount or

premium prior to maturity

[] Buy and hold investments

Taxation: Investors must consider the tax implications of

different

structured products

Note: For additional considerations, see page 22.

Page 21

|

| [GRAPHIC OMITTED] Recap [] The Asset Allocation Challenge - -- Lower Returns - -- Higher Volatility - -- Increased Correlation [] Structured Products Overview: Outcome Oriented investments, designed to achieve a particular investment objective or return. - -- Structural Diversification(SM) - -- Shaped Returns - -- Features: Risk Mitigation, Enhanced Returns, Access and Yield Generating - -- Anatomy of Structured Products: Performance + Principal Components [] Types of Structured Notes & CDs - -- Protection (1): Full Principal Protection - -- Enhancement: Limited Principal Protected - -- Opportunity: Full Principal at Risk [] Considerations Page 22 1. Principal protected if held to maturity, subject to the credit of the issuer. |

| [GRAPHIC OMITTED] Important Information Before purchasing a structured note or CD, investors should carefully consider the risks associated with an investment in the structured note or CD and whether the structured note or CD is a suitable investment for them. Before investing, prospective investors should read the prospectus or disclosure statement, as applicable, relating to the particular structured note or CD. In addition, investors are encouraged to consult with their investment, legal, accounting, tax and other advisers in connection with any investment in a structured note or CD. The content of this DWS Investments presentation is intended for informational and educational purposes only. Before committing to any investment, investors should seek the advice of an independent financial advisor. Page 23 |

| [GRAPHIC OMITTED] Selected Risk Considerations Structured notes and CDs are complicated investments that may offer investors some protection from downside risk in exchange for foregoing some upside potential to achieve that protection and are intended as "buy and hold" investments. Investing in Structured notes and CDs is not the equivalent to investing directly in the underlying(s) and involve significant risks such as: Market risk -- The return on a structured note or CD at maturity, if any, is linked to the performance of the underlying(s) and will depend on various features that are specific to a particular structured note or CD, including, among others any applicable barriers or caps. Depending on the particular structure of the structured note or CD, the structured note or CD may not guarantee any return of your investment and may result in a partial or complete loss. Structured Notes or CDs may not pay more than the principal amount and may pay substantially less than the principal amount -- You may receive a lower payment at maturity than you would have received if you had invested in the underlying(s) . Certain structured notes or CDs may not return more than the principal amount and certain structured notes or CDs may return substantially less than the principal amount. Principal protection only at maturity -- If applicable, a principal protection feature applies only if the securities or instruments are held to maturity and is subject to the issuer's creditworthiness. Certain built-in costs are likely to adversely affect the value of the Structured Notes or CDs prior to maturity -- Certain built-in costs, such as the agent's commission and the Issuer's estimated cost of hedging, are likely to adversely affect the value of the structured notes or CDs prior to maturity. You should be willing and able to hold your structured notes or CDs to maturity. No interest or dividend payments or voting rights -- You will not receive interest payments on the structured notes or CDs or have voting rights or rights to receive cash dividends or other distributions on the structured notes, CDs or the underlying(s) . Lack of liquidity -- There may be little or no secondary market for the structured notes or CDs. The structured notes or CDs will not be listed on any securities exchange. Page 24 |

| [GRAPHIC OMITTED] Selected Risk Considerations (cont. ) The Issuer's research, opinions or recommendations could affect the level of the underlying(s) or the market value of the Structured Notes or CDs -- The Issuer and its affiliates and agents may publish research, express opinions or provide recommendations that are inconsistent with investing in or holding the structured notes or CDs, which could affect the level or price of the underlying(s) or the value of the structured notes or CDs. Potential conflicts -- Because the Issuer and its affiliates play a variety of roles in connection with the issuance of the structured notes or CDs, including acting as calculation agent and hedging its obligations under the structured notes or CDs, the economic interests of the calculation agent and other affiliates of the Issuer are potentially adverse to your interests as an investor in structured notes or CDs. Many economic and market factors will affect the value of the Structured Notes or CDs -- In addition to the level of the underlying(s) on any day, the value of the structured notes or CDs will be affected by a number of complex and interrelated economic and market factors that may either offset or magnify each other. These can include interest rate level, implied volatility and time remaining to maturity The structured notes and CDs are subject to the Issuer's creditworthiness -- An actual or anticipated downgrade in the Issuer's credit rating will likely have an adverse effect on the market value of the structured notes and CDs. The Issuer's creditworthiness will not enhance the likely performance of the investment but may affect the ability of the Issuer to meet its obligations. The payment at maturity on the structured notes and CDs, including the return of principal at maturity if applicable, is subject to the Issuer's creditworthiness. CDs also have the feature of FDIC insurance up to applicable FDIC insurance limits. The credit worthiness of an issuer does not affect or enhance the likely performance of the investment other than the ability of the issuer to meet its obligations. Additional Considerations -- Other risks may apply to a particular structured note or CD. You should read the risk factors in the offering document for a particular structured note or CD prior to making any investment. Page 25 |

|

[GRAPHIC OMITTED]

DWS Structured Products Americas Contacts

Christopher Warren Christopher Ferreira

Managing Director - Head of Structured Products Americas Assistant Vice

President, Structured Products Marketing

DWS Investments Distributors, Inc. DWS Investments

Distributors, Inc.

345 Park Avenue, 27th Floor 345 Park Avenue, 25th

Floor

Office 212 454 2123 Office 212 454

2207

Fax 212 454 7171 Fax 212 454

7171

Email chris.warren@db.com Email

christopher.ferreira@db.com

Jason Hubschman Rupert Watts

Director - Head of Structuring & Product Development Associate, Structured

Products Marketing

DWS Investments Distributors, Inc. DWS Investments

Distributors, Inc.

345 Park Avenue, 25th Floor 345 Park Avenue, 25th

Floor

Office 212 454 7194 Office 212 454

1553

Fax 212 454 7171 Fax 212 454

7171

Email jason.hubschman@db.com Email

rupert.watts@db.com

Jeff Goldstein Emily Agress

Vice President, Structured Products Marketing Associate, Structured

Products Marketing

DWS Investments Distributors, Inc. DWS Investments

Distributors, Inc.

345 Park Avenue, 25th Floor 345 Park Avenue, 25th

Floor

Office 212 454 4372 Office 212 454

3977

Fax 212 454 7171 Fax 212 454

7171

Email

emily.agress@db.com

Email jeffrey.goldstein@db.com

Page 26

|

| Important Information Before purchasing a structured product, investors should carefully consider the risks associated with an investment in the structured product and whether the structured product is suitable for them. Before investing, prospective investors should read the prospectus relating to the particular structured product. In addition, investors are encouraged to consult with their investment, legal, accounting, tax and other advisors in connection with any investment in a structured product. The issuer has filed a registration statement (including a prospectus) with the SEC for the offering to which this communication relates. Before you invest, you should read the prospectus in that registration statement and other documents the issuer has filed with the SEC for more complete information about the issuer and this offering. You may get these documents for free by visiting EDGAR on the SEC web site at www.sec.gov. Alternatively, the issuer, any underwriter or any dealer participating in the offering will arrange to send you the prospectus if you request it by calling 1-800-311-4409. DWS Investments is the US retail brand name of Deutsche Asset Management (DeAM), the global asset management division of Deutsche Bank AG. X-markets is the Deutsche Bank worldwide platform for structured notes. ISSUER FREE WRITING PROSPECTUS File Pursuant to Rule 433 Registration Statement No. 333-162195 Dated: February 22, 2010 NOT FDIC/NCUA INSURED OR GUARANTEED MAY LOSE VALUE / NO BANK GUARANTEE NOT A DEPOSIT NOT INSURED BY ANY FEDERAL GOVERNMENT AGENCY DWS Investments is part of Deutsche Asset Management, which is the marketing name in the US for the asset management activities of Deutsche Bank AG, Deutsche Bank Trust Company Americas, Deutsche Investment Management Americas Inc. and DWS Trust Company. DWS Investments Distributors, Inc. 222 South Riverside Plaza Chicago, IL 60606-5808 rep@dws. com Tel (800) 621-1148 DWS Structured Products dws-sp@db. com Tel (866) 637-9185 www.dws-sp.com Page 27 (02/10) R-15909-1 |