|

FREE WRITING PROSPECTUS Registration Statement No. 333-162195

Filed Pursuant to Rule 433 Dated: July 8, 2010

- --------------------------------------------------------------------------------

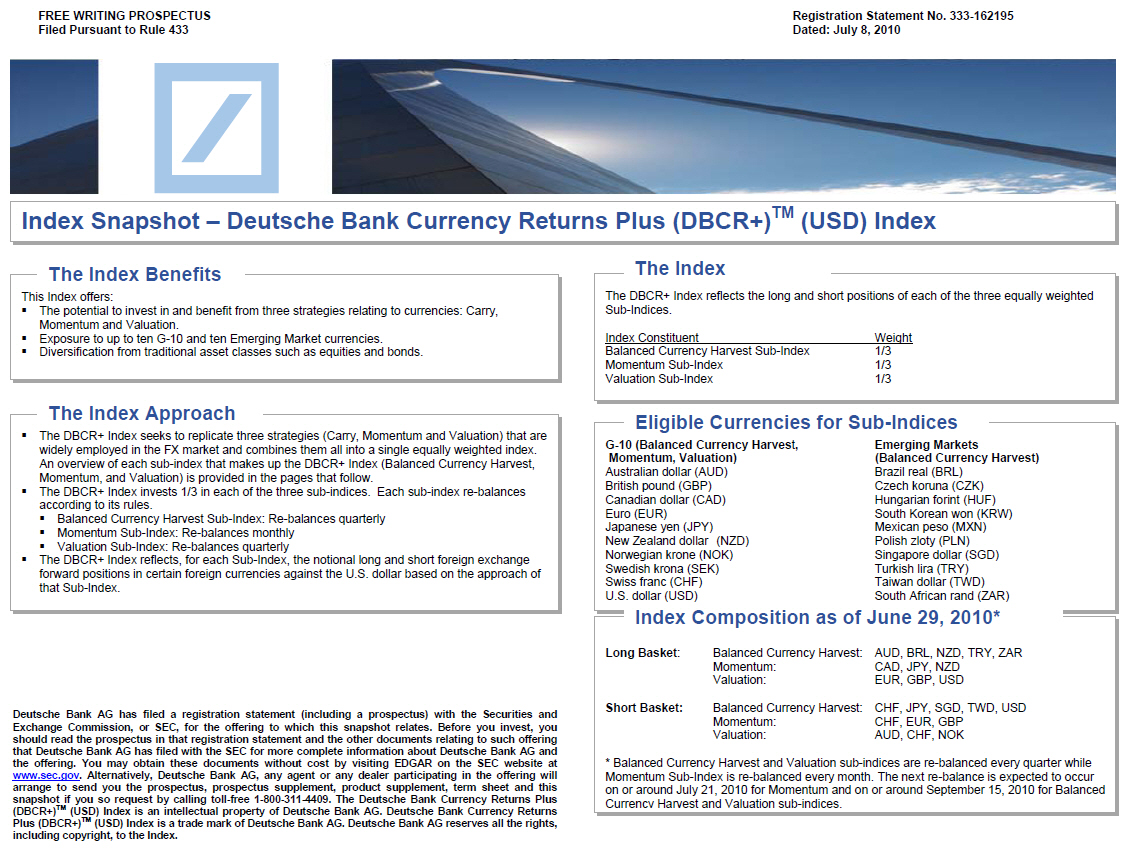

Index Snapshot -- Deutsche Bank Currency Returns Plus (DBCR+) (TM) (USD) Index

- --------------------------------------------------------------------------------

The Index Benefits

This Index offers:

* The potential to invest in and benefit from three strategies relating to

currencies: Carry, Momentum and Valuation.

* Exposure to up to ten G-10 and ten Emerging Market currencies.

* Diversification from traditional asset classes such as equities and bonds.

The Index Approach

* The DBCR+ Index seeks to replicate three strategies (Carry, Momentum and

Valuation) that are widely employed in the FX market and combines them all

into a single equally weighted index.

An overview of each sub-index that makes up the DBCR+ Index (Balanced

Currency Harvest, Momentum, and Valuation) is provided in the pages that

follow.

* The DBCR+ Index invests 1/3 in each of the three sub-indices. Each

sub-index re-balances according to its rules.

* Balanced Currency Harvest Sub-Index: Re-balances quarterly

* Momentum Sub-Index: Re-balances monthly

* Valuation Sub-Index: Re-balances quarterly

* The DBCR+ Index reflects, for each Sub-Index, the notional long and short

foreign exchange forward positions in certain foreign currencies against

the U.S. dollar based on the approach of that Sub-Index.

The Index

The DBCR+ Index reflects the long and short positions of each of the three

equally weighted Sub-Indices.

Index Constituent Weight

- ------------------------------------------

Balanced Currency Harvest Sub-Index 1/3

Momentum Sub-Index 1/3

Valuation Sub-Index 1/3

Eligible Currencies for Sub-Indices

- -----------------------------------

G-10 (Balanced Currency Harvest, Emerging Markets

Momentum, Valuation) (Balanced Currency Harvest)

Australian dollar (AUD) Brazil real (BRL)

British pound (GBP) Czech koruna (CZK)

Canadian dollar (CAD) Hungarian forint (HUF)

Euro (EUR) South Korean won (KRW)

Japanese yen (JPY) Mexican peso (MXN)

New Zealand dollar (NZD) Polish zloty (PLN)

Norwegian krone (NOK) Singapore dollar (SGD)

Swedish krona (SEK) Turkish lira (TRY)

Swiss franc (CHF) Taiwan dollar (TWD)

U.S. dollar (USD) South African rand (ZAR)

Index Composition as of June 29, 2010*

- --------------------------------------

Long Basket: Balanced Currency Harvest: AUD, BRL, NZD, TRY, ZAR

Momentum: CAD, JPY, NZD

Valuation: EUR, GBP, USD

Short Basket: Balanced Currency Harvest: CHF, JPY, SGD, TWD, USD

Momentum: CHF, EUR, GBP

Valuation: AUD, CHF, NOK

* Balanced Currency Harvest and Valuation sub-indices are re-balanced every

quarter while Momentum Sub-Index is re-balanced every month. The next

re-balance is expected to occur on or around July 21, 2010 for Momentum and on

or around September 15, 2010 for Balanced Currency Harvest and Valuation

sub-indices.

Deutsche Bank AG has filed a registration statement (including a prospectus)

with the Securities and Exchange Commission, or SEC, for the offering to which

this snapshot relates. Before you invest, you should read the prospectus in

that registration statement and the other documents relating to such offering

that Deutsche Bank AG has filed with the SEC for more complete information

about Deutsche Bank AG and the offering. You may obtain these documents

without cost by visiting EDGAR on the SEC website at www.sec.gov.

Alternatively, Deutsche Bank AG, any agent or any dealer participating in the

offering will arrange to send you the prospectus, prospectus supplement,

product supplement, term sheet and this snapshot if you so request by calling

toll-free 1-800-311-4409. The Deutsche Bank Currency Returns Plus (DBCR+) (TM)

(USD) Index is an intellectual property of Deutsche Bank AG. Deutsche Bank

Currency Returns Plus (DBCR+) (TM) (USD) Index is a trade mark of Deutsche

Bank AG. Deutsche Bank AG reserves all the rights, including copyright, to the

Index.

page 1

|

|

- --------------------------------------------------------------------------------

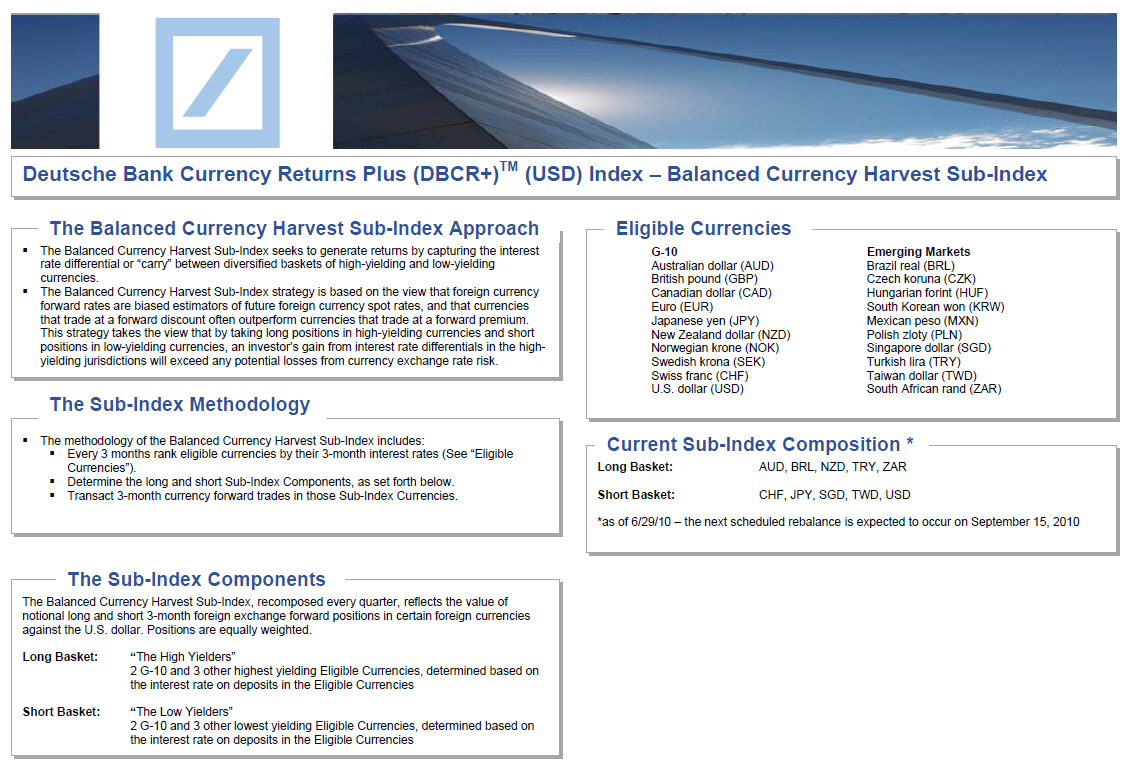

Deutsche Bank Currency Returns Plus (DBCR+) (TM) (USD) Index -- Balanced

Currency Harvest Sub-Index

- --------------------------------------------------------------------------------

The Balanced Currency Harvest Sub -Index Approach

-------------------------------------------------

* The Balanced Currency Harvest Sub-Index seeks to generate returns by

capturing the interest rate differential or "carry" between diversified

baskets of high-yielding and low-yielding currencies.

* The Balanced Currency Harvest Sub-Index strategy is based on the view that

foreign currency forward rates are biased estimators of future foreign

currency spot rates, and that currencies that trade at a forward discount

often outperform currencies that trade at a forward premium. This strategy

takes the view that by taking long positions in high-yielding currencies

and short positions in low-yielding currencies, an investor's gain from

interest rate differentials in the high-yielding jurisdictions will exceed

any potential losses from currency exchange rate risk.

The Sub-Index Methodology

-------------------------

* The methodology of the Balanced Currency Harvest Sub-Index includes:

* Every 3 months rank eligible currencies by their 3-month interest

rates (See "Eligible Currencies") .

* Determine the long and short Sub-Index Components, as set forth below.

* Transact 3-month currency forward trades in those Sub-Index

Currencies.

The Sub-Index Components

------------------------

The Balanced Currency Harvest Sub-Index, recomposed every quarter, reflects the

value of notional long and short 3-month foreign exchange forward positions in

certain foreign currencies against the U.S. dollar. Positions are equally

weighted.

Long Basket: "The High Yielders"

2 G-10 and 3 other highest yielding Eligible Currencies, determined

based on the interest rate on deposits in the Eligible Currencies

Short Basket: "The Low Yielders"

2 G-10 and 3 other lowest yielding Eligible Currencies, determined

based on the interest rate on deposits in the Eligible Currencies

Eligible Currencies

- -------------------

G-10 Emerging Markets

Australian dollar (AUD) Brazil real (BRL)

British pound (GBP) Czech koruna (CZK)

Canadian dollar (CAD) Hungarian forint (HUF)

Euro (EUR) South Korean won (KRW)

Japanese yen (JPY) Mexican peso (MXN)

New Zealand dollar (NZD) Polish zloty (PLN)

Norwegian krone (NOK) Singapore dollar (SGD)

Swedish krona (SEK) Turkish lira (TRY)

Swiss franc (CHF) Taiwan dollar (TWD)

U.S. dollar (USD) South African rand (ZAR)

Current Sub-Index Composition*

- ------------------------------

Long Basket: AUD, BRL, NZD, TRY, ZAR

Short Basket: CHF, JPY, SGD, TWD, USD

*as of 6/29/10 -- the next scheduled rebalance is expected to occur on

September 15, 2010

page 2

|

|

- --------------------------------------------------------------------------------

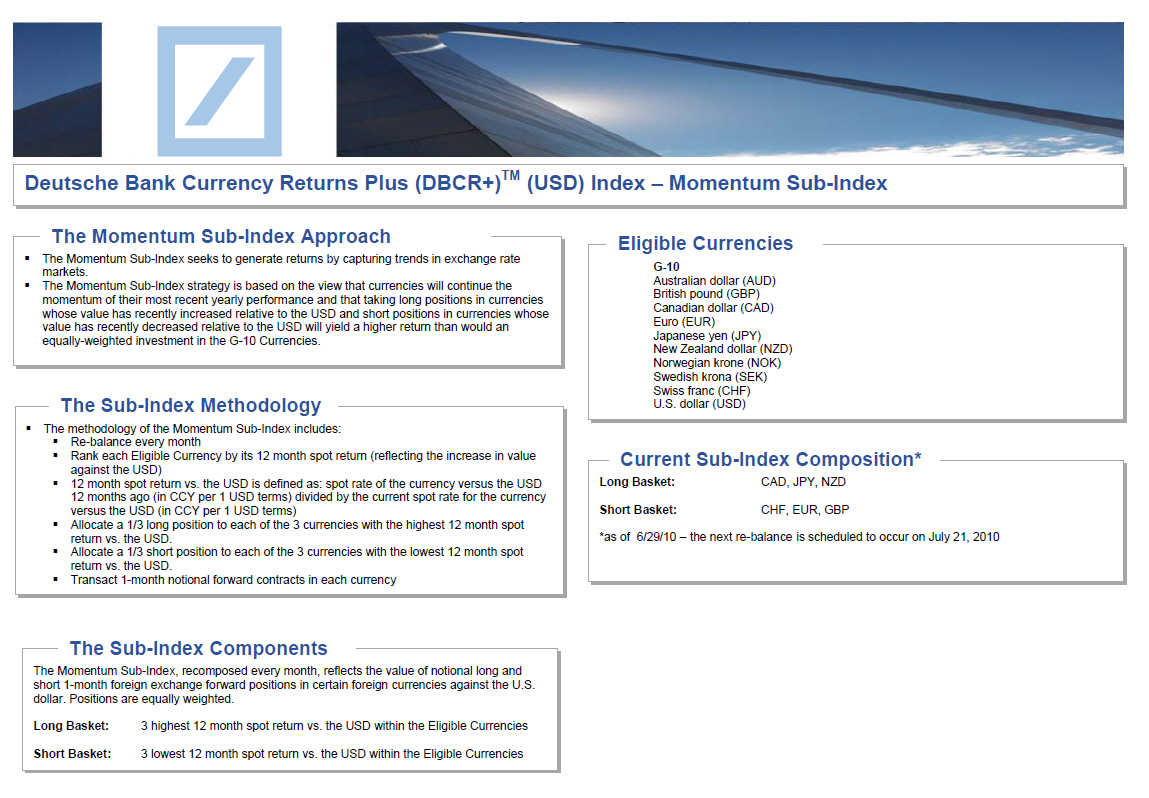

Deutsche Bank Currency Returns Plus (DBCR+) (TM) (USD) Index -- Momentum

Sub-Index

- --------------------------------------------------------------------------------

The Momentum Sub -Index Approach

--------------------------------

* The Momentum Sub-Index seeks to generate returns by capturing trends in

exchange rate markets.

* The Momentum Sub-Index strategy is based on the view that currencies will

continue the momentum of their most recent yearly performance and that

taking long positions in currencies whose value has recently increased

relative to the USD and short positions in currencies whose value has

recently decreased relative to the USD will yield a higher return than

would an equally -weighted investment in the G-10 Currencies.

The Sub-Index Methodology

-------------------------

* The methodology of the Momentum Sub-Index includes:

* Re-balance every month

* Rank each Eligible Currency by its 12 month spot return (reflecting

the increase in value against the USD)

* 12 month spot return vs. the USD is defined as: spot rate of the

currency versus the USD 12 months ago (in CCY per 1 USD terms) divided

by the current spot rate for the currency versus the USD (in CCY per 1

USD terms)

* Allocate a 1/3 long position to each of the 3 currencies with the

highest 12 month spot return vs. the USD.

* Allocate a 1/3 short position to each of the 3 currencies with the

lowest 12 month spot return vs. the USD.

* Transact 1-month notional forward contracts in each currency

The Sub-Index Components

------------------------

The Momentum Sub-Index, recomposed every month, reflects the value of notional

long and short 1-month foreign exchange forward positions in certain foreign

currencies against the U.S. dollar. Positions are equally weighted.

Long Basket: 3 highest 12 month spot return vs. the USD within the Eligible

Currencies

Short Basket: 3 lowest 12 month spot return vs. the USD within the Eligible

Currencies

Eligible Currencies

- -------------------

G-10

Australian dollar (AUD) British pound (GBP) Canadian dollar (CAD) Euro

(EUR) Japanese yen (JPY) New Zealand dollar (NZD) Norwegian krone (NOK)

Swedish krona (SEK) Swiss franc (CHF) U.S. dollar (USD)

Current Sub-Index Composition*

- ------------------------------

Long Basket: CAD, JPY, NZD

Short Basket: CHF, EUR, GBP

*as of 6/29/10 -- the next re-balance is scheduled to occur on July 21, 2010

page 3

|

|

- --------------------------------------------------------------------------------

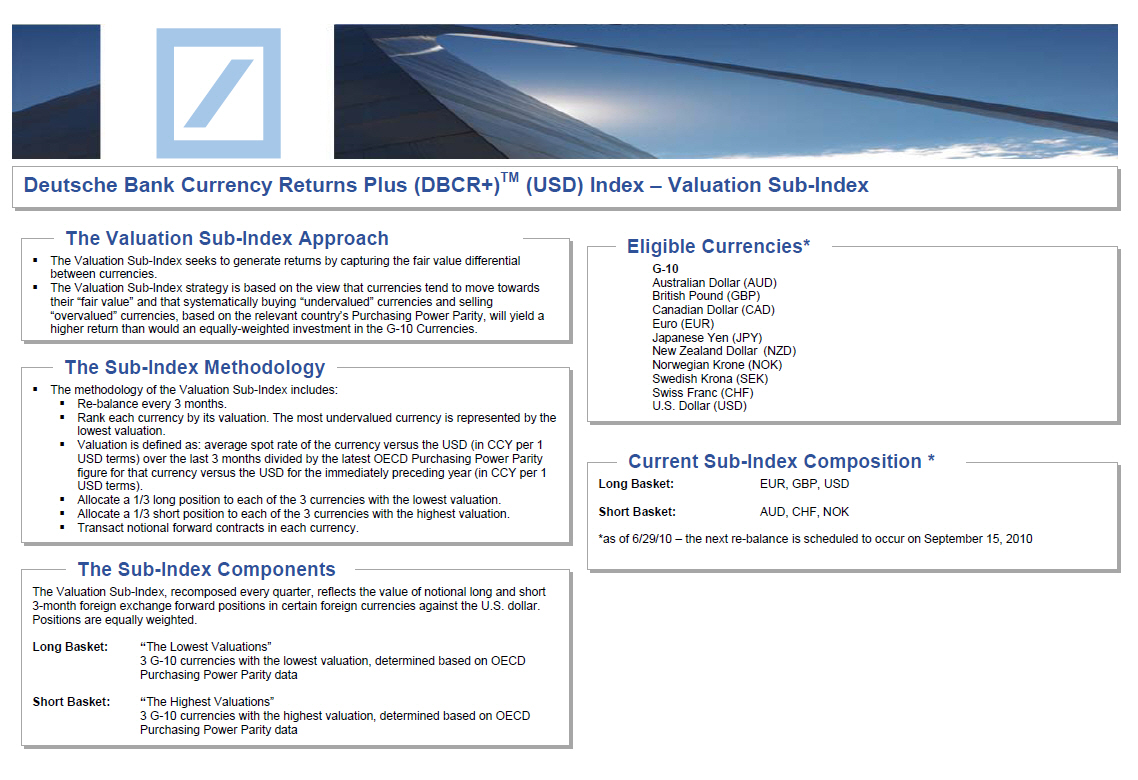

Deutsche Bank Currency Returns Plus (DBCR+) (TM) (USD) Index -- Valuation

Sub-Index

- --------------------------------------------------------------------------------

The Valuation Sub-Index Approach

--------------------------------

* The Valuation Sub-Index seeks to generate returns by capturing the fair

value differential between currencies.

* The Valuation Sub-Index strategy is based on the view that currencies tend

to move towards their "fair value" and that systematically buying

"undervalued" currencies and selling "overvalued" currencies, based on the

relevant country's Purchasing Power Parity, will yield a higher return than

would an equally-weighted investment in the G-10 Currencies.

The Sub-Index Methodology

-------------------------

* The methodology of the Valuation Sub-Index includes:

* Re-balance every 3 months.

* Rank each currency by its valuation. The most undervalued currency is

represented by the lowest valuation.

* Valuation is defined as: average spot rate of the currency versus the

USD (in CCY per 1 USD terms) over the last 3 months divided by the

latest OECD Purchasing Power Parity figure for that currency versus

the USD for the immediately preceding year (in CCY per 1 USD terms).

* Allocate a 1/3 long position to each of the 3 currencies with the

lowest valuation.

* Allocate a 1/3 short position to each of the 3 currencies with the

highest valuation.

* Transact notional forward contracts in each currency.

The Sub-Index Components

------------------------

The Valuation Sub-Index, recomposed every quarter, reflects the value of

notional long and short 3-month foreign exchange forward positions in certain

foreign currencies against the U.S. dollar. Positions are equally weighted.

Long Basket: "The Lowest Valuations"

3 G-10 currencies with the lowest valuation, determined based on

OECD Purchasing Power Parity data

Short Basket: "The Highest Valuations"

3 G-10 currencies with the highest valuation, determined based on

OECD Purchasing Power Parity data

Eligible Currencies*

- --------------------

G-10

Australian Dollar (AUD)

British Pound (GBP)

Canadian Dollar (CAD)

Euro (EUR)

Japanese Yen (JPY)

New Zealand Dollar (NZD)

Norwegian Krone (NOK)

Swedish Krona (SEK)

Swiss Franc (CHF)

U.S. Dollar (USD)

Current Sub-Index Composition*

- ------------------------------

Long Basket: EUR, GBP, USD

Short Basket: AUD, CHF, NOK

*as of 6/29/10 -- the next re-balance is scheduled to occur on September 15,

2010

page 4

|

|

- --------------------------------------------------------------------------------

Index Snapshot -- Deutsche Bank Currency Returns Plus (DBCR+) (TM) (USD) Index

- --------------------------------------------------------------------------------

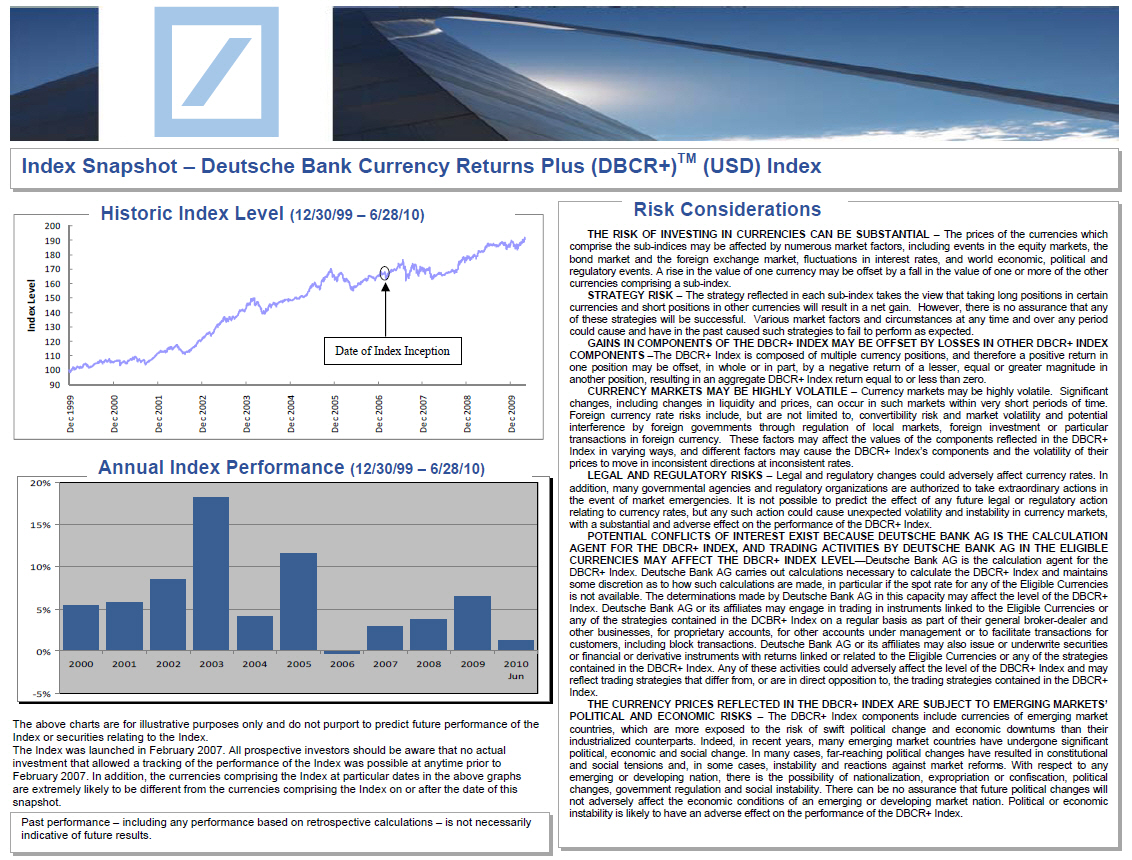

Historic Index Level (12/30/99 -- 6/28/10)

[GRAPHIC OMITTED]

Annual Index Performance (12/30/99 -- 6/28/10)

[GRAPHIC OMITTED]

The above charts are for illustrative purposes only and do not purport to

predict future performance of the Index or securities relating to the Index.

The Index was launched in February 2007. All prospective investors should be

aware that no actual investment that allowed a tracking of the performance of

the Index was possible at anytime prior to February 2007. In addition, the

currencies comprising the Index at particular dates in the above graphs are

extremely likely to be different from the currencies comprising the Index on or

after the date of this snapshot.

- --------------------------------------------------------------------------------

Past performance -- including any performance based on retrospective

calculations -- is not necessarily indicative of future results.

- --------------------------------------------------------------------------------

Risk Considerations

-------------------

THE RISK OF INVESTING IN CURRENCIES CAN BE SUBSTANTIAL -- The prices of the

currencies which comprise the sub-indices may be affected by numerous market

factors, including events in the equity markets, the bond market and the

foreign exchange market, fluctuations in interest rates, and world economic,

political and regulatory events. A rise in the value of one currency may be

offset by a fall in the value of one or more of the other currencies comprising

a sub-index.

STRATEGY RISK -- The strategy reflected in each sub-index takes the view

that taking long positions in certain currencies and short positions in other

currencies will result in a net gain. However, there is no assurance that any

of these strategies will be successful. Various market factors and

circumstances at any time and over any period could cause and have in the past

caused such strategies to fail to perform as expected.

GAINS IN COMPONENTS OF THE DBCR+ INDEX MAY BE OFFSET BY LOSSES IN OTHER

DBCR+ INDEX COMPONENTS --The DBCR+ Index is composed of multiple currency

positions, and therefore a positive return in one position may be offset, in

whole or in part, by a negative return of a lesser, equal or greater magnitude

in another position, resulting in an aggregate DBCR+ Index return equal to or

less than zero.

CURRENCY MARKETS MAY BE HIGHLY VOLATILE -- Currency markets may be highly

volatile. Significant changes, including changes in liquidity and prices, can

occur in such markets within very short periods of time. Foreign currency rate

risks include, but are not limited to, convertibility risk and market

volatility and potential interference by foreign governments through regulation

of local markets, foreign investment or particular transactions in foreign

currency. These factors may affect the values of the components reflected in

the DBCR+ Index in varying ways, and different factors may cause the DBCR+

Index's components and the volatility of their prices to move in inconsistent

directions at inconsistent rates.

LEGAL AND REGULATORY RISKS -- Legal and regulatory changes could adversely

affect currency rates. In addition, many governmental agencies and regulatory

organizations are authorized to take extraordinary actions in the event of

market emergencies. It is not possible to predict the effect of any future

legal or regulatory action relating to currency rates, but any such action

could cause unexpected volatility and instability in currency markets, with a

substantial and adverse effect on the performance of the DBCR+ Index.

POTENTIAL CONFLICTS OF INTEREST EXIST BECAUSE DEUTSCHE BANK AG IS THE

CALCULATION AGENT FOR THE DBCR+ INDEX, AND TRADING ACTIVITIES BY DEUTSCHE BANK

AG IN THE ELIGIBLE CURRENCIES MAY AFFECT THE DBCR+ INDEX LEVEL --Deutsche Bank

AG is the calculation agent for the DBCR+ Index. Deutsche Bank AG carries out

calculations necessary to calculate the DBCR+ Index and maintains some

discretion as to how such calculations are made, in particular if the spot rate

for any of the Eligible Currencies is not available. The determinations made by

Deutsche Bank AG in this capacity may affect the level of the DBCR+ Index.

Deutsche Bank AG or its affiliates may engage in trading in instruments linked

to the Eligible Currencies or any of the strategies contained in the DCBR+

Index on a regular basis as part of their general broker-dealer and other

businesses, for proprietary accounts, for other accounts under management or to

facilitate transactions for customers, including block transactions. Deutsche

Bank AG or its affiliates may also issue or underwrite securities or financial

or derivative instruments with returns linked or related to the Eligible

Currencies or any of the strategies contained in the DBCR+ Index. Any of these

activities could adversely affect the level of the DBCR+ Index and may reflect

trading strategies that differ from, or are in direct opposition to, the

trading strategies contained in the DBCR+ Index.

THE CURRENCY PRICES REFLECTED IN THE DBCR+ INDEX ARE SUBJECT TO EMERGING

MARKETS' POLITICAL AND ECONOMIC RISKS -- The DBCR+ Index components include

currencies of emerging market countries, which are more exposed to the risk of

swift political change and economic downturns than their industrialized

counterparts. Indeed, in recent years, many emerging market countries have

undergone significant political, economic and social change. In many cases,

far-reaching political changes have resulted in constitutional and social

tensions and, in some cases, instability and reactions against market reforms.

With respect to any emerging or developing nation, there is the possibility of

nationalization, expropriation or confiscation, political changes, government

regulation and social instability. There can be no assurance that future

political changes will not adversely affect the economic conditions of an

emerging or developing market nation. Political or economic instability is

likely to have an adverse effect on the performance of the DBCR+ Index.

page 5

|