|

Bloomberg Ticker Issuer Free Writing Prospectus

ER DBCRUSI Filed pursuant to Rule 433

Registration Statement No. 333-162195

Dated: August 5, 2010

DB Currency Returns Index

July 2010

[GRAPHIC OMITTED]

Deutsche Bank's Currency Returns Index has existed since February 2007.

Accordingly, any index performance shown in this presentation preceding that

inception date does not reflect the performance of an actual index, but has

been retrospectively calculated, as described herein.

Deutsche Bank AG has filed a registration statement (including a prospectus)

with the SEC for the offerings to which this communication may relate. Before

you invest, you should read the prospectus in that registration statement and

other documents Deutsche Bank AG has filed with the SEC for more complete

information about Deutsche Bank AG and this offering. You may get these

documents for free by visiting EDGAR on the SEC website at www.sec.gov.

Alternatively, Deutsche Bank AG, any underwriter or any dealer participating in

the offering will arrange to send you the prospectus if you request it by

calling toll-free 1-800-311-4409.

0

|

|

DB Currency Returns Index

Introduction

[] The following 3 strategies reflect widely used FX investment styles -

[] Carry

[] Momentum

[] Valuation

[] These form the core investment approach of a number of FX-only funds.

[] In general, there is a relatively low correlation (1) between the returns

of employing these strategies and the returns gained from investing in more

traditional asset classes such as equities and bonds.

[] DBCR provides benchmark exposure to these systematic strategies. The Index

is constructed by equally weighting the three indices using these trading

strategies.

[] The DBCR Index has delivered annualized excess returns of 2.03% (i. e. ,

returns excluding interest income and calculated as compounded annual

returns from start to end date) from February 2007 to Jun 30, 2010 with a

Sharpe Ratio(2) of 0.33 (i. e. , the annualized excess return divided by

historical annualized volatility of the daily return). Based on

retrospective calculations, the DBCR Index would have achieved annualized

excess returns of 4.91% from January 2000 to February 2007, with a Sharpe

Ratio of 0.94. DB PROVIDES NO ASSURANCE THAT THESE RETURNS OR RATIOS WILL

PREDICT FUTURE RETURNS OR RATIOS.

Source: Deutsche Bank, Dec 28, 2000 to Jun 30, 2010. The DBCR Index was

launched in February 2007. All prospective investors should be aware that no

actual investment that allowed a tracking of the performance of the Index was

possible at any time prior to February 2007, and the Index is constructed by

equally weighting the returns for the three component indices: Carry, Momentum

and Valuation, which themselves did not exist prior to December 2005, March

2007 and March 2007, respectively. The fees and charges in connection with the

Index are reflected in the Index performance both after launch and in simulated

performance prior to February 2007.

1 Correlation analysis is a useful tool in the construction of a diversified

investment portfolio. Combining financial investments that have a series of

returns that behave differently from each other achieves portfolio

diversification. Correlation has been calculated using log of daily returns

(correlation ranges from '-1' to '+1' with '-1' implying returns which are

perfectly opposite to each other, '+1' implying returns which always move in

the same direction, and '0' implying no relationship between the two returns).

2 The Sharpe Ratio is a measure of the excess return per unit of risk in an

investment asset. Here, risk is measured as the standard deviation of the log

of daily returns for the respective Index. The Sharpe

Ratio is used to characterize how well the return of an asset compensates the

investor for the risk taken. A higher Sharpe Ratio is considered more

desirable.

Past performance, historical correlation and Sharpe Ratio, actual or simulated,

are not reliable indicators of future results.

See the risk considerations on page 6.

1

|

|

DB Currency Returns Index

The Three Strategies

Three currency strategies widely used in the currency markets

[] Carry: Carry trades are widely used in the currency markets. In a Carry

trade one systematically sells low interest rate currencies and buys high

interest rate currencies. Such a strategy is based on what is known as

"forward-rate bias" or the "forward premium puzzle," that is, the

expectation that the forward rate is not an unbiased estimate of the future

spot rate. Positive returns will occur under such strategy when an

investor's gain from interest rate differentials between the high yielding

and low yielding jurisdictions exceeds any potential losses from currency

rate movements between the relevant currencies.

[] Momentum: A widely observed feature of currency markets is that many

exchange rates trend on a multi-year basis. This strategy is based on the

view that currencies will continue the momentum of their most recent yearly

performance. Momentum trends are considered to emerge mainly because some

participants in the currency markets act quickly on news while others

respond more slowly. Therefore, a strategy that follows the trend may make

positive returns over time.

[] Valuation: This strategy takes the view that, in the long-run, currencies

tend to move towards their "fair value. " Consequently, systematically

buying "undervalued" currencies and selling "overvalued" currencies may be

profitable for a long term investor. One of the underlying themes of this

strategy is that even if fundamentals might not work for currencies in the

short-to medium-term, they tend to work in the long-term. One of the oldest

measures of "fair value" is "purchasing power parity," which reflects the

comparative price levels of currencies, and this strategy uses purchasing

power parity to assess each currency's relative value.

Over the last few decades, at particular periods of time, each of these

strategies has individually experienced some significant losses. Various market

factors and circumstances at any time and over any period could cause, and have

in the past caused, such strategies to fail to perform as expected. DB provides

no assurance that any of these strategies is or will remain profitable.

2

|

|

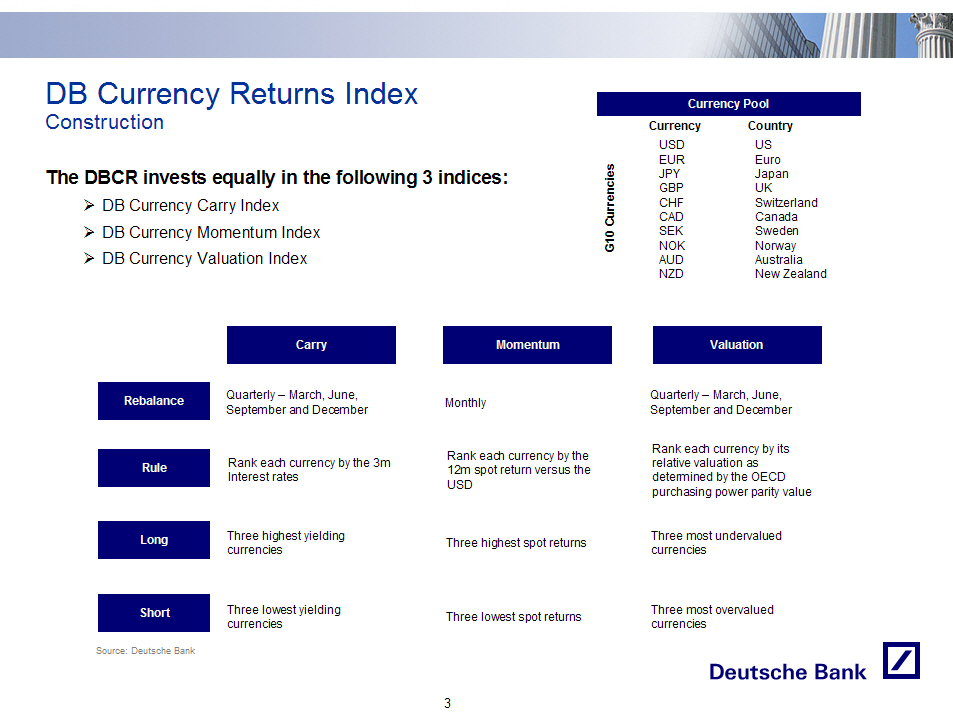

DB Currency Returns Index

Construction

The DBCR invests equally in the following 3 indices:

[] DB Currency Carry Index

[] DB Currency Momentum Index

[] DB Currency Valuation Index

- -------------------------

Currency Pool

- -------------------------

Currency Country

USD US

EUR Euro

JPY Japan

GBP UK

CHF Switzerland

CAD Canada

SEK Sweden

NOK Norway

AUD Australia

NZD New Zealand

Carry Momentum Valuation

- -------------------------------------------------------------------------------------------------

Quarterly -- March, June, Quarterly -- March, June,

Rebalance September and December Monthly September and December

Rank each currency by the Rank each currency by its

Rule Rank each currency by the 3m 12m spot return versus the relative valuation as

Interest rates USD determined by the OECD

USD purchasing power parity value

Long Three highest yielding Three highest spot returns Three most undervalued

currencies currencies

Short Three lowest yielding Three lowest spot returns Three most overvalued

currencies currencies

- -------------------------------------------------------------------------------------------------

Source: Deutsche Bank

3

|

|

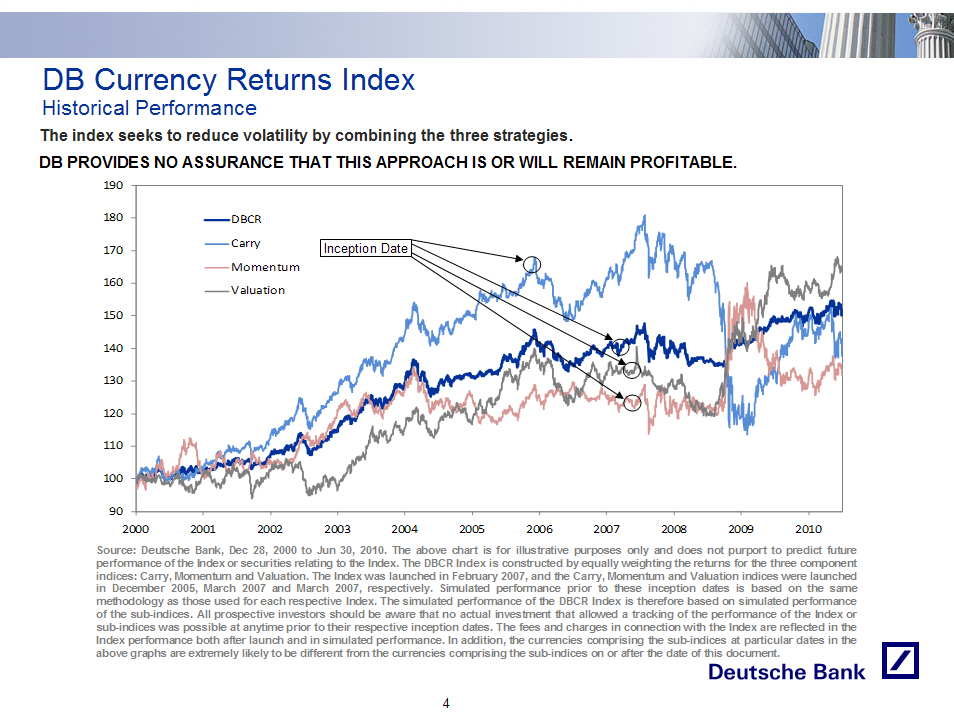

DB Currency Returns Index

Historical Performance

The index seeks to reduce volatility by combining the three strategies.

DB PROVIDES NO ASSURANCE THAT THIS APPROACH IS OR WILL REMAIN PROFITABLE.

[GRAPHIC OMITTED]

Source: Deutsche Bank, Dec 28, 2000 to Jun 30, 2010. The above chart is for

illustrative purposes only and does not purport to predict future performance

of the Index or securities relating to the Index. The DBCR Index is constructed

by equally weighting the returns for the three component indices: Carry,

Momentum and Valuation. The Index was launched in February 2007, and the Carry,

Momentum and Valuation indices were launched in December 2005, March 2007 and

March 2007, respectively. Simulated performance prior to these inception dates

is based on the same methodology as those used for each respective Index. The

simulated performance of the DBCR Index is therefore based on simulated

performance of the sub-indices. All prospective investors should be aware that

no actual investment that allowed a tracking of the performance of the Index or

sub-indices was possible at anytime prior to their respective inception dates.

The fees and charges in connection with the Index are reflected in the Index

performance both after launch and in simulated performance. In addition, the

currencies comprising the sub-indices at particular dates in the above graphs

are extremely likely to be different from the currencies comprising the

sub-indices on or after the date of this document.

4

|

|

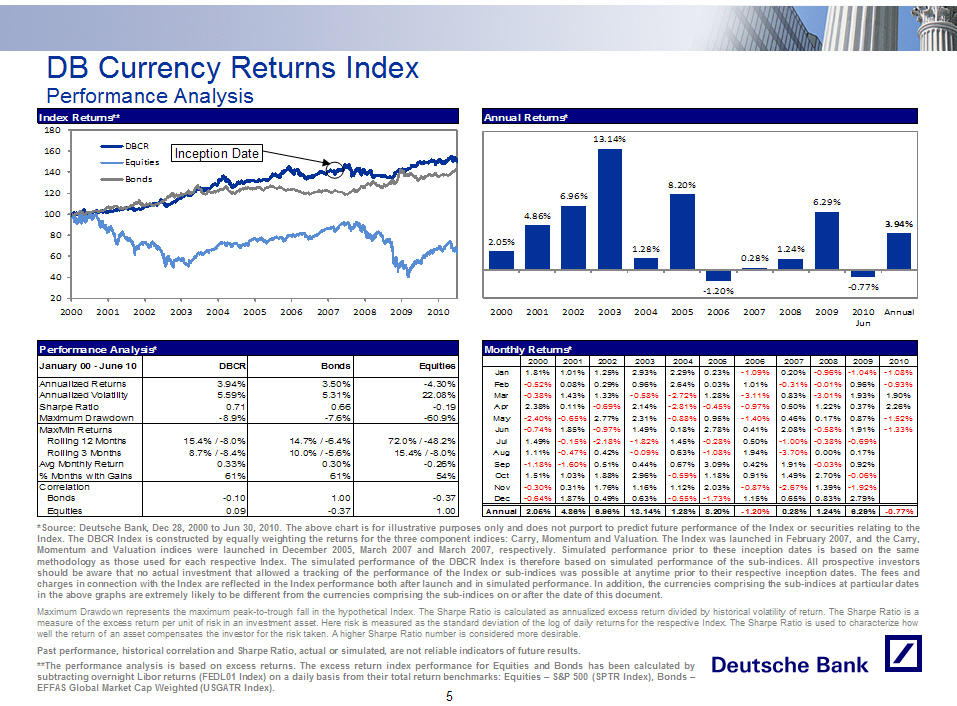

DB Currency Returns Index

Performance Analysis

Index Returns**

- ---------------

[GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

Performance Analysis*

- --------------------------------------------------------------------------------

January 00 - June 10 DBCR Bonds Equities

- --------------------------------------------------------------------------------

Annualized Returns 3.94% 3.50% -4.30%

Annualized Volatility 5.59% 5.31% 22.08%

Sharpe Ratio 0.71 0.66 -0.19

Maximum Drawdown12 -8.9% -7.6% -60.9%

- --------------------------------------------------------------------------------

Max/Min Returns

Rolling 12 Months 15.4% / -8.0% 14.7% / -6.4% 72.0% / -48.2%

Rolling 3 Months 8.7% / -8.4% 10.0% / -5.6% 15.4% / -8.0%

Avg Monthly Return 0.33% 0.30% -0.26%

% Months with Gains 61% 61% 54%

- --------------------------------------------------------------------------------

Correlation

Bonds -0.10 1.00 -0.37

Equities 0.09 -0.37 1.00

- --------------------------------------------------------------------------------

Annual Returns*

- ---------------

[GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

Monthly Returns*

- -----------------------------------------------------------------------------------

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

- -----------------------------------------------------------------------------------

Jan 1.81% 1.01% 1.25% 2.93% 2.29% 0.23% -1.09% 0.20% -0.96% -1.04% -1.08%

Feb -0.52% 0.08% 0.29% 0.96% 2.64% 0.03% 1.01% -0.31% -0.01% 0.96% -0.93%

Mar -0.38% 1.43% 1.33% -0.58% -2.72% 1.28% -3.11% 0.83% -3.01% 1.93% 1.90%

Apr 2.38% 0.11% -0.69% 2.14% -2.81% -0.45% -0.97% 0.50% 1.22% 0.37% 2.26%

May -2.40% -0.65% 2.77% 2.31% -0.88% 0.95% -1.40% 0.46% 0.17% 0.87% -1.52%

Jun -0.74% 1.85% -0.97% 1.49% 0.18% 2.78% 0.41% 2.08% -0.58% 1.91% -1.33%

Jul 1.49% -0.15% -2.18% -1.82% 1.45% -0.28% 0.50% -1.00% -0.38% -0.69%

Aug 1.11% -0.47% 0.42% -0.09% 0.63% -1.08% 1.94% -3.70% 0.00% 0.17%

Sep -1.18% -1.60% 0.51% 0.44% 0.67% 3.09% 0.42% 1.91% -0.03% 0.92%

Oct 1.51% 1.03% 1.88% 2.96% -0.59% 1.18% 0.91% 1.49% 2.70% -0.06%

Nov -0.30% 0.31% 1.76% 1.16% 1.12% 2.03% -0.87% -2.67% 1.39% -1.92%

Dec -0.64% 1.87% 0.49% 0.63% -0.55% -1.73% 1.15% 0.65% 0.83% 2.79%

===================================================================================

Annual 2.05% 4.86% 6.96% 13.14% 1.28% 8.20% -1.20% 0.28% 1.24% 6.29% -0.77%

- -----------------------------------------------------------------------------------

*Source: Deutsche Bank, Dec 28, 2000 to Jun 30, 2010. The above chart is for

illustrative purposes only and does not purport to predict future performance

of the Index or securities relating to the Index. The DBCR Index is constructed

by equally weighting the returns for the three component indices: Carry,

Momentum and Valuation. The Index was launched in February 2007, and the Carry,

Momentum and Valuation indices were launched in December 2005, March 2007 and

March 2007, respectively. Simulated performance prior to these inception dates

is based on the same methodology as those used for each respective Index. The

simulated performance of the DBCR Index is therefore based on simulated

performance of the sub-indices. All prospective investors should be aware that

no actual investment that allowed a tracking of the performance of the Index or

sub-indices was possible at anytime prior to their respective inception dates.

The fees and charges in connection with the Index are reflected in the Index

performance both after launch and in simulated performance. In addition, the

currencies comprising the sub-indices at particular dates in the above graphs

are extremely likely to be different from the currencies comprising the

sub-indices on or after the date of this document.

Maximum Drawdown represents the maximum peak-to-trough fall in the hypothetical

Index. The Sharpe Ratio is calculated as annualized excess return divided by

historical volatility of return. The Sharpe Ratio is a measure of the excess

return per unit of risk in an investment asset. Here risk is measured as the

standard deviation of the log of daily returns for the respective Index. The

Sharpe Ratio is used to characterize how well the return of an asset

compensates the investor for the risk taken. A higher Sharpe Ratio number is

considered more desirable.

Past performance, historical correlation and Sharpe Ratio, actual or simulated,

are not reliable indicators of future results.

**The performance analysis is based on excess returns. The excess return index

performance for Equities and Bonds has been calculated by subtracting overnight

Libor returns (FEDL01 Index) on a daily basis from their total return

benchmarks: Equities -- S and P 500 (SPTR Index), Bonds --EFFAS Global Market Cap

Weighted (USGATR Index).

5

|

|

Certain Risks Relating to the DB Currency Returns Index

[] DBCR HAS LIMITED PERFORMANCE HISTORY -- Publication of DBCR began in

February 2007. Therefore, DBCR has very limited performance history. No

actual investment which allowed tracking of the performance of DBCR was

possible before that date. In addition, each of the sub-indices comprising

the DBCR has limited performance history. The retrospective data contained

herein is based on simulated results for the DBCR Index, which, in turn, is

based on simulated results for each of the sub-indices.

[] THE RISK OF INVESTING IN CURRENCIES CAN BE SUBSTANTIAL -- The prices of the

currencies which comprise the sub-indices may be affected by numerous

market factors, including events in the equity markets, the bond market and

the foreign exchange market, fluctuations in interest rates, and world

economic, political and regulatory events. A rise in the value of one

currency may be offset by a fall in the value of one or more of the other

currencies comprising a sub-index.

[] STRATEGY RISK -- The strategy reflected in each sub-index takes the view

that taking long positions in certain currencies and short positions in

other currencies will result in a net gain. However, there is no assurance

that any of these strategies will be successful. Various market factors and

circumstances at any time and over any period could cause, and have in the

past caused, such strategies to fail to perform as expected.

[] GAINS IN COMPONENTS OF THE DBCR INDEX MAY BE OFFSET BY LOSSES IN OTHER DBCR

INDEX COMPONENTS -- The DBCR Index is composed of multiple currency

positions, and therefore a positive return in one position may be offset,

in whole or in part, by a negative return of a lesser, equal or greater

magnitude in another position, resulting in an aggregate DBCR Index return

equal to or less than zero.

[] CURRENCY MARKETS MAY BE HIGHLY VOLATILE -- Currency markets may be highly

volatile. Significant changes, including changes in liquidity and prices,

can occur in such markets within very short periods of time. Foreign

currency rate risks include, but are not limited to, convertibility risk

and market volatility and potential interference by foreign governments

through regulation of local markets, foreign investment or particular

transactions in foreign currency. These factors may affect the values of

the components reflected in the DBCR Index in varying ways, and different

factors may cause the DBCR Index's components and the volatility of their

prices to move in inconsistent directions at inconsistent rates.

[] LEGAL AND REGULATORY RISKS -- Legal and regulatory changes could adversely

affect currency rates. In addition, many governmental agencies and

regulatory organizations are authorized to take extraordinary actions in

the event of market emergencies. It is not possible to predict the effect

of any future legal or regulatory action relating to currency rates, but

any such action could cause unexpected volatility and instability in

currency markets, with a substantial and adverse effect on the performance

of the DBCR Index.

[] POTENTIAL CONFLICTS OF INTEREST EXIST BECAUSE DEUTSCHE BANK AG IS THE

CALCULATION AGENT FOR THE DBCR INDEX, AND TRADING ACTIVITIES BY DEUTSCHE

BANK AG IN THE ELIGIBLE CURRENCIES MAY AFFECT THE DBCR INDEX LEVEL --

Deutsche Bank AG is the calculation agent for the DBCR Index. Deutsche Bank

AG carries out calculations necessary to calculate the DBCR Index and

maintains some discretion as to how such calculations are made, in

particular if the spot rate for any of the Eligible Currencies is not

available. The determinations made by Deutsche Bank AG in this capacity may

affect the level of the DBCR Index. Deutsche Bank AG or its affiliates may

engage in trading in instruments linked to the Eligible Currencies or any

of the strategies contained in the DCBR Index on a regular basis as part of

their general broker-dealer and other businesses, for proprietary accounts,

for other accounts under management or to facilitate transactions for

customers, including block transactions. Deutsche Bank AG or its affiliates

may also issue or underwrite securities or financial or derivative

instruments with returns linked or related to the Eligible Currencies or

any of the strategies contained in the DBCR Index. Any of these activities

could adversely affect the level of the DBCR Index and may reflect trading

strategies that differ from, or are in direct opposition to, the trading

strategies contained in the DBCR Index.

[] LIMITED ACCESS TO INDEX, AND ASSOCIATED COSTS -- Access to the index may be

available only through the use of an investment vehicle. In such instances,

the performance of any investment product based on the DBCR Index will be

lower than the performance of the DBCR Index because of fees, costs, and

product features. In such offerings, investors should rely on the

information provided in the offering memorandum or prospectus. Past

performance, including any performance based on retrospective calculations,

of the DBCR Index and its sub-indices is not necessarily indicative of

future results.

6

|

|

Appendix 1:

The Underlying Indices

[GRAPHIC OMITTED]

7

|

|

DB Currency Carry Index

Bloomberg Ticker : DBHTG10E

[] The Carry Index seeks to generate returns by capturing the interest rate

differential or "carry" between baskets of high-yielding and low-yielding

currencies.

[] The Carry Index strategy is based on the view that foreign currency forward

rates are biased estimators of future foreign currency spot rates, and that

currencies that trade at a forward discount often outperform currencies

that trade at a forward premium.

[] This strategy takes the view that by taking long positions in high-yielding

currencies and short positions in low-yielding currencies, an investor's

gain from interest rate differentials in the high- yielding jurisdictions

will exceed any potential losses from currency exchange rate risk.

[] Over the last few decades, at particular periods of time, this strategy has

individually experienced some significant losses. Various market factors

and circumstances at any time and over any period could cause, and have in

the past caused, this strategy to fail to perform as expected.

[] The DB Currency Carry Index strategy is implemented as follows:

[] Re-balance every 3 months

[] Rank each currency by its 3-month interest rate

[] Allocate a 1/3 long position to each of the three currencies with the

highest 3-month interest rate

[] Allocate a 1/3 short position to each of the three currencies with the

lowest 3-month interest rate

[] Transact forward contracts in each currency to reflect the above

8

|

|

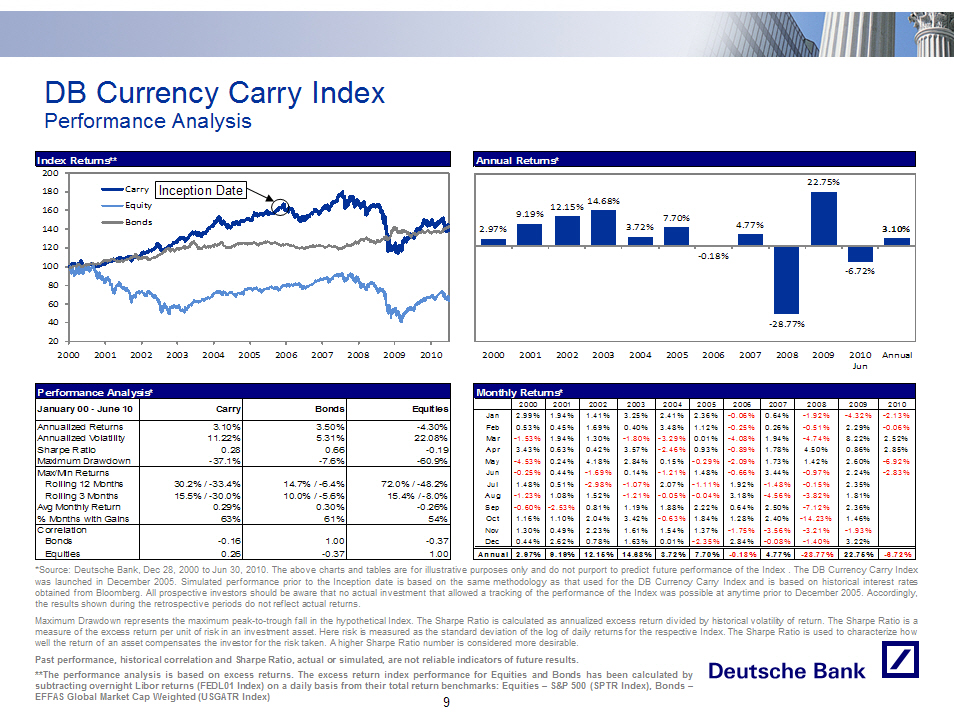

DB Currency Carry Index

Performance Analysis

Index Returns**

- ---------------

[GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

Performance Analysis*

- --------------------------------------------------------------------------------

January 00 - June 10 Carry Bonds Equities

- --------------------------------------------------------------------------------

Annualized Returns 3.10% 3.50% -4.30%

Annualized Volatility 11.22% 5.31% 22.08%

Sharpe Ratio 0.28 0.66 -0.19

Maximum Drawdown -37.1% -7.6% -60.9%

- --------------------------------------------------------------------------------

Max/Min Returns

Rolling 12 Months 30.2% / -33.4% 14.7% / -6.4% 72.0% / -48.2%

Rolling 3 Months 15.5% / -30.0% 10.0% / -5.6% 15.4% / -8.0%

Avg Monthly Return 0.29% 0.30% -0.26%

% Months with Gains 63% 61% 54%

- --------------------------------------------------------------------------------

Correlation

Bonds -0.16 1.00 -0.37

Equities 0.26 -0.37 1.00

- --------------------------------------------------------------------------------

Annual Returns*

- ---------------

[GRAPHIC OMITTED]

- ------------------------------------------------------------------------------------

Monthly Returns*

- ------------------------------------------------------------------------------------

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

- ------------------------------------------------------------------------------------

Jan 2.99% 1.94% 1.41% 3.25% 2.41% 2.36% -0.06% 0.64% -1.92% -4.32% -2.13%

Feb 0.53% 0.45% 1.69% 0.40% 3.48% 1.12% -0.25% 0.26% -0.51% 2.29% -0.06%

Mar -1.53% 1.94% 1.30% -1.80% -3.29% 0.01% -4.08% 1.94% -4.74% 8.22% 2.52%

Apr 3.43% 0.63% 0.42% 3.57% -2.46% 0.93% -0.89% 1.78% 4.50% 0.86% 2.85%

May -4.53% 0.24% 4.18% 2.84% 0.15% -0.29% -2.09% 1.73% 1.42% 2.60% -6.92%

Jun -0.25% 0.44% -1.69% 0.14% -1.21% 1.48% -0.66% 3.44% -0.97% 2.24% -2.83%

Jul 1.48% 0.51% -2.98% -1.07% 2.07% -1.11% 1.92% -1.48% -0.15% 2.35%

Aug -1.23% 1.08% 1.52% -1.21% -0.05% -0.04% 3.18% -4.56% -3.82% 1.81%

Sep -0.60% -2.53% 0.81% 1.19% 1.88% 2.22% 0.64% 2.50% -7.12% 2.36%

Oct 1.16% 1.10% 2.04% 3.42% -0.63% 1.84% 1.28% 2.40% -14.23% 1.46%

Nov 1.30% 0.49% 2.23% 1.61% 1.54% 1.37% -1.75% -3.56% -3.21% -1.93%

Dec 0.44% 2.62% 0.78% 1.63% 0.01% -2.35% 2.84% -0.08% -1.40% 3.22%

====================================================================================

Annual 2.97% 9.19% 12.15% 14.68% 3.72% 7.70% -0.18% 4.77% -28.77% 22.75% -6.72%

- ------------------------------------------------------------------------------------

*Source: Deutsche Bank, Dec 28, 2000 to Jun 30, 2010. The above charts and

tables are for illustrative purposes only and do not purport to predict future

performance of the Index. The DB Currency Carry Index was launched in December

2005. Simulated performance prior to the Inception date is based on the same

methodology as that used for the DB Currency Carry Index and is based on

historical interest rates obtained from Bloomberg. All prospective investors

should be aware that no actual investment that allowed a tracking of the

performance of the Index was possible at anytime prior to December 2005.

Accordingly, the results shown during the retrospective periods do not reflect

actual returns.

Maximum Drawdown represents the maximum peak-to-trough fall in the hypothetical

Index. The Sharpe Ratio is calculated as annualized excess return divided by

historical volatility of return. The Sharpe Ratio is a measure of the excess

return per unit of risk in an investment asset. Here risk is measured as the

standard deviation of the log of daily returns for the respective Index. The

Sharpe Ratio is used to characterize how well the return of an asset

compensates the investor for the risk taken. A higher Sharpe Ratio number is

considered more desirable.

Past performance, historical correlation and Sharpe Ratio, actual or simulated,

are not reliable indicators of future results.

**The performance analysis is based on excess returns. The excess return index

performance for Equities and Bonds has been calculated by subtracting overnight

Libor returns (FEDL01 Index) on a daily basis from their total return

benchmarks: Equities -- S and P 500 (SPTR Index), Bonds --EFFAS Global Market Cap

Weighted (USGATR Index)

9

|

|

DB Currency Momentum Index

Bloomberg Ticker : DBMOMUSF

[] The Momentum Index seeks to generate returns by capturing trends in

exchange rate markets.

[] The Momentum Index strategy is based on the view that currencies will

continue the momentum of their most recent yearly performance and that

taking long positions in currencies whose value has recently increased

relative to the USD and short positions in currencies whose value has

recently decreased relative to the USD will yield a higher return than

would an equally-weighted investment in the G-10 Currencies.

[] Over the last few decades, at particular periods of time, this strategy has

individually experienced some significant losses. Various market factors

and circumstances at any time and over any period could cause, and have in

the past caused, this strategy to fail to perform as expected.

[] The DB Currency Momentum Index strategy is implemented as follows

[] Re-balance every month

[] Rank each Currency by its 12-month spot return vs. the USD

[] 12-month Spot Return vs. the USD is defined as: spot rate of the

currency versus the USD 12 months ago (in units of currency per 1 USD

terms) divided by the current spot rate for the currency versus the

USD (in units of currency per 1 USD terms

[] Allocate a 1/3 long position to each of the three currencies with the

highest 12-month spot return vs. the USD

[] Allocate a 1/3 short position to each of the three currencies with the

lowest 12-month spot return vs. the USD

[] Transact forward contracts in each currency to reflect the above

10

|

|

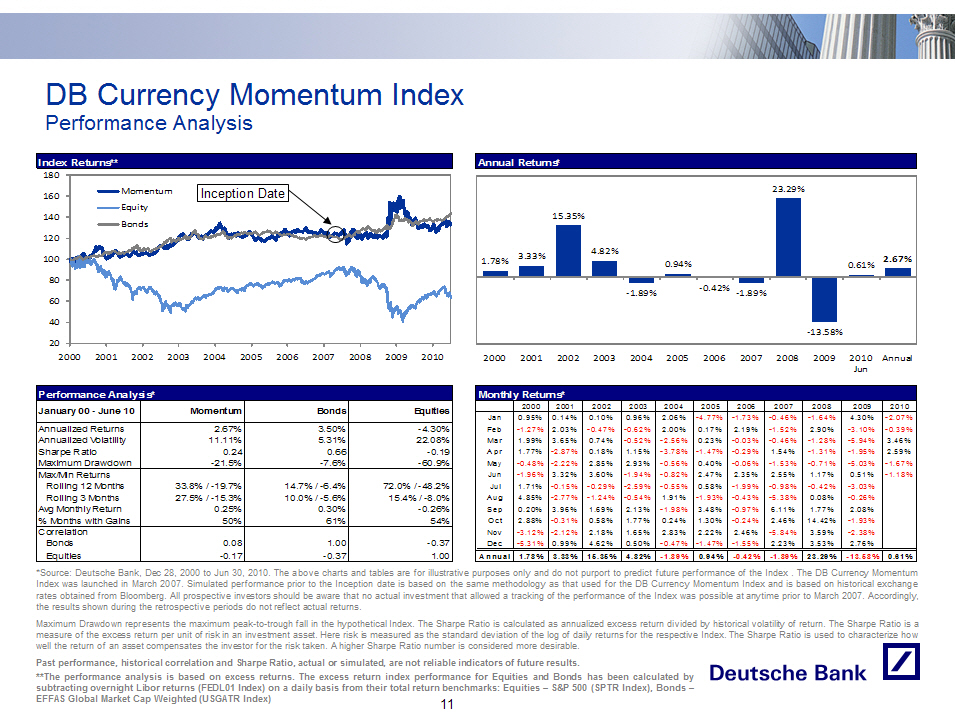

DB Currency Momentum Index

Performance Analysis

Index Returns**

- ---------------

[GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

Performance Analysis*

- --------------------------------------------------------------------------------

January 00 - June 10 Momentum Bonds Equities

- --------------------------------------------------------------------------------

Annualized Returns 2.67% 3.50% -4.30%

Annualized Volatility 11.11% 5.31% 22.08%

Sharpe Ratio 0.24 0.66 -0.19

Maximum Drawdown -21.5% -7.6% -60.9%

- --------------------------------------------------------------------------------

Max/Min Returns

Rolling 12 Months 33.8% / -19.7% 14.7% / -6.4% 72.0% / -48.2%

Rolling 3 Months 27.5% / -15.3% 10.0% / -5.6% 15.4% / -8.0%

Avg Monthly Return 0.25% 0.30% -0.26%

% Months with Gains 50% 61% 54%

- --------------------------------------------------------------------------------

Correlation

Bonds 0.08 1.00 -0.37

Equities -0.17 -0.37 1.00

- --------------------------------------------------------------------------------

Annual Returns*

- ---------------

[GRAPHIC OMITTED]

- ------------------------------------------------------------------------------------

Monthly Returns*

- ------------------------------------------------------------------------------------

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

- ------------------------------------------------------------------------------------

Jan 0.95% 0.14% 0.10% 0.96% 2.06% -4.77% -1.73% -0.46% -1.64% 4.30% -2.07%

Feb -1.27% 2.03% -0.47% -0.62% 2.00% 0.17% 2.19% -1.52% 2.90% -3.10% -0.39%

Mar 1.99% 3.65% 0.74% -0.52% -2.56% 0.23% -0.03% -0.46% -1.28% -5.94% 3.46%

Apr 1.77% -2.87% 0.18% 1.15% -3.78% -1.47% -0.29% 1.54% -1.31% -1.95% 2.59%

May -0.48% -2.22% 2.85% 2.93% -0.56% 0.40% -0.06% -1.53% -0.71% -5.03% -1.67%

Jun -1.96% 3.32% 3.60% -1.94% -0.82% 2.47% 2.35% 2.55% 1.17% 0.51% -1.18%

Jul 1.71% -0.15% -0.29% -2.59% -0.55% 0.58% -1.99% -0.98% -0.42% -3.03%

Aug 4.85% -2.77% -1.24% -0.54% 1.91% -1.93% -0.43% -5.38% 0.08% -0.26%

Sep 0.20% 3.96% 1.69% 2.13% -1.98% 3.48% -0.97% 6.11% 1.77% 2.08%

Oct 2.88% -0.31% 0.58% 1.77% 0.24% 1.30% -0.24% 2.46% 14.42% -1.93%

Nov -3.12% -2.12% 2.18% 1.65% 2.83% 2.22% 2.46% -5.84% 3.59% -2.38%

Dec -5.31% 0.99% 4.62% 0.50% -0.47% -1.47% -1.55% 2.23% 3.53% 2.76%

====================================================================================

Annual 1.78% 3.33% 15.35% 4.82% -1.89% 0.94% -0.42% -1.89% 23.29% -13.58% 0.61%

- ------------------------------------------------------------------------------------

*Source: Deutsche Bank, Dec 28, 2000 to Jun 30, 2010. The above charts and

tables are for illustrative purposes only and do not purport to predict future

performance of the Index . The DB Currency Momentum Index was launched in March

2007. Simulated performance prior to the Inception date is based on the same

methodology as that used for the DB Currency Momentum Index and is based on

historical exchange rates obtained from Bloomberg. All prospective investors

should be aware that no actual investment that allowed a tracking of the

performance of the Index was possible at anytime prior to March 2007.

Accordingly, the results shown during the retrospective periods do not reflect

actual returns.

Maximum Drawdown represents the maximum peak-to-trough fall in the hypothetical

Index. The Sharpe Ratio is calculated as annualized excess return divided by

historical volatility of return. The Sharpe Ratio is a measure of the excess

return per unit of risk in an investment asset. Here risk is measured as the

standard deviation of the log of daily returns for the respective Index. The

Sharpe Ratio is used to characterize how well the return of an asset

compensates the investor for the risk taken. A higher Sharpe Ratio number is

considered more desirable.

Past performance, historical correlation and Sharpe Ratio, actual or simulated,

are not reliable indicators of future results.

**The performance analysis is based on excess returns. The excess return index

performance for Equities and Bonds has been calculated by subtracting overnight

Libor returns (FEDL01 Index) on a daily basis from their total return

benchmarks: Equities -- S and P 500 (SPTR Index), Bonds --EFFAS Global Market Cap

Weighted (USGATR Index)

11

|

|

DB Currency Valuation Index

Bloomberg Ticker : DBPPPUSF

[] The Valuation Index seeks to generate returns by capturing the fair value

differential between currencies.

[] The Valuation Index strategy is based on the view that currencies tend to

move towards their "fair value" and that systematically buying

"undervalued" currencies and selling "overvalued" currencies, based on the

relevant country's purchasing power parity, will yield a higher return than

would an equally-weighted investment in the G-10 Currencies.

[] Over the last few decades, at particular periods of time, this strategy has

individually experienced some significant losses. Various market factors

and circumstances at any time and over any period could cause, and have in

the past caused, this strategy to fail to perform as expected.

[] The DB Currency Valuation Index strategy is implemented as follows:

[] Re-balance every 3 months

[] Rank each currency by its valuation. The most undervalued currency is

represented by the highest Valuation Currency Fix Rate.

[] Valuation Currency Fix Rate is defined as: Average spot level of the

currency versus the USD (in units of currency per 1 USD terms) over

the last 3 months divided by the latest yearly Organization for

Economic Co-operation and Development (OECD) purchasing power parity

figure for that currency versus the USD (in units of currency per 1

USD terms)

[] Allocate a 1/3 long position to each of the three currencies with the

lowest valuation

[] Allocate a 1/3 short position to each of the three currencies with the

highest valuation

[] Transact forward contracts in each currency to reflect the above

12

|

|

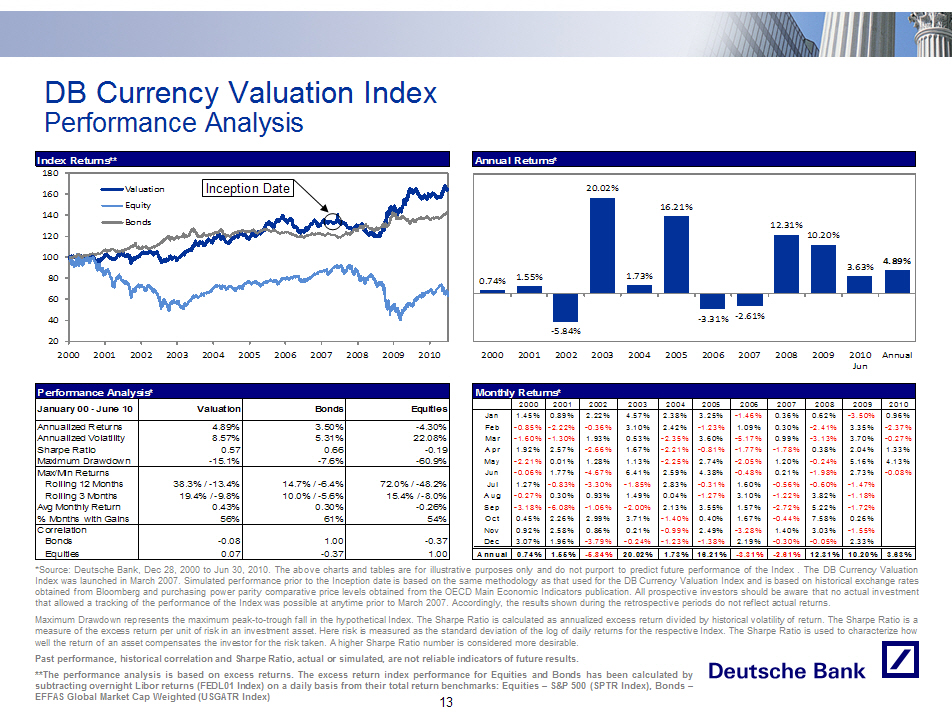

DB Currency Valuation Index

Performance Analysis

Index Returns**

- ---------------

[GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

Performance Analysis*

- --------------------------------------------------------------------------------

January 00 - June 10 Valuation Bonds Equities

- --------------------------------------------------------------------------------

Annualized Returns 4.89% 3.50% -4.30%

Annualized Volatility 8.57% 5.31% 22.08%

Sharpe Ratio 0.57 0.66 -0.19

Maximum Drawdown -15.1% -7.6% -60.9%

- --------------------------------------------------------------------------------

Max/Min Returns

Rolling 12 Months 38.3% / -13.4% 14.7% / -6.4% 72.0% / -48.2%

Rolling 3 Months 19.4% / -9.8% 10.0% / -5.6% 15.4% / -8.0%

Avg Monthly Return 0.43% 0.30% -0.26%

% Months with Gains 56% 61% 54%

- --------------------------------------------------------------------------------

Correlation

Bonds -0.08 1.00 -0.37

Equities 0.07 -0.37 1.00

- --------------------------------------------------------------------------------

Annual Returns*

- ---------------

[GRAPHIC OMITTED]

- --------------------------------------------------------------------------------

Monthly Returns*

- --------------------------------------------------------------------------------

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

- --------------------------------------------------------------------------------

Jan 1.45% 0.89% 2.22% 4.57% 2.38% 3.25% -1.46% 0.36% 0.62% -3.50% 0.96%

Feb -0.85% -2.22% -0.36% 3.10% 2.42% -1.23% 1.09% 0.30% -2.41% 3.35% -2.37%

Mar -1.60% -1.30% 1.93% 0.53% -2.35% 3.60% -5.17% 0.99% -3.13% 3.70% -0.27%

Apr 1.92% 2.57% -2.66% 1.67% -2.21% -0.81% -1.77% -1.78% 0.38% 2.04% 1.33%

May -2.21% 0.01% 1.28% 1.13% -2.25% 2.74% -2.05% 1.20% -0.24% 5.16% 4.13%

Jun -0.06% 1.77% -4.67% 6.41% 2.59% 4.38% -0.48% 0.21% -1.98% 2.73% -0.08%

Jul 1.27% -0.83% -3.30% -1.85% 2.83% -0.31% 1.60% -0.56% -0.60% -1.47%

Aug -0.27% 0.30% 0.93% 1.49% 0.04% -1.27% 3.10% -1.22% 3.82% -1.18%

Sep -3.18% -6.08% -1.06% -2.00% 2.13% 3.55% 1.57% -2.72% 5.22% -1.72%

Oct 0.45% 2.26% 2.99% 3.71% -1.40% 0.40% 1.67% -0.44% 7.58% 0.26%

Nov 0.92% 2.58% 0.86% 0.21% -0.99% 2.49% -3.28% 1.40% 3.03% -1.55%

Dec 3.07% 1.96% -3.79% -0.24% -1.23% -1.38% 2.19% -0.30% -0.05% 2.33%

================================================================================

Annual 0.74% 1.55% -5.84% 20.02% 1.73% 16.21% -3.31% -2.61% 12.31% 10.20% 3.63%

- --------------------------------------------------------------------------------

*Source: Deutsche Bank, Dec 28, 2000 to Jun 30, 2010. The above charts and

tables are for illustrative purposes only and do not purport to predict future

performance of the Index . The DB Currency Valuation Index was launched in

March 2007. Simulated performance prior to the Inception date is based on the

same methodology as that used for the DB Currency Valuation Index and is based

on historical exchange rates obtained from Bloomberg and purchasing power

parity comparative price levels obtained from the OECD Main Economic Indicators

publication. All prospective investors should be aware that no actual

investment that allowed a tracking of the performance of the Index was possible

at anytime prior to March 2007. Accordingly, the results shown during the

retrospective periods do not reflect actual returns.

Maximum Drawdown represents the maximum peak-to-trough fall in the hypothetical

Index. The Sharpe Ratio is calculated as annualized excess return divided by

historical volatility of return. The Sharpe Ratio is a measure of the excess

return per unit of risk in an investment asset. Here risk is measured as the

standard deviation of the log of daily returns for the respective Index. The

Sharpe Ratio is used to characterize how well the return of an asset

compensates the investor for the risk taken. A higher Sharpe Ratio number is

considered more desirable.

Past performance, historical correlation and Sharpe Ratio, actual or simulated,

are not reliable indicators of future results.

**The performance analysis is based on excess returns. The excess return index

performance for Equities and Bonds has been calculated by subtracting overnight

Libor returns (FEDL01 Index) on a daily basis from their total return

benchmarks: Equities -- S and P 500 (SPTR Index), Bonds --EFFAS Global Market Cap

Weighted (USGATR Index)

13

|