Issuer Free Writing Prospectus Filed pursuant to Rule 433 Registration Statement No. 333-162195 Dated: November 8, 2010 | |

|

Global Markets Equity

Liquid Alpha

Liquid Alpha USD 5 Excess Return Index

DBLAUE5J

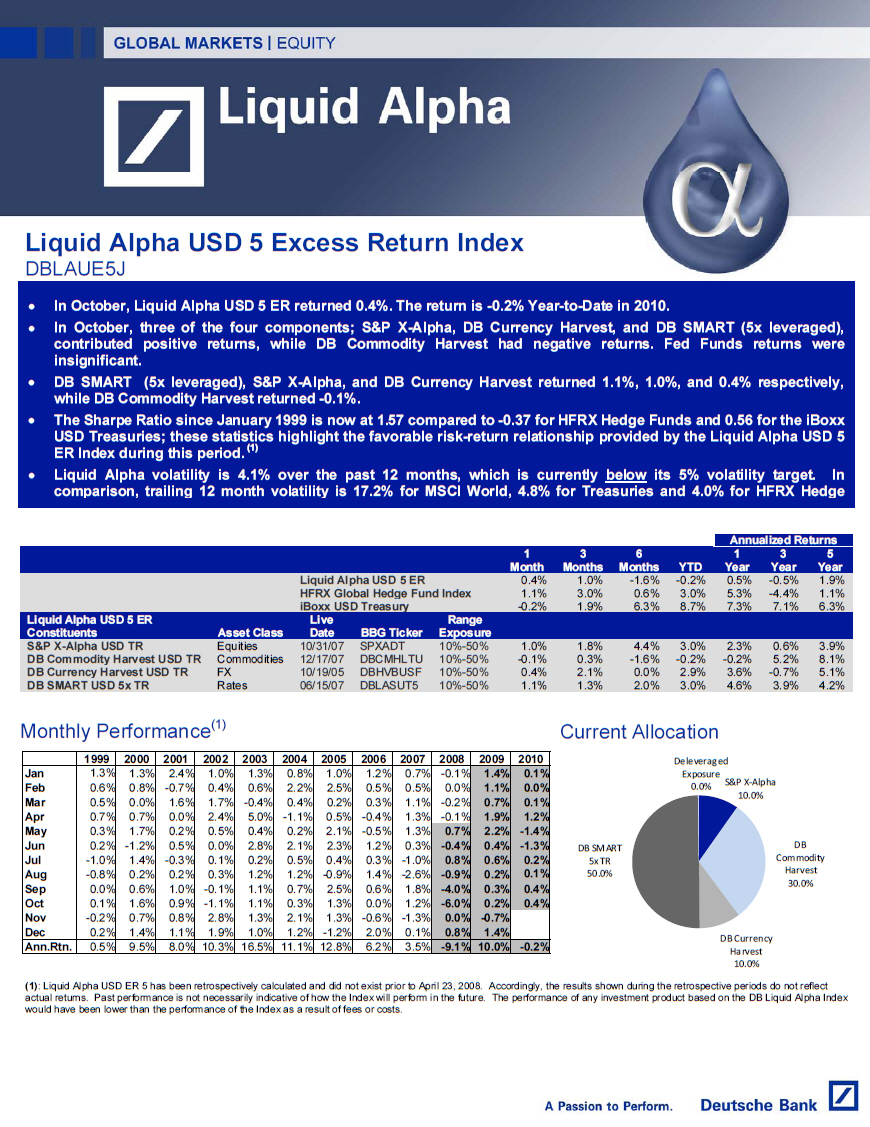

[] In October, Liquid Alpha USD 5 ER returned 0.4%. The return is -0.2%

Year-to-Date in 2010.

[] In October, three of the four components; S and P X-Alpha, DB Currency

Harvest, and DB SMART (5x leveraged), contributed positive returns, while

DB Commodity Harvest had negative returns. Fed Funds returns were

insignificant.

[] DB SMART (5x leveraged), S and P X-Alpha, and DB Currency Harvest returned

1.1%, 1.0%, and 0.4% respectively, while DB Commodity Harvest returned

-0.1%.

[] The Sharpe Ratio since January 1999 is now at 1.57 compared to -0.37 for

HFRX Hedge Funds and 0.56 for the iBoxx USD Treasuries; these statistics

highlight the favorable risk-return relationship provided by the Liquid

Alpha USD 5 ER Index during this period. (1)

[] Liquid Alpha volatility is 4.1% over the past 12 months, which is currently

below its 5% volatility target. In comparison, trailing 12 month volatility

is 17.2% for MSCI World, 4.8% for Treasuries and 4.0% for HFRX Hedge

Annualized Returns

1 3 6 1 3 5

Month Months Months YTD Year Year Year

Liquid Alpha USD 5 ER 0.4% 1.0% -1.6% -0.2% 0.5% -0.5% 1.9%

HFRX Global Hedge Fund Index 1.1% 3.0% 0.6% 3.0% 5.3% -4.4% 1.1%

iBoxx USD Treasury -0.2% 1.9% 6.3% 8.7% 7.3% 7.1% 6.3%

Liquid Alpha USD 5 ER Live Range

Constituents Asset Class Date BBG Ticker Exposure

S and P X-Alpha USD TR Equities 10/31/07 SPXADT 10%-50% 1.0% 1.8% 4.4% 3.0% 2.3% 0.6% 3.9%

DB Commodity Harvest USD TR Commodities 12/17/07 DBCMHLTU 10%-50% -0.1% 0.3% -1.6% -0.2% -0.2% 5.2% 8.1%

DB Currency Harvest USD TR FX 10/19/05 DBHVBUSF 10%-50% 0.4% 2.1% 0.0% 2.9% 3.6% -0.7% 5.1%

DB SMART USD 5x TR Rates 06/15/07 DBLASUT5 10%-50% 1.1% 1.3% 2.0% 3.0% 4.6% 3.9% 4.2%

Monthly Performance(1)

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

Jan 1.3% 1.3% 2.4% 1.0% 1.3% 0.8% 1.0% 1.2% 0.7% -0.1% 1.4% 0.1%

Feb 0.6% 0.8% -0.7% 0.4% 0.6% 2.2% 2.5% 0.5% 0.5% 0.0% 1.1% 0.0%

Mar 0.5% 0.0% 1.6% 1.7% -0.4% 0.4% 0.2% 0.3% 1.1% -0.2% 0.7% 0.1%

Apr 0.7% 0.7% 0.0% 2.4% 5.0% -1.1% 0.5% -0.4% 1.3% -0.1% 1.9% 1.2%

May 0.3% 1.7% 0.2% 0.5% 0.4% 0.2% 2.1% -0.5% 1.3% 0.7% 2.2% -1.4%

Jun 0.2% -1.2% 0.5% 0.0% 2.8% 2.1% 2.3% 1.2% 0.3% -0.4% 0.4% -1.3%

Jul -1.0% 1.4% -0.3% 0.1% 0.2% 0.5% 0.4% 0.3% -1.0% 0.8% 0.6% 0.2%

Aug -0.8% 0.2% 0.2% 0.3% 1.2% 1.2% -0.9% 1.4% -2.6% -0.9% 0.2% 0.1%

Sep 0.0% 0.6% 1.0% -0.1% 1.1% 0.7% 2.5% 0.6% 1.8% -4.0% 0.3% 0.4%

Oct 0.1% 1.6% 0.9% -1.1% 1.1% 0.3% 1.3% 0.0% 1.2% -6.0% 0.2% 0.4%

Nov -0.2% 0.7% 0.8% 2.8% 1.3% 2.1% 1.3% -0.6% -1.3% 0.0% -0.7%

Dec 0.2% 1.4% 1.1% 1.9% 1.0% 1.2% -1.2% 2.0% 0.1% 0.8% 1.4%

Ann.Rtn. 0.5% 9.5% 8.0% 10.3% 16.5% 11.1% 12.8% 6.2% 3.5% -9.1% 10.0% -0.2%

(1): Liquid Alpha USD ER 5 has been retrospectively calculated and did not exist

prior to April 23, 2008. Accordingly, the results shown during the retrospective

periods do not reflect actual returns. Past performance is not necessarily

indicative of how the Index will perform in the future. The performance of any

investment product based on the DB Liquid Alpha Index would have been lower than

the performance of the Index as a result of fees or costs.

Current Allocation

[GRAPHIC OMITTED]

|

|

Overview

- - Liquid Alpha USD 5 ER is a multi-asset medium- to long-term investment

strategy which gives access to a diversified pool of alpha generating

assets using a dynamic allocation tool

- - The strategy has the objective to generate absolute non-directional

returns, un-correlated to the traditional markets, through a combination of

diversified proprietary alpha generating strategies from different asset

classes. The Index has been live since April 23, 2008

- - The allocation among the Underlying Indices occurs quarterly and is based

on their returns, correlation and volatilities using a quantitative Mean

Variance Optimizer model

- - The quantitative model combines the different sources of alpha and cash to

generate an Index with a target volatility of 5%

- - Seeks to manage downside risk through a stop-loss mechanism which is

triggered if the Index return over 60-business days is below 4% over any 3

consecutive days

Performance Analysis Jan 99 -- Oct 10(1)

Liquid Alpha 5% iBoxx USD HFRX Global Hedge

USD ER Treasury Fund Index

Annualized Return 6.5% 5.7% 2.3%

Volatility 4.1% 4.8% 4.0%

Sharpe Ratio(2) (3.01%) 1.57 0.56 -0.37

Maximum Drawdown -13.4% -7.4% -26.3%

- - Drawdown Start Date Jul-07 Dec-08 Jul-07

- - Drawdown End Date Oct-10 Jun-10 Oct-10

Correlation versus:

HFRX Global Hedge Fund Index 0.46 -0.23 1.00

iBoxx USD Treasury TR Index -0.08 1.00 -0.23

Rolling 12 Month Volatility: Jan 00 -- October 10(1)

[GRAPHIC OMITTED]

Relative Performance: October 30, 2010(1)

[GRAPHIC OMITTED]

CERTAIN RISKS OF LIQUID ALPHA

LIQUID ALPHA HAS LIMITED PERFORMANCE HISTORY -- Publication of Liquid Alpha

began on April 23, 2008. Therefore, it has very limited performance history and

no actual investment which allowed tracking of the performance of Liquid Alpha

was possible before that date.

AN INVESTMENT LINKED OR RELATED TO LIQUID ALPHA WILL NOT BE THE SAME AS AN

INVESTMENT IN THE ALPHA INDICES -- The Liquid Alpha closing level on any trading

day will depend on the performance of the 5 underlying index constituents (the

"Alpha Indices"). The weighting of each Alpha Index is determined by an

Optimized Asset Allocator ("OAA"), which seeks to maximize returns for a given

level of volatility. You should, therefore, carefully consider the composition

and calculation of each Alpha Index.

THE ALPHA INDICES EXPOSE YOUR INVESTMENT TO EQUITY, COMMODITY, CURRENCY AND

INTEREST RATE RISKS --The Alpha Indices expose you to several asset classes and

their respective risks, including risks relating to exchange rate fluctuations,

foreign equity markets, commodity markets and emerging markets. In addition, the

rates component is five times leveraged. To learn more about Liquid Alpha, see

Underlying Supplement No. 4 dated September 29, 2009 filed with the Securities

and Exchange Commission.

THE ALPHA INDICES ARE NOT EQUALLY WEIGHTED IN THE LIQUID ALPHA MODEL AND MAY

OFFSET EACH OTHER -- The Alpha Indices are assigned different weightings in

Liquid Alpha via an Optimized Asset Allocation Model. The same return generated

by two Alpha Indices, whether positive or negative, may have a different effect

on the performance of Liquid Alpha. Additionally, positive returns generated by

one or more Alpha Index may be moderated or more than offset by smaller positive

returns or negative returns generated by the other Alpha Indices.

THE ACTUAL EXPERIENCED VOLATILITY OF EACH ALPHA INDEX AND LIQUID ALPHA MODEL MAY

NOT EQUAL THE TARGET VOLATILITY, WHICH MAY HAVE A NEGATIVE IMPACT ON THE

PERFORMANCE OF LIQUID ALPHA -- The weighting of each Alpha Index in the Liquid

Alpha Model is adjusted to target a volatility level of 5%. Because this

adjustment is based on the volatility of the previous 60 business days, the

actual volatility realized on the Alpha Indices and the Liquid Alpha Model will

not necessarily equal the volatility target.

THE CALCULATION OF LIQUID ALPHA'S CLOSING LEVEL WILL INCLUDE A DEDUCTION OF

COSTS FROM THE ALPHA INDICES -- On each trading day, the calculation of Liquid

Alpha's closing level will include a deduction of costs from the Alpha Indices

currently ranging between a minimum of 21 basis points per annum and maximum of

63 basis points per annum, depending on the individual weightings of the Alpha

Indices.

(1): Liquid Alpha USD ER 5 has been retrospectively calculated and did not exist

prior to April 23, 2008. Accordingly, the results shown during the retrospective

periods do not reflect actual returns. Past performance is not necessarily

indicative of how the Index will perform in the future. The performance of any

investment product based on the DB Liquid Alpha Index would have been lower than

the performance of the Index as a result of fees or costs.

(2): Value indicates Risk Free Rate over Period computed from daily levels of

the DB Fed Funds Equivalent Index.

|

| IMPORTANT INFORMATION Use of hypothetical information: Backtested, hypothetical or simulated performance results discussed herein have inherent limitations. Unlike an actual performance record based on actual client portfolios, simulated results are achieved by means of the retroactive application of a backtested model itself designed with the benefit of hindsight. Taking into account historical events the backtesting of performance also differs from actual account performance because an actual investment strategy may be adjusted any time, for any reason, including a response to material, economic or market factors. The backtested performance includes hypothetical results that do not reflect the reinvestment of dividends and other earnings or the deduction of advisory fees, brokerage or other commissions, and any other expenses that a client would have paid or actually paid. No representation is made that any trading strategy or account will or is likely to achieve profits or losses similar to those shown. Alternative modeling techniques or assumptions might produce significantly different results and prove to be more appropriate. Past hypothetical backtest results are neither an indicator nor guarantee of future returns. Actual results will vary, perhaps materially, from the analysis. Past performance: The past performance of securities, indexes or other instruments referred to herein does not guarantee or predict future performance. Deutsche Bank may hold positions: We or our affiliates or persons associated with us or such affiliates may: maintain a long or short position in securities referred to herein, or in related futures or options, purchase or sell, make a market in, or engage in any other transaction involving such securities, and earn brokerage or other compensation. Instruments linked to this index typically involve a high degree of risk, are not transferable and typically will not be listed or traded on any exchange and are intended for sale only to sophisticated investors who are capable of understanding and assuming the risks involved. The market value of any structured security linked to this index may be affected by changes in economic, financial and political factors (including but not limited to, spot and forward interest and exchange rates), time to maturity, market conditions and volatility and the equity prices and credit quality of any issuer or reference issuer. Any investor should conduct his/her own investigation and analysis of any product linked to this index and consult with its own professional advisors as to the risks involved in making such a purchase; since, it may be difficult to realize the investment prior to maturity, obtain reliable information about the market value of such investments or the extent of the risks to which they are exposed, including the risk of total loss of capital. Tax: Deutsche Bank AG, including its subsidiaries and affiliates, does not provide legal, tax or accounting advice. This communication was prepared solely in connection with the promotion or marketing, to the extent permitted by applicable law, of the transaction or matter addressed herein, and was not intended or written to be used, and cannot be used or relied upon, by any taxpayer for purposes of avoiding any U.S. federal income tax penalties. The recipient of this communication should seek advice from an independent tax advisor regarding any tax matters addressed herein based on its particular circumstances. Any information relating to taxation is based on information currently available. The levels and bases of, and relief from, taxation can change and the benefits of products where discussed may cease to exist. Because of the importance of tax considerations to all option transactions, the investor considering options should consult with his/her tax advisor as to how taxes affect the outcome of contemplated option transactions. Not insured: These instruments are not insured by the Federal Deposit Insurance Corporation (FDIC) or any other U.S. governmental agency. These instruments are not insured by any statutory scheme or governmental agency of the United Kingdom. The distribution of this document and availability of these products and services in certain jurisdictions may be restricted by law. These securities have not been registered under the United States Securities Act of 1933 and trading in the securities has not been approved by the United States Commodity Exchange Act, as amended. The Bank and affiliates: "Deutsche Bank" means Deutsche Bank AG and its affiliated companies, as the context requires. Deutsche Bank Private Wealth Management refers to Deutsche Bank's wealth management activities for high-net-worth clients around the world. Deutsche Bank Alex. Brown is a division of Deutsche Bank Securities Inc. Free writing prospectus: Deutsche Bank AG has filed a registration statement (including a prospectus) with the SEC for the offerings to which this communication may relate. Before you invest, you should read the prospectus in that registration statement and other documents the issuer has filed with the SEC for more complete information about the issuer and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the issuer, any underwriter or any dealer participating in the offering will arrange to send you the prospectus if you request it by calling toll-free 1-800-311-4409. |