ISSUER FREE WRITING PROSPECTUS No. 2341B Filed Pursuant to Rule 433 Registration Statement No. 333-184193 Dated February 2, 2015 Deutsche Bank AG Trigger Performance Securities |

Linked to the Vanguard FTSE Emerging Markets ETF due on or about February 28, 2019

| Investment Description |

The Trigger Performance Securities (the “Securities”) are unsubordinated and unsecured obligations of Deutsche Bank AG, London Branch (the “Issuer”) with returns linked to the performance of the Vanguard FTSE Emerging Markets ETF (the “Underlying”). If the Underlying Return is positive, for each $10.00 Face Amount of Securities, Deutsche Bank AG will repay the Face Amount at maturity and pay a return on the Face Amount equal to the Underlying Return multiplied by the Participation Rate of between 149.00% and 159.00% (the actual Participation Rate will be determined on the Trade Date). If the Underlying Return is zero or negative and the Final Price is greater than or equal to the Trigger Price, Deutsche Bank AG will repay the Face Amount per $10.00 Face Amount of Securities at maturity. However, if the Final Price is less than the Trigger Price, you will be fully exposed to the negative Underlying Return and, for each $10.00 Face Amount of Securities, Deutsche Bank AG will pay you less than the Face Amount at maturity, resulting in a loss on the Face Amount to investors that is proportionate to the percentage decline in the price of the Underlying. Investing in the Securities involves significant risks. You will not receive coupon payments during the approximately 4-year term of the Securities. You may lose a significant portion or all of your initial investment. You will not receive dividends or other distributions paid on the Underlying or any component securities held by the Underlying. The contingent repayment of the Face Amount applies only if you hold the Securities to maturity. Any payment on the Securities, including any repayment of the Face Amount provided at maturity, is subject to the creditworthiness of the Issuer. If the Issuer were to default on its payment obligations or become subject to a Resolution Measure (as described on page 2), you might not receive any amounts owed to you under the terms of the Securities and you could lose your entire investment.

| Features | Key Dates1 | ||

q Participation in Positive Underlying Returns: If the Underlying Return is positive, for each $10.00 Face Amount of Securities, the Issuer will repay the Face Amount at maturity and pay a return on the Face Amount equal to the Underlying Return multiplied by the Participation Rate. If the Underlying Return is negative, investors may be exposed to the decline in the price of the Underlying at maturity. q Downside Exposure with Contingent Repayment of the Face Amount at Maturity: If the Underlying Return is zero or negative and the Final Price is greater than or equal to the Trigger Price, the Issuer will repay the Face Amount per $10.00 Face Amount of Securities at maturity. However, if the Final Price is less than the Trigger Price, you will be fully exposed to the negative Underlying Return and, for each $10.00 Face Amount of Securities, the Issuer will pay you less than the Face Amount at maturity, resulting in a loss on the Face Amount to investors that is proportionate to the percentage decline in the price of the Underlying. The contingent repayment of the Face Amount applies only if you hold the Securities to maturity. You may lose a significant portion or all of your initial investment. Any payment on the Securities is subject to the creditworthiness of the Issuer. If the Issuer were to default on its payment obligations or become subject to a Resolution Measure, you might not receive any amounts owed to you under the terms of the Securities and you could lose your entire investment. | Trade Date Settlement Date Final Valuation Date2 Maturity Date2 | February 24, 2015 February 27, 2015 February 22, 2019 February 28, 2019 | |

2 See page 4 for additional details | |||

NOTICE TO INVESTORS: THE SECURITIES ARE SIGNIFICANTLY RISKIER THAN CONVENTIONAL DEBT SECURITIES. THE ISSUER IS NOT NECESSARILY OBLIGATED TO REPAY THE FULL FACE AMOUNT OF SECURITIES AT MATURITY, AND THE SECURITIES CAN HAVE DOWNSIDE MARKET RISK SIMILAR TO THE UNDERLYING. THIS MARKET RISK IS IN ADDITION TO THE CREDIT RISK INHERENT IN PURCHASING AN OBLIGATION OF DEUTSCHE BANK AG. YOU SHOULD NOT PURCHASE THE SECURITIES IF YOU DO NOT UNDERSTAND OR ARE NOT COMFORTABLE WITH THE SIGNIFICANT RISKS INVOLVED IN INVESTING IN THE SECURITIES. THE SECURITIES WILL NOT BE LISTED ON ANY SECURITIES EXCHANGE.

YOU SHOULD CAREFULLY CONSIDER THE RISKS DESCRIBED UNDER “KEY RISKS” BEGINNING ON PAGE 5 OF THIS FREE WRITING PROSPECTUS, UNDER “RISK FACTORS” BEGINNING ON PAGE 7 OF THE ACCOMPANYING PRODUCT SUPPLEMENT AND UNDER “RISK FACTORS” BEGINNING ON PAGE 2 OF THE ACCOMPANYING PROSPECTUS ADDENDUM BEFORE PURCHASING ANY SECURITIES. EVENTS RELATING TO ANY OF THOSE RISKS, OR OTHER RISKS AND UNCERTAINTIES, COULD ADVERSELY AFFECT THE MARKET VALUE OF, AND THE RETURN ON, YOUR SECURITIES. YOU MAY LOSE A SIGNIFICANT PORTION OR ALL OF YOUR INITIAL INVESTMENT IN THE SECURITIES.

| Security Offering |

We are offering Trigger Performance Securities linked to the performance of the Vanguard FTSE Emerging Markets ETF. The Securities are not subject to a predetermined maximum gain and, accordingly, any return at maturity will be determined by the performance of the Underlying. The Securities are our unsubordinated and unsecured obligations and are offered for a minimum investment of 100 Securities at the price to public described below. The Initial Price, Participation Rate and Trigger Price will be determined on the Trade Date.

| Underlying | Initial Price | Participation Rate | Trigger Price | CUSIP/ ISIN |

Vanguard FTSE Emerging Markets ETF (Ticker: VWO) | 149.00% to 159.00% | 80.00% of the Initial Price | 25190E726 / US25190E7269 |

See “Additional Terms Specific to the Securities” in this free writing prospectus. The Securities will have the terms specified in product supplement B dated September 28, 2012, the prospectus supplement dated September 28, 2012 relating to our Series A global notes of which these Securities are a part, the prospectus dated September 28, 2012, the prospectus addendum dated December 24, 2014 and this free writing prospectus.

The Issuer’s estimated value of the Securities on the Trade Date is approximately $9.70 to $9.90 per $10.00 Face Amount of Securities, which is less than the Issue Price. Please see “Issuer’s Estimated Value of the Securities” on the following page of this free writing prospectus for additional information.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the Securities or passed upon the accuracy or the adequacy of this free writing prospectus or the accompanying product supplement B, prospectus supplement, prospectus or prospectus addendum. Any representation to the contrary is a criminal offense. The Securities are not bank deposits and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency.

| Offering of Securities | Price to Public | Discounts and Commissions(1) | Proceeds to Us |

| Trigger Performance Securities linked to the Vanguard FTSE Emerging Markets ETF | |||

| Per Security | $10.00 | $0.00 | $10.00 |

| Total | $ | $ | $ |

| (1) | With respect to sales to certain fee-based advisory accounts for which UBS Financial Services Inc. is an investment adviser, UBS Financial Services Inc. will act as placement agent for such sales at an Issue Price of $10.00 per $10.00 Face Amount of Securities and will not receive a sales commission. For more information about discounts and commissions, please see “Supplemental Plan of Distribution (Conflicts of Interest)” on the last page of this free writing prospectus. |

Deutsche Bank Securities Inc. (“DBSI”) is our affiliate. For more information see “Supplemental Plan of Distribution (Conflicts of Interest)” on the last page of this free writing prospectus.

| UBS Financial Services Inc. | Deutsche Bank Securities |

| Issuer’s Estimated Value of the Securities |

The Issuer’s estimated value of the Securities is equal to the sum of our valuations of the following two components of the Securities: (i) a bond and (ii) an embedded derivative(s). The value of the bond component of the Securities is calculated based on the present value of the stream of cash payments associated with a conventional bond with a principal amount equal to the Face Amount of Securities, discounted at an internal funding rate, which is determined primarily based on our market-based yield curve, adjusted to account for our funding needs and objectives for the period matching the term of the Securities. The internal funding rate is typically lower than the rate we would pay when we issue conventional debt securities on equivalent terms. This difference in funding rate, as well as the agent’s commissions, if any, and the estimated cost of hedging our obligations under the Securities, reduces the economic terms of the Securities to you and is expected to adversely affect the price at which you may be able to sell the Securities in any secondary market. The value of the embedded derivative(s) is calculated based on our internal pricing models using relevant parameter inputs such as expected interest and dividend rates and mid-market levels of price and volatility of the assets underlying the Securities or any futures, options or swaps related to such underlying assets. Our internal pricing models are proprietary and rely in part on certain assumptions about future events, which may prove to be incorrect.

The Issuer’s estimated value of the Securities on the Trade Date (as disclosed on the cover of this free writing prospectus) is less than the Issue Price of the Securities. The difference between the Issue Price and the Issuer’s estimated value of the Securities on the Trade Date is due to the inclusion in the Issue Price of the agent’s commissions, if any, and the cost of hedging our obligations under the Securities through one or more of our affiliates. Such hedging cost includes our or our affiliates’ expected cost of providing such hedge, as well as the profit we or our affiliates expect to realize in consideration for assuming the risks inherent in providing such hedge.

The Issuer’s estimated value of the Securities on the Trade Date does not represent the price at which we or any of our affiliates would be willing to purchase your Securities in the secondary market at any time. Assuming no changes in market conditions or our creditworthiness and other relevant factors, the price, if any, at which we or our affiliates would be willing to purchase the Securities from you in secondary market transactions, if at all, would generally be lower than both the Issue Price and the Issuer’s estimated value of the Securities on the Trade Date. Our purchase price, if any, in secondary market transactions will be based on the estimated value of the Securities determined by reference to (i) the then-prevailing internal funding rate (adjusted by a spread) or another appropriate measure of our cost of funds and (ii) our pricing models at that time, less a bid spread determined after taking into account the size of the repurchase, the nature of the assets underlying the Securities and then-prevailing market conditions. The price we report to financial reporting services and to distributors of our Securities for use on customer account statements would generally be determined on the same basis. However, during the period of approximately six months beginning from the Trade Date, we or our affiliates may, in our sole discretion, increase the purchase price determined as described above by an amount equal to the declining differential between the Issue Price and the Issuer’s estimated value of the Securities on the Trade Date, prorated over such period on a straight-line basis, for transactions that are individually and in the aggregate of the expected size for ordinary secondary market repurchases.

| Resolution Measures |

Under the German Recovery and Resolution Act (Sanierungs- und Abwicklungsgesetz, or “SAG”), which went into effect on January 1, 2015, the Securities may be subject to any Resolution Measure by our competent resolution authority if we become, or are deemed by our competent supervisory authority to have become, “non-viable” (as defined under the then applicable law) and are unable to continue our regulated banking activities without a Resolution Measure becoming applicable to us. A “Resolution Measure” may include: (i) a write down, including to zero, of any payment (or delivery obligations) on the Securities; (ii) a conversion of the Securities into ordinary shares or other instruments qualifying as core equity tier 1 capital; and/or (iii) any other resolution measure, including (but not limited to) any transfer of the Securities to another entity, the amendment of the terms and conditions of the Securities or the cancellation of the Securities. By acquiring the Securities, you will be bound by and will be deemed to consent to the imposition of any Resolution Measure by our competent resolution authority as set forth in the accompanying prospectus addendum dated December 24, 2014. Please read the risk factor “The Securities may be written down, be converted or become subject to other resolution measures. You may lose part or all of your investment if any such measure becomes applicable to us” in this free writing prospectus and see the accompanying prospectus addendum for further information.

| Additional Terms Specific to the Securities |

You should read this free writing prospectus, together with product supplement B dated September 28, 2012, the prospectus supplement dated September 28, 2012 relating to our Series A global notes of which these Securities are a part, the prospectus dated September 28, 2012 and the prospectus addendum dated December 24, 2014. You may access these documents on the website of the Securities and Exchange Commission (the “SEC”) at www.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

| ¨ | Product supplement B dated September 28, 2012: |

| ¨ | Prospectus supplement dated September 28, 2012: |

| ¨ | Prospectus dated September 28, 2012: |

| ¨ | Prospectus addendum dated December 24, 2014: |

Deutsche Bank AG has filed a registration statement (including a prospectus) with the Securities and Exchange Commission, for the offering to which this free writing prospectus relates. Before you invest in the Securities offered hereby, you should read these documents and any other documents relating to this offering that Deutsche Bank AG has filed with the SEC for more complete information about Deutsche Bank AG and this offering. You may obtain these documents without cost by visiting EDGAR on the SEC website at www.sec.gov. Our Central Index Key, or CIK, on the SEC website is 0001159508. Alternatively, Deutsche Bank AG, any agent or any dealer participating in this offering will arrange to send you the prospectus, prospectus addendum, prospectus supplement, product supplement and this free writing prospectus if you so request by calling toll-free 1-800-311-4409.

The trustee has appointed Deutsche Bank Trust Company Americas as its authenticating agent with respect to our Series A global notes.

You may revoke your offer to purchase the Securities at any time prior to the time at which we accept such offer by notifying the applicable agent. We reserve the right to change the terms of, or reject any offer to purchase, the Securities prior to their issuance. We will notify you in the event of any changes to the terms of the Securities, and you will be asked to accept such changes in connection with your purchase of the Securities. You may also choose to reject such changes, in which case we may reject your offer to purchase the Securities.

References to “Deutsche Bank AG,” “we,” “our” and “us” refer to Deutsche Bank AG, including, as the context requires, acting through one of its branches. In this free writing prospectus, “Securities” refers to the Trigger Performance Securities that are offered hereby, unless the context otherwise requires.

If the terms described in this free writing prospectus are inconsistent with those described in the accompanying product supplement, prospectus supplement, prospectus or prospectus addendum, the terms described in this free writing prospectus shall control.

This free writing prospectus, together with the documents listed above, contains the terms of the Securities and supersedes all other prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth in “Key Risks” in this free writing prospectus, “Risk Factors” in the accompanying product supplement and “Risk Factors” in the accompanying prospectus addendum, as the Securities involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisers before deciding to invest in the Securities.

| Investor Suitability |

The suitability considerations identified below are not exhaustive. Whether or not the Securities are a suitable investment for you will depend on your individual circumstances, and you should reach an investment decision only after you and your investment, legal, tax, accounting and other advisors have carefully considered the suitability of an investment in the Securities in light of your particular circumstances. You should also review “Key Risks” on page 5 of this free writing prospectus, “Risk Factors” on page 7 of the accompanying product supplement and “Risk Factors” on page 2 of the accompanying prospectus addendum.

| The Securities may be suitable for you if, among other considerations: | The Securities may not be suitable for you if, among other considerations: | |

¨ You fully understand the risks inherent in an investment in the Securities, including the risk of loss of your entire investment. ¨ You can tolerate the loss of a significant portion or all of your investment and are willing to make an investment that may have similar downside market risk as an investment in the shares of the Underlying or in the component securities held by the Underlying. ¨ You believe that the price of the Underlying will increase over the term of the Securities. ¨ You would be willing to invest in the Securities if the Participation Rate was set equal to the bottom of the range indicated on the cover of this free writing prospectus. ¨ You can tolerate fluctuations in the value of the Securities prior to maturity that may be similar to or exceed the downside fluctuations in the price of the Underlying. ¨ You do not seek current income from your investment and are willing to forgo any dividends or any other distributions paid on the Underlying or any component securities held by the Underlying. ¨ You are willing and able to hold the Securities to the Maturity Date, as set forth on the cover of this free writing prospectus, and accept that there may be little or no secondary market for the Securities. ¨ You seek an investment with exposure to companies in emerging markets. ¨ You are willing and able to assume the credit risk of Deutsche Bank AG for all payments under the Securities, and understand that if Deutsche Bank AG defaults on its obligations or becomes subject to a Resolution Measure, you might not receive any amounts due to you, including any repayment of the Face Amount. | ¨ You do not fully understand the risks inherent in an investment in the Securities, including the risk of loss of your entire investment. ¨ You require an investment designed to guarantee a full return of the Face Amount at maturity. ¨ You cannot tolerate the loss of a significant portion or all of your investment or are unwilling to make an investment that may have similar downside market risk as an investment in the shares of the Underlying or in the component securities held by the Underlying. ¨ You believe that the closing price of the Underlying is likely to be less than the Trigger Price on the Final Valuation Date. ¨ You would be unwilling to invest in the Securities if the Participation Rate was set equal to the bottom of the range indicated on the cover of this free writing prospectus. ¨ You cannot tolerate fluctuations in the value of the Securities prior to maturity that may be similar to or exceed the downside fluctuations in the price of the Underlying. ¨ You seek current income from this investment or prefer to receive any dividends or any other distributions paid on the Underlying or any component securities held by the Underlying. ¨ You are unwilling or unable to hold the Securities to the Maturity Date, as set forth on the cover of this free writing prospectus, or seek an investment for which there will be an active secondary market. ¨ You do not seek an investment with exposure to companies in emerging markets. ¨ You are unwilling or unable to assume the credit risk of Deutsche Bank AG for all payments under the Securities, including any repayment of the Face Amount. |

3

| Indicative Terms | ||

| Issuer | Deutsche Bank AG, London Branch | |

| Issue Price | 100% of the Face Amount of Securities | |

| Face Amount | $10.00 | |

| Term | Approximately 4 years | |

Trade Date1 | February 24, 2015 | |

Settlement Date1 | February 27, 2015 | |

Final Valuation Date1, 2 | February 22, 2019 | |

Maturity Date1, 2, 3 | February 28, 2019 | |

| Underlying | Vanguard FTSE Emerging Markets ETF (Ticker: VWO) | |

| Trigger Price | 80% of the Initial Price | |

| Participation Rate | 149.00% to 159.00%. The actual Participation Rate will be determined on the Trade Date. | |

| Payment at Maturity (per $10.00 Face Amount of Securities) | If the Underlying Return is positive, Deutsche Bank AG will pay you a cash payment per $10.00 Face Amount of Securities at maturity equal to the Face Amount plus a return on the Face Amount equal to the Underlying Return multiplied by the Participation Rate, calculated as follows: $10.00 + ($10.00 × Underlying Return × Participation Rate) If the Underlying Return is zero or negative and the Final Price is greater than or equal to the Trigger Price on the Final Valuation Date, Deutsche Bank AG will pay you a cash payment per $10.00 Face Amount of Securities at maturity equal to the Face Amount. If the Final Price is less than the Trigger Price on the Final Valuation Date, Deutsche Bank AG will pay you a cash payment per $10.00 Face Amount of Securities at maturity that is less than the Face Amount, calculated as follows: $10.00 + ($10.00 × Underlying Return) In this circumstance, you will lose a significant portion or all of the Face Amount in an amount proportionate to the percentage decline in the price of the Underlying. | |

| Underlying Return | Final Price – Initial Price Initial Price | |

| Closing Price | On any trading day, the last reported sale price of one share of the Underlying on the relevant exchange multiplied by the then-current Share Adjustment Factor, as determined by the calculation agent. | |

| Initial Price | The Closing Price of the Underlying on the Trade Date | |

| Final Price | The Closing Price of the Underlying on the Final Valuation Date | |

| Share Adjustment Factor | Initially 1.0, subject to adjustments for certain actions affecting the Underlying. See “Description of Securities — Anti-Dilution Adjustments for Funds” in the accompanying product supplement. | |

INVESTING IN THE SECURITIES INVOLVES SIGNIFICANT RISKS. YOU MAY LOSE A SIGNIFICANT PORTION OR ALL OF YOUR INITIAL INVESTMENT. ANY PAYMENT ON THE SECURITIES, INCLUDING ANY REPAYMENT OF THE FACE AMOUNT AT MATURITY, IS SUBJECT TO THE CREDITWORTHINESS OF THE ISSUER. IF DEUTSCHE BANK AG WERE TO DEFAULT ON ITS PAYMENT OBLIGATIONS OR BECOMES SUBJECT TO A RESOLUTION MEASURE, YOU MIGHT NOT RECEIVE ANY AMOUNTS OWED TO YOU UNDER THE SECURITIES AND YOU COULD LOSE YOUR ENTIRE INVESTMENT.

| Investment Timeline |

Trade Date: | The Initial Price is observed, the Participation Rate is set and the Trigger Price is determined. | ||

| Maturity Date: | The Final Price is determined and the Underlying Return is calculated on the Final Valuation Date. If the Underlying Return is positive, Deutsche Bank AG will pay you a cash payment per $10.00 Face Amount of Securities at maturity equal to the Face Amount plus a return on the Face Amount equal to the Underlying Return multiplied by the Participation Rate, calculated as follows: $10.00 + ($10.00 x Underlying Return x Participation Rate) If the Underlying Return is zero or negative and the Final Price is greater than or equal to the Trigger Price on the Final Valuation Date, Deutsche Bank AG will pay you a cash payment per $10.00 Face Amount of Securities at maturity equal to the Face Amount. If the Final Price is less than the Trigger Price on the Final Valuation Date, Deutsche Bank AG will pay you a cash payment per $10.00 Face Amount of Securities at maturity that is less than the Face Amount, calculated as follows: $10.00 + ($10.00 × Underlying Return) In this circumstance, you will lose a significant portion or all of the Face Amount in an amount proportionate to the percentage decline in the price of the Underlying. |

| 1 | In the event that we make any changes to the expected Trade Date or Settlement Date, the Final Valuation Date and Maturity Date may be changed to ensure that the stated term of the Securities remains the same. |

| 2 | Subject to postponement as described under “Description of Securities — Adjustments to Valuation Dates and Payment Dates” in the accompanying product supplement. |

| 3 | Notwithstanding the provisions under “Description of Securities — Adjustments to Valuation Dates and Payment Dates” in the accompanying product supplement, in the event the Final Valuation Date is postponed, the Maturity Date will be the fourth business day after the Final Valuation Date as postponed. |

4

| Key Risks |

An investment in the Securities involves significant risks. Investing in the Securities is not equivalent to investing directly in the Underlying or in any of the component securities held by the Underlying. Some of the risks that apply to an investment in the Securities are summarized below, but we urge you to read the more detailed explanation of risks relating to the Securities generally in the “Risk Factors” sections of the accompanying product supplement and prospectus addendum. We also urge you to consult your investment, legal, tax, accounting and other advisers before you invest in the Securities.

| ¨ | Your Investment in the Securities May Result in a Loss of Your Initial Investment — The Securities differ from ordinary debt securities in that Deutsche Bank AG will not necessarily pay you your initial investment in the Securities at maturity. The return on the Securities at maturity is linked to the performance of the Underlying and will depend on whether, and the extent to which, the Underlying Return is positive, zero or negative and if the Underlying Return is negative, whether the Final Price is less than the Trigger Price. If the Final Price is less than the Trigger Price, you will be fully exposed to any negative Underlying Return and, for each $10.00 Face Amount of Securities, Deutsche Bank AG will pay you less than the Face Amount at maturity, resulting in a loss on the Face Amount that is proportionate to the percentage decline in the price of the Underlying. In this circumstance, you will lose a significant portion or all of your initial investment at maturity. |

| ¨ | Contingent Repayment of Your Initial Investment Applies Only If You Hold the Securities to Maturity — You should be willing to hold your Securities to maturity. If you are able to sell your Securities prior to maturity in the secondary market, you may have to sell them at a loss relative to your initial investment even if the price of the Underlying at such time is greater than the Trigger Price at the time of sale. You can receive the full potential benefit of the Trigger Price only if you hold your Securities to maturity. |

| ¨ | The Participation Rate Applies Only at Maturity — You should be willing to hold your Securities to maturity. If you are able to sell your Securities prior to maturity in the secondary market, the price you receive will likely not reflect the full effect of the Participation Rate and the return you realize may be less than the Underlying’s return even if such return is positive. You can receive the full benefit of the Participation Rate only if you hold your Securities to maturity. |

| ¨ | No Coupon Payments — Deutsche Bank AG will not pay any coupon payments with respect to the Securities. |

| ¨ | The Securities Are Subject to the Credit of Deutsche Bank AG — The Securities are unsubordinated and unsecured obligations of Deutsche Bank AG and are not, either directly or indirectly, an obligation of any third party. Any payment to be made on the Securities, including any repayment of the Face Amount per $10.00 Face Amount of Securities at maturity, depends on the ability of Deutsche Bank AG to satisfy its obligations as they come due. An actual or anticipated downgrade in Deutsche Bank AG’s credit rating or increase in the credit spreads charged by the market for taking the credit risk of Deutsche Bank AG will likely have an adverse effect on the value of the Securities. As a result, the actual and perceived creditworthiness of Deutsche Bank AG will affect the value of the Securities, and in the event Deutsche Bank AG were to default on its obligations or becomes subject to a Resolution Measure, you might not receive any amount owed to you under the terms of the Securities and you could lose your entire investment. |

| ¨ | The Securities May Be Written Down, Be Converted or Become Subject to Other Resolution Measures. You May Lose Some or All of Your Investment If Any Such Measure Becomes Applicable to Us — On May 15, 2014, the European Parliament and the Council of the European Union published a directive for establishing a framework for the recovery and resolution of credit institutions and investment firms (commonly referred to as the “Bank Recovery and Resolution Directive”). The Bank Recovery and Resolution Directive requires each member state of the European Union to adopt and publish by December 31, 2014 the laws, regulations and administrative provisions necessary to comply with the Bank Recovery and Resolution Directive. Germany has adopted SAG, which went into effect on January 1, 2015. SAG may result in the Securities being subject to the powers exercised by our competent resolution authority to impose a Resolution Measure on us, which may include: writing down, including to zero, any payment on the Securities; converting the Securities into ordinary shares or other instruments qualifying as core equity tier 1 capital; or applying any other resolution measure, including (but not limited to) transferring the Securities to another entity, amending the terms and conditions of the Securities or cancelling of the Securities. Furthermore, because the Securities are subject to any Resolution Measure, secondary market trading in the Securities may not follow the trading behavior associated with similar types of securities issued by other financial institutions which may be or have been subject to a Resolution Measure. Imposition of a Resolution Measure would likely occur if we become, or are deemed by our competent supervisory authority to have become, “non-viable” (as defined under the then applicable law) and are unable to continue our regulated banking activities without a Resolution Measure becoming applicable to us. You may lose some or all of your investment in the Securities if a Resolution Measure becomes applicable to us. |

By acquiring the Securities, you will be bound by and will be deemed to consent to the imposition of any Resolution Measure by our competent resolution authority. As a result, you would have no claim or other right against us arising out of any Resolution Measure and the imposition of any Resolution Measure will not constitute a default or an event of default under the Securities, under the senior indenture or for the purpose of the U.S. Trust Indenture Act of 1939, as amended. In addition, the trustee, the paying agent and The Depository Trust Company (“DTC”) and any participant in DTC or other intermediary through which you hold such Securities may take any and all necessary action, or abstain from taking any action, if required, to implement the imposition of any Resolution Measure with respect to the Securities. Accordingly, you may have limited or circumscribed rights to challenge any decision of our competent resolution authority to impose any Resolution Measure. Please see the accompanying prospectus addendum dated December 24, 2014, including the risk factor “The securities may be written down, be converted or become subject to other resolution measures. You may lose part or all of your investment if any such measure becomes applicable to us” on page 2 of the prospectus addendum.

| ¨ | The Issuer’s Estimated Value of the Securities on the Trade Date Will Be Less Than the Issue Price of the Securities — The Issuer’s estimated value of the Securities on the Trade Date (as disclosed on the cover of this free writing prospectus) is less than the Issue Price of the Securities. The difference between the Issue Price and the Issuer’s estimated value of the Securities on the Trade Date is due to the inclusion in the Issue Price of the agent’s commissions, if any, and the cost of hedging our obligations under the Securities through one or more of our affiliates. Such hedging cost includes our or our affiliates' expected cost of providing such hedge, as well as the profit we or our affiliates expect to realize in consideration for assuming the risks inherent in providing such hedge. The Issuer’s estimated value of the Securities is determined by reference to an internal funding rate and our pricing models. The internal funding rate |

5

is typically lower than the rate we would pay when we issue conventional debt securities on equivalent terms. This difference in funding rate, as well as the agent’s commissions, if any, and the estimated cost of hedging our obligations under the Securities, reduces the economic terms of the Securities to you and is expected to adversely affect the price at which you may be able to sell the Securities in any secondary market. In addition, our internal pricing models are proprietary and rely in part on certain assumptions about future events, which may prove to be incorrect. If at any time a third party dealer were to quote a price to purchase your Securities or otherwise value your Securities, that price or value may differ materially from the estimated value of the Securities determined by reference to our internal funding rate and pricing models. This difference is due to, among other things, any difference in funding rates, pricing models or assumptions used by any dealer who may purchase the Securities in the secondary market. |

| ¨ | Investing in the Securities Is Not the Same as Investing in the Underlying or the Component Securities Held by the Underlying — The return on your Securities may not reflect the return you would realize if you invested directly in the Underlying or the component securities held by the Underlying. |

| ¨ | If the Price of the Underlying Changes, the Value of the Securities may not Change in the Same Manner — The Securities may trade quite differently from the shares of the Underlying. Changes in the price of the shares of the Underlying may not result in comparable changes in the value of the Securities. |

| ¨ | No Dividend Payments or Voting Rights — As a holder of the Securities, you will not have any voting rights or rights to receive cash dividends or other distributions or other rights that holders of the component securities held by the Underlying or holders of shares of the Underlying would have. |

| ¨ | There Are Risks Associated with Investments in Securities Linked to the Values of Equity Securities Issued by Non-U.S. Companies — The Underlying holds component stocks that are issued by companies incorporated outside of the U.S. Because the component stocks also trade outside the U.S., the Securities are subject to the risks associated with non-U.S. securities markets. Generally, non-U.S. securities markets may be more volatile than U.S. securities markets and market developments may affect non-U.S. securities markets differently than U.S. securities markets, which may adversely affect the price of the Underlying and the value of your Securities. Furthermore, there are risks associated with investments in securities linked to the values of equity securities issued by non-U.S. companies. There is generally less publicly available information about non-U.S. companies than about those U.S. companies that are subject to the reporting requirements of the SEC, and non-U.S. companies are subject to accounting, auditing and financial reporting standards and requirements that differ from those applicable to U.S. reporting companies. In addition, the prices of equity securities issued by non-U.S. companies may be adversely affected by political, economic, financial and social factors that may be unique to the particular countries in which the non-U.S. companies are incorporated. These factors include the possibility of recent or future changes in a non-U.S. government’s economic and fiscal policies (including any direct or indirect intervention to stabilize the economy and/or securities market of the country of such non-U.S. government), the presence, and extent, of cross shareholdings in non-U.S. companies, the possible imposition of, or changes in, currency exchange laws or other non-U.S. laws or restrictions applicable to non-U.S. companies or investments in non-U.S. securities and the possibility of fluctuations in the rate of exchange between currencies. Moreover, certain aspects of a particular non-U.S. economy may differ favorably or unfavorably from the U.S. economy in important respects, such as growth of gross national product, rate of inflation, capital reinvestment, resources and self-sufficiency. |

| ¨ | The Securities Are Subject to Currency Exchange Rate Risk — Because the Underlying invests in stocks denominated in foreign currencies that are converted into U.S. dollars for purposes of calculating the price of the Underlying, holders of the Securities will be exposed to currency exchange rate risk with respect to each of the currencies represented in the Underlying. Of particular importance to currency exchange rate risk are: |

| ¨ | existing and expected rates of inflation; |

| ¨ | existing and expected interest rate levels; |

| ¨ | political, civil or military unrest; |

| ¨ | the balance of payments between countries represented in the Underlying and the United States; and |

| ¨ | the extent of governmental surpluses or deficits in the countries represented in the Underlying and the United States. |

All of these factors are in turn sensitive to the monetary, fiscal and trade policies pursued by the governments of the countries represented in the Underlying, the United States and other countries important to international trade and finance. An investor’s net exposure to currency exchange rate risk will depend on the extent to which the currencies represented in the Underlying strengthen or weaken against the U.S. dollar and the relative weight of each currency represented in the Underlying. If, taking into account such weighting, the U.S. dollar strengthens against the component currencies as a whole, the price of the Underlying will be adversely affected and the value of the Securities may be reduced. Additionally, the volatility and/or the correlation (including the direction and the extent of such correlation) of the exchange rates between the U.S. dollar and the currencies represented in the Underlying could affect the value of the Securities.

| ¨ | The Securities Are Subject to Emerging Markets Risk — The value of the Securities is subject to the political and economic risks of emerging market countries by linking to the performance of the Underlying. The component securities held by the Underlying include stocks of companies that are located in emerging market countries and whose securities trade on the exchanges of emerging market countries. In recent years, some emerging markets have undergone significant political, economic and social upheaval. Such far-reaching changes have resulted in constitutional and social tensions and, in some cases, instability and reaction against market reforms has occurred. With respect to any emerging market nation, there is the possibility of nationalization, expropriation or confiscation, political changes, government regulation and social instability. Future political changes may adversely affect the economic conditions of an emerging market nation. Political or economic instability could adversely affect the value of the Securities and the amount payable to you on the Securities. |

| ¨ | Fluctuation of NAV — The net asset value (“NAV”) of the Underlying may fluctuate with changes in the market value of the Underlying’s securities holdings. The price of the shares of the Underlying may fluctuate in accordance with changes in the Underlying’s NAV as well as the shares’ supply and demand on the applicable stock exchanges. Therefore, the price of the shares of the Underlying may differ from its NAV per share and the shares of the Underlying may trade at, greater than or less than the Underlying’s NAV per share. |

6

| ¨ | The Anti-Dilution Protection Is Limited — The calculation agent will make adjustments to the Share Adjustment Factor, which will initially be set at 1.0, for certain events affecting the shares of the Underlying. The calculation agent is not required, however, to make such adjustments in response to all events that could affect the shares of the Underlying. If an event occurs that does not require the calculation agent to make an adjustment, the value of the Securities may be materially and adversely affected. In addition, you should be aware that the calculation agent may, in its sole discretion, make adjustments to the Share Adjustment Factor or any other terms of the Securities that are in addition to, or that differ from, those described in the accompanying product supplement to reflect changes occurring in relation to the Underlying in circumstances where the calculation agent determines that it is appropriate to reflect those changes to ensure an equitable result. Any alterations to the specified anti-dilution adjustments described in the accompanying product supplement may be materially adverse to investors in the Securities. You should read “Description of Securities — Anti-Dilution Adjustments for Funds” in the accompanying product supplement in order to understand the adjustments that may be made to the Securities. |

| ¨ | Adjustments to the Underlying or to Its Tracked Index Could Adversely Affect the Value of the Securities — The Vanguard Group, Inc. (the “VGI”) is the investment advisor to the Underlying, which seeks investment results that correspond generally to the level and yield performance, before fees and expenses, of the FTSE Emerging Index (the “Tracked Index”). The stocks included in the Tracked Index are selected by FTSE International Limited (“FTSE”). The Tracked Index is calculated and published by FTSE. FTSE can add, delete or substitute the stocks composing the Tracked Index, which could change the value of the Tracked Index. Pursuant to its investment strategy or otherwise, VGI may add, delete or substitute the component securities held by the Underlying. Any of these actions could cause or contribute to large movements in the prices of the component securities held by the Underlying, which could cause the Final Price to be less than the Trigger Price, in which case you will lose a significant portion or all of your initial investment. |

| ¨ | The Underlying and Its Tracked Index Are Different — The performance of the Underlying may not exactly replicate the performance of the Tracked Index because the Underlying will reflect transaction costs and fees that are not included in the calculation of the Tracked Index. It is also possible that the Underlying may not fully replicate or may in certain circumstances diverge significantly from the performance of the Tracked Index due to the temporary unavailability of certain securities in the secondary market, the performance of any derivative instruments contained in the Underlying or due to other circumstances. FTSE may invest up to 10% of the Underlying’s assets in futures contracts, options on futures contracts, other types of options, and swaps related to the Tracked Index as well as cash and cash equivalents, including shares of money market funds advised by FTSE or its affiliates. The Underlying may use options and futures contracts, convertible securities and structured notes in seeking performance that corresponds to the Tracked Index and in managing cash flows. Finally, because the shares of the Underlying are traded on NYSE Arca and are subject to market supply and investor demand, the market value of one share of the Underlying may differ from the net asset value per share of the Underlying. For all of the foregoing reasons, the performance of the Underlying may not correlate with the performance of the Tracked Index. |

| ¨ | The Underlying’s Tracked Index Has Recently Changed — The Underlying’s Tracked Index recently completed a process of transitioning to a new tracked index, which could reduce the performance of the component securities, and limit the utility of available information about the performance of the Underlying. Until 2013, the tracked index for the Underlying was the MSCI Emerging Markets Index (the “MXEA”). In October 2012, VGI announced that the Underlying would adopt the Tracked Index as its new target index over the following months. In the first phase of the transition, which began on January 10, 2013, the Underlying ceased tracking the MXEA, and began temporarily tracking the FTSE Emerging Transition Index (the “Transition Index”), a “dynamic” index that gradually reduced its exposure to South Korean equities by approximately 4% each week for a period of 25 weeks, while proportionately adding exposure to stocks of companies located in other countries based on their weightings in the new index. In the second phase of the transition, in July 2013, the Underlying ceased tracking the Transition Index and began tracking the Tracked Index. For more information, see the sections entitled “The Underlying” and “Vanguard FTSE Emerging Markets ETF” in this free writing prospectus. |

| ¨ | There Is No Affiliation Between the Underlying and Us, and We Have Not Participated in the Preparation of, or Verified, Any Disclosure by the Underlying — We are not affiliated with the Underlying or the issuers of the component stocks held by the Underlying or underlying the Tracked Index (such stocks, “Underlying Stocks,” the issuers of Underlying Stocks, “Underlying Stock Issuers”). However, we or our affiliates may currently or from time to time in the future engage in business with many of the Underlying Stock Issuers. In the course of this business, we or our affiliates may acquire non-public information about the Underlying Stock Issuers, and we will not disclose any such information to you. Nevertheless, neither we nor our affiliates have participated in the preparation of, or verified, any information about the Underlying Stocks or any of the Underlying Stock Issuers. You, as an investor in the Securities, should make your own investigation into the Underlying Stocks and the Underlying Stock Issuers. Neither the Underlying nor any of the Underlying Stock Issuers is involved in this offering of Securities in any way and none of them has any obligation of any sort with respect to your Securities. Neither the Underlying nor any of the Underlying Stock Issuers has any obligation to take your interests into consideration for any reason, including when taking any corporate actions that might affect the value of your Securities. |

| ¨ | Past Performance of the Underlying, its Tracked Index or the Component Securities Held by the Underlying Is No Guide to Future Performance — The actual performance of the Underlying, the Tracked Index or the component securities held by the Underlying over the term of the Securities may bear little relation to the historical closing prices of the shares of the Underlying or of the component securities held by the Underlying or the historical closing levels of the Tracked Index, and may bear little relation to the hypothetical return examples set forth elsewhere in this free writing prospectus. Furthermore, due to the transition described in the section entitled “Vanguard FTSE Emerging Markets ETF” in this free writing prospectus, the Underlying’s historical performance may be of limited value in assessing its performance. Prior to January 2013, the performance of the Underlying resulted from its tracking of the performance of the MXEA. In January 2013, the Underlying began tracking the performance of the Transition Index and, in July 2013, the Underlying began tracking the Tracked Index. We cannot predict the future performance of the Underlying, the Tracked Index or the component securities held by the Underlying. |

| ¨ | Assuming No Changes in Market Conditions and Other Relevant Factors, the Price You May Receive for Your Securities in Secondary Market Transactions Would Generally Be Lower Than Both the Issue Price and the Issuer’s Estimated Value of the Securities on the Trade Date — While the payment(s) on the Securities described in this free writing prospectus is based on the full Face Amount of your Securities, the Issuer’s estimated value of the Securities on the Trade Date (as disclosed on the cover of this free writing prospectus) is less than the Issue Price of the Securities. The Issuer’s estimated value of the Securities on the Trade Date does not represent the price at which we or any of our affiliates would be willing to purchase your Securities in the secondary market at any time. |

7

Assuming no changes in market conditions or our creditworthiness and other relevant factors, the price, if any, at which we or our affiliates would be willing to purchase the Securities from you in secondary market transactions, if at all, would generally be lower than both the Issue Price and the Issuer’s estimated value of the Securities on the Trade Date. Our purchase price, if any, in secondary market transactions would be based on the estimated value of the Securities determined by reference to (i) the then-prevailing internal funding rate (adjusted by a spread) or another appropriate measure of our cost of funds and (ii) our pricing models at that time, less a bid spread determined after taking into account the size of the repurchase, the nature of the assets underlying the Securities and then-prevailing market conditions. The price we report to financial reporting services and to distributors of our Securities for use on customer account statements would generally be determined on the same basis. However, during the period of approximately six months beginning from the Trade Date, we or our affiliates may, in our sole discretion, increase the purchase price determined as described above by an amount equal to the declining differential between the Issue Price and the Issuer’s estimated value of the Securities on the Trade Date, prorated over such period on a straight-line basis, for transactions that are individually and in the aggregate of the expected size for ordinary secondary market repurchases.

In addition to the factors discussed above, the value of the Securities and our purchase price in secondary market transactions after the Trade Date, if any, will vary based on many economic and market factors, including our creditworthiness, and cannot be predicted with accuracy. These changes may adversely affect the value of your Securities, including the price you may receive in any secondary market transactions. Any sale prior to the Maturity Date could result in a substantial loss to you. The Securities are not designed to be short-term trading instruments. Accordingly, you should be able and willing to hold your Securities to maturity.

| ¨ | The Securities Will Not Be Listed and There Will Likely Be Limited Liquidity — The Securities will not be listed on any securities exchange. There may be little or no secondary market for the Securities. We or our affiliates intend to act as market makers for the Securities but are not required to do so and may cease such market making activities at any time. Even if there is a secondary market, it may not provide enough liquidity to allow you to sell the Securities when you wish to do so or at a price advantageous to you. Because we do not expect other dealers to make a secondary market for the Securities, the price at which you may be able to sell your Securities is likely to depend on the price, if any, at which we or our affiliates are willing to buy the Securities. If, at any time, we or our affiliates do not act as market makers, it is likely that there would be little or no secondary market in the Securities. If you have to sell your Securities prior to maturity, you may not be able to do so or you may have to sell them at a substantial loss, even in cases where the price of the Underlying has increased since the Trade Date. |

| ¨ | Many Economic and Market Factors Will Affect the Value of the Securities — While we expect that, generally, the price of the shares of the Underlying will affect the value of the Securities more than any other single factor, the value of the Securities prior to maturity will also be affected by a number of other factors that may either offset or magnify each other, including: |

| ¨ | the expected volatility of the Underlying; |

| ¨ | the composition of the Underlying; |

| ¨ | the price and dividend rates of the shares of the Underlying and the component securities held by the Underlying; |

| ¨ | the exchange rates between the U.S. dollar and the non-U.S. currencies that the component securities held by the Underlying are traded in; |

| ¨ | the occurrence of certain events affecting the Underlying that may or may not require an anti-dilution adjustment; |

| ¨ | the time remaining to the maturity of the Securities; |

| ¨ | interest rates and yields in the market generally and in the markets of the shares of the Underlying and the component securities held by the Underlying; |

| ¨ | geopolitical conditions and a variety of economic, financial, political, regulatory or judicial events that affect the Underlying, the Tracked Index or markets generally; |

| ¨ | supply and demand for the Securities; and |

| ¨ | our creditworthiness, including actual or anticipated downgrades in our credit ratings. |

Because the Securities will be outstanding until the Maturity Date, their value may decline significantly due to the factors described above even if the price of the Underlying remains unchanged from the Initial Price, and any sale prior to the Maturity Date could result in a substantial loss to you. You must hold the Securities to maturity to receive the stated payout from the Issuer.

| ¨ | Potential Deutsche Bank AG Impact on Price — Trading or transactions by Deutsche Bank AG or its affiliates in the component securities held by the Underlying, the Underlying and/or over-the-counter options, futures or other instruments with returns linked to the performance of the Underlying or the component securities held by the Underlying, may adversely affect the price of the component securities held by the Underlying and/or the share price of the Underlying, and, therefore, the value of the Securities. |

| ¨ | Trading and Other Transactions by Us, UBS AG or Our or Its Affiliates in the Equity and Equity Derivative Markets May Impair the Value of the Securities — We or our affiliates expect to hedge our exposure from the Securities by entering into equity and equity derivative transactions, such as over-the-counter options, futures or exchange-traded instruments. We, UBS AG or our or its affiliates may also engage in trading in instruments linked or related to the Underlying on a regular basis as part of our or its general broker-dealer and other businesses, for proprietary accounts, for other accounts under management or to facilitate transactions for customers, including block transactions. Such trading and hedging activities may affect the price of the Underlying and make it less likely that you will receive a positive return on your investment in the Securities. It is possible that we, UBS AG or our or its affiliates could receive substantial returns from these hedging and trading activities while the value of the Securities declines. We, UBS AG or our or its affiliates may also issue or underwrite other securities or financial or derivative instruments with returns linked or related to the Underlying. Introducing competing products into the marketplace in this manner could adversely affect the value of the Securities. Any of the foregoing activities described in this paragraph may reflect trading strategies that differ from, or are in direct opposition to, investors’ trading and investment strategies related to the Securities. |

| ¨ | We, UBS AG or Our or Its Affiliates May Publish Research, Express Opinions or Provide Recommendations That Are Inconsistent with Investing in or Holding the Securities. Any Such Research, Opinions or Recommendations Could Adversely |

8

Affect the Price of the Underlying and the Value of the Securities — We, UBS AG or our or its affiliates may publish research from time to time on financial markets and other matters that could adversely affect the value of the Securities, or express opinions or provide recommendations that are inconsistent with purchasing or holding the Securities. Any research, opinions or recommendations expressed by us, UBS AG or our or its affiliates may not be consistent with each other and may be modified from time to time without notice. You should make your own independent investigation of the merits of investing in the Securities and the Underlying. |

| ¨ | Potential Conflicts of Interest — Deutsche Bank AG or its affiliates may engage in business with the Underlying Stock Issuers whose Securities are held by the Underlying, which may present a conflict between Deutsche Bank AG and you, as a holder of the Securities. We and our affiliates play a variety of roles in connection with the issuance of the Securities, including acting as calculation agent, hedging our obligations under the Securities and determining the Issuer’s estimated value of the Securities on the Trade Date and the price, if any, at which we or our affiliates would be willing to purchase the Securities from you in secondary market transactions. In performing these roles, our economic interests and those of our affiliates are potentially adverse to your interests as an investor in the Securities. The calculation agent will determine, among other things, all values, prices and levels required to be determined for the purposes of the Securities on any relevant date or time. The calculation agent also has some discretion about certain adjustments to the Share Adjustment Factor and will be responsible for determining whether a market disruption event has occurred. Any determination by the calculation agent could adversely affect the return on the Securities. |

| ¨ | The U.S. Federal Income Tax Consequences of an Investment in the Securities Are Uncertain — There is no direct legal authority regarding the proper U.S. federal income tax treatment of the Securities, and we do not plan to request a ruling from the Internal Revenue Service (the “IRS”). Consequently, significant aspects of the tax treatment of the Securities are uncertain, and the IRS or a court might not agree with the treatment of the Securities as prepaid financial contracts that are not debt. If the IRS were successful in asserting an alternative treatment for the Securities, the tax consequences of ownership and disposition of the Securities could be materially and adversely affected. |

Even if the treatment of the Securities as prepaid financial contracts is respected, purchasing a Security could be treated as entering into a “constructive ownership transaction.” In that case, all or a portion of any long-term capital gain you would otherwise recognize on the maturity or disposition of the Security would be recharacterized as ordinary income to the extent such gain exceeded the "net underlying long-term capital gain," and a notional interest charge would apply with respect to the deemed tax liability that would have been incurred if such income had accrued at a constant rate over the period you held the Security.

As described below under “What Are the Tax Consequences of an Investment in the Securities?”, in 2007 the U.S. Treasury Department and the IRS released a notice requesting comments on various issues regarding the U.S. federal income tax treatment of “prepaid forward contracts” and similar instruments. Any Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the Securities, possibly with retroactive effect. You should review carefully the section of the accompanying product supplement entitled “U.S. Federal Income Tax Consequences,” and consult your tax adviser regarding the U.S. federal tax consequences of an investment in the Securities (including possible alternative treatments, the potential application of the “constructive ownership” regime and the issues presented by the 2007 notice), as well as tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction.

9

| Scenario Analysis and Examples at Maturity |

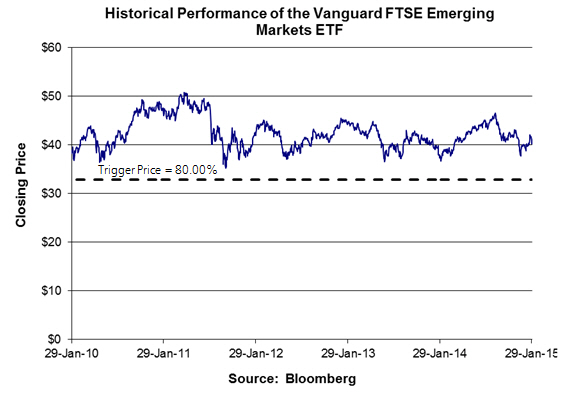

The following table and hypothetical examples below illustrate the Payment at Maturity per $10.00 Face Amount of Securities for a hypothetical range of performances for the Underlying from -100.00% to +100.00% and assume an Initial Price of $40.00, a Trigger Price of $32.00 (80.00% of the hypothetical Initial Price) and a Participation Rate of 154.00% (the midpoint of the Participation Rate range of 149.00% to 159.00%). The actual Initial Price, Trigger Price and Participation Rate will be determined on the Trade Date. The hypothetical Payment at Maturity examples set forth below are for illustrative purposes only and may not be the actual returns applicable to a purchaser of the Securities. The actual Payment at Maturity will be determined based on the Final Price on the Final Valuation Date. You should consider carefully whether the Securities are suitable to your investment goals. The numbers appearing in the table and in the examples below may have been rounded for ease of analysis and it has been assumed that no event affecting the Underlying has occurred during the term of the Securities that would cause the calculation agent to adjust the Share Adjustment Factor.

| Final Price | Underlying Return (%) | Payment at Maturity ($) | Return on Securities (%) |

| $80.00 | 100.00% | $25.40 | 154.00% |

| $76.00 | 90.00% | $23.86 | 138.60% |

| $72.00 | 80.00% | $22.32 | 123.20% |

| $68.00 | 70.00% | $20.78 | 107.80% |

| $64.00 | 60.00% | $19.24 | 92.40% |

| $60.00 | 50.00% | $17.70 | 77.00% |

| $56.00 | 40.00% | $16.16 | 61.60% |

| $52.00 | 30.00% | $14.62 | 46.20% |

| $48.00 | 20.00% | $13.08 | 30.80% |

| $44.00 | 10.00% | $11.54 | 15.40% |

| $40.00 | 0.00% | $10.00 | 0.00% |

| $36.00 | -10.00% | $10.00 | 0.00% |

| $32.00 | -20.00% | $10.00 | 0.00% |

| $28.00 | -30.00% | $7.00 | -30.00% |

| $24.00 | -40.00% | $6.00 | -40.00% |

| $20.00 | -50.00% | $5.00 | -50.00% |

| $16.00 | -60.00% | $4.00 | -60.00% |

| $12.00 | -70.00% | $3.00 | -70.00% |

| $8.00 | -80.00% | $2.00 | -80.00% |

| $4.00 | -90.00% | $1.00 | -90.00% |

| $0.00 | -100.00% | $0.00 | -100.00% |

Example 1 — The Final Price of $44.00 is greater than the Initial Price of $40.00, resulting in an Underlying Return of 10.00%. Because the Underlying Return is 10.00%, Deutsche Bank AG will pay you a Payment at Maturity of $11.54 per $10.00 Face Amount of Securities (a return of 15.40% over the 4-year term of the Securities), calculated as follows:

$10.00 + ($10.00 x Underlying Return x Participation Rate)

$10.00 + ($10.00 x 10.00% x 154.00%) = $11.54

Example 2 — The Final Price is equal to the Initial Price of $40.00, resulting in an Underlying Return of zero. Because the Underlying Return is zero, Deutsche Bank AG will pay you a Payment at Maturity of $10.00 per $10.00 Face Amount of Securities (a return of 0.00% over the 4-year term of the Securities).

Example 3 — The Final Price of $36.00 is less than the Initial Price of $40.00, resulting in an Underlying Return of -10.00%. Because the Underlying Return is negative and the Final Price is greater than the Trigger Price, Deutsche Bank AG will pay you a Payment at Maturity of $10.00 per $10.00 Face Amount of Securities (a return of 0.00% over the 4-year term of the Securities).

Example 4 — The Final Price of $12.00 is less than the Initial Price of $40.00, resulting in an Underlying Return of -70.00%. Because the Underlying Return is negative and the Final Price is less than the Trigger Price, Deutsche Bank AG will pay you a Payment at Maturity of $3.00 per $10.00 Face Amount of Securities (a return of -70.00% over the 4-year term of the Securities), calculated as follows:

$10.00 + ($10.00 x Underlying Return)

$10.00 + ($10.00 x -70.00%) = $3.00

If the Final Price is less than the Trigger Price, you will be fully exposed to any negative Underlying Return, resulting in a loss on the Face Amount that is proportionate to the percentage decline in the price of the Underlying. In this circumstance, you will lose a significant portion or all of your initial investment at maturity. Any payment on the Securities, including any repayment of the Face Amount at maturity, is subject to the creditworthiness of the Issuer and if the Issuer were to default on its payment obligations or become subject to a Resolution Measure, you could lose your entire investment.

10

| The Underlying |

All disclosures contained in this free writing prospectus regarding the Underlying are derived from publicly available information. Neither Deutsche Bank AG nor any of its affiliates have participated in the preparation of, or verified, such information about the Underlying contained in this free writing prospectus. You should make your own investigation into the Underlying.

We obtained the historical closing price information set forth below from Bloomberg L.P., and we have not participated in the preparation of, or verified, such information. You should not take the historical closing prices of the Underlying as an indication of future performance. The Underlying is registered under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Companies with securities registered under the Exchange Act and investment companies registered under the Investment Company Act of 1940, as amended, are required to file financial and other information specified by the SEC periodically. Information filed by the Underlying with the SEC can be reviewed electronically through a web site maintained by the SEC. The address of the SEC’s web site is http://www.sec.gov. Information filed with the SEC by the Underlying under the Exchange Act can be located by reference to its SEC file number provided below.

In addition, information filed with the SEC can be inspected and copied at the Public Reference Section of the SEC, 100 F Street, N.E., Room 1580, Washington, D.C. 20549. Copies of this material can also be obtained from the Public Reference Section, at prescribed rates.

11

| Vanguard FTSE Emerging Markets ETF |

We have derived all information contained in this free writing prospectus regarding the Vanguard FTSE Emerging Markets ETF (the “Underlying”), including, without limitation, its make-up, method of calculation and changes in its components, from publicly available information. We have not participated in the preparation of, or verified, such publicly available information. Such information reflects the policies of, and is subject to change by The Vanguard International Equity Index Funds (the “Vanguard Trust”) and The Vanguard Group, Inc. (“VGI”). The Vanguard FTSE Emerging Markets ETF is an investment portfolio maintained and managed by VGI. VGI is the investment adviser to the Vanguard FTSE Emerging Markets ETF. The Vanguard FTSE Emerging Markets ETF is an exchange traded fund that trades on the NYSE Arca under the ticker symbol “VWO.”

The Vanguard Trust is a registered investment company that consists of numerous separate investment portfolios, including the Vanguard FTSE Emerging Markets ETF. Information provided to or filed with the SEC by the Vanguard Trust pursuant to the Securities Act of 1933, as amended, and the Investment Company Act of 1940, as amended, can be located by reference to SEC file numbers 033-32548 and 811-05972, respectively, through the SEC’s website at http://www.sec.gov. For additional information regarding the Vanguard Trust, VGI and the Vanguard FTSE Emerging Markets ETF, please see the Vanguard FTSE Emerging Markets ETF’s prospectus. In addition, information may be obtained from other sources including, but not limited to, press releases, newspaper articles and other publicly disseminated documents, and we have not participated in the preparation of, or verified, such publicly available information.

The Underlying seeks to replicate as closely as possible, before fees and expenses, the performance of the FTSE Emerging Index (the “Tracked Index”) that measures the investment return of stocks issued by companies located in emerging market countries. The Underlying employs an indexing investment approach by investing substantially all (approximately 95%) of its assets in the common stocks included in the Tracked Index (while employing a form of sampling strategy to reduce risk). The Underlying recently transitioned from tracking the performance of the FTSE Emerging Transition Index (the “Transition Index”) and currently tracks the performance of the Tracked Index. Both the Transition Index and the Tracked Index were developed by FTSE International Limited (“FTSE”) and are calculated, maintained and published by FTSE. FTSE is under no obligation to continue to publish, and may discontinue or suspend the publication of the Transition Index and/or the Tracked Index at any time.

Historically, the Underlying sought to track the performance of the MSCI Emerging Markets Index (the “MXEA”). However, in October 2012, it was announced that the Underlying would switch to tracking the performance of the Tracked Index. Because MXEA includes exposure to equities in South Korea but the Tracked Index does not, the Underlying began tracking the performance of the Transition Index in January 2013 to gradually eliminate its South Korean equities holdings in order to reduce the impact on its existing fund shareholders. The Transition Index was a “dynamic” index that represented the components of the Tracked Index plus the equity of companies located in South Korea. The Underlying followed the Transition Index as it gradually reduced its South Korean equity exposure by approximately 4% each week over a period of 25 weeks while proportionately adding exposure to stocks of companies located in other countries based on their weightings in the Tracked Index. In July 2013, the Underlying finished its transition and began tracking the performance of the Tracked Index.

The FTSE Emerging Index

The Tracked Index is a market-capitalization weighted index representing, as of February 27, 2014, the performance of over 800 large and mid-cap companies in 22 emerging markets. The Tracked Index was launched on June 30, 2000, with a base date of December 31, 1986, and a base value of 100.

Eligibility Countries

The following criteria must be met before a country’s companies can be included in the Tracked Index:

| · | permission for direct equity investment by non-nationals; |

| · | availability of accurate and timely data; |

| · | non-existence of any significant exchange controls which would prevent the timely repatriation of capital or dividends; |

| · | the demonstration of significant international investor interest in the local equity market; and |

| · | existence of adequate liquidity in the market. |

A country’s classification as developed, advanced emerging, or secondary emerging is largely dependent on the following factors:

| · | wealth (GNI per capita); |

| · | total stock market capitalization; |

| · | breadth and depth of market; |

| · | any restrictions on foreign investment; |

| · | free flow of foreign exchange; |

| · | reliable and transparent price discovery; |

| · | efficient market infrastructure (trading, reporting and settlement systems, derivatives market and other factors); and |

| · | oversight by independent regulator |

12

Determining Company Nationality

A company will be allocated to a single country. If a company is incorporated in one country and has its sole listing in the same country, the company will be allocated to that country. In other circumstances, FTSE will refer the company to the FTSE Nationality Committee, which will decide the appropriate nationality for the company. If a company is incorporated in a country, has a listing in that country and listings in other countries, the FTSE Nationality Committee will normally assign the company to the country of incorporation. If a company is incorporated in a country, and is listed only in countries other than the country of incorporation, the FTSE Nationality Committee will normally allocate the company to the country with the greatest liquidity. If a company is incorporated in a country other than a developed country, has no listing in that country and is listed only in one or more developed countries, that company will only be eligible for FTSE Global Equity Index Series inclusion if the country of incorporation is internationally recognized as having a low taxation status that has been approved by the FTSE Nationality Committee.

Eligible Securities

Most types of equity securities are eligible for the Tracked Index. Companies in the business of holding equity and other investments (e.g., investment trusts) which are assumed by the Industry Classification Benchmark as Subsector equity investment instruments and non-equity investment instruments which are assumed by the Industry Classification Benchmark as Subsector non-equity investment instruments are eligible for inclusion. Limited liability partnerships and limited liability companies are not eligible for inclusion. Where a unit comprises equity and non-equity, it will not be eligible for inclusion. Convertible preferred shares and loan stocks are excluded until converted. If a company does not list all of its shares in an eligible class, or does not list an entire class, the unlisted shares are not eligible for the Tracked Index, but they may be included in the review universe for the purpose of ranking companies by their full market capitalization.

Adjustments Applied to Eligible Securities

Eligible companies may be subject to adjustment for free float and multiple classes, as described below.

Free float restrictions include:

| · | shares directly owned by state, regional, municipal and local governments (excluding shares held by independently managed pension plans for governments); |

| · | shares held by sovereign wealth funds where each holding is 10% or greater. If the holding subsequently decreases below 10%, the shares will remain restricted until the holding falls below 7%; |

| · | shares held by directors, senior executives and managers of the company, and by their family and direct relations, and by companies with which they are affiliated; |

| · | shares held within employee share plans; |

| · | shares held by public companies or by non-listed subsidiaries of public companies; |

| · | shares held by founders, promoters, former directors, founding venture capital and private equity firms, private companies and individuals (including employees) where the holding is 10% or greater. If the holding subsequently decreases below 10%, the shares will remain restricted until the holding falls below 7%; |

| · | all shares where the holder is subject to a lock-up provision (for the duration of that provision); |

| · | shares held for publicly announced strategic reasons, including shares held by several holders acting in concert; and |

| · | shares that are subject to on-going contractual agreements (such as swaps) where they would ordinarily be treated as restricted. |

Where there are multiple classes of equity capital in a company, all classes are included and priced separately, provided that:

| · | the secondary class’s full market capitalization (i.e., before the application of any investability weightings) is greater than 25% of the full market capitalization of the company’s principal class and the secondary class is eligible in its own right in all respects; and |

| · | all partly-paid classes of equity are priced on a fully-paid basis if the calls are fixed and are payable at known future dates. Those where future calls are uncertain in either respect are priced on a partly-paid basis. |

Liquidity of Constituents

Each constituent security will be tested for liquidity by calculation of its median daily trading per month. The median trade is calculated by ranking each daily trade total and selecting the middle ranking day. Daily totals with zero trades are included in the ranking; therefore, a security that fails to trade for more than half of the days in a month will have a median trade of zero.