Term sheet No. 688AQ To prospectus dated October 10, 2006, prospectus supplement dated November 13, 2006, product supplement AQ dated February 4, 2009 and underlying supplement 17 dated August 11, 2008 | Registration Statement No. 333-137902 Dated July 1, 2009; Rule 433 |

Deutsche Bank AG, London Branch

$

Buffered Barrier Rebate Securities Linked to a Basket of Equity Components due March 31*, 2011

General

| • | The securities are designed for investors who seek a return linked to the appreciation of a weighted basket of equity components, up to a cap of between 30.0% and 40.0% (to be determined on the Trade Date). If the Basket Closing Level exceeds the Upper Barrier on any day during the Observation Period, a Rebate of 10.0% will be paid at maturity. The first 15% of any decline in the Ending Basket Level as compared to the Initial Basket Level is protected. Accordingly, if the Basket declines by more than 15% from its initial level, investors must be willing to lose up to 85% of their investment. Investors should be willing to forgo interest and dividend payments. |

| • | Senior unsecured obligations of Deutsche Bank AG, London Branch maturing March 31*, 2011. |

| • | Denominations of $1,000 (the “Face Amount“) and multiples thereof, and minimum initial investments of $1,000. |

| • | The securities are expected to price on or about July 28*, 2009 and are expected to settle three business days later on or about July 31*, 2009 (the “Settlement Date“). |

Key Terms

Issuer: | Deutsche Bank AG, London Branch. |

Basket: | The securities are linked to a basket consisting of the S&P 500® Index, the S&P MidCap 400® Index, the Russell 2000® Index and the iShares® MSCI EAFE® Index Fund (each, a“Basket Component” and collectively, the“Basket Components”). |

| Basket Component | Component Weighting | Initial Component Level† | ||

| S&P 500® Index | 40.00% | |||

| S&P MidCap 400® Index | 25.00% | |||

| Russell 2000® Index | 25.00% | |||

| iShares® MSCI EAFE® Index Fund | 10.00% |

| † | The Initial Component Levels will be set on the Trade Date |

Issue Price: | 100% of the Face Amount. |

Payment at Maturity: | At maturity, you will receive a cash payment, for each $1,000 Face Amount, of $1,000 plus the Additional Amount, which may be positive or negative. In no event will the Payment at Maturity be less than $150, subject to the credit of the Issuer. |

Additional Amount: | The Additional Amount paid at maturity per $1,000 Face Amount will equal: |

If a Barrier Event has not occurred and

| • | the Ending Basket Level is greater than or equal to the Initial Basket Level: $1,000 x Basket Return |

| • | the Ending Basket Level declines from the Initial Basket Level by 15% or less: $0 |

| • | the Ending Basket Level declines from the Initial Basket Level by more than 15%: $1,000 x (Basket Return + Buffer Amount) |

If a Barrier Event has occurred and

| • | the Ending Basket Level is greater than or equal to the Initial Basket Level: $1,000 x Rebate |

| • | the Ending Basket Level declines from the Initial Basket Level by 15% or less: $1,000 x Rebate |

| • | the Ending Basket Level declines from the Initial Basket Level by more than 15%: $1,000 x (Basket Return + Buffer Amount + Rebate) |

Buffer Amount: | 15% |

Basket Return: | The performance of the Basket from the Initial Basket Level to the Ending Basket Level, calculated as follows: |

Ending Basket Level – Initial Basket Level

Initial Basket Level

The Basket Return may be positive or negative.

Barrier Event: | A Barrier Event occurs if, on any trading day during the Observation Period, the Basket Closing Level is greater than the Upper Barrier. |

Upper Barrier: | 130% to 140% of the Initial Basket Level (to be determined on the Trade Date). |

Observation Period: | The period of trading days on which there is no market disruption event with respect to the Basket commencing on (and including) the Trade Date to (and including) the Final Valuation Date. |

Rebate: | 10.0% |

Initial Basket Level: | 100 |

Ending Basket Level: | The Basket Closing Level on the Final Valuation Date. |

Basket Closing Level: | On any trading day during the Observation Period, the Basket Closing Level will be calculated as follows: |

100 x [1 + (S&P 500® Index return x 40.00%) + (S&P MidCap 400® Index return x 25.00%) + (Russell 2000® Index return x 25.00%) + (iShares® MSCI EAFE® Index Fund return x 10.00%)] For any trading day, the return for each Basket Component which is an index is the percentage change from the respective Initial Component Level to the respective index closing level on the such trading day. For any trading day, the return for each Basket Component which is an exchange traded fund is the percentage change from the respective Initial Component Level to the closing price of one share of the fund on such trading day multiplied by the then-current Share Adjustment Factor for that exchange traded fund. |

Share Adjustment Factor: | Initially 1.0, subject to adjustment for certain actions affecting the iShares® MSCI EAFE® Index Fund. See “Description of Securities — Anti-dilution Adjustments for Funds” in the accompanying product supplement. |

Trade Date: | July 28*, 2009 |

Final Valuation Date: | March 28*, 2011, subject to postponement in the event of a market disruption event and as described under “Description of Securities—Adjustments to Valuation Dates and Payment Dates” in the accompanying product supplement. |

Maturity Date: | March 31*, 2011, subject to postponement in the event of a market disruption event and as described under “Description of Securities—Adjustments to Valuation Dates and Payment Dates” in the accompanying product supplement. |

Listing: | The securities will not be listed on any securities exchange. |

CUSIP: | 2515A0 L8 4 |

ISIN: | US2515A0L844 |

| * | Expected. In the event that we make any change to the expected Trade Date and Settlement Date, the Final Valuation Date and Maturity Date may be changed so that the stated term of the securities and the length of the Observation Period remain the same. |

Investing in the securities involves a number of risks. See “Risk Factors” beginning on page 9 of the accompanying product supplement and “Selected Risk Considerations” beginning on page TS-6 of this term sheet.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities or passed upon the accuracy or the adequacy of this term sheet or the accompanying product supplement, underlying supplement, prospectus supplement or prospectus. Any representation to the contrary is a criminal offense.

Price to Public | Max. Total Discounts, Commissions and Fees(1) | Minimum Proceeds to Us | ||||

| Per Security | $1,000.00 | $7.50 | $992.50 | |||

| Total | $ | $ | $ |

| (1) | For more detailed information about discounts and commissions, please see “Supplemental Underwriting Information” on the last page of this term sheet. The securities will be sold with varying underwriting discounts and commissions in an amount not to exceed $7.50 per $1,000.00 of securities. |

The securities are not bank deposits and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency. In addition, the securities arenot guaranteed under the Federal Deposit Insurance Corporation’s Temporary Liquidity Guarantee Program.

| Deutsche Bank Securities | Deutsche Bank Trust Company Americas |

ADDITIONAL TERMS SPECIFIC TO THE SECURITIES

| • | You should read this term sheet together with the prospectus dated October 10, 2006, as supplemented by the prospectus supplement dated November 13, 2006 relating to our Series A global notes of which these securities are a part, and the more detailed information contained in product supplement AQ dated February 4, 2009 and in underlying supplement 17 dated August 11, 2008. You may access these documents on the SEC website atwww.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website): |

| • | Product supplement AQ dated February 4, 2009: |

http://www.sec.gov/Archives/edgar/data/1159508/000119312509018934/d424b21.pdf

| • | Underlying supplement 17 dated August 11, 2008: |

http://www.sec.gov/Archives/edgar/data/1159508/000119312508173702/d424b21.pdf

| • | Prospectus supplement dated November 13, 2006: |

http://www.sec.gov/Archives/edgar/data/1159508/000119312506233129/d424b3.htm

| • | Prospectus dated October 10, 2006: |

http://www.sec.gov/Archives/edgar/data/1159508/000095012306012432/u50845fv3asr.htm

| • | Our Central Index Key, or CIK, on the SEC website is 0001159508. As used in this term sheet, “we,” “us” or “our” refers to Deutsche Bank AG, including, as the context requires, acting through one of its branches. |

| • | This term sheet, together with the documents listed above, contains the terms of the securities and supersedes all other prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth in “Risk Factors” in the accompanying product supplement, as the securities involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisers before deciding to invest in the securities. |

| • | Deutsche Bank AG has filed a registration statement (including a prospectus) with the Securities and Exchange Commission, or SEC, for the offering to which this term sheet relates. Before you invest, you should read the prospectus in that registration statement and the other documents relating to this offering that Deutsche Bank AG has filed with the SEC for more complete information about Deutsche Bank AG and this offering. You may obtain these documents without cost by visiting EDGAR on the SEC website at www.sec.gov. Alternatively, Deutsche Bank AG, any agent or any dealer participating in this offering will arrange to send you the prospectus, prospectus supplement, product supplement, underlying supplement and this term sheet if you so request by calling toll-free 1-800-311-4409. |

| • | You may revoke your offer to purchase the securities at any time prior to the time at which we accept such offer on the date the securities are priced. We reserve the right to change the terms of, or reject any offer to purchase the securities prior to their issuance. In the event of any changes to the terms of the securities, we will notify you and you will be asked to accept such changes in connection with your purchase. You may also choose to reject such changes in which case we may reject your offer to purchase. |

TS-1

What is the Payment at Maturity of the Securities Assuming a Range of Performance for the Basket?

The following table illustrates a range of hypothetical Payments at Maturity of the securities. The “payment return” as used in this term sheet is the number, expressed as a percentage, that results from comparing the Payment at Maturity per $1,000 Face Amount of securities to $1,000. The hypothetical payment returns set forth below assume an Initial Basket Level of 100, an Upper Barrier of 135.00 (135% of the Initial Basket Level (the midpoint of the range indicated on the cover of this term sheet)), a Buffer Amount of 15%, and a Rebate of 10%. The actual Upper Barrier will be set on the Trade Date. The hypothetical payment returns set forth below are for illustrative purposes only and are not the actual payment returns applicable to a purchaser of the securities. The numbers appearing in the following table and examples have been rounded for ease of analysis.

The BasketNever Closes Above the Upper Barrier on any Trading Day during the Observation Period | The Basket Closes Above the Upper Barrier on any Trading Day during the Observation Period | |||||||||||||

Hypothetical Level | Basket (%) | Additional ($) | Payment at ($) | Payment (%) | Additional ($) | Payment at ($) | Payment (%) | |||||||

200.00 | 100.00% | N/A | N/A | N/A | $100.00 | $1,100.00 | 10.00% | |||||||

175.00 | 75.00% | N/A | N/A | N/A | $100.00 | $1,100.00 | 10.00% | |||||||

150.00 | 50.00% | N/A | N/A | N/A | $100.00 | $1,100.00 | 10.00% | |||||||

135.00 | 35.00% | $350.00 | $1,350.00 | 35.00% | $100.00 | $1,100.00 | 10.00% | |||||||

130.00 | 30.00% | $300.00 | $1,300.00 | 30.00% | $100.00 | $1,100.00 | 10.00% | |||||||

125.00 | 25.00% | $250.00 | $1,250.00 | 25.00% | $100.00 | $1,100.00 | 10.00% | |||||||

115.00 | 15.00% | $150.00 | $1,150.00 | 15.00% | $100.00 | $1,100.00 | 10.00% | |||||||

110.00 | 10.00% | $100.00 | $1,100.00 | 10.00% | $100.00 | $1,100.00 | 10.00% | |||||||

105.00 | 5.00% | $50.00 | $1,050.00 | 5.00% | $100.00 | $1,100.00 | 10.00% | |||||||

100.00 | 0.00% | $0.00 | $1,000.00 | 0.00% | $100.00 | $1,100.00 | 10.00% | |||||||

95.00 | -5.00% | $0.00 | $1,000.00 | 0.00% | $100.00 | $1,100.00 | 10.00% | |||||||

90.00 | -10.00% | $0.00 | $1,000.00 | 0.00% | $100.00 | $1,100.00 | 10.00% | |||||||

85.00 | -15.00% | $0.00 | $1,000.00 | 0.00% | $100.00 | $1,100.00 | 10.00% | |||||||

75.00 | -25.00% | -$100.00 | $900.00 | -10.00% | $0.00 | $1,000.00 | 0.00% | |||||||

70.00 | -30.00% | -$150.00 | $850.00 | -15.00% | -$50.00 | $950.00 | -5.00% | |||||||

60.00 | -40.00% | -$250.00 | $750.00 | -25.00% | -$150.00 | $850.00 | -15.00% | |||||||

50.00 | -50.00% | -$350.00 | $650.00 | -35.00% | -$250.00 | $750.00 | -25.00% | |||||||

25.00 | -75.00% | -$600.00 | $400.00 | -60.00% | -$500.00 | $500.00 | -50.00% | |||||||

0.00 | -100.00% | -$850.00 | $150.00 | -85.00% | -$750.00 | $250.00 | -75.00% | |||||||

The following hypothetical examples illustrate how the Payments at Maturity set forth in the table above are calculated.

Example 1: The level of the Basket increases by 25% from the Initial Basket Level of 100.00 to an Ending Basket Level of 125.00, and:

| • | no Barrier Event occurs. Because the Ending Basket Level is greater than the Initial Basket Level and no Barrier Event occurs, the investor receives a Payment at Maturity of $1,250.00 per $1,000 Face Amount of securities, calculated as follows: |

$1,000 + ($1,000 x Basket Return) =

$1,000 + ($1,000 x 25.00%) = $1,250.00

TS-2

| • | a Barrier Event occurs. Because the Ending Basket Level is greater than the Initial Basket Level and a Barrier Event occurs, the investor receives a Payment at Maturity of $1,100.00 per $1,000 Face Amount of securities, calculated as follows: |

$1,000 + ($1,000 x Rebate) =

$1,000 + ($1,000 x 10.0%) = $1,100.00

Example 2: The level of the Basket decreases by 5% from the Initial Basket Level of 100.00 to an Ending Basket Level of 95.00, and:

| • | no Barrier Event occurs. Because the Basket decreases by less than the Buffer Amount of 15% and no Barrier Event occurs, the investor receives a Payment at Maturity of $1,000.00 per $1,000 Face Amount of securities. |

| • | a Barrier Event occurs. Because the Basket decreases by less than the Buffer Amount of 15% and a Barrier Event occurs, the investor receives a Payment at Maturity of $1,100.00 per $1,000 Face Amount of securities, calculated as follows: |

$1,000 + ($1,000 x Rebate) =

$1,000 + ($1,000 x 10.0%) = $1,100.00

Example 3: The level of the Basket decreases by 40% from the Initial Basket Level of 100.00 to an Ending Basket Level of 60.00, and:

| • | no Barrier Event occurs. Because the Basket decreases by more than the Buffer Amount of 15% and no Barrier Event occurs, the investor receives a Payment at Maturity of $750.00 per $1,000 Face Amount of securities, calculated as follows: |

$1,000 + [$1,000 x (Basket Return + Buffer Amount)] =

$1,000 + [$1,000 x (-40.00% + 15.00%)] = $750.00

| • | a Barrier Event occurs. Because the Basket decreases by more than the Buffer Amount of 15% and a Barrier Event occurs, the investor receives a Payment at Maturity of $850.00 per $1,000 Face Amount of securities, calculated as follows: |

$1,000 + [$1,000 x (Basket Return + Buffer Amount + Rebate)] =

$1,000 + [$1,000 x (-40.00% + 15.00% + 10.0%)] = $850.00

Selected Purchase Considerations

| • | APPRECIATION POTENTIAL IS LIMITED — The securities provide the opportunity to participate in any positive Basket Return up to a cap of 30% to 40% (the Upper Barrier, which will be determined on the Trade Date). If a Barrier Event occurs, your return will be limited to a Rebate of 10.0%, regardless of any positive performance of the Basket. Because the securities are our senior unsecured obligations, payment of any amount at maturity is subject to our ability to pay our obligations as they become due. |

| • | LIMITED PROTECTION AGAINST LOSS — Payment at maturity of the securities is protected against a decline in the Ending Basket Level, as compared to the Initial Basket Level, of up to 15% (the Buffer Amount) if no Barrier Event occurs and up to 25% (the sum of the Buffer Amount and the Rebate) if a Barrier Event occurs. If the Ending Basket Level declines as compared to the Initial Basket Level, for every 1% decline of the Basket beyond 15% (the Buffer Amount) of the Initial Basket Level if no Barrier Event occurs and beyond 25% (the sum of the Buffer Amount and the Rebate) of the Initial Basket Level if a Barrier Event occurs, you will lose an amount equal to 1% of the Face Amount of your securities. You may lose up to 85% of your investment if no Barrier Event occurs and up to 75% of your investment if a Barrier Event occurs. |

TS-3

| • | RETURN LINKED TO THE PERFORMANCE OF A WEIGHTED BASKET OF COMPONENTS— The return on the securities, which may be positive or negative, is linked to a basket consisting of the S&P 500® Index, the S&P MidCap 400® Index, the Russell 2000® Index and the iShares® MSCI EAFE® Index Fund. |

The S&P 500® Index

The S&P 500® Index is intended to provide a performance benchmark for the U.S. equity markets. The calculation of the level of the S&P 500® Index is based on the relative value of the aggregate market value of the common stocks of 500 companies as of a particular time as compared to the aggregate average market value of the common stocks of 500 similar companies during the base period of the years 1941 through 1943.This is just a summary of the S&P 500® Index. For more information on the S&P 500® Index, including information concerning its composition, calculation methodology and adjustment policy, please see the section entitled “The S&P Indices — The S&P 500 Index” in the accompanying underlying supplement no. 17 dated August 11, 2008.

The S&P MidCap 400® Index

The S&P MidCap 400® Index is intended to provide a benchmark for performance measurement of the medium capitalization segment of the U.S. equity markets. It tracks the stock price movement of 400 companies with mid-sized market capitalizations, primarily ranging from $1.5 billion to $5.5 billion.This is just a summary of the S&P MidCap 400® Index. For more information on the S&P MidCap 400® Index, including information concerning its composition, calculation methodology and adjustment policy, please see the section entitled “The S&P Indices — The S&P MidCap 400® Index” in the accompanying underlying supplement no. 17 dated August 11, 2008.

The Russell 2000® Index

The Russell 2000® Index is designed to track the performance of the small capitalization segment of the U.S. equity market. The Russell 2000® Index measures the composite price performance of stocks of approximately 2,000 companies domiciled in the U.S. and its territories and consists of the smallest 2,000 companies included in the Russell 3000® Index. The Russell 2000® Index represents approximately 10% of the total market capitalization of the Russell 3000® Index.This is just a summary of the Russell 2000® Index. For more information on the Russell 2000® Index, including information concerning its composition, calculation methodology and adjustment policy, please see the section entitled “The Russell Indices — Russell 2000® Index” in the accompanying underlying supplement no. 17 dated August 11, 2008.

The iShares® MSCI EAFE® Index Fund (the “Index Fund”)

The iShares® MSCI EAFE® Index Fund is an exchange-traded fund managed by iShares® Trust, a registered investment company. The iShares® Trust consists of numerous separate investment portfolios, including the iShares® MSCI EAFE® Index Fund. The iShares® MSCI EAFE® Index Fund seeks to provide investment results that correspond generally to the price and yield performance, before fees and expenses, of publicly traded securities in the European, Australasian and Far Eastern markets, as measured by the MSCI EAFE® Index. The iShares® MSCI EAFE® Index Fund trades on the NYSE Arca, Inc. under the ticker symbol “EFA.” It is possible that this fund may not fully replicate or may in certain circumstances diverge significantly from the performance of the MSCI EAFE® Index due to the temporary unavailability of certain securities in the secondary markets, the performance of any derivative instruments contained in this fund, the fees and expenses of the fund or due to other circumstances.This section is a summary only of the iShares® MSCI EAFE® Index Fund. For more information on the iShares Exchange

TS-4

Traded Funds, including information concerning calculation methodology and adjustment policy, please see the section entitled “The iShares Exchange Traded Funds — Methodology” in the accompanying underlying supplement no. 17 dated August 11, 2008. For more information on the MSCI EAFE® Index, please see the section entitled “The MSCI Indices — The MSCI EAFE® Index” in the accompanying underlying supplement no. 17 dated August 11, 2008.

| • | UNCERTAIN TAX CONSEQUENCES—You should review carefully the section of the accompanying product supplement entitled “Certain U.S. Federal Income Tax Consequences.” Although the tax consequences of an investment in the securities are uncertain, we believe it is reasonable to treat the securities as prepaid financial contracts for U.S. federal income tax purposes. Based on current law, under this treatment you should not be required to recognize taxable income prior to the maturity of your securities, other than pursuant to a sale or exchange, and your gain or loss on the securities should be long-term capital gain or loss if you hold the securities for more than one year. If, however, the Internal Revenue Service (the “IRS“) were successful in asserting an alternative treatment for the securities, the timing and/or character of income on the securities might differ materially and adversely from the description herein. We do not plan to request a ruling from the IRS, and no assurance can be given that the IRS or a court will agree with the tax treatment described in this term sheet and the accompanying product supplement. |

In December 2007, the Department of the Treasury (“Treasury“) and the IRS released a notice requesting comments on various issues regarding the U.S. federal income tax treatment of “prepaid forward contracts” and similar instruments, such as the securities. The notice focuses in particular on whether to require holders of these instruments to accrue income over the term of their investment. It also asks for comments on a number of related topics, including the character of income or loss with respect to these instruments; the relevance of factors such as the nature of the underlying property to which the instruments are linked; the degree, if any, to which income (including any mandated accruals) realized by non-U.S. holders should be subject to withholding tax; and whether these instruments are or should be subject to the “constructive ownership” regime, which very generally can operate to recharacterize certain long-term capital gain as ordinary income that is subject to an interest charge. While the notice requests comments on appropriate transition rules and effective dates, any Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the securities, possibly with retroactive effect.

Under current law, the United Kingdom will not impose withholding tax on payments made with respect to the securities.

For a discussion of certain German tax considerations relating to the securities, you should refer to the section in the accompanying prospectus supplement entitled “Taxation by Germany of Non-Resident Holders.”

We do not provide any advice on tax matters. Both U.S. and non-U.S. holders should consult their tax advisers regarding all aspects of the U.S. federal tax consequences of investing in the securities (including possible alternative treatments and the issues presented by the December 7, 2007 notice), as well as any tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction.

TS-5

Selected Risk Considerations

An investment in the securities involves significant risks. Investing in the securities is not equivalent to investing directly in the Basket Components or in any of the components underlying the Basket Components. These risks are explained in more detail in the “Risk Factors” section of the accompanying product supplement.

| • | YOUR INVESTMENT IN THE SECURITIES MAY RESULT IN A LOSS — Payment at maturity of the securities is protected against a decline in the Ending Basket Level, as compared to the Initial Basket Level, of up to 15% (the Buffer Amount) if no Barrier Event occurs and up 25% (the sum of the Buffer Amount and the Rebate) if a Barrier Event occurs. If the Ending Basket Level declines as compared to the Initial Basket Level, for every 1% decline of the Basket beyond 15% (the Buffer Amount) of the Initial Basket Level if no Barrier Event occurs and beyond 25% (the sum of the Buffer Amount and the Rebate) of the Initial Basket Level if a Barrier Event occurs, you will lose an amount equal to 1% of the Face Amount of your securities. You may lose up to 85% of your investment if no Barrier Event occurs and up to 75% of your investment if a Barrier Event occurs. |

| • | IF A BARRIER EVENT OCCURS, YOUR ADDITIONAL AMOUNT WILL BE LIMITED TO THE REBATE, REGARDLESS OF ANY POSITIVE PERFORMANCE OF THE BASKET — If a Barrier Event occurs, your Additional Amount will be limited to the Rebate, regardless of any positive performance of the Basket. You will not benefit from any appreciation of the Basket beyond the Rebate. If a Barrier Event does not occur, your return will be limited by the Upper Barrier and in no event will you receive more than $1,300 to $1,400 (to be determined on the Trade Date) per $1,000 security Face Amount at maturity. |

| • | THE SECURITIES ARE SUBJECT TO OUR CREDITWORTHINESS— An actual or anticipated downgrade in our credit rating will likely have an adverse effect on the market value of the securities. The payment at maturity on the securities is subject to our creditworthiness. |

| • | THE SECURITIES DO NOT PAY INTEREST — Unlike ordinary debt securities, the securities do not pay interest and do not guarantee any return of your initial investment at maturity. |

| • | ASSUMING NO CHANGES IN MARKET CONDITIONS OR ANY OTHER RELEVANT FACTORS, THE MARKET VALUE OF THE SECURITIES ON THE SETTLEMENT DATE (AS DETERMINED BY DEUTSCHE BANK AG) WILL BE LESS THAN THE ORIGINAL ISSUE PRICE — While the payment at maturity described in this term sheet is based on the full Face Amount of your securities, the original Issue Price of the securities includes the agents’ commission and the cost of hedging our obligations under the securities through one or more of our affiliates. Therefore, the market value of the securities on the Settlement Date, assuming no changes in market conditions or other relevant factors, will be less than the original Issue Price. The inclusion of commissions and hedging costs in the original Issue Price will also decrease the price, if any, at which we will be willing to purchase the securities after the Settlement Date, and any sale on the secondary market could result in a substantial loss to you. Our hedging costs include the projected profit that we or our affiliates are expected to realize in consideration for assuming the risks inherent in managing the hedging transactions. The securities are not designed to be short-term trading instruments. Accordingly, you should be willing and able to hold your securities to maturity. |

TS-6

| • | THE SECURITIES WILL NOT BE LISTED AND THERE WILL LIKELY BE LIMITED LIQUIDITY — The securities will not be listed on any securities exchange. Deutsche Bank AG or its affiliates intend to offer to purchase the securities in the secondary market but are not required to do so and may cease such market-making activities at any time. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the securities easily. Because other dealers are not likely to make a secondary market for the securities, the price at which you may be able to trade your securities is likely to depend on the price, if any, at which Deutsche Bank AG or its affiliates are willing to buy the securities. |

| • | TRADING BY US OR OUR AFFILIATES MAY IMPAIR THE VALUE OF THE SECURITIES— We and our affiliates are active participants in the equity markets as dealers, proprietary traders and agents for our customers, and therefore at any given time we may be a party to one or more equities transactions. In addition, we or one or more of our affiliates may hedge our exposure from the securities by entering into various transactions. We may adjust these hedges at any time and from time to time. Our trading and hedging activities may have a material effect on the prices of the component stocks underlying the Basket Components and consequently have an impact on the performance of the Basket, and may adversely affect the Basket Return and/or may cause the Basket to close above the Upper Barrier. It is possible that we or our affiliates could receive significant returns from these hedging activities while the value of or amounts payable under the securities may decline. |

| • | CHANGES IN THE VALUE OF THE BASKET COMPONENTS MAY OFFSET EACH OTHER — Price movements in the Basket Components may not correlate with each other. At a time when the levels of some of the Basket Components increase, the levels of other Basket Components may not increase as much or may decline. Therefore, in calculating the Basket Return, increases in the level of one or more of the Basket Components may be moderated, offset or more than offset by lesser increases or declines in the levels of the other Basket Components. |

| • | THE BASKET COMPONENTS ARE UNEQUALLY WEIGHTED— The Basket Components are unequally weighted. Accordingly, performances by the Basket Components with higher weightings will influence the Ending Basket Level and therefore the Basket Return to a greater degree than the performances of Basket Components with lower weightings. If one or more of the Basket Components with higher weightings perform poorly, that poor performance could negate or diminish the effect on the Ending Basket Level of any positive performance by the lower weighted Basket Components. |

| • | NO COUPON OR DIVIDEND PAYMENTS OR VOTING RIGHTS — As a holder of the securities, you will not receive coupon payments, and you will not have voting rights or rights to receive cash dividends or other distributions or other rights that holders of the component stocks underlying the Basket Components or holders of shares of the iShares® MSCI EAFE® Index Fund would have. |

| • | WE AND OUR AFFILIATES AND AGENTS MAY PUBLISH RESEARCH, EXPRESS OPINIONS OR PROVIDE RECOMMENDATIONS THAT ARE INCONSISTENT WITH INVESTING IN OR HOLDING THE SECURITIES. ANY SUCH RESEARCH, OPINIONS OR RECOMMENDATIONS COULD AFFECT THE LEVEL OF THE BASKET TO WHICH THE SECURITIES ARE LINKED OR THE MARKET VALUE OF THE SECURITIES — Deutsche Bank AG, its affiliates and agents publish research from time to time on financial markets and other matters that may influence the value of the securities, or express opinions or provide recommendations that are inconsistent with |

TS-7

purchasing or holding the securities. Deutsche Bank AG, its affiliates and agents may have published research or other opinions that are inconsistent with the investment view implicit in the securities. Any research, opinions or recommendations expressed by Deutsche Bank AG, its affiliates or agents may not be consistent with each other and may be modified from time to time without notice. Investors should make their own independent investigation of the merits of investing in the securities and each Basket Component to which the securities are linked. |

| • | OUR ACTIONS AS CALCULATION AGENT AND OUR HEDGING ACTIVITY MAY ADVERSELY AFFECT THE VALUE OF THE SECURITIES — We and our affiliates play a variety of roles in connection with the issuance of the securities, including acting as calculation agent and hedging our obligations under the securities. In performing these duties, the economic interests of the calculation agent and other affiliates of ours are potentially adverse to your interests as an investor in the securities. |

| • | MANY ECONOMIC AND MARKET FACTORS WILL AFFECT THE VALUE OF THE SECURITIES — In addition to the levels of the Basket Components on any day, the value of the securities will be affected by a number of complex and interrelated economic and market factors that may either offset or magnify each other, including: |

| • | whether the Basket Closing Level has exceeded the Upper Barrier on any trading day during the Observation Period and, if not, whether the level of the Basket is close to the Upper Barrier; |

| • | the expected volatility of each Basket Component; |

| • | the time remaining to maturity of the securities; |

| • | the dividend rate on the stocks held by the iShares® MSCI EAFE® Index Fund (while not paid to holders of the securities, dividend payments on the stocks held by the iShares® MSCI EAFE® Index Fund may influence the market price of the shares of the iShares® MSCI EAFE® Index Fund and the market value of options on exchange traded fund shares and, therefore, affect the value of the securities); |

| • | the occurrence of certain events affecting the iShares® MSCI EAFE® Index Fund that may or may not require an anti-dilution adjustment; |

| • | the market price and dividend rate on the component stocks underlying each Basket Component; |

| • | interest and yield rates in the market generally and in the markets of the component stocks underlying each Basket Component; |

| • | a variety of economic, financial, political, regulatory or judicial events; |

| • | the composition of the Basket Components and any changes to the component stocks underlying the Basket Components; |

| • | supply and demand for the securities; and |

| • | our creditworthiness, including actual or anticipated downgrades in our credit ratings. |

| • | ANTI-DILUTION PROTECTION IS LIMITED — The calculation agent will make adjustments to the Share Adjustment Factor, which will initially be set at 1.0, for certain events affecting the shares of the iShares® MSCI EAFE® Index Fund. See “Description of Securities — Anti-Dilution Adjustments for Funds” in the accompanying product supplement. The calculation agent is not required, however, to make such adjustments in response to all events that could affect the shares of the iShares® MSCI EAFE® Index Fund. If an event occurs that does not require the calculation agent to make an adjustment, the value of the securities may be materially and adversely affected. |

TS-8

| • | ADJUSTMENTS TO THE ISHARES® MSCI EAFE® INDEX FUND OR TO THE MSCI EAFE INDEX COULD ADVERSELY AFFECT THE VALUE OF THE SECURITIES — Barclays Global Fund Advisors (“BGFA”) is the investment advisor to the iShares® MSCI EAFE® Index Fund, which seeks investment results that correspond generally to the level and yield performance, before fees and expenses, of the MSCI EAFE® Index. The stocks included in the MSCI EAFE® Index are selected by MSCI Inc. (“MSCI”), the publisher of the MSCI EAFE® Index. The MSCI EAFE® Index is calculated and published by MSCI. MSCI can add, delete or substitute the stocks underlying the MSCI EAFE® Index, which could change the value of the MSCI EAFE® Index. Pursuant to its investment strategy or otherwise, BGFA may add, delete, or substitute the stocks composing the iShares® MSCI EAFE® Index Fund. Any of these actions could cause or contribute to large movements in the prices of the component securities held by the iShares® MSCI EAFE® Index Fund, which could adversely affect the value of the securities. |

| • | TRANSITION OF THE ISHARES® MSCI EAFE® INDEX FUND’S INVESTMENT ADVISOR — On April 9, 2009, Barclays Global Investors UK Holdings Limited (“Barclays”), the parent company of BGFA, entered into an agreement to sell its interest in BGFA and certain affiliated companies to Blue Sparkle, L.P., a Cayman Islands limited partnership (the “Transaction”). Blue Sparkle, L.P. is an investment vehicle for private equity funds affiliated with CVC Capital Partners Group SICAV-FIS S.A., a private equity and investment advisory firm. The Transaction is subject to certain regulatory approvals, as well as other conditions to closing. Under the Investment Company Act of 1940, as amended, completion of the Transaction will cause the automatic termination of the iShares® MSCI EAFE® Index Fund’s current investment advisory agreement with BGFA. In order for the management of the iShares® MSCI EAFE® Index Fund to continue uninterrupted, the iShares® MSCI EAFE® Index Fund’s Board of Directors or Trustees (the “Board”) will be asked to approve a new investment advisory agreement with BGFA. If approved by the Board, the new investment advisory agreement will be submitted to the shareholders of the iShares® MSCI EAFE® Index Fund for their approval. The failure to obtain such approvals could cause interruptions in the management of the iShares® MSCI EAFE® Index Fund which could have an adverse effect on the value of the iShares® MSCI EAFE® Index Fund and consequently on the value of your securities. |

| • | THE ISHARES® MSCI EAFE® INDEX FUND AND THE MSCI EAFE® INDEX ARE DIFFERENT — The performance of the iShares® MSCI EAFE® Index Fund may not exactly replicate the performance of the MSCI EAFE® Index because the iShares® MSCI EAFE® Index Fund will reflect transaction costs and fees that are not included in the calculation of the MSCI EAFE® Index. It is also possible that the iShares® MSCI EAFE® Index Fund may not fully replicate or may in certain circumstances diverge significantly from the performance of the MSCI EAFE® Index due to the temporary unavailability of certain securities in the secondary market, the performance of any derivative instruments contained in this fund or due to other circumstances. BGFA may invest up to 10% of the iShares® MSCI EAFE® Index Fund’s assets in futures contracts, options on futures contracts, other types of options, and swaps related to the MSCI EAFE® Index as well as cash and cash equivalents, including shares of money market funds advised by BGFA or its affiliates. The iShares® MSCI EAFE® Index Fund may use options and futures contracts, convertible securities and structured notes in seeking performance that corresponds to the MSCI EAFE® Index and in managing cash flows. |

| • | CURRENCY EXCHANGE RISK — The prices of the stocks underlying the MSCI EAFE® Index are converted into U.S. dollars in calculating the level of the MSCI EAFE® Index. |

TS-9

As a result, the holders of the securities will be exposed to currency exchange risk with respect to each of the currencies in which the equity securities underlying the MSCI EAFE® Index trade. Currency markets may be highly volatile, particularly in relation to emerging or developing nations’ currencies and, in certain market conditions, also in relation to developed nations’ currencies. Significant changes, including changes in liquidity and prices, can occur in such markets within very short periods of time. Foreign currency rate risks include, but are not limited to, convertibility risk and market volatility and potential interference by foreign governments through regulation of local markets, foreign investment or particular transactions in foreign currency. These factors may adversely affect the values of the component stocks underlying the MSCI EAFE® Index, and the value of your securities. |

| • | NON-U.S. SECURITIES MARKETS RISKS — The stocks included in the MSCI EAFE® Index are issued by foreign companies in foreign securities markets. These stocks may be more volatile and may be subject to different political, market, economic, exchange rate, regulatory and other risks which may have a negative impact on the performance of the securities. |

| • | THE U.S. FEDERAL INCOME TAX CONSEQUENCES OF AN INVESTMENT IN THE SECURITIES ARE UNCLEAR —There is no direct legal authority regarding the proper U.S. federal income tax treatment of the securities, and we do not plan to request a ruling from the IRS. Consequently, significant aspects of the tax treatment of the securities are uncertain, and no assurance can be given that the IRS or a court will agree with the treatment of the securities as prepaid financial contracts. If the IRS were successful in asserting an alternative treatment for the securities, the timing and/or character of income thereon might differ materially and adversely from the description herein. For example, because the iShares® MSCI EAFE® Index Fund is a Basket Component, the securities could be treated (in whole or in part) as subject to the “constructive ownership” regime, which very generally can operate to recharacterize certain long-term capital gain as ordinary income that is subject to an interest charge. In addition, as described above under “Uncertain Tax Consequences,” in December 2007, Treasury and the IRS released a notice requesting comments on various issues regarding the U.S. federal income tax treatment of “prepaid forward contracts” and similar instruments, such as the securities. Any Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the securities, possibly with retroactive effect. Both U.S. and non-U.S. holders should review carefully the section of the accompanying product supplement entitled “Certain U.S. Federal Income Tax Consequences,” and consult their tax advisers regarding the U.S. federal income tax consequences of an investment in the securities (including possible alternative treatments and the issues presented by the December 2007 notice), as well as any tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction. |

TS-10

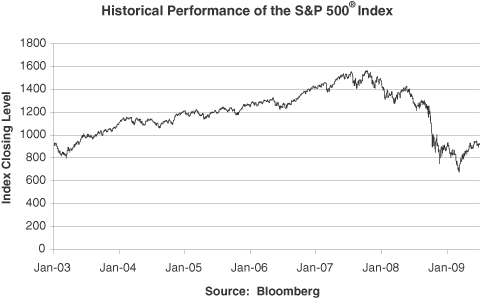

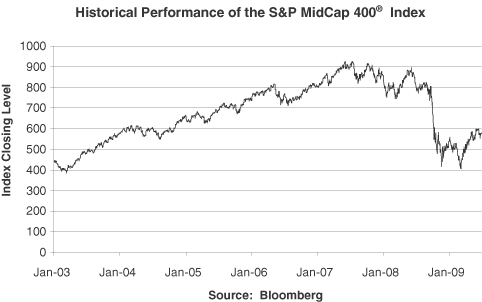

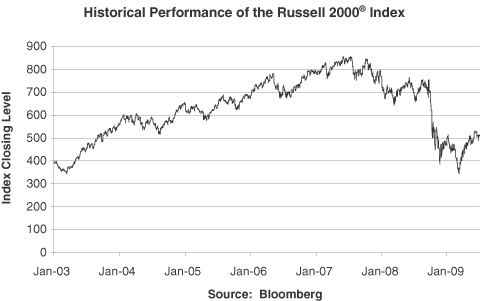

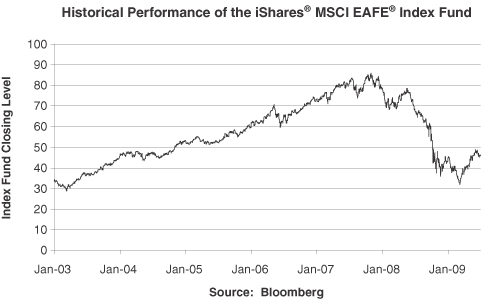

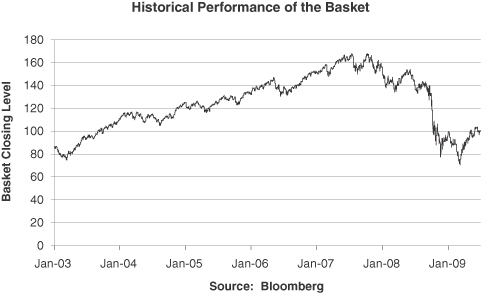

Historical Information

The following graphs show the historical performance of each of the Basket Components from January 1, 2003 through June 30, 2009. The closing level of the S&P 500® Index on June 30, 2009 was 919.32. The closing level of the S&P MidCap 400® Index on June 30, 2009 was 578.14. The closing level of the Russell 2000® Index on June 30, 2009 was 508.28. The closing level of the iShares® MSCI EAFE® Index Fund on June 30, 2009 was 45.81. The fifth graph shows the retrospective performance of the Basket, calculated by setting the level of the basket on June 30, 2009 equal to 100.

We obtained the various Basket Component closing levels below from Bloomberg, and we have not participated in the preparation of, or verified, such information.The historical levels of each Basket Component should not be taken as an indication of future performance, and no assurance can be given as to the Ending Basket Level of the Basket or Basket Return. We cannot give you assurance that the performance of the Basket will result in the return of your initial investment in excess of the Buffer Amount.

TS-11

TS-12

TS-13

Supplemental Underwriting Information

Deutsche Bank Securities Inc. (“DBSI”) and Deutsche Bank Trust Company Americas, acting as agents for Deutsche Bank AG, will not receive a commission in connection with the sale of the securities. DBSI may pay referral fees to other broker-dealers of up to 0.50% or $5.00 per $1,000 Face Amount. DBSI may pay custodial fees to other broker-dealers of up to 0.25% or $2.50 per $1,000 Face Amount. Deutsche Bank AG will reimburse DBSI for such fees. See “Underwriting” in the accompanying product supplement.

Settlement

We expect to deliver the securities against payment for the securities on the Settlement Date indicated above, which may be a date that is greater than three business days following the Trade Date. Under Rule 15c6-1 of the Securities Exchange Act of 1934, as amended, trades in the secondary market generally are required to settle in three business days, unless the parties to a trade expressly agree otherwise. Accordingly, purchasers who wish to transact in securities more than three business days prior to the original issue date will be required to specify alternative settlement arrangements to prevent a failed settlement if the securities are to be issued more than three business days after the Trade Date.

TS-14