ISSUER FREE WRITING PROSPECTUS NO. 764BF Filed Pursuant to Rule 433 Registration Statement No. 333-162195 Dated November 6, 2009 Yield Optimization Notes with Contingent Protection Enhanced Income Strategies for Equity Investors |  |

Deutsche Bank AG

$ Securities linked to the common stock of Bank of America Corporation due on or about November 18, 2011

$ Securities linked to the American Depositary Shares of Rio Tinto plc due on or about November 18, 2011

Investment Description

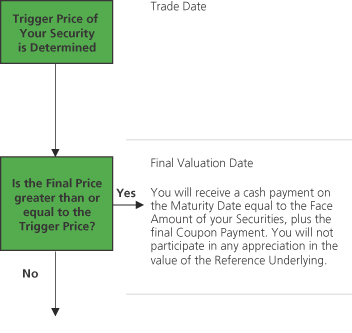

Yield Optimization Notes with Contingent Protection (the “Securities”) are senior unsecured obligations of Deutsche Bank AG, London Branch (the “Issuer”) with returns linked to the performance of the stock or American depositary shares of a specific company described herein (the “Reference Underlying”). The Securities pay a monthly coupon (specified below) and provide either a return of your initial investment or shares of the Reference Underlying at maturity. The coupon is designed to compensate you for the risk that you may receive a share of the Reference Underlying at maturity for each Security you hold, the value of which, on the Final Valuation Date, will be worth less than your initial investment. At maturity you will receive 100% of your initial investment if the Final Price of the Reference Underlying is greater than or equal to the Trigger Price. If the Final Price of the Reference Underlying is less than the Trigger Price, at maturity you will receive for each Security one share of the Reference Underlying (subject to adjustments in the case of certain events described in the accompanying product supplement). Each Security will have a face amount (the “Face Amount”) equal to the Closing Price of one share of the Reference Underlying on the Trade Date. Deutsche Bank AG will make monthly coupon payments (the “Coupon Payments”) during the term of the Securities regardless of the performance of the Reference Underlying.Investing in the Securities involves significant risks. You may lose some or all of your investment and will not participate in any appreciation in the value of the Reference Underlying from the Trade Date through the Final Valuation Date. The contingent protection feature applies only if you hold the Securities to maturity. Any payment on the Securities, including any contingent protection, is subject to the creditworthiness of the Issuer.

Features

| q | Income: Regardless of the performance of the Reference Underlying, Deutsche Bank AG will pay you coupons designed to compensate you for the possibility that you could lose some or all of your initial investment. |

| q | Tactical Investment Opportunity: If you believe the Reference Underlying will trend sideways over the term of the Securities — neither moving positively by more than the coupon paid on the Securities nor negatively by more than the amount of contingent protection — the Securities may provide improved performance compared to a direct investment in the Reference Underlying. |

| q | Contingent Protection Feature: If you hold the Securities to maturity and the Final Price of the Reference Underlying is equal to or greater than the Trigger Price on the Final Valuation Date, you will receive 100% of your initial investment at maturity, subject to the creditworthiness of Deutsche Bank AG. You will not participate in any appreciation in the value of the Reference Underlying. If you hold the Securities to maturity and the Final Price of the Reference Underlying is less than the Trigger Price on the Final Valuation Date, you will receive one share of the Reference Underlying for each Security you hold, which will likely be worth less than your initial investment and may have no value at all. |

Key Dates1

| Trade Date | November 13, 2009 | |

| Settlement Date | November 18, 2009 | |

| Final Valuation Date2 | November 14, 2011 | |

| Maturity Date3 | November 18, 2011 |

| 1 | The Securities are expected to price on or about November 13, 2009 and settle on or about November 18, 2009. In the event that we make any changes to the expected Trade Date and Settlement Date, the Final Valuation Date and Maturity Date will be changed to ensure that the stated term of the Securities remains the same. |

| 2 | Subject to postponement and as described under “Description of Securities—Adjustments to Valuation Dates and Payment Dates” in the accompanying product supplement. |

| 3 | In the event the Final Valuation Date is postponed due to a market disruption event, the Maturity Date will be the third business day after the Final Valuation Date as postponed. |

Security Offerings

We are offering two separate Yield Optimization Notes with Contingent Protection (each, a “Security”). Each Security is linked to the common stock of a different company, and each has a different Trigger Price. The coupon rate, the Initial Price and Trigger Price for each Security will be set on the Trade Date. The performance of each Security will not depend on the performance of any other Security.

| Reference Underlyings | Ticker | Relevant Exchange | Coupon Per Annum† | Initial Price of a Share of the | Trigger Price | CUSIP/ISIN | ||||||

| Bank of America Corporation | BAC | New York Stock Exchange | 10.00% to 12.00% per annum | 65% of the Initial Price | 25154N 70 4 / US25154N7049 | |||||||

| American depositary shares of Rio Tinto plc | RTP | New York Stock Exchange | 10.00% to 12.00% per annum | 75% of the Initial Price | 25154N 80 3 / US25154N8039 |

| † | The Coupon Per Annum will be set on the Trade Date. The Coupon will be paid monthly in arrears as described under “Coupon Payment Dates” below. |

| †† | The Initial Price of a Share of the Reference Underlying will be set on the Trade Date |

See “Additional Terms Specific to the Securities” in this free writing prospectus. The Securities will have the terms specified in product supplement BF dated September 29, 2009, the prospectus supplement dated September 29, 2009 relating to our Series A global notes of which these Securities are a part, the prospectus dated September 29, 2009 and this free writing prospectus. See “Key Risks” on page 6 of this free writing prospectus and “Risk Factors” beginning on page 7 in the accompanying product supplement.

Deutsche Bank AG has filed a registration statement (including a prospectus) with the Securities and Exchange Commission, or SEC, for the offering to which this free writing prospectus relates. Before you invest in the Securities offered hereby, you should read these documents and any other documents relating to this offering that Deutsche Bank AG has filed with the SEC for more complete information about Deutsche Bank AG and this offering. You may obtain these documents without cost by visiting EDGAR on the SEC website at www.sec.gov. Our Central Index Key, or CIK, on the SEC website is 0001159508. Alternatively, Deutsche Bank AG, any agent or any dealer participating in this offering will arrange to send you the prospectus, prospectus supplement, product supplement, underlying supplement and this free writing prospectus if you so request by calling toll-free 1-800-311-4409.

You may revoke your offer to purchase Securities at any time prior to the time at which we accept such offer by notifying the applicable agent. We reserve the right to change the terms of, or reject any offer to purchase, Securities prior to their issuance. We will notify you in the event of any changes to the terms of the Securities, and you will be asked to accept such changes in connection with your purchase of the Securities. You may also choose to reject such changes, in which case we may reject your offer to purchase Securities.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of Securities or passed upon the accuracy or the adequacy of this free writing prospectus, the underlying supplement the accompanying prospectus, the prospectus supplement and product supplement BF. Any representation to the contrary is a criminal offense. The Securities are not bank deposits and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other governmental agency.

| Price to Public | Discounts and Commissions | Proceeds to Us | ||||||||

Offering of Securities | Total | Per Security | Total | Per Security | Total | |||||

| Bank of America Corporation | $ | 100% | $ | 2.75% | $ | |||||

| American Depositary Shares of Rio Tinto plc | $ | 100% | $ | 2.75% | $ | |||||

Deutsche Bank Securities Inc. (“DBSI“) is our affiliate. For more information see “Supplemental Plan of Distribution (Conflicts of Interest)” on the last page of this free writing prospectus.

UBS Financial Services Inc. | Deutsche Bank Securities |

Additional Terms Specific to the Securities

You should read this free writing prospectus, together with the product supplement BF dated September 29, 2009, the prospectus supplement dated September 29, 2009 relating to our Series A global notes of which these Securities are a part and the prospectus dated September 29, 2009. You may access these documents on the SEC website atwww.sec.gov as follows (or if such address has changed, by reviewing our filings for the relevant date on the SEC website):

| ¨ | Product supplement BF dated September 29, 2009: |

http://www.sec.gov/Archives/edgar/data/1159508/000119312509204416/d424b21.pdf

| ¨ | Prospectus supplement dated September 29, 2009: |

http://www.sec.gov/Archives/edgar/data/1159508/000119312509200021/d424b31.pdf

| ¨ | Prospectus dated September 29, 2009: |

http://www.sec.gov/Archives/edgar/data/1159508/000095012309047023/f03158be424b2xpdfy.pdf

References to “Deutsche Bank AG,” “we,” “our” and “us” refer to Deutsche Bank AG, including, as the context requires, acting through one of its branches. In this free writing prospectus, “Securities” refers to the Yield Optimization Notes with Contingent Protection that are offered hereby, unless the context otherwise requires. This free writing prospectus, together with the documents listed above, contains the terms of the Securities and supersedes all other prior or contemporaneous oral statements as well as any other written materials including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set forth in “Key Risks” in this free writing prospectus and “Risk Factors” in the accompanying product supplement, as the Securities involve risks not associated with conventional debt securities. We urge you to consult your investment, legal, tax, accounting and other advisers before deciding to invest in the Securities.

Investor Suitability

The suitability considerations identified below are not exhaustive. Whether or not the Securities are a suitable investment for you will depend on your individual circumstances, and you should reach an investment decision only after you and your investment, legal, tax, accounting and other advisors have carefully considered the suitability of an investment in the Securities in light of your particular circumstances. You should also review “Key Risks” on page 6 of this free writing prospectus and “Risk Factors” on page 7 of the accompanying product supplement.

The Securities may be suitable for you if:

| ¨ | You are willing to receive shares of the Reference Underlying at maturity that may be worth less than the Face Amount or may have no value at all. |

| ¨ | You believe the price of the Reference Underlying is not likely to appreciate by more than the sum of the Coupon Payments made on the Securities. |

| ¨ | You believe the Final Price of the Reference Underlying is not likely to be less than the Trigger Price on the Final Valuation Date. |

| ¨ | You are willing to make an investment that will be exposed to the downside performance of the Reference Underlying in the event that the Final Price is less than the Trigger Price on the Final Valuation Date. |

| ¨ | You are willing to accept the risk of fluctuations in the market price of the Reference Underlying. |

| ¨ | You are willing to forgo the dividends paid on the Reference Underlying. |

| ¨ | You are willing to invest in the Securities based on the relevant anticipated coupon range (the actual coupon rate per annum will be determined on the Trade Date). |

| ¨ | You are willing to hold the Securities to maturity, a term of 24 months, and accept that there may be no secondary market for the Securities. |

| ¨ | You are comfortable with the creditworthiness of Deutsche Bank AG, as Issuer of the Securities. |

The Securities may not be suitable for you if:

| ¨ | You seek an investment that is 100% principal protected. |

| ¨ | You are not willing to receive shares of the Reference Underlying at maturity. |

| ¨ | You believe the market price of the Reference Underlying is likely to appreciate during the term of the Securities by more than the sum of the Coupon Payments made on the Securities. |

| ¨ | You believe the Final Price of the Reference Underlying will be less than the Trigger Price. |

| ¨ | You are not willing to accept the risks of owning equities in general and the Reference Underlying in particular. |

| ¨ | You prefer to receive the dividends paid on the Reference Underlying. |

| ¨ | You prefer lower risk and, therefore, accept the potentially lower returns of fixed income investments with comparable maturities and credit ratings that bear interest at a prevailing market rate. |

| ¨ | You are unable or unwilling to hold the Securities to maturity. |

| ¨ | You seek an investment for which there will be an active secondary market. |

| ¨ | You are not willing or are unable to assume the credit risk associated with Deutsche Bank AG, as Issuer of the Securities. |

2

Indicative Terms

| Issuer | Deutsche Bank AG, London Branch | |

| Issue Price | Equal to the Initial Price (as defined below) of the Reference Underlying | |

| Term | 24 months | |

| Reference Underlyings | Bank of America Corporation (Ticker: BAC) American depositary shares of Rio Tinto plc (Ticker: RTP) | |

| Coupon Payments | Coupons paid monthly in arrears on an unadjusted basis on the Coupon Payment Dates in twenty four equal installments based on the coupon rate per annum, regardless of the performance of the Reference Underlying. The coupon rate per annum is expected to be between 10.00% to 12.00% of the Face Amount of each Security, and will be determined on the Trade Date. | |

| Face Amount per Security | Equal to the Initial Price (as defined below) of the Reference Underlying | |

| Trade Date | November 13, 2009 | |

| Settlement Date | November 18, 2009 | |

| Final Valuation Date* | November 14, 2011 | |

| Maturity Date* | November 18, 2011 | |

| Coupon Payment Dates* | Coupons will be paid monthly in arrears in twenty-four equal installments on the coupon payment dates listed below: | |||

December 18, 2009 January 19, 2010 February 18, 2010 March 18, 2010 April 19, 2010 May 18, 2010 June 18, 2010 July 19, 2010 August 18, 2010 September 20, 2010 October 18, 2010 November 18, 2010 | December 20, 2010 January 18, 2011 February 18, 2011 March 18, 2011 April 18, 2011 May 18, 2011 June 20, 2011 July 18, 2011 August 18, 2011 September 19, 2011 October 18, 2011 November 18, 2011 | |||

| Installments | For each Security, 0.8333% to 1.00% of the Face Amount (to be determined on the Trade Date). | |

| Payment at Maturity (per Security) | If the Final Price of the Reference Underlying is greater than or equal to the Trigger Price, you will be entitled to a cash payment on the Maturity Date (in addition to any Coupon Payment) equal to the Face Amount.

If the Final Price is less than the Trigger Price, you will receive one share of the Reference Underlying per Security (subject to adjustments in the case of certain corporate events as described in the accompanying product supplement).

The Securities are not principal protected. The Reference Underlying you may receive at maturity could be worth less than your initial investment and may have no value at all. | |

| Initial Price | The Closing Price of one share of the relevant Reference Underlying on the Trade Date. | |

| Final Price | The Closing Price of one share of the relevant Reference Underlying on the Final Valuation Date | |

| Trigger Price | For the Security linked to the common stock of Bank of America Corporation, 65% of the relevant Initial Price. For the Security linked to the American depositary shares of Rio Tinto plc, 75% of the relevant Initial Price. | |

| Closing Price | On any scheduled trading day, the last reported sale price of the relevant Reference Underlying on the relevant exchange as determined by the calculation agent. | |

| Share Adjustment Factor | Initially 1.0 for each Reference Underlying, subject to adjustment for certain actions affecting each Underlying. See “Description of Securities – Anti-dilution Adjustments for Common Stock” in the accompanying product supplement. | |

| * | The Final Valuation Date, Maturity Date and Coupon Payment Dates above are subject to adjustments as described under “Adjustments to Valuation Dates and Payment Dates” in the accompanying product supplement. |

Determining Payment at Maturity Per Securities

You will receive one share of the Reference Underlying for each Security you own (subject to adjustments in the case of certain corporate events as described in the accompanying product supplement).

If the Closing Price of the Reference Underlying on the Maturity Date is less than the Initial Price, the shares you receive at maturity will be worth less than the Face Amount of your Securities.

Your Securities are not principal protected. If the Final Price is less than the Trigger Price, you will receive one share of the Reference Underlying for each Security you own. In that case, the shares you receive may be worth significantly less than your original investment amount and may have no value at all.

3

What are the Tax Consequences of an Investment in the Securities?

You should review carefully the section of the accompanying product supplement entitled “U.S. Federal Income Tax Consequences.” Although the tax consequences of an investment in the Securities are unclear, we believe that it is reasonable to treat a Security for U.S. federal income tax purposes as a put option (the “Put Option”), written by you to us with respect to the Reference Underlying, secured by a cash deposit equal to the issue price of the Security (the “Deposit”), which will bear an annual yield, based on our cost of borrowing, as shown below. Under this treatment, less than the full amount of each coupon payment will be attributable to the interest on the Deposit, and the excess of each coupon payment over the portion of the coupon payment attributable to the interest on the Deposit will represent a portion of the option premium attributable to your grant of the Put Option (the “Put Premium”) as shown below:

Reference Underlying | Coupon (to be determined on Trade Date) | Interest on Deposit per Annum | Put Premium per Annum | |||

Bank of America Corporation | 10.00% to 12.00% per annum | % | % | |||

American depositary shares of Rio Tinto PLC | 10.00% to 12.00% per annum | % | % |

Interest on the Deposit will be treated as ordinary interest income, while the Put Premium will not be taken into account prior to sale, exchange or maturity of the Securities.

Due to the absence of authorities that directly address instruments that are similar to the Securities, significant aspects of the U.S. federal income tax consequences of an investment in the Securities are uncertain. We do not plan to request a ruling from the Internal Revenue Service (the “IRS”), and the IRS or a court might not agree with the tax treatment described in this free writing prospectus and the accompanying product supplement. If the IRS were successful in asserting an alternative treatment for the Securities, the tax consequences of the ownership and disposition of the Securities could be affected materially and adversely.

In December 2007, Treasury and the IRS released a notice requesting comments on various issues regarding the U.S. federal income tax treatment of “prepaid forward contracts” and similar instruments. While it is not clear whether the Securities would be viewed as similar to the typical prepaid forward contract described in the notice, any Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the Securities, possibly with retroactive effect.

Neither we nor UBS Financial Services Inc. provides any advice on tax matters. Both U.S. and non-U.S. holders should consult their tax advisers regarding all aspects of the U.S. federal tax consequences of investing in the Securities (including possible alternative treatments and the issues presented by the December 2007 notice), as well as tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction.

Hypothetical Examples

The following table and hypothetical examples below illustrate the payment at maturity for a hypothetical range of performance for a stock price. The following examples and table are hypothetical and provided for illustrative purposes only. They do not purport to be representative of every possible scenario concerning increases or decreases in the price of the Reference Underlying relative to its Initial Price. We cannot predict the Final Price of the relevant Reference Underlying. You should not take these examples as an indication or assurance of the expected performance of the relevant Reference Underlying. You should consider carefully whether the Yield Optimization Notes are suitable to your investment goals. The numbers in the examples and table below have been rounded for ease of analysis.

The following examples and table illustrate the payment at maturity per security on a hypothetical offering of securities based on the following assumptions*:

Term: Hypothetical coupon per annum**: Hypothetical initial price of the Reference Underlying: Hypothetical Trigger Price: Face amount: Dividend yield on the Reference Underlying***: | 24 months 11.00% (or $0.92 per month) $100.00 per share $75.00 (75.00% of the Initial Price) $100.00 per security (set equal to the Initial Price) 2.00% |

| * | Actual coupon rate in respect of Coupon Payments, Initial Price, Trigger Price and Face Amount with respect to each Security to be set on the Trade Date. |

| ** | Coupon payments will be paid monthly in arrears during the term of the securities on an unadjusted basis. |

| *** | Assumed dividend yield received by holders of the Reference Underlying during the term of the Securities. Holders of the securities will not be entitled to any dividend payments made on the Reference Underlying. |

Scenario 1: The Final Price of the Reference Underlying is equal to or greater than the hypothetical Trigger Price of $75.00.

Since the Final Price of the Reference Underlying is not less than the hypothetical Trigger Price of $75.00, your initial investment is protected and you will receive at maturity a cash payment equal to the face amount of the securities. This investment would outperform an investment in the Reference Underlying if the price appreciation of the Reference Underlying (plus dividends, if any) is less than 11.00%.

If the Closing Price of the Reference Underlying on the Final Valuation Date is $100.00 (no change in the price of the Reference Underlying):

Payment at maturity: Coupons: Total: Total return on the securities: | $100.00 $ 22.00 $122.00 22.00% | ($0.92 × 24 = $22) |

In this example, the total return on the securities is 22.00% while the total return on the Reference Underlying would be 2% if you invested in the Reference Underlying directly (including dividends).

4

If the Closing Price of the Reference Underlying on the Final Valuation Date is $130.00 (an increase of 30%):

Payment at maturity: Coupons: Total: Total return on the securities: | $100.00 $ 22.00 $122.00 22.00% | ($0.92 × 24 = $22) |

In this example, the total return on the securities is 22.00% while the total return on the Reference Underlying would be 32% if you invested in the Reference Underlying directly (including dividends).

If the Closing Price of the Reference Underlying on the Final Valuation Date is $85.00 (a decline of 15%):

Payment at maturity: Coupons: Total: Total return on the securities: | $100.00 $ 22.00 $122.00 22.00% | ($0.92 × 24 = $22) |

In this example, the total return on the securities is 22.00% while the total return on the stock would be a loss of 13% if you invested in the Reference Underlying directly (including dividends).

Scenario 2: The Final Price of the Reference Underlying is less than the hypothetical Trigger Price of $75.00.

Since the Final Price of the Reference Underlying is less than the hypothetical Trigger Price of $75.00, you will receive at maturity one share of the Reference Underlying for each security you hold. The value received at maturity and the total return on the securities at that time depends on the Closing Price of the Reference Underlying on the Maturity Date.

If the Closing Price of the Reference Underlying on the Maturity Date is $50.00 (a decline of 50%):

Value on the Maturity Date of share received: Coupons: Total: Total return on the securities: | $50.00 $22.00 $72.00 -28.00% | ($0.92 × 24 = $22) |

In this example, the total return on the securities is a loss of 28.00% while the total return on the Reference Underlying would be a loss of 48% if you invest in the Reference Underlying directly (including dividends). In this example, you will receive one share of the Reference Underlying per Security at maturity.

5

| Reference Underlying | The Hypothetical Final Price is Greater Than or Equal to the Hypothetical Trigger Price | The Hypothetical Final Price is Less Than the Hypothetical Trigger Price | ||||||||

Hypothetical Price(1) | Stock Price Return | Total Maturity + Payments(2) | Total Return on the at Maturity(3) | Total at Maturity + Coupon Payments(4) | Total Return on the Securities Maturity(5) | |||||

$150.00 | 50.00% | $122.00 | 22.00% | N/A | N/A | |||||

$145.00 | 45.00% | $122.00 | 22.00% | N/A | N/A | |||||

$140.00 | 40.00% | $122.00 | 22.00% | N/A | N/A | |||||

$135.00 | 35.00% | $122.00 | 22.00% | N/A | N/A | |||||

$130.00 | 30.00% | $122.00 | 22.00% | N/A | N/A | |||||

$125.00 | 25.00% | $122.00 | 22.00% | N/A | N/A | |||||

$120.00 | 20.00% | $122.00 | 22.00% | N/A | N/A | |||||

$115.00 | 15.00% | $122.00 | 22.00% | N/A | N/A | |||||

$110.00 | 10.00% | $122.00 | 22.00% | N/A | N/A | |||||

$105.00 | 5.00% | $122.00 | 22.00% | N/A | N/A | |||||

$100.00 | 0.00% | $122.00 | 22.00% | N/A | N/A | |||||

$95.00 | -5.00% | $122.00 | 22.00% | N/A | N/A | |||||

$90.00 | -10.00% | $122.00 | 22.00% | N/A | N/A | |||||

$85.00 | -15.00% | $122.00 | 22.00% | N/A | N/A | |||||

$80.00 | -20.00% | $122.00 | 22.00% | N/A | N/A | |||||

$75.00 | -25.00% | $122.00 | 22.00% | N/A | N/A | |||||

$70.00 | -30.00% | $122.00 | 22.00% | N/A | N/A | |||||

$65.00 | -35.00% | N/A | N/A | $87.00 | -13.00% | |||||

$60.00 | -40.00% | N/A | N/A | $82.00 | -18.00% | |||||

$55.00 | -45.00% | N/A | N/A | $77.00 | -23.00% | |||||

$50.00 | -50.00% | N/A | N/A | $72.00 | -28.00% | |||||

| (1) | If the hypothetical Final Price of the Reference Underlying is not less than the hypothetical Trigger Price, the hypothetical Final Price is as of the Final Valuation Date. If the hypothetical Final Price of the Reference Underlying is less than the hypothetical Trigger Price, the hypothetical Final Price is as of the Maturity Date. |

| (2) | Payment consists of the face amount plus coupon payments of 11.00% per annum. |

| (3) | The total return on the securities at maturity includes coupon payments of 11.00% per annum. |

| (4) | Payment consists of the cash equivalent of one share of the Reference Underlying plus coupon payments of 11.00% per annum. |

| (5) | If the hypothetical Final Price is less than the hypothetical Trigger Price, the total return at maturity will only be positive in the event that the market price of the Reference Underlying on the Maturity Date is substantially greater than the hypothetical Final Price of such Reference Underlying on the Final Valuation Date. Such an increase in price is not likely to occur. |

An investment in the Securities involves significant risks. Some of the risks that apply to an investment in each Security offered hereby are summarized below, and we urge you to read the more detailed explanation of risks relating to the Securities generally in the “Risk Factors” section of the accompanying product supplement. We also urge you to consult your investment, legal, tax, accounting and other advisers before you invest in the Securities offered hereby.

| ¨ | YOUR INVESTMENT IN THE SECURITIES MAY RESULT IN A LOSS OF YOUR INITIAL INVESTMENT — The Securities do not guarantee any return of your initial investment. The return on the Securities at maturity is linked to the performance of the Reference Underlying and will depend on whether, and to the extent which, the Final Price is less than the Trigger Level on the Final Valuation Date. Your initial investment is protected so long as the Final Price is equal to or greater than the Trigger Price on the Final Valuation Date. If the Final Price is less than the Trigger Price on the Final Valuation Date, you will be fully exposed to any decline in the price of the Reference Underlying and you will receive one share of the Reference Underlying per Security at maturity. The Reference Underlying’s volatility can change significantly over the term of the Securities and the price of the Reference Underlying could fall sharply, which could result in a significant loss of your investment.Accordingly, if the Final Price of the Reference Underlying stock is less than the Trigger Price, the shares you receive may be worth significantly less than your original investment amount and may have no value at all. |

6

| ¨ | YOU SHOULD NOT EXPECT TO PARTICIPATE IN ANY APPRECIATION IN THE PRICE OF THE REFERENCE UNDERLYING— You will not participate in any appreciation in the price of the Reference Underlying and you will only receive the Face Amount per Security (excluding any Coupon Payment) if the Final Price is equal to or greater than the Initial Price. Your return on the Securities (excluding any Coupon Payment) at maturity will only exceed the Face Amount of the Securities in the unlikely event in which (1) the Final Price of the Reference Underlying is less than the Trigger Price on the Final Valuation Date (and, therefore, you receive a share of the Reference Underlying instead of a cash payment of the Face Amount at maturity) and (2) the market price of a share of the Reference Underlying at maturity is greater than the Initial Price. At a minimum, this circumstance would require the value of a share of an Reference Underlying to appreciate by at least 53.85% in the case of the Security linked to the common stock of Bank of America Corporation and at least 33.33% in the case of the Security linked to the American depositary shares of Rio Tinto plc, in each case from the Final Valuation Date to the Maturity Date (a period of approximately four trading days). |

| ¨ | CREDIT OF THE ISSUER — The Securities are senior unsecured obligations of the Issuer, Deutsche Bank AG, and are not, either directly or indirectly, an obligation of any third party. Any payment to be made on the Securities, including coupon payments and any contingent protection provided at maturity, depends on the ability of Deutsche Bank AG to satisfy its obligations as they come due. As a result, the actual and perceived creditworthiness of Deutsche Bank AG will affect the market value of the Securities and in the event Deutsche Bank AG were to default on its obligations you may not receive the contingent protection or any other amount owed to you under the terms of the Securities. |

| ¨ | CONTINGENT PROTECTION OF YOUR INITIAL INVESTMENT APPLIES ONLY IF YOU HOLD THE SECURITIES TO MATURITY — You should be willing to hold your Securities to maturity. If you sell your Securities prior to maturity in the secondary market, you may have to sell them at a discount and your initial investment will not be protected. |

| ¨ | INVESTING IN THE SECURITIES IS NOT THE SAME AS INVESTING IN THE REFERENCE UNDERLYING — The return on your Securities may not reflect the return you would realize if you directly invested in the Reference Underlying. For instance, you will not receive or be entitled to receive any dividend payments or other distributions or other rights that holders of the Reference Underlying would have. |

| ¨ | SINGLE STOCK RISK — The price of the Reference Underlying can rise or fall sharply due to factors specific to that Reference Underlying and its issuer, such as stock price volatility, earnings, financial conditions, corporate, industry and regulatory developments, management changes and decisions and other events, as well as general market factors, such as general stock market volatility and levels, interest rates and economic and political conditions. |

| ¨ | IF THE CLOSING PRICE OF THE REFERENCE UNDERLYING CHANGES, THE MARKET VALUE OF YOUR SECURITIES MAY NOT CHANGE IN THE SAME MANNER — Your Securities may trade quite differently from the Reference Underlying. Changes in the market price of the Reference Underlying may not result in a comparable change in the value of your Securities. |

| ¨ | THERE MAY BE LITTLE OR NO SECONDARY MARKET FOR THE SECURITIES— The Securities will not be listed on any securities exchange. Deutsche Bank AG or its affiliates intends to offer to purchase the Securities in the secondary market but is not required to do so and may cease such market making activities at any time. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell your Securities easily. Because other dealers are not likely to make a secondary market for the Securities, the price at which you may be able to trade your Securities is likely to depend on the price, if any, at which Deutsche Bank AG or its affiliates is willing to buy the Securities. |

| ¨ | MANY ECONOMIC AND MARKET FACTORS WILL IMPACT THE VALUE OF THE SECURITIES — We expect that, generally, the stock price of the Reference Underlying, volatility of the Reference Underlying, factors specific to the issuer of the Reference Underlying, such as earnings, financial conditions, corporate, industry and regulatory developments, management changes and decisions and other events, will affect the value of the Securities more than any other single factor. The value of the Securities will be affected by a number of other factors that may either offset or magnify each other, including: |

| • | the time remaining to maturity of the Securities; |

| • | the market price and dividend rates of the Reference Underlying and the stock market generally; |

| • | interest and yield rates in the market generally and in the markets of the Reference Underlying; |

| • | a variety of economic, financial, political, regulatory or judicial events; |

| • | the exchange rates and the volatility of the exchange rates between the U.S. dollar and the currencies in which the Reference Underlying is based; |

| • | supply and demand for the Securities; and |

| • | our creditworthiness, including actual or anticipated downgrades in our credit ratings. |

| ¨ | THE SECURITIES HAVE CERTAIN BUILT-IN COSTS — While the payment at maturity described in this free writing prospectus is based on your entire initial investment, the original issue price of the Securities includes the agents’ commission and the estimated cost of hedging our obligations under the Securities through one or more of our affiliates. As a result, the price, if any, at which Deutsche Bank AG or its affiliates would be willing to purchase Securities from you prior to maturity in secondary market transactions, if at all, will likely be lower than the original issue price, and any sale prior to the maturity date could result in a substantial loss to you. The Securities are not designed to be short-term trading instruments. Accordingly, you should be able and willing to hold your Securities to maturity. |

| ¨ | POTENTIAL DEUTSCHE BANK AG IMPACT ON PRICE— Trading or transactions by Deutsche Bank AG or its affiliates in the Reference Underlying and/or over the counter options, futures or other instruments with returns linked to the performance of the Reference Underlying, may adversely affect the market price of the Reference Underlying and therefore, the market value of the Securities. |

| ¨ | POTENTIAL CONFLICT OF INTEREST — Deutsche Bank AG and its affiliates may engage in business with the issuer of the Reference Underlying, which may present a conflict between the obligations of Deutsche Bank AG and you, as a holder of the Securities. The calculation agent, an affiliate of Deutsche Bank AG, will determine the Final Price of the Reference Underlying and payment at maturity based on Closing Price of the Reference Underlying in the market. The calculation agent can postpone the determination of the Final Price of the Reference Underlying or the Maturity Date if a market disruption event occurs on the Final Valuation Date. |

7

| ¨ | WE AND OUR AFFILIATES OR UBS AG AND ITS AFFILIATES, MAY PUBLISH RESEARCH, EXPRESS OPINIONS OR PROVIDE RECOMMENDATIONS THAT ARE INCONSISTENT WITH INVESTING IN OR HOLDING THE SECURITIES. ANY SUCH RESEARCH, OPINIONS OR RECOMMENDATIONS COULD AFFECT THE FINAL PRICE OF THE REFERENCE UNDERLYING AND THE VALUE OF SECURITIES — We, our affiliates and agents, and UBS AG and its affiliates, publish research from time to time on financial markets and other matters that may influence the value of the Securities, or express opinions or provide recommendations that may be inconsistent with purchasing or holding the Securities. Any research, opinions or recommendations expressed by us, our affiliates or agents, or UBS AG or its affiliates, may not be consistent with each other and may be modified from time to time without notice. Investors should make their own independent investigation of the merits of investing in the Securities and the Reference Underlying to which the Securities are linked. |

| ¨ | THE ANTI-DILUTION PROTECTION IS LIMITED — The calculation agent will make adjustments to the Share Adjustment Factors, which will initially be set at 1.0, for certain events affecting the Reference Underlying. See “Description of Securities — Anti-Dilution Adjustments for Common Stock” in the accompanying product supplement. The calculation agent is not required, however, to make such adjustments in response to all events that could affect the Reference Underlying. If an event occurs that does not require the calculation agent to make an adjustment, the value of the Securities may be materially and adversely affected. |

| ¨ | IN SOME CIRCUMSTANCES, YOU MAY RECEIVE THE COMMON STOCK OF ANOTHER COMPANY AND NOT THE REFERENCE UNDERLYING AT MATURITY — Following certain corporate events relating to the respective issuer of the Reference Underlying where such issuer is not the surviving entity, you may receive the common stock of a successor to the respective Reference Underlying Issuer or any cash or any other assets distributed to holders of the Reference Underlying in such corporate event. The occurrence of these corporate events and the consequent adjustments may materially and adversely affect the value of the Securities. For more information, see the section “Description of Securities — Anti-Dilution Adjustments for Common Stock” in the accompanying product supplement. Regardless of the occurrence of one or more dilution or reorganization events, you should note that at maturity you will receive an amount in cash equal to the Face Amount per Security unless the Final Price of the Reference Underlying is less than the Trigger Price (as such Trigger Price may be adjusted by the Calculation Agent upon occurrence of one or more such events). |

| ¨ | THERE IS NO AFFILIATION BETWEEN THE ISSUERS OF THE REFERENCE UNDERLYING AND US, AND WE ARE NOT RESPONSIBLE FOR ANY DISCLOSURE BY SUCH ISSUER — We are not affiliated with the issuers of the Reference Underlying (the “Reference Underlying Issuer”). However, we and our affiliates may currently or from time to time in the future engage in business with the Reference Underlying Issuers. Nevertheless, neither we nor our affiliates assume any responsibility for the accuracy or the completeness of any information about the Reference Underlying and the Reference Underlying Issuers. You, as an investor in the Securities, should make your own investigation into the Reference Underlying and its Issuer. Neither Reference Underlying Issuer is involved in the Securities offered hereby in any way and neither has any obligation of any sort with respect to your Securities. Neither Reference Underlying Issuer has any obligation to take your interests into consideration for any reason, including when taking any corporate actions that might affect the value of your Securities. |

| ¨ | FLUCTUATIONS IN EXCHANGE RATES MAY AFFECT YOUR INVESTMENT — There are significant risks related to an investment in a Security that is linked to an American depositary share (as evidenced by American depositary receipts) (an “ADS”), which is quoted and traded in U.S. dollars, representing shares quoted and traded in a foreign currency (the “Reference Stock”). An ADS, which is quoted and traded in U.S. dollars, may trade differently from its Reference Stock. In recent years, the rates of exchange between the U.S. dollar and some other currencies have been highly volatile, and this volatility may continue in the future. These risks generally depend on economic and political events over which we have no control. Fluctuations in any particular exchange rate that have occurred in the past are not necessarily indicative, however, of fluctuations that may occur during the term of the Securities. Changes in the exchange rate between the U.S. dollar and a foreign currency may affect the U.S. dollar equivalent of the price of the Reference Stocks on non-U.S. securities markets and, as a result, may affect the market price of the ADSs to which the Securities are linked, which may consequently affect the value of the Securities. |

| ¨ | NON-U.S. SECURITIES MARKETS RISKS — An investment in the Securities linked to the value of the ADSs of Rio Tinto plc involves risks associated with the securities markets in those countries where the shares of Rio Tinto plc are traded, including risks of markets volatility, governmental intervention in those markets and cross shareholdings in companies in certain countries. Also, non-U.S. companies are generally subject to accounting, auditing and financial reporting standards and requirements, and securities trading rules different from those applicable to U.S. reporting companies. The prices of securities in non-U.S. markets may be affected by political, economic, financial and social factors in such markets, including changes in a country’s government, economic and fiscal policies, currency exchange laws or other laws or restrictions. Moreover, the economies of such countries may differ favorably or unfavorably from the economy of the United States in such respects as growth of gross national product, rate of inflation, capital reinvestment, resources and self sufficiency. Such countries may be subjected to different and, in some cases, more adverse economic environments. |

| ¨ | THERE ARE IMPORTANT DIFFERENCES BETWEEN THE RIGHTS OF HOLDERS OF ADSs AND THE RIGHTS OF HOLDERS OF THE COMMON STOCK OF A FOREIGN COMPANY — You should be aware that the Security linked to the ADS of Rio Tinto plc is linked to an ADS and not the Reference Stock represented by such ADS, and there exist important differences between the rights of holders of ADSs and the rights of holders of the corresponding Reference Stock. Each ADS is a security evidenced by American depositary receipts that represents four ordinary shares of Rio Tinto plc, par value of 10 pence. Generally, ADSs are issued under a deposit agreement which sets forth the rights and responsibilities of the depositary, the foreign issuer and holders of the ADSs, which may be different from the rights of holders of ordinary shares of the foreign issuer. For example, the foreign issuer may make distributions in respect of its ordinary shares that are not passed on to the holders of its ADSs. Any such differences between the rights of holders of ADSs and holders of the corresponding Reference Stocks may be significant and may materially and adversely affect the value of the Securities linked to such ADSs. |

| ¨ | PAST PERFORMANCE OF THE REFERENCE UNDERLYING IS NO GUIDE TO FUTURE PERFORMANCE — The actual performance of the Reference Underlying may bear little relation to the historical prices of the relevant Reference Underlying, and may bear little relation to the hypothetical return examples set forth elsewhere in this free writing prospectus. We cannot predict the future performance of the Reference Underlying. |

8

| ¨ | THE U.S. TAX CONSEQUENCES OF AN INVESTMENT IN THE SECURITIES ARE UNCLEAR– There is no authority regarding the proper U.S. federal income tax treatment of the Securities, and we do not plan to request a ruling from the IRS. Consequently, significant aspects of the tax treatment of the Securities are uncertain, and the IRS or a court might not agree with the treatment of the Securities described herein. If the IRS were successful in asserting an alternative treatment for the Securities, the tax consequences of the ownership and disposition of the Securities could be affected materially and adversely. In addition, as described above under “What are the Tax Consequences of an Investment in the Securities?”, in December 2007 Treasury and the IRS released a notice requesting comments on various issues regarding the U.S. federal income tax treatment of “prepaid forward contracts” and similar instruments. While it is not clear whether the Securities would be viewed as similar to the typical prepaid forward contract described in the notice, any Treasury regulations or other guidance promulgated after consideration of these issues could materially and adversely affect the tax consequences of an investment in the Securities, possibly with retroactive effect. Both U.S. and non-U.S. holders should review carefully the section of the accompanying product supplement entitled “U.S. Federal Income Tax Consequences,” and consult their tax advisers regarding the U.S. federal tax consequences of an investment in the Securities (including possible alternative treatments and the issues presented by this notice), as well as tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction. |

Information about the Reference Underlyings

All disclosures contained in this free writing prospectus regarding each Reference Underlying are derived from publicly available information. Neither Deutsche Bank AG nor any of its affiliates assumes any responsibilities for the adequacy or accuracy of information about any Reference Underlying contained in this free writing prospectus. You should make your own investigation into each Reference Underlying.

Included on the following pages is a brief description of the Reference Underlying Issuer of each of the respective underlying stocks. We obtained the closing price information set forth below from Bloomberg without independent verification. You should not take the historical prices of the Reference Underlyings as an indication of future performance. Each of the Reference Underlyings is registered under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Companies with securities registered under the Exchange Act are required to file financial and other information specified by the SEC periodically. Information filed by the respective issuers of the Reference Underlyings with the SEC can be reviewed electronically through a web site maintained by the SEC. The address of the SEC’s web site is http://www.sec.gov. Information filed with the SEC by the respective issuers of the Reference Underlyings under the Exchange Act can be located by reference to its SEC file number provided below.

In addition, information filed with the SEC can be inspected and copied at the Public Reference Section of the SEC, 100 F Street, N.E., Room 1580, Washington, D.C. 20549. Copies of this material can also be obtained from the Public Reference Section, at prescribed rates.

Bank of America Corporation

According to publicly available information, Bank of America Corporation (“Bank of America”) is a financial holding company that provides a diversified range of banking and nonbanking financial services and products through its banks and various nonbanking subsidiaries throughout the United States. Information filed by Bank of America with the SEC under the Exchange Act can be located by reference to its SEC file number: 1-6523, or its CIK Code: 0000070858. Bank of America’s common stock is listed on the New York Stock Exchange under the ticker symbol “BAC”.

Historical Information

The following table sets forth the quarterly high and low closing prices for common stock of Bank of America, based on daily closing prices on the primary exchange for Bank of America, as reported by Bloomberg. Bank of America’s closing price on November 4, 2009 was $14.70. The actual Initial Price will be the closing price of Bank of America’s common stock on the Trade Date.

Quarter Begin | Quarter End | Quarterly High | Quarterly Low | Quarterly Close | ||||

| 1/2/2004 | 3/31/2004 | 41.38 | 39.15 | 40.49 | ||||

| 4/1/2004 | 6/30/2004 | 42.72 | 38.96 | 42.31 | ||||

| 7/1/2004 | 9/30/2004 | 44.98 | 41.81 | 43.33 | ||||

| 10/1/2004 | 12/31/2004 | 47.44 | 43.62 | 46.99 | ||||

| 1/3/2005 | 3/31/2005 | 47.08 | 43.66 | 44.10 | ||||

| 4/1/2005 | 6/30/2005 | 47.08 | 44.01 | 45.61 | ||||

| 7/1/2005 | 9/30/2005 | 45.98 | 41.60 | 42.10 | ||||

| 10/3/2005 | 12/30/2005 | 46.99 | 41.57 | 46.15 | ||||

| 1/3/2006 | 3/31/2006 | 47.08 | 43.09 | 45.54 | ||||

| 4/3/2006 | 6/30/2006 | 50.47 | 45.48 | 48.10 | ||||

| 7/3/2006 | 9/29/2006 | 53.62 | 47.98 | 53.57 | ||||

| 10/2/2006 | 12/29/2006 | 54.90 | 51.66 | 53.39 | ||||

| 1/3/2007 | 3/30/2007 | 54.05 | 49.46 | 51.02 | ||||

| 4/2/2007 | 6/29/2007 | 51.82 | 48.80 | 48.89 | ||||

| 7/2/2007 | 9/28/2007 | 51.87 | 47.00 | 50.27 | ||||

| 10/1/2007 | 12/31/2007 | 52.71 | 40.56 | 41.26 | ||||

| 1/2/2008 | 3/31/2008 | 45.03 | 35.31 | 37.91 | ||||

| 4/1/2008 | 6/30/2008 | 40.37 | 22.54 | 23.87 | ||||

| 7/1/2008 | 9/30/2008 | 38.13 | 18.52 | 35.00 | ||||

| 10/1/2008 | 12/31/2008 | 34.48 | 11.25 | 14.08 | ||||

| 1/2/2009 | 3/31/2009 | 14.33 | 3.14 | 6.82 | ||||

| 4/1/2009 | 6/30/2009 | 14.17 | 7.06 | 13.20 | ||||

| 7/1/2009 | 9/30/2009 | 17.98 | 11.84 | 16.92 | ||||

| 10/1/2009* | 11/4/2009* | 18.59 | 14.58 | 14.70 |

| * | As of the date of this free writing prospectus available information for the fourth calendar quarter of 2009 includes data for the period through November 4, 2009. Accordingly, the “Quarterly High,” “Quarterly Low” and “Quarterly Close” data indicated are for this shortened period only and do not reflect complete data for the fourth calendar quarter of 2009. |

9

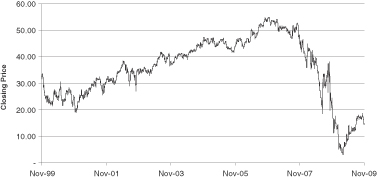

The graph below illustrates the performance of Bank of America Corporation’s common stock from November 3, 1999 through November 3, 2009, based on information from Bloomberg. Past performance of the Reference Underlying is not indicative of the future performance of the Reference Underlying.

Historical Performance of the Common Stock of

Bank of America Corporation

Source: Bloomberg

Rio Tinto plc

According to publicly available information, Rio Tinto plc and Rio Tinto Limited operate as one business organization (the “Company”) even though both continue to be separate legal entities with separate share listings. The Company is a mining and exploration company. The Company’s business is finding, mining and processing mineral resources. Its major products include aluminum, copper, diamonds, energy products, gold, industrial minerals (borates, titanium dioxide, salt and talc), and iron ore. The Company’s activities are represented in Australia and North America. There are also businesses in South America, Asia, Europe and southern Africa. Information filed by Rio Tinto plc with the SEC under the Exchange Act can be located by reference to its SEC file number: 1–10533, or its CIK Code: 0000863064. Rio Tinto plc’s American depositary shares are listed on the New York Stock Exchange under the ticker symbol “RTP”. Each ADS represents four Rio Tinto plc ordinary shares, par value of 10 pence. The principal market for Rio Tinto plc shares is the London Stock Exchange. In addition to its principal listing, the American depositary shares of Rio Tinto plc ordinary shares are trade on the New York Stock Exchange.

Historical Information

The following table sets forth the quarterly high and low closing prices for Rio Tinto plc’s American depositary shares, based on daily closing prices on the primary exchange for the ADSs, as reported by Bloomberg. Rio Tinto plc’s ADS closing price on November 4, 2009 was $187.22. The Initial Price will be the closing price of Rio Tinto’s American depositary shares on the Trade Date.

Quarter Begin | Quarter End | Quarterly High | Quarterly Low | Quarterly Close | ||||

| 1/2/2004 | 3/31/2004 | 95.51 | 79.34 | 83.17 | ||||

| 4/1/2004 | 6/30/2004 | 87.07 | 71.46 | 81.08 | ||||

| 7/1/2004 | 9/30/2004 | 91.11 | 80.47 | 89.84 | ||||

| 10/1/2004 | 12/31/2004 | 98.72 | 85.57 | 98.57 | ||||

| 1/3/2005 | 3/31/2005 | 118.08 | 92.26 | 107.29 | ||||

| 4/1/2005 | 6/30/2005 | 108.12 | 95.76 | 100.82 | ||||

| 7/1/2005 | 9/30/2005 | 138.01 | 101.69 | 135.86 | ||||

| 10/3/2005 | 12/30/2005 | 151.56 | 123.05 | 151.15 | ||||

| 1/3/2006 | 3/31/2006 | 176.20 | 152.14 | 174.95 | ||||

| 4/3/2006 | 6/30/2006 | 208.57 | 156.57 | 177.24 | ||||

| 7/3/2006 | 9/29/2006 | 181.31 | 151.34 | 160.27 | ||||

| 10/2/2006 | 12/29/2006 | 194.27 | 154.17 | 179.59 | ||||

| 1/3/2007 | 3/30/2007 | 194.89 | 163.62 | 192.54 | ||||

| 4/2/2007 | 6/29/2007 | 271.70 | 201.43 | 258.72 | ||||

| 7/2/2007 | 9/28/2007 | 302.57 | 198.32 | 290.23 | ||||

| 10/1/2007 | 12/31/2007 | 404.28 | 282.54 | 354.88 | ||||

| 1/2/2008 | 3/31/2008 | 392.16 | 280.01 | 348.07 | ||||

| 4/1/2008 | 6/30/2008 | 469.01 | 363.42 | 418.36 | ||||

| 7/1/2008 | 9/30/2008 | 366.20 | 184.88 | 210.87 | ||||

| 10/1/2008 | 12/31/2008 | 190.16 | 51.32 | 75.14 | ||||

| 1/2/2009 | 3/31/2009 | 124.12 | 66.91 | 113.30 | ||||

| 4/1/2009 | 6/30/2009 | 179.60 | 107.06 | 138.50 | ||||

| 7/1/2009 | 9/16/2009 | 182.63 | 124.48 | 170.29 | ||||

| 10/1/2009* | 11/4/2009* | 198.26 | 160.88 | 187.22 |

| * | As of the date of this free writing prospectus available information for the fourth calendar quarter of 2009 includes data for the period through November 4, 2009. Accordingly, the “Quarterly High,” “Quarterly Low” and “Quarterly Close” data indicated are for this shortened period only and do not reflect complete data for the fourth calendar quarter of 2009. |

10

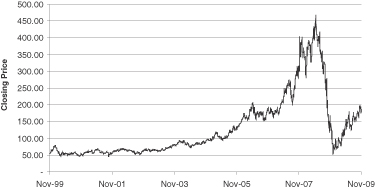

The graph below illustrates the performance of Rio Tinto’s common stock through November 3, 2009, based on information from Bloomberg. Past performance of the Reference Underlying is not indicative of the future performance of the Reference Underlying.

Historical Performance of the Common Stock of

Rio Tinto PLC

Source: Bloomberg

Supplemental Plan of Distribution (Conflicts of Interest)

UBS Financial Services Inc. and its affiliates, and Deutsche Bank Securities Inc., acting as agents for Deutsche Bank AG, will receive or allow as a concession or reallowance to other dealers discounts and commissions of 2.75% of the face amount of each Security. We have agreed that UBS Financial Services Inc. may sell all or part of the Securities that it purchases from us to its affiliates at the price to the public indicated on the cover of this free writing prospectus minus a concession not to exceed the discounts and commissions indicated on the cover. DBSI, one of the agents for this offering, is our affiliate. In accordance with NASD Rule 2720, DBSI may not make sales in this offering to any discretionary account without the prior written approval of the customer. See “Underwriting (Conflicts of Interest)” in the accompanying product supplement.

11