FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Private Issuer

Dated May 6, 2003

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the month of May 6, 2003

Commission File Number 001-15244

CREDIT SUISSE GROUP

(Translation of registrant's name into English)

Paradeplatz 8, P.O. Box 1, CH-8070 Zurich, Switzerland

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F ![]() Form 40-F

Form 40-F ![]()

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Note: Regulation S-T Rule 101(b)(1) only permits the submission in paper of a Form 6-K if submitted solely to provide an attached annual report to security holders.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Note: Regulation S-T Rule 101(b)(7) only permits the submission in paper of a Form 6-K if submitted to furnish a report or other document that the registrant foreign private issuer must furnish and make public under the laws of the jurisdiction in which the registrant is incorporated, domiciled or legally organized (the registrant's "home country"), or under the rules of the home country exchange on which the registrant's securities are traded, as long as the report or other document is not a press release, is not required to be and has not been distributed to the registrant's security holders, and, if discussing a material event, has already been the subject of a Form 6-K submission or other Commission filing on EDGAR.

Indicate by check mark whether by furnishing the information contained in this Form, the registrant is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes ![]() No

No ![]()

If "Yes" is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): 82-

|

e-mail media.relations@credit-suisse.com |

| CREDIT SUISSE GROUP REPORTS NET PROFIT OF CHF 652 MILLION FOR THE FIRST QUARTER 2003 |  |

| Credit Suisse First Boston Returns to Profitability | |

| Credit Suisse Financial Services Reports | |

| Improved Results Across All Segments | |

Zurich, May 6, 2003 – Credit Suisse Group today announced a net profit of CHF 652 million for the first quarter of 2003, in line with the Group’s preliminary outlook announced on April 25, 2003. Credit Suisse First Boston returned to profitability in the first quarter, due in large part to the significantly improved performance of its Institutional Securities segment. Winterthur’s results recovered further in the first quarter, with both Life & Pensions and Insurance improving their profitability versus the fourth quarter due primarily to increased investment income, tariff increases and lower administration costs. Private Banking recorded a higher segment profit than in the fourth quarter of 2002, as well as net new assets of CHF 1.5 billion. At the same time, Corporate & Retail Banking reported a significant increase in profitability compared to the weak fourth quarter of 2002. Oswald J. Grübel, Co-CEO of Credit Suisse Group and Chief Executive Officer of Credit Suisse Financial Services, stated, "Credit Suisse Group’s first quarter results demonstrate real progress on our goal to return the Group to profitability in 2003. In addition, we are pleased that all of Credit Suisse Financial Services’ segments improved their results in the first quarter, reflecting our targeted measures to reduce costs and adapt the business to prevailing market conditions." John J. Mack, Co-CEO of Credit Suisse Group and Chief Executive Officer of Credit Suisse First Boston, said, "Credit Suisse First Boston’s return to profitability in the first quarter confirms that the measures we have taken to restore our earnings strength are paying off. Last week, we announced the successful conclusion of the sale of Pershing to The Bank of New York. We also finalized the agreement with US regulators last week, which is an important step forward for the Firm and the entire industry in restoring investor confidence." |

1

Group Results

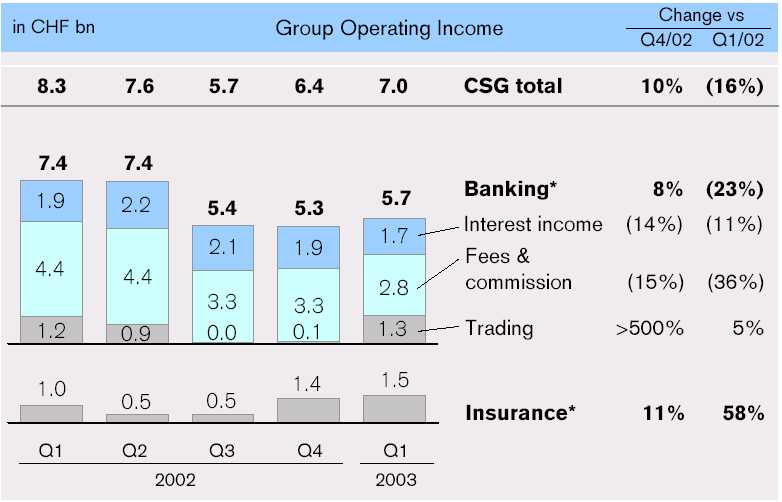

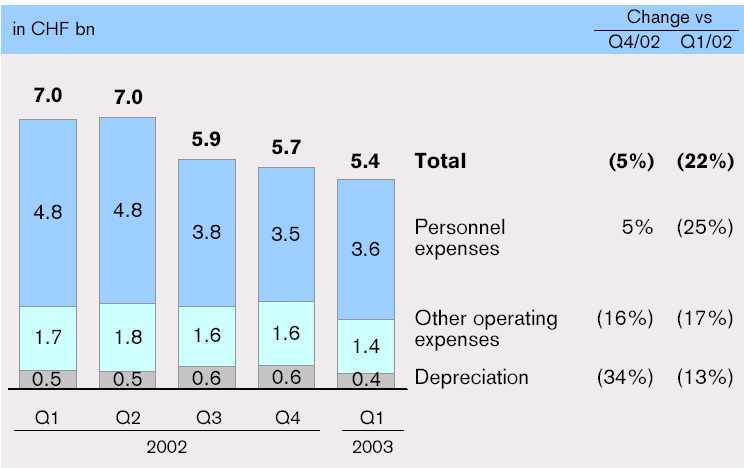

In the first quarter of 2003, Credit Suisse Group reported a net profit of CHF 652 million, including writedowns on the Group’s investments in Swiss Life and Swiss International Airlines of CHF 73 million and CHF 77 million, respectively, and CHF 204 million of amortization of acquired intangible assets and goodwill, after tax. This compared with a net loss of CHF 950 million in the fourth quarter of 2002, in which results were impacted by after-tax exceptional items of CHF 1.3 billion and the one-time positive cumulative effect of a change in accounting principlefor periods prior to 2002 of CHF 520 million. Compared to the first quarter of 2002, net profit increased by CHF 284 million or 77%. The Group’s operating income was CHF 7.0 billion in the first quarter of 2003, up 10% versus the previous quarter but down 16% versus the first quarter of 2002. The Group’s operating expenses decreased 2% versus the fourth quarter to CHF 5.0 billi on and were down 23% compared to the first quarter of 2002.

Earnings per share for the first quarter of 2003 were CHF 0.53, versus a loss of CHF 0.80 for the fourth quarter and a profit of CHF 0.31 for the first quarter of 2002. The Group’s return on equity was 9.2% in the first quarter of 2003, versus -13.0% in the fourth quarter and 4.1% in the first quarter of 2002. The Group’s consolidated BIS tier 1 ratio was 10.0% as of March 31, 2003, up from 9.7% as of December 31, 2002. This increase is attributable to earnings generated in the first quarter, offset by moderate growth in risk-weighted assets in the banking segments and slightly lower equity in the insurance business, and to the positive impact of the Pershing sale transaction that closed on May 1, 2003.

2

Business Unit Results

The segment results described below represent net operating profit before minority interests, excluding exceptional items (at Private Banking, Institutional Securities and CSFB Financial Services segments) and the one-time positive cumulative effect of a change in accounting principle for periods prior to 2002 in the fourth quarter of 2002. For further information on Credit Suisse Group’s first quarter 2003 and fourth quarter 2002 results, please refer to the respective Quarterly Reports, including the reconciliation of operating results to consolidated results contained therein.

All of Credit Suisse Financial Services’ segments improved their performance in the first quarter of 2003 versus the previous quarter. However, as the business unit’s fourth quarter 2002 result benefited from the one-time positive cumulative effect of a change in accounting principle for periods prior to 2002 of CHF 266 million, its first quarter 2003 net profit of CHF 666 million represents a decline of 6% quarter-on-quarter. Compared to the first quarter of 2002, net profit was up 13%. Before the amortization of acquired intangible assets and goodwill, excluding exceptional items in the fourth quarter of 2002 of CHF 73 million and the cumulative effect of a change in accounting principle for periods prior to 2002, first quarter 2003 net operating profit was CHF 690 million, up 29% versus the fourth quarter and up 11% versus the first quarter of 2002.

3

Private Banking reported a segment profit of CHF 371 million in the first quarter 2003, up 10% versus the previous quarter but down 39% compared to the first quarter of 2002. Operating income declined 2% versus the previous quarter to CHF 1.3 billion and was down 21% versus the first quarter of 2002, primarily as a result of reduced transaction volumes in the securities business due to investor passivity and the market-driven lower asset base. First quarter operating expenses decreased 7% versus the fourth quarter and 8% versus the first quarter of 2002.

Corporate & Retail Banking posted a segment profit of CHF 124 million in the first quarter of 2003, up 158% versus the weak fourth quarter but down 15% compared to the first quarter of 2002. Operating income rose 3% quarter-on-quarter to CHF 734 million but was down 7% versus the first quarter of 2002. First quarter operating expenses were down 14% and 3% versus the fourth and first quarters of 2002, respectively. The cost/income ratio was 67.4% for the first quarter of 2003, compared to 80.8% in the fourth quarter of 2002.

Life & Pensions recorded a segment profit of CHF 111 million in the first quarter of 2003, an increase of CHF 96 million versus the first quarter of 2002 and of CHF 18 million compared to the fourth quarter of 2002. Investment income was CHF 1.2 billion for the first quarter of 2003, up CHF 429 million versus the first quarter of 2002. Life & Pensions reported a decrease in gross premiums written of 4%, or CHF 263 million, to CHF 6.5 billion compared to the first quarter of 2002. Adjusted for acquisitions, divestitures and exchange rate impacts, premiums fell 2% versus the first quarter of 2002. The expense ratio for the first quarter of 2003 was 6.8%, compared to 6.4% in the first quarter of 2002.

Insurance reported a segment profit of CHF 92 million in the first quarter of 2003, an increase of CHF 239 million compared to the first quarter of 2002 and of CHF 86 million compared to the fourth quarter of 2002. First quarter 2003 investment income was CHF 289 million, up CHF 202 million versus the first quarter of 2002. Net premiums earned rose CHF 227 million, or 6%, to CHF 4.0 billion versus the first quarter of 2002. Adjusted for acquisitions, divestitures and exchange rate impacts, the premium volume increased 13%. The combined ratio improved 3.2 percentage points in the first quarter to 100.7%, compared to 103.9% in the first quarter of 2002.

The Credit Suisse First Boston business unit reported a net profit of USD 161 million (CHF 221 million) in the first quarter of 2003, compared to a net loss of USD 811 million (CHF 1.3 billion) in the fourth quarter and a net loss of USD 19 million (CHF 32 million) in the first quarter of 2002. Before the amortization of acquired intangible assets and goodwill, excluding exceptional items in the fourth quarter of 2002 of CHF 1.4 billion before tax, or CHF 1.3 billion after tax, and the one-time positive cumulative effect of a change in accounting principle for periods prior to 2002, first quarter net operating profit was USD 292 million (CHF 400 million), compared to a net operating profit of USD 11 million (CHF 15 million) in the fourth quarter and up 88% from a net operating profit of USD 155 million (CHF 259 million) in the first quarter of 2002. Trends in operating income and expenses were affected by a change in reporting for Pershing; effective Jan uary 1, 2003, Pershing’s operating income was reported net of expenses. First quarter operating income increased 24% on a US dollar basis versus the previous quarter, reflecting significantly increased revenues in the Institutional Securities segment. With cost control remaining one of its top priorities, Credit Suisse First Boston significantly improved its pre-tax margin in the first quarter versus both the fourth and first quarters of 2002. Total operating expenses were 16% higher than in the fourth quarter and 16% lower than in the first quarter of 2002. Excluding Pershing, total operating expenses were 27% higher quarter-on-quarter because of increased incentive compensation tied to performance. However, compared to the first quarter of 2002 – again excluding Pershing – operating expenses were down 10% on a 12% reduction in headcount and various cost containment measures.

4

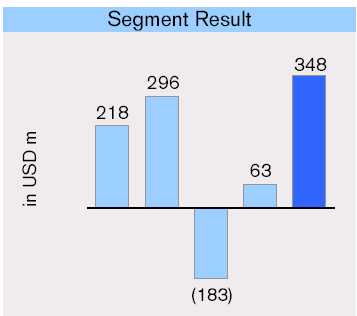

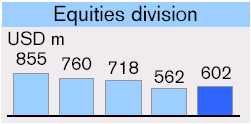

Institutional Securities reported a segment profit of USD 348 million (CHF 476 million) in the first quarter of 2003, up 452% versus the fourth quarter and 60% versus the first quarter of 2002. First quarter 2003 operating income was up 39% versus the prior quarter, to USD 2.6 billion (CHF 3.6 billion), reflecting stronger results in Fixed Income. Compared to the first quarter of 2002, operating income declined 5% as improved Fixed Income results were insufficient to offset industry-wide declines in equities and M&A volumes. Segment operating expenses were consistent with overall Firm trends cited above. In the first quarter of 2003, despite the continuing challenging market environment, the Equity division’s rankings in research, sales and trading generally remained consistent or improved, and Credit Suisse First Boston retained its number one ranking in global high yield new issuances.

CSFB Financial Services reported a segment profit of USD 37 million (CHF 51 million) for the first quarter of 2003, a decline of 23% versus the fourth quarter and 47% versus the first quarter of 2002. This performance reflects lower results from Private Client Services and Pershing, which were impacted by low customer activity and unfavorable market conditions, as well as from Credit Suisse Asset Management, which experienced a decline in assets under management. Operating income for the segment was down 37% compared to the fourth quarter and 43% compared to the first quarter of 2002, and operating expenses were below both periods by 41% and 44%, respectively. Excluding Pershing, operating income was flat compared to the fourth quarter and was down 5% compared to the first quarter of 2002, while operating expenses were below both periods by 3% and 5%, respectively.

5

Net New Assets

Credit Suisse Financial Services reported net new assets of CHF 0.3 billion in the first quarter of 2003, with net inflows of CHF 1.5 billion at Private Banking and of CHF 2.2 billion at Life & Pensions partially offset by a net outflow of CHF 3.4 billion from Corporate & Retail Banking due to a shift from time deposit accounts of corporate clients to transaction accounts, which do not qualify as assets under management. Credit Suisse First Boston reported a net asset outflow of CHF 3.8 billion in the first quarter, as a CHF 1.5 billion net inflow at Private Client Services was offset by net outflows of CHF 5.2 billion from Credit Suisse Asset Management and CHF 0.1 billion from Institutional Securities. For Credit Suisse Group, an overall net asset outflow of CHF 3.5 billion was recorded in the first quarter of 2003, compared with a net asset outflow of CHF 6.6 billion in the fourth quarter of 2002. The Group’s total assets under management were CHF 1,160.5 billion as of March 31, 2003, a decline of 2.9% versus December 31, 2002.

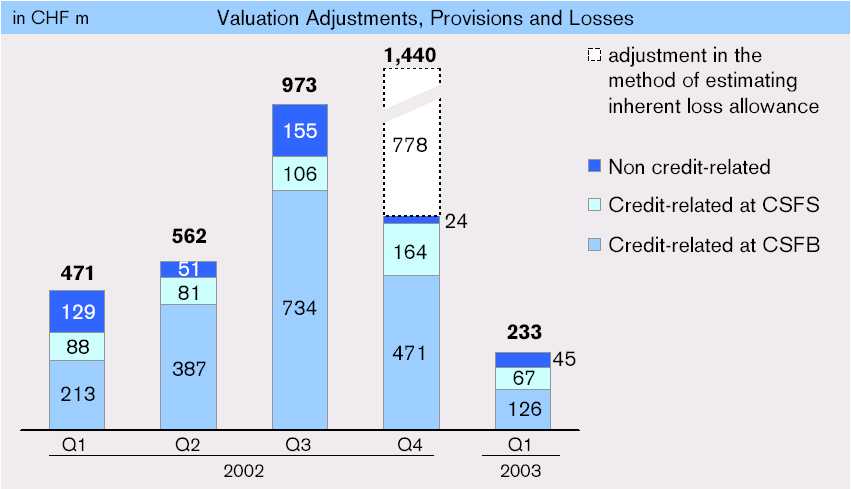

Valuation Adjustments, Provisions and Losses

Total valuation adjustments, provisions and losses of CHF 233 million were recorded in the first quarter of 2003, a decrease of 90% compared with CHF 2.4 billion in the fourth quarter of 2002. Compared to the first quarter of 2002, valuation adjustments, provisions and losses decreased 51%.

Outlook

Given the continued challenging market environment and global uncertainty, Credit Suisse Group remains cautious in its outlook for 2003. The Group made progress towards its goal to return to solid profitability in 2003 but remains exposed to continued volatility in the financial markets, especially as regards the Life & Pensions business.

6

Enquiries

Credit Suisse Group, Media Relations Telephone +41 1 333 8844

Credit Suisse Group, Investor Relations Telephone +41 1 333 4570

The Quarterly Report Q1 2003 and the slide presentation will be available from around 07.30 CET / 06.30 BST / 01.30 EST at www.credit-suisse.com/results/docu.

Credit Suisse Group

Credit Suisse Group is a leading global financial services company headquartered in Zurich. The business unit Credit Suisse Financial Services provides private clients and small and medium-sized companies with Private Banking and financial advisory services, banking products, and Pension and Insurance solutions from Winterthur. The business unit Credit Suisse First Boston, an Investment Bank, serves global institutional, corporate, government and individual clients in its role as a financial intermediary. Credit Suisse Group’s registered shares (CSGN) are listed in Switzerland and Frankfurt, and in the form of American Depositary Shares (CSR) in New York. The Group employs around 73,000 staff worldwide. As of March 31, 2003, it reported assets under management of CH 1,160.5 billion.

Cautionary statement regarding forward-looking information

This press release contains statements that constitute forward-looking statements. In addition, in the future we, and others on our behalf, may make statements that constitute forward-looking statements. Such forward-looking statements may include, without limitation, statements relating to our plans, objectives or goals; our future economic performance or prospects; the potential effect on our future performance of certain contingencies; and assumptions underlying any such statements. Words such as “believes,” “anticipates,” “expects,” "intends” and “plans” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. We do not intend to update these forward-looking statements except as may be required by applicable laws. By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that predictions, forecasts, projections and other outcomes described or implied in forward-looking statements will not be achieved. We caution you that a number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in such forward-looking statements. These factors include (i) market and interest rate fluctuations; (ii) the strength of the global economy in general and the strength of the economies of the countries in which we conduct our operations in particular; (iii) the ability of counterparties to meet their obligations to us; (iv) the effects of, and changes in, fiscal, monetary, trade and tax policies, and currency fluctuations; (v) political and social developments, including war, civil unrest or terrorist activity; (vi) the possibility of foreign exchange controls, expropriation, nationalization or confiscation of assets in countries in which we conduct our operations; (vii) the ability to maintain sufficient liquidity and access capital markets; (viii) operational factors such as systems failure, human error, or the failure to properly implement procedures; (ix) actions taken by regulators with respect to our business and practices in one or more of the countries in which we conduct our operations; (x) the effects of changes in laws, regulations or accounting policies or practices; (xi) competition in geographic and business areas in which we conduct our operations; (xii) the ability to retain and recruit qualified personnel; (xiii) the ability to maintain our reputation and promote our brands; (xiv) the ability to increase market share and control expenses; (xv) technological changes; (xvi) the timely development and acceptance of our new products and services and the perceived overall value of these products and services by users; (xvii) acquisitions, including the ability to integrate successfully acquired businesses; (xviii) the adverse resolution of litigation and other contingencies; and (xix) our success at managing the risks involved in the foregoing. We caution you that the foregoing list of important factors is not exclusive; when evaluating forward-looking statements, you should carefully consider the foregoing factors and other uncertainties and events, as well as the risks identified in our most recently filed Form 20-F and reports on Form 6-K furnished to the US Securities and Exchange Commission.

Cautionary statement regarding non-GAAP financial information

This press release may contain non-GAAP financial information. A reconciliation of such non-GAAP financial information to the most directly comparable measures under generally accepted accounting principles, is posted on our website website at http://www.credit-suisse.com/sec.html.

7

Presentation of Credit Suisse Group’s First Quarter Results 2003 via Webcast and Telephone Conference

| Date | Tuesday, May 6, 2003 |

| Time | 15.00 CET / 14.00 BST / 09.00 EST |

| Speakers | Philip K. Ryan, CFO of Credit Suisse Group |

| Ulrich Körner, CFO of Credit Suisse Financial Services | |

| Barbara Yastine, CFO of Credit Suisse First Boston | |

| All presentations will be held in English. | |

| Webcast | http://www.credit-suisse.com/results |

| Telephone | Europe: +41 91 610 5600 |

| UK: +44 207 866 4111 | |

| USA: +1 412 858 4600 | |

| Reference: “Credit Suisse Group quarterly results” | |

| Q&A | You will have the opportunity to ask the speakers questions via telephone conference following the presentations. |

| Playback | Video on demand – available approximately three hours after the event at http://www.credit-suisse.com/results |

| Telephone – available approximately one hour after the event; please dial: | |

| Europe: +41 91 612 4330 | |

| UK: +44 207 866 4300 | |

| USA: +1 412 858 1440 | |

| Conference ID: 631# | |

| Note | We recommend that you dial in approximately ten minutes before the start of the presentation for the webcast and telephone conference. Further instructions and technical test functions are now available on our website. |

8

QUARTERLY REPORT 2003 Q1

Credit Suisse Group is a leading global financial services company headquartered in Zurich. Credit Suisse Financial Services provides private clients and small and medium-sized companies with private banking and financial advisory services, banking products, and pension and insurance solutions from Winterthur. Credit Suisse First Boston, the investment bank, serves global institutional, corporate, government and individual clients in its role as a financial intermediary. Credit Suisse Group’s registered shares (CSGN) are listed in Switzerland and Frankfurt, and in the form of American Depositary Shares (CSR) in New York. The Group employs around 73,000 staff worldwide.

QUARTERLY REPORT 2003

EDITORIAL

CREDIT SUISSE GROUP FINANCIAL HIGHLIGHTS Q1/2003

AN OVERVIEW OF CREDIT SUISSE GROUP

Equity capital

Net new assets

Operating income and expenses

Valuation adjustments, provisions and losses

Outlook

RISK MANAGEMENT

Overall risk trends

Trading risks

Credit risk exposure

REVIEW OF BUSINESS UNITS | CREDIT SUISSE FINANCIAL SERVICES

Private Banking

Corporate & Retail Banking

Life & Pensions

Insurance

REVIEW OF BUSINESS UNITS | CREDIT SUISSE FIRST BOSTON

Institutional Securities

CSFB Financial Services

RECONCILIATION OF OPERATING TO CONSOLIDATED RESULTS

Reconciliation of operating to consolidated results

CONSOLIDATED RESULTS | CREDIT SUISSE GROUP

LOANS

INFORMATION FOR INVESTORS

Enquiries

Financial Publications

This symbol is used to indicate topics on which further information is available on our website. Go to www.credit-suisse.com/results/bookmarks.html to find links to the relevant information. The additional information -indicated is openly accessible and does not form part of the Quarterly Report. Some areas of Credit Suisse Group’s websites are only available in English.

Cautionary statement regarding forward-looking information

This Quarterly Report contains statements that constitute forward-looking statements. In addition, in the future we, and others on our behalf, may make statements that constitute forward-looking statements. Such forward-looking statements may include, without limitation, statements relating to our plans, objectives or goals; our future economic performance or prospects; the potential effect on our future performance of certain contingencies; and assumptions underlying any such statements.

Words such as "believes," "anticipates," "expects," "intends" and "plans" and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. We do not intend to update these forward-looking statements except as may be required by applicable laws.

By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that predictions, forecasts, projections and other outcomes described or implied in forward-looking statements will not be achieved. We caution you that a number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in such forward-looking statements. These factors include (i) market and interest rate fluctuations; (ii) the strength of the global economy in general and the strength of the economies of the countries in which we conduct our operations in particular; (iii) the ability of counterparties to meet their obligations to us; (iv) the effects of, and changes in, fiscal, monetary, trade and tax policies, and currency fluctuations; (v) political and social developments, including war, civil unrest or terrorist activity; (vi) the possibility of foreign exchange controls, expropriation, nationalization or confiscation of assets in countries in which we conduct our operations; (vii) the ability to maintain sufficient liquidity and access capital markets; (viii) operational factors such as systems failure, human error, or the failure to properly implement procedures; (ix) actions taken by regulators with respect to our business and practices in one or more of the countries in which we conduct our operations; (x) the effects of changes in laws, regulations or accounting policies or practices; (xi) competition in geographic and business areas in which we conduct our operations; (xii) the ability to retain and recruit qualified personnel; (xiii) the ability to maintain our reputation and promote our brands; (xiv) the ability to increase market share and control expenses; (xv) technological changes; (xvi) the timely development and acceptance of our new products and services and the perceived overall value of these products and se rvices by users; (xvii) acquisitions, including the ability to integrate successfully acquired businesses; (xviii) the adverse resolution of litigation and other contingencies; and (xix) our success at managing the risks involved in the foregoing.

We caution you that the foregoing list of important factors is not exclusive; when evaluating forward-looking statements, you should carefully consider the foregoing factors and other uncertainties and events, as well as the risks identified in our most recently filed Form 20-F and reports on Form 6-K furnished to the US Securities and Exchange Commission.

Cautionary statement regarding non-GAAP financial information

This Quarterly Report may contain non-GAAP financial information. A reconciliation of such non-GAAP financial information to the most directly comparable measures under generally accepted accounting principles is contained in this report and is posted on our website at www.credit-suisse.com/sec.html.

EDITORIAL

Oswald J. Grübel

Co-CEO Credit Suisse Group

Chief Executive Officer

Credit Suisse Financial Services

John J. Mack

Co-CEO Credit Suisse Group

Chief Executive Officer

Credit Suisse First Boston

Dear shareholders, clients and colleagues

In the first quarter of 2003 Credit Suisse Group returned to profitability. The Group recorded a net profit of CHF 652 million in a challenging environment, after reporting a net loss of CHF 950 million in the previous quarter. The measures that we took across the Group to restore earnings strength and adapt the cost structure to the current business environment are beginning to pay off. The Group expects continuing challenging conditions for the remainder of the year. However, we are fully committed to achieving our goal of profitability in 2003.

All segments of Credit Suisse Financial Services improved profitability and reported better results than in the fourth quarter of 2002. Credit Suisse Financial Services posted a net profit of CHF 666 million in the first quarter of 2003, compared with a net profit of CHF 705 million in the previous quarter, which included the one-time positive cumulative effect of a change in accounting principle in the amount of CHF 266 million for periods prior to 2002. Private Banking recorded an increased segment profit and an increased level of net new assets compared with the fourth quarter of 2002. Corporate & Retail Banking increased its segment profit considerably compared to a weak fourth quarter.

Our insurance segments, Life & Pensions and Insurance, further improved their operating performance in the first quarter of 2003 and both segments increased their segment profits compared to the previous quarter. These improvements resulted primarily from tariff increases and stronger investment income. The realignment of the Winterthur organization has resulted in the merger of its two Corporate Centers and redefined management levels for the countries where the life and non-life businesses are being merged.

Credit Suisse First Boston restored its profitability in the first quarter of 2003, with a net profit of USD 161 million (CHF 221 million) compared to a net loss of USD 811 million (CHF 1.3 billion) in the previous quarter. Its Institutional Securities segment improved significantly from the fourth quarter of 2002, benefiting in particular from a strong performance by the Fixed Income division, notably lower cost levels and credit provisions. In the fourth quarter of 2002, the business unit reached an agreement in principle with certain US regulators involving research analyst independence and IPO allocations to corporate executives, and an ultimate settlement was recently finalized. In addition, certain structural and financial legacies and costs were reduced considerably.

The Group's consolidated BIS tier 1 ratio increased further to 10.0%, compared to 9.7% as of December 31, 2002 reflecting the quarter’s earnings and the sale of Pershing, partly offset by moderate growth in risk-weighted assets in the banking business.

While we are not yet satisfied with our results, we are pleased that the first quarter performance is the first tangible result of our efforts to return the Group to profitability. We expect 2003 to be challenging and will continue to focus on cost control and the strength of our franchises.

Oswald J. Grübel John J. Mack

May 2003

CREDIT SUISSE GROUP FINANCIAL HIGHLIGHTS Q1/2003

| Consolidated income statement | ||||||||||||

| Change | Change | |||||||||||

| in % from | in % from | |||||||||||

| in CHF m | 1Q2003 | 4Q2002 | 1Q2002 | 4Q2002 | 1Q2002 | |||||||

| Operating income | 7,024 | 6,395 | 8,330 | 10 | (16) | |||||||

| Gross operating profit | 2,004 | 1,284 | 1,832 | 56 | 9 | |||||||

| Net profit/(loss) | 652 | (950) | 368 | – | 77 | |||||||

| Return on equity | ||||||||||||

| Change | Change | |||||||||||

| in % from | in % from | |||||||||||

| in % | 1Q2003 | 4Q2002 | 1Q2002 | 4Q2002 | 1Q2002 | |||||||

| Return on equity | 9.2 | (13.0) | 4.1 | – | 124 | |||||||

| Consolidated balance sheet | ||||||||||||

| Change | ||||||||||||

| in % from | ||||||||||||

| in CHF m | 31.03.03 | 31.12.02 | 31.12.02 | |||||||||

| Total assets | 992,143 | 955,656 | 4 | |||||||||

| Shareholders' equity | 31,402 | 31,394 | 0 | |||||||||

| Minority interests in shareholders' equity | 2,879 | 2,878 | 0 | |||||||||

| Capital data | ||||||||||||

| Change | ||||||||||||

| in % from | ||||||||||||

| in CHF m | 31.03.03 | 31.12.02 | 31.12.02 | |||||||||

| BIS risk-weighted assets | 205,548 | 201,466 | 2 | |||||||||

| BIS tier 1 capital | 20,517 | 19,544 | 5 | |||||||||

| of which non-cumulative perpetual preferred securities | 2,146 | 2,162 | (1) | |||||||||

| BIS total capital | 34,685 | 33,290 | 4 | |||||||||

| Capital ratios | ||||||||||||

| in % | 31.03.03 | 31.12.02 | ||||||||||

| BIS tier 1 ratio | Credit Suisse | 7.5 | 7.4 | |||||||||

| Credit Suisse First Boston | 1) | 10.5 | 10.3 | |||||||||

| Credit Suisse Group | 2) | 10.0 | 9.7 | |||||||||

| BIS total capital ratio | Credit Suisse Group | 16.9 | 16.5 | |||||||||

| Assets under management/client assets | ||||||||||||

| Change | ||||||||||||

| in % from | ||||||||||||

| in CHF bn | 31.03.03 | 31.12.02 | 31.12.02 | |||||||||

| Advisory assets under management | 588.5 | 605.6 | (3) | |||||||||

| Discretionary assets under management | 572.0 | 589.7 | (3) | |||||||||

| Total assets under management | 1,160.5 | 1,195.3 | (3) | |||||||||

| Client assets | 1,256.7 | 1,793.2 | (30) | |||||||||

| Net new assets | ||||||||||||

| Change | Change | |||||||||||

| in % from | in % from | |||||||||||

| in CHF bn | 1Q2003 | 4Q2002 | 1Q2002 | 4Q2002 | 1Q2002 | |||||||

| Net new assets | (3.5) | (6.6) | 13.5 | (47) | – | |||||||

| 1) Ratio is based on a tier 1 capital of CHF 11.2 bn (31.12.02: CHF 10.6 bn), of which non-cumulative perpetual preferred securities is CHF 1.0 bn (31.12.02: CHF 1.0 bn). | ||||||||||||

| 2) Ratio is based on a tier 1 capital of CHF 20.5 bn (31.12.02: CHF 19.5 bn), of which non-cumulative perpetual preferred securities is CHF 2.1 bn (31.12.02: CHF 2.2 bn). | ||||||||||||

| Number of employees (full-time equivalents) | |||||||||||

| Change | |||||||||||

| in % from | |||||||||||

| 31.03.03 | 31.12.02 | 31.12.02 | |||||||||

| Switzerland | banking | 20,952 | 21,270 | (1) | |||||||

| insurance | 6,876 | 7,063 | (3) | ||||||||

| Outside Switzerland | banking | 20,726 | 25,057 | (17) | |||||||

| insurance | 24,817 | 25,067 | (1) | ||||||||

| Total employees Credit Suisse Group | 73,371 | 78,457 | (6) | ||||||||

| Share data | |||||||||||

| Change | |||||||||||

| in % from | |||||||||||

| 31.03.03 | 31.12.02 | 31.12.02 | |||||||||

| Shares issued | 1,189,891,720 | 1,189,891,720 | 0 | ||||||||

| To be issued upon conversion of MCS | 1) | 40,413,838 | 40,413,838 | 0 | |||||||

| Shares outstanding | 1,230,305,558 | 1,230,305,558 | 0 | ||||||||

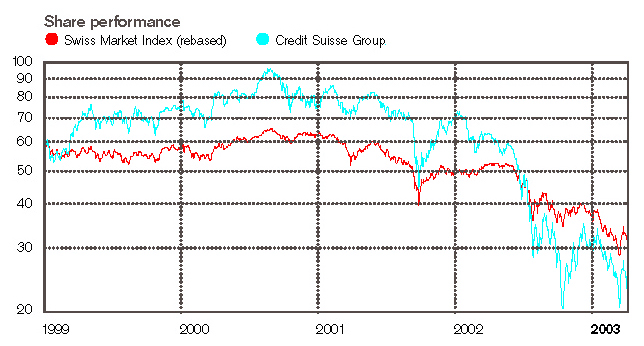

| Share price in CHF | 23.50 | 30.00 | (22) | ||||||||

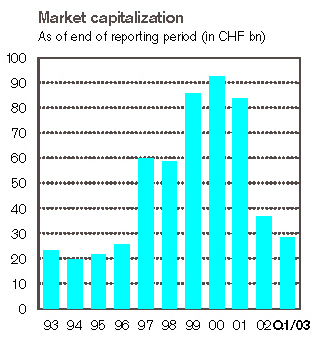

| Market capitalization in CHF m | 28,912 | 36,909 | (22) | ||||||||

| Book value per share in CHF | 23.18 | 23.18 | 0 | ||||||||

| 1) Maximum number of shares related to Mandatory Convertible Securities (MCS) issued by Credit Suisse Group Finance (Guernsey) Ltd. in December 2002. | |||||||||||

| Share price | |||||||||||

| Change | Change | ||||||||||

| in % from | in % from | ||||||||||

| in CHF | 1Q2003 | 4Q2002 | 1Q2002 | 4Q2002 | 1Q2002 | ||||||

| High (closing price) | 34.45 | 35.70 | 73.60 | (4) | (53) | ||||||

| Low (closing price) | 20.70 | 20.60 | 56.50 | 0 | (63) | ||||||

| Earnings per share | |||||||||||

| Change | Change | ||||||||||

| in % from | in % from | ||||||||||

| in CHF | 1Q2003 | 4Q2002 | 1Q2002 | 4Q2002 | 1Q2002 | ||||||

| Basic earnings per share | 0.53 | (0.80) | 0.31 | – | 71 | ||||||

| Diluted earnings per share | 0.53 | (0.80) | 0.31 | – | 71 | ||||||

AN OVERVIEW OF CREDIT SUISSE GROUP

Credit Suisse Group returned to profitability in the first quarter of 2003, reporting a net profit of CHF 652 million, compared with a net loss of CHF 950 million in the fourth quarter of 2002. Compared to the first quarter of 2002, the net profit increased CHF 284 million, or 77%. Credit Suisse Financial Services recorded a net profit of CHF 666 million, with all segments posting improved results. Credit Suisse First Boston recorded a net profit of USD 161 million (CHF 221 million) with a significant improvement in the results of the Institutional Securities segment.

The first quarter 2003 results demonstrate Credit Suisse Group's progress on returning to profitability despite continuing challenging market conditions.

Winterthur’s results continued to recover in the first quarter of 2003, with both Life & Pensions and Insurance improving profitability compared to the previous quarter due to stronger investment income and tariff increases. Private Banking recorded a higher segment profit than in the fourth quarter of 2002, primarily due to lower operating expenses. Corporate & Retail Banking increased its segment profit considerably compared to a weak fourth quarter. Overall, Credit Suisse Financial Services reported a net profit of CHF 666 million in the first quarter of 2003, down 6% compared to the fourth quarter of 2002 and up 13% compared to the corresponding period of the previous year. In the fourth quarter of 2002, Credit Suisse Financial Services’ results benefited from the one-time cumulative effect of a change in accounting principle for periods prior to 2002.

Credit Suisse First Boston posted a first quarter net profit of USD 161 million (CHF 221 million), compared with a net loss of USD 811 million (CHF 1.3 billion) in the previous quarter, which was impacted by exceptional items of USD 813 million (CHF 1.3 billion) after-tax. Compared to the first quarter of 2002, the business unit’s net profit increased USD 180 million (CHF 253 million). Institutional Securities improved its segment result in the first quarter of 2003 significantly compared to the previous quarter, benefiting particularly from strong results in the Fixed Income business. CSFB Financial Services reported a lower segment result compared to the fourth quarter of 2002, mainly due to weak equity markets and lower assets under management.

After accounting for the Corporate Center, which includes writedowns on the Group’s investments in Swiss Life and Swiss International Airlines of CHF 73 million and CHF 77 million, respectively, the Group reported a net profit of CHF 652 million for the first quarter of 2003, compared with a net loss of CHF 950 million in the previous quarter. In the first quarter of 2003, net profit included CHF 204 million of amortization of acquired intangible assets and goodwill after-tax. The fourth quarter 2002 results were impacted by exceptional items of CHF 1.3 billion after-tax and the positive one-time cumulative effect of a change in accounting principle for periods prior to 2002 in the amount of CHF 520 million. Compared to the first quarter of 2002, net profit increased CHF 284 million, or 77%. Earnings per share for the first quarter of 2003 were CHF 0.53 versus a loss of CHF 0.80 for the fourth quarter of 2002 and a profit of CHF 0. 31 for the first quarter of 2002. The Group’s return on equity was 9.2% in the first quarter of 2003 versus -13.0% in the fourth quarter and 4.1% in the first quarter of 2002.

Equity capital

During the first quarter of 2003, Credit Suisse Group further improved its capital base in addition to the improvements reported in the fourth quarter of 2002. The Group’s consolidated BIS tier 1 ratio stood at 10.0% as of March 31, 2003, up from 9.7% as of December 31, 2002. This increase was due to earnings generated in the first quarter of 2003, offset by moderate growth in risk-weighted assets in the banking business and slightly lower equity in the insurance business. The Pershing sale transaction also had a positive impact on core capital.

On the basis of the final local statutory accounts of Winterthur’s operating entities for 2002, which were completed in April 2003, Credit Suisse Group updated Winterthur’s consolidated EU solvency ratio effective December 31, 2002, to 142%. At year-end 2002, the local solvency ratios of Winterthur’s operating entities worldwide continued to exceed regulatory requirements: for the ten largest entities, the average local coverage was above 200% and the lowest ratio was 135% at year-end. The consolidated EU solvency ratio is a supplementary financial disclosure for Winterthur and has no impact on published financial statements and note disclosures, regulatory insurance filings, or the Group’s internal economic risk capital models. This update does not change the Group’s view regarding the capitalization of Winterthur.

Net new assets

Credit Suisse Financial Services reported net new assets of CHF 0.3 billion in the first quarter of 2003, with net inflows of CHF 1.5 billion at Private Banking and CHF 2.2 billion at Life & Pensions, offset by a net outflow of CHF 3.4 billion from Corporate & Retail Banking due to a shift from time deposit into transaction accounts, which do not qualify as assets under management. Credit Suisse First Boston reported a net asset outflow of CHF 3.8 billion in the first quarter of 2003, as CHF 1.5 billion of net new assets from Private Client Services were offset by a net outflow of CHF 5.2 billion from Credit Suisse Asset Management and CHF 0.1 billion from Institutional Securities. For Credit Suisse Group, an overall net asset outflow of CHF 3.5 billion was recorded in the first quarter of 2003, compared with a net asset outflow of CHF 6.6 billion recorded in the fourth quarter of 2002. The Group’s total assets under managem ent stood at CHF 1,160.5 billion as of March 31, 2003, corresponding to a decline of 2.9% versus December 31, 2002.

Operating income and expenses

The Group’s operating income was CHF 7.0 billion in the first quarter of 2003, up 10% on the previous quarter but down 16% on the first quarter of 2002. Credit Suisse Financial Services reported operating income of CHF 3.4 billion in the first quarter of 2003, a decrease of 4% versus the previous quarter and an increase of 3% versus the first quarter of 2002. At Private Banking, operating income decreased 2% versus the previous quarter due to investor passivity and a reduced asset base. Corporate & Retail Banking posted a 3% increase in operating income quarter-on-quarter, mainly driven by higher transaction-based and trading income. At Credit Suisse First Boston, first quarter 2003 operating income increased 24% on a US dollar basis versus the previous quarter to USD 2.9 billion (CHF 4.0 billion), mainly reflecting a significant increase in revenue in the Fixed Income business within Institutional Securities from USD 587 millio n (CHF 806 million) to USD 1.4 billion (CHF 1.9 billion). Compared to the first quarter of 2002, Credit Suisse First Boston’s operating income decreased 11%, reflecting weak market conditions in the mergers and acquisitions and equity new issuance markets. The increase in operating income versus the fourth quarter of 2002 was partially offset by a decline in operating income at CSFB Financial Services of 37% versus the previous quarter, principally related to the sale of Pershing. Excluding Pershing, operating income of CSFB Financial Services was flat compared with the fourth quarter of 2002 and decreased 5% compared to the first quarter of 2002.

The Group’s operating expenses decreased 2% quarter-on-quarter to CHF 5.0 billion, and were down 23% on the first quarter of 2002. At Credit Suisse Financial Services, first quarter operating expenses decreased 7% compared to the previous quarter and 5% versus the first quarter of 2002. At Credit Suisse First Boston, first quarter operating expenses increased 16% versus the previous quarter due to a rise in incentive compensation linked to improved performance and compared to an unusually low fourth quarter incentive compensation level. Compared to the first quarter of 2002, Credit Suisse First Boston’s operating expenses decreased 16%, reflecting headcount reductions and cost containment measures. For the first quarter of 2003, Credit Suisse First Boston’s other operating expenses were down 18% compared with the fourth quarter of 2002 and 15% compared with the first quarter of 2002.

Valuation adjustments, provisions and losses

Total valuation adjustments, provisions and losses were CHF 233 million in the first quarter of 2003 compared with CHF 2.4 billion in the fourth quarter of 2002, which included a charge of CHF 778 million in respect of an adjustment in the method of estimating inherent losses related to lending activities. In the first quarter of 2003, valuation adjustments, provisions and losses included a charge of CHF 32 million related to inherent loan loss risks. Compared to the first quarter of 2002, valuation adjustments, provisions and losses decreased 51%.

Outlook

Credit Suisse Group remains cautious in its outlook for 2003 given the continued challenging market environment and global uncertainty. The Group made progress towards its goal to return to profitability in 2003 but remains exposed to continued volatility in the financial markets.

| Overview of business unit results 1) | |||||||||||||||||||||||||

| Credit Suisse Financial Services | Credit Suisse First Boston | Adjust. incl. Corporate Center | Credit Suisse Group | ||||||||||||||||||||||

| in CHF m | 1Q2003 | 4Q2002 | 1Q2002 | 1Q2003 | 4Q2002 | 1Q2002 | 1Q2003 | 4Q2002 | 1Q2002 | 1Q2003 | 4Q2002 | 1Q2002 | |||||||||||||

| Operating income | 3,393 | 3,517 | 3,306 | 3,915 | 3,321 | 5,338 | (284) | (443) | (314) | 7,024 | 6,395 | 8,330 | |||||||||||||

| Personnel expenses | 1,369 | 1,408 | 1,443 | 2,177 | 1,896 | 3,216 | 93 | 160 | 178 | 3,639 | 3,464 | 4,837 | |||||||||||||

| Other operating expenses | 779 | 896 | 814 | 904 | 1,184 | 1,302 | (302) | (433) | (455) | 1,381 | 1,647 | 1,661 | |||||||||||||

| Operating expenses | 2,148 | 2,304 | 2,257 | 3,081 | 3,080 | 4,518 | (209) | (273) | (277) | 5,020 | 5,111 | 6,498 | |||||||||||||

| Gross operating profit | 1,245 | 1,213 | 1,049 | 834 | 241 | 820 | (75) | (170) | (37) | 2,004 | 1,284 | 1,832 | |||||||||||||

| Depreciation of non-current assets | 2) | 220 | 334 | 205 | 130 | 156 | 207 | 70 | 144 | 69 | 420 | 634 | 481 | ||||||||||||

| Amortization of acquired intangible assets and goodwill | 25 | 92 | 29 | 206 | 308 | 357 | 1 | 3 | (1) | 232 | 403 | 385 | |||||||||||||

| Valuation adjustments, provisions and losses | 81 | 105 | 99 | 176 | 1,977 | 338 | (24) | 342 | 34 | 233 | 2,424 | 471 | |||||||||||||

| Profit/(loss) before extraordinary items, cumulative effect of change in accounting principle and taxes | 919 | 682 | 716 | 322 | (2,200) | (82) | (122) | (659) | (139) | 1,119 | (2,177) | 495 | |||||||||||||

| Extraordinary income/(expenses), net | 7 | 24 | (3) | 0 | 220 | 0 | (56) | 125 | (2) | (49) | 369 | (5) | |||||||||||||

| Cumulative effect of change in accounting principle | 3) | – | 266 | – | – | 254 | – | – | 0 | – | – | 520 | – | ||||||||||||

| Taxes | 3) | (252) | (318) | (119) | (101) | 474 | 50 | (25) | 162 | (18) | (378) | 318 | (87) | ||||||||||||

| Net profit/(loss) before minority interests | 674 | 654 | 594 | 221 | (1,252) | (32) | (203) | (372) | (159) | 692 | (970) | 403 | |||||||||||||

| Minority interests | (8) | 51 | (2) | 0 | 0 | 0 | (32) | (31) | (33) | (40) | 20 | (35) | |||||||||||||

| Net profit/(loss) | 3) | 666 | 705 | 592 | 221 | (1,252) | (32) | (235) | (403) | (192) | 652 | (950) | 368 | ||||||||||||

| 1) The Group’s consolidated results are prepared in accordance with Swiss GAAP, while the Group’s segment reporting principles are applied to the presentation of segment results. The business unit results reflect the results of the separate segments comprising the respective business units as well as certain acquisition-related costs, exceptional items and cumulative effect of change in accounting principle that are not allocated to the segments. For a complete reconciliation of the business unit results to the Group’s consolidated results and a discussion of the material reconciling items, please refer to “Reconciliation of operating to consolidated results”. | |||||||||||||||||||||||||

| 2) Includes amortization of Present Value of Future Profits (PVFP) from the insurance business within Credit Suisse Financial Services. | |||||||||||||||||||||||||

| 3) In 4Q2002, Credit Suisse Group adopted a change in accounting principle relating to the recognition of deferred tax assets on net operating losses. The retroactive application of this change in accounting principle would have resulted in taxes for 4Q2002 and 1Q2002 for Credit Suisse Financial Services of CHF –635 m and CHF –85 m, respectively, for Credit Suisse First Boston of CHF 276 m and CHF 50 m, respectively, and for Credit Suisse Group of CHF –198 m and CHF –53 m, respectively. | |||||||||||||||||||||||||

| Assets under management/client assets | |||||||||||

| Change | |||||||||||

| in % from | |||||||||||

| in CHF bn | 31.03.03 | 31.12.02 | 31.12.02 | ||||||||

| Credit Suisse Financial Services | |||||||||||

| Private Banking | 1) | ||||||||||

| Assets under management | 457.0 | 465.7 | (1.9) | ||||||||

| of which discretionary | 118.2 | 121.5 | (2.7) | ||||||||

| Client assets | 486.3 | 494.8 | (1.7) | ||||||||

| Corporate & Retail Banking | 1) | ||||||||||

| Assets under management | 64.1 | 70.3 | (8.8) | ||||||||

| Client assets | 82.6 | 86.3 | (4.3) | ||||||||

| Life & Pensions | |||||||||||

| Assets under management (discretionary) | 111.7 | 110.8 | 0.8 | ||||||||

| Client assets | 111.7 | 110.8 | 0.8 | ||||||||

| Insurance | |||||||||||

| Assets under management (discretionary) | 31.0 | 30.7 | 1.0 | ||||||||

| Client assets | 31.0 | 30.7 | 1.0 | ||||||||

| Credit Suisse Financial Services | |||||||||||

| Assets under management | 663.8 | 677.5 | (2.0) | ||||||||

| of which discretionary | 1) | 262.1 | 264.2 | (0.8) | |||||||

| Client assets | 711.6 | 722.6 | (1.5) | ||||||||

| Credit Suisse First Boston | |||||||||||

| Institutional Securities | |||||||||||

| Assets under management | 30.8 | 31.3 | (1.6) | ||||||||

| of which Private Equity on behalf of clients (discretionary) | 20.8 | 20.9 | (0.5) | ||||||||

| Client assets | 79.2 | 83.9 | (5.6) | ||||||||

| CSFB Financial Services | |||||||||||

| Assets under management | 465.9 | 486.5 | (4.2) | ||||||||

| of which discretionary | 281.9 | 297.2 | (5.1) | ||||||||

| Client assets | 465.9 | 986.7 | (52.8) | ||||||||

| Credit Suisse First Boston | |||||||||||

| Assets under management | 496.7 | 517.8 | (4.1) | ||||||||

| of which discretionary | 309.9 | 325.5 | (4.8) | ||||||||

| Client assets | 545.1 | 1,070.6 | (49.1) | ||||||||

| Credit Suisse Group | |||||||||||

| Assets under management | 1,160.5 | 1,195.3 | (2.9) | ||||||||

| of which discretionary | 1) | 572.0 | 589.7 | (3.0) | |||||||

| Client assets | 1,256.7 | 1,793.2 | (29.9) | ||||||||

| 1) 2002 comparative figures have been restated to reflect the realignment of the private client business as of 01.01.2003. This entailed moving certain client segments in Switzerland from Private Banking to Corporate & Retail Banking as well as re-evaluating the balances of 2002 discretionary assets. | |||||||||||

| Net new assets | |||||||||||

| Change | Change | ||||||||||

| in % from | in % from | ||||||||||

| in CHF bn | 1Q2003 | 4Q2002 | 1Q2002 | 4Q2002 | 1Q2002 | ||||||

| Credit Suisse Financial Services | |||||||||||

| Private Banking | 1) | 1.5 | 0.9 | 9.2 | 66.7 | (83.7) | |||||

| Corporate & Retail Banking | 1) | (3.4) | (0.2) | (1.4) | – | 142.9 | |||||

| Life & Pensions | 2.2 | (1.3) | 3.0 | – | (26.7) | ||||||

| Credit Suisse Financial Services | 0.3 | (0.6) | 10.8 | – | (97.2) | ||||||

| Credit Suisse First Boston | |||||||||||

| Institutional Securities | (0.1) | – | 3.5 | – | – | ||||||

| CSFB Financial Services | (3.7) | (6.0) | (0.8) | (38.3) | 362.5 | ||||||

| Credit Suisse First Boston | (3.8) | (6.0) | 2.7 | (36.7) | – | ||||||

| Credit Suisse Group | (3.5) | (6.6) | 13.5 | (47.0) | – | ||||||

| 1) 2002 comparative figures have been restated to reflect the realignment of the private client business as of 01.01.2003. This entailed moving certain client segments in Switzerland from Private Banking to Corporate & Retail Banking. | |||||||||||

RISK MANAGEMENT

Credit Suisse Group’s overall position risk fell by 3% in the first quarter of 2003 compared to the previous quarter, predominantly due to further equity position reductions and lower credit risks. Credit Suisse First Boston’s average trading Value-at-Risk, or VaR, increased primarily as a consequence of higher interest rate positions. The Group’s credit risk exposures increased by 3% quarter-on-quarter.

Overall risk trends

Economic risk capital, or ERC, is an emerging best practice for measuring and reporting all quantifiable risks across a financial organization on a consistent and comprehensive basis. It is referred to as “economic” capital because it treats positions solely on an economic basis, irrespective of differences in accounting or regulatory treatment. Credit Suisse Group has established this tool over the last few years to achieve several objectives: to better assess the composition and trend of our risk portfolio; to improve risk control and limits; to allocate capital; to bettter assess our risk-bearing capacity in relation to financial resources; and to provide a benchmark for risk/return analysis by business. ERC is defined as the economic capital needed to remain solvent even under extreme market, business and operational conditions, based on conservative assumptions.

Credit Suisse Group distinguishes among three fundamental sources of risk. Position risk ERC measures the potential unexpected loss in economic value associated with the Group’s portfolio of positions over a 1-year horizon that is exceeded with a given, small probability (1% for daily risk management purposes; 0.03% for capital management purposes). Business risk ERC captures the risk related to the Group’s commission and fee-based activities by estimating the potential worst-case negative margin for these activities during a severe market downturn. Operational risk ERC represents the estimated worst-case loss resulting from inadequate or failed internal processes and systems, human error or external events.

Position risk ERC constitutes the most important risk category. Total 99%, 1-year position risk ERC was down 3% in the first quarter of 2003 compared with the previous quarter, due primarily to further equity position reductions and lower credit risks. At the end of the first quarter of 2003, 51% of the Group’s position risk ERC was with Credit Suisse First Boston, 45% with Credit Suisse Financial Services (of which 68% was with the insurance units and 32% was with the banking units) and 4% with the Corporate Center.

Trading risks

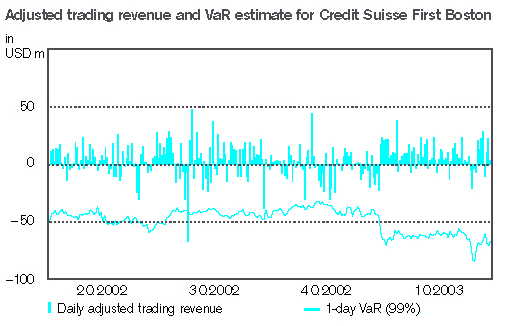

The average 1-day, 99% VaR at Credit Suisse First Boston in the first quarter of 2003 was USD 49.2 million, compared to USD 39.4 million in the fourth quarter of 2002. The increase was primarily attributable to an increase in interest rate positions. As shown in the backtesting chart, Credit Suisse First Boston had no backtesting exceptions in the first quarter of 2003. Over the last 12 months, Credit Suisse First Boston had one backtesting exception (on average, an accurate 1-day, 99% VaR model would have no more than 2.5 exceptions per annum).

Credit risk exposure

Credit-related balance sheet exposure increased 3% for Credit Suisse Group in the first quarter of 2003, as a slight decline in exposure at Credit Suisse Financial Services was offset by an increase in exposure at Credit Suisse First Boston.

Effective in the first quarter of 2003, loans held for sale are no longer reported as part of total due from banks and customers, gross with the related credit provisions reported separately, instead they are presented on a net lower of cost or market basis. This change resulted in a reclassification in the tables on page 10 which impacted both the loans, impaired loans and the valuation accounts as of March 31, 2003.

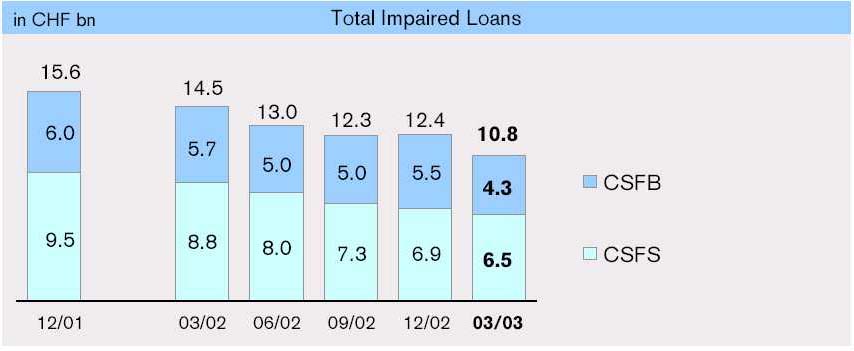

Impaired loans for Credit Suisse Group declined as of the end of the first quarter due to a reduction in impaired loans at both business units. Total non-performing loans declined 9% at Credit Suisse Financial Services. The decline in impaired loans at Credit Suisse First Boston is primarily attributable to the previously mentioned change in presentation and a decrease in non-performing loans. Coverage of non-performing loans increased slightly for both business units and Credit Suisse Group. Coverage of total impaired loans at Credit Suisse Group improved during the quarter, as coverage at Credit Suisse First Boston improved from 66.5% at December 31, 2002 to 71.6% at March 31, 2003, while coverage of impaired loans declined slightly at Credit Suisse Financial Services. Credit quality for the Group was largely unchanged from year-end 2002.

| Key Position Risk Trends | ||||||||||||

| Change in % from | Change Analysis: Brief Summary | |||||||||||

| in CHF m | 1Q2003 | 4Q2002 | 1Q2002 | 1Q2003 vs 4Q2002 | ||||||||

| Developed Market Fixed Income & Foreign Exchange ERC | 3,922 | 7% | (28%) | Reduced risk-offset between CSFB and Winterthur with respect to interest rate-sensitive positions | ||||||||

| Equity Investment ERC | 3,071 | (16%) | (65%) | Mostly due to lower equity exposures at Winterthur | ||||||||

| Swiss & Retail Lending ERC | 2,057 | (2%) | (3%) | Continued write-off of aged exposures, offsetting increase in default risk due to downgrades | ||||||||

| International Lending ERC | 3,455 | (10%) | (14%) | Reduced exposures and lower US dollar exchange rate | ||||||||

| Emerging Markets ERC | 1,755 | (11%) | (29%) | Exposure reductions in Brazil and counterparty rating upgrade | ||||||||

| Real Estate ERC & Structured Asset ERC | 1) | 4,284 | 1% | (9%) | No material change | |||||||

| Insurance Underwriting ERC | 1,019 | 24% | 15% | Due to refined insurance loss distribution modelling and assumed growth in volume | ||||||||

| Simple sum across risk categories | 19,563 | (4%) | (31%) | Lower Equity and Lending ERC | ||||||||

| Diversification Benefit | (6,465) | (5%) | (39%) | In line with overall risk reduction | ||||||||

| Total position risk ERC | 13,098 | (3%) | (26%) | Lower Equity and ERC | ||||||||

99%, 1-year position risk ERC, excluding foreign exchange translation risk. For an assessment of the total risk profile, operational risk ERC and business risk ERC have to be considered as well. For a more detailed description of the Group’s ERC model, please refer to our Annual Report 2001 and 2002, which are available on our website: www.credit-suisse.com. Note that prior period risk data have been restated for methodology changes. | ||||||||||||

| 1) This category comprises the real estate investments of Winterthur, Credit Suisse First Boston’s commercial real estate exposures, Credit Suisse First Boston’s residential real estate exposures, Credit Suisse First Boston’s asset-backed securities exposures as well as the real estate acquired at auction and real estate for own use in Switzerland. | ||||||||||||

| CSFB trading exposures (1-day, 99% VaR) | |||||

| in USD m | 1Q2003 | 4Q2002 | 3Q2002 | 2Q2002 | |

| Total VaR | |||||

| Period end | 54.5 | 41.3 | 38.9 | 59.3 | |

| Average | 49.2 | 39.4 | 43.7 | 46.4 | |

| Maximum | 76.3 | 46.5 | 57.4 | 59.3 | |

| Minimum | 39.4 | 31.9 | 37.6 | 36.8 | |

| in USD m | 31.03.03 | 31.12.02 | 30.09.02 | 30.06.02 | |

| VaR by risk type | |||||

| Interest rate | 56.9 | 48.3 | 59.3 | 54.7 | |

| Foreign exchange | 15.3 | 10.8 | 7.6 | 18.7 | |

| Equity | 17.6 | 10.1 | 12.1 | 16.5 | |

| Commodity | 0.8 | 1.0 | 1.2 | 0.5 | |

| Subtotal | 90.6 | 70.2 | 80.2 | 90.4 | |

| Diversification benefit | (36.1) | (28.9) | (41.3) | (31.1) | |

| Total | 54.5 | 41.3 | 38.9 | 59.3 | |

Credit Suisse First Boston computes these VaR estimates separately for each risk type and for the whole portfolio using the historical simulation methodology. Diversification benefit reflects the net difference between the sum of the 99% percentile loss for each risk type and for the total portfolio. | |||||

| Total credit risk exposure 1) | |||||||||||||

| Credit Suisse Financial Services | Credit Suisse First Boston | Credit Suisse Group | |||||||||||

| in CHF m | 31.03.03 | 31.12.02 | 31.03.03 | 31.12.02 | 31.03.03 | 31.12.02 | |||||||

| Due from banks | 2) | 29,889 | 32,752 | 56,851 | 44,016 | 57,569 | 39,469 | ||||||

| Due from customers and mortgages | 2) | 133,372 | 132,353 | 72,941 | 82,395 | 205,030 | 213,206 | ||||||

| Total due from banks and customers, gross | 2) | 163,261 | 165,105 | 129,792 | 126,411 | 262,599 | 252,675 | ||||||

| Contingent liabilities | 12,460 | 12,349 | 28,280 | 27,862 | 39,866 | 39,104 | |||||||

| Irrevocable commitments | 2,917 | 2,263 | 80,403 | 86,599 | 84,415 | 90,048 | |||||||

| Total banking products | 178,638 | 179,717 | 238,475 | 240,872 | 386,880 | 381,827 | |||||||

| Loans held for sale | 3) | 0 | – | 18,373 | – | 18,373 | – | ||||||

| Derivative instruments | 4) | 1,957 | 2,375 | 56,230 | 54,243 | 57,016 | 54,757 | ||||||

| Securities lending – banks | 0 | 0 | 37 | 0 | 37 | 0 | |||||||

| Securities lending – customers | 0 | 0 | 30 | 64 | 30 | 64 | |||||||

| Reverse repurchase agreements – banks | 2,052 | 2,270 | 157,862 | 158,544 | 156,312 | 156,397 | |||||||

| Reverse repurchase agreements – customers | 11,989 | 13,944 | 53,399 | 57,571 | 65,081 | 71,384 | |||||||

| Total traded products | 15,998 | 18,589 | 267,558 | 270,422 | 278,476 | 282,602 | |||||||

| Total credit risk exposure, gross | 194,636 | 198,306 | 524,406 | 511,294 | 683,729 | 664,429 | |||||||

| Loan valuation allowances and provisions | (3,820) | (4,092) | (3,271) | (3,817) | (7,092) | (7,911) | |||||||

| Total credit risk exposure, net | 190,816 | 194,214 | 521,135 | 507,477 | 676,637 | 656,518 | |||||||

| 1) Credit Suisse Financial Services/Credit Suisse First Boston reflect business unit amounts. Total consolidated Credit Suisse Group amounts include adjustments and Corporate Center. | |||||||||||||

| 2) Excluding loans held for sale, securities lending and reverse repurchase transactions. | |||||||||||||

| 3) Effective 1Q2003, loans held for sale are presented net of the related loan valuation allowances. | |||||||||||||

| 4) Positive replacement values considering netting agreements. | |||||||||||||

| Total loan portfolio exposure and allowances and provisions for credit risk 1) | |||||||||||||

| Credit Suisse Financial Services | Credit Suisse First Boston | Credit Suisse Group | |||||||||||

| in CHF m | 31.03.03 | 31.12.02 | 31.03.03 | 31.12.02 | 31.03.03 | 31.12.02 | |||||||

| Non-performing loans | 2,749 | 3,004 | 2,616 | 3,351 | 5,365 | 6,355 | |||||||

| Non-interest earning loans | 1,897 | 2,108 | 402 | 217 | 2,299 | 2,325 | |||||||

| Total non-performing loans | 4,646 | 5,112 | 3,018 | 3,568 | 7,664 | 8,680 | |||||||

| Restructured loans | 80 | 52 | 201 | 229 | 281 | 281 | |||||||

| Potential problem loans | 1,726 | 1,723 | 1,123 | 1,685 | 2,848 | 3,408 | |||||||

| Total other impaired loans | 1,806 | 1,775 | 1,324 | 1,914 | 3,129 | 3,689 | |||||||

| Total impaired loans | 6,452 | 6,887 | 4,342 | 5,482 | 10,793 | 12,369 | |||||||

| Total due from banks and customers, gross | 163,261 | 165,105 | 129,792 | 126,411 | 262,599 | 252,675 | |||||||

| Valuation allowances | 3,779 | 4,053 | 3,111 | 3,647 | 6,891 | 7,703 | |||||||

| of which on principal | 3,010 | 3,201 | 2,866 | 3,416 | 5,875 | 6,617 | |||||||

| of which on interest | 769 | 852 | 245 | 231 | 1,016 | 1,086 | |||||||

| Total due from banks and customers, net | 159,482 | 161,052 | 126,681 | 122,764 | 255,708 | 244,972 | |||||||

| Provisions for contingent liabilities and irrevocable commitments | 41 | 39 | 160 | 170 | 201 | 208 | |||||||

| Total valuation allowances and provisions | 3,820 | 4,092 | 3,271 | 3,817 | 7,092 | 7,911 | |||||||

| Ratios | |||||||||||||

| Valuation allowances as % of total non-performing loans | 81.3% | 79.3% | 103.1% | 102.2% | 89.9% | 88.7% | |||||||

| Valuation allowances as % of total impaired loans | 58.6% | 58.9% | 71.6% | 66.5% | 63.8% | 62.3% | |||||||

| 1) Credit Suisse Financial Services/Credit Suisse First Boston reflect business unit amounts. Total consolidated Credit Suisse Group amounts include adjustments and the Corporate Center. | |||||||||||||

REVIEW OF BUSINESS UNITS | CREDIT SUISSE FINANCIAL SERVICES

Credit Suisse Financial Services recorded a net profit of CHF 666 million and a net operating profit, excluding the amortization of acquired intangible assets and goodwill, of CHF 690 million in the first quarter of 2003. Winterthur achieved an improved operating performance through tariff increases, a selective underwriting policy and stronger investment results. Primarily as a result of lower operating expenses, Private Banking recorded a higher segment profit than in the fourth quarter of 2002. Corporate & Retail Banking increased its segment result considerably compared to a weak fourth quarter of 2002.

Credit Suisse Financial Services recorded a net profit of CHF 666 million in the first quarter of 2003, down 6% versus the fourth quarter of 2002 and up 13% versus the corresponding period in the previous year. Fourth quarter 2002 results benefited from the one-time cumulative effect of a change in accounting principle of CHF 266 million for periods prior to 2002. Net operating profit before the amortization of acquired intangible assets and goodwill for the first quarter of 2003 amounted to CHF 690 million. The net operating profit was positively impacted by the investment income in the insurance segments, which increased by CHF 1.1 billion to CHF 1.5 billion compared to the previous quarter.

The refocusing of the European initiative on Private Banking clients is progressing well and has already led to cost improvements. With regard to the realignment of the Winterthur organization, the merger of the two Corporate Centers has been completed and the management levels have been defined in the countries in which the life and non-life businesses are being merged.

Credit Suisse Financial Services made progress towards its goal to return to profitability in 2003 but remains exposed to continued volatility in the financial markets, particularly in Life & Pensions.

Private Banking

In the first quarter of 2003, Private Banking reported a segment profit of CHF 371 million, up 10% versus the previous quarter and down 39% versus the corresponding period in the previous year. Operating income decreased 2% versus the previous quarter to CHF 1.3 billion. The decrease in operating income of 21% versus the first quarter of 2002 was mainly attributable to lower transaction volumes in the securities business due to investor passivity and the market-driven lower asset base. Operating expenses decreased 7% compared to the previous quarter and 8% versus the first quarter of 2002. The gross margin stood at 113.8 bp in the first quarter of 2003, compared with 112.4 bp in the previous quarter and 126.4 bp in the first quarter of 2002.

Net new assets amounted to CHF 1.5 billion in the first quarter of 2003, compared to CHF 0.9 billion in the previous quarter. Assets under management decreased 1.9% versus year-end 2002 to CHF 457.0 billion, due to market performance and the foreign exchange impact.

In Europe, substantial progress was achieved in the refocusing of the European initiative on private banking clients, most significantly in Germany and Spain. In onshore Europe and in Asia, Private Banking achieved above-average growth of net new assets. To protect clients’ capital and improve risk-return profiles, Private Banking launched a number of innovative products, tailored to market conditions, as an alternative to direct investments in equities or fixed income products. In the second quarter of 2003, Private Banking is introducing a new advisory concept that will focus on in-depth client asset and liability management.

Corporate & Retail Banking

Corporate & Retail Banking posted a segment profit of CHF 124 million in the first quarter of 2003, up 158% versus the previous quarter and down 15% versus the corresponding period in the previous year. Operating income rose 3% quarter-on-quarter to CHF 734 million, due primarily to increased commission and trading income, which compensated for the lower interest income. In the first quarter of 2003, the net interest margin stood at 214 bp, down from 219 bp in the previous quarter. Compared with the first quarter of 2002, operating income decreased by 7%, mainly driven by lower transaction-based commission income and the lower interest rate environment.

Operating expenses decreased 14% versus the previous quarter to CHF 473 million, partly due to seasonality. The credit-related provisions recorded were CHF 24 million below the statistical valuation adjustments. In the first quarter of 2003, total impaired loans declined by CHF 397 million to CHF 6.1 billion as of March 31, 2003. The cost/income ratio stood at 67.4% in the first quarter of 2003, compared with 80.8% in the previous quarter. The return on average allocated capital increased quarter-on-quarter from 4.0% to 10.7%.

Assets under management stood at CHF 64.1 billion at the end of the first quarter of 2003, down 8.8% versus year-end 2002. The net asset outflow of CHF 3.4 billion in the first quarter of 2003 was attributable to shifts from time deposit accounts of corporate clients to transaction accounts. These transaction accounts do not qualify as assets under management. In the first quarter of 2003, Corporate & Retail Banking, together with Private Banking, achieved good growth in the Swiss private mortgage business.

Life & Pensions

In the first quarter 2003, Life & Pensions reported a segment profit of CHF 111 million, an increase of CHF 96 million versus the corresponding period in the previous year. Compared to the fourth quarter of 2002, segment profit increased CHF 18 million or 19%. This result was primarily driven by a reduction in administration costs and a positive investment performance.

In the first quarter of 2003, Life & Pensions reported a decrease in gross premiums written of 4%, or CHF 263 million, to CHF 6.5 billion compared to the corresponding period in the previous year. Adjusted for acquisitions, divestitures and exchange rate impacts, premium volume decreased by 2%. The first quarter decline was due both to Life & Pensions’ ongoing selective underwriting and strong reported single premium growth in Italy, the UK and Belgium in the first quarter of 2002. Net new assets in the first quarter of 2003 amounted to CHF 2.2 billion, compared to CHF 3.0 billion in the first quarter of 2002, reflecting lower premium volume.

Administration costs decreased 6% to CHF 322 million, compared to the first quarter of 2002, largely due to cost reduction measures. The total expense ratio in the first quarter of 2003 stood at 6.8%, compared to 6.4% in the corresponding period of the previous year, primarily due to the reduction in premium income and higher amortization of deferred acquisition costs (DAC), in line with the development of investment income.

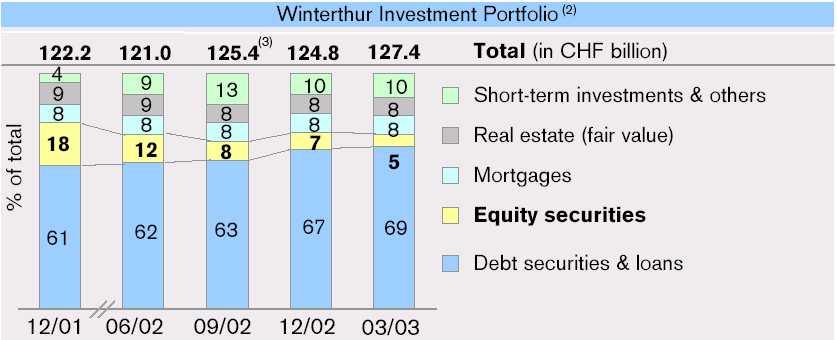

Investment income increased CHF 429 million to CHF 1.2 billion in the first quarter of 2003, compared to the corresponding period in the previous year. The increase of CHF 888 million compared to the fourth quarter of 2002 partly reflects a decrease in impairments of CHF 481 million, to CHF 268 million, recorded in the first quarter of 2003. In the reporting period, the total return on invested assets amounted to 4.9%, compared with 3.2% in the first quarter of 2002. Current income thereof was 3.9%, whereas realized gains/losses and other income/expenses were 1.1%. The proportion of investments held in equities was 5% as of March 31, 2003, compared with 8% as of December 31, 2002.

Insurance

Insurance reported a segment profit of CHF 92 million in the first quarter of 2003, an increase of CHF 239 million compared to the corresponding period of the previous year. Compared to the fourth quarter of 2002, segment profit increased CHF 86 million. The strong recovery of the Insurance result in the first quarter of 2003 is mainly driven by a significant improvement in the underwriting result due to the continued implementation of tariff increases and a strict underwriting policy, as well as improvements in investment income, compared to the first quarter of 2002. This result was partially offset by charges of CHF 63 million after-tax for the realignment of the organization and the international business portfolio.

In the first quarter of 2003, Insurance’s net premiums earned increased CHF 227 million, or 6%, to CHF 4.0 billion compared to the corresponding period in the previous year. Adjusted for acquisitions, divestitures and exchange rate impacts, the increase was 13%, primarily due to tariff increases across all major markets.

Insurance improved its net underwriting result by CHF 137 million in the first quarter of 2003 versus the corresponding period of the previous year, resulting in a decrease in the combined ratio of 3.2 percentage points to 100.7% in the first quarter of 2003, compared to 103.9% in the first quarter of 2002. This improvement resulted mainly from a decrease in the claims ratio of 4.2 percentage points to 71.0% in the first quarter of 2003 versus the corresponding period in the previous year, reflecting improved pricing and continued streamlining of the portfolio. In addition, fewer large losses resulting from natural catastrophes were reported during the quarter.

In the first quarter of 2003, administration costs decreased by 6% to CHF 472 million versus the corresponding period in the previous year. The overall expense ratio increased 1.0 percentage point to 29.7% in the first quarter of 2003, compared to the corresponding period of the previous year, due to higher policy acquisition costs mainly related to premium growth and the effect of fully integrating the book of business acquired from Prudential plc.

Insurance reported an increase in net investment income of CHF 202 million in the first quarter of 2003, to CHF 289 million, versus the corresponding period in the previous year. Compared with the fourth quarter of 2002, net investment income increased by CHF 230 million. In the first quarter of 2003, total return on invested assets amounted to 3.5%, compared with 1.2% in the first quarter of 2002. Current income was 3.9%, whereas realized gains/losses and other income/expenses were -0.5%. The proportion of investments held in equities was 5% as of March 31, 2003, compared with 7% as of December 31, 2002.

| Credit Suisse Financial Services business unit income statement 1) | |||||||||||

| Change | Change | ||||||||||

| in % from | in % from | ||||||||||

| in CHF m | 1Q2003 | 4Q2002 | 1Q2002 | 4Q2002 | 1Q2002 | ||||||

| Operating income | 2) | 3,393 | 3,517 | 3,306 | (4) | 3 | |||||

| Personnel expenses | 1,369 | 1,405 | 1,443 | (3) | (5) | ||||||

| Other operating expenses | 779 | 897 | 814 | (13) | (4) | ||||||

| Operating expenses | 2,148 | 2,302 | 2,257 | (7) | (5) | ||||||

| Gross operating profit | 1,245 | 1,215 | 1,049 | 2 | 19 | ||||||

| Depreciation of non-current assets | 168 | 256 | 162 | (34) | 4 | ||||||

| Amortization of Present Value of Future Profits (PVFP) | 52 | 62 | 43 | (16) | 21 | ||||||

| Valuation adjustments, provisions and losses | 81 | 105 | 99 | (23) | (18) | ||||||

| Net operating profit before extraordinary and exceptional items, cumulative effect of change in accounting principle and taxes | 944 | 792 | 745 | 19 | 27 | ||||||

| Extraordinary income/(expenses), net | 7 | 24 | (3) | (71) | – | ||||||

| Taxes | 3) 4) | (253) | (332) | (120) | (24) | 111 | |||||

| Net operating profit before exceptional items, cumulative effect of change in accounting principle and minority interests | 698 | 484 | 622 | 44 | 12 | ||||||

| Amortization of acquired intangible assets and goodwill | (25) | (37) | (29) | (32) | (14) | ||||||

| Exceptional items | 0 | (73) | 0 | (100) | – | ||||||

| Tax impact | 1 | 14 | 1 | (93) | – | ||||||

| Cumulative effect of change in accounting principle | 3) | – | 266 | – | – | – | |||||

| Net profit before minority interests | 674 | 654 | 594 | 3 | 13 | ||||||

| Minority interests | (8) | 51 | (2) | – | 300 | ||||||

| Net profit | 666 | 705 | 592 | (6) | 13 | ||||||

| 1) The business unit results reflect the results of the separate segments comprising the business unit. Certain acquisition-related costs, including amortization of acquired intangible assets and goodwill, exceptional items and cumulative effect of change in accounting principle not allocated to the segments are included in the business unit results. For a complete reconciliation of the business unit results to the Group’s consolidated results and a discussion of the material reconciling items, please refer to “Reconciliation of operating to consolidated results”. | |||||||||||

| 2) For the purpose of the consolidated financial statements, operating income for the insurance business is defined as net premiums earned, less claims incurred and change in technical provisions and expenses for processing claims, less commissions, plus net investment income from the insurance business. | |||||||||||

| 3) In 4Q2002, Credit Suisse Group adopted a change in accounting principle relating to the recognition of deferred tax assets on net operating losses. The retroactive application of this change in accounting principle would have resulted in taxes for 4Q2002 and 1Q2002 of CHF –649 m and CHF –86 m, respectively. | |||||||||||

| 4) Excluding tax impact on amortization of acquired intangible assets and goodwill as well as exceptional items. | |||||||||||

| Reconciliation to net operating profit | ||||||||||||

| Change | Change | |||||||||||

| in % from | in % from | |||||||||||