FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Private Issuer

Dated August 5, 2003

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the month of August 5, 2003

Commission File Number 001-15244

CREDIT SUISSE GROUP

(Translation of registrant's name into English)

Paradeplatz 8, P.O. Box 1, CH-8070 Zurich, Switzerland

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F ![]() Form 40-F

Form 40-F ![]()

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Note: Regulation S-T Rule 101(b)(1) only permits the submission in paper of a Form 6-K if submitted solely to provide an attached annual report to security holders.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Note: Regulation S-T Rule 101(b)(7) only permits the submission in paper of a Form 6-K if submitted to furnish a report or other document that the registrant foreign private issuer must furnish and make public under the laws of the jurisdiction in which the registrant is incorporated, domiciled or legally organized (the registrant's "home country"), or under the rules of the home country exchange on which the registrant's securities are traded, as long as the report or other document is not a press release, is not required to be and has not been distributed to the registrant's security holders, and, if discussing a material event, has already been the subject of a Form 6-K submission or other Commission filing on EDGAR.

Indicate by check mark whether by furnishing the information contained in this Form, the registrant is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes ![]() No

No ![]()

If "Yes" is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): 82-

|

e-mail media.relations@credit-suisse.com |

| CREDIT SUISSE GROUP DOUBLES NET PROFIT IN THE SECOND QUARTER 2003 TO CHF 1.3 BILLION AND REPORTS NET PROFIT OF CHF 2.0 BILLION FOR THE FIRST HALF 2003 |

| Both Business Units Report Significantly Improved Results |

| Financial Highlights | |||||||||

| in CHF million | 2Q2003 | 1Q2003 | Change in % | 6 months | Change in % | ||||

| vs 1Q2003 | 2003 | vs 6m 2002 | |||||||

| Operating income | 7,549 | 7,024 | 7 | 14,573 | -9 | ||||

| Operating expenses | 5,071 | 5,020 | 1 | 10,091 | -23 | ||||

| Net profit | 1,346 | 652 | 106 | 1,998 | n/a | ||||

| Return on equity in % | 18.5 | 9.2 | 101 | 13.8 | n/a | ||||

| Earnings per share (in CHF) | 1.09 | 0.53 | 106 | 1.62 | n/a | ||||

| n/a: not applicable | |||||||||

Zurich, August 5, 2003 – Credit Suisse Group today announced a net profit of CHF 1.3 billion for the second quarter of 2003 and a net profit of CHF 2.0 billion for the first half of 2003. Net profit for the second quarter of 2003 was more than double that of the first quarter of 2003. Credit Suisse First Boston achieved solid results in the second quarter of 2003, driven by strong performance in the Institutional Securities segment. At Credit Suisse Financial Services, both Private Banking and Corporate & Retail Banking increased their operating income substantially, while Winterthur’s results continued to improve in the second quarter of 2003, with reduced administration costs in both insurance segments.

|

1

Oswald J. Grübel, Co-CEO of Credit Suisse Group and Chief Executive Officer of

Credit Suisse Financial Services, stated, "The doubling of the Group’s net profit in the second quarter of 2003 demonstrates the underlying strength of our businesses. I am pleased that all segments of Credit Suisse Financial Services again reported stronger results compared with the first quarter of 2003, reflecting healthier operating income and the success of our efficiency measures."

John J. Mack, Co-CEO of Credit Suisse Group and Chief Executive Officer of Credit Suisse First Boston, said, "Credit Suisse First Boston’s results firmly underscore its top-line momentum in the second quarter of 2003 and the strength of its franchise. Although many markets remain challenging, we are both confident that the Group will continue to make progress towards its goal of achieving sound profitability in 2003.”

Group Results: Second Quarter of 2003

Credit Suisse Group reported a net profit of CHF 1.3 billion in the second quarter of 2003. The second quarter 2003 net profit increased CHF 694 million compared with the first quarter of 2003 and represents a strong improvement compared with the net loss of CHF 579 million in the second quarter of 2002. The Group’s operating income was CHF 7.5 billion in the second quarter of 2003, up 7% on the first quarter of 2003 and down slightly compared with the second quarter of 2002. The Group’s operating expenses increased 1% compared with the first quarter of 2003 to CHF 5.1 billion – mainly reflecting increased incentive compensation accruals due to improved performance – but were down 23% compared with the second quarter of 2002. The Group’s valuation adjustments, provisions and losses were CHF 131 million in the second quarter of 2003, down 44% or CHF 102 million compared with the first quarter of 2003 and down 77% or CHF 431 million compared with the second quarter of 2002, due predominantly to lower valuations, provisions and losses at Credit Suisse First Boston, reflecting an improved credit environment and recoveries. Earnings per share for the second quarter of 2003 were CHF 1.09, compared with CHF 0.53 for the first quarter of 2003. The Group’s return on equity was 18.5% in the second quarter of 2003, compared with 9.2% for the first quarter of 2003.

2

Credit Suisse Group continued to strengthen its capital base during the second quarter of 2003, due primarily to earnings generation, managed balance sheet growth and the sale of non-core businesses (Pershing). The Group’s consolidated BIS tier 1 ratio was 11.1% as of June 30, 2003, an increase from 10.0% as of March 31, 2003. In cooperation with the Swiss Federal Banking Commission, the capital treatment of the Group’s investment in Winterthur is being refined; this will have an effect on the consolidated BIS capital calculations. The capital charge for the Winterthur Group investment will no longer be reflected as an addition to risk-weighted assets but as a reduction to regulatory capital. Subsequent to final regulatory approval, the revised methodology is expected to be applied as of the period ended September 30, 2003. If this methodology was applied retroactively, the Group’s consolidated BIS tier 1 ratio would be 10.3% as of June 30, 2003, compared with 9.3% as of March 31, 2003.

Winterthur’s announced divestitures of Churchill in the UK, Winterthur Italy and Republic in the US are expected to further improve the Group’s capital base upon completion in the second half of 2003. The synthetic securitization of prime Swiss residential mortgages of approximately CHF 3.0 billion, originated by the Corporate & Retail Banking segment, is also expected to have a positive effect on the Group’s capital position in the second half of 2003.

Group Results: First Half of 2003

The Group reported a net profit of CHF 2.0 billion for the first half of 2003, compared with a net loss of CHF 211 million for the first half of 2002. The Group’s operating income was CHF 14.6 billion for the first six months of 2003, down 9% compared with the first half of 2002, while the Group’s first half 2003 operating expenses decreased 23% to CHF 10.1 billion over the same period in 2002.

3

Credit Suisse Financial Services

| CSFS Business Unit Result | |||||||||

| in CHF million | 2Q2003 | 1Q2003 | Change in % | 6 months | Change in % | ||||

| vs 1Q2003 | 2003 | vs 6m 2002 | |||||||

| Operating income | 3,435 | 3,393 | 1 | 6,828 | 13 | ||||

| Operating expenses | 2,100 | 2,148 | -2 | 4,248 | -8 | ||||

| Business unit result | 808 | 666 | 21 | 1,474 | 400 | ||||

| Net profit | 829 | 684 | 21 | 1,513 | 418 | ||||

Credit Suisse Financial Services reported improved results across all of its segments in the second quarter of 2003. The business unit recorded a net profit of CHF 829 million for the second quarter of 2003, up CHF 145 million compared with the first quarter of 2003 and up CHF 1.1 billion compared with the second quarter of 2002. Taking account of statistical rather than actual credit provisions, Credit Suisse Financial Services reported a business unit profit of CHF 808 million in the second quarter of 2003, corresponding to an increase of CHF 142 million compared with the first quarter of 2003 and of CHF 1.1 billion compared with the second quarter of 2002. Second quarter 2003 operating income of CHF 3.4 billion increased 1% compared with the first quarter of 2003 and was up 26% compared with the second quarter of 2002, while operating expenses were down 2% compared with the first quarter of 2003 and down 12% versus the second quarter of 2002.

| CSFS Segment Results | |||||||||

| in CHF million | 2Q2003 | 1Q2003 | Change in % | 6 months | Change in % | ||||

| vs 1Q2003 | 2003 | vs 6m 2002 | |||||||

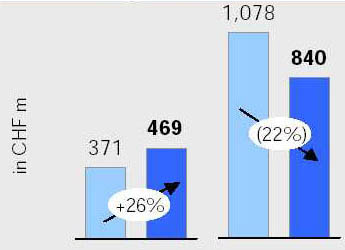

| Private Banking | 469 | 371 | 26 | 840 | -22 | ||||

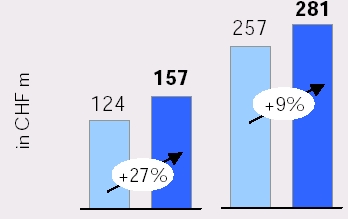

| Corporate & Retail Banking | 157 | 124 | 27 | 281 | 9 | ||||

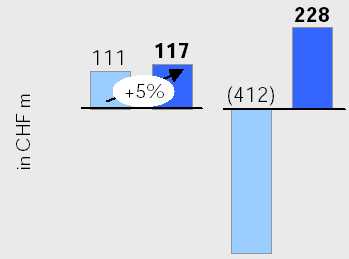

| Life & Pensions | 117 | 111 | 5 | 228 | n/a | ||||

| Insurance | 102 | 92 | 11 | 194 | n/a | ||||

4

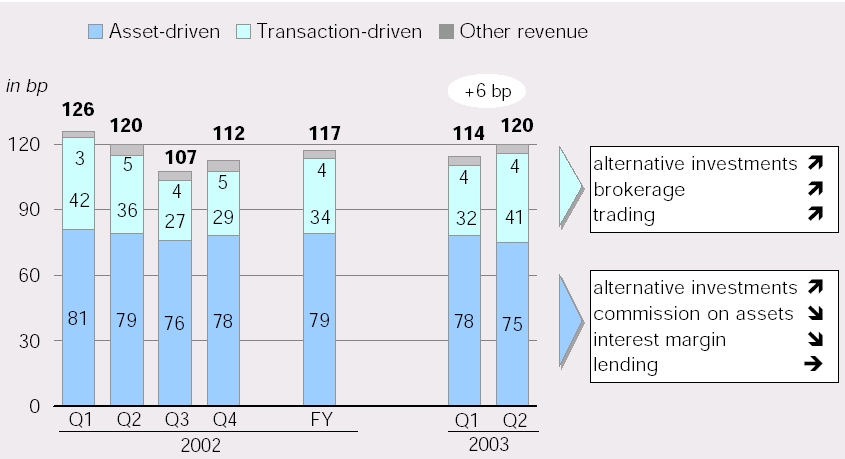

Private Banking reported a segment profit of CHF 469 million in the second quarter of 2003, up 26% compared with the first quarter of 2003 and in line with the strong second quarter of 2002. Operating income increased 9% compared with the first quarter of 2003 – driven mainly by higher transaction-based income – but declined 8% compared with the second quarter of 2002, due mainly to a lower asset base. Operating expenses increased CHF 22 million, or 3%, to CHF 793 million compared with the first quarter of 2003, as the reduction in base salary costs in line with headcount development was exceeded by higher performance-related compensation accruals and charges for headcount reductions. Compared with the second quarter of 2002, operating expenses decreased CHF 89 million, or 10%, reflecting ongoing efficiency measures. The cost/income ratio improved for the third consecutive quarter, declining 4.6 percentage points to 58.6% from the first quarter. The gross margin increased to 120.4 bp in the second quarter of 2003, compared with 113.8 bp in the first quarter of 2003 and 120.1 bp in the second quarter of 2002.

Corporate & Retail Banking reported a segment profit of CHF 157 million in the second quarter of 2003, up 27% compared with the first quarter of 2003 and up 41% compared with the second quarter of 2002. Operating income rose 7% compared with the first quarter of 2003 to CHF 784 million, due mainly to realized gains from the recovery portfolio within other ordinary income, and higher interest and trading income, but was practically unchanged compared with the second quarter of 2002. Second quarter 2003 operating expenses rose by CHF 11 million, or 2%, compared with the first quarter of 2003, to CHF 484 million, due to higher personnel expenses. A reduction in base salary costs in line with headcount development was exceeded by higher performance-related compensation accruals and charges for headcount reductions. Compared with the second quarter of 2002, operating expenses decreased CHF 68 million, or 12%, due to ongoing efficiency measures. The cost/income ratio improved further in the second quarter of 2003 to 64.8%, compared with 67.4% in the first quarter of 2003 and 72.5% in the second quarter of 2002. The return on average allocated capital increased compared with the first quarter of 2003 from 10.7% to 13.3%.

5

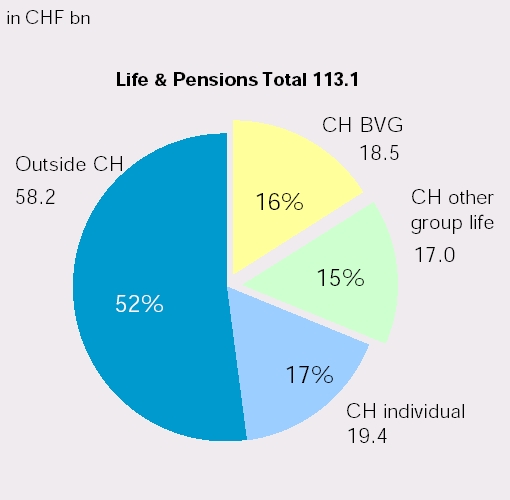

Life & Pensions reported a segment profit of CHF 228 million in the first half of 2003, compared with a segment loss of CHF 412 million in the first half of 2002. This result was driven primarily by a significant improvement in investment performance as well as a reduction in administration costs. In the second quarter of 2003, the segment profit increased by CHF 6 million, or 5%, to CHF 117 million, compared with the first quarter of 2003. In the first half of 2003, gross premiums written declined 3%, or CHF 293 million, to CHF 10.0 billion, compared with the first half of 2002. Adjusted for acquisitions, divestitures and exchange rate impacts, the volume of gross premiums written decreased 1% compared with the first half of 2002. Administration costs decreased 17% to CHF 599 million in the first half of 2003, and the expense ratio improved by 0.6 percentage points to 8.4%, compared with the first half of 2002. Investment income increased CHF 1.7 billion to CHF 2.5 billion in the first half of 2003 compared with the first half of 2002, due primarily to a significant decrease in impairments and realized losses on equity investments.

Insurance reported a segment profit of CHF 194 million in the first half of 2003, compared with a segment loss of CHF 637 million in the first half of 2002. This recovery was driven primarily by a significant improvement in the Insurance segment’s underwriting results due to the implementation of broad-based tariff increases, a continued strict underwriting policy, a significant improvement in investment performance and reduced administration costs. In the second quarter of 2003, the segment profit increased by CHF 10 million, or 11%, to CHF 102 million, compared with the first quarter of 2003. For the first half of 2003, net premiums earned rose 4% compared with the first half of 2002, to CHF 8.1 billion, and – adjusted for acquisitions, divestitures and exchange rate impacts – were up 10%. The Insurance segment reported an improvement in net investment income from a loss of CHF 179 million in the first half of 2002 to income of CHF 604 million in the first half of 2003, due primarily to a significant decrease in impairments and realized losses on equity investments.

6

Credit Suisse First Boston

| CSFB Business Unit Result | |||||||||

| in USD million | 2Q2003 | 1Q2003 | Change in % | 6 months | Change in % | ||||

| vs 1Q2003 | 2003 | vs 6m 2002 | |||||||

| Operating income | 3,187 | 2,920 | 9 | 6,107 | -10 | ||||

| Operating expenses | 2,328 | 2,169 | 7 | 4,497 | -14 | ||||

| Net profit | 296 | 161 | 84 | 457 | n/a | ||||

Credit Suisse First Boston’s results are reported and discussed below on a US dollar basis.

At Credit Suisse First Boston, increased operating income and continued cost control were the primary factors driving the improved performance compared with the first quarter of 2003. The business unit reported a net profit of USD 296 million (CHF 395 million) in the second quarter of 2003, compared with a net profit of USD 161 million (CHF 221 million) in the first quarter of 2003 and a net profit of USD 61 million (CHF 101 million) in the second quarter of 2002. Excluding the amortization of acquired intangible assets and goodwill net of tax, net operating profit increased 46% to USD 426 million (CHF 570 million) compared with the first quarter of 2003 and was up 86% compared with the second quarter of 2002. Excluding Pershing, which was sold to The Bank of New York effective May 1, 2003, net operating profit increased 55% compared with the first quarter of 2003 and 105% compared with the second quarter of 2002. Operating income increased 9% from the first quarter of 2003 to USD 3.2 billion (CHF 4.2 billion), mainly reflecting broad performance improvements across products and geographies and continued tight expense controls. Operating expenses rose 7% compared with the first quarter of 2003 – due mainly to increased incentive compensation accruals linked to improved performance – but declined 12% compared with the second quarter of 2002, reflecting headcount reductions and cost containment efforts. For the second quarter of 2003, Credit Suisse First Boston reported an 18.5% operating return on average allocated capital and an 18.3% operating pre-tax margin, compared with an operating return on average allocated capital of 12.4% and an operating pre-tax margin of 13.2% in the first quarter of 2003.

7

| CSFB Segment Results | |||||||||

| in USD million | 2Q2003 | 1Q2003 | Change in % | 6 months | Change in % | ||||

| vs 1Q2003 | 2003 | vs 6m 2002 | |||||||

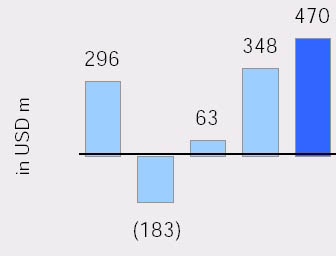

| Institutional Securities | 470 | 348 | 35 | 818 | 59 | ||||

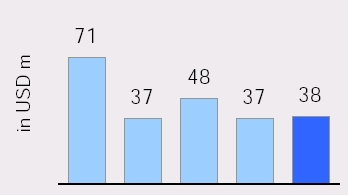

| CSFB Financial Services | 38 | 37 | 3 | 75 | -47 | ||||

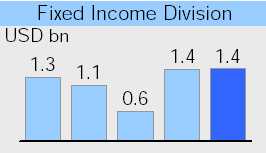

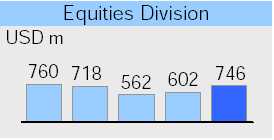

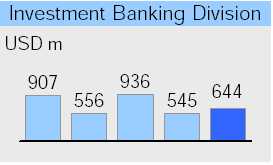

Institutional Securities reported a segment profit of USD 470 million (CHF 628 million) for the second quarter of 2003, compared with USD 348 million (CHF 476 million) in the first quarter of 2003 and USD 296 million (CHF 477 million) in the second quarter of 2002. Operating income increased 10% to USD 2.9 billion (CHF 3.8 billion) from the first quarter of 2003, with the Fixed Income division continuing to report strong results – comparable to first quarter levels – led by leveraged finance and mortgages, where Credit Suisse First Boston ranked number one in global high yield new issues and global commercial mortgage-backed securities transactions. Revenue increased compared with the first quarter of 2003 in both the Equity and Investment Banking divisions. Operating income in the second quarter of 2003 decreased 2% compared with the second quarter of 2002. Expense trends for the segment were consistent with those of Credit Suisse First Boston overall.

8

CSFB Financial Services reported a segment profit of USD 38 million (CHF 50 million) for the second quarter of 2003, up 3% compared with the first quarter of 2003 but down 46% compared with the second quarter of 2002, primarily reflecting the sale of Pershing. Operating income of USD 299 million (CHF 397 million) for the second quarter of 2003 was down 2% compared with the first quarter of 2003 and 46% compared with the second quarter of 2002. Excluding Pershing (whose 2003 net results are shown in operating income net of expenses), operating income increased 3% compared with the first quarter of 2003, due mainly to improved results at Credit Suisse Asset Management, and declined 13% compared with the second quarter of 2002, due mainly to lower results at Private Client Services. In the second quarter of 2003, operating expenses increased 5% compared with the first quarter of 2003 but were down 42% compared with the second quarter of 2002. Excluding Pershing, operating expenses in the second quarter of 2003 were down 5% compared with the second quarter of 2002.

Net New Assets

Credit Suisse Group recorded a net asset inflow of CHF 2.3 billion in the second quarter of 2003, compared with a net asset outflow of CHF 3.5 billion in the first quarter of 2003. The Group’s total assets under management were CHF 1,234.2 billion as of June 30, 2003. This corresponds to an increase of 6.4% compared with March 31, 2003, primarily reflecting the recent improvements in the markets. Credit Suisse Financial Services reported net new assets of CHF 4.8 billion in the second quarter of 2003, with net inflows of CHF 3.8 billion at Private Banking, CHF 0.5 billion at Corporate & Retail Banking and CHF 0.5 billion at Life & Pensions. Credit Suisse First Boston reported a net asset outflow of CHF 2.5 billion in the second quarter of 2003, as CHF 1.0 billion of net new assets at Institutional Securities was offset by net outflows of CHF 3.5 billion from CSFB Financial Services (CHF 1.7 billion from Credit Suisse Asset Management and CHF 1.8 billion from Private Client Services).

9

| Net New Assets and Assets under Management (AuM) in the second quarter of 2003 | |||||

| in CHF billion | Net New Assets | Total AuM | Change in AuM in | ||

| % vs 31.03.03 | |||||

| Private Banking | 3.8 | 493.8 | 8.1 | ||

| Corporate & Retail Banking | 0.5 | 66.8 | 4.2 | ||

| Life & Pensions | 0.5 | 117.0 | 4.7 | ||

| Insurance | n/a | 32.6 | 5.2 | ||

| Credit Suisse Financial Services | 4.8 | 710.2 | 7.0 | ||

| Institutional Securities | 1.0 | 31.0 | 0.6 | ||

| CSFB Financial Services | -3.5 | 493.0 | 5.8 | ||

| Credit Suisse First Boston | -2.5 | 524.0 | 5.5 | ||

| Credit Suisse Group | 2.3 | 1,234.2 | 6.4 | ||

Outlook

Given the current business environment, Credit Suisse Group expects continued sound profitability for 2003, although many of the Group’s markets remain challenging. The Group anticipates that operating income will remain strong in the banking industry – albeit with a seasonally lower third quarter in Private Banking – and expects improved technical results in the insurance segments going forward. Life & Pensions and Credit Suisse First Boston remain exposed to the volatility of the capital markets. A strong client focus, further improvements in efficiency and revenue growth remain the key priorities across the Group.

Enquiries

Credit Suisse Group, Media Relations Telephone +41 1 333 8844

Credit Suisse Group, Investor Relations Telephone +41 1 333 4570

10

Commentary on Results – Non-GAAP Financial Information

For additional information with respect to Credit Suisse Group’s results for the second quarter and first half of 2003, we refer you to the Group’s Quarterly Report Q2 2003, as well as the Group’s slide presentation for analysts and press, posted on the Internet at www.credit-suisse.com/results. This press release may contain non-GAAP financial information. A reconciliation of such non-GAAP financial information to the most directly comparable measures under Swiss Generally Accepted Accounting Principles (as well as other related information) is also included in the Quarterly Report Q2 2003. The segment results described above represent net operating profit before minority interests, excluding acquisition-related costs.

Credit Suisse Group

Credit Suisse Group is a leading global financial services company headquartered in Zurich. The business unit Credit Suisse Financial Services provides private clients and small and medium-sized companies with Private Banking and financial advisory services, banking products, and Pension and Insurance solutions from Winterthur. The business unit Credit Suisse First Boston, an Investment Bank, serves global institutional, corporate, government and individual clients in its role as a financial intermediary. Credit Suisse Group’s registered shares (CSGN) are listed in Switzerland and Frankfurt, and in the form of American Depositary Shares (CSR) in New York. The Group employs around 72,500 staff worldwide. As of June 30, 2003, it reported assets under management of CHF 1,234.2 billion.

Cautionary Statement Regarding Forward-looking Information

This press release contains statements that constitute forward-looking statements. In addition, in the future we, and others on our behalf, may make statements that constitute forward-looking statements. Such forward-looking statements may include, without limitation, statements relating to our plans, objectives or goals; our future economic performance or prospects; the potential effect on our future performance of certain contingencies; and assumptions underlying any such statements. Words such as “believes,” “anticipates,” “expects,” "intends” and “plans” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. We do not intend to update these forward-looking statements except as may be required by applicable laws. By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that predictions, forecasts, projections and other outcomes described or implied in forward-looking statements will not be achieved. We caution you that a number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in such forward-looking statements. These factors include (i) market and interest rate fluctuations; (ii) the strength of the global economy in general and the strength of the economies of the countries in which we conduct our operations in particular; (iii) the ability of counterparties to meet their obligations to us; (iv) the effects of, and changes in, fiscal, monetary, trade and tax policies, and currency fluctuations; (v) political and social developments, including war, civil unrest or terrorist activity; (vi) the possibility of foreign exchange controls, expropriation, nationalization or confiscation of assets in countries in which we conduct our operations; (vii) the ability to maintain sufficient liquidity and access capital markets; (viii) operational factors such as systems failure, human error, or the failure to properly implement procedures; (ix) actions taken by regulators with respect to our business and practices in one or more of the countries in which we conduct our operations; (x) the effects of changes in laws, regulations or accounting policies or practices; (xi) competition in geographic and business areas in which we conduct our operations; (xii) the ability to retain and recruit qualified personnel; (xiii) the ability to maintain our reputation and promote our brands; (xiv) the ability to increase market share and control expenses; (xv) technological changes; (xvi) the timely development and acceptance of our new products and services and the perceived overall value of these products and services by users; (xvii) acquisitions, including the ability to integrate successfully acquired businesses; (xviii) the adverse resolution of litigation and other contingencies; and (xix) our success at managing the risks involved in the foregoing. We caution you that the foregoing list of important factors is not exclusive; when evaluating forward-looking statements, you should carefully consider the foregoing factors and other uncertainties and events, as well as the risks identified in our most recently filed Form 20-F and reports on Form 6-K furnished to the US Securities and Exchange Commission.

Cautionary statement regarding non-GAAP financial information

This press release may contain non-GAAP financial information. A reconciliation of such non-GAAP financial information to the most directly comparable measures under generally accepted accounting principles, is posted on our website at http://www.credit-suisse.com/sec.html.

11

Today’s Presentation of the Results

| Speakers | |

| • | Oswald J. Grübel, Co-CEO of Credit Suisse Group and Chief Executive Officer of Credit Suisse Financial Services |

| • | John J. Mack, Co-CEO of Credit Suisse Group and Chief Executive Officer of Credit Suisse First Boston |

| • | Philip K. Ryan, Chief Financial Officer of Credit Suisse Group |

| • | Ulrich Körner, Chief Financial Officer of Credit Suisse Financial Services |

| • | Barbara Yastine, Chief Financial Officer of Credit Suisse First Boston |

| Analysts’ presentation, Zurich (English) | |

| • | August 5, 2003, 9.00 am CET / 7.00 am GMT / 3.00 am EST at the Credit Suisse Forum St. Peter, Zurich |

| • | Internet: |

| - | Live broadcast at www.credit-suisse.com/results | |

| - | Video playback available approximately 3 hours after the event |

| • | Telephone: |

| - | Live audio dial-in on +41 91 610 5600 (Europe), +44 866 291 4166 (UK), or +1 207 107 0611 (US), ask for “Credit Suisse Group quarterly results”; please dial in 10 minutes before the start of the presentation | |

| - | Telephone replay available approximately 1 hour after the event on | |

| +41 91 612 4330 (Europe), +44 207 866 4300 (UK) or +1 412 858 1440 (US), conference ID 090# | ||

| Media conference, Zurich (English/German) | |

| • | August 5, 2003, 11.00 am CET / 9.00 am GMT / 5.00 am EST at the Credit Suisse Forum St. Peter, Zurich |

| • | Simultaneous interpreting: German – English, English – German |

| • | Internet: |

| - | Live broadcast at www.credit-suisse.com/results | |

| - | Video playback available approximately 3 hours after the event |

| • | Telephone: | |

| - | Live audio dial-in on +41 91 610 5600 (Europe), +44 866 291 4166 (UK), or +1 207 107 0611 (US), ask for “Credit Suisse Group quarterly results”; please dial in 10 minutes before the start of the presentation | |

| - | Telephone replay available approximately 1 hour after the event on +41 91 612 4330 (Europe), +44 207 866 43 00 (UK) or +1 412 858 1440 (US), conference ID 285# (English)or 270# (German) |

12

QUARTERLY REPORT 2003 Q2

Co-CEO Credit Suisse Group

Chief Executive Officer

Credit Suisse Financial Services

Co-CEO Credit Suisse Group

Chief Executive Officer

Credit Suisse First Boston

August 2003

| Consolidated income statement | ||||||||||||||||||

| Change | Change | Change | ||||||||||||||||

| in % from | in % from | in % from | ||||||||||||||||

| 6 months | ||||||||||||||||||

| in CHF m | 2Q2003 | 1Q2003 | 2Q2002 | 1Q2003 | 2Q2002 | 2003 | 2002 | 2002 | ||||||||||

| Operating income | 7,549 | 7,024 | 7,647 | 7 | (1) | 14,573 | 15,977 | (9) | ||||||||||

| Gross operating profit | 2,478 | 2,004 | 1,079 | 24 | 130 | 4,482 | 2,911 | 54 | ||||||||||

| Net profit/(loss) | 1,346 | 652 | (579) | 106 | – | 1,998 | (211) | – | ||||||||||

| Return on equity | ||||||||||||||||||

| Change | Change | Change | ||||||||||||||||

| in % from | in % from | in % from | ||||||||||||||||

| 6 months | ||||||||||||||||||

| in % | 2Q2003 | 1Q2003 | 2Q2002 | 1Q2003 | 2Q2002 | 2003 | 2002 | 2002 | ||||||||||

| Return on equity | 18.5 | 9.2 | (6.6) | 101 | – | 13.8 | (1.2) | – | ||||||||||

| Consolidated balance sheet | ||||||||||||

| Change | Change | |||||||||||

| in % from | in % from | |||||||||||

| in CHF m | 30.06.03 | 31.03.03 | 31.12.02 | 31.03.03 | 31.12.02 | |||||||

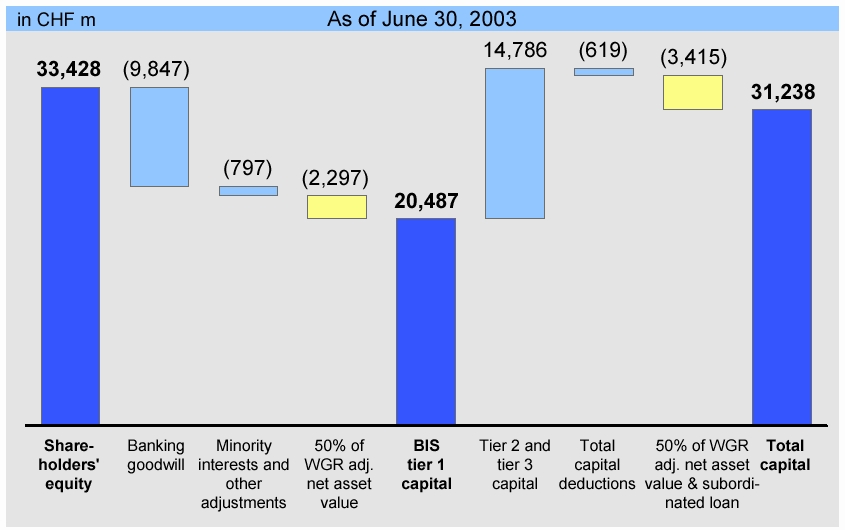

| Total assets | 1,016,645 | 992,143 | 955,656 | 2 | 6 | |||||||

| Shareholders' equity | 33,428 | 31,402 | 31,394 | 6 | 6 | |||||||

| Minority interests in shareholders' equity | 2,940 | 2,879 | 2,878 | 2 | 2 | |||||||

| Capital data | ||||||||||||

| Change | Change | |||||||||||

| in % from | in % from | |||||||||||

| in CHF m | 30.06.03 | 31.03.03 | 31.12.02 | 31.03.03 | 31.12.02 | |||||||

| BIS risk-weighted assets | 204,820 | 205,548 | 201,466 | 0 | 2 | |||||||

| BIS tier 1 capital | 22,784 | 20,517 | 19,544 | 11 | 17 | |||||||

| of which non-cumulative perpetual preferred securities | 2,167 | 2,146 | 2,162 | 1 | 0 | |||||||

| BIS total capital | 36,950 | 34,685 | 33,290 | 7 | 11 | |||||||

| Capital ratios | ||||||||

| in % | 30.06.03 | 31.03.03 | 31.12.02 | |||||

| BIS tier 1 ratio | Credit Suisse | 7.5 | 7.5 | 7.4 | ||||

| Credit Suisse First Boston 1) | 11.0 | 10.5 | 10.3 | |||||

| Credit Suisse Group 2) 3) | 11.1 | 10.0 | 9.7 | |||||

| BIS total capital ratio | Credit Suisse Group 3) | 18.0 | 16.9 | 16.5 | ||||

| Assets under management/client assets | ||||||||||||

| Change | Change | |||||||||||

| in % from | in % from | |||||||||||

| in CHF bn | 30.06.03 | 31.03.03 | 31.12.02 | 31.03.03 | 31.12.02 | |||||||

| Advisory assets under management | 628.5 | 588.5 | 605.6 | 7 | 4 | |||||||

| Discretionary assets under management | 605.7 | 572.0 | 589.7 | 6 | 3 | |||||||

| Total assets under management | 1,234.2 | 1,160.5 | 1,195.3 | 6 | 3 | |||||||

| Client assets | 1,324.6 | 1,256.7 | 1,793.2 | 5 | (26) | |||||||

| Net new assets | ||||||||||||||||||

| Change | Change | Change | ||||||||||||||||

| in % from | in % from | in % from | ||||||||||||||||

| 6 months | ||||||||||||||||||

| in CHF bn | 2Q2003 | 1Q2003 | 2Q2002 | 1Q2003 | 2Q2002 | 2003 | 2002 | 2002 | ||||||||||

| Net new assets | 2.3 | (3.5) | 4.2 | – | (45) | (1.2) | 17.7 | – | ||||||||||

| 1) Ratio is based on a tier 1 capital of CHF 11.3 bn (31.03.03: CHF 11.2 bn; 31.12.02: CHF 10.6 bn), of which non-cumulative perpetual preferred securities is CHF 1.0 bn (31.03.03: CHF 1.0 bn; 31.12.02: CHF 1.0 bn). | ||||||||||||||||||

| 2) Ratio is based on a tier 1 capital of CHF 22.8 bn (31.03.03: CHF 20.5 bn; 31.12.02: CHF 19.5 bn), of which non-cumulative perpetual preferred securities is CHF 2.2 bn (31.03.03: CHF 2.1 bn; 31.12.02: CHF 2.2 bn). | ||||||||||||||||||

| 3) In cooperation with the Swiss Federal Banking Commission, the capital treatment of the Group’s investment in Winterthur is being refined; this will have an effect on the consolidated BIS capital calculations. If this new methodology was applied retroactively, the Group’s consolidated BIS tier 1 ratio would be 10.3% (31.03.03: 9.3%; 31.12.02: 9.0%). The Group’s BIS total capital ratio would be 15.7% (31.03.03: 14.9%; 31.12.02: 14.4%). | ||||||||||||||||||

| Number of employees (full-time equivalents) | |||||||||||||

| Change | Change | ||||||||||||

| in % from | in % from | ||||||||||||

| 30.06.03 | 31.03.03 | 31.12.02 | 31.03.03 | 31.12.02 | |||||||||

| Switzerland | banking | 20,541 | 20,952 | 21,270 | (2) | (3) | |||||||

| insurance | 6,797 | 6,876 | 7,063 | (1) | (4) | ||||||||

| Outside Switzerland | banking | 20,108 | 20,726 | 25,057 | (3) | (20) | |||||||

| insurance | 25,055 | 24,817 | 25,067 | 1 | 0 | ||||||||

| Total employees Credit Suisse Group | 72,501 | 73,371 | 78,457 | (1) | (8) | ||||||||

| Share data | |||||||||||

| Change | Change | ||||||||||

| in % from | in % from | ||||||||||

| 30.06.03 | 31.03.03 | 31.12.02 | 31.03.03 | 31.12.02 | |||||||

| Shares issued | 1,189,980,152 | 1,189,891,720 | 1,189,891,720 | 0 | 0 | ||||||

| To be issued upon conversion of MCS 1) | 40,413,838 | 40,413,838 | 40,413,838 | 0 | 0 | ||||||

| Shares outstanding | 1,230,393,990 | 1,230,305,558 | 1,230,305,558 | 0 | 0 | ||||||

| Share price in CHF | 35.65 | 23.50 | 30.00 | 52 | 19 | ||||||

| Market capitalization in CHF m | 43,864 | 28,912 | 36,909 | 52 | 19 | ||||||

| Book value per share in CHF | 24.78 | 23.18 | 23.18 | 7 | 7 | ||||||

| 1) Maximum number of shares related to Mandatory Convertible Securities (MCS) issued by Credit Suisse Group Finance (Guernsey) Ltd. in December 2002. | |||||||||||

| Share price | |||||||||||||||||

| Change | Change | Change | |||||||||||||||

| in % from | in % from | in % from | |||||||||||||||

| 6 months | |||||||||||||||||

| in CHF | 2Q2003 | 1Q2003 | 2Q2002 | 1Q2003 | 2Q2002 | 2003 | 2002 | 2002 | |||||||||

| High (closing price) | 39.30 | 34.45 | 63.50 | 14 | (38) | 39.30 | 73.60 | (47) | |||||||||

| Low (closing price) | 23.25 | 20.70 | 41.65 | 12 | (44) | 20.70 | 41.65 | (50) | |||||||||

| Calculation of earnings per share (EPS) | |||||||||||||||||

| Change | Change | Change | |||||||||||||||

| in % from | in % from | in % from | |||||||||||||||

| 6 months | |||||||||||||||||

| 2Q2003 | 1Q2003 | 2Q2002 | 1Q2003 | 2Q2002 | 2003 | 2002 | 2002 | ||||||||||

| Net profit/(loss) in CHF m | 1,346 | 652 | (579) | 106 | – | 1,998 | (211) | – | |||||||||

| Diluted net profit/(loss) in CHF m | 1,346 | 652 | (579) | 106 | – | 1,998 | (211) | – | |||||||||

| Weighted average shares outstanding | 1,230,330,673 | 1,230,305,558 | 1,189,243,577 | 1) | 0 | 3 | 1,230,318,185 | 1,189,147,860 | 1) | 3 | |||||||

| Dilutive impact 2) | 4,922,814 | 2,015,114 | 0 | 144 | – | 2,258,634 | 0 | – | |||||||||

| Weighted average shares, diluted | 1,235,253,487 | 1,232,320,672 | 1,189,243,577 | 0 | 4 | 1,232,576,819 | 1,189,147,860 | 4 | |||||||||

| Basic earnings per share in CHF | 1.09 | 0.53 | (0.49) | 106 | – | 1.62 | (0.18) | – | |||||||||

| Diluted earnings per share in CHF | 1.09 | 0.53 | (0.49) | 106 | – | 1.62 | (0.18) | – | |||||||||

| 1) Adjusted for weighted average shares repurchased. | |||||||||||||||||

| 2) The calculation for the diluted loss per share in 2Q2002 and for the 6 months 2002 excludes the effect of the potential exchange of convertible bonds and the potential exercise of options to purchase shares, as the effect would be anti-dilutive. | |||||||||||||||||

Equity capital

Net new assets

Operating income and expenses

Valuation adjustments, provisions and losses

Stock-based compensation

Outlook

| Overview of Credit Suisse Group 1) | |||||||||||||||||||||||||

| Credit Suisse Financial Services | Credit Suisse First Boston | Corporate Center | Credit Suisse Group | ||||||||||||||||||||||

| in CHF m | 2Q2003 | 1Q2003 | 2Q2002 | 2Q2003 | 1Q2003 | 2Q2002 | 2Q2003 | 1Q2003 | 2Q2002 | 2Q2003 | 1Q2003 | 2Q2002 | |||||||||||||

| Operating income | 3,435 | 3,451 | 2,655 | 3,996 | 3,752 | 5,276 | 118 | (179) | (284) | 7,549 | 7,024 | 7,647 | |||||||||||||

| Personnel expenses | 1,394 | 1,369 | 1,474 | 2,348 | 2,232 | 3,362 | 82 | 38 | (20) | 3,824 | 3,639 | 4,816 | |||||||||||||

| Other operating expenses | 706 | 779 | 909 | 652 | 667 | 883 | (111) | (65) | (40) | 1,247 | 1,381 | 1,752 | |||||||||||||

| Operating expenses | 2,100 | 2,148 | 2,383 | 3,000 | 2,899 | 4,245 | (29) | (27) | (60) | 5,071 | 5,020 | 6,568 | |||||||||||||

| Gross operating profit | 1,335 | 1,303 | 272 | 996 | 853 | 1,031 | 147 | (152) | (224) | 2,478 | 2,004 | 1,079 | |||||||||||||

| Depreciation of non-current assets 2) | 192 | 220 | 217 | 138 | 130 | 185 | 145 | 70 | 64 | 475 | 420 | 466 | |||||||||||||

| Amortization of acquired intangible assets and goodwill | 27 | 25 | 46 | 201 | 206 | 330 | (5) | 1 | (2) | 223 | 232 | 374 | |||||||||||||

| Valuation adjustments, provisions and losses | 63 | 57 | 103 | 63 | 176 | 420 | 5 | 0 | 39 | 131 | 233 | 562 | |||||||||||||

| Profit/(loss) before extraordinary items and taxes | 1,053 | 1,001 | (94) | 594 | 341 | 96 | 2 | (223) | (325) | 1,649 | 1,119 | (323) | |||||||||||||

| Extraordinary income/(expenses), net | 8 | (51) | 84 | 0 | 0 | 26 | 53 | 2 | 0 | 61 | (49) | 110 | |||||||||||||

| Taxes 3) | (222) | (258) | (378) | (180) | (101) | 0 | 83 | (19) | (39) | (319) | (378) | (417) | |||||||||||||

| Net profit/(loss) before minority interests | 839 | 692 | (388) | 414 | 240 | 122 | 138 | (240) | (364) | 1,391 | 692 | (630) | |||||||||||||

| Minority interests | (10) | (8) | 85 | (19) | (19) | (21) | (16) | (13) | (13) | (45) | (40) | 51 | |||||||||||||

| Net profit/(loss) | 829 | 684 | (303) | 395 | 221 | 101 | 122 | (253) | (377) | 1,346 | 652 | (579) | |||||||||||||

| 1) Business unit results in accordance with Swiss GAAP. For a reconciliation of operating basis business unit results (reflecting the results of the separate segments comprising the business units) to Swiss GAAP basis, please refer to “Reconciliation of operating results to Swiss GAAP”. | |||||||||||||||||||||||||

| 2) Includes amortization of Present Value of Future Profits (PVFP) from the insurance business within Credit Suisse Financial Services. | |||||||||||||||||||||||||

| 3) In 4Q2002, Credit Suisse Group adopted a change in accounting principle relating to the recognition of deferred tax assets on net operating losses. The retroactive application of this change in accounting principle would have resulted in taxes for 2Q2002 for Credit Suisse Financial Services of CHF –196 m, for Credit Suisse First Boston of CHF 192 m, and for Credit Suisse Group of CHF –41 m. | |||||||||||||||||||||||||

| Assets under management/client assets | |||||||||||

| Change | Change | ||||||||||

| in % from | in % from | ||||||||||

| in CHF bn | 30.06.03 | 31.03.03 | 31.12.02 | 31.03.03 | 31.12.02 | ||||||

| Credit Suisse Financial Services | |||||||||||

| Private Banking 1) | |||||||||||

| Assets under management | 493.8 | 457.0 | 465.7 | 8.1 | 6.0 | ||||||

| of which discretionary | 128.3 | 118.2 | 121.5 | 8.5 | 5.6 | ||||||

| Client assets | 522.3 | 486.3 | 494.8 | 7.4 | 5.6 | ||||||

| Corporate & Retail Banking 1) | &nbs p; | ||||||||||

| Assets under management | 66.8 | 64.1 | 70.3 | 4.2 | (5.0) | ||||||

| Client assets | 85.0 | 82.6 | 86.3 | 2.9 | (1.5) | ||||||

| Life & Pensions | |||||||||||

| Assets under management (discretionary) | 117.0 | 111.7 | 110.8 | 4.7 | 5.6 | ||||||

| Client assets | 117.0 | 111.7 | 110.8 | 4.7 | 5.6 | ||||||

| Insurance | |||||||||||

| Assets under management (discretionary) | 32.6 | 31.0 | 30.7 | 5.2 | 6.2 | ||||||

| Client assets | 32.6 | 31.0 | 30.7 | 5.2 | 6.2 | ||||||

| Credit Suisse Financial Services | |||||||||||

| Assets under management | 710.2 | 663.8 | 677.5 | 7.0 | 4.8 | ||||||

| of which discretionary 1) | 279.1 | 262.1 | 264.2 | 6.5 | 5 .6 | ||||||

| Client assets | 756.9 | 711.6 | 722.6 | 6.4 | 4.7 | ||||||

| Credit Suisse First Boston | |||||||||||

| Institutional Securities | |||||||||||

| Assets under management | 31.0 | 30.8 | 31.3 | 0.6 | (1.0) | ||||||

| of which Private Equity on behalf of clients (discretionary) | 20.6 | 20.8 | 20.9 | (1.0) | (1.4) | ||||||

| Client assets | 74.7 | 79.2 | 83.9 | (5.7) | (11.0) | ||||||

| CSFB Financial Services | |||||||||||

| Assets under management | 493.0 | 465.9 | 486.5 | 5.8 | 1.3 | ||||||

| of which discretionary | 299.9 | 281.9 | 297.2 | 6.4 | 0.9 | ||||||

| Client assets | 493.0 | 465.9 | 986.7 | 5.8 | (50.0) | ||||||

| Credit Suisse First Boston | |||||||||||

| Assets under management | 524.0 | 496.7 | 517.8 | 5.5 | 1.2 | ||||||

| of which discretionary | 326.6 | 309.9 | 325.5 | 5.4 | 0.3 | ||||||

| Client assets | 567.7 | 545.1 | 1,070.6 | 4.1 | (47.0) | ||||||

| Credit Suisse Group | |||||||||||

| Assets under management | 1,234.2 | 1,160.5 | 1,195.3 | 6.4 | 3.3 | ||||||

| of which discretionary 1) | 605.7 | 572.0 | 589.7 | 5.9 | 2 .7 | ||||||

| Client assets | 1,324.6 | 1,256.7 | 1,793.2 | 5.4 | (26.1) | ||||||

| 1) 2002 comparative figures have been restated to reflect the realignment of the private client business as of 01.01.2003. This entailed moving certain client segments in Switzerland from Private Banking to Corporate & Retail Banking as well as re-evaluating the balances of 2002 discretionary assets. | |||||||||||

| Net new assets | ||||||||||||||||||

| Change | Change | Change | ||||||||||||||||

| in % from | in % from | in % from | ||||||||||||||||

| 6 months | ||||||||||||||||||

| in CHF bn | 2Q2003 | 1Q2003 | 2Q2002 | 1Q2003 | 2Q2002 | 2003 | 2002 | 2002 | ||||||||||

| Credit Suisse Financial Services | ||||||||||||||||||

| Private Banking 1) | 3.8 | 1.5 | 5.6 | 153.3 | (32.1) | 5.3 | 14.8 | (64.2) | ||||||||||

| Corporate & Retail Banking 1) | 0.5 | (3.4) | 0.3 | – | 66.7 | (2.9) | (1.1) | 163.6 | ||||||||||

| Life & Pensions | 0.5 | 2.2 | 1.3 | (77.3) | (61.5) | 2.7 | 4.3 | (37.2) | ||||||||||

| Credit Suisse Financial Services | 4.8 | 0.3 | 7.2 | – | (33.3) | 5.1 | 18.0 | (71.7) | ||||||||||

| Credit Suisse First Boston | ||||||||||||||||||

| Institutional Securities | 1.0 | (0.1) | 1.4 | – | (28.6) | 0.9 | 4.9 | (81.6) | ||||||||||

| CSFB Financial Services | (3.5) | (3.7) | (4.4) | (5.4) | (20.5) | (7.2) | (5.2) | 38.5 | ||||||||||

| Credit Suisse First Boston | (2.5) | (3.8) | (3.0) | (34.2) | (16.7) | (6.3) | (0.3) | – | ||||||||||

| Credit Suisse Group | 2.3 | (3.5) | 4.2 | – | (45.2) | (1.2) | 17.7 | – | ||||||||||

| 1) 2002 comparative figures have been restated to reflect the realignment of the private client business as of 01.01.2003. This entailed moving certain client segments in Switzerland from Private Banking to Corporate & Retail Banking. | ||||||||||||||||||

Economic Risk Capital

Overall risk trends

CSFB trading risks

Credit risk exposure

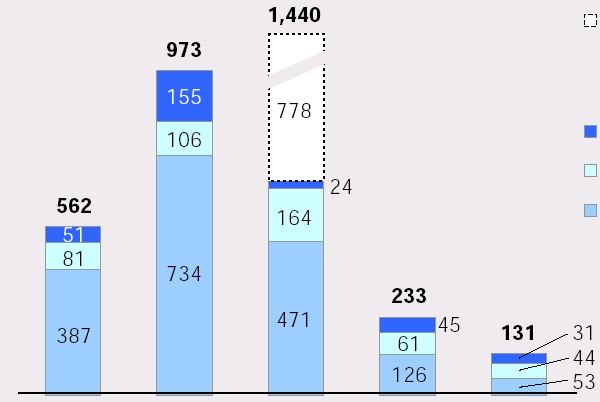

| Key Position Risk Trends | ||||||||

| Change Analysis: Brief Summary | ||||||||

| Change in % from | ||||||||

| in CHF m | 2Q2003 | 1Q2003 | 2Q2002 | 2Q2003 vs 1Q2003 | ||||

| Real Estate ERC & | ||||||||

| Structured Asset ERC 1) | 4,149 | (5%) | (1%) | Lower commercial and residential real estate exposures at CSFB due to securitizations and loan sales as well as lower asset-backed-securities exposures at CSFB following restructurings and pay downs. | ||||

| Developed Market Fixed Income & | ||||||||

| Foreign Exchange ERC | 4,068 | 26% | 1% | Higher foreign exchange exposures at Winterthur and higher credit spread exposures at CSFB. | ||||

| Equity Investment ERC | 3,252 | (4%) | (51%) | Lower traded equity and private equity exposures at CSFB as well as lower equity investment risk at the Corporate Center f ollowing the disposal of the remaining Swiss Life position, partially offset by higher equity position at Winterthur. | ||||

| International Lending ERC | 3,118 | (10%) | (13%) | Reduced lending and counterparty risk at CSFB due to lower exposures, loan sales and counterparty rating upgrades, pa rtially offset by higher credit risk profile associated with Winterthur’s bond portfolio. | ||||

| Swiss & Retail Lending ERC | 1,949 | (5%) | (6%) | Lower lending risk at the CSFS banking and insurance segments | ||||

| Emerging Markets ERC | 1,628 | (7%) | (35%) | Lower Brazil, Venezuela, Russia and South Africa exposures at CSFB. | ||||

| Insurance Underwriting ERC | 1,045 | 3% | 26% | Due to higher Euro exchange rate (no material risk change on a local currency basis). | ||||

| Simple sum across risk categories | 19,209 | |||||||

| Diversification benefit | (7,062) | |||||||

| Total position risk ERC | 12,147 | (3%) | (20%) | |||||

99%, 1-year position risk ERC, excluding foreign exchange translation risk. For an assessment of the total risk profile, operational risk ERC and business risk ERC have to be considered as well. Note that prior period risk data have been restated for methodology changes in order to maintain consistency over time. For a more detailed description of the Group’s ERC model, please refer to Credit Suisse Group's Annual Report 2001 and 2002, which are available on the website: www.credit-suisse.com. | ||||||||

| 1) This category comprises the real estate investments of Winterthur, Credit Suisse First Boston’s commercial real estate exposures, Credit Suisse First Boston’s residential real estate exposures, Credit Suisse First Boston’s asset-backed securities exposures as well as the real estate acquired at auction and real estate for own use in Switzerland. | ||||||||

| CSFB trading exposures (1-day, 99% VaR) | |||||||

| in USD m | 2Q2003 | 1Q2003 | 2Q2002 | ||||

| Total VaR | |||||||

| Period end | 75.6 | 54.5 | 59.3 | ||||

| Average | 64.3 | 49.2 | 46.4 | ||||

| Maximum | 107.9 | 76.3 | 59.3 | ||||

| Minimum | 47.5 | 39.4 | 36.8 | ||||

| in USD m | 30.06.03 | 31.03.03 | 31.12.02 | ||||

| VaR by risk type | |||||||

| Interest rate | 87.2 | 56.9 | 54.7 | ||||

| Foreign exchange | 10.9 | 15.3 | 18.7 | ||||

| Equity | 19.0 | 17.6 | 16.5 | ||||

| Commodity | 0.6 | 0.8 | 0.5 | ||||

| Subtotal | 117.7 | 90.6 | 90.4 | ||||

| Diversification benefit | (42.1) | (36.1) | (31.1) | ||||

| Total | 75.6 | 54.5 | 59.3 | ||||

Credit Suisse First Boston computes these VaR estimates separately for each risk type and for the whole portfolio using the historical simulation methodology. Diversification benefit reflects the net difference between the sum of the 99% percentile loss for each risk type and for the total portfolio. | |||||||

| Total credit risk exposure 1) | |||||||||||||||||||

| Credit Suisse Financial Services | Credit Suisse First Boston | Credit Suisse Group | |||||||||||||||||

| in CHF m | 30.06.03 | 31.03.03 | 31.12.02 | 30.06.03 | 31.03.03 | 31.12.02 | 30.06.03 | 31.03.03 | 31.12.02 | ||||||||||

| Due from banks 2) | 32,482 | 29,889 | 32,752 | 68,037 | 56,851 | 44,016 | 68,939 | 57,569 | 39,469 | ||||||||||

| Due from customers and mortgages 2) | 136,180 | 133,372 | 132,353 | 83,880 | 72,941 | 82,395 | 219,270 | 205,030 | 213,206 | ||||||||||

| Total due from banks and customers, gross 2) | 168,662 | 163,261 | 165,105 | 151,917 | 129,792 | 126,411 | 288,209 | 262,599 | 252,675 | ||||||||||

| Contingent liabilities | 12,330 | 12,460 | 12,349 | 29,586 | 28,280 | 27,862 | 41,056 | 39,866 | 39,104 | ||||||||||

| Irrevocable commitments 3) | 3,670 | 2,917 | 2,263 | 80,773 | 76,281 | 81,884 | 85,036 | 80,293 | 85,333 | ||||||||||

| Total banking products | 184,662 | 178,638 | 179,717 | 262,276 | 234,353 | 236,157 | 414,301 | 382,758 | 377,112 | ||||||||||

| Loans held for sale 4) | 0 | 0 | – | 16,338 | 18,373 | – | 16,338 | 18,373 | – | ||||||||||

| Derivative instruments 5) | 2,390 | 1,957 | 2,375 | 58,478 | 56,230 | 54,243 | 59,618 | 57,016 | 54,757 | ||||||||||

| Securities lending – banks | 0 | 0 | 0 | 0 | 37 | 0 | 0 | 37 | 0 | ||||||||||

| Securities lending – customers | 0 | 0 | 0 | 69 | 30 | 64 | 69 | 30 | 64 | ||||||||||

| Reverse repurchase agreements – banks | 2,311 | 2,052 | 2,270 | 148,620 | 157,862 | 158,544 | 146,443 | 156,312 | 156,397 | ||||||||||

| Reverse repurchase agreements – customers | 8,084 | 11,989 | 13,944 | 52,734 | 53,399 | 57,571 | 60,536 | 65,081 | 71,384 | ||||||||||

| Forward reverse repurchase agreements | 0 | 0 | 0 | 13,855 | 12,262 | 7,617 | 13,855 | 12,262 | 7,617 | ||||||||||

| Total traded products | 12,785 | 15,998 | 18,589 | 273,756 | 279,820 | 278,039 | 280,521 | 290,738 | 290,219 | ||||||||||

| Total credit risk exposure, gross | 197,447 | 194,636 | 198,306 | 552,370 | 532,546 | 514,196 | 711,160 | 691,869 | 667,331 | ||||||||||

| Loan valuation allowances and provisions | (3,480) | (3,820) | (4,092) | (3,053) | (3,271) | (3,817) | (6,532) | (7,092) | (7,911) | ||||||||||

| Total credit risk exposure, net | 193,967 | 190,816 | 194,214 | 549,317 | 529,275 | 510,379 | 704,628 | 684,777 | 659,420 | ||||||||||

| 1) Credit Suisse Financial Services/Credit Suisse First Boston reflect business unit amounts. Total consolidated Credit Suisse Group amounts include adjustments and Corporate Center. | |||||||||||||||||||

| 2) Excluding loans held for sale, securities lending and reverse repurchase transactions. | |||||||||||||||||||

| 3) Excluding forward reverse repurchase agreements. Prior periods restated. | |||||||||||||||||||

| 4) Effective 1Q2003, loans held for sale are presented net of the related loan valuation allowances. | |||||||||||||||||||

| 5) Positive replacement values considering netting agreements. | |||||||||||||||||||

| Total loan portfolio exposure and allowances and provisions for credit risk 1) | |||||||||||||||||||

| Credit Suisse Financial Services | Credit Suisse First Boston | Credit Suisse Group | |||||||||||||||||

| in CHF m | 30.06.03 | 31.03.03 | 31.12.02 | 30.06.03 | 31.03.03 | 31.12.02 | 30.06.03 | 31.03.03 | 31.12.02 | ||||||||||

| Non-performing loans | 2,600 | 2,749 | 3,004 | 1,926 | 2,616 | 3,351 | 4,526 | 5,365 | 6,355 | ||||||||||

| Non-interest earning loans | 1,706 | 1,897 | 2,108 | 437 | 402 | 217 | 2,143 | 2,299 | 2,325 | ||||||||||

| Total non-performing loans | 4,306 | 4,646 | 5,112 | 2,363 | 3,018 | 3,568 | 6,669 | 7,664 | 8,680 | ||||||||||

| Restructured loans | 63 | 80 | 52 | 198 | 201 | 229 | 261 | 281 | 281 | ||||||||||

| Potential problem loans | 1,599 | 1,726 | 1,723 | 965 | 1,123 | 1,685 | 2,565 | 2,848 | 3,408 | ||||||||||

| Total other impaired loans | 1,662 | 1,806 | 1,775 | 1,163 | 1,324 | 1,914 | 2,826 | 3,129 | 3,689 | ||||||||||

| Total impaired loans | 5,968 | 6,452 | 6,887 | 3,526 | 4,342 | 5,482 | 9,495 | 10,793 | 12,369 | ||||||||||

| Total due from banks and customers, gross | 168,662 | 163,261 | 165,105 | 151,917 | 129,792 | 126,411 | 288,209 | 262,599 | 252,675 | ||||||||||

| Valuation allowances | 3,446 | 3,779 | 4,053 | 2,928 | 3,111 | 3,647 | 6,373 | 6,891 | 7,703 | ||||||||||

| of which on principal | 2,749 | 3,010 | 3,201 | 2,692 | 2,866 | 3,416 | 5,441 | 5,875 | 6,617 | ||||||||||

| of which on interest | 697 | 769 | 852 | 236 | 245 | 231 | 932 | 1,016 | 1,086 | ||||||||||

| Total due from banks and customers, net | 165,216 | 159,482 | 161,052 | 148,989 | 126,681 | 122,764 | 281,836 | 255,708 | 244,972 | ||||||||||

| Provisions for contingent liabilities and irrevocable commitments | 34 | 41 | 39 | 125 | 160 | 170 | 159 | 201 | 208 | ||||||||||

| Total valuation allowances and provisions | 3,480 | 3,820 | 4,092 | 3,053 | 3,271 | 3,817 | 6,532 | 7,092 | 7,911 | ||||||||||

| Ratios | |||||||||||||||||||

| Valuation allowances as % of total non-performing loans | 80.0% | 81.3% | 79.3% | 123.9% | 103.1% | 102.2% | 95.6% | 89.9% | 88.7% | ||||||||||

| Valuation allowances as % of total impaired loans | 57.7% | 58.6% | 58.9% | 83.0% | 71.6% | 66.5% | 67.1% | 63.8% | 62.3% | ||||||||||

| 1) Credit Suisse Financial Services/Credit Suisse First Boston reflect business unit amounts. Total consolidated Credit Suisse Group amounts include adjustments and Corporate Center. | |||||||||||||||||||

Private Banking

Corporate & Retail Banking

Life & Pensions

Insurance

| Credit Suisse Financial Services business unit income statement – operating 1) | |||||||||||||||||

| Change | Change | Change | |||||||||||||||

| in % from | in % from | in % from | |||||||||||||||

| 6 months | |||||||||||||||||

| in CHF m | 2Q2003 | 1Q2003 | 2Q2002 | 1Q2003 | 2Q2002 | 2003 | 2002 | 2002 | |||||||||

| Operating income 2) | 3,435 | 3,393 | 2,718 | 1 | 26 | 6,828 | 6,024 | 13 | |||||||||

| Personnel expenses | 1,394 | 1,369 | 1,474 | 2 | (5) | 2,763 | 2,917 | (5) | |||||||||

| Other operating expenses | 706 | 779 | 909 | (9) | (22) | 1,485 | 1,723 | (14) | |||||||||

| Operating expenses | 2,100 | 2,148 | 2,383 | (2) | (12) | 4,248 | 4,640 | (8) | |||||||||

| Gross operating profit | 1,335 | 1,245 | 335 | 7 | 299 | 2,580 | 1,384 | 86 | |||||||||

| Depreciation of non-current assets | 154 | 168 | 174 | (8) | (11) | 322 | 336 | (4) | |||||||||

| Amortization of Present Value of Future Profits (PVFP) | 38 | 52 | 43 | (27) | (12) | 90 | 86 | 5 | |||||||||

| Valuation adjustments, provisions and losses | 90 | 81 | 95 | 11 | (5) | 171 | 194 | (12) | |||||||||

| Net operating profit before extraordinary items, acquisition-related costs and taxes | 1,053 | 944 | 23 | 12 | – | 1,997 | 768 | 160 | |||||||||

| Extraordinary income/(expenses), net | 8 | 7 | 21 | 14 | (62) | 15 | 18 | (17) | |||||||||

| Taxes 3) 4) | (216) | (253) | (380) | (15) | (43) | (469) | (500) | (6) | |||||||||

| Net operating profit/(loss) before acquisition-related costs and minority interests | 845 | 698 | (336) | 21 | – | 1,543 | 286 | 440 | |||||||||

| Amortization of acquired intangible assets and goodwill | (27) | (25) | (46) | 8 | (41) | (52) | (75) | (31) | |||||||||

| Tax impact | 0 | 1 | 0 | (100) | – | 1 | 1 | 0 | |||||||||

| Business unit result before minority interests | 818 | 674 | (382) | 21 | – | 1,492 | 212 | – | |||||||||

| Minority interests | (10) | (8) | 85 | 25 | – | (18) | 83 | – | |||||||||

| Business unit result 5) | 808 | 666 | (297) | 21 | – | 1,474 | 295 | 400 | |||||||||

| Increased/(decreased) credit-related valuation adjustments, net of tax 6) | (21) | (18) | 6 | 17 | – | (39) | 3 | – | |||||||||

| Net profit/(loss) | 829 | 684 | (303) | 21 | – | 1,513 | 292 | 418 | |||||||||

| Reconciliation to net operating profit/(loss) | |||||||||||||||||

| Business unit result | 808 | 666 | (297) | 21 | – | 1,474 | 295 | 400 | |||||||||

| Amortization of acquired intangible assets and goodwill, net of tax | (27) | (24) | (26) | 7) | 13 | 4 | (51) | (54) | 7) | (6) | |||||||

| Net operating profit/(loss) | 835 | 690 | (271) | 21 | – | 1,525 | 349 | 337 | |||||||||

| 1) The operating basis business unit results reflect the results of the separate segments comprising the business unit. Certain acquisition-related costs, including amortization of acquired intangible assets and goodwill, not allocated to the segments are included in the business unit results. Certain other items, including credit-related valuation adjustments resulting from the difference between the statistical and actual credit provisions and gains/losses from sales of investments within the insurance business are presented in the operating basis business unit results based on the Group’s segment reporting principles. For a reconciliation and a discussion of the material reconciling items, please refer to “Reconciliation of operating results to Swiss GAAP”. | |||||||||||||||||

| 2) For the purpose of the consolidated financial statements, operating income for the insurance business is defined as net premiums earned, less claims incurred and change in technical provisions and expenses for processing claims, less commissions, plus net investment income from the insurance business. | |||||||||||||||||

| 3) In 4Q2002, Credit Suisse Group adopted a change in accounting principle relating to the recognition of deferred tax assets on net operating losses. The retroactive application of this change in accounting principle would have resulted in taxes for 2Q2002 and for the 6 months 2002 of CHF –196 m and CHF –282 m, respectively. | |||||||||||||||||

| 4) Excluding tax impact on amortization of acquired intangible assets and goodwill. | |||||||||||||||||

| 5) Represents net profit/(loss) excluding credit-related valuation adjustments resulting from the difference between the statistical and actual credit provisions, net of tax. | |||||||||||||||||

| 6) Increased/(decreased) credit-related valuation adjustments before tax of CHF –27 m, CHF –24 m, CHF 8 m, CHF –51 m and CHF 4 m for 2Q2003, 1Q2003, 2Q2002, 6 months 2003 and 6 months 2002, respectively. | |||||||||||||||||

| 7) Excluding a CHF 20 m write-off relating to a participation. | |||||||||||||||||

| Credit Suisse Financial Services business unit key information | |||||||||||

| 6 months | |||||||||||

| 2Q2003 | 1Q2003 | 2Q2002 | 2003 | 2002 | |||||||

| Cost/income ratio 1) | 66.7% | 68.6% | 97.9% | 67.7% | 84.9% | ||||||

| Cost/income ratio – operating 2) 3) | 65.6% | 68.3% | 94.1% | 66.9% | 82.6% | ||||||

| Cost/income ratio – operating, banking 2) | 60.8% | 64.7% | 64.5% | 62.7% | 60.6% | ||||||

| Return on average allocated capital 1) | 26.0% | 22.4% | (12.9%) | 24.0% | 3.4% | ||||||

| Return on average allocated capital – operating 2) | 26.2% | 22.6% | (11.9%) | 24.2% | 4.4% | ||||||

| Average allocated capital in CHF m | 12,898 | 12,369 | 12,016 | 12,761 | 12,157 | ||||||

| Growth in assets under management | 7.0% | (2.0%) | (5.7%) | 4.8% | (4.7%) | ||||||

| of which net new assets | 0.7% | 0.0% | 1.0% | 0.8% | 2.4% | ||||||

| of which market movement and structural effects | 6.3% | (2.1%) | (6.7%) | 4.1% | (6.7%) | ||||||

| of which acquisitions/(divestitures) | (0.1%) | – | – | (0.1%) | (0.4%) | ||||||

| of which discretionary | 2.6% | (0.3%) | (1.5%) | 2.2% | (0.7%) | ||||||

| 30.06.03 | 31.03.03 | 31.12.02 | |||||||||

| Assets under management in CHF bn | 710.2 | 663.8 | 677.5 | ||||||||

| Number of employees (full-time equivalents) | 52,490 | 52,871 | 53,755 | ||||||||

| 1) Based on the business unit results on a Swiss GAAP basis. | |||||||||||

| 2) Based on the operating basis business unit results, which exclude certain acquisition-related costs not allocated to the segments and reflect certain reclassifications discussed in the “Reconciliation of operating results to Swiss GAAP”. | |||||||||||

| 3) Excluding amortization of PVFP from the insurance business within Credit Suisse Financial Services. | |||||||||||

| Overview of business unit Credit Suisse Financial Services – operating 1) | |||||||||||

| Credit | |||||||||||

| Corporate | Suisse | ||||||||||

| Private | & Retail | Life & | Financial | ||||||||

| 2Q2003, in CHF m | Banking | Banking | Pensions | Insurance | Services | ||||||

| Operating income 2) | 1,429 | 784 | 513 | 709 | 3,435 | ||||||

| Personnel expenses | 546 | 313 | 180 | 355 | 1,394 | ||||||

| Other operating expenses | 247 | 171 | 123 | 165 | 706 | ||||||

| Operating expenses | 793 | 484 | 303 | 520 | 2,100 | ||||||

| Gross operating profit | 636 | 300 | 210 | 189 | 1,335 | ||||||

| Depreciation of non-current assets | 45 | 24 | 34 | 51 | 154 | ||||||

| Amortization of Present Value of Future Profits (PVFP) | – | – | 36 | 2 | 38 | ||||||

| Valuation adjustments, provisions and losses | 19 | 71 | – | – | 90 | ||||||

| Net operating profit before extraordinary items, acquisition-related costs and taxes | 572 | 205 | 140 | 136 | 1,053 | ||||||

| Extraordinary income/(expenses), net | 7 | 1 | 0 | 0 | 8 | ||||||

| Taxes 3) | (110) | (49) | (23) | (34) | (216) | ||||||

| Net operating profit before acquisition-related costs and minority interests | 469 | 157 | 117 | 102 | 845 | ||||||

| Amortization of acquired intangible assets and goodwill | (27) | ||||||||||

| Business unit result before minority interests | 818 | ||||||||||

| Minority interests | (10) | ||||||||||

| Business unit result 4) | 808 | ||||||||||

| Other data: | |||||||||||

| Average allocated capital 5) | 2,349 | 4,721 | 5,828 | 12,898 | |||||||

| 1) The operating basis business unit results reflect the results of the separate segments comprising the business unit. Certain acquisition-related costs, including amortization of acquired intangible assets and goodwill, not allocated to the segments are included in the business unit results. Certain other items, including credit-related valuation adjustments resulting from the difference between the statistical and actual credit provisions and gains/losses from sales of investments within the insurance business are presented in the operating basis business unit results based on the Group’s segment reporting principles. For a reconciliation and a discussion of the material reconciling items, please refer to “Reconciliation of operating results to Swiss GAAP”. | |||||||||||

| 2) Operating income for the insurance business is defined as net premiums earned, less claims incurred and change in technical provisions and expenses for processing claims, less commissions, plus net investment income from the insurance business. | |||||||||||

| 3) Excluding tax impact on amortization of acquired intangible assets and goodwill. | |||||||||||

| 4) Represents net profit excluding credit-related valuation adjustments resulting from the difference between the statistical and actual credit provisions. | |||||||||||

| 5) Amount relating to Life & Pensions and Insurance segments represents the average shareholders' equity of “Winterthur” Swiss Insurance Company. | |||||||||||

| Private Banking income statement 1) | |||||||||||||||||

| Change | Change | Change | |||||||||||||||

| in % from | in % from | in % from | |||||||||||||||

| 6 months | |||||||||||||||||

| in CHF m | 2Q2003 | 1Q2003 | 2Q2002 | 1Q2003 | 2Q2002 | 2003 | 2002 | 2002 | |||||||||

| Net interest income | 301 | 310 | 322 | (3) | (7) | 611 | 648 | (6) | |||||||||

| Net commission and service fee income | 968 | 889 | 1,056 | 9 | (8) | 1,857 | 2,239 | (17) | |||||||||

| Net trading income | 151 | 102 | 142 | 48 | 6 | 253 | 287 | (12) | |||||||||

| Other ordinary income | 9 | 9 | 26 | 0 | (65) | 18 | 32 | (44) | |||||||||

| Operating income | 1,429 | 1,310 | 1,546 | 9 | (8) | 2,739 | 3,206 | (15) | |||||||||

| Personnel expenses | 546 | 515 | 561 | 6 | (3) | 1,061 | 1,114 | (5) | |||||||||

| Other operating expenses | 247 | 256 | 321 | (4) | (23) | 503 | 604 | (17) | |||||||||

| Operating expenses | 793 | 771 | 882 | 3 | (10) | 1,564 | 1,718 | (9) | |||||||||

| Gross operating profit | 636 | 539 | 664 | 18 | (4) | 1,175 | 1,488 | (21) | |||||||||

| Depreciation of non-current assets | 45 | 57 | 52 | (21) | (13) | 102 | 101 | 1 | |||||||||

| Valuation adjustments, provisions and losses 2) | 19 | 4 | 23 | 375 | (17) | 23 | 34 | (32) | |||||||||

| Net operating profit before extraordinary items and taxes | 572 | 478 | 589 | 20 | (3) | 1,050 | 1,353 | (22) | |||||||||

| Extraordinary income/(expenses), net | 7 | 7 | 21 | 0 | (67) | 14 | 19 | (26) | |||||||||

| Taxes 3) | (110) | (114) | (140) | (4) | (21) | (224) | (294) | (24) | |||||||||

| Net operating profit before minority interests (segment result) | 469 | 371 | 470 | 26 | 0 | 840 | 1,078 | (22) | |||||||||

| Other data: | |||||||||||||||||

| Increased/(decreased) credit-related valuation adjustments 2) | (7) | 0 | (9) | – | (22) | (7) | (7) | 0 | |||||||||

| 1) 2002 comparative figures have been restated to reflect the realignment of the private client business as of 01.01.2003. This entailed moving certain client segments in Switzerland from Private Banking to Corporate & Retail Banking. Certain acquisition-related costs, including amortization of acquired intangible assets and goodwill not allocated to the segments are included in the business unit results. | |||||||||||||||||

| 2) Increased/(decreased) credit-related valuation adjustments resulting from the difference between the statistical and actual credit provisions. | |||||||||||||||||

| 3) In 4Q2002, Credit Suisse Group adopted a change in accounting principle relating to the recognition of deferred tax assets on net operating losses. The retroactive application of this change in accounting principle would have resulted in taxes for 2Q2002 and for the 6 months 2002 of CHF –131 m and CHF –271 m, respectively. | |||||||||||||||||

| Private Banking balance sheet information 1) | |||||||||||

| Change | Change | ||||||||||

| in % from | in % from | ||||||||||

| in CHF m | 30.06.03 | 31.03.03 | 31.12.02 | 31.03.03 | 31.12.02 | ||||||

| Total assets | 158,982 | 152,910 | 155,363 | 4 | 2 | ||||||

| Due from customers | 31,948 | 33,493 | 35,580 | (5) | (10) | ||||||

| Mortgages | 24,527 | 23,603 | 22,935 | 4 | 7 | ||||||

| 1) 2002 comparative figures have been restated to reflect the realignment of the private client business as of 01.01.2003. This entailed moving certain client segments in Switzerland from Private Banking to Corporate & Retail Banking. | |||||||||||

| Private Banking key information 1) | |||||||||||

| 6 months | |||||||||||

| 2Q2003 | 1Q2003 | 2Q2002 | 2003 | 2002 | |||||||

| Cost/income ratio 2) | 58.6% | 63.2% | 60.4% | 60.8% | 56.7% | ||||||

| Average allocated capital in CHF m | 2,349 | 2,261 | 2,434 | 2,304 | 2,381 | ||||||

| Pre-tax margin 2) | 40.5% | 37.0% | 39.5% | 38.8% | 42.8% | ||||||

| Fee income/operating income | 67.7% | 67.9% | 68.3% | 67.8% | 69.8% | ||||||

| Net new assets in CHF bn | 3.8 | 1.5 | 5.6 | 5.3 | 14.8 | ||||||

| Growth in assets under management | 8.1% | (1.9%) | (7.3%) | 6.0% | (5.1%) | ||||||

| of which net new assets | 0.8% | 0.3% | 1.1% | 1.1% | 2.8% | ||||||

| of which market movement and structural effects | 7.2% | (2.2%) | (8.3%) | 4.9% | (8.0%) | ||||||

| Net margin 3) | 39.5 bp | 32.2 bp | 36.5 bp | 35.9 bp | 41.5 bp | ||||||

| Gross margin 4) | 120.4 bp | 113.8 bp | 120.1 bp | 117.2 bp | 123.3 bp | ||||||

| 30.06.03 | 31.03.03 | 31.12.02 | |||||||||

| Assets under management in CHF bn | 493.8 | 457.0 | 465.7 | ||||||||

| Number of employees (full-time equivalents) | 11,964 | 12,249 | 12,587 | ||||||||

| 1) 2002 comparative figures have been restated to reflect the realignment of the private client business as of 01.01.2003. This entailed moving certain client segments in Switzerland from Private Banking to Corporate & Retail Banking. | |||||||||||

| 2) Based on the segment results, which exclude certain acquisition-related costs not allocated to the segment. | |||||||||||

| 3) Net operating profit before minority interests (segment result)/average assets under management. | |||||||||||

| 4) Operating income/average assets under management. | |||||||||||

| Corporate & Retail Banking income statement 1) | |||||||||||||||||

| Change | Change | Change | |||||||||||||||

| in % from | in % from | in % from | |||||||||||||||

| 6 months | |||||||||||||||||

| in CHF m | 2Q2003 | 1Q2003 | 2Q2002 | 1Q2003 | 2Q2002 | 2003 | 2002 | 2002 | |||||||||

| Net interest income | 515 | 502 | 520 | 3 | (1) | 1,017 | 1,060 | (4) | |||||||||

| Net commission and service fee income | 147 | 149 | 168 | (1) | (13) | 296 | 340 | (13) | |||||||||

| Net trading income | 76 | 69 | 82 | 10 | (7) | 145 | 145 | 0 | |||||||||

| Other ordinary income | 46 | 14 | 23 | 229 | 100 | 60 | 38 | 58 | |||||||||

| Operating income | 784 | 734 | 793 | 7 | (1) | 1,518 | 1,583 | (4) | |||||||||

| Personnel expenses | 313 | 300 | 312 | 4 | 0 | 613 | 606 | 1 | |||||||||

| Other operating expenses | 171 | 173 | 240 | (1) | (29) | 344 | 434 | (21) | |||||||||

| Operating expenses | 484 | 473 | 552 | 2 | (12) | 957 | 1,040 | (8) | |||||||||

| Gross operating profit | 300 | 261 | 241 | 15 | 24 | 561 | 543 | 3 | |||||||||

| Depreciation of non-current assets | 24 | 22 | 23 | 9 | 4 | 46 | 45 | 2 | |||||||||

| Valuation adjustments, provisions and losses 2) | 71 | 77 | 72 | (8) | (1) | 148 | 160 | (8) | |||||||||

| Net operating profit before extraordinary items and taxes | 205 | 162 | 146 | 27 | 40 | 367 | 338 | 9 | |||||||||

| Extraordinary income/(expenses), net | 1 | 0 | 0 | – | – | 1 | (1) | – | |||||||||

| Taxes 3) | (49) | (38) | (35) | 29 | 40 | (87) | (80) | 9 | |||||||||

| Net operating profit before minority interests (segment result) | 157 | 124 | 111 | 27 | 41 | 281 | 257 | 9 | |||||||||

| Other data: | |||||||||||||||||

| Increased/(decreased) credit-related valuation adjustments 2) | (20) | (24) | 17 | (17) | – | (44) | 11 | – | |||||||||

| 1) 2002 comparative figures have been restated to reflect the realignment of the private client business as of 01.01.2003. This entailed moving certain client segments in Switzerland from Private Banking to Corporate & Retail Banking. Certain acquisition-related costs, including amortization of acquired intangible assets and goodwill, not allocated to the segments are included in the business unit results. | |||||||||||||||||

| 2) Increased/(decreased) credit-related valuation adjustments resulting from the difference between the statistical and actual credit provisions. | |||||||||||||||||

| 3) In 4Q2002, Credit Suisse Group adopted a change in accounting principle relating to the recognition of deferred tax assets on net operating losses. The retroactive application of this change in accounting principle would not have had an impact on the taxes reported for 2Q2002 and for the 6 months 2002. | |||||||||||||||||

| Corporate & Retail Banking balance sheet information 1) | |||||||||||

| Change | Change | ||||||||||

| in % from | in % from | ||||||||||

| in CHF m | 30.06.03 | 31.03.03 | 31.12.02 | 31.03.03 | 31.12.02 | ||||||

| Total assets | 93,624 | 93,104 | 94,203 | 1 | (1) | ||||||

| Due from customers | 26,004 | 26,952 | 27,179 | (4) | (4) | ||||||

| Mortgages | 58,616 | 57,927 | 57,165 | 1 | 3 | ||||||

| Due to customers in savings and investment deposits | 27,848 | 27,830 | 27,081 | 0 | 3 | ||||||

| Due to customers, other | 27,749 | 27,561 | 27,509 | 1 | 1 | ||||||

| 1) 2002 comparative figures have been restated to reflect the realignment of the private client business as of 01.01.2003. This entailed moving certain client segments in Switzerland from Private Banking to Corporate & Retail Banking. | |||||||||||

| Corporate & Retail Banking key information 1) | |||||||||||

| 6 months | |||||||||||

| 2Q2003 | 1Q2003 | 2Q2002 | 2003 | 2002 | |||||||

| Cost/income ratio 2) | 64.8% | 67.4% | 72.5% | 66.1% | 68.5% | ||||||

| Return on average allocated capital 2) | 13.3% | 10.7% | 8.4% | 11.9% | 10.0% | ||||||

| Average allocated capital in CHF m | 4,721 | 4,656 | 5,265 | 4,710 | 5,139 | ||||||

| Pre-tax margin 2) | 26.3% | 22.1% | 18.4% | 24.2% | 21.3% | ||||||

| Personnel expenses/operating income | 39.9% | 40.9% | 39.3% | 40.4% | 38.3% | ||||||

| Net interest margin | 221 bp | 214 bp | 224 bp | 217 bp | 227 bp | ||||||

| Loan growth | (0.3%) | 0.6% | (0.9%) | 0.3% | 1.4% | ||||||

| Net new assets in CHF bn | 0.5 | (3.4) | 0.3 | (2.9) | (1.1) | ||||||

| 30.06.03 | 31.03.03 | 31.12.02 | |||||||||

| Deposit/loan ratio | 65.7% | 65.3% | 64.7% | ||||||||

| Assets under management in CHF bn | 66.8 | 64.1 | 70.3 | ||||||||

| Number of employees (full-time equivalents) | 8,674 | 8,929 | 9,038 | ||||||||

| Number of branches | 221 | 221 | 223 | ||||||||

| 1) 2002 comparative figures have been restated to reflect the realignment of the private client business as of 01.01.2003. This entailed moving certain client segments in Switzerland from Private Banking to Corporate & Retail Banking. | |||||||||||

| 2) Based on the segment results, which exclude certain acquisition-related costs not allocated to the segment. | |||||||||||

| Life & Pensions income statement 1) | |||||||||||||||||

| Change | Change | Change | |||||||||||||||

| in % from | in % from | in % from | |||||||||||||||

| 6 months | |||||||||||||||||

| in CHF m | 2Q2003 | 1Q2003 | 2Q2002 | 1Q2003 | 2Q2002 | 2003 | 2002 | 2002 | |||||||||

| Gross premiums written | 3,466 | 6,499 | 3,496 | (47) | (1) | 9,965 | 10,258 | (3) | |||||||||

| Reinsurance ceded | (13) | (23) | (101) | (43) | (87) | (36) | (197) | (82) | |||||||||

| Net premiums written | 3,453 | 6,476 | 3,395 | (47) | 2 | 9,929 | 10,061 | (1) | |||||||||

| Change in provision for unearned premiums | 0 | (10) | (2) | (100) | (100) | (10) | (41) | (76) | |||||||||

| Net premiums earned | 3,453 | 6,466 | 3,393 | (47) | 2 | 9,919 | 10,020 | (1) | |||||||||

| Death and other benefits incurred | (2,870) | (4,100) | (2,834) | (30) | 1 | (6,970) | (6,647) | 5 | |||||||||

| Change in provision for future policyholder benefits (technical) | (1,098) | (2,871) | (1,071) | (62) | 3 | (3,969) | (4,360) | (9) | |||||||||

| Change in provision for future policyholder benefits (separate account) 2) | (916) | 211 | 687 | – | – | (705) | 546 | – | |||||||||

| Dividends to policyholders incurred | (202) | (24) | 678 | – | – | (226) | 813 | – | |||||||||

| Policy acquisition costs (including change in DAC/PVFP) | (120) | (120) | (118) | – | 2 | (240) | (198) | 21 | |||||||||

| Administration costs | (277) | (322) | (377) | (14) | (27) | (599) | (721) | (17) | |||||||||

| Investment income general account | 1,296 | 1,221 | 4 | 6 | – | 2,517 | 796 | 216 | |||||||||

| Investment income separate account 2) | 916 | (211) | (687) | – | – | 705 | (546) | – | |||||||||

| Interest received and paid | (14) | (19) | 4 | (26) | – | (33) | (23) | 43 | |||||||||

| Interest on bonuses credited to policyholders | (53) | (33) | (47) | 61 | 13 | (86) | (76) | 13 | |||||||||

| Other income/(expenses) | 25 | (13) | 87 | – | (71) | 12 | 93 | (87) | |||||||||

| Net operating profit/(loss) before taxes | 140 | 185 | (281) | (24) | – | 325 | (303) | – | |||||||||

| Taxes 3) | (23) | (74) | (146) | (69) | (84) | (97) | (109) | (11) | |||||||||

| Net operating profit/(loss) before minority interests (segment result) | 117 | 111 | (427) | 5 | – | 228 | (412) | – | |||||||||

| 1) The presentation of segment results differs from the presentation of the Group's consolidated results as it reflects the way the insurance business is managed, which is in line with peers in the insurance industry. Certain acquisition-related costs, including amortization of acquired intangible assets and goodwill not allocated to the segments are included in the business unit results. | |||||||||||||||||

| 2) This represents the market impact for separate account (or unit-linked) business, where the investment risk is borne by the policyholder. | |||||||||||||||||

| 3) In 4Q2002, Credit Suisse Group adopted a change in accounting principle relating to the recognition of deferred tax assets on net operating losses. The retroactive application of this change in accounting principle would have resulted in taxes for 2Q2002 and for the 6 months 2002 of CHF –8 m and CHF 55 m, respectively. | |||||||||||||||||

| Life & Pensions key information | |||||||||||

| 6 months | |||||||||||

| 2Q2003 | 1Q2003 | 2Q2002 | 2003 | 2002 | |||||||

| Expense ratio 1) | 11.5% | 6.8% | 14.2% | 8.4% | 9.0% | ||||||

| Growth in gross premiums written | (0.9%) | (3.9%) | 9.7% | (2.9%) | 9.4% | ||||||

| Return on invested assets (excluding separate account business) | |||||||||||

| Current income | 4.2% | 3.9% | 4.5% | 4.0% | 4.2% | ||||||

| Realized gains/losses and other income/expenses | 0.9% | 1.1% | (4.4%) | 1.0% | (2.5%) | ||||||

| Total return on invested assets 2) | 5.1% | 4.9% | 0.1% | 5.0% | 1.7% | ||||||

| Net new assets in CHF bn 3) | 0.5 | 2.2 | 1.3 | 2.7 | 4.3 | ||||||

| Total sales in CHF m 4) | 4,164 | 7,372 | 4,484 | 11,536 | 12,267 | ||||||

| 30.06.03 | 31.03.03 | 31.12.02 | |||||||||

| Assets under management in CHF bn 5) | 117.0 | 111.7 | 110.8 | ||||||||

| Technical provisions in CHF m | 113,059 | 108,490 | 105,939 | ||||||||

| Number of employees (full-time equivalents) | 7,519 | 7,629 | 7,815 | ||||||||

| 1) Operating expenses (i.e. policy acquisition costs and administration costs)/gross premiums written. Previous periods restated to reflect change in calculation. | |||||||||||