FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Private Issuer

Dated February 25, 2003

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the month of February 25, 2003

Commission File Number 001-15244

CREDIT SUISSE GROUP

(Translation of registrant's name into English)

Paradeplatz 8, P.O. Box 1, CH-8070 Zurich, Switzerland

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F.

Form 20-F ![]() Form 40-F

Form 40-F ![]()

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Note: Regulation S-T Rule 101(b)(1) only permits the submission in paper of a Form 6-K if submitted solely to provide an attached annual report to security holders.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Note: Regulation S-T Rule 101(b)(7) only permits the submission in paper of a Form 6-K if submitted to furnish a report or other document that the registrant foreign private issuer must furnish and make public under the laws of the jurisdiction in which the registrant is incorporated, domiciled or legally organized (the registrant's "home country"), or under the rules of the home country exchange on which the registrant's securities are traded, as long as the report or other document is not a press release, is not required to be and has not been distributed to the registrant's security holders, and, if discussing a material event, has already been the subject of a Form 6-K submission or other Commission filing on EDGAR.

Indicate by check mark whether by furnishing the information contained in this Form, the registrant is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes ![]() No

No ![]()

If "Yes" is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): 82-

|

e-mail media.relations@csg.ch |

| CREDIT SUISSE GROUP ANNOUNCES RESULTS FOR FOURTH QUARTER AND FULL YEAR 2002 |  |

| Reports Net Loss of CHF 950 Million for the | |

| Fourth Quarter And Net Loss of CHF 3.3 Billion for the Full Year 2002 | |

| Reports Progress in Implementation of Key Measures | |

| To Restore Profitability in 2003 | |

Zurich, February 25, 2003 – Credit Suisse Group today announced a net loss of CHF 950 million for the fourth quarter and a net loss of CHF 3.3 billion for the full year 2002, in line with the Group’s preliminary outlook announced on January 21, 2003. Fourth quarter 2002 results were influenced by the continuing financial market weakness, a number of exceptional items and a change in accounting principles to allow for the recognition of deferred tax assets. Winterthur’s results recovered in the fourth quarter 2002. Private Banking reported CHF 18.7 billion in net new assets for the full year 2002. Credit Suisse First Boston continued to achieve significant cost reductions, while maintaining strong market positions in its key businesses. Credit Suisse Group is entering 2003 with a stronger balance sheet and an improved capital base. The Group's Board of Directors will propose a dividend of CHF 0.10 per share to the Annual General Meeting on April 25, 2003. |

Oswald J. Grübel, Co-CEO of Credit Suisse Group and Chief Executive Officer of Credit Suisse Financial Services, stated, "We have made significant progress in implementing key measures announced in the third quarter to restore the Group's core earnings strength. At Credit Suisse Financial Services, we continued to realign the European initiative to focus on private banking clients, thus generating considerable savings in terms of infrastructure, IT and personnel expenses. At Winterthur, results recovered due to a satisfactory operating performance and the positive impact of a change in accounting principles, and we are actively pursuing initiatives to reduce costs and withdraw from markets and businesses with unsatisfactory results in order to position us for a return to profitability in 2003."

John J. Mack, Co-CEO of Credit Suisse Group and Chief Executive Officer of Credit Suisse First Boston, said, "At Credit Suisse First Boston, we continued progress on cost reduction efforts in the fourth quarter, achieving a 14% decrease in operating expenses compared to the previous quarter and, at the same time, improved our global market rankings for 2002 in key businesses. In the fourth quarter, we also initiated a further cost reduction program to reduce annual operating expenses by an additional USD 500 million and accelerated the disposal of legacy asset portfolios that were hindering our financial performance and flexibility. In addition, we made substantial progress in resolving key regulatory issues facing Credit Suisse First Boston. As we move forward in 2003, we remain intensively focused on returning to profitability."

Fourth Quarter 2002 Group Results

Credit Suisse Group’s results for the fourth quarter of 2002 were influenced by the continuing financial market weakness, a number of exceptional items and a change in accounting

principles to allow for the recognition of deferred tax assets. For the quarter, the Group reported a net loss of CHF 950 million, compared with a net loss of CHF 2.1 billion in the third quarter 2002 and a net loss of CHF 830 million in the fourth quarter of 2001. The Group’s operating income stood at CHF 6.4 billion in the fourth quarter 2002, up 13% on the previous quarter but down 22% on the fourth quarter of 2001. Including restructuring charges presented as exceptional items at the business units, the Group’s operating expenses decreased 5% versus the third quarter to CHF 5.1 billion, and were down 26% on the fourth quarter 2001.

Full Year 2002 Group Results

For the full year 2002, the Group reported a net loss of CHF 3.3 billion, compared with a net profit of CHF 1.6 billion for the previous year. The Group’s operating income stood at CHF 28.0 billion for 2002, down 28% on the previous year. The Group’s full year operating expenses declined 22% versus 2001 to CHF 23.5 billion, primarily as a result of job reductions, a significant decrease in bonuses and the sale of non-core businesses. Earnings per share for 2002 amounted to a loss of CHF 2.78 versus a profit of CHF 1.33 for 2001, and the Group’s return on equity was -10.0%, versus 4.1% in 2001.

Exceptional Items and Recognition of Deferred Tax Assets On

Net Operating Losses in the Fourth Quarter 2002

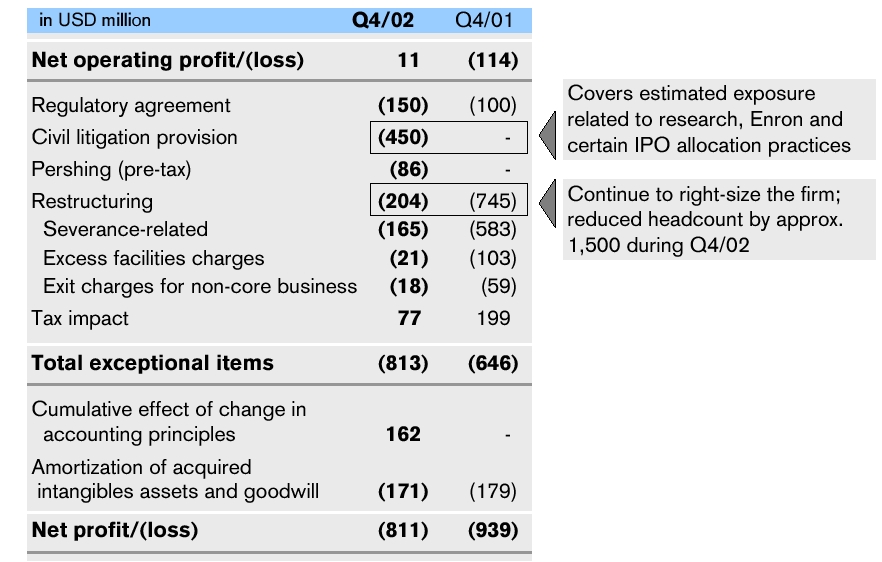

Exceptional items recorded in the fourth quarter at Credit Suisse First Boston included a pre-tax charge of USD 450 million (CHF 702 million) for private litigation involving research analyst independence, certain IPO allocation practices, Enron and other related litigation; a pre-tax charge of USD 150 million (CHF 234 million) for the agreement in principle with various US regulators involving

research analyst independence and the allocation of IPO shares to executive officers; an after-tax loss of USD 250 million (CHF 390 million) in connection with the sale of Pershing; and a pre-tax restructuring charge of USD 204 million (CHF 319 million) in connection with its USD 500 million cost reduction program. At Credit Suisse Financial Services, exceptional items of CHF 73 million were recorded in the fourth quarter in connection with the focusing of the European initiative on private banking clients. Exceptional items for the Group in the fourth quarter 2002 totaled CHF 1.5 billion before tax and CHF 1.3 billion after tax.

The previously announced change in the Group’s accounting principles to allow for the recognition of deferred tax assets with respect to net operating losses, which is reflected in the fourth quarter, resulted in a positive cumulative effect for the Group of CHF 520 million from prior years and CHF 1.3 billion for the financial year 2002.

Business Unit Results

The Credit Suisse Financial Services business unit reported a net profit of CHF 705 million in the fourth quarter and a net loss of CHF 165 million for the full year 2002. This compared with a net loss of CHF 1.2 billion in the third quarter 2002 and a net profit of CHF 3.6 billion for 2001. Fourth quarter net profit benefited from the recognition of deferred tax assets on net operating losses as a result of the change in accounting principles in the amount of CHF 472 million for the financial year 2002, as well as the cumulative effect of CHF 266 million from prior years, primarily at Winterthur. Credit Suisse Financial Services reported a 54% increase in operating income to CHF 3.5 billion versus the third quarter, reflecting a CHF 1.2 billion increase in operating income in the insurance business and stable operating income in banking. Fourth

quarter operating expenses remained stable quarter-on-quarter and year-on-year despite expansion in certain markets.

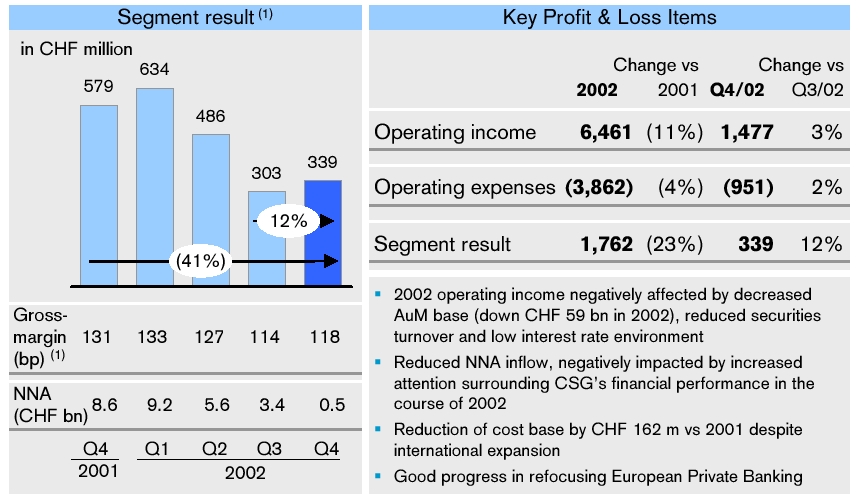

Private Banking reported a segment profit (net operating profit before the above-mentioned exceptional items, the cumulative effect of a change in accounting principles and minority interests) of CHF 339 million in the fourth quarter 2002, up 12% versus the third quarter. Operating income rose 3% quarter-on-quarter but remained below the average of the previous quarters due to investor inactivity and a reduced asset base. Fourth quarter operating expenses increased 2% quarter-on-quarter, due mainly to project costs. For the full year 2002, Private Banking reported a segment profit of CHF 1.8 billion, down 23% versus the previous year.

Corporate & Retail Banking posted a segment profit (net operating profit before the cumulative effect of a change in accounting principles and minority interests) of CHF 46 million in the fourth quarter 2002, down 55% compared to the third quarter. Operating income declined 7% quarter-on-quarter, due, in particular, to a decrease in transaction-related commission income. Fourth quarter operating expenses rose 8% versus the third quarter, mainly as a result of project costs. For the full year 2002, Corporate & Retail Banking recorded a 19% increase in its segment profit, to CHF 363 million, versus 2001. The cost/income ratio was 68.7% in 2002, compared with 71.1% in 2001.

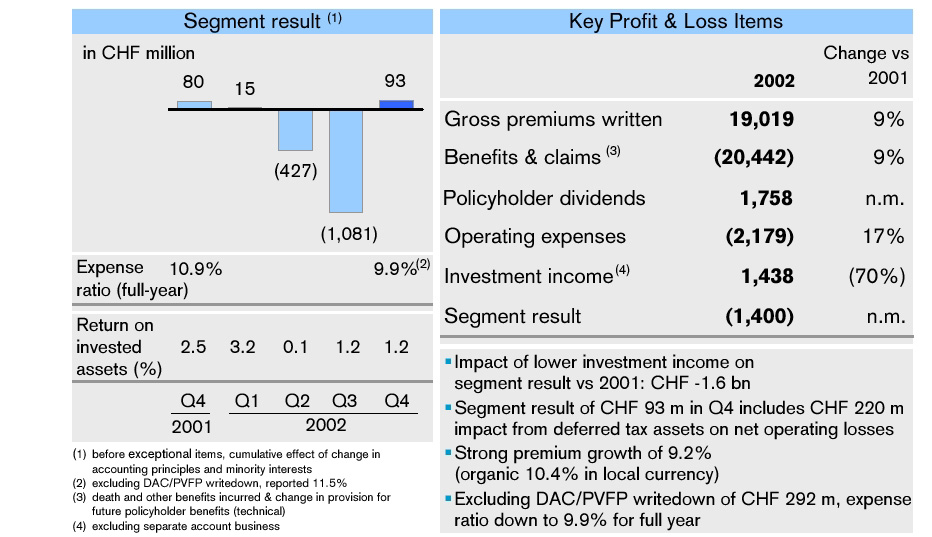

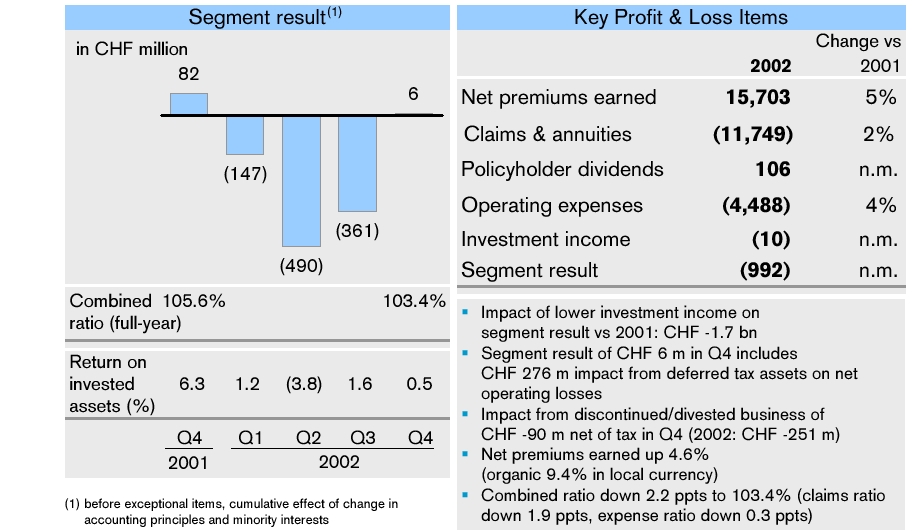

Life & Pensions recorded a segment profit (net operating profit before the cumulative effect of a change in accounting principles and minority interests) of CHF 93 million in the fourth quarter and a segment loss of CHF 1.4 billion for the full year 2002. Fourth quarter investment income was up 8% to CHF 333 million versus the previous

quarter. The full year loss reflects a CHF 3.3 billion decline in investment income, with an impact on the segment result of CHF 1.6 billion compared with the previous year. Life & Pensions reported a 9% increase in gross premiums written. Adjusted for acquisitions, divestitures and exchange rate impacts, premiums rose 10%. Operating expenses, comprising acquisition and non-deferrable costs, were up CHF 311 million year-on-year. This increase reflected the strong premium growth and additional DAC (deferred acquisition costs) and PVFP (present value of future profits) writedowns of CHF 292 million due to a change in the long-term assumptions regarding investment income. Excluding these writedowns, the expense ratio for 2002 was 9.9%, down from 10.9% in the prior year. Including these writedowns, the expense ratio for 2002 was 11.5%.

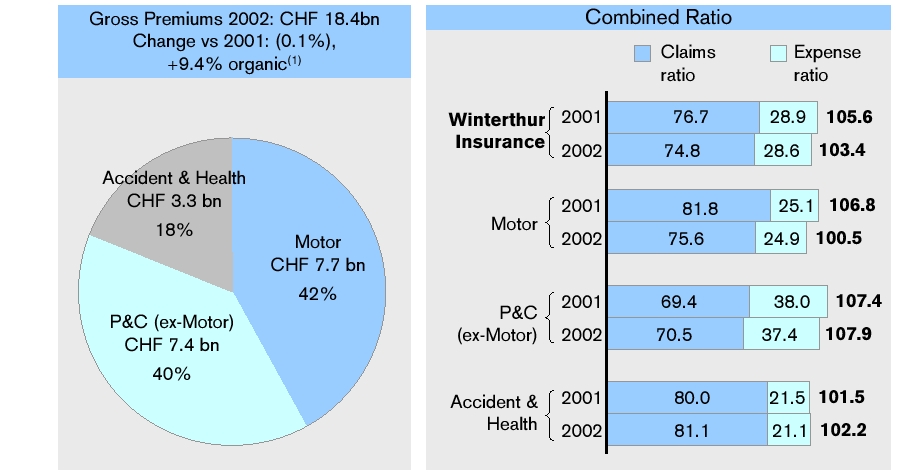

Insurance reported a segment profit (net operating profit before the cumulative effect of a change in accounting principles and minority interests) of CHF 6 million in the fourth quarter and a segment loss of CHF 992 million for the full year 2002. Fourth quarter investment income amounted to CHF 59 million. The full year loss reflects a CHF 2.2 billion decline in investment income, with an impact on the segment result of CHF 1.7 billion compared to 2001. For the full year 2002, net premiums earned rose 5% versus 2001. Adjusted for acquisitions, divestitures and exchange rate impacts, the segment reported a 9% increase in net premiums earned. The combined ratio improved by 2.2 percentage points, to 103.4%, compared with 2001.

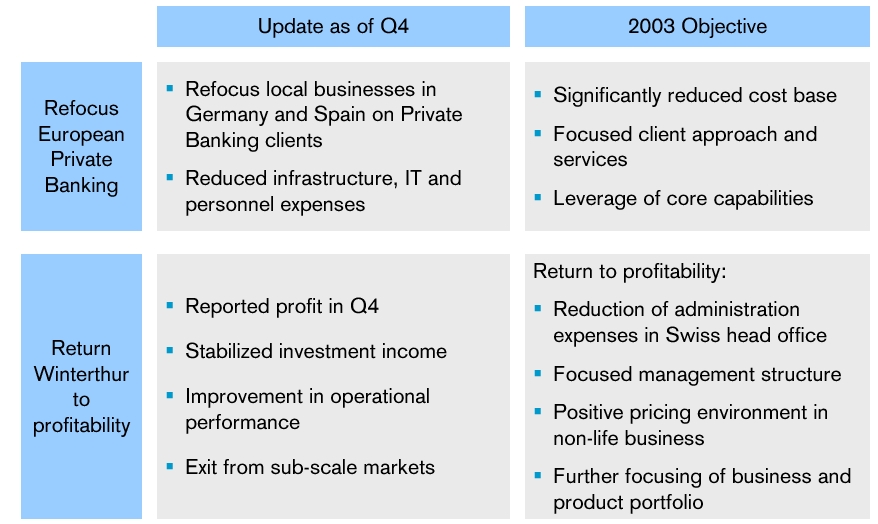

As announced by Winterthur today, the Insurance and Life & Pensions units will be brought together under a joint management structure, effective March 1, 2003. The combination of the head offices in Winterthur is expected to result in a reduction of approximately 350 jobs. Programs to

increase efficiency will also be initiated in the countries in which Winterthur operates. The financial results of the two units will continue to be reported as separate segments.

In addition, given the continuing financial markets weakness and global uncertainty, Credit Suisse Financial Services has decided to implement a plan designed to further reduce costs in its banking business by approximately CHF 300 million, including a reduction of approximately 900 jobs. A series of measures to accompany the reduction in jobs has been formulated in conjunction with Credit Suisse Group’s staff council in Switzerland.

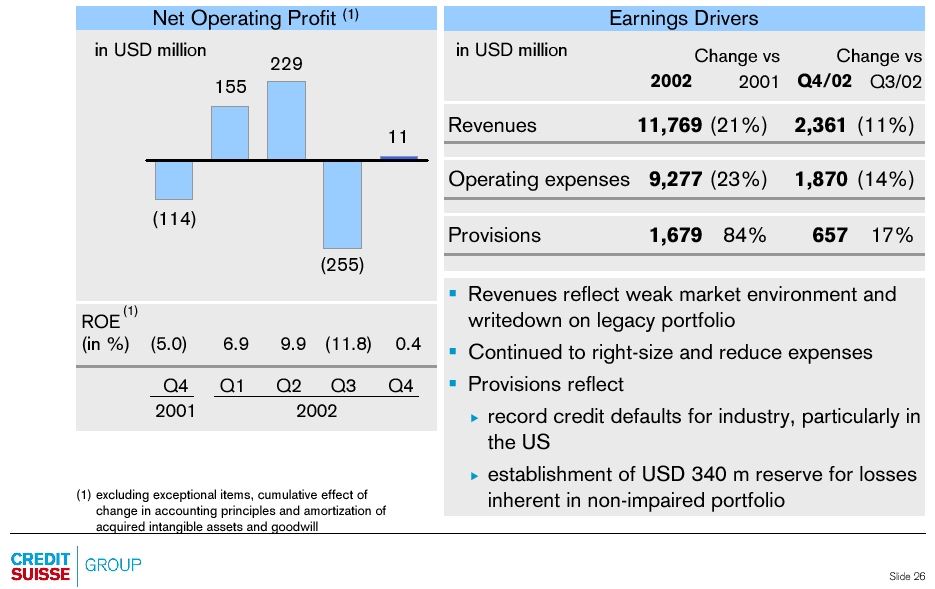

The Credit Suisse First Boston business unit reported a net loss of USD 811 million (CHF 1.3 billion) for the fourth quarter and a net loss of USD 1.2 billion (CHF 1.9 billion) for the full year 2002, including after-tax exceptional items of USD 813 million (CHF 1.3 billion) described above. This compares to a net loss of USD 425 million (CHF 679 million) in the previous quarter and a net loss of USD 821 million (CHF 1.4 billion) for the full year 2001. The fourth quarter net result benefited from the recognition of deferred tax assets on net operating losses as a result of a change in accounting principles in the amount of USD 556 million (CHF 868 million) for the financial year 2002, as well as a positive cumulative effect of USD 162 million (CHF 254 million) from prior years. Fourth quarter operating income was down 11% on the previous quarter in US dollar terms, primarily due to reduced revenues in the Institutional Securities segment. The business unit reduced operating expenses in the fourth quarter by 14% in US dollar terms versus the third quarter 2002, as part of continued efforts to adapt the business unit’s cost structure to the current environment.

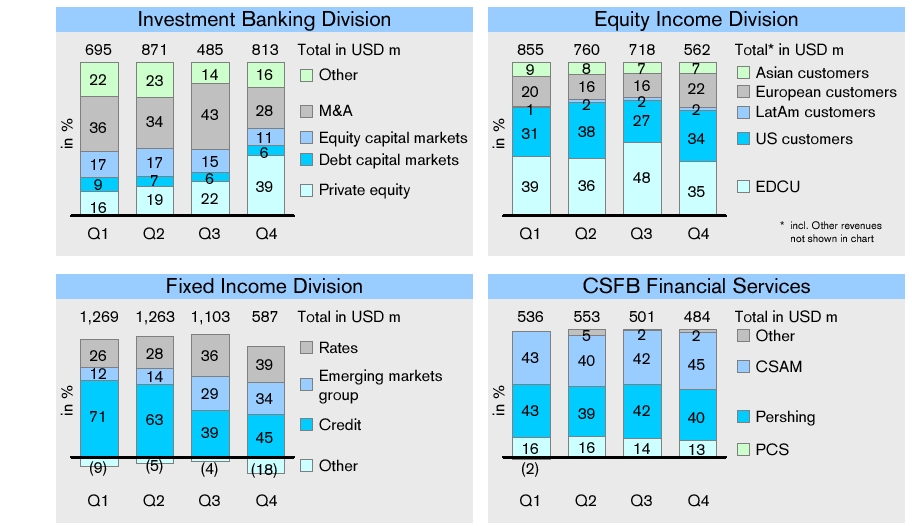

The Institutional Securities segment reported a decrease in operating income of 12% quarter-on-quarter, reflecting declines in the Fixed Income and Equity businesses. The segment reduced operating expenses in the fourth quarter 2002 by 16% compared with the third quarter, primarily through reductions in incentive compensation. For the full year 2002, the segment's operating income declined 23% and operating expenses fell 24% versus the previous year. In 2002, the Institutional Securities segment succeeded in maintaining or improving its market rankings. The Fixed Income business ranked number one in high yield and asset-backed new issuances and improved its overall global debt issuance position to second. The Equity division ranked fourth in global equity new issuances in 2002, tied for first place in global equity research, ranked first in pan-European and Latin American research and second in non-Japan Asia research. Furthermore, in investment banking, Credit Suisse First Boston ranked third in terms of US dollar volume of announced M&A transactions for 2002.

Operating income in the CSFB Financial Services segment decreased 3% quarter-on-quarter. Fourth quarter 2002 operating expenses declined 4% compared to the third quarter, reflecting the impact of a number of cost reduction initiatives. In January 2003, Credit Suisse First Boston announced an agreement to sell its Pershing unit, as outlined below. For the full year 2002, operating income decreased 13% and operating expenses were down 15% compared to 2001.

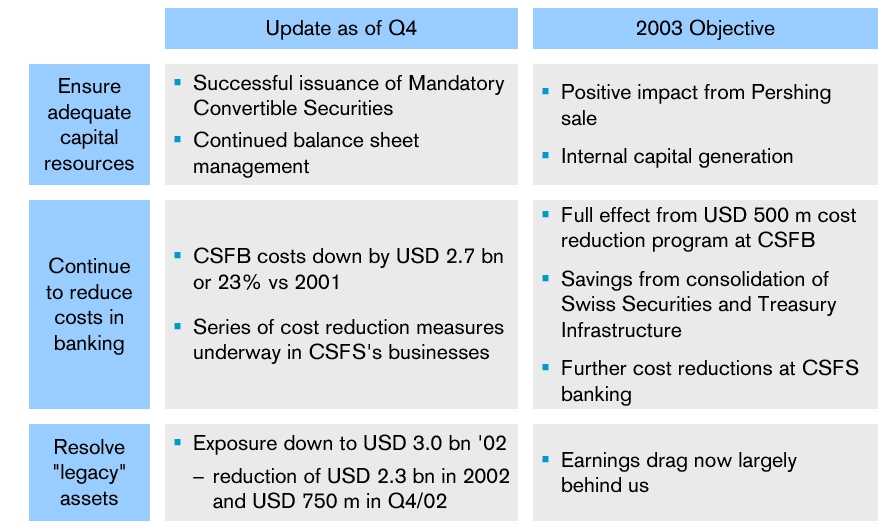

Capital Base

Credit Suisse Group’s consolidated BIS tier 1 ratio stood at 9.7% as of December 31, 2002, up from 9.0% at the end of the third quarter of 2002. This increase was attributable to the issuance by the Group of Mandatory Convertible Securities in

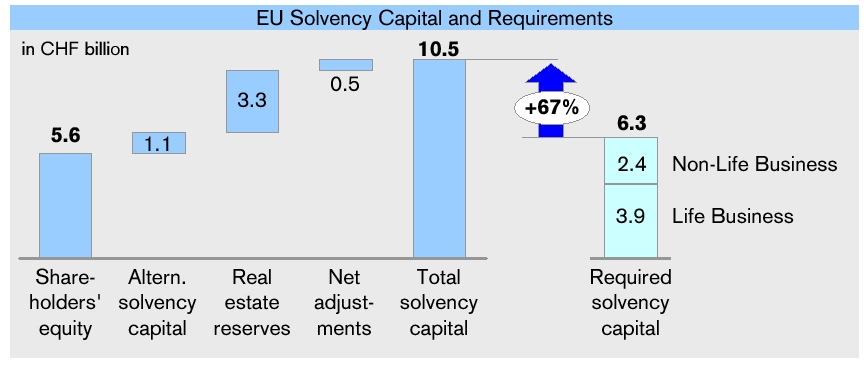

the amount of CHF 1.25 billion in December 2002, as well as to a reduction in risk-weighted assets and the currency translation effect of the lower US dollar versus the Swiss franc. The Mandatory Convertible Securities issue qualifies as equity capital and, accordingly, as tier 1 capital under BIS rules. The BIS tier 1 ratio for the Group’s banking business stood at 10.0% as of December 31, 2002, up from 9.4% at the end of the third quarter. Winterthur’s solvency margin (calculated in line with the EU directive) increased to 167% as of December 31, 2002, compared with 155% as of September 30, 2002.

The sale of Pershing to The Bank of New York, expected to close in the first half of 2003 subject to certain regulatory and other conditions, will increase the regulatory capital of Credit Suisse First Boston and Credit Suisse Group through the elimination of USD 500 million (CHF 695 million) of goodwill and a USD 1.6 billion (CHF 2.2 billion) reduction in risk-weighted assets. Furthermore, the sale will result in the elimination of USD 900 million (CHF 1.3 billion) of acquired intangible assets before tax, or USD 585 million (CHF 813 million) after tax.

Net New Assets

In the fourth quarter 2002, Credit Suisse Financial Services reported a net asset outflow of CHF 0.6 billion, with net inflows of CHF 0.5 billion at Private Banking and CHF 0.2 billion at Corporate & Retail Banking offset by a net outflow of CHF 1.3 billion from Life & Pensions. At Private Banking, net new assets declined versus the third quarter due mainly to the impact of increased attention surrounding Credit Suisse Group’s financial performance in the course of 2002. Credit Suisse First Boston reported a net asset outflow of CHF 6.0 billion in the fourth quarter, as a CHF 2.7 billion net inflow of private client assets was offset

by a net outflow of CHF 8.7 billion from Credit Suisse Asset Management related primarily to performance issues. For Credit Suisse Group, an overall net asset outflow of CHF 6.6 billion was recorded in the fourth quarter, versus a net outflow of CHF 13.7 billion in the third quarter 2002.

For the full year 2002, the Group reported a net asset outflow of CHF 2.6 billion, with CHF 18.9 billion in net new assets at Credit Suisse Financial Services – related primarily to Private Banking – offset by outflows of CHF 21.5 billion from Credit Suisse First Boston. The Group’s total assets under management stood at CHF 1,195.3 billion as of December 31, 2002, corresponding to a decline of 2.2% versus September 30, 2002, and a decrease of 16.4% versus December 31, 2001.

Valuation Adjustments, Provisions and Losses

Fourth quarter valuation adjustments, provisions and losses include a charge of CHF 778 million relating to an adjustment in the method of estimating inherent losses related to lending activities. This previously announced adjustment was considered necessary to better reflect in the loan provision the continued deterioration of the credit markets. The impact on the income statement of this charge, after tax, was offset by a release from the reserve for general banking risks, which was recorded as extraordinary income. Excluding the provision for inherent loan losses, credit provisions were CHF 637 million in the fourth quarter 2002, down 22% versus the third quarter, and were CHF 2.3 billion for the full year 2002, up 34% versus 2001, reflecting the deterioration in the credit environment globally. Overall, total valuation adjustments, provisions and losses were CHF 2.4 billion in the fourth quarter, reflecting the provision for inherent loan losses, US legal provisions, and increased valuation adjustments and losses.

Dividend Proposal

The Group’s Board of Directors has decided to propose a dividend of CHF 0.10 per share to the Annual General Meeting on April 25, 2003. This compares to a par value reduction of CHF 2 per share for the financial year 2001. If approved by the Annual General Meeting on April 25, 2003, this dividend will be paid out on May 2, 2003.

Termination of Share Buyback Program

Credit Suisse Group is terminating the share buyback program launched in March 2001, under which it purchased the equivalent of 15,330,000 shares with a par value of CHF 1 each. The value of the shares repurchased was CHF 1.1 billion, and the Group's share capital was reduced by this amount. The second trading line for shares on virt-x will be closed with immediate effect.

Advisory Board

Credit Suisse Group will streamline its Swiss and International Advisory Boards to create a single Advisory Board that will concentrate on the Group's main activities in Switzerland and Europe, with a special focus on Credit Suisse Financial Services. The new Advisory Board will comprise approximately 20 members, effective as of 2003.

Outlook

Credit Suisse Group remains cautious in its outlook for 2003 given the continued challenging market environment and global uncertainty. The Group continues to expect that the measures taken during 2002, as well as those being implemented in 2003, will restore its profitability in 2003. Additionally, the Group is entering 2003 with a stronger balance sheet and an improved capital base.

Enquiries

Credit Suisse Group, Media Relations Telephone +41 1 333 8844

Credit Suisse Group, Investor Relations Telephone +41 1 333 4570

For further information relating to Credit Suisse Group’s results for the fourth quarter and full year 2002, please refer to the Quarterly Report Q4 2002, including the reconciliation contained therein of the business unit results to Credit Suisse Group’s reported results. The Quarterly Report Q4 2002 as well as the slide presentation to analysts and the media are available on our website at: www.credit-suisse.com/results/docu

Credit Suisse Group

Credit Suisse Group is a leading global financial services company headquartered in Zurich. The business unit Credit Suisse Financial Services provides private clients and small and medium-sized companies with Private Banking and financial advisory services, banking products, and Pension and Insurance solutions from Winterthur. The business unit Credit Suisse First Boston, an Investment Bank, serves global institutional, corporate, government and individual clients in its role as a financial intermediary. Credit Suisse Group’s registered shares (CSGN) are listed in Switzerland and Frankfurt, and in the form of American Depositary Shares (CSR) in New York. The Group employs around 78,000 staff worldwide. As of December 31, 2002, it reported assets under management of CHF 1,195.3 billion.

Cautionary Statement Regarding Litigation

The legal reserve charge relating to private litigation represents management’s current estimate after consultation with counsel of the probable aggregate costs associated with such matters. Credit Suisse First Boston believes that it has substantial defenses in these private litigation matters, which are at an early stage. Given that it is difficult to predict the outcome of these matters, where claimants seek large or indeterminate damages or where the cases present novel theories or involve a large number of parties, Credit Suisse First Boston cannot state with confidence what the timing or eventual outcome will actually be. The legal reserve may be subject to revision in the future.

Cautionary Statement Regarding Forward-looking Information

This press release contains statements that constitute forward-looking statements. In addition, in the future we, and others on our behalf, may make statements that constitute forward-looking statements. Such forward-looking statements may include, without limitation, statements relating to our plans, objectives or goals; our future economic performance or prospects; the potential effect on our future performance of certain contingencies; and assumptions underlying any such statements. Words such as “believes,” “anticipates,” “expects,” "intends” and “plans” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. We do not intend to update these forward-looking statements except as may be required by applicable laws. By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that predictions, forecasts, projections and other outcomes described or implied in forward-looking statements will not be achieved. We caution you that a number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in such forward-looking statements. These factors include (i) market and interest rate fluctuations; (ii) the strength of the global economy in general and the strength of the economies of the countries in which we conduct our operations in particular; (iii) the ability of counterparties to meet their obligations to us; (iv) the effects of, and changes in, fiscal, monetary, trade and tax policies, and currency fluctuations; (v) political and social developments, including war, civil unrest or terrorist activity; (vi) the possibility of foreign exchange controls, expropriation, nationalization or confiscation of assets in countries in which we conduct our operations; (vii) the ability to maintain sufficient liquidity and access capital markets; (viii) operational factors such as systems failure, human error, or the failure to properly implement procedures; (ix) actions taken by regulators with respect to our business and practices in one or more of the countries in which we conduct our operations; (x) the effects of changes in laws, regulations or accounting policies or practices; (xi) competition in geographic and business areas in which we conduct our operations; (xii) the ability to retain and recruit qualified personnel; (xiii) the ability to maintain our reputation and promote our brands; (xiv) the ability to increase market share and control expenses; (xv) technological changes; (xvi) the timely development and acceptance of our new products and services and the perceived overall value of these products and services by users; (xvii) acquisitions, including the ability to integrate successfully acquired businesses; (xviii) the adverse resolution of litigation and other contingencies; and (xix) our success at managing the risks involved in the foregoing. We caution you that the foregoing list of important factors is not exclusive; when evaluating forward-looking statements, you should carefully consider the foregoing factors and other uncertainties and events, as well as the risks identified in our most recently filed Form 20-F and reports on Form 6-K furnished to the US Securities and Exchange Commission.

Today’s Presentation of the Results

| Speakers | |||

| • | Oswald J. G | ||

| Analysts’ presentation, Zurich (English) | |||

| • | February 25, 2003, 10.00 am CET / 9.00 am GMT / 4.00 am EST at the Credit Suisse Forum St. Peter, Zurich | ||

| • | Internet: | ||

| – | Live broadcast at www.credit-suisse.com/results | ||

| – | Video playback available approximately 3 hours after the event | ||

| • | Telephone: | ||

| – | Live audio dial-in on +41 91 610 5600 (Europe), +44 207 866 4111 (UK), or +1 412 858 4600 (USA), ask for “Credit Suisse Group quarterly results”; please dial in 10 minutes before the start of the presentation | ||

| – | Telephone replay available approximately 1 hour after the event on | ||

| +41 91 612 4330 (Europe), +44 207 866 4300 (UK) or +1 412 858 1440 (USA), conference ID 091# | |||

| Media conference, Zurich (English/German) | ||

| • | February 25, 2003, 12.00 noon CET / 11.00 am GMT / 6.00 am EST at the Credit Suisse Forum St. Peter, Zurich | |

| • | Simultaneous interpreting: German – English, English – German | |

| • | Internet: | |

| – | Live broadcast at www.credit-suisse.com/results | |

| – | Video playback available approximately 3 hours after the event | |

| • | Telephone: | |

| – | Live audio dial-in on +41 91 610 5600 (Europe), +44 207 866 4111 (UK), or +1 412 858 4600 (USA), ask for “Credit Suisse Group quarterly results”; please dial in 10 minutes before the start of the presentation | |

| – | Telephone replay available approximately 1 hour after the event on | |

| +41 91 612 4330 (Europe), +44 207 866 43 00 (UK) or +1 412 858 1440 (USA), conference ID 139# (English) or 241# (German) | ||

| Speakers | |

| • | Oswald J. Grübel, Co-CEO of Credit Suisse Group and Chief Executive Officer of Credit Suisse Financial Services |

| • | John J. Mack, Co-CEO of Credit Suisse Group and Chief Executive Officer of Credit Suisse First Boston (via videoconference) |

| • | Philip K. Ryan, Chief Financial Officer of Credit Suisse Group |

![]()

Winterthur media release

Winterthur streamlines its management structures

Winterthur, February 25, 2003 – Winterthur, a subsidiary of Credit Suisse Group, is realigning its organizational structure. The Insurance and Life & Pensions divisions will be brought together under a joint management structure within Winterthur Group, headed by CEO Leonhard Fischer, and will have a single Executive Board. The streamlining of these central management structures is aimed at achieving a significant increase in efficiency and will entail a reduction of approximately 350 jobs at the Winterthur head office. The new organizational framework and the measures already initiated will provide Winterthur with a solid basis from which to increase its profitability and strengthen its position in the insurance market.

As a result of the new organizational structure, the two Winterthur units – Insurance (property and liability business) and Life & Pensions (life insurance and retirement provision) – will be combined within Germany, Italy, Spain and Belgium. In Switzerland, however, life and non-life insurance will continue to be managed separately due to the substantial size of both of these units. They will work together very closely and increasingly exploit their synergies. In the UK, these two units will also remain separate because their business models are very different and synergies are minimal.

In the wake of the reorganization, the head offices of the two units will be brought together in Winterthur. The reorganization of the head office in Winterthur is expected to entail a reduction of approximately 350 jobs, including some redundancies. A series of measures to accompany the reduction in jobs has been formulated in conjunction with Credit Suisse Group's staff council in Switzerland. In addition, Winterthur Group's asset management unit will be integrated in the new organization. Financial results will continue to be reported separately. Markus Dennler, the current CEO of Winterthur Life & Pensions, will take on new responsibilities within Credit Suisse Group, and Manfred Broska, the current CEO of Winterthur Insurance, will retire.

Winterthur is committed to significantly improving its efficiency. "Ambitious cost management, operational excellence and qualitative growth are therefore our priorities," stated Leonhard Fischer with regard to the company’s strategic orientation. Programs already initiated in order to improve efficiency will continue and will be integrated in the new organization. The management of all Swiss and foreign Market Units has been charged with the task of launching additional initiatives to boost productivity. Duplications in support functions both in Switzerland and in companies outside Switzerland will be reduced. The cost savings which are realized will have a substantial impact on Winterthur Group’s administration costs.

The aim is to concentrate on those markets in which the Winterthur Group operates profitably, or in which it can achieve profitability in a foreseeable period of time. Winterthur aims to have a

business model targeting sustainable profitability for each of its markets. In markets where this is not possible, the respective companies will be sold.

Oswald J. Grübel, Co-CEO of Credit Suisse Group and CEO of Credit Suisse Financial Services, stated: "We are facing a fundamental change in the insurance sector, as companies must henceforth be profitable despite much lower investment income. With the timely implementation of the new organizational structure as well as the measures already initiated, Winterthur has created an excellent basis from which to operate in a more competitive market environment."

Leonhard Fischer, CEO of Winterthur Group, said: "Thanks to its excellent employees and its strong brand, Winterthur has - in the longer term - all the prerequisites to achieve a leading position in the insurance business in terms of profitability, productivity and quality."

| For questions, please contact: | |

| Winterthur, media relations | Tel. +41 52 261 61 04 |

| Internet: www.winterthur.com | |

Winterthur Group

Winterthur Group is a leading Swiss insurance company with head office in Winterthur and, as an international company, ranks among the top five insurers in Europe. The Group's products include a broad range of property and liability insurance products, as well as insurance solutions in life and pensions that are tailored to the individual needs of private and corporate clients. With approximately 32,000 employees worldwide, Winterthur Group achieved a premium volume of CHF 37.4 billion in 2002 and managed CHF 133.7 billion in assets.

Credit Suisse Group

Credit Suisse Group is a leading global financial services company headquartered in Zurich. The business unit Credit Suisse Financial Services provides private clients and small and medium-sized companies with private banking and financial advisory services, banking products, and pension and insurance solutions from Winterthur. The business unit Credit Suisse First Boston, an investment bank, serves global institutional, corporate, government and individual clients in its role as a financial intermediary. Credit Suisse Group’s registered shares (CSGN) are listed in Switzerland and Frankfurt, and in the form of American Depositary Shares (CSR) in New York. The Group employs around 78,000 staff worldwide. As of December 31, 2002, it reported assets under management of CHF 1,195.3 billion.

Cautionary statement regarding forward-looking information

This press release contains statements that constitute forward-looking statements. In addition, in the future we, and others on our behalf, may make statements that constitute forward-looking statements. Such forward-looking statements may include, without limitation, statements relating to our plans, objectives or goals; our future economic performance or prospects; the potential effect on our future performance of certain contingencies; and assumptions underlying any such statements.

Words such as “believes,” “anticipates,” “expects,” intends” and “plans” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. We do not intend to update these forward-looking statements except as may be required by applicable laws.

By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that predictions, forecasts, projections and other outcomes described or implied in forward-looking statements will not be achieved. We caution you that a number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in such forward-looking statements. These factors include (i) market and interest rate fluctuations; (ii) the strength of the global economy in general and the strength of the economies of the countries in which we conduct our operations in particular; (iii) the ability of counterparties to meet their obligations to us; (iv) the effects of, and changes in, fiscal, monetary, trade and tax policies, and currency fluctuations; (v) political and social developments, including war, civil unrest or terrorist activity; (vi) the possibility of foreign exchange controls, expropriation, nationalization or confiscation of assets in countries in which we conduct our operations; (vii) the ability to maintain sufficient liquidity and access capital markets; (viii) operational factors such as systems failure, human error, or the failure to properly implement procedures; (ix) actions taken by regulators with respect to our business and practices in one or more of the countries in which we conduct our operations; (x) the effects of changes in laws, regulations or accounting policies or practices; (xi) competition in geographic and business areas in which we conduct our operations; (xii) the ability to retain and recruit qualified personnel; (xiii) the ability to maintain our reputation and promote our brands; (xiv) the ability to increase market share and control expenses; (xv) technological changes; (xvi) the timely development and acceptance of our new products and services and the perceived overall value of these products and services by users; (xvii) acquisitions, including the ability to integrate successfully acquired businesses; (xviii) the adverse resolution of litigation and other contingencies; and (xix) our success at managing the risks involved in the foregoing.

We caution you that the foregoing list of important factors is not exclusive; when evaluating forward-looking statements, you should carefully consider the foregoing factors and other uncertainties and events, as well as the risks identified in Credit Suisse Group’s most recently filed Form 20-F and reports on Form 6-K furnished to the US Securities and Exchange Commission.

An overview of Credit Suisse Group

Credit Suisse Financial Services

Reconciliation of operating to consolidated results

Consolidated results Credit Suisse Group

Credit Suisse Group is a leading global financial services company headquartered in Zurich. Credit Suisse Financial Services provides private clients and small and medium-sized companies with private banking and financial advisory services, banking products, and pension and insurance solutions from Winterthur. Credit Suisse First Boston, the investment bank, serves global institutional, corporate, government and individual clients in its role as a financial intermediary. Credit Suisse Group‘s registered shares (CSGN) are listed in Switzerland and Frankfurt, and in the form of American Depositary Shares (CSR) in New York. The Group employs around 78,000 staff worldwide.

1 Editorial 2 Financial highlights Q4/2002 4 An overview of Credit Suisse Group 9 Risk Management 12 Review of business units 12 Credit Suisse Financial Services 22 Credit Suisse First Boston 33 Reconciliation of operating to consolidated results 37 Consolidated results Credit Suisse Group 37 Consolidated income statement 38 Consolidated balance sheet 44 Information for investors

Cautionary statement regarding forward-looking information

This Quarterly Report contains statements that constitute forward-looking statements. In addition, in the future we, and others on our behalf, may make statements that constitute forward-looking statements. Such forward-looking statements may include, without limitation, statements relating to our plans, objectives or goals; our future economic performance or prospects; the potential effect on our future performance of certain contingencies; and assumptions underlying any such statements.

Words such as “believes,” “anticipates,” “expects,” “intends” and “plans” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. We do not intend to update these forward-looking statements except as may be required by applicable laws.

By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that predictions, forecasts, projections and other outcomes described or implied in forward-looking statements will not be achieved. We caution you that a number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in such forward-looking statements. These factors include (i) market and interest rate fluctuations; (ii) the strength of the global economy in general and the strength of the economies of the countries in which we conduct our operations in particular; (iii) the ability of counterparties to meet their obligations to us; (iv) the effects of, and changes in, fiscal, monetary, trade and tax policies, and currency fluctuations; (v) political and social developments, including war, civil unrest or terrorist activity; (vi) the possibility of foreign exchange controls, expropriation, nationalization or confiscation of assets in countries in which we conduct our operations; (vii) the ability to maintain sufficient liquidity and access capital markets; (viii) operational factors such as systems failure, human error, or the failure to properly implement procedures; (ix) actions taken by regulators with respect to our business and practices in one or more of the countries in which we conduct our operations; (x) the effects of changes in laws, regulations or accounting policies or practices; (xi) competition in geographic and business areas in which we conduct our operations; (xii) the ability to retain and recruit qualified personnel; (xiii) the ability to maintain our reputation and promote our brands; (xiv) the ability to increase market share and control expenses; (xv) technological changes; (xvi) the timely development and acceptance of our new products and services and the perceived overall value of these products and services by users; (xvii) acquisitions, including the ability to integrate successfully acquired businesses; (xviii) the adverse resolution of litigation and other contingencies; and (xix) our success at managing the risks involved in the foregoing.

We caution you that the foregoing list of important factors is not exclusive; when evaluating forward-looking statements, you should carefully consider the foregoing factors and other uncertainties and events, as well as the risks identified in our most recently filed Form 20-F and reports on Form 6-K furnished to the US Securities and Exchange Commission.

EDITORIAL

Oswald J. Grübel

Co-CEO Credit Suisse Group

Chief Executive Officer Credit Suisse Financial Services

John J. Mack

Co-CEO Credit Suisse Group

Chief Executive Officer Credit Suisse First Boston

Dear shareholders, clients and colleagues

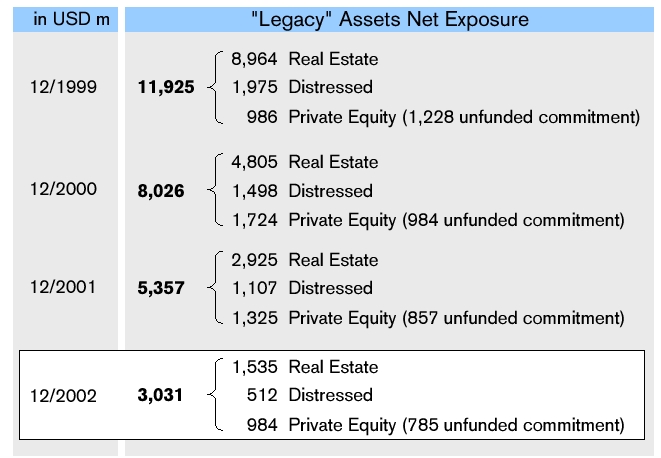

Credit Suisse Group‘s performance in the fourth quarter and full year 2002 was not satisfactory. To position the Group for profitability in 2003, we took aggressive steps during the year to address investment losses in our insurance business, set aside provisions for regulatory and litigation matters, reduce our exposure to legacy assets in our investment banking business and reduce costs across the Group. While we have taken these actions, our core businesses continued to hold leadership positions in key markets.

In the fourth quarter of 2002, the Group reported a net loss of CHF 950 million, compared with a net loss of CHF 2.1 billion in the third quarter. For the full year 2002, the Group posted a net loss of CHF 3.3 billion, compared with a net profit of CHF 1.6 billion in 2001.

The business unit Credit Suisse Financial Services reported a net profit of CHF 705 million in the fourth quarter, including exceptional items of CHF 73 million recognized as a result of focusing the European initiative on private banking clients, and a net loss of CHF 165 million for the full year.

Private Banking delivered a slightly higher profit than in the third quarter, despite project costs and low transaction-based income. Corporate & Retail Banking‘s profit was down quarter-on-quarter but up for the full year.

Despite continuing weakness in the financial markets, both Life & Pensions and Insurance returned to profitability in the fourth quarter. This was attributable to a satisfactory operating performance and the positive impact of a change in accounting principles. Winterthur is continuing to focus on achieving profitability for 2003 by concentrating on core markets, right pricing and the reduction of administration costs, with less reliance on investment income than in the past.

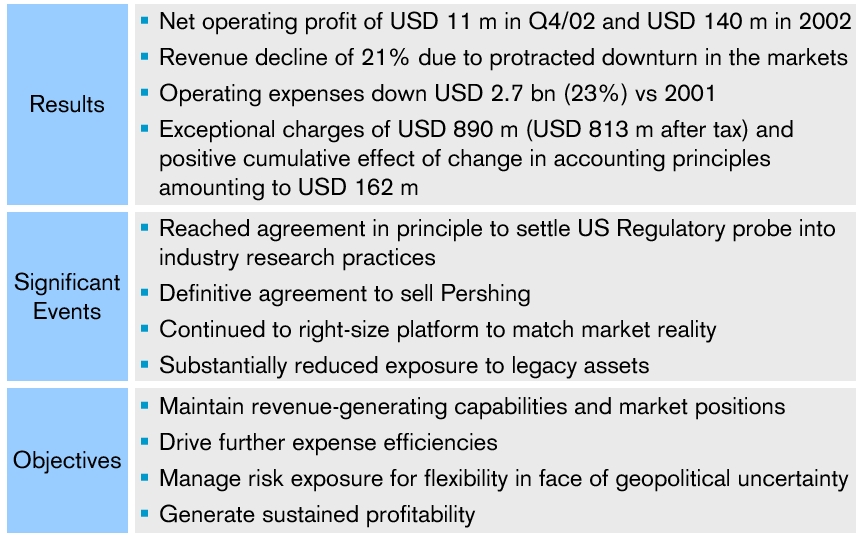

The business unit Credit Suisse First Boston recorded a net loss for the fourth quarter of USD 811 million (CHF 1.3 billion), including a number of after-tax exceptional items totaling USD 813 million (CHF 1.3 billion), and a net loss of USD 1.2 billion (CHF 1.9 billion) for the year 2002.

Credit Suisse First Boston faced deteriorating conditions in the equity and investment banking businesses throughout the year but succeeded in maintaining its market shares and rankings, while implementing a cost reduction program and reducing its exposure to certain legacy private equity, real estate and distressed debt assets. Revenues declined 21% in 2002 compared with the previous year. Full year operating expenses at Credit Suisse First Boston were down 23% compared with 2001. Credit Suisse First Boston also reached an agreement in principle with certain US regulators in the fourth quarter to settle US investigations relating to research analyst independence and IPO allocations.

The Group‘s consolidated BIS tier 1 ratio stood at 9.7% as of December 31, 2002, up from 9.0% at the end of the third quarter, while the banking BIS tier 1 ratio rose to 10.0%. Winterthur‘s solvency margin stood at 167% at the end of the fourth quarter, compared with 155% as of September 30, 2002. Through the issuance of Mandatory Convertible Securities, the prudent management of risk-weighted assets, provisioning for inherent loan losses and litigation in the US, and the future impact on capital of the Pershing sale, we are entering 2003 with a stronger balance sheet and an improved capital base.

As Credit Suisse Group emerges from an unusually difficult year, we – together with the Group‘s entire management team – are focusing intensively on restoring the Group to profitability in the year ahead, to create value for our shareholders, clients and employees.

Oswald J. Grübel John J. Mack

February 2003

CREDIT SUISSE GROUP FINANCIAL HIGHLIGHTS Q4/2002

| Consolidated income statement | ||||||||||

| Change | Change | Change | ||||||||

| in % from | in % from | 12 months | in % from | |||||||

| in CHF m | 4Q2002 | 3Q2002 | 4Q2001 | 3Q2002 | 4Q2001 | 2002 | 2001 | 2001 | ||

| Operating income | 6'395 | 5'666 | 8'161 | 13 | (22) | 28'038 | 39'154 | (28) | ||

| Gross operating profit | 1'284 | 314 | 1'264 | 309 | 2 | 4'509 | 8'870 | (49) | ||

| Net profit/(loss) | (950) | (2'148) | (830) | (56) | 14 | (3'309) | 1'587 | – | ||

| Return on equity | ||||||||||

| Change | Change | Change | ||||||||

| in % from | in % from | 12 months | in % from | |||||||

| in % | 4Q2002 | 3Q2002 | 4Q2001 | 3Q2002 | 4Q2001 | 2002 | 2001 | 2001 | ||

| Return on equity | (13.0) | (26.9) | (9.3) | (52) | 40 | (10.0) | 4.1 | – | ||

| Consolidated balance sheet | ||||||||||

| Change | Change | |||||||||

| in % from | in % from | |||||||||

| in CHF m | 31.12.02 | 30.09.02 | 31.12.01 | 30.09.02 | 31.12.01 | |||||

| Total assets | 955'656 | 999'158 | 1'022'513 | (4) | (7) | |||||

| Shareholders‘ equity | 31'394 | 32'461 | 38'921 | (3) | (19) | |||||

| Minority interests in shareholders‘ equity | 2'878 | 3'071 | 3'121 | (6) | (8) | |||||

| Capital data | ||||||||||

| Change | Change | |||||||||

| in % from | in % from | |||||||||

| in CHF m | 31.12.02 | 30.09.02 | 31.12.01 | 30.09.02 | 31.12.01 | |||||

| BIS risk-weighted assets | 201'466 | 218'700 | 222'874 | (8) | (10) | |||||

| BIS tier 1 capital | 19'544 | 19'669 | 21'155 | (1) | (8) | |||||

| of which non-cumulative perpetual preferred securities | 2'162 | 2'218 | 2'076 | (3) | 4 | |||||

| BIS total capital | 33'290 | 33'647 | 34'888 | (1) | (5) | |||||

| Solvency capital Winterthur | 10'528 | 10'127 | 8'555 | 4 | 23 | |||||

| Capital ratios | ||||||||||

| in % | 31.12.02 | 30.09.02 | 31.12.01 | |||||||

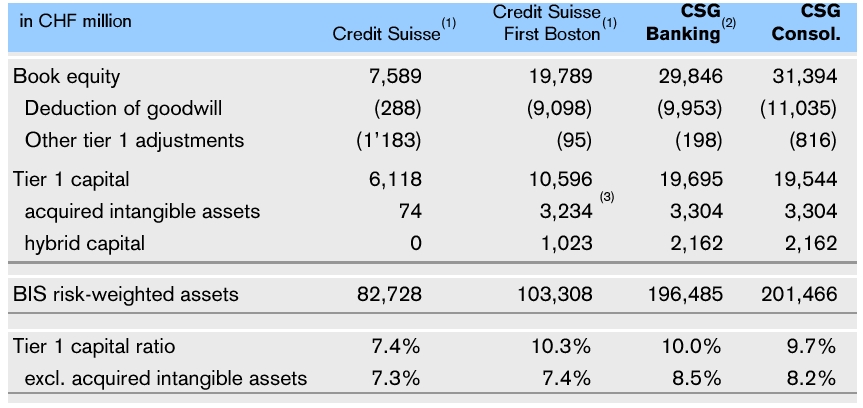

| BIS tier 1 ratio | Credit Suisse | 7.4 | 7.0 | 6.9 | ||||||

| Credit Suisse First Boston | 1) | 10.3 | 11.9 | 12.9 | ||||||

| Credit Suisse Group | 2) | 9.7 | 9.0 | 9.5 | ||||||

| Credit Suisse Group (banking) | 3) | 10.0 | 9.4 | 8.8 | ||||||

| BIS total capital ratio | Credit Suisse Group | 16.5 | 15.4 | 15.7 | ||||||

| EU solvency margin | Winterthur | 167.5 | 155.1 | 128.6 | ||||||

| Assets under management/client assets 4) | ||||||||||

| Change | Change | |||||||||

| in % from | in % from | |||||||||

| in CHF bn | 31.12.02 | 30.09.02 | 31.12.01 | 30.09.02 | 31.12.01 | |||||

| Advisory assets under management | 605.1 | 606.3 | 723.5 | 0 | (16) | |||||

| Discretionary assets under management | 590.2 | 615.5 | 707.1 | (4) | (17) | |||||

| Total assets under management | 1'195.3 | 1'221.8 | 1'430.6 | (2) | (16) | |||||

| Client assets | 1'793.2 | 1'821.0 | 2'138.2 | (2) | (16) | |||||

| Net new assets 4) | ||||||||||

| Change | Change | Change | ||||||||

| in % from | in % from | 12 months | in % from | |||||||

| in CHF bn | 4Q2002 | 3Q2002 | 4Q2001 | 3Q2002 | 4Q2001 | 2002 | 2001 | 2001 | ||

| Net new assets | (6.6) | (13.7) | 18.5 | (52) | – | (2.6) | 67.5 | – | ||

| 1) Ratio is based on a tier 1 capital of CHF 10.6 bn (30.09.02: CHF 13.3 bn; 31.12.01: CHF 15.2 bn), of which non-cumulative perpetual preferred securities is CHF 1.0 bn (30.09.02: CHF 1.1 bn; 31.12.01: CHF 1.1 bn). | ||||||||||

| 2) Ratio is based on a tier 1 capital of CHF 19.5 bn (30.09.02: CHF 19.7 bn; 31.12.01: CHF 21.2 bn), of which non-cumulative perpetual preferred securities is CHF 2.2 bn (30.09.02: CHF 2.2 bn; 31.12.01: CHF 2.1 bn). | ||||||||||

| 3) Ratio is based on a tier 1 capital of CHF 19.7 bn (30.09.02: CHF 20.2 bn; 31.12.01: CHF 19.4 bn), of which non-cumulative perpetual preferred securities is CHF 2.2 bn (30.09.02: CHF 2.2 bn; 31.12.01: CHF 2.1 bn). | ||||||||||

| 4) Certain reclassifications have been made to conform to the current presentation. | ||||||||||

| Number of employees | |||||||||||||

| Change | Change | ||||||||||||

| in % from | in % from | ||||||||||||

| 31.12.02 | 30.09.02 | 31.12.01 | 30.09.02 | 31.12.01 | |||||||||

| Switzerland | banking | 21'270 | 21'700 | 21'794 | (2) | (2) | |||||||

| insurance | 7'063 | 7'169 | 6'849 | (1) | 3 | ||||||||

| Outside Switzerland | banking | 25'057 | 26'586 | 28'415 | (6) | (12) | |||||||

| insurance | 25'067 | 24'982 | 23'103 | 0 | 9 | ||||||||

| Total employees Credit Suisse Group | 78'457 | 80'437 | 80'161 | (2) | (2) | ||||||||

| Share data | |||||||||||||

| Change | Change | ||||||||||||

| in % from | in % from | ||||||||||||

| 31.12.02 | 30.09.02 | 31.12.01 | 30.09.02 | 31.12.01 | |||||||||

| Shares issued | 1'189'891'720 | 1'189'348'956 | 1'196'609'811 | 0 | (1) | ||||||||

| To be issued upon conversion of MCS 1) | 40'413'838 | 0 | 0 | – | – | ||||||||

| Shares repurchased 2) | 0 | 0 | 7'730'000 | – | – | ||||||||

| Shares outstanding | 1'230'305'558 | 1'189'348'956 | 1'188'879'811 | 3 | 3 | ||||||||

| Share price in CHF | 30.00 | 28.90 | 70.80 | 4 | (58) | ||||||||

| Market capitalization in CHF m | 36'909 | 34'372 | 84'173 | 7 | (56) | ||||||||

| Book value per share in CHF | 23.18 | 24.71 | 29.92 | (6) | (23) | ||||||||

| 1) Maximum number of shares related to Mandatory Convertible Securities (MCS) issued by Credit Suisse Group Finance (Guernsey) Ltd. | |||||||||||||

| 2) Shares cancelled on 09.08.02, as previously approved by the Annual General Meeting. | |||||||||||||

| Share price | |||||||||||||

| Change | Change | Change | |||||||||||

| in % from | in % from | 12 months | in % from | ||||||||||

| in CHF | 4Q2002 | 3Q2002 | 4Q2001 | 3Q2002 | 4Q2001 | 2002 | 2001 | 2001 | |||||

| High (closing price) | 35.70 | 48.85 | 71.30 | (27) | (50) | 73.60 | 87.00 | (15) | |||||

| Low (closing price) | 20.60 | 26.80 | 51.60 | (23) | (60) | 20.60 | 44.80 | (54) | |||||

| Earnings per share | |||||||||||||

| Change | Change | Change | |||||||||||

| in % from | in % from | 12 months | in % from | ||||||||||

| in CHF | 4Q2002 | 3Q2002 | 4Q2001 | 3Q2002 | 4Q2001 | 2002 | 2001 | 2001 | |||||

| Basic earnings per share | (0.80) | (1.81) | (0.70) | (56) | 14 | (2.78) | 1.33 | – | |||||

| Diluted earnings per share | (0.80) | (1.81) | (0.69) | (56) | 16 | (2.77) | 1.32 | – | |||||

AN OVERVIEW OF CREDIT SUISSE GROUP

Credit Suisse Group reported a net loss of CHF 950 million in the fourth quarter of 2002, compared with a net loss of CHF 2.1 billion in the third quarter of 2002. Credit Suisse Financial Services reported a net profit of CHF 705 million in the fourth quarter. Credit Suisse First Boston recorded a net loss of USD 811 million (CHF 1.3 billion) in the fourth quarter, including after-tax exceptional items totaling USD 813 million (CHF 1.3 billion). For the full year 2002, the Group posted a net loss of CHF 3.3 billion, compared with a net profit of CHF 1.6 billion in 2001. In spite of this unsatisfactory result, the Group is entering 2003 with a stronger balance sheet and an improved capital base.

Continuing financial market weakness and a number of exceptional items impacted Credit Suisse Group‘s results in the fourth quarter of 2002.

Winterthur's results recovered in the fourth quarter, with both Life & Pensions and Insurance returning to profitability due to a satisfactory operating performance and the positive impact of a change in accounting principles. Private Banking recorded a slightly higher profit than in the third quarter, despite project costs and low transaction-based income. Corporate & Retail Banking‘s profit was down versus the third quarter but up for the full year. Credit Suisse Financial Services reported a net profit of CHF 705 million in the fourth quarter, including exceptional items of CHF 73 million recognized in connection with the focusing of the European initiative on private banking clients. This compared with a net loss of CHF 1.2 billion in the third quarter 2002.

Credit Suisse First Boston posted a fourth quarter net loss of USD 811 million (CHF 1.3 billion), compared to a net loss of USD 425 million (CHF 679 million) in the previous quarter. This result reflects a pre-tax charge of USD 450 million (CHF 702 million) for private litigation involving research analyst independence, certain IPO allocation practices, Enron and other related litigation; a pre-tax charge of USD 150 million (CHF 234 million) for the agreement in principle with various US regulators involving research analyst independence and the allocation of IPO shares to executive officers; an after-tax loss of USD 250 million (CHF 390 million) in connection with the sale of Pershing; and a pre-tax restructuring charge of USD 204 million (CHF 319 million) in connection with Credit Suisse First Boston‘s USD 500 million cost reduction program. These combined items had a total pre-tax impact of USD 890 million (CHF 1.4 billion), or USD 813 million (CHF 1.3 billion) after tax, in the fourth quarter.

Credit Suisse Group announced a change in its accounting principles in the fourth quarter of 2002 to allow for the recognition of deferred tax assets with respect to net operating losses, resulting in a positive cumulative effect of CHF 520 million from prior years and CHF 1.3 billion for the financial year 2002. Additionally, CHF 778 million of the increase in loan loss provisions recorded by the Group in the fourth quarter relates to an adjustment in the method of estimating inherent losses related to lending activities, to better reflect the current credit environment. This was offset by a release of the reserve for general banking risks, which was reported as extraordinary income. After accounting for the Corporate Center, which includes writedowns on the Group‘s investments in Swiss International Airlines and Warburg Pincus Private Equity of CHF 112 million and CHF 134 million, respectively, Credit Suisse Group reported a net loss of CHF 950 million for the fourth quarter of 2002. This compared with a net loss of CHF 2.1 billion in the third quarter 2002 and a net loss of CHF 830 million in the fourth quarter of 2001. For the full year 2002, after accounting for the Corporate Center, which includes writedowns on the Group‘s participation in Swiss Life of CHF 539 million, in addition to the above-mentioned writedowns in the fourth quarter, the Group reported a net loss of CHF 3.3 billion, compared with a net profit of CHF 1.6 billion for the previous year. Earnings per share for 2002 amounted to a loss of CHF 2.78 versus a profit of CHF 1.33 for 2001, and the Group‘s return on equity was -10.0% versus 4.1% in 2001.

Equity capital

Credit Suisse Group‘s consolidated BIS tier 1 ratio stood at 9.7% as of December 31, 2002, up from 9.0% at the end of the third quarter of 2002. This was attributable to the issuance by the Group of Mandatory Convertible Securities of CHF 1.25 billion in December 2002, as well as to a reduction in risk-weighted assets and the currency translation effect of the lower US dollar versus the Swiss franc. The Mandatory Convertible Securities issue qualifies as equity capital and, accordingly, as tier 1 capital under BIS rules. The BIS tier 1 ratio for the Group‘s banking business stood at 10.0% as of December 31, 2002, up from 9.4% at the end of the third quarter. Winterthur‘s solvency margin (calculated in line with the EU directive) stood at 167% at the end of 2002, compared with 155% as of September 30, 2002.

The sale of Pershing to The Bank of New York, expected to close in the first half of 2003 subject to certain regulatory and other conditions, will increase the regulatory capital of Credit Suisse First Boston and Credit Suisse Group through the elimination of USD 500 million (CHF 695 million) of goodwill and a USD 1.6 billion (CHF 2.2 billion) reduction in risk-weighted assets. Furthermore, the sale will result in the elimination of USD 900 million (CHF 1.3 billion) of acquired intangible assets before tax, or USD 585 million (CHF 813 million) after tax.

The Group has strengthened its balance sheet and improved its capital base through the issuance of Mandatory Convertible Securities, the prudent management of risk-weighted assets, provisioning for inherent loan losses and litigation in the US, and the future impact on capital of the Pershing sale.

Net new assets

Credit Suisse Financial Services reported a net asset outflow of CHF 0.6 billion in the fourth quarter 2002, with net inflows of CHF 0.5 billion at Private Banking and of CHF 0.2 billion at Corporate & Retail Banking offset by a net outflow of CHF 1.3 billion from Life & Pensions. At Private Banking, net new assets declined versus the third quarter due mainly to the impact of increased attention surrounding Credit Suisse Group‘s financial performance in the course of 2002. Credit Suisse First Boston reported a net asset outflow of CHF 6.0 billion in the fourth quarter, as a CHF 2.7 billion net inflow of private client assets was offset by a net outflow of CHF 8.7 billion from Credit Suisse Asset Management related primarily to performance issues. For Credit Suisse Group, an overall net asset outflow of CHF 6.6 billion was recorded in the fourth quarter, compared with a net outflow of CHF 13.7 billion in the third quarter 2002. For the full year 2002, the Group reported a net asset outflow of CHF 2.6 billion, as CHF 18.9 billion in net new assets reported by Credit Suisse Financial Services – related primarily to Private Banking – were offset by outflows of CHF 21.5 billion from Credit Suisse First Boston. The Group‘s total assets under management stood at CHF 1,195.3 billion as of December 31, 2002, corresponding to a decline of 2.2% versus September 30, 2002, and a decrease of 16.4% versus year-end 2001.

Operating income and expenses

The Group‘s operating income stood at CHF 6.4 billion in the fourth quarter 2002, up 13% on the previous quarter but down 22% on the fourth quarter of 2001. Credit Suisse Financial Services reported a 54% increase in operating income to CHF 3.5 billion versus the third quarter, reflecting a CHF 1.2 billion increase in operating income in the insurance business and stable operating income in banking. At Private Banking, operating income rose 3% to CHF 1.5 billion but remained below the average of the previous quarters due to investor inactivity and a reduced asset base. Corporate & Retail Banking posted a 7% decrease in operating income quarter- on-quarter due, in particular, to a decrease in transaction-related commission income. At Credit Suisse First Boston, fourth quarter operating income was down 11% on the previous quarter to USD 2.4 billion (CHF 3.4 billion), mainly reflecting revenue declines in the Fixed Income and Equity businesses, as well as at CSFB Financial Services. For the full year 2002, the Group‘s operating income stood at CHF 28.0 billion, down 28% on the previous year.

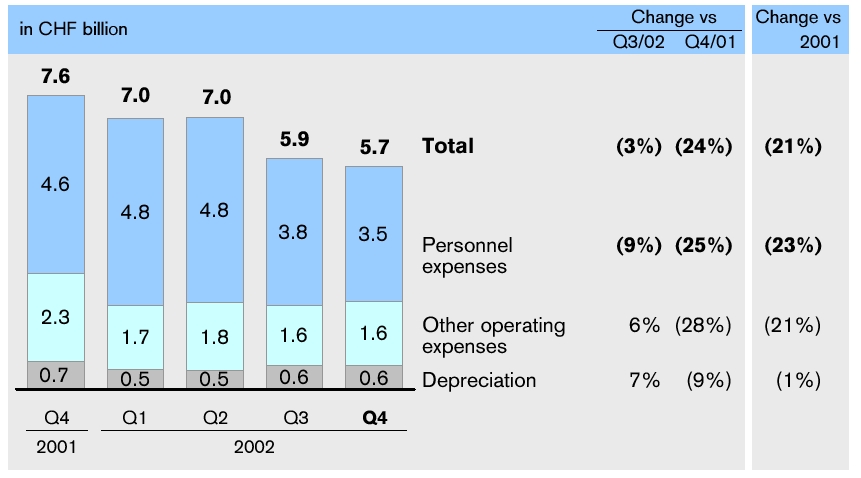

Including restructuring charges presented as exceptional items at the business units, the Group‘s operating expenses decreased 5% quarter-on-quarter to CHF 5.1 billion, and were down 26% on the fourth quarter 2001. At Credit Suisse Financial Services, fourth quarter operating expenses remained stable quarter-on-quarter and year-on-year despite expansion in certain markets. At Credit Suisse First Boston, fourth quarter operating expenses decreased 14% in US dollar terms versus the third quarter and were down 13% on the fourth quarter of 2001, reflecting continued efforts to adapt the business unit‘s cost structure to the current environment. The Group‘s full year operating expenses declined 22% versus 2001 to CHF 23.5 billion, primarily as a result of headcount reductions, a significant decrease in bonuses and the sale of non-core businesses.

Valuation adjustments, provisions and losses

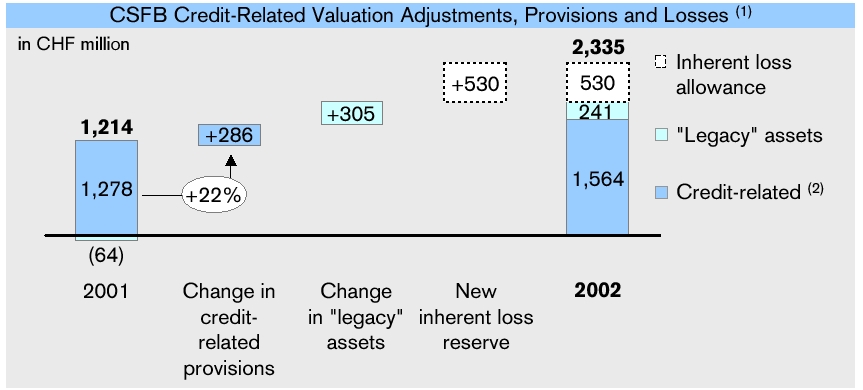

Fourth quarter valuation adjustments, provisions and losses include a charge of CHF 778 million relating to an adjustment in the method of estimating inherent losses related to lending activities. This adjustment was considered necessary to better reflect in the loan provision the continued deterioration of the credit markets. The impact on the income statement of this charge, after tax, was offset by a release from the reserve for general banking risks, which was recorded as extraordinary income. Excluding the provision for inherent loan losses, credit provisions were CHF 637 million in the fourth quarter 2002, down 22% versus the third quarter, and were CHF 2.3 billion for the full year 2002, up 34% versus 2001, reflecting the deterioration in the credit environment globally.

Overall, total valuation adjustments, provisions and losses were CHF 2.4 billion in the fourth quarter, reflecting the provision for inherent loan losses, US legal provisions, and increased valuation adjustments and losses.

Recognition of deferred tax assets on net operating losses

Credit Suisse Group changed its accounting principles in the fourth quarter of 2002 to allow for the recognition of deferred tax assets on net operating losses. As a result of this change, a positive cumulative effect of CHF 520 million was recognized from prior years and CHF 1.3 billion for 2002. At Credit Suisse Financial Services, fourth quarter net profit benefited from the first-time recognition of deferred tax assets on net operating losses in the amount of CHF 472 million for 2002, as well as a cumulative effect of CHF 266 million from prior years, primarily at Winterthur. At Credit Suisse First Boston, the fourth quarter net result reflects a benefit of USD 556 million (CHF 868 million) related to 2002, as well as a positive cumulative effect of USD 162 million (CHF 254 million) from prior years.

Dividend proposal

The Group‘s Board of Directors has decided to propose a dividend of CHF 0.10 per share to the Annual General Meeting on April 25, 2003. This compares to a par value reduction of CHF 2 per share for the financial year 2001. If approved by the Annual General Meeting on April 25, 2003, this dividend will be paid out on May 2, 2003.

Outlook

Credit Suisse Group remains cautious in its outlook for 2003 given the continued challenging market environment and global uncertainty. The Group continues to expect that the measures taken during 2002, as well as those being implemented in 2003, will restore its profitability in 2003. Additionally, the Group is entering 2003 with a stronger balance sheet and an improved capital base.

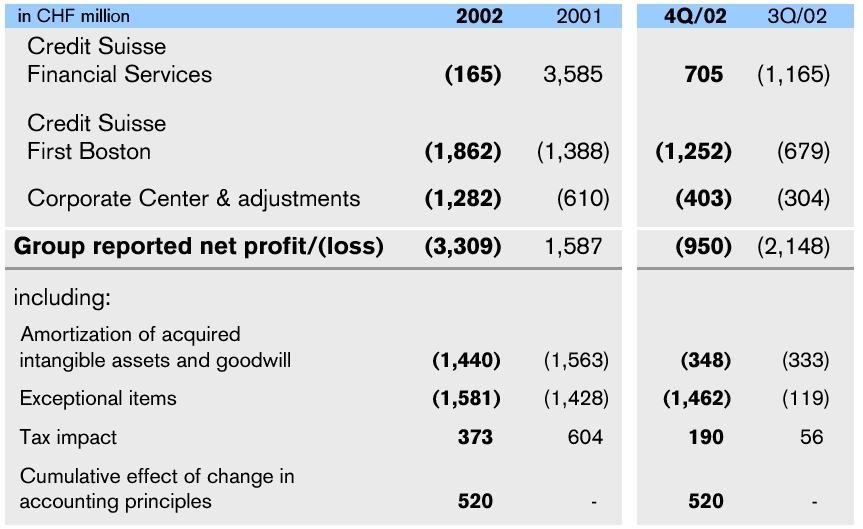

| Overview of business unit results 1) | ||||||||||||||||

| Credit Suisse Financial Services | Credit Suisse First Boston | Adjust. incl. Corporate Center | Credit Suisse Group | |||||||||||||

| in CHF m | 4Q2002 | 3Q2002 | 4Q2001 | 4Q2002 | 3Q2002 | 4Q2001 | 4Q2002 | 3Q2002 | 4Q2001 | 4Q2002 | 3Q2002 | 4Q2001 | ||||

| Operating income | 3'517 | 2'289 | 3'582 | 3'321 | 3'757 | 4'572 | (443) | (380) | 7 | 6'395 | 5'666 | 8'161 | ||||

| Personnel expenses | 1'408 | 1'490 | 1'244 | 1'896 | 2'179 | 3'174 | 160 | 124 | 207 | 3'464 | 3'793 | 4'625 | ||||

| Other operating expenses | 896 | 884 | 1'065 | 1'184 | 1'157 | 1'747 | (433) | (482) | (540) | 1'647 | 1'559 | 2'272 | ||||

| Operating expenses | 2'304 | 2'374 | 2'309 | 3'080 | 3'336 | 4'921 | (273) | (358) | (333) | 5'111 | 5'352 | 6'897 | ||||

| Gross operating profit/(loss) | 1'213 | (85) | 1'273 | 241 | 421 | (349) | (170) | (22) | 340 | 1'284 | 314 | 1'264 | ||||

| Depreciation of non-current assets 2) | 334 | 289 | 296 | 156 | 209 | 282 | 144 | 94 | 121 | 634 | 592 | 699 | ||||

| Amortization of acquired intangible assets and goodwill | 92 | 31 | 52 | 308 | 308 | 379 | 3 | (2) | (4) | 403 | 337 | 427 | ||||

| Valuation adjustments, provisions and losses | 105 | 91 | 48 | 1'977 | 867 | 1'207 | 342 | 15 | 34 | 2'424 | 973 | 1'289 | ||||

| Profit/(loss) before extraordinary items, cumulative effect of change in accounting principle and taxes | 682 | (496) | 877 | (2'200) | (963) | (2'217) | (659) | (129) | 189 | (2'177) | (1'588) | (1'151) | ||||

| Extraordinary income/(expenses), net | 24 | 6 | 8 | 220 | (1) | 0 | 125 | (136) | (265) | 369 | (131) | (257) | ||||

| Cumulative effect of change in accounting principle 3) | 266 | – | – | 254 | – | – | 0 | – | – | 520 | – | – | ||||

| Taxes 3) | (318) | (692) | (150) | 474 | 285 | 633 | 162 | (3) | 55 | 318 | (410) | 538 | ||||

| Net profit/(loss) before minority interests | 654 | (1'182) | 735 | (1'252) | (679) | (1'584) | (372) | (268) | (21) | (970) | (2'129) | (870) | ||||

| Minority interests | 51 | 17 | 22 | 0 | 0 | (1) | (31) | (36) | 19 | 20 | (19) | 40 | ||||

| Net profit/(loss) 3) | 705 | (1'165) | 757 | (1'252) | (679) | (1'585) | (403) | (304) | (2) | (950) | (2'148) | (830) | ||||

| 1) The Group‘s consolidated results are prepared in accordance with Swiss GAAP, while the Group‘s segment reporting principles are applied to the presentation of segment results. The business unit results reflect the results of the separate segments comprising the respective business units as well as certain acquisition-related costs and exceptional items that are not allocated to the segments. For a complete reconciliation of the business unit results to the Group‘s consolidated results and a discussion of the material reconciling items, please refer to pages 33-36. | ||||||||||||||||

| 2) Includes amortization of Present Value of Future Profits (PVFP) from the insurance business within Credit Suisse Financial Services. | ||||||||||||||||

| 3) In 4Q2002, Credit Suisse Group adopted a change in accounting principle relating to the recognition of deferred tax assets on net operating losses. If the change in accounting principle had not been adopted in 4Q2002, taxes in 4Q2002 would have been CHF -790 m for Credit Suisse Financial Services, CHF -394 m for Credit Suisse First Boston and CHF -1,023 m for Credit Suisse Group. The retroactive application of this change in accounting principle would have resulted in taxes for 4Q2002, 3Q2002 and 4Q2001 for Credit Suisse Financial Services of CHF -635 m, CHF -593 m and CHF -209 m, respectively, for Credit Suisse First Boston of CHF 276 m, CHF 290 m and CHF 909 m, respectively, and for Credit Suisse Group of CHF -198 m, CHF -306 m and CHF 755 m, respectively. | ||||||||||||||||

| Assets under management/client assets | |||||||||

| Change | Change | ||||||||

| in % from | in % from | ||||||||

| in CHF bn | 31.12.02 | 30.09.02 | 31.12.01 | 30.09.02 | 31.12.01 | ||||

| Credit Suisse Financial Services | |||||||||

| Private Banking | |||||||||

| Assets under management | 488.0 | 494.5 | 546.8 | (1.3) | (10.8) | ||||

| of which discretionary | 121.6 | 123.8 | 131.5 | (1.8) | (7.5) | ||||

| Client assets | 518.0 | 526.7 | 583.3 | (1.7) | (11.2) | ||||

| Corporate & Retail Banking | |||||||||

| Assets under management | 48.0 | 47.8 | 55.9 | 0.4 | (14.1) | ||||

| Client assets | 63.1 | 63.1 | 73.3 | 0.0 | (13.9) | ||||

| Life & Pensions | |||||||||

| Assets under management (discretionary) | 110.8 | 113.0 | 115.2 | (1.9) | (3.8) | ||||

| Client assets | 110.8 | 113.0 | 115.2 | (1.9) | (3.8) | ||||

| Insurance | |||||||||

| Assets under management (discretionary) | 30.7 | 31.1 | 30.5 | (1.3) | 0.7 | ||||

| Client assets | 30.7 | 31.1 | 30.5 | (1.3) | 0.7 | ||||

| Credit Suisse Financial Services | |||||||||

| Assets under management | 677.5 | 686.4 | 748.4 | (1.3) | (9.5) | ||||

| of which discretionary | 264.7 | 269.2 | 278.9 | (1.7) | (5.1) | ||||

| Client assets | 722.6 | 733.9 | 802.3 | (1.5) | (9.9) | ||||

| Credit Suisse First Boston | |||||||||

| Institutional Securities | |||||||||

| Assets under management | 31.3 | 35.2 | 41.7 | (11.1) | (24.9) | ||||

| of which Private Equity on behalf of clients (discretionary) | 20.9 | 24.7 | 29.3 | (15.4) | (28.7) | ||||

| Client assets | 83.9 | 86.8 | 121.7 | (3.3) | (31.1) | ||||

| CSFB Financial Services | |||||||||

| Assets under management | 486.5 | 500.2 | 640.5 | (2.7) | (24.0) | ||||

| of which discretionary | 297.2 | 313.8 | 393.6 | (5.3) | (24.5) | ||||

| Client assets | 986.7 | 1'000.3 | 1'214.2 | (1.4) | (18.7) | ||||

| Credit Suisse First Boston | |||||||||

| Assets under management | 517.8 | 535.4 | 682.2 | (3.3) | (24.1) | ||||

| of which discretionary | 325.5 | 346.3 | 428.2 | (6.0) | (24.0) | ||||

| Client assets | 1'070.6 | 1'087.1 | 1'335.9 | (1.5) | (19.9) | ||||

| Credit Suisse Group | |||||||||

| Assets under management | 1'195.3 | 1'221.8 | 1'430.6 | (2.2) | (16.4) | ||||

| of which discretionary | 590.2 | 615.5 | 707.1 | (4.1) | (16.5) | ||||

| Client assets | 1'793.2 | 1'821.0 | 2'138.2 | (1.5) | (16.1) | ||||

| Net new assets | |||||||||

| Change | Change | Change | |||||||

| in % from | in % from | 12 months | in % from | ||||||

| in CHF bn | 4Q2002 | 3Q2002 | 4Q2001 | 3Q2002 | 4Q2001 | 2002 | 2001 | 2001 | |

| Credit Suisse Financial Services | |||||||||

| Private Banking | 0.5 | 3.4 | 8.6 | (85.3) | (94.2) | 18.7 | 35.7 | (47.6) | |

| Corporate & Retail Banking | 0.2 | (2.3) | 0.9 | – | (77.8) | (3.2) | 1.3 | – | |

| Life & Pensions | (1.3) | 0.4 | 1.8 | – | – | 3.4 | 5.0 | (32.0) | |

| Credit Suisse Financial Services | (0.6) | 1.5 | 11.3 | – | – | 18.9 | 42.0 | (55.0) | |

| Credit Suisse First Boston | |||||||||

| Institutional Securities | – | (3.0) | 0.5 | – | – | 1.9 | 0.5 | 280.0 | |

| CSFB Financial Services 1) | (6.0) | (12.2) | 6.7 | (50.8) | – | (23.4) | 25.0 | – | |

| Credit Suisse First Boston | (6.0) | (15.2) | 7.2 | (60.5) | – | (21.5) | 25.5 | – | |

| Credit Suisse Group | (6.6) | (13.7) | 18.5 | (51.8) | – | (2.6) | 67.5 | – | |

Certain reclassifications have been made to conform to the current presentation. | |||||||||

| 1) Net new discretionary assets for institutional asset management. | |||||||||

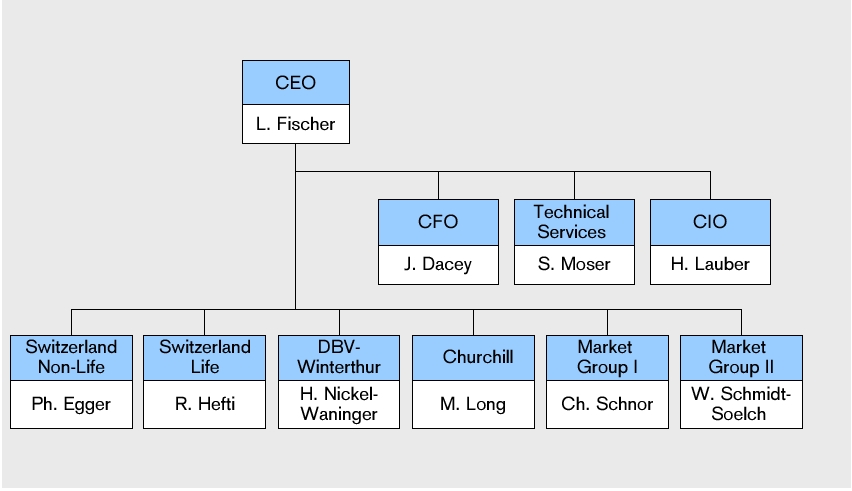

Group Executive Board, effective January 1, 2003

Oswald J. Grübel Co-CEO Credit Suisse Group; Chief Executive Officer Credit Suisse Financial Services

John J. Mack Co-CEO Credit Suisse Group; Chief Executive Officer Credit Suisse First Boston

Hans-Ulrich Doerig Vice-Chairman of the Group Executive Board; Head of Corporate Center, Credit Suisse Group

Brady W. Dougan Co-President, Institutional Securities, Credit Suisse First Boston

Brian D. Finn Co-President, Institutional Securities, Credit Suisse First Boston

David P. Frick General Counsel, Credit Suisse Group

Ulrich Körner Chief Financial Officer, Credit Suisse Financial Services

Jeffrey M. Peek Head of CSFB Financial Services, Credit Suisse First Boston

Philip K. Ryan Chief Financial Officer, Credit Suisse Group

Richard E. ThornburghChief Risk Officer, Credit Suisse Group

Stephen R. Volk Chairman, Credit Suisse First Boston

Alex W. Widmer Head of Private Banking, Credit Suisse Financial Services

RISK MANAGEMENT

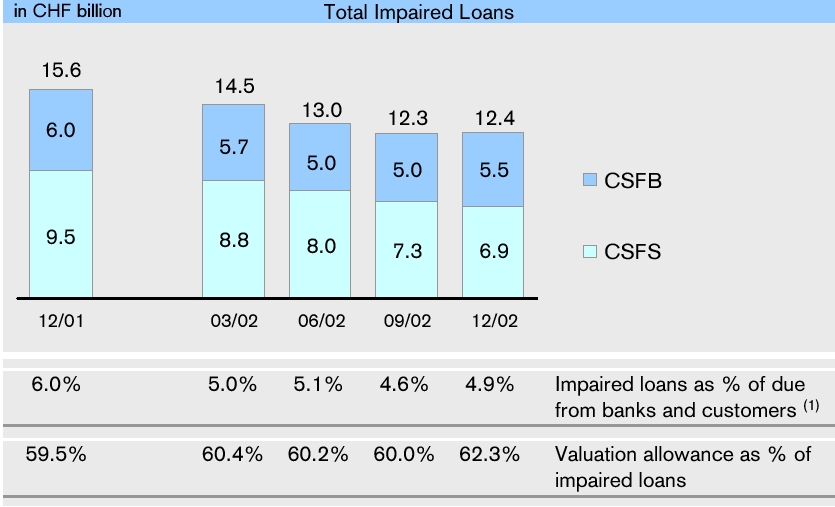

Credit Suisse Group‘s overall position risks fell by 9% in the fourth quarter 2002 versus the previous quarter, predominantly due to further equity position reductions, lower foreign exchange risks and a substantial reduction of exposures in Brazil. Credit Suisse First Boston‘s average trading risks were lower as a consequence of reduced credit spread positions. The Group‘s credit risk exposures declined by 6% quarter-on-quarter.

Overall risk trends

Economic Risk Capital (ERC) is an emerging best practice tool for measuring and reporting all quantifiable risks across a financial organization on a consistent and comprehensive basis. It is referred to as “economic” because it treats positions solely on an economic basis, irrespective of differences in accounting or regulatory treatment. Credit Suisse Group has invested significant resources in developing this tool over the last few years to achieve several objectives: to better assess the composition and trend of our risk portfolio; to provide a benchmark for risk/return analysis by business; to improve risk control and limits; to support a target credit rating; and to allocate capital. ERC is defined as the economic capital needed to remain solvent even under extreme market, business and operational conditions, based on conservative assumptions.

Credit Suisse Group distinguishes between three fundamental sources of risk. Position risk ERC measures the potential unexpected loss in economic value associated with the Group‘s portfolio of positions over a one-year horizon that is exceeded with a given, small probability (1% for daily risk management purposes; 0.03% for capital management purposes). Business risk ERC captures the risk related to the Group‘s commission and fee-based activities by estimating the potential worst-case negative margin that these activities might experience during a severe market downturn. Operational risk ERC represents the estimated worst-case loss resulting from inadequate or failed internal processes and systems, human error or external events.

Position risk ERC constitutes the most important risk category and comprises more than 80% of the overall risk profile. Total 99%, 1-year position risk ERC was down 9% in the fourth quarter 2002 compared with the previous quarter, due primarily to further equity position reductions and reductions in the foreign exchange and emerging markets areas. As highlighted in the table below, Credit Suisse Group has substantially reduced its position risk profile over the course of 2002, predominantly through a significant reduction in its equity market-related risks. Other notable developments include a substantial reduction in emerging market risks, due mainly to lower positions in Brazil, and a material reduction in foreign exchange rate risks, primarily due to a reduction of the foreign exchange risks embedded in the investment portfolios of the Winterthur units. At the end of the fourth quarter of 2002, 53% of the Group‘s position risk ERC was with Credit Suisse First Boston, 42% with Credit Suisse Financial Services (of which 66% was with the insurance units and 34% was with the banking units) and 5% with the Corporate Center.

| Key Position Risk Trends | |||||

| In CHF m | Change in % from | Change Analysis: Brief Summary | |||

| 4Q2002 | 3Q2002 | 4Q2001 | 4Q2002 vs 3Q2002 | ||

| Interest Rate, Credit Spread & Foreign Exchange ERC | 3'666 | (15%) | (21%) | Driven by a reduction in foreign exchange risk at the Winterthur units | |

| Equity Investment ERC | 3'674 | (9%) | (65%) | Driven by the sale of strategic investments | |

| Swiss & Retail Lending ERC | 2'097 | 0% | (9%) | No material change | |

| International Lending ERC | 3'840 | (2%) | (4%) | No material change | |

| Emerging Markets ERC | 1'977 | (15%) | (26%) | Predominantly from position reductions in Brazil | |

| Real Estate ERC & Structured Asset ERC 1) | 3'953 | (8%) | (10%) | Continued reduction in legacy commercial real estate exposures in the US | |

| Insurance Underwriting ERC | 819 | (2%) | 9% | Sale of Winterthur Portugal | |

| Simple Sum across Risk Categories | 20'025 | (8%) | (32%) | Lower Equity and Emerging Markets ERC | |

| Diversification Benefit | (6'723) | (7%) | (41%) | In line with overall risk reduction | |

| Total Position Risk ERC | 13'303 | (9%) | (26%) | Lower Equity and Emerging Markets ERC | |

For a more detailed description of the Group‘s ERC model, please refer to our Annual Report 2001, which is available on our website www.credit-suisse.com. Note that comparatives have been restated for methodology changes in order to maintain consistency over time. | |||||