UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of February 15, 2007

Commission File Number 001-15244

CREDIT SUISSE GROUP

(Translation of registrant’s name into English)

Paradeplatz 8, P.O. Box 1, CH-8070 Zurich, Switzerland

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F | Form 40-F |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Note: Regulation S-T Rule 101(b)(1) only permits the submission in paper of a Form 6-K if submitted solely to provide an attached annual report to security holders.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Note: Regulation S-T Rule 101(b)(7) only permits the submission in paper of a Form 6-K if submitted to furnish a report or other document that the registrant foreign private issuer must furnish and make public under the laws of the jurisdiction in which the registrant is incorporated, domiciled or legally organized (the registrant’s “home country”), or under the rules of the home country exchange on which the registrant’s securities are traded, as long as the report or other document is not a press release, is not required to be and has not been distributed to the registrant’s security holders, and, if discussing a material event, has already been the subject of a Form 6-K submission or other Commission filing on EDGAR.

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes | No |

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): 82-.

| CREDIT SUISSE GROUP | |

Paradeplatz 8 P.O. Box CH-8070 Zurich Switzerland | Telephone +41 844 33 88 44 Fax +41 44 333 88 77 media.relations@credit-suisse.com

| |

Media Release

Credit Suisse Group Reports Net Income of CHF 11.3 Billion for 2006

Credit Suisse Group today reported net income of CHF 11,327 million for the full year 2006, up 94% compared to net income of CHF 5,850 million for 2005. Net income for 2006 included a net capital gain of CHF 1,817 million from the sale of Winterthur, which was recorded in the fourth quarter.

Basic earnings per share from continuing operations were CHF 7.53 for the full year 2006, compared to CHF 3.98 for 2005. Basic earnings per share were CHF 10.30 for the full year 2006, compared to CHF 5.17 for 2005.

Fourth-quarter 2006 net income totaled CHF 4,673 million, compared to net income of CHF 1,103 million in the fourth quarter of 2005.

Credit Suisse recorded net new assets of CHF 95.4 billion for the full year 2006.

Financial highlights |

|

|

|

|

|

|

|

|

|

|

|

in CHF million |

| 12 mths |

| Change in % vs |

| 4Q2006 |

| Change in % |

| Change in % |

|

|

| 2006 |

| 12 mths 2005 |

|

|

| vs 3Q2006 |

| vs 4Q2005 |

|

Net revenues |

| 38,603 |

| 27 |

| 10,814 |

| 34 |

| 43 |

|

Total operating expenses |

| 24,414 |

| 5 |

| 6,520 |

| 15 |

| 0 |

|

Income from continuing operations |

| 8,281 |

| 83 |

| 2,599 |

| 77 |

| 284 |

|

Income from discontinued operations, |

|

|

|

|

|

|

|

|

|

|

|

net of tax |

| 3,070 |

| 134 |

| 2,074 |

| 389 |

| 387 |

|

Net income |

| 11,327 |

| 94 |

| 4,673 |

| 147 |

| 324 |

|

Return on equity |

| 27.5 | % | — |

| 44.1 | % | — |

| — |

|

Basic earnings per share from |

|

|

|

|

|

|

|

|

|

|

|

continuing operations (CHF) |

| 7.53 |

| — |

| 2.42 |

| — |

| — |

|

Basic earnings per share (CHF) |

| 10.30 |

| — |

| 4.35 |

| — |

| — |

|

BIS tier 1 ratio (as of December 31) |

| 13.9 | % | — |

| — |

| — |

| — |

|

Zurich, February 15, 2007 "2006 was a record year for Credit Suisse. Our integrated banking model proved successful and provided us with an effective platform to capture the growth opportunities arising from high levels of client activity, while at the same time significantly improving our profitability," stated Oswald J. Grübel, CEO of Credit Suisse.

He added: "In our first year as an integrated bank, we have made excellent progress in strengthening our operating efficiency but there is still great potential for further improvement as we continue to invest in the growth of our business."

He concluded: "Our clients have responded well to our integrated approach and Credit Suisse now has excellent opportunities for further growth in the context of globalization, which we believe will create dynamic markets for the foreseeable future."

| Media Release |

February 15, 2007 Page 2/8 |

Segment results |

|

|

|

|

|

|

|

|

|

| |

in CHF million |

| 12 mths |

| Change in % vs |

| 4Q2006 |

| Change in % |

| Change in % |

|

|

| 2006 |

| 12 mths 2005 |

|

|

| vs 3Q2006 |

| vs 4Q2005 |

|

Investment | Net revenues | 20,469 |

| 32 |

| 6,085 |

| 45 |

| 63 |

|

Banking | Total operating expenses | 14,556 |

| 4 |

| 3,723 |

| 8 |

| 8 |

|

| Income from continuing |

|

|

|

|

|

|

|

|

|

|

| operations before taxes | 5,951 |

| 272 |

| 2,342 |

| 209 |

| — |

|

Private | Net revenues | 11,678 |

| 11 |

| 2,973 |

| 11 |

| 9 |

|

Banking | Total operating expenses | 7,155 |

| 8 |

| 1,871 |

| 11 |

| 9 |

|

| Income from continuing |

|

|

|

|

|

|

|

|

|

|

| operations before taxes | 4,596 |

| 16 |

| 1,143 |

| 12 |

| 11 |

|

Asset | Net revenues | 2,861 |

| 2 |

| 738 |

| 7 |

| (3) |

|

Management | Total operating expenses | 2,352 |

| 31 |

| 648 |

| 21 |

| 26 |

|

| Income from continuing |

|

|

|

|

|

|

|

|

|

|

| operations before taxes | 508 |

| (50) |

| 89 |

| (44) |

| (63) |

|

Investment Banking

The Investment Banking segment reported record income from continuing operations before taxes of CHF 5,951 million for the full year 2006, an increase of CHF 4,352 million compared to 2005, with strong contributions across the underwriting, advisory, fixed income trading and equity trading businesses. Excluding the CHF 508 million of credits from insurance settlements for litigation and related costs in 2006 and the CHF 960 million charge to increase litigation reserves in 2005, income from continuing operations before taxes rose 113% in 2006. Net revenues increased 32% to a record level in 2006, driven by a strong performance across all key business areas and regions amid favorable market conditions, high levels of deal activity and improved market share in certain products. Total operating expenses for the full year increased 4%, or 15% excluding the insurance settlements and litigation charge. The compensation/revenue ratio was 50.1% in 2006, compared to 55.5% for 2005. The pre-tax income margin was 29.1%, or 26.6% excluding the insurance settlements, compared to 16.5% excluding the litigation charge in 2005.

In the fourth quarter of 2006, income from continuing operations before taxes totaled a record CHF 2,342 million, an increase of CHF 2,056 million compared to the fourth quarter of 2005. Net revenues grew 63% to a record level in the fourth quarter of 2006, benefiting from strong performances in both the investment banking and trading businesses. Total operating expenses rose 8% compared to the fourth quarter of 2005, primarily reflecting higher compensation expenses in line with higher revenues, partly offset by a decrease in other expenses due to improvements in operating efficiency. The compensation/revenue ratio was 42.2% in the fourth quarter of 2006, compared to 53.5% in the first three quarters of the year. The pre-tax income margin was 38.5% in the fourth quarter of 2006, compared to 7.7% in the fourth quarter of 2005.

Private Banking

The Private Banking segment, which comprises the Wealth Management and Corporate & Retail Banking businesses, reported record income from continuing operations before taxes of CHF 4,596 million for the full year 2006, an increase of 16% compared to 2005.

In the fourth quarter of 2006, income from continuing operations before taxes was CHF 1,143 million, an increase of 11% compared to the fourth quarter of 2005.

| Media Release |

February 15, 2007 Page 3/8 |

The Wealth Management business reported record income from continuing operations before taxes of CHF 3,237 million for the full year 2006, an improvement of 22% compared to 2005. Net revenues grew 15% and total operating expenses rose 12%. The pre-tax income margin was 39.6% for 2006, compared to 37.3% in 2005.

In the fourth quarter of 2006, income from continuing operations before taxes amounted to CHF 811 million, up 15% from the fourth quarter of 2005. This increase reflected strong net revenues driven by higher commissions and fees, mainly from brokerage, product issuances and asset-based fees, as well as higher net interest income from higher liability margins and liability volumes. The growth in net revenues more than offset a 10% rise in total operating expenses, driven primarily by higher personnel expenses related to strategic investments in the global business and higher performance-related compensation expenses. The pre-tax income margin was 39.0% for the fourth quarter of 2006, compared to 37.6% in the fourth quarter of 2005.

The Corporate & Retail Banking business reported a 4% increase in income from continuing operations before taxes to CHF 1,359 million for the full year 2006, compared to 2005. Net revenues increased 4% in 2006 and total operating expenses rose 1%. The pre-tax income margin was 38.9% for 2006, compared to 38.7% in 2005.

In the fourth quarter of 2006, income from continuing operations before taxes was CHF 332 million, an increase of 3%, compared to the same period of 2005. Net revenues grew 6%, driven by higher asset-based commissions and fees and increased net interest income. Total operating expenses rose by 7% due to higher compensation and benefits, primarily reflecting higher performance-related compensation expenses. The pre-tax income margin was 37.1% for the fourth quarter of 2006, compared to 38.0% in the fourth quarter of 2005.

Asset Management

The Asset Management segment reported income from continuing operations before taxes of CHF 508 million for the full year 2006, a decline of 50% compared to 2005. This decrease reflects lower private equity and other investment-related gains, which are cyclical in nature, and higher operating expenses, partly due to the realignment of the business in 2006. Net revenues rose 2% compared to the previous year and net revenues before private equity and other investment-related gains grew 12%, reflecting the growth in assets under management. Private equity and other investment-related gains totaled CHF 502 million in 2006, a decrease of 28% from 2005. Total operating expenses rose 31% in 2006, including CHF 225 million of realignment costs. The pre-tax income margin was 17.8% for 2006, compared to 35.9% in 2005. As of December 31, 2006, assets under management totaled CHF 669.9 billion, an increase of 14% from December 31, 2005.

In the fourth quarter of 2006, income from continuing operations before taxes totaled CHF 89 million, a decrease of 63% compared to the fourth quarter of 2005. Net revenues declined 3% in the fourth quarter of 2006 compared to the same period of the previous year. Net revenues before private equity and other investment-related gains improved by 18%, compared to the fourth quarter of 2005, reflecting the growth in assets under management. Private equity and other investment-related gains totaled CHF 92 million in the fourth quarter of 2006, a decrease of 56% compared to the same period of 2005. Total operating expenses increased 26% in the fourth quarter of 2006, primarily reflecting higher compensation and benefits related to the ongoing efforts to hire new investment talent and build product development and

| Media Release |

February 15, 2007 Page 4/8 |

distribution capabilities and other expenses related to the realignment of Asset Management. The pre-tax income margin was 12.1% for the fourth quarter of 2006, compared to 31.8% in the fourth quarter of 2005. Credit Suisse continued to realign Asset Management in the fourth quarter of 2006 as part of the previously announced strategy to reposition businesses with low profitability, reshape the product offering, improve investment and sales processes, and reduce the overall cost base.

Net New Assets

The Wealth Management business generated CHF 50.5 billion of net new assets in 2006, an increase of 18% compared to 2005. In the fourth quarter of 2006, Wealth Management recorded CHF 8.6 billion of net new assets. The Asset Management business reported CHF 50.8 billion of net new assets in 2006, including money market assets of CHF 33.4 billion and alternative investment assets of CHF 12.5 billion. In the fourth quarter, Asset Management recorded a net outflow of CHF 2.9 billion. Overall, Credit Suisse recorded CHF 95.4 billion of net new assets for the full year 2006, including net new assets of CHF 6.9 billion in the fourth quarter. Total assets under management were CHF 1,485.1 billion as of December 31, 2006, an increase of 13% from December 31, 2005.

Sale of the Insurance Business

On December 22, 2006, Credit Suisse Group completed the sale of Winterthur for cash consideration of CHF 12.3 billion. The Group realized a net capital gain of CHF 1,817 million on the transaction. As a result of the sale of Winterthur, the results of Winterthur’s operations are reported as income from discontinued operations, net of tax. Income from discontinued operations in the fourth quarter of 2006 was CHF 2,074 million, including the gain from the sale. For the full year 2006, income from discontinued operations was CHF 3,070 million, compared to CHF 1,310 million for the full year 2005.

Dividend Proposal and Share Repurchase Program

The Board of Directors of Credit Suisse Group will propose a cash dividend of CHF 2.24 per share for the financial year 2006 and a par value reduction of CHF 0.46 per share at the Annual General Meeting on May 4, 2007. This compares to a dividend of CHF 2.00 per share for the financial year 2005.

The Board of Directors will also propose a share repurchase program of up to CHF 8 billion at the Annual General Meeting. Subject to the approval of shareholders, the program will commence after the Annual General Meeting and run for a maximum of three years.

Outlook

Credit Suisse believes that the growth prospects for the global economy will remain good and expects client activity to continue at around the levels of 2006. Interest rates are unlikely to increase significantly and valuations for equities are still relatively low. High corporate earnings will attract capital flows into the equity markets, which will continue to trend higher with occasional corrections. Credit Suisse has had a good start to 2007 and is well positioned to capture these growth opportunities with its integrated banking model.

Information

Media Relations Credit Suisse, telephone +41 844 33 88 44, media.relations@credit-suisse.com

Investor Relations Credit Suisse, telephone +41 44 333 71 49, investor.relations@credit-suisse.com

| Media Release |

February 15, 2007 Page 5/8 |

For additional information on Credit Suisse Group’s fourth-quarter and full-year 2006 results, please refer to the Group’s Quarterly Report Q4/2006, as well as the Group’s slide presentation for analysts and the press, which are available on the Internet at: www.credit-suisse.com/results

Credit Suisse Group

As one of the world's leading banks, Credit Suisse provides its clients with investment banking, private banking and asset management services worldwide. Credit Suisse offers advisory services, comprehensive solutions and innovative products to companies, institutional clients and high-net-worth private clients globally, as well as retail clients in Switzerland. Credit Suisse is active in over 50 countries and employs approximately 45,000 people. Credit Suisse's parent company, Credit Suisse Group, is a leading global financial services company headquartered in Zurich. Credit Suisse Group's registered shares (CSGN) are listed in Switzerland and, in the form of American Depositary Shares (CS), in New York. Further information about Credit Suisse can be found at www.credit-suisse.com.

Cautionary Statement Regarding Forward-Looking Information

This press release contains statements that constitute forward-looking statements. In addition, in the future we, and others on our behalf, may make statements that constitute forward-looking statements. Such forward-looking statements may include, without limitation, statements relating to our plans, objectives or goals; our future economic performance or prospects; the potential effect on our future performance of certain contingencies; and assumptions underlying any such statements.

Words such as “believes,” “anticipates,” “expects,” "intends” and “plans” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. We do not intend to update these forward-looking statements except as may be required by applicable laws.

By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that predictions, forecasts, projections and other outcomes described or implied in forward-looking statements will not be achieved. We caution you that a number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in such forward-looking statements. These factors include (i) market and interest rate fluctuations; (ii) the strength of the global economy in general and the strength of the economies of the countries in which we conduct our operations in particular; (iii) the ability of counterparties to meet their obligations to us; (iv) the effects of, and changes in, fiscal, monetary, trade and tax policies, and currency fluctuations; (v) political and social developments, including war, civil unrest or terrorist activity; (vi) the possibility of foreign exchange controls, expropriation, nationalization or confiscation of assets in countries in which we conduct our operations; (vii) the ability to maintain sufficient liquidity and access capital markets; (viii) operational factors such as systems failure, human error, or the failure to implement procedures properly; (ix) actions taken by regulators with respect to our business and practices in one or more of the countries in which we conduct our operations; (x) the effects of changes in laws, regulations or accounting policies or practices; (xi) competition in geographic and business areas in which we conduct our operations; (xii) the ability to retain and recruit qualified personnel; (xiii) the ability to maintain our reputation and promote our brand; (xiv) the ability to increase market share and control expenses; (xv) technological changes; (xvi) the timely development and acceptance of our new products and services and the perceived overall value of these products and services by users; (xvii) acquisitions, including the ability to integrate acquired businesses successfully, and divestitures, including the ability to sell non-core assets; (xviii) the adverse resolution of litigation and other contingencies; and (xix) our success at managing the risks involved in the foregoing.

We caution you that the foregoing list of important factors is not exclusive; when evaluating forward-looking statements, you should carefully consider the foregoing factors and other uncertainties and events, as well as the risks identified in our most recently filed Form 20-F and reports on Form 6-K furnished to the US Securities and Exchange Commission.

| Media Release |

February 15, 2007 Page 6/8 |

Presentation of the fourth-quarter and full-year 2006 results

Analyst and Media Conference

§ | Thursday, February 15, 2007 |

| 09:30 CET / 08:30 GMT / 03:30 EST |

Credit Suisse Forum St. Peter, Zurich

§ | Simultaneous interpreting: German – English, English – German |

§ | Speakers |

Oswald J. Grübel, Chief Executive Officer of Credit Suisse

| Renato Fassbind, Chief Financial Officer of Credit Suisse |

§ | Internet |

Live broadcast at: www.credit-suisse.com/results

Video playback available approximately 3 hours after the event

§ | Telephone |

| Live audio dial-in on +41 91 610 5600 (Europe), +44 207 107 0611 (UK) and |

+1 866 291 4166 (US); ask for "Credit Suisse Group quarterly results".

Please dial in 10-15 minutes before the start of the presentation.

| Telephone replay available approximately 1 hour after the event on +41 91 612 4330 (Europe), |

+44 207 108 6233 (UK) and +1 866 416 2558 (US); conference ID English – 596#, conference

ID German – 311#.

|

Credit Suisse Group |

| Quarterly Report 2006/Q4 |

|

| Cover: Manish Kumar, Investment Banking (CMOS), New York Photographer: John Wildgoose |

| Financial calendar : please see inside back cover. |

| Credit Suisse Group financial highlights | ||||||||||||||||||

| 12 months | ||||||||||||||||||

| in CHF m, except where indicated | 4Q 2006 | 3Q 2006 | 4Q 2005 | Change in % from 3Q 2006 | Change in % from 4Q 2005 | 2006 | 2005 | Change in % from 2005 | ||||||||||

| Consolidated statements of income | ||||||||||||||||||

| Net revenues | 10,814 | 8,076 | 7,566 | 34 | 43 | 38,603 | 30,489 | 27 | ||||||||||

| Income from continuing operations before taxes,minority interests, extraordinary items andcumulative effect of accounting changes | 4,314 | 2,460 | 1,059 | 75 | 307 | 14,300 | 7,401 | 93 | ||||||||||

| Income from continuing operations beforeextraordinary items and cumulative effectof accounting changes | 2,599 | 1,468 | 677 | 77 | 284 | 8,281 | 4,526 | 83 | ||||||||||

| Income from discontinued operations, net of tax | 2,074 | 424 | 426 | 389 | 387 | 3,070 | 1,310 | 134 | ||||||||||

| Net income | 4,673 | 1,892 | 1,103 | 147 | 324 | 11,327 | 5,850 | 94 | ||||||||||

| Return on equity | 44.1% | 18.9% | 11.2% | – | – | 27.5% | 15.4% | – | ||||||||||

| Earnings per share, in CHF | ||||||||||||||||||

| Basic earnings per share from continuing operationsbefore cumulative effect of accounting changes | 2.42 | 1.35 | 0.59 | – | – | 7.53 | 3.98 | – | ||||||||||

| Basic earnings per share | 4.35 | 1.74 | 0.98 | – | – | 10.30 | 5.17 | – | ||||||||||

| Diluted earnings per share from continuing operationsbefore cumulative effect of accounting changes | 2.29 | 1.29 | 0.59 | – | – | 7.19 | 3.90 | – | ||||||||||

| Diluted earnings per share | 4.12 | 1.67 | 0.95 | 9.83 | 5.02 | |||||||||||||

| Cost/income ratio – reported | 60.3% | 70.0% | 86.5% | – | – | 63.2% | 76.2% | – | ||||||||||

| Cost/income ratio1) | 65.7% | 75.9% | 93.1% | – | – | 69.6% | 81.6% | – | ||||||||||

| Net new assets, in CHF bn | 6.9 | 31.1 | 8.0 | – | – | 95.4 | 57.4 | – | ||||||||||

| in CHF m, except where indicated | 31.12.06 | 30.09.06 | 31.12.05 | Change in % from 30.09.06 | Change in % from 31.12.05 | |||||||

| Assets under management, in CHF bn | 1,485.1 | 1,441.3 | 1,319.4 | 3.0 | 12.6 | |||||||

| Consolidated balance sheets | ||||||||||||

| Total assets | 1,255,956 | 2) | 1,473,113 | 1,339,052 | (15) | (6) | ||||||

| Shareholders' equity | 43,586 | 41,643 | 42,118 | 5 | 3 | |||||||

| Consolidated BIS capital data | ||||||||||||

| Risk-weighted assets | 253,676 | 252,139 | 232,891 | 1 | 9 | |||||||

| Tier 1 ratio | 13.9% | 10.8% | 11.3% | – | – | |||||||

| Total capital ratio | 18.4% | 13.2% | 13.7% | – | – | |||||||

| Number of employees | ||||||||||||

| Switzerland – Banking | 20,353 | 20,261 | 20,194 | 0 | 1 | |||||||

| Outside Switzerland – Banking | 24,518 | 24,456 | 24,370 | 0 | 1 | |||||||

| Winterthur | 0 | 2) | 18,984 | 18,959 | – | – | ||||||

| Number of employees (full-time equivalents) | 44,871 | 63,701 | 63,523 | (30) | (29) | |||||||

| Stock market data | ||||||||||||

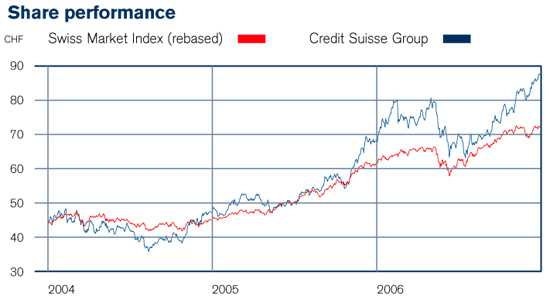

| Share price per common share, in CHF | 85.25 | 72.35 | 67.00 | 18 | 27 | |||||||

| High (closing price) year-to-date, in CHF | 85.35 | 74.20 | 68.50 | 15 | 25 | |||||||

| Low (closing price) year-to-date, in CHF | 62.70 | 62.70 | 46.85 | 0 | 34 | |||||||

| Share price per American Depositary Share, in USD | 69.85 | 57.95 | 50.95 | 21 | 37 | |||||||

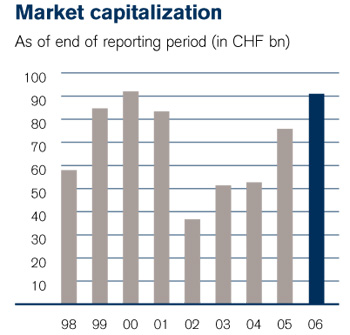

| Market capitalization, in CHF m | 90,575 | 77,946 | 75,399 | 16 | 20 | |||||||

| Market capitalization, in USD m | 74,213 | 62,432 | 57,337 | 19 | 29 | |||||||

| Book value per share, in CHF | 41.02 | 38.65 | 37.43 | 6 | 10 | |||||||

| Share information | ||||||||||||

| Shares issued | 1,214,862,013 | 1,214,054,870 | 1,247,752,166 | 0 | (3) | |||||||

| Treasury shares | (152,394,952) | (136,710,156) | (122,391,983) | 11 | 25 | |||||||

| Shares outstanding | 1,062,467,061 | 1,077,344,714 | 1,125,360,183 | (1) | (6) | |||||||

| 1) Excludes minority interest revenues of CHF 998 million, CHF 640 million, CHF 554 million, CHF 3,663 million and CHF 2,074 million and minority interest expenses of CHF 71 million, CHF 10 million, CHF 15 million, CHF 103 million and CHF 32 million in 4Q 2006, 3Q 2006, 4Q 2005, 12 months 2006 and 12 months 2005, respectively, from the consolidation of certain private equity funds and other entities in which the Group does not have a significant economic interest in such revenues and expenses. 2) The Group completed the sale of Winterthur to AXA on December 22, 2006. | ||||||||||||

Contents |

Credit Suisse Group

Contents

Enquiries

Message from the Chief Executive Officer

Dear shareholders, clients and colleagues

Strong annual results with basic earnings per share from continuing operations of CHF 7.53

Returning capital to our shareholders

Investment Banking delivers strong results

Continued expansion in Private Banking

Realignment of Asset Management

Strategic priorities going forward

Outlook

Credit Suisse Group

Summary of segment results

Investment Banking

Private Banking

Asset Management

Credit Suisse Group consolidated results

Net revenues

Provision for credit losses

Total operating expenses

Income tax expense

Minority interests

Discontinued operations

Recent developments

Dividend proposal and share repurchase program

Factors affecting results of operations

Credit Suisse Group structure

Investment Banking

Private Banking

Wealth Management

Corporate & Retail Banking

Asset Management

Assets under management

Assets under management

Client assets

Net new assets

Capital

Credit Suisse Group

Credit Suisse

Risk management

Economic Risk Capital trends

Trading risks

Loan exposure

Condensed consolidated financial statements

Consolidated statements of income (unaudited)

Consolidated balance sheets (unaudited)

Consolidated statements of changes in shareholders’ equity (unaudited)

Comprehensive income (unaudited)

Consolidated statements of cash flows (unaudited)

Consolidated statements of cash flows - continued (unaudited)

Notes to the condensed consolidated financial statements unaudited

Summary of significant accounting policies

Basis of presentation

Recently adopted accounting standards

EITF 04-5, FSP SOP 78-9-1 and EITF 96-16

SFAS 123R

SFAS 154

SFAS 155

SFAS 156

FSP FTB 85-4-1

FSP FIN 46(R)-6

SFAS 158

SAB 108

Standards to be adopted in future periods

FIN 48

SFAS 157

Discontinued operations

Segment reporting

Interest and dividend income and interest expense

Trading activities

Commissions and fees

Loans

Accumulated other comprehensive income

Earnings per share

Pension

Guarantees and commitments

Guarantees

Disposal-related contingencies and other indemnifications

Disposal-related contingencies

Other indemnifications

Other commitments

Variable interest entities

Collateralized debt obligations

Commercial paper conduits

Financial intermediation

Litigation

Information for investors

Foreign currency translation rates

Cautionary statement regarding forward-looking information

| Enquiries |

| Credit Suisse Group Investor Relations Ian Roundell, Marc Buchheister Tel. +41 44 333 7149 Fax +41 44 333 2587 investor.relations@credit-suisse.com Credit Suisse Group Media Relations Charles Naylor, Andrés Luther Tel. +41 844 33 8844 Fax +41 44 333 8877 media.relations@credit-suisse.com |

Message from the Chief Executive Officer |

|

| Oswald J. Grübel |

| Chief Executive Officer |

| Dear shareholders, clients and colleagues |

| 2006 was a record year for Credit Suisse. Our integrated banking model proved successful and provided us with an effective platform to capture the growth opportunities arising from high levels of client activity while significantly improving our profitability. We are particularly pleased with our performance in Investment Banking. In our first year as an integrated bank we made excellent progress in strengthening our operating efficiency but there is still great potential for further improvement as we continue to invest in the growth of our business. Our clients have responded well to our integrated approach and Credit Suisse now has excellent opportunities for further growth in the context of globalization, which we believe will create dynamic markets for the foreseeable future. |

| Strong annual results with basic earnings per share from continuing operations of CHF 7.53 |

| Credit Suisse Group reported a significant improvement in profitability in 2006, driven by good net revenues and improved operating efficiency. Net income totaled CHF 11.3 billion, including a net capital gain of CHF 1.8 billion from the sale of Winterthur, which was recorded in the fourth quarter of 2006. Income from continuing operations was CHF 8.3 billion or CHF 7.53 per share. Basic earnings per share were CHF 10.30. Our return on equity improved significantly to 27.5% in 2006 from 15.4% in 2005. In the fourth quarter of 2006, net income rose to CHF 4.7 billion, compared to CHF 1.1 billion in the fourth quarter of 2005. We generated net new assets of CHF 95.4 billion in 2006, compared to CHF 57.4 billion in 2005. |

| Returning capital to our shareholders |

| Credit Suisse Group today has the strongest capital base in its history. We are pleased that we have the requisite resources to grow our business while, at the same time, returning capital to our shareholders. At the forthcoming Annual General Meeting on May 4, 2007, the Board of Directors of Credit Suisse Group will ask the shareholders to approve a further share buyback program of up to CHF 8 billion over three years. It will also propose a distribution of CHF 2.70 per share for the financial year 2006, comprising a cash dividend of CHF 2.24 per share and a par value reduction of CHF 0.46 per share. |

| Investment Banking delivers strong results |

| We achieved record results in Investment Banking in 2006, reflecting a strong performance in all key businesses and regions amid favorable market conditions, high levels of client activity and improved market share in a range of products. Against this backdrop, we generated record revenues in advisory and debt and equity underwriting and significantly increased our trading revenues. Income from continuing operations before taxes grew by 272% compared to 2005. Excluding credits from insurance settlements for litigation and related costs in 2006 and a charge to increase litigation reserves in 2005, income from continuing operations before taxes grew by 113%. Our strong results reflect continued progress against our strategy to deliver a more profitable business. Highlights in Investment Banking in 2006 included our continued leadership position in some of the world’s fastest growing emerging markets, such as China, Russia, Brazil and Mexico. This was demonstrated, among other things, by our number one market share ranking in equity issuance and announced mergers and acquisitions in Latin America and our recognition as the “China Equity House” in International Financing Review’s Asia Awards 2006. Credit Suisse was presented with the “European IPO House of the Year” award in the annual Financial News Awards for Excellence in Investment Banking for 2006. In addition The Banker magazine’s annual Investment Banking Awards 2006 recognized Credit Suisse as the “Best Bank of the Year for IPOs.” We also maintained our leadership position in other important growth areas such as commercial mortgage-backed securities, leveraged finance and financial sponsors. We advised on a number of notable transactions that were announced in the fourth quarter of the year, including Google Inc.’s acquisition of YouTube, the sale of Raytheon Aircraft Company to Hawker Beechcraft Corporation and the acquisition of Corus Group plc by Tata Steel. |

| Continued expansion in Private Banking |

| In our Private Banking segment, which comprises the Wealth Management and Corporate & Retail Banking businesses, we delivered very strong results with significantly higher net revenues in 2006. This revenue growth outpaced an increase in total operating expenses driven partly by ongoing strategic investments in the Wealth Management business. This resulted in record income from continuing operations before taxes for 2006. Asset gathering also reached a record level, with net new assets of CHF 50.5 billion in Wealth Management, representing a growth rate of 7.3%. We continued to expand our global reach in Wealth Management through 2006 and announced the launch of new onshore operations in Brazil, Russia, Australia, Qatar and Lebanon. |

| Realignment of Asset Management |

| In our Asset Management segment, we generated strong net new assets of CHF 50.8 billion in 2006, including alternative investment assets of CHF 12.5 billion. Our net revenues before private equity and other investment-related gains increased 12%, driven by higher asset management revenues and private equity commissions and fees. Income from continuing operations before taxes decreased by half compared to 2005, reflecting higher total operating expenses, partly due to realignment expenses, and lower private equity and other investment-related gains. We achieved further progress in the realignment of Asset Management during the fourth quarter of the year, as part of the previously announced strategy to reposition businesses with low profitability, reshape the product offering, improve investment and sales processes and reduce the overall cost base. In addition, we continued to invest in expanding the geographic footprint of our Asset Management business in key markets in 2006, while also taking steps to broaden our alternative investment business with a series of strategic alliances aimed at adding new capabilities and at increasing our product offering. |

| Strategic priorities going forward |

| We have defined three clear strategic priorities in order to accelerate the expansion of our business going forward. We will continue to capitalize on our integrated banking model by building on a series of targeted internal initiatives that drive revenue growth and reduce costs. We will deploy our capital as efficiently as possible. The target for our investments is an annual rate of return of 20% or above in the medium term. We will continue to expand our activities in high-growth markets and products. For example, we signed an agreement to acquire the Brazilian asset manager Hedging-Griffo in the fourth quarter of 2006. This strategic step will help us to leverage our integrated banking model in Brazil to provide a comprehensive range of investment banking, private banking and asset management services to onshore clients in this market. We also aim to realize our third priority through measures such as the expansion of our activities in dynamic emerging markets and the growth of leading businesses and products, including alternative investments and structured products. Our objective is to generate long-term, sustainable returns. We will therefore focus on and invest in businesses which fit our model and are in line with that objective. |

| Outlook |

| The growth prospects for the global economy remain good and we expect client activity to continue at around the levels of 2006. Interest rates are unlikely to increase significantly and valuations for equities are still relatively low. High corporate earnings will attract capital flows into the equity markets, which will continue to trend higher with occasional corrections. We have had a good start to 2007 and are well positioned to capture these growth opportunities with our integrated banking model. Yours sincerely Oswald J. Grübel February 2007 |

Credit Suisse Group |

| Credit Suisse Group reported net income of CHF 4,673 million in the fourth quarter of 2006, an increase of CHF 3,570 million compared to the fourth quarter of 2005. Fourth quarter net income included a net capital gain of CHF 1,817 million from the sale of Winterthur. Net income for the full year 2006 was CHF 11,327 million, an increase of CHF 5,477 million, or 94%, compared to the full year 2005. Income from continuing operations in 2006 was CHF 8,281 million, an increase of 83%. In the fourth quarter, Investment Banking results improved significantly as a result of favorable market conditions and increased client and deal activity. Private Banking also reported good results as higher revenues associated with client activity were partially offset by higher compensation expenses, including costs of strategic investments in the Wealth Management business. Asset Management results declined reflecting lower private equity and other investment-related gains and higher compensation and other operating expenses, partly due to the business realignment. |

Summary of segment results |

| Investment Banking |

| Investment Banking reported record income from continuing operations before taxes of CHF 2,342 million in the fourth quarter of 2006, an increase of CHF 2,056 million compared to the fourth quarter of 2005. These results reflected strong performance across all key business areas and regions amid favorable market conditions, high levels of deal activity and improved market share in certain products. For the full year 2006, Investment Banking reported income from continuing operations before taxes of CHF 5,951 million, an increase of CHF 4,352 million compared to the full year 2005. Excluding the CHF 508 million credits from insurance settlements for litigation and related costs in 2006 and the CHF 960 million charge to increase litigation reserves in 2005, income from continuing operations before taxes for the full year 2006 increased 113% compared to the full year 2005. |

| Private Banking |

| Private Banking reported record income from continuing operations before taxes of CHF 1,143 million in the fourth quarter of 2006, CHF 117 million, or 11%, above the fourth quarter of 2005. The fourth quarter of 2006 was characterized by strong equity markets, which led to strong client activity and a 9% increase in revenues. Operating expenses increased 9%, reflecting ongoing strategic investments in international growth in the Wealth Management business and new business initiatives in Corporate & Retail Banking. Full year 2006 income from continuing operations before taxes was a record CHF 4,596 million, 16% higher than in 2005. Private Banking reported net new assets of CHF 9.7 billion in the fourth quarter of 2006 and CHF 52.2 billion in full year 2006. Assets under management were CHF 940.3 billion as of December 31, 2006, an increase of 12.3% compared to December 31, 2005. |

| Asset Management |

| Asset Management income from continuing operations before taxes was CHF 89 million in the fourth quarter of 2006, a decrease of CHF 152 million, or 63%, from the fourth quarter of 2005. This reflected lower private equity and other investment-related gains compared to the strong fourth quarter of 2005 and higher operating expenses, partly due to realignment costs. Full year 2006 income from continuing operations before taxes was CHF 508 million, a decrease of 50% from the full year 2005. Asset Management reported a net asset outflow of CHF 2.9 billion in the fourth quarter of 2006 and net new assets of CHF 50.8 billion in full year 2006. Assets under management increased to CHF 669.9 billion as of December 31, 2006 from CHF 589.4 billion as of December 31, 2005. |

Credit Suisse Group consolidated results |

| The Group recorded net income of CHF 4,673 million in the fourth quarter of 2006, an increase of CHF 3,570 million compared to the fourth quarter of 2005. Fourth quarter net income included a net capital gain of CHF 1,817 million from the sale of Winterthur. Basic earnings per share increased to CHF 4.35, compared with CHF 0.98 in the fourth quarter of 2005. The return on equity in the fourth quarter of 2006 was 44.1% compared to 11.2% in the fourth quarter of 2005. |

| Income from continuing operations before extraordinary items and cumulative effect of accounting changes for the fourth quarter of 2006 was CHF 2,599 million or CHF 2.42 per share. This compares to CHF 677 million or CHF 0.59 per share in the fourth quarter of 2005. |

| Full year net income was CHF 11,327 million, an increase of 5,477 million, or 94%, compared to full year 2005. Full year 2006 basic earnings per share improved to CHF 10.30. Full year 2006 return on equity was 27.5%, compared to 15.4% in 2005. For the full years 2006 and 2005, income from continuing operations before extraordinary items and cumulative effect of accounting changes was CHF 8,281 million and CHF 4,526 million, or CHF 7.53 and CHF 3.98 per share, respectively. |

| Net revenues |

| The Group reported net revenues of CHF 10,814 million in the fourth quarter of 2006, an increase of CHF 3,248 million, or 43%, compared to the fourth quarter of 2005. Full year 2006 net revenues were CHF 38,603 million, 27% above full year 2005. |

| Net interest income was 9% higher in the fourth quarter of 2006 compared to the fourth quarter of 2005, primarily reflecting an increase in Private Banking largely due to an increase in liability margins and volumes. |

| Commissions and fees increased 25% compared to the fourth quarter of 2005, primarily as a result of higher underwriting and advisory fees in Investment Banking, and to a lesser extent, higher brokerage and issuing fees in Private Banking due to stronger client activity. |

| The following tables set forth an overview of segment results for the fourth quarter of 2006 and 2005, respectively: | ||||||||||||

| 4Q 2006, in CHF m | Investment Banking | Private Banking | Asset Management | Corporate Center | 1) | Credit Suisse Group | ||||||

| Net revenues | 6,085 | 2,973 | 738 | 1,018 | 10,814 | |||||||

| Provision for credit losses | 20 | (41) | 1 | 0 | (20) | |||||||

| Compensation and benefits | 2,566 | 1,037 | 327 | 170 | 4,100 | |||||||

| Other expenses | 1,157 | 834 | 321 | 108 | 2,420 | |||||||

| Total operating expenses | 3,723 | 1,871 | 648 | 278 | 6,520 | |||||||

| Income from continuing operations before taxes and minority interests | 2,342 | 1,143 | 89 | 740 | 4,314 | |||||||

| 4Q 2005, in CHF m | Investment Banking | Private Banking | Asset Management | Corporate Center | 1) | Credit Suisse Group | ||||||

| Net revenues | 3,735 | 2,716 | 757 | 358 | 7,566 | |||||||

| Provision for credit losses | (13) | (21) | 0 | 0 | (34) | |||||||

| Compensation and benefits | 2,136 | 888 | 252 | 708 | 3,984 | |||||||

| Other expenses | 1,326 | 823 | 264 | 144 | 2,557 | |||||||

| Total operating expenses | 3,462 | 1,711 | 516 | 852 | 6,541 | |||||||

| Income/(loss) from continuing operations before taxes and minority interests | 286 | 1,026 | 241 | (494) | 1,059 | |||||||

| 1) Includes consolidation eliminations, revenues and expenses from certain parent company investments and certain other revenues and expenses not allocated to the segments. Also includes minority interest revenues of CHF 998 million and CHF 554 million in 4Q 2006 and 4Q 2005, respectively, and minority interest expenses of CHF 71 million and CHF 15 million in 4Q 2006 and 4Q 2005, respectively, from the consolidation of certain private equity funds and other entities in which the Group does not have a significant economic interest in such income. | ||||||||||||

| The following table presents the Group's condensed consolidated statements of income: | ||||||||||||||||||

| 12 months | ||||||||||||||||||

| in CHF m | 4Q 2006 | 3Q 2006 | 4Q 2005 | Change in % from 3Q 2006 | Change in % from 4Q 2005 | 2006 | 2005 | Change in % from 2005 | ||||||||||

| Net revenues | 10,814 | 8,076 | 7,566 | 34 | 43 | 38,603 | 30,489 | 27 | ||||||||||

| Provision for credit losses | (20) | (40) | (34) | (50) | (41) | (111) | (144) | (23) | ||||||||||

| Compensation and benefits | 4,100 | 3,427 | 3,984 | 20 | 3 | 15,697 | 13,974 | 12 | ||||||||||

| Other expenses | 2,420 | 2,229 | 2,557 | 9 | (5) | 8,717 | 9,258 | (6) | ||||||||||

| Total operating expenses | 6,520 | 5,656 | 6,541 | 15 | 0 | 24,414 | 23,232 | 5 | ||||||||||

| Income from continuing operations before taxes,minority interests, extraordinary items andcumulative effect of accounting changes | 4,314 | 2,460 | 1,059 | 75 | 307 | 14,300 | 7,401 | 93 | ||||||||||

| Income tax expense/(benefit) | 805 | 367 | (108) | 119 | – | 2,389 | 927 | 158 | ||||||||||

| Minority interests | 910 | 625 | 490 | 46 | 86 | 3,630 | 1,948 | 86 | ||||||||||

| Income from continuing operations beforeextraordinary items and cumulative effectof accounting changes | 2,599 | 1,468 | 677 | 77 | 284 | 8,281 | 4,526 | 83 | ||||||||||

| Income from discontinued operations, net of tax | 2,074 | 424 | 426 | 389 | 387 | 3,070 | 1,310 | 134 | ||||||||||

| Extraordinary items, net of tax | 0 | 0 | 0 | – | – | (24) | 0 | – | ||||||||||

| Cumulative effect of accounting changes, net of tax | 0 | 0 | 0 | – | – | 0 | 14 | (100) | ||||||||||

| Net income | 4,673 | 1,892 | 1,103 | 147 | 324 | 11,327 | 5,850 | 94 | ||||||||||

| Trading revenues increased 130% compared to the fourth quarter of 2005, primarily reflecting Investment Banking’s strong trading revenues in the fourth quarter of 2006, in particular in fixed income. |

| Other revenues in the fourth quarter of 2006 increased 46%, compared to the fourth quarter of 2005, which was the result of higher minority interest-related revenues from consolidated private equity funds and other entities in which the Group does not have a significant economic interest in such revenues. |

| Provision for credit losses |

| The Group reported a net release of provisions for credit losses of CHF 20 million in the fourth quarter of 2006 compared to a net release of CHF 34 million in the fourth quarter of 2005. For the full year 2006, the net release of provision for credit losses was CHF 111 million compared to CHF 144 million in 2005. While the credit environment is likely to remain favorable in the near term, we do not expect these very benign conditions to continue. |

| Total operating expenses |

| The Group reported total operating expenses of CHF 6,520 million in the fourth quarter of 2006, CHF 21 million below the fourth quarter of 2005. Compensation and benefits increased CHF 116 million, or 3%, to CHF 4,100 million compared to the fourth quarter of 2005, which included a CHF 630 million expense, recorded in the Corporate Center, relating to a change in the Group’s accounting for share-based compensation awards subject to a non-competition provision that have scheduled vesting beyond an employee’s eligibility for early retirement. In the fourth quarter of 2006, compensation and benefits primarily reflected higher performance-based compensation in Investment Banking and Private Banking. |

| Other expenses in the fourth quarter of 2006 were CHF 2,420 million, a decrease of CHF 137 million, or 5%, compared to the fourth quarter of 2005 primarily reflecting lower professional fees, a credit from an insurance settlement and lower travel and entertainment expenses in Investment Banking offset by realignment costs in Asset Management. |

| For the full year 2006, the Group reported total operating expenses of CHF 24,414 million, an increase of CHF 1,182 million, or 5%, compared to the previous year. Full year 2006 expenses included credits from insurance settlements for litigation and related costs of CHF 508 million. Full year 2005 expenses included the reserve for private litigation matters of CHF 960 million and a CHF 630 million expense relating to the above-mentioned change in the Group’s accounting for share-based compensation awards. Excluding these items, total operating expenses increased 15%, primarily as a result of higher performance-based compensation expenses in Investment Banking and Private Banking. |

| Income tax expense |

| The Group recorded income tax expense of CHF 805 million in the fourth quarter of 2006 reflecting the Group's higher income from continuing operations before taxes. This compared to a net tax benefit of CHF 108 million in the fourth quarter of 2005, reflecting the release of tax contingency accruals and the impact of the above-mentioned change in the Group’s accounting for share-based compensation awards. |

| The Group tax expense is not affected by minority interest revenues and expenses from consolidated private equity and other entities in which the Group does not have a significant economic interest in such revenues and expenses. The amount of non-taxable income relating to these investments varies from one period to the next and was CHF 927 million in the fourth quarter of 2006 compared to CHF 539 million in the fourth quarter of 2005. The Group’s effective tax rate in the fourth quarter of 2006 was 19%. Excluding the effect of non-taxable income from these investments, the Group’s effective tax rate in the fourth quarter of 2006 was 24%. The Group’s effective tax rate in the fourth quarter of 2005 was negative as a result of the release of tax contingency accruals and the impact of the above-mentioned change in the Group’s accounting for share-based awards. |

| Minority interests |

| Minority interests were CHF 910 million in the fourth quarter of 2006, an increase of CHF 420 million compared to the fourth quarter of 2005. This increase was primarily due to revenues from certain private equity funds and other entities that were consolidated for the first time in 2006. For further details, see “Notes to the condensed consolidated financial statements - unaudited - Recently adopted accounting standards.” |

| The Group’s net revenues and operating expenses reflect the consolidation of certain private equity funds and other entities in which the Group does not have a significant economic interest in such revenues and expenses. The consolidation of these entities does not affect net income as the amounts recorded in net revenues and expenses are offset by corresponding amounts reported as minority interests. This minority interest income, which is reported in the Corporate Center, was CHF 927 million in the fourth quarter of 2006, and is comprised of revenues of CHF 998 million, primarily other revenues, and compensation and other expenses of CHF 71 million. |

| Discontinued operations |

| On December 22, 2006, the Group completed the sale of Winterthur for cash consideration of CHF 12.3 billion. The Group realized a net capital gain of CHF 1,817 million on the transaction. As a result of the sale of Winterthur, the results of operations of Winterthur are reflected in Income from discontinued operations, net of tax in the consolidated statements of income for all periods presented. Income from discontinued operations in the fourth quarter of 2006 was CHF 2,074 million, including the gain from the sale. For full year 2006, income from discontinued operations was CHF 3,070 million compared to CHF 1,310 million for full year 2005. |

| For further details, see “Notes to the condensed consolidated financial statements - unaudited - Discontinued operations.” |

|

|

|

Credit Suisse Group structure |

| The Group’s business consists of three segments: Investment Banking, Private Banking and Asset Management. The three segments are complemented by Shared Services, which provides support in the areas of finance, legal and compliance, risk management and information technology. Prior period results presented in this Quarterly Report have been revised to reflect the operational and management structure in place during 2006. |

| The Group’s segments are managed and reported on a pre-tax basis. Minority interest-related revenues and expenses resulting from the consolidation of certain private equity funds and other entities in which the Group does not have a significant economic interest in such revenues and expenses are reported in the Corporate Center. Net income is unaffected by the consolidation of these entities due to offsetting minority interests. |

|

Recent developments |

| Credit Suisse remains focused on its strategy to provide more value to its clients through its integrated banking model and active growth of its global footprint. During the fourth quarter of 2006, Credit Suisse announced additional onshore operations in the high-growth market of Brazil through the acquisition of Hedging-Griffo. Hedging-Griffo is a leading asset management company with a large and well-established client base and also serves high-net-worth individuals through its private banking platform in Brazil. It manages CHF 9.2 billion in assets under management for high-net worth individuals in Brazil and over the past three years has increased these assets at an average annual growth rate of 38.5%. This acquisition will support Credit Suisse’s integrated banking model by adding significant scale to its onshore asset management business, strengthen its private banking businesses and complement Credit Suisse’s position as a premier investment bank in Brazil. This transaction is expected to close by the middle of 2007, subject to regulatory approval. |

Dividend proposal and share repurchase program |

| Credit Suisse Group’s Board of Directors will propose a distribution of CHF 2.70 per share to the shareholders at the Annual General Meeting on May 4, 2007. The proposed distribution consists of a cash dividend of CHF 2.24, to be paid out on May 10, 2007, and a par value reduction of CHF 0.46, to be paid out on July 18, 2007. Both distributions are subject to approval at the Annual General Meeting. |

| The Board of Directors will also propose a new share repurchase program of up to CHF 8 billion at the Annual General Meeting. If approved by the shareholders, the program will commence after the Annual General Meeting and last for a maximum of three years. The shares would be repurchased through a second trading line on virt-x and cancelled. |

Factors affecting results of operations |

| The fourth quarter of 2006 was characterized by strong global equity markets, supported by solid company earnings and economic growth, modest inflation fears and a favorable interest rate environment across all regions. US stock markets were consistently buoyant throughout the period, as all major indices reported an increase, with the Dow Jones Industrial Average up 7%, the S&P 500 up 6% and the Nasdaq Composite Index up 7%. |

| European stock markets also improved during the quarter, as the Swiss Market Index increased 4%, the FTSE 100 4% and the German DAX 10%. Key markets in Asia also showed improvement, with the Nikkei increasing 7% during the quarter. Positive market developments resulted in strong trading conditions across all markets. |

| US interest rates were steady as the US Federal Reserve held the target federal funds rate at 5.25% during the fourth quarter of 2006. The European Central Bank raised its target rate in the quarter, reaching a five-year high of 3.5%, and indicated that further increases could be expected, although at a slower pace. The Bank of Japan kept its key interest rate stable at 0.25%, reflecting the recent weak economic data. The Swiss National Bank raised its target three-month Libor by 0.25% in December, citing expected continued economic growth throughout 2007. |

| Global debt underwriting activity recovered from two consecutive quarters of decreasing volumes to set an annual issuance record. The fourth quarter of 2006 ranked as the second highest quarter ever. A high level of financing activity and mergers and acquisitions activity across many sectors helped drive debt issuance volume, with both investment grade and high-yield debt volumes up from the fourth quarter of 2005. |

| Global equity underwriting volumes reached record levels in the quarter and for the year, driven by the continued recovery in the initial public offering market and the revival of convertible issuances. Global initial public offering volume rose for the third successive year, surpassing the previous record in 2000. On a regional basis, Europe accounted for the largest number and dollar volume of IPOs, and China was highest on an individual country basis. |

| The volume of announced mergers and acquisitions transactions in the fourth quarter represented the busiest quarter of the year and was higher than the fourth quarter of 2005. The total volume of announced mergers and acquisitions transactions in 2006 exceeded the previous record set in 2000. Financial sponsors continued to drive mergers and acquisitions activity, and European volume growth outpaced the US compared to the prior year. |

Investment Banking |

| Investment Banking provides financial advisory, lending and capital raising services and sales and trading to institutional, corporate and government clients worldwide. |

| Investment Banking reported record income from continuing operations before taxes of CHF 2,342 million in the fourth quarter of 2006, an increase of CHF 2,056 million, compared to the fourth quarter of 2005. These results reflected strong performance across all key business areas and regions amid favorable market conditions, high levels of deal activity and improved market share in certain products. The weakening of the average rate of the US dollar against the Swiss franc from the fourth quarter of 2005 adversely affected revenues and favorably impacted expenses. |

| For the full year 2006, Investment Banking reported income from continuing operations before taxes of CHF 5,951 million, an increase of CHF 4,352 million compared to the full year 2005. Excluding the CHF 508 million of credits from insurance settlements for litigation and related costs in 2006 and the CHF 960 million charge to increase litigation reserves in 2005, income from continuing operations before taxes for the full year 2006 increased 113% compared to the full year 2005. |

| Investment Banking’s progress in implementing its strategy to deliver a more profitable franchise positioned it to capitalize on favorable market conditions prevalent during 2006. Consequently, Investment Banking was able to achieve a number of its financial objectives set out in December 2004 and continues to make incremental progress in other areas of its strategy. For the full year 2006, Investment Banking delivered strong revenue growth and began to make progress on cost management initiatives. |

| Investment Banking will continue to build upon its existing strong franchises, including the emerging markets, leveraged finance and mortgage businesses. In 2006, Credit Suisse maintained its leading position in some of the fastest growing emerging markets, including China, Russia, Brazil and Mexico. The acquisition of Hedging-Griffo is expected to complement Credit Suisse’s position as a premier investment bank in Brazil. In addition, Investment Banking will continue to grow businesses where there are gaps to peers, such as prime services, commodities and derivatives, with an aim to further diversify its revenue mix and reduce earnings volatility. With this foundation in place, Investment Banking is well positioned to leverage revenue synergies obtained through the integrated bank, with a strong focus on delivering solutions and support to Private Banking and Asset Management clients. |

| In the fourth quarter of 2006, pre-tax income margin was 38.5%, and pre-tax return on average economic risk capital was 58.2%, compared to 7.7% and 10.8%, respectively, in the fourth quarter of 2005. For the full year 2006, pre-tax income margin was 29.1%, and pre-tax return on average economic risk capital was 40.3%. Excluding the insurance settlements, pre-tax income margin for the full year 2006 was 26.6%, and pre-tax return on average economic risk capital was 37.1%. |

| Net revenues were a record CHF 6,085 million, up CHF 2,350 million, or 63%, in the fourth quarter of 2006 compared to the fourth quarter of 2005, reflecting strong performance in both the investment banking and trading businesses. This revenue growth was well diversified, spread across most product classes and regions. In US dollar terms, net revenues were up 75%, compared to the fourth quarter of 2005. For the full year 2006, net revenues were CHF 20,469 million, up CHF 4,922 million, or 32%, compared to the full year 2005. |

| Provisions for credit losses were CHF 20 million in the fourth quarter of 2006, compared to a net release of CHF 13 million in the fourth quarter of 2005. Compared to September 30, 2006, total impaired loans decreased CHF 65 million to CHF 188 million, and valuation allowances as a percentage of total impaired loans increased 35 percentage points to 136% as of December 31, 2006. The overall credit environment continued to be favorable in the fourth quarter of 2006. While the credit environment is likely to remain favorable in the near term, the very benign credit environment is not expected to continue, which may result in a modest increase in net new provision levels towards the end of 2007. |

| Total operating expenses were CHF 3,723 million in the fourth quarter of 2006, up CHF 261 million, or 8%, compared to the fourth quarter of 2005. In US dollar terms, total operating expenses were up 15% compared to the fourth quarter of 2005. Compensation and benefits increased CHF 430 million, or 20%, due primarily to higher compensation expenses in line with higher revenues, with discretionary bonus representing a considerable portion of the total amount. Compensation and benefits for a given year are determined by the strength and breadth of business results, staffing levels and the impact of share-based compensation programs. The compensation/ revenue ratio of 42.2% in the fourth quarter of 2006 was significantly lower than the 53.5% in the first three quarters of 2006 due to the strong revenue performance in the quarter. Other expenses decreased CHF 169 million, or 13%, from the fourth quarter of 2005, indicating progress made in improving Investment Banking’s operating efficiency. Other expenses in the fourth quarter of 2006 reflected lower professional fees, a credit from an insurance settlement for litigation and related costs of CHF 34 million and lower travel and entertainment expenses, partially offset by higher commissions in line with higher transaction volumes. Other expenses in the fourth quarter of 2005 included a contingency accrual of CHF 28 million for value-added tax and CHF 24 million for premiums paid for policies acquired in the expanded life insurance finance business. |

| For the full year 2006, total operating expenses were CHF 14,556 million, up CHF 535 million, or 4%, compared to the full year 2005. Excluding the 2006 insurance settlements and the 2005 litigation charge, total operating expenses increased CHF 2,003 million, or 15%. Compensation and benefits increased CHF 1,640 million, or 19%, due to higher compensation expenses in line with higher revenues, with discretionary bonus representing a considerable portion of the total amount. The compensation/revenue ratio of 50.1% in 2006 was below the targeted level of 53.5% and a decline from 55.5% for the full year 2005. Other expenses decreased CHF 1,105 million, or 20%, compared to the full year 2005. Excluding the insurance settlements and the litigation charge, other expenses were up CHF 363 million, or 8%, from the full year 2005, due primarily to higher commissions in line with higher business activity, higher professional fees due to increased deal activity and the Centers of Excellence start-up initiatives and higher premises and equipment expenses. |

| The following table presents the results of the Investment Banking segment: | ||||||||||||||||||

| 12 months | ||||||||||||||||||

| in CHF m | 4Q 2006 | 3Q 2006 | 4Q 2005 | Change in % from 3Q 2006 | Change in % from 4Q 2005 | 2006 | 2005 | Change in % from 2005 | ||||||||||

| Net interest income | 347 | 688 | 421 | (50) | (18) | 2,640 | 3,372 | (22) | ||||||||||

| Commissions and fees | 2,836 | 1,853 | 1,984 | 53 | 43 | 8,941 | 6,709 | 33 | ||||||||||

| Trading revenues | 2,713 | 1,580 | 1,203 | 72 | 126 | 8,368 | 4,931 | 70 | ||||||||||

| Other revenues | 189 | 70 | 127 | 170 | 49 | 520 | 535 | (3) | ||||||||||

| Total noninterest revenues | 5,738 | 3,503 | 3,314 | 64 | 73 | 17,829 | 12,175 | 46 | ||||||||||

| Net revenues | 6,085 | 4,191 | 3,735 | 45 | 63 | 20,469 | 15,547 | 32 | ||||||||||

| Provision for credit losses | 20 | (19) | (13) | – | – | (38) | (73) | (48) | ||||||||||

| Compensation and benefits | 2,566 | 2,241 | 2,136 | 15 | 20 | 10,261 | 8,621 | 19 | ||||||||||

| Other expenses | 1,157 | 1,211 | 1,326 | (4) | (13) | 4,295 | 1) | 5,400 | 2) | (20) | ||||||||

| Total operating expenses | 3,723 | 3,452 | 3,462 | 8 | 8 | 14,556 | 14,021 | 4 | ||||||||||

| Income from continuingoperations before taxes | 2,342 | 758 | 286 | 209 | – | 5,951 | 1,599 | 272 | ||||||||||

| 1) Includes credits from insurance settlements for litigation and related costs of CHF 508 million, of which CHF 34 million relates to 4Q 2006. 2) Includes a CHF 960 million charge to increase the reserve for certain private litigation matters. | ||||||||||||||||||

| The following table presents the revenue details of the Investment Banking segment: | ||||||||||||||||||

| 12 months | ||||||||||||||||||

| in CHF m | 4Q 2006 | 3Q 2006 | 4Q 2005 | Change in % from 3Q 2006 | Change in % from 4Q 2005 | 2006 | 2005 | Change in % from 2005 | ||||||||||

| Debt underwriting | 686 | 451 | 394 | 52 | 74 | 2,206 | 1,484 | 49 | ||||||||||

| Equity underwriting | 484 | 224 | 343 | 116 | 41 | 1,270 | 931 | 36 | ||||||||||

| Underwriting | 1,170 | 675 | 737 | 73 | 59 | 3,476 | 2,415 | 44 | ||||||||||

| Advisory and other fees | 785 | 377 | 448 | 108 | 75 | 1,900 | 1,475 | 29 | ||||||||||

| Total investment banking | 1,955 | 1,052 | 1,185 | 86 | 65 | 5,376 | 3,890 | 38 | ||||||||||

| Fixed income | 2,755 | 2,137 | 1,566 | 29 | 76 | 9,598 | 7,004 | 37 | ||||||||||

| Equity | 1,596 | 1,062 | 1,021 | 50 | 56 | 5,881 | 4,340 | 36 | ||||||||||

| Total trading | 4,351 | 3,199 | 2,587 | 36 | 68 | 15,479 | 11,344 | 36 | ||||||||||

| Other (including loan portfolio) | (221) | (60) | (37) | 268 | 497 | (386) | 313 | – | ||||||||||

| Net revenues | 6,085 | 4,191 | 3,735 | 45 | 63 | 20,469 | 15,547 | 32 | ||||||||||

| Total investment banking revenues include debt underwriting, equity underwriting and advisory and other fees. In the fourth quarter of 2006, investment banking revenues were a record CHF 1,955 million, up CHF 770 million, or 65%, compared to the fourth quarter of 2005, reflecting record revenues in all key businesses, which were positively impacted by favorable market conditions, high levels of deal activity and volumes and improved market share in certain products in the quarter. For the full year 2006, total investment banking revenues were also a record CHF 5,376 million, up CHF 1,486 million, or 38%, from the full year 2005. These results reflected Credit Suisse’s participation in several high profile transactions, certain improvements in market share and an increase in the breadth and diversity of the business. Credit Suisse's emerging markets business demonstrated increased strength during the year with a number one market share ranking in equity issuance and announced mergers and acquisitions in Latin America for the full year 2006 and its recognition as the "China Equity House" from International Financing Review’s Asia Awards 2006. |

| Debt underwriting revenues were CHF 686 million in the fourth quarter of 2006, up CHF 292 million, or 74%, compared to the fourth quarter of 2005. These results primarily reflected significantly higher revenues in leveraged finance, which benefited from higher industry-wide issuance volumes, improved market share and continued strength in the financial sponsor client base. During the quarter, Credit Suisse executed the combined high-yield bond offering and syndicated loan facility in connection with the leveraged buyout of Freescale Semiconductor by a private equity consortium, representing the largest amount of high-yield net new money raised in a single day. The investment grade capital markets business had good revenue growth compared to the fourth quarter of 2005, in line with the focus on profitability in this business. For the full year 2006, debt underwriting revenues were CHF 2,206 million, up CHF 722 million, or 49%, compared to the full year 2005, due primarily to more favorable market conditions and increased market share. For the full year 2006, Credit Suisse ranked third in global high-yield securities new issuance volumes. |

| Equity underwriting revenues in the fourth quarter of 2006 were CHF 484 million, up CHF 141 million, or 41%, compared to the fourth quarter of 2005, primarily reflecting higher industry-wide equity issuance activity and improved global equity market share. For the full year 2006, equity underwriting revenues were CHF 1,270 million, up CHF 339 million, or 36%, from the full year 2005, primarily reflecting record industry-wide equity issuance volumes resulting from improvement in both the initial public offering and convertibles markets. Credit Suisse ranked fourth in global initial public offering market share for the full year 2006, down from first in the full year 2005, despite its higher global initial public offering new issuance volumes in 2006 in line with industry trends. Credit Suisse also maintained a leading position in financial sponsor-backed equity offerings. During the quarter, Credit Suisse was a joint bookrunner in the largest initial public offering to date for the Industrial and Commercial Bank of China Limited, China’s leading commercial bank, and also participated in a number of other key equity transactions across a broad range of industries and geographies. The Banker magazine's annual Investment Banking Awards 2006 recognized Credit Suisse as the "Best Bank of the Year for IPOs." In Europe, Credit Suisse was presented with the "European IPO House of the Year” award in the annual Financial News Awards for Excellence in Investment Banking for 2006. |

| Advisory and other fees were CHF 785 million in the fourth quarter of 2006, up CHF 337 million, or 75%, compared to the fourth quarter of 2005, due primarily to increased activity and a number of high-fee transactions in the fourth quarter of 2006. Credit Suisse ranked fourth in global announced mergers and acquisitions and seventh in global completed mergers and acquisitions in the fourth quarter of 2006, up from thirteenth and eighth, respectively, in the fourth quarter of 2005. Notable transactions announced in the fourth quarter of 2006 reflected the breadth of Credit Suisse’s advisory business and included Google, Inc.’s acquisition of YouTube, the sale of Raytheon Aircraft Company to Hawker Beechcraft Corporation and the acquisition of Corus Group plc by Tata Steel. For the full year 2006, advisory and other fees increased CHF 425 million, or 29%, to CHF 1,900 million compared to the full year 2005, primarily due to a significant increase in industry-wide activity and increased market share. For the full year 2006, Credit Suisse ranked sixth in global announced mergers and acquisitions, up from tenth for the full year 2005 and reflecting the largest market share increase among the top ten ranked banks. For the full year 2006, Credit Suisse ranked eighth in global completed mergers and acquisitions, with improved market share from the full year 2005. The advisory and other fees results also reflected significantly higher revenues from the private fund group, which raises capital for hedge funds, private equity funds and real estate funds. |

| Total trading revenues include results from fixed income and equity sales and trading. Total trading revenues for the fourth quarter of 2006 were CHF 4,351 million, up CHF 1,764 million, or 68%, compared to the fourth quarter of 2005, due to strong performance in both fixed income and equity trading. For the full year 2006, total trading revenues were CHF 15,479 million, up CHF 4,135 million, or 36%, compared to the full year 2005. |

| Investment Banking’s average daily VaR in the fourth quarter of 2006 was CHF 71 million, flat from the fourth quarter of 2005 and down from CHF 80 million in the third quarter of 2006. Compared to the third quarter of 2006, average daily VaR decreased mainly due to reduced equity and interest rate exposures, although commodity risk increased. Average economic risk capital increased CHF 2.4 billion to CHF 16.9 billion, compared to the fourth quarter of 2005, in line with the strategy to extend incremental capital to support high-growth and high-margin activities. |

| Fixed income trading generated revenues of CHF 2,755 million in the fourth quarter of 2006, up CHF 1,189 million, or 76%, compared to the fourth quarter of 2005. These results reflected the second highest level of fixed income trading revenues for a quarter and primarily reflected higher revenues in the commercial mortgage-backed securities, emerging markets trading, global foreign exchange and leveraged finance businesses. Credit spreads remained narrow in the quarter resulting in continued liquidity in the marketplace and solid activity levels. The commercial mortgage-backed securities business was positively impacted by a number of large deals in the quarter. Investment Banking continued to expand its residential mortgage-backed securities business, and revenues in the fourth quarter of 2006 were flat compared to the fourth quarter of 2005, despite softer US market conditions. The high-yield market had significant new issue supply in the quarter which benefited the trading results in the leveraged finance business. In addition, the commodities business continued its revenue growth in the fourth quarter. For the full year 2006, fixed income trading recorded revenues of CHF 9,598 million, an increase of CHF 2,594 million, or 37%, from the full year 2005, due primarily to strong performance in the commercial mortgage-backed securities, global foreign exchange and leveraged finance businesses. |

| Equity trading revenues of CHF 1,596 million increased CHF 575 million, or 56%, compared to the fourth quarter of 2005, due primarily to higher revenues in the derivatives and cash businesses and equity proprietary trading. These results reflected the second highest level of equity trading revenues for a quarter. The derivatives business improved significantly from the weak performance in the fourth quarter of 2005 and the uneven performance in the third quarter of 2006. Market conditions in the derivatives business improved in the US and Asia in the fourth quarter of 2006, and the business had high levels of client-driven activity. The cash businesses benefited from an increase in deal activity in most regions, stronger secondary markets and continued strong performance from the advanced execution services business. Equity proprietary trading had a strong performance across most strategies and regions amid positive market conditions. For the full year 2006, equity trading had revenues of CHF 5,881 million, up CHF 1,541 million, or 36%, compared to the full year 2005, due primarily to higher revenues in the cash, convertibles and derivatives businesses. Credit Suisse was ranked number one among high-touch clients in Institutional Investor’s 2006 All-America Research Team analyst rankings. |