UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________

Form 6-K

______________

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

October 21, 2010

Commission File Number 001-15244

CREDIT SUISSE GROUP AG

(Translation of registrant’s name into English)

Paradeplatz 8, P.O. Box 1, CH-8070 Zurich, Switzerland

(Address of principal executive office)

______________

Commission File Number 001-33434

CREDIT SUISSE AG

(Translation of registrant’s name into English)

Paradeplatz 8, P.O. Box, CH-8070 Zurich, Switzerland

(Address of principal executive office)

______________

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F  | Form 40-F  |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Note: Regulation S-T Rule 101(b)(1) only permits the submission in paper of a Form 6-K if submitted solely to provide an attached annual report to security holders.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Note: Regulation S-T Rule 101(b)(7) only permits the submission in paper of a Form 6-K if submitted to furnish a report or other document that the registrant foreign private issuer must furnish and make public under the laws of the jurisdiction in which the registrant is incorporated, domiciled or legally organized (the registrant’s “home country”), or under the rules of the home country exchange on which the registrant’s securities are traded, as long as the report or other document is not a press release, is not required to be and has not been distributed to the registrant’s security holders, and, if discussing a material event, has already been the subject of a Form 6-K submission or other Commission filing on EDGAR.

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes | No |

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): 82-.

| CREDIT SUISSE GROUP AG | ||

Paradeplatz 8 P.O. Box CH-8070 Zurich Switzerland | Telephone +41 844 33 88 44 Fax +41 44 333 88 77 media.relations@credit-suisse.com | |

Media Release |

Credit Suisse Group reports net income of CHF 0.6 billion in 3Q10; underlying net income of CHF 1 billion*; total net new assets of CHF 14.6 billion and tier 1 ratio of 16.7% |

All divisions profitable in a difficult quarter characterized by low market volumes and subdued client activity. Continued disciplined investments position Credit Suisse well for market recovery Private Banking: encouraging performance in an environment marked by very low client activity o Pre-tax income of CHF 836 million o Net new assets of CHF 12.6 billion in Private Banking o Wealth Management Clients with pre-tax income of CHF 612 million and gross margin at 118 basis points o Corporate & Institutional Clients with pre-tax income of CHF 224 million with continued strong pre-tax profit margin Investment Banking: solid market share performance in a weak revenue environment o Pre-tax income of CHF 395 million o Solid revenues in fixed income sales and trading, and underwriting and advisory o Equities down vs. previous quarter due to lower industry-wide client volumes Asset Management: continued progress in implementing strategy and building third-party capital and fee-based business model o Pre-tax income of CHF 135 million o Agreement to acquire noncontrolling stake in York Capital Management furthers strategy to build higher margin, capital-efficient business o Net new assets of CHF 3.6 billion continues trend with positive inflows for the fifth consecutive quarter Results in 9M10 continue to underscore value of Credit Suisse’s strategy, business model and sustainability of performance: o Net income of CHF 4.3 billion o Return on equity of 15.9% o Total net new assets of CHF 55.1 billion |

| Media Release | |

October 21, 2010 Page 2/8 |

Zurich, October 21, 2010 Credit Suisse Group reported net income of CHF 609 million in 3Q10 compared to CHF 1,593 million in 2Q10. Core net revenues were CHF 6,284 million in 3Q10 compared to CHF 8,420 million in 2Q10. Underlying net income was CHF 960 million. The return on equity was 7.0% in 3Q10 with the underlying return on equity at 11.2%. Diluted earnings per share were CHF 0.48. The tier 1 ratio was 16.7% as of the end of 3Q10.

Brady W. Dougan, Chief Executive Officer, said: “Delivering underlying net income of one billion Swiss francs was a solid result in a quarter characterized by challenging conditions with low market volumes and subdued client activity. We are continuing to make disciplined investments in client-focused, capital- efficient, high-return businesses. These investments have expanded our market share in the targeted businesses and are producing strong net new assets. Our strategy had already anticipated the impact of tighter regulation, both in Investment Banking, where we have exited less capital-efficient businesses, and in Private Banking, where we have continued to build our global on and off-shore presence. We have built a business model, global platform and a strong market position which will enable us to deliver high returns and generate stro ng cash flow as markets improve.”

He added: “We saw an encouraging performance in Private Banking, which continued to attract strong net new assets with a particularly strong performance from Asia Pacific, where we saw annualized growth of over 20%. This underscores the trust clients have in Credit Suisse. Revenues have remained relatively subdued and this business is near a cyclical low characterized by the low interest rate environment and further impacted by low levels of client activity. However, we believe the prospects for growth remain very attractive and our Private Bank is poised to capitalize as markets improve thanks to our disciplined investment in our global platform. In Switzerland, our Corporate & Institutional Clients business, which is an important provider of financing and services to the Swiss economy, achieved another strong result and maintained a str ong pre-tax profit margin.”

With regard to Investment Banking, he said: “We are encouraged by our continued momentum in gaining market share. Fixed income and our underwriting and advisory businesses achieved a solid performance reflecting our improving competitive position. In equities the performance of our client-focused business was in line with industry volume. Equities has also shown lower overall revenue volatility year to date than the industry, underscoring our continued strong client-focused market positions.”

On the performance of Asset Management, he said “We are pleased with the strategic progress, the solid result and the strong net asset inflows. The announced acquisition of a noncontrolling interest in York Capital Management is an important next step in the continuing implementation of a strategy focused on high margin, capital-efficient businesses capable of leveraging our global platform.”

He concluded: “Our results for the first nine months, with a return on equity of 15.9%, underscore that our business model is able to produce strong returns over the cycle. We anticipated much of the regulatory change, both in terms of capital requirements and the new cross-border regime. This means that we are well placed to meet these new requirements and at the same time compete and deliver attractive returns to our shareholders.”

| Media Release | |

October 21, 2010 Page 3/8 |

| in CHF million | 9M10 | 9M09 | 3Q10 | 2Q10 | 3Q09 | Change in % | Change in % |

| 3Q10 vs. 2Q10 | 3Q10 vs. 3Q09 | ||||||

| Net income attributable to shareholders | 4,257 | 5,931 | 609 | 1,593 | 2,354 | (62) | (74) |

| Diluted earnings per share (CHF) | 3.29 | 4.59 | 0.48 | 1.15 | 1.81 | (58) | (73) |

| Return on equity attributable to shareholders (annualized) | 15.9% | 21.8% | 7% | 17.8% | 25.1% | - | - |

| Tier 1 ratio (end of period) | - | - | 16.7% | 16.3% | 16.4% | - | - |

Core results 1) | |||||||

| Net revenues | 23,665 | 27,084 | 6,284 | 8,420 | 8,917 | (25) | (30) |

| Provision for credit losses | (56) | 546 | (26) | 20 | 53 | - | - |

| Total operating expenses | 18,228 | 19,300 | 5,557 | 6,594 | 6,244 | (16) | (11) |

| Income from continuing operations before taxes | 5,493 | 7,238 | 753 | 1,806 | 2,620 | (58) | (71) |

1) Core Results include the results of the three segments, the Corporate Center and discontinued operations, but do not include noncontrolling interests without significant economic interest. | |||||||

Segment Results

Private Banking

Private Banking, which comprises the Wealth Management Clients and Corporate & Institutional Clients businesses, reported income before taxes of CHF 836 million in 3Q10. This included non-credit related provisions from auction rate securities (ARS) of CHF 44 million. While this was a solid result in view of the subdued 3Q10 market environment, characterized by a seasonal slowdown, it was 4% below the 2Q10 level. This reflected a 6% decline in net revenues to CHF 2,826 million, mainly due to lower brokerage fees, while total operating expenses decreased 5%.

The Wealth Management Clients business reported income before taxes of CHF 612 million in 3Q10, down 3% from 2Q10. Net revenues were 5% lower than in 2Q10. Recurring revenues were down 4% reflecting a decrease in net interest income and lower recurring commissions and fees. Transaction-based revenues declined 9%, mainly related to significantly lower brokerage fees and foreign exchange income from client transactions, reflecting the seasonal slowdown and particularly low client activity. The gross margin was 118 basis points, down 2 basis points from 2Q10, reflecting mainly the decrease in net revenues and the 3.4% lower average assets under management. Despite the non-credit related provisions from ARS, operating expenses decreased 5% from reductions across most expense ca tegories, including IT costs and seasonally lower marketing and sales expenses as a major driver.

The Corporate & Institutional Clients business, which is an important provider of financing and services to the Swiss economy, reported income before taxes of CHF 224 million in 3Q10, down 7% from 2Q10. Net revenues declined 7% compared to 2Q10 reflecting a 5% decline in net interest income and 12% lower non-interest income. The decrease in net interest income mainly reflected lower loan margins on slightly lower average volumes and slightly lower deposit margins on stable average volumes. Non-interest income declined to CHF 153 million as fair value losses related to Clock Finance, a synthetic collateralized loan portfolio, totaled CHF 21 million compared to losses of CHF 1 million in 2Q10 . Excluding Clock Finance losses, underlying non-interest income remained stable. Despite the higher number of corporate insolvencies in Switzerland, further net releases of provision for credit losses of CHF 16 million were booked in 3Q10 after releases of CHF 13 million in 2Q10.

| Media Release | |

October 21, 2010 Page 4/8 |

Investment Banking

Investment Banking reported income before taxes of CHF 395 million in 3Q10, down 50% compared to 2Q10, as the business was impacted by a decline in client volumes that was exacerbated by a seasonal slowdown. Net revenues of CHF 3,421 million were underpinned by solid fixed income sales and trading as well as underwriting and advisory business despite the challenging market conditions, with market share momentum maintained across most products. Compared to 2Q10, net revenues declined 17%, reflecting a particularly weak July, normal summer seasonality in August and some improvement in September. Investment Banking’s results reflected net fair value losses on Credit Suisse debt of CHF 57 million in 3Q10, compared to CHF 62 million in 2Q10. The results were also impacted by debt valuation adjustment (DVA) losses of CHF 172 million in 3Q10 comp ared to DVA gains of CHF 121 million in 2Q10, relating to structured note liabilities. The pre-tax income margin was 11.5% compared to 19.1% in 2Q10. The pre-tax return on average utilized economic capital was 8.5% in 3Q10, compared to 15.8% in 2Q10.

Fixed income sales and trading results were higher than in the prior quarter, driven by strong revenues in US residential mortgage backed securities (RMBS) trading and credit businesses with solid results in global rates and emerging markets. Equity sales and trading results reflected our client-focused business model which saw continued momentum in market share and was impacted by lower client volume. Underwriting and advisory results were solid and in line with industry-wide capital issuance levels and M&A activity. Debt underwriting revenues were strong, driven by higher industry-wide issuance levels, particularly in high yield while revenues in the equity underwriting and advisory businesses reflected continued weakness in equity issuance levels and completed M&A volumes compared to historical levels.

Compensation and benefits of CHF 1,872 million in 3Q10 were lower than 2Q10, primarily reflecting the foreign exchange translation impact. In US dollars, compensation and benefits increased slightly compared to 2Q10, reflecting a small increase in performance-related compensation and benefits largely offset by a decrease in social security taxes on share award deliveries. Total other operating expenses decreased 9% from 2Q10, primarily reflecting the foreign currency translation impact, a slight decrease in commission expenses and a decrease in general and administrative expenses across most expense categories.

Risk-weighted assets of USD 151 billion as of the end of 3Q10 rose from USD 142 billion in 2Q10, primarily related to higher lending commitments in leveraged finance and corporate banking, the foreign exchange translation impact on the operational risk component and increase in other client-related risk-weighted asset usage. Average one-day, 99% Value at Risk was CHF 118 million in 3Q10, compared to CHF 117 million in 2Q10.

Asset Management

Asset Management reported income before taxes of CHF 135 million in 3Q10 compared to CHF 22 million in 2Q10, with net revenues of CHF 582 million compared to CHF 502 million in 2Q10, primarily reflecting higher investment-related gains and increased fee-based revenues partially offset by lower income from equity participations and 2Q10 gains of CHF 36 million from the sale of securities purchased from Credit Suisse money market funds. Net revenues before investment-related gains and securities purchased from Credit Suisse money market funds were up 2%. The increase in fee-based revenues was driven by higher performance fees and carried interest, partially offset by lower asset management and placement, transaction and other fees.

| Media Release | |

October 21, 2010 Page 5/8 |

Income from equity participations declined, reflecting a loss from the reduction in our ownership interest in Aberdeen to 21.0% from 21.9% due to an issuance of shares by Aberdeen. Total operating expenses were down 7% reflecting a decrease in compensation and benefits and lower commission expenses.

In 3Q10, Asset Management agreed to acquire a significant noncontrolling interest in York Capital Management (York), a leading global event-driven hedge fund manager, with the transaction expected to close in the fourth quarter of 2010. In addition, Asset Management expects to enter into arrangements to provide distribution services to York funds on a non-exclusive basis. The acquisition was part of the implementation of Credit Suisse’s strategy to focus on higher margin, capital-efficient businesses able to leverage our global platform.

| in CHF million | 3Q10 | 2Q10 | 3Q09 | Change in % | Change in % | |

| vs. 2Q10 | vs. 3Q09 | |||||

| Private | Net revenues | 2,826 | 2,991 | 2,833 | (6) | 0 |

| Banking | Provision for credit losses | (8) | 3 | 35 | - | - |

| Total operating expenses | 1,998 | 2,114 | 1,931 | (5) | 3 | |

| Income before taxes | 836 | 874 | 867 | (4) | (4) | |

| Investment | Net revenues | 3,421 | 4,099 | 5,046 | (17) | (32) |

| Banking | Provision for credit losses | (18) | 17 | 18 | - | - |

| Total operating expenses | 3,044 | 3,298 | 3,282 | (8) | (7) | |

| Income before taxes | 395 | 784 | 1,746 | (50) | (77) | |

| Asset | Net revenues | 582 | 502 | 765 | 16 | (24) |

| Management | Provision for credit losses | 0 | 0 | 0 | - | - |

| Total operating expenses | 447 | 480 | 454 | (7) | (2) | |

| Income before taxes | 135 | 22 | 311 | - | (57) | |

Net New Assets

Private Banking recorded strong net new assets of CHF 12.6 billion in 3Q10. Wealth Management Clients contributed net new assets of CHF 12.4 billion benefiting from substantial inflows in the international businesses, including strong contributions from emerging markets. The annualized quarterly growth rate in net new assets in Wealth Management Clients was 6.2% in 3Q10. Corporate & Institutional Clients acquired net new assets of CHF 0.2 billion.

Asset Management reported net new assets of CHF 3.6 billion including net inflows of CHF 5.2 billion in alternative investments, primarily in real estate & commodities, emerging markets, exchange traded funds (ETFs) and index strategies, and outflows of CHF 1.5 billion in traditional investments, as outflows in the Swiss advisory business and fixed income & equities were partially offset by inflows in multi-asset class solutions.

The Group’s total assets under management were CHF 1,251.2 billion as of the end of 3Q10, up 0.7% from the end of 2Q10, primarily reflecting positive market performance and net new assets in Private Banking and Asset Management, partially offset by adverse foreign exchange-related movements.

| Media Release | |

October 21, 2010 Page 6/8 |

Benefits of the integrated bank

Credit Suisse generated CHF 1.0 billion in collaboration revenues from the integrated bank in 3Q10 compared to CHF 1.2 billion in 2Q10, bringing the total in 9M10 to CHF 3.2 billion.

Capital position

Credit Suisse’s capital position remains very strong. The tier 1 ratio was 16.7% as of the end of 3Q10, compared to 16.3% as of the end of 2Q10.

First nine months of 2010

Credit Suisse Group reported net income of CHF 4,257 million in 9M10, compared to CHF 5,931 million in the prior-year period. Core net revenues were CHF 23,665 million compared to CHF 27,084 million in the prior-year period. The return on equity was 15.9% and diluted earnings per share were CHF 3.29. Total net new assets were CHF 55.1 billion.

| Nine Months | ||||

| in CHF billion | 9M10 | 9M09 | % change | |

| Financial Highlights | Net income attributable to shareholders | 4,257 | 5,931 | (28) |

| Diluted earnings per share (CHF) | 3.29 | 4.59 | (28) | |

| Return on equity attributable to shareholders (annualized) | 15.9% | 21.8% | - | |

| Private Banking | Income before taxes | 2,602 | 2,794 | (7) |

| Investment Banking | Income before taxes | 2,973 | 5,815 | (49) |

| Asset Management | Income before taxes | 323 | (124) | - |

* Underlying net income (3Q10): Excludes net fair value charges on Credit Suisse vanilla debt of CHF 589 million (before tax) due to tightening credit spreads and cross currency swaps relating to Credit Suisse long-term debt, a non-taxable benefit of CHF 43 million relating to the UK levy on variable compensation and litigation charges of CHF 73 million (before tax), yielding underlying net income adjusted for a normalized tax rate of CHF 960 million.

Information

Media Relations Credit Suisse AG, telephone +41 844 33 88 44, media.relations@credit-suisse.com

Investor Relations Credit Suisse AG, telephone +41 44 333 71 49, investor.relations@credit-suisse.com

Credit Suisse AG

Credit Suisse AG is one of the world's leading financial services providers and is part of the Credit Suisse group of companies (referred to here as 'Credit Suisse'). As an integrated bank, Credit Suisse offers clients its combined expertise in the areas of private banking, investment banking and asset management. Credit Suisse provides advisory services, comprehensive solutions and innovative products to companies, institutional clients and high-net-worth private clients globally, as well as to retail clients in Switzerland. Credit Suisse is headquartered in Zurich and operates in over 50 countries worldwide. The group employs approximately 50,500 people. The registered shares (CSGN) of Credit Suisse's parent company, Credit Suisse Group AG, are listed in Switzerland and, in the form of American Depositary Shares (CS), in New York. Further informa tion about Credit Suisse can be found at www.credit-suisse.com.

Cautionary statement regarding forward-looking information and non-GAAP information

This press release contains statements that constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act. In addition, in the future we, and others on our behalf, may make statements that constitute forward-looking statements. Such forward-looking statements may include, without limitation, statements relating to the following:

| – | our plans, objectives or goals; |

| – | our future economic performance or prospects; |

| Media Release | |

October 21, 2010 Page 7/8 |

| – | the potential effect on our future performance of certain contingencies; and |

| – | assumptions underlying any such statements. |

Words such as “believes,” “anticipates,” “expects,” “intends” and “plans” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. We do not intend to update these forward-looking statements except as may be required by applicable securities laws. By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that predictions, forecasts, projections and other outcomes described or implied in forward-looking statements will not be achieved. We caution you that a number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in such forward-looking statements . These factors include:

| – | the ability to maintain sufficient liquidity and access capital markets; |

| – | market and interest rate fluctuations; |

| – | the strength of the global economy in general and the strength of the economies of the countries in which we conduct our operations, in particular the risk of a continued US or global economic downturn in 2010 and beyond; |

| – | the direct and indirect impacts of continuing deterioration of subprime and other real estate markets; |

| – | further adverse rating actions by credit rating agencies in respect of structured credit products or other credit-related exposures or of monoline insurers; |

| – | the ability of counterparties to meet their obligations to us; |

| – | the effects of, and changes in, fiscal, monetary, trade and tax policies, and currency fluctuations; |

| – | political and social developments, including war, civil unrest or terrorist activity; |

| – | the possibility of foreign exchange controls, expropriation, nationalization or confiscation of assets in countries in which we conduct our operations; |

| – | operational factors such as systems failure, human error, or the failure to implement procedures properly; |

| – | actions taken by regulators with respect to our business and practices in one or more of the countries in which we conduct our operations; |

| – | the effects of changes in laws, regulations or accounting policies or practices; |

| – | competition in geographic and business areas in which we conduct our operations; |

| – | the ability to retain and recruit qualified personnel; |

| – | the ability to maintain our reputation and promote our brand; |

| – | the ability to increase market share and control expenses; |

| – | technological changes; |

| – | the timely development and acceptance of our new products and services and the perceived overall value of these products and services by users; |

| – | acquisitions, including the ability to integrate acquired businesses successfully, and divestitures, including the ability to sell non-core assets; |

| – | the adverse resolution of litigation and other contingencies; |

| – | the ability to achieve our cost efficiency goals and other cost targets; and |

| – | our success at managing the risks involved in the foregoing. |

We caution you that the foregoing list of important factors is not exclusive. When evaluating forward-looking statements, you should carefully consider the foregoing factors and other uncertainties and events, as well as the information set forth in our Annual Report 2009 under IX – Additional information – Risk Factors.

This press release contains non-GAAP financial information. Information needed to reconcile such non-GAAP financial information to the most directly comparable measures under GAAP can be found in the Credit Suisse Financial Release 3Q10.

| Media Release | |

October 21, 2010 Page 8/8 |

Presentation of Credit Suisse Group’s 3Q10 results via audio webcast and telephone conference

Date Thursday, October 21, 2010

Time 09:00 Zurich / 08:00 London / 03:00 New York

Speakers Brady W. Dougan, Chief Executive Officer

David Mathers, Chief Financial Officer

The presentations will be held in English.

Audio webcast www.credit-suisse.com/results

Telephone Switzerland: +41 44 580 40 01

Europe: +44 1452 565 510

US: +1 866 389 9771

Reference: Credit Suisse Group quarterly results

| Q&A session | You will have the opportunity to ask questions during the telephone conference following the presentations. |

Playback Playback available approximately 2 hours after the event at

www.credit-suisse.com/results or on the telephone numbers below:

Switzerland:+41 44 580 34 56

Europe: +44 1452 550 000

US: +1 866 247 4222

Conference ID: 16597995#

Third Quarter 2010 Results

Zurich

October 21, 2010

Cautionary statement regarding forward-looking and non-GAAP information

This presentation contains forward-looking statements within the meaning of the Private Securities

Litigation Reform Act of 1995. Forward-looking statements involve inherent risks and uncertainties,

and we might not be able to achieve the predictions, forecasts, projections and other outcomes we

describe or imply in forward-looking statements.

Litigation Reform Act of 1995. Forward-looking statements involve inherent risks and uncertainties,

and we might not be able to achieve the predictions, forecasts, projections and other outcomes we

describe or imply in forward-looking statements.

A number of important factors could cause results to differ materially from the plans, objectives,

expectations, estimates and intentions we express in these forward-looking statements, including

those we identify in "Risk Factors" in our Annual Report on Form 20-F for the fiscal year ended

December 31, 2009 filed with the US Securities and Exchange Commission, and in other public

filings and press releases. We do not intend to update these forward-looking statements except as

may be required by applicable laws.

expectations, estimates and intentions we express in these forward-looking statements, including

those we identify in "Risk Factors" in our Annual Report on Form 20-F for the fiscal year ended

December 31, 2009 filed with the US Securities and Exchange Commission, and in other public

filings and press releases. We do not intend to update these forward-looking statements except as

may be required by applicable laws.

This presentation contains non-GAAP financial information. Information needed to reconcile such

non-GAAP financial information to the most directly comparable measures under GAAP can be

found in Credit Suisse Group's third quarter report 2010.

non-GAAP financial information to the most directly comparable measures under GAAP can be

found in Credit Suisse Group's third quarter report 2010.

Third Quarter 2010 Results

Slide 1

Cautionary statement

Third quarter 2010 results detail

David Mathers, Chief Financial Officer

Introduction

Brady W. Dougan, Chief Executive Officer

Regulatory capital review

David Mathers, Chief Financial Officer

Summary

Brady W. Dougan, Chief Executive Officer

Third Quarter 2010 Results

Slide 2

3Q10:

Good result in a

quarter characterized

by challenging

conditions with low

market volumes and

subdued client

activity

quarter characterized

by challenging

conditions with low

market volumes and

subdued client

activity

Strongly positioned

with a distinctive

strategy

with a distinctive

strategy

§ Anticipated regulatory changes

§ Client-focused and capital-efficient business model

§ Ability to deliver high returns and book value accretion

§ Underlying net income of CHF 1 bn and underlying RoE of 11%

(CHF 4.0 bn and 15% in 9M10)

(CHF 4.0 bn and 15% in 9M10)

§ Solid pre-tax income in Private Bank with continued strong Wealth

Management inflows of CHF 12.4 bn; gross margin at 118 bp

Management inflows of CHF 12.4 bn; gross margin at 118 bp

§ Investment Banking with maintained market share performance in a weak

revenue environment, exacerbated by the seasonal slowdown

revenue environment, exacerbated by the seasonal slowdown

§ Asset Management with continued progress to grow its core business; net

new assets of CHF 3.6 bn represent positive asset flows for the fifth

consecutive quarter

new assets of CHF 3.6 bn represent positive asset flows for the fifth

consecutive quarter

Third Quarter 2010 Results

Slide 3

Introduction

Third quarter 2010 results detail

David Mathers, Chief Financial Officer

Introduction

Brady W. Dougan, Chief Executive Officer

Regulatory capital review

David Mathers, Chief Financial Officer

Summary

Brady W. Dougan, Chief Executive Officer

Third Quarter 2010 Results

Slide 4

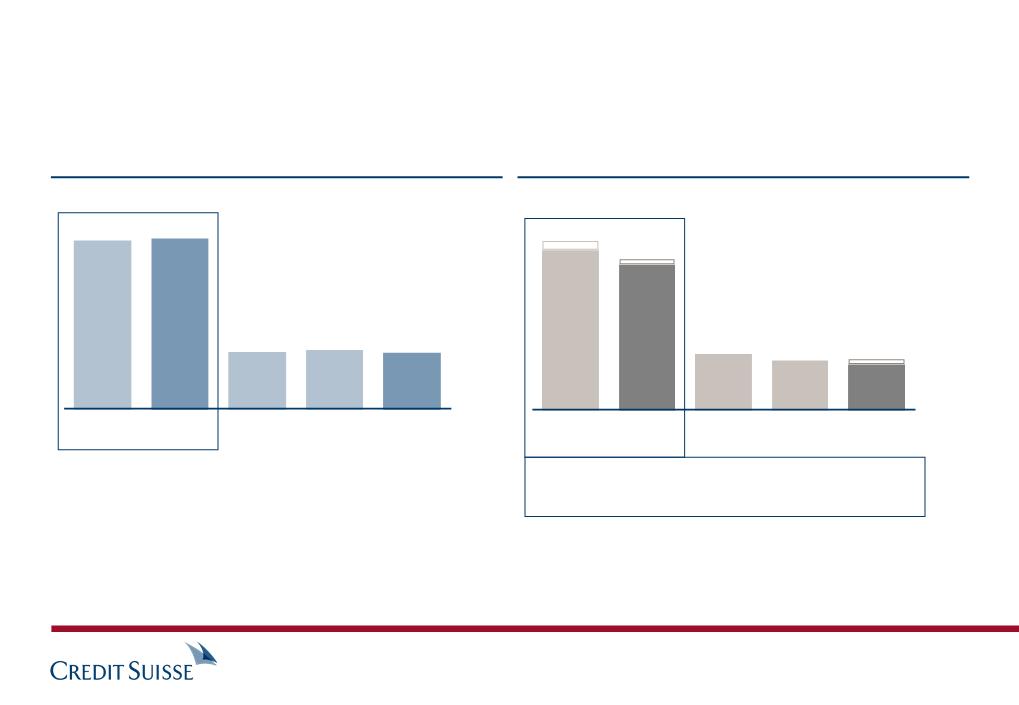

Core results in CHF bn 3Q10 2Q10 3Q09 9M10 9M09

Net revenues

Pre-tax income

Net income attributable to shareholders

Diluted earnings per share in CHF

Return on equity

Net new assets in CHF bn

Underlying results

Third Quarter 2010 Results

Slide 5

6.3 8.4 8.9 23.7 27.1

0.8 1.8 2.6 5.5 7.2

0.6 1.6 2.4 4.3 5.9

0.48 1.15 1.81 3.29 4.59

7% 18% 25% 16% 22%

14.6 14.5 16.7 55.1 31.7

Net revenues

Pre-tax income

Net income

Return on equity

6.9 7.5 9.0 23.1 27.7

1.4 1.6 2.9 5.7 8.6

1.0 1.1 2.2 4.0 6.3

11% 12% 23% 15% 23%

Results overview

1) Excluding non-credit related provisions of CHF 44 m related to ARS in 3Q10

Third Quarter 2010 Results

Slide 6

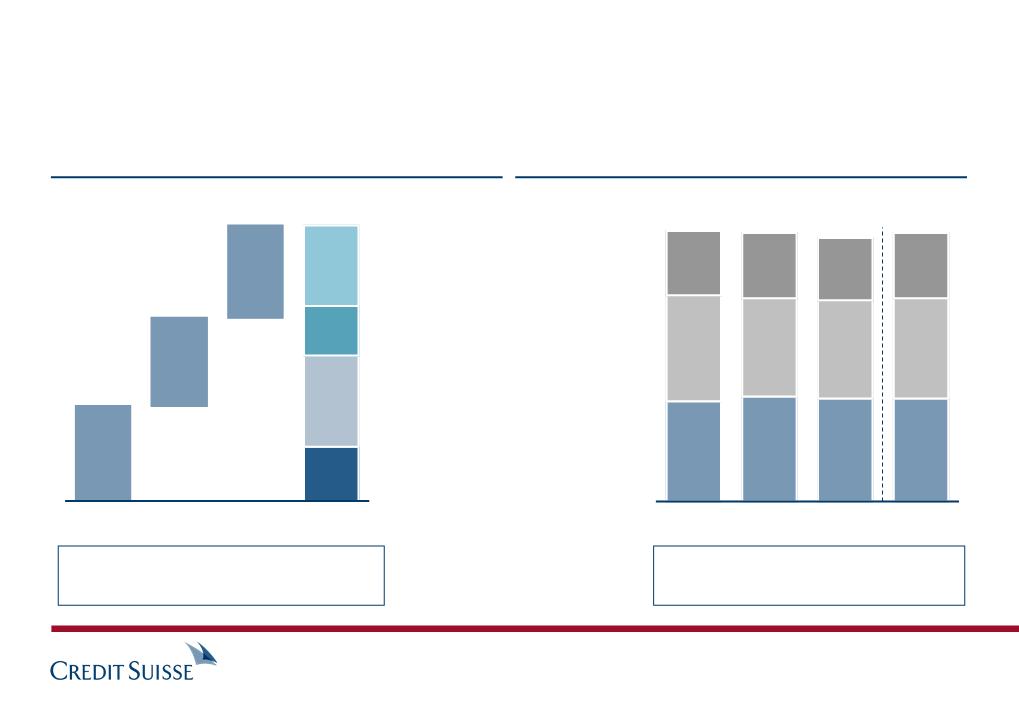

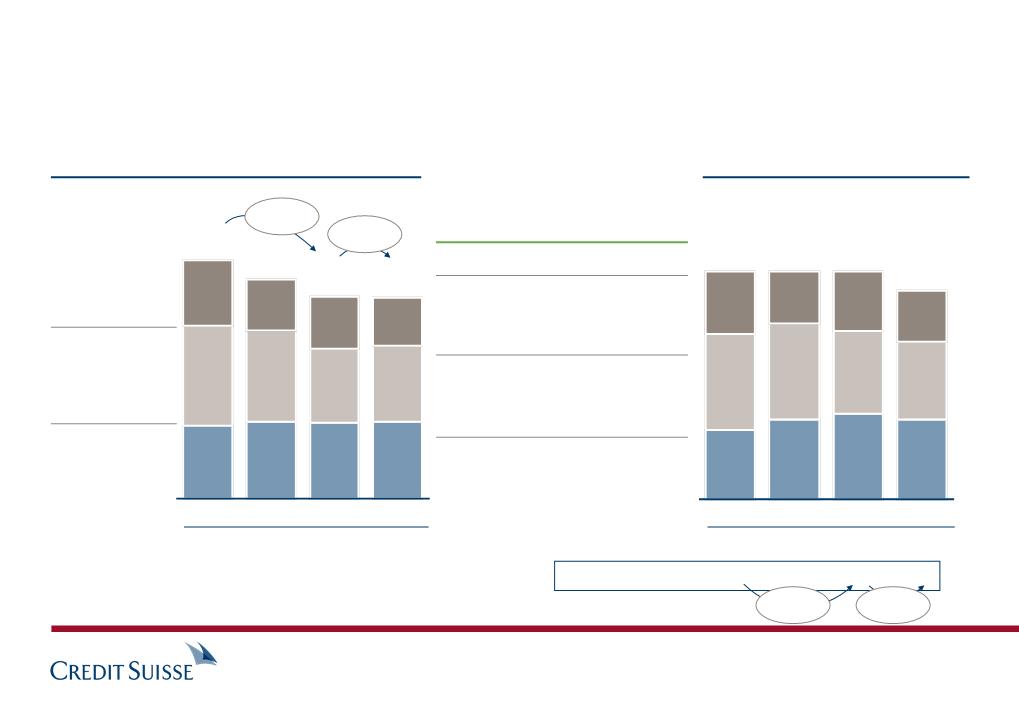

Private Banking with continued strong asset inflows and

solid pre-tax income, despite seasonally low client activity

solid pre-tax income, despite seasonally low client activity

§ Continued strong net new assets evidencing the strength and resilience of our

business model

business model

– Net new assets of CHF 12.4 bn in Wealth Management at 6.2% annualized growth

rate with 20% growth in Asia Pacific

rate with 20% growth in Asia Pacific

– 9M10 net new assets in Wealth Management of CHF 37.2 bn and in total

CHF 45.0 bn for Private Banking, already exceeding FY 2009 amounts

CHF 45.0 bn for Private Banking, already exceeding FY 2009 amounts

§ Solid pre-tax income, despite seasonal summer slowdown leading to lower

brokerage revenues

brokerage revenues

– Underlying pre-tax income of CHF 880 m1) ahead of 2Q10 and 3Q09

– Gross margin at 118 basis points in Wealth Management

§ Continued upgrading of relationship managers (up 60 net, 140 gross)

§ Corporate & Institutional Clients business continues to deliver strong results

633

2,106

723

612

2,516

7,299

2,429

2,385

7,365

1) Excluding proceeds from captive insurance settlements of CHF 100 m in 1Q09

2) Excluding non-credit related provisions of CHF 44 m related to ARS in 3Q10

Pre-tax income

CHF m

3Q09

2Q10

3Q10

Pre-tax income margin in %

29 27 30 25 28

1)

9M09

9M10

Net revenues

CHF m

3Q09

2Q10

3Q10

9M09

9M10

§ Client sentiment continued to be risk-

averse

averse

§ Seasonal 3Q slowdown leading to low

brokerage fees

brokerage fees

656

1)

2)

2)

1,966

2)

2)

§ Expenses down 8% vs. 2Q10

Third Quarter 2010 Results

Slide 7

2)

Wealth Management with solid pre-tax income, despite seasonal

summer slowdown

summer slowdown

45

47

46

46

47

44

44

45

29

29

28

29

Net new assets (NNA) in 2010

CHF bn

9M

Asia Pacific

Americas

EMEA

Switzerland

1Q

2Q

12.9

11.9

3Q

12.4

37.2

Net new assets growth rate in %

6.4% 5.8% 6.2% 6.2%

Gross margin on revenues in 2010

Basis points

NNA in CHF bn by region in 3Q10 were 1.2 from Switzerland, 4.3 from EMEA, 3.1 from Americas and 3.8 from Asia Pacific NNA growth rates are annualized

9M

1Q

2Q

3Q

Average AuM in CHF bn

814 837 809 820

Recurring

commissions

& fees

commissions

& fees

Recurring net

interest

income

interest

income

Transaction-

based revenues

based revenues

121

120

118

120

10.9

6.7

12.3

7.3

Third Quarter 2010 Results

Slide 8

Wealth Management with continued strong asset inflows, but

lower brokerage fees affecting the gross margin

lower brokerage fees affecting the gross margin

Swiss booking

center

center

Global,

(onshore &

offshore)

(onshore &

offshore)

§ Globally diversified inflows

§ Switzerland with superior value proposition

beyond client confidentiality

beyond client confidentiality

§ Further expanding of HNWI market share

(11) bn

Wealth

Management

Management

Further upside potential on margin

§ Broadening product & service offering

§ Reaching full productivity of recently added

relationship managers

relationship managers

96

+24 bn

+13 bn

+6 bn

Higher

Lower

(4) bn

+20 bn

+8 bn

+8 bn

2009

Net new assets

(CHF)

(CHF)

9M10

112

2009

Gross margin

(basis points)

(basis points)

9M10

Breadth, depth and

maturity of product

offering

maturity of product

offering

103

114

111

119

114

119

HNWI+ only

Switzerland

(onshore)

Mature

markets

markets

(offshore)

Emerging

markets

markets

(offshore)

International

booking centers

(excluding US)

booking centers

(excluding US)

+8 bn

+12 bn

135

142

Third Quarter 2010 Results

Slide 9

§ Current net new assets trends expected to continue

§ Relative gross margin contribution expected to remain stable, with upside when markets improve

§ Western Europe "Big-4" (Germany, Italy, UK,

France) account for AuM of CHF 106 bn

France) account for AuM of CHF 106 bn

§ AuM at risk of some CHF 25 to 35 bn, assuming

adverse events in all markets

adverse events in all markets

Mature offshore business is shrinking - more than offset by growth

in other businesses with similar margins

in other businesses with similar margins

588

680

144

224

241

Pre-tax income

CHF m

§ Continued strong pre-tax margin

§ Net releases from credit provisions,

reflecting quality of the loan book

reflecting quality of the loan book

§ Stable revenues with higher

contribution from commissions and

fees

contribution from commissions and

fees

§ Strong net new assets of CHF 7.8 bn

during 9M10

during 9M10

Fair value change on loan hedges

(88) (34) (61) (1) (21)

Provision for credit losses

130 (42) 40 (13) (16)

3Q09

2Q10

3Q10

Pre-tax income margin in %

43 50 36 51 51

9M09

9M10

1) Excluding fair value change on loan hedges

Third Quarter 2010 Results

Slide 10

1)

Corporate & Institutional Client business continues to deliver

strong results

strong results

Third Quarter 2010 Results

Slide 11

Investment Banking results impacted by weaker client trading

volumes, exacerbated by seasonality

volumes, exacerbated by seasonality

§ Results reflect a particularly weak July, normal summer seasonality in August

and some improvement in September

and some improvement in September

§ Solid fixed income sales and trading results driven by strong results in US

RMBS trading and Credit businesses; solid contribution from Rates and

Emerging Markets

RMBS trading and Credit businesses; solid contribution from Rates and

Emerging Markets

§ Equity sales and trading results impacted by lower industry-wide volumes

in Cash Equities, seasonal decline in Prime Services and weaker client flows

in Derivatives compared with a particularly strong 2Q10

in Cash Equities, seasonal decline in Prime Services and weaker client flows

in Derivatives compared with a particularly strong 2Q10

§ Solid underwriting and advisory performance in light of muted activity

levels; continued strong pipeline; capital markets trends showed improvement

in September

levels; continued strong pipeline; capital markets trends showed improvement

in September

Net revenues in USD

Net revenues in CHF

Pre-tax income

Pre-tax income margin

Pre-tax return on economic capital

Investment Banking (CHF bn) 3Q10 2Q10 3Q09 9M10 9M09

Note: Excluding impact of movements in spreads on own debt of CHF (57) m, CHF (62) m, CHF (251) m, CHF (178) m and CHF (155) m in 3Q10, 2Q10, 3Q09, 9M10 and 9M09, respectively.

(16)%

(9)%

Third Quarter 2010 Results

Slide 12

3.5 3.8 5.0 12.2 15.9

3.5 4.2 5.3 12.9 17.7

0.5 0.8 2.0 3.2 6.0

13% 20% 38% 24% 34%

9% 17% 41% 22% 38%

Investment Banking impacted by challenging market conditions,

seasonal trends and the strengthening Swiss franc

seasonal trends and the strengthening Swiss franc

Debt underwriting

Fixed income sales and trading

3Q10

3Q09

2Q10

1Q10

4Q09

§ Strong results in Structured Products driven by

continued resilience in non-agency US RMBS

trading

continued resilience in non-agency US RMBS

trading

§ Strong results in Credit businesses driven by

client flows and record high yield new issue

activity

client flows and record high yield new issue

activity

§ Solid contribution from Rates and Emerging

Markets

Markets

§ Flow-sales force expansion largely complete and

impact of investments starting to materialize;

better penetration with key clients and improved

breadth and intensity of coverage

impact of investments starting to materialize;

better penetration with key clients and improved

breadth and intensity of coverage

1) Excludes impact of movements in spreads on own debt

Fixed income sales & trading and underwriting revenues 1)

CHF bn

2.0

1.5

0.5

3.2

2.7

0.5

1.4

1.0

0.4

3.0

2.7

0.3

1.5

0.5

+3%

+12%

Third Quarter 2010 Results

Slide 13

in USD bn

2.9 1.4 3.0 1.8 2.0

2.0

Increased fixed income revenues

3Q10

3Q09

2Q10

1Q10

4Q09

§ Revenue decline across most major businesses despite

continued market share strength

continued market share strength

− Lower revenues in Cash Equities driven by an industry-

wide decline in volumes, particularly in electronic

trading

wide decline in volumes, particularly in electronic

trading

− Seasonal decline in Prime Services revenues

− Lower revenues from Derivatives driven by weaker

client flows

client flows

§ Maintained market share strength

− Ranked #1 in market share for global cash products

− Top 3 position in Prime Services

§ Revenues include debit valuation adjustments (DVA) on fair

valued structured note liabilities of CHF (118) m, CHF 64 m

and CHF (19) m in 3Q10, 2Q10 and 1Q10, respectively

valued structured note liabilities of CHF (118) m, CHF 64 m

and CHF (19) m in 3Q10, 2Q10 and 1Q10, respectively

1) Excludes impact of movements in spreads on own debt

2) Source: Leading market share analysis provider

Equity sales & trading and underwriting revenues 1)

CHF bn

Equity underwriting

Equity sales and trading

2.2

1.9

0.3

1.6

1.1

0.5

1.9

1.7

0.2

1.9

1.7

0.2

1.3

1.1

0.2

(35)%

(30)%

Third Quarter 2010 Results

Slide 14

2)

in USD bn

2.1 1.6 1.8 1.8 1.2

2.1 1.6 1.8 1.8 1.2

Equity revenues affected by lower industry-wide trading volumes

1) Underwriting revenues are also included in the Securities view revenues on slides 13 and 14

Advisory and underwriting 1)

CHF bn

3Q09

2Q10

3Q10

Debt underwriting

Advisory

Equity underwriting

4Q09

1Q10

0.3

0.4

0.1

0.8

1.2

0.3

0.4

0.5

0.2

0.9

0.2

0.5

0.3

1.0

0.2

0.5

0.2

0.2

0.5

§ Resilient results driven by strong debt

issuance levels, partially offset by

continued weak equity issuance and

lower completed M&A volumes

issuance levels, partially offset by

continued weak equity issuance and

lower completed M&A volumes

§ Pipeline significantly above year-ago

levels across products; execution of

pipeline subject to market conditions

levels across products; execution of

pipeline subject to market conditions

(10)%

Third Quarter 2010 Results

Slide 15

0.9

(2)%

in USD bn

0.7 1.2 0.8 0.9 0.9

Solid results in advisory and underwriting

0

11

30

39

33

8

5

6

23

29

5

1

1

1

<(25)

(25)-0

0-25

25-50

50-75

75-100

100-125

>125

Client-focused model evident from revenue mix and lower daily

revenue volatility

revenue volatility

§ Successful client-focused strategy

resulting in 89% contribution from direct

client revenues

resulting in 89% contribution from direct

client revenues

§ Indirect client revenues and arbitrage

trading constitute 9% and 2% of total

Investment Banking net revenues,

respectively

trading constitute 9% and 2% of total

Investment Banking net revenues,

respectively

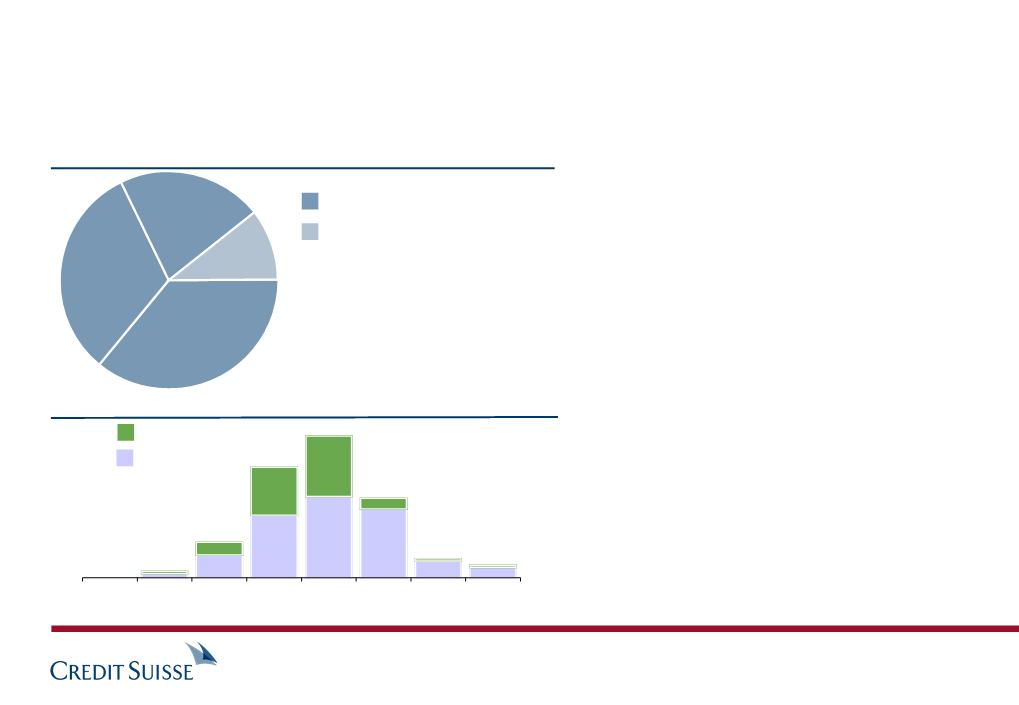

Contribution to Investment Banking net revenues (9M10)

1) Direct client revenues consist primarily of fees and commissions, gains and losses

from matching of client trades and revenues from client financing activities

from matching of client trades and revenues from client financing activities

2) Indirect client revenues consist of gains, losses and financing on inventory

positions held for market making activities

positions held for market making activities

Credit Suisse 9M10 daily revenue distribution

§ As in previous quarters, 3Q10 daily revenue

distribution was generally tightly concentrated

distribution was generally tightly concentrated

– No outsized daily gains or losses

– Only one loss day in 3Q10 and three loss

days YTD, each smaller than CHF (25)m

days YTD, each smaller than CHF (25)m

CHF m

11%

Fixed Income Sales

& Trading 35%

& Trading 35%

Equity

Sales &

Trading

Sales &

Trading

32%

Underwriting

& Advisory

22%

Direct client revenues 1)

Indirect client revenues

and arbitrage trading 2)

and arbitrage trading 2)

1H 10

3Q10

Third Quarter 2010 Results

Slide 16

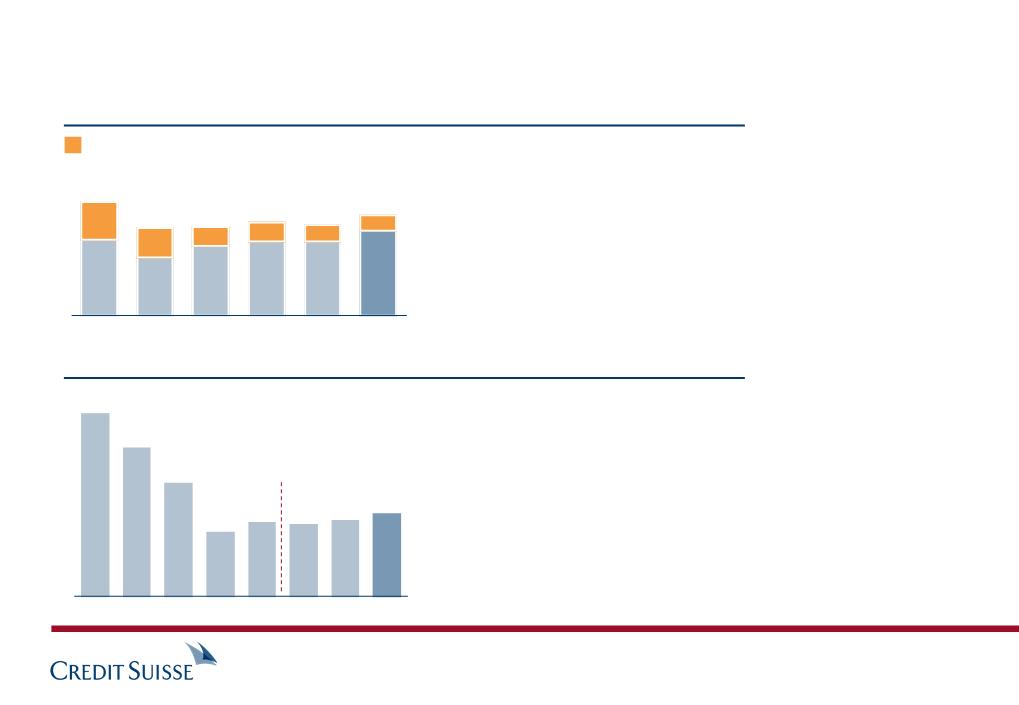

Investment Banking average 1-Day VaR (USD m)

§ The 9% increase in VaR from 2Q10 primarily reflects

increased risk usage in support of client businesses, including

interest rate and credit, foreign exchange and equities

increased risk usage in support of client businesses, including

interest rate and credit, foreign exchange and equities

§ No backtesting exceptions in 3Q10

105

Investment Banking RWAs (period end in USD bn)

§ Continued focus on disciplined alignment of capital to high-

returning, client businesses

returning, client businesses

§ Increase from 2Q10 primarily relating to:

− Higher lending commitments in Leveraged Finance and

Corporate Banking

Corporate Banking

− FX translation impact on operational risk component

− Increases in other client-related RWA usage

1H08

2H08

1H09

2H09

1H10

2Q10

102

89

156

205

253

99

1Q10

139

Exit businesses

26

113

140

17

123

144

127

17

2Q09

4Q09

1Q10

2Q10

142

15

127

4Q08

163

34

129

151

3Q10

114

14

137

3Q10

Third Quarter 2010 Results

Slide 17

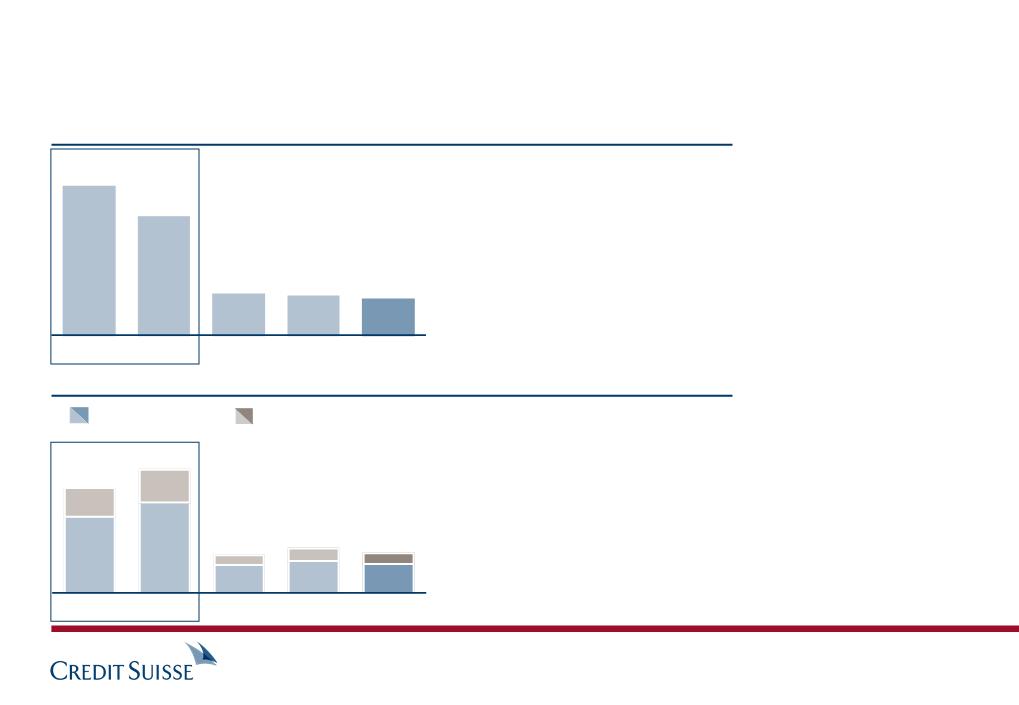

Continued discipline in allocating capital

3,080

866

Commission expenses

G&A expenses

2)

3,595

2,644

951

Investment Banking compensation expenses (CHF m)

Investment Banking non-compensation expenses (CHF m)

3Q09

2Q10

1) Excluding fair value on own debt and excluding UK bonus levy

2) Excludes litigation charges of 29 m, 47 m, 383 m, 29 m and 430 m in 3Q10, 3Q09, 2Q09, 9M10 and 9M09

9M10

§ Decreases across most expense categories including legal,

advertising and travel and entertainment expenses as well as

favorable FX translation impact

advertising and travel and entertainment expenses as well as

favorable FX translation impact

2,214

6,210

7,782

9M09

2,014

1,107

3Q10

§ Consistent approach to compensation accrual reflecting risk-

adjusted profitability and competitive market conditions

adjusted profitability and competitive market conditions

§ 9M10 compensation expenses down 20% from 9M09;

Investment Banking compensation/revenue1) ratio of 54% in

3Q10 and 48% for 9M10

Investment Banking compensation/revenue1) ratio of 54% in

3Q10 and 48% for 9M10

§ Credit Suisse Group compensation/revenue ratio1) of 50% in

3Q10 and 47% for 9M10

3Q10 and 47% for 9M10

806

301

2,129

1,284

933

351

1,872

1,143

848

295

3Q09

2Q10

9M10

9M09

3Q10

Third Quarter 2010 Results

Slide 18

Compensation and non-compensation expenses

Competency

Asset

Allocation

Allocation

Alternative

Investments

Investments

Swiss

platform

platform

Product suite

Collaboration

§ MACS (private &

institutional clients)

institutional clients)

§ Private Equity /

Hedge Funds

Hedge Funds

§ ETFs / Index

strategies

strategies

§ Commodities

§ Fixed Income

and Equities

and Equities

§ Key discretionary mandate capability for Private Bank

§ Access to UHNWI & HNWI and institutional clients

§ Utilizing technology & financing from the Investment Bank

§ Joint product development and sales with IB

§ Product for our Swiss and European clients in the

Private Bank

Private Bank

Leverage the

integrated bank

integrated bank

Build leading investment

capabilities via in-house

funds and partnerships

capabilities via in-house

funds and partnerships

Build higher margin,

capital-efficient business

capital-efficient business

Strategic Pillars

Third Quarter 2010 Results

Slide 19

Asset Management focused on core competencies that

capitalize on the strength of Credit Suisse's global footprint

capitalize on the strength of Credit Suisse's global footprint

Leverage the

integrated bank

integrated bank

Build leading

investment

capabilities with

superior performance

investment

capabilities with

superior performance

§ York Capital Management is a premier USD 14 bn hedge fund with 19-

year track record and broad-based product platform

year track record and broad-based product platform

§ Joint equity ownership aligns interests and helps retain best investment

talent

talent

Build higher margin,

capital-efficient

business

capital-efficient

business

§ Investment in management company, not underlying funds

– Reflects capital-light approach with focus on recurring fee income

– Consistent with recently enacted US financial reforms

Third Quarter 2010 Results

Slide 20

Pending acquisition of minority stake in York Capital important

step in executing on Asset Management strategy

step in executing on Asset Management strategy

§ Fills gap in our product offering to institutional and wealth management

clients

clients

§ Combines York’s world-class product suite with Credit Suisse’ global

distribution

distribution

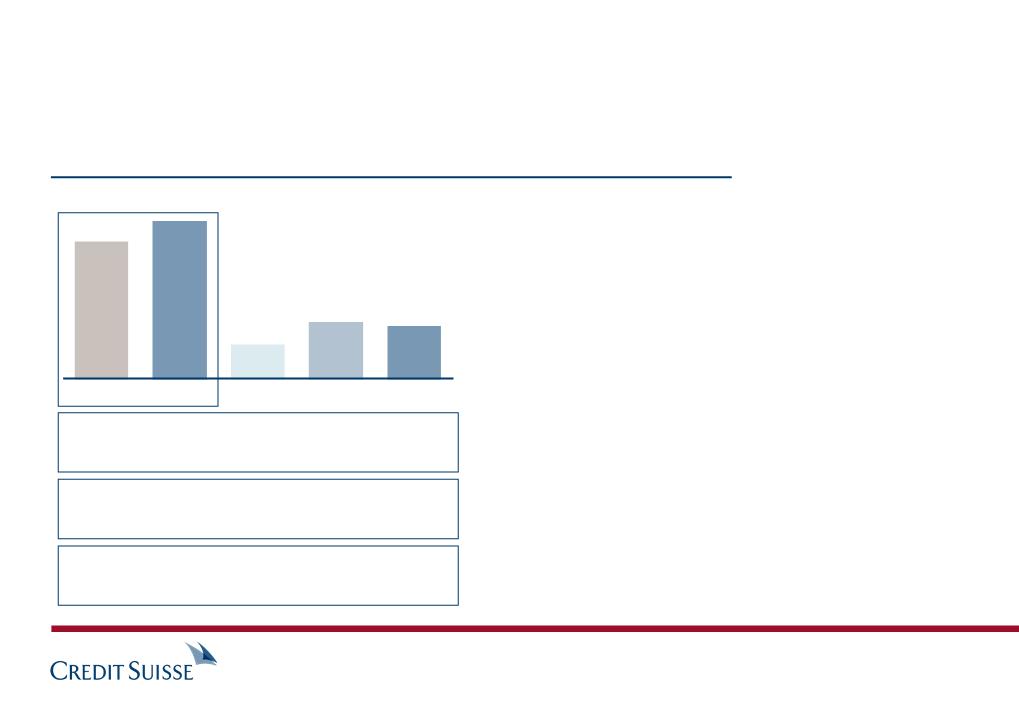

(352)

323

104

135

22

Pre-tax income

CHF m

3Q09

2Q10

3Q10

9M09

9M10

1)

Fee-based revenues

CHF m

9M09

9M10

3Q09

2Q10

3Q10

Performance fees and carried interest

Management fees

Placement, transaction and other fees

Fee-based margin on average AuM

38 39 38 37 40

1,171

1,241

408

406

421

1) Excluding gain on sale of business of CHF 21 m in 2Q09 and CHF 207 m in 3Q09

1)

Pre-tax income margin in %

(36) 19 19 4 23

From 2Q10

§ Revenues up 16%

§ Expenses down 7%

Third Quarter 2010 Results

Slide 21

Asset Management continues progress in 2010

Net new assets

CHF bn

§ Strong inflows of CHF 5.2 bn in alternative

investments

investments

– Strong inflows in real estate, commodity

funds and ETFs

funds and ETFs

– Continued inflows from emerging market

product offerings

product offerings

– Resilient private equity fund-of-fund flows

§ Outflows of CHF 1.6 bn mainly in lower

margin assets

margin assets

1Q10

2Q10

3Q10

Annualized net new asset growth %

(3.7) 3.9 10.8 1.2 3.4 5.2

1H09

2H09

9M10

(7.6)

11.2

1.3

3.6

8.0

16.1

Third Quarter 2010 Results

Slide 22

Asset Management with positive asset inflows for the fifth

consecutive quarter

consecutive quarter

Third quarter 2010 results detail

David Mathers, Chief Financial Officer

Introduction

Brady W. Dougan, Chief Executive Officer

Regulatory capital review

David Mathers, Chief Financial Officer

Summary

Brady W. Dougan, Chief Executive Officer

Third Quarter 2010 Results

Slide 23

2008

2009

Basel 2 risk-weighted assets (in CHF bn) and capital ratios (in %)

2007

10.0

13.3

257

324

(30)%

16.3

222

2Q10

16.3

233

1) Excluding hybrid capital of CHF 11.5 bn

(2)%

§ Increase strong Basel II tier 1 ratio to

16.7%

16.7%

§ Core tier 1 ratio of 12.1% 1)

§ Regulatory leverage ratio increased to

4.3%

(vs. 3.9% in 2Q10)

4.3%

(vs. 3.9% in 2Q10)

§ Consistent dividend accrual policy in line

with historic payout ratio

with historic payout ratio

228

16.7%

3Q10

Third Quarter 2010 Results

Slide 24

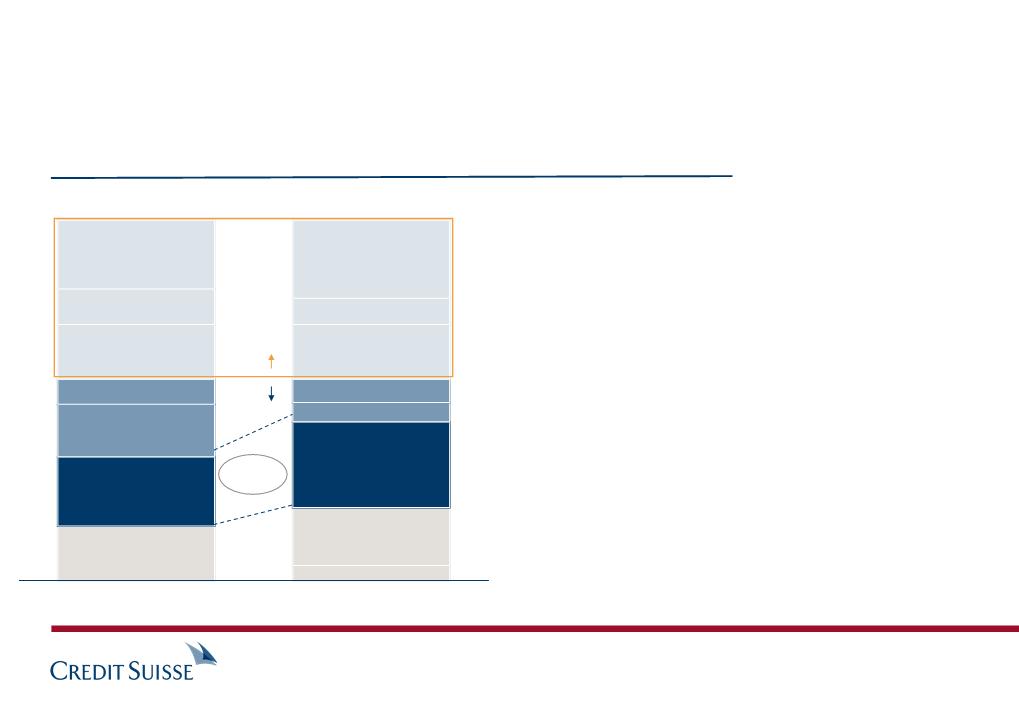

Maintained leading capital position

Basel 2

(3Q10)

(3Q10)

Basel

2.5

2.5

Gross-up of

Deductions

Deductions

CVA &

other

other

Stressed

VaR

VaR

Basel 3

(after

mitigation)

(after

mitigation)

IDR /

Migration

Migration

Securi-

tization

tization

Basel 3

(before

mitigation)

(before

mitigation)

Mitigation

impact

impact

Change

to Basel 2.5

to Basel 2.5

Change

to Basel 3

to Basel 3

Mitigation

impact

impact

Businesses

primarily

affected

primarily

affected

§ Emerging

markets

markets

§ Credit

§ Credit

§ Structured

products

products

§ Structured

products

products

§ "Exit

businesses"

businesses"

§ Rates

§ Foreign

exchange

exchange

§ Equities

§ Emerging

markets

markets

§ Credit

§ Equity

derivatives

derivatives

CHF bn

228

+15

+20

+10

330 to

350

350

+65

Approx.

270

270

+65

Approx.

400

400

(50) to

(70)

(70)

Note: Estimates based on current positions; certain Basel 3 methodology changes are still subject to validation

+45

+130

Third Quarter 2010 Results

Slide 25

Risk-weighted assets projection under Basel rule changes

Exit

businesses

businesses

§ RWA-equivalent reduction of CHF 20 to 25 bn

Businesses

primarily affected

primarily affected

Mitigating and reduction impact (approximated amounts)

Structured

products

products

§ Anticipate roughly CHF 3 bn nominal reduction in low rated positions,

reflecting change in asset mix and risk reductions by 2012

reflecting change in asset mix and risk reductions by 2012

§ RWA-equivalent reduction of CHF 15 to 20 bn

Emerging

markets

markets

§ CHF 5 bn RWA-equivalent reduction achieved through refocusing the

business towards a more flow-based model

business towards a more flow-based model

Derivatives

§ CHF 5 to 10 bn RWA-equivalent reduction related to uncollateralized

exposures that will either mature by 2012, or that can be collateralized /

hedged

exposures that will either mature by 2012, or that can be collateralized /

hedged

§ CHF 5 to 10 bn RWA-equivalent reduction resulting from a shift of OTC

derivatives to central counterparties clearing

derivatives to central counterparties clearing

Third Quarter 2010 Results

Slide 26

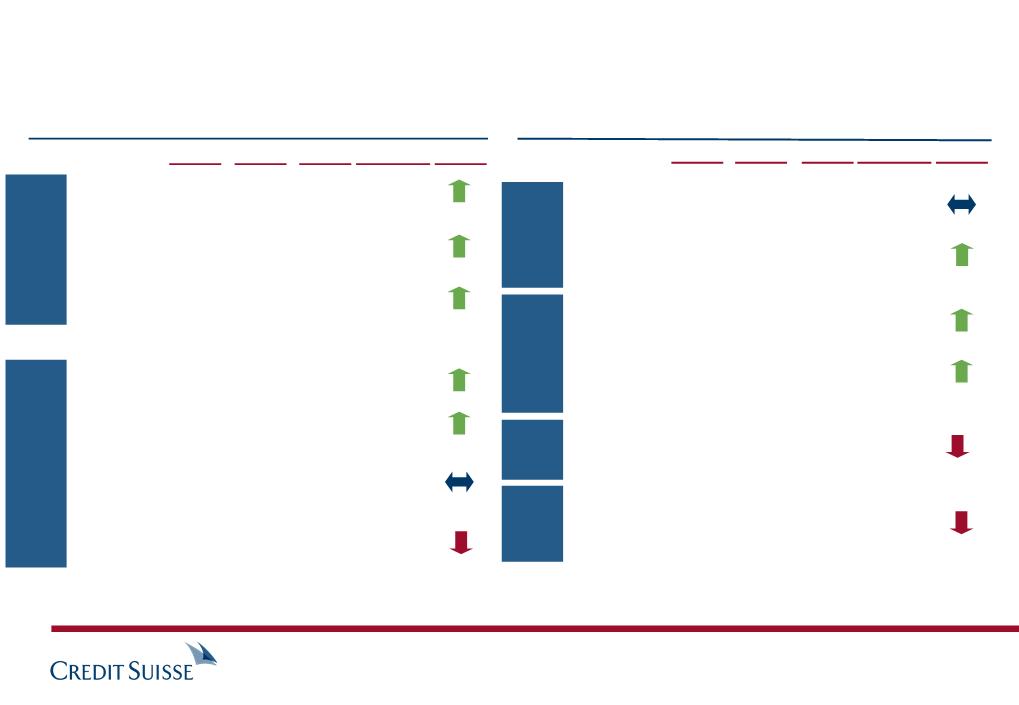

Background on CHF 50 to CHF 70 bn RWA mitigation impact

§ Starting point: CHF 27.5 bn core tier 1 capital (excl. hybrids)

Assumptions underlying the capital projections

1) Bloomberg consensus to 2012. Kept constant for 2013. Net income shown is not endorsed or verified and is used solely for illustrative purposes. Actual net income may differ significantly.

2) Primarily for residual deferred tax assets, pension plan adjustments, and participations in financial institutions

Common Equity Capital Ratio

§ Net income based on market expectations1); assumes

dividend payout ratio of 30%

dividend payout ratio of 30%

§ Based on Basel 3 RWA of CHF 340 bn (net of mitigation)

§ 5% organic RWA growth p.a. to 2012 to CHF 375 bn; kept

constant thereafter (i.e. in line with constant net income)

constant thereafter (i.e. in line with constant net income)

§ Net income kept constant from 2013 level1); dividend

payout ratio of 30%

payout ratio of 30%

§ Regulatory deductions to capital of approx. CHF 6 bn2)

phased-in from 2014 to 2018 on a straight-line basis

phased-in from 2014 to 2018 on a straight-line basis

§ Deferred tax assets on net operating losses to be utilized by 2014

(only 50% utilized in "stressed scenario")

(only 50% utilized in "stressed scenario")

§ Partial phase-out of "Claudius" notes by 2019

Basel 2 in 3Q10

Retained earnings

4Q10 to 2013

4Q10 to 2013

Increased RWA with

Basel 2.5 & Basel 3

Basel 2.5 & Basel 3

Basel 3 in 2013

Retained earnings

2014 to 2019

2014 to 2019

Phase-in of

deductions

deductions

Basel 3 in 2019

+7%

12%

12%

(6)%

+9%

(2)%

18%

Business growth

(1)%

Would be still over 10% under a "stressed

scenario" with 50% lower net income

scenario" with 50% lower net income

Third Quarter 2010 Results

Slide 27

Capital simulation under Basel 3 (for illustrative purposes only)

Views on the viability of the contingent convertible market

Who

Why

§ Traditional holders of bank capital notes will seek to replace holdings as they are being

called or mature

called or mature

§ Sovereign Wealth Funds and other funds will seek opportunities to invest in new asset

classes - especially as high-trigger CoCo mimics their deep-value investment thesis

classes - especially as high-trigger CoCo mimics their deep-value investment thesis

§ Superior economic value, higher yield and 'out-of-the-money' conversion may be viewed as

an attractive investment proposition also for more traditional investor groups

an attractive investment proposition also for more traditional investor groups

§ In a continued low interest rates environment, there is significant institutional and retail

investor appetite for higher-yielding assets

investor appetite for higher-yielding assets

§ Substantial current inventory of bank capital notes that will be called or mature

– Current Tier 1 and Tier 2 capital market outstanding estimated at EUR 450 bn

§ CoCo structure arguably a superior value to investors compared to a traditional

bankruptcy / liquidation scenario

bankruptcy / liquidation scenario

§ Substantial 'out-of-the-money' conversion, especially on low-trigger CoCo, should allow

for participation of traditional fixed income investor groups

for participation of traditional fixed income investor groups

Note: source Dealogic

Third Quarter 2010 Results

Slide 28

High trigger:

§ 3% of RWA requirement; 7% tier 1 trigger point

§ May replace existing hybrid capital

Note: Based on CHF 340 bn of Basel 3 risk-weighted assets 1) Inflated due to sizable issuance volumes in 2008; would be around 500 bps otherwise

Current

capital/funding components

capital/funding components

Future

capital/funding components

capital/funding components

Lower

tier 2 capital

tier 2 capital

Hybrid capital

34

"Claudius"

Upper

tier 2 capital

tier 2 capital

Shareholders'

equity

equity

192

Senior

long-term

debt

long-term

debt

Total

Regulatory

debt capital

debt capital

§ Weighted

spread: 480 bps

spread: 480 bps

§ Implied annual

spread costs:

CHF 1.2 bn

spread costs:

CHF 1.2 bn

750 bps1)

500 bps

350 bps

Indicative spreads

to senior debt:

to senior debt:

192

20

10

34

Senior long term debt:

§ Larger CoCo & equity balances imply a reduced requirement to fund

via senior bond markets

via senior bond markets

§ Spreads on senior bonds may price tighter, as the risk-profile of the

issuer improves and the theoretical liquidation value increases

issuer improves and the theoretical liquidation value increases

3.3

11.5

2.0

130

128

Low trigger:

§ 6% of RWA requirement; 5% tier 1 trigger point

§ May replace existing Tier 2 capital

28

Third Quarter 2010 Results

Slide 29

11.0

100 bps

CoCo:

§ CoCo structures (and excess equity) to fully substitute current

subordinated capital bonds

subordinated capital bonds

§ While the total amount of regulatory capital will increase, the average

"unit price" may come down, depending on spread assumptions

"unit price" may come down, depending on spread assumptions

Changes in the capital structure (for illustrative purposes only)

Third quarter 2010 results detail

David Mathers, Chief Financial Officer

Introduction

Brady W. Dougan, Chief Executive Officer

Regulatory capital review

David Mathers, Chief Financial Officer

Summary

Brady W. Dougan, Chief Executive Officer

Third Quarter 2010 Results

Slide 30

Questions & Answers

Third Quarter 2010 Results

Slide 31

3Q10:

Good result in a

quarter characterized

by challenging

conditions with low

market volumes and

subdued client

activity

quarter characterized

by challenging

conditions with low

market volumes and

subdued client

activity

Strongly positioned

with a distinctive

strategy

with a distinctive

strategy

§ Anticipated regulatory changes

§ Client-focused and capital-efficient business model

§ Ability to deliver high returns and book value accretion

§ Underlying net income of CHF 1 bn and underlying RoE of 11%

(CHF 4.0 bn and 15% in 9M10)

(CHF 4.0 bn and 15% in 9M10)

§ Solid pre-tax income in Private Bank with continued strong Wealth

Management inflows of CHF 12.4 bn; gross margin at 118 bp

Management inflows of CHF 12.4 bn; gross margin at 118 bp

§ Investment Banking with maintained market share performance in a

weak revenue environment, exacerbated by the seasonal slowdown

weak revenue environment, exacerbated by the seasonal slowdown

§ Asset Management with continued progress to grow its core

business; net new assets of CHF 3.6 bn represent positive asset

flows for the fifth consecutive quarter

business; net new assets of CHF 3.6 bn represent positive asset

flows for the fifth consecutive quarter

Third Quarter 2010 Results

Slide 32

Summary

Slide

34

35

36

37

38

39

40 to 41

42

Third Quarter 2010 Results

Slide 33

Appendix

Reconciliation from reported to underlying results

Collaboration revenues

Gross margin analysis in Wealth Management Clients business

Market share momentum in the Investment Bank

Balance sheet structure

Commercial mortgage exposures detail

Loan portfolio characteristics

Underlying results in the Corporate Center

Net revenues

Prov. for credit losses / (release)

Total operating expenses

Pre-tax income

Income tax expense

Noncontrolling interests

Net income

Return on equity

3Q10

reported

reported

3Q10

underlying

underlying

Impact from

the tightening

of spreads on

own debt1)

the tightening

of spreads on

own debt1)

UK

bonus levy

bonus levy

Normalization

to tax rate of

28%

to tax rate of

28%

CHF bn

1) Including fair valuation gains/losses on cross currency swaps relating to our long-term debt Note: numbers may not add to total due to rounding

Litigation

provisions

provisions

Third Quarter 2010 Results

Slide 34

6,284 589 - - - 6,873

(26) - - - - (26)

5,557 - 43 (73) - 5,527

753 589 (43) 73 - 1,372

117 170 - 30 67 384

(27) - - - - (27)

609 419 (43) 43 (67) 961

7.0% 11.2%

Underlying return on equity of 14.9% in 9M10

Reconciliation to underlying results

CHF bn

§ Stable revenues, whilst impacted by lower client

activity

activity

§ The pipeline on tailored-solutions for

Private Banking clients continues to build

Private Banking clients continues to build

1Q10

2Q10

Collaboration revenues

§ 9M10 already significantly exceeds FY 2009

§ CHF 8.6 bn of assets referrals for Private Banking

– Net new assets of CHF 3.6 bn

– Custody assets of CHF 5.0 bn

§ Generated CHF 2.0 bn in new mandates for

Asset Management

Asset Management

Asset referrals

3Q10

9M10

1.0

1.2

1.0

3.2

Third Quarter 2010 Results

Slide 35

Collaboration revenues

40

46

49

46

55

55

48

45

36

30

34

29

Quarterly average

2007

2008

2009

9M10

2,910

2,674

2,468

2,455

Net revenues

CHF m

Recurring

commissions

& fees

commissions

& fees

Recurring net

interest income

interest income

Transaction-

based revenues

based revenues

(15)%

(1)%

(15)%

Revenue drivers going forward

1,214

1,120

901

924

898

939

927

941

798

616

640

590

+9%

§ Increase in overall interest rate

environment

environment

§ Client activity (brokerage, product

issuing fees)

issuing fees)

§ Integrated solutions revenues

§ Level and mix of managed

investment products

investment products

§ Performance fees

AuM = Assets under Management

Quarterly average

2007

2008

2009

9M10

131

131

131

120

Gross margin

Basis points

§ Overall: Higher AuM

Third Quarter 2010 Results

Slide 36

Avg. AuM (CHF bn) 888 817 755 820

Wealth Management with stable revenues but reduction in

transaction-related and interest-related gross margin

transaction-related and interest-related gross margin

Source: Thomson Financial, Dealogic, Tradeweb, Euromoney magazine and Greenwich Associates

Note: Emerging markets fee data includes India, China, Indonesia, Brazil, Mexico, Russia, Middle East and Africa

1) YTD 9M10 represents most current data available

2) Represents trend compared to FY09

Securities

2) Rank based on a leading market share analysis provider;

market share based on Credit Suisse estimates

market share based on Credit Suisse estimates

3) Based on Credit Suisse estimates

4) Represents leveraged loans secondary trading

Underwriting and advisory

Fixed

Income

Income

2007

YTD 9M101)

2008

US cash

equities 2)

equities 2)

#2/12%

#4/12%

#5/12%

US electronic

trading 2)

trading 2)

#1/8%

#1/8%

#1/8%

Prime

services 2)

services 2)

Top 3/

>10%

Top 6/

~6%

Top 3/

>10%

Foreign

exchange

exchange

#8/4%

#14/2%

#9/3%

RMBS pass

- -throughs

- -throughs

#1/19%

#1/18%

#1/18%

Leveraged

loans 4)

loans 4)

#2/19%

#4/13%

#2/16%

2009

Equities

US rates

#6/9%

#10/5%

#8/6%

Trend2)

2007

YTD 9M10

2008

2009

Trend2)

(Rank/market share)

(Rank/market share)

#1/13%

#1/11%

#3/13%

NA

#1/19%

#3/13%

#5 - #6

9% - 10%

3)

3)

DCM

Investment

grade global

grade global

#10/4%

#13/3%

#12/4%

#5/5%

High yield

global

global

#4/9%

#2/11%

#3/11%

#3/10%

ECM

ECM global

#7/6%

#7/6%

#7/5%

#7/5%

Emerging

Markets

Markets

M&A

Global

announced

announced

#5/16%

#6/20%

#7/17%

#4/16%

Global

completed

completed

#8/15%

#8/18%

#7/19%

#5/16%

Total fees

#1/12%

#2/8%

#1/8%

#2/7%

Third Quarter 2010 Results

Slide 37

Continued client market share momentum; upside potential

remains

remains

Assets

Equity & liabilities

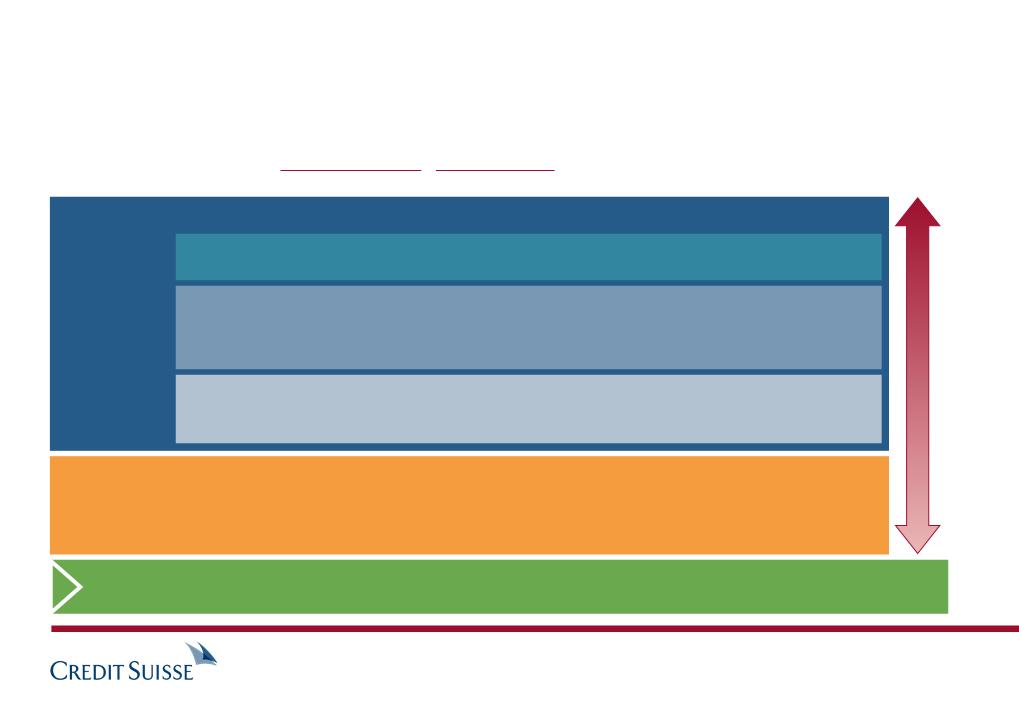

Asset and liabilities by category (end 3Q10 in CHF bn)

Reverse 222

repo

Encumbered 99

trading assets

1,067

1,067

Funding- 152

neutral assets 1)

Cash 2) 51

Unencumbered 165

liquid assets 4)

Customer 217

loans

Other 161

illiquid assets

Repo 243

Short positions 78

Funding- 152

neutral liabilities 1)

Short-term debt 2) 49

Other short-term liab 3) 50

Customer 271

deposits

Long-term debt 179

Total equity 45

125%

coverage

Match

funded

funded

§ Strong balance sheet structure and liquidity

maintained; well-positioned to succeed in

changing regulatory environment

maintained; well-positioned to succeed in

changing regulatory environment

§ 44% of balance sheet is match funded

§ Stable and low cost deposit base as key

funding advantage

funding advantage

§ Regulatory leverage ratio at 4.3%

§ 17% of balance sheet financed by long-term

debt (vs. 12% at end 2006)

debt (vs. 12% at end 2006)

§ Further lengthened long-term debt profile to

6.6 years duration (vs. 4.9 at end 2006) 5)

6.6 years duration (vs. 4.9 at end 2006) 5)

473

594

Third Quarter 2010 Results

Slide 38

1) Primarily brokerage receivables/payables, positive/negative replacement values and cash collateral

2) Includes due from/to banks

3) Primarily includes excess of funding neutral liabilities (brokerage payables) over corresponding assets

4) Primarily includes unencumbered trading assets, investment securities and excess reverse repo agreements, after

haircuts

haircuts

5) weighted average, assuming that callable securities are redeemed at final maturity, latest in 2030

Maintained strong funding structure

7

1) This price represents the average mark on loans and bonds combined

36

26

(93)%

19

15

13

9

3Q07

4Q07

1Q08

2Q08

3Q08

4Q08

1Q09

Commercial mortgages (CHF bn)

Exposure by region

§ Further reductions in exposure

achieved in 3Q10 due to sales and FX

movements

achieved in 3Q10 due to sales and FX

movements

§ Average price of remaining positions

is 48% (from 44% in 2Q10)1)

is 48% (from 44% in 2Q10)1)

§ Positions are fair valued;

no reclassifications to accrual book

no reclassifications to accrual book

Other

6%

Asia

8%

Germany

25%

US

16%

UK

2%

Other

Continental

Europe

Europe

50%

Office

47%

47%

Retail

5%

Hotel

21%

Multi-

family

family

20%

Exposure by loan type

2Q09

7

3.6

3Q09

3.1

4Q09

2.7

1Q10

2.6

2Q10

2.4

3Q10

Third Quarter 2010 Results

Slide 39

Commercial mortgage exposure reduction in Investment Banking

Developed market lending

§ Corporate loan portfolio 78% is investment grade, and is mostly

(91%) accounted for on a fair value basis

(91%) accounted for on a fair value basis

§ Fair value is a forward looking view which balances accounting

risks, matching treatment of loans and hedges

risks, matching treatment of loans and hedges

§ Loans are carried at an average mark of approx. 99% with

average mark of 96% in non-investment grade portfolio

average mark of 96% in non-investment grade portfolio

§ Continuing good performance of individual credits: limited

specific provisions during the quarter

specific provisions during the quarter

Unfunded

commitments

commitments

Loans

Hedges

CHF bn

Emerging market lending

§ Well-diversified by name and evenly spread between EMEA,

Americas and Asia and approx. 30% accounted for on a fair

value basis

Americas and Asia and approx. 30% accounted for on a fair

value basis

§ Emerging market loans are carried at an average mark of

approx. 97%

approx. 97%

§ No significant provisions during the quarter

Note: Average mark data is net of fair value discounts and credit

provisions

provisions

46

8

(17)

Loans

Hedges

CHF bn

15

(9)

Third Quarter 2010 Results

Slide 40

Investment Banking loan book

6% BB+ to BB

2% BB- and below

Portfolio ratings

composition, by CRM

transaction rating

composition, by CRM

transaction rating

Private Banking Loan Book

LTV = Loan to value

Total: CHF 182 bn

65%

27%

BBB

AAA to A

Total loan book of CHF 182 bn focused on Switzerland and 85% collateralized; primarily on accrual accounting basis

Third Quarter 2010 Results

Slide 41

Wealth Management Clients: CHF 132 bn

§ Portfolio remains geared towards mortgages (CHF 90 bn) and securities-backed

lending (CHF 35 bn) with conservative lending standards

lending (CHF 35 bn) with conservative lending standards

§ Residential real-estate: Prices for real-estate increase in most regions, especially in

Zurich, lake Geneva region and major tourist spots, slightly declining in structurally

weaker regions; outlook: flat with risk of some price falls only conceivable in the

Lake Geneva region and certain tourist regions

Zurich, lake Geneva region and major tourist spots, slightly declining in structurally

weaker regions; outlook: flat with risk of some price falls only conceivable in the

Lake Geneva region and certain tourist regions

Corporate & Institutional Clients: CHF 50 bn

§ Over 67% collateralized by mortgages and securities

§ Counterparties mainly Swiss corporates incl. real-estate industry

§ Sound credit quality with relatively low concentrations;

§ Stabilization of portfolio quality in line with continued recovery of Swiss

economy

economy

§ Ship finance portfolio (CHF 6 bn) remains under special focus due to

increased risk level caused by overcapacity in the market

increased risk level caused by overcapacity in the market

§ Commercial real-estate: Prices slightly increase for office space, prices for retail

space move sideways; outlook negative for both office and retail

space due to a slack/ decrease in demand coupled with still growing floorspace;

central and prime locations less affected by this decline in prices

space move sideways; outlook negative for both office and retail

space due to a slack/ decrease in demand coupled with still growing floorspace;