UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________

Form 6-K

______________

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

April 27, 2011

Commission File Number 001-15244

CREDIT SUISSE GROUP AG

(Translation of registrant’s name into English)

Paradeplatz 8, P.O. Box 1, CH-8070 Zurich, Switzerland

(Address of principal executive office)

______________

Commission File Number 001-33434

CREDIT SUISSE AG

(Translation of registrant’s name into English)

Paradeplatz 8, P.O. Box, CH-8070 Zurich, Switzerland

(Address of principal executive office)

______________

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F  | Form 40-F  |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Note: Regulation S-T Rule 101(b)(1) only permits the submission in paper of a Form 6-K if submitted solely to provide an attached annual report to security holders.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Note: Regulation S-T Rule 101(b)(7) only permits the submission in paper of a Form 6-K if submitted to furnish a report or other document that the registrant foreign private issuer must furnish and make public under the laws of the jurisdiction in which the registrant is incorporated, domiciled or legally organized (the registrant’s “home country”), or under the rules of the home country exchange on which the registrant’s securities are traded, as long as the report or other document is not a press release, is not required to be and has not been distributed to the registrant’s security holders, and, if discussing a material event, has already been the subject of a Form 6-K submission or other Commission filing on EDGAR.

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes | No |

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): 82-.

| CREDIT SUISSE GROUP AG | ||

Paradeplatz 8 P.O. Box CH-8070 Zurich Switzerland | Telephone +41 844 33 88 44 Fax +41 44 333 88 77 media.relations@credit-suisse.com | |

Media Release

Credit Suisse Group reports underlying* pre-tax profit of CHF 2.2 billion and underlying net income of CHF 1.6 billion; underlying return on equity 18.8%

Including fair value losses of CHF 617 million, CHF 467 million after tax, on own debt and stand-alone derivatives relating to own funding liabilities, pre-tax profit was CHF 1.6 billion and net income CHF 1.1 billion, return on equity of 13.4%

Net new assets totalled CHF 19.1 billion; very strong capital position with a tier 1 ratio of 18.2%

| · | Private Banking pre-tax income of CHF 0.9 billion with net new assets of CHF 18.0 billion |

| · | Investment Banking pre-tax income of CHF 1.3 billion; strong fixed income and solid equity sales and trading results; solid underwriting and advisory results; continued positive market share momentum |

| · | Asset Management pre-tax income of CHF 172 million; building fee-based revenues, net new assets of CHF 4.5 billion |

| · | Overall strong, high-quality operating results, evidencing continued client momentum and market share gains across businesses |

| · | Credit Suisse continued to build on an already very high capital position; tier 1 ratio of 18.2%, Core tier 1 ratio of 13.0%, announced two transactions to create up to 70% of its maximum potential issuance of high-trigger contingent capital suggested under the proposed Swiss regulations and capital requirements by 2019; deferred tax assets reduced by CHF 0.8 billion |

| · | During 1Q11 Credit Suisse continued to work closely with regulators to help build a more stable financial system. In line with its expectations, regulatory trends show progress in developing a more level playing field for the global banking industry |

Zurich, April 27, 2011 Credit Suisse reported underlying core results as follows: pre-tax income of 2.2 billion, net income of CHF 1.6 billion on net revenue of CHF 8.4 billion and return on equity of 18.8%. This excludes fair value losses of CHF 617 million (CHF 467 million after tax) on own debt and stand-alone derivatives relating to own funding liabilities. Net income attributable to shareholders was CHF 1.1 billion in 1Q11 on net revenues of CHF 8.2 billion and a return on equity attributable to shareholders of 13.4%. Diluted earnings per share were

| Media Release | |

April 27, 2011 Page 2/7 |

CHF 0.90 and the tier 1 ratio was 18.2% as of the end of 1Q11. The weakening of the average rate of the US dollar and euro against the Swiss franc adversely affected results in 1Q11 compared to the previous year period.

Brady W. Dougan, Chief Executive Officer, said: “With an underlying return on equity of 18.8% we have provided further evidence that our business model generates stable, high-quality earnings. In a quarter marked by significant market uncertainty, we have maintained our strong momentum with clients, gaining market share and generating CHF 19.1 billion net new assets. At the same time, we have continued to work with regulators to help build a more robust financial system, spearheading the creation of a market for contingent convertible capital. I am convinced that clients and investors will recognize that, by being an early adopter of new regulatory requirements, Credit Suisse is extremely well positioned and will be better placed to create significant value for them.”

Commenting on Private Banking, he said: “We achieved a good performance in Private Banking with continued positive client momentum and inflow of assets. This is the result of our longstanding efforts to build a multi-shore business and a comprehensive advisory process in Wealth Management, where we achieved an excellent result with CHF 15.7 billion in net new assets.”

Commenting on Investment Banking, he said: “Our Investment Bank continues to win market share with strong fixed income and solid equity sales and trading results as well as a solid performance in underwriting and advisory. The environment for fixed income trading improved in the first quarter and we are particularly pleased that the investment in this part of our business has begun to show a material impact on our performance. We also maintained our strong position in equity sales and trading. Our pipeline in underwriting and advisory remains strong and we are well positioned to capture increases in issuance levels and M&A activity.”

Commenting on Asset Management, he said: “In Asset Management we continue to successfully execute our strategy including our acquisitions such as Hedging-Griffo in Brazil and our stake in York Capital. There has been continued improvement in investment performance, performance fees have continued to grow and we believe there is further upside potential. We are also pleased with our steady quarterly net asset inflows.”

Commenting on the regulatory environment, he said: “In light of the financial crisis, banks need to embrace a stronger capital regime and with Basel III we have the framework to allow for consistent capital treatment globally. In 2010 the Swiss Expert Commission made proposals on how the Swiss large banks could address the too-big-to-fail issue. We support the Expert Commission’s proposals and believe they can be implemented without a large impact on our competitive position under Basel III. We are encouraged that measures proposed by regulators outside of Switzerland suggest that progress toward a more level playing field is being made.”

Commenting on the outlook, he said: “We expect the market environment to remain constructive. We also expect clients to remain active with an increased appetite for higher return assets and comprehensive advisory services. However, the macroeconomic recovery continues to be gradual and impacted by external and market events. Nonetheless, we have substantial momentum across all of our client based businesses and we remain well prepared to continue to capitalize on our improved market position.”

| Media Release | |

April 27, 2011 Page 3/7 |

| in CHF million (unless otherwise stated) | 1Q11 | 4Q10 | 1Q10 | Change in % | Change in % |

| vs. 4Q10 | vs. 1Q10 | ||||

| Net income attributable to shareholders | 1,139 | 841 | 2,055 | 35 | (45) |

| Diluted earnings per share (CHF) | 0.90 | 0.59 | 1.63 | 53 | (45) |

| Return on equity attributable to shareholders (annualized) | 13.4% | 9.8% | 22.3% | - | - |

| Tier 1 ratio (end of period) | 18.2% | 17.2% | 16.4% | - | - |

| Assets under management from continuing operations (CHF billion) | 1,282.4 | 1,253.0 | 1,270.9 | 2.3 | 0.9 |

| Core results | |||||

| Net revenues | 7,813 | 6,960 | 8,961 | 12 | (13) |

| Provision for credit losses | (7) | (23) | (50) | (70) | (86) |

| Total operating expenses | 6,195 | 5,676 | 6,077 | 9 | 2 |

| Income from continuing operations before taxes* | 1,625 | 1,307 | 2,934 | 24 | (45) |

Underlying results** | |||||

| Net revenues | 8,430 | 7,146 | 8,759 | 18 | (3.8) |

| Pre-tax income | 2,242 | 1,493 | 2,732 | 50.2 | (17.9) |

| Net income attributable to shareholders | 1,606 | 987 | 1,926 | 62.7 | (16.6) |

| Return on equity attributable to shareholders (annualized) | 18.8% | 11.5% | 20.9% | - | - |

| *Includes the results of the three segments and the Corporate Center, but does not include noncontrolling interests without significant economic interest. | |||||

| **Excluding fair value losses of CHF 617 million (CHF 467 million after tax) on own debt and stand-alone derivatives relating to own funding liabilities. | |||||

Segment Results

Private Banking

Private Banking, which comprises the Wealth Management Clients and Corporate & Institutional Clients businesses, reported income before taxes of CHF 855 million in 1Q11, down 4% compared to 1Q10. Net revenues were stable at CHF 2,896 million. This reflected 13% higher transaction-based revenues from an increase in client activity, offset by 5% lower recurring commissions and fees and a 3% lower net interest income. The decline in recurring commissions and fees was mainly from lower investment product management fees, primarily due to the positive impact from a change in estimate for prior-year fee accruals in 1Q10. Total operating expenses increased, reflecting slightly higher compensation and benefits, mainly from increased headcount. Provision for credit losses remained on a low level of CHF 12 million.

The Wealth Management Clients business reported income before taxes of CHF 623 million in 1Q11, down 8% compared to 1Q10, as stable net revenues and lower provision for credit losses were outweighed by slightly higher operating expenses. Net revenues reflected 4% lower net interest income and 5% lower recurring commissions and fees. This was offset by 11% higher transaction-based revenues, driven by higher brokerage and product issuing fees from an increased client activity, higher foreign exchange income from client transactions and revenues from integrated solutions. The gross margin of 118 basis points decreased 3 basis points from the prior year quarter as a lower margin related to recurring commissions and fees and net interest income was only partially offset by a higher transaction-based margin.

| Media Release | |

April 27, 2011 Page 4/7 |

The Corporate & Institutional Clients business, an important provider of financing for the Swiss economy, reported strong income before taxes of CHF 232 million, up 8% from 1Q10. A 6% increase in net revenues was accompanied by stable operating expenses and no provision for credit losses. Revenues were driven by a strong increase in transaction-based revenues.

Investment Banking

Investment Banking reported pre-tax income of CHF 1,343 million, down 25% compared to 1Q10 and up 141% from 4Q10. Net revenues of CHF 4,929 million were down 6% from 1Q10 and were up 42% from 4Q10. In US dollars, net revenues were 8% higher compared to 1Q10 and 49% higher compared to 4Q10, while pre-tax income was 15% lower compared to 1Q10 and 154% higher compared to 4Q10.

Net revenues included strong fixed income and solid equity sales and trading results, reflecting our franchise build-out, an improved market environment, an increase in client trading volumes and continued market share momentum. Our underwriting and advisory results were solid although lower than the seasonally strong 4Q10. Results reflected fair value losses on Credit Suisse vanilla debt and debit valuation adjustments (DVA) relating to certain structured note liabilities. Compensation and benefits of CHF 2,408 million in 1Q11 were higher than 1Q10, reflecting primarily higher social security taxes relating to share award deliveries in 1Q11. The average one-day, 99% risk management value-at-risk (VaR) was CHF 93 million in 1Q11, compared to CHF 104 million in 4Q10.

Asset Management

Asset Management reported pre-tax income of CHF 172 million, up 4% compared to 1Q10 and down 4% compared to 4Q10. Net revenues were down 6% from 1Q10 and 4% from 4Q10. Net revenues before investment-related gains and securities purchased from our money market funds were CHF 431 million, up 9% compared to 1Q10, reflecting improved results in diversified investments, alternative investments and traditional investments. Operating expenses of CHF 419 million were down 10% compared to 1Q10 with lower compensation and benefits, general and administrative and commission expenses. Assets under management were CHF 436 billion, up 2% compared to 4Q10, with positive market performance and net new assets.

Net New Assets

Private Banking recorded net new assets of CHF18.0 billion. The Wealth Management Clients business contributed net new assets of CHF 15.7 billion. Corporate & Institutional Clients contributed net new assets of CHF 2.3 billion. Compared to the end of 1Q10, assets under management were up 1.3%, reflecting net new assets and positive equity and bond market movements, mostly offset by adverse foreign exchange-related movements, mainly from the weakening of the euro and the US dollar during this period.

Asset Management reported net new assets of CHF 4.5 billion in 1Q11, including net inflows of CHF 3.9 billion in traditional investments, as inflows in multi-asset class solutions, equities and fixed income were partially offset by outflows from Swiss advisory and net inflows of CHF 0.6 billion in alternative investments, as inflows in real estate and commodities and exchange traded funds (ETFs) were mostly offset by private equity realizations and outflows in hedge funds. Compared to 1Q10, assets under management were stable with net new assets and positive market performance offset by adverse foreign exchange-related movements.

| Media Release | |

April 27, 2011 Page 5/7 |

Credit Suisse Group’s total assets under management were CHF 1,282.4 billion, stable compared to 1Q10 and up CHF 29 billion, or 2.3%, compared to the end of 4Q10, reflecting net new assets and positive market performance.

| in CHF million | 1Q11 | 4Q10 | 1Q10 | Change in % | Change in % | |

| vs. 4Q10 | vs. 1Q10 | |||||

| Private | Net revenues | 2,896 | 2,914 | 2,900 | (1) | 0 |

| Banking | Provision for credit losses | 12 | 4 | 19 | 200 | (37) |

| Total operating expenses | 2,029 | 2,086 | 1,989 | (3) | 2 | |

| Income before taxes | 855 | 824 | 892 | 4 | (4) | |

| Investment | Net revenues | 4,929 | 3,478 | 5,216 | 42 | (6) |

| Banking | Provision for credit losses | (19) | (27) | (69) | (30) | (72) |

| Total operating expenses | 3,605 | 2,947 | 3,491 | 22 | 3 | |

| Income before taxes | 1,343 | 558 | 1,794 | 141 | (25) | |

| Asset | Net revenues | 591 | 617 | 631 | (4) | (6) |

| Management | Provision for credit losses | 0 | 0 | 0 | - | - |

| Total operating expenses | 419 | 437 | 465 | (4) | (10) | |

| Income/(loss) before taxes | 172 | 180 | 166 | (4) | 4 | |

Capital and liquidity

Credit Suisse’s capital position remains very high. The tier 1 ratio was 18.2% as of the end of 1Q11, compared to 17.2% as of the end of 4Q10 and 16.4% as of the end of 1Q10. Core tier 1 ratio was 13.0% as of the end of 1Q11 compared to 12.2% at the end of 4Q10. Our total shareholders’ equity increased CHF 0.8 billion to CHF 34.1 billion as of the end of 1Q11 from CHF 33.3 billion as of the end of 4Q10. Net deferred tax assets decreased CHF 0.8 billion. Risk-weighted assets decreased 3% to CHF 212.2 billion as of the end of 1Q11.

Credit Suisse Group has worked closely with its primary regulator, FINMA, and the Swiss National Bank to agree the terms of two landmark buffer capital transactions, announced in February, to fulfil what will be required of large Swiss banks under proposed Swiss capital adequacy regulations. With these transactions Credit Suisse Group has already secured more than 70% of its maximum potential issuance of high-trigger contingent capital suggested under the proposed Swiss regulations.

Collaboration revenues

Revenues from the collaboration between Private Banking, Investment Banking and Asset Management were CHF 1.1 billion for 1Q11 or 14.1% of net revenues.

*Excluding fair value losses of CHF 617 million (CHF 467 million after tax) on own debt and stand-alone derivatives relating to own funding liabilities.

Information

Media Relations Credit Suisse AG, telephone +41 844 33 88 44, media.relations@credit-suisse.com

Investor Relations Credit Suisse AG, telephone +41 44 333 71 49, investor.relations@credit-suisse.com

| Media Release | |

April 27, 2011 Page 6/7 |

Credit Suisse AG

Credit Suisse AG is one of the world's leading financial services providers and is part of the Credit Suisse group of companies (referred to here as 'Credit Suisse'). As an integrated bank, Credit Suisse offers clients its combined expertise in the areas of private banking, investment banking and asset management. Credit Suisse provides advisory services, comprehensive solutions and innovative products to companies, institutional clients and high-net-worth private clients globally, as well as to retail clients in Switzerland. Credit Suisse is headquartered in Zurich and operates in over 50 countries worldwide. The group employs approximately 50,100 people. The registered shares (CSGN) of Credit Suisse's parent company, Credit Suisse Group AG, are listed in Switzerland and, in the form of American Depositary Shares (CS), in New York. Further information about Credit Suisse can be found at www.credit-suisse.com.

Cautionary statement regarding forward-looking information and non-GAAP information

This press release contains statements that constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act. In addition, in the future we, and others on our behalf, may make statements that constitute forward-looking statements. Such forward-looking statements may include, without limitation, statements relating to the following:

| – | our plans, objectives or goals; |

| – | our future economic performance or prospects; |

| – | the potential effect on our future performance of certain contingencies; and |

| – | assumptions underlying any such statements. |

Words such as “believes,” “anticipates,” “expects,” “intends” and “plans” and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. We do not intend to update these forward-looking statements except as may be required by applicable securities laws. By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, and risks exist that predictions, forecasts, projections and other outcomes described or implied in forward-looking statements will not be achieved. We caution you that a number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in such forward-looking statements. These factors include:

| – | the ability to maintain sufficient liquidity and access capital markets; |

| – | market and interest rate fluctuations and interest rate levels; |

| – | the strength of the global economy in general and the strength of the economies of the countries in which we conduct our operations, in particular the risk of continued slow economic recovery in the US or other developed countries in 2011 and beyond; |

| – | the direct and indirect impacts of continuing deterioration or slow recovery in residential and commercial real estate markets; |

| – | adverse rating actions by credit rating agencies in respect of sovereign issuers, structured credit products or other credit-related exposures; |

| – | the ability of counterparties to meet their obligations to us; |

| – | the effects of, and changes in, fiscal, monetary, trade and tax policies, and currency fluctuations; |

| – | political and social developments, including war, civil unrest or terrorist activity; |

| – | the possibility of foreign exchange controls, expropriation, nationalization or confiscation of assets in countries in which we conduct our operations; |

| – | operational factors such as systems failure, human error, or the failure to implement procedures properly; |

| – | actions taken by regulators with respect to our business and practices in one or more of the countries in which we conduct our operations; |

| – | the effects of changes in laws, regulations or accounting policies or practices; |

| – | competition in geographic and business areas in which we conduct our operations; |

| – | the ability to retain and recruit qualified personnel; |

| – | the ability to maintain our reputation and promote our brand; |

| – | the ability to increase market share and control expenses; |

| – | technological changes; |

| – | the timely development and acceptance of our new products and services and the perceived overall value of these products and services by users; |

| – | acquisitions, including the ability to integrate acquired businesses successfully, and divestitures, including the ability to sell non-core assets; |

| – | the adverse resolution of litigation and other contingencies; |

| – | the ability to achieve our cost efficiency goals and cost targets; and |

| – | our success at managing the risks involved in the foregoing. |

We caution you that the foregoing list of important factors is not exclusive. When evaluating forward-looking statements, you should carefully consider the foregoing factors and other uncertainties and events, as well as the information set forth in our Annual Report 2010 under IX – Additional information – Risk Factors.

This press release contains non-GAAP financial information. Information needed to reconcile such non-GAAP financial information to the most directly comparable measures under GAAP can be found in the Credit Suisse Financial Release 1Q11.

| Media Release | |

April 27, 2011 Page 7/7 |

Presentation of Credit Suisse Group’s 1Q11 results via audio webcast and telephone conference

| Date | Wednesday, April 27, 2011 | ||

| Time | 09:00 Zurich / 08:00 London / 03:00 New York | ||

| Speakers | Brady W. Dougan, Chief Executive Officer David Mathers, Chief Financial Officer The presentations will be held in English. | ||

| Audio webcast | www.credit-suisse.com/results | ||

| Telephone | Switzerland: | +41 44 580 40 01 | |

| Europe: | +44 1452 565 510 | ||

| US: | +1 866 389 9771 | ||

| Reference: Credit Suisse Group quarterly results | |||

| Q&A session | You will have the opportunity to ask questions during the telephone conference following the presentations. | ||

| Playback | Playback available approximately 2 hours after the event at | ||

| www.credit- suisse.com/results or on the telephone numbers below: | |||

| Switzerland: | +41 44 580 34 56 | ||

| Europe: | +44 1452 550 000 | ||

| US: | +1 866 247 4222 | ||

| Conference ID: 56853338# | |||

First Quarter Results 2011

Zurich

April 27, 2011

Cautionary statement regarding forward-looking and non-GAAP information

This presentation contains forward-looking statements within the meaning of the Private Securities

Litigation Reform Act of 1995. Forward-looking statements involve inherent risks and uncertainties,

and we might not be able to achieve the predictions, forecasts, projections and other outcomes we

describe or imply in forward-looking statements.

Litigation Reform Act of 1995. Forward-looking statements involve inherent risks and uncertainties,

and we might not be able to achieve the predictions, forecasts, projections and other outcomes we

describe or imply in forward-looking statements.

A number of important factors could cause results to differ materially from the plans, objectives,

expectations, estimates and intentions we express in these forward-looking statements, including

those we identify in "Risk Factors" in our Annual Report on Form 20-F for the fiscal year ended

December 31, 2010 filed with the US Securities and Exchange Commission, and in other public

filings and press releases. We do not intend to update these forward-looking statements except as

may be required by applicable laws.

expectations, estimates and intentions we express in these forward-looking statements, including

those we identify in "Risk Factors" in our Annual Report on Form 20-F for the fiscal year ended

December 31, 2010 filed with the US Securities and Exchange Commission, and in other public

filings and press releases. We do not intend to update these forward-looking statements except as

may be required by applicable laws.

This presentation contains non-GAAP financial information. Information needed to reconcile such

non-GAAP financial information to the most directly comparable measures under GAAP can be

found in Credit Suisse Group's first quarter report 2011.

non-GAAP financial information to the most directly comparable measures under GAAP can be

found in Credit Suisse Group's first quarter report 2011.

First Quarter Results 2011

Slide 1

Cautionary statement

First quarter 2011 results detail

David Mathers, Chief Financial Officer

Introduction

Brady W. Dougan, Chief Executive Officer

Summary

Brady W. Dougan, Chief Executive Officer

First Quarter Results 2011

Slide 2

Delivering

client-focused

franchise

client-focused

franchise

Balanced and

high quality

results

high quality

results

Further

strengthened

our capital

position

strengthened

our capital

position

§ Underlying results: pre-tax income of CHF 2.2 bn, net income of CHF 1.6 bn and

after-tax return on equity of 19%

after-tax return on equity of 19%

§ Net new assets of CHF 19 bn

§ Basel 2 tier 1 capital ratio of 18.2% and core tier 1 ratio of 13.0%

§ Executed more than 70% of required high trigger Contingent Capital

§ Shareholders’ equity up 2% (CHF 0.8 bn) and deferred tax assets down 9% (CHF 0.8 bn)

§ Strong liquidity and funding position as competitive advantage

§ Global regulatory trends indicating emergence of a more level playing field

Private Banking with strong inflows and improved transaction revenues offsetting decline in net

interest income

interest income

Investment Banking with record first quarter revenues (in USD) driven by continued market

share momentum and beneficial impact of client flow-sales expansion

share momentum and beneficial impact of client flow-sales expansion

Asset Management with solid inflows and higher quality results reflecting increased fee-based

revenues and reduced expenses

revenues and reduced expenses

First Quarter Results 2011

Slide 3

Introduction

First quarter 2011 results detail

Introduction

Summary

First Quarter Results 2011

Slide 4

Reported in CHF bn

Net revenues

Pre-tax income

Net income attributable to shareholders

Diluted earnings per share in CHF

A reconciliation from reported results to underlying results can be found in the appendix of this presentation

Net revenues

Pre-tax income

Net income attributable to shareholders

Diluted earnings per share in CHF

Pre-tax income margin

Return on equity

Net new assets in CHF bn

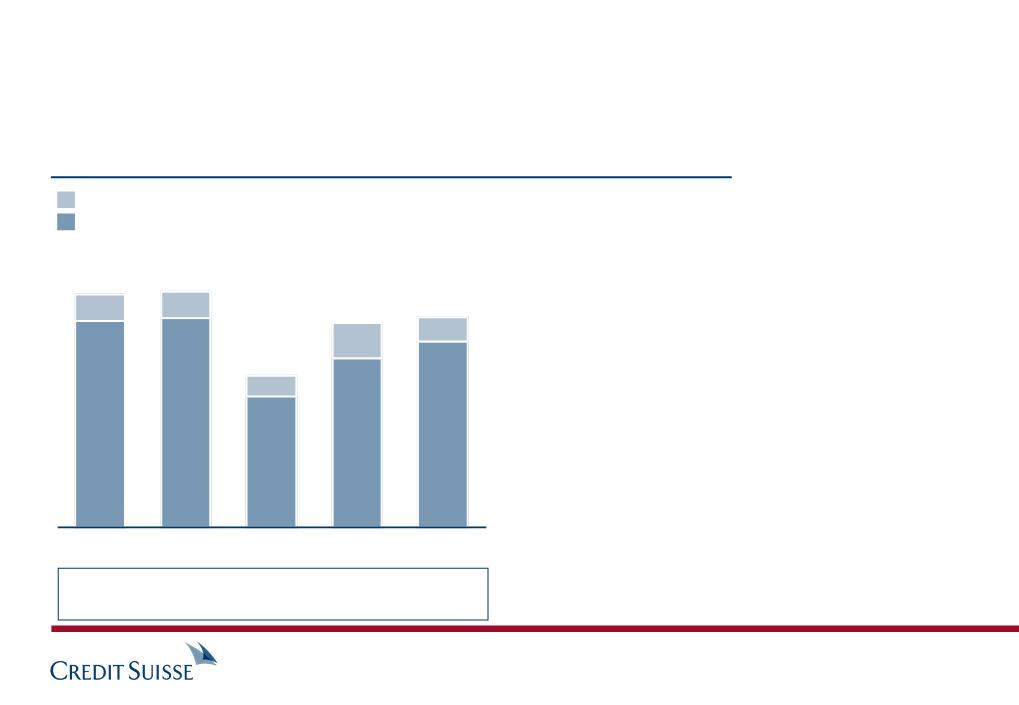

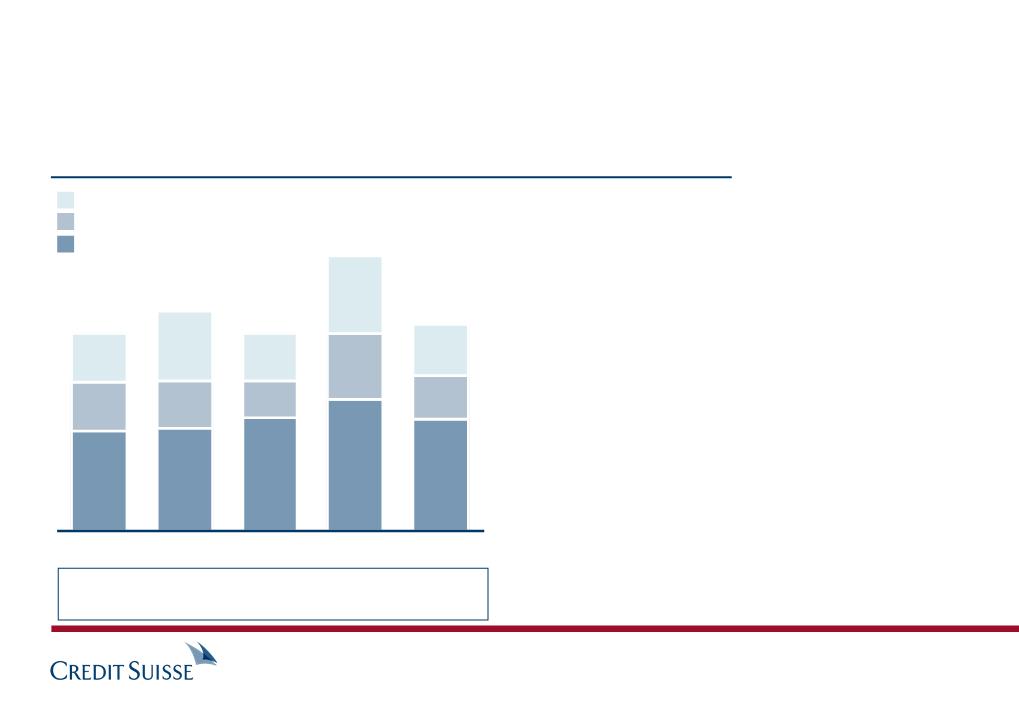

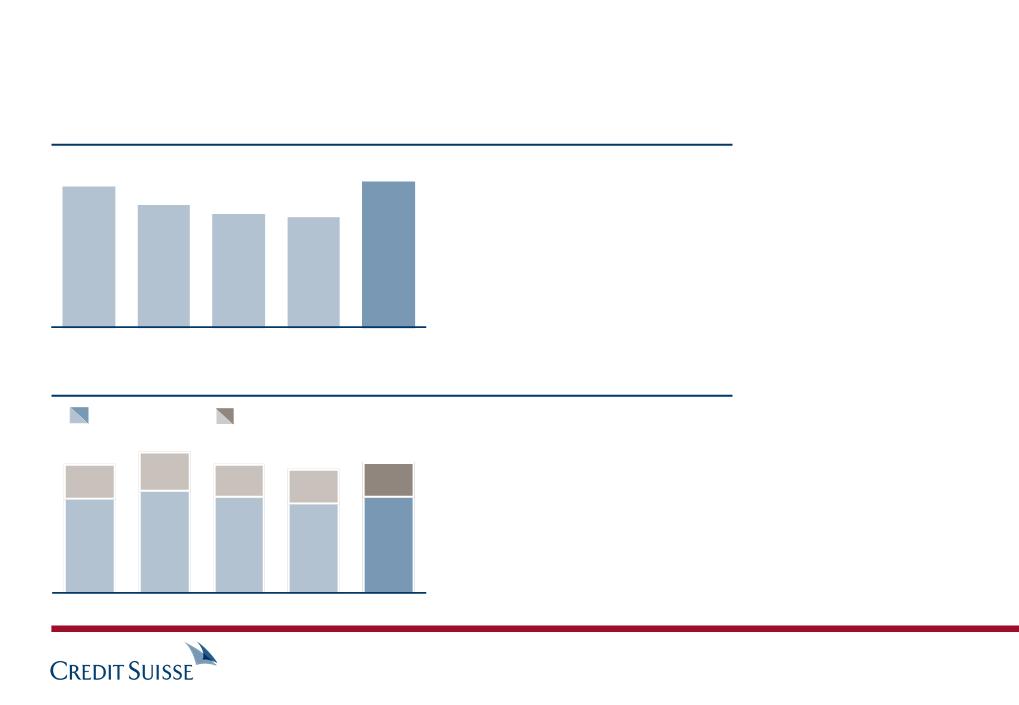

Underlying in CHF bn 1Q11 4Q10 3Q10 2Q10 1Q10

First Quarter Results 2011

Slide 5

8.4 7.1 6.9 7.5 8.8

2.2 1.5 1.4 1.6 2.7

1.6 1.0 1.0 1.1 1.9

1.28 0.71 0.76 0.74 1.53

27% 21% 20% 21% 31%

19% 12% 11% 12% 21%

19.1 13.9 14.6 14.5 26.0

7.8 7.0 6.3 8.4 9.0

1.6 1.3 0.8 1.8 2.9

1.1 0.8 0.6 1.6 2.1

0.90 0.59 0.48 1.15 1.63

Core results overview

§ Pre-tax margin of 30% in 1Q11

§ 1Q11 expenses of CHF 2 bn in line with 2010 quarterly run-rate, reflecting continued investment

into our international franchise offset by ongoing cost saving measures

into our international franchise offset by ongoing cost saving measures

§ Continue to upgrade relationship manager population while keeping headcount stable

§ Productivity gains from front-to-back efficiency enhancements

Strong

asset

inflows

asset

inflows

§ Net new assets of CHF 18 bn, with very strong inflows in Wealth Management of

CHF 15.7 bn, representing an annual growth rate of 7.8%

CHF 15.7 bn, representing an annual growth rate of 7.8%

§ Evidence of clients’ trust in Credit Suisse multi-shore business model

§ Net interest income suffered from an FX-related decrease in average deposits and lower

reinvestment rates

reinvestment rates

§ Transaction-based revenues increased due to higher brokerage and product issuing fees,

including stronger demand for structured products

including stronger demand for structured products

§ Continue to benefit from strength of our Swiss businesses in an environment with strong

economic fundamentals

economic fundamentals

Diverging

revenue

trends

revenue

trends

Continue

focus on

efficiency

focus on

efficiency

First Quarter Results 2011

Slide 6

Private Banking with solid performance despite ongoing low

interest environment

interest environment

Net revenues

Provisions for credit losses

Total operating expenses

Pre-tax income

Pre-tax income margin

Gross margin in basis points

Net new assets in CHF bn

Number of relationship managers

CHF m 1Q11 4Q10 3Q10 2Q10 1Q10

First Quarter Results 2011

Slide 7

2,433 2,464 2,385 2,516 2,464

12 14 8 16 32

1,798 1,844 1,765 1,867 1,755

623 606 612 633 677

26% 25% 26% 25% 28%

118 120 118 120 121

15.7 8.1 12.4 11.9 12.9

4,200 4,200 4,190 4,130 4,110

Wealth Management with strong asset inflows and

stable results

stable results

1Q10

921

+149

Increase

assuming stable

FX rates

assuming stable

FX rates

Transaction-

based

revenues

based

revenues

Net interest

income

income

Recurring

commissions

& fees

commissions

& fees

956

587

2,464

1Q11

880

904

649

2,433

(180)

Impact from

stronger

Swiss franc

stronger

Swiss franc

§ Higher brokerage and product issuing fees,

including stronger demand for structured products,

reflecting increased client activity

including stronger demand for structured products,

reflecting increased client activity

§ Mainly reflects gain from change in estimate for fee

accruals that benefited 1Q10

accruals that benefited 1Q10

§ Low fee level continues to reflect risk-averse asset

mix

mix

§ Mainly reflects reduction in average deposit

volumes (FX-related) and lower margins

volumes (FX-related) and lower margins

§ Ongoing impact from low interest rate environment

Net revenues in CHF m

Strengthening of Swiss franc negatively

impacted pre-tax income by CHF 130 m

impacted pre-tax income by CHF 130 m

+11%

(5)%

(4)%

+6%

First Quarter Results 2011

Slide 8

Adverse foreign exchange impact masks underlying

growth trend in Wealth Management

growth trend in Wealth Management

Wealth Management - Net interest income in CHF m

2008

Quarterly average

939

880

2009

2010

§ Interest income suffered due to a FX rate-driven decrease

in average deposit volumes and a continued roll-over of

the portfolio at a low reinvestment rate

in average deposit volumes and a continued roll-over of

the portfolio at a low reinvestment rate

§ Scenario analysis:

– a roll-off at current low rates would lead to approx.

CHF 20 m reduction in quarterly revenues

CHF 20 m reduction in quarterly revenues

– a 100 bp parallel shift in major interest rates would lead

to approx. CHF 75 to 100 m additional quarterly

revenues over time

to approx. CHF 75 to 100 m additional quarterly

revenues over time

927

937

1Q11

Note: Scenario analysis assumes stable volumes

First Quarter Results 2011

Slide 9

Short-term pressure but mid-term potential in net interest

income

income

Wealth Management - Transaction-based revenues in CHF m

798

616

649

640

601

2007

Quarterly average

2009

2010

1Q11

2008

Brokerage & product issuing revenues

Other transaction-based revenues

§ Since 2007, lower client activity and change in

product mix negatively affected revenues

product mix negatively affected revenues

§ Client behavior expected to normalize over

time

time

– seeing signs of a recovery since 3Q10 low-

point

point

§ Further upside from integrated solutions

revenues from intensified collaboration with

Investment Banking

revenues from intensified collaboration with

Investment Banking

First Quarter Results 2011

Slide 10

Recent recovery in transaction-based revenues

Net new assets in CHF bn

Annualized net new assets growth in %

6.4 5.8 6.2 4.0 7.8

1Q10

2Q10

3Q10

4Q10

1Q11

15.7

EMEA

Americas

Asia Pacific

Switzerland

12.9

11.9

12.4

8.1

4.0

3.0

4.0

4.7

§ 1Q11 growth rate of 7.8% well above

our 6% target growth rate

our 6% target growth rate

§ Total inflows of CHF 140 bn since

2008 evidencing significant market

share gains

2008 evidencing significant market

share gains

§ Broad inflows across all client

segments with strong contribution

from emerging markets

segments with strong contribution

from emerging markets

First Quarter Results 2011

Slide 11

Wealth Management with continued strong and broadly

distributed net new asset inflows

distributed net new asset inflows

Highlights

1Q11

1Q11

Net revenues

Provisions for credit losses

Total operating expenses

Pre-tax income

Pre-tax income margin

Net new assets in CHF bn

CHF m 1Q11 4Q10 3Q10 2Q10 1Q10

§ Maintained very strong pre-tax margin at 50%

§ Solid net new assets of CHF 2.3 bn

§ Continued low credit provisions, reflecting quality of the loan book

First Quarter Results 2011

Slide 12

463 450 441 475 436

0 (10) (16) (13) (13)

231 242 233 247 234

232 218 224 241 215

50% 48% 51% 51% 49%

2.3 1.5 0.2 1.9 5.7

Corporate & Institutional Clients business continues to

deliver strong results

deliver strong results

Solid

underwriting

and advisory

results

underwriting

and advisory

results

§ Strong debt underwriting revenues, driven by continued strength in high yield

issuance volumes

issuance volumes

§ Solid results in equity underwriting and advisory, although lower compared to the

seasonally strong 4Q10, driven by lower industry-wide issuance volumes and

completed M&A activity

seasonally strong 4Q10, driven by lower industry-wide issuance volumes and

completed M&A activity

§ Revenues continued to be solid reflecting an increase in client volumes

§ Sustained strong market share positions across key businesses

§ Record revenues in Derivatives and stable results in Cash Equities and Prime

Services

Services

Solid equity

sales and

trading

results

sales and

trading

results

§ Strong revenues reflecting franchise build-out, market share gains, increased

client activity and an improved market environment from 4Q10

client activity and an improved market environment from 4Q10

§ Strong results in Securitized Products, Rates and Credit

§ Impact of sales force expansion continues to materialize, with further opportunity

to capitalize on increasing client volumes

to capitalize on increasing client volumes

Strong fixed

income sales

and trading

results

income sales

and trading

results

First Quarter Results 2011

Slide 13

Strong Investment Banking results

Net revenues (USD)

Pre-tax income (USD)

.

5,367 3,618 3,456 3,793 4,986

1,499 624 467 794 1,756

.

Net revenues

Provisions for credit losses

Compensation and benefits

Other operating expenses

Pre-tax income

Pre-tax income margin

CHF m 1Q11 4Q10 3Q10 2Q10 1Q10

Note: Excluding impact of movements in spreads on own debt of CHF (52) m, CHF (54) m, CHF (57) m, CHF (62) m and CHF (59) m in 1Q11, 4Q10, 3Q10, 2Q10 and 1Q10, respectively.

Including debit valuation adjustments (DVA) related to certain structured note liabilities of CHF (85) m, CHF 15 m, CHF (172) m, CHF 121 m and CHF (37) m in 1Q11, 4Q10, 3Q10, 2Q10

and1Q10, respectively.

and1Q10, respectively.

Significant quarter-on-quarter revenue momentum in USD

First Quarter Results 2011

Slide 14

4,981 3,532 3,478 4,161 5,275

(19) (27) (18) 17 (69)

2,408 1,823 1,872 2,014 2,324

1,198 1,124 1,172 1,284 1,167

1,394 612 452 846 1,853

28% 17% 13% 20% 35%

Investment Banking delivered strong results in 1Q11

1) Excludes impact of movements in spreads on own debt and includes DVA of CHF (20) m, CHF 5 m,

CHF (54) m, CHF 57 m and CHF (17) m in 1Q11, 4Q10, 3Q10, 2Q10 and 1Q10, respectively

CHF (54) m, CHF 57 m and CHF (17) m in 1Q11, 4Q10, 3Q10, 2Q10 and 1Q10, respectively

Fixed income sales & trading and underwriting revenues in CHF bn 1)

Debt underwriting

Fixed income sales and trading

2.0

1.5

0.5

3.2

2.7

0.5

2.0

1.5

0.5

1.5

0.9

0.6

1Q10

2Q10

3Q10

4Q10

1Q11

in USD bn

3.0 1.8 2.0 1.6 3.3

3.0

2.5

0.5

§ Increased client activity and revenues across most

businesses; in US dollar terms revenues increased

10% from 1Q10

businesses; in US dollar terms revenues increased

10% from 1Q10

§ Strong revenues in Securitized Products, driven by

increased client flows in non-agency RMBS

increased client flows in non-agency RMBS

§ Credit performance driven by robust Leveraged

Finance trading and strong new issue activity

Finance trading and strong new issue activity

§ Strong results in Rates, benefitting from higher

client flows, expanded footprint and higher interest

rate volatility

client flows, expanded footprint and higher interest

rate volatility

First Quarter Results 2011

Slide 15

Strong fixed income revenues reflecting franchise build-out,

improved market share and an increase in client activity from 4Q10

improved market share and an increase in client activity from 4Q10

100%

119%

10.5%

4.9%

2.2%

1.1%

1Q10

1Q11

Credit

FX

Global

Rates

Rates

Emerging

Markets

Markets

Indexed sales credits

§ Sales force expansion

in 2010 enabled

broader and deeper

product offering

in 2010 enabled

broader and deeper

product offering

§ Sales credit growth

particularly strong in

Rates and FX

particularly strong in

Rates and FX

§ Significant revenue

opportunity remains

across products

opportunity remains

across products

Contribution to fixed income sales credit growth 1)

1) Sales credits limited to secondary trading activity; excludes all capital

markets and advisory revenues and new issue-related sales credits

markets and advisory revenues and new issue-related sales credits

First Quarter Results 2011

Slide 16

Impact of sales force expansion continues to materialize, with

further opportunity to capitalize on increasing client volumes

further opportunity to capitalize on increasing client volumes

1) Excludes impact of movements in spreads on own debt and includes DVA of CHF (65) m, CHF 10 m,

CHF (118) m, CHF 64 m and CHF (19) m in 1Q11, 4Q10, 3Q10, 2Q10 and 1Q10, respectively

CHF (118) m, CHF 64 m and CHF (19) m in 1Q11, 4Q10, 3Q10, 2Q10 and 1Q10, respectively

2) Source: Greenwich Associates for rank and Credit Suisse estimates for market share

Equity sales & trading and underwriting revenues in CHF bn 1)

Equity underwriting

Equity sales and trading

§ Record revenues in Derivatives driven by increased

client flows, an improvement in corporate derivatives

and a more favorable trading environment

client flows, an improvement in corporate derivatives

and a more favorable trading environment

§ Stable results in Cash Equities and Prime Services

on mixed market trends and continued market share

gains

on mixed market trends and continued market share

gains

§ Maintained #1 positions and improved market share

in US cash equities trading and US electronic

trading 2)

in US cash equities trading and US electronic

trading 2)

§ Revenues reflect adverse foreign exchange impact of

a strengthening Swiss franc; in US dollar terms,

revenues were slightly higher compared to 1Q10

a strengthening Swiss franc; in US dollar terms,

revenues were slightly higher compared to 1Q10

1.9

1.7

0.2

1.7

1.4

0.3

1.3

1.1

0.2

1.9

1.7

0.2

1Q10

2Q10

3Q10

4Q10

1Q11

in USD bn

1.8 1.8 1.2 1.7 1.9

1.7

1.5

0.2

First Quarter Results 2011

Slide 17

Equity revenues continued to be solid, driven by increased

client volumes and sustained market share positions

client volumes and sustained market share positions

1) Underwriting revenues are also included in the Securities view revenues on slides 15 and 17

Advisory and underwriting in CHF bn 1)

Advisory

Debt underwriting

Equity underwriting

0.9

0.2

0.5

0.2

1.2

0.3

0.3

0.6

1.0

0.3

0.5

0.2

0.9

0.2

0.2

0.5

§ Solid debt underwriting revenues driven by

continued strong high yield issuance volumes and

improved market share

continued strong high yield issuance volumes and

improved market share

§ Equity underwriting revenues stable compared to

1Q10, but lower than a strong 4Q10 given a

decline in industry-wide issuance levels

1Q10, but lower than a strong 4Q10 given a

decline in industry-wide issuance levels

§ Advisory results reflect lower industry-wide

completed M&A activity vs. 4Q10; M&A and

capital markets pipelines remain strong

completed M&A activity vs. 4Q10; M&A and

capital markets pipelines remain strong

§ Improved or maintained market share across key

products

products

1Q10

2Q10

3Q10

4Q10

1Q11

in USD bn

0.8 0.9 0.9 1.3 1.0

0.9

0.2

0.2

0.5

First Quarter Results 2011

Slide 18

Solid advisory and underwriting revenues, although lower than

a seasonally strong 4Q10

a seasonally strong 4Q10

Securities

3. Represents leveraged loans secondary trading

4. Emerging markets fee data includes India, China, Indonesia, Brazil, Mexico, Russia, Middle East and

Africa

Africa

Underwriting and advisory

Fixed

Income

Income

2008

Current

2009

US cash

equities 1)

equities 1)

#2/12%

#5/12%

US electronic

trading 1)

trading 1)

#1/8%

#1/8%

Prime

services 2)

services 2)

Top 3/

>10%

Top 3/

>10%

Foreign

exchange

exchange

#8/4%

#9/3%

RMBS pass

-throughs

-throughs

#1/19%

#1/18%

Leveraged

loans 3)

loans 3)

#2/19%

#2/16%

2010

Equities

US rates

#8/7%

#8/6%

Trend

2008

1Q11

2009

2010

Trend

(Rank/market share)

(Rank/market share)

#1/13%

#1/11%

#3/13%

NA

#1/17%

#3/13%

#7/8%

Source: Dealogic, Tradeweb, Euromoney magazine and Greenwich Associates

1. Market share based on Credit Suisse estimates; rank based on Greenwich Associates

2. Based on Credit Suisse estimates

DCM

Investment

grade global

grade global

#8/5%

#12/4%

#8/4%

High yield

global

global

#4/9%

#3/7%

#3/8%

ECM

ECM global

#7/6%

#7/5%

#6/6%

Emer-

ging

Markets

ging

Markets

M&A

Global

announced

announced

#8/12%

#8/13%

#3/16%

Global

completed

completed

#9/13%

#7/16%

#4/15%

Total

fees4)

fees4)

#1/12%

#1/8%

#1/8%

#1/14%

#1/12%

#3/13%

NA

#1/18%

#3/13%

#7/8%

#12/3%

#2/10%

#5/7%

#4/19%

#10/10%

#1/8%

High yield

secondary

secondary

#5/11%

#5/11%

#7/10%

#7/10%

First Quarter Results 2011

Slide 19

Continued client market share momentum; upside potential remains

Leveraged finance

Rates

Securitized products

Equity derivatives

Prime Services

M&A

FX

Investment grade

Emerging markets

Cash equities

Equity capital

markets

Commodities

Revenue contribution in

1Q 2011

1Q 2011

Market environment

Credit

Suisse

market

share

Suisse

market

share

Strong

Worse than historic levels

Better than historic levels

Upside

potential

potential

Average quarterly revenue

contribution in FY 2010

contribution in FY 2010

Revenue contribution from major business lines

First Quarter Results 2011

Slide 20

Improved revenues across most businesses driven by higher client

activity, market share gains and a more favorable market environment

activity, market share gains and a more favorable market environment

1,167

305

Commission expenses

G&A expenses

1,284

933

351

Investment Banking compensation expenses in CHF m

Investment Banking non-compensation expenses in CHF m

§ Increase in G&A from 4Q10 driven by a CHF 34 m increase

in litigation provisions, higher professional and consulting

fees driven by regulatory changes, and non-income taxes

in litigation provisions, higher professional and consulting

fees driven by regulatory changes, and non-income taxes

§ 1Q11 commission expenses reflect the reclassification of

CHF 22 m of commodities storage costs from contra

revenue to commission expense

CHF 22 m of commodities storage costs from contra

revenue to commission expense

862

2,014

2,324

1,823

1,172

§ Increase from 1Q10 driven by higher social security taxes of

CHF 70 m relating to share award deliveries in 1Q11 (prior

year deliveries occurred in 2Q10)

CHF 70 m relating to share award deliveries in 1Q11 (prior

year deliveries occurred in 2Q10)

§ Compensation/revenue ratio of 48% in 1Q11 compared to

49% in full-year 2010 and 44% in 1Q10

49% in full-year 2010 and 44% in 1Q10

877

295

1,872

1,124

823

301

2,408

1,197

887

310

3Q10

4Q10

2Q10

1Q10

1Q11

3Q10

4Q10

2Q10

1Q10

1Q11

Note: Compensation/revenue ratio excluding fair value on own debt

First Quarter Results 2011

Slide 21

Compensation and non-compensation expenses

§ Solid asset inflows of CHF 4.5 bn in 1Q11

§ Positive inflows for the seventh consecutive quarter, reflecting strong

investment performance and an expansion of our product offering

investment performance and an expansion of our product offering

Growing fee-

based revenues

based revenues

§ Fee-based revenues up 9% from 1Q10, adjusted for FX impact

§ Potential upside from performance fees

§ Positive fund raising trends result in higher placement fees

§ Total operating expenses down 4% from 1Q10, adjusted for FX impact

§ Disciplined approach to spending and execution of efficiency programs

§ Further efficiency initiatives in the pipeline

Significant and

sustainable

expense

reductions

sustainable

expense

reductions

Continued

business

momentum

business

momentum

First Quarter Results 2011

Slide 22

Better results through increased scale, strong investment performance

and a general improvement in efficiency

and a general improvement in efficiency

Asset Management delivers better and higher quality results

Net revenues

Compensation and benefits

Other operating expenses

Pre-tax income

Pre-tax income margin

Net new assets in CHF bn

CHF m 1Q11 4Q10 3Q10 2Q10 1Q10

First Quarter Results 2011

Slide 23

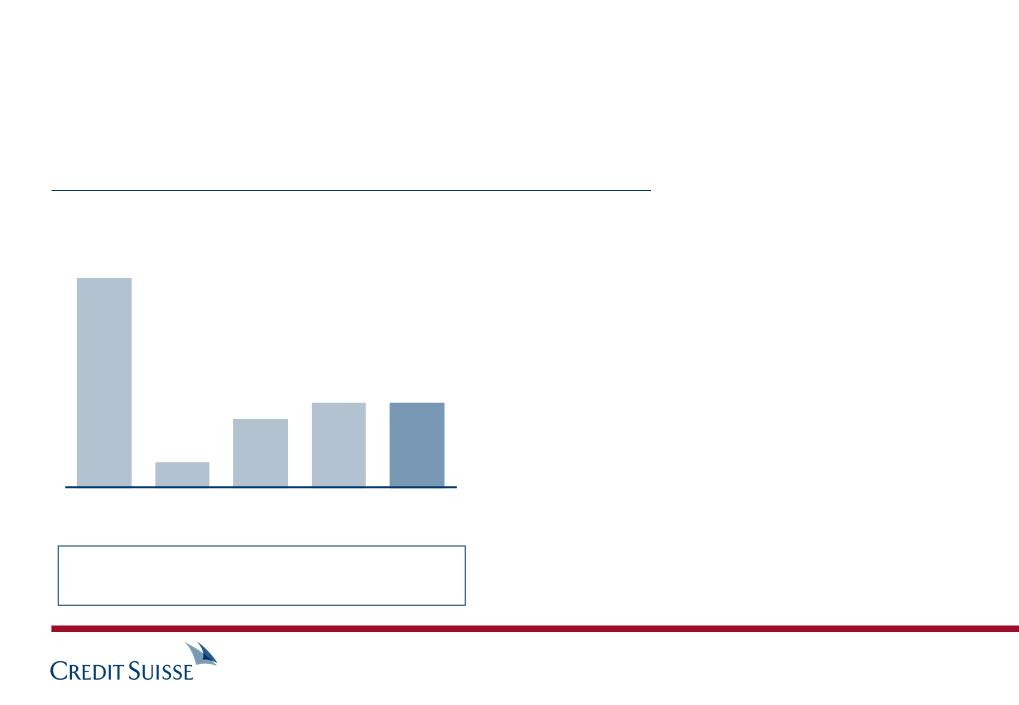

591 617 582 502 631

260 250 261 289 282

159 187 186 191 183

172 180 135 22 166

29% 29% 23% 4% 26%

4.5 4.5 3.6 1.3 11.2

Asset Management consistently building sound profitability

and steady asset inflows

and steady asset inflows

11.2

4.5

1.3

4.5

3.6

Net new assets in CHF bn

Annualized net new assets growth in %

10.8 1.2 3.4 4.3 4.2

1Q10

2Q10

3Q10

4Q10

1Q11

MACS = multi-asset class solutions

§ Strong inflows in asset allocation (MACS)

driven by improving investment performance

driven by improving investment performance

§ Equities and single-manager hedge fund

inflows reflect solid performance, expanded

product offering and renewed client interest

inflows reflect solid performance, expanded

product offering and renewed client interest

First Quarter Results 2011

Slide 24

Solid net new asset inflows in Asset Management

1Q10

(28)

+65

Underlying

growth

growth

433

1Q11

443

Business

divestitures

divestitures

CHF m

405

Fee-based gross margin in basis points

41

41

+9%

Stable

Foreign

exchange

exchange

(27)

Total operating

expenses in CHF m

expenses in CHF m

465

419

Proforma

(30)

+14

435

(30)

(4)%

First Quarter Results 2011

Slide 25

Asset Management fee-based revenue with underlying

growth; progress in driving efficiency gains

growth; progress in driving efficiency gains

Performance fees and carried interest in CHF m

1Q

2Q

(11)

37

3Q

4Q

1Q11

34

2009

1Q

2Q

3Q

4Q

2010

26

168

16

3

40

128

§ Performance fee recognition typically

semi-annual (Hedging Griffo) or

annual (York Capital)

semi-annual (Hedging Griffo) or

annual (York Capital)

§ Full year impact of annual performance

fees from York Capital expected in 4Q11

fees from York Capital expected in 4Q11

§ Carried interest earned upon investment

realizations

realizations

First Quarter Results 2011

Slide 26

Seasonality of performance fees with upside potential

Italy

Spain

Portugal

Greece

Ireland

Total Net

Gross

Gross

Net

Exposure in EUR bn

Sovereigns

Financial

institutions

institutions

Corporates /

Other

Other

Other exposures to

First Quarter Results 2011

Slide 27

2.3 0.3 1.0 0.9

0.1 0.1 0.9 0.9

0.2 0.0 0.1 0.1

0.1 0.0 0.1 0.1

0.0 0.0 0.3 0.4

2.7 0.4 2.4 2.4

4.5 5.6

Selected European risk exposures at end 1Q11

Basel 2 risk-weighted assets in CHF bn and tier 1 capital ratios in %

10.0

13.3

257

324

16.3

222

2010

1Q11

Strong capital base

§ Basel 2 tier 1 ratio of 18.2%

§ Core tier 1 ratio of 13.0%

§ Proforma Basel 2.5 core tier 1 ratio of

10.2%

10.2%

§ Regulatory capital reflects CHF 423 m

deduction for quarterly dividend accrual

(amount in line with dividend for FY 2010)

deduction for quarterly dividend accrual

(amount in line with dividend for FY 2010)

2008

2009

2007

(35)%

(3)%

18.2

219

212

Tier 1 ratio

Core tier 1 ratio

8.7

8.6

10.8

17.2

13.0

12.2

First Quarter Results 2011

Slide 28

Maintained leading capital position

Capital development in CHF bn

31.2

34.1

(2.2)

(0.7)

Dividend accrual

2010 and 1Q11

2010 and 1Q11

FVOD3)

Shareholders’

equity

equity

Regulatory

deductions

deductions

Common Equity

Tier 1 Capital1)

Tier 1 Capital1)

End

1Q11

1Q11

January

1, 2013

Consensus2)

earnings 2011-12

Consensus dividends

2011-20122)

2011-20122)

Common Equity

Tier 1 Capital

Tier 1 Capital

11.5

(2.5)

40.2

Risk-weighted assets development in CHF bn

212

Basel 2

end 1Q11

end 1Q11

330 to 350

Basel 34)

by Jan. 1st

by Jan. 1st

2013

+ 181

(50 to 70)

Basel 2.5 & 3

changes

changes

Mitigation

1) Applying January 1, 2013 Basel 3 capital rules 2) Bloomberg consensus net income and dividend estimates for 2011 and 2012 adjusted for 1Q11 net income and dividend accrual. Not endorsed or

verified and is used solely for illustrative purposes. Actual net income may differ significantly. 3) FVOD = fair value changes from movements in spreads on own debt and structured notes, net of tax

4) Assumes no gross increase in RWA from business growth

verified and is used solely for illustrative purposes. Actual net income may differ significantly. 3) FVOD = fair value changes from movements in spreads on own debt and structured notes, net of tax

4) Assumes no gross increase in RWA from business growth

Proforma CET1

ratio 9.2%

end 1Q11

ratio 9.2%

end 1Q11

Proforma CET1

ratio 11.8%

Jan 1, 2013

ratio 11.8%

Jan 1, 2013

Approx. 400

First Quarter Results 2011

Slide 29

Common Equity Tier 1 ratio simulation for January 1, 2013 (Basel 3)

5.0

5.5

End

2010

2010

End

1Q11

1Q11

1Q11

"earn-out"

"earn-out"

CHF bn

3.2

3.5

9.0

8.2

(9)%

Net DTA on net operating losses

Net DTA on timing differences

§ Significant DTA utilization in 1Q11

– Net DTA on net operating losses reduced by CHF 0.5 bn,

driven by profitable US businesses, resulting in a higher

effective Group tax rate

driven by profitable US businesses, resulting in a higher

effective Group tax rate

– Net DTA on timing differences reduced by CHF 0.3 bn

§ Net DTA on net operating losses expected to be substantially

reduced by the beginning of 2014

reduced by the beginning of 2014

§ Any residual balance of net DTA on timing differences by

1.1.2014 not expected to lead to regulatory capital deduction

under the “15% limit on specific items under Basel 3”

1.1.2014 not expected to lead to regulatory capital deduction

under the “15% limit on specific items under Basel 3”

First Quarter Results 2011

Slide 30

Reduction in net deferred tax assets (DTA)

1) Based on CHF 340 bn of Basel 3 risk-weighted assets

20

End 1Q11 capital/

funding components

funding components

Indicative spreads

over senior debt

over senior debt

CHF bn

6

2

2

Low trigger con-

tingent capital

tingent capital

6% of RWA

5% trigger point

Senior

long-term

debt

long-term

debt

137

134

164

Total

164

Senior long-term

debt

debt

Hybrid

tier 1

capital

(& Claudius

notes)

(& Claudius

notes)

Tier 2

capital

capital

475 bp

440 bp

14

11

27

625 bp

(at time of issuance)

Future capital / funding components1)

High trigger con-

tingent capital

tingent capital

3% of RWA

7% trigger point

30

§ Expected to price in line with tier 2 debt

§ May reflect new developments in

regulations around acceptable

structures (e.g. write-down features)

regulations around acceptable

structures (e.g. write-down features)

§ Completed CHF 6 bn private placement

and USD 2 bn public offering in Feb-11

and USD 2 bn public offering in Feb-11

§ Secured over 70% of requirement

§ Increased contingent capital and equity

balances imply a lower funding

requirement via senior bond markets

balances imply a lower funding

requirement via senior bond markets

§ Spreads may price tighter, as the risk

profile improves and the theoretical

liquidation value increases

profile improves and the theoretical

liquidation value increases

High trigger

tier 2 BCN

tier 2 BCN

2

First Quarter Results 2011

Slide 31

New regulatory regime compared to current subordinated capital

Assets

Equity & liabilities

Asset and liabilities by category (end 1Q11 in CHF bn)

1) Primarily brokerage receivables/payables, positive/negative replacement values and cash collateral

2) Includes due from/to banks

3) Primarily includes excess of funding neutral liabilities (brokerage payables) over corresponding assets

4) Primarily includes unencumbered trading assets, investment securities and excess reverse repo

agreements, after haircuts

agreements, after haircuts

Note: Basel 3 liquidity rules and calculation of NSFR and LCR ratios are not finalized; statements and ratios

shown here are based on interpretation of current proposals

shown here are based on interpretation of current proposals

Reverse 177

repo

Encumbered 88

trading assets

1,016

1,016

Funding- 133

neutral assets 1)

Cash 2) 75

Unencumbered 168

liquid assets 4)

Customer 217

loans

Other 158

illiquid assets

Repo 178

Short positions 87

Funding- 133

neutral liabilities 1)

Short-term debt 2) 92

Other short-term liab 3) 42

Customer 265

deposits

Long-term debt 176

Total equity 43

122%

coverage

Match

funded

funded

§ Well prepared for Basel 3 liquidity and funding requirements

– Excess short-term (30 days) liquidity of CHF 119 bn

represents a ratio of 127% under Swiss regulation; approach

similar to the Basel 3 "Liquidity coverage ratio (LCR)"

represents a ratio of 127% under Swiss regulation; approach

similar to the Basel 3 "Liquidity coverage ratio (LCR)"

– Basel 3 "Net Stable Funding Ratio (NSFR)" (1-year)

estimated at around 94%, with future funding plans projected

to raise the ratio to over 100% by 2013

estimated at around 94%, with future funding plans projected

to raise the ratio to over 100% by 2013

§ Regulatory leverage ratio at 4.7% (vs. 4.2% at 1Q10)

§ Funding spreads remain amongst the tightest of the peer group

§ Already completed more than 40% of CHF 16 bn long-term

debt funding plan for year 2011

debt funding plan for year 2011

398

618

First Quarter Results 2011

Slide 32

Strong funding and liquidity position

Annual rate of return on equity above 15% reflecting

increased capital requirements under Basel 3

increased capital requirements under Basel 3

14%

2009

2010

2013 to 2015

target

target

Greater

than 15%

than 15%

21%

1Q11

19%

16%

22%

§ 2010 returns were ahead of cost of equity under Basel 2

§ 2010 return under Basel 3 capital requirement is lower,

but does not reflect any mitigating actions (re-pricing,

portfolio realignments and run-off of CHF 0.5 bn losses

in "Exit" businesses)

but does not reflect any mitigating actions (re-pricing,

portfolio realignments and run-off of CHF 0.5 bn losses

in "Exit" businesses)

§ 1Q11 returns well ahead of cost of equity under Basel 3

2010

Based on end 2010, Basel 2

implied minimum equity

implied minimum equity

Credit Suisse Group

After-tax return on equity

After-tax return on equity

Investment Banking

Pro-forma after-tax return on equity

Pro-forma after-tax return on equity

1Q11

Based on Jan 1, 2013, Basel 3

implied minimum equity

implied minimum equity

11%

16%

2010

1Q11

Implied minimum equity calculation: Basel 2 assumes 12.5% target core tier 1 ratio with hybrid capital representing buffer capital; Basel 3 assumed 10% CET1 ratio per Swiss capital regime proposals

Proforma returns based on 2010 and 1Q11 effective Group tax rate

23%

pro-forma

based on Basel 2

implied minimum

equity

based on Basel 2

implied minimum

equity

Underlying

First Quarter Results 2011

Slide 33

First quarter 2011 results detail

Introduction

Summary

First Quarter Results 2011

Slide 34

Delivering

client-focused

franchise

client-focused

franchise

Balanced and

high quality

results

high quality

results

Further

strengthened

our capital

position

strengthened

our capital

position

§ Underlying results: pre-tax income of CHF 2.2 bn, net income of CHF 1.6 bn and

after-tax return on equity of 19%

after-tax return on equity of 19%

§ Net new assets of CHF 19 bn

§ Basel 2 tier 1 capital ratio of 18.2% and core tier 1 ratio of 13.0%

§ Executed more than 70% of required high trigger Contingent Capital

§ Shareholders’ equity up 2% (CHF 0.8 bn) and deferred tax assets down 9% (CHF 0.8 bn)

§ Strong liquidity and funding position as competitive advantage

§ Global regulatory trends indicating emergence of a more level playing field

Private Banking with strong inflows and improved transaction revenues offsetting decline in

net interest income

net interest income

Investment Banking with record first quarter revenues (in USD) driven by continued market

share momentum and beneficial impact of client flow-sales expansion

share momentum and beneficial impact of client flow-sales expansion

Asset Management with solid inflows and higher quality results reflecting increased fee-

based revenues and reduced expenses

based revenues and reduced expenses

First Quarter Results 2011

Slide 35

Summary

Slides

37 to 38

39

40

41

42

43

44

45

46 to 47

First Quarter Results 2011

Slide 36

Appendix

Reconciliation to underlying results

Underlying results in the Corporate Center

Collaboration revenues

Investment Banking capital simulation

Optimizing returns in Investment Banking

Regulatory capital (Basel 2) roll-forward

Basel 2.5 impact by division

Commercial mortgage exposures detail

Loan portfolio characteristics

1) Including fair valuation gains/losses on stand-alone derivatives related to certain of our funding liabilities

1Q11

reported

reported

1Q11

underlying

underlying

Impact from

the movement

of spreads on

own debt1)

the movement

of spreads on

own debt1)

CHF m

Net revenues

Provisions for credit losses / (release))

Total operating expenses

Pre-tax income

Income tax expense

Net income

Return on equity

First Quarter Results 2011

Slide 37

7.813 0.617 8.430

(0.007) - (0.007)

6.195 - 6.195

1.625 0.617 2.242

0.462 0.150 0.615

1.139 0.467 1.606

13.4% 18.8%

Reconciliation from reported to underlying results 1Q11

Net revenues

Prov. for credit losses / (release)

Total operating expenses

Pre-tax income

Income tax expense

Discontinued operations

Noncontrolling interests

Net income

Return on equity

2010

reported

reported

2010

underlying

underlying

Impact from

movements in

spreads on

own debt1)

movements in

spreads on

own debt1)

UK

bonus levy

bonus levy

Normalization

to tax rate of

28%

to tax rate of

28%

CHF m

1) Including fair valuation gains/losses on stand-alone derivatives related to certain of our funding liabilities

Litigation

provisions

provisions

First Quarter Results 2011

Slide 38

30,625 (343) - - - 30,282

(79) - - - - (79)

23,904 - (404) (289) - 23,211

6,800 (343) 404 289 - 7,150

1,548 (124) - 116 488 2,028

(19) - - - - (19)

(135) - - - - (135)

5,098 (219) 404 173 (488) 4,968

14.4% 14.1%

Reconciliation from reported to underlying results 2010

Reported pre-tax income / (loss)

Losses/(gains) from the movement of spreads on own debt1)

Impairment in a equity method investment

Litigation provisions

UK bonus levy

Litigation and settlement expenses

Reclassification of gain to discontinued operations2)

Adjusted pre-tax income / (loss)

CHF m

2010

2009

1) Including fair valuation gains/losses on stand-alone derivatives related to certain of our funding liabilities

2) Gain on sale of part of Asset Management's traditional fund business Note: numbers may not add to total due to rounding

The underlying Corporate Center pre-tax loss reflects:

– consolidation and elimination adjustments

– expenses for centrally sponsored projects

– certain expenses and revenues that have not been allocated to the segments

1Q11

First Quarter Results 2011

Slide 39

(1,948) (660) (745)

327 (590) 562

- - 47

- 216 -

- 404 -

818 - -

228 - -

(575) (630) (136)

Results in the Corporate Center

CHF bn

§ Collaboration revenues are up 10% vs. 1Q10

across all regions

across all regions

§ As markets normalize, we expect revenues to

increase in line with overall performance

increase in line with overall performance

§ The pipeline on tailored solutions for Private

Banking clients continues to build

Banking clients continues to build

1Q10

2Q10

3Q10

1Q11

4Q10

14.3%

15.9%

17.2%

14.1%

11.2%

Collaboration revenues

Core results net revenues

1.0

9.0

1.2

8.4

1.0

6.3

1.2

7.0

1.1

7.8

First Quarter Results 2011

Slide 40

Collaboration revenues

137

End 2010

(Basel 2)

(Basel 2)

Proforma end 2012

(Basel 3, post mitigation)

(Basel 3, post mitigation)

247

+80%

17

at 12.5%

core tier1 ratio

core tier1 ratio

at 10%

CET1 ratio

CET1 ratio

25

+47%

Implied minimum shareholders’ equity calculation: for Basel 2, assumed 12.5% target core tier 1 ratio with hybrid capital representing buffer capital; for Basel 3, assumed 10% CET1 ratio per Swiss capital

regime proposals

regime proposals

in CHF bn

Investment Banking

gross risk-weighted

assets

gross risk-weighted

assets

Implied minimum

shareholders’ equity

shareholders’ equity

First Quarter Results 2011

Slide 41

Investment Banking capital simulation

Build

position in

Banking

position in

Banking

Industry

leader-

ship in

Equities

leader-

ship in

Equities

Achieve

capital

efficient

scale in

Fixed

Income

capital

efficient

scale in

Fixed

Income

Overall

First Quarter Results 2011

Slide 42

§ Cash Equities and Prime Services largely unaffected by

Basel 3

Basel 3

§ Focus on derivatives flow businesses, where Basel 3 has

limited impact

limited impact

§ Continue to improve M&A and underwriting market share

§ Lock in #1 position within financial sponsors

§ Business largely unaffected by Basel 3 changes

§ Maintain leadership in RMBS and High-Yield products,

where returns are expected to be good also under Basel 3

where returns are expected to be good also under Basel 3

§ Continue to build capital-efficient scale in Rates and FX

client-flow capabilities

client-flow capabilities

§ Exit wind-down businesses

(pre-tax loss of CHF 0.5 bn in 2010 and 120 m in 1Q11)

(pre-tax loss of CHF 0.5 bn in 2010 and 120 m in 1Q11)

§ Product re-pricing or

enhanced market share

as industry adjusts to

increased capital

requirements

enhanced market share

as industry adjusts to

increased capital

requirements

§ Portfolio focus on

scaleable capital-

efficient and client-

focused businesses

scaleable capital-

efficient and client-

focused businesses

§ Continued cost

discipline with further

benefit from efficiency

gains and the inte-

grated banking model

discipline with further

benefit from efficiency

gains and the inte-

grated banking model

Optimizing returns in Investment Banking

37.7 17.2% 218.7

1.1

0.3

(0.4)

(0.4)

0.2

(6.5)

38.5 18.2% 212.2

(2.7) 30.6

35.8 14.7% 242.8

End 2010 (Basel 2)

Net income

Fair value movements

FX impact

2011 dividend accrual

Other1)

Change in RWA

End 1Q11 (Basel 2)

Basel 2.5 impact

End 1Q11 (Basel 2.5)

Tier 1

RWA

in CHF bn

in CHF bn

Capital

in CHF bn

in CHF bn

Ratio

in %

in %

End 2010

Net income

Share-based compensation

& other share activity2)

& other share activity2)

FX impact

Other

End 1Q11

Shareholders' equity

Common

in CHF bn

in CHF bn

Per share

in CHF

in CHF

Note: numbers may not add to total due to rounding

1) Reflects the issuance and redemption of tier 1 capital, the effect of share-based compensation and the change in regulatory deductions

2) Includes impact from issuance of shares for share-based compensation purposes (14.8 m shares) and reduction in treasury shares (12.2 m shares)

First Quarter Results 2011

Slide 43

33.3 28.35

1.1 0.97

0.2 (0.44)

(0.4) (0.37)

(0.1) (0.15)

34.1 28.36

Tier 1 capital and shareholders' equity roll-forward

Risk-weighted assets in CHF m

Under Basel 2

Incremental Basel 2.5 impact

Total under Basel 2.5

Capital deductions in CHF m

Under Basel 2

Incremental Basel 2.5 impact

Total under Basel 2.5

Private

Banking

Banking

Asset

Management

Management

Investment

Banking

Banking

Corporate

Center

Center

Total

First Quarter Results 2011

Slide 44

64,041 124,233 12,709 11,213 212,196

11 30,032 - 594 30,637

64,052 154,265 12,709 11,807 242,833

306 447 459 22 1,234

- 2,743 - - 2,743

306 3,190 459 22 3,977

Basel 2.5 impact by division

7

1) This price represents the average mark on loans and bonds combined

36

26

(96)%

19

15

13

9

3Q07

4Q

1Q08

2Q

3Q

4Q

1Q09

Commercial mortgages (CHF bn)

Exposure by region

§ Average price of remaining positions

is stable at 56%1)

is stable at 56%1)

§ Positions are fair valued;

no reclassifications to accrual book

no reclassifications to accrual book

Other

2%

Asia

2%

US

18%

Continental

Europe (ex. Germany)

Europe (ex. Germany)

80%

Office

82%

82%

Retail 2%

Hotel

21%

Exposure by loan type

2Q

7

3.6

3Q

3.1

4Q

2.7

1Q10

2.6

2Q

2.4

3Q

4Q

Hotel

14%

14%

1.5

1.5

1Q11

First Quarter Results 2011

Slide 45

Commercial mortgage exposure reduction in Investment Banking

Developed market lending

§ Corporate loan portfolio 76% is investment grade, and is mostly

(92%) accounted for on a fair value basis

(92%) accounted for on a fair value basis

§ Fair value is a forward looking view which balances accounting

risks, matching treatment of loans and hedges

risks, matching treatment of loans and hedges

§ Loans are carried at an average mark of approx. 99% with

average mark of 97% in non-investment grade portfolio

average mark of 97% in non-investment grade portfolio

§ Continuing good performance of individual credits: limited

specific provisions during the quarter

specific provisions during the quarter

Unfunded

commitments

commitments

Loans

Hedges

CHF bn

Emerging market lending

§ Well-diversified by name and evenly spread between EMEA,

Americas and Asia and approx. 25% accounted for on a fair

value basis

Americas and Asia and approx. 25% accounted for on a fair

value basis

§ Emerging market loans are carried at an average mark of

approx. 95%

approx. 95%

§ No significant provisions during the quarter