UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 6-K/A

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

UNDER THE SECURITIES EXCHANGE ACT OF 1934

March 24, 2017

Commission File Number 001-15244

CREDIT SUISSE GROUP AG

(Translation of registrant’s name into English)

Paradeplatz 8, CH 8001 Zurich, Switzerland

(Address of principal executive office)

(Address of principal executive office)

Commission File Number 001-33434

CREDIT SUISSE AG

(Translation of registrant’s name into English)

Paradeplatz 8, CH 8001 Zurich, Switzerland

(Address of principal executive office)

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or

Form 40-F.

Form 40-F.

Form 20-F  Form 40-F

Form 40-F

Form 40-F Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Note: Regulation S-T Rule 101(b)(1) only permits the submission in paper of a Form 6-K if submitted solely to provide an attached annual report to security holders.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Note: Regulation S-T Rule 101(b)(7) only permits the submission in paper of a Form 6-K if submitted to furnish a report or other document that the registrant foreign private issuer must furnish and make public under the laws of the jurisdiction in which the registrant is incorporated, domiciled or legally organized (the registrant’s “home country”), or under the rules of the home country exchange on which the registrant’s securities are traded, as long as the report or other document is not a press release, is not required to be and has not been distributed to the registrant’s security holders, and, if discussing a material event, has already been the subject of a Form 6-K submission or other Commission filing on EDGAR.

This report on Form 6-K/A of Credit Suisse Group AG and Credit Suisse AG supersedes and replaces the report on Form 6-K of Credit Suisse Group AG and Credit Suisse AG dated February 14, 2017 (accession number 0001370368-17-000012) in its entirety.

Fourth Quarter and Full Year 2016 Results Presentation to Investors and Analysts Revised – March 24, 2017 As announced on March 24, 2017, we updated our previously reported unaudited financial results for 4Q16 and 2016 to reflect additional after tax charges of CHF 272 million. These charges reflect an increase in the existing litigation provision by CHF 300 million for a settlement in principle to resolve the RMBS matter with the National Credit Union Administration Board. In addition, in our APAC division the previously reported amounts as of the end of 2016 for AuM and 2016 NNA have been reduced by CHF 1.4 billion and CHF 1 billion, respectively.This revised presentation updates those financial results and related information to reflect these charges and changes in AuM and NNA and does not update or modify any other information contained in the presentation originally published on February 14, 2017 that does not relate to these charges or changes to AuM and NNA. Specifically, terms such as “to date”, “current” or similar language used herein refers to the time at which these statements were originally made on February 14, 2017.

Disclaimer (1/2) The data presented in this presentation relating to the Swiss Universal Bank refers to the division of Credit Suisse Group as the same is currently managed within Credit Suisse Group. The scope, revenues and expenses of the Swiss Universal Bank vary from the planned scope of Credit Suisse (Schweiz) AG and its subsidiaries, for which a partial initial public offering (IPO) is planned, market conditions permitting. Any such IPO would involve the sale of a minority stake and would be subject to, among other things, all necessary approvals.It is therefore not possible to make a like-for-like comparison of the Swiss Universal Bank as a division of Credit Suisse Group on the one hand and Credit Suisse (Schweiz) AG as a potential IPO vehicle on the other hand.Cautionary statement regarding forward-looking statements This presentation contains forward-looking statements that involve inherent risks and uncertainties, and we might not be able to achieve the predictions, forecasts, projections and other outcomes we describe or imply in forward-looking statements. A number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions we express in these forward-looking statements, including those we identify in "Risk Factors” in our Annual Report on Form 20-F for the fiscal year ended December 31, 2015 and in “Cautionary statement regarding forward-looking information" in our fourth quarter earnings release 2016 filed with the US Securities and Exchange Commission, and in other public filings and press releases. We do not intend to update these forward-looking statements except as may be required by applicable law. In particular, the terms “Illustrative”, “Ambition”, “Outlook” and “Goal” are not intended to be viewed as targets or projections, nor are they considered to be Key Performance Indicators. All such illustrations, ambitions and goals are subject to a large number of inherent risks, assumptions and uncertainties, many of which are completely outside of our control. Accordingly, this information should not be relied on for any purpose. We do not intend to update these illustrations, ambitions or goals.We may not achieve the benefits of our strategic initiativesWe may not achieve all of the expected benefits of our strategic initiatives. Factors beyond our control, including but not limited to the market and economic conditions, changes in laws, rules or regulations and other challenges discussed in our public filings, could limit our ability to achieve some or all of the expected benefits of these initiatives.Estimates and assumptionsIn preparing this presentation, management has made estimates and assumptions that affect the numbers presented. Actual results may differ. Figures throughout presentation may also be subject to rounding adjustments. In particular, pro forma figures from Wealth Management and connected activities within APAC are based on preliminary estimates.Cautionary Statements Relating to Interim Financial InformationThis presentation contains certain unaudited interim financial information for the year-to-date 2017, the date of our last published quarterly financial statements. This information has been derived from management accounts, is preliminary in nature, does not reflect the complete results of the first quarter of 2017 and is subject to change, including as a result of any normal quarterly adjustments in relation to the financial statements for the first quarter of 2017. This information has not been subject to any review by our independent registered public accounting firm. There can be no assurance that the final results for these periods will not differ from these preliminary results, and any such differences could be material. Quarterly financial results for the first quarter of 2017 will be included in our 1Q17 Financial Report. These interim results of operations are not necessarily indicative of the results to be achieved for the remainder of 1Q17 or the full first quarter of 2017.

Disclaimer (2/2) Statement regarding non-GAAP financial measuresThis presentation also contains non-GAAP financial measures, including adjusted results. Information needed to reconcile such non-GAAP financial measures to the most directly comparable measures under US GAAP can be found in this presentation in the Appendix, which is available on our website at credit-suisse.com.Statement regarding capital, liquidity and leverageAs of January 1, 2013, Basel III was implemented in Switzerland along with the Swiss “Too Big to Fail” legislation and regulations thereunder (in each case, subject to certain phase-in periods). As of January 1, 2015, the Bank for International Settlements (BIS) leverage ratio framework, as issued by the Basel Committee on Banking Supervision (BCBS), was implemented in Switzerland by FINMA. Our related disclosures are in accordance with our interpretation of such requirements, including relevant assumptions. Changes in the interpretation of these requirements in Switzerland or in any of our assumptions or estimates could result in different numbers from those shown in this presentation. Capital and ratio numbers for periods prior to 2013 are based on estimates, which are calculated as if the Basel III framework had been in place in Switzerland during such periods. Unless otherwise noted, leverage exposure is based on the BIS leverage ratio framework and consists of period-end balance sheet assets and prescribed regulatory adjustments. Beginning in 2015, the Swiss leverage ratio is calculated as Swiss total capital, divided by period-end leverage exposure. The look-through BIS tier 1 leverage ratio and CET1 leverage ratio are calculated as look-through BIS tier 1 capital and CET1 capital, respectively, divided by end-period leverage exposure.Selling restrictionsThis document, and the information contained herein, is not an offer to sell or a solicitation of offers to purchase or subscribe for securities of Credit Suisse Group AG or Credit Suisse (Schweiz) AG in Switzerland, the United States or any other jurisdiction. This document is not a prospectus within the meaning of article 652a of the Swiss Code of Obligations, nor is it a listing prospectus as defined in the listing rules of the SIX Swiss Exchange AG or any other exchange or regulated trading facility in Switzerland or a prospectus or offering document under any other applicable laws. Copies of this document may not be sent to jurisdictions, or distributed in or sent from jurisdictions, in which such documents are barred or prohibited by law. A decision to invest in securities of Credit Suisse Group AG or Credit Suisse (Schweiz) AG should be based exclusively on a written agreement with Credit Suisse Group AG or an offering and listing prospectus to be published by Credit Suisse Group AG or Credit Suisse (Schweiz) AG for such purpose. Any offer and sale of securities of Credit Suisse (Schweiz) AG will not be registered under the U.S. Securities Act of 1933, as amended, and may not be offered in the United States of America absent such registration or an exemption from registration. There will be no public offering of such securities in the United States of America.

4Q16 and Full Year 2016Earnings ReviewTidjane Thiam, Chief Executive OfficerDavid Mathers, Chief Financial Officer

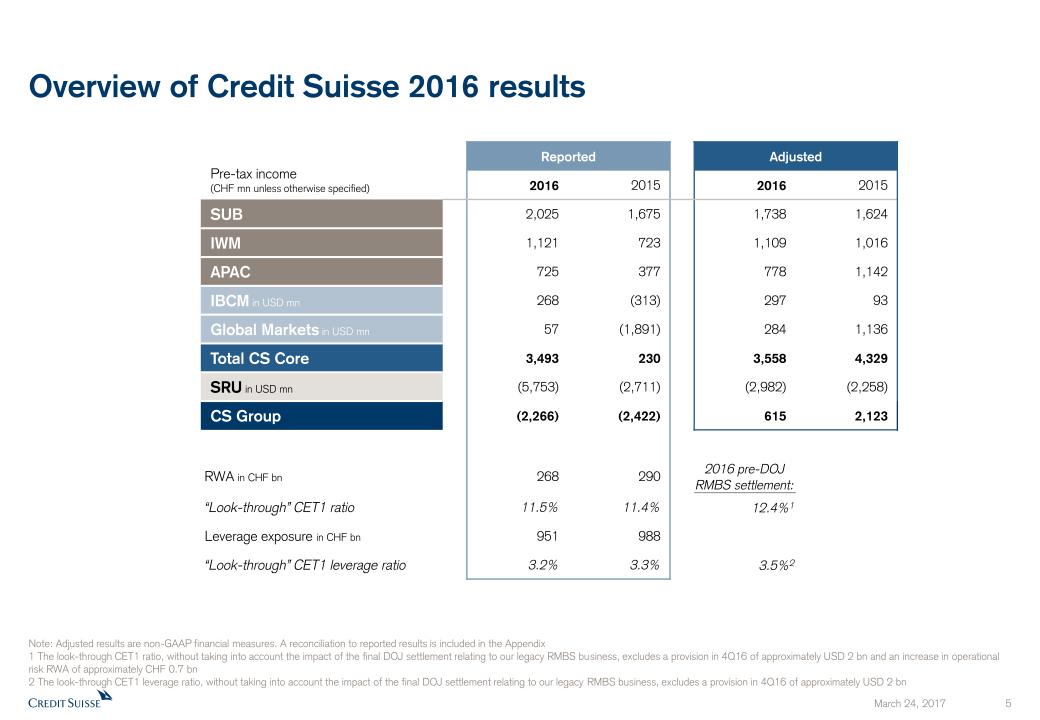

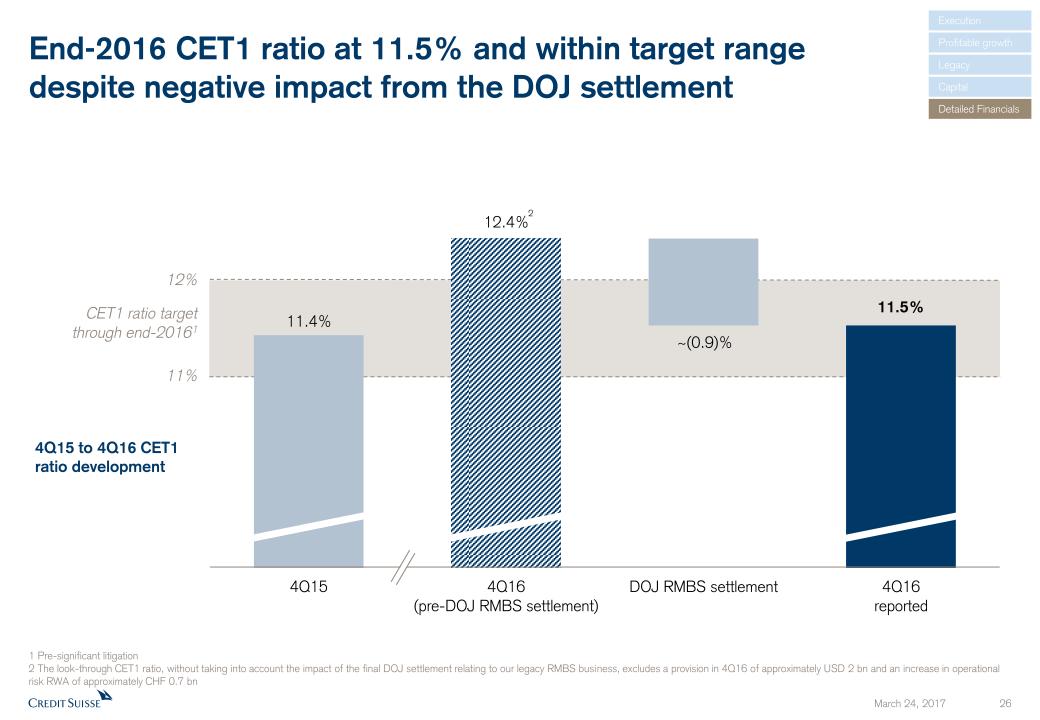

Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix 1 The look-through CET1 ratio, without taking into account the impact of the final DOJ settlement relating to our legacy RMBS business, excludes a provision in 4Q16 of approximately USD 2 bn and an increase in operational risk RWA of approximately CHF 0.7 bn2 The look-through CET1 leverage ratio, without taking into account the impact of the final DOJ settlement relating to our legacy RMBS business, excludes a provision in 4Q16 of approximately USD 2 bn Overview of Credit Suisse 2016 results Pre-tax income(CHF mn unless otherwise specified) Reported Adjusted 2016 2015 2016 2015 SUB 2,025 1,675 1,738 1,624 IWM 1,121 723 1,109 1,016 APAC 725 377 778 1,142 IBCM in USD mn 268 (313) 297 93 Global Markets in USD mn 57 (1,891) 284 1,136 Total CS Core 3,493 230 3,558 4,329 SRU in USD mn (5,753) (2,711) (2,982) (2,258) CS Group (2,266) (2,422) 615 2,123 RWA in CHF bn 268 290 2016 pre-DOJ RMBS settlement: “Look-through” CET1 ratio 11.5% 11.4% 12.4%1 Leverage exposure in CHF bn 951 988 “Look-through” CET1 leverage ratio 3.2% 3.3% 3.5%2

We are well positioned to capture growth and benefit from improved market conditions Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix1 Measured at constant FX rates (see Appendix) 2 Relating to Wealth Management in SUB, IWM and APAC 3 Gross global revenues from advisory, debt and equity underwriting generated across all divisions before cross-divisional revenue sharing agreements 4 Dealogic as of December 31, 2016 5 Annualized numbers do not take account of variations in operating results, seasonality and other factors and may not be indicative of actual, full-year results 6 Estimated 4Q16 annualized exit rate shown at Investor Day 2016 7 The look-through CET1 ratio, without taking into account the impact of the final DOJ settlement relating to our legacy RMBS business, excludes a provision in 4Q16 of approximately USD 2 bn and an increase in operational risk RWA of approximately CHF 0.7 bn Growing profitablyWealth Management achieved CHF 27.5 bn of NNA in 2016, a 53%2 increase year-on-year; Assets under Management increased by 8% to CHF 733 bn2 in 2016 at higher gross and net marginsGlobal advisory and underwriting3 delivered increased revenues and outperformance against the market4Benefits from Global Markets restructuring starting to emerge: 4Q16 annualized5 adjusted cost base below USD 5.2 bn6 and increasing momentum across Credit and Equities 2 Strengthening our capital position“Look-through” CET1 ratio at 11.5% (12.4%7 pre-DOJ RMBS settlement) 4 Executing with disciplineSignificant increase in operating leverage: adjusted net cost savings of CHF 1.9 bn1 achieved in 2016, exceeding our target of > CHF 1.4 bn1 1 Resolving key legacy issuesSettlement with DOJ related to RMBS matterContinued progress in reducing legacy portfolio in the SRU 3

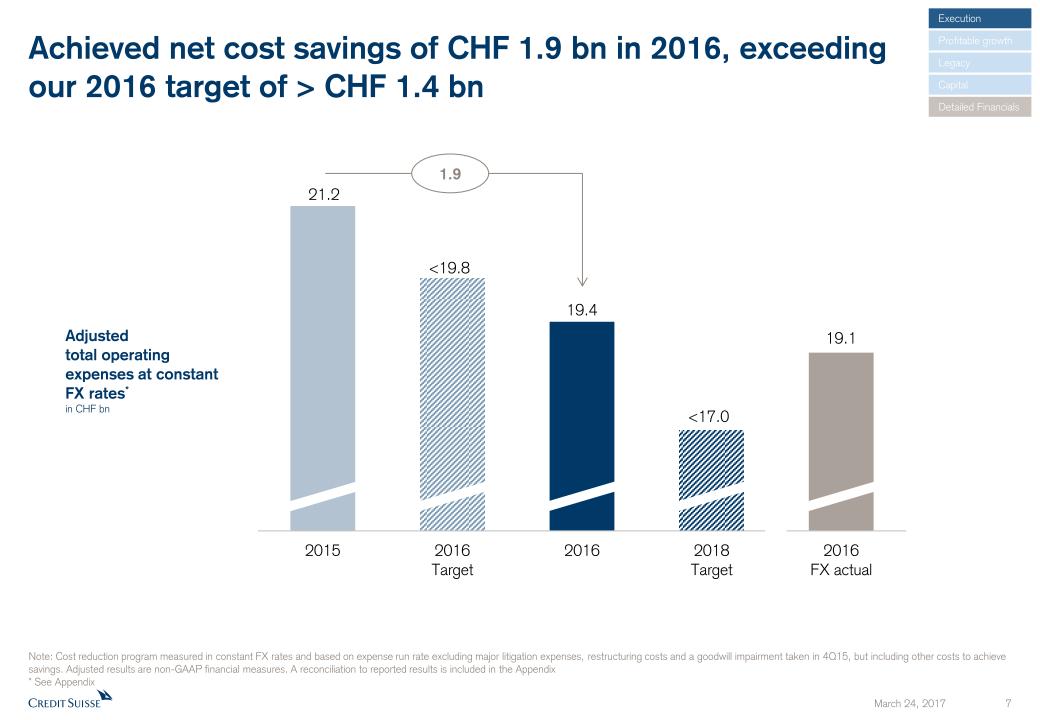

Adjustedtotal operating expenses at constant FX rates*in CHF bn Achieved net cost savings of CHF 1.9 bn in 2016, exceedingour 2016 target of > CHF 1.4 bn Note: Cost reduction program measured in constant FX rates and based on expense run rate excluding major litigation expenses, restructuring costs and a goodwill impairment taken in 4Q15, but including other costs to achieve savings. Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix * See Appendix 1.9 Execution Profitable growth Legacy Detailed Financials Capital

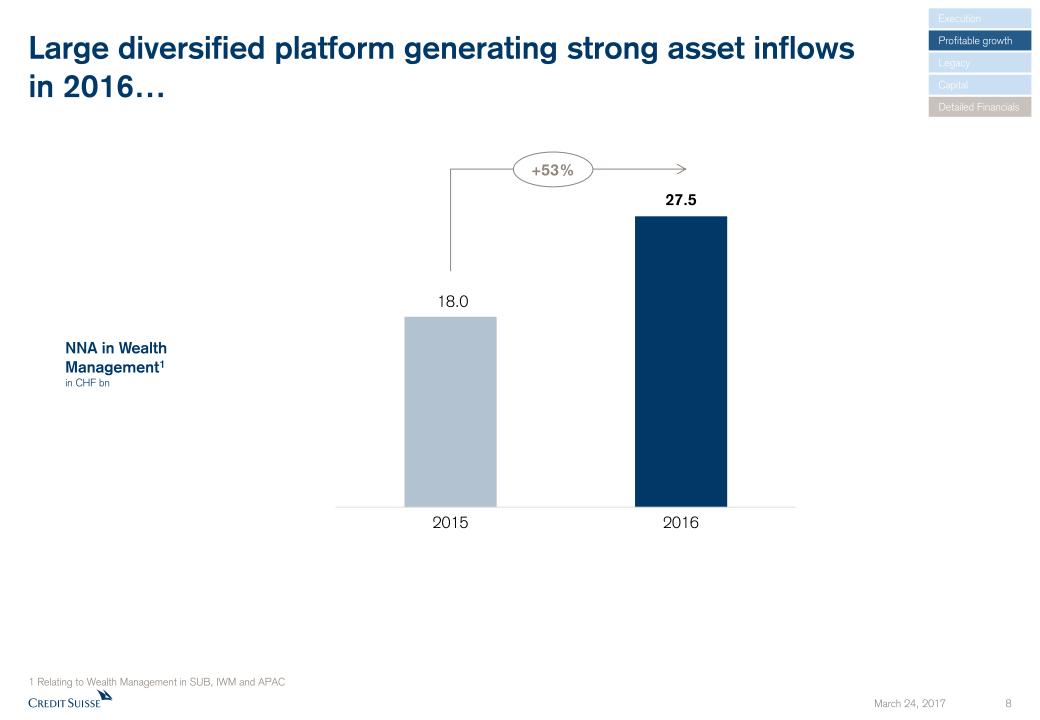

Large diversified platform generating strong asset inflowsin 2016… NNA in Wealth Management1in CHF bn 2015 2016 +53% 1 Relating to Wealth Management in SUB, IWM and APAC Execution Profitable growth Legacy Detailed Financials Capital

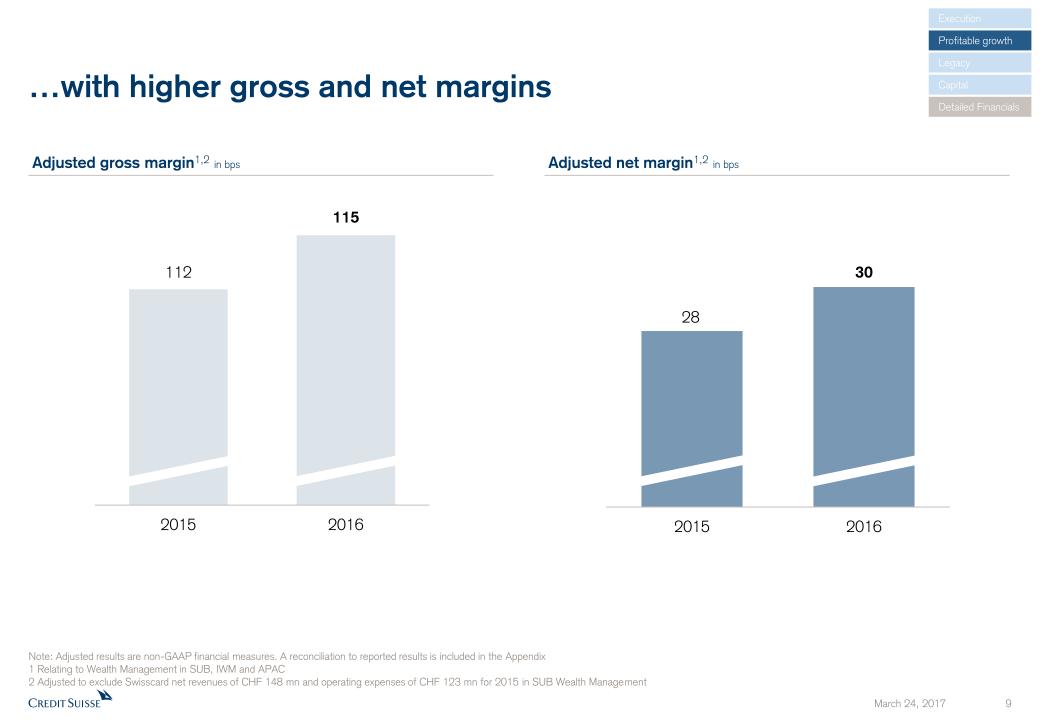

…with higher gross and net margins Adjusted gross margin1,2 in bps Adjusted net margin1,2 in bps Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix1 Relating to Wealth Management in SUB, IWM and APAC2 Adjusted to exclude Swisscard net revenues of CHF 148 mn and operating expenses of CHF 123 mn for 2015 in SUB Wealth Management Execution Profitable growth Legacy Detailed Financials Capital

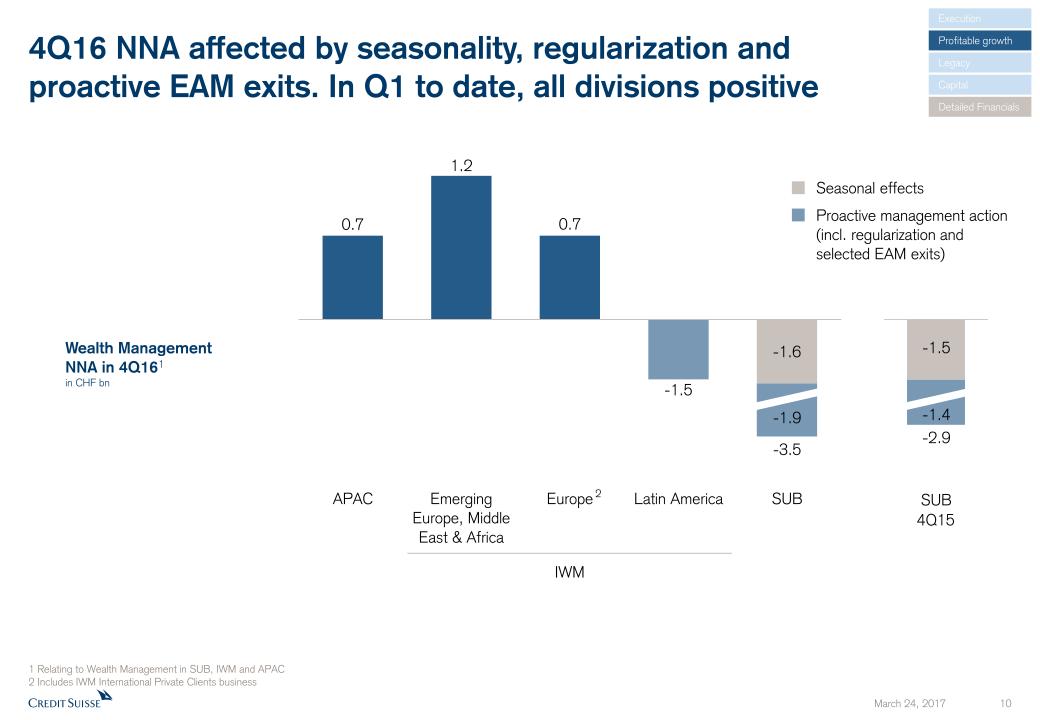

4Q16 NNA affected by seasonality, regularization andproactive EAM exits. In Q1 to date, all divisions positive 1 Relating to Wealth Management in SUB, IWM and APAC2 Includes IWM International Private Clients business Wealth Management NNA in 4Q161in CHF bn -3.5 2 4Q15 -2.9 -1.9 Seasonal effects Proactive management action (incl. regularization and selected EAM exits) -1.5 -1.4 Execution Profitable growth Legacy Detailed Financials Capital IWM

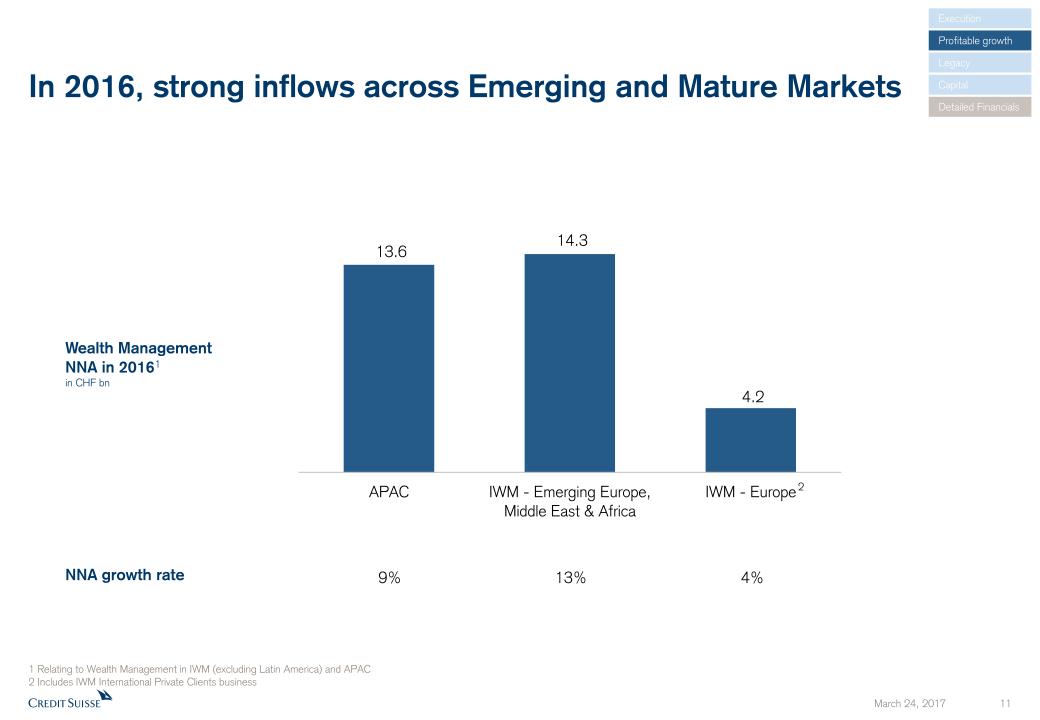

In 2016, strong inflows across Emerging and Mature Markets 1 Relating to Wealth Management in IWM (excluding Latin America) and APAC2 Includes IWM International Private Clients business Wealth Management NNA in 20161in CHF bn 2 NNA growth rate 9% 13% 4% Execution Profitable growth Legacy Detailed Financials Capital

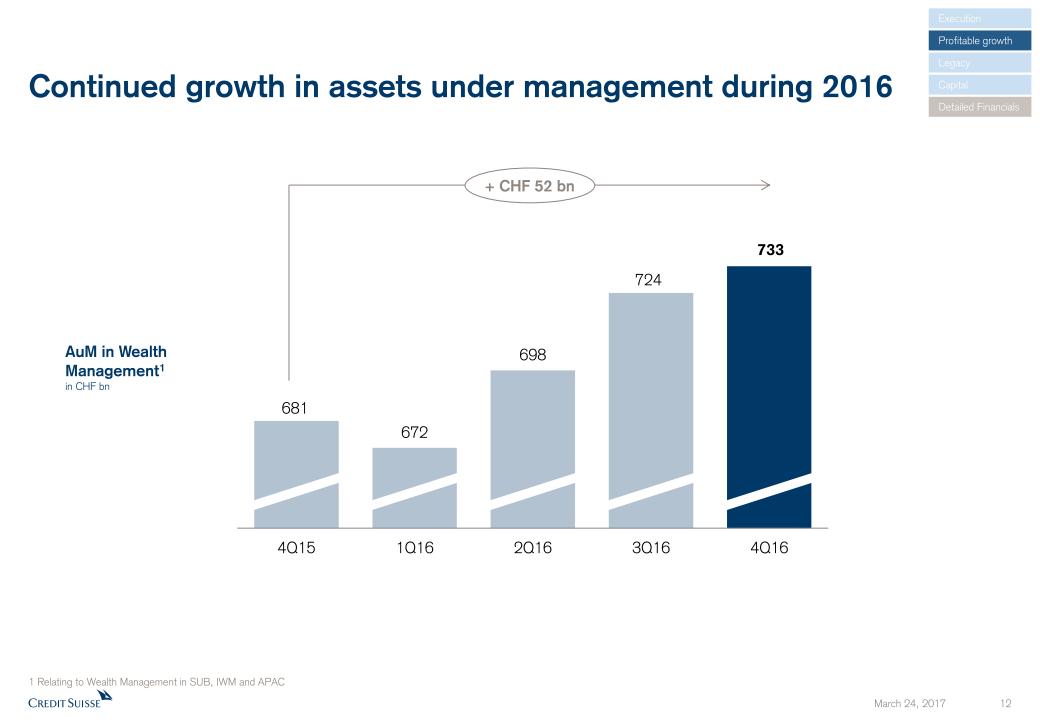

Continued growth in assets under management during 2016 AuM in Wealth Management1in CHF bn 1 Relating to Wealth Management in SUB, IWM and APAC + CHF 52 bn Execution Profitable growth Legacy Detailed Financials Capital

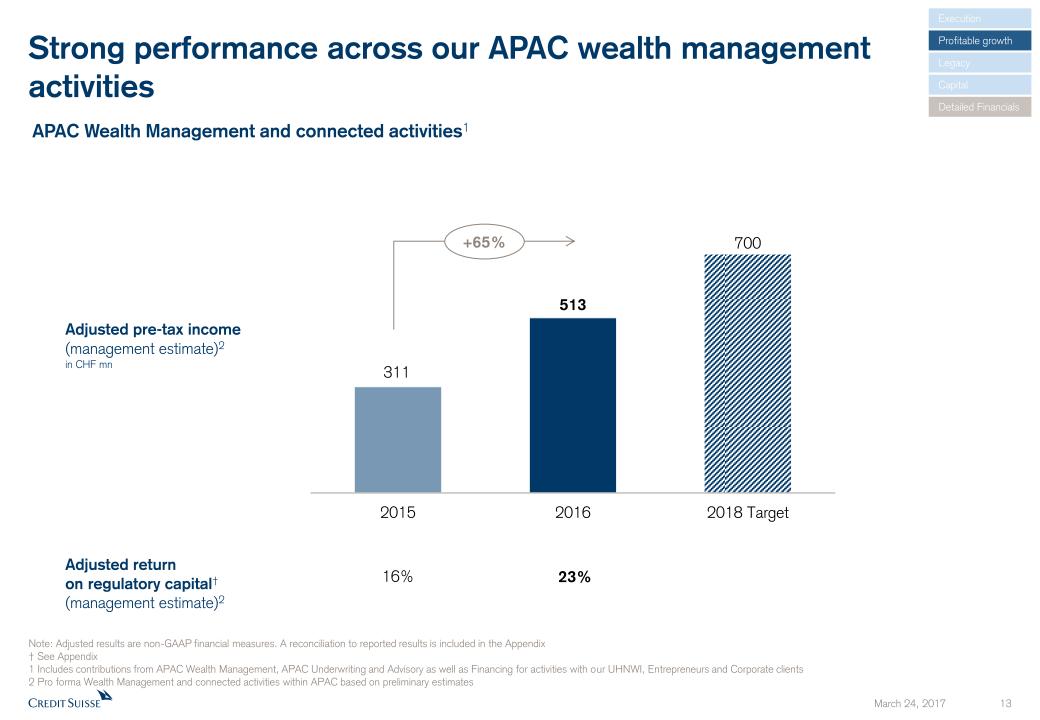

Strong performance across our APAC wealth managementactivities Adjusted pre-tax income(management estimate)2in CHF mn Adjusted return on regulatory capital† (management estimate)2 16% 23% APAC Wealth Management and connected activities1 Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix† See Appendix1 Includes contributions from APAC Wealth Management, APAC Underwriting and Advisory as well as Financing for activities with our UHNWI, Entrepreneurs and Corporate clients2 Pro forma Wealth Management and connected activities within APAC based on preliminary estimates +65% Execution Profitable growth Legacy Detailed Financials Capital

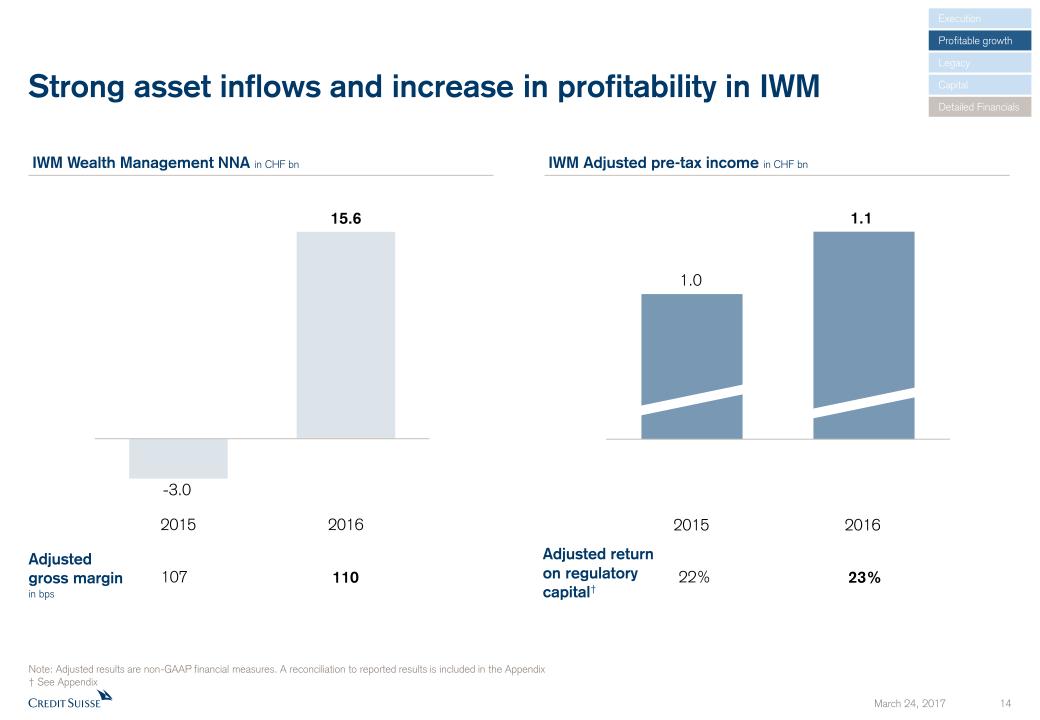

Strong asset inflows and increase in profitability in IWM Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix† See Appendix Adjusted return on regulatorycapital† 23% IWM Wealth Management NNA in CHF bn IWM Adjusted pre-tax income in CHF bn Adjusted gross marginin bps 107 110 22% 2015 2016 Execution Profitable growth Legacy Detailed Financials Capital

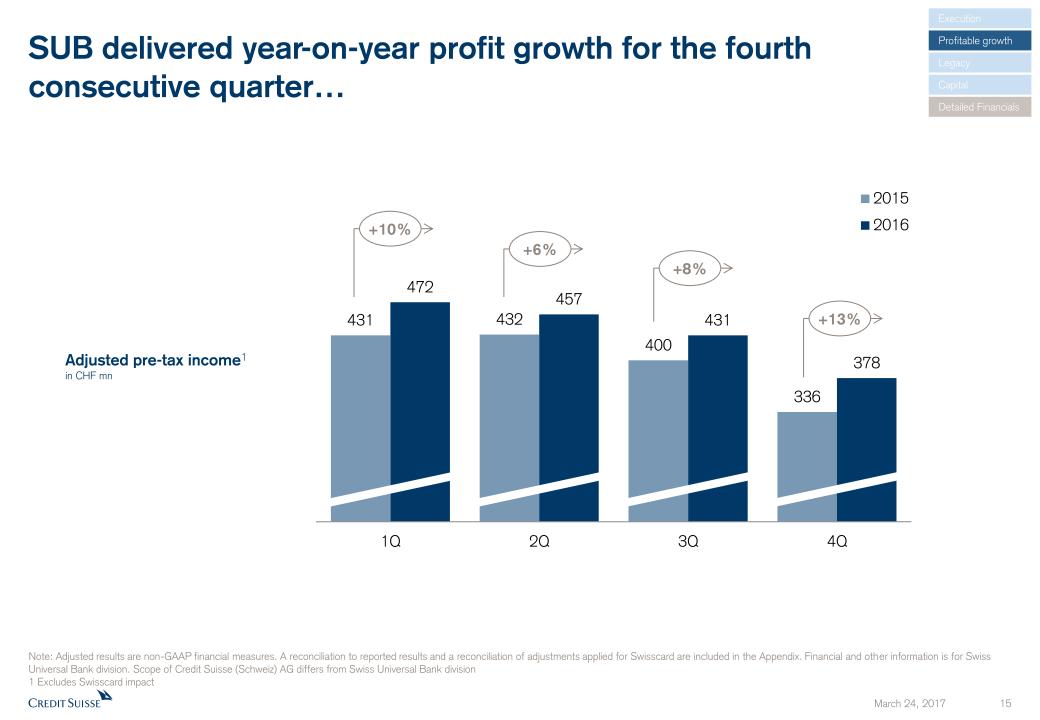

SUB delivered year-on-year profit growth for the fourthconsecutive quarter… Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results and a reconciliation of adjustments applied for Swisscard are included in the Appendix. Financial and other information is for Swiss Universal Bank division. Scope of Credit Suisse (Schweiz) AG differs from Swiss Universal Bank division1 Excludes Swisscard impact Adjusted pre-tax income1in CHF mn +10% +6% +8% +13% Execution Profitable growth Legacy Detailed Financials Capital

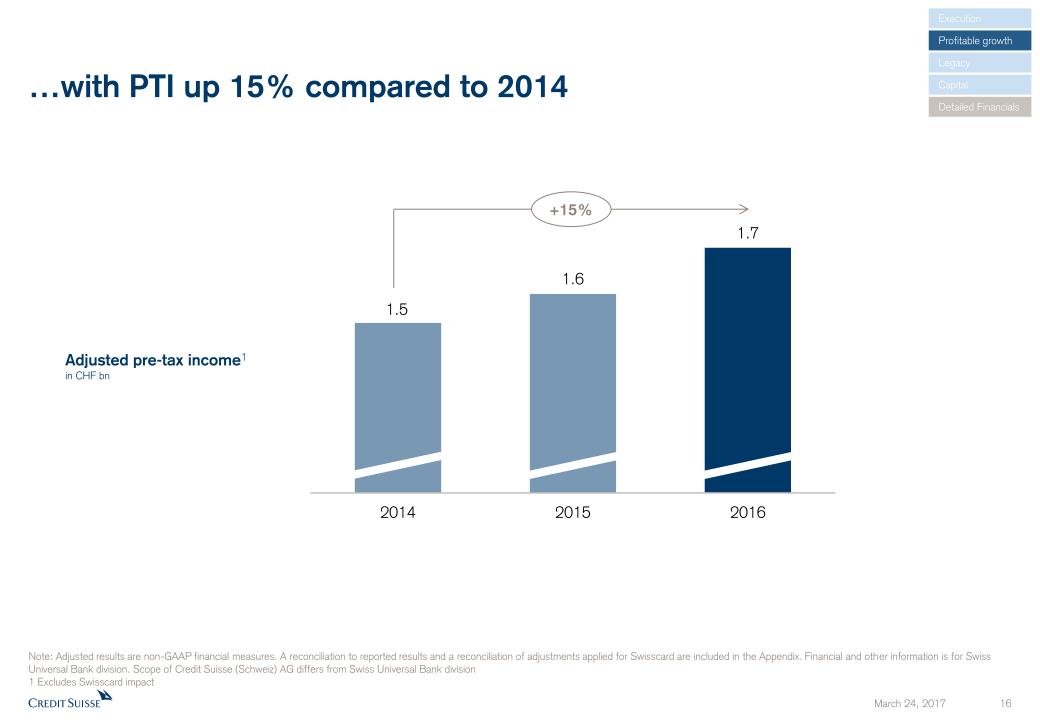

…with PTI up 15% compared to 2014 Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results and a reconciliation of adjustments applied for Swisscard are included in the Appendix. Financial and other information is for Swiss Universal Bank division. Scope of Credit Suisse (Schweiz) AG differs from Swiss Universal Bank division1 Excludes Swisscard impact Adjusted pre-tax income1in CHF bn Execution Profitable growth Legacy Detailed Financials Capital +15%

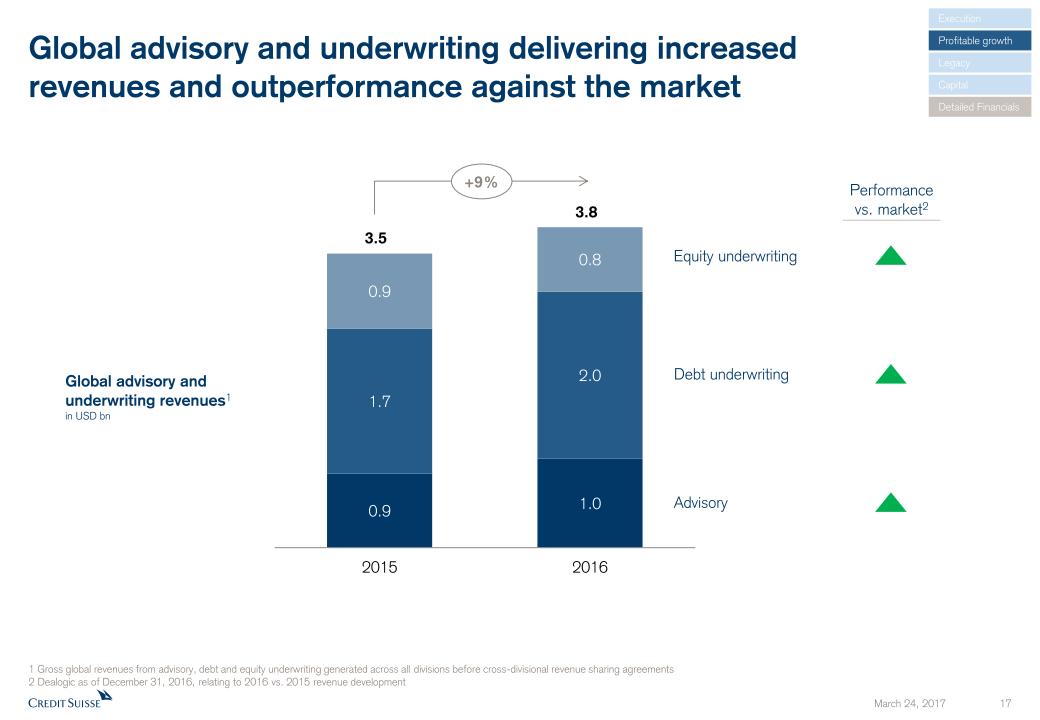

Global advisory and underwriting delivering increased revenues and outperformance against the market Global advisory and underwriting revenues1in USD bn Advisory Equity underwriting Debt underwriting 1 Gross global revenues from advisory, debt and equity underwriting generated across all divisions before cross-divisional revenue sharing agreements2 Dealogic as of December 31, 2016, relating to 2016 vs. 2015 revenue development +9% Performance vs. market2 Execution Profitable growth Legacy Detailed Financials Capital

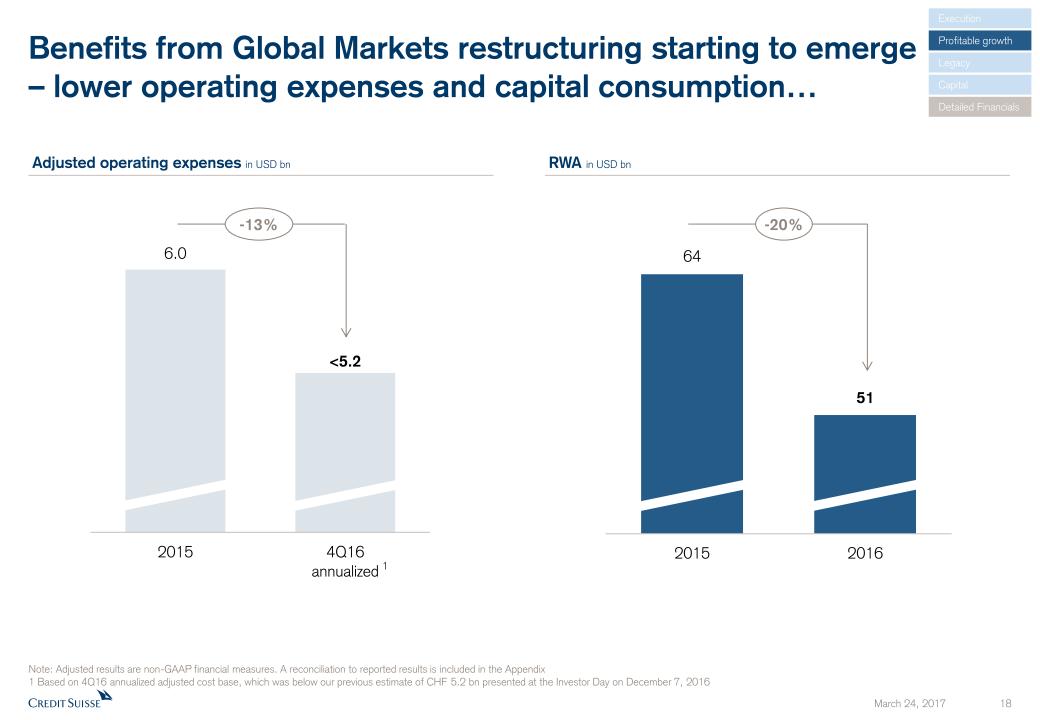

Benefits from Global Markets restructuring starting to emerge– lower operating expenses and capital consumption… -13% Adjusted operating expenses in USD bn Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix1 Based on 4Q16 annualized adjusted cost base, which was below our previous estimate of CHF 5.2 bn presented at the Investor Day on December 7, 2016 1 RWA in USD bn -20% Execution Profitable growth Legacy Detailed Financials Capital

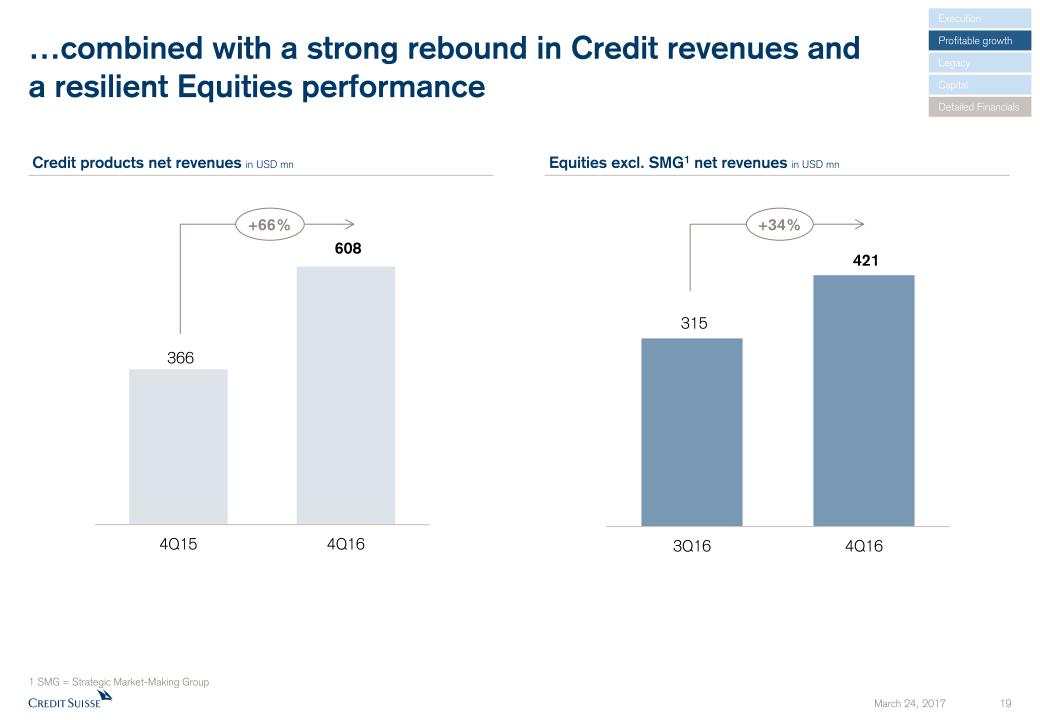

…combined with a strong rebound in Credit revenues anda resilient Equities performance Credit products net revenues in USD mn Equities excl. SMG1 net revenues in USD mn +34% +66% 1 SMG = Strategic Market-Making Group Execution Profitable growth Legacy Detailed Financials Capital

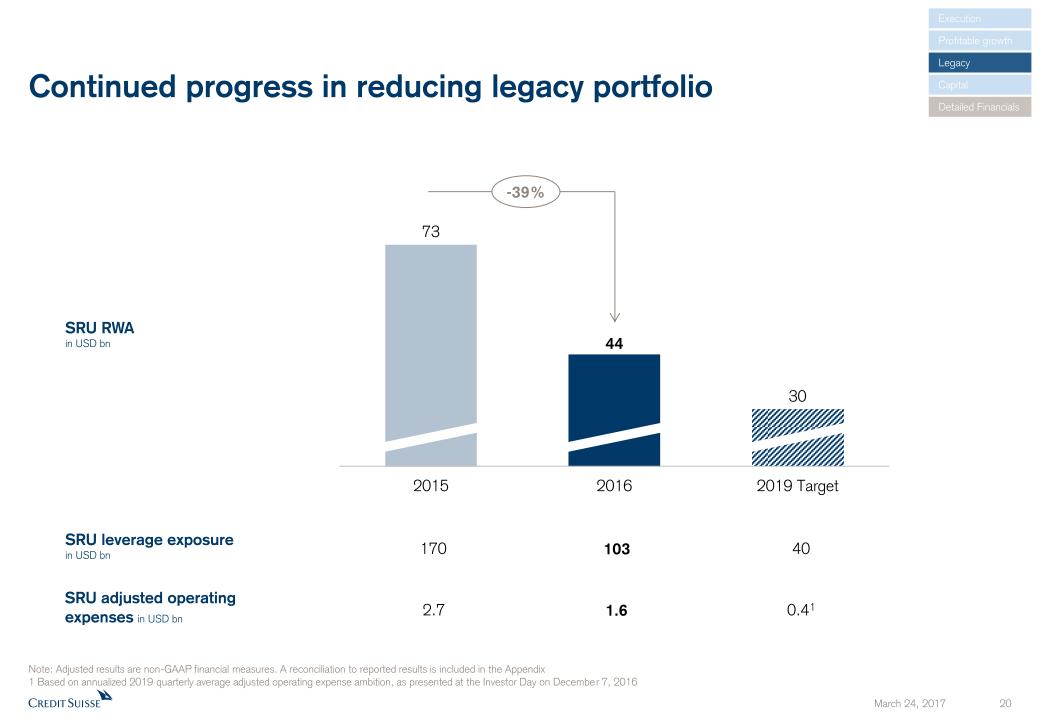

SRU RWAin USD bn Continued progress in reducing legacy portfolio -39% SRU leverage exposurein USD bn 170 103 SRU adjusted operating expenses in USD bn 2.7 1.6 Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix1 Based on annualized 2019 quarterly average adjusted operating expense ambition, as presented at the Investor Day on December 7, 2016 40 0.41 Execution Profitable growth Legacy Detailed Financials Capital

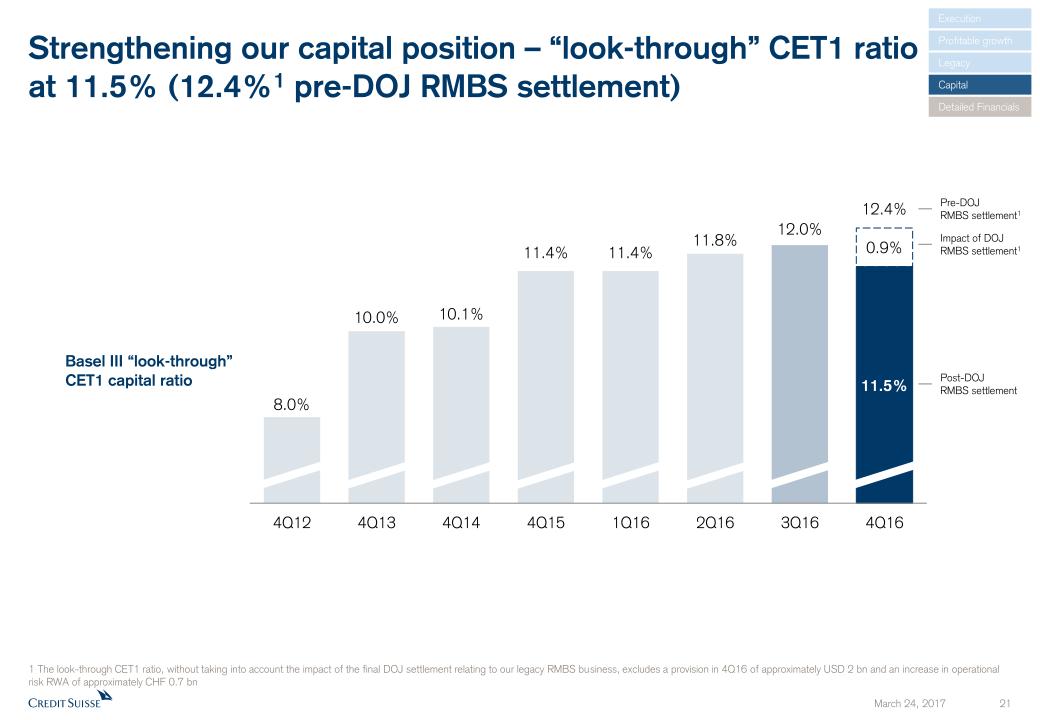

Strengthening our capital position – “look-through” CET1 ratioat 11.5% (12.4%1 pre-DOJ RMBS settlement) Basel III “look-through” CET1 capital ratio Impact of DOJ RMBS settlement1 Post-DOJRMBS settlement 12.4% Pre-DOJRMBS settlement1 1 The look-through CET1 ratio, without taking into account the impact of the final DOJ settlement relating to our legacy RMBS business, excludes a provision in 4Q16 of approximately USD 2 bn and an increase in operational risk RWA of approximately CHF 0.7 bn Execution Profitable growth Legacy Detailed Financials Capital

Current trading and outlook Continued momentum in January across Wealth Management and Investment Banking We have seen positive inflows across each of our Wealth Management1 businesses in JanuarySignificant rebound in client activity levels across capital markets and trading, with Credit and Securitized Productsrevenues up over 100% year-on-year2, somewhat offset by lower trading volumes and volatility levels in EquitiesIBCM revenues up 90% year-on-year2 with broad based strength in Advisory, ECM and DCMWell positioned to capture profitable growth opportunities and benefit from improved market conditions 1 Relating to Wealth Management in SUB, IWM and APAC2 Month of January 2017 vs. 2016 Execution Profitable growth Legacy Detailed Financials Capital

Detailed Financials

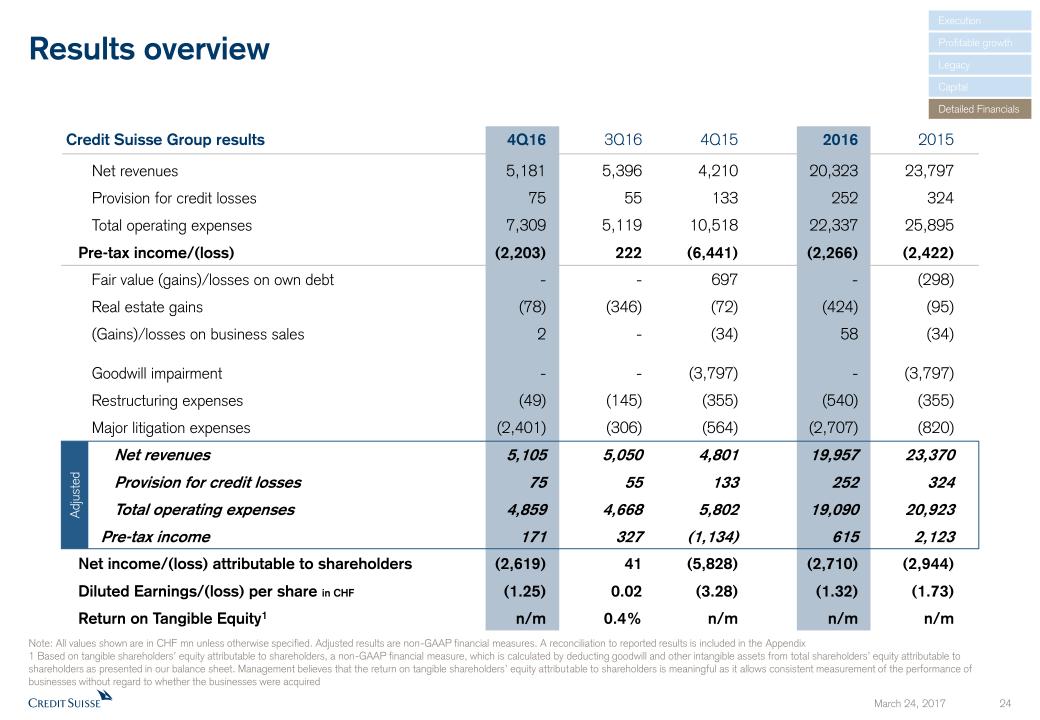

Adjusted Results overview Credit Suisse Group results 4Q16 3Q16 4Q15 2016 2015 Net revenues 5,181 5,396 4,210 20,323 23,797 Provision for credit losses 75 55 133 252 324 Total operating expenses 7,309 5,119 10,518 22,337 25,895Pre-tax income/(loss) (2,203) 222 (6,441) (2,266) (2,422) Fair value (gains)/losses on own debt - - 697 - (298) Real estate gains (78) (346) (72) (424) (95) (Gains)/losses on business sales 2 - (34) 58 (34) Goodwill impairment - - (3,797) - (3,797) Restructuring expenses (49) (145) (355) (540) (355) Major litigation expenses (2,401) (306) (564) (2,707) (820) Net revenues 5,105 5,050 4,801 19,957 23,370 Provision for credit losses 75 55 133 252 324 Total operating expenses 4,859 4,668 5,802 19,090 20,923 Pre-tax income 171 327 (1,134) 615 2,123Net income/(loss) attributable to shareholders (2,619) 41 (5,828) (2,710) (2,944)Diluted Earnings/(loss) per share in CHF (1.25) 0.02 (3.28) (1.32) (1.73)Return on Tangible Equity1 n/m 0.4% n/m n/m n/m Note: All values shown are in CHF mn unless otherwise specified. Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix1 Based on tangible shareholders’ equity attributable to shareholders, a non-GAAP financial measure, which is calculated by deducting goodwill and other intangible assets from total shareholders’ equity attributable to shareholders as presented in our balance sheet. Management believes that the return on tangible shareholders’ equity attributable to shareholders is meaningful as it allows consistent measurement of the performance of businesses without regard to whether the businesses were acquired Execution Profitable growth Legacy Detailed Financials Capital

1 Business impact includes business moves and internally driven methodology and policy impact; methodology & policy reflects external methodology changes only2 Net of FX and major external methodology changes 3 Includes FX impact of CHF 8 bn and the impact of CHF (13) bn from the change in accounting treatment of collateralized loan obligations (CLOs) in 1Q164 IWM excludes the impact of CHF (13) bn from the change in accounting treatment of collateralized loan obligations (CLOs) in 1Q16 Basel III RWA in CHF bn 290 268 4Q16 vs. 4Q15 Basel III RWA business impact2 in CHF bn (33) 7 (28) +9 Leverage exposure in CHF bn 4Q15 4Q16 FX impact& Other3 Business impact (32) (5) 4Q16 capital ratios impacted by DOJ settlement;continued reallocation of resources to growth areas APAC +5 IWM +2 SUB +1 4Q16 vs. 4Q15 Leverage exposure business impact2 in CHF bn SUB +12 APAC +9 IBCM +5 (63) (5) +6 +30 11.5% 11.4% CET1 ratio 3.2% 3.3% CET1 leverage ratio 4.4% 4.5% Tier1 leverage ratio 4 Business impact1 FX impact Methodology & policy1 (12) (2) IWM4 +4 4 IBCM +1 Execution Profitable growth Legacy Detailed Financials Capital

End-2016 CET1 ratio at 11.5% and within target rangedespite negative impact from the DOJ settlement 4Q15 to 4Q16 CET1 ratio development 12% 11% CET1 ratio targetthrough end-20161 2 1 Pre-significant litigation2 The look-through CET1 ratio, without taking into account the impact of the final DOJ settlement relating to our legacy RMBS business, excludes a provision in 4Q16 of approximately USD 2 bn and an increase in operational risk RWA of approximately CHF 0.7 bn Execution Profitable growth Legacy Detailed Financials Capital

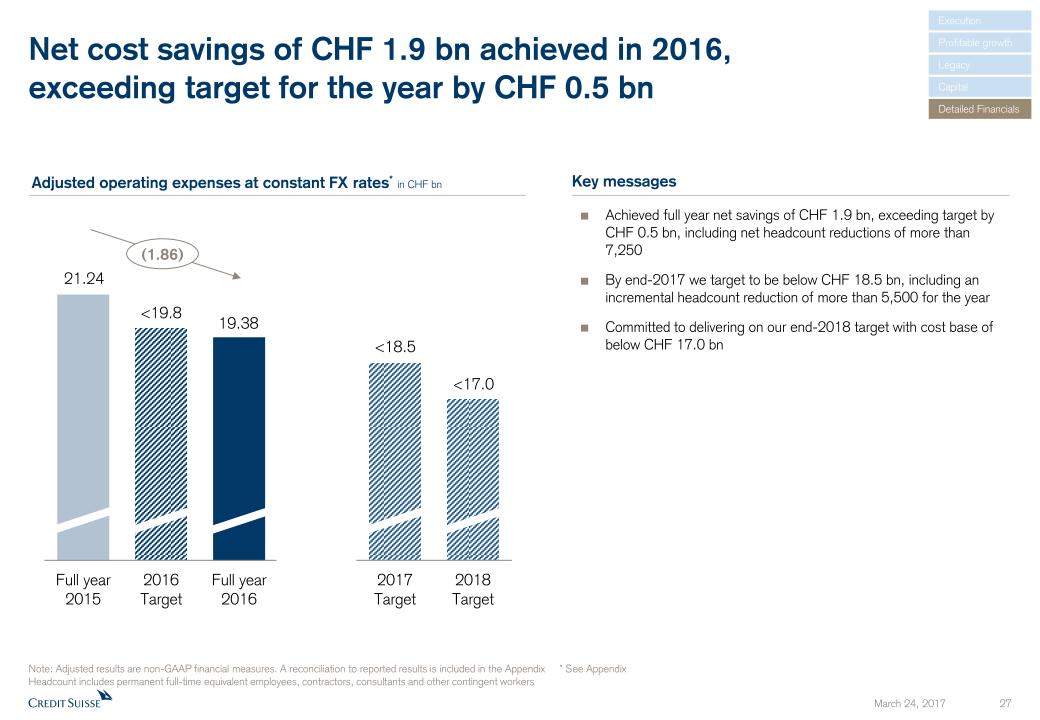

Net cost savings of CHF 1.9 bn achieved in 2016,exceeding target for the year by CHF 0.5 bn Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix * See AppendixHeadcount includes permanent full-time equivalent employees, contractors, consultants and other contingent workers Adjusted operating expenses at constant FX rates* in CHF bn Achieved full year net savings of CHF 1.9 bn, exceeding target by CHF 0.5 bn, including net headcount reductions of more than 7,250By end-2017 we target to be below CHF 18.5 bn, including an incremental headcount reduction of more than 5,500 for the yearCommitted to delivering on our end-2018 target with cost base of below CHF 17.0 bn Key messages 21.24 <19.8 19.38 <17.0 (1.86) <18.5 Execution Profitable growth Legacy Detailed Financials Capital

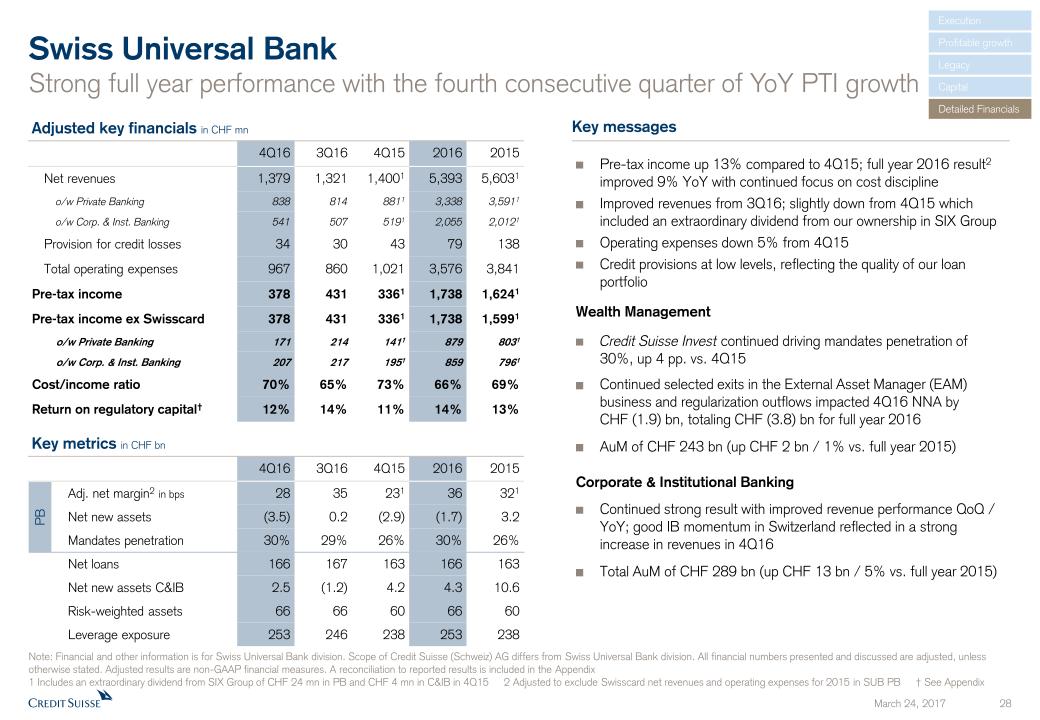

Swiss Universal Bank Strong full year performance with the fourth consecutive quarter of YoY PTI growth Key messages PB Key metrics in CHF bn Adjusted key financials in CHF mn 4Q16 3Q16 4Q15 2016 2015 Adj. net margin2 in bps 28 35 231 36 321 Net new assets (3.5) 0.2 (2.9) (1.7) 3.2 Mandates penetration 30% 29% 26% 30% 26% Net loans 166 167 163 166 163 Net new assets C&IB 2.5 (1.2) 4.2 4.3 10.6 Risk-weighted assets 66 66 60 66 60 Leverage exposure 253 246 238 253 238 4Q16 3Q16 4Q15 2016 2015 Net revenues 1,379 1,321 1,4001 5,393 5,6031 o/w Private Banking 838 814 8811 3,338 3,5911 o/w Corp. & Inst. Banking 541 507 5191 2,055 2,0121 Provision for credit losses 34 30 43 79 138 Total operating expenses 967 860 1,021 3,576 3,841 Pre-tax income 378 431 3361 1,738 1,6241 Pre-tax income ex Swisscard 378 431 3361 1,738 1,5991 o/w Private Banking 171 214 1411 879 8031 o/w Corp. & Inst. Banking 207 217 1951 859 7961 Cost/income ratio 70% 65% 73% 66% 69% Return on regulatory capital† 12% 14% 11% 14% 13% Note: Financial and other information is for Swiss Universal Bank division. Scope of Credit Suisse (Schweiz) AG differs from Swiss Universal Bank division. All financial numbers presented and discussed are adjusted, unless otherwise stated. Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix1 Includes an extraordinary dividend from SIX Group of CHF 24 mn in PB and CHF 4 mn in C&IB in 4Q15 2 Adjusted to exclude Swisscard net revenues and operating expenses for 2015 in SUB PB † See Appendix Pre-tax income up 13% compared to 4Q15; full year 2016 result2 improved 9% YoY with continued focus on cost disciplineImproved revenues from 3Q16; slightly down from 4Q15 which included an extraordinary dividend from our ownership in SIX GroupOperating expenses down 5% from 4Q15Credit provisions at low levels, reflecting the quality of our loan portfolioWealth Management Credit Suisse Invest continued driving mandates penetration of 30%, up 4 pp. vs. 4Q15Continued selected exits in the External Asset Manager (EAM) business and regularization outflows impacted 4Q16 NNA by CHF (1.9) bn, totaling CHF (3.8) bn for full year 2016 AuM of CHF 243 bn (up CHF 2 bn / 1% vs. full year 2015)Corporate & Institutional BankingContinued strong result with improved revenue performance QoQ / YoY; good IB momentum in Switzerland reflected in a strong increase in revenues in 4Q16Total AuM of CHF 289 bn (up CHF 13 bn / 5% vs. full year 2015) Execution Profitable growth Legacy Detailed Financials Capital

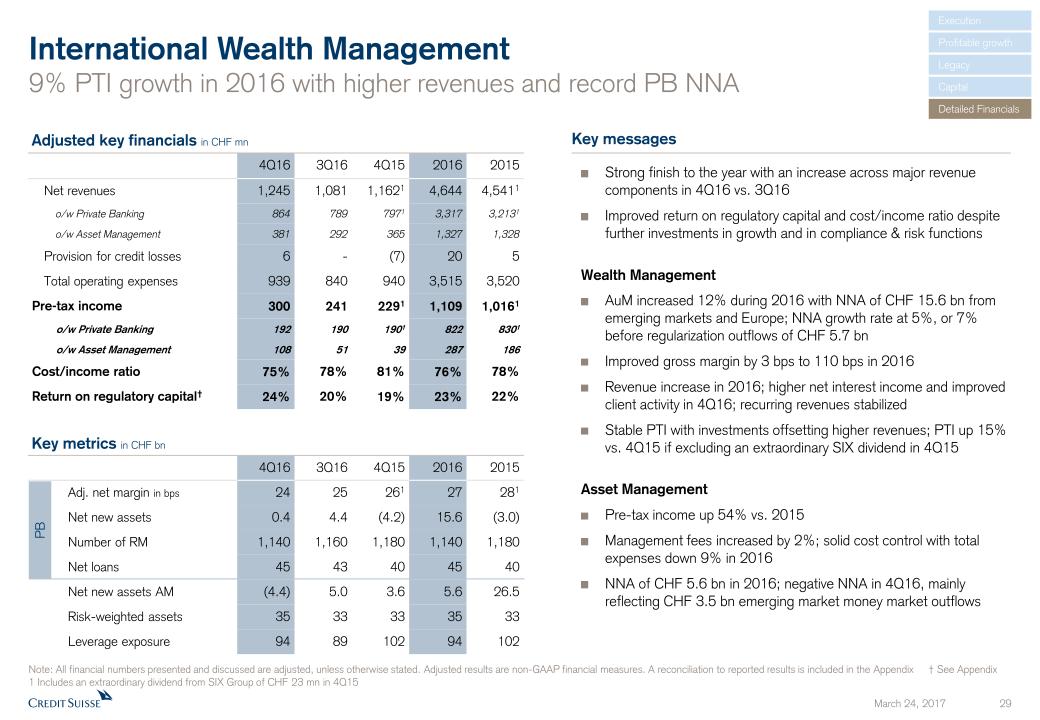

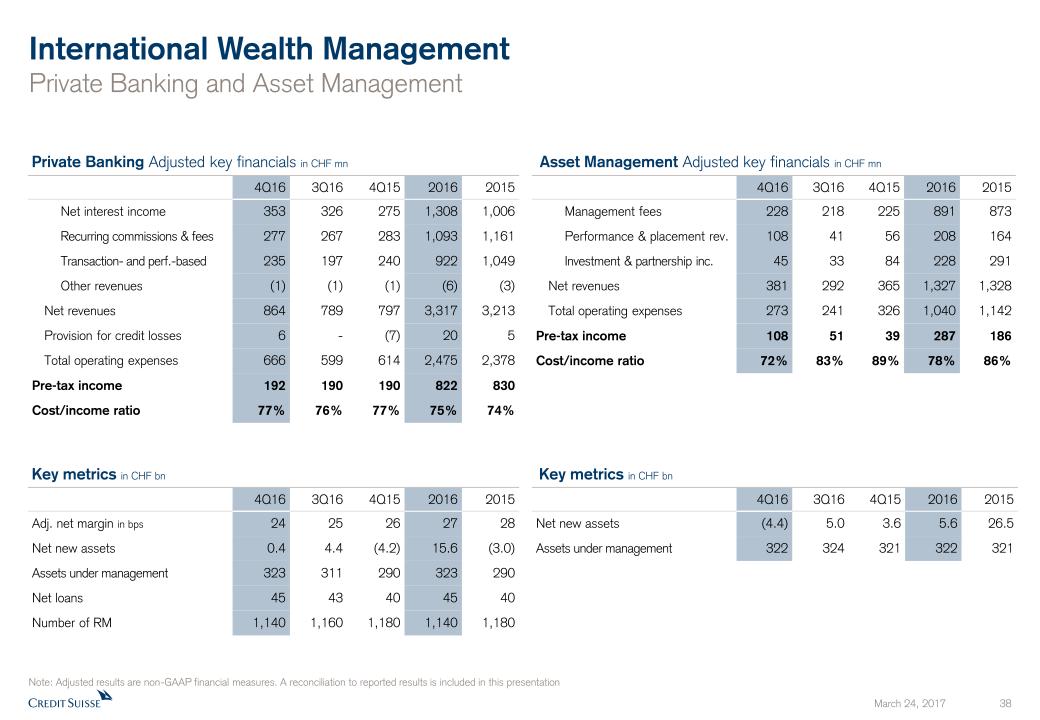

International Wealth Management9% PTI growth in 2016 with higher revenues and record PB NNA Note: All financial numbers presented and discussed are adjusted, unless otherwise stated. Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix † See Appendix 1 Includes an extraordinary dividend from SIX Group of CHF 23 mn in 4Q15 Adjusted key financials in CHF mn 4Q16 3Q16 4Q15 2016 2015 Net revenues 1,245 1,081 1,1621 4,644 4,5411 o/w Private Banking 864 789 7971 3,317 3,2131 o/w Asset Management 381 292 365 1,327 1,328 Provision for credit losses 6 - (7) 20 5 Total operating expenses 939 840 940 3,515 3,520 Pre-tax income 300 241 2291 1,109 1,0161 o/w Private Banking 192 190 1901 822 8301 o/w Asset Management 108 51 39 287 186 Cost/income ratio 75% 78% 81% 76% 78% Return on regulatory capital† 24% 20% 19% 23% 22% PB 4Q16 3Q16 4Q15 2016 2015 Adj. net margin in bps 24 25 261 27 281 Net new assets 0.4 4.4 (4.2) 15.6 (3.0) Number of RM 1,140 1,160 1,180 1,140 1,180 Net loans 45 43 40 45 40 Net new assets AM (4.4) 5.0 3.6 5.6 26.5 Risk-weighted assets 35 33 33 35 33 Leverage exposure 94 89 102 94 102 Key messages Strong finish to the year with an increase across major revenue components in 4Q16 vs. 3Q16Improved return on regulatory capital and cost/income ratio despite further investments in growth and in compliance & risk functionsWealth ManagementAuM increased 12% during 2016 with NNA of CHF 15.6 bn from emerging markets and Europe; NNA growth rate at 5%, or 7% before regularization outflows of CHF 5.7 bnImproved gross margin by 3 bps to 110 bps in 2016Revenue increase in 2016; higher net interest income and improved client activity in 4Q16; recurring revenues stabilizedStable PTI with investments offsetting higher revenues; PTI up 15% vs. 4Q15 if excluding an extraordinary SIX dividend in 4Q15Asset ManagementPre-tax income up 54% vs. 2015Management fees increased by 2%; solid cost control with total expenses down 9% in 2016NNA of CHF 5.6 bn in 2016; negative NNA in 4Q16, mainly reflecting CHF 3.5 bn emerging market money market outflows Key metrics in CHF bn Execution Profitable growth Legacy Detailed Financials Capital

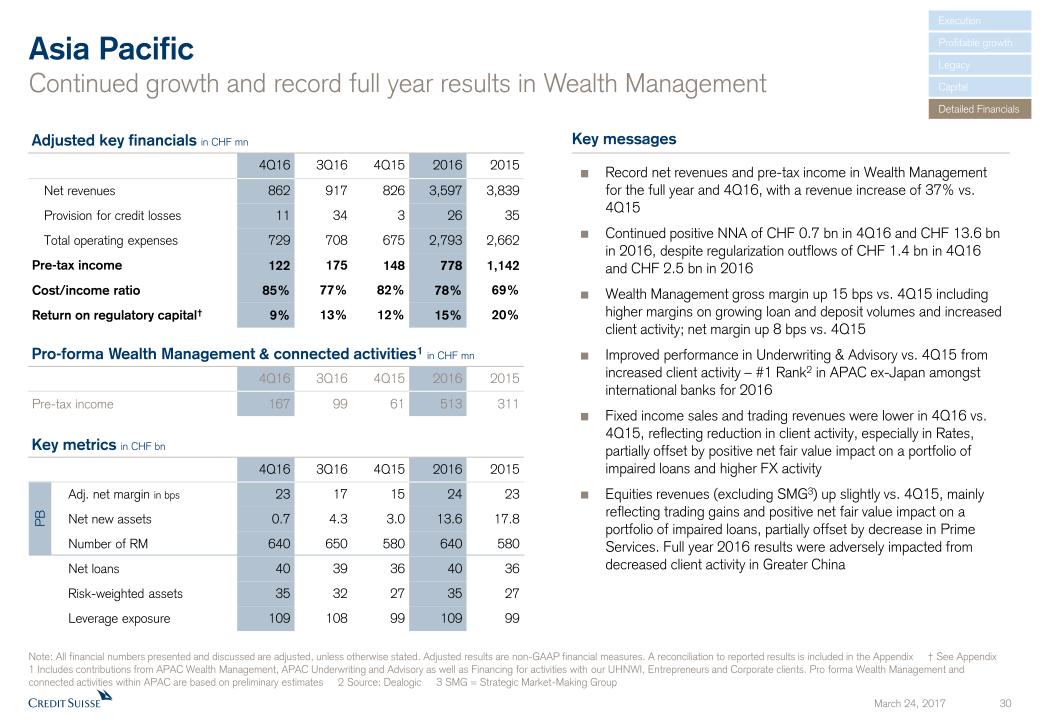

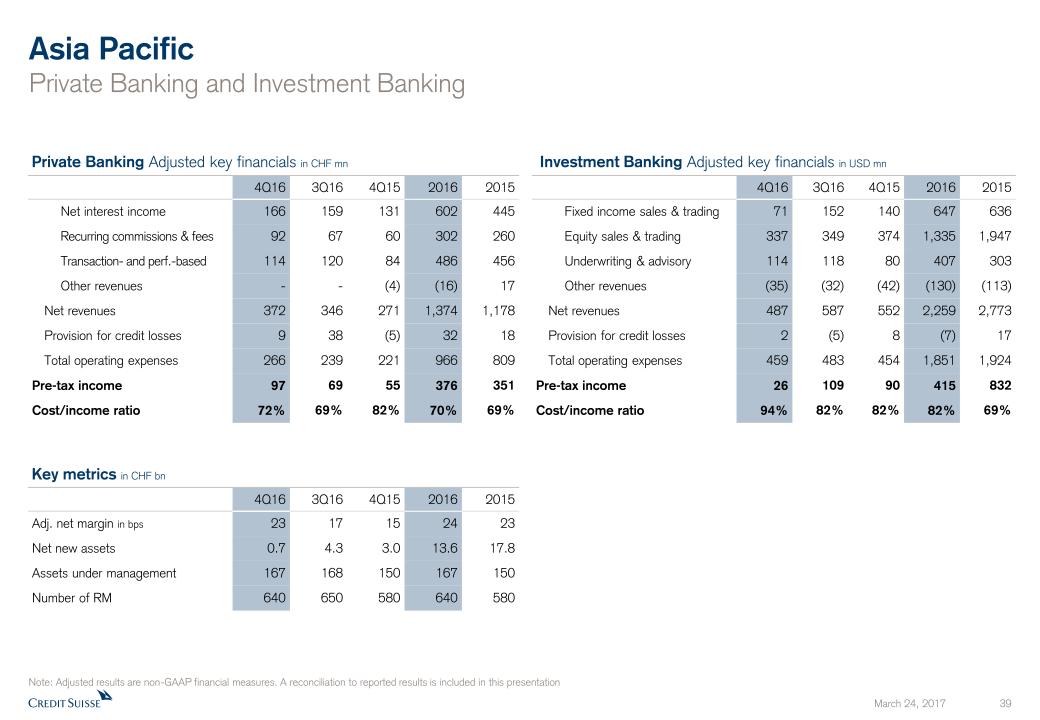

PB Adjusted key financials in CHF mn Asia PacificContinued growth and record full year results in Wealth Management 4Q16 3Q16 4Q15 2016 2015 Net revenues 862 917 826 3,597 3,839 Provision for credit losses 11 34 3 26 35 Total operating expenses 729 708 675 2,793 2,662 Pre-tax income 122 175 148 778 1,142 Cost/income ratio 85% 77% 82% 78% 69% Return on regulatory capital† 9% 13% 12% 15% 20% 4Q16 3Q16 4Q15 2016 2015 Adj. net margin in bps 23 17 15 24 23 Net new assets 0.7 4.3 3.0 13.6 17.8 Number of RM 640 650 580 640 580 Net loans 40 39 36 40 36 Risk-weighted assets 35 32 27 35 27 Leverage exposure 109 108 99 109 99 Note: All financial numbers presented and discussed are adjusted, unless otherwise stated. Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix † See Appendix1 Includes contributions from APAC Wealth Management, APAC Underwriting and Advisory as well as Financing for activities with our UHNWI, Entrepreneurs and Corporate clients. Pro forma Wealth Management and connected activities within APAC are based on preliminary estimates 2 Source: Dealogic 3 SMG = Strategic Market-Making Group Key messages Key metrics in CHF bn 4Q16 3Q16 4Q15 2016 2015 Pre-tax income 167 99 61 513 311 Pro-forma Wealth Management & connected activities1 in CHF mn Execution Profitable growth Legacy Detailed Financials Capital Record net revenues and pre-tax income in Wealth Management for the full year and 4Q16, with a revenue increase of 37% vs. 4Q15Continued positive NNA of CHF 0.7 bn in 4Q16 and CHF 13.6 bn in 2016, despite regularization outflows of CHF 1.4 bn in 4Q16 and CHF 2.5 bn in 2016Wealth Management gross margin up 15 bps vs. 4Q15 including higher margins on growing loan and deposit volumes and increased client activity; net margin up 8 bps vs. 4Q15Improved performance in Underwriting & Advisory vs. 4Q15 from increased client activity – #1 Rank2 in APAC ex-Japan amongst international banks for 2016Fixed income sales and trading revenues were lower in 4Q16 vs. 4Q15, reflecting reduction in client activity, especially in Rates, partially offset by positive net fair value impact on a portfolio of impaired loans and higher FX activityEquities revenues (excluding SMG3) up slightly vs. 4Q15, mainly reflecting trading gains and positive net fair value impact on a portfolio of impaired loans, partially offset by decrease in Prime Services. Full year 2016 results were adversely impacted from decreased client activity in Greater China

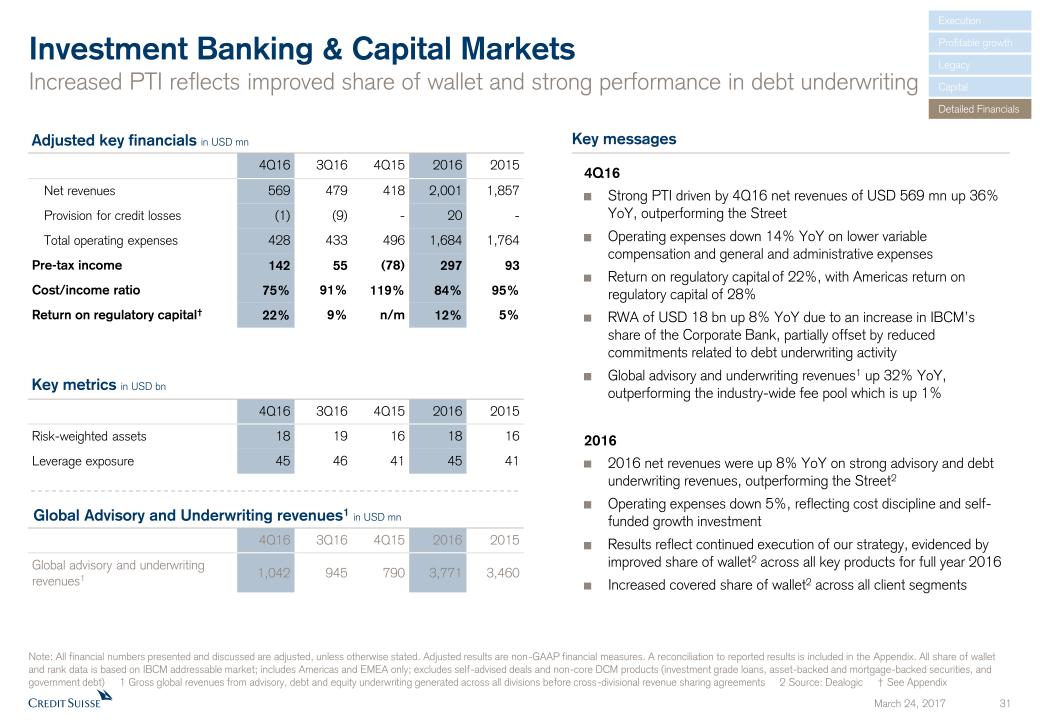

Key messages Investment Banking & Capital MarketsIncreased PTI reflects improved share of wallet and strong performance in debt underwriting Note: All financial numbers presented and discussed are adjusted, unless otherwise stated. Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix. All share of wallet and rank data is based on IBCM addressable market; includes Americas and EMEA only; excludes self-advised deals and non-core DCM products (investment grade loans, asset-backed and mortgage-backed securities, and government debt) 1 Gross global revenues from advisory, debt and equity underwriting generated across all divisions before cross-divisional revenue sharing agreements 2 Source: Dealogic † See Appendix 4Q16Strong PTI driven by 4Q16 net revenues of USD 569 mn up 36% YoY, outperforming the StreetOperating expenses down 14% YoY on lower variable compensation and general and administrative expensesReturn on regulatory capital of 22%, with Americas return on regulatory capital of 28%RWA of USD 18 bn up 8% YoY due to an increase in IBCM’s share of the Corporate Bank, partially offset by reduced commitments related to debt underwriting activityGlobal advisory and underwriting revenues1 up 32% YoY, outperforming the industry-wide fee pool which is up 1%20162016 net revenues were up 8% YoY on strong advisory and debt underwriting revenues, outperforming the Street2Operating expenses down 5%, reflecting cost discipline and self-funded growth investmentResults reflect continued execution of our strategy, evidenced by improved share of wallet2 across all key products for full year 2016Increased covered share of wallet2 across all client segments 4Q16 3Q16 4Q15 2016 2015 Risk-weighted assets 18 19 16 18 16 Leverage exposure 45 46 41 45 41 Adjusted key financials in USD mn 4Q16 3Q16 4Q15 2016 2015 Net revenues 569 479 418 2,001 1,857 Provision for credit losses (1) (9) - 20 - Total operating expenses 428 433 496 1,684 1,764 Pre-tax income 142 55 (78) 297 93 Cost/income ratio 75% 91% 119% 84% 95% Return on regulatory capital† 22% 9% n/m 12% 5% Key metrics in USD bn 4Q16 3Q16 4Q15 2016 2015 Global advisory and underwriting revenues1 1,042 945 790 3,771 3,460 Global Advisory and Underwriting revenues1 in USD mn Execution Profitable growth Legacy Detailed Financials Capital

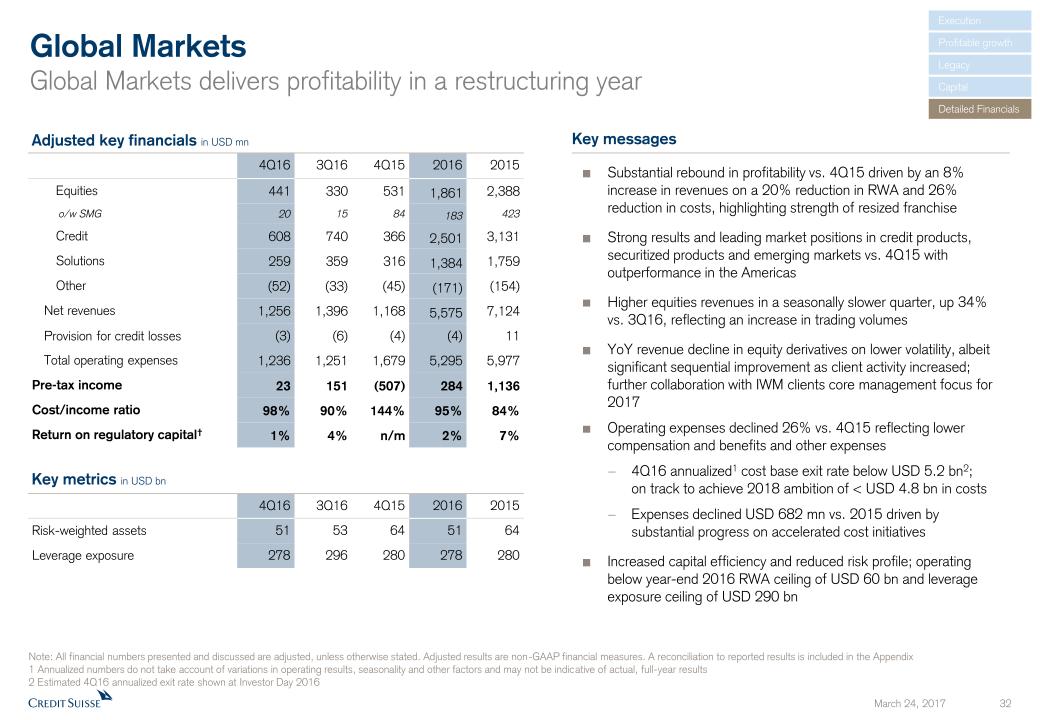

Key messages Global MarketsGlobal Markets delivers profitability in a restructuring year 4Q16 3Q16 4Q15 2016 2015 Equities 441 330 531 1,861 2,388 o/w SMG 20 15 84 183 423 Credit 608 740 366 2,501 3,131 Solutions 259 359 316 1,384 1,759 Other (52) (33) (45) (171) (154) Net revenues 1,256 1,396 1,168 5,575 7,124 Provision for credit losses (3) (6) (4) (4) 11 Total operating expenses 1,236 1,251 1,679 5,295 5,977 Pre-tax income 23 151 (507) 284 1,136 Cost/income ratio 98% 90% 144% 95% 84% Return on regulatory capital† 1% 4% n/m 2% 7% Substantial rebound in profitability vs. 4Q15 driven by an 8% increase in revenues on a 20% reduction in RWA and 26% reduction in costs, highlighting strength of resized franchiseStrong results and leading market positions in credit products, securitized products and emerging markets vs. 4Q15 with outperformance in the AmericasHigher equities revenues in a seasonally slower quarter, up 34% vs. 3Q16, reflecting an increase in trading volumesYoY revenue decline in equity derivatives on lower volatility, albeit significant sequential improvement as client activity increased; further collaboration with IWM clients core management focus for 2017Operating expenses declined 26% vs. 4Q15 reflecting lower compensation and benefits and other expenses 4Q16 annualized1 cost base exit rate below USD 5.2 bn2;on track to achieve 2018 ambition of < USD 4.8 bn in costsExpenses declined USD 682 mn vs. 2015 driven by substantial progress on accelerated cost initiatives Increased capital efficiency and reduced risk profile; operating below year-end 2016 RWA ceiling of USD 60 bn and leverage exposure ceiling of USD 290 bn 4Q16 3Q16 4Q15 2016 2015 Risk-weighted assets 51 53 64 51 64 Leverage exposure 278 296 280 278 280 Key metrics in USD bn Note: All financial numbers presented and discussed are adjusted, unless otherwise stated. Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix1 Annualized numbers do not take account of variations in operating results, seasonality and other factors and may not be indicative of actual, full-year results 2 Estimated 4Q16 annualized exit rate shown at Investor Day 2016 Execution Profitable growth Legacy Detailed Financials Capital Adjusted key financials in USD mn

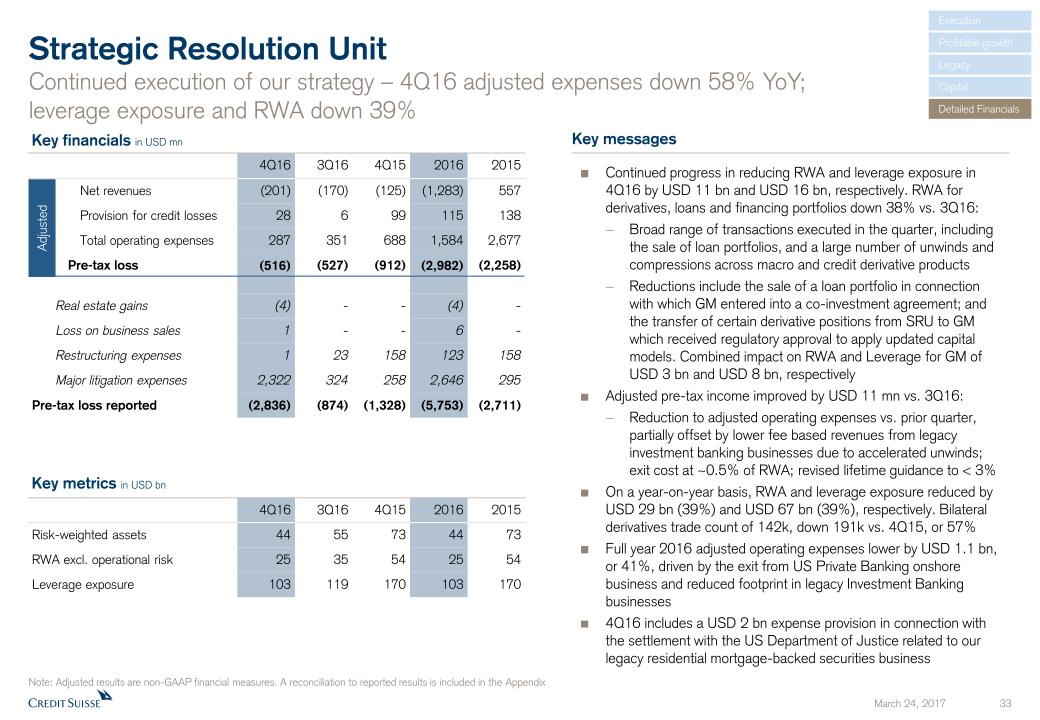

Adjusted Key messages Strategic Resolution UnitContinued execution of our strategy – 4Q16 adjusted expenses down 58% YoY;leverage exposure and RWA down 39% Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix Key financials in USD mn 4Q16 3Q16 4Q15 2016 2015 Net revenues (201) (170) (125) (1,283) 557 Provision for credit losses 28 6 99 115 138 Total operating expenses 287 351 688 1,584 2,677 Pre-tax loss (516) (527) (912) (2,982) (2,258) Real estate gains (4) - - (4) - Loss on business sales 1 - - 6 - Restructuring expenses 1 23 158 123 158 Major litigation expenses 2,322 324 258 2,646 295 Pre-tax loss reported (2,836) (874) (1,328) (5,753) (2,711) 4Q16 3Q16 4Q15 2016 2015 Risk-weighted assets 44 55 73 44 73 RWA excl. operational risk 25 35 54 25 54 Leverage exposure 103 119 170 103 170 Key metrics in USD bn Continued progress in reducing RWA and leverage exposure in 4Q16 by USD 11 bn and USD 16 bn, respectively. RWA for derivatives, loans and financing portfolios down 38% vs. 3Q16:Broad range of transactions executed in the quarter, including the sale of loan portfolios, and a large number of unwinds and compressions across macro and credit derivative productsReductions include the sale of a loan portfolio in connection with which GM entered into a co-investment agreement; and the transfer of certain derivative positions from SRU to GM which received regulatory approval to apply updated capital models. Combined impact on RWA and Leverage for GM of USD 3 bn and USD 8 bn, respectivelyAdjusted pre-tax income improved by USD 11 mn vs. 3Q16:Reduction to adjusted operating expenses vs. prior quarter, partially offset by lower fee based revenues from legacy investment banking businesses due to accelerated unwinds; exit cost at ~0.5% of RWA; revised lifetime guidance to < 3%On a year-on-year basis, RWA and leverage exposure reduced by USD 29 bn (39%) and USD 67 bn (39%), respectively. Bilateral derivatives trade count of 142k, down 191k vs. 4Q15, or 57%Full year 2016 adjusted operating expenses lower by USD 1.1 bn, or 41%, driven by the exit from US Private Banking onshore business and reduced footprint in legacy Investment Banking businesses4Q16 includes a USD 2 bn expense provision in connection with the settlement with the US Department of Justice related to our legacy residential mortgage-backed securities business Execution Profitable growth Legacy Detailed Financials Capital

Summary Executing with disciplineGrowing profitablyResolving key legacy issuesStrengthening our capital position 1 3 2 4

Appendix

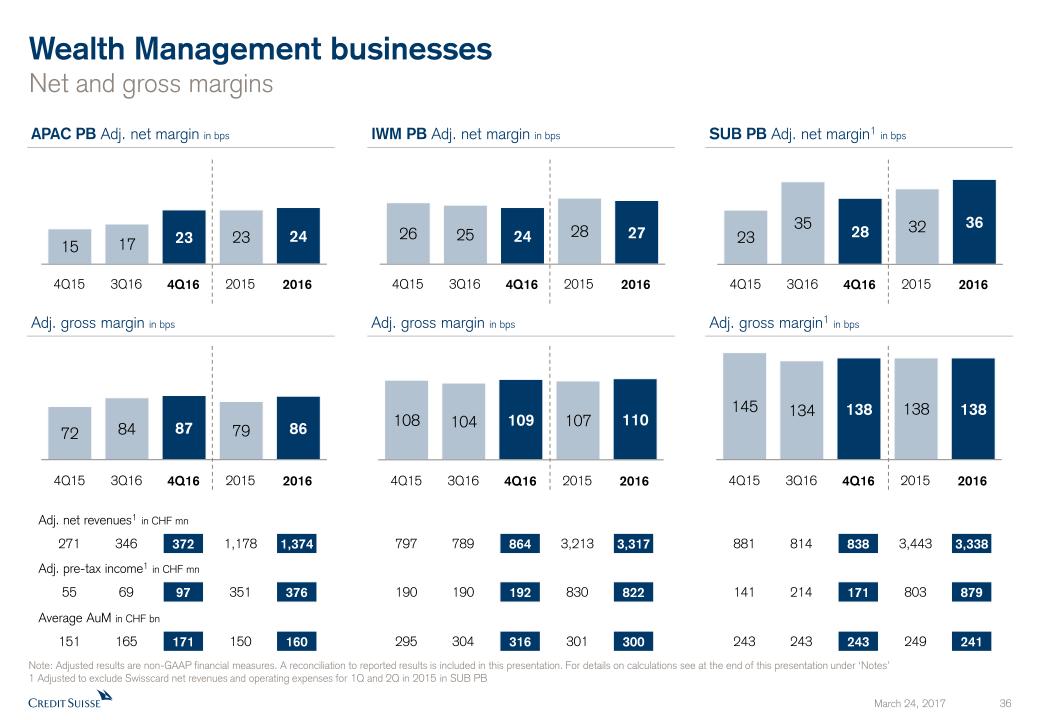

Wealth Management businessesNet and gross margins Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in this presentation. For details on calculations see at the end of this presentation under ‘Notes’1 Adjusted to exclude Swisscard net revenues and operating expenses for 1Q and 2Q in 2015 in SUB PB SUB PB Adj. net margin1 in bps Adj. gross margin1 in bps IWM PB Adj. net margin in bps Adj. gross margin in bps APAC PB Adj. net margin in bps 151 160 150 4Q15 2016 4Q16 Adj. gross margin in bps Average AuM in CHF bn 55 376 351 Adj. pre-tax income1 in CHF mn 271 1,374 1,178 Adj. net revenues1 in CHF mn 3Q16 2015 4Q15 2016 4Q16 3Q16 2015 4Q15 2016 4Q16 3Q16 2015 4Q15 2016 4Q16 3Q16 2015 4Q15 2016 4Q16 3Q16 2015 4Q15 2016 4Q16 3Q16 2015 165 69 346 171 97 372 295 300 301 190 822 830 797 3,317 3,213 304 190 789 316 192 864 243 241 249 141 879 803 881 3,338 3,443 243 214 814 243 171 838

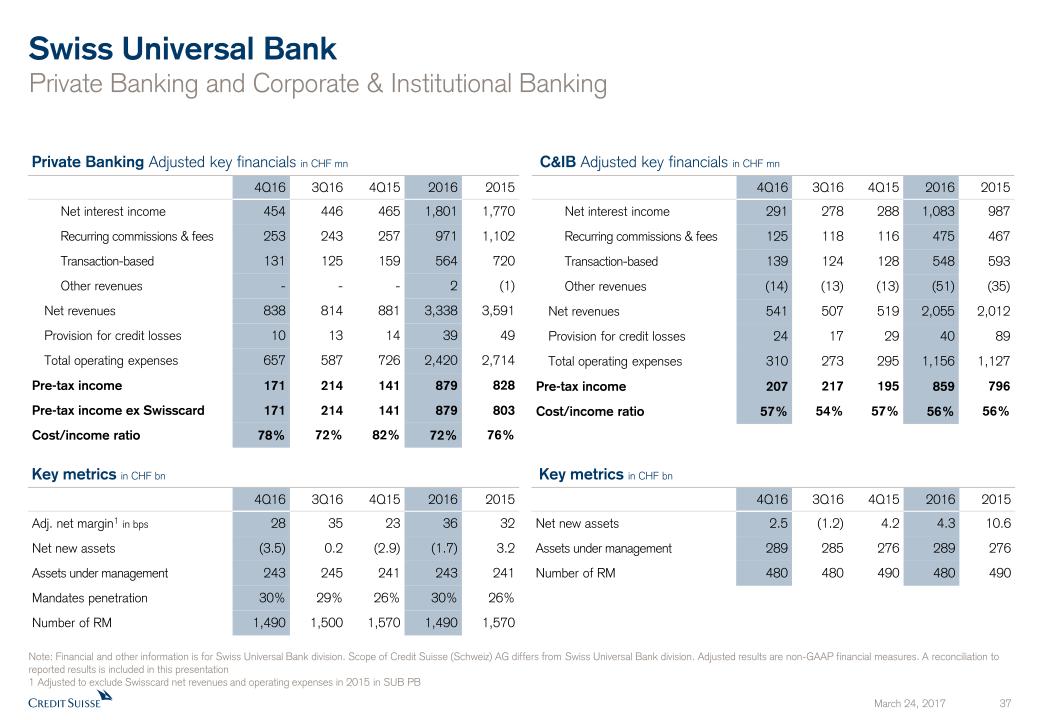

Swiss Universal BankPrivate Banking and Corporate & Institutional Banking Note: Financial and other information is for Swiss Universal Bank division. Scope of Credit Suisse (Schweiz) AG differs from Swiss Universal Bank division. Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in this presentation1 Adjusted to exclude Swisscard net revenues and operating expenses in 2015 in SUB PB Private Banking Adjusted key financials in CHF mn C&IB Adjusted key financials in CHF mn Key metrics in CHF bn Key metrics in CHF bn 4Q16 3Q16 4Q15 2016 2015 Net interest income 291 278 288 1,083 987 Recurring commissions & fees 125 118 116 475 467 Transaction-based 139 124 128 548 593 Other revenues (14) (13) (13) (51) (35) Net revenues 541 507 519 2,055 2,012 Provision for credit losses 24 17 29 40 89 Total operating expenses 310 273 295 1,156 1,127 Pre-tax income 207 217 195 859 796 Cost/income ratio 57% 54% 57% 56% 56% 4Q16 3Q16 4Q15 2016 2015 Adj. net margin1 in bps 28 35 23 36 32 Net new assets (3.5) 0.2 (2.9) (1.7) 3.2 Assets under management 243 245 241 243 241 Mandates penetration 30% 29% 26% 30% 26% Number of RM 1,490 1,500 1,570 1,490 1,570 4Q16 3Q16 4Q15 2016 2015 Net new assets 2.5 (1.2) 4.2 4.3 10.6 Assets under management 289 285 276 289 276 Number of RM 480 480 490 480 490 4Q16 3Q16 4Q15 2016 2015 Net interest income 454 446 465 1,801 1,770 Recurring commissions & fees 253 243 257 971 1,102 Transaction-based 131 125 159 564 720 Other revenues - - - 2 (1) Net revenues 838 814 881 3,338 3,591 Provision for credit losses 10 13 14 39 49 Total operating expenses 657 587 726 2,420 2,714 Pre-tax income 171 214 141 879 828 Pre-tax income ex Swisscard 171 214 141 879 803 Cost/income ratio 78% 72% 82% 72% 76%

International Wealth ManagementPrivate Banking and Asset Management Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in this presentation Private Banking Adjusted key financials in CHF mn Asset Management Adjusted key financials in CHF mn Key metrics in CHF bn Key metrics in CHF bn 4Q16 3Q16 4Q15 2016 2015 Net interest income 353 326 275 1,308 1,006 Recurring commissions & fees 277 267 283 1,093 1,161 Transaction- and perf.-based 235 197 240 922 1,049 Other revenues (1) (1) (1) (6) (3) Net revenues 864 789 797 3,317 3,213 Provision for credit losses 6 - (7) 20 5 Total operating expenses 666 599 614 2,475 2,378 Pre-tax income 192 190 190 822 830 Cost/income ratio 77% 76% 77% 75% 74% 4Q16 3Q16 4Q15 2016 2015 Adj. net margin in bps 24 25 26 27 28 Net new assets 0.4 4.4 (4.2) 15.6 (3.0) Assets under management 323 311 290 323 290 Net loans 45 43 40 45 40 Number of RM 1,140 1,160 1,180 1,140 1,180 4Q16 3Q16 4Q15 2016 2015 Management fees 228 218 225 891 873 Performance & placement rev. 108 41 56 208 164 Investment & partnership inc. 45 33 84 228 291 Net revenues 381 292 365 1,327 1,328 Total operating expenses 273 241 326 1,040 1,142 Pre-tax income 108 51 39 287 186 Cost/income ratio 72% 83% 89% 78% 86% 4Q16 3Q16 4Q15 2016 2015 Net new assets (4.4) 5.0 3.6 5.6 26.5 Assets under management 322 324 321 322 321

Asia PacificPrivate Banking and Investment Banking Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in this presentation Private Banking Adjusted key financials in CHF mn Investment Banking Adjusted key financials in USD mn Key metrics in CHF bn 4Q16 3Q16 4Q15 2016 2015 Net interest income 166 159 131 602 445 Recurring commissions & fees 92 67 60 302 260 Transaction- and perf.-based 114 120 84 486 456 Other revenues - - (4) (16) 17 Net revenues 372 346 271 1,374 1,178 Provision for credit losses 9 38 (5) 32 18 Total operating expenses 266 239 221 966 809 Pre-tax income 97 69 55 376 351 Cost/income ratio 72% 69% 82% 70% 69% 4Q16 3Q16 4Q15 2016 2015 Adj. net margin in bps 23 17 15 24 23 Net new assets 0.7 4.3 3.0 13.6 17.8 Assets under management 167 168 150 167 150 Number of RM 640 650 580 640 580 4Q16 3Q16 4Q15 2016 2015 Fixed income sales & trading 71 152 140 647 636 Equity sales & trading 337 349 374 1,335 1,947 Underwriting & advisory 114 118 80 407 303 Other revenues (35) (32) (42) (130) (113) Net revenues 487 587 552 2,259 2,773 Provision for credit losses 2 (5) 8 (7) 17 Total operating expenses 459 483 454 1,851 1,924 Pre-tax income 26 109 90 415 832 Cost/income ratio 94% 82% 82% 82% 69%

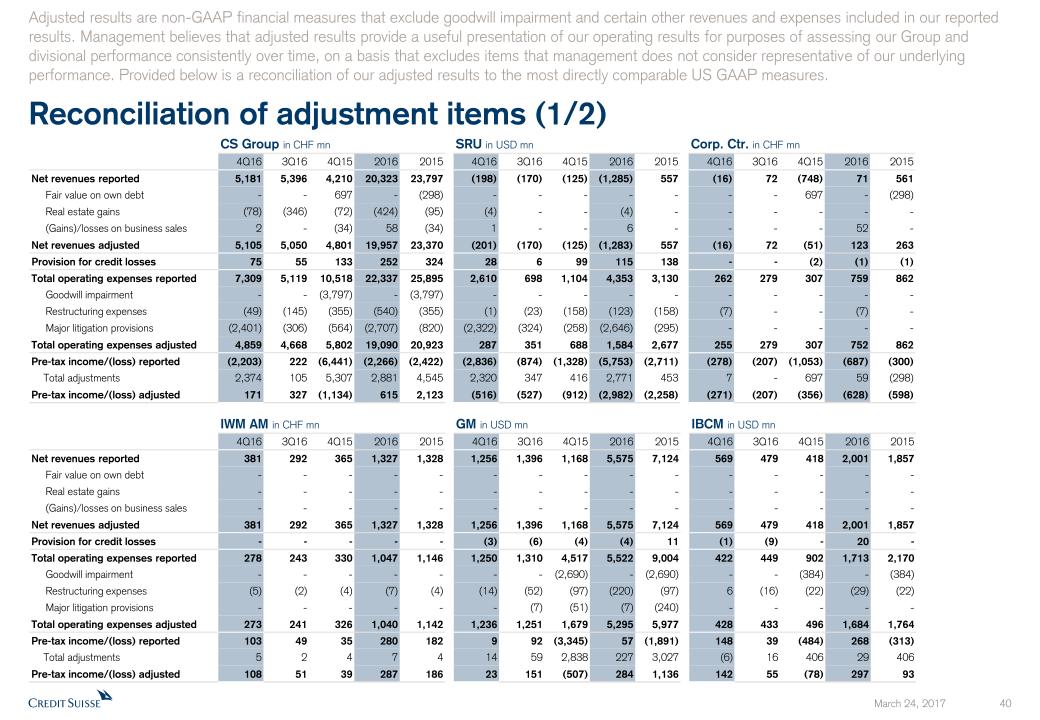

Reconciliation of adjustment items (1/2) IWM AM in CHF mn GM in USD mn IBCM in USD mn 4Q16 3Q16 4Q15 2016 2015 4Q16 3Q16 4Q15 2016 2015 4Q16 3Q16 4Q15 2016 2015 Net revenues reported 381 292 365 1,327 1,328 1,256 1,396 1,168 5,575 7,124 569 479 418 2,001 1,857 Fair value on own debt - - - - - - - - - - - - - - - Real estate gains - - - - - - - - - - - - - - - (Gains)/losses on business sales - - - - - - - - - - - - - - - Net revenues adjusted 381 292 365 1,327 1,328 1,256 1,396 1,168 5,575 7,124 569 479 418 2,001 1,857 Provision for credit losses - - - - - (3) (6) (4) (4) 11 (1) (9) - 20 - Total operating expenses reported 278 243 330 1,047 1,146 1,250 1,310 4,517 5,522 9,004 422 449 902 1,713 2,170 Goodwill impairment - - - - - - - (2,690) - (2,690) - - (384) - (384) Restructuring expenses (5) (2) (4) (7) (4) (14) (52) (97) (220) (97) 6 (16) (22) (29) (22) Major litigation provisions - - - - - - (7) (51) (7) (240) - - - - - Total operating expenses adjusted 273 241 326 1,040 1,142 1,236 1,251 1,679 5,295 5,977 428 433 496 1,684 1,764 Pre-tax income/(loss) reported 103 49 35 280 182 9 92 (3,345) 57 (1,891) 148 39 (484) 268 (313) Total adjustments 5 2 4 7 4 14 59 2,838 227 3,027 (6) 16 406 29 406 Pre-tax income/(loss) adjusted 108 51 39 287 186 23 151 (507) 284 1,136 142 55 (78) 297 93 Adjusted results are non-GAAP financial measures that exclude goodwill impairment and certain other revenues and expenses included in our reported results. Management believes that adjusted results provide a useful presentation of our operating results for purposes of assessing our Group and divisional performance consistently over time, on a basis that excludes items that management does not consider representative of our underlying performance. Provided below is a reconciliation of our adjusted results to the most directly comparable US GAAP measures. CS Group in CHF mn SRU in USD mn Corp. Ctr. in CHF mn 4Q16 3Q16 4Q15 2016 2015 4Q16 3Q16 4Q15 2016 2015 4Q16 3Q16 4Q15 2016 2015 Net revenues reported 5,181 5,396 4,210 20,323 23,797 (198) (170) (125) (1,285) 557 (16) 72 (748) 71 561 Fair value on own debt - - 697 - (298) - - - - - - - 697 - (298) Real estate gains (78) (346) (72) (424) (95) (4) - - (4) - - - - - - (Gains)/losses on business sales 2 - (34) 58 (34) 1 - - 6 - - - - 52 - Net revenues adjusted 5,105 5,050 4,801 19,957 23,370 (201) (170) (125) (1,283) 557 (16) 72 (51) 123 263 Provision for credit losses 75 55 133 252 324 28 6 99 115 138 - - (2) (1) (1) Total operating expenses reported 7,309 5,119 10,518 22,337 25,895 2,610 698 1,104 4,353 3,130 262 279 307 759 862 Goodwill impairment - - (3,797) - (3,797) - - - - - - - - - - Restructuring expenses (49) (145) (355) (540) (355) (1) (23) (158) (123) (158) (7) - - (7) - Major litigation provisions (2,401) (306) (564) (2,707) (820) (2,322) (324) (258) (2,646) (295) - - - - - Total operating expenses adjusted 4,859 4,668 5,802 19,090 20,923 287 351 688 1,584 2,677 255 279 307 752 862 Pre-tax income/(loss) reported (2,203) 222 (6,441) (2,266) (2,422) (2,836) (874) (1,328) (5,753) (2,711) (278) (207) (1,053) (687) (300) Total adjustments 2,374 105 5,307 2,881 4,545 2,320 347 416 2,771 453 7 - 697 59 (298) Pre-tax income/(loss) adjusted 171 327 (1,134) 615 2,123 (516) (527) (912) (2,982) (2,258) (271) (207) (356) (628) (598)

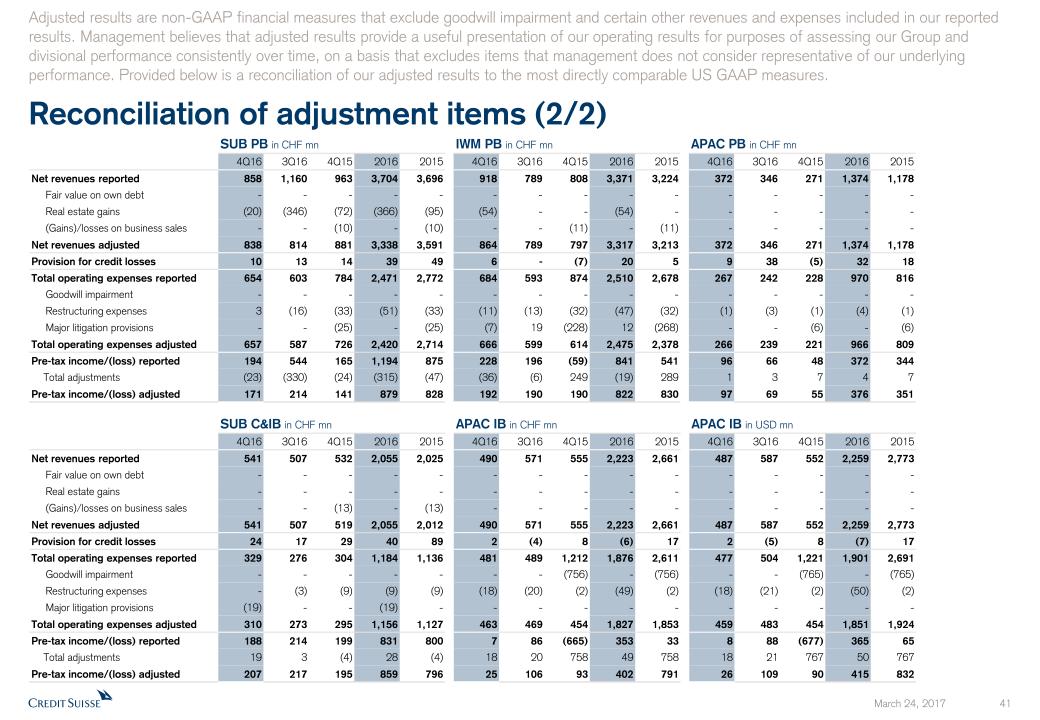

SUB PB in CHF mn IWM PB in CHF mn APAC PB in CHF mn 4Q16 3Q16 4Q15 2016 2015 4Q16 3Q16 4Q15 2016 2015 4Q16 3Q16 4Q15 2016 2015 Net revenues reported 858 1,160 963 3,704 3,696 918 789 808 3,371 3,224 372 346 271 1,374 1,178 Fair value on own debt - - - - - - - - - - - - - - - Real estate gains (20) (346) (72) (366) (95) (54) - - (54) - - - - - - (Gains)/losses on business sales - - (10) - (10) - - (11) - (11) - - - - - Net revenues adjusted 838 814 881 3,338 3,591 864 789 797 3,317 3,213 372 346 271 1,374 1,178 Provision for credit losses 10 13 14 39 49 6 - (7) 20 5 9 38 (5) 32 18 Total operating expenses reported 654 603 784 2,471 2,772 684 593 874 2,510 2,678 267 242 228 970 816 Goodwill impairment - - - - - - - - - - - - - - - Restructuring expenses 3 (16) (33) (51) (33) (11) (13) (32) (47) (32) (1) (3) (1) (4) (1) Major litigation provisions - - (25) - (25) (7) 19 (228) 12 (268) - - (6) - (6) Total operating expenses adjusted 657 587 726 2,420 2,714 666 599 614 2,475 2,378 266 239 221 966 809 Pre-tax income/(loss) reported 194 544 165 1,194 875 228 196 (59) 841 541 96 66 48 372 344 Total adjustments (23) (330) (24) (315) (47) (36) (6) 249 (19) 289 1 3 7 4 7 Pre-tax income/(loss) adjusted 171 214 141 879 828 192 190 190 822 830 97 69 55 376 351 SUB C&IB in CHF mn APAC IB in CHF mn APAC IB in USD mn 4Q16 3Q16 4Q15 2016 2015 4Q16 3Q16 4Q15 2016 2015 4Q16 3Q16 4Q15 2016 2015 Net revenues reported 541 507 532 2,055 2,025 490 571 555 2,223 2,661 487 587 552 2,259 2,773 Fair value on own debt - - - - - - - - - - - - - - - Real estate gains - - - - - - - - - - - - - - - (Gains)/losses on business sales - - (13) - (13) - - - - - - - - - - Net revenues adjusted 541 507 519 2,055 2,012 490 571 555 2,223 2,661 487 587 552 2,259 2,773 Provision for credit losses 24 17 29 40 89 2 (4) 8 (6) 17 2 (5) 8 (7) 17 Total operating expenses reported 329 276 304 1,184 1,136 481 489 1,212 1,876 2,611 477 504 1,221 1,901 2,691 Goodwill impairment - - - - - - - (756) - (756) - - (765) - (765) Restructuring expenses - (3) (9) (9) (9) (18) (20) (2) (49) (2) (18) (21) (2) (50) (2) Major litigation provisions (19) - - (19) - - - - - - - - - - - Total operating expenses adjusted 310 273 295 1,156 1,127 463 469 454 1,827 1,853 459 483 454 1,851 1,924 Pre-tax income/(loss) reported 188 214 199 831 800 7 86 (665) 353 33 8 88 (677) 365 65 Total adjustments 19 3 (4) 28 (4) 18 20 758 49 758 18 21 767 50 767 Pre-tax income/(loss) adjusted 207 217 195 859 796 25 106 93 402 791 26 109 90 415 832 Reconciliation of adjustment items (2/2) Adjusted results are non-GAAP financial measures that exclude goodwill impairment and certain other revenues and expenses included in our reported results. Management believes that adjusted results provide a useful presentation of our operating results for purposes of assessing our Group and divisional performance consistently over time, on a basis that excludes items that management does not consider representative of our underlying performance. Provided below is a reconciliation of our adjusted results to the most directly comparable US GAAP measures.

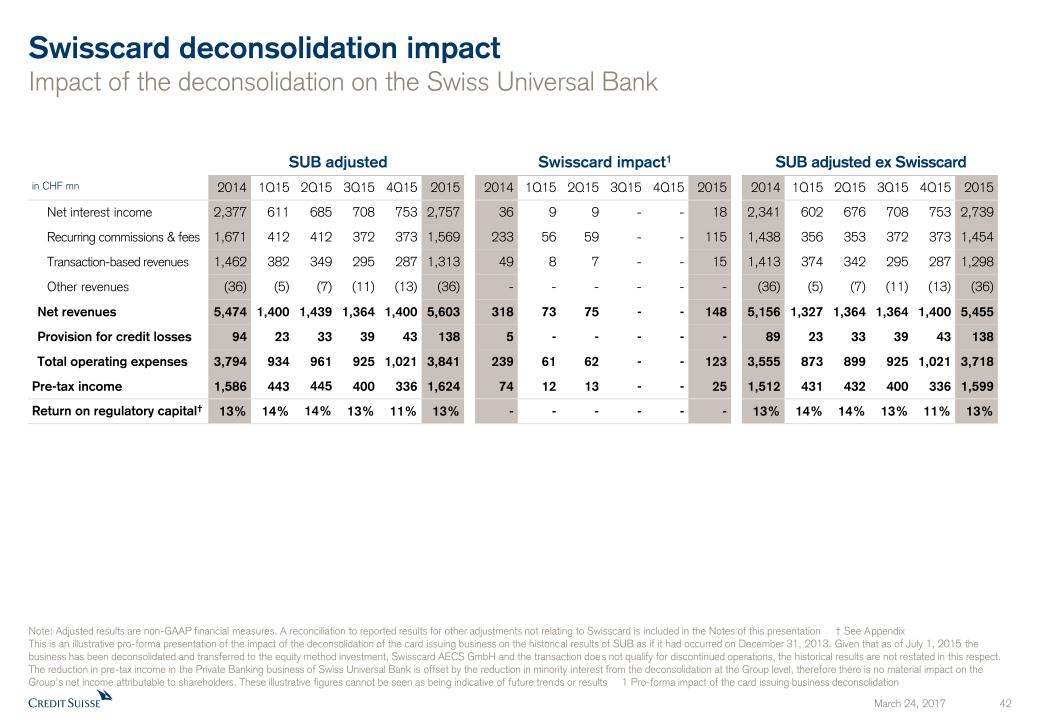

Swisscard deconsolidation impactImpact of the deconsolidation on the Swiss Universal Bank Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results for other adjustments not relating to Swisscard is included in the Notes of this presentation † See AppendixThis is an illustrative pro-forma presentation of the impact of the deconsolidation of the card issuing business on the historical results of SUB as if it had occurred on December 31, 2013. Given that as of July 1, 2015 the business has been deconsolidated and transferred to the equity method investment, Swisscard AECS GmbH and the transaction does not qualify for discontinued operations, the historical results are not restated in this respect. The reduction in pre-tax income in the Private Banking business of Swiss Universal Bank is offset by the reduction in minority interest from the deconsolidation at the Group level, therefore there is no material impact on the Group’s net income attributable to shareholders. These illustrative figures cannot be seen as being indicative of future trends or results 1 Pro-forma impact of the card issuing business deconsolidation in CHF mn 2014 1Q15 2Q15 3Q15 4Q15 2015 2014 1Q15 2Q15 3Q15 4Q15 2015 2014 1Q15 2Q15 3Q15 4Q15 2015 Net interest income 2,377 611 685 708 753 2,757 36 9 9 - - 18 2,341 602 676 708 753 2,739 Recurring commissions & fees 1,671 412 412 372 373 1,569 233 56 59 - - 115 1,438 356 353 372 373 1,454 Transaction-based revenues 1,462 382 349 295 287 1,313 49 8 7 - - 15 1,413 374 342 295 287 1,298 Other revenues (36) (5) (7) (11) (13) (36) - - - - - - (36) (5) (7) (11) (13) (36) Net revenues 5,474 1,400 1,439 1,364 1,400 5,603 318 73 75 - - 148 5,156 1,327 1,364 1,364 1,400 5,455 Provision for credit losses 94 23 33 39 43 138 5 - - - - - 89 23 33 39 43 138 Total operating expenses 3,794 934 961 925 1,021 3,841 239 61 62 - - 123 3,555 873 899 925 1,021 3,718 Pre-tax income 1,586 443 445 400 336 1,624 74 12 13 - - 25 1,512 431 432 400 336 1,599 Return on regulatory capital† 13% 14% 14% 13% 11% 13% - - - - - - 13% 14% 14% 13% 11% 13% SUB adjusted Swisscard impact1 SUB adjusted ex Swisscard

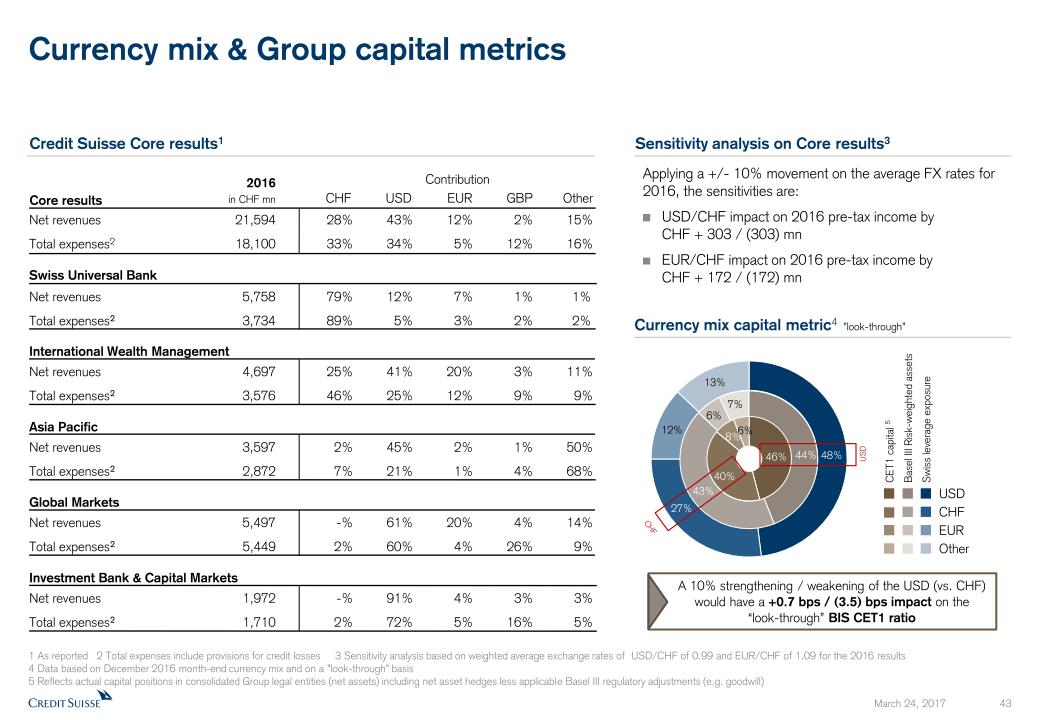

Currency mix & Group capital metrics Currency mix capital metric4 ”look-through” A 10% strengthening / weakening of the USD (vs. CHF) would have a +0.7 bps / (3.5) bps impact on the“look-through” BIS CET1 ratio CHF 1 As reported 2 Total expenses include provisions for credit losses 3 Sensitivity analysis based on weighted average exchange rates of USD/CHF of 0.99 and EUR/CHF of 1.09 for the 2016 results 4 Data based on December 2016 month-end currency mix and on a ”look-through” basis 5 Reflects actual capital positions in consolidated Group legal entities (net assets) including net asset hedges less applicable Basel III regulatory adjustments (e.g. goodwill) Basel III Risk-weighted assets Swiss leverage exposure CHF EUR Other USD USD CET1 capital 5 Contribution Swiss Universal Bank Net revenues 5,758 79% 12% 7% 1% 1%Total expenses2 3,734 89% 5% 3% 2% 2% International Wealth Management Net revenues 4,697 25% 41% 20% 3% 11%Total expenses2 3,576 46% 25% 12% 9% 9% Net revenues 21,594 28% 43% 12% 2% 15%Total expenses2 18,100 33% 34% 5% 12% 16% Asia Pacific Net revenues 3,597 2% 45% 2% 1% 50%Total expenses2 2,872 7% 21% 1% 4% 68% Global Markets Net revenues 5,497 -% 61% 20% 4% 14%Total expenses2 5,449 2% 60% 4% 26% 9% Investment Bank & Capital Markets Net revenues 1,972 -% 91% 4% 3% 3%Total expenses2 1,710 2% 72% 5% 16% 5% Credit Suisse Core results1 Core results 2016in CHF mn CHF USD EUR GBP Other Applying a +/- 10% movement on the average FX rates for 2016, the sensitivities are:USD/CHF impact on 2016 pre-tax income by CHF + 303 / (303) mnEUR/CHF impact on 2016 pre-tax income by CHF + 172 / (172) mn Sensitivity analysis on Core results3

Notes Throughout the presentation rounding differences may occurAll risk-weighted assets (RWA) and leverage exposure figures shown in this presentation are as of the end of the respective period and on a “look-through” basisGross and net margins are shown in basis points (bps)Gross margin = adj. net revenues annualized / average AuM; net margin = adj. pre-tax income annualized / average AuMMandates penetration reflects advisory and discretionary mandates as percentage of total AuM, excluding AuM from the external asset manager (EAM) business General notes Adj. = Adjusted; AM = Asset Management; APAC = Asia Pacific; AuM = Assets under Management; bps = basis points; Corp. Ctr. = Corporate Center; C&IB = Corporate & Institutional Banking; DCM = Debt Capital Markets; DOJ = Department of Justice; EAM = External Asset Manager; ECM = Equity Capital Markets; GM = Global Markets; IB = Investment Banking; IBCM = Investment Banking & Capital Markets; IWM = International Wealth Management; n/m = not meaningful; NNA = Net new assets; PB = Private Banking; pp. = percentage points; PTI = Pre-tax income; QoQ = Quarter-on-quarter; RM = Relationship Manager(s); RMBS = Residential Mortgage-Backed Securities; SMG = Systematic Market-Making Group; SRU = Strategic Resolution Unit; SUB = Swiss Universal Bank; UHNWI = Ultra High Net Worth Individuals; WM = Wealth Management; YoY = Year-on-year Abbreviations Specific notes * “Adjusted operating expenses at constant FX rates” include adjustments as made in all our disclosures for restructuring expenses, major litigation expenses and a goodwill impairment taken in 4Q15 as well as adjustments for FX, applying the following main currency exchange rates for 1Q15: USD/CHF 0.9465, EUR/CHF 1.0482, GBP/CHF 1.4296, 2Q15: USD/CHF 0.9383, EUR/CHF 1.0418, GBP/CHF 1.4497, 3Q15: USD/CHF 0.9684, EUR/CHF 1.0787, GBP/CHF 1.4891, 4Q15: USD/CHF 1.0000, EUR/CHF 1.0851, GBP/CHF 1.5123, 1Q16: USD/CHF 0.9928, EUR/CHF 1.0941, GBP/CHF 1.4060, 2Q16: USD/CHF 0.9756, EUR/CHF 1.0956, GBP/CHF 1.3845, 3Q16: USD/CHF 0.9728, EUR/CHF 1.0882, GBP/CHF 1.2764, 4Q16: USD/CHF 1.0101, EUR/CHF 1.0798, GBP/CHF 1.2451. These currency exchange rates are unweighted, i.e. a straight line average of monthly rates. We apply this calculation consistently for the periods under review.† Regulatory capital reflects the worst of 10% of RWA and 3.5% of leverage exposure. Return on regulatory capital is based on (adjusted) returns after tax assuming a tax rate of 30% for all periods and capital allocated based on the worst of 10% of average RWA and 3.5% of average leverage exposure. For Global Markets and Investment Banking & Capital Markets, return on regulatory capital is based on US dollar denominated numbers.

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

CREDIT SUISSE GROUP AG and CREDIT SUISSE AG

(Registrants)

Date: March 24, 2017

By:

/s/ Christian Schmid

Christian Schmid

Managing Director

By:

/s/ Stephan Flückiger

Stephan Flückiger

Director