UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________

Form 6-K

______________

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

November 30, 2017

Commission File Number 001-15244

CREDIT SUISSE GROUP AG

(Translation of registrant’s name into English)

Paradeplatz 8, 8001 Zurich, Switzerland

(Address of principal executive office)

______________

Commission File Number 001-33434

CREDIT SUISSE AG

(Translation of registrant’s name into English)

Paradeplatz 8, 8001 Zurich, Switzerland

(Address of principal executive office)

______________

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

| Form 20-F ☒ | Form 40-F ☐ |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Note: Regulation S-T Rule 101(b)(1) only permits the submission in paper of a Form 6-K if submitted solely to provide an attached annual report to security holders.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Note: Regulation S-T Rule 101(b)(7) only permits the submission in paper of a Form 6-K if submitted to furnish a report or other document that the registrant foreign private issuer must furnish and make public under the laws of the jurisdiction in which the registrant is incorporated, domiciled or legally organized (the registrant’s “home country”), or under the rules of the home country exchange on which the registrant’s securities are traded, as long as the report or other document is not a press release, is not required to be and has not been distributed to the registrant’s security holders, and, if discussing a material event, has already been the subject of a Form 6-K submission or other Commission filing on EDGAR.

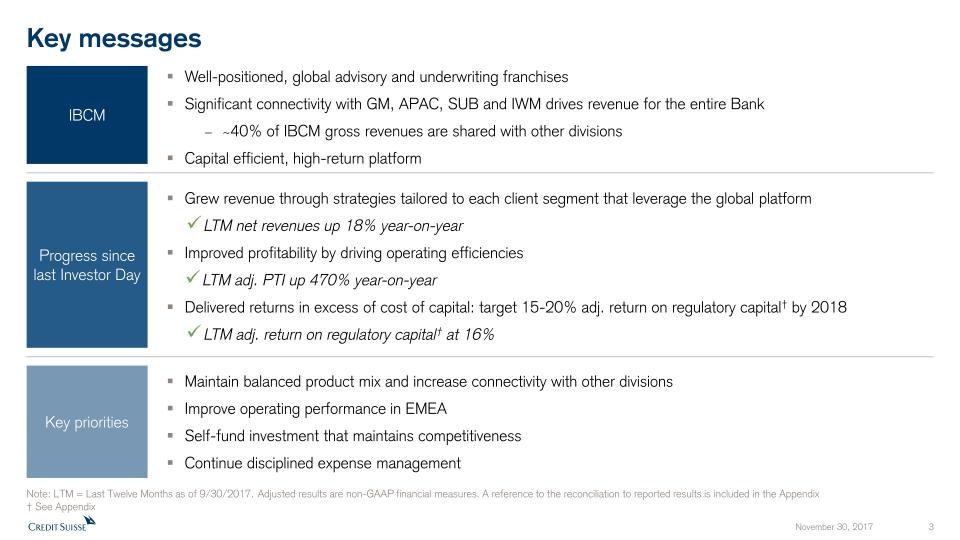

This report includes the slides for the presentation to investors in connection with Investor Day 2017 on November 30, 2017.

Credit Suisse Investor Day 2017Tidjane Thiam, CEO Credit Suisse November 30, 2017

Disclaimer This material does not purport to contain all of the information that you may wish to consider. This material is not to be relied upon as such or used in substitution for the exercise of independent judgment.Cautionary statement regarding forward-looking statementsThis presentation contains forward-looking statements that involve inherent risks and uncertainties, and we might not be able to achieve the predictions, forecasts, projections and other outcomes we describe or imply in forward-looking statements. A number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions we express in these forward-looking statements, including those we identify in "Risk factors” in our Annual Report on Form 20-F for the fiscal year ended December 31, 2016 and in the “Cautionary statement regarding forward-looking information" in our media release relating to Investor Day, published on November 30, 2017 and filed with the US Securities and Exchange Commission, and in other public filings and press releases. We do not intend to update these forward-looking statements. In particular, the terms “Estimate”, “Illustrative”, “Ambition”, “Objective”, “Outlook” and “Goal” are not intended to be viewed as targets or projections, nor are they considered to be Key Performance Indicators. All such estimates, illustrations, ambitions and goals are subject to a large number of inherent risks, assumptions and uncertainties, many of which are completely outside of our control. These risks, assumptions and uncertainties include, but are not limited to, general market conditions, market volatility, interest rate volatility and levels, global and regional economic conditions, political uncertainty, changes in tax policies, regulatory changes, changes in levels of client activity as a result of any of the foregoing and other factors. Accordingly, this information should not be relied on for any purpose. We do not intend to update these estimates, illustrations, ambitions or goals. We may not achieve the benefits of our strategic initiativesWe may not achieve all of the expected benefits of our strategic initiatives. Factors beyond our control, including but not limited to the market and economic conditions, changes in laws, rules or regulations and other challenges discussed in our public filings, could limit our ability to achieve some or all of the expected benefits of these initiatives. Estimates, assumptions and opinionsIn preparing this presentation, management has made estimates and assumptions that affect the numbers presented. Actual results may differ. Annualized numbers do not take account of variations in operating results, seasonality and other factors and may not be indicative of actual, full-year results. Figures throughout this presentation may also be subject to rounding adjustments. All opinions and views constitute judgments as of the date of writing without regard to the date on which the reader may receive or access the information. This information is subject to change at any time without notice and we do not intend to update this information. Statement regarding non-GAAP financial measuresThis presentation also contains non-GAAP financial measures, including adjusted results. Information needed to reconcile such non-GAAP financial measures to the most directly comparable measures under US GAAP can be found in this presentation in the Appendix, which is available on our website at www.credit-suisse.com. Statement regarding capital, liquidity and leverageAs of January 1, 2013, Basel III was implemented in Switzerland along with the Swiss “Too Big to Fail” legislation and regulations thereunder (in each case, subject to certain phase-in periods). As of January 1, 2015, the Bank for International Settlements (BIS) leverage ratio framework, as issued by the Basel Committee on Banking Supervision (BCBS), was implemented in Switzerland by FINMA. Our related disclosures are in accordance with our interpretation of such requirements, including relevant assumptions. Changes in the interpretation of these requirements in Switzerland or in any of our assumptions or estimates could result in different numbers from those shown in this presentation. Capital and ratio numbers for periods prior to 2013 are based on estimates, which are calculated as if the Basel III framework had been in place in Switzerland during such periods. Unless otherwise noted, leverage exposure is based on the BIS leverage ratio framework and consists of period-end balance sheet assets and prescribed regulatory adjustments. Beginning in 2015, the Swiss leverage ratio is calculated as Swiss total capital, divided by period-end leverage exposure. The look-through BIS tier 1 leverage ratio and CET1 leverage ratio are calculated as look-through BIS tier 1 capital and CET1 capital, respectively, divided by end-period leverage exposure.SourcesCertain material in this presentation has been prepared by Credit Suisse on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. Credit Suisse has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to accuracy, completeness or reliability of such information.

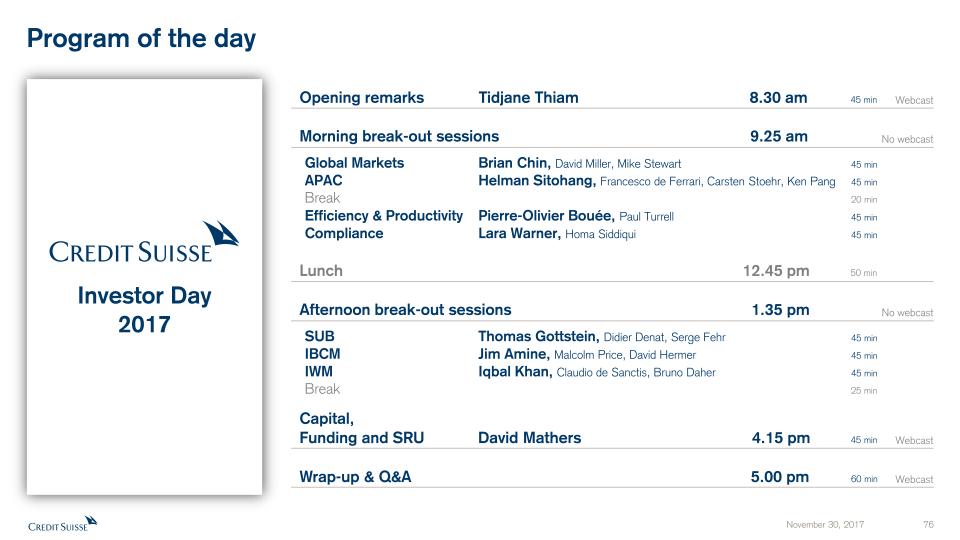

Program of the day Opening remarks Tidjane Thiam 8.30 am 45 min Webcast Morning break-out sessions 9.25 am No webcast Global Markets Brian Chin, David Miller, Mike Stewart 45 minAPAC Helman Sitohang, Francesco de Ferrari, Carsten Stoehr, Ken Pang 45 minBreak 20 minEfficiency & Productivity Pierre-Olivier Bouée, Paul Turrell 45 minCompliance Lara Warner, Homa Siddiqui 45 min Lunch 12.45 pm 50 min Afternoon break-out sessions 1.35 pm No webcast SUB Thomas Gottstein, Didier Denat, Serge Fehr 45 minIBCM Jim Amine, Malcolm Price, David Hermer 45 minIWM Iqbal Khan, Claudio de Sanctis, Bruno Daher 45 minBreak 25 min Capital,Funding and SRU David Mathers 4.15 pm 45 min Webcast Wrap-up & Q&A 5.00 pm 60 min Webcast Investor Day 2017

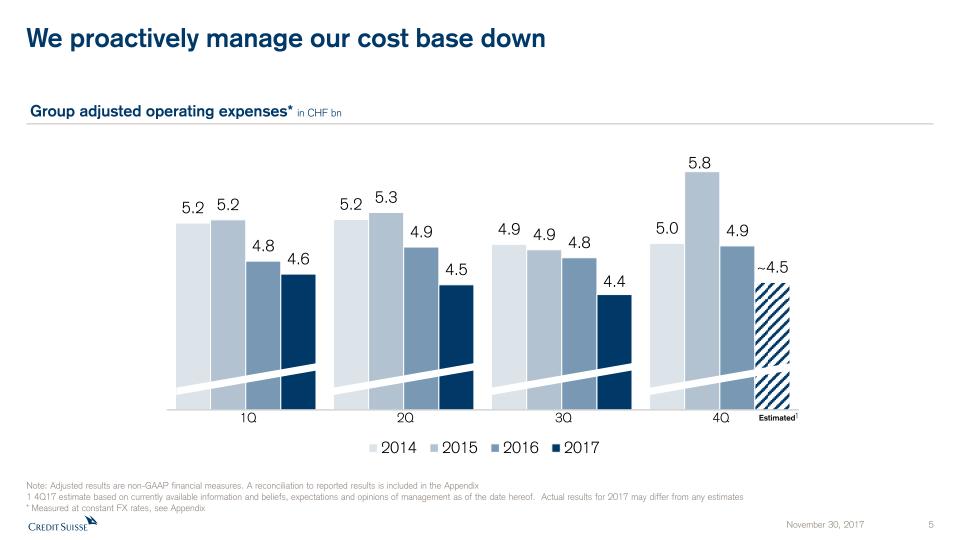

Delivering against our objectives Costs Reduce our cost base Net cost savings* since 2015 CHF 2.9 bn at 3Q17 Risk Right-size and de-risk our Global Markets activities GM RWA reduction2 -47% 3Q17 vs. 3Q15 Legacy Resolve legacy issues and wind-down the SRU SRU RWA reduction3 -70% 3Q17 vs. 3Q15 Capital Strengthen our capital position CET1 ratio 13.2% at 3Q17 Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix *Measured using Group adjusted operating expenses at constant FX rates, see Appendix1 Relating to SUB PC, IWM PB and APAC PB within WM&C 2 See page 46 for details on measurement 3 Excludes operational risk RWA of CHF 19 bn in 3Q15 and CHF 20 bn in 3Q17 Growth Deliver profitable growth and generate capital organically CHF 3.7 bn in 9M17 Core adjusted PTI CHF 33.2 bn in 9M17 NNA in Wealth Management1

The way forward Our strategy and progress The opportunity Agenda

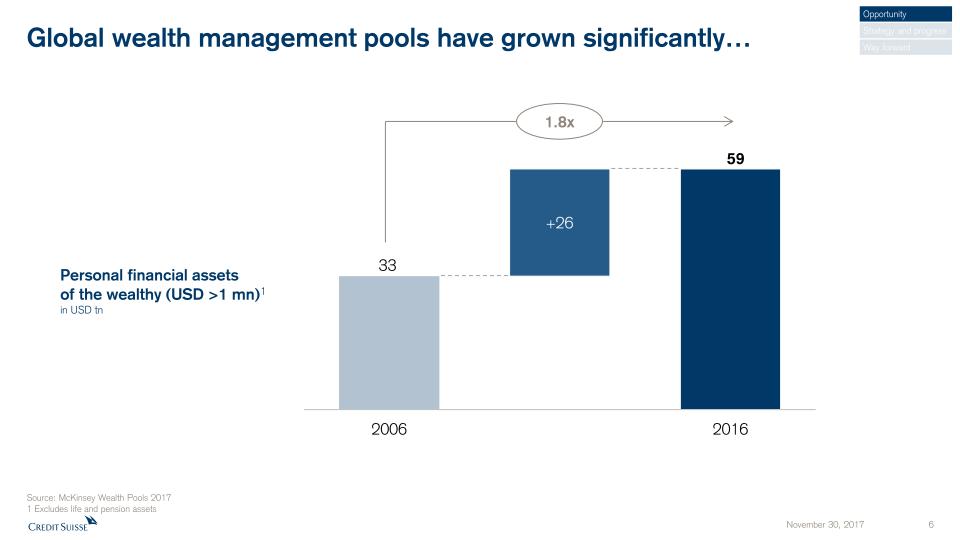

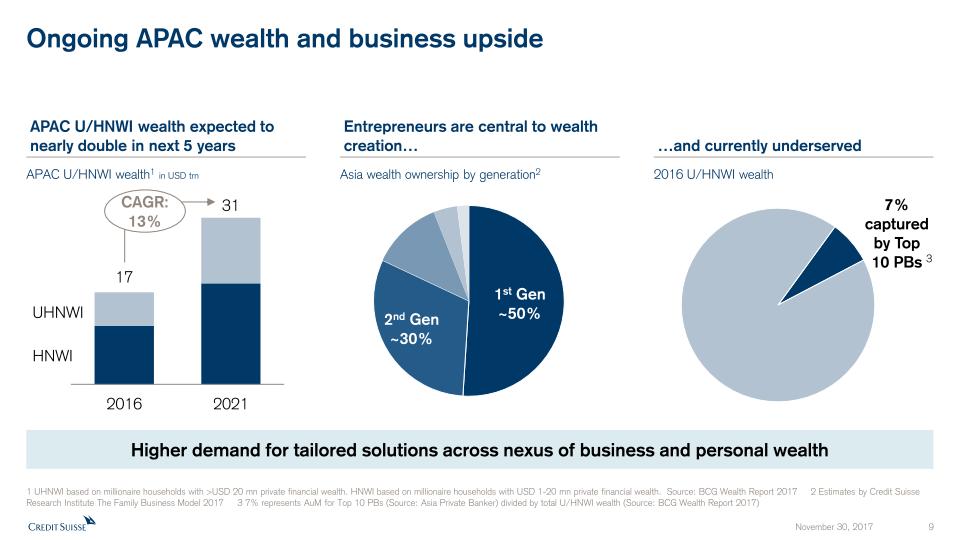

Source: McKinsey Wealth Pools 20171 Excludes life and pension assets Global wealth management pools have grown significantly… 1.8x Personal financial assetsof the wealthy (USD >1 mn)1in USD tn Opportunity Strategy and progress Way forward

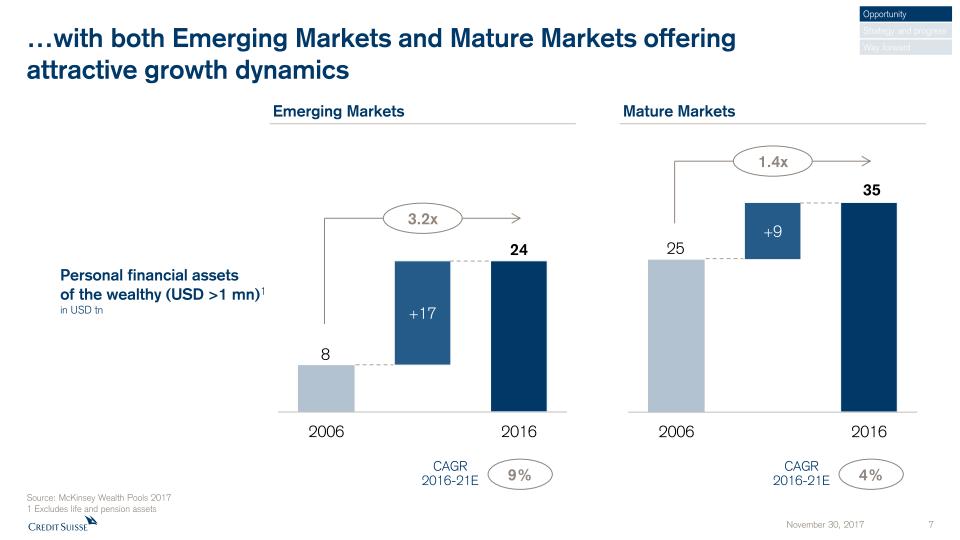

Source: McKinsey Wealth Pools 20171 Excludes life and pension assets …with both Emerging Markets and Mature Markets offeringattractive growth dynamics 1.4x Mature Markets Emerging Markets 3.2x 9% CAGR2016-21E 4% Personal financial assetsof the wealthy (USD >1 mn)1in USD tn CAGR2016-21E Opportunity Strategy and progress Way forward

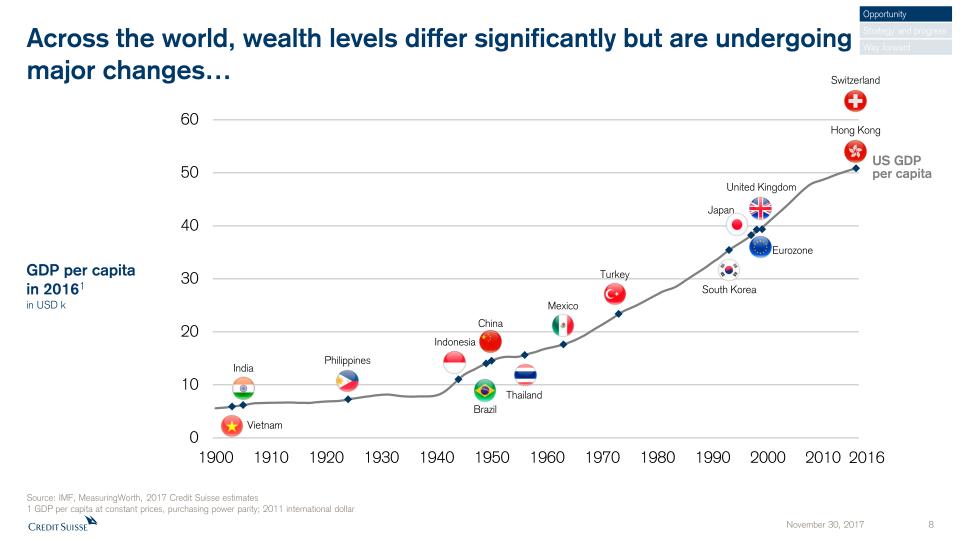

Across the world, wealth levels differ significantly but are undergoingmajor changes… GDP per capitain 20161in USD k Source: IMF, MeasuringWorth, 2017 Credit Suisse estimates1 GDP per capita at constant prices, purchasing power parity; 2011 international dollar Vietnam India Philippines Indonesia Brazil China Thailand Mexico South Korea Hong Kong Japan United Kingdom Eurozone Switzerland 2016 Turkey Opportunity Strategy and progress Way forward US GDP per capita

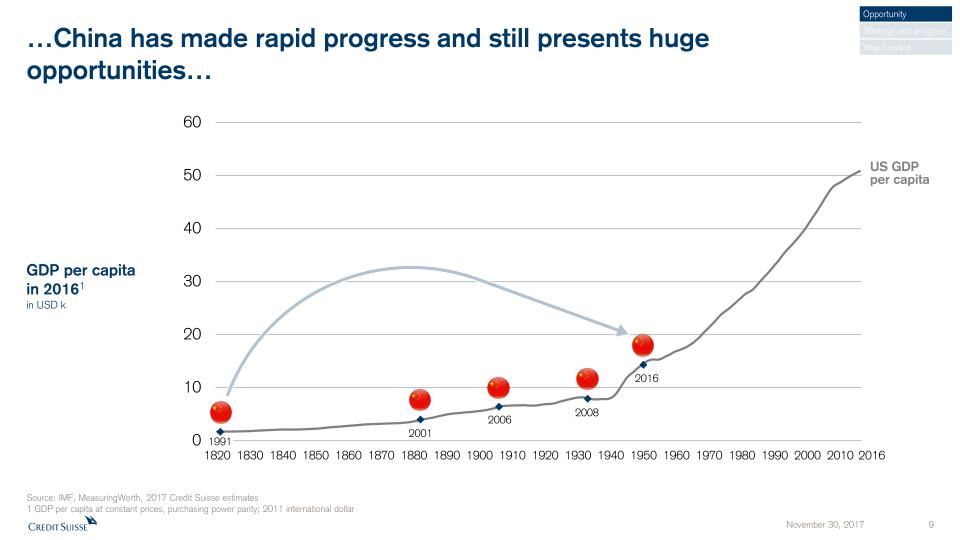

…China has made rapid progress and still presents hugeopportunities… GDP per capitain 20161in USD k Source: IMF, MeasuringWorth, 2017 Credit Suisse estimates1 GDP per capita at constant prices, purchasing power parity; 2011 international dollar US GDP per capita 2016 1991 2001 2006 2008 2016 Opportunity Strategy and progress Way forward

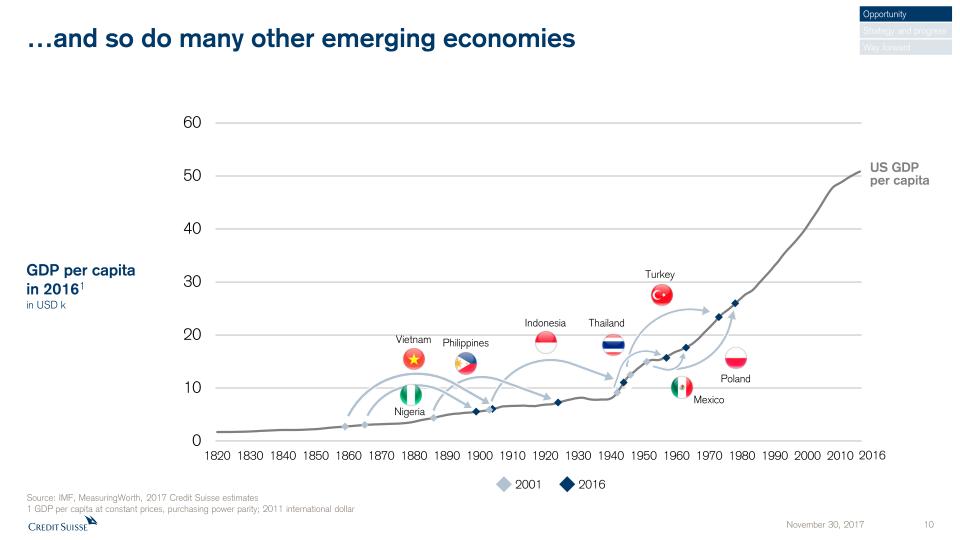

…and so do many other emerging economies GDP per capitain 20161in USD k Source: IMF, MeasuringWorth, 2017 Credit Suisse estimates1 GDP per capita at constant prices, purchasing power parity; 2011 international dollar Vietnam Philippines Thailand 2016 Mexico Nigeria Turkey Poland 2016 2001 Opportunity Strategy and progress Way forward US GDP per capita Indonesia

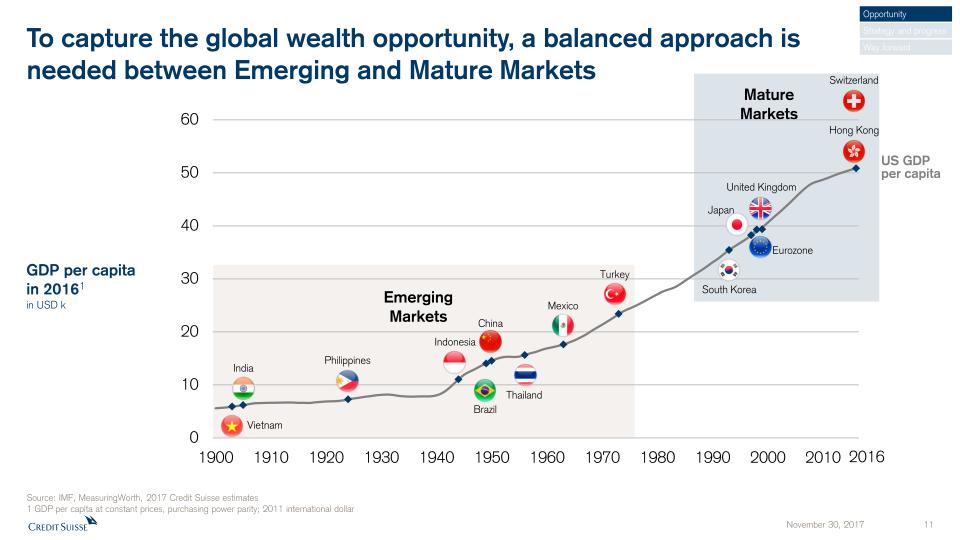

Emerging Markets MatureMarkets To capture the global wealth opportunity, a balanced approach isneeded between Emerging and Mature Markets GDP per capitain 20161in USD k Source: IMF, MeasuringWorth, 2017 Credit Suisse estimates1 GDP per capita at constant prices, purchasing power parity; 2011 international dollar Vietnam India Philippines Indonesia Brazil China Thailand Mexico South Korea Hong Kong Japan United Kingdom Eurozone Switzerland 2016 Turkey Opportunity Strategy and progress Way forward US GDP per capita

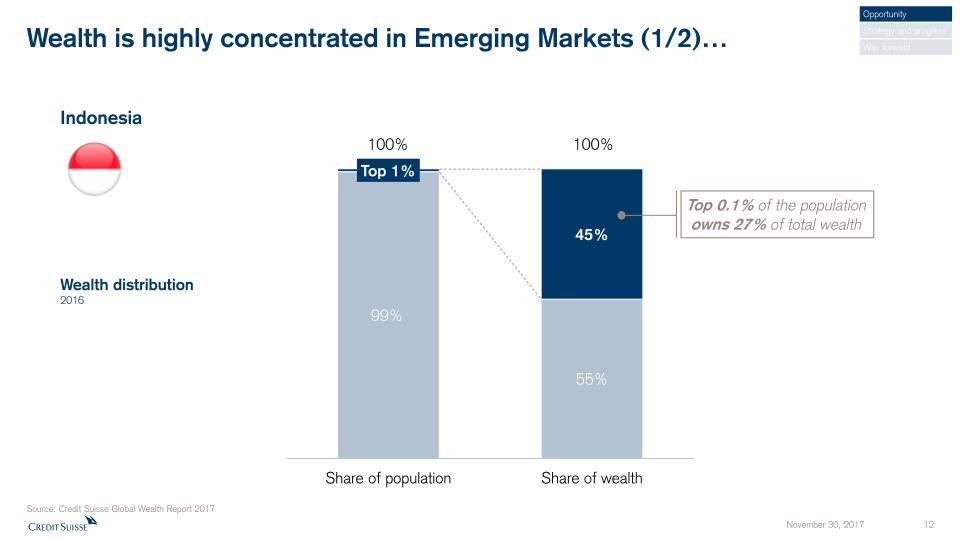

Wealth is highly concentrated in Emerging Markets (1/2)… Source: Credit Suisse Global Wealth Report 2017 Opportunity Strategy and progress Way forward Wealth distribution2016 100% 100% Top 0.1% of the population owns 27% of total wealth Indonesia

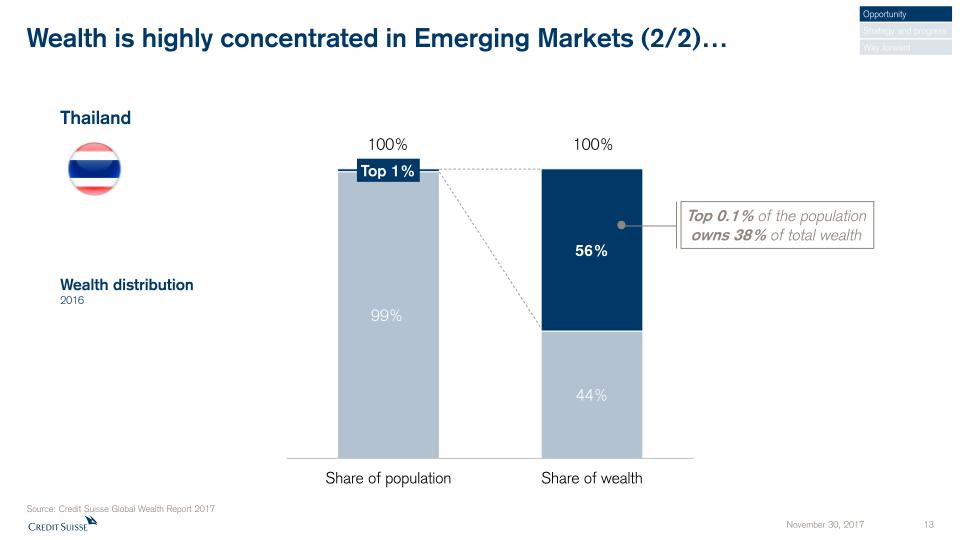

Wealth is highly concentrated in Emerging Markets (2/2)… Thailand Source: Credit Suisse Global Wealth Report 2017 Opportunity Strategy and progress Way forward Wealth distribution2016 100% 100% Top 0.1% of the population owns 38% of total wealth

Astor Ford Gould Vanderbilt Rockefeller Field Carnegie Mellon Weyerhaeuser …as all wealth is created by entrepreneurs Opportunity Strategy and progress Way forward

Wealth creation in Emerging Markets is mostly driven by first andsecond generation entrepreneurs Emerging Markets generational ownership of family-owned companies Source: Credit Suisse Research Institute, “The CS Family 1000” as of September 27, 2017 Opportunity Strategy and progress Way forward

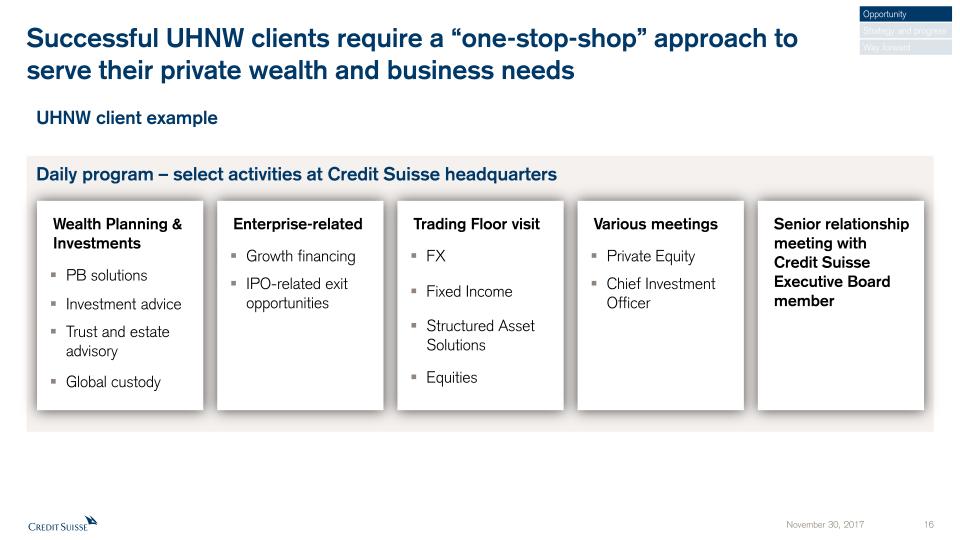

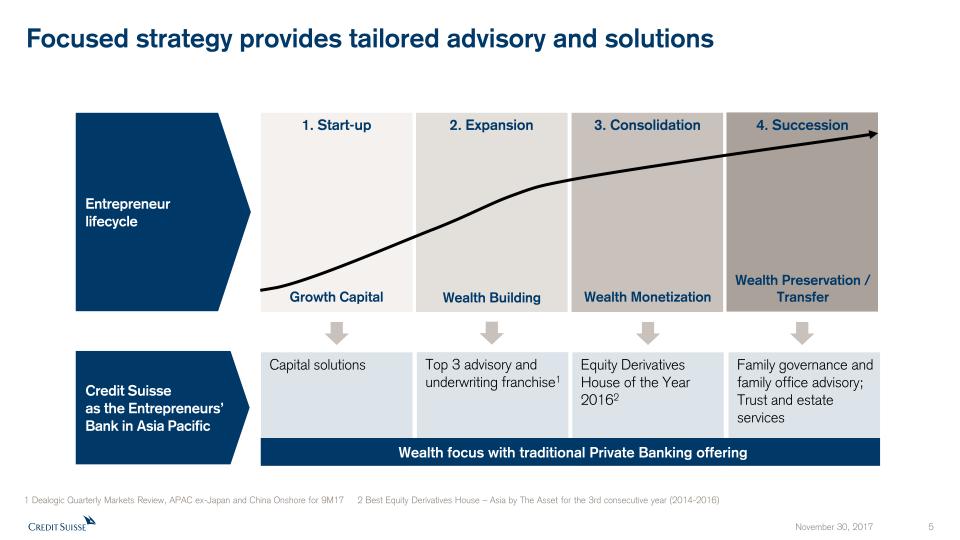

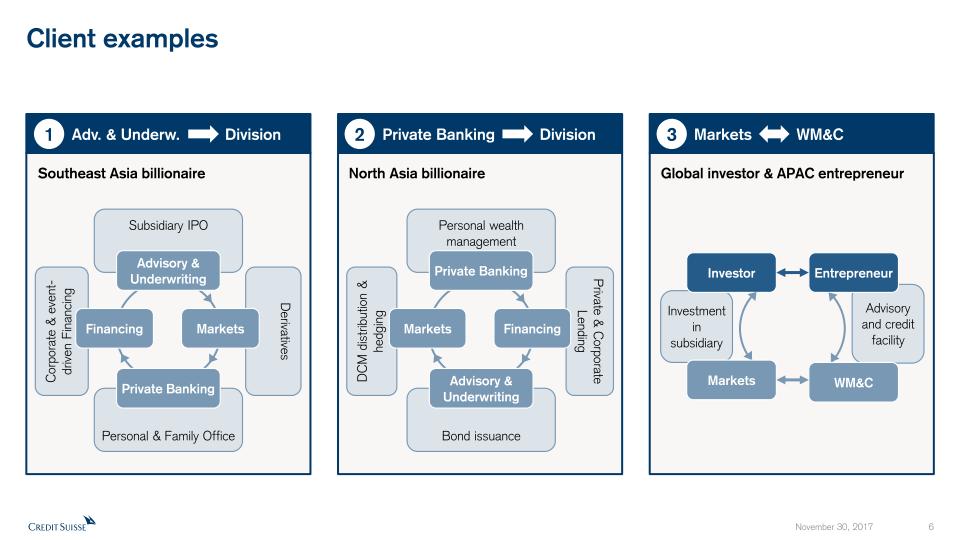

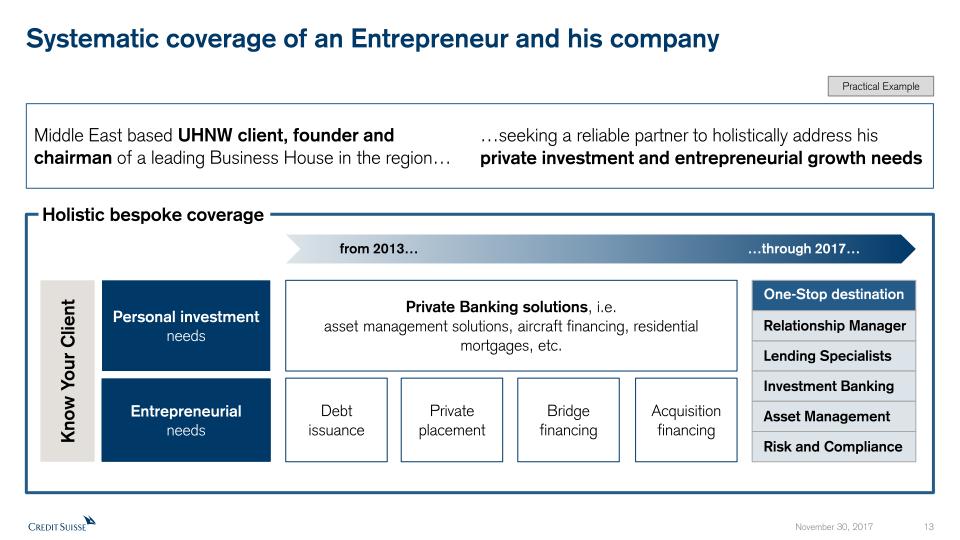

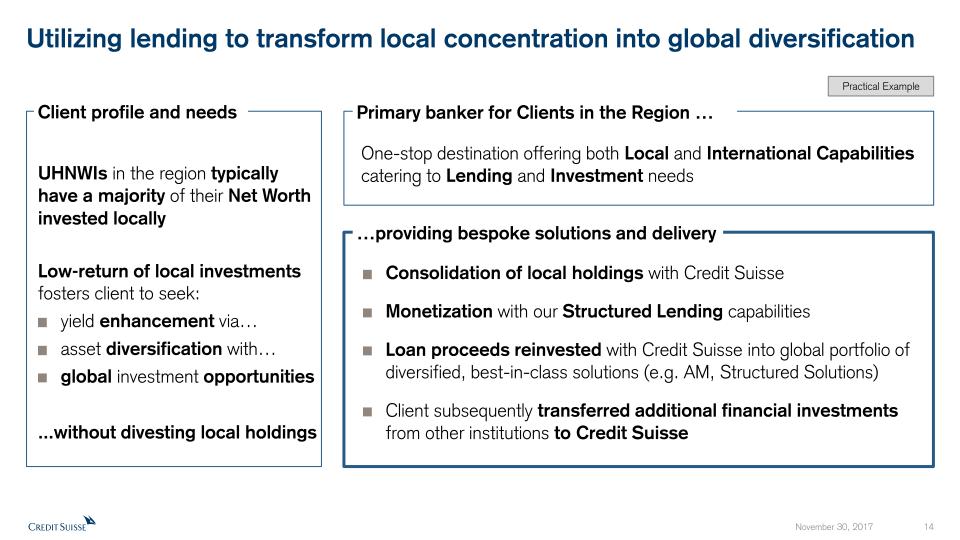

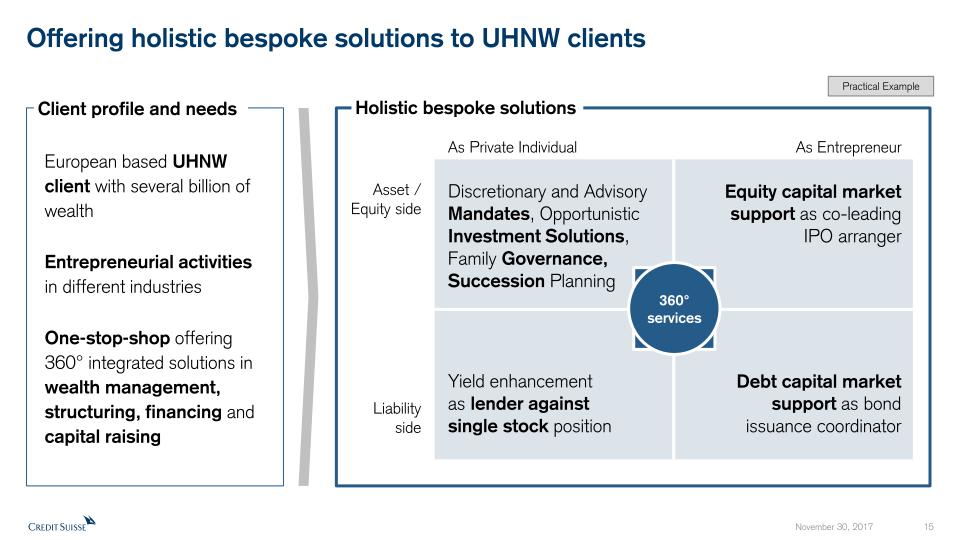

Successful UHNW clients require a “one-stop-shop” approach toserve their private wealth and business needs Daily program – select activities at Credit Suisse headquarters UHNW client example Trading Floor visitFXFixed IncomeStructured Asset SolutionsEquities Senior relationship meeting withCredit Suisse Executive Board member Various meetingsPrivate EquityChief Investment Officer Wealth Planning & InvestmentsPB solutionsInvestment adviceTrust and estate advisoryGlobal custody Enterprise-relatedGrowth financingIPO-related exit opportunities Opportunity Strategy and progress Way forward

Quality of execution is key Long-term trusted relationships, based on history, heritage, discretion and confidentialityRecruitment and retention of top-notch RMsBroad and deep investment and advisory offeringBest-in-class global execution and capital markets, advisory and financing capabilitiesFocus on sustainability and impact investingProactive management of wealth transfer across generationsState-of-the-art digital capabilities Opportunity Strategy and progress Way forward

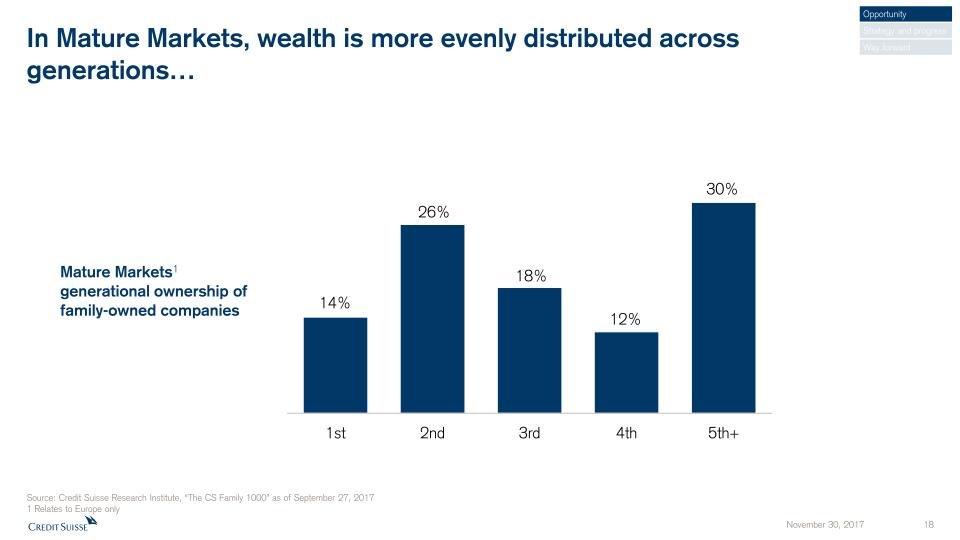

Mature Markets1generational ownership of family-owned companies In Mature Markets, wealth is more evenly distributed acrossgenerations… Source: Credit Suisse Research Institute, “The CS Family 1000” as of September 27, 20171 Relates to Europe only Opportunity Strategy and progress Way forward

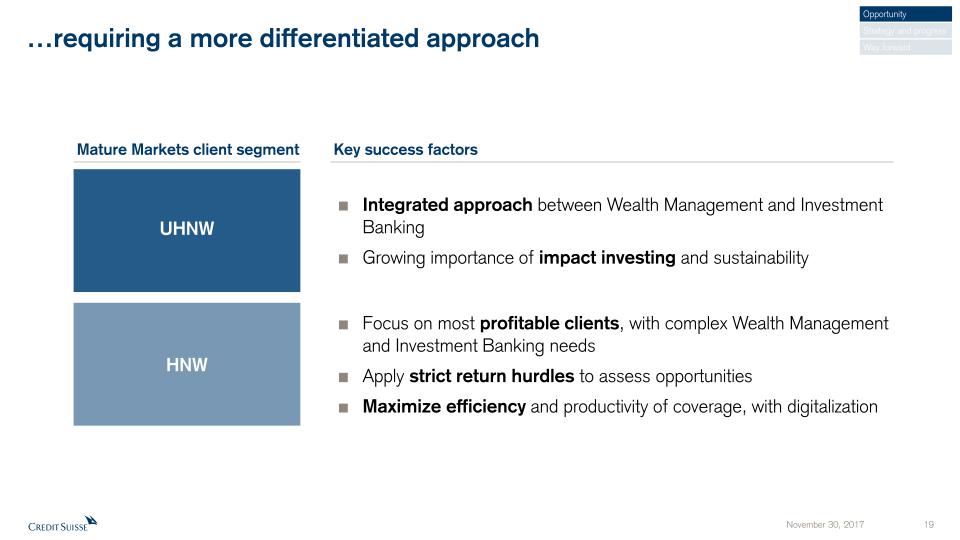

…requiring a more differentiated approach UHNW Integrated approach between Wealth Management and Investment BankingGrowing importance of impact investing and sustainability HNW Mature Markets client segment Key success factors Focus on most profitable clients, with complex Wealth Management and Investment Banking needsApply strict return hurdles to assess opportunitiesMaximize efficiency and productivity of coverage, with digitalization Opportunity Strategy and progress Way forward

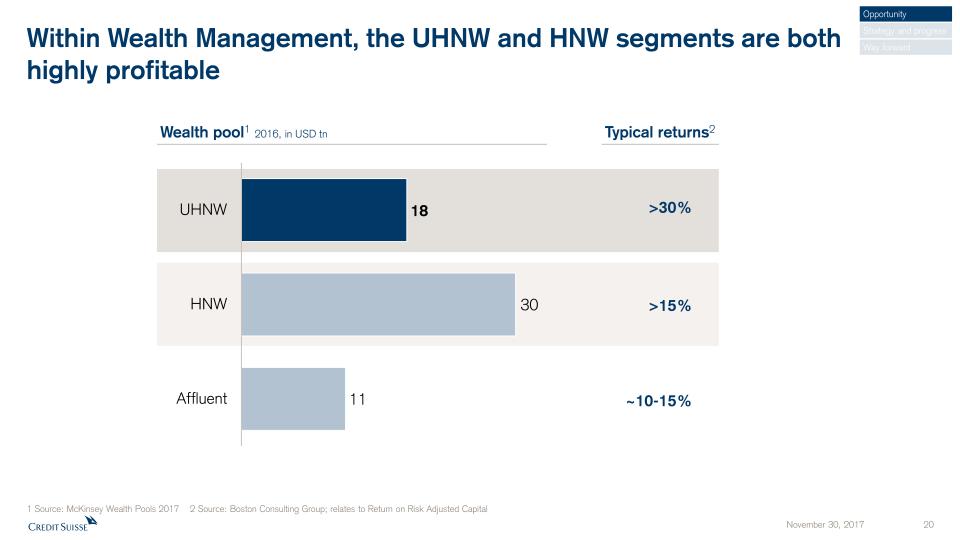

Within Wealth Management, the UHNW and HNW segments are bothhighly profitable 1 Source: McKinsey Wealth Pools 2017 2 Source: Boston Consulting Group; relates to Return on Risk Adjusted Capital ~10-15% >15% Wealth pool1 2016, in USD tn Typical returns2 >30% Opportunity Strategy and progress Way forward

Our strategy A leading Wealth Manager… …with strong Investment Banking capabilities Opportunity Strategy and progress Way forward

Delivering against our objectives Costs Reduce our cost base Risk Right-size and de-risk our Global Markets activities Capital Strengthen our capital position Legacy Resolve legacy issues and wind-down the SRU Growth Deliver profitable growth and generate capital organically Opportunity Strategy and progress Way forward

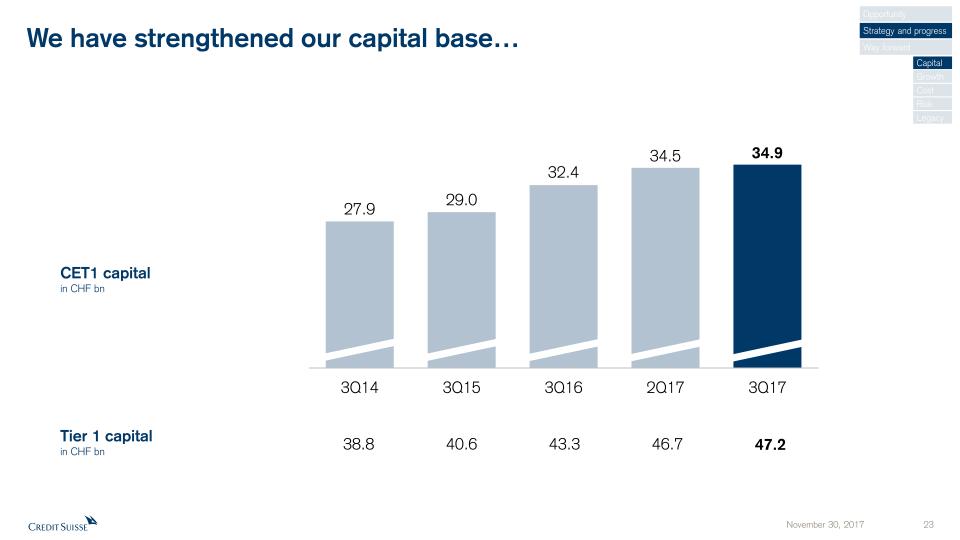

We have strengthened our capital base… CET1 capital in CHF bn 40.6 Tier 1 capitalin CHF bn 43.3 47.2 38.8 46.7 Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

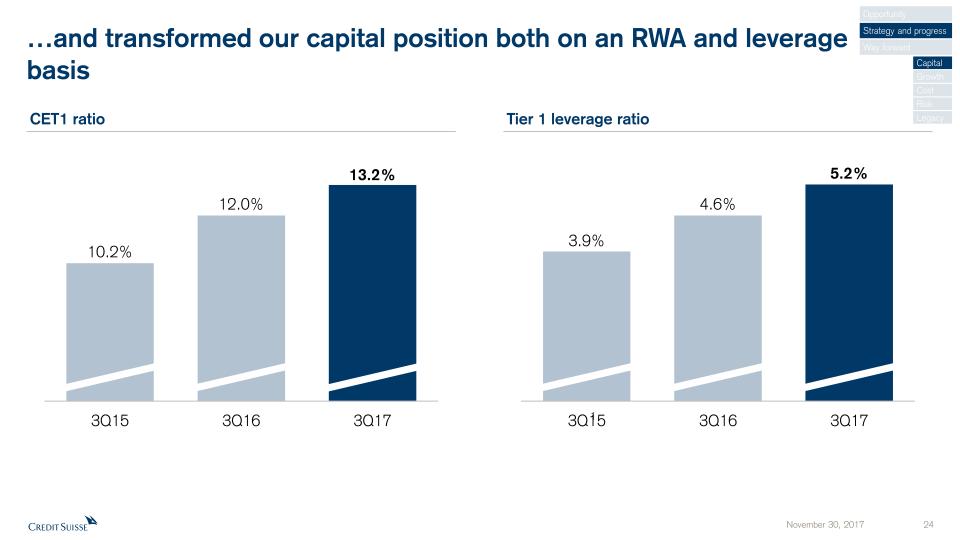

…and transformed our capital position both on an RWA and leveragebasis CET1 ratio Tier 1 leverage ratio 1 Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

We are allocating increasing amounts of capital towards Wealth Management and IBCM as we right-size our Markets activities… 1 Includes Global Markets, APAC Markets and SRU. SRU excludes operational risk RWA of CHF 19 bn in 2Q15 and CHF 20 bn in 3Q17 SUB, IWM, APAC WM&C and IBCM RWA in CHF bn Markets activities RWA1 in CHF bn -33% +20% Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

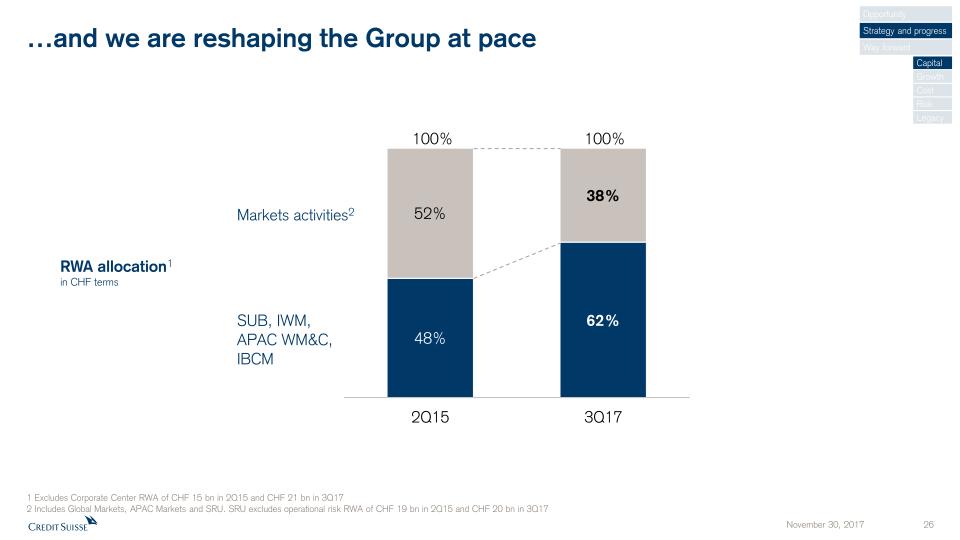

…and we are reshaping the Group at pace 1 Excludes Corporate Center RWA of CHF 15 bn in 2Q15 and CHF 21 bn in 3Q172 Includes Global Markets, APAC Markets and SRU. SRU excludes operational risk RWA of CHF 19 bn in 2Q15 and CHF 20 bn in 3Q17 SUB, IWM, APAC WM&C, IBCM Markets activities2 RWA allocation1in CHF terms 100% 100% Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

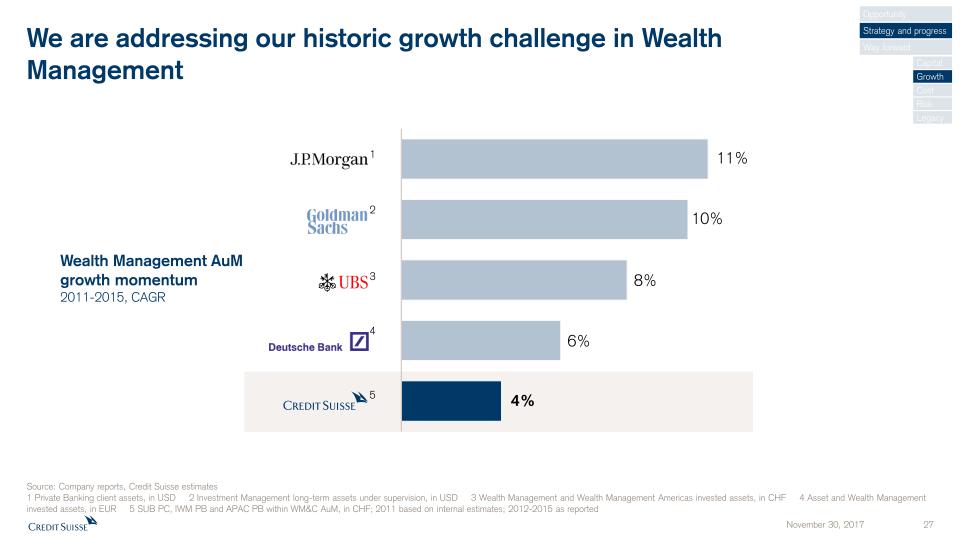

We are addressing our historic growth challenge in WealthManagement Wealth Management AuMgrowth momentum2011-2015, CAGR 1 2 4 3 5 Source: Company reports, Credit Suisse estimates1 Private Banking client assets, in USD 2 Investment Management long-term assets under supervision, in USD 3 Wealth Management and Wealth Management Americas invested assets, in CHF 4 Asset and Wealth Management invested assets, in EUR 5 SUB PC, IWM PB and APAC PB within WM&C AuM, in CHF; 2011 based on internal estimates; 2012-2015 as reported Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

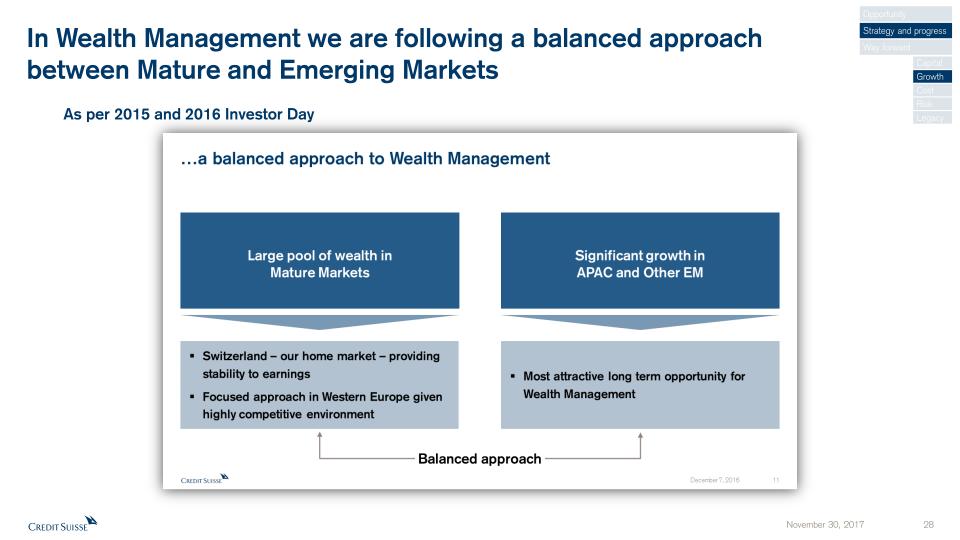

In Wealth Management we are following a balanced approachbetween Mature and Emerging Markets As per 2015 and 2016 Investor Day Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

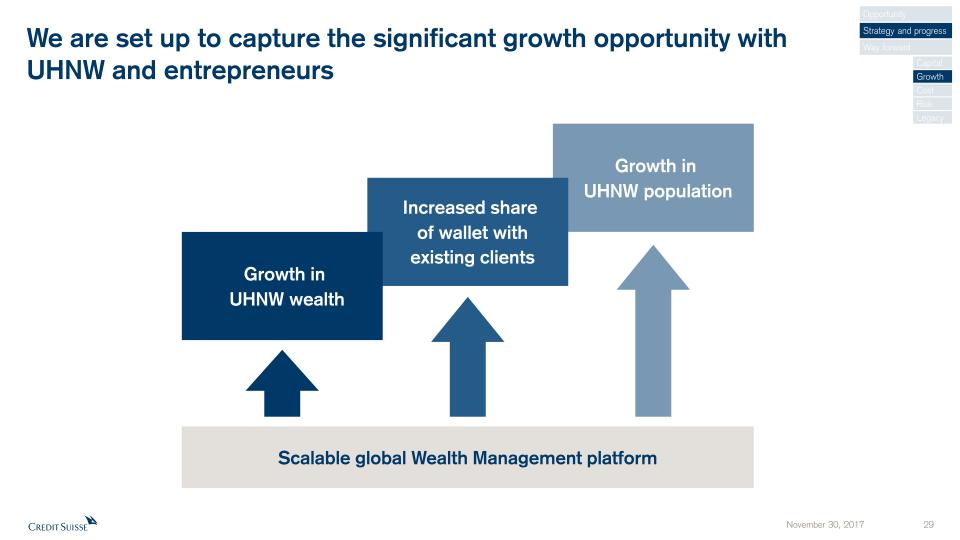

We are set up to capture the significant growth opportunity withUHNW and entrepreneurs Scalable global Wealth Management platform Growth in UHNW population Increased share of wallet withexisting clients Growth in UHNW wealth Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

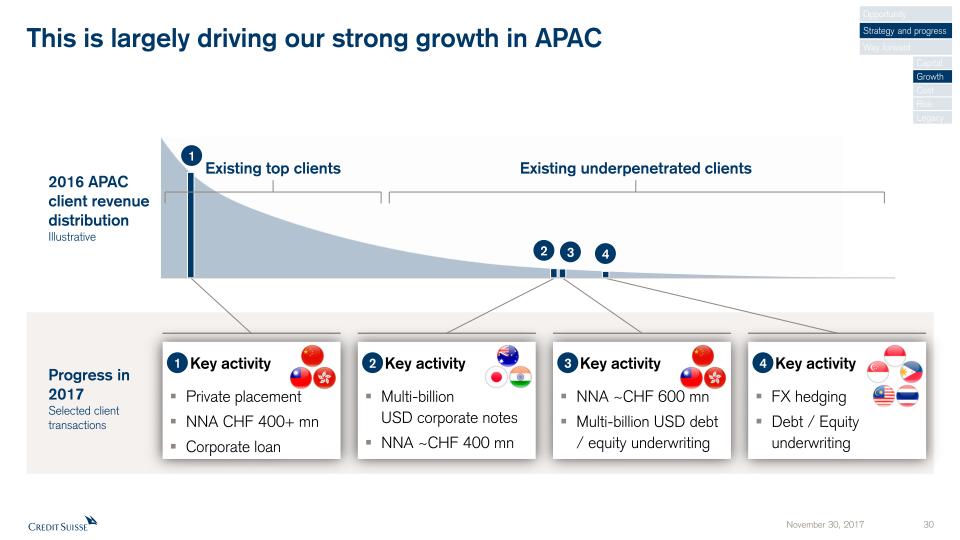

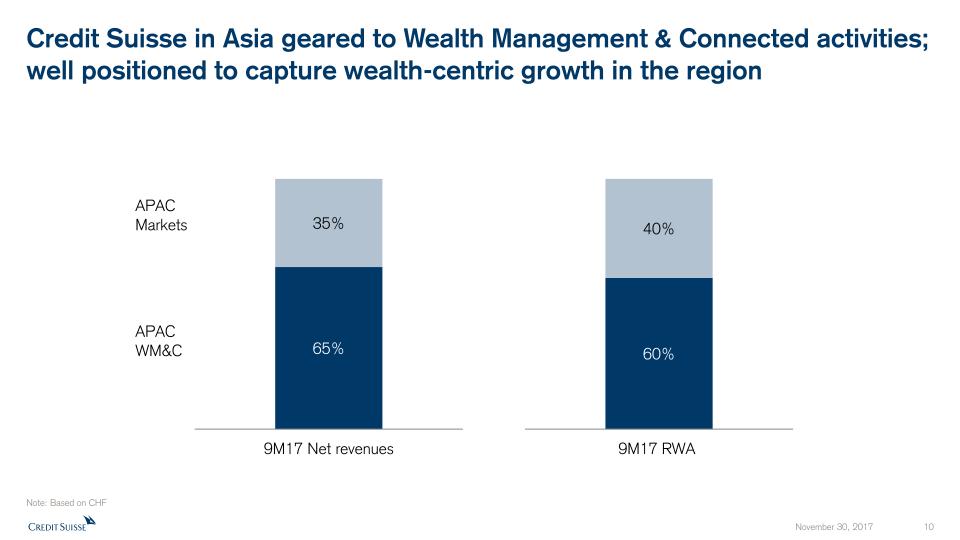

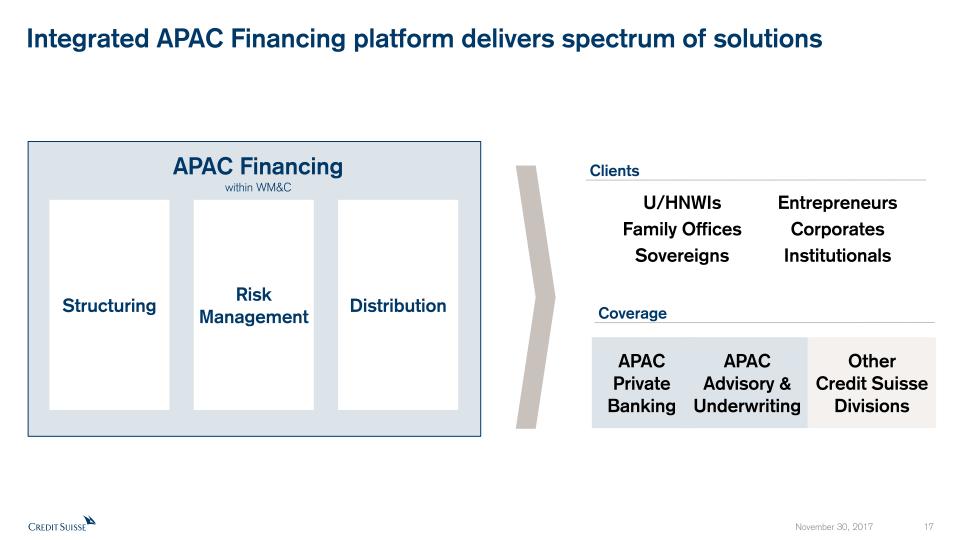

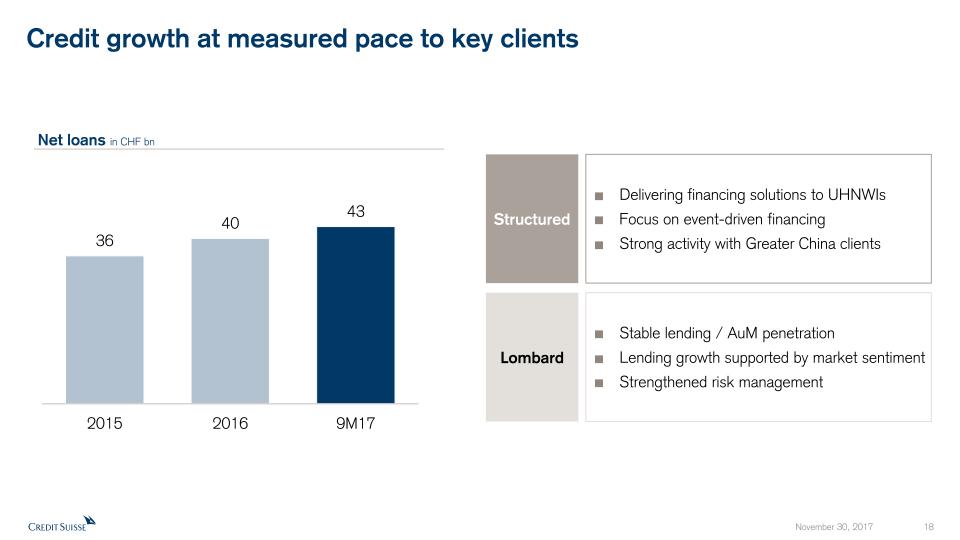

2016 APAC client revenue distributionIllustrative Multi-billionUSD corporate notesNNA ~CHF 400 mn This is largely driving our strong growth in APAC FX hedgingDebt / Equity underwriting NNA ~CHF 600 mnMulti-billion USD debt / equity underwriting Private placementNNA CHF 400+ mnCorporate loan Progress in 2017Selected client transactions Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy 2 3 4 Existing underpenetrated clients Existing top clients 1 1 2 3 4 Key activity Key activity Key activity Key activity

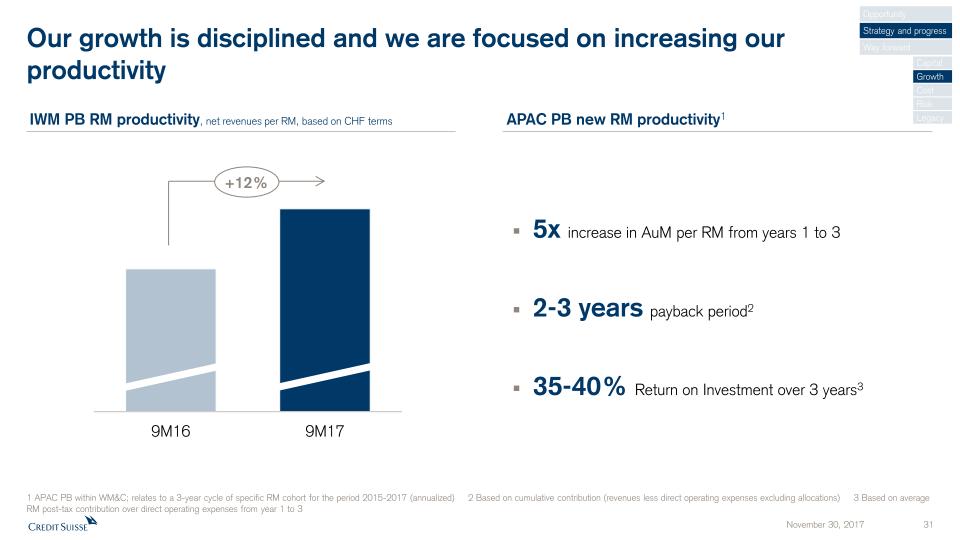

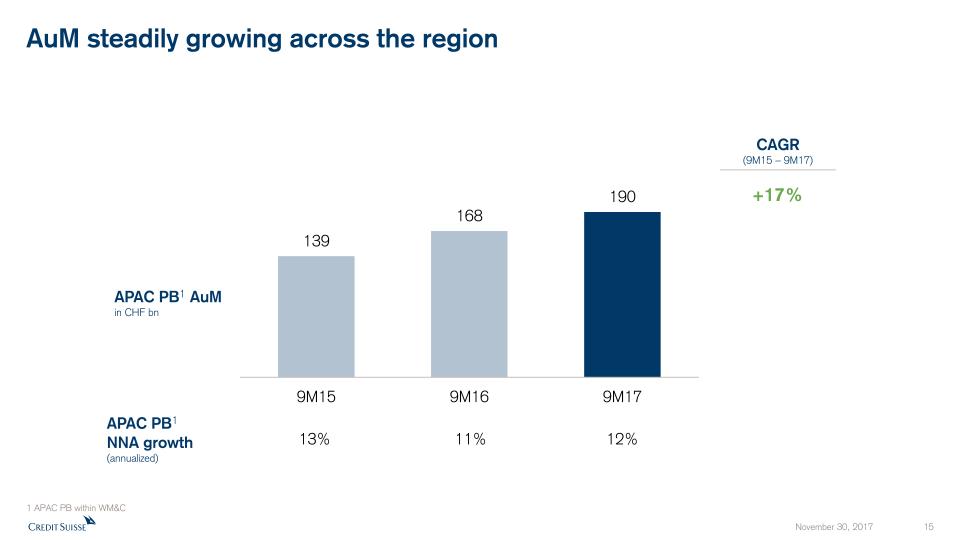

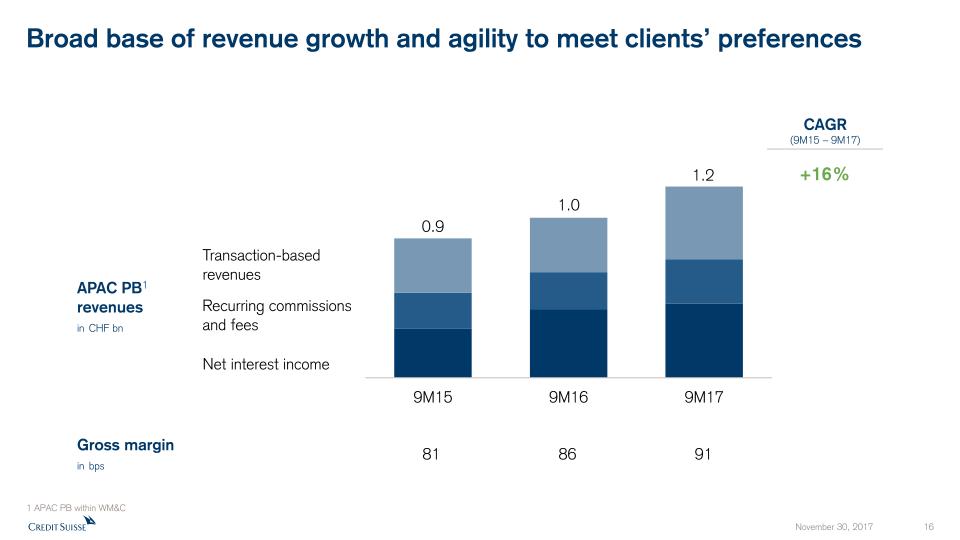

Our growth is disciplined and we are focused on increasing ourproductivity APAC PB new RM productivity1 IWM PB RM productivity, net revenues per RM, based on CHF terms +12% 1 APAC PB within WM&C; relates to a 3-year cycle of specific RM cohort for the period 2015-2017 (annualized) 2 Based on cumulative contribution (revenues less direct operating expenses excluding allocations) 3 Based on average RM post-tax contribution over direct operating expenses from year 1 to 3 5x increase in AuM per RM from years 1 to 32-3 years payback period235-40% Return on Investment over 3 years3 Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

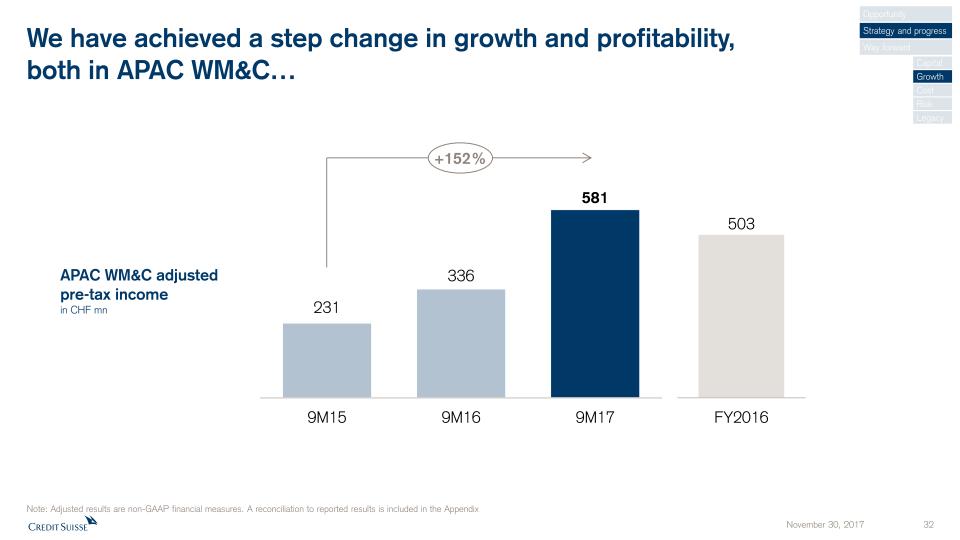

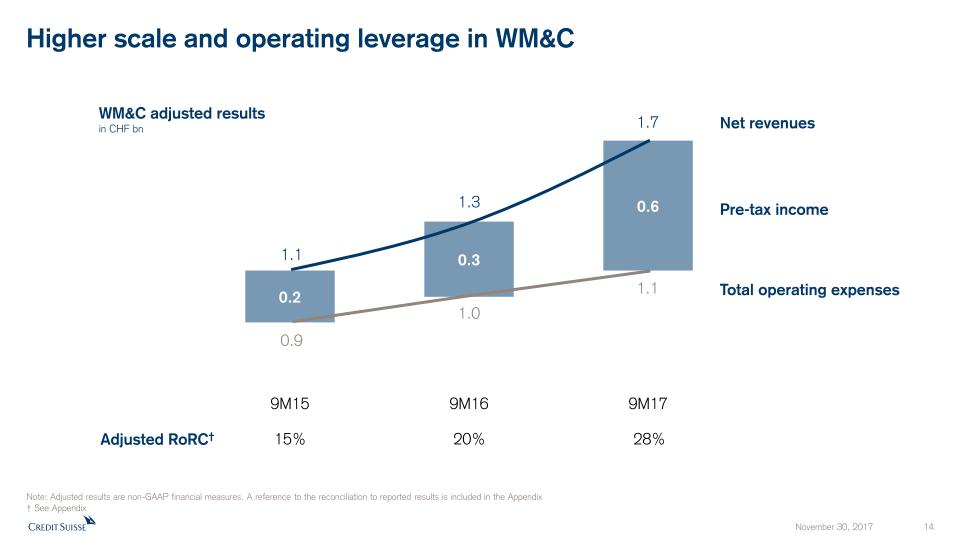

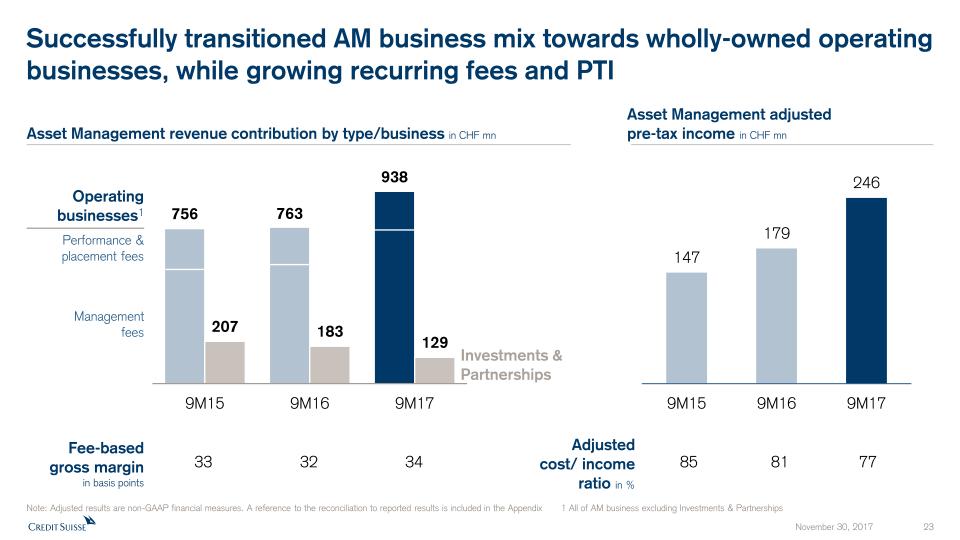

We have achieved a step change in growth and profitability,both in APAC WM&C… Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix +152% APAC WM&C adjustedpre-tax incomein CHF mn Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

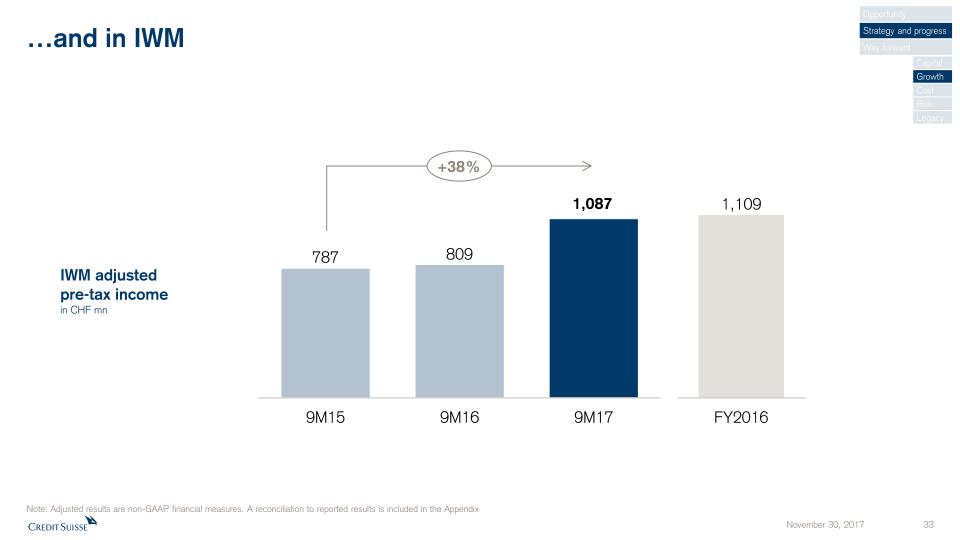

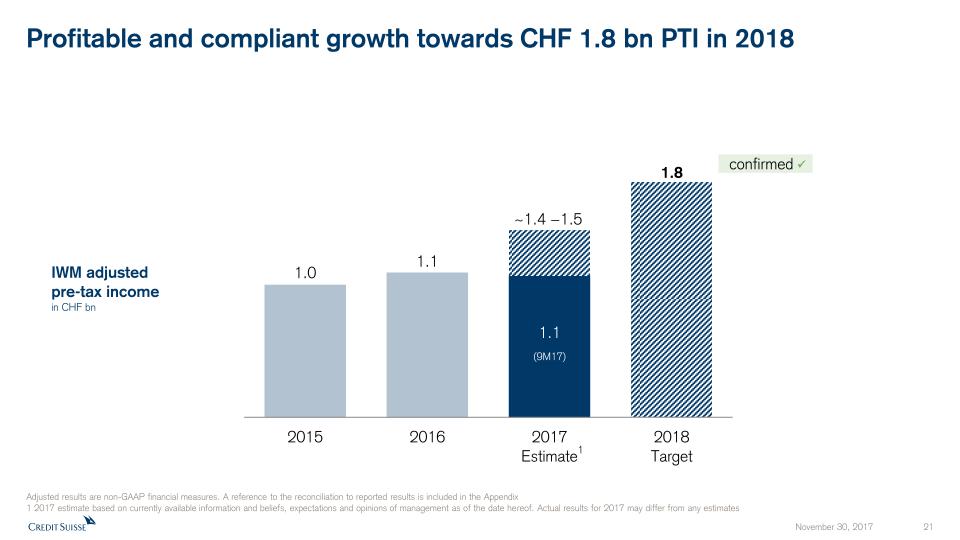

…and in IWM Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix +38% IWM adjustedpre-tax incomein CHF mn Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

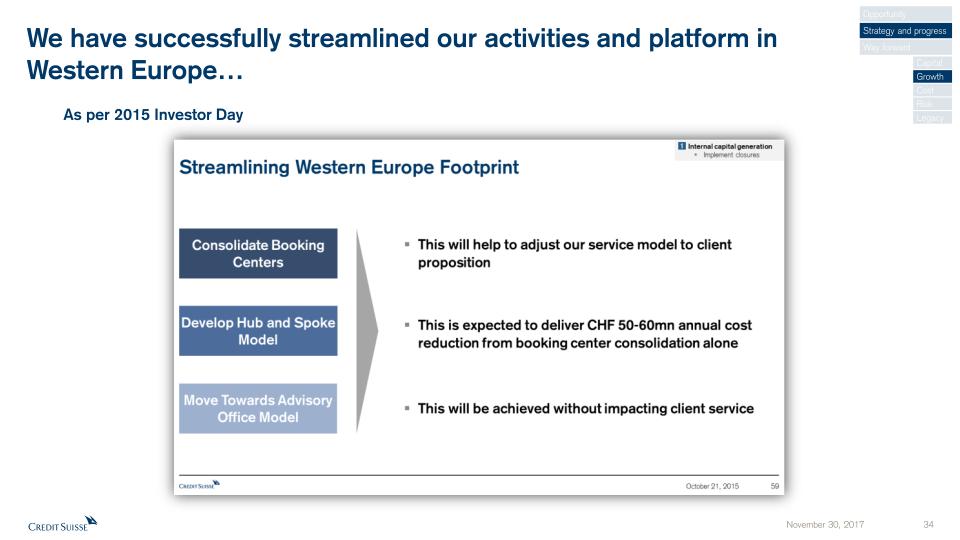

We have successfully streamlined our activities and platform inWestern Europe… Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy As per 2015 Investor Day

positive negative …and returned to profitability through positive operating leverage… Revenues Operating expenses Pre-tax income IWM Europepre-tax incomein CHF mn 9M16 9M17 -12% +13% Opportunity Strategy and progress Way forward + >100 mn Capital Growth Cost Risk Legacy

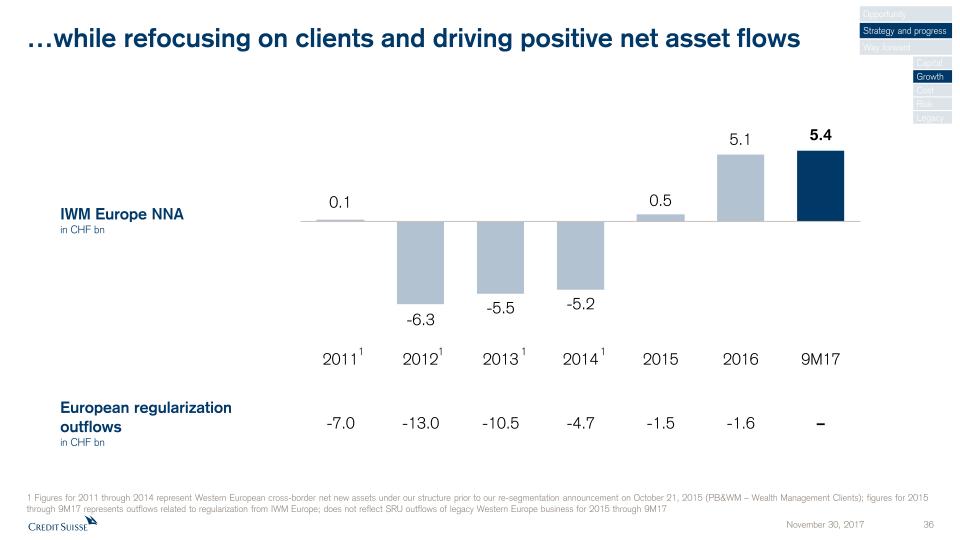

…while refocusing on clients and driving positive net asset flows European regularization outflowsin CHF bn IWM Europe NNAin CHF bn 1 1 1 1 -13.0 -7.0 -10.5 -4.7 -1.5 -1.6 – 1 Figures for 2011 through 2014 represent Western European cross-border net new assets under our structure prior to our re-segmentation announcement on October 21, 2015 (PB&WM – Wealth Management Clients); figures for 2015 through 9M17 represents outflows related to regularization from IWM Europe; does not reflect SRU outflows of legacy Western Europe business for 2015 through 9M17 Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

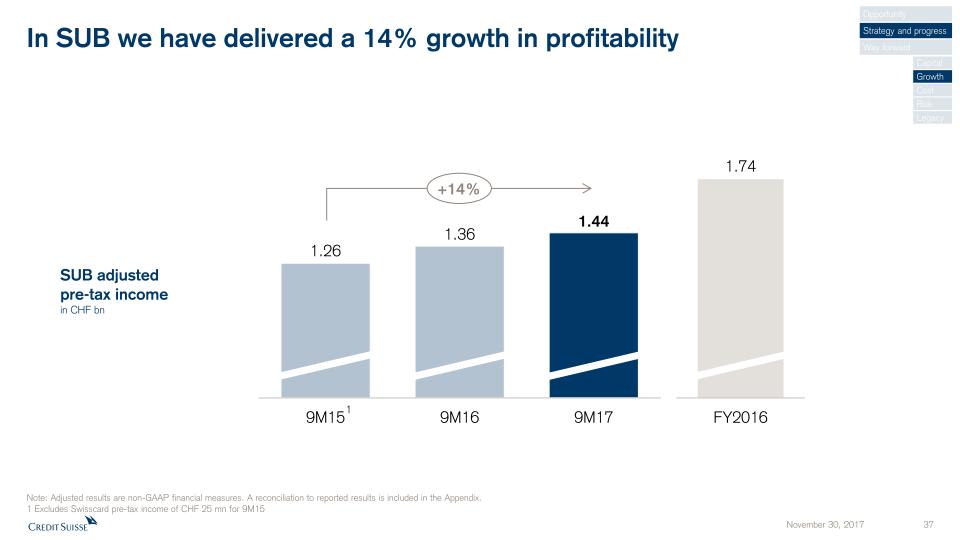

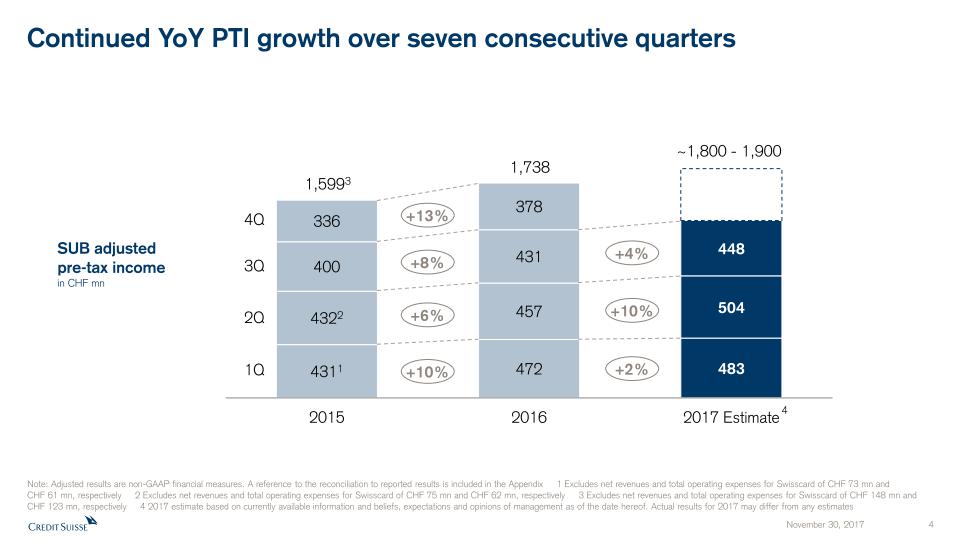

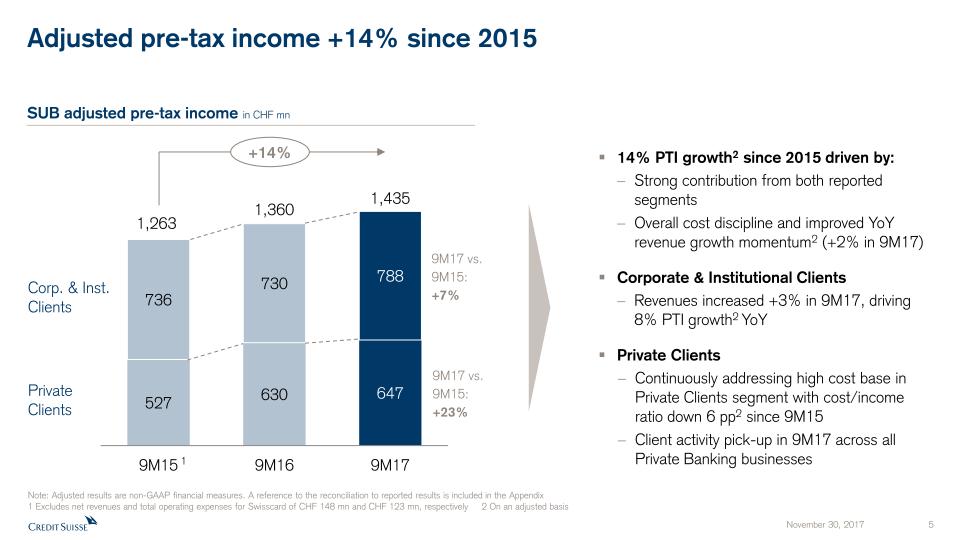

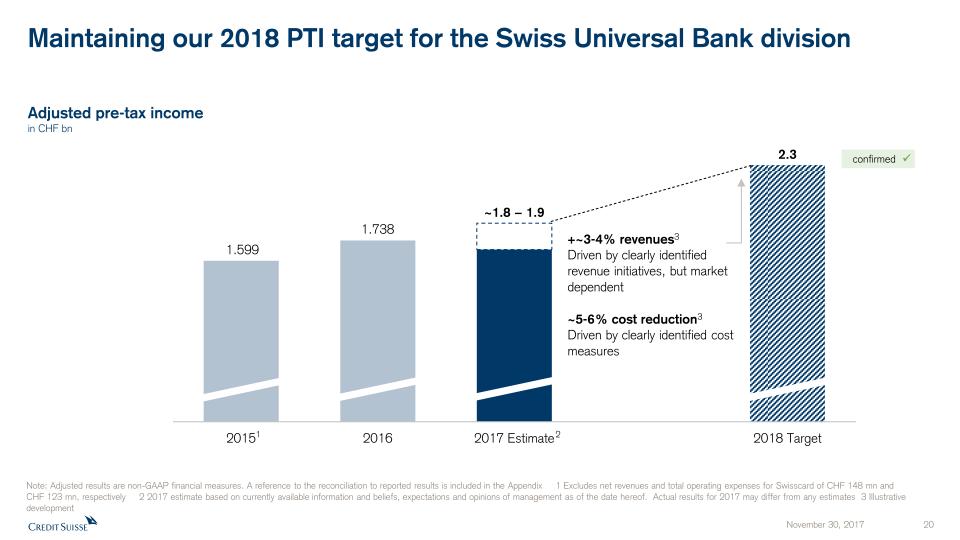

In SUB we have delivered a 14% growth in profitability Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix. 1 Excludes Swisscard pre-tax income of CHF 25 mn for 9M15 1 SUB adjustedpre-tax incomein CHF bn +14% Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

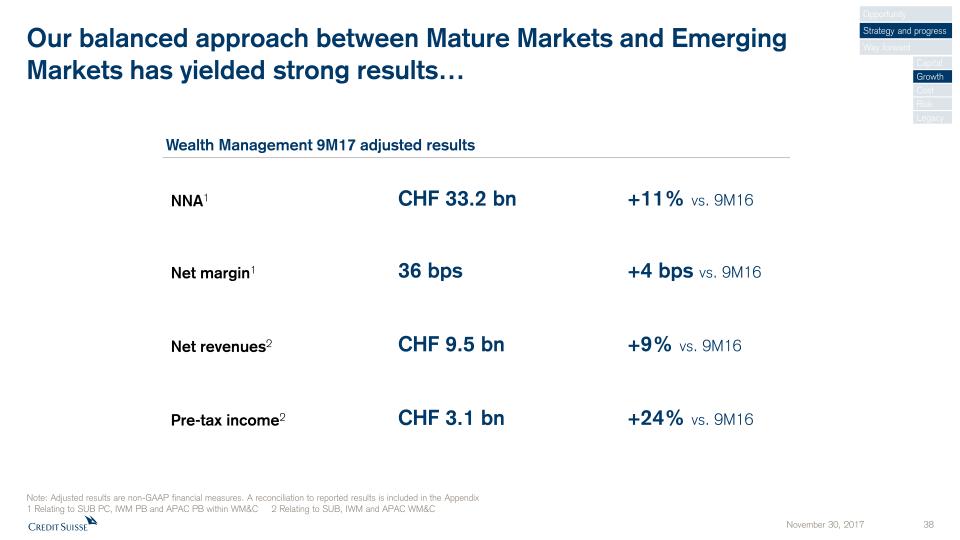

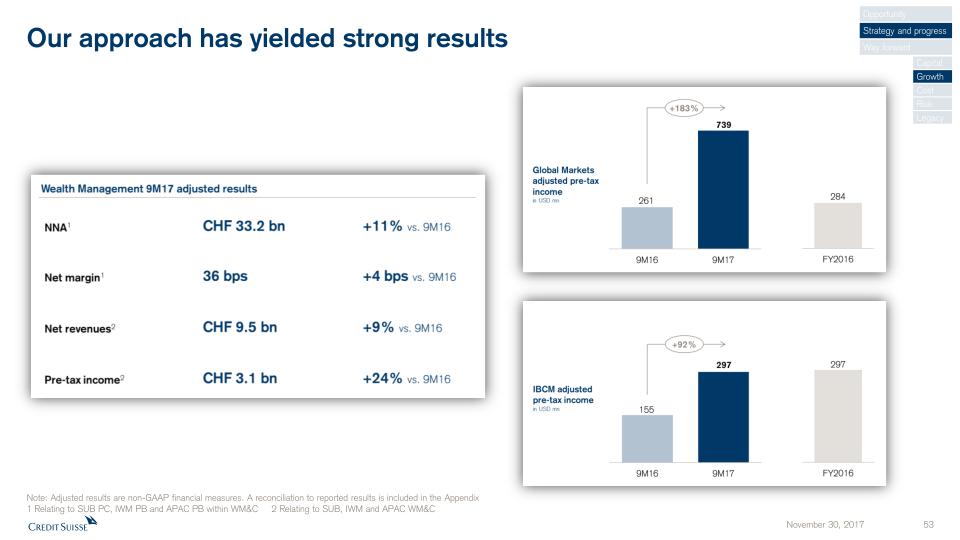

Our balanced approach between Mature Markets and EmergingMarkets has yielded strong results… Net margin1 Net revenues2 NNA1 CHF 33.2 bn 36 bps +9% vs. 9M16 Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix1 Relating to SUB PC, IWM PB and APAC PB within WM&C 2 Relating to SUB, IWM and APAC WM&C CHF 9.5 bn Wealth Management 9M17 adjusted results +4 bps vs. 9M16 +11% vs. 9M16 Pre-tax income2 +24% vs. 9M16 CHF 3.1 bn Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

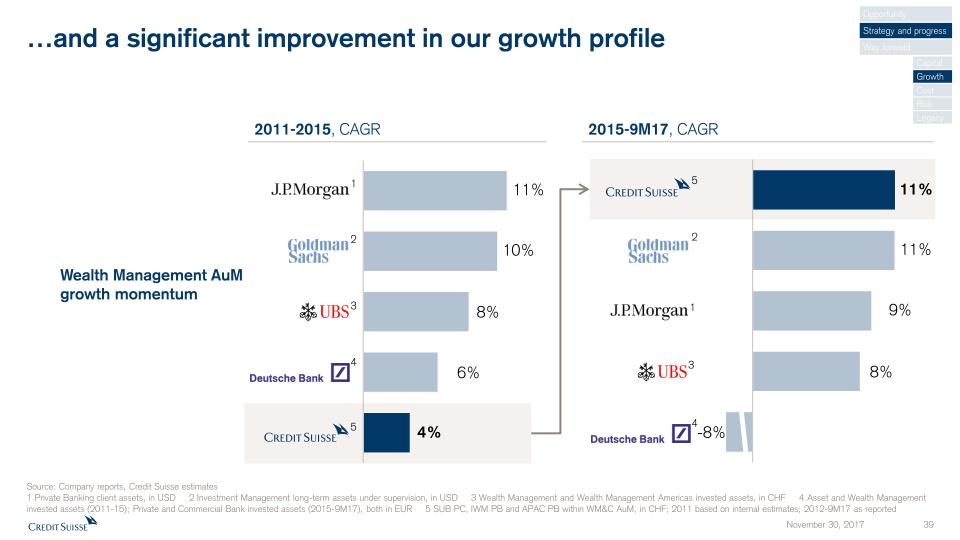

…and a significant improvement in our growth profile Wealth Management AuMgrowth momentum 2011-2015, CAGR 2015-9M17, CAGR 1 2 4 3 5 5 3 2 4 1 Source: Company reports, Credit Suisse estimates1 Private Banking client assets, in USD 2 Investment Management long-term assets under supervision, in USD 3 Wealth Management and Wealth Management Americas invested assets, in CHF 4 Asset and Wealth Management invested assets (2011-15); Private and Commercial Bank invested assets (2015-9M17), both in EUR 5 SUB PC, IWM PB and APAC PB within WM&C AuM, in CHF; 2011 based on internal estimates; 2012-9M17 as reported Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

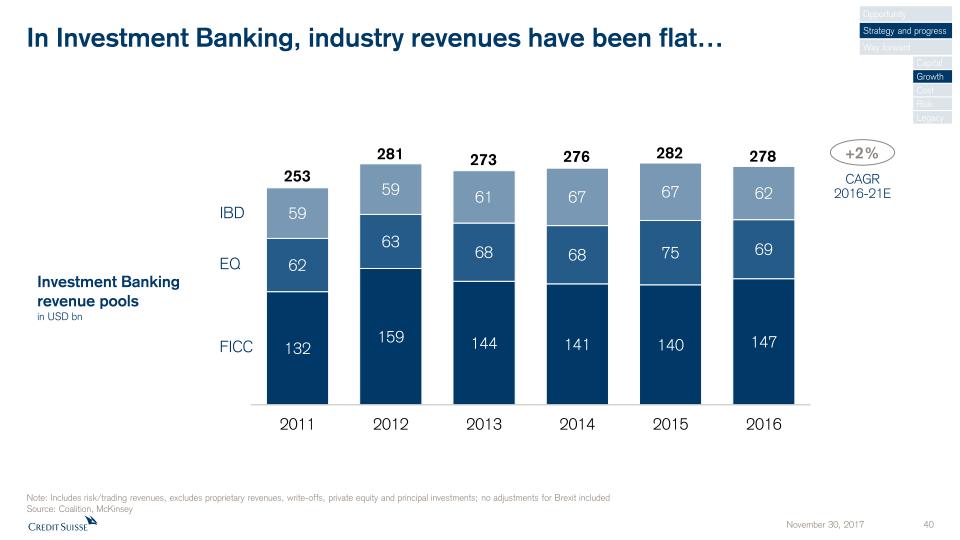

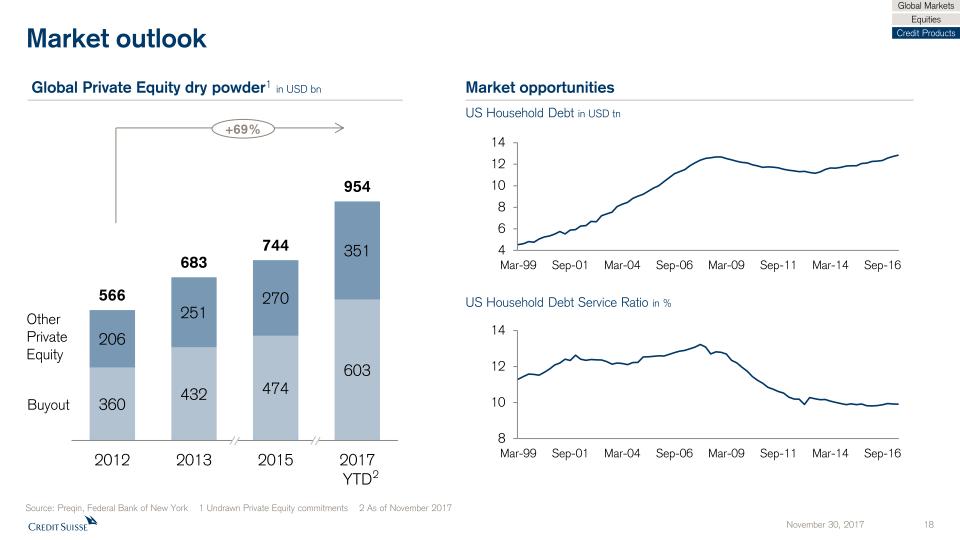

In Investment Banking, industry revenues have been flat… Note: Includes risk/trading revenues, excludes proprietary revenues, write-offs, private equity and principal investments; no adjustments for Brexit includedSource: Coalition, McKinsey Investment Banking revenue poolsin USD bn FICC IBD EQ +2% 253 281 273 276 282 278 CAGR2016-21E Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

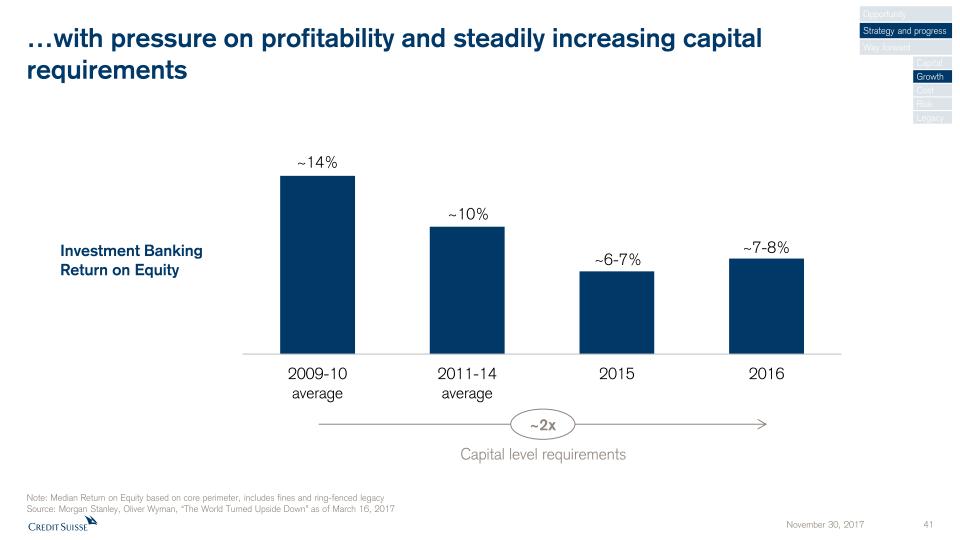

…with pressure on profitability and steadily increasing capitalrequirements Note: Median Return on Equity based on core perimeter, includes fines and ring-fenced legacySource: Morgan Stanley, Oliver Wyman, “The World Turned Upside Down” as of March 16, 2017 Investment BankingReturn on Equity ~2x Capital level requirements Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

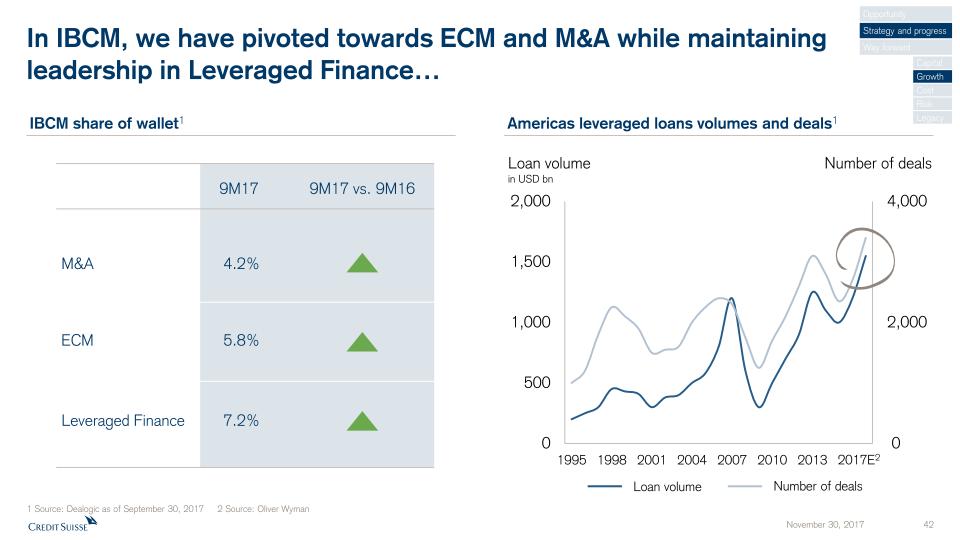

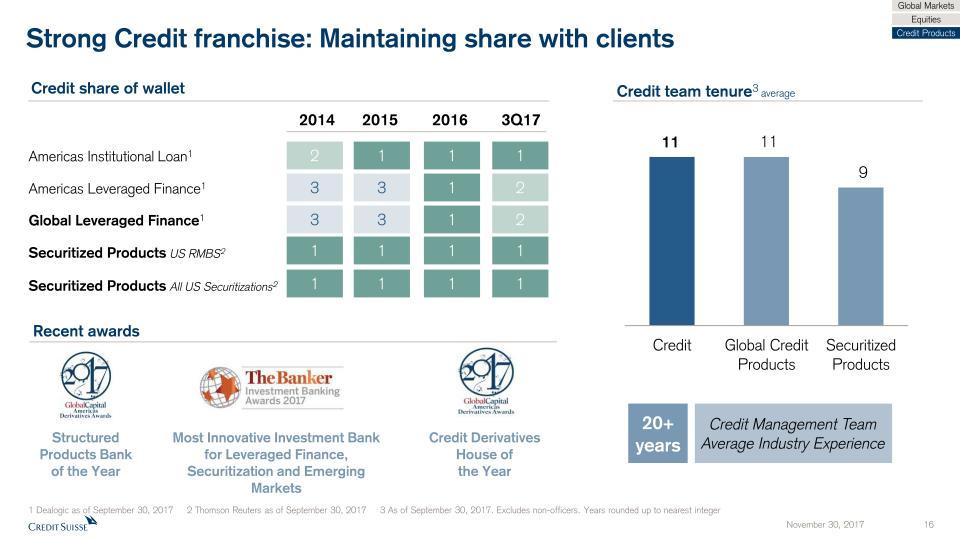

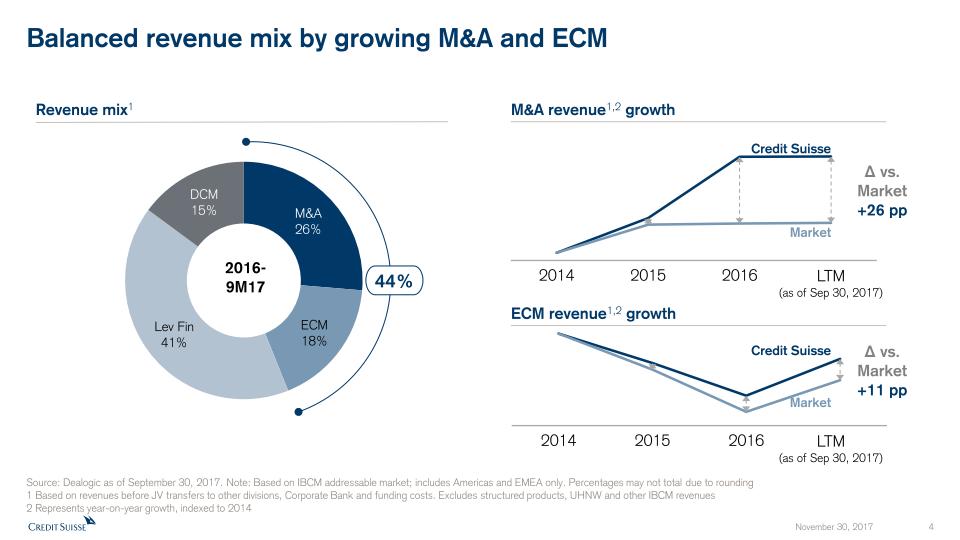

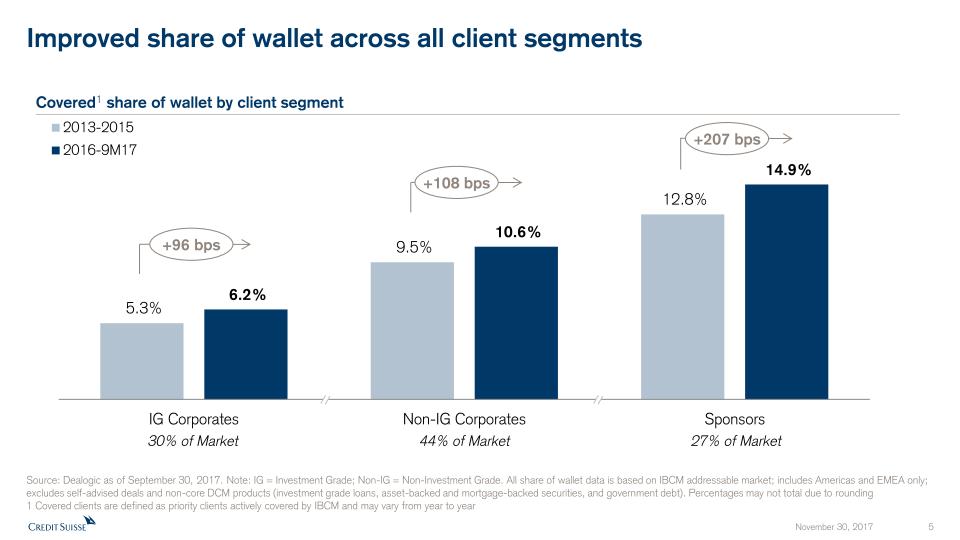

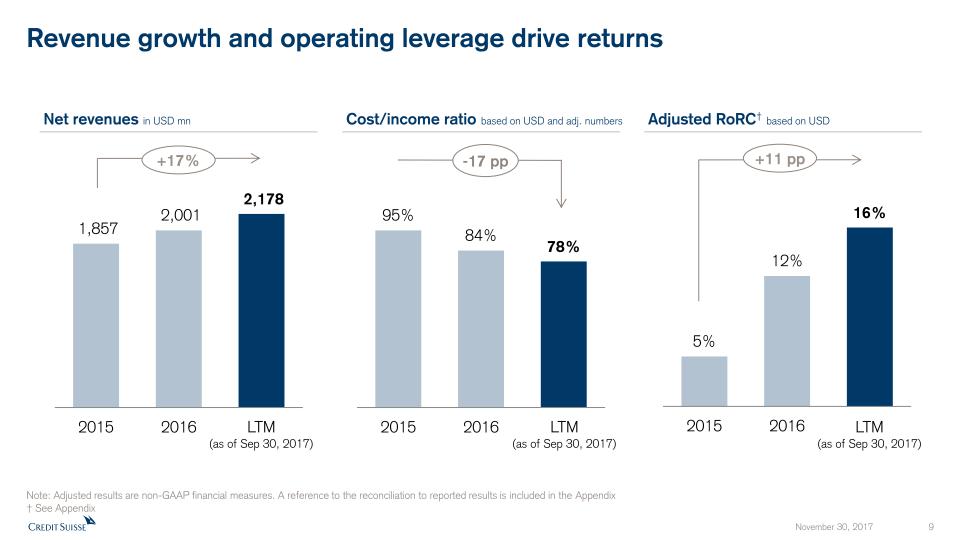

In IBCM, we have pivoted towards ECM and M&A while maintaining leadership in Leveraged Finance… M&A ECM Leveraged Finance 9M17 vs. 9M16 Americas leveraged loans volumes and deals1 IBCM share of wallet1 9M17 4.2% 5.8% 7.2% 1 Source: Dealogic as of September 30, 2017 2 Source: Oliver Wyman Loan volume in USD bn Number of deals Number of deals Loan volume Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy 2017E2

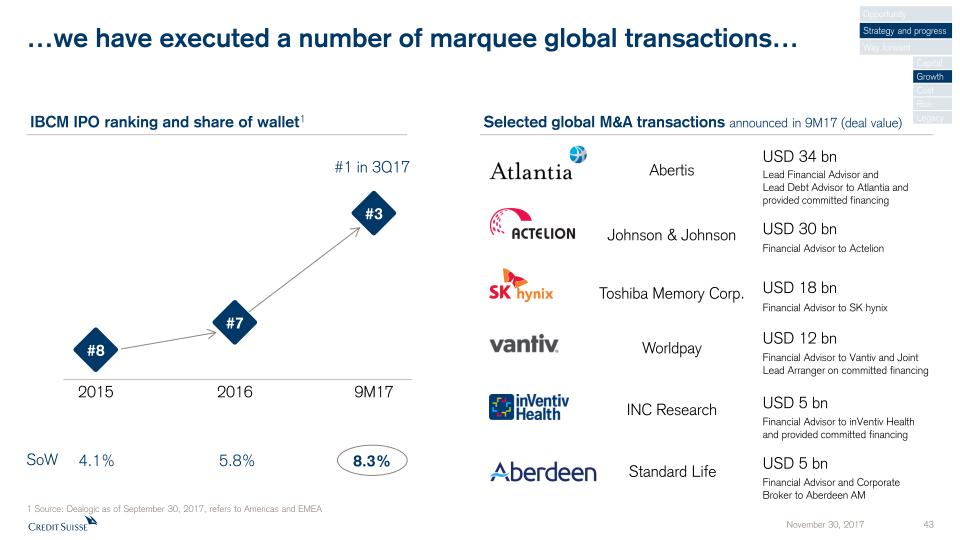

…we have executed a number of marquee global transactions… Selected global M&A transactions announced in 9M17 (deal value) IBCM IPO ranking and share of wallet1 1 Source: Dealogic as of September 30, 2017, refers to Americas and EMEA SoW 8.3% 5.8% 4.1% #1 in 3Q17 Abertis USD 34 bn Lead Financial Advisor and Lead Debt Advisor to Atlantia andprovided committed financing USD 30 bn Financial Advisor to Actelion INC Research USD 5 bn Financial Advisor to inVentiv Health and provided committed financing USD 5 bn Financial Advisor and Corporate Broker to Aberdeen AM Johnson & Johnson Standard Life Worldpay USD 12 bn Financial Advisor to Vantiv and Joint Lead Arranger on committed financing Toshiba Memory Corp. USD 18 bn Financial Advisor to SK hynix Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

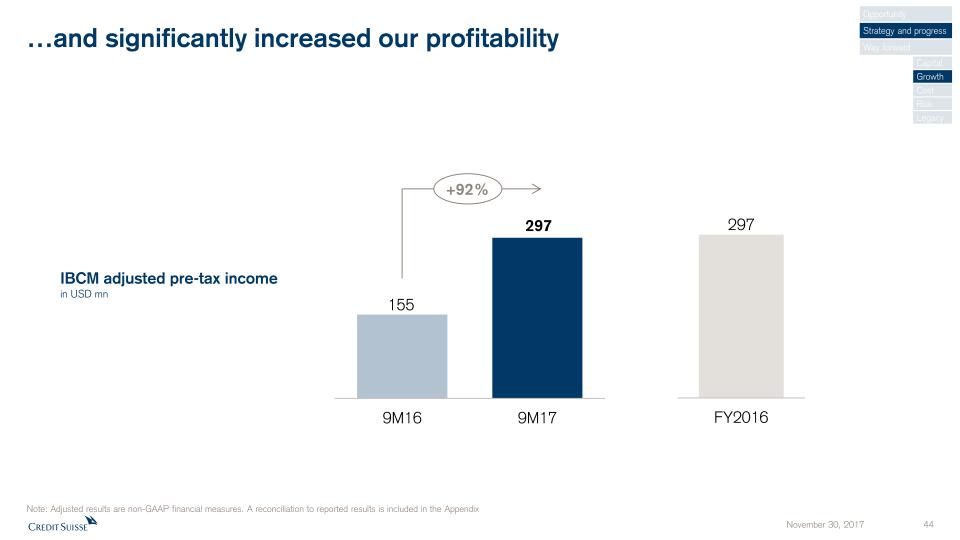

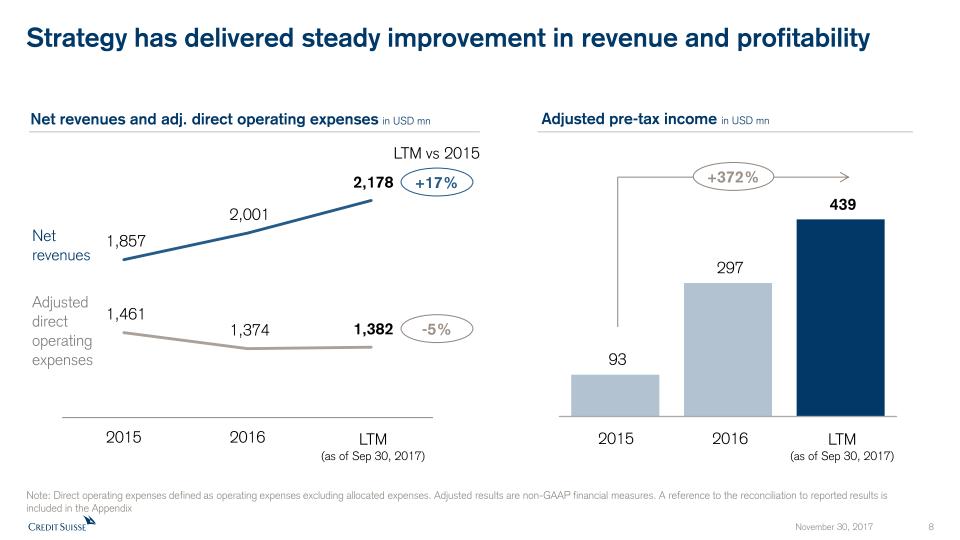

…and significantly increased our profitability IBCM adjusted pre-tax incomein USD mn +92% Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

In Global Markets, we have right-sized our activities… As per 2015 Investor Day Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

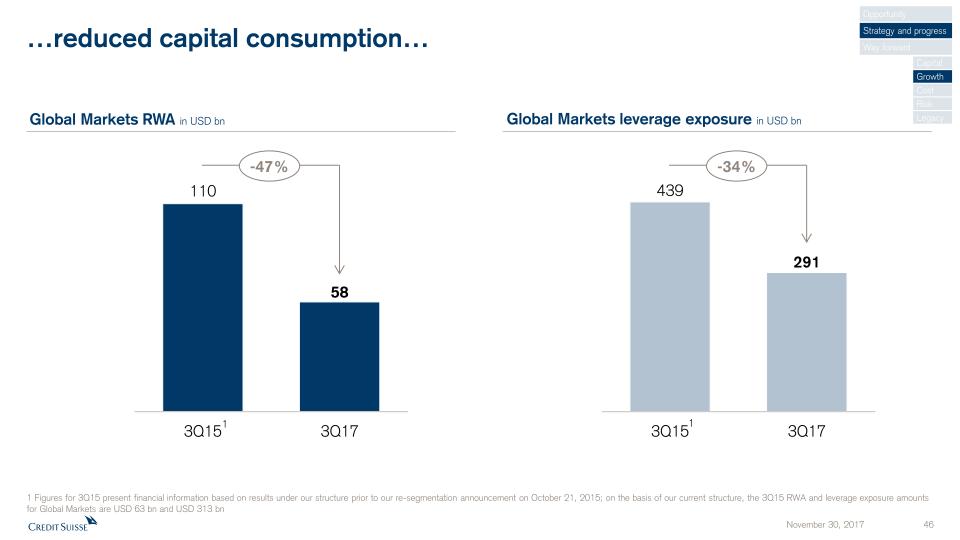

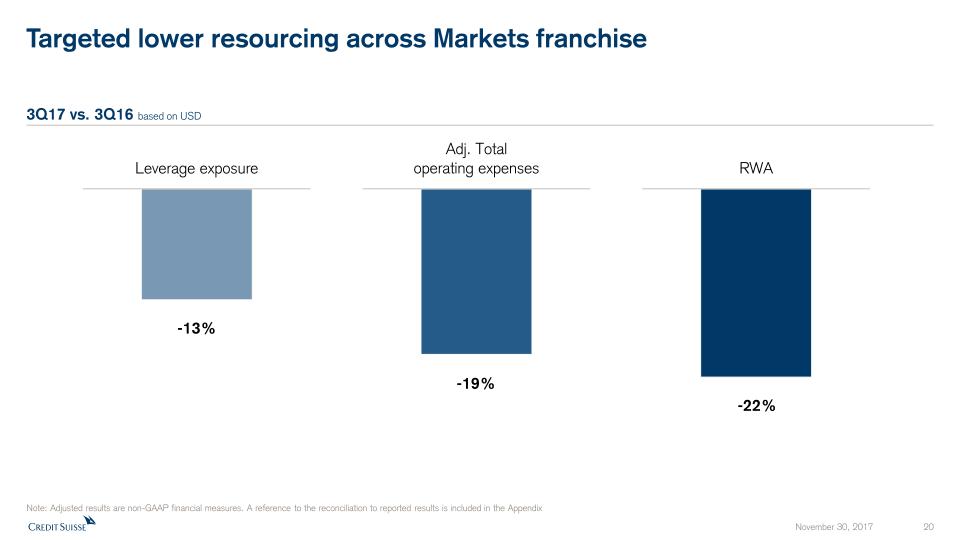

…reduced capital consumption… Global Markets leverage exposure in USD bn 1 Figures for 3Q15 present financial information based on results under our structure prior to our re-segmentation announcement on October 21, 2015; on the basis of our current structure, the 3Q15 RWA and leverage exposure amounts for Global Markets are USD 63 bn and USD 313 bn Global Markets RWA in USD bn -47% 1 -34% 1 Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

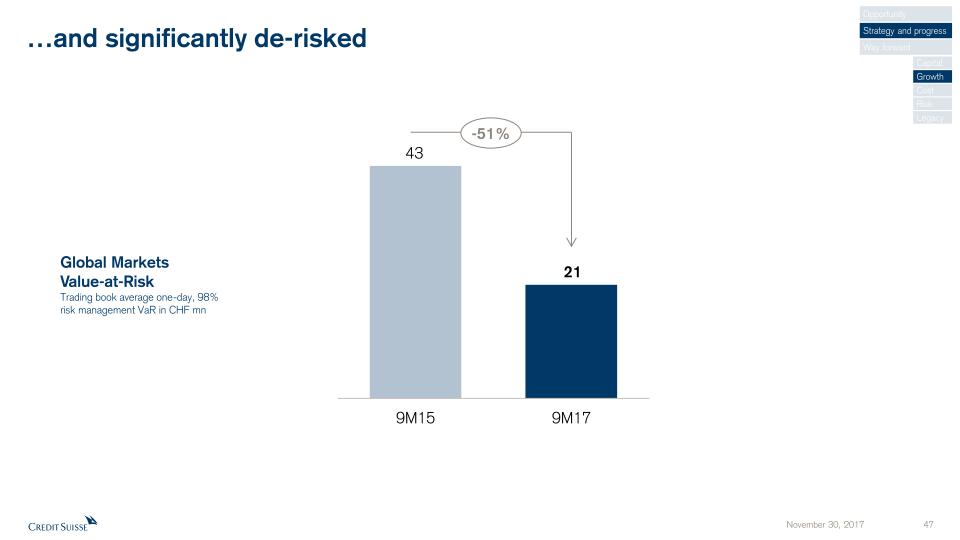

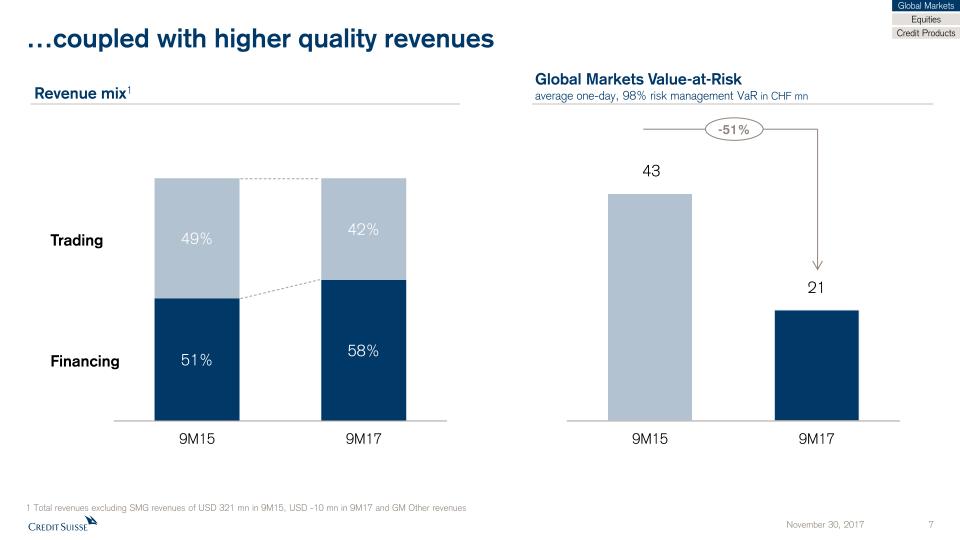

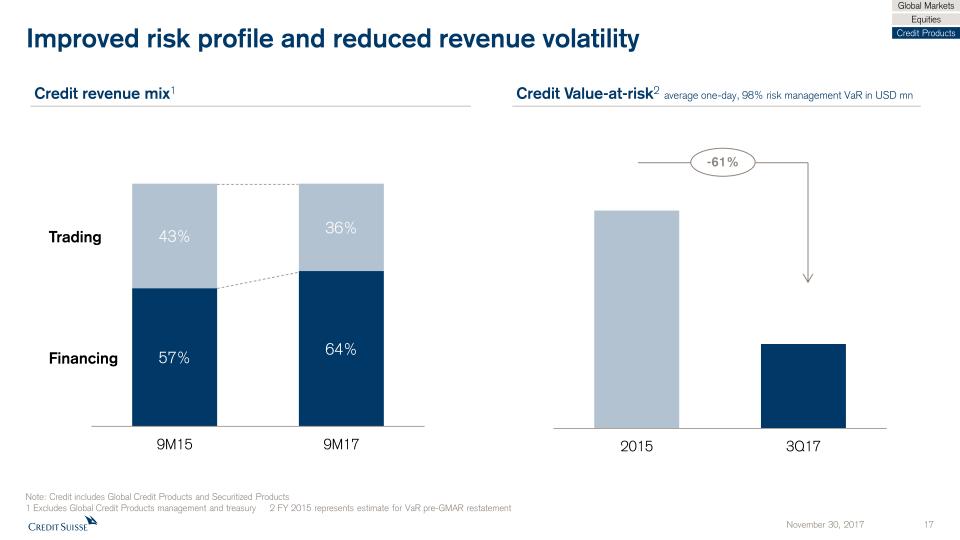

…and significantly de-risked -51% Global MarketsValue-at-RiskTrading book average one-day, 98%risk management VaR in CHF mn Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

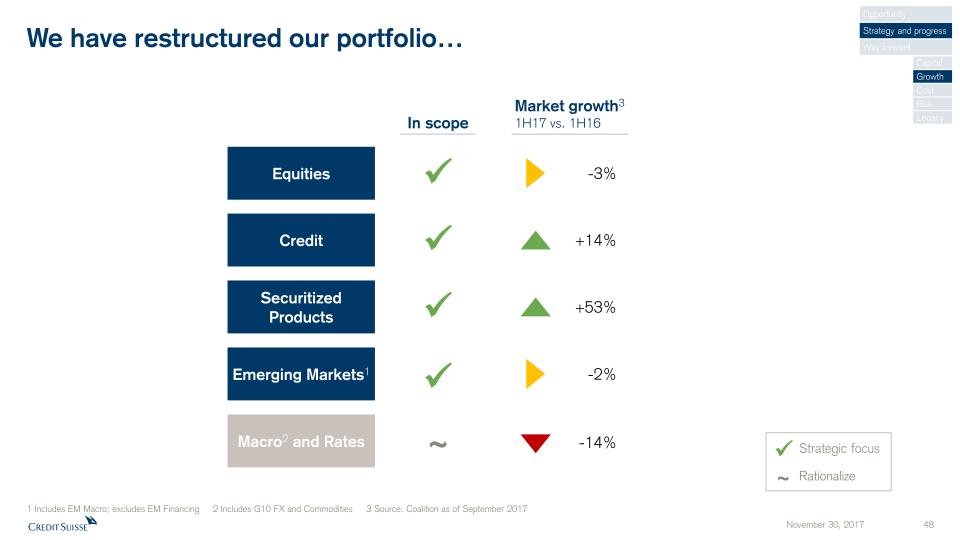

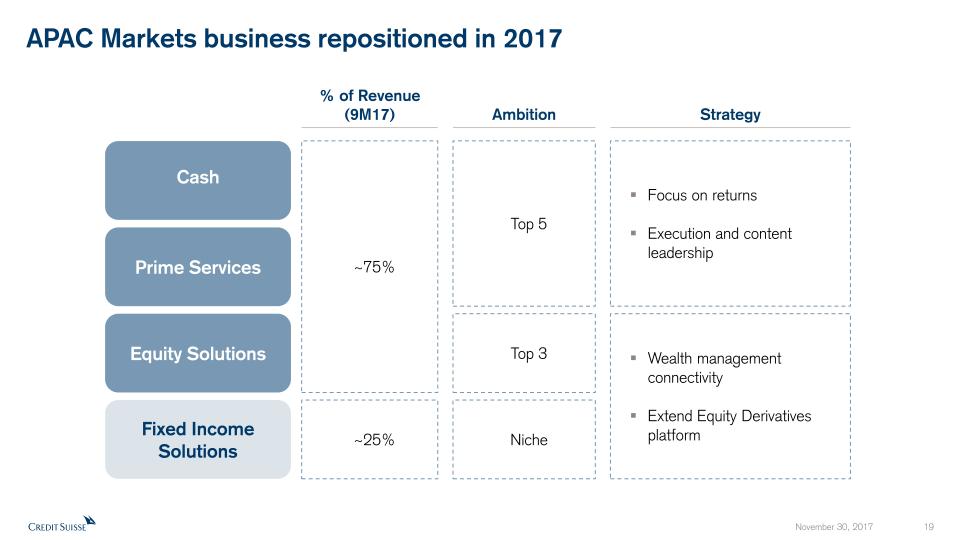

We have restructured our portfolio… Equities Credit Securitized Products In scope Market growth31H17 vs. 1H16 -3% +53% +14% 1 Includes EM Macro; excludes EM Financing 2 Includes G10 FX and Commodities 3 Source: Coalition as of September 2017 Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy Strategic focus Rationalize Macro2 and Rates -14% ~ ~ Emerging Markets1 -2%

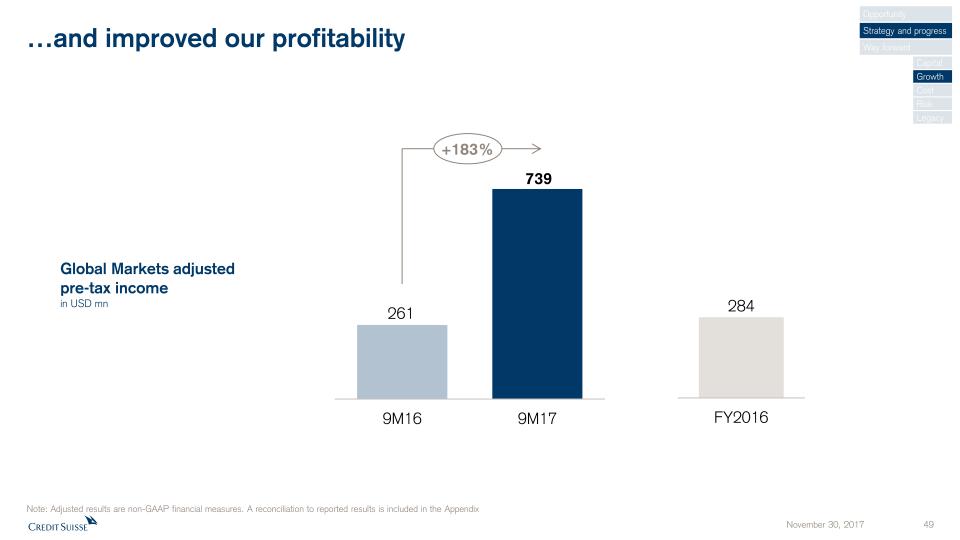

…and improved our profitability Global Markets adjusted pre-tax incomein USD mn Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix +183% Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

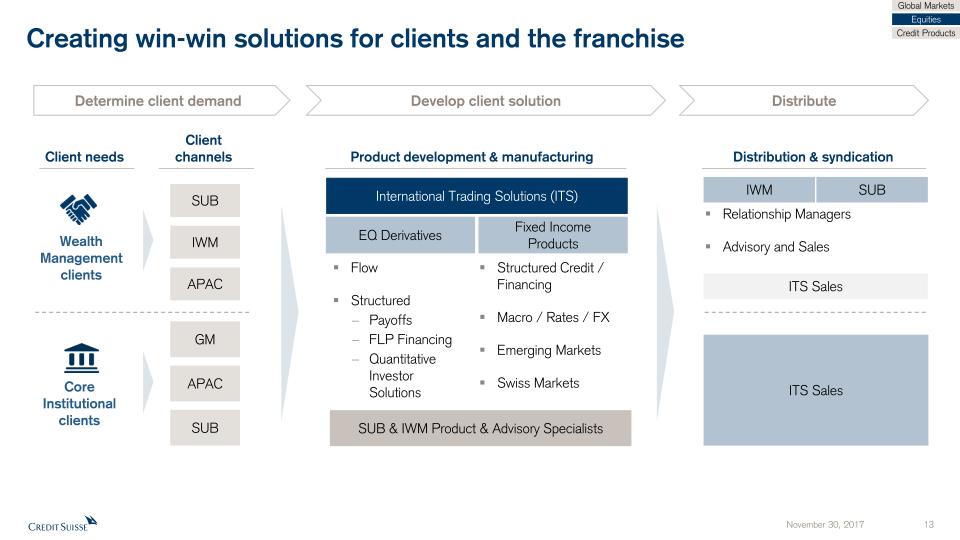

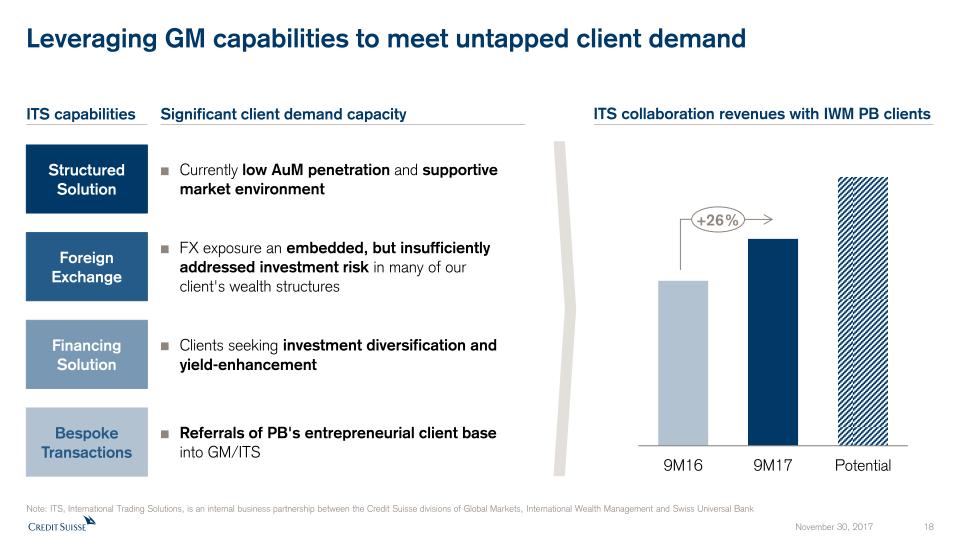

We have launched our new joint venture International TradingSolutions... Product development & manufacturing International Trading Solutions SUB & IWM Product & Advisory Specialists Equity Derivatives Fixed Income Products Flow Products Structured EQ Derivatives Structured Credit & Financing Macro / Rates / FX Emerging Markets Swiss Markets Client needs Distribution & syndication Wealth Management distribution ITSsales and distribution Global Marketssales and distribution Wealth Management Core Institutional Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

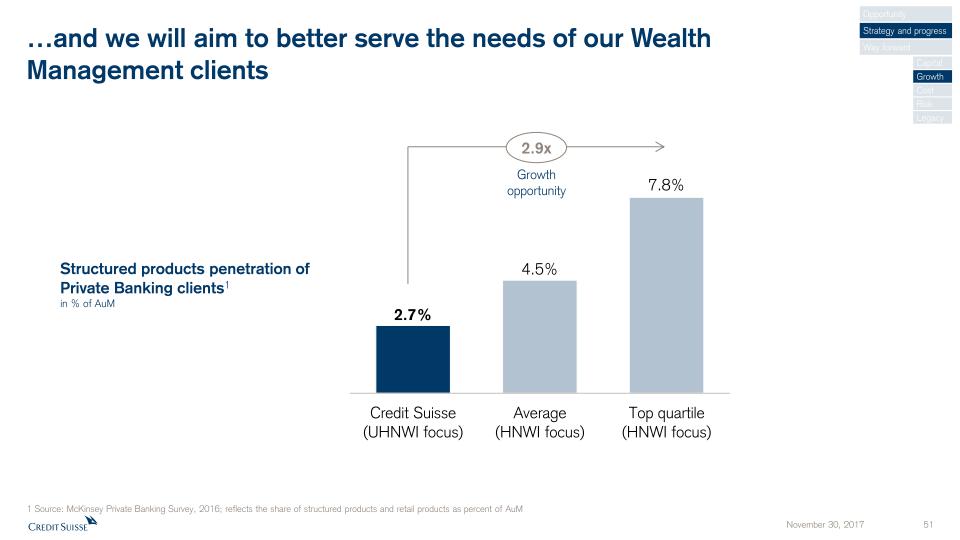

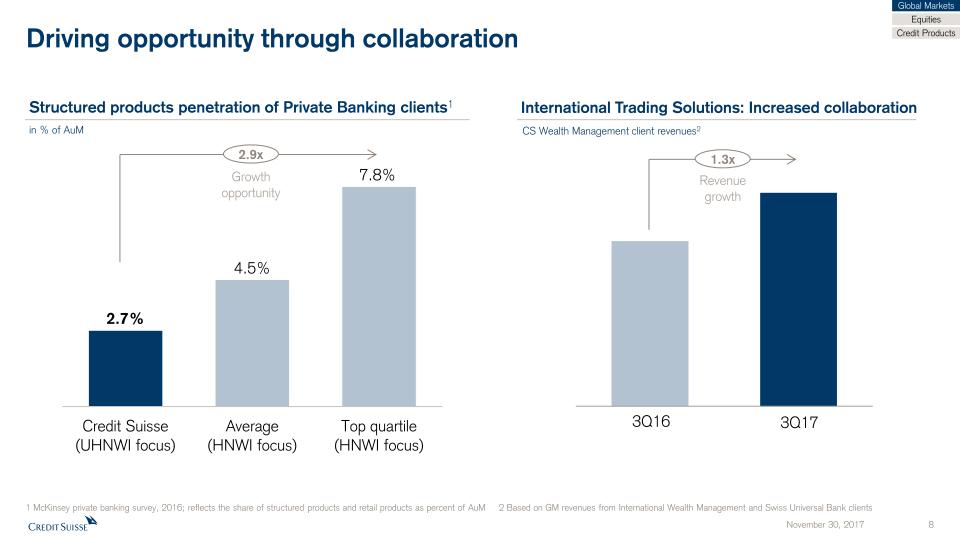

…and we will aim to better serve the needs of our WealthManagement clients 1 Source: McKinsey Private Banking Survey, 2016; reflects the share of structured products and retail products as percent of AuM 2.9x Growth opportunity Structured products penetration of Private Banking clients1in % of AuM Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

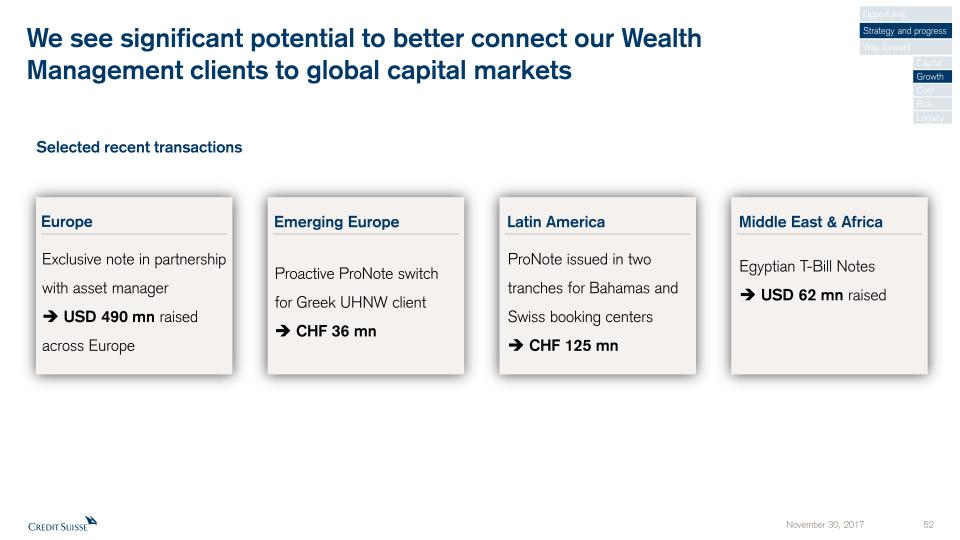

We see significant potential to better connect our WealthManagement clients to global capital markets Europe Exclusive note in partnership with asset manager USD 490 mn raised across Europe Emerging Europe Latin America Middle East & Africa Proactive ProNote switch for Greek UHNW client CHF 36 mn ProNote issued in two tranches for Bahamas and Swiss booking centers CHF 125 mn Egyptian T-Bill Notes USD 62 mn raised Selected recent transactions Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

Our approach has yielded strong results Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix1 Relating to SUB PC, IWM PB and APAC PB within WM&C 2 Relating to SUB, IWM and APAC WM&C

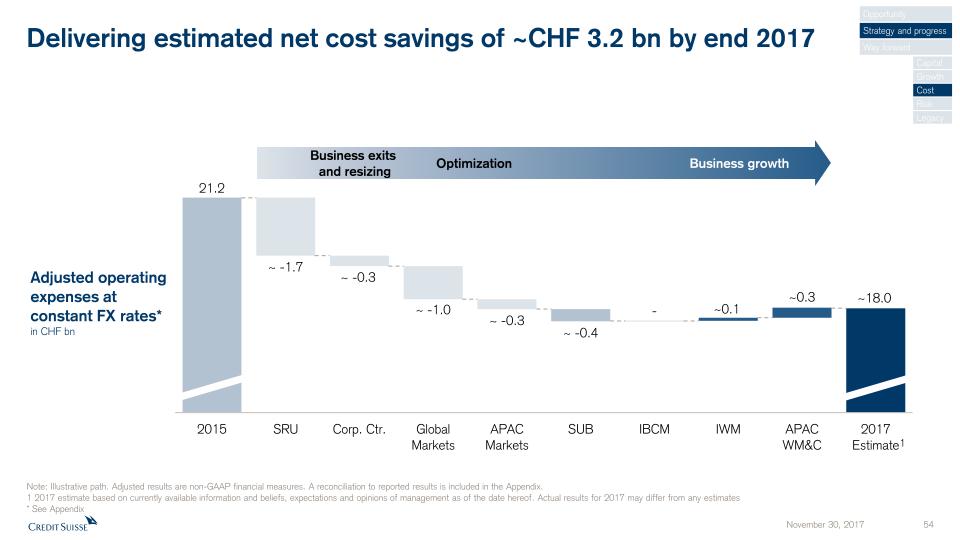

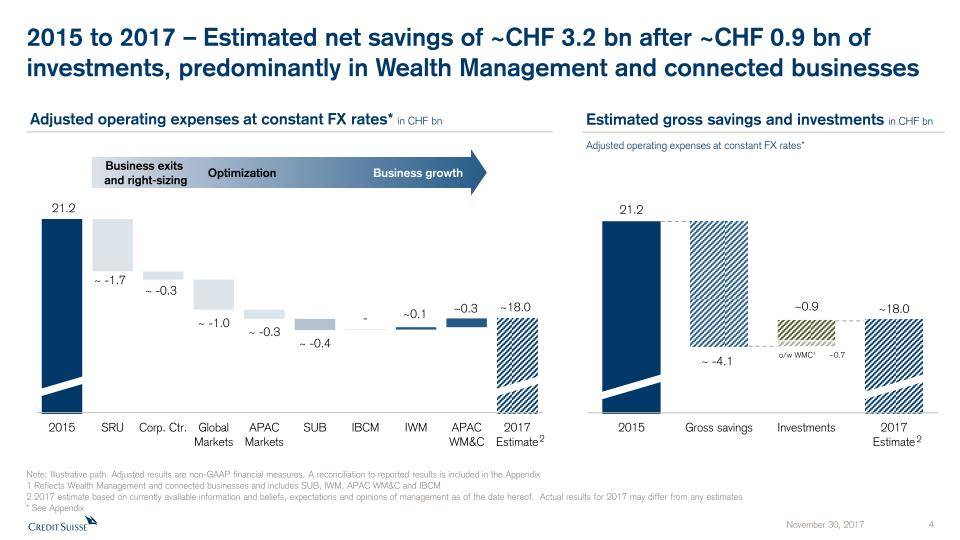

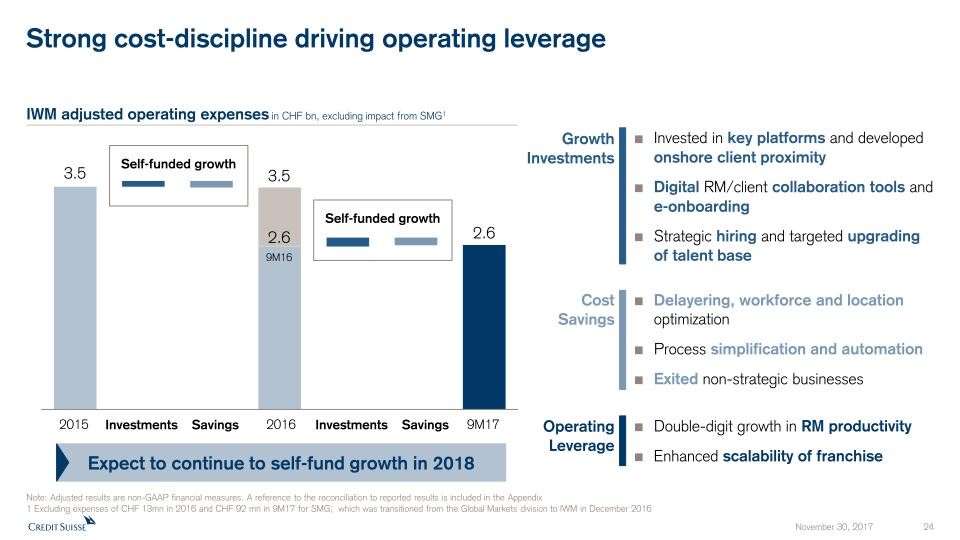

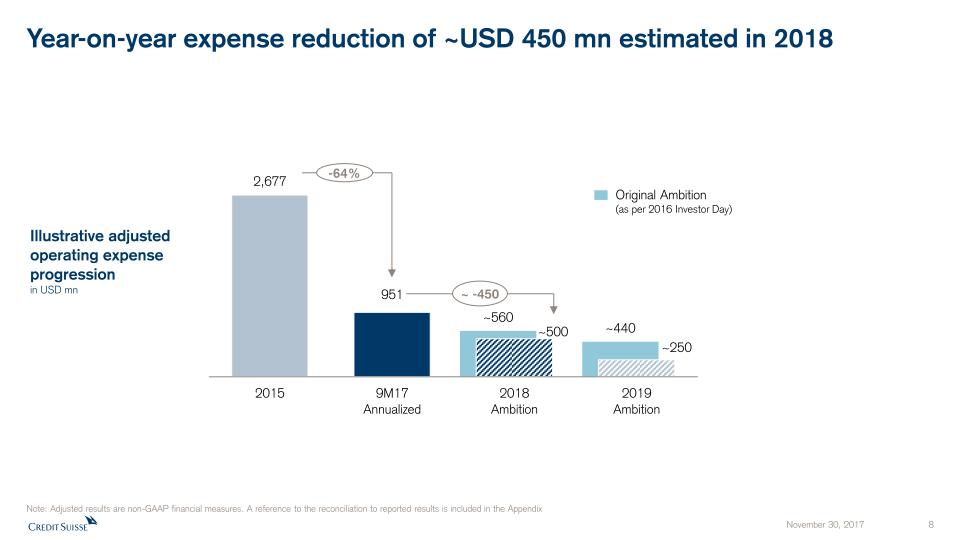

Delivering estimated net cost savings of ~CHF 3.2 bn by end 2017 Adjusted operating expenses at constant FX rates*in CHF bn Business exits and resizing Optimization Business growth Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy Note: Illustrative path. Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix.1 2017 estimate based on currently available information and beliefs, expectations and opinions of management as of the date hereof. Actual results for 2017 may differ from any estimates* See Appendix 1

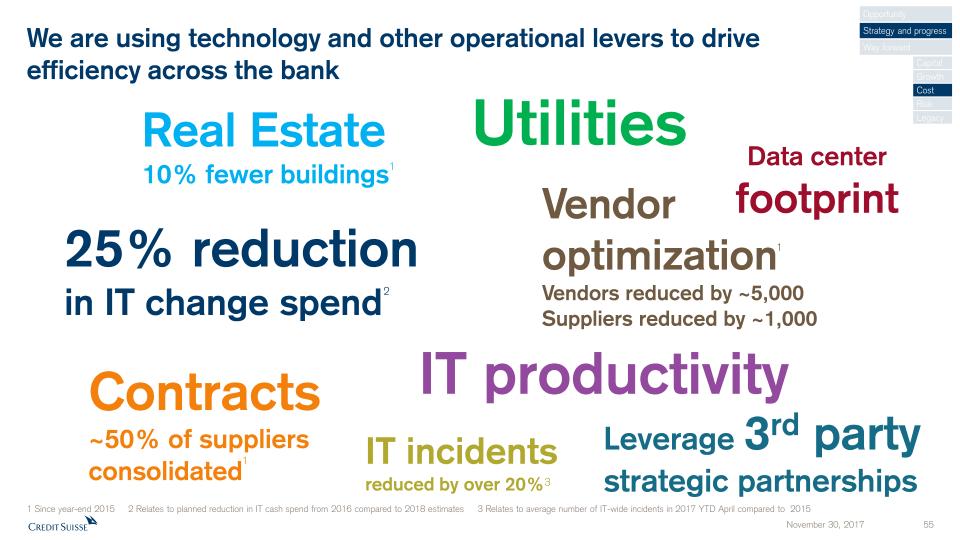

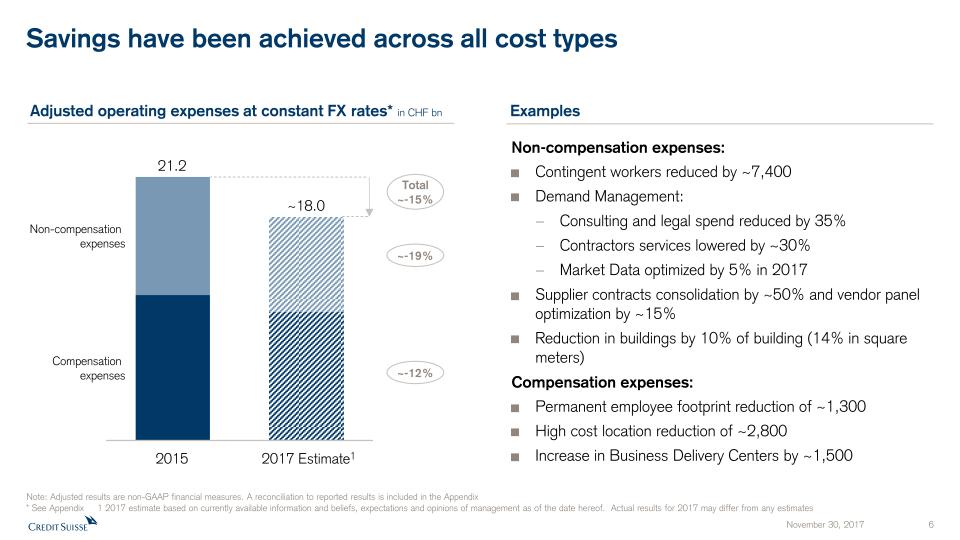

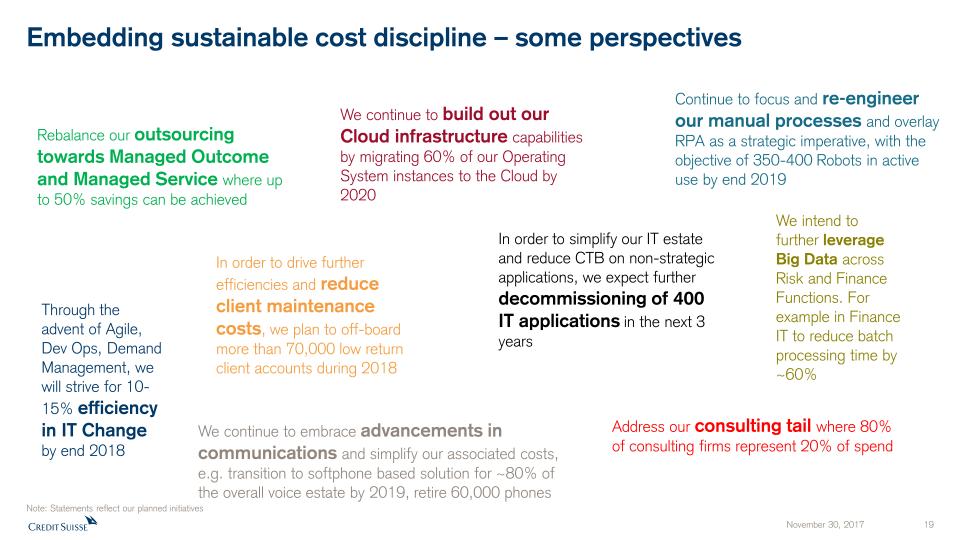

We are using technology and other operational levers to driveefficiency across the bank Real Estate10% fewer buildings IT productivity Vendor optimizationVendors reduced by ~5,000Suppliers reduced by ~1,000 Contracts~50% of suppliers consolidated Leverage 3rd party strategic partnerships Utilities Data centerfootprint 25% reductionin IT change spend IT incidents reduced by over 20%3 Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy 1 Since year-end 2015 2 Relates to planned reduction in IT cash spend from 2016 compared to 2018 estimates 3 Relates to average number of IT-wide incidents in 2017 YTD April compared to 2015 2 1 1 1

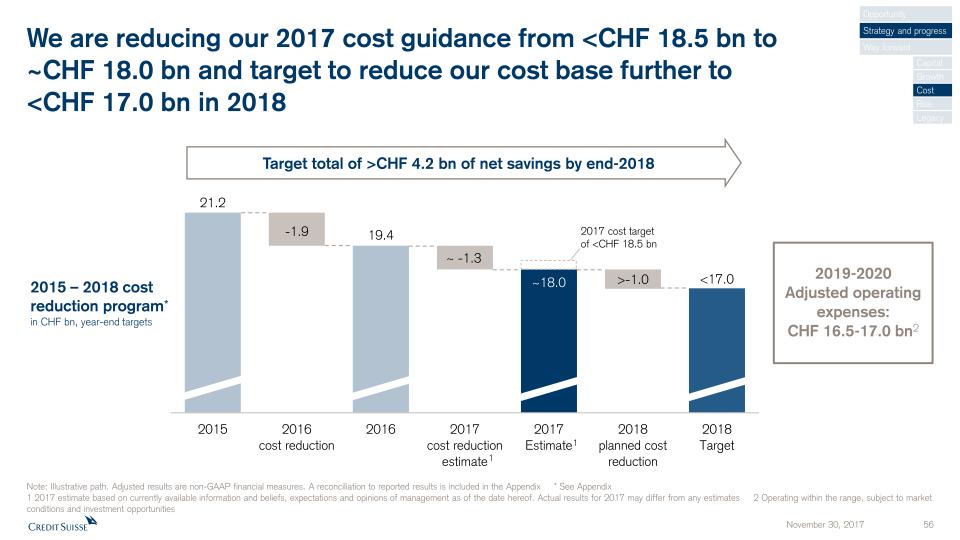

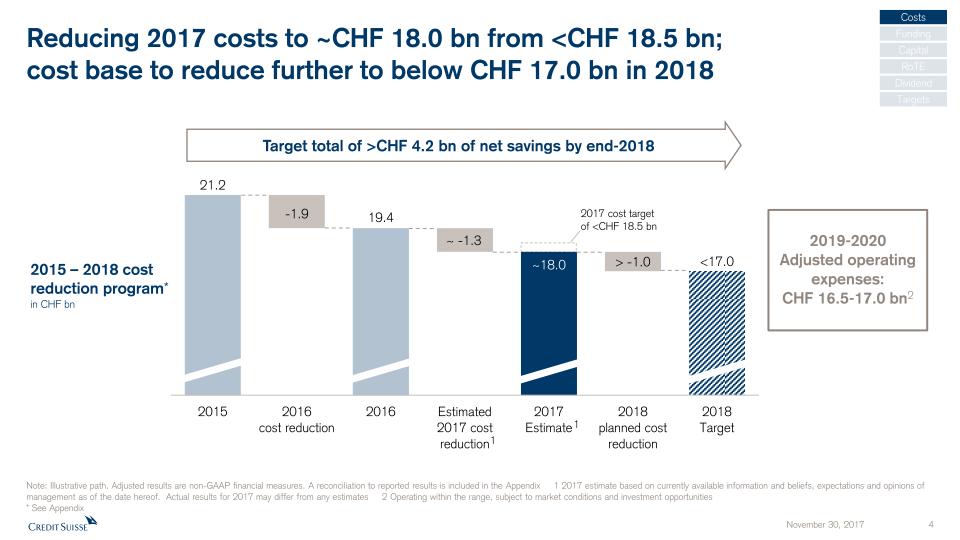

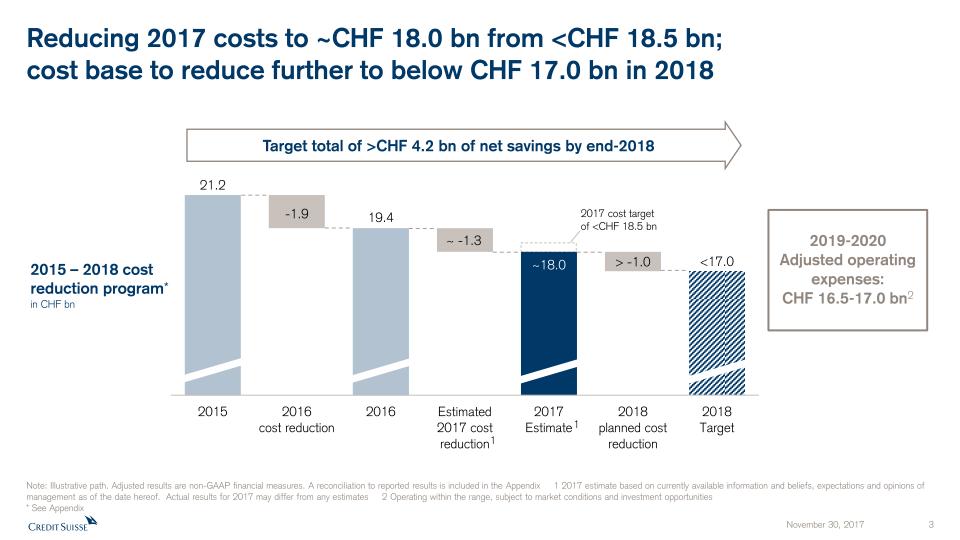

We are reducing our 2017 cost guidance from <CHF 18.5 bn to~CHF 18.0 bn and target to reduce our cost base further to <CHF 17.0 bn in 2018 Target total of >CHF 4.2 bn of net savings by end-2018 Note: Illustrative path. Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix * See Appendix1 2017 estimate based on currently available information and beliefs, expectations and opinions of management as of the date hereof. Actual results for 2017 may differ from any estimates 2 Operating within the range, subject to market conditions and investment opportunities 2017 cost target of <CHF 18.5 bn 2015 – 2018 cost reduction program* in CHF bn, year-end targets Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy 1 1 2019-2020Adjusted operating expenses: CHF 16.5-17.0 bn2

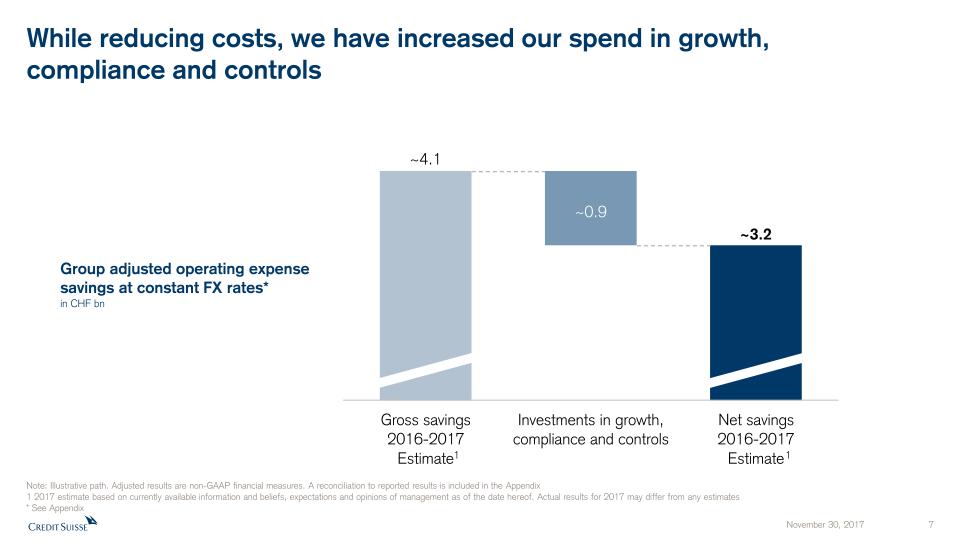

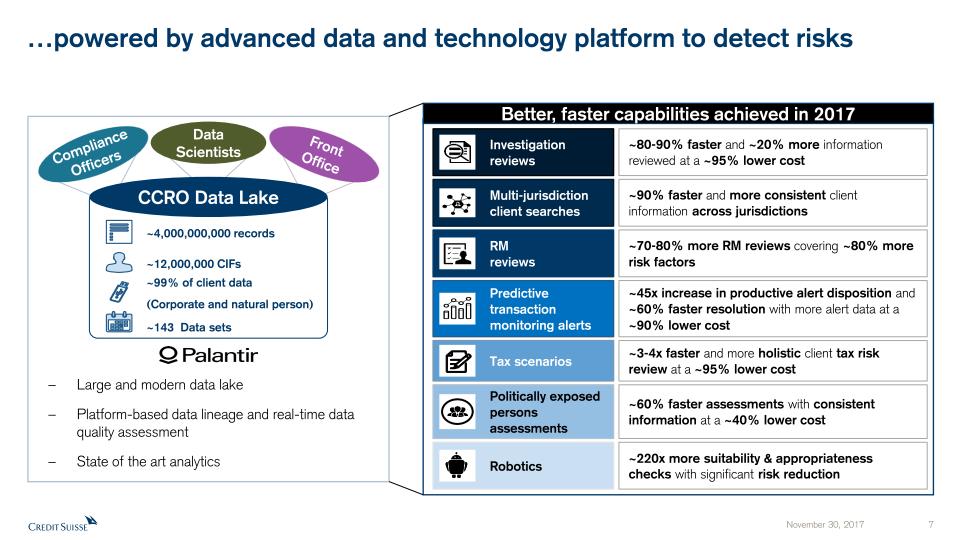

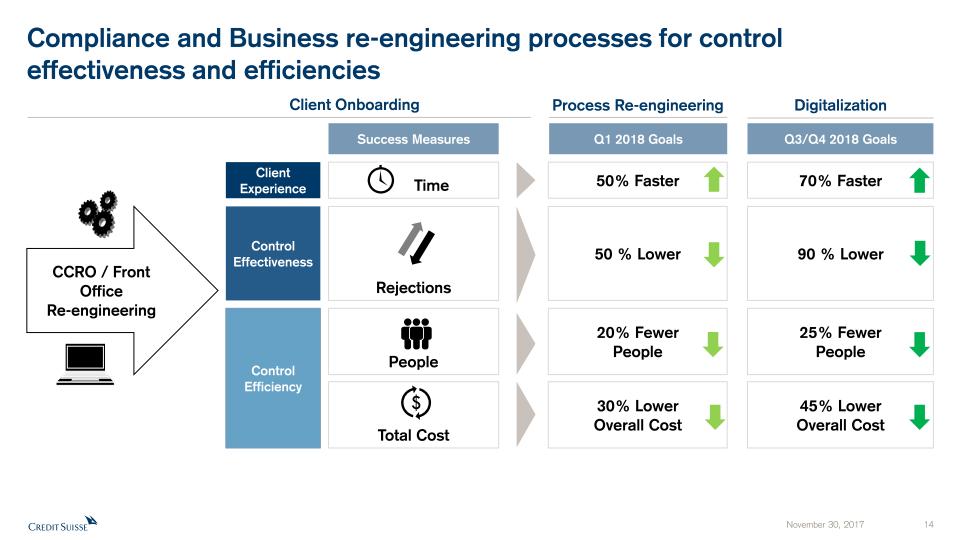

While reducing costs, we have increased our spend in complianceand controls… 1000+ controlimprovements 85% faster10% of costs101 major investigations closedInvestigations Technology40+ robots Clientonboarding Global client risk90% faster assessment using Single Client View 75% more reviews80% more risk factorsEmployee risksurveillance 50-70% faster50-90% fewer rejections30-45% cheaper Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy 1 In 2017 2 By 4Q2018 3 Since 2016 1 1 1 2 3 3

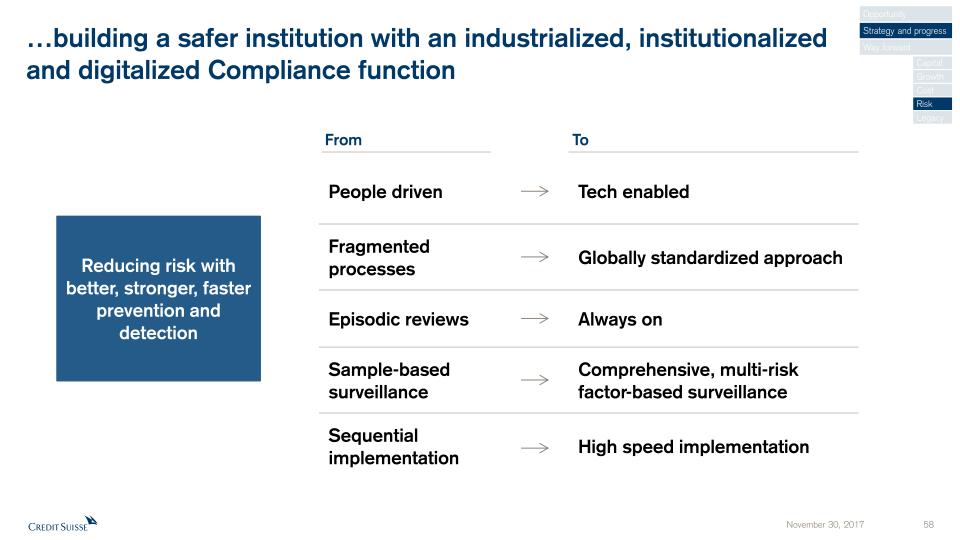

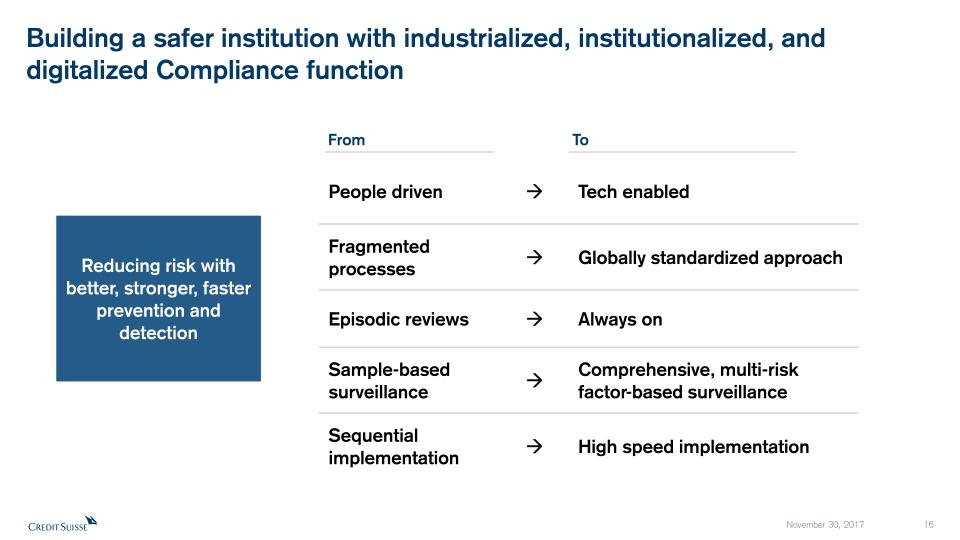

…building a safer institution with an industrialized, institutionalizedand digitalized Compliance function Reducing risk with better, stronger, faster prevention and detection People driven Tech enabled Fragmented processes Globally standardized approach Episodic reviews Always on Sample-based surveillance Comprehensive, multi-risk factor-based surveillance Sequential implementation High speed implementation From To Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

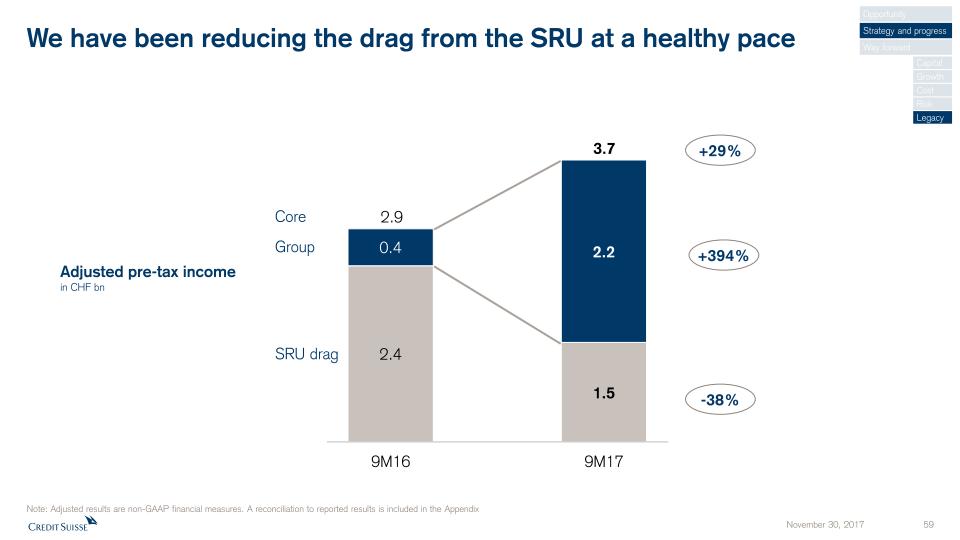

We have been reducing the drag from the SRU at a healthy pace Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix Adjusted pre-tax incomein CHF bn Core SRU drag Group +29% -38% 3.7 2.9 +394% Opportunity Strategy and progress Way forward Capital Growth Cost Risk Legacy

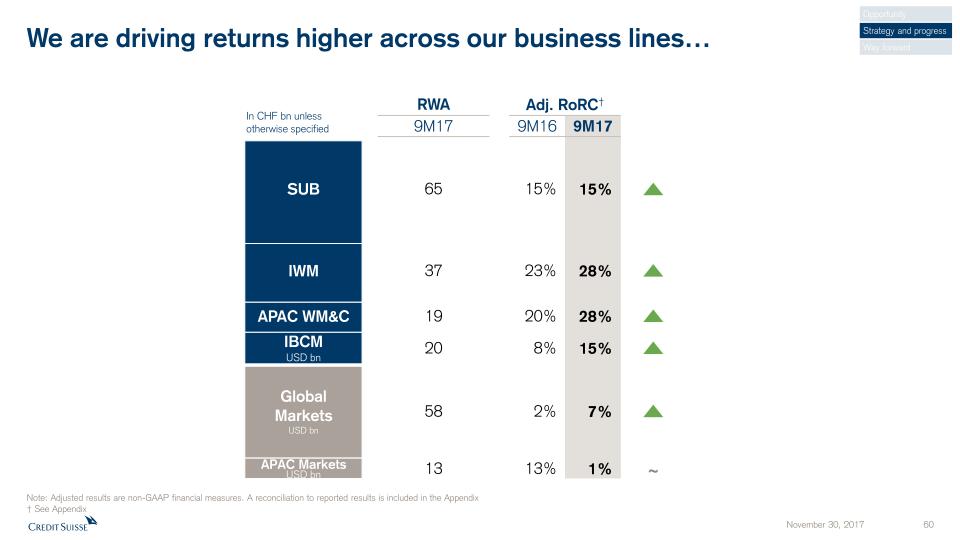

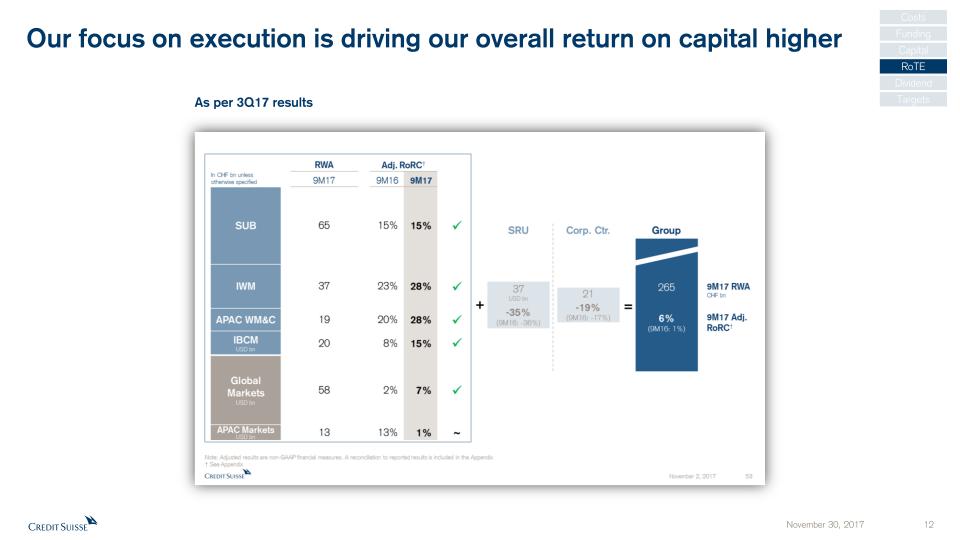

We are driving returns higher across our business lines… Adj. RoRC† RWA 15% 28% 28% 15% 7% 1% Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix† See Appendix In CHF bn unlessotherwise specified 9M17 9M16 15% 23% 20% 8% 2% 13% 9M17 ~ 65 37 19 20 58 SUB IWM APAC WM&C IBCMUSD bn GlobalMarketsUSD bn APAC MarketsUSD bn 13 Opportunity Strategy and progress Way forward

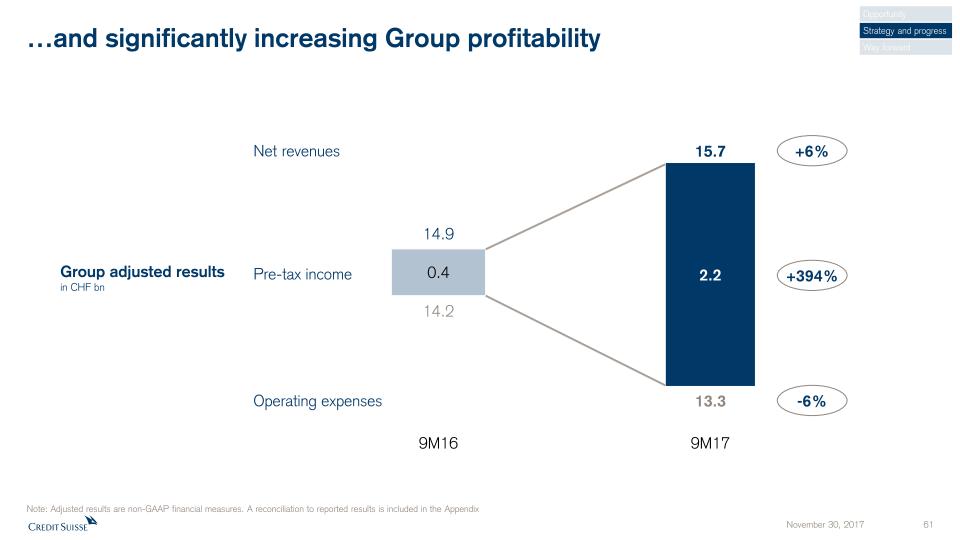

2.2 0.4 …and significantly increasing Group profitability Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix Net revenues Operating expenses Pre-tax income Group adjusted resultsin CHF bn 15.7 14.9 14.2 13.3 9M16 9M17 -6% +6% +394% Opportunity Strategy and progress Way forward

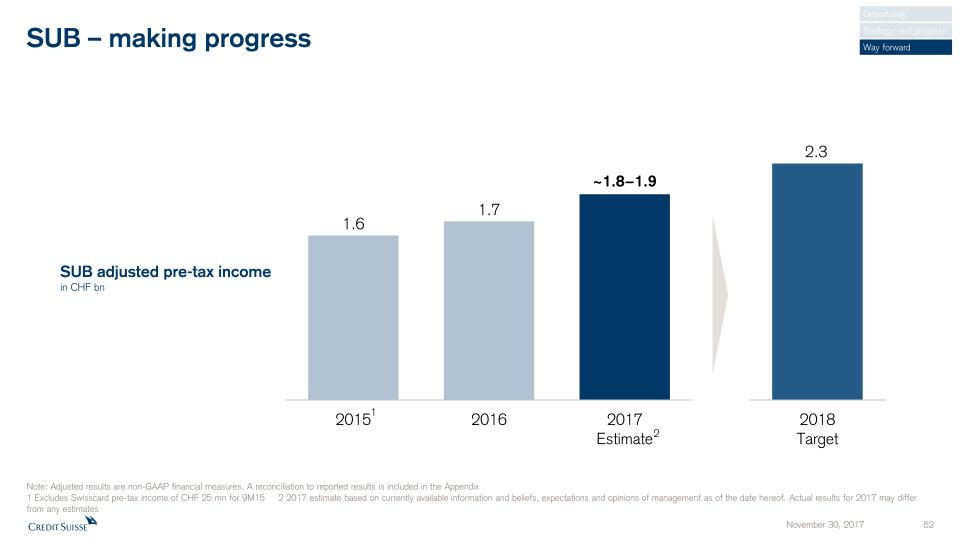

SUB – making progress SUB adjusted pre-tax incomein CHF bn Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix1 Excludes Swisscard pre-tax income of CHF 25 mn for 9M15 2 2017 estimate based on currently available information and beliefs, expectations and opinions of management as of the date hereof. Actual results for 2017 may differ from any estimates 1 Opportunity Strategy and progress Way forward 2

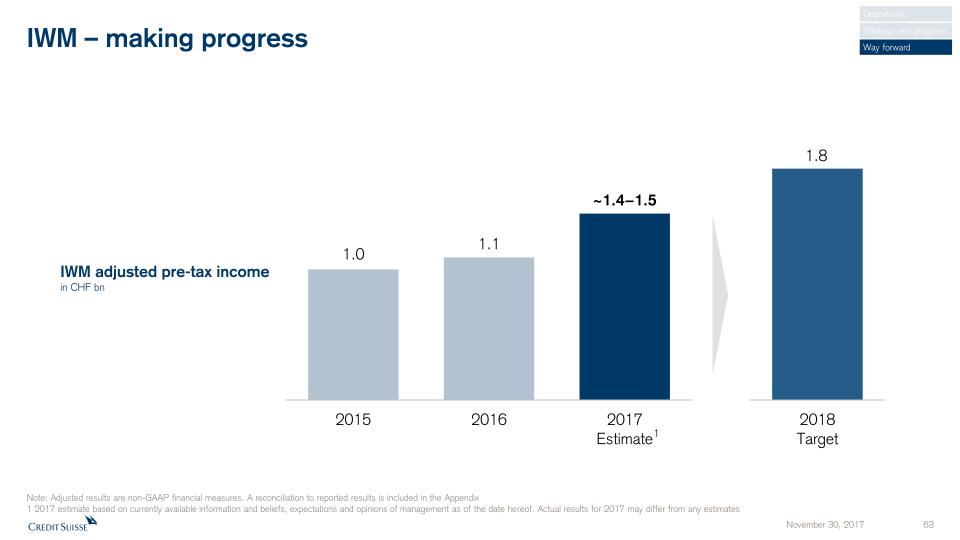

IWM – making progress Opportunity Strategy and progress Way forward 1 Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix1 2017 estimate based on currently available information and beliefs, expectations and opinions of management as of the date hereof. Actual results for 2017 may differ from any estimates IWM adjusted pre-tax incomein CHF bn

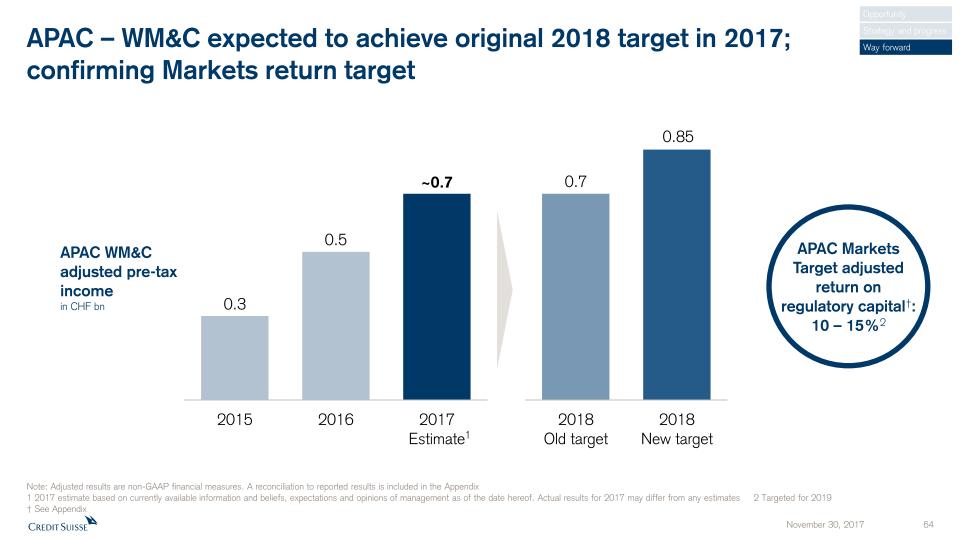

APAC – WM&C expected to achieve original 2018 target in 2017;confirming Markets return target APAC WM&Cadjusted pre-taxincomein CHF bn Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix1 2017 estimate based on currently available information and beliefs, expectations and opinions of management as of the date hereof. Actual results for 2017 may differ from any estimates 2 Targeted for 2019 † See Appendix APAC MarketsTarget adjusted return on regulatory capital†: 10 – 15%2 Opportunity Strategy and progress Way forward 1

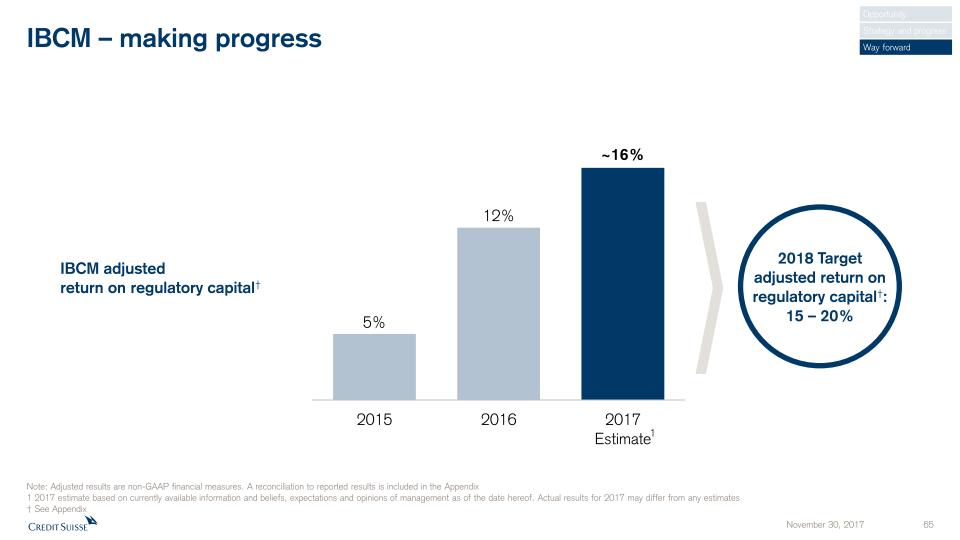

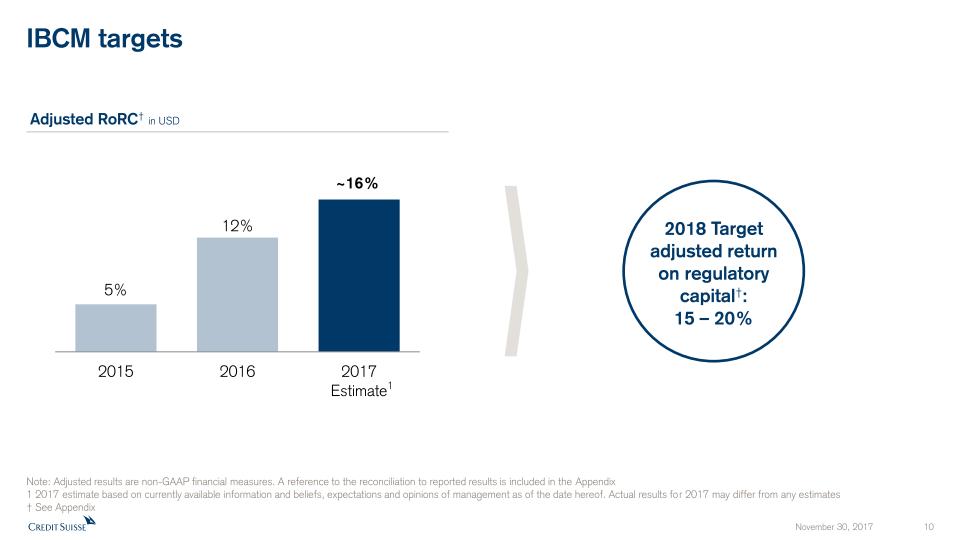

IBCM – making progress IBCM adjustedreturn on regulatory capital† Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix1 2017 estimate based on currently available information and beliefs, expectations and opinions of management as of the date hereof. Actual results for 2017 may differ from any estimates † See Appendix 2018 Targetadjusted return on regulatory capital†: 15 – 20% Opportunity Strategy and progress Way forward 1

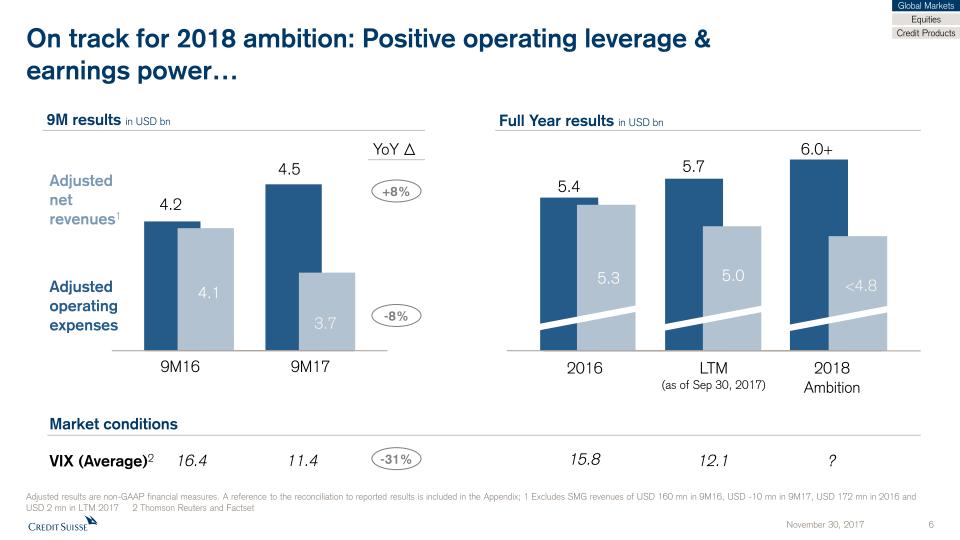

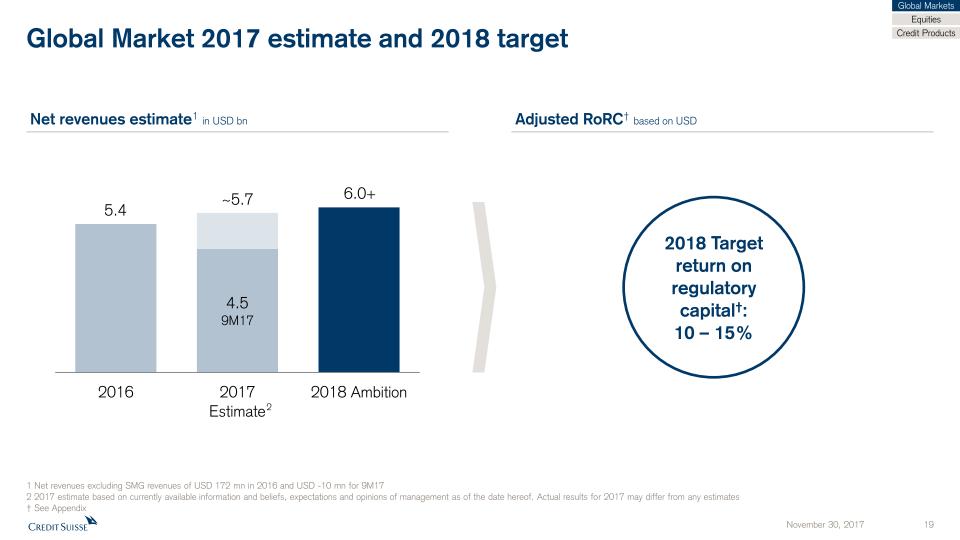

Global Markets – making progress Adjusted figures 2018 Ambition 2016 Results Net revenues USD 6.0 bn+ USD 5.6 bn USD ~5.7 bn 2017 Estimate1 Operating expenses <USD 4.8 bn USD 5.3 bn USD ~5.0 bn Opportunity Strategy and progress Way forward 2018 Targetadjusted return on regulatory capital†: 10 – 15% Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix1 2017 estimate based on currently available information and beliefs, expectations and opinions of management as of the date hereof. Actual results for 2017 may differ from any estimates. Net revenues exclude SMG † See Appendix

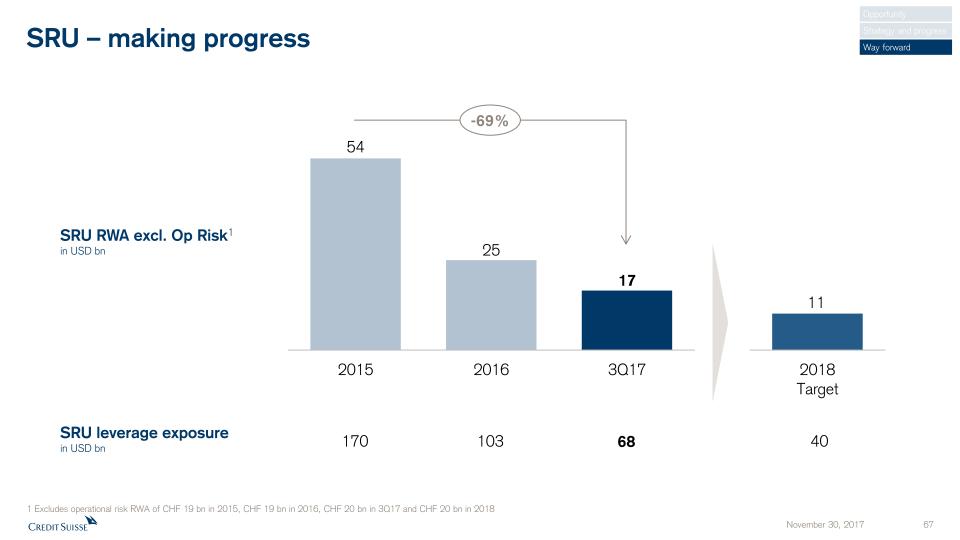

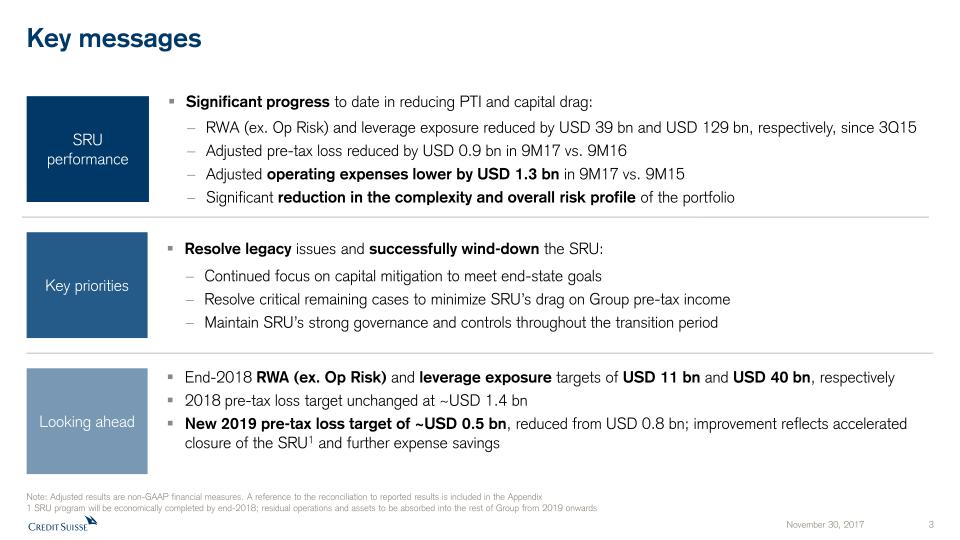

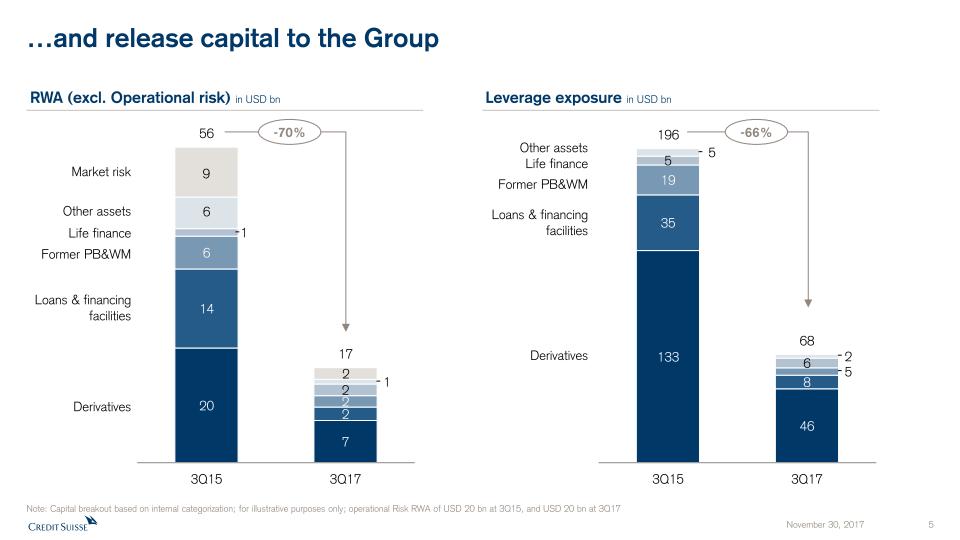

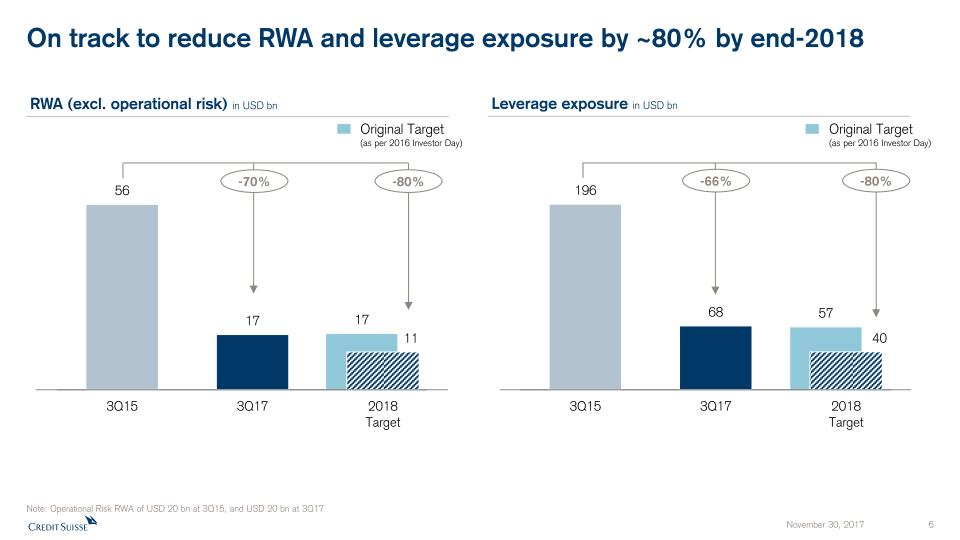

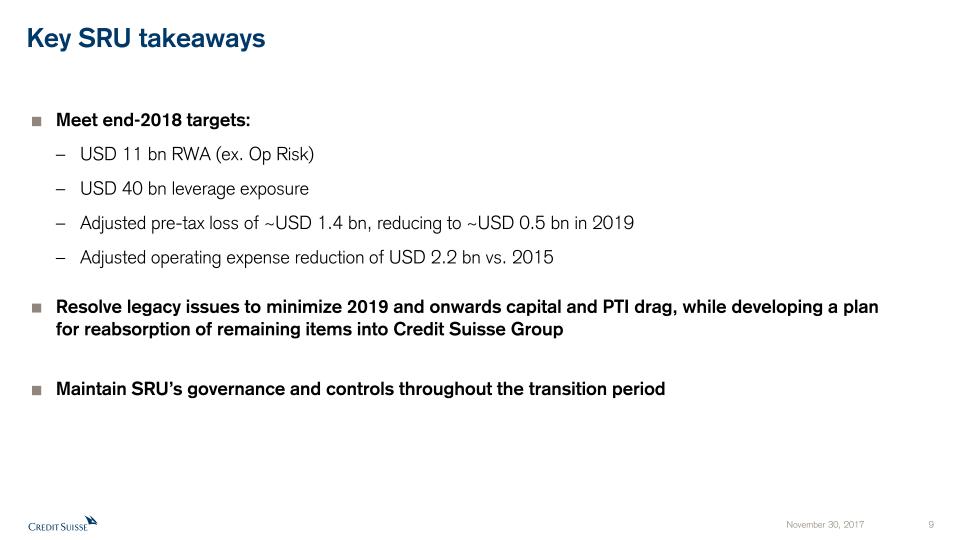

SRU – making progress Opportunity Strategy and progress Way forward 1 Excludes operational risk RWA of CHF 19 bn in 2015, CHF 19 bn in 2016, CHF 20 bn in 3Q17 and CHF 20 bn in 2018 SRU RWA excl. Op Risk1in USD bn SRU leverage exposurein USD bn -69% 170 103 68 40

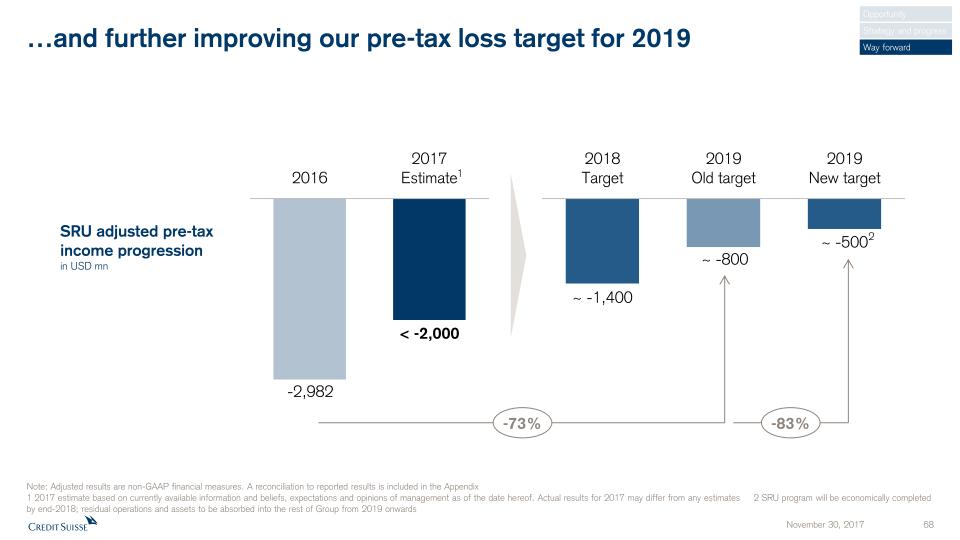

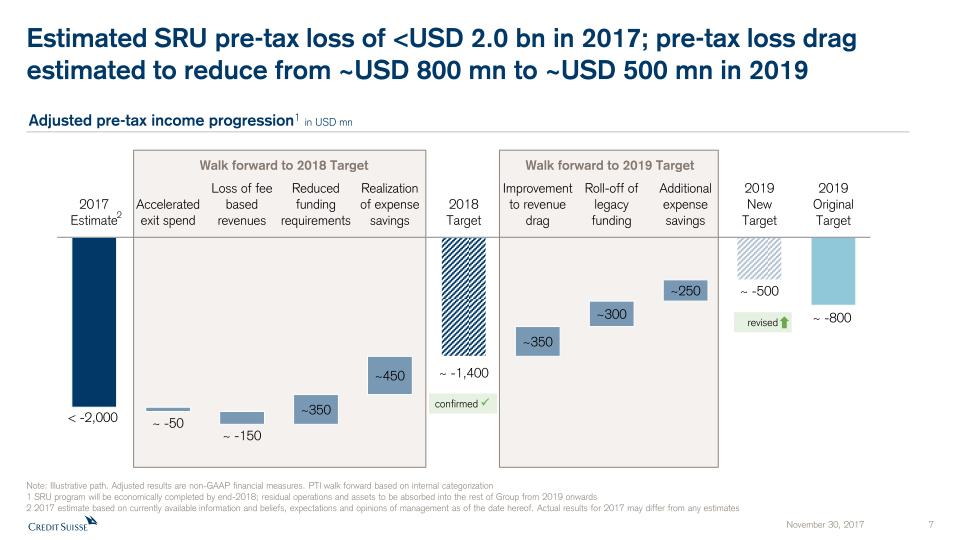

…and further improving our pre-tax loss target for 2019 -83% -73% SRU adjusted pre-tax income progressionin USD mn Note: Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix1 2017 estimate based on currently available information and beliefs, expectations and opinions of management as of the date hereof. Actual results for 2017 may differ from any estimates 2 SRU program will be economically completed by end-2018; residual operations and assets to be absorbed into the rest of Group from 2019 onwards 2 Opportunity Strategy and progress Way forward 1

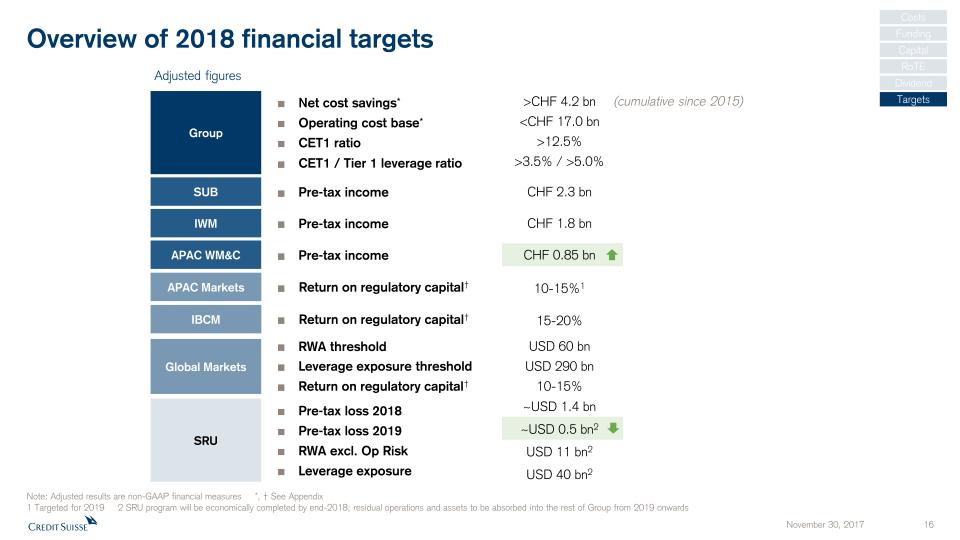

Overview of financial targets for Group and divisions in 2018… Group Net cost savings*Operating cost base*CET1 ratioCET1 / Tier 1 leverage ratio SUB Pre-tax income CHF 2.3 bn IWM Pre-tax income CHF 1.8 bn >CHF 4.2 bn<CHF 17.0 bn>12.5%>3.5% / >5.0% Adjusted figures 10-15%1 APAC Markets Return on regulatory capital† Global Markets RWA thresholdLeverage exposure thresholdReturn on regulatory capital† USD 60 bnUSD 290 bn10-15% APAC WMC Pre-tax income CHF 0.85 bn 15-20% IBCM Return on regulatory capital† SRU Pre-tax loss 2018Pre-tax loss 2019RWA excl. Op RiskLeverage exposure ~USD 1.4 bn~USD 0.5 bn2USD 11 bn2USD 40 bn2 Opportunity Strategy and progress Way forward (cumulative since 2015) Note: Adjusted results are non-GAAP financial measures *, † See Appendix 1 Targeted for 2019 2 SRU program will be economically completed by end-2018; residual operations and assets to be absorbed into the rest of Group from 2019 onwards

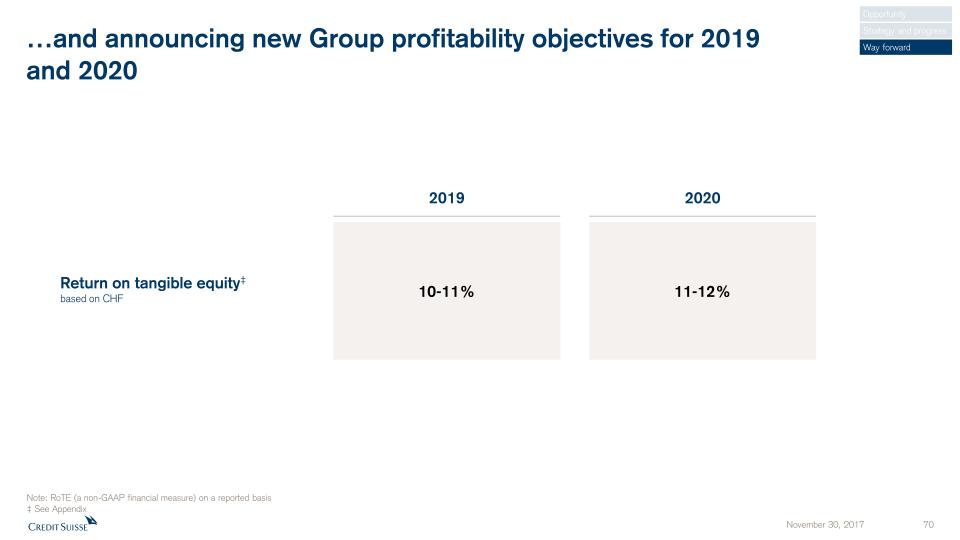

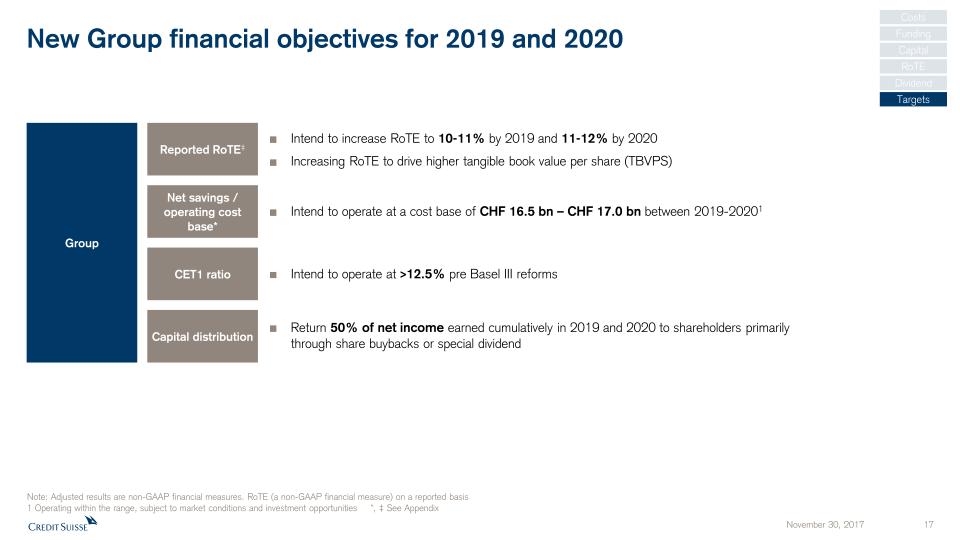

…and announcing new Group profitability objectives for 2019and 2020 Opportunity Strategy and progress Way forward 2020 11-12% 10-11% 2019 Return on tangible equity‡based on CHF Note: RoTE (a non-GAAP financial measure) on a reported basis‡ See Appendix

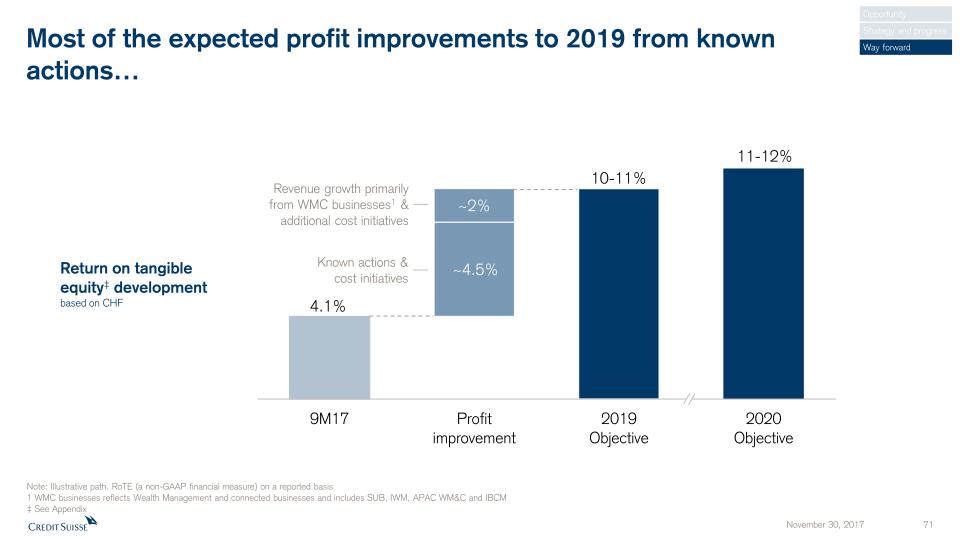

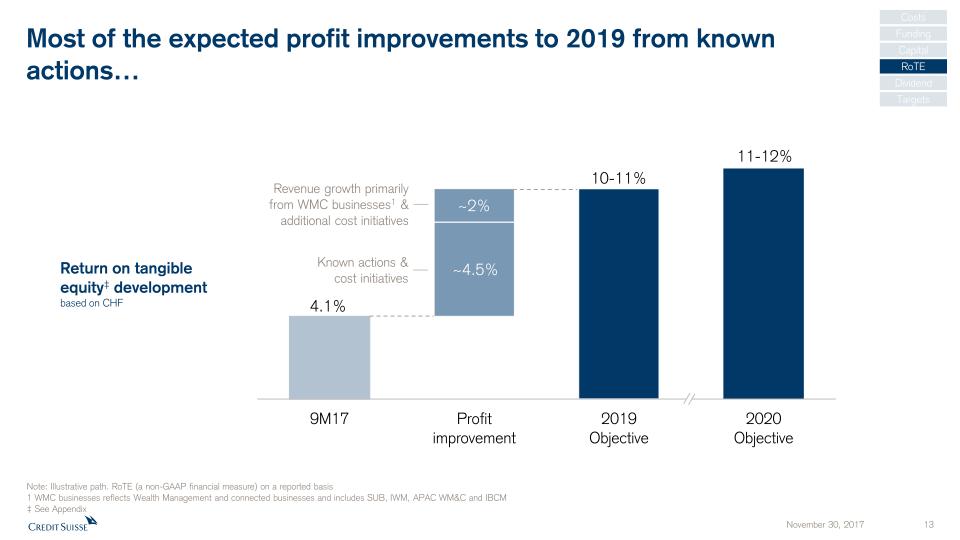

Most of the expected profit improvements to 2019 from knownactions… Return on tangible equity‡ developmentbased on CHF Revenue growth primarily from WMC businesses1 & additional cost initiatives Known actions &cost initiatives Opportunity Strategy and progress Way forward Note: Illustrative path. RoTE (a non-GAAP financial measure) on a reported basis1 WMC businesses reflects Wealth Management and connected businesses and includes SUB, IWM, APAC WM&C and IBCM‡ See Appendix

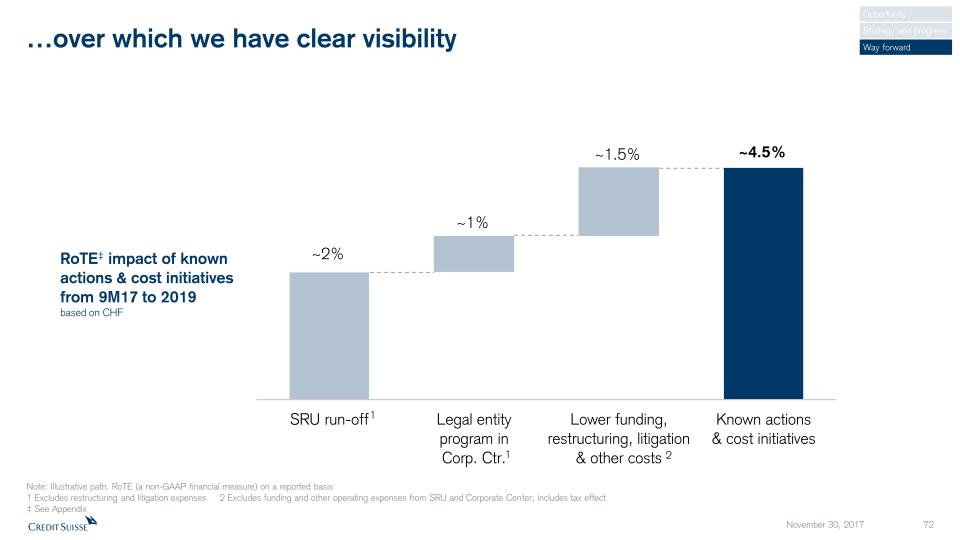

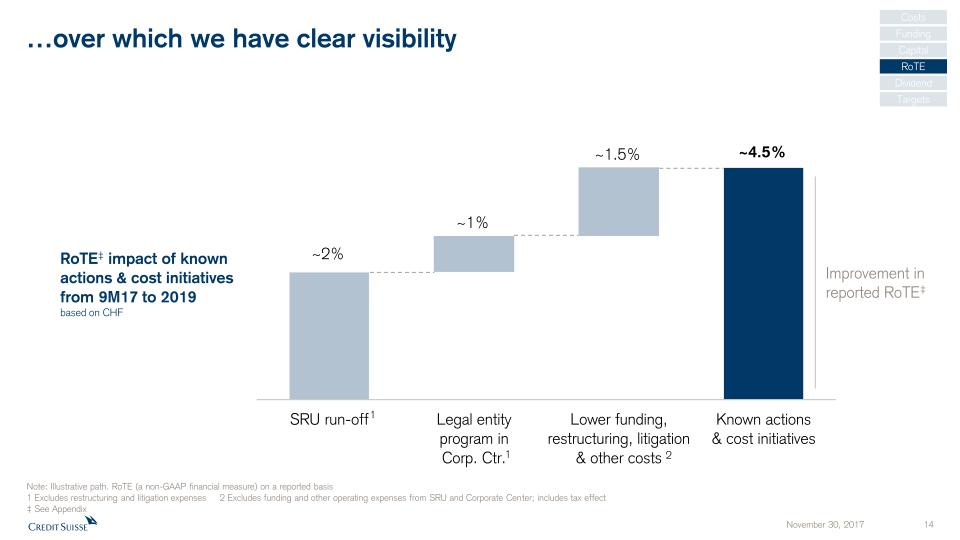

…over which we have clear visibility 2 1 1 Opportunity Strategy and progress Way forward Note: Illustrative path. RoTE (a non-GAAP financial measure) on a reported basis1 Excludes restructuring and litigation expenses 2 Excludes funding and other operating expenses from SRU and Corporate Center; includes tax effect‡ See Appendix RoTE‡ impact of known actions & cost initiativesfrom 9M17 to 2019based on CHF

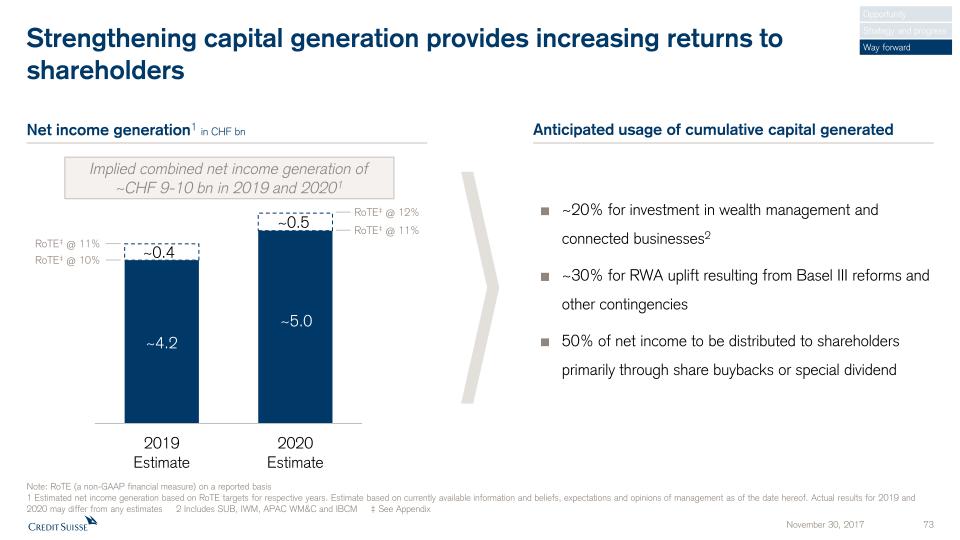

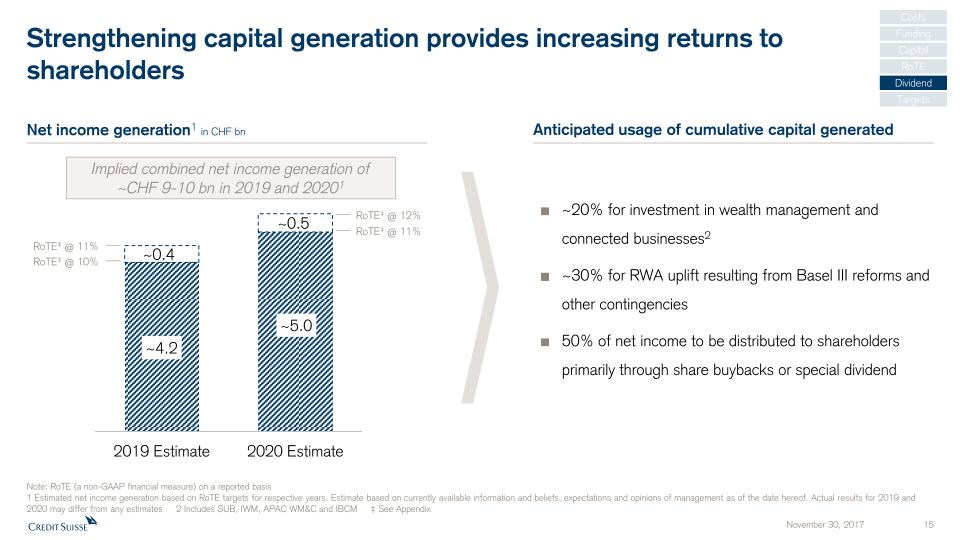

Anticipated usage of cumulative capital generated Strengthening capital generation provides increasing returns to shareholders RoTE‡ @ 11% RoTE‡ @ 10% RoTE‡ @ 12% RoTE‡ @ 11% Implied combined net income generation of~CHF 9-10 bn in 2019 and 20201 Net income generation1 in CHF bn ~20% for investment in wealth management and connected businesses2~30% for RWA uplift resulting from Basel III reforms and other contingencies50% of net income to be distributed to shareholders primarily through share buybacks or special dividend Note: RoTE (a non-GAAP financial measure) on a reported basis1 Estimated net income generation based on RoTE targets for respective years. Estimate based on currently available information and beliefs, expectations and opinions of management as of the date hereof. Actual results for 2019 and 2020 may differ from any estimates 2 Includes SUB, IWM, APAC WM&C and IBCM ‡ See Appendix Opportunity Strategy and progress Way forward

The way forward Our strategy and progress The opportunity Summary

Conclusion Execute with disciplineDeliver value for our shareholders

Program of the day Opening remarks Tidjane Thiam 8.30 am 45 min Webcast Morning break-out sessions 9.25 am No webcast Global Markets Brian Chin, David Miller, Mike Stewart 45 minAPAC Helman Sitohang, Francesco de Ferrari, Carsten Stoehr, Ken Pang 45 minBreak 20 minEfficiency & Productivity Pierre-Olivier Bouée, Paul Turrell 45 minCompliance Lara Warner, Homa Siddiqui 45 min Lunch 12.45 pm 50 min Afternoon break-out sessions 1.35 pm No webcast SUB Thomas Gottstein, Didier Denat, Serge Fehr 45 minIBCM Jim Amine, Malcolm Price, David Hermer 45 minIWM Iqbal Khan, Claudio de Sanctis, Bruno Daher 45 minBreak 25 min Capital,Funding and SRU David Mathers 4.15 pm 45 min Webcast Wrap-up & Q&A 5.00 pm 60 min Webcast Investor Day 2017

Appendix

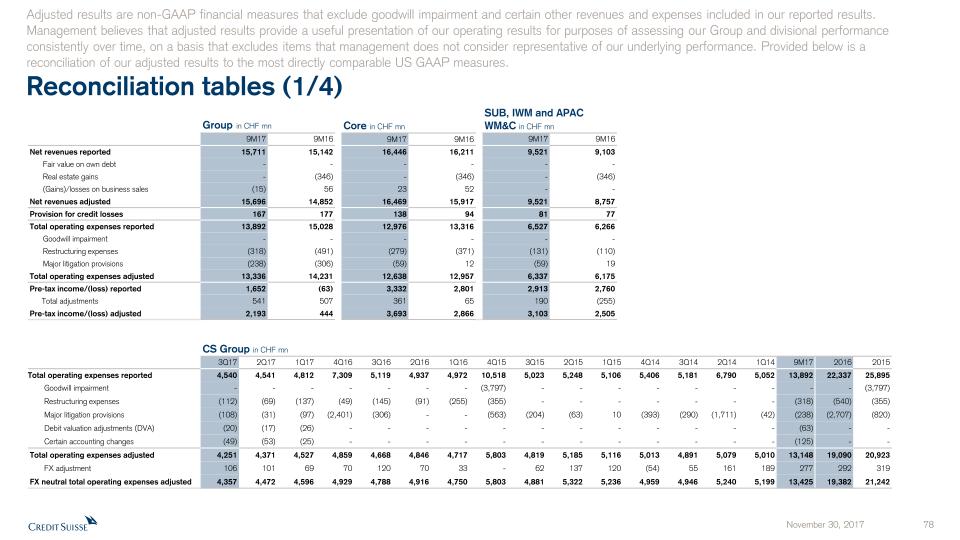

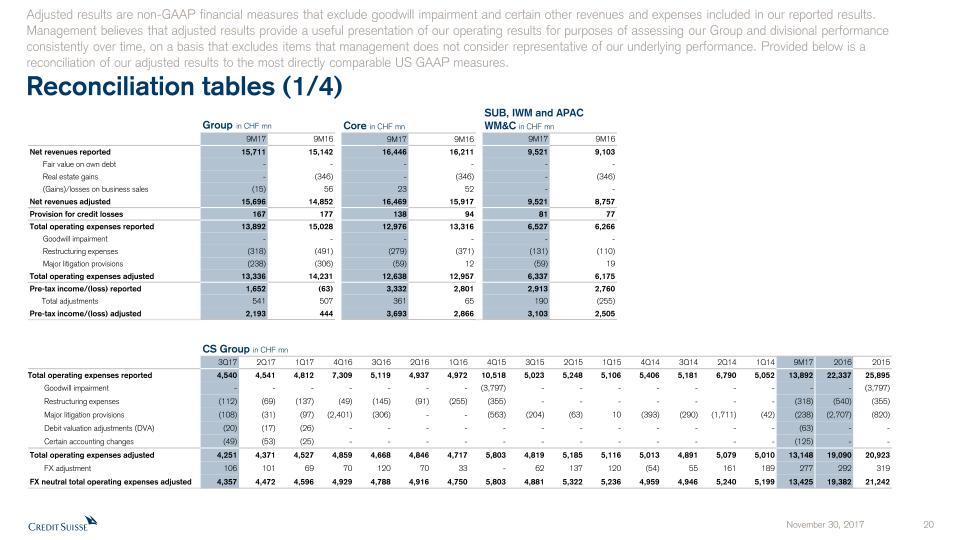

Reconciliation tables (1/4) Adjusted results are non-GAAP financial measures that exclude goodwill impairment and certain other revenues and expenses included in our reported results. Management believes that adjusted results provide a useful presentation of our operating results for purposes of assessing our Group and divisional performance consistently over time, on a basis that excludes items that management does not consider representative of our underlying performance. Provided below is a reconciliation of our adjusted results to the most directly comparable US GAAP measures. Group in CHF mn Core in CHF mn SUB, IWM and APAC WM&C in CHF mn 9M17 9M16 9M17 9M16 9M17 9M16 Net revenues reported 15,711 15,142 16,446 16,211 9,521 9,103 ��Fair value on own debt - - - - - - Real estate gains - (346) - (346) - (346) (Gains)/losses on business sales (15) 56 23 52 - - Net revenues adjusted 15,696 14,852 16,469 15,917 9,521 8,757 Provision for credit losses 167 177 138 94 81 77 Total operating expenses reported 13,892 15,028 12,976 13,316 6,527 6,266 Goodwill impairment - - - - - - Restructuring expenses (318) (491) (279) (371) (131) (110) Major litigation provisions (238) (306) (59) 12 (59) 19 Total operating expenses adjusted 13,336 14,231 12,638 12,957 6,337 6,175 Pre-tax income/(loss) reported 1,652 (63) 3,332 2,801 2,913 2,760 Total adjustments 541 507 361 65 190 (255) Pre-tax income/(loss) adjusted 2,193 444 3,693 2,866 3,103 2,505 CS Group in CHF mn 3Q17 2Q17 1Q17 4Q16 3Q16 2Q16 1Q16 4Q15 3Q15 2Q15 1Q15 4Q14 3Q14 2Q14 1Q14 9M17 2016 2015 Total operating expenses reported 4,540 4,541 4,812 7,309 5,119 4,937 4,972 10,518 5,023 5,248 5,106 5,406 5,181 6,790 5,052 13,892 22,337 25,895 Goodwill impairment - - - - - - - (3,797) - - - - - - - - - (3,797) Restructuring expenses (112) (69) (137) (49) (145) (91) (255) (355) - - - - - - - (318) (540) (355) Major litigation provisions (108) (31) (97) (2,401) (306) - - (563) (204) (63) 10 (393) (290) (1,711) (42) (238) (2,707) (820) Debit valuation adjustments (DVA) (20) (17) (26) - - - - - - - - - - - - (63) - - Certain accounting changes (49) (53) (25) - - - - - - - - - - - - (125) - - Total operating expenses adjusted 4,251 4,371 4,527 4,859 4,668 4,846 4,717 5,803 4,819 5,185 5,116 5,013 4,891 5,079 5,010 13,148 19,090 20,923 FX adjustment 106 101 69 70 120 70 33 - 62 137 120 (54) 55 161 189 277 292 319 FX neutral total operating expenses adjusted 4,357 4,472 4,596 4,929 4,788 4,916 4,750 5,803 4,881 5,322 5,236 4,959 4,946 5,240 5,199 13,425 19,382 21,242

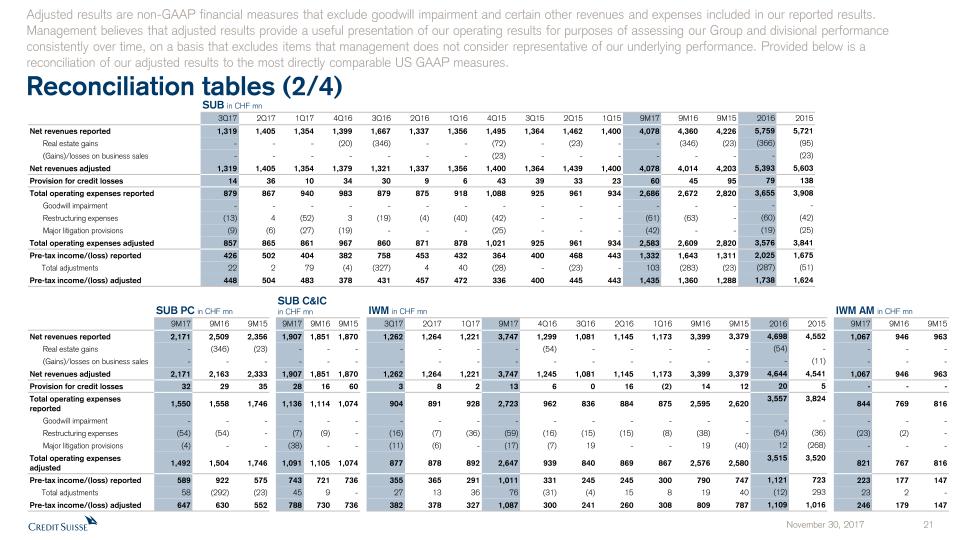

Reconciliation tables (2/4) Adjusted results are non-GAAP financial measures that exclude goodwill impairment and certain other revenues and expenses included in our reported results. Management believes that adjusted results provide a useful presentation of our operating results for purposes of assessing our Group and divisional performance consistently over time, on a basis that excludes items that management does not consider representative of our underlying performance. Provided below is a reconciliation of our adjusted results to the most directly comparable US GAAP measures. SUB in CHF mn 3Q17 2Q17 1Q17 4Q16 3Q16 2Q16 1Q16 4Q15 3Q15 2Q15 1Q15 9M17 9M16 9M15 2016 2015 Net revenues reported 1,319 1,405 1,354 1,399 1,667 1,337 1,356 1,495 1,364 1,462 1,400 4,078 4,360 4,226 5,759 5,721 Real estate gains - - - (20) (346) - - (72) - (23) - - (346) (23) (366) (95) (Gains)/losses on business sales - - - - - - - (23) - - - - - - - (23) Net revenues adjusted 1,319 1,405 1,354 1,379 1,321 1,337 1,356 1,400 1,364 1,439 1,400 4,078 4,014 4,203 5,393 5,603 Provision for credit losses 14 36 10 34 30 9 6 43 39 33 23 60 45 95 79 138 Total operating expenses reported 879 867 940 983 879 875 918 1,088 925 961 934 2,686 2,672 2,820 3,655 3,908 Goodwill impairment - - - - - - - - - - - - - - - - Restructuring expenses (13) 4 (52) 3 (19) (4) (40) (42) - - - (61) (63) - (60) (42) Major litigation provisions (9) (6) (27) (19) - - - (25) - - - (42) - - (19) (25) Total operating expenses adjusted 857 865 861 967 860 871 878 1,021 925 961 934 2,583 2,609 2,820 3,576 3,841 Pre-tax income/(loss) reported 426 502 404 382 758 453 432 364 400 468 443 1,332 1,643 1,311 2,025 1,675 Total adjustments 22 2 79 (4) (327) 4 40 (28) - (23) - 103 (283) (23) (287) (51) Pre-tax income/(loss) adjusted 448 504 483 378 431 457 472 336 400 445 443 1,435 1,360 1,288 1,738 1,624 SUB PC in CHF mn SUB C&ICin CHF mn IWM in CHF mn IWM AM in CHF mn 9M17 9M16 9M15 9M17 9M16 9M15 3Q17 2Q17 1Q17 9M17 4Q16 3Q16 2Q16 1Q16 9M16 9M15 2016 2015 9M17 9M16 9M15 Net revenues reported 2,171 2,509 2,356 1,907 1,851 1,870 1,262 1,264 1,221 3,747 1,299 1,081 1,145 1,173 3,399 3,379 4,698 4,552 1,067 946 963 Real estate gains - (346) (23) - - - - - - - (54) - - - - - (54) - - - - (Gains)/losses on business sales - - - - - - - - - - - - - - - - - (11) - - - Net revenues adjusted 2,171 2,163 2,333 1,907 1,851 1,870 1,262 1,264 1,221 3,747 1,245 1,081 1,145 1,173 3,399 3,379 4,644 4,541 1,067 946 963 Provision for credit losses 32 29 35 28 16 60 3 8 2 13 6 0 16 (2) 14 12 20 5 - - - Total operating expenses reported 1,550 1,558 1,746 1,136 1,114 1,074 904 891 928 2,723 962 836 884 875 2,595 2,620 3,557 3,824 844 769 816 Goodwill impairment - - - - - - - - - - - - - - - - - - - - - Restructuring expenses (54) (54) - (7) (9) - (16) (7) (36) (59) (16) (15) (15) (8) (38) - (54) (36) (23) (2) - Major litigation provisions (4) - - (38) - - (11) (6) - (17) (7) 19 - - 19 (40) 12 (268) - - - Total operating expenses adjusted 1,492 1,504 1,746 1,091 1,105 1,074 877 878 892 2,647 939 840 869 867 2,576 2,580 3,515 3,520 821 767 816 Pre-tax income/(loss) reported 589 922 575 743 721 736 355 365 291 1,011 331 245 245 300 790 747 1,121 723 223 177 147 Total adjustments 58 (292) (23) 45 9 - 27 13 36 76 (31) (4) 15 8 19 40 (12) 293 23 2 - Pre-tax income/(loss) adjusted 647 630 552 788 730 736 382 378 327 1,087 300 241 260 308 809 787 1,109 1,016 246 179 147

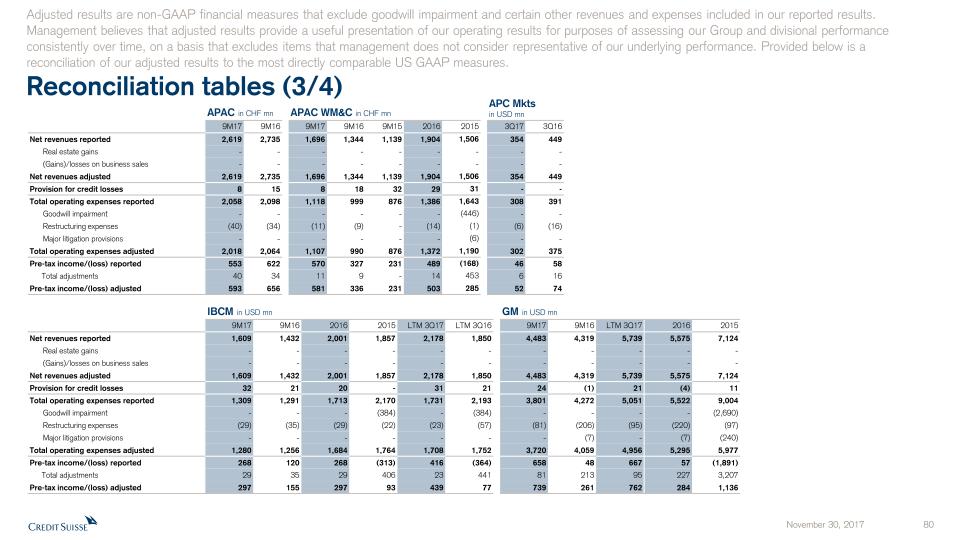

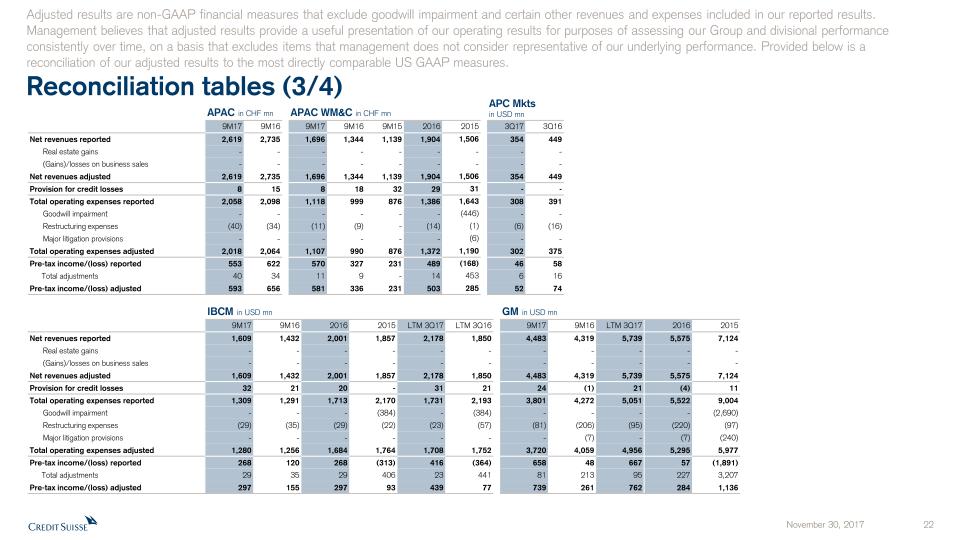

Reconciliation tables (3/4) Adjusted results are non-GAAP financial measures that exclude goodwill impairment and certain other revenues and expenses included in our reported results. Management believes that adjusted results provide a useful presentation of our operating results for purposes of assessing our Group and divisional performance consistently over time, on a basis that excludes items that management does not consider representative of our underlying performance. Provided below is a reconciliation of our adjusted results to the most directly comparable US GAAP measures. APAC in CHF mn APAC WM&C in CHF mn APC Mktsin USD mn 9M17 9M16 9M17 9M16 9M15 2016 2015 3Q17 3Q16 Net revenues reported 2,619 2,735 1,696 1,344 1,139 1,904 1,506 354 449 Real estate gains - - - - - - - - - (Gains)/losses on business sales - - - - - - - - - Net revenues adjusted 2,619 2,735 1,696 1,344 1,139 1,904 1,506 354 449 Provision for credit losses 8 15 8 18 32 29 31 - - Total operating expenses reported 2,058 2,098 1,118 999 876 1,386 1,643 308 391 Goodwill impairment - - - - - - (446) - - Restructuring expenses (40) (34) (11) (9) - (14) (1) (6) (16) Major litigation provisions - - - - - - (6) - - Total operating expenses adjusted 2,018 2,064 1,107 990 876 1,372 1,190 302 375 Pre-tax income/(loss) reported 553 622 570 327 231 489 (168) 46 58 Total adjustments 40 34 11 9 - 14 453 6 16 Pre-tax income/(loss) adjusted 593 656 581 336 231 503 285 52 74 IBCM in USD mn GM in USD mn 9M17 9M16 2016 2015 LTM 3Q17 LTM 3Q16 9M17 9M16 LTM 3Q17 2016 2015 Net revenues reported 1,609 1,432 2,001 1,857 2,178 1,850 4,483 4,319 5,739 5,575 7,124 Real estate gains - - - - - - - - - - - (Gains)/losses on business sales - - - - - - - - - - - Net revenues adjusted 1,609 1,432 2,001 1,857 2,178 1,850 4,483 4,319 5,739 5,575 7,124 Provision for credit losses 32 21 20 - 31 21 24 (1) 21 (4) 11 Total operating expenses reported 1,309 1,291 1,713 2,170 1,731 2,193 3,801 4,272 5,051 5,522 9,004 Goodwill impairment - - - (384) - (384) - - - - (2,690) Restructuring expenses (29) (35) (29) (22) (23) (57) (81) (206) (95) (220) (97) Major litigation provisions - - - - - - - (7) - (7) (240) Total operating expenses adjusted 1,280 1,256 1,684 1,764 1,708 1,752 3,720 4,059 4,956 5,295 5,977 Pre-tax income/(loss) reported 268 120 268 (313) 416 (364) 658 48 667 57 (1,891) Total adjustments 29 35 29 406 23 441 81 213 95 227 3,207 Pre-tax income/(loss) adjusted 297 155 297 93 439 77 739 261 762 284 1,136

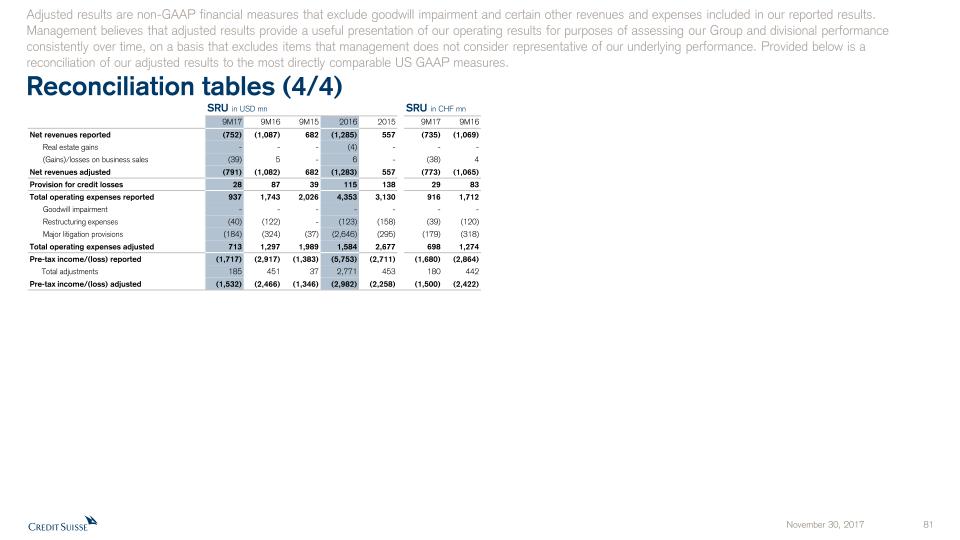

Reconciliation tables (4/4) Adjusted results are non-GAAP financial measures that exclude goodwill impairment and certain other revenues and expenses included in our reported results. Management believes that adjusted results provide a useful presentation of our operating results for purposes of assessing our Group and divisional performance consistently over time, on a basis that excludes items that management does not consider representative of our underlying performance. Provided below is a reconciliation of our adjusted results to the most directly comparable US GAAP measures. SRU in USD mn SRU in CHF mn 9M17 9M16 9M15 2016 2015 9M17 9M16 Net revenues reported (752) (1,087) 682 (1,285) 557 (735) (1,069) Real estate gains - - - (4) - - - (Gains)/losses on business sales (39) 5 - 6 - (38) 4 Net revenues adjusted (791) (1,082) 682 (1,283) 557 (773) (1,065) Provision for credit losses 28 87 39 115 138 29 83 Total operating expenses reported 937 1,743 2,026 4,353 3,130 916 1,712 Goodwill impairment - - - - - - - Restructuring expenses (40) (122) - (123) (158) (39) (120) Major litigation provisions (184) (324) (37) (2,646) (295) (179) (318) Total operating expenses adjusted 713 1,297 1,989 1,584 2,677 698 1,274 Pre-tax income/(loss) reported (1,717) (2,917) (1,383) (5,753) (2,711) (1,680) (2,864) Total adjustments 185 451 37 2,771 453 180 442 Pre-tax income/(loss) adjusted (1,532) (2,466) (1,346) (2,982) (2,258) (1,500) (2,422)

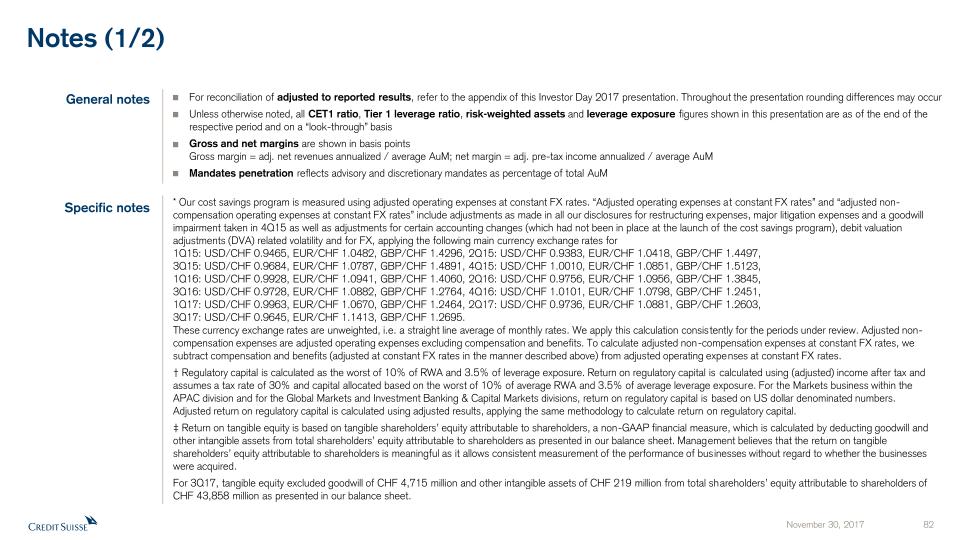

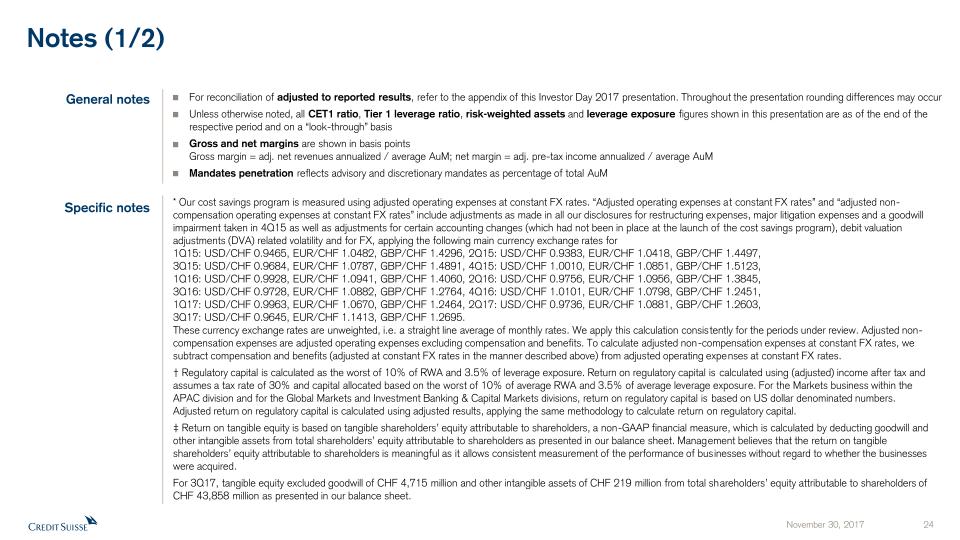

Notes (1/2) For reconciliation of adjusted to reported results, refer to the appendix of this Investor Day 2017 presentation. Throughout the presentation rounding differences may occurUnless otherwise noted, all CET1 ratio, Tier 1 leverage ratio, risk-weighted assets and leverage exposure figures shown in this presentation are as of the end of the respective period and on a “look-through” basisGross and net margins are shown in basis pointsGross margin = adj. net revenues annualized / average AuM; net margin = adj. pre-tax income annualized / average AuMMandates penetration reflects advisory and discretionary mandates as percentage of total AuM General notes Specific notes * Our cost savings program is measured using adjusted operating expenses at constant FX rates. “Adjusted operating expenses at constant FX rates” and “adjusted non-compensation operating expenses at constant FX rates” include adjustments as made in all our disclosures for restructuring expenses, major litigation expenses and a goodwill impairment taken in 4Q15 as well as adjustments for certain accounting changes (which had not been in place at the launch of the cost savings program), debit valuation adjustments (DVA) related volatility and for FX, applying the following main currency exchange rates for1Q15: USD/CHF 0.9465, EUR/CHF 1.0482, GBP/CHF 1.4296, 2Q15: USD/CHF 0.9383, EUR/CHF 1.0418, GBP/CHF 1.4497,3Q15: USD/CHF 0.9684, EUR/CHF 1.0787, GBP/CHF 1.4891, 4Q15: USD/CHF 1.0010, EUR/CHF 1.0851, GBP/CHF 1.5123,1Q16: USD/CHF 0.9928, EUR/CHF 1.0941, GBP/CHF 1.4060, 2Q16: USD/CHF 0.9756, EUR/CHF 1.0956, GBP/CHF 1.3845,3Q16: USD/CHF 0.9728, EUR/CHF 1.0882, GBP/CHF 1.2764, 4Q16: USD/CHF 1.0101, EUR/CHF 1.0798, GBP/CHF 1.2451,1Q17: USD/CHF 0.9963, EUR/CHF 1.0670, GBP/CHF 1.2464, 2Q17: USD/CHF 0.9736, EUR/CHF 1.0881, GBP/CHF 1.2603,3Q17: USD/CHF 0.9645, EUR/CHF 1.1413, GBP/CHF 1.2695.These currency exchange rates are unweighted, i.e. a straight line average of monthly rates. We apply this calculation consistently for the periods under review. Adjusted non-compensation expenses are adjusted operating expenses excluding compensation and benefits. To calculate adjusted non-compensation expenses at constant FX rates, we subtract compensation and benefits (adjusted at constant FX rates in the manner described above) from adjusted operating expenses at constant FX rates.† Regulatory capital is calculated as the worst of 10% of RWA and 3.5% of leverage exposure. Return on regulatory capital is calculated using (adjusted) income after tax and assumes a tax rate of 30% and capital allocated based on the worst of 10% of average RWA and 3.5% of average leverage exposure. For the Markets business within the APAC division and for the Global Markets and Investment Banking & Capital Markets divisions, return on regulatory capital is based on US dollar denominated numbers. Adjusted return on regulatory capital is calculated using adjusted results, applying the same methodology to calculate return on regulatory capital. ‡ Return on tangible equity is based on tangible shareholders’ equity attributable to shareholders, a non-GAAP financial measure, which is calculated by deducting goodwill and other intangible assets from total shareholders’ equity attributable to shareholders as presented in our balance sheet. Management believes that the return on tangible shareholders’ equity attributable to shareholders is meaningful as it allows consistent measurement of the performance of businesses without regard to whether the businesses were acquired.For 3Q17, tangible equity excluded goodwill of CHF 4,715 million and other intangible assets of CHF 219 million from total shareholders’ equity attributable to shareholders of CHF 43,858 million as presented in our balance sheet.

Notes (2/2) Abbreviations Adj. = Adjusted; AI = Artificial Intelligence; AM = Asset Management; AML = Anti-Money Laundering; APAC = Asia Pacific; AT1 = Additional Tier 1; AuM = Assets under Management; BCBS = Basel Committee on Banking Supervision; BIS = Bank for International Settlements; bps = basis points; CAGR = Compound Annual Growth Rate; CCRO = Chief Compliance and Regulatory Affairs Officer; CET1 = Common Equity Tier 1; CIC = Corporate & Institutional Clients; CIF = Customer/Client Information File; Corp. Ctr. = Corporate Center; CVA = Credit Valuation Adjustment; DCM = Debt Capital Markets; EAM = External Asset Manager; ECM = Equity Capital Markets; EM = Emerging Markets; EMEA = Europe, Middle East & Africa; EPS = Earnings Per Share; EQ = Equities; EU = European Union; FICC = Fixed Income, Currencies & Commodities; FINMA = Swiss Financial Market Supervisory Authority; FLP = Fund Linked Products; FRTB = Fundamental Review of the Trading Book; FX = Foreign Exchange; G10 = Group of Ten; GDP = Gross Domestic Product; GM = Global Markets; IBCM = Investment Banking & Capital Markets; IBD = Investment Banking Department; IC = Investment Consultant; IMF = International Monetary Fund; IP = Investor Products; IPO = Initial Public Offering; IRB = Internal Ratings Based; IT = Information Technology; ITS = International Trading Solutions; IWM = International Wealth Management; JV = Joint Venture; LSC = Large Swiss Corporates; M&A = Mergers & Acquisitions; MI = Management Information; Mkts = Markets; NNA = Net new assets; Op Risk = Operational Risk; PB = Private Banking; PC = Private Clients; PEP = Politically Exposed Person; pp = percentage points; PTI = Pre-tax income; PWMC = Private & Wealth Management Clients; RM = Relationship Manager(s); RoRC = Return on Regulatory Capital; RoTE = Return on Tangible Equity; RPA = Robotic Process Automation; RWA = Risk-weighted assets; SA-CCR = Standardized Approach to Counterparty Credit Risk; SME = Small and Medium-Sized Enterprises; SMG = Systematic Market-Making Group; SoW = Share of Wallet; SRU = Strategic Resolution Unit; SUB = Swiss Universal Bank; TBTF = Too Big To Fail; TBVS = Tangible Book Value per Share; (U)HNW(I) = (Ultra) High Net Worth (Individuals); VaR = Value-at-Risk; VIX = Volatility Index; WM = Wealth Management; WM&C = Wealth Management & Connected; YoY = Year over year; YTD = Year to Date

Credit Suisse Investor Day 2017Overview of Capital & FundingDavid Mathers November 30, 2017

Disclaimer This material does not purport to contain all of the information that you may wish to consider. This material is not to be relied upon as such or used in substitution for the exercise of independent judgment.Cautionary statement regarding forward-looking statementsThis presentation contains forward-looking statements that involve inherent risks and uncertainties, and we might not be able to achieve the predictions, forecasts, projections and other outcomes we describe or imply in forward-looking statements. A number of important factors could cause results to differ materially from the plans, objectives, expectations, estimates and intentions we express in these forward-looking statements, including those we identify in "Risk factors” in our Annual Report on Form 20-F for the fiscal year ended December 31, 2016 and in the “Cautionary statement regarding forward-looking information" in our media release relating to Investor Day, published on November 30, 2017 and filed with the US Securities and Exchange Commission, and in other public filings and press releases. We do not intend to update these forward-looking statements. In particular, the terms “Estimate”, “Illustrative”, “Ambition”, “Objective”, “Outlook” and “Goal” are not intended to be viewed as targets or projections, nor are they considered to be Key Performance Indicators. All such estimates, illustrations, ambitions and goals are subject to a large number of inherent risks, assumptions and uncertainties, many of which are completely outside of our control. These risks, assumptions and uncertainties include, but are not limited to, general market conditions, market volatility, interest rate volatility and levels, global and regional economic conditions, political uncertainty, changes in tax policies, regulatory changes, changes in levels of client activity as a result of any of the foregoing and other factors. Accordingly, this information should not be relied on for any purpose. We do not intend to update these estimates, illustrations, ambitions or goals. We may not achieve the benefits of our strategic initiativesWe may not achieve all of the expected benefits of our strategic initiatives. Factors beyond our control, including but not limited to the market and economic conditions, changes in laws, rules or regulations and other challenges discussed in our public filings, could limit our ability to achieve some or all of the expected benefits of these initiatives. Estimates, assumptions and opinionsIn preparing this presentation, management has made estimates and assumptions that affect the numbers presented. Actual results may differ. Annualized numbers do not take account of variations in operating results, seasonality and other factors and may not be indicative of actual, full-year results. Figures throughout this presentation may also be subject to rounding adjustments. All opinions and views constitute judgments as of the date of writing without regard to the date on which the reader may receive or access the information. This information is subject to change at any time without notice and we do not intend to update this information. Statement regarding non-GAAP financial measuresThis presentation also contains non-GAAP financial measures, including adjusted results. Information needed to reconcile such non-GAAP financial measures to the most directly comparable measures under US GAAP can be found in this presentation in the Appendix, which is available on our website at www.credit-suisse.com. Statement regarding capital, liquidity and leverageAs of January 1, 2013, Basel III was implemented in Switzerland along with the Swiss “Too Big to Fail” legislation and regulations thereunder (in each case, subject to certain phase-in periods). As of January 1, 2015, the Bank for International Settlements (BIS) leverage ratio framework, as issued by the Basel Committee on Banking Supervision (BCBS), was implemented in Switzerland by FINMA. Our related disclosures are in accordance with our interpretation of such requirements, including relevant assumptions. Changes in the interpretation of these requirements in Switzerland or in any of our assumptions or estimates could result in different numbers from those shown in this presentation. Capital and ratio numbers for periods prior to 2013 are based on estimates, which are calculated as if the Basel III framework had been in place in Switzerland during such periods. Unless otherwise noted, leverage exposure is based on the BIS leverage ratio framework and consists of period-end balance sheet assets and prescribed regulatory adjustments. Beginning in 2015, the Swiss leverage ratio is calculated as Swiss total capital, divided by period-end leverage exposure. The look-through BIS tier 1 leverage ratio and CET1 leverage ratio are calculated as look-through BIS tier 1 capital and CET1 capital, respectively, divided by end-period leverage exposure.SourcesCertain material in this presentation has been prepared by Credit Suisse on the basis of publicly available information, internally developed data and other third-party sources believed to be reliable. Credit Suisse has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to accuracy, completeness or reliability of such information.

Overview of Capital & Funding Update on cost reduction plans 1 Funding cost update 2 Capital update (including Basel III reforms) 3 RoTE target 4 Capital distribution & dividend plan 5 Financial targets 6

Reducing 2017 costs to ~CHF 18.0 bn from <CHF 18.5 bn;cost base to reduce further to below CHF 17.0 bn in 2018 Note: Illustrative path. Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix 1 2017 estimate based on currently available information and beliefs, expectations and opinions of management as of the date hereof. Actual results for 2017 may differ from any estimates 2 Operating within the range, subject to market conditions and investment opportunities* See Appendix Costs Funding Capital RoTE Dividend Targets Target total of >CHF 4.2 bn of net savings by end-2018 2017 cost target of <CHF 18.5 bn 2015 – 2018 cost reduction program* in CHF bn 1 1 2019-2020Adjusted operating expenses: CHF 16.5-17.0 bn2

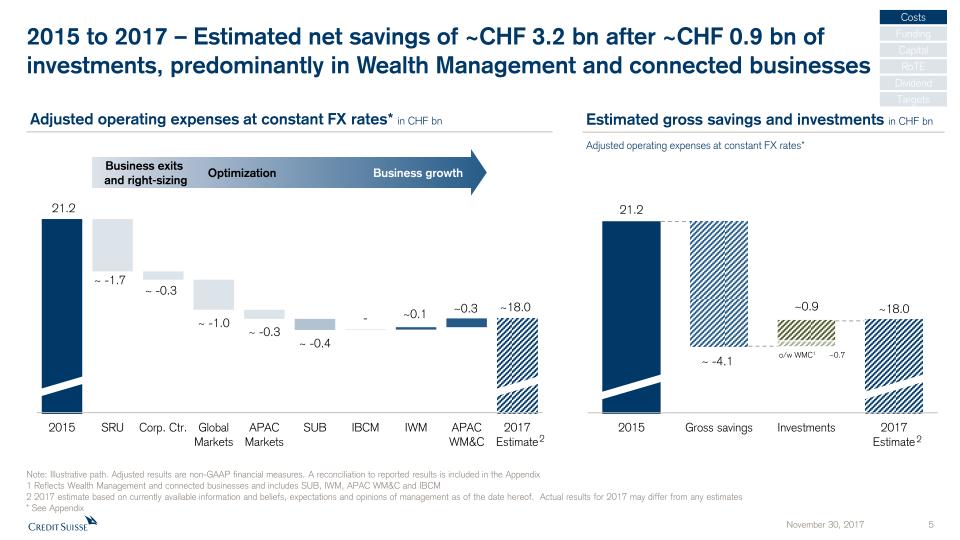

Costs Funding Capital RoTE Dividend Targets Business exits and right-sizing Optimization Business growth Adjusted operating expenses at constant FX rates* in CHF bn Estimated gross savings and investments in CHF bn Adjusted operating expenses at constant FX rates* Note: Illustrative path. Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix1 Reflects Wealth Management and connected businesses and includes SUB, IWM, APAC WM&C and IBCM2 2017 estimate based on currently available information and beliefs, expectations and opinions of management as of the date hereof. Actual results for 2017 may differ from any estimates* See Appendix o/w WMC1 ~0.7 2015 to 2017 – Estimated net savings of ~CHF 3.2 bn after ~CHF 0.9 bn of investments, predominantly in Wealth Management and connected businesses 2 2

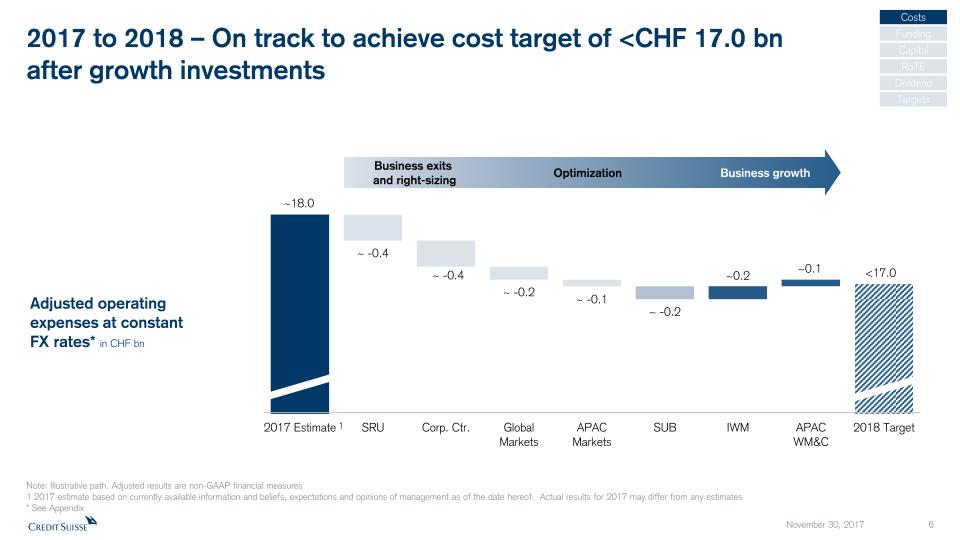

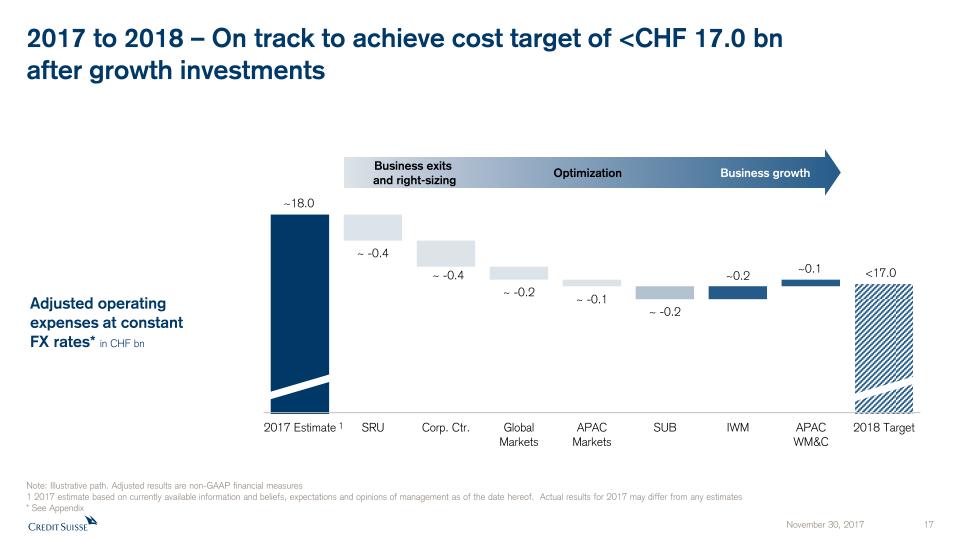

2017 to 2018 – On track to achieve cost target of <CHF 17.0 bnafter growth investments Costs Funding Capital RoTE Dividend Targets Business exits and right-sizing Business growth Adjusted operating expenses at constant FX rates* in CHF bn Note: Illustrative path. Adjusted results are non-GAAP financial measures1 2017 estimate based on currently available information and beliefs, expectations and opinions of management as of the date hereof. Actual results for 2017 may differ from any estimates* See Appendix 1 Optimization

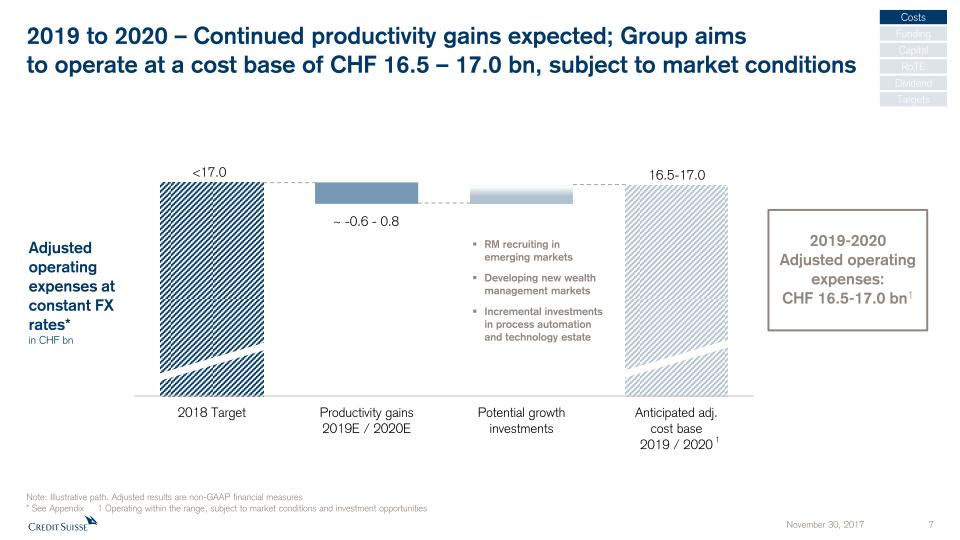

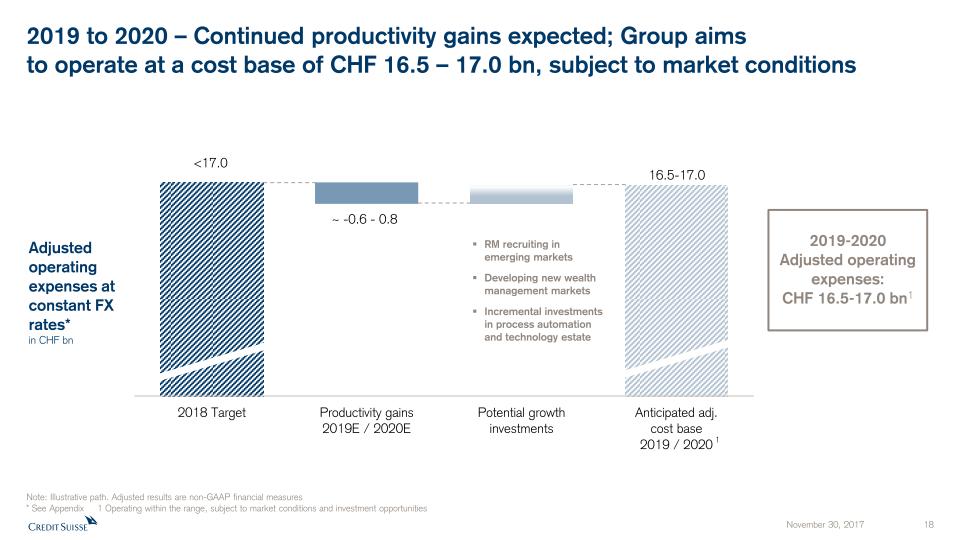

2019 to 2020 – Continued productivity gains expected; Group aims to operate at a cost base of CHF 16.5 – 17.0 bn, subject to market conditions Costs Funding Capital Dividend Targets RM recruiting in emerging marketsDeveloping new wealth management marketsIncremental investments in process automation and technology estate 1 ~ -0.6 - 0.8 16.5-17.0 Adjusted operating expenses at constant FX rates*in CHF bn Note: Illustrative path. Adjusted results are non-GAAP financial measures* See Appendix 1 Operating within the range, subject to market conditions and investment opportunities RoTE 2019-2020Adjusted operating expenses: CHF 16.5-17.0 bn1

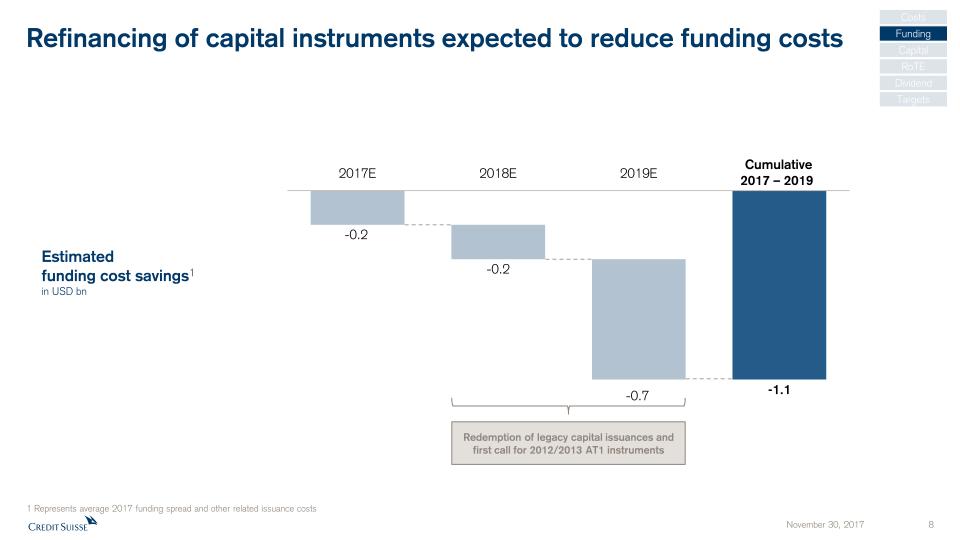

Refinancing of capital instruments expected to reduce funding costs Costs Funding Capital Dividend Targets Estimatedfunding cost savings1in USD bn Cumulative2017 – 2019 Redemption of legacy capital issuances and first call for 2012/2013 AT1 instruments RoTE 1 Represents average 2017 funding spread and other related issuance costs

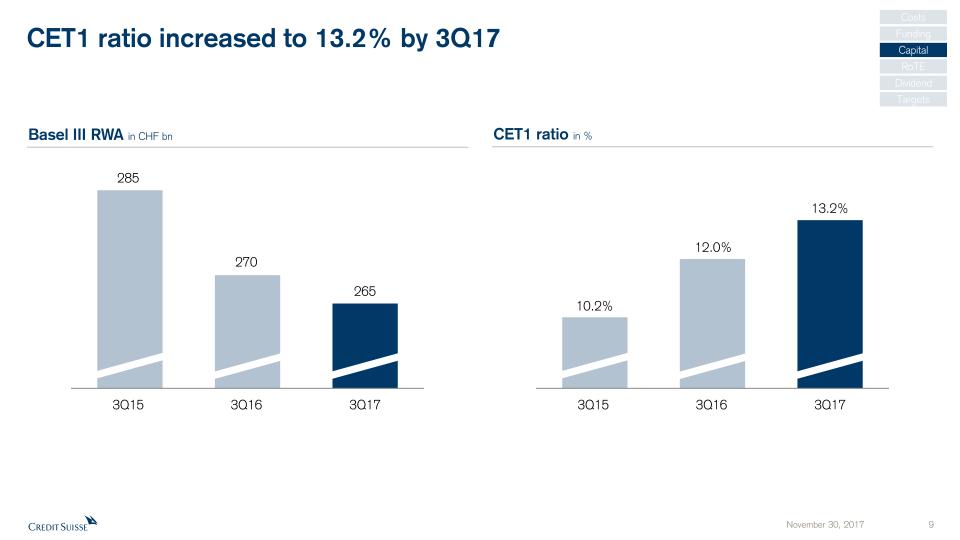

CET1 ratio increased to 13.2% by 3Q17 285 265 10.2% 12.0% 3Q15 3Q16 Basel III RWA in CHF bn CET1 ratio in % 270 3Q17 13.2% 3Q15 3Q16 3Q17 Costs Funding Capital Dividend Targets RoTE

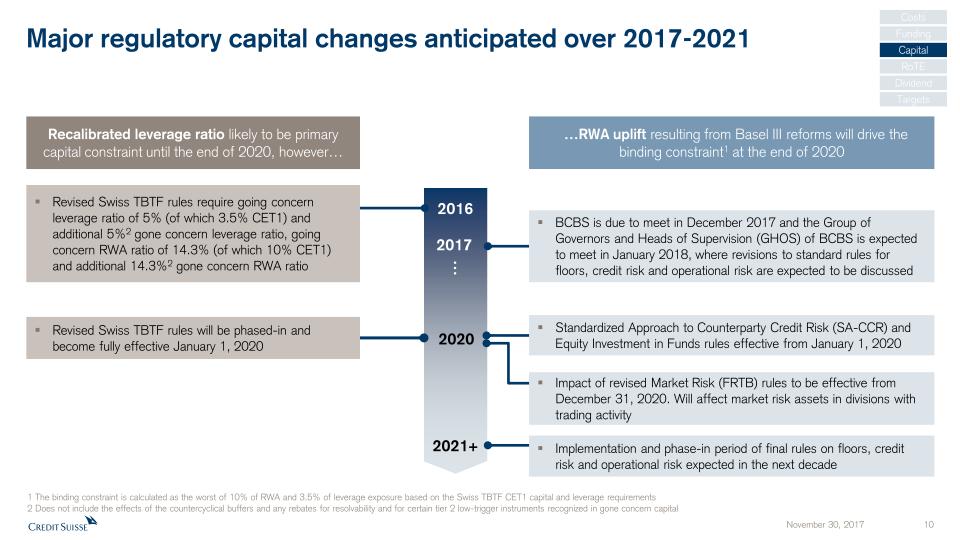

Recalibrated leverage ratio likely to be primary capital constraint until the end of 2020, however… 1 The binding constraint is calculated as the worst of 10% of RWA and 3.5% of leverage exposure based on the Swiss TBTF CET1 capital and leverage requirements2 Does not include the effects of the countercyclical buffers and any rebates for resolvability and for certain tier 2 low-trigger instruments recognized in gone concern capital …RWA uplift resulting from Basel III reforms will drive the binding constraint1 at the end of 2020 2017 Standardized Approach to Counterparty Credit Risk (SA-CCR) and Equity Investment in Funds rules effective from January 1, 2020 2020 2021+ Revised Swiss TBTF rules will be phased-in and become fully effective January 1, 2020 2016 BCBS is due to meet in December 2017 and the Group of Governors and Heads of Supervision (GHOS) of BCBS is expected to meet in January 2018, where revisions to standard rules for floors, credit risk and operational risk are expected to be discussed Revised Swiss TBTF rules require going concern leverage ratio of 5% (of which 3.5% CET1) and additional 5%2 gone concern leverage ratio, going concern RWA ratio of 14.3% (of which 10% CET1) and additional 14.3%2 gone concern RWA ratio Major regulatory capital changes anticipated over 2017-2021 Implementation and phase-in period of final rules on floors, credit risk and operational risk expected in the next decade … Costs Funding Capital Dividend RoTE Impact of revised Market Risk (FRTB) rules to be effective from December 31, 2020. Will affect market risk assets in divisions with trading activity Targets

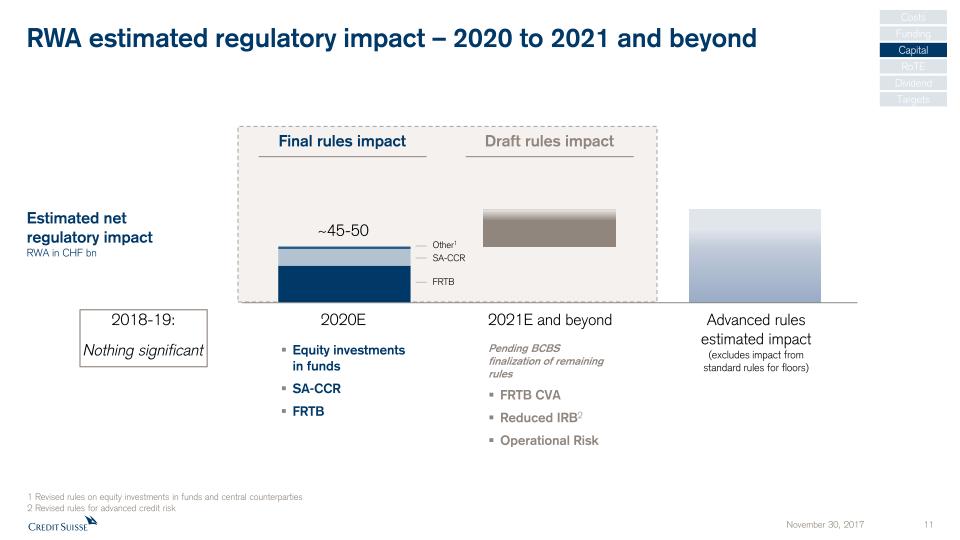

RWA estimated regulatory impact – 2020 to 2021 and beyond 2020E 2021E and beyond Advanced rules estimated impact (excludes impact from standard rules for floors) Equity investments in fundsSA-CCRFRTB Final rules impact Pending BCBS finalization of remaining rulesFRTB CVAReduced IRB2Operational Risk Draft rules impact Estimated netregulatory impactRWA in CHF bn Costs Funding Capital Dividend Targets 1 Revised rules on equity investments in funds and central counterparties2 Revised rules for advanced credit risk FRTB SA-CCR Other1 RoTE 2018-19:Nothing significant

Our focus on execution is driving our overall return on capital higher Costs Funding Capital Dividend Targets RoTE As per 3Q17 results

Most of the expected profit improvements to 2019 from knownactions… Return on tangible equity‡ developmentbased on CHF Revenue growth primarily from WMC businesses1 & additional cost initiatives Known actions &cost initiatives Note: Illustrative path. RoTE (a non-GAAP financial measure) on a reported basis1 WMC businesses reflects Wealth Management and connected businesses and includes SUB, IWM, APAC WM&C and IBCM‡ See Appendix Costs Funding Capital Dividend Targets RoTE

…over which we have clear visibility 2 1 1 Note: Illustrative path. RoTE (a non-GAAP financial measure) on a reported basis1 Excludes restructuring and litigation expenses 2 Excludes funding and other operating expenses from SRU and Corporate Center; includes tax effect‡ See Appendix RoTE‡ impact of known actions & cost initiativesfrom 9M17 to 2019based on CHF Improvement in reported RoTE‡ Costs Funding Capital Dividend Targets RoTE

Anticipated usage of cumulative capital generated Strengthening capital generation provides increasing returns to shareholders RoTE‡ @ 11% RoTE‡ @ 10% RoTE‡ @ 12% RoTE‡ @ 11% Implied combined net income generation of~CHF 9-10 bn in 2019 and 20201 Net income generation1 in CHF bn ~20% for investment in wealth management and connected businesses2~30% for RWA uplift resulting from Basel III reforms and other contingencies50% of net income to be distributed to shareholders primarily through share buybacks or special dividend Note: RoTE (a non-GAAP financial measure) on a reported basis1 Estimated net income generation based on RoTE targets for respective years. Estimate based on currently available information and beliefs, expectations and opinions of management as of the date hereof. Actual results for 2019 and 2020 may differ from any estimates 2 Includes SUB, IWM, APAC WM&C and IBCM ‡ See Appendix Costs Funding Capital Dividend Targets RoTE

Overview of 2018 financial targets Group Net cost savings*Operating cost base*CET1 ratioCET1 / Tier 1 leverage ratio SUB Pre-tax income CHF 2.3 bn IWM Pre-tax income CHF 1.8 bn >CHF 4.2 bn<CHF 17.0 bn>12.5%>3.5% / >5.0% Adjusted figures 10-15%1 APAC Markets Return on regulatory capital† Global Markets RWA thresholdLeverage exposure thresholdReturn on regulatory capital† USD 60 bnUSD 290 bn10-15% APAC WM&C Pre-tax income CHF 0.85 bn 15-20% IBCM Return on regulatory capital† SRU Pre-tax loss 2018Pre-tax loss 2019RWA excl. Op RiskLeverage exposure ~USD 1.4 bn~USD 0.5 bn2USD 11 bn2USD 40 bn2 (cumulative since 2015) Note: Adjusted results are non-GAAP financial measures *, † See Appendix 1 Targeted for 2019 2 SRU program will be economically completed by end-2018; residual operations and assets to be absorbed into the rest of Group from 2019 onwards Costs Funding Capital RoTE Dividend Targets

New Group financial objectives for 2019 and 2020 Costs Funding Capital Dividend Targets Group Reported RoTE‡ Net savings / operating cost base* CET1 ratio Intend to increase RoTE to 10-11% by 2019 and 11-12% by 2020Increasing RoTE to drive higher tangible book value per share (TBVPS) Intend to operate at a cost base of CHF 16.5 bn – CHF 17.0 bn between 2019-20201 Intend to operate at >12.5% pre Basel III reforms Note: Adjusted results are non-GAAP financial measures. RoTE (a non-GAAP financial measure) on a reported basis1 Operating within the range, subject to market conditions and investment opportunities *, ‡ See Appendix RoTE Capital distribution Return 50% of net income earned cumulatively in 2019 and 2020 to shareholders primarily through share buybacks or special dividend

Appendix November 30, 2017 18

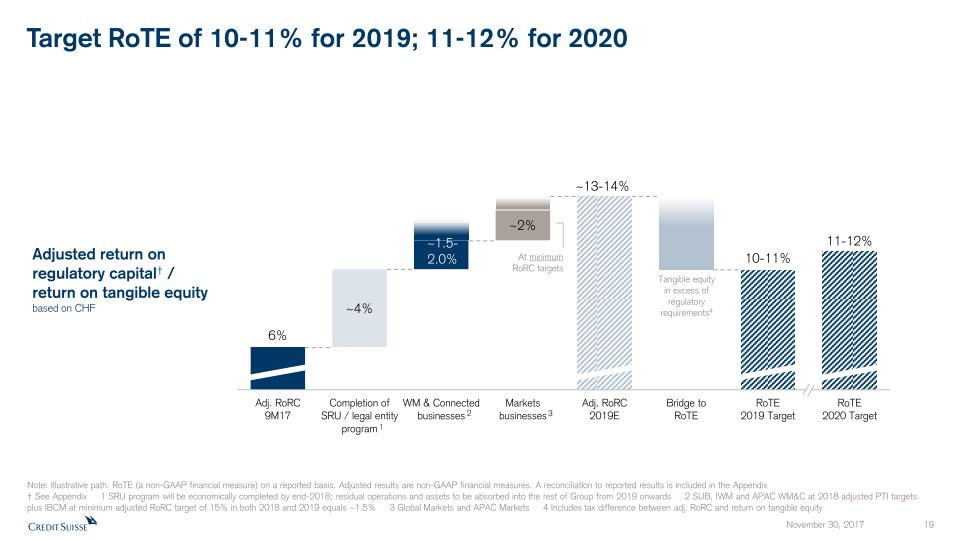

Target RoTE of 10-11% for 2019; 11-12% for 2020 Tangible equity in excess of regulatory requirements4 Adjusted return on regulatory capital† /return on tangible equity based on CHF ~13-14% At minimumRoRC targets Note: Illustrative path. RoTE (a non-GAAP financial measure) on a reported basis. Adjusted results are non-GAAP financial measures. A reconciliation to reported results is included in the Appendix† See Appendix 1 SRU program will be economically completed by end-2018; residual operations and assets to be absorbed into the rest of Group from 2019 onwards 2 SUB, IWM and APAC WM&C at 2018 adjusted PTI targets plus IBCM at minimum adjusted RoRC target of 15% in both 2018 and 2019 equals ~1.5% 3 Global Markets and APAC Markets 4 Includes tax difference between adj. RoRC and return on tangible equity 2 3 1

Reconciliation tables (1/4) Adjusted results are non-GAAP financial measures that exclude goodwill impairment and certain other revenues and expenses included in our reported results. Management believes that adjusted results provide a useful presentation of our operating results for purposes of assessing our Group and divisional performance consistently over time, on a basis that excludes items that management does not consider representative of our underlying performance. Provided below is a reconciliation of our adjusted results to the most directly comparable US GAAP measures. Group in CHF mn Core in CHF mn SUB, IWM and APAC WM&C in CHF mn 9M17 9M16 9M17 9M16 9M17 9M16 Net revenues reported 15,711 15,142 16,446 16,211 9,521 9,103 Fair value on own debt - - - - - - Real estate gains - (346) - (346) - (346) (Gains)/losses on business sales (15) 56 23 52 - - Net revenues adjusted 15,696 14,852 16,469 15,917 9,521 8,757 Provision for credit losses 167 177 138 94 81 77 Total operating expenses reported 13,892 15,028 12,976 13,316 6,527 6,266 Goodwill impairment - - - - - - Restructuring expenses (318) (491) (279) (371) (131) (110) Major litigation provisions (238) (306) (59) 12 (59) 19 Total operating expenses adjusted 13,336 14,231 12,638 12,957 6,337 6,175 Pre-tax income/(loss) reported 1,652 (63) 3,332 2,801 2,913 2,760 Total adjustments 541 507 361 65 190 (255) Pre-tax income/(loss) adjusted 2,193 444 3,693 2,866 3,103 2,505 CS Group in CHF mn 3Q17 2Q17 1Q17 4Q16 3Q16 2Q16 1Q16 4Q15 3Q15 2Q15 1Q15 4Q14 3Q14 2Q14 1Q14 9M17 2016 2015 Total operating expenses reported 4,540 4,541 4,812 7,309 5,119 4,937 4,972 10,518 5,023 5,248 5,106 5,406 5,181 6,790 5,052 13,892 22,337 25,895 Goodwill impairment - - - - - - - (3,797) - - - - - - - - - (3,797) Restructuring expenses (112) (69) (137) (49) (145) (91) (255) (355) - - - - - - - (318) (540) (355) Major litigation provisions (108) (31) (97) (2,401) (306) - - (563) (204) (63) 10 (393) (290) (1,711) (42) (238) (2,707) (820) Debit valuation adjustments (DVA) (20) (17) (26) - - - - - - - - - - - - (63) - - Certain accounting changes (49) (53) (25) - - - - - - - - - - - - (125) - - Total operating expenses adjusted 4,251 4,371 4,527 4,859 4,668 4,846 4,717 5,803 4,819 5,185 5,116 5,013 4,891 5,079 5,010 13,148 19,090 20,923 FX adjustment 106 101 69 70 120 70 33 - 62 137 120 (54) 55 161 189 277 292 319 FX neutral total operating expenses adjusted 4,357 4,472 4,596 4,929 4,788 4,916 4,750 5,803 4,881 5,322 5,236 4,959 4,946 5,240 5,199 13,425 19,382 21,242

Reconciliation tables (2/4) Adjusted results are non-GAAP financial measures that exclude goodwill impairment and certain other revenues and expenses included in our reported results. Management believes that adjusted results provide a useful presentation of our operating results for purposes of assessing our Group and divisional performance consistently over time, on a basis that excludes items that management does not consider representative of our underlying performance. Provided below is a reconciliation of our adjusted results to the most directly comparable US GAAP measures. SUB in CHF mn 3Q17 2Q17 1Q17 4Q16 3Q16 2Q16 1Q16 4Q15 3Q15 2Q15 1Q15 9M17 9M16 9M15 2016 2015 Net revenues reported 1,319 1,405 1,354 1,399 1,667 1,337 1,356 1,495 1,364 1,462 1,400 4,078 4,360 4,226 5,759 5,721 Real estate gains - - - (20) (346) - - (72) - (23) - - (346) (23) (366) (95) (Gains)/losses on business sales - - - - - - - (23) - - - - - - - (23) Net revenues adjusted 1,319 1,405 1,354 1,379 1,321 1,337 1,356 1,400 1,364 1,439 1,400 4,078 4,014 4,203 5,393 5,603 Provision for credit losses 14 36 10 34 30 9 6 43 39 33 23 60 45 95 79 138 Total operating expenses reported 879 867 940 983 879 875 918 1,088 925 961 934 2,686 2,672 2,820 3,655 3,908 Goodwill impairment - - - - - - - - - - - - - - - - Restructuring expenses (13) 4 (52) 3 (19) (4) (40) (42) - - - (61) (63) - (60) (42) Major litigation provisions (9) (6) (27) (19) - - - (25) - - - (42) - - (19) (25) Total operating expenses adjusted 857 865 861 967 860 871 878 1,021 925 961 934 2,583 2,609 2,820 3,576 3,841 Pre-tax income/(loss) reported 426 502 404 382 758 453 432 364 400 468 443 1,332 1,643 1,311 2,025 1,675 Total adjustments 22 2 79 (4) (327) 4 40 (28) - (23) - 103 (283) (23) (287) (51) Pre-tax income/(loss) adjusted 448 504 483 378 431 457 472 336 400 445 443 1,435 1,360 1,288 1,738 1,624 SUB PC in CHF mn SUB C&ICin CHF mn IWM in CHF mn IWM AM in CHF mn 9M17 9M16 9M15 9M17 9M16 9M15 3Q17 2Q17 1Q17 9M17 4Q16 3Q16 2Q16 1Q16 9M16 9M15 2016 2015 9M17 9M16 9M15 Net revenues reported 2,171 2,509 2,356 1,907 1,851 1,870 1,262 1,264 1,221 3,747 1,299 1,081 1,145 1,173 3,399 3,379 4,698 4,552 1,067 946 963 Real estate gains - (346) (23) - - - - - - - (54) - - - - - (54) - - - - (Gains)/losses on business sales - - - - - - - - - - - - - - - - - (11) - - - Net revenues adjusted 2,171 2,163 2,333 1,907 1,851 1,870 1,262 1,264 1,221 3,747 1,245 1,081 1,145 1,173 3,399 3,379 4,644 4,541 1,067 946 963 Provision for credit losses 32 29 35 28 16 60 3 8 2 13 6 0 16 (2) 14 12 20 5 - - - Total operating expenses reported 1,550 1,558 1,746 1,136 1,114 1,074 904 891 928 2,723 962 836 884 875 2,595 2,620 3,557 3,824 844 769 816 Goodwill impairment - - - - - - - - - - - - - - - - - - - - - Restructuring expenses (54) (54) - (7) (9) - (16) (7) (36) (59) (16) (15) (15) (8) (38) - (54) (36) (23) (2) - Major litigation provisions (4) - - (38) - - (11) (6) - (17) (7) 19 - - 19 (40) 12 (268) - - - Total operating expenses adjusted 1,492 1,504 1,746 1,091 1,105 1,074 877 878 892 2,647 939 840 869 867 2,576 2,580 3,515 3,520 821 767 816 Pre-tax income/(loss) reported 589 922 575 743 721 736 355 365 291 1,011 331 245 245 300 790 747 1,121 723 223 177 147 Total adjustments 58 (292) (23) 45 9 - 27 13 36 76 (31) (4) 15 8 19 40 (12) 293 23 2 - Pre-tax income/(loss) adjusted 647 630 552 788 730 736 382 378 327 1,087 300 241 260 308 809 787 1,109 1,016 246 179 147