As filed with the Securities and Exchange Commission on 25 February 2020

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

o REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR 12(g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended 31 December 2019

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

o SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission file number 001-15246

LLOYDS BANKING GROUP plc

(previously Lloyds TSB Group plc)

(Exact name of Registrant as Specified in Its Charter)

Scotland

(Jurisdiction of Incorporation or Organization)

25 Gresham Street

London EC2V 7HN

United Kingdom

(Address of Principal Executive Offices)

Kate Cheetham, Company Secretary

Tel +44 (0) 20 7356 2104, Fax +44 (0) 20 7356 1808

25 Gresham Street

London EC2V 7HN

United Kingdom

(Name, telephone, e-mail and/or facsimile number and address of Company contact person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading symbol | Name of each exchange on which registered |

| Ordinary shares of nominal value 10 pence each, represented by American Depositary Shares | | The New York Stock Exchange |

| $1,500,000,000 4.344% Subordinated Securities due in 2048 | LYG48A | The New York Stock Exchange |

| $824,033,000 5.3% Subordinated Securities due 2045 | LYG45 | The New York Stock Exchange |

| $1,750,000,000 3.574% Senior Notes due in 2028 (callable in 2027) | LYG28A | The New York Stock Exchange |

| $1,500,000,000 4.375% Senior Notes due 2028 | LYG28B | The New York Stock Exchange |

| $1,250,000,000 4.55% Senior Notes due 2028 | LYG28C | The New York Stock Exchange |

| $1,250,000,000 3.75% Senior Notes due 2027 | LYG27 | The New York Stock Exchange |

| $1,500,000,000 4.65% Subordinated Securities due 2026 | LYG26 | The New York Stock Exchange |

| $1,500,000,000 4.45% Senior Notes due 2025 | LYG25A | The New York Stock Exchange |

| $1,327,685,000 4.582% Subordinated Securities due 2025 | LYG25 | The New York Stock Exchange |

| $1,250,000,000 3.5% Senior Notes due 2025 | LYG25 | The New York Stock Exchange |

| $1,000,000,000 3.90% Senior Notes due 2024 | LYG24A | The New York Stock Exchange |

| $1,000,000,000 4.5% Subordinated Securities due 2024 | LYG24 | The New York Stock Exchange |

| $1,500,000,000 2.858% Senior Notes due 2023 | LYG23B | The New York Stock Exchange |

| $1,750,000,000 4.05% Senior Notes due 2023 | LYG23A | The New York Stock Exchange |

| $2,250,000,000 2.907% Senior Notes due 2023 (callable in 2022) | LYG23 | The New York Stock Exchange |

| $1,500,000,000 3.0% Senior Notes due 2022 | LYG22 | The New York Stock Exchange |

| $1,500,000,000 2.25% Senior Notes due 2022 | LYG22 | The New York Stock Exchange |

| $1,250,000,000 3.3% Senior Notes due 2021 | LYG21A | The New York Stock Exchange |

| $1,000,000,000 Floating Rate Senior Notes due 2021 | LYG21B | The New York Stock Exchange |

| $500,000,000 Floating Rate Senior Notes due 2021 | LYG21A | The New York Stock Exchange |

| $1,000,000,000 3.1% Senior Notes due 2021 | LYG21 | The New York Stock Exchange |

| $2,500,000,000 6.375% Senior Notes due 2021 | LYG21 | The New York Stock Exchange |

| $1,000,000,000 2.7% Senior Notes due 2020 | LYG20A | The New York Stock Exchange |

| $1,000,000,000 2.4% Senior Notes due 2020 | LYG20 | The New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

7.50% Fixed Rate Reset Additional Tier 1 Perpetual Subordinated Contingent Convertible Securities

6.75% Callable Fixed Rate Reset AT1 Perpetual Subordinated Contingent Convertible Securities

5.125% Callable Fixed Rate Reset AT1 Perpetual Subordinated Contingent Convertible Securities

The number of outstanding shares of each of Lloyds Banking Group plc’s classes of capital or common stock as of 31 December 2019 was:

| Ordinary shares, nominal value 10 pence each | | | 70,052,557,838 |

| Preference shares, nominal value 25 pence each | | | 412,201,226 |

| Preference shares, nominal value 25 cents each | | | 809,160 |

| Preference shares, nominal value 25 euro cents each | | | Nil |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes x No o

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes o No x

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company.

See the definitions of “large accelerated filer,” “accelerated filer,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer x Accelerated filer o Non-Accelerated filer o Emerging Growth Company o

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards†provided pursuant to Section 13(a) of the Exchange Act.

Yes o No o

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements including in this filing:

U.S. GAAP o International Financial Reporting Standards as issued by the International Accounting Standards Board x Other o

If ‘Other’ has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

Item 17 o Item o 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No x

†The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

PRESENTATION OF INFORMATION

In this annual report, references to the ‘Company’ are to Lloyds Banking Group plc; references to ‘Lloyds Banking Group’, ‘Lloyds’ or the ‘Group’ are to Lloyds Banking Group plc and its subsidiary and associated undertakings; references to ‘Lloyds Bank’ are to Lloyds Bank plc; and references to the ‘consolidated financial statements’ or ‘financial statements’ are to Lloyds Banking Group’s consolidated financial statements included in this annual report. References to the ‘Financial Conduct Authority’ or ‘FCA’ and to the ‘Prudential Regulation Authority’ or ‘PRA’ are to the United Kingdom (the UK) Financial Conduct Authority and the UK Prudential Regulation Authority. References to the ‘Financial Services Authority’ or ‘FSA’ are to their predecessor organisation, the UK Financial Services Authority.

The consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB). Certain disclosures required by IFRS have been included in sections highlighted as ‘Audited’ within the Operating and financial review and prospects section of this Annual Report on Form 20-F on pages 15 to 112. Disclosures marked as audited indicate that they are within the scope of the audit of the financial statements taken as a whole; these disclosures are not subject to a separate opinion.

In this annual report, amounts described as ‘statutory’ refer to amounts included within the Group’s consolidated financial statements.

Lloyds Banking Group publishes its consolidated financial statements expressed in British pounds (‘pounds sterling’, ‘sterling’ or ‘£’), the lawful currency of the UK. In this annual report, references to ‘pence’ and ‘p’ are to one-hundredth of one pound sterling; references to ‘US dollars’, ‘US$’ or ‘$’ are to the lawful currency of the United States (the US); references to ‘cent’ or ‘c’ are to one-hundredth of one US dollar; references to ‘euro’ or ‘€’ are to the lawful currency of the member states of the European Union (EU) that have adopted a single currency in accordance with the Treaty establishing the European Communities, as amended by the Treaty of European Union; references to ‘euro cent’ are to one-hundredth of one euro; and references to ‘Japanese yen’, ‘Japanese ¥’ or ‘¥’ are to the lawful currency of Japan. Solely for the convenience of the reader, this annual report contains translations of certain pounds sterling amounts into US dollars at specified rates. These translations should not be construed as representations by Lloyds Banking Group that the pounds sterling amounts actually represent such US dollar amounts or could be converted into US dollars at the rate indicated or at any other rate. Unless otherwise stated, the translations of pounds sterling into US dollars have been made at the noon buying rate in New York City for cable transfers in pounds sterling as certified for customs purposes by the Federal Reserve Bank of New York (the Noon Buying Rate) in effect on 31 December 2019. The Noon Buying Rate on 31 December 2019 differs from certain of the actual rates used in the preparation of the consolidated financial statements, which are expressed in pounds sterling, and therefore US dollar amounts appearing in this annual report may differ significantly from actual US dollar amounts which were translated into pounds sterling in the preparation of the consolidated financial statements in accordance with IFRS.

BUSINESS OVERVIEW

Lloyds Banking Group is a leading provider of financial services to individual and business customers in the UK. At 31 December 2019, Lloyds Banking Group’s total assets were £833,893 million and Lloyds Banking Group had 63,069 employees (on a full-time equivalent basis). Lloyds Banking Group plc’s market capitalisation at that date was £43,783 million. The Group reported a profit before tax for the 12 months to 31 December 2019 of £4,393 million, and its capital ratios at that date were 21.3 per cent for total capital, 16.7 per cent for tier 1 capital and 13.6 per cent for common equity tier 1 capital.

Set out below is the Group’s summarised income statement for each of the last two years:

| | | 2019

£m | | | 2018

£m | |

| Net interest income | | | 10,180 | | | | 13,396 | |

| Other income | | | 32,176 | | | | 8,695 | |

| Total income | | | 42,356 | | | | 22,091 | |

| Insurance claims | | | (23,997 | ) | | | (3,465 | ) |

| Total income, net of insurance claims | | | 18,359 | | | | 18,626 | |

| Operating expenses | | | (12,670 | ) | | | (11,729 | ) |

| Trading surplus | | | 5,689 | | | | 6,897 | |

| Impairment | | | (1,296 | ) | | | (937 | ) |

| Profit before tax | | | 4,393 | | | | 5,960 | |

Lloyds Banking Group’s main business activities are retail and commercial banking and long-term savings, protection and investment and it operates primarily in the UK. Services are offered through a number of well recognised brands including Lloyds Bank, Halifax, Bank of Scotland and Scottish Widows, and through a range of distribution channels including the largest branch network and digital bank in the UK.

At 31 December 2019, the Group’s three primary operating divisions, which are also financial reporting segments, were: Retail; Commercial Banking; and Insurance and Wealth. Retail provides banking, mortgages, personal loans, motor finance, credit cards and other financial services to personal and small business customers. Commercial Banking provides banking and related services to business clients, from small and medium-sized entities (SMEs) to large corporates. Insurance and Wealth provides long-term savings, protection and investment products as well as general insurance products.

Profit before tax is analysed on pages 17 to 22 on a statutory basis and, for the Group’s segments, on pages 24 to 30 on an underlying basis. The key principles adopted in the preparation of this basis of reporting are described on page 24. The Group Executive Committee, which is the chief operating decision maker for the Group, reviews the Group’s internal reporting based around these segments (which reflect the Group’s organisational and management structures) in order to assess performance and allocate resources; this reporting is on an underlying basis. IFRS 8,Operating Segmentsrequires that the Group presents its segmental profit before tax on the basis reviewed by the chief operating decision maker that is most consistent with the measurement principles used in measuring the Group’s statutory profit before tax. Accordingly, the Group presents its segmental underlying basis profit before tax in note 4 to the financial statements in compliance with IFRS 8. The table below shows the results of Lloyds Banking Group’s segments in the last two fiscal years, and their aggregation. Further information on non-GAAP measures and the reconciliations required by the Securities and Exchange Commission’s Regulation G are set out on pages F-25 to F-29.

| | | 2019

£m | | | 2018

£m | 1

|

| Retail | | | 3,839 | | | | 4,211 | |

| Commercial Banking | | | 1,777 | | | | 2,183 | |

| Insurance and Wealth | | | 1,101 | | | | 927 | |

| Other | | | 814 | | | | 745 | |

| Profit before tax – underlying basis | | | 7,531 | | | | 8,066 | |

| 1 | Segmental analysis restated, as explained on page F-25. |

Lloyds Banking Group plc was incorporated as a public limited company and registered in Scotland under the UK Companies Act 1985 on 21 October 1985 with the registered number 95000. Lloyds Banking Group plc’s registered office is The Mound, Edinburgh EH1 1YZ, Scotland, and its principal executive offices in the UK are located at 25 Gresham Street, London EC2V 7HN, United Kingdom, telephone number + 44 (0) 20 7626 1500.

SELECTED CONSOLIDATED FINANCIAL DATA

The financial information set out in the tables below has been derived from the annual reports and accounts of Lloyds Banking Group plc for each of the past five years adjusted, where restatement was required, for subsequent changes in accounting policy and presentation.

| | | | 2019 | | | | 20181,2 | | | | 20171,2,3 | | | | 20161,2,3 | | | | 20151,2,3 | |

| Income statement data for the year ended 31 December (£m) | | | | | | | | | | | | | | | | | | | | |

| Total income, net of insurance claims | | | 18,359 | | | | 18,626 | | | | 18,659 | | | | 17,267 | | | | 17,421 | |

| Operating expenses | | | (12,670 | ) | | | (11,729 | ) | | | (12,346 | ) | | | (12,627 | ) | | | (15,387 | ) |

| Trading surplus | | | 5,689 | | | | 6,897 | | | | 6,313 | | | | 4,640 | | | | 2,034 | |

| Impairment losses | | | (1,296 | ) | | | (937 | ) | | | (688 | ) | | | (752 | ) | | | (390 | ) |

| Profit before tax | | | 4,393 | | | | 5,960 | | | | 5,625 | | | | 3,888 | | | | 1,644 | |

| Profit for the year | | | 3,006 | | | | 4,506 | | | | 3,999 | | | | 2,255 | | | | 1,036 | |

| Profit for the year attributable to ordinary shareholders | | | 2,459 | | | | 3,975 | | | | 3,494 | | | | 1,742 | | | | 546 | |

| Dividends for the year4,5 | | | 2,375 | | | | 2,288 | | | | 2,195 | | | | 2,175 | | | | 1,962 | |

| Balance sheet data at 31 December (£m) | | | | | | | | | | | | | | | | | | | | |

| Share capital | | | 7,005 | | | | 7,116 | | | | 7,197 | | | | 7,146 | | | | 7,146 | |

| Shareholders’ equity | | | 41,697 | | | | 43,434 | | | | 43,551 | | | | 42,670 | | | | 41,234 | |

| Other equity instruments | | | 5,906 | | | | 6,491 | | | | 5,355 | | | | 5,355 | | | | 5,355 | |

| Customer deposits | | | 421,320 | | | | 418,066 | | | | 418,124 | | | | 415,460 | | | | 418,326 | |

| Subordinated liabilities | | | 17,130 | | | | 17,656 | | | | 17,922 | | | | 19,831 | | | | 23,312 | |

| Loans and advances to customers | | | 494,988 | | | | 484,858 | | | | 472,498 | | | | 457,958 | | | | 455,175 | |

| Total assets | | | 833,893 | | | | 797,598 | | | | 812,109 | | | | 817,793 | | | | 806,688 | |

| Share information | | | | | | | | | | | | | | | | | | | | |

| Basic earnings per ordinary share | | | 3.5p | | | | 5.5p | | | | 4.9p | | | | 2.4p | | | | 0.8p | |

| Diluted earnings per ordinary share | | | 3.4p | | | | 5.5p | | | | 4.8p | | | | 2.4p | | | | 0.8p | |

| Net asset value per ordinary share | | | 59.5p | | | | 61.0p | | | | 60.5p | | | | 59.8p | | | | 57.9p | |

| Dividends per ordinary share4,6 | | | 3.37p | | | | 3.21p | | | | 3.05p | | | | 3.05p | | | | 2.75p | |

| Equivalent cents per share6,7 | | | 4.33c | | | | 4.14c | | | | 4.06c | | | | 3.95c | | | | 4.03c | |

| Market price per ordinary share (year end) | | | 62.5p | | | | 51.9p | | | | 68.1p | | | | 62.5p | | | | 73.1p | |

| Number of shareholders (thousands) | | | 2,361 | | | | 2,404 | | | | 2,450 | | | | 2,510 | | | | 2,563 | |

| Number of ordinary shares in issue (millions)8 | | | 70,053 | | | | 71,164 | | | | 71,973 | | | | 71,374 | | | | 71,374 | |

| Financial ratios (%)9 | | | | | | | | | | | | | | | | | | | | |

| Dividend payout ratio10 | | | 96.6 | | | | 57.6 | | | | 62.8 | | | | 124.9 | | | | 359.3 | |

| Post-tax return on average shareholders’ equity | | | 5.7 | | | | 9.3 | | | | 8.0 | | | | 4.1 | | | | 1.3 | |

| Post-tax return on average assets | | | 0.36 | | | | 0.55 | | | | 0.49 | | | | 0.27 | | | | 0.12 | |

| Average shareholders’ equity to average assets | | | 5.2 | | | | 5.3 | | | | 5.3 | | | | 5.2 | | | | 5.1 | |

| Cost:income ratio11 | | | 69.0 | | | | 63.0 | | | | 66.2 | | | | 73.1 | | | | 88.3 | |

| Capital ratios (%) | | | | | | | | | | | | | | | | | | | | |

| Total capital | | | 21.3 | | | | 22.9 | | | | 21.2 | | | | 21.2 | | | | 21.5 | |

| Tier 1 capital | | | 16.7 | | | | 18.2 | | | | 17.2 | | | | 16.8 | | | | 16.4 | |

| Common equity tier 1 capital/Core tier 1 capital | | | 13.6 | | | | 14.6 | | | | 14.1 | | | | 13.4 | | | | 12.8 | |

| 1 | The Group has adopted IFRS 16Leaseswith effect from 1 January 2019, in accordance with the transition requirements of the standard, comparative information has not been restated. |

| 2 | The Group has implemented the amendments to IAS 12Income Taxeswith effect from 1 January 2019 and as a result tax relief on distributions on other equity instruments, previously taken directly to retained profits, is now reported within tax expense in the income statement. Comparatives have been restated. |

| 3 | The Group adopted IFRS 9 and IFRS 15 with effect from 1 January 2018; in accordance with the transition requirements, comparative information was not restated. |

| 4 | Annual dividends comprise both interim and estimated final dividend payments. The total dividend for the year represents the interim dividend paid during the year and the final dividend, which is paid and accounted for in the following year. |

| 5 | Dividends for the year in 2016 included a special dividend totalling £356 million; (2015: £357 million). |

| 6 | Dividends per ordinary share in 2016 included a recommended special dividend of 0.5 pence (2015: 0.5 pence). |

| 7 | Translated into US dollars at the Noon Buying Rate on the date each payment was made, with the exception of the final dividend in respect of 2019, which has been translated at the Noon Buying Rate on 14 February 2020. |

| 8 | For 2016 and previous years, this figure excluded the limited voting ordinary shares owned by the Lloyds Bank Foundations. The limited voting ordinary shares were redesignated as ordinary shares on 1 July 2017. |

| 9 | Averages are calculated on a monthly basis from the consolidated financial data of Lloyds Banking Group. |

| 10 | Total dividend for the year divided by earnings attributable to ordinary shareholders adjusted for tax relief on distributions to other equity holders. |

| 11 | The cost:income ratio is calculated as total operating expenses as a percentage of total income (net of insurance claims). |

BUSINESS

HISTORY AND DEVELOPMENT OF LLOYDS BANKING GROUP

The history of the Group can be traced back to the 18th century when the banking partnership of Taylors and Lloyds was established in Birmingham, England. Lloyds Bank Plc was incorporated in 1865 and during the late 19th and early 20th centuries entered into a number of acquisitions and mergers, significantly increasing the number of banking offices in the UK. In 1995, it continued to expand with the acquisition of the Cheltenham and Gloucester Building Society.

TSB Group plc became operational in 1986 when, following UK Government legislation, the operations of four Trustee Savings Banks and other related companies were transferred to TSB Group plc and its new banking subsidiaries. By 1995, the TSB Group had, either through organic growth or acquisition, developed life and general insurance operations, investment management activities, and a motor vehicle hire purchase and leasing operation to supplement its retail banking activities.

In 1995, TSB Group plc merged with Lloyds Bank Plc. Under the terms of the merger, the TSB and Lloyds Bank groups were combined under TSB Group plc, which was re-named Lloyds TSB Group plc, with Lloyds Bank Plc, which was subsequently re-named Lloyds TSB Bank plc, the principal subsidiary. In 1999, the businesses, assets and liabilities of TSB Bank plc, the principal banking subsidiary of the TSB Group prior to the merger, and its subsidiary Hill Samuel Bank Limited were vested in Lloyds TSB Bank plc, and in 2000, Lloyds TSB Group acquired Scottish Widows. In addition to already being one of the leading providers of banking services in the UK, the acquisition of Scottish Widows also positioned Lloyds TSB Group as one of the leading suppliers of long-term savings and protection products in the UK.

The HBOS Group had been formed in September 2001 by the merger of Halifax plc and Bank of Scotland. The Halifax business began with the establishment of the Halifax Permanent Benefit Building Society in 1852; the society grew through a number of mergers and acquisitions including the merger with Leeds Permanent Building Society in 1995 and the acquisition of Clerical Medical in 1996. In 1997 the Halifax converted to plc status and floated on the London stock market. Bank of Scotland was founded in July 1695, making it Scotland’s first and oldest bank.

On 18 September 2008, with the support of the UK Government, the boards of Lloyds TSB Group plc and HBOS plc announced that they had reached agreement on the terms of a recommended acquisition by Lloyds TSB Group plc of HBOS plc. The shareholders of Lloyds TSB Group plc approved the acquisition at the Company’s general meeting on 19 November 2008. On 16 January 2009, the acquisition was completed and Lloyds TSB Group plc changed its name to Lloyds Banking Group plc.

Pursuant to two placing and open offers which were completed by the Company in January and June 2009 and the Rights Issue completed in December 2009, the UK Government acquired 43.4 per cent of the Company’s issued ordinary share capital. Following sales of shares in September 2013 and March 2014 and the completion of trading plans with Morgan Stanley & Co. International plc (Morgan Stanley), the UK Government completed the sale of its shares in May 2017, returning the Group to full private ownership.

Pursuant to its decision approving state aid to the Group, the European Commission required the Group to dispose of a retail banking business meeting minimum requirements for the number of branches, share of the UK personal current accounts market and proportion of the Group’s mortgage assets. Following disposals in 2014, the Group sold its remaining interest in TSB to Banco de Sabadell (Sabadell) in 2015, and all EC state aid requirements were met by 30 June 2017.

On 1 June 2017, following the receipt of competition and regulatory approval, the Group acquired 100 per cent of the ordinary share capital of MBNA Limited, which together with its subsidiaries operates a UK consumer credit card business, from FIA Jersey Holdings Limited, a wholly-owned subsidiary of Bank of America.

The Group successfully launched its new non ring-fenced bank, Lloyds Bank Corporate Markets plc in 2018, transferring in the non ring-fenced business from the rest of the Group, thereby meeting its legal requirements under ring-fencing legislation.

On 23 October 2018, the Group announced a partnership with Schroders to create a market-leading wealth management proposition. The three key components of the partnership are: (i) the establishment of a new financial planning joint venture; (ii) the Group taking a 19.9 per cent stake in Schroders high net worth UK wealth management business; and (iii) the appointment of Schroders as the active investment manager of approximately £80 billion of the Group’s insurance and wealth related assets. The joint venture, Schroders Personal Wealth, was launched to the market in the third quarter of 2019. The Group’s interest in the joint venture is 50.1 per cent.

BUSINESS

STRATEGY OF LLOYDS BANKING GROUP

The Group is a leading provider of financial services to individual and business customers in the UK. The Group’s main business activities are retail and commercial banking, and long-term savings, protection and investment. Services are provided through a number of well recognised brands including Lloyds Bank, Halifax, Bank of Scotland and Scottish Widows and through a range of distribution channels, including the largest branch network and digital bank in the UK.

As the Group looks to the future, it sees the external environment evolving rapidly. Changing customer behaviours, the pace of technological evolution and changes in regulation all present opportunities. Given the Group’s strong capabilities and the significant progress made in recent years, the Group believes that it is in a unique position to compete and win in this environment by developing additional competitive advantages. The Group will continue to transform itself to succeed in this digital world and the next phase of its strategy will ensure that the Group has the capabilities to deliver future success.

STRATEGIC PRIORITIES

In 2018 the Group launched the third phase of its strategic plan. The Group identified four strategic priorities focused on the financial needs and behaviours of the customer of the future: further enhancing the Group’s leading customer experience; further digitising the Group; maximising Group capabilities; and transforming ways of working. The Group will invest more than £3 billion in these strategic initiatives through the plan period that will drive the Group’s transformation into a digitised, simple, low risk, customer-focused UK financial services provider.

Delivering a leading customer experience

The Group will drive stronger customer relationships through best in class propositions while continuing to provide the Group’s customers with brilliant servicing and a seamless experience across all channels. This will include:

| – | remaining the number 1 digital bank in the UK with open banking functionality; |

| | |

| – | unrivalled reach with UK’s largest branch network serving complex needs; and |

| | |

| – | data-driven and personalised customer propositions. |

Digitising the Group

The Group will deploy new technology to drive additional operational efficiencies that will make banking simple and easier for customers whilst reducing operating costs, pursuing the following initiatives:

| – | deeper end-to-end transformation targeting over 70 per cent of cost base; |

| | |

| – | simplification and progressive modernisation of our data and IT infrastructure; and |

| | |

| – | technology enabled productivity improvements across the business. |

Maximising the Group’s capabilities

The Group will deepen customer relationships, grow in targeted segments and better address our customers’ banking and insurance needs as an integrated financial services provider. This will include:

| – | increasing Financial Planning and Retirement (FP&R) open book assets by more than £50 billion by 2020 with more than 1 million new pension customers; |

| | |

| – | implementing an integrated FP&R proposition with single customer view; and |

| | |

| – | start-up, SME and Mid Market net lending growth (more than £6 billion in the plan period). |

Transforming ways of working

The Group is making its biggest ever investment in people, increasing colleague training and development by 50 per cent to 4.4 million hours per annum and embracing new technology to drive better customer outcomes. The hard work, commitment and expertise of the Group’s colleagues has enabled it to deliver to date and the Group will further invest in capabilities and agile working practices. The Group has already restructured the business and reorganised the leadership team to ensure effective implementation of the new strategy.

BUSINESS AND ACTIVITIES OF LLOYDS BANKING GROUP

The Group’s activities are organised into three financial reporting segments: Retail; Commercial Banking; and Insurance and Wealth. In 2019 the Group transferred Cardnet, its card payment acceptance service, from Retail into Commerical Banking and also transferred certain equity business from Commercial Banking into Central items. Comparatives have been restated accordingly.

Further information on the Group’s financial reporting segments is set out on pages 27 to 29 and in note 4 to the financial statements.

MATERIAL CONTRACTS

The Company and its subsidiaries are party to various contracts in the ordinary course of business.

BUSINESS

ENVIRONMENTAL MATTERS

Helping the transition to a sustainable low carbon economy

The UK is committed to the vision of a sustainable, low carbon future. The Group’s unique position within the UK economy means that the successful transition to a more sustainable, low carbon economy is of strategic importance.

The Group supports the aims of the 2015 Paris Agreement and the UK Government’s Clean Growth Strategy, which will require a radical reinvention of ways of working, living and doing business including new Government policies and sustainable finance solutions. In 2018 the Group set out its Sustainability Strategy and when reporting on its progress, the Group supports the Taskforce on Climate-Related Financial Disclosure (TCFD) framework, and currently plans to achieve full disclosure by 2022 in line with the TCFD recommendations and the UK Government’s Green Finance Strategy.

OUR STRATEGY

The Group’s goal and approach

As a signal of the Group’s commitment the Group has set an ambitious goal, working with customers, Government and the market to help reduce the emissions it finances by more than 50 per cent by 2030, supporting the UK’s ambition to be net zero by 2050 and the 2015 Paris Agreement. During the course of 2020, the Group intends to conduct a review of its portfolio to establish its current financed emissions and set appropriate metrics and targets for material sectors.

In order to meet its goal, the Group will:

| Identify new opportunities to support customers and clients and finance the UK transition to a low carbon economy |

| | |

| Identify and manage material sustainability and climate related risks across the Group, disclosing these, their impacts on the Group and its financial planning processes, in line with the TCFD framework |

| | |

| Use the Group’s scale and reach to help drive progress towards a sustainable and resilient UK economy through engagement with customers, communities, industry, Government, shareholders and suppliers |

| | |

| Embed sustainability into the way the Group does business and manages its own operations in a more sustainable way |

The Group’s ambition

The Group has set itself seven leadership ambitions to support the UK’s transition to a sustainable future:

Business: become a leading UK commercial bank for sustainable growth, supporting clients to transition to sustainable business models and operations, and to pursue new clean growth opportunities

Homes: be a leading UK provider of customer support on energy efficient, sustainable homes

Vehicles: be a leading UK provider of low emission/green vehicle fleets

Pensions and investments: be a leading UK pension provider that offers customers and colleagues sustainable investment choices, and challenge the companies the Group invests in to behave more sustainably and responsibly

Insurance: be a leading UK insurer in improving the resilience of customers’ lives against extreme weather caused by climate change

Green bonds: be a leading UK bank in the green/sustainable bonds market

The Group’s own footprint: be a leading UK bank in reducing the Group’s own carbon footprint and challenging suppliers to ensure the Group’s own consumption of resources, goods and services is sustainable

Metrics and targets

In 2018, the Group committed to develop a reporting framework to track performance against our sustainability strategy. This includes measures for: the Group’s own energy use, emissions, water and waste; Group and portfolio metrics that drive emission reductions related to financing activity; the amount of green finance provided; and metrics that track climate change risk (including exposure to high carbon sectors and sectors at high risk from climate change).

The complexity of accessing robust data has prevented the Group from setting a full suite of targets in 2019. The Group intends, however, to set appropriate targets during 2020 for material sectors. The Group’s new goal to help reduce the emissions it finances by more than 50 per cent by 2030 will frame the level of ambition across the Group’s targets and metrics.

Extending the Group’s own carbon footprint measurement

The Group met its 2030 carbon reduction target in 2019, having reduced emissions by 63 per cent since 2009. The Group also expanded its Scope 3 emissions measurement to include additional categories of emissions from business travel and colleague commuting. The Group continues to pursue our targets to reduce emissions by 80 per cent by 2050, operational waste by 80 per cent by 2025 (compared to 2014/15) and water consumption by 40 per cent by 2030 (compared to 2009). The Group will be developing new carbon, energy and travel targets in 2020.

Green finance

The Group has provided more than £4.9 billion in green finance since 2016 through its Clean Growth Finance Initiative, Commercial Real Estate Green Loans Initiative, Renewable Energy Financing, and green bonds facilitation. While green loan standards are evolving, the Group has teamed up with leading sustainability consultants when developing green finance products to determine a list of qualifying green criteria. These green finance products support a range of eligible activity including; reducing emissions, improving energy efficiency, reducing waste, improving water efficiency, and funding low carbon transport and renewable energy.

BUSINESS

Climate risk sectors

In line with TCFD recommendations, the Group has identified its loans and advances to customers in high carbon sectors and a selection of other sectors that will be exposed to transition risk (see table). This is the Group’s initial view and will be reviewed as its transition risk insight develops. The Group continues to work with customers to support transition, taking into account both risks and opportunities.

The Group’s exposure to high carbon sectors is low (less than 0.5 per cent of total loans and advances to customers). In addition, data for these loans and advances is presented at an overall sector level and not all customers in these sectors will have high emissions or be exposed to significant transition risks. For example:

| Utilities includes financing to entities that have both renewable energy and non-renewable energy generation. The Group has provided finance for more than 40 renewable energy projects, including supporting projects such as the Neart na Gaoithe offshore wind farm; |

| | |

| Real estate and mortgages will include loans and advances supported by assets which have a full range of Energy Performance Certificate (EPC) ratings including energy efficient properties; |

| | |

| UK motor finance includes loans and advances for low emission vehicles. |

| | |

| Loans and advances to customers in high carbon sectors and selected other sectors subject to transition risks. |

| | | | | | | Loans and advances to

customers (£m)2 | | % of total loans and advances

to customers3 |

| Sector/area1 | | Dec-2019 | | | Dec-2018 | | | Dec-2019 | | Dec-2018 |

| | Energy | | Coal Mining | | | 21 | | | | 28 | | | | <0.01 | % | | | <0.01 | % |

| | | | Oil and Gas | | | 1,368 | | | | 975 | | | | 0.27 | % | | | 0.20 | % |

| | Utilities | | (Electric and Gas) | | | 964 | | | | 1,251 | | | | 0.19 | % | | | 0.26 | % |

| | Total | | | | | 2,353 | | | | 2,254 | | | | 0.47 | % | | | 0.46 | % |

| | Agriculture, Forestry and Fishing | | | 7,558 | | | | 7,314 | | | | 1.52 | % | | | 1.50 | % |

| | Construction and Real Estate | | | 28,228 | | | | 29,470 | | | | 5.67 | % | | | 6.04 | % |

| | Transportation (Automotive, Aviation, Shipping and Rail) | | | 4,353 | | | | 5,429 | | | | 0.87 | % | | | 1.11 | % |

| | Cement, Chemicals and Steel Manufacture | | | 143 | | | | 250 | | | | 0.03 | % | | | 0.05 | % |

| | Mortgages | | | 299,141 | | | | 297,497 | | | | 60.05 | % | | | 60.96 | % |

| | UK Motor Finance | | | 15,976 | | | | 14,933 | | | | 3.21 | % | | | 3.06 | % |

| 1 | Exposures are based on 2007 Standard Industrial Classification codes except for Agriculture, Forestry and Fishing (based on NACE code A00-0) and Mortgages and UK Motor Finance, where the full portfolios have been used. These exposures will include green and other sustainable finance loans, which support the transition to the low carbon economy. As such, these figures and/or trends should not be read as the only measure to gauge transition risk or financed emissions. |

| 2 | Disclosures are based on loans and advances to customers on a statutory basis, before allowance for impairment losses. Analysis covers at least 95% of loans and advances and does not include data from the Insurance and Wealth division. |

| 3 | Total loan and advances to customers were £488,088m at 31 December 2018 and £498,247m at 31 December 2019. |

Risk management

Climate risk is a key emerging risk for the Group. The Group’s approach to identifying and managing climate risk is founded on embedding it into its existing risk management framework, and integrating it through policies, authorities and risk control mechanisms. During 2019, the Group updated its TCFD implementation plan to incorporate Prudential Regulatory Authority (PRA) supervisory expectations and refined deliverables, with further resource invested in the programme.

In 2019, the Group included commentary on climate change risk within its Internal Capital Capacity Adequacy Assessment Process (ICAAP) submission, and in 2020 the Group is building on this through its analysis of initial scenarios to assess the impact on capital requirements. The Group is also engaged in the industry response to the Bank of England Discussion Paper to identify the best approach to explore the financial risks posed by climate change within its 2021 Biennial Exploratory Scenario (BES).

The Group has updated its external sector statements to include positions on six new sectors including manufacturing, automotive, agriculture, animal welfare, fisheries and UNESCO World Heritage Sites. This is in addition to the existing statements on power, coal, mining, oil and gas, forestry and defence. www.lloydsbankinggroup.com/Our-Group/responsible-business/reporting-centre/. The Group’s statement on coal has been updated and made more ambitious. The Group continues with its policy of not financing new coal fired power stations. The Group has now tightened its requirements for providing general banking or funding, and now requires new clients to have less than 30 per cent of their revenue from the operation of coal fired power stations and/or coal mines (previously less than 50 per cent).

In addition, existing customers whose overall operations include coal mining and coal power generation or who supply equipment or services to the sector will be expected to explain how they plan to reduce their reliance on revenue from coal fired power stations and/or coal mines. This includes reducing such revenue to less than 30 per cent by 2025 and, where relevant, to eliminate UK coal power generation in line with UK Government commitments.

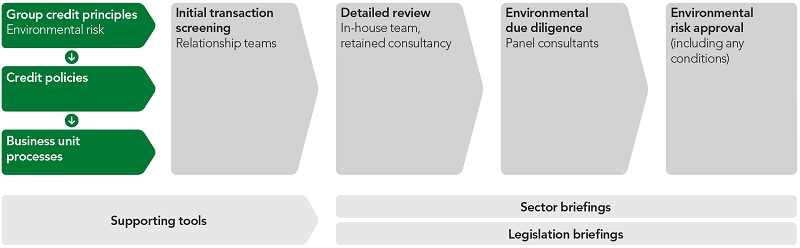

Sustainability is now a mandatory part of credit applications in Commercial Banking for facilities greater than £500,000, and we continue to develop sector specific guidance to help relationship managers identify climate risks. The Group will review climate risk as part of the 2020 annual refresh of the Group’s Risk Appetite.

In line with TCFD, the Group is also developing forward-looking scenario analysis, incorporating physical and transition risks, to help identify risks and opportunities over the short, medium and long-term. For example, Commercial Banking are conducting analysis on the real estate sector for business as usual and low carbon transition scenarios and the Insurance business has conducted an initial climate stress test. The Group is working with external consultants to enhance scenario analysis across divisions and will use the outputs to support scenario analysis assessments and inform credit risk appetite decisions and future disclosures.

BUSINESS

Governance

Given the strategic importance of the Group’s sustainability ambitions, the Group’s governance structure provides clear oversight and ownership of the sustainability strategy. This includes:

Lloyds Banking Group Board Responsible Business Committee Group Executive Committee Group Executive Sustainability Committee Other internal governance Audit Committee Board Risk Committee GEC Risk Committee Divisional Risk Committees Group sustainability team Divisional forums/ working groups Group sustainability forum TCFD working group

| – | The Responsible Business Committee (RBC), a sub-committee of the Board, chaired by Sara Weller, Group Non-Executive Director and which includes the Chairman, Lord Blackwell as a member |

| | |

| – | The Group Executive Sustainability Committee (GESC) which provides oversight and recommends decisions to the Group Executive Committee (GEC) |

| | |

| – | The TCFD working group, co-chaired by senior executives in risk and sustainability, coordinates the implementation of the TCFD recommendations and supports adherence to key regulatory requirements on climate risk |

| | |

| – | The Group Chief Risk Officer (CRO) has assumed responsibility for identifying and managing the risks arising from climate change, alongside the CROs for key legal entities |

Our Group sustainability team is supported by divisional sustainability governance forums led by Divisional Managing Directors, ensuring a coordinated approach to oversight, delivery and reporting of the Group’s sustainability strategy.

How we are delivering against our ambitions

In 2019, the Group has focused on developing new products, services and processes to achieve its ambitions, and progress has been recognised.

| Lloyds Banking Group achieved the Leadership level in the 2019 Carbon Disclosure Project (CDP) Climate Change survey, scoring an A minus; the highest placed financial services firm on the Fortune Sustainability All Stars list; and won the Real Estate Capital Sustainable Finance Provider of the Year |

| | |

| One in 14 electric cars in the UK was supplied by Group subsidiary Lex Autolease in 2019, supported by a £1 million cashback offer on pure electric vehicle (EV) orders, reducing future carbon dioxide emissions by an estimated 28 kilotonnes |

| | |

| The Group continues to partner with the Cambridge Institute for Sustainability Leadership to provide high quality training to executives and colleagues in risk management, product development and client facing roles. In 2019, over 800 colleagues were trained, ensuring they are able to support clients on this journey |

| | |

| Since 2018 the Group has supported renewable energy projects that power the equivalent of 5.1 million homes, achieving the Group’s Helping Britain Prosper Plan 2020 target a year early |

Evolving our disclosure

In 2020, the Group will continue to review and enhance its methodologies and framework for reporting Environmental, Social and Governance risks. This review will take into account a range of industry guidelines including TCFD, Principles for Responsible Banking, Sustainability Accounting Standards Board (SASB), the evolving World Economic Forum (WEF) ESG standards, and regulatory reporting requirements with a view to further enhancing our disclosures and responding to the evolving needs of both our shareholders and other stakeholders.

BUSINESS

Initiatives and collaboration

Climate change is a global challenge that requires collaboration across companies and industries to ensure the risks and opportunities can be adequately identified and managed. To support this, the Group participates in several industry initiatives and has signed up to key principles that drive action on climate change and sustainability, including:

United Nations Environment Programme

Finance Initiative (UNEP FI)

The Group became a member of UNEP FI in 2019 and joined its Phase 2 Banking TCFD Pilot.

The Group also became a signatory to the Principles for Responsible Banking and Principles for Sustainable Insurance.

Coalition for Climate Resilient Investment

In September 2019, the Group joined the newly formed coalition that aims to transform infrastructure investment by integrating climate risks into decision making.

University of Cambridge Banking Environment Initiative (BEI) – Bank 2030

The Group has been working with 12 leading banks to develop a roadmap for how the industry can direct capital towards environmentally and socially sustainable economic development.

The Climate Group

In 2019, the Group was one of only a handful of businesses globally to sign up to all three of The Climate Group’s campaigns:

| RE100 – a commitment to source 100 per cent of the Group’s electricity from renewable sources by 2030 (achieved in 2019) |

| | |

| EP100 – a commitment to set ambitious energy productivity targets by 2030 |

| | |

| EV100 – a commitment to accelerate the transition to Electric Vehicles by 2030 |

Climate Financial Risk Forum

In 2019, the Group joined the PRA and FCA’s joint Climate Financial Risk Forum, participating in the Risk Management Working Group that aims to deliver a UK best practice handbook on implementation of the TCFD recommendations.

Greenhouse gas emissions

The Group has voluntarily reported greenhouse gas emissions and environmental performance since 2009, and since 2013 this has been reported in line with the requirements of the Companies Act 2006. Our total emissions, in tonnes of CO2equivalent, are reported in the table below. Deloitte LLP has provided limited level ISAE 3000 (Revised) and ISAE 3410 assurance over selected non-financial indicators as noted by . Their full, independent assurance statement is available online at www.lloydsbankinggroup.com/our-group/responsible-business

. Their full, independent assurance statement is available online at www.lloydsbankinggroup.com/our-group/responsible-business

Methodology

The Group follows the principles of the Greenhouse Gas (GHG) Protocol Corporate Accounting and Reporting Standard to calculate our Scope 1, 2 and 3 emissions from our worldwide operations. The reporting period is 1 October 2018 to 30 September 2019, which is different to that of the Directors’ report (January 2019 – December 2019). This is in line with Regulations in that the majority of the emissions reporting year falls within the period of the Directors’ Report. Emissions are reported based on an operational boundary. The scope of reporting is in line with the GHG Protocol and covers Scope 1, Scope 2 and Scope 3 emissions. Reported Scope 1 emissions cover emissions generated from gas and oil used in buildings, emissions from UK company-owned vehicles used for business travel and emissions from the use of air conditioning and chiller/refrigerant plant. Reported Scope 2 emissions cover emissions generated from the use and purchase of electricity for own use, calculated using both the location and market based methodologies. Reported Scope 3 emissions relate to business travel and commuting undertaken by colleagues and emissions associated with waste and the extraction and distribution of each of our energy sources; electricity, gas and oil. In 2019 the Group has expanded Scope 3 emissions as part of our sustainability strategy to increase transparency of reporting of the Group’s carbon footprint, and to drive reductions in additional categories of emissions; these include Waste Emissions, Upstream Business Travel (the well to tank emissions of rail, air, road vehicles, hired vehicles); Hotels; Commuting; Tube; Taxis. A detailed definition of these emissions can be found in the Group’s 2019 Reporting Criteria online at www.lloydsbankinggroup.com/our-group/responsible-business

Intensity ratio

| Legacy | | | | | | | | | |

| | | Oct 2018 –

Sept 2019 | | | Oct 2017 –

Sept 2018 | | | Oct 2016 –

Sept 2017 | |

| GHG emissions (CO2e) per £m of underlying income (Location Based)1 | | | 11.5 | | | | 13.0 | | | | 15.5 | |

| GHG emissions (CO2e) per £m of underlying income (Market Based)1 | | | 5.6 | | | | 6.2 | | | | 16.4 | |

| | | | | | | | | | | | | |

| Expanded | | | | | | | | | | | | |

| | | | Oct 2018 –

Sept 2019 | | | | Oct 2017 –

Sept 2018 | | | | Oct 2016 –

Sept 2017 | |

| GHG emissions (CO2e) per £m of underlying income (Location Based) – expanded scope2 | | | 15.8 | | | | 17.3 | | | | – | |

| GHG emissions (CO2e) per £m of underlying income (Market Based) – expanded scope2 | | | 9.9 | | | | 10.5 | | | | – | |

| 1 | Intensities have been restated for 2016-2017 and 2017-2018 to reflect changes to emissions data only, replacing estimated data with actuals; underlying income figures for those years have not changed. |

| 2 | Scope 3 emissions have been expanded to include additional elements within the Group’s own operations including emissions from waste, colleague commuting and additional elements of business travel (including taxis, tube, well to tank emissions of business travel and hotels). We have disclosed these figures parallel to legacy scope numbers to allow fairer comparison to numbers previously disclosed and to demonstrate performance versus our previous targets. |

BUSINESS

This year, the Group’s overall location based carbon emissions were 207,768 tCO2e; a 14.6 per cent decrease since 2018 and 63.1 per cent against the Group’s 2009 baseline (legacy scope). Reductions achieved are attributable to an extensive energy optimisation programme and reductions in business travel, alongside decarbonisation of the UK electricity grid. In addition, there has been a reduction in property foot print and headcount.

The Group’s market based emissions figure is equal to 101,042 tCO2e – a comparative decrease of 12.9 per cent year on year and 82.0 per cent against 2009 baseline. Further reductions in market emissions are attributable to the purchase of renewable energy certificates for each of the Group’s operations outside of the UK equivalent to their consumption since January 2019. The Group continues to source solar, wind, hydro and biomass Renewable Energy Guarantees of Origin (REGOs) equivalent to our total UK electricity consumption.

| CO2E emissions (tonnes) – Expanded scope | | | | | | | | | |

| CO2E Emissions Tonnes: | | Oct18 –

Sep19 | | | Oct17 –

Sep181 | | | Oct16 –

Sep171 | |

| Total CO2e (market based) | | | 179,324 | | | | 197,484 | | | | n/a | |

| Total CO2e (location based) | | | 286,051 | | | | 324,816 | | | | n/a | |

| Total Scope 1 | | | 47,524 | | | | 49,299 | | | | 51,953 | |

| Total Scope 2 (market based) | | | 387 | | | | 1,951 | | | | 178,711 | |

| Total Scope 2 (location based) | | | 107,113 | | | | 129,284 | | | | 162,598 | |

| Total Scope 32 | | | 131,414 | | | | 146,233 | | | | n/a | |

| |

| CO2E emissions (tonnes) – Legacy scope | | | | | | | | | | | | |

| CO2E Emissions Tonnes: | | | Oct18 –

Sep19 | | | | Oct17 –

Sep181 | | | | Oct16 –

Sep171 | |

| Total CO2e (market based) | | | 101,042 | | | | 115,961 | | | | 303,065 | |

| Total CO2e (location based) | | | 207,768 | | | | 243,293 | | | | 286,892 | |

| Total Scope 3 | | | 53,131 | | | | 64,710 | | | | 72,876 | |

| 1 | Restated 2018/2017 and 2017/2016 emissions data to improve the accuracy of reporting, using actual data to replace estimates. |

| | |

| | Emissions in tonnes CO2e in line with the GHG Protocol Corporate Standard (2004) including revised Scope 2 guidance (2015) which discloses a Market Based figure in addition to the Location Based figure. |

| | |

| | The measure and reporting criteria for Scope 1, 2, 3 emissions is provided in the Lloyds Banking Group Reporting Criteria statement available online at www.lloydsbankinggroup.com/our-group/responsible-business |

| | |

| | Scope 1 emissions include mobile and stationary combustion of fuel and operation of facilities. |

| | |

| | Scope 2 emissions have been calculated in accordance with GHG Protocol guidelines, in both Location and Market Based methodologies. |

| | |

| 2 | Scope 3 emissions have been expanded to include additional elements within the Group’s own operations including emissions from waste, colleague commuting and additional elements of business travel (including taxis, tube, well to tank emissions of business travel and hotels). We have also disclosed legacy scope numbers to allow fairer comparison to numbers previously disclosed and to demonstrate performance versus our previous targets. |

| | |

| Indicator is subject to Limited ISAE3000 (revised) and 3410 (ISAE3410) assurance by Deloitte LLP for the 2019 Annual Responsible Business Reporting. Deloitte’s 2019 assurance statement and the 2019 Reporting Criteria are available online at www.lloydsbankinggroup.com/our-group/responsible-business |

Omissions

Emissions associated with joint ventures and investments are not included in this disclosure as they fall outside the scope of our operational boundary. The Group does not have any emissions associated with imported heat, steam or imported cooling and is not aware of any other material sources of omissions from our reporting.

PROPERTIES

At 31 December 2019, Lloyds Banking Group occupied 1,768 properties in the UK. Of these, 371 were held as freeholds and 1,397 as leasehold. The majority of these properties are retail branches, widely distributed throughout England, Scotland, Wales and Northern Ireland. Other buildings include the Lloyds Banking Group’s head office in the City of London with other customer service and support centres located to suit business needs but clustered largely in eight core geographic conurbations – London, Edinburgh, Glasgow, Midlands (Birmingham), Northwest (Chester and Manchester), West Yorkshire (Halifax and Leeds), South (Brighton and Andover) and Southwest (Bristol and Cardiff).

In addition, there are 132 properties which are either sub-let or vacant. There are also a number of Automated Teller Machine (ATM) units situated throughout the UK, the majority of which are held as leasehold. The Group also has business operations elsewhere in the world, primarily holding property on a leasehold basis.

BUSINESS

LEGAL ACTIONS AND REGULATORY MATTERS

During the ordinary course of business the Group is subject to threatened or actual legal proceedings and regulatory reviews and investigations both in the UK and overseas. Set out below is a summary of the more significant matters.

PROVISIONS FOR FINANCIAL COMMITMENTS AND GUARANTEES

Provisions are recognised for expected credit losses on undrawn loan commitments and financial guarantees.

PAYMENT PROTECTION INSURANCE (EXCLUDING MBNA)

The Group increased the provision for PPI costs by a further £2,450 million in the year ended 31 December 2019, bringing the total amount provided to £21,875 million.

The charge in 2019 was largely due to the significant increase in PPI information requests (PIRs) leading up to the deadline for submission of claims on 29 August 2019, and also reflects costs relating to complaints received from the Official Receiver as well as administration costs. An initial review of around 60 per cent of the five million PIRs received in the run-up to the PPI deadline has been undertaken, with the conversion rate remaining low, and consistent with the provision assumption of around 10 per cent. The Group has reached final agreement with the Official Receiver.

At 31 December 2019, a provision of £1,578 million remained unutilised relating to complaints and associated administration costs excluding amounts relating to MBNA. Total cash payments were £2,201 million during the year ended 31 December 2019.

Sensitivities

The total amount provided for PPI represents the Group’s best estimate of the likely future cost. A number of risks and uncertainties remain including processing the remaining PIRs and outstanding complaints. The cost could differ from the Group’s estimates and the assumptions underpinning them, and could result in a further provision being required. These may also be impacted by any further regulatory changes and potential additional remediation arising from the continuous improvement of the Group’s operational practices.

For every one per cent increase in PIR conversion rate on the stock as at the industry deadline, the Group would expect an additional charge of approximately £100 million.

PAYMENT PROTECTION INSURANCE (MBNA)

MBNA increased its PPI provision by £367 million in the year ended 31 December 2019 but the Group’s exposure continues to remain capped at £240 million under the terms of the sale and purchase agreement.

OTHER PROVISIONS FOR LEGAL ACTIONS AND REGULATORY MATTERS

In the course of its business, the Group is engaged in discussions with the PRA, FCA and other UK and overseas regulators and other governmental authorities on a range of matters. The Group also receives complaints in connection with its past conduct and claims brought by or on behalf of current and former employees, customers, investors and other third parties and is subject to legal proceedings and other legal actions. Where significant, provisions are held against the costs expected to be incurred in relation to these matters and matters arising from related internal reviews. During the year ended 31 December 2019 the Group charged a further £445 million in respect of legal actions and other regulatory matters, and the unutilised balance at 31 December 2019 was £528 million (31 December 2018: £861 million). The most significant items are as follows.

Arrears handling related activities

The Group has provided an additional £188 million in the year ended 31 December 2019 for the costs of identifying and rectifying certain arrears management fees and activities, taking the total provided to date to £981 million. The Group has put in place a number of actions to improve its handling of customers in these areas and has made good progress in reimbursing arrears fees to impacted customers.

Packaged bank accounts

The Group had provided a total of £795 million up to 31 December 2018 in respect of complaints relating to alleged mis-selling of packaged bank accounts, with no further amounts provided during the year ended 31 December 2019. A number of risks and uncertainties remain, particularly with respect to future volumes.

Customer claims in relation to insurance branch business in Germany

The Group continues to receive claims in Germany from customers relating to policies issued by Clerical Medical Investment Group Limited (subsequently renamed Scottish Widows Limited), with smaller numbers received from customers in Austria and Italy. The industry-wide issue regarding notification of contractual ‘cooling off’ periods continued to lead to an increasing number of claims in 2016 and 2017. Whilst complaint volumes have declined, new litigation claim volumes per month have remained fairly constant throughout 2019. Up to 31 December 2019 the Group had provided a total of £656 million. The validity of the claims facing the Group depends upon the facts and circumstances in respect of each claim. As a result, the ultimate financial effect, which could be significantly different from the current provision, will be known only once all relevant claims have been resolved.

HBOS Reading – review

The Group has now completed its compensation assessment for all 71 business customers within the customer review, with more than 98 per cent of these offers to individuals accepted. In total, more than £100 million in compensation has been offered to victims of the HBOS Reading fraud prior to the publication of Sir Ross Cranston’s independent quality assurance review of the customer review, of which £94 million has so far been accepted, in addition to £9 million for ex-gratia payments and £6 million for the re-imbursements of legal fees. Sir Ross’s review was concluded on 10 December 2019 and made a number of recommendations, including a re-assessment of direct and consequential losses by an independent panel. The Group has committed to implementing Sir Ross’s recommendations in full. In addition, further ex gratia payments of £35,000 have been made to 200 individuals in recognition of the additional delay which will be caused whilst the Group takes further steps to implement Sir Ross’s recommendations. It is not possible to estimate at this stage what the financial impact will be.

HBOS Reading – FCA investigation

The FCA’s investigation into the events surrounding the discovery of misconduct within the Reading-based Impaired Assets team of HBOS has concluded. The Group has settled the matter with the FCA and paid a fine of £45.5 million, as per the FCA’s final notice dated 21 June 2019.

BUSINESS

INTERCHANGE FEES

With respect to multi-lateral interchange fees (MIFs), the Group is not involved in the ongoing litigation (as described below) which involves card schemes such as Visa and Mastercard. However, the Group is a member/licensee of Visa and Mastercard and other card schemes. The litigation in question is as follows:

| – | litigation brought by retailers against both Visa and Mastercard continues in the English Courts (and includes appeals heard by the Supreme Court, judgment awaited); and |

| – | litigation brought on behalf of UK consumers in the English Courts against Mastercard. |

Any impact on the Group of the litigation against Visa and Mastercard remains uncertain at this time. Insofar as Visa is required to pay damages to retailers for interchange fees set prior to June 2016, contractual arrangements to allocate liability have been agreed between various UK banks (including the Group) and Visa Inc, as part of Visa Inc’s acquisition of Visa Europe in 2016. These arrangements cap the maximum amount of liability to which the Group may be subject, and this cap is set at the cash consideration received by the Group for the sale of its stake in Visa Europe to Visa Inc in 2016.

LIBOR AND OTHER TRADING RATES

In July 2014, the Group announced that it had reached settlements totalling £217 million (at 30 June 2014 exchange rates) to resolve with UK and US federal authorities legacy issues regarding the manipulation several years ago of Group companies’ submissions to the British Bankers’ Association (BBA) London Interbank Offered Rate (LIBOR) and Sterling Repo Rate. The Swiss Competition Commission concluded its investigation against Lloyds Bank plc in June 2019. The Group continues to cooperate with various other government and regulatory authorities, including a number of US State Attorneys General, in conjunction with their investigations into submissions made by panel members to the bodies that set LIBOR and various other interbank offered rates.

Certain Group companies, together with other panel banks, have also been named as defendants in private lawsuits, including purported class action suits, in the US in connection with their roles as panel banks contributing to the setting of US Dollar, Japanese Yen and Sterling LIBOR and the Australian BBSW Reference Rate. Certain of the plaintiffs’ claims have been dismissed by the US Federal Court for Southern District of New York (subject to appeals).

Certain Group companies are also named as defendants in (i) UK based claims; and (ii) two Dutch class actions, raising LIBOR manipulation allegations. A number of the claims against the Group in relation to the alleged mis-sale of interest rate hedging products also include allegations of LIBOR manipulation.

It is currently not possible to predict the scope and ultimate outcome on the Group of the various outstanding regulatory investigations not encompassed by the settlements, any private lawsuits or any related challenges to the interpretation or validity of any of the Group’s contractual arrangements, including their timing and scale.

UK SHAREHOLDER LITIGATION

In August 2014, the Group and a number of former directors were named as defendants in a claim by a number of claimants who held shares in Lloyds TSB Group plc (LTSB) prior to the acquisition of HBOS plc, alleging breaches of duties in relation to information provided to shareholders in connection with the acquisition and the recapitalisation of LTSB. Judgment was delivered on 15 November 2019. The Group and former directors successfully defended the claims. The claimants have sought permission to appeal. It is currently not possible to determine the ultimate impact on the Group (if any).

TAX AUTHORITIES

The Group has an open matter in relation to a claim for group relief of losses incurred in its former Irish banking subsidiary, which ceased trading on 31 December 2010. In 2013 HMRC informed the Group that their interpretation of the UK rules which allow the offset of such losses denies the claim for group relief of losses. If HMRC’s position is found to be correct, management estimate that this would result in an increase in current tax liabilities of approximately £800 million (including interest) and a reduction in the Group’s deferred tax asset of approximately £250 million. The Group does not agree with HMRC’s position and, having taken appropriate advice, does not consider that this is a case where additional tax will ultimately fall due. There are a number of other open matters on which the Group is in discussion with HMRC (including the tax treatment of certain costs arising from the divestment of TSB Banking Group plc), none of which is expected to have a material impact on the financial position of the Group.

MORTGAGE ARREARS HANDLING ACTIVITIES – FCA INVESTIGATION

On 26 May 2016, the Group was informed that an enforcement team at the FCA had commenced an investigation in connection with the Group’s mortgage arrears handling activities. It is not currently possible to make a reliable assessment of any liability resulting from the investigation including any financial penalty.

CONTINGENT LIABILITIES RELATING TO OTHER LEGAL ACTIONS AND REGULATORY MATTERS

In addition, during the ordinary course of business the Group is subject to other complaints and threatened or actual legal proceedings (including class or group action claims) brought by or on behalf of current or former employees, customers, investors or other third parties, as well as legal and regulatory reviews, challenges, investigations and enforcement actions, both in the UK and overseas. All such material matters are periodically reassessed, with the assistance of external professional advisers where appropriate, to determine the likelihood of the Group incurring a liability. In those instances where it is concluded that it is more likely than not that a payment will be made, a provision is established to management’s best estimate of the amount required at the relevant balance sheet date. In some cases it will not be possible to form a view, for example because the facts are unclear or because further time is needed properly to assess the merits of the case, and no provisions are held in relation to such matters. In these circumstances, specific disclosure in relation to a contingent liability will be made where material. However the Group does not currently expect the final outcome of any such case to have a material adverse effect on its financial position, operations or cash flows.

BUSINESS

COMPETITIVE ENVIRONMENT

The Group provides financial services to individual and business customers, predominantly in the UK but also overseas. The main business activities of the Group are retail and commercial banking and long-term savings, protection and investment.

MARKET DYNAMICS

The Group continues to operate in an increasingly competitive environment, driven by regulatory changes, shifting customer behaviours and increasing levels of innovation across the sector.

Across the Group’s traditional business lines, ring-fencing regulation has seen a number of competitors deploy excess liquidity to support asset growth within the UK, specifically within mortgages where customer rates have in the last few years hit record lows. While this is beneficial for customers, this has depressed margins across the UK banking sector and more recently has resulted in some smaller participants stepping back from the market.

Beyond this, digital-only providers have grown their share of the UK market within the past year. This growth has predominantly been driven by neo-banks that provide a more traditional customer offering alongside leading digital functionality and are able to target selected customer segments. This is supported by the emergence of marketplace models which enable these providers to collaborate with more specialist fintechs to provide a broader suite of products and financial services, both for personal and business banking customers.

In response, a number of traditional competitors have attempted to replicate the success of neo-banks by developing their own digital-only offerings, often under separate and newly created brand names. A number of international peers have also entered the UK market through digital only challengers, taking advantage of the supportive regulatory environment and increasing similarity in customer behaviours across multiple geographies.

Elsewhere, The Group has also started to see the first signs of large technology companies participating in financial services, often partnering with local incumbent banks across different geographies. While the scale of their future ambitions is uncertain at this stage, the power of their brand and large customer bases pose future disruption threats.

THE GROUP’S RESPONSE

The Group continues to respond effectively to the increasingly competitive environment, supported by its significant reach and proven track record of providing products and services that its customers value with this underpinned by significant investment capacity.

Across its core markets such as mortgages, the Group looked to prioritise value while maintaining share and supporting its purpose of Helping Britain Prosper. As marginal players have withdrawn from the market, the Group has more recently strengthened its position, including through the acquisition of Tesco Bank’s mortgage portfolio in September. Alongside this, the Group has also continued to invest in areas where it is under-represented, such as Insurance and Commercial Banking, in line with the commitments outlined at the start of this strategic plan.

In response to changes to the competitive environment from the ongoing shift in digital usage and new entrants, the Group’s multi-channel and multi-brand offering enables it to continue to effectively meet the varying needs of its diverse customer base. The Group’s digital channel is now its most prominent, with 75 per cent of products now originated digitally and we operates the largest digital bank in the UK with 16.4 million customers and 10.7 million mobile app customers, while its customer satisfaction scores remain strong.

In addition, the Group remains committed to retaining the largest branch network in the UK. This allows its customers to interact with the Group in whichever way they prefer, while also providing a human touch point for more complex financial needs. The Group’s network is also key to building and deepening its business banking relationships. The Group sees these as unique competitive advantages, and combined with its ongoing commitment to innovation, provide the Group with a strong platform to maintain relevance and deepen relationships with its customer base.

Link to principal risks

| Regulatory and legal |

| Conduct |

| Operational |

| People |

Link to strategic priorities

| Delivering a leading customer experience |

| Maximising Group capabilities |

For more information see “Risk Factors – Business and economic risks – The Group’s businesses are conducted in competitive environments, with increased competition scrutiny, and the Group’s financial performance depends upon management’s ability to respond effectively to competitive pressures and scrutiny.”

This page is intentionally blank

operating and financial reView and prospects

The results discussed below are not necessarily indicative of Lloyds Banking Group’s results in future periods. The following information contains certain forward looking statements. For a discussion of certain cautionary statements relating to forward looking statements, seeForward looking statements.

The following discussion is based on and should be read in conjunction with the consolidated financial statements and the related notes thereto included elsewhere in this annual report. For a discussion of the accounting policies used in the preparation of the consolidated financial statements, seeAccounting policiesin note 2 to the financial statements.

TABLE OF CONTENTS

operating and financial reView and prospects

OVERVIEW AND TREND INFORMATION

ECONOMY

Highlights

| Given our focus on UK customers, the Group’s prospects are closely linked to the fortunes of the UK economy. |

| On the assumption that the global economy remains broadly stable, we would expect the UK economy to grow in 2020 to 2022 at a pace slightly above that achieved in the past two years. |

| Our low risk business model and focus on efficiency positions us well irrespective of macro conditions. Nevertheless, if the economy was to be impacted significantly by crystallisation of either domestic or international risks, Group financial performance would be impacted. |

Overview

As a leading UK bank, our prospects are closely aligned to the outlook for the UK economy. Through 2019, the economy continued to show resilience to twin challenges from a slowing global economy and increasing domestic political uncertainty. Although growth of the UK economy has slowed to its weakest since the financial crisis a decade ago, and interest rates remain very low, unemployment has fallen further to a 44 year low and house prices have continued to grow. Barring any sudden shocks to business or consumer confidence, growth is expected to rise mildly in 2020, but international trade-protectionism, the current coronavirus outbreak in China, geo-political instability and the nature of the UK’s exit from the EU, all present risks to that outlook.

Market dynamics

During 2019, there have been divergent trends between UK businesses and households. For businesses, uncertainty for the domestic political and economic outlook translated into a second consecutive year of reduced investment spending and commercial real estate prices fell slightly. Low productivity growth remains a key challenge for the UK economy, however, the flip-side has been buoyant employment. Households continued to increase spending in 2019 as low unemployment boosted pay growth whilst softening global growth reduced inflation.