Citibank

2007 Industrial Manufacturing Conference

March 2007

Safe Harbor

Today’s presentation includes forward

looking statements that involve risks.

Please refer to Form 10K for the year

ending December 31, 2006 for details on

factors that may influence results.

2

2

Strong Foundation for the Future

Diversified business portfolio

Industry

Geography

Recurring revenue

Dramatic growth

Operational excellence

Enterprise leverage

Strong balance sheet and cash generation

Positioned to Deliver Solid

Financial Results in All Economic Cycles

3

Where We Were

Heavy Machinery

Deep Cyclical

Engineered Products

Product-centric

Match GDP Growth

Change Averse

Low Tech

Disconnected Businesses

Happy to Be Good

Old Ingersoll Rand

4

Portfolio Transformation 2000 through 2007

Strategic review of prospects for all businesses

Strengthened core businesses

Improved marginal performers

Divested non-core operations ($4 Billion revenues)

Pumps

Bearings

Drills

Dresser-Rand

Road Development – Announced Feb. 2007

Made 65 bolt-on acquisitions since 2000 ($3 Billion revenues)

Core Platform to Deliver Consistent Growth

5

Where We Are Going

Heavy Machinery

Deep Cyclical

Engineered Products

Product-centric

Match GDP Growth

Change Averse

Low Tech

Disconnected Businesses

Diversified Industrial

Balanced Across the Cycle

Commercial Businesses

Customer Focused

Outpacing Market Growth

Change Culture

Innovative, Visionary

Leveraged Enterprise

Working to Be Great

Old Ingersoll Rand

New Ingersoll Rand

6

Dramatic Growth ...

Operational Excellence ...

Dual Citizenship ...

by focusing on innovative solutions

for our customers

by pursuing continuous improvement

in all our operations

by leveraging enterprise-wide strengths

Ingersoll Rand is a global

diversified enterprise with market

leading brands

We are dedicated to driving

Shareholder Value by achieving:

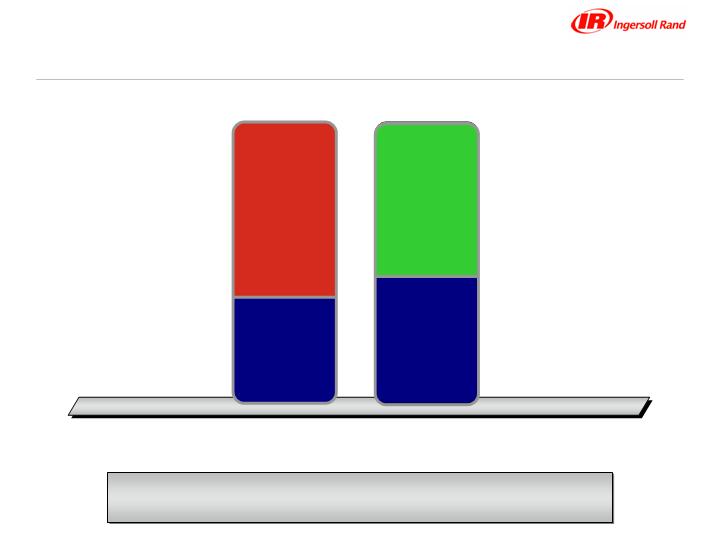

% of Total Revenue

* Primarily Pumps, Dresser-Rand, Drills, and Underground Mining Equipment

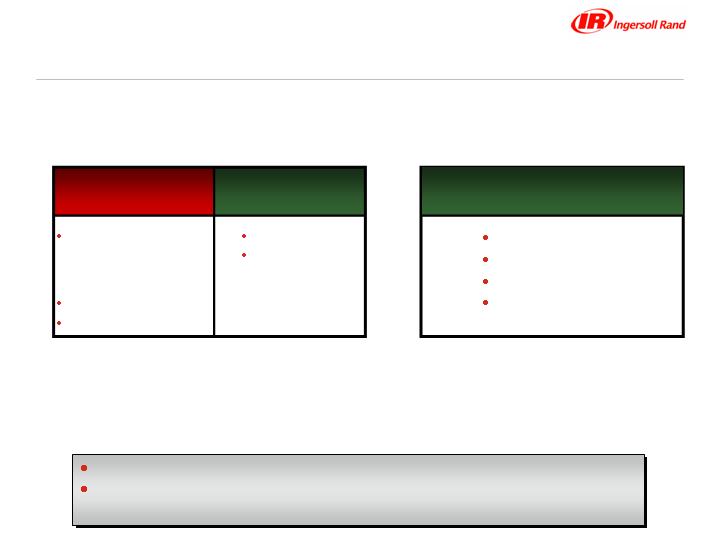

Substantial Upgrade of Business Portfolio

Higher Growth and Lower Cycles

62%

38%

57%

43%

Automotive Components

Road Development

*Mining & Process

Security Technologies

Industrial Technologies

(Utility Equipment

and Attachments)

Climate Control Tech.

Compact Vehicle Tech.

Security Technologies

Industrial Technologies

(Utility Equipment

and Attachments)

1994

2006

Divested

Acquired

We Have Transformed the Business Portfolio

Pro Forma for Sale of

Road Development

8

Sale to Volvo Construction AB of Sweden

$1.3 Billion net proceeds

Target completion for transaction second quarter of 2007

Record substantial earnings gain on sale

Net cash proceeds to exceed $900 Million

Continued reinvestment in core business for innovation

and consistent growth

Bolt on acquisitions

Share buyback

Sale of Road Development Business

9

Sale of Road Development

$725 Million revenues for full year 2006

Major product lines include:

Asphalt paving equipment

Compactors

Milling machines

Material handling equipment

Road Development earnings in 2007 reported in

discontinued operations

10

Segment Reporting Structure 2007

After Sale of Road Development

$ Millions

Construction Technologies Segment Eliminated

Utility Equipment and Attachment Results Reported in

Compact Vehicle Technologies Segment

Road Development

Sold

Utility Equipment

Attachments

Bobcat

Club Car

Construction

Technologies

Compact Vehicle

Technologies

Bobcat

Club Car

Utility Equipment

Attachments

Compact Vehicle

Technologies

2006 Segments

2007

Reported Revenues

$1,362

Reported Revenues

$2,641

Reported Revenues

Pro Forma 2006

$3,278

2006

11

Powerful Market Leading Brands

#1 N. America

lock and door

hardware

#1 Worldwide

golf cars

#1 N. America

air compressors,

air tools

#1 Worldwide

compact

equipment

#1 N. America

remote display

cases

#1 N. American

service provider

#1 Worldwide

transport

refrigeration

#1 or #2 in Major Markets

12

A Balanced, Global Growth Portfolio

Diversified Product and Geographic Mix;

Growth in High Potential Markets

N. America

62%

Europe

25%

Latin

America

4%

Asia

9%

Compact Vehicle

Technologies

31%

Climate Control

Technologies

30%

Security

Technologies

21%

Industrial

Technologies

18%

2006 Pro Forma Revenues $10.7 Billion

Revenues Exclude Road Development

13

Dramatic Growth

Innovation

Recurring Revenue

Acquisitions

2006 and 2007

Growth Initiatives

14

Market-Defining Innovations

Innovation Across Our Businesses

15

Innovation

Net Revenue from Innovation

$ Millions

Over $1.3 Billion in 2006 Revenues from Products

Introduced Over the Last 3 Years

2006

$225

2005

$335

$300

2004

$200

2003

16

Recurring Revenue

Recurring Revenue More than Doubled Since 2000

$ Millions

21%

% of

Total

2000

$1,190

16%

2001

$1,323

2002

$1,455

2003

$1,705

2005

$2,173

$2,413

2006

2004

$1,908

11% Growth

in 2006

17

Acquisitions

More than 65 acquisitions since 2000; added more than

$3 billion in revenues

Continuing progress in 2006

ZEKS compressed-air treatment technologies

BOC Edwards low-pressure air business

Geith attachments

Expanding into New Products and Markets

18

Increase Investments for Growth in 2006 and 2007

New product/new customer development

Expand geographic reach

Channel expansion

Recurring revenue growth

Completed $80 Mil. program in 2006, additional investment in

2007

Grow 2x GDP in Developed Countries

Grow 20% to 25% in Developing World

19

Annual Revenues

Demonstrating Growth Across Our Businesses

2004

13.9%

$9,394

2005

12.3%

$10,547

YOY

Growth

2003

8.8%

$8,249

2001

$7,389

$7,583

2002

2.6%

2006

8.2%

$11,409

20

Operational Excellence

Reduce costs

Improve processes

Increase efficiency

Institutionalize a continuous-improvement culture

Focus On Reducing Working Capital and CAPEX

A Simple Story; a Complex Effort:

21

Operational Excellence

Expanding Lean Six Sigma

Positive impact on operations

Reduce costs, working capital

and CAPEX

Formalized business operating

system

Continuous improvement

Repeatable results across

business processes

Optimize processes using lean

methods and Six Sigma tools

Significant change to operating

culture

Improved Business Execution

22

Earnings Per Share

Cyclical Machinery

Diversified Industrial

Target

12%- 15%

Annual Growth

-$1.00

-$0.50

$0.00

$0.50

$1.00

$1.50

$2.00

$2.50

$3.00

$3.50

$4.00

90

OO

O6

O7

2007 Forecast

$3.50-$3.60

$4.50

EPS

23

$762

Improved Available Cash Flow

$ Millions

* Excluding restructuring

Total $2.7 Billion

(2001 – 2004)

Total $304 Million

(1991 - 1994)

1992

1993

1991

$90

$143

$687*

2002

2001

$618*

$630

2003

1994

2004

$804

$38

$33

2005

$784

2006

$900 Million Target for 2007

24

ROIC

2004

13.0%

2005

14.0%

2003

8.3%

2001

8.6%

9.8%

2002

Improving the Way We Leverage Our Capital

Target 15%

2006

14.2%

25

Revenues

$ Millions

2002

$35

2003

$135

2004

$285

2005

$400

2006

$550

$750

2008

Target

Dual Citizenship

Enterprise Growth Initiatives

26

Dividends and Share Repurchase

13% Increase in quarterly dividends in 2006,

90% increase over last three years

Completed $2 Billion repurchase first authorized in 2004

Purchased 2.6 Million shares in October 2006

Purchased 51 Million shares since start of program,

reduced outstanding share count by 14%

New repurchase program authorized for $2 Billion in

December 2006

Deploying Cash to Create Shareholder Value

27

Cash Deployment

$ Millions

Balanced Approach to Cash Deployments

2006 Target Actual

Acquisitions $400 - $600 $122

Share Buyback 600 - 400 1,096

Subtotal $1,000 $ 1,218

R&D and Engineering 150 - 170 175

Growth Investments 80 77

Total $1.2 Billion $1.5 Billion

2007

Acquisitions $400 - $600

Share Buyback 600 - 400

Subtotal $1,000

R&D and Engineering 175 - 200

Growth Investments 80

OpEx Investments 70

Total $1.3 Billion

Additional Cash

Available from

the Sale of the

Road

Development

Business

28

Opportunity Ahead

Completed record year in 2006, expecting record revenues, EPS

and cash flow in 2007

Diversified business portfolio and lean business model to dampen

impact of market cycles

Deploying cash to generate value for shareholders

Additional purchasing power from sale of Road Development

Increased investments for growth and operational excellence

Well positioned to deliver

Consistent profitable growth

Strong cash flow

Successfully Executing Sound Long-term Growth Strategy

29

30