Exhibit 99.1

Key Highlights 1 Banco de Chile Earnings Report 3Q21

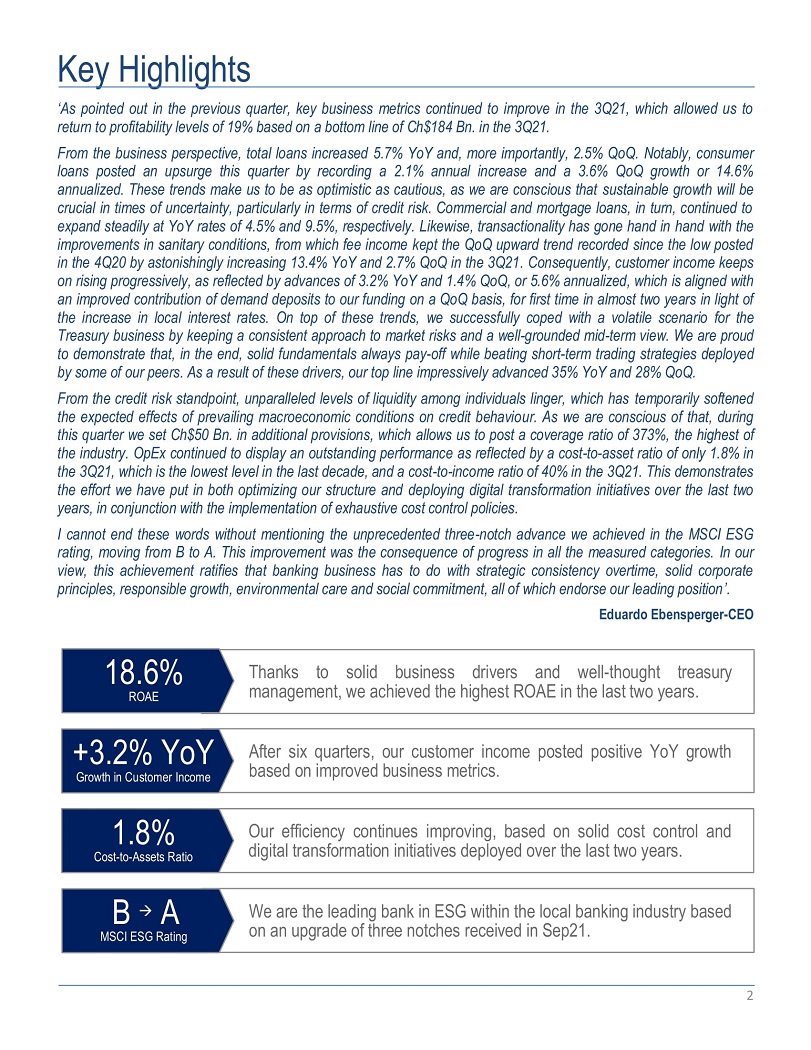

Key Highlights ‘As pointed out in the previous quarter, key business metrics continued to improve in the 3 Q 21 , which allowed us to return to profitability levels of 19 % based on a bottom line of Ch $ 184 Bn . in the 3 Q 21 . From the business perspective, total loans increased 5 . 7 % YoY and, more importantly, 2 . 5 % QoQ . Notably, consumer loans posted an upsurge this quarter by recording a 2 . 1 % annual increase and a 3 . 6 % QoQ growth or 14 . 6 % annualized . These trends make us to be as optimistic as cautious, as we are conscious that sustainable growth will be crucial in times of uncertainty, particularly in terms of credit risk . Commercial and mortgage loans, in turn, continued to expand steadily at YoY rates of 4 . 5 % and 9 . 5 % , respectively . Likewise, transactionality has gone hand in hand with the improvements in sanitary conditions, from which fee income kept the QoQ upward trend recorded since the low posted in the 4 Q 20 by astonishingly increasing 13 . 4 % YoY and 2 . 7 % QoQ in the 3 Q 21 . Consequently, customer income keeps on rising progressively, as reflected by advances of 3 . 2 % YoY and 1 . 4 % QoQ, or 5 . 6 % annualized, which is aligned with an improved contribution of demand deposits to our funding on a QoQ basis, for first time in almost two years in light of the increase in local interest rates . On top of these trends, we successfully coped with a volatile scenario for the Treasury business by keeping a consistent approach to market risks and a well - grounded mid - term view . We are proud to demonstrate that, in the end, solid fundamentals always pay - off while beating short - term trading strategies deployed by some of our peers . As a result of these drivers, our top line impressively advanced 35 % YoY and 28 % QoQ . From the credit risk standpoint, unparalleled levels of liquidity among individuals linger, which has temporarily softened the expected effects of prevailing macroeconomic conditions on credit behaviour . As we are conscious of that, during this quarter we set Ch $ 50 Bn . in additional provisions, which allows us to post a coverage ratio of 373 % , the highest of the industry . OpEx continued to display an outstanding performance as reflected by a cost - to - asset ratio of only 1 . 8 % in the 3 Q 21 , which is the lowest level in the last decade, and a cost - to - income ratio of 40 % in the 3 Q 21 . This demonstrates the effort we have put in both optimizing our structure and deploying digital transformation initiatives over the last two years, in conjunction with the implementation of exhaustive cost control policies . I cannot end these words without mentioning the unprecedented three - notch advance we achieved in the MSCI ESG rating, moving from B to A . This improvement was the consequence of progress in all the measured categories . In our view, this achievement ratifies that banking business has to do with strategic consistency overtime, solid corporate principles, responsible growth, environmental care and social commitment, all of which endorse our leading position’ . Eduardo Ebensperger - CEO Tha n k s t o s o l i d b u s i n e s s d r i v e r s a n d w e l l - t h o ught t re a s ur y management, we achieved the highest ROAE in the last two years. 18.6% ROAE After six quarters, our customer income posted positive YoY growth based on improved business metrics. +3.2% YoY Growth in Customer Income Our efficiency continues improving, based on solid cost control and digital transformation initiatives deployed over the last two years. 1.8% Cost - to - Assets Ratio We are the leading bank in ESG within the local banking industry based on an upgrade of three notches received in Sep21. B A MSCI ESG Rating 2

Financial Snapshot 3Q21 (In billions of Ch$) Net Income 88 184 1 1 . 9 90 . 7 19 .6 ( 9 . 7 ) ( 17 . 9 ) 3 Q 2 0 3 Q 2 1 Loa n Lo s s P r o v . Non - c u s t o m e r Income O p . E x pen s e s I n c o m e t a x & Others +108.8% C u s t o m e r Income ~24,000 SMEs Participated in the 6 th version of our “Entrepreneur Challenge” 0.92% NPLs Lowest delinquency ratio in recent years as of Sep21 (>90 days past - due) Ratios 3Q21 YTD ROAE 18.6% 17.5% NIM 3.6% 3.5% LLP / Avg. Loans 1.1% 0.9% Efficiency Ratio 40.1% 43.3% TIER I Ratio 12.4% 12.4% +51% YoY in origination of Mortgage Loans, in spite of the increase in interest rates (~Ch$433 Bn. in the 3Q21) 40% Cost - to - Income ratio in the 3Q21, based on solid efficiency initiatives 208% Average LCR Ratio in the 3Q21, based on solid buffers and proactive management of mismatches 373% Coverage Ratio (including additional allowances), which is the highest among peers as of Sep21 12.4% CET1 and 16 . 3 % BIS Ratios . The Soundest Capital position among major lo c al b a n k s Talent For 8 th consecutive year we ranked as the best bank in talent attraction by M e r c o +117% YoY and +28% QoQ in origination of Consumer Loans returning to pre - Covid levels (~Ch$520 Bn. in the 3Q21) 3

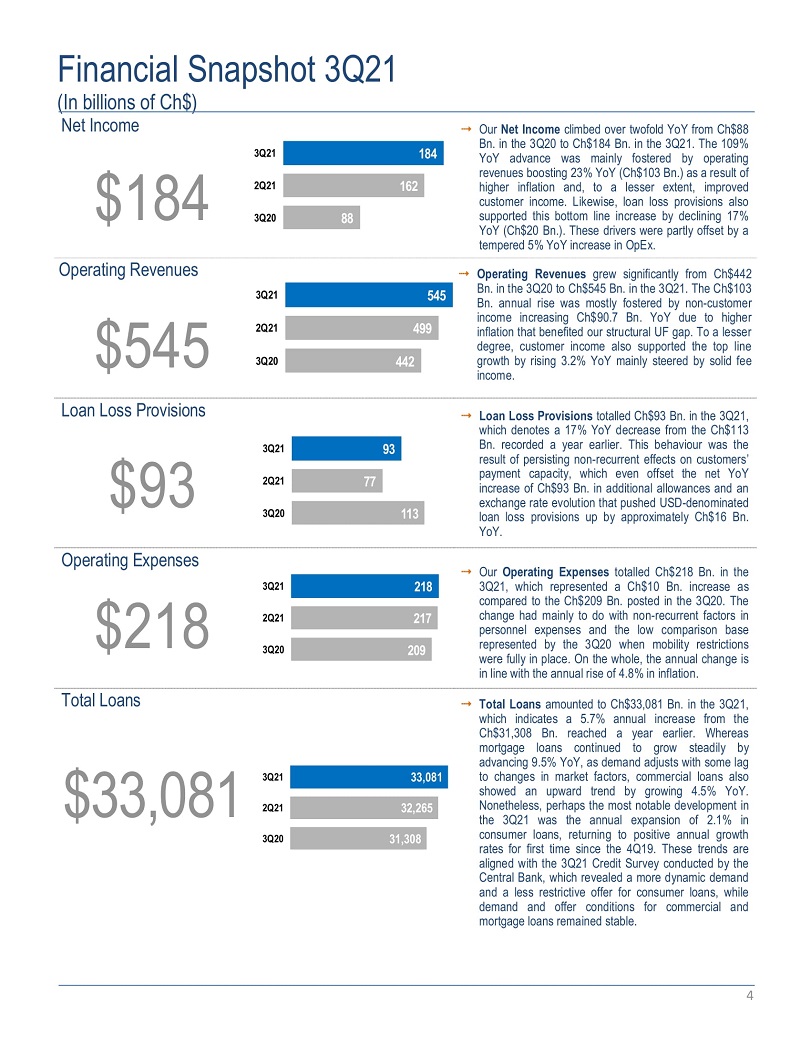

Financial Snapshot 3Q21 (In billions of Ch$) Net Income Our Net Income climbed over twofold YoY from Ch $ 88 Bn . in the 3 Q 20 to Ch $ 184 Bn . in the 3 Q 21 . The 109 % YoY advance was mainly fostered by operating revenues boosting 23 % YoY (Ch $ 103 Bn . ) as a result of higher inflation and, to a lesser extent, improved customer income . Likewise, loan loss provisions also supported this bottom line increase by declining 17 % YoY (Ch $ 20 Bn . ) . These drivers were partly offset by a tempered 5 % YoY increase in OpEx . $184 3Q21 184 2Q21 162 3Q20 88 Operating Revenues Operating Revenues grew significantly from Ch $ 442 Bn . in the 3 Q 20 to Ch $ 545 Bn . in the 3 Q 21 . The Ch $ 103 Bn . annual rise was mostly fostered by non - customer income increasing Ch $ 90 . 7 Bn . YoY due to higher inflation that benefited our structural UF gap . To a lesser degree, customer income also supported the top line growth by rising 3 . 2 % YoY mainly steered by solid fee income . $545 3 Q 2 1 545 2Q21 499 3Q20 442 Loan Loss Provisions Loan Loss Provisions totalled Ch $ 93 Bn . in the 3 Q 21 , which denotes a 17 % YoY decrease from the Ch $ 113 Bn . recorded a year earlier . This behaviour was the result of persisting non - recurrent effects on customers’ payment capacity, which even offset the net YoY increase of Ch $ 93 Bn . in additional allowances and an exchange rate evolution that pushed USD - denominated loan loss provisions up by approximately Ch $ 16 Bn . YoY . $93 3Q21 93 2Q21 77 3Q20 113 Operating Expenses Our Operating Expenses totalled Ch $ 218 Bn . in the 3 Q 21 , which represented a Ch $ 10 Bn . increase as compared to the Ch $ 209 Bn . posted in the 3 Q 20 . The change had mainly to do with non - recurrent factors in personnel expenses and the low comparison base represented by the 3 Q 20 when mobility restrictions were fully in place . On the whole, the annual change is in line with the annual rise of 4 . 8 % in inflation . $218 3Q21 2Q21 3Q20 218 217 209 Total Loans Total Loans amounted to Ch $ 33 , 081 Bn . in the 3 Q 21 , which indicates a 5 . 7 % annual increase from the Ch $ 31 , 308 Bn . reached a year earlier . Whereas mortgage loans continued to grow steadily by advancing 9 . 5 % YoY, as demand adjusts with some lag to changes in market factors, commercial loans also showed an upward trend by growing 4 . 5 % YoY . Nonetheless, perhaps the most notable development in the 3 Q 21 was the annual expansion of 2 . 1 % in consumer loans, returning to positive annual growth rates for first time since the 4 Q 19 . These trends are aligned with the 3 Q 21 Credit Survey conducted by the Central Bank, which revealed a more dynamic demand and a less restrictive offer for consumer loans, while demand and offer conditions for commercial and mortgage loans remained stable . $33,081 3Q21 2Q21 33,081 32,265 3Q20 31,308 4

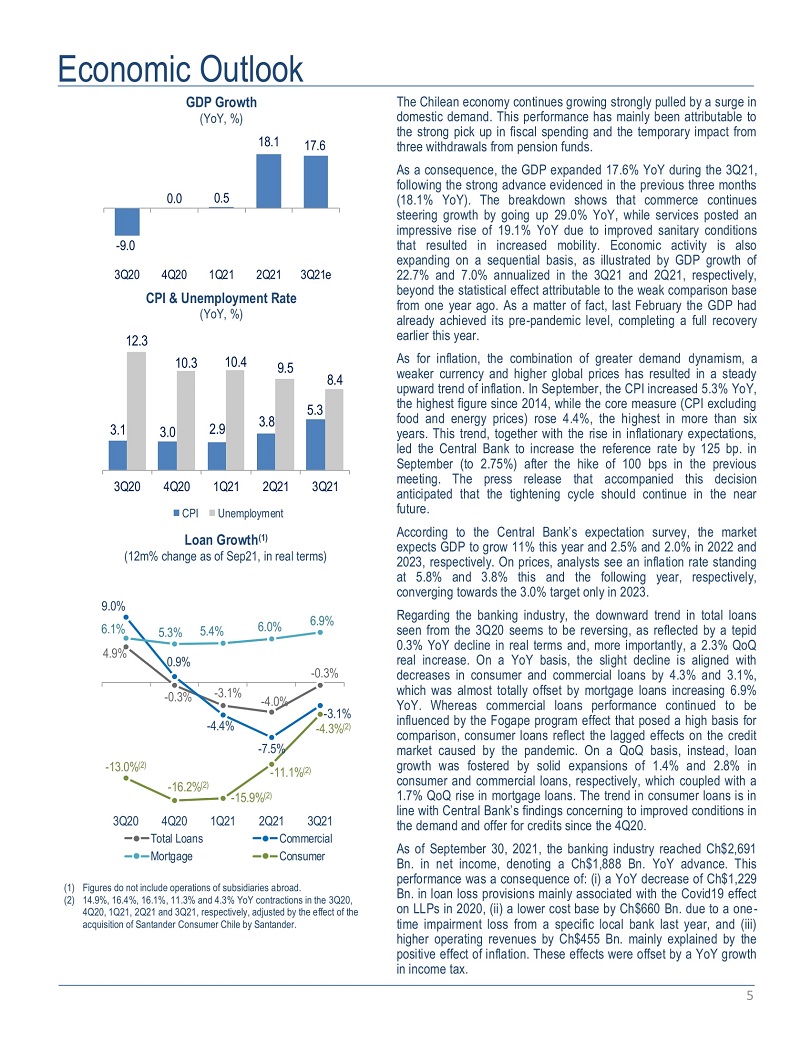

Economic Outlook GDP Growth (YoY, %) 18. 1 0. 0 0. 5 17 . 6 3 Q 2 1 e 3 . 1 3 . 0 2 . 9 3. 8 5. 3 - 9.0 3Q20 4Q20 1Q21 2Q21 CPI & Unemployment Rate (YoY, %) 12.3 10.3 10.4 9. 5 8. 4 3Q20 4Q20 1Q21 2Q21 3Q21 CPI Unemployment Loan Growth (1) (12m% change as of Sep21, in real terms) - 0 . 3 % - 3.1 % - 4.0 % - 0.3 % 0 . 9 % - 4 . 4 % 9.0% 6.1% 4.9 % 5.3 % 5 . 4 % 6.0 % 6 .9 % - 13.0% (2) - 16.2% (2) - 7.5% - 11.1% (2) - 15.9% (2) - 3.1% - 4.3% (2) 3 Q 2 0 4Q20 Total Loans Mortgage 1 Q 2 1 2 Q 2 1 3 Q 2 1 C o m m e r ci a l Consumer 5 (1) Figures do not include operations of subsidiaries abroad. (2) 14.9%, 16.4%, 16.1%, 11.3% and 4.3% YoY contractions in the 3Q20, 4Q20, 1Q21, 2Q21 and 3Q21, respectively, adjusted by the effect of the acquisition of Santander Consumer Chile by Santander. The Chilean economy continues growing strongly pulled by a surge in domestic demand . This performance has mainly been attributable to the strong pick up in fiscal spending and the temporary impact from three withdrawals from pension funds . As a consequence, the GDP expanded 17 . 6 % YoY during the 3 Q 21 , following the strong advance evidenced in the previous three months ( 18 . 1 % YoY) . The breakdown shows that commerce continues steering growth by going up 29 . 0 % YoY, while services posted an impressive rise of 19 . 1 % YoY due to improved sanitary conditions that resulted in increased mobility . Economic activity is also expanding on a sequential basis, as illustrated by GDP growth of 22 . 7 % and 7 . 0 % annualized in the 3 Q 21 and 2 Q 21 , respectively, beyond the statistical effect attributable to the weak comparison base from one year ago . As a matter of fact, last February the GDP had already achieved its pre - pandemic level, completing a full recovery earlier this year . As for inflation, the combination of greater demand dynamism, a weaker currency and higher global prices has resulted in a steady upward trend of inflation . In September, the CPI increased 5 . 3 % YoY, the highest figure since 2014 , while the core measure (CPI excluding food and energy prices) rose 4 . 4 % , the highest in more than six years . This trend, together with the rise in inflationary expectations, led the Central Bank to increase the reference rate by 125 bp . in September (to 2 . 75 % ) after the hike of 100 bps in the previous meeting . The press release that accompanied this decision anticipated that the tightening cycle should continue in the near future . According to the Central Bank’s expectation survey, the market expects GDP to grow 11 % this year and 2 . 5 % and 2 . 0 % in 2022 and 2023 , respectively . On prices, analysts see an inflation rate standing at 5 . 8 % and 3 . 8 % this and the following year, respectively, converging towards the 3 . 0 % target only in 2023 . Regarding the banking industry, the downward trend in total loans seen from the 3 Q 20 seems to be reversing, as reflected by a tepid 0 . 3 % YoY decline in real terms and, more importantly, a 2 . 3 % QoQ real increase . On a YoY basis, the slight decline is aligned with decreases in consumer and commercial loans by 4 . 3 % and 3 . 1 % , which was almost totally offset by mortgage loans increasing 6 . 9 % YoY . Whereas commercial loans performance continued to be influenced by the Fogape program effect that posed a high basis for comparison, consumer loans reflect the lagged effects on the credit market caused by the pandemic . On a QoQ basis, instead, loan growth was fostered by solid expansions of 1 . 4 % and 2 . 8 % in consumer and commercial loans, respectively, which coupled with a 1 . 7 % QoQ rise in mortgage loans . The trend in consumer loans is in line with Central Bank’s findings concerning to improved conditions in the demand and offer for credits since the 4 Q 20 . As of September 30 , 2021 , the banking industry reached Ch $ 2 , 691 Bn . in net income, denoting a Ch $ 1 , 888 Bn . YoY advance . This performance was a consequence of : (i) a YoY decrease of Ch $ 1 , 229 Bn . in loan loss provisions mainly associated with the Covid 19 effect on LLPs in 2020 , (ii) a lower cost base by Ch $ 660 Bn . due to a one - time impairment loss from a specific local bank last year, and (iii) higher operating revenues by Ch $ 455 Bn . mainly explained by the positive effect of inflation . These effects were offset by a YoY growth in income tax .

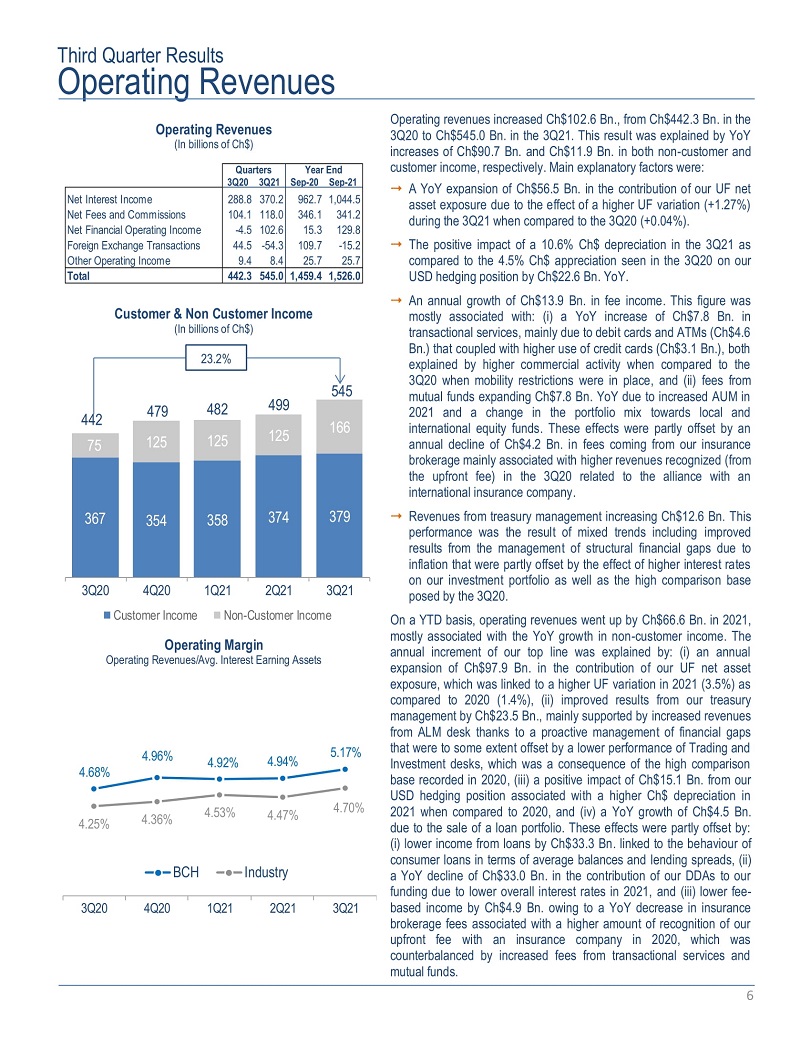

Third Quarter Results Operating Revenues Operating revenues increased Ch$102.6 Bn., from Ch$442.3 Bn. in the 3 Q 20 to Ch $ 545 . 0 Bn . in the 3 Q 21 . This result was explained by YoY increases of Ch $ 90 . 7 Bn . and Ch $ 11 . 9 Bn . in both non - customer and customer income, respectively . Main explanatory factors were : A YoY expansion of Ch $ 56 . 5 Bn . in the contribution of our UF net asset exposure due to the effect of a higher UF variation (+ 1 . 27 % ) during the 3 Q 21 when compared to the 3 Q 20 (+ 0 . 04 % ) . The positive impact of a 10 . 6 % Ch $ depreciation in the 3 Q 21 as compared to the 4 . 5 % Ch $ appreciation seen in the 3 Q 20 on our USD hedging position by Ch $ 22 . 6 Bn . YoY . An annual growth of Ch $ 13 . 9 Bn . in fee income . This figure was mostly associated with : (i) a YoY increase of Ch $ 7 . 8 Bn . in transactional services, mainly due to debit cards and ATMs (Ch $ 4 . 6 Bn . ) that coupled with higher use of credit cards (Ch $ 3 . 1 Bn . ), both explained by higher commercial activity when compared to the 3 Q 20 when mobility restrictions were in place, and (ii) fees from mutual funds expanding Ch $ 7 . 8 Bn . YoY due to increased AUM in 2021 and a change in the portfolio mix towards local and international equity funds . These effects were partly offset by an annual decline of Ch $ 4 . 2 Bn . in fees coming from our insurance brokerage mainly associated with higher revenues recognized (from the upfront fee) in the 3 Q 20 related to the alliance with an international insurance company . Revenues from treasury management increasing Ch $ 12 . 6 Bn . This performance was the result of mixed trends including improved results from the management of structural financial gaps due to inflation that were partly offset by the effect of higher interest rates on our investment portfolio as well as the high comparison base posed by the 3 Q 20 . On a YTD basis, operating revenues went up by Ch $ 66 . 6 Bn . in 2021 , mostly associated with the YoY growth in non - customer income . The annual increment of our top line was explained by : (i) an annual expansion of Ch $ 97 . 9 Bn . in the contribution of our UF net asset exposure, which was linked to a higher UF variation in 2021 ( 3 . 5 % ) as compared to 2020 ( 1 . 4 % ), (ii) improved results from our treasury management by Ch $ 23 . 5 Bn . , mainly supported by increased revenues from ALM desk thanks to a proactive management of financial gaps that were to some extent offset by a lower performance of Trading and Investment desks, which was a consequence of the high comparison base recorded in 2020 , (iii) a positive impact of Ch $ 15 . 1 Bn . from our USD hedging position associated with a higher Ch $ depreciation in 2021 when compared to 2020 , and (iv) a YoY growth of Ch $ 4 . 5 Bn . due to the sale of a loan portfolio . These effects were partly offset by : (i) lower income from loans by Ch $ 33 . 3 Bn . linked to the behaviour of consumer loans in terms of average balances and lending spreads, (ii) a YoY decline of Ch $ 33 . 0 Bn . in the contribution of our DDAs to our funding due to lower overall interest rates in 2021 , and (iii) lower fee - based income by Ch $ 4 . 9 Bn . owing to a YoY decrease in insurance brokerage fees associated with a higher amount of recognition of our upfront fee with an insurance company in 2020 , which was counterbalanced by increased fees from transactional services and mutual funds . Operating Revenues ( I n b ill i on s o f C h$ ) Quarters 3Q20 3Q21 Y ea r E n d Sep - 20 Sep - 21 Net Interest Income 288.8 370.2 962.7 1,044.5 Net Fees and Commissions 104.1 118.0 346.1 341.2 Net Financial Operating Income - 4.5 102.6 15.3 129.8 Foreign Exchange Transactions 44.5 - 54.3 109.7 - 15.2 Other Operating Income 9.4 8.4 25.7 25.7 Total 442.3 545.0 1,459.4 1,526.0 Customer & Non Customer Income ( I n b ill i on s o f C h$ ) 367 354 358 374 379 75 125 125 125 166 442 479 482 499 545 3 Q 2 0 4 Q 2 0 1 Q 2 1 2 Q 2 1 3 Q 2 1 Customer Income Non - Customer Income Operating Margin Operating Revenues/Avg. Interest Earning Assets 4.68 % 4.96 % 4.92 % 4.94 % 5 . 1 7 % 4.2 5 % 4 . 36 % 4.53 % 4.47 % 4.7 0 % 3 Q 2 0 4 Q 2 0 1 Q 2 1 2 Q 2 1 3 Q 2 1 BC H I ndu s t r y 23.2% 6

Third Quarter Results Loan Loss Provisions & Allowances Our loan loss provisions accounted for Ch $ 92 . 9 Bn . in the 3 Q 21 , which represents a decrease of 17 . 4 % or Ch $ 19 . 6 Bn . when compared to a year earlier . The improvement in LLP continued to be influenced by non - recurrent factors that resulted in better than normal payment capacity, particularly among individuals, that coupled with tempered growth in riskier lending products . In this environment, the decrease in LLP was supported by both the retail and the wholesale banking segments, which posted an overall decrease of Ch $ 131 . 3 Bn . in recurrent LLP . This trend was partly offset by higher additional provisions and the impact of higher exchange rates . The main drivers conducting the annual change in risk expenses were : Net credit quality improvement of Ch $ 131 . 3 Bn . YoY in the 3 Q 21 , which continued to be steered by low delinquency as demonstrated by our NPL ratio (> 90 days overdue loans) of 0 . 9 % in the 3 Q 21 , which is almost 20 bps . below the two - year average . Aligned with this, the retail banking segment had an annual improvement of Ch $ 109 . 6 Bn . in LLP, fostered by both below trend asset quality indicators in this segment and a high comparison base in the 3 Q 20 explained by the recalibration of group - based models . To a lesser extent, the wholesale banking segment contributed with a net improvement of Ch $ 21 . 7 Bn . , explained by a high comparison base owing to the impact of mobility restrictions that lingered a year earlier on companies’ payment capacity . These factors were partly offset by: A net effect of higher additional provisions by Ch $ 93 . 0 Bn . due to the release of Ch $ 43 Bn . in the 3 Q 20 (as result of recalibration of group - based provisioning models) and the establishment of Ch $ 50 . 0 Bn . in the 3 Q 21 . A negative impact of ~Ch $ 16 . 4 Bn . on our USD denominated loan loss allowances due to the sharp Ch $ depreciation of 10 . 6 % in the 3 Q 21 as compared to the 4 . 5 % Ch $ appreciation in the 3 Q 20 . Loan growth explaining ~Ch $ 2 . 3 Bn . YoY due to average loans increasing of 5 . 7 % YoY, mainly in the retail banking segment . Based on the above, our LLP to average loans ratio reached 1 . 14 % in the 3 Q 21 , denoting a 32 bp . YoY improvement . On a YTD basis, LLP decreased 40 . 7 % YoY from Ch $ 377 . 5 Bn . as of Sep 20 to Ch $ 223 . 8 Bn . as of Sep 21 , mainly as a result of : A net credit quality improvement of Ch $ 281 . 9 Bn . related to credit quality indicators that have experienced significant advances when compared to 2020 . As reported in previous quarters, this trend has been related to the measures taken by the government, the Central Bank and the Congress to assist individuals and companies to tackle Covid - 19 aftermath . Thus, the retail banking segment concentrated a Ch $ 208 . 5 Bn . YoY improvement while the wholesale banking segment benefited from an effect of Ch $ 73 . 4 Bn . YoY . These effects were partly offset by : (i) higher additional provisions set during the period by Ch $ 113 . 0 Bn . to be suitably prepared for expected lagged effects in asset quality, (ii) negative exchange rate effect of higher Ch $ depreciation in 2021 ( 14 . 0 % ) than in 2020 ( 4 . 3 % ) explaining ~Ch $ 11 . 0 Bn . of higher LLP, and (iii) loan growth conducting an increase of ~Ch $ 4 . 2 Bn . based on average loans expanding 4 . 6 % on a YoY basis . Loan Loss Provisions & Allowances ( I n b ill i on s o f C h$ ) Quarters 3Q2 0 3Q2 1 Year End S e p - 2 0 S e p - 2 1 Loan Loss Allowances Initial Allowances - 679.3 - 687.5 - 685.4 - 746.9 Charge - offs 70.3 66.7 276.9 185.1 Sales of Loans 0.0 0.0 0.2 14.5 Provisions established, net - 157.3 - 55.6 - 357.9 - 129.0 Final Allowances - 766.2 - 676.4 - 766.2 - 676.4 Provisions Established - 157.3 - 55.6 - 357.9 - 129.0 Prov. Financial Guarantees - 10.1 - 3.7 - 21.3 - 2.1 Additional Provisions 43.0 - 50.0 - 27.0 - 140.0 Recoveries 11.8 16.4 28.7 47.4 Loan Loss Provisions - 112.5 - 92.9 - 377.5 - 223.8 Credit Quality Ratios Allowances / Total loans 2.45% 2.04% 2.45% 2.04% Allowances / Total Past Due (1) 3.30x 3.73x 3.30x 3.73x Provisions / Avg. Loans 1.46% 1.14% 1.65% 0.93% Charge - offs / Avg. Loans 0.91% 0.82% 1.21% 0.77% Total Past Due / Total Loans 0.98% 0.92% 0.98% 0.92% Recoveries / Avg. Loans 0.15% 0.20% 0.13% 0.20% (1) Including additional allowances. Provisions / Average Loans 1 . 46 % 1 . 09 % 0 . 69 % 0.9 6 % 1 . 4 2 % 1 . 5 1 % 0 . 72 % 0.8 5 % 1 . 14 % 1.09% 3 Q 2 0 4Q20 1Q21 2Q21 Total Past Due / Total Loans 3 Q 2 1 B C H Industry 1 . 33 % 0 . 98 % 0.97% 0 . 9 6 % 1 . 04 % 0 . 9 2 % 2 . 06 % 1 . 87 % 1 . 64 % 1 . 56 % 1 . 55 % 1 . 45 % 2 Q 2 0 3 Q 2 0 4 Q 2 0 1 Q 2 1 2 Q 2 1 3 Q 2 1 BCH I n du s t r y 7

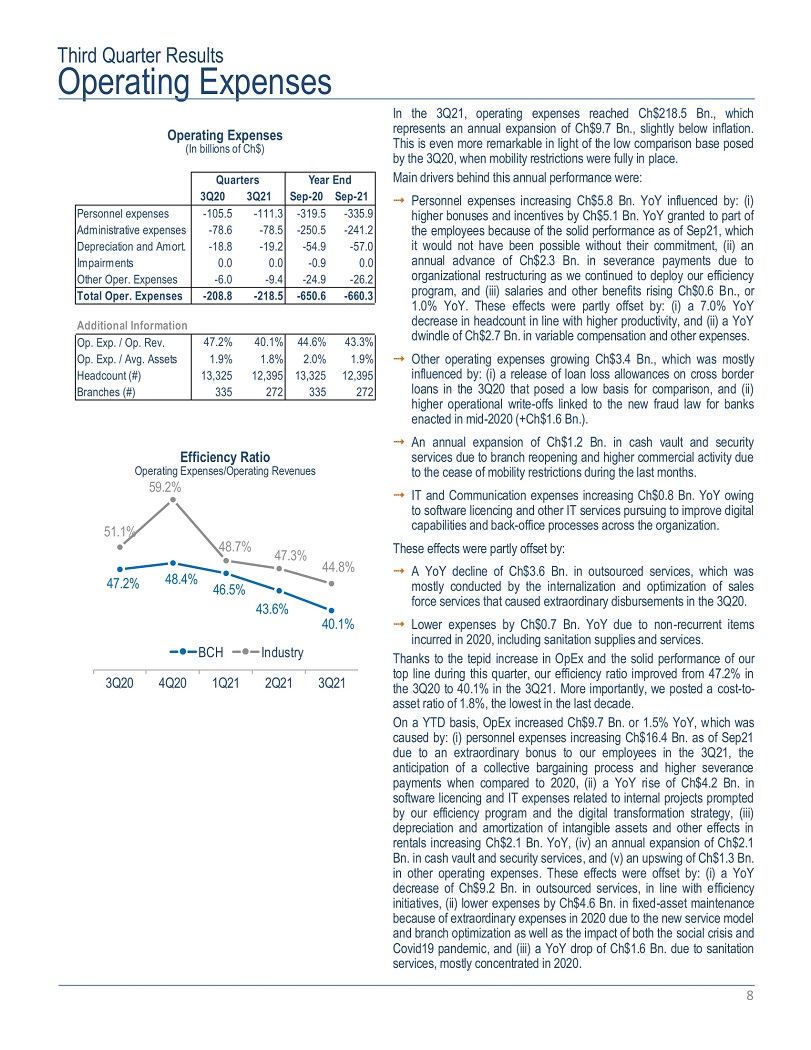

Third Quarter Results Operating Expenses In the 3Q21, operating expenses reached Ch$218.5 Bn., which represents an annual expansion of Ch$9.7 Bn., slightly below inflation. This is even more remarkable in light of the low comparison base posed by the 3Q20, when mobility restrictions were fully in place. Main drivers behind this annual performance were: Personnel expenses increasing Ch $ 5 . 8 Bn . YoY influenced by : (i) higher bonuses and incentives by Ch $ 5 . 1 Bn . YoY granted to part of the employees because of the solid performance as of Sep 21 , which it would not have been possible without their commitment, (ii) an annual advance of Ch $ 2 . 3 Bn . in severance payments due to organizational restructuring as we continued to deploy our efficiency program, and (iii) salaries and other benefits rising Ch $ 0 . 6 Bn . , or 1 . 0 % YoY . These effects were partly offset by : (i) a 7 . 0 % YoY decrease in headcount in line with higher productivity, and (ii) a YoY dwindle of Ch $ 2 . 7 Bn . in variable compensation and other expenses . Other operating expenses growing Ch $ 3 . 4 Bn . , which was mostly influenced by : (i) a release of loan loss allowances on cross border loans in the 3 Q 20 that posed a low basis for comparison, and (ii) higher operational write - offs linked to the new fraud law for banks enacted in mid - 2020 (+Ch $ 1 . 6 Bn . ) . An annual expansion of Ch $ 1 . 2 Bn . in cash vault and security services due to branch reopening and higher commercial activity due to the cease of mobility restrictions during the last months . IT and Communication expenses increasing Ch $ 0 . 8 Bn . YoY owing to software licencing and other IT services pursuing to improve digital capabilities and back - office processes across the organization . These effects were partly offset by : A YoY decline of Ch $ 3 . 6 Bn . in outsourced services, which was mostly conducted by the internalization and optimization of sales force services that caused extraordinary disbursements in the 3 Q 20 . Lower expenses by Ch $ 0 . 7 Bn . YoY due to non - recurrent items i n c u r r e d i n 2 0 20 , i n c l u d i n g s a n i t a t i o n s u p p l i es and s er v i c e s . Thanks to the tepid increase in OpEx and the solid performance of our top line during this quarter, our efficiency ratio improved from 47 . 2 % in the 3 Q 20 to 40 . 1 % in the 3 Q 21 . More importantly, we posted a cost - to - asset ratio of 1 . 8 % , the lowest in the last decade . On a YTD basis, OpEx increased Ch $ 9 . 7 Bn . or 1 . 5 % YoY, which was caused by : (i) personnel expenses increasing Ch $ 16 . 4 Bn . as of Sep 21 due to an extraordinary bonus to our employees in the 3 Q 21 , the anticipation of a collective bargaining process and higher severance payments when compared to 2020 , (ii) a YoY rise of Ch $ 4 . 2 Bn . in software licencing and IT expenses related to internal projects prompted by our efficiency program and the digital transformation strategy, (iii) depreciation and amortization of intangible assets and other effects in rentals increasing Ch $ 2 . 1 Bn . YoY, (iv) an annual expansion of Ch $ 2 . 1 Bn . in cash vault and security services, and (v) an upswing of Ch $ 1 . 3 Bn . in other operating expenses . These effects were offset by : (i) a YoY decrease of Ch $ 9 . 2 Bn . in outsourced services, in line with efficiency initiatives, (ii) lower expenses by Ch $ 4 . 6 Bn . in fixed - asset maintenance because of extraordinary expenses in 2020 due to the new service model and branch optimization as well as the impact of both the social crisis and Covid 19 pandemic, and (iii) a YoY drop of Ch $ 1 . 6 Bn . due to sanitation services, mostly concentrated in 2020 . Operating Expenses ( I n b ill i on s o f C h$ ) Quarters 3Q20 3Q21 Year End Sep - 20 Sep - 21 Personnel expenses - 105.5 - 111.3 - 319.5 - 335.9 Administrative expenses - 78.6 - 78.5 - 250.5 - 241.2 Depreciation and Amort. - 18.8 - 19.2 - 54.9 - 57.0 Impairments 0.0 0.0 - 0.9 0.0 Other Oper. Expenses - 6.0 - 9.4 - 24.9 - 26.2 Total Oper. Expenses - 208.8 - 218.5 - 650.6 - 660.3 Additional Information Op. Exp. / Op. Rev. 47.2% 40.1% 44.6% 43.3% Op. Exp. / Avg. Assets 1.9% 1.8% 2.0% 1.9% H e ad c oun t ( # ) 13,325 12,395 13,325 12,395 Branches (#) 335 272 335 272 47 . 2 % 48 . 4 % 46. 5 % 43 . 6 % 40 .1 % 51.1 % Efficiency Ratio Operating Expenses/Operating Revenues 59.2% 48 .7 % 47 . 3 % 44 . 8 % 3 Q 2 0 4 Q 2 0 1 Q 2 1 2 Q 2 1 3 Q 2 1 B C H I n du s t ry 8

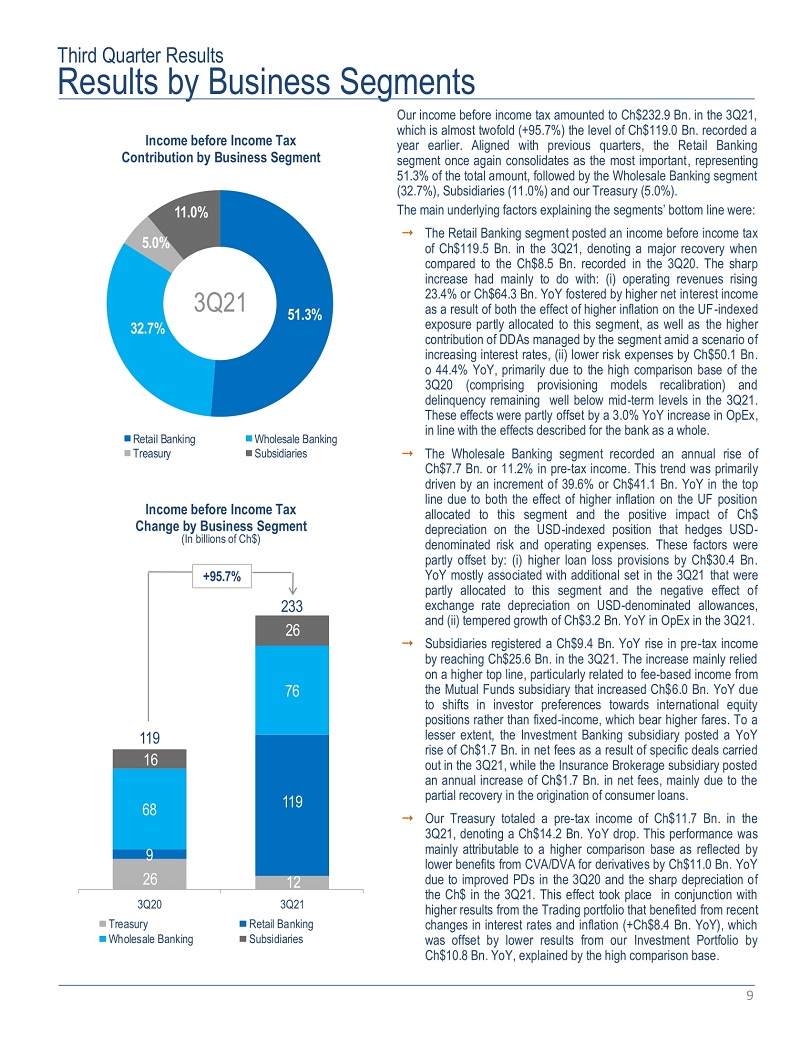

Third Quarter Results Results by Business Segments Our income before income tax amounted to Ch$232.9 Bn. in the 3Q21, which is almost twofold (+95.7%) the level of Ch$119.0 Bn. recorded a year earlier . Aligned with previous quarters, the Retail Banking segment once again consolidates as the most important, representing 51 . 3 % of the total amount, followed by the Wholesale Banking segment ( 32 . 7 % ), Subsidiaries ( 11 . 0 % ) and our Treasury ( 5 . 0 % ) . The main underlying factors explaining the segments’ bottom line were : The Retail Banking segment posted an income before income tax of Ch $ 119 . 5 Bn . in the 3 Q 21 , denoting a major recovery when compared to the Ch $ 8 . 5 Bn . recorded in the 3 Q 20 . The sharp increase had mainly to do with : (i) operating revenues rising 23 . 4 % or Ch $ 64 . 3 Bn . YoY fostered by higher net interest income as a result of both the effect of higher inflation on the UF - indexed exposure partly allocated to this segment, as well as the higher contribution of DDAs managed by the segment amid a scenario of increasing interest rates, (ii) lower risk expenses by Ch $ 50 . 1 Bn . o 44 . 4 % YoY, primarily due to the high comparison base of the 3 Q 20 (comprising provisioning models recalibration) and delinquency remaining well below mid - term levels in the 3 Q 21 . These effects were partly offset by a 3 . 0 % YoY increase in OpEx, in line with the effects described for the bank as a whole . The Wholesale Banking segment recorded an annual rise of Ch $ 7 . 7 Bn . or 11 . 2 % in pre - tax income . This trend was primarily driven by an increment of 39 . 6 % or Ch $ 41 . 1 Bn . YoY in the top line due to both the effect of higher inflation on the UF position allocated to this segment and the positive impact of Ch $ depreciation on the USD - indexed position that hedges USD - denominated risk and operating expenses . These factors were partly offset by : (i) higher loan loss provisions by Ch $ 30 . 4 Bn . YoY mostly associated with additional set in the 3 Q 21 that were partly allocated to this segment and the negative effect of exchange rate depreciation on USD - denominated allowances, and (ii) tempered growth of Ch $ 3 . 2 Bn . YoY in OpEx in the 3 Q 21 . Subsidiaries registered a Ch $ 9 . 4 Bn . YoY rise in pre - tax income by reaching Ch $ 25 . 6 Bn . in the 3 Q 21 . The increase mainly relied on a higher top line, particularly related to fee - based income from the Mutual Funds subsidiary that increased Ch $ 6 . 0 Bn . YoY due to shifts in investor preferences towards international equity positions rather than fixed - income, which bear higher fares . To a lesser extent, the Investment Banking subsidiary posted a YoY rise of Ch $ 1 . 7 Bn . in net fees as a result of specific deals carried out in the 3 Q 21 , while the Insurance Brokerage subsidiary posted an annual increase of Ch $ 1 . 7 Bn . in net fees, mainly due to the partial recovery in the origination of consumer loans . Our Treasury totaled a pre - tax income of Ch $ 11 . 7 Bn . in the 3 Q 21 , denoting a Ch $ 14 . 2 Bn . YoY drop . This performance was mainly attributable to a higher comparison base as reflected by lower benefits from CVA/DVA for derivatives by Ch $ 11 . 0 Bn . YoY due to improved PDs in the 3 Q 20 and the sharp depreciation of the Ch $ in the 3 Q 21 . This effect took place in conjunction with higher results from the Trading portfolio that benefited from recent changes in interest rates and inflation (+Ch $ 8 . 4 Bn . YoY), which was offset by lower results from our Investment Portfolio by Ch $ 10 . 8 Bn . YoY, explained by the high comparison base . Income before Income Tax Contribution by Business Segment 51 . 3 % 32 . 7 % 5 . 0 % 1 1 . 0 % R eta i l B an k i n g Treasury Wholesale Banking Subsidiaries 3 Q 2 1 Income before Income Tax Change by Business Segment (In billions of Ch$) 26 12 9 119 68 76 16 26 1 1 9 233 3Q20 Treasury Wholesale Banking 3Q21 R e t a i l B a n k i ng Subsidiaries +95.7% 9

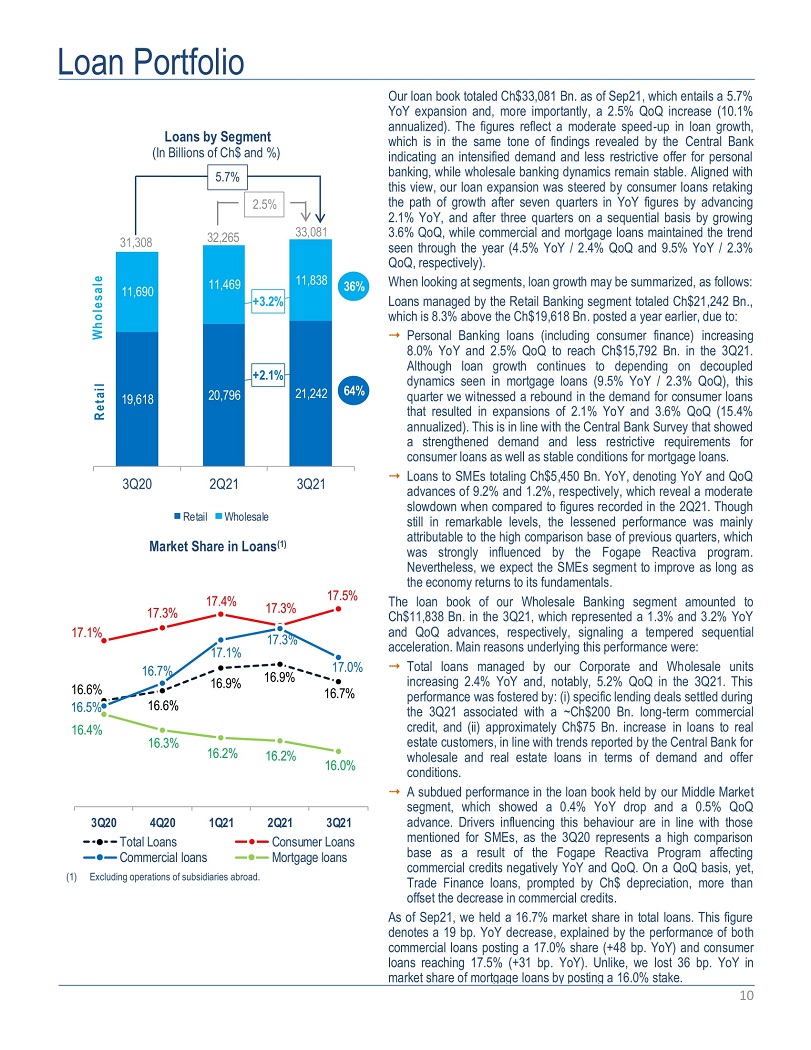

Loan Portfolio Loans by Segment (In Billions of Ch$ and %) 1 9 ,618 20 , 796 21 , 242 11 , 690 11 , 469 11 , 838 31 , 308 32 , 265 33 , 081 3 Q 2 0 2 Q 2 1 3 Q 2 1 Retail Wholesale Market Share in Loans (1) + 2. 1 % + 3 . 2 % 2.5% R e t a i l Wholesale 64 % 36 % 5.7% 17.1% 16.7% 16.3% 16.2 % 16.6% 16.5% 16.4 % 16.6% 3 Q 2 0 1 Q 2 1 4Q20 Total Loans Commercial loans 2Q21 3 C on s u me r Loa n Mortgage loans 10 (1) Excluding operations of subsidiaries abroad. Our loan book totaled Ch $ 33 , 081 Bn . as of Sep 21 , which entails a 5 . 7 % YoY expansion and, more importantly, a 2 . 5 % QoQ increase ( 10 . 1 % annualized) . The figures reflect a moderate speed - up in loan growth, which is in the same tone of findings revealed by the Central Bank indicating an intensified demand and less restrictive offer for personal banking, while wholesale banking dynamics remain stable . Aligned with this view, our loan expansion was steered by consumer loans retaking the path of growth after seven quarters in YoY figures by advancing 2 . 1 % YoY, and after three quarters on a sequential basis by growing 3 . 6 % QoQ, while commercial and mortgage loans maintained the trend seen through the year ( 4 . 5 % YoY / 2 . 4 % QoQ and 9 . 5 % YoY / 2 . 3 % QoQ, respectively) . When looking at segments, loan growth may be summarized, as follows : Loans managed by the Retail Banking segment totaled Ch $ 21 , 242 Bn . , which is 8 . 3 % above the Ch $ 19 , 618 Bn . posted a year earlier, due to : Personal Banking loans (including consumer finance) increasing 8 . 0 % YoY and 2 . 5 % QoQ to reach Ch $ 15 , 792 Bn . in the 3 Q 21 . Although loan growth continues to depending on decoupled dynamics seen in mortgage loans ( 9 . 5 % YoY / 2 . 3 % QoQ), this quarter we witnessed a rebound in the demand for consumer loans that resulted in expansions of 2 . 1 % YoY and 3 . 6 % QoQ ( 15 . 4 % annualized) . This is in line with the Central Bank Survey that showed a strengthened demand and less restrictive requirements for consumer loans as well as stable conditions for mortgage loans . Loans to SMEs totaling Ch $ 5 , 450 Bn . YoY, denoting YoY and QoQ advances of 9 . 2 % and 1 . 2 % , respectively, which reveal a moderate slowdown when compared to figures recorded in the 2 Q 21 . Though still in remarkable levels, the lessened performance was mainly attributable to the high comparison base of previous quarters, which was strongly influenced by the Fogape Reactiva program . Nevertheless, we expect the SMEs segment to improve as long as the economy returns to its fundamentals . The loan book of our Wholesale Banking segment amounted to Ch $ 11 , 838 Bn . in the 3 Q 21 , which represented a 1 . 3 % and 3 . 2 % YoY and QoQ advances, respectively, signaling a tempered sequential acceleration . Main reasons underlying this performance were : Total loans managed by our Corporate and Wholesale units increasing 2 . 4 % YoY and, notably, 5 . 2 % QoQ in the 3 Q 21 . This performance was fostered by : (i) specific lending deals settled during the 3 Q 21 associated with a ~Ch $ 200 Bn . long - term commercial credit, and (ii) approximately Ch $ 75 Bn . increase in loans to real estate customers, in line with trends reported by the Central Bank for wholesale and real estate loans in terms of demand and offer conditions . A subdued performance in the loan book held by our Middle Market segment, which showed a 0 . 4 % YoY drop and a 0 . 5 % QoQ advance . Drivers influencing this behaviour are in line with those mentioned for SMEs, as the 3 Q 20 represents a high comparison base as a result of the Fogape Reactiva Program affecting commercial credits negatively YoY and QoQ . On a QoQ basis, yet, Trade Finance loans, prompted by Ch $ depreciation, more than offset the decrease in commercial credits . As of Sep 21 , we held a 16 . 7 % market share in total loans . This figure denotes a 19 bp . YoY decrease, explained by the performance of both commercial loans posting a 17 . 0 % share (+ 48 bp . YoY) and consumer loans reaching 17 . 5 % (+ 31 bp . YoY) . Unlike, we lost 36 bp . YoY in market share of mortgage loans by posting a 16 . 0 % stake .

Funding & Capital f l u c u ta Demand Deposits to Loans Ratio (As of Sep30, 2021) 5 3 % 4 9 % 42% 2 7 % 24 % 4 3 % (1) Figures do not include operations of subsidiaries abroad. +20bp Sh a r e h o l d e r s Equity Assets Tier I Basic Capital Assets Tier I Basic Capital RWA BIS Ratio T o t a l C a p i t a l RWA 8 . 0 % 7 . 6 % 11.6% 15.0% 8 . 2 % 7 . 7 % 12 . 4 % 16.3% BCH Capital Adequacy Ratios Sep - 20 Sep - 21 + 15b p + 85b p + 132b p Comprehensive Income as of Sep21 (Ch$ Bn.) Y oY C hange (321) +166 +334 + 115 + 170 345 584 38 327 390 N e t I n c o m e C o m p r ehe n sive I n c o m e Funding & Liquidity 11 For first time in more than two years, we are witnessing a sort of slowdown in the evolution of Demand Deposit Accounts (DDAs), which posted a 21 . 3 % YoY increase and a 1 . 1 % QoQ advance by totalling Ch $ 17 , 607 Bn . in the 3 Q 21 . Whereas these growth rates are the lowest since the 3 Q 19 , this phenomenon was expected to take place to the extent non - recurrent liquidity conditions and lowest interest rates begin to disappear . Even though we acknowledge it is not possible to state that this is a breakpoint in terms of DDA funding, since a fourth withdrawal from pension funds is on congress agenda, we believe the path expected for the monetary policy interest rate should discourage depositors – individuals and companies – to hold significant amount of savings in the form of DDAs from now on . Notwithstanding the above, we continue to be the local bank with the more advantageous relationship between assets and DDAs, as demonstrated by ratios of DDAs to total loans and DDAs to total assets of 36 % and 53 % , respectively in the 3 Q 21 , above the levels posted a year earlier . Likewise, in the 3 Q 21 we were the leading bank in DDAs within the local banking system by holding a market share of 20 . 8 % . Based on these dynamics, we have begun to reactivate funding prospects associated with long - term bonds in order to address our mid - term growth in a more normalized liquidity environment, despite higher interest rates . As a result, in the 3 Q 21 we placed bonds overseas for an amount of ~Ch $ 67 Bn . or ~USD 83 million in markets such as Japan and Australia . Also, we keep on utilizing funding from commercial papers for short - term needs . Our aim is to continue analysing funding choices by taking advantage of our credit ratings and facilities we have developed over the last decade . C a p i tal A d e qu acy Our equity totalled Ch $ 4 , 042 Bn . in the 3 Q 21 , amount that was 11 . 3 % or Ch $ 410 Bn . over the Ch $ 3 , 631 posted a year earlier . The main drivers resulting in a bolstered equity were, as follows : Retention of Ch $ 242 . 8 Bn . with charge to our 2020 net income, including both the 40 % capitalization of our net distributable earnings for the FY 2020 and the effect of inflation on equity . A net income increase of Ch $ 116 . 1 Bn . YoY, once deducted the provision for minimum dividends . An annual improvement of Ch $ 50 . 8 Bn . in cumulative OCI in equity, which stemmed from the sharp and steady increase in local long - term interest rates YTD, which resulted in : (i) an improvement of Ch $ 164 . 8 Bn . in fair value adjustment of cash flows hedge accounting derivatives, and (ii) a decrease of Ch $ 113 . 9 Bn . in marking - to - market of available - for - sale securities . 509 +172 Based on the above, in the 3Q21 we remained the local bank with the 542 +218 soundest capital structure, as denoted by CET1 and BIS ratios that advanced 85 bp. YoY and 132 bp., reaching 12.4% and 16.3%, 550 +213 respectively. Our BIS III ratios continued to be close to these figures. Comprehensive Income (CI) Our CI increased by approximately Ch$218.2 Bn. YoY from Ch$323.3 Bn. as of Sep20 to Ch$541.5 Bn. as of Sep21. The increase is primarily 213 +958 related to: (i) higher net income explaining Ch$172.3 Bn. of the total change due the effect of Covid19 on business activity last year, and (ii) 107 +885 the positive net joint effect of local interest rate increases on available for sale and hedge accounting positions amounting to ~Ch $ 99 . 7 Bn . As reported in previous quarters, instead of other banking players, we continue to show consistent comprehensive results while creating value for our shareholders . This is particularly important in the context of Basel III in order to maintain adequate CET 1 buffers .

Consolidated Statement of Income (Chilean GAAP - In millions of Chilean pesos (MCh$) and US dollars (MUS$)) Quarters Year Ended 3Q20 MCh$ 2Q21 3Q21 MCh$ MCh$ 3Q21 MUS$ % Change 3Q21/3Q20 3Q21/2Q21 Sep - 20 MCh$ Sep - 21 MCh$ Sep - 21 MUS$ % Change Sep - 21/Sep - 20 Interest revenue and expense 12 I nt e rest re v en u e I nt e rest e x pe nse 360,567 (71,724) 488,563 (148,866) 539,391 (169,147) 664.6 (208.4) 49 . 6 % 13 5 .8 % 10 . 4 % 13 . 6 % 1,355,618 (392,880) 1,515,435 (470,917) 1,867.2 (580.2) 11 . 8 % 19 . 9 % Net interest income 288,843 339,697 370,244 456.2 28.2 % 9.0 % 962,738 1,044,518 1,287.0 8.5 % Fees and commissions Income from fees and commissions Expenses from fees and commissions 129,226 (25,135) 140,423 (25,512) 149,893 (31,869) 184.7 (39.3) 16 . 0 % 26 . 8 % 6.7 % 24 . 9 % 427,827 (81,757) 427,087 (85,882) 526.2 (105.8) (0. 2 ) % 5.0 % Net fees and commissions income 104,091 114,911 118,024 145.4 13.4 % 2.7 % 346,070 341,205 420.4 (1.4) % Net Financial Operating Income (4,529) 21,970 102,622 126.4 - 367.1 % 15,264 129,802 159.9 750.4 % Foreign exchange transactions, net 44,484 12,668 (54,319) (66.9) - - 109,677 (15,239) (18.8) (113.9) % Other operating income 9,437 9,372 8,392 10.3 (11.1) % (10.5) % 25,679 25,720 31.7 0.2 % Total Operating Revenues 442,326 498,618 544,963 671.5 23.2 % 9.3 % 1,459,428 1,526,006 1,880.2 4.6 % Provisions for loan losses (112,543) (76,804) (92,910) (114.5) (17.4) % 21.0 % (377,511) (223,781) (275.7) (40.7) % Operating revenues, net of provisions for loan losses 329,783 421,814 452,053 557.0 37.1 % 7.2 % 1,081,917 1,302,225 1,604.5 20.4 % Operating expenses Personnel expenses (105,486) (110,898) (111,335) (137.2) 5.5 % 0.4 % (319,493) (335,929) (413.9) 5.1 % Administrative expenses (78,561) (79,290) (78,530) (96.8) (0.0) % (1.0) % (250,481) (241,193) (297.2) (3.7) % Depreciation and amortization (18,756) (19,149) (19,235) (23.7) 2.6 % 0.4 % (54,868) (57,003) (70.2) 3.9 % Impairments (15) (2) 0 0.0 (100.0) % - (882) (3) (0.0) (99.7) % Other operating expenses (5,955) (8,027) (9,366) (11.5) 57.3 % 16.7 % (24,875) (26,178) (32.3) 5.2 % Total operating expenses (208,773) (217,366) (218,466) (269.2) 4.6 % 0.5 % (650,599) (660,306) (813.6) 1.5 % Net operating income 121,010 204,448 233,587 287.8 93.0 % 14.3 % 431,318 641,919 790.9 48.8 % Income attributable to affiliates (1,967) (1,529) (662) (0.8) (66.3) % (56.7) % (392) (2,848) (3.5) 626.5 % Income before income tax 119,043 202,919 232,925 287.0 95.7 % 14.8 % 430,926 639,071 787.4 48.3 % Income tax (30,804) (40,542) (48,689) (60.0) 58.1 % 20.1 % (94,102) (129,966) (160.1) 38.1 % Net Income for the period 88,239 162,377 184,236 227.0 108.8 % 13.5 % 336,824 509,105 627.3 51.1 % Non - Controlling interest 1 - 1 0.0 - - 1 1 0.0 0.0 % Net Income attributable to bank's owners 88,238 162,377 184,235 227.0 108.8 % 13.5 % 336,823 509,104 627.3 51.1 % FV Adjustment AFS Securities (7,259) (48,771) (68,834) (84.8) 848.3 % 41.1 % (1,397) (117,098) (144.3) 8,282.1 % FV Adjustment CF Hedge Accounting 28,044 80,834 115,948 142.9 313.5 % 43.4 % (17,075) 198,321 244.4 (1,261.5) % Other effects (5,613) (8,552) (39,885) (49.1) 610.6 % 366.4 % 4,922 (48,822) (60.2) (1,091.9) % Comprehensive Income 103,410 185,888 191,464 235.9 85.2 % 3.0 % 323,273 541,505 667.2 67.5 % These results have been prepared in accordance with Chilean GAAP on an unaudited, consolidated basis . All figures are expressed in nominal Chilean pesos (historical pesos), unless otherwise stated . All figures expressed in US dollars (except earnings per ADR) were converted using the exchange rate of Ch $ 811 . 6 per US $ 1 . 00 as of September 30 , 2021 . Earnings per ADR were calculated considering the nominal net income, the exchange rate and the number of shares outstanding at the end of each period . Banco de Chile files its consolidated financial statements, together with those of its subsidiaries, with the Financial Market Commission, on a monthly basis . In addition, Banco de Chile files its quarterly financial statements (notes included) with the SEC in form 6 K, simultaneously or previously to file this quarterly earnings report . Such documentation is equally available at Banco de Chile’s website both in Spanish and English .

Selected Financial Information (Chilean GAAP - In millions of Chilean pesos (MCh$) and US dollars (MUS$)) ASSETS S ep - 2 0 MCh$ Jun - 2 1 M C h $ S ep - 2 1 MCh$ S ep - 2 1 M U S$ % Change Sep - 21/Sep - 20 Sep - 21/Jun - 21 Cash and due from banks 2,134,787 2,407,350 3,099,335 3,818.8 45.2 % 28.7 % Transactions in the course of collection 490,166 616,932 410,644 506.0 (16.2) % (33.4) % Financial Assets held - for - trading 4,021,785 3,537,495 3,141,762 3,871.1 (21.9) % (11.2) % Receivables from repurchase agreements and security borrowings 57,572 92,797 76,496 94.3 32.9 % (17.6) % Derivate instruments 2,985,428 1,738,135 2,844,672 3,505.0 (4.7) % 63.7 % Loans and advances to Banks 2,410,953 3,446,995 2,017,505 2,485.8 (16.3) % (41.5) % Loans to customers, net Commercial loans 18,144,967 18,509,509 18,958,457 23,359.4 4.5 % 2.4 % Residential mortgage loans 9,221,258 9,871,740 10,097,517 12,441.5 9.5 % 2.3 % Consumer loans 3,942,083 3,883,497 4,024,884 4,959.2 2.1 % 3.6 % Loans to customers 31,308,308 32,264,746 33,080,858 40,760.1 5.7 % 2.5 % Allowances for loan losses (766,224) (687,469) (676,379) (833.4) (11.7) % (1.6) % Total loans to customers, net 30,542,084 31,577,277 32,404,479 39,926.7 6.1 % 2.6 % Financial Assets Available - for - Sale 1,266,087 2,364,328 3,440,313 4,238.9 171.7 % 45.5 % Financial Assets Held - to - maturity - 127,770 302,532 372.8 - 136.8 % Investments in other companies 48,984 43,588 48,088 59.3 (1.8) % 10.3 % Intangible assets 60,093 66,798 68,401 84.3 13.8 % 2.4 % Property and Equipment 218,147 221,296 223,688 275.6 2.5 % 1.1 % Leased assets 128,974 112,167 103,224 127.2 (20.0) % (8.0) % Current tax assets 25,028 1,515 671 0.8 (97.3) % (55.7) % Deferred tax assets 333,333 381,804 387,291 477.2 16.2 % 1.4 % Other assets 606,452 579,999 649,322 800.1 7.1 % 12.0 % Total Assets 45,329,873 47,316,246 49,218,423 60,643.7 8.6 % 4.0 % LIABILITIES & EQUITY S ep - 2 0 Jun - 2 1 S ep - 2 1 S ep - 2 1 M C h $ M C h $ M C h $ M U S$ % Change Sep - 21/Sep - 20 Sep - 21/Jun - 21 Liabilities Current accounts and other demand deposits Transactions in the course of payment Payables from repurchase agreements and security lending Saving accounts and time deposits Derivate instruments Borrowings from financial institutions Debt issued Other financial obligations Lease liabilities Current tax liabilities Deferred tax liabilities Provisions Other liabilities 14,518,325 17,408,414 17,607,258 21,694.5 1,010,028 710,418 337,560 415.9 284,917 150,185 111,438 137.3 8,854,870 7,869,674 8,972,204 11,055.0 3,120,577 1,782,856 2,644,144 3,257.9 3,869,391 4,968,562 4,814,758 5,932.4 8,709,673 8,771,310 8,758,172 10,791.2 100,395 218,703 259,116 319.3 125,223 108,185 99,013 122.0 456 24,218 82,930 102.2 0 - - - 590,953 730,243 882,161 1,086.9 513,597 639,961 608,030 749.2 21 . 3 % 1 . 1 % ( 66 . 6 ) % ( 52 . 5 ) % ( 60 . 9 ) % ( 25 . 8 ) % 1 . 3 % 14 . 0 % ( 15 . 3 ) % 48 . 3 % 24 . 4 % ( 3 . 1 ) % 0 . 6 % ( 0 . 1 ) % 158 . 1 % 18 . 5 % ( 20 . 9 ) % ( 8 . 5 ) % 18 , 086 . 4 % 242 . 4 % - - 49 . 3 % 20 . 8 % 18 . 4 % ( 5 . 0 ) % Total liabilities 41,698,405 43,382,729 45,176,784 55,663.9 8.3 % 4.1 % Equity of the Bank's owners Capital R ese r ve s Other comprehensive income Retained earnings from previous periods Income for the period Provisions for minimum dividends Non - Controlling Interest 2,418,833 2,418,833 2,418,833 2,980.3 703,206 703,476 703,571 866.9 (70,085) (26,348) (19,214) (23.7) 412,641 655,478 655,478 807.6 336,823 324,869 509,104 627.3 (169,951) (142,792) (226,135) (278.6) 1 1 2 - 0 . 0 % 0 . 0 % 0 . 1 % 0 . 0 % ( 72 . 6 ) % ( 27 . 1 ) % 58 . 8 % 0 . 0 % 51 . 1 % 56 . 7 % 33 . 1 % 58 . 4 % 100 . 0 % 100 . 0 % Total equity 3,631,468 3,933,517 4,041,639 4,979.8 11.3 % 2.7 % Total Liabilities & Equity 45,329,873 47,316,246 49,218,423 60,643.7 8.6 % 4.0 % These results have been prepared in accordance with Chilean GAAP on an unaudited, consolidated basis . All figures are expressed in nominal Chilean pesos (historical pesos), unless otherwise stated . All figures expressed in US dollars (except earnings per ADR) were converted using the exchange rate of Ch $ 811 . 6 per US $ 1 . 00 as of September 30 , 2021 . Earnings per ADR were calculated considering the nominal net income, the exchange rate and the number of shares outstanding at the end of each period . Banco de Chile files its consolidated financial statements, together with those of its subsidiaries, with the Financial Market Commission, on a monthly basis . In addition, Banco de Chile files its quarterly financial statements (notes included) with the SEC in form 6 K, simultaneously or previously to file this quarterly earnings report . Such documentation is equally available at Banco de Chile’s website both in Spanish and English . 13

Selected Financial Information (Chilean GAAP - In millions of Chilean pesos (MCh$) and US dollars (MUS$)) Key Performance Ratios 3Q20 Quarter 2Q21 3Q21 Sep - 20 Y ea r E nde d Jun - 21 Sep - 21 Earnings per Share (1) (2) Net income per Share (Ch$) 0.87 1.61 1.82 3.33 3.22 5.04 Net income per ADS (Ch$) 174.70 321.48 364.76 666.86 643.20 1,007.96 Net income per ADS (US$) 0.22 0.44 0.45 0.85 0.88 1.24 Book value per Share (Ch$) 35.95 38.94 40.01 35.95 38.94 40.01 Shares outstanding (Millions) 101,017 101,017 101,017 101,017 101,017 101,017 Profitability Ratios (3)(4) Net Interest Margin 3.08% 3.39% 3.61% 3.56% 3.41% 3.48% Net Financial Margin 3.48% 3.71% 3.97% 3.96% 3.72% 3.81% Fees & Comm. / Avg. Interest Earnings Assets 1.10% 1.14% 1.12% 1.26% 1.12% 1.12% Operating Revs. / Avg. Interest Earnings Assets 4.68% 4.94% 5.17% 5.31% 4.93% 5.01% Return on Average Total Assets 0.79% 1.41% 1.53% 1.01% 1.43% 1.46% Return on Average Equity 9.79% 16.76% 18.57% 12.50% 17.00% 17.54% Capital Ratios Equity / Total Assets 8.01% 8.31% 8.21% 8.01% 8.31% 8.21% T i e r I ( B as i c C ap it a l ) / T o t a l A sse t s 7.56% 7.72% 7.71% 7.56% 7.72% 7.71% T i e r I ( B as i c C ap it a l ) / R i sk - W e i gh t e d A sse t s 11.59% 12.51% 12.44% 11.59% 12.51% 12.44% Total Capital / Risk - Weighted Assets 14.98% 16.42% 16.30% 14.98% 16.42% 16.30% Credit Quality Ratios Total Past Due / Total Loans to Customers 0.98% 1.04% 0.92% 0.98% 1.04% 0.92% Allowance for Loan Losses / Total Past Due (5) 329.70% 325.74% 372.56% 329.70% 325.74% 372.56% Impaired Loans / Total Loans to Customers 4.11% 3.23% 3.00% 4.11% 3.23% 3.00% Loan Loss Allowances / Impaired Loans 59.52% 65.91% 68.18% 59.52% 65.91% 68.18% Loan Loss Allowances / Total Loans to Customers 2.45% 2.13% 2.04% 2.45% 2.13% 2.04% Loan Loss Provisions / Avg. Loans to Customers (4) 1.46% 0.96% 1.14% 1.65% 0.83% 0.93% Operating and Productivity Ratios Operating Expenses / Operating Revenues 47.20% 43.59% 40.09% 44.58% 45.04% 43.27% O pe r a ti n g E xpense s / A ve r ag e T o t a l A sse t s ( 3 ) ( 4 ) 1.86% 1.88% 1.81% 1.95% 1.94% 1.90% Balance Sheet Data (1)(3) Avg. Interest Earnings Assets (million Ch$) 37,831,844 40,360,140 42,184,569 36,667,800 39,799,005 40,594,193 Avg. Assets (million Ch$) 44,793,380 46,138,598 48,266,736 44,395,250 45,539,598 46,448,644 Avg. Equity (million Ch$) 3,604,924 3,875,844 3,968,616 3,592,463 3,821,703 3,870,674 Avg. Loans to Customers (million Ch$) 30,911,720 31,976,113 32,663,446 30,555,285 31,618,251 31,966,649 Avg. Interest Bearing Liabilities (million Ch$) 22,276,803 21,639,857 22,279,263 22,678,963 21,414,832 21,702,975 Risk - Weighted Assets (Million Ch$) 31,340,664 31,440,210 32,491,090 31,340,664 31,440,210 32,491,090 Additional Data Exchange rate (Ch$/US$) 784.31 734.00 811.60 784.31 734.00 811.60 Employees (#) 13,325 12,404 12,395 13,325 12,404 12,395 Branches (#) 335 277 272 335 277 272 Notes (1) Figures are expressed in nominal Chilean pesos. (2) Figures are calculated considering nominal net income, the shares outstanding and the exchange rate existing at the end of each period. (3) Ratios consider daily average balances. (4) Annualized data. (5) Including additional allowances. 14 These results have been prepared in accordance with Chilean GAAP on an unaudited, consolidated basis . All figures are expressed in nominal Chilean pesos (historical pesos), unless otherwise stated . All figures expressed in US dollars (except earnings per ADR) were converted using the exchange rate of Ch $ 811 . 6 per US $ 1 . 00 as of September 30 , 2021 . Earnings per ADR were calculated considering the nominal net income, the exchange rate and the number of shares outstanding at the end of each period . Banco de Chile files its consolidated financial statements, together with those of its subsidiaries, with the Financial Market Commission, on a monthly basis . In addition, Banco de Chile files its quarterly financial statements (notes included) with the SEC in form 6 K, simultaneously or previously to file this quarterly earnings report . Such documentation is equally available at Banco de Chile’s website both in Spanish and English .

Summary of differences between Chile GAAP and IFRS The most significant differences are as follows : Under Chilean GAAP, the merger of Banco de Chile and Citibank Chile was accounted for under the pooling - of - interest method, while under IFRS, and for external financial reporting purposes, the merger of the two banks was accounted for as a business combination in which the Bank is the acquirer as required by IFRS 3 “Business Combinations” . Under IFRS 3 , the Bank recognised all acquired net assets at fair value as determined at the acquisition date, as well as the goodwill resulting from the purchase price consideration in excess of net assets recognised . Allowances for loan losses are calculated based on specific guidelines set by the Financial Market Commission based on an expected losses approach . Under IFRS 9 “Financial instruments” allowances for loan losses should be calculated on a discounted basis u nder the “expected credit loss” model that focuses on the risk that an asset will default rather than whether a loss has actually been incurred or not . Assets received in lieu of payments are measured at historical cost or fair value, less cost to sell, if lower, on a portfolio basis and written - off if not sold after a certain period in accordance with specific guidelines set by the Financial Market Commission . Under IFRS, these assets are deemed non - current assets held - for - sale and their accounting treatment is set by IFRS 5 “Non - current assets held for sale and Discontinued operations” . In accordance with IFRS 5 these assets are measured at historical cost or fair value, less cost to sell, if lower . Accordingly, under IFRS these assets are not written off unless impaired . Chilean companies are required to distribute at least 30 % of their net income to shareholders unless a majority of shareholders approve the retention of profits . In accordance with Chilean GAAP, the Bank records a minimum dividend allowance based on its distribution policy, which requires distribution of at least 60 % of the period net income, as permitted by the Financial Market Commission . Under IFRS, only the portion of dividends that is required to be distributed by Chilean Law must be recorded, i . e . , 30 % as required by Chilean Corporations Law . Forward - Looking Information The information contained herein incorporates by reference statements which constitute ‘‘forward - looking statements,’’ in that they include statements regarding the intent, belief or current expectations of our directors and officers with respect to our future operating performance . Such statements include any forecasts, projections and descriptions of anticipated cost savings or other synergies . You should be aware that any such forward - looking statements are not guarantees of future performance and may involve risks and uncertainties, and that actual results may differ from those set forth in the forward - looking statements as a result of various factors (including, without limitations, the actions of competitors, future global economic conditions, market conditions, foreign exchange rates, and operating and financial risks related to managing growth and integrating acquired businesses), many of which are beyond our control . The occurrence of any such factors not currently expected by us would significantly alter the results set forth in these statements . Factors that could cause actual results to differ materially and adversely include, but are not limited to : changes in general economic, business or political or other conditions in Chile or changes in general economic or business conditions in Latin America; changes in capital markets in general that may affect policies or attitudes toward lending to Chile or Chilean companies; unexpected developments in certain existing litigation; increased costs; unanticipated increases in financing and other costs or the inability to obtain additional debt or equity financing on attractive terms. Undue reliance should not be placed on such statements, which speak only as of the date that they were made . Our independent public accountants have not examined or compiled the forward - looking statements and, accordingly, do not provide any assurance with respect to such statements . These cautionary statements should be considered in connection with any written or oral forward - looking statements that we may issue in the future . We do not undertake any obligation to release publicly any revisions to such forward - looking statements to reflect later events or circumstances or to reflect the occurrence of unanticipated events . Contacts Pablo Mejia Head of Investor Relations Investor Relations | Banco de Chile pmejiar@bancochile.c l Daniel Galarce Head of Financial Control & Capital Financial Control & Capital Area | Banco de Chile dgalarce@bancochile.cl