0001161154eto:DerivativesNotDesignatedAsHedgingInstrumentsInterestRateDerivativesMembereto:July2021Membereto:ForwardStartingSwapsMember2020-01-012020-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2020

or

| | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number 1-31219

ENERGY TRANSFER OPERATING, L.P.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Delaware | | 73-1493906 |

| (state or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

8111 Westchester Drive, Suite 600, Dallas, Texas 75225

(Address of principal executive offices) (zip code)

Registrant’s telephone number, including area code: (214) 981-0700

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| 7.375% Series C Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Units | | ETPprC | | New York Stock Exchange |

| 7.625% Series D Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Units | | ETPprD | | New York Stock Exchange |

| 7.600% Series E Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Units | | ETPprE | | New York Stock Exchange |

| | | | |

| | | | |

| | | | |

| | | | |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ý No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes ý No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer ý Smaller reporting company ☐ Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on an attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes ☐ No ý

DOCUMENTS INCORPORATED BY REFERENCE

None

TABLE OF CONTENTS

| | | | | | | | |

| | PAGE |

|

| | |

| ITEM 1. | | |

| | |

| ITEM 1A. | | |

| | |

| ITEM 1B. | | |

| | |

| ITEM 2. | | |

| | |

| ITEM 3. | | |

| | |

| ITEM 4. | | |

| | |

|

| | |

| ITEM 5. | | |

| | |

| ITEM 6. | | |

| | |

| ITEM 7. | | |

| | |

| ITEM 7A. | | |

| | |

| ITEM 8. | | |

| | |

| ITEM 9. | | |

| | |

| ITEM 9A. | | |

| | |

| ITEM 9B. | | |

| | |

|

| | |

| ITEM 10. | | |

| | |

| ITEM 11. | | |

| | |

| ITEM 12. | | |

| | |

| ITEM 13. | | |

| | |

| ITEM 14. | | |

| | |

|

| | |

| ITEM 15. | | |

| | |

| ITEM 16. | | |

| | |

| | |

Definitions

The following is a list of certain acronyms and terms used throughout this document:

| | | | | | | | | | | |

| /d | | per day |

| | | |

| AOCI | | accumulated other comprehensive income (loss) |

| | | |

| AROs | | asset retirement obligations |

| | | |

| Bbls | | barrels |

| | | |

| BBtu | | billion British thermal units |

| | | |

| Bcf | | billion cubic feet |

| | | |

| Btu | | British thermal unit, an energy measurement used by gas companies to convert the volume of gas used to its heat equivalent, and thus calculate the actual energy used |

| | | |

| Capacity | | capacity of a pipeline, processing plant or storage facility refers to the maximum capacity under normal operating conditions and, with respect to pipeline transportation capacity, is subject to multiple factors (including natural gas injections and withdrawals at various delivery points along the pipeline and the utilization of compression) which may reduce the throughput capacity from specified capacity levels |

| | | |

| CDM | | CDM Resource Management LLC and CDM Environmental & Technical Services LLC, collectively |

| | | |

| Citrus | | Citrus, LLC, a 50/50 joint venture which owns FGT |

| | | |

| | | |

| | | |

| Dakota Access | | Dakota Access, LLC, a less than wholly-owned subsidiary of ETO |

| | | |

| DOE | | United States Department of Energy |

| | | |

| DOJ | | United States Department of Justice |

| | | |

| DOT | | United States Department of Transportation |

| | | |

| Energy Transfer Canada | | Energy Transfer Canada ULC (formerly SemCAMS Midstream ULC), a less than wholly-owned subsidiary of ETO |

| | | |

| EPA | | United States Environmental Protection Agency |

| | | |

| ET | | Energy Transfer LP, the parent company of ETO |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| ETC Sunoco | | ETC Sunoco Holdings LLC (formerly Sunoco Inc.), a wholly-owned subsidiary of ETO |

| | | |

| ETC Tiger | | ETC Tiger Pipeline, LLC, a wholly-owned subsidiary of ETO, which owns the Tiger Pipeline |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| ETP GP | | Energy Transfer Partners GP, L.P., the general partner of ETO |

| | | |

| ETP Holdco | | ETP Holdco Corporation, a wholly-owned subsidiary of ETO |

| | | |

| ETP LLC | | Energy Transfer Partners, L.L.C., the general partner of ETP GP |

| | | |

| Exchange Act | | Securities Exchange Act of 1934 |

| | | |

| ExxonMobil | | Exxon Mobil Corporation |

| | | |

| FEP | | Fayetteville Express Pipeline LLC |

| | | |

| FERC | | Federal Energy Regulatory Commission |

| | | |

| FGT | | Florida Gas Transmission Pipeline and/or Florida Gas Transmission Company, LLC, a wholly-owned subsidiary of Citrus |

| | | |

| GAAP | | accounting principles generally accepted in the United States of America |

| | | |

| | | |

| | | |

| HFOTCO | | Houston Fuel Oil Terminal Company, a wholly-owned subsidiary of ETO, which owns the Houston Terminal |

| | | |

| | | |

| | | |

| IDRs | | incentive distribution rights |

| | | |

| KMI | | Kinder Morgan Inc. |

| | | |

| | | | | | | | | | | |

| Lake Charles LNG | | Lake Charles LNG Company, LLC, a wholly-owned subsidiary of ETO |

| | | |

| LCL | | Lake Charles LNG Export Company, LLC, a wholly-owned subsidiary of ETO |

| | | |

| | | |

| | | |

| LIBOR | | London Interbank Offered Rate |

| | | |

| LNG | | liquefied natural gas |

| | | |

| Lone Star | | Lone Star NGL LLC, a wholly-owned subsidiary of ETO |

| | | |

| | | |

| | | |

| MBbls | | thousand barrels |

| | | |

| MEP | | Midcontinent Express Pipeline LLC |

| | | |

| | | |

| | | |

| Mid-Valley | | Mid-Valley Pipeline Company, a wholly-owned subsidiary of ETO |

| | | |

| MMBbls | | million barrels |

| | | |

| MMcf | | million cubic feet |

| | | |

| MTBE | | methyl tertiary butyl ether |

| | | |

| NGL | | natural gas liquid, such as propane, butane and natural gasoline |

| | | |

| NYMEX | | New York Mercantile Exchange |

| | | |

| NYSE | | New York Stock Exchange |

| | | |

| ORS | | Ohio River System LLC, a less than wholly-owned subsidiary of ETO |

| | | |

| OSHA | | federal Occupational Safety and Health Act |

| | | |

| OTC | | over-the-counter |

| | | |

| Panhandle | | Panhandle Eastern Pipe Line Company, LP, a wholly-owned subsidiary of ETO |

| | | |

| PCBs | | polychlorinated biphenyls |

| | | |

| | | |

| | | |

| PEP | | Permian Express Partners LLC, a less than wholly-owned subsidiary of ETO |

| | | |

| PES | | Philadelphia Energy Solutions Refining and Marketing LLC |

| | | |

| Phillips 66 | | Phillips 66 Partners LP |

| | | |

| PHMSA | | Pipeline Hazardous Materials Safety Administration |

| | | |

| Preferred Unitholders | | Unitholders of the Series A Preferred Units, Series B Preferred Units, Series C Preferred Units, Series D Preferred Units, Series E Preferred Units, Series F Preferred Units and Series G Preferred Units, collectively |

| | | |

| | | |

| | | |

| Regency | | Regency Energy Partners LP, a wholly-owned subsidiary of ETO |

| | | |

| | | |

| | | |

| | | |

| | | |

| RIGS | | Regency Intrastate Gas System, a wholly-owned subsidiary of ETO |

| | | |

| Rover | | Rover Pipeline LLC, a less than wholly-owned subsidiary of ETO |

| | | |

| Sea Robin | | Sea Robin Pipeline Company, LLC, a wholly-owned subsidiary of Panhandle |

| | | |

| SEC | | Securities and Exchange Commission |

| | | |

| SemGroup | | SemGroup, LLC (formerly SemGroup Corporation) |

| | | |

| Series A Preferred Units | | 6.250% Series A Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Units |

| | | |

| Series B Preferred Units | | 6.625% Series B Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Units |

| | | |

| Series C Preferred Units | | 7.375% Series C Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Units |

| | | |

| Series D Preferred Units | | 7.625% Series D Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Units |

| | | |

| | | | | | | | | | | |

| Series E Preferred Units | | 7.600% Series E Fixed-to-Floating Rate Cumulative Redeemable Perpetual Preferred Units |

| | | |

| Series F Preferred Units | | 6.750% Series F Fixed-Rate Reset Cumulative Redeemable Perpetual Preferred Units |

| | | |

| Series G Preferred Units | | 7.125% Series G Fixed-Rate Reset Cumulative Redeemable Perpetual Preferred Units |

| | | |

| Shell | | Royal Dutch Shell plc |

| | | |

| Southwest Gas | | Pan Gas Storage, LLC (d.b.a. Southwest Gas Storage Company) |

| | | |

| SPLP | | Sunoco Pipeline L.P., a wholly-owned subsidiary of ETO |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Sunoco Logistics Operations | | Sunoco Logistics Partners Operations L.P, a wholly-owned subsidiary of ETO |

| | | |

| Sunoco (R&M) | | Sunoco (R&M), LLC |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| | | |

| Transwestern | | Transwestern Pipeline Company, LLC, a wholly-owned subsidiary of ETO |

| | | |

| TRRC | | Texas Railroad Commission |

| | | |

| Trunkline | | Trunkline Gas Company, LLC, a wholly-owned subsidiary of Panhandle |

| | | |

| Unitholders | | Preferred Unitholders and our common unitholder (Energy Transfer LP), collectively |

| | | |

| USAC | | USA Compression Partners, LP, a subsidiary of ETO |

| USACE | | United States Army Corps of Engineers |

| | | |

| White Cliffs | | White Cliffs Pipeline, L.L.C. |

Adjusted EBITDA is a term used throughout this document, which we define as total Partnership earnings before interest, taxes, depreciation, depletion, amortization and other non-cash items, such as non-cash compensation expense, gains and losses on disposals of assets, the allowance for equity funds used during construction, unrealized gains and losses on commodity risk management activities, inventory valuation adjustments, non-cash impairment charges, losses on extinguishments of debt and other non-operating income or expense items. Adjusted EBITDA reflect amounts for unconsolidated affiliates based on the same recognition and measurement methods used to record equity in earnings of unconsolidated affiliates. Adjusted EBITDA related to unconsolidated affiliates excludes the same items with respect to the unconsolidated affiliate as those excluded from the calculation of Segment Adjusted EBITDA and consolidated Adjusted EBITDA, such as interest, taxes, depreciation, depletion, amortization and other non-cash items. Although these amounts are excluded from Adjusted EBITDA related to unconsolidated affiliates, such exclusion should not be understood to imply that we have control over the operations and resulting revenues and expenses of such affiliates. We do not control our unconsolidated affiliates; therefore, we do not control the earnings or cash flows of such affiliates. The use of Segment Adjusted EBITDA or Adjusted EBITDA related to unconsolidated affiliates as an analytical tool should be limited accordingly.

Forward-Looking Statements

Certain matters discussed in this report, excluding historical information, as well as some statements by Energy Transfer Operating, L.P. (the “Partnership,” or “ETO”) in periodic press releases and some oral statements of the Partnership’s officials during presentations about the Partnership, include forward-looking statements. These forward-looking statements are identified as any statement that does not relate strictly to historical or current facts. Statements using words such as “anticipate,” “believe,” “intend,” “project,” “plan,” “expect,” “continue,” “estimate,” “goal,” “forecast,” “may,” “will” or similar expressions help identify forward-looking statements. Although the Partnership and its General Partner believe such forward-looking statements are based on reasonable assumptions and current expectations and projections about future events, no assurance can be given that such assumptions, expectations, or projections will prove to be correct. Forward-looking statements are subject to a variety of risks, uncertainties and assumptions. If one or more of these risks or uncertainties materialize, or if underlying assumptions prove incorrect, the Partnership’s actual results may vary materially from those anticipated, projected or expected, forecasted, estimated or expressed in forward-looking statements since many of the factors that determine these results are subject to uncertainties and risks that are difficult to predict and beyond management’s control. For additional discussion of risks, uncertainties and assumptions, see the risk factor summary below and “Item 1A. Risk Factors” included in this annual report and summarized below.

Risk Factor Summary

Summary of Risks Related to the Partnership’s Business

Results of Operations and Financial Condition. Our results of operations and financial condition could be impacted by many risks that are beyond our control, including the following:

•fluctuations in the demand for and price of natural gas, NGLs, crude oil and refined products;

•the outbreak of COVID-19 and recent geopolitical developments in the crude oil market;

•an impairment of goodwill and intangible assets;

•an interruption of supply of crude oil to our facilities;

•the loss of any key producers or customers;

•failure to retain or replace existing customers or volumes due to declining demand or increased competition;

•unfavorable changes in natural gas price spreads between two or more physical locations;

•production declines over time, which we may not be able to replace with production from newly drilled wells;

•our customers’ ability to use our pipelines and third-party pipelines over which we have no control;

•the inability to access or continue to access lands owned by third parties;

•the overall forward market for crude oil and other products we store;

•a natural disaster, catastrophe, terrorist attack or other similar event;

•union disputes and strikes or work stoppages by unionized employees;

•cybersecurity breaches and other disruptions or failures of our information systems;

•failure to establish or maintain adequate corporate governance;

•product liability claims and litigation;

•actions taken by certain of our joint ventures that we do not control;

•increasing levels of congestion in the Houston Ship Channel;

•the costs of providing pension and other postretirement health care benefits and related funding requirements;

•mergers among customers and competitors;

•fraudulent activity or misuse of proprietary data involving our outsourcing partners; and

•failure of the liquefaction project to secure long-term contractual arrangements or necessary approvals.

Indebtedness. Our business, results of operations, cash flows and financial condition, as well as our ability to make distributions, could be impacted by the following:

•our debt level and debt agreements, or increases in interest rates;

•changes in LIBOR reporting practices or the method in which LIBOR is determined;

•the credit and risk profile of our general partner and its owners;

•a downgrade of our credit ratings; and

•losses resulting from the use of derivative financial instruments.

Capital Projects and Future Growth. Our business, results of operations, cash flows, financial condition, and future growth could be impacted by the following:

•failure to make acquisitions on economically acceptable terms, or to successfully integrate acquired assets;

•failure to secure debt and equity financing for capital projects on acceptable terms;

•failure to construct new pipelines or to do so efficiently;

•failure to execute our growth strategy due to increased competition within any of our core businesses; and

•failure to attract and retain qualified employees.

Regulatory Matters. Our business, results of operations, cash flows, financial condition, and future growth could be impacted by the following:

•increased regulation of hydraulic fracturing or produced water disposal;

•legal or regulatory actions related to the Dakota Access Pipeline;

•competition for water resources or limitations on water usage for hydraulic fracturing;

•laws, regulations and policies governing the rates, terms and conditions of our services;

•failure to recover the full amount of increases in the costs of our pipeline operations;

•imposition of regulation on assets not previously subject to regulation;

•costs and liabilities resulting from performance of pipeline integrity programs and related repairs;

•new or more stringent pipeline safety controls or enforcement of legal requirements;

•costs and liabilities associated with environmental and worker health and safety laws and regulations;

•climate change legislation or regulations restricting emissions of greenhouse gases;

•regulatory provisions of the Dodd-Frank Act and the rules adopted thereunder;

•deepwater drilling laws and regulations, delays in the processing and approval of drilling permits and exploration, development, oil spill-response and decommissioning plans, and related developments; and

•laws and regulations governing the specifications of products that we store and transport.

Risks Relating to Our Partnership Structure

Cash Distributions to Unitholders. Our cash distributions could be impacted by the following:

•cash distributions are not guaranteed and may fluctuate with our performance and other external factors;

•limitations on available cash that are imposed by our distribution policy;

•our general partner’s absolute discretion in determining the level of cash reserves; and

•unitholders’ potential liability to repay distributions.

Our General Partner. Our stakeholders could be impacted by risks related to our general partner, including:

•transfer of control of our general partner to a third party without unitholder consent; and

•substantial cost reimbursements due to our general partner.

Our Subsidiaries. Risks that are unique to our subsidiaries and/or our relationship to our subsidiaries could reduce our subsidiaries’ cash available for distributions to us, including:

•the potential issuance of additional common units by Sunoco LP or USAC;

•a significant decrease in demand for or the price of motor fuel in the areas Sunoco LP serves;

•seasonal industry trends, which may cause Sunoco LP’s operating costs to fluctuate;

•disruptions in Sunoco LP’s operations due to dangers inherent in motor fuel transportation;

•adverse publicity for Sunoco LP resulting from negative events or developments;

•increased costs to retain necessary land use, which could disrupt Sunoco LP’s operations; and

•federal, state and local laws and regulations that govern the industries in which our subsidiaries operate.

Risks Related to Conflicts of Interest. Our stakeholders could be impacted by conflicts of interest, including:

•our general partner may favor its own interests to the detriment of our Unitholders;

•fiduciary duties owed to Sunoco LP, USAC and their respective unitholders by their general partners; and

•potential conflicts of interest faced by directors and officers in managing our business.

Tax Risks. Our stakeholders could be impacted by tax risks, including:

•our tax treatment depends on our status as a partnership for federal income tax purposes, and not being subject to a material amount of entity-level taxation;

•our cash available for distribution to Unitholders may be substantially reduced if we become subject to entity-level taxation as a result of the Internal Revenue Service (“IRS”) treating us as a corporation or legislative, judicial or administrative changes, and may also be reduced by any audit adjustments if imposed directly on the partnership;

•even if Unitholders do not receive any cash distributions from us, Unitholders will be required to pay taxes on their share of our taxable income;

•a Unitholder’s share of our taxable income may be increased as a result of the IRS successfully contesting any of the federal income tax positions we take; and

•tax-exempt entities and non-U.S. Unitholders face unique tax issues from owning our common units that may result in adverse tax consequences to them.

PART I

ITEM 1. BUSINESS

Overview

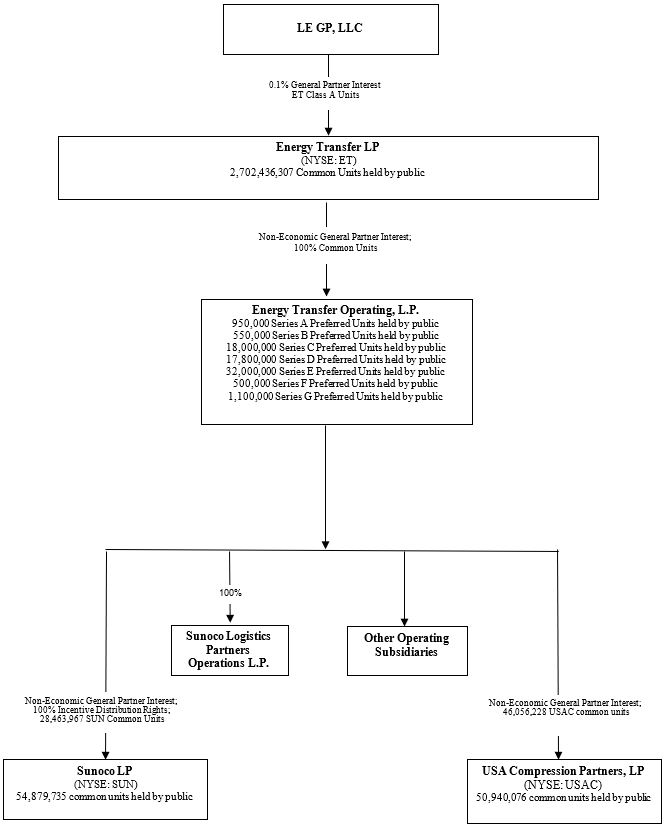

We (Energy Transfer Operating, L.P., a Delaware limited partnership, “ETO” or the “Partnership”) are a consolidated subsidiary of Energy Transfer LP (“ET”). In October 2018, ET completed the merger of ETO with a wholly-owned subsidiary of ET in a unit-for-unit exchange (the “Energy Transfer Merger”), as discussed further below, at which time the Partnership changed its name from Energy Transfer Partners, L.P. to Energy Transfer Operating, L.P.

We are managed by our general partner, Energy Transfer Partners GP, L.P. (our “General Partner” or “ETP GP”), and ETP GP is managed by its general partner, Energy Transfer Partners, L.L.C. (“ETP LLC”), which is wholly owned by ET. The primary activities in which we are engaged, all of which are in the United States and Canada, are as follows:

•natural gas operations, including the following:

•natural gas midstream and intrastate transportation and storage;

•interstate natural gas transportation and storage; and

•crude oil, NGL and refined products transportation, terminalling services and acquisition and marketing activities, as well as NGL storage and fractionation services.

In addition, we own investments in other businesses, including Sunoco LP and USAC, both of which are publicly traded master limited partnerships.

The following chart summarizes our organizational structure as of February 12, 2021. For simplicity, certain immaterial entities and ownership interests have not been depicted.

Unless the context requires otherwise, the Partnership and its subsidiaries are collectively referred to in this report as “we,” “us,” “ETO,” “Energy Transfer” or “the Partnership.”

Significant Achievements in 2020 and Beyond

•During the third quarter of 2020, the Partnership completed its Lone Star Express expansion under budget and ahead of schedule.

•During this first quarter of 2020, we completed the integration of the recently acquired SemGroup business and we began to realize financial savings from those actions.

•During the fourth quarter of 2020, the Partnership completed construction of the Orbit Gulf Coast export terminal at Nederland and in January of 2021 loaded the first Very Large Ethane Carrier (“VLEC”) with 911,000 barrels of ethane destined for the northeastern Jiangsu Province, China.

Segment Overview

See Note 16 to our consolidated financial statements in “Item 8. Financial Statements and Supplementary Data” for additional financial information about our segments.

Intrastate Transportation and Storage Segment

Natural gas transportation pipelines receive natural gas from other mainline transportation pipelines, storage facilities and gathering systems and deliver the natural gas to industrial end-users, storage facilities, utilities, power generators and other third-party pipelines. Through our intrastate transportation and storage segment, we own and operate (through wholly-owned subsidiaries or through joint venture interests) approximately 9,400 miles of natural gas transportation pipelines with approximately 22 Bcf/d of transportation capacity and three natural gas storage facilities located in the state of Texas.

Energy Transfer operates one of the largest intrastate pipeline systems in the United States providing energy logistics to major trading hubs and industrial consumption areas throughout the United States. Our intrastate transportation and storage segment focuses on the transportation of natural gas to major markets from various prolific natural gas producing areas (Permian, Barnett, Haynesville and Eagle Ford Shale) through our Oasis pipeline, our ETC Katy pipeline, our natural gas pipeline and storage systems that are referred to as the ET Fuel System, and our HPL System, as further described below.

Our intrastate transportation and storage segment’s results are determined primarily by the amount of capacity our customers reserve as well as the actual volume of natural gas that flows through the transportation pipelines. Under transportation contracts, our customers are charged (i) a demand fee, which is a fixed fee for the reservation of an agreed amount of capacity on the transportation pipeline for a specified period of time and which obligates the customer to pay a fee even if the customer does not transport natural gas on the respective pipeline, (ii) a transportation fee, which is based on the actual throughput of natural gas by the customer, (iii) fuel retention based on a percentage of gas transported on the pipeline, or (iv) a combination of the three, generally payable monthly.

We also generate revenues and margin from the sale of natural gas to electric utilities, independent power plants, local distribution companies, industrial end-users and marketing companies on our HPL System. Generally, we purchase natural gas from either the market (including purchases from our marketing operations) or from producers at the wellhead. To the extent the natural gas comes from producers, it is primarily purchased at a discount to a specified market price and typically resold to customers based on an index price. In addition, our intrastate transportation and storage segment generates revenues from fees charged for storing customers’ working natural gas in our storage facilities and from managing natural gas for our own account.

Interstate Transportation and Storage Segment

Natural gas transportation pipelines receive natural gas from supply sources including other transportation pipelines, storage facilities and gathering systems and deliver the natural gas to industrial end-users and other pipelines. Through our interstate transportation and storage segment, we directly own and operate approximately 12,340 miles of interstate natural gas pipelines with approximately 10.7 Bcf/d of transportation capacity and another approximately 6,780 miles and 10.7 Bcf/d of transportation capacity through joint venture interests.

ETO’s vast interstate natural gas network spans the United States from Florida to California and Texas to Michigan, offering a comprehensive array of pipeline and storage services. Our pipelines have the capability to transport natural gas from nearly all Lower 48 onshore and offshore supply basins to customers in the Southeast, Gulf Coast, Southwest, Midwest, Northeast and Canada. Through numerous interconnections with other pipelines, our interstate systems can access virtually any supply or market in the country. As discussed further herein, our interstate segment operations are regulated by the FERC, which has broad regulatory authority over the business and operations of interstate natural gas pipelines.

Lake Charles LNG, our wholly-owned subsidiary, owns an LNG import terminal and regasification facility located on Louisiana’s Gulf Coast near Lake Charles, Louisiana. The import terminal has approximately 9.0 Bcf of above ground storage capacity and the regasification facility has a send out capacity of 1.8 Bcf/d. Lake Charles LNG derives all of its revenue from a series of long-term contracts with a wholly-owned subsidiary of Shell.

LCL, a wholly-owned subsidiary of ETO, is currently developing a natural gas liquefaction facility for the export of LNG. The project would utilize existing dock and storage facilities owned by Lake Charles LNG located on the Lake Charles site. LCL entered into a prior development agreement with Shell in March 2019; however, Shell withdrew from the project in March 2020 due to adverse market factors affecting Shell's business following the onset of the COVID-19 pandemic. We intend to continue to develop the project, possibly in conjunction with one or more equity partners, and we plan to evaluate a variety of alternatives to advance the project, including the possibility of reducing the size of the project from three trains (16.45 million tonnes per annum of LNG capacity) to two trains (11.0 million tonnes per annum). The project as currently designed is fully permitted by federal, state and local authorities, has all necessary export licenses and benefits from the infrastructure related to the existing regasification facility at the same site, including four LNG storage tanks, two deep water docks and other assets. In light of the existing brownfield infrastructure and the advanced state of the development of the project, we plan to continue to pursue the project on a disciplined, cost effective basis, and ultimately we will determine whether to make a final investment decision to proceed with the project based on market conditions, capital expenditure considerations and our success in securing equity participation by third parties as well as long-term LNG offtake commitments on satisfactory terms.

The results from our interstate transportation and storage segment are primarily derived from the fees we earn from natural gas transportation and storage services.

Midstream Segment

The midstream industry consists of natural gas gathering, compression, treating, processing, storage, and transportation, and is generally characterized by regional competition based on the proximity of gathering systems and processing plants to natural gas producing wells and the proximity of storage facilities to production areas and end-use markets. Gathering systems generally consist of a network of small diameter pipelines and, if necessary, compression systems, that collect natural gas from points near producing wells and transports it to larger pipelines for further transportation.

Treating plants remove carbon dioxide and hydrogen sulfide from natural gas that is higher in carbon dioxide, hydrogen sulfide or certain other contaminants, to ensure that it meets pipeline quality specifications. Natural gas processing involves the separation of natural gas into pipeline quality natural gas, or residue gas, and a mixed NGL stream. Some natural gas produced by a well does not meet the pipeline quality specifications established by downstream pipelines or is not suitable for commercial use and must be processed to remove the mixed NGL stream. In addition, some natural gas can be processed to take advantage of favorable margins for NGLs extracted from the gas stream.

Through our midstream segment, we own and operate natural gas gathering and NGL pipelines, natural gas processing plants, natural gas treating facilities and natural gas conditioning facilities with an aggregate processing capacity of approximately 8.7 Bcf/d. Our midstream segment focuses on the gathering, compression, treating, blending, and processing, and our operations are currently concentrated in major producing basins and shales in South Texas, West Texas, New Mexico, North Texas, East Texas, West Virginia, Pennsylvania, Ohio, Oklahoma, Kansas and Louisiana. Many of our midstream assets are integrated with our intrastate transportation and storage assets.

Our midstream segment also includes a 60% interest in Edwards Lime Gathering, LLC, which operates natural gas gathering, oil pipeline and oil stabilization facilities in South Texas and a 75% membership interest in ORS, which operates a natural gas gathering system in the Utica shale in Ohio.

Our midstream segment results are derived primarily from margins we earn for natural gas volumes that are gathered, transported, purchased and sold through our pipeline systems and the natural gas and NGL volumes processed at our processing and treating facilities.

NGL and Refined Products Transportation and Services Segment

Our NGL operations transport, store and execute acquisition and marketing activities utilizing a complementary network of pipelines, storage and blending facilities, and strategic off-take locations that provide access to multiple NGL markets.

Our NGL and refined products transportation and services segment includes:

•approximately 4,823 miles of NGL pipelines;

•Nederland Terminal and connecting pipelines which provide transportation of ethane, propane, butane and natural gasoline from our Mont Belvieu Facility to our Nederland Terminal where these products can be exported;

•Marcus Hook Terminal which includes fractionation, storage and exporting assets. This facility is connected to our Mariner East pipeline system, which provides for the transportation of ethane and LPG products from western Pennsylvania, West Virginia and eastern Ohio to our Marcus Hook Terminal where these component products can be exported, processed or locally distributed;

•NGL and propane fractionation facilities with an aggregate capacity of 975 MBbls/d;

•NGL storage facility in Mont Belvieu with a working storage capacity of approximately 50 MMBbls; and

•other NGL storage assets, located at our Cedar Bayou and Hattiesburg storage facilities, and our Nederland, Marcus Hook and Inkster NGL terminals with an aggregate storage capacity of approximately 17 MMBbls.

In the first quarter of 2020, we completed and placed into operation a seventh fractionator at our Mont Belvieu facility. In addition, we placed into service the Lone Star Express pipeline in the third quarter of 2020. The NGL pipelines primarily transport NGLs from the Permian and Delaware basins and the Barnett and Eagle Ford Shales to Mont Belvieu.

NGL terminalling services are facilitated by approximately 10 MMBbls of NGL storage capacity. These operations also support our liquids blending activities, including the use of our patented butane blending technology. Refined products operations provide transportation and terminalling services through the use of approximately 2,918 miles of refined products pipelines and 37 active refined products marketing terminals. Our marketing terminals are located primarily in the northeast, midwest and southwest United States, with approximately 8 MMBbls of refined products storage capacity. Our refined products operations utilize our integrated pipeline and terminalling assets, as well as acquisition and marketing activities, to service refined products markets in several regions throughout the United States. The mix of products delivered through our refined products pipelines varies seasonally, with gasoline demand peaking during the summer months, and demand for heating oil and other distillate fuels peaking in the winter. The products transported in these pipelines include multiple grades of gasoline and middle distillates, such as heating oil, diesel and jet fuel. Rates for shipments on these product pipelines are regulated by the FERC and other state regulatory agencies, as applicable.

Revenues in this segment are principally generated from fees charged to customers under dedicated contracts or take-or-pay contracts. Under a dedicated contract, the customer agrees to deliver the total output from particular processing plants that are connected to the NGL pipeline. Take-or-pay contracts have minimum throughput commitments requiring the customer to pay regardless of whether a fixed volume is transported. Fees are market-based, negotiated with customers and competitive with regional regulated pipelines and fractionators. Storage revenues are derived from base storage and throughput fees. This segment also derives revenues from the marketing of NGLs and processing and fractionating refinery off-gas.

Crude Oil Transportation and Services Segment

Our crude oil operations provide transportation (via pipeline and trucking), terminalling and acquisition and marketing services to crude oil markets throughout the southwest, midwest, northwestern and northeastern United States. Through our crude oil transportation and services segment, we own and operate (through wholly-owned subsidiaries or joint venture interests) approximately 10,850 miles of crude oil trunk and gathering pipelines in the southwest and midwest United States. This segment includes equity ownership interests in four crude oil pipelines, the Bakken Pipeline system, Bayou Bridge Pipeline, White Cliffs Pipeline and Maurepas Pipeline. Our crude oil terminalling services operate with an aggregate storage capacity of approximately 71 MMBbls, including approximately 29 MMBbls at our Gulf Coast terminal in Nederland, Texas, approximately 18.2 MMBbls at our Gulf coast terminal on the Houston Ship Channel and approximately 7.7 MMBbls at our Cushing facility in Cushing, Oklahoma. Our crude oil acquisition and marketing activities utilize our pipeline and terminal assets, our proprietary fleet crude oil tractor trailers and truck unloading facilities, as well as third-party assets, to service crude oil markets principally in the midcontinent United States.

Revenues throughout our crude oil pipeline systems are generated from tariffs paid by shippers utilizing our transportation services. These tariffs are filed with the FERC and other state regulatory agencies, as applicable.

Our crude oil acquisition and marketing activities include the gathering, purchasing, marketing and selling of crude oil. Specifically, the crude oil acquisition and marketing activities include:

•purchasing crude oil at both the wellhead from producers, and in bulk from aggregators at major pipeline interconnections and trading locations;

•storing inventory during contango market conditions (when the price of crude oil for future delivery is higher than current prices);

•buying and selling crude oil of different grades at different locations in order to maximize value;

•transporting crude oil using the pipelines, terminals and trucks or, when necessary or cost effective, pipelines, terminals or trucks owned and operated by third parties; and

•marketing crude oil to major integrated oil companies, independent refiners and resellers through various types of sale and exchange transactions.

Investment in Sunoco LP

Sunoco LP is engaged in the distribution of motor fuels to independent dealers, distributors, and other commercial customers and the distribution of motor fuels to end-user customers at retail sites operated by commission agents. Additionally, it receives rental income through the leasing or subleasing of real estate used in the retail distribution of motor fuel. Sunoco LP also operates 78 retail stores located in Hawaii and New Jersey.

Sunoco LP is a distributor of motor fuels and other petroleum products which Sunoco LP supplies to third-party dealers and distributors, to independent operators of commission agent locations and other commercial consumers of motor fuel. Also included in the wholesale operations are transmix processing plants and refined products terminals. Transmix is the mixture of various refined products (primarily gasoline and diesel) created in the supply chain (primarily in pipelines and terminals) when various products interface with each other. Transmix processing plants separate this mixture and return it to salable products of gasoline and diesel.

Sunoco LP is the exclusive wholesale supplier of the Sunoco-branded motor fuel, supplying an extensive distribution network of approximately 5,556 Sunoco-branded company and third-party operated locations throughout the East Coast, Midwest, South Central and Southeast regions of the United States. Sunoco LP believes it is one of the largest independent motor fuel distributors of Chevron, ExxonMobil and Valero branded motor fuel in the United States. In addition to distributing motor fuels, Sunoco LP also distributes other petroleum products such as propane and lubricating oil, and Sunoco LP receives rental income from real estate that it leases or subleases.

Sunoco LP operations primarily consist of fuel distribution and marketing.

Investment in USAC

USAC provides natural gas compression services throughout the United States, including the Utica, Marcellus, Permian Basin, Delaware Basin, Eagle Ford, Mississippi Lime, Granite Wash, Woodford, Barnett, Haynesville, Niobrara and Fayetteville shales. USAC provides compression services to its customers primarily in connection with infrastructure applications, including both allowing for the processing and transportation of natural gas through the domestic pipeline system and enhancing crude oil production through artificial lift processes. As such, USAC’s compression services play a critical role in the production, processing and transportation of both natural gas and crude oil. As of December 31, 2020, USAC had 3,726,181 horsepower in its fleet.

USAC operates a modern fleet of compression units, with an average age of approximately seven years. USAC’s standard new-build compression units are generally configured for multiple compression stages allowing USAC to operate its units across a broad range of operating conditions. As part of USAC’s services, it engineers, designs, operates, services and repairs its compression units and maintains related support inventory and equipment.

USAC provides compression services to its customers under fixed-fee contracts with initial contract terms typically between six months and five years, depending on the application and location of the compression unit. USAC typically continues to provide compression services at a specific location beyond the initial contract term, either through contract renewal or on a month-to-month or longer basis. USAC primarily enters into fixed-fee contracts whereby its customers are required to pay a monthly fee even during periods of limited or disrupted throughput, which enhances the stability and predictability of its cash flows. USAC is not directly exposed to commodity price risk because it does not take title to the natural gas or crude oil involved in its services and because the natural gas used as fuel by its compression units is supplied by its customers without cost to USAC.

USAC’s assets and operations are all located and conducted in the United States.

All Other Segment

Our “All Other” segment includes the following:

•Our marketing operations in which we market the natural gas that flows through our gathering and intrastate transportation assets, referred to as on-system gas. We also attract other customers by marketing volumes of natural gas that do not move through our assets, referred to as off-system gas. For both on-system and off-system gas, we purchase natural gas from

natural gas producers and other suppliers and sell that natural gas to utilities, industrial consumers, other marketers and pipeline companies, thereby generating gross margins based upon the difference between the purchase and resale prices of natural gas, less the costs of transportation. For the off-system gas, we purchase gas or act as an agent for small independent producers that may not have marketing operations.

•Our natural gas compression equipment business which has operations in Arkansas, California, Colorado, Louisiana, New Mexico, Oklahoma, Pennsylvania and Texas.

•Our wholly-owned subsidiary, Dual Drive Technologies, Ltd. (“DDT”), which provides compression services to customers engaged in the transportation of natural gas, including our other segments.

•Our subsidiaries are involved in the management of coal and natural resources properties and the related collection of royalties. We also earn revenues from other land management activities, such as selling standing timber, leasing coal-related infrastructure facilities, and collecting oil and gas royalties. These operations also include end-user coal handling facilities.

•PEI Power LLC and PEI Power II LLC, which own and operate a facility in Pennsylvania that generates a total of 75 megawatts of electrical power.

•Our 51% ownership interest in Energy Transfer Canada, which owns and operates natural gas processing and gathering facilities in Alberta, Canada.

Asset Overview

The descriptions below include summaries of significant assets within the Partnership’s reportable segments. Amounts, such as capacities, volumes and miles included in the descriptions below are approximate and are based on information currently available; such amounts are subject to change based on future events or additional information.

Intrastate Transportation and Storage

The following details our pipelines and storage facilities in the intrastate transportation and storage segment:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Description of Assets | | Ownership Interest | | Miles of Natural Gas Pipeline | | Pipeline Throughput Capacity

(Bcf/d) | | Working Storage Capacity

(Bcf/d) |

| ET Fuel System | | 100 | % | | 3,150 | | | 5.2 | | | 11.2 | |

Oasis Pipeline (1) | | 100 | % | | 750 | | | 2.0 | | | — | |

| HPL System | | 100 | % | | 3,920 | | | 5.3 | | | 52.5 | |

| ETC Katy Pipeline | | 100 | % | | 460 | | | 2.9 | | | — | |

| Regency Intrastate Gas | | 100 | % | | 450 | | | 2.1 | | | — | |

| Comanche Trail Pipeline | | 16 | % | | 195 | | | 1.1 | | | — | |

| Trans-Pecos Pipeline | | 16 | % | | 143 | | | 1.4 | | | — | |

| Old Ocean Pipeline, LLC | | 50 | % | | 240 | | | 0.2 | | | — | |

| Red Bluff Express Pipeline | | 70 | % | | 108 | | | 1.4 | | | — | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

(1)Includes bi-directional capabilities

The following information describes our principal intrastate transportation and storage assets:

•The ET Fuel System serves some of the most prolific production areas in the United States and is comprised of intrastate natural gas pipeline and related natural gas storage facilities. The ET Fuel System has many interconnections with pipelines providing direct access to power plants, other intrastate and interstate pipelines, and has bi-directional capabilities. It is strategically located near high-growth production areas and provides access to the three major natural gas trading centers in Texas, the Waha Hub near Pecos, Texas, the Maypearl Hub in Central Texas and the Carthage Hub in East Texas.

The ET Fuel System also includes our Bethel natural gas storage facility, with a working capacity of 6.0 Bcf, an average withdrawal capacity of 300 MMcf/d and an injection capacity of 75 MMcf/d, and our Bryson natural gas storage facility, with a working capacity of 5.2 Bcf, an average withdrawal capacity of 120 MMcf/d and an average injection capacity of 96 MMcf/d. Storage capacity on the ET Fuel System is contracted to third parties under fee-based arrangements that extend through 2023.

In addition, the ET Fuel System is integrated with our Godley processing plant which gives us the ability to bypass the plant when processing margins are unfavorable by blending the untreated natural gas from the North Texas System with natural gas on the ET Fuel System while continuing to meet pipeline quality specifications.

•The Oasis Pipeline is primarily a 36-inch natural gas pipeline. It has bi-directional capabilities with approximately 1.3 Bcf/d of throughput capacity moving west-to-east and greater than 750 MMcf/d of throughput capacity moving east-to-west. The Oasis pipeline connects to the Waha and Katy market hubs and has many interconnections with other pipelines, power plants, processing facilities, municipalities and producers.

The Oasis pipeline is integrated with our gathering system known as the Southeast Texas System and is an important component to maximizing our Southeast Texas System’s profitability. The Oasis pipeline enhances the Southeast Texas System by (i) providing access for natural gas gathered on the Southeast Texas System to other third-party supply and market points and interconnecting pipelines and (ii) allowing us to bypass our processing plants and treating facilities on the Southeast Texas System when processing margins are unfavorable by blending untreated natural gas from the Southeast Texas System with gas on the Oasis pipeline while continuing to meet pipeline quality specifications.

•The HPL System is an extensive network of intrastate natural gas pipelines, an underground Bammel storage reservoir and related transportation assets. The system has access to multiple sources of historically significant natural gas supply reserves from South Texas, the Gulf Coast of Texas, East Texas and the western Gulf of Mexico, and is directly connected to major gas distribution, electric and industrial load centers in Houston, Corpus Christi, Texas City, Beaumont and other cities located along the Gulf Coast of Texas. The HPL System is well situated to gather and transport gas in many of the major gas producing areas in Texas including a strong presence in the key Houston Ship Channel and Katy Hub markets, allowing us to play an important role in the Texas natural gas markets. The HPL System also offers its shippers off-system opportunities due to its numerous interconnections with other pipeline systems, its direct access to multiple market hubs at Katy, the Houston Ship Channel, Carthage and Agua Dulce, as well as our Bammel storage facility.

The Bammel storage facility has a total working gas capacity of approximately 52.5 Bcf, a peak withdrawal rate of 1.3 Bcf/d and a peak injection rate of 0.6 Bcf/d. The Bammel storage facility is located near the Houston Ship Channel market area and the Katy Hub, and is ideally suited to provide a physical backup for on-system and off-system customers. As of December 31, 2020, we had approximately 19.0 Bcf committed under fee-based arrangements with third parties and approximately 28.7 Bcf stored in the facility for our own account.

•The ETC Katy Pipeline connects three treating facilities, one of which we own, with our gathering system known as Southeast Texas System. The ETC Katy pipeline serves producers in East and North Central Texas and provided access to the Katy Hub. The ETC Katy pipeline expansions include the 36-inch East Texas extension to connect our Reed compressor station in Freestone County to our Grimes County compressor station, the 36-inch Katy expansion connecting Grimes to the Katy Hub, and the 42-inch Southeast Bossier pipeline connecting our Cleburne to Carthage pipeline to the HPL System.

•RIGS is a 450-mile intrastate pipeline that delivers natural gas from northwest Louisiana to downstream pipelines and markets.

•Comanche Trail Pipeline is a 195-mile intrastate pipeline that delivers natural gas from the Waha Hub near Pecos, Texas to the United States/Mexico border near San Elizario, Texas. The Partnership owns a 16% membership interest in and operates Comanche Trail.

•Trans-Pecos Pipeline is a 143-mile intrastate pipeline that delivers natural gas from the Waha Hub near Pecos, Texas to the United States/Mexico border near Presidio, Texas. The Partnership owns a 16% membership interest in and operates Trans-Pecos.

•Old Ocean is a 240-mile intrastate pipeline system that delivers natural gas from Ellis County, Texas to Brazoria County, Texas. The Partnership owns a 50% membership interest in and operates Old Ocean.

•The Red Bluff Express Pipeline is an approximately 108-mile intrastate pipeline that runs through the heart of the Delaware basin and connects our Orla Plant, as well as third-party plants to the Waha Oasis Header. The Partnership owns a 70% membership interest in and operates Red Bluff Express.

Interstate Transportation and Storage

The following details our pipelines in the interstate transportation and storage segment:

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| Description of Assets | | Ownership Interest | | Miles of Natural Gas Pipeline | | Pipeline Throughput Capacity

(Bcf/d) | | Working Gas Capacity

(Bcf/d) |

| Florida Gas Transmission | | 50 | % | | 5,362 | | | 3.5 | | | — | |

| Transwestern Pipeline | | 100 | % | | 2,614 | | | 2.1 | | | — | |

Panhandle Eastern Pipe Line (1) | | 100 | % | | 6,298 | | | 2.8 | | | 73.4 | |

| Trunkline Gas Company | | 100 | % | | 2,190 | | | 0.9 | | | 13.0 | |

| Tiger Pipeline | | 100 | % | | 197 | | | 2.4 | | | — | |

| Fayetteville Express Pipeline | | 50 | % | | 185 | | | 2.0 | | | — | |

| Sea Robin Pipeline | | 100 | % | | 740 | | | 2.0 | | | — | |

| Stingray Pipeline | | 100 | % | | 287 | | | 0.4 | | | — | |

| Rover Pipeline | | 32.6 | % | | 719 | | | 3.4 | | | — | |

| Midcontinent Express Pipeline | | 50 | % | | 512 | | | 1.8 | | | — | |

| Gulf States Transmission | | 100 | % | | 10 | | | 0.1 | | | — | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

| | | | | | | | |

(1)Natural gas storage assets are owned by Southwest Gas.

The following information describes our principal interstate transportation and storage assets:

•Florida Gas Transmission Pipeline (“FGT”) has mainline capacity of 3.5 Bcf/d and approximately 5,362 miles of pipelines extending from south Texas through the Gulf Coast region of the United States to south Florida. The FGT system receives natural gas from various onshore and offshore natural gas producing basins. FGT is the principal transporter of natural gas to the Florida energy market, delivering approximately 60% of the natural gas consumed in the state. In addition, FGT’s system operates and maintains multiple interconnects with major interstate and intrastate natural gas pipelines, which provide FGT’s customers access to diverse natural gas producing regions. FGT’s customers include electric utilities, independent power producers, industrial end-users and local distribution companies. FGT is owned by Citrus, a 50/50 joint venture with KMI.

•Transwestern Pipeline transports natural gas supply from the Permian Basin in West Texas and eastern New Mexico, the San Juan Basin in northwestern New Mexico and southern Colorado, and the Anadarko Basin in the Texas and Oklahoma panhandles. The system has bi-directional capabilities and can access Texas and Midcontinent natural gas market hubs, as well as major western markets in Arizona, Nevada and California. Transwestern’s customers include local distribution companies, producers, marketers, electric power generators and industrial end-users.

•Panhandle Eastern Pipe Line’s transmission system consists of four large diameter pipelines with bi-directional capabilities, extending approximately 1,300 miles from producing areas in the Anadarko Basin of Texas, Oklahoma and Kansas through Missouri, Illinois, Indiana, Ohio and into Michigan. Panhandle contracts for over 73 Bcf of natural gas storage.

•Trunkline Gas Company’s transmission system consists of one large diameter pipeline with bi-directional capabilities, extending approximately 1,400 miles from the Gulf Coast areas of Texas and Louisiana through Arkansas, Mississippi, Tennessee, Kentucky, Illinois, Indiana and Michigan. Trunkline has one natural gas storage field located in Louisiana.

•Tiger Pipeline is a bi-directional system that extends through the heart of the Haynesville Shale and ends near Delhi, Louisiana, interconnecting with multiple interstate pipelines.

•Fayetteville Express Pipeline originates near Conway County, Arkansas and continues eastward to Panola County, Mississippi with multiple pipeline interconnections along the route. Fayetteville Express Pipeline is owned by a 50/50 joint venture with KMI.

•Sea Robin Pipeline’s system consists of two offshore Louisiana natural gas supply pipelines extending 120 miles into the Gulf of Mexico.

•Stingray Pipeline is an interstate natural gas pipeline system with related assets located in the western Gulf of Mexico and Johnson Bayou, Louisiana. Stingray has recently filed with the FERC to abandon a portion of its system to be used in non-

gas service and the remaining portion to be operated as a non-FERC-regulated gathering system. The proceeding is pending a decision from FERC.

•Rover Pipeline is a large diameter pipeline with total capacity to transport 3.4 Bcf/d natural gas from processing plants in West Virginia, Eastern Ohio and Western Pennsylvania for delivery to other pipeline interconnects in Ohio and Michigan, where the gas is delivered for distribution to markets across the United States, as well as to Ontario, Canada.

•Midcontinent Express Pipeline originates near Bennington, Oklahoma and traverses northern Louisiana and central Mississippi to an interconnect with the Transcontinental Gas Pipeline system in Butler, Alabama. The Midcontinent Express Pipeline is owned by a 50/50 joint venture with KMI, the operator of the system.

•Gulf States Transmission is a 10-mile interstate pipeline that extends from Harrison County, Texas to Caddo Parish, Louisiana.

Regasification Facility

Lake Charles LNG, our wholly-owned subsidiary, owns an LNG import terminal and regasification facility located on Louisiana’s Gulf Coast near Lake Charles, Louisiana. The import terminal has approximately 9.0 Bcf of above ground LNG storage capacity and the regasification facility has a send out capacity of 1.8 Bcf/d.

Liquefaction Project

LCL, a wholly-owned subsidiary of ETO, is in the process of developing an LNG liquefaction project at the site of our Lake Charles LNG import terminal and regasification facility. The project would utilize existing dock and storage facilities owned by Lake Charles LNG located on the Lake Charles site. LCL entered into a prior development agreement with Shell in March 2019; however, Shell withdrew from the project in March 2020 due to adverse market factors affecting Shell's business following the onset of the COVID-19 pandemic. We intend to continue to develop the project, possibly in conjunction with one or more equity partners, and we plan to evaluate a variety of alternatives to advance the project, including the possibility of reducing the size of the project from three trains (16.45 million tonnes per annum of LNG capacity) to two trains (11.0 million tonnes per annum). The project as currently designed is fully permitted by federal, state and local authorities, has all necessary export licenses and benefits from the infrastructure related to the existing regasification facility at the same site, including four LNG storage tanks, two deep water docks and other assets. In light of the existing brownfield infrastructure and the advanced state of the development of the project, we plan to continue to pursue the project on a disciplined, cost effective basis, and ultimately we will determine whether to make a final investment decision to proceed with the project based on market conditions, capital expenditure considerations and our success in securing equity participation by third parties as well as long-term LNG offtake commitments on satisfactory terms. LCL is actively involved in a variety of activities related to the development of the project and has also been marketing LNG offtake to numerous potential customers in Asia and Europe.

The export of LNG produced by the liquefaction project from the United States would be undertaken under long-term export authorizations issued by the DOE to LCL. In March 2013, LCL obtained a DOE authorization to export LNG to countries with which the United States has or will have Free Trade Agreements (“FTA”) for trade in natural gas (the “FTA Authorization”). In July 2016, LCL also obtained a conditional DOE authorization to export LNG to countries that do not have an FTA for trade in natural gas (the “Non-FTA Authorization”). In October 2020, the DOE extended the FTA Authorization and Non-FTA Authorization to 30- and 25-year terms, respectively, following first deliveries on or before December 2025, consistent with the FERC authorization for the project. The FTA Authorization and Non-FTA Authorization have 25- and 20-year terms, respectively, commencing with the completion of construction of the liquefaction facility. In addition, LCL received its wetlands permits from the USACE to perform wetlands mitigation work and to perform modification and dredging work for the temporary and permanent dock facilities at the Lake Charles LNG facilities.

Midstream

The following details our assets in the midstream segment:

| | | | | | | | | | | | |

| Description of Assets | | Net Gas Processing Capacity

(MMcf/d) | | | | |

| South Texas Region: | | | | | | |

| Southeast Texas System | | 410 | | | | | |

| Eagle Ford System | | 1,920 | | | | | |

| Ark-La-Tex Region | | 1,442 | | | | | |

| North Central Texas Region | | 700 | | | | | |

| Permian Region | | 2,740 | | | | | |

| Midcontinent Region | | 1,238 | | | | | |

| Eastern Region | | 200 | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

The following information describes our principal midstream assets:

South Texas Region:

•The Southeast Texas System is an integrated system that gathers, compresses, treats, processes, dehydrates and transports natural gas from the Austin Chalk trend and Eagle Ford shale formation. The Southeast Texas System is a large natural gas gathering system covering thirteen counties between Austin and Houston. This system is connected to the Katy Hub through the ETC Katy Pipeline and is also connected to the Oasis Pipeline. The Southeast Texas System includes two natural gas processing plants (La Grange and Alamo) with aggregate capacity of 410 MMcf/d. The La Grange and Alamo processing plants are natural gas processing plants that process the rich gas that flows through our gathering system to produce residue gas and NGLs. Residue gas is delivered into our intrastate pipelines and NGLs are delivered into our NGL pipelines to Lone Star.

Our treating facilities remove carbon dioxide and hydrogen sulfide from natural gas gathered into our system before the natural gas is introduced to transportation pipelines to ensure that the gas meets pipeline quality specifications.

•The Eagle Ford Gathering System consists of 30-inch and 42-inch natural gas gathering pipelines with over 1.4 Bcf/d of capacity originating in Dimmitt County, Texas, and extending to both our King Ranch gas plant in Kleberg County, Texas and Jackson plant in Jackson County, Texas. The Eagle Ford Gathering System includes four processing plants (Chisholm, Kenedy, Jackson and King Ranch) with aggregate capacity of 1.92 Bcf/d. Our Chisholm, Kenedy, Jackson and King Ranch processing plants are connected to our intrastate transportation pipeline systems for deliveries of residue gas and are also connected with our NGL pipelines for delivery of NGLs to Lone Star.

Ark-La-Tex Region:

•Our Northern Louisiana assets are comprised of several gathering systems in the Haynesville Shale with access to multiple markets through interconnects with several pipelines, including our Tiger Pipeline. Our Northern Louisiana assets include the Bistineau, Creedence, and Tristate Systems, which collectively include three natural gas treating facilities, with aggregate capacity of 1.4 Bcf/d.

•The Ark-La-Tex assets gather, compress, treat and dehydrate natural gas in several parishes in north and west Louisiana and several counties in East Texas. These assets also include cryogenic natural gas processing facilities, a refrigeration plant, a conditioning plant, amine treating plants, a residue gas pipeline that provides market access for natural gas from our processing plants, including connections with pipelines that provide access to the Perryville Hub and other markets in the Gulf Coast region, and an NGL pipeline that provides connections to the Mont Belvieu market for NGLs produced from our processing plants. Collectively, the ten natural gas processing facilities (Dubach, Dubberly, Lisbon, Salem, Elm Grove, Minden, Ada, Brookeland, Lincoln Parish and Mt. Olive) have an aggregate capacity of 1.3 Bcf/d.

•Through the gathering and processing systems described above and their interconnections with RIGS in north Louisiana, as well as other pipelines, we offer producers wellhead-to-market services, including natural gas gathering, compression, processing, treating and transportation.

North Central Texas Region:

•The North Central Texas System is an integrated system located in four counties in North Central Texas that gathers, compresses, treats, processes and transports natural gas from the Barnett and Woodford Shales. Our North Central Texas assets include our Godley and Crescent plants, which process rich gas produced from the Barnett Shale and STACK play, with aggregate capacity of 700 MMcf/d. The Godley plant is integrated with the ET Fuel System.

Permian Region:

•The Permian Basin Gathering System offers wellhead-to-market services to producers in eleven counties in West Texas, as well as two counties in New Mexico which surround the Waha Hub, one of Texas’s developing NGL-rich natural gas market areas. As a result of the proximity of our system to the Waha Hub, the Waha Gathering System has a variety of market outlets for the natural gas that we gather and process, including several major interstate and intrastate pipelines serving California, the midcontinent region of the United States and Texas natural gas markets. The NGL market outlets includes Lone Star’s liquids pipelines. The Permian Basin Gathering System includes eleven processing facilities (Waha, Coyanosa, Red Bluff, Halley, Jal, Keyston, Tippet, Orla, Panther, Rebel and Arrowhead) with an aggregate processing capacity of 2.4 Bcf/d and one natural gas conditioning facility with aggregate capacity of 200 MMcf/d.

•We own a 50% membership interest in Mi Vida JV LLC, a joint venture which owns a 200 MMcf/d cryogenic processing plant in West Texas. We operate the plant and related facilities on behalf of the joint venture.

•We own a 50% membership interest in Ranch Westex JV, LLC, which processes natural gas delivered from the NGL-rich Bone Spring and Avalon Shale formations in West Texas. The joint venture owns a 25 MMcf/d refrigeration plant and a 125 MMcf/d cryogenic processing plant.

Midcontinent Region:

•The Midcontinent Systems are located in two large natural gas producing regions in the United States, the Hugoton Basin in southwest Kansas, and the Anadarko Basin in western Oklahoma and the Texas Panhandle and the STACK in central Oklahoma. These mature basins have continued to provide generally long-lived, predictable production volume. Our Midcontinent assets are extensive systems that gather, compress and dehydrate low-pressure gas. The Midcontinent Systems include sixteen natural gas processing facilities (Mocane, Beaver, Antelope Hills, Woodall, Wheeler, Sunray, Hemphill, Phoenix, Hamlin, Spearman, Red Deer, Lefors, Cargray, Gray, Rose Valley, and Hopeton) with an aggregate capacity of approximately 1.2 Bcf/d.

•We operate our Midcontinent Systems at low pressures to maximize the total throughput volumes from the connected wells. Wellhead pressures are therefore adequate to allow for flow of natural gas into the gathering lines without the cost of wellhead compression.

•We also own the Hugoton Gathering System that has 1,900 miles of pipeline extending over nine counties in Kansas and Oklahoma. This system is operated by a third party.

Eastern Region:

•The Eastern Region assets are located in eleven counties in Pennsylvania, four counties in Ohio, three counties in West Virginia, and gather natural gas from the Marcellus and Utica basins. Our Eastern Region assets include approximately 600 miles of natural gas gathering pipeline, natural gas trunklines, fresh-water pipelines, and nine gathering and processing systems, as well as the 200 MMcf/d Revolution processing plant, which feeds into our Mariner East and Rover pipeline systems.

•We also own a 51% membership interest in Aqua – ETC Water Solutions LLC, a joint venture that transports and supplies fresh water to natural gas producers drilling in the Marcellus Shale in Pennsylvania.

•We own a 75% membership interest in ORS. On behalf of ORS, we operate its Ohio Utica River System, which consists of 47 miles of 36-inch, 13 miles of 30-inch and 3 miles of 24-inch gathering trunklines, that delivers up to 3.6 Bcf/d to Rockies Express Pipeline, Texas Eastern Transmission, Leach Xpress, Rover and DEO TPL-18.

NGL and Refined Products Transportation and Services

The following details the assets in our NGL and refined products transportation and services segment:

| | | | | | | | | | | | | | | | | | | | |

| Description of Assets | | Miles of Liquids Pipeline (1) | | NGL Fractionation / Processing Capacity

(MBbls/d) | | Working Storage Capacity

(MBbls) |

| Liquids Pipelines: | | | | | | |

| Lone Star Express | | 892 | | | — | | | — | |

| West Texas Gateway Pipeline | | 510 | | | — | | | — | |

| Lone Star | | 1,400 | | | — | | | — | |

| Mariner East | | 667 | | | — | | | — | |

| Mariner South | | 67 | | | — | | | — | |

| Mariner West | | 398 | | | — | | | — | |

White Cliffs Pipeline(2) | | 540 | | | — | | | — | |

| Other NGL Pipelines | | 279 | | | — | | | — | |

| Liquids Fractionation and Services Facilities: | | | | | | |

| Mont Belvieu Facilities | | 182 | | | 940 | | | 50,000 | |

Sea Robin Processing Plant(3) | | — | | | 26 | | | — | |

Refinery Services(3) | | 100 | | | 35 | | | — | |

| Hattiesburg Storage Facilities | | — | | | — | | | 5,200 | |

| Cedar Bayou | | — | | | — | | | 1,600 | |

| NGL Terminals: | | | | | | |

| Nederland | | — | | | — | | | 1,900 | |

| Orbit Gulf Coast | | 70 | | | — | | | 1,200 | |

| Marcus Hook Terminal | | — | | | 132 | | | 6,000 | |

| Inkster | | — | | | — | | | 860 | |

| Refined Products Pipelines: | | | | | | |

| Eastern region pipelines | | 1,016 | | | — | | | — | |

| Midcontinent region pipelines | | 332 | | | — | | | — | |

| Southwest region pipelines | | 376 | | | — | | | — | |

| Inland Pipeline | | 690 | | | — | | | — | |

| JC Nolan Pipeline | | 504 | | | — | | | — | |

| Refined Products Terminals: | | | | | | |

| Eagle Point | | — | | | — | | | 6,700 | |

| Marcus Hook Terminal | | — | | | — | | | 930 | |

| Marcus Hook Tank Farm | | — | | | — | | | 1,900 | |

| Marketing Terminals | | — | | | — | | | 7,700 | |

| JC Nolan Terminal | | — | | | — | | | 134 | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

| | | | | | |

(1)Miles of pipeline as reported to PHMSA.

(2)The White Cliffs Pipeline consists of two parallel, 12-inch common carrier pipelines: one crude oil pipeline and one NGL pipeline.

(3)Additionally, the Sea Robin Processing Plant and Refinery Services have inlet volume capacities of 850 MMcf/d and 54 MMcf/d, respectively.

The following information describes our principal NGL and refined products transportation and services assets:

•The Lone Star Express System is an interstate NGL pipeline consisting of 24-inch and 30-inch long-haul transportation pipeline, with throughput capacity of approximately 500 MBbls/d, that delivers mixed NGLs from processing plants in the

Permian Basin, the Barnett Shale, and from East Texas to the Mont Belvieu NGL storage facility. In the third quarter of 2020, we completed an expansion of the pipeline, which added approximately 400 MBbls/d of NGL pipeline capacity from Lone Star’s pipeline system near Wink, Texas to the Lone Star Express 30-inch pipeline south of Fort Worth, Texas. It is expected to be in service by the fourth quarter of 2020.

•The West Texas Gateway Pipeline transports NGLs produced in the Permian and Delaware Basins and the Eagle Ford Shale to Mont Belvieu, Texas and has a throughput capacity of approximately 240 MBbls/d.

•The Mariner East pipeline transports NGLs from the Marcellus and Utica Shales areas in Western Pennsylvania, West Virginia and Eastern Ohio to destinations in Pennsylvania, including our Marcus Hook Terminal on the Delaware River, where they are processed, stored and distributed to local, domestic and waterborne markets. The first phase of the project, referred to as Mariner East 1, consisted of interstate and intrastate propane and ethane service and commenced operations in the fourth quarter of 2014 and the first quarter of 2016, respectively. The second phase of the project, referred to as Mariner East 2, began service in December 2018. The Mariner East pipeline has a throughput capacity of approximately 345 MBbls/d.

•The Mariner South liquids pipeline system consists of three pipelines and delivers export-grade propane, butane and natural gasoline from Lone Star’s Mont Belvieu, Texas storage and fractionation complex to our marine terminal in Nederland, Texas and has a total throughput capacity of approximately 600 MBbls/d.

•The Mariner West pipeline provides transportation of ethane from the Marcellus shale processing and fractionating areas in Houston, Pennsylvania to Marysville, Michigan and the Canadian border and has a throughput capacity of approximately 50 MBbls/d.

•The White Cliffs NGL pipeline, in which we have 51% ownership interest and was acquired by ET in the SemGroup acquisition and contributed to ETO in January 2020, transports NGLs produced in the DJ Basin to Cushing, where it interconnects with the Southern Hills Pipeline to move NGLs to Mont Belvieu, Texas and has a throughput capacity of approximately 90 MBbls/d.

•Other NGL pipelines include the 127-mile Justice pipeline with capacity of 375 MBbls/d, the 45-mile Freedom pipeline with a capacity of 56 MBbls/d, the 20-mile Spirit pipeline with a capacity of 20 MBbls/d and a 50% interest in the 87-mile Liberty pipeline with a capacity of 140 MBbls/d.

•Our Mont Belvieu storage facility is an integrated liquids storage facility with approximately 50 MMBbls of salt dome capacity providing 100% fee-based cash flows. The Mont Belvieu storage facility has access to multiple NGL and refined products pipelines, the Houston Ship Channel trading hub, and numerous chemical plants, refineries and fractionators.

•Our Mont Belvieu fractionators handle NGLs delivered from several sources, including the Lone Star Express pipeline and the Justice pipeline. Fractionator VI was placed in service in February 2019 and Fractionator VII was placed in service in the first quarter of 2020.