Table of Contents

Filed Pursuant to Rule 424(b)(5)

Registration File Number 333-130564;

333-130564-01;

333-130564-02;

333-130564-03

PROSPECTUS SUPPLEMENT

(To Prospectus dated April 11, 2006)

$175,000,000

Sunoco Logistics Partners Operations L.P.

6.125% Senior Notes due 2016

Guaranteed By

Sunoco Logistics Partners L.P. and Subsidiaries

This is an offering by Sunoco Logistics Partners Operations L.P. of $175,000,000 of 6.125% Senior Notes due 2016. Interest is payable on the notes on May 15 and November 15 of each year beginning November 15, 2006. Interest on the notes will accrue from May 8, 2006. The notes will mature on May 15, 2016.

We may redeem all or part of the notes at any time at a price of 100% of their principal amount plus a make-whole premium and accrued and unpaid interest to the redemption date. The notes will not be entitled to the benefit of any sinking fund payment.

The notes will be our senior unsecured obligations and will rank equally in right of payment with all of our existing and future senior debt and senior to any future subordinated debt that we may incur. The notes will be unconditionally guaranteed by our parent, Sunoco Logistics Partners L.P., and our subsidiaries on a senior unsecured basis so long as they guarantee any of our other long-term indebtedness. Their guarantees of the notes will rank equally in right of payment with their existing and future senior debt, including their guarantees of indebtedness under our revolving credit facility and our outstanding 7.25% Senior Notes due 2012, and senior to any future subordinated debt that they may incur.

Investing in the notes involves risks. Please read “Risk Factors” beginning on page S-12 of this prospectus supplement and on page 4 of the accompanying prospectus.

| Per Note | Total | ||||

Public Offering Price | 99.858% | $ | 174,751,500 | ||

Underwriting Discount | 0.650% | $ | 1,137,500 | ||

Proceeds to Sunoco Logistics Partners Operations L.P. (before expenses) | 99.208% | $ | 173,614,000 | ||

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus supplement or the accompanying prospectus is accurate or complete. Any representation to the contrary is a criminal offense.

The notes will not be listed on any national securities exchange. Currently, there is no public market for the notes.

It is expected that delivery of the notes will be made to investors in registered book-entry form only through the facilities of the The Depository Trust Company on or about May 8, 2006.

Joint Book-Running Managers

| BARCLAYS CAPITAL | CITIGROUP |

LEHMAN BROTHERS

CREDIT SUISSE

RBS GREENWICH CAPITAL

RAYMOND JAMES

SUNTRUST ROBINSON HUMPHREY

WACHOVIA SECURITIES

May 2, 2006

Table of Contents

Table of Contents

This document is in two parts. The first part is this prospectus supplement, which describes the specific terms of this offering of notes. The second part is the accompanying prospectus, which gives more general information, some of which may not apply to this offering of notes. If the information about the offering varies between this prospectus supplement and the accompanying prospectus, you should rely on the information in this prospectus supplement.

You should rely only on the information contained or incorporated by reference in this prospectus supplement and the accompanying prospectus. We have not authorized anyone to provide you with additional or different information. If anyone provides you with additional, different or inconsistent information, you should not rely on it. We are offering to sell the notes, and seeking offers to buy the notes, only in jurisdictions where offers and sales are permitted. You should not assume that the information we have included in this prospectus supplement or the accompanying prospectus is accurate as of any date other than the dates shown in these documents or that any information we have incorporated by reference is accurate as of any date other than the date of the document incorporated by reference. Our business, financial condition, results of operations and prospects may have changed since that date.

We expect delivery of the notes will be made against payment therefor on or about May 8, 2006, which is the fourth business day following the date of pricing of the notes (this settlement cycle being referred to as “T+4”). Under Rule 15c6-1 of the Securities Exchange Act of 1934, trades in the secondary market generally are required to settle in three business days, unless the parties to the trade expressly agree otherwise. Accordingly, purchasers who wish to trade notes on the day of pricing or the next succeeding two business days will be required, by virtue of the fact that the notes initially will settle in T+4, to specify an alternate settlement cycle at the time of any trade to prevent a failed settlement. Such purchasers should consult their own advisors in that regard.

| Prospectus Supplement | ||

| S-1 | ||

| S-12 | ||

| S-16 | ||

| S-17 | ||

| S-18 | ||

| S-19 | ||

| S-21 | ||

| S-29 | ||

| S-33 | ||

| S-35 | ||

| S-35 | ||

| S-36 | ||

| S-38 | ||

| Prospectus dated April 11, 2006 | ||

| 1 | ||

About Sunoco Logistic Partners L.P. and Sunoco Logistics Partners Operations L.P. | 1 | |

| 2 | ||

| 2 | ||

| 4 | ||

| 19 | ||

| 21 | ||

| 21 | ||

| 21 | ||

| 24 | ||

| 32 | ||

| 43 | ||

| 48 | ||

| 62 | ||

| 63 | ||

| 64 | ||

| 65 | ||

| 65 | ||

i

Table of Contents

This summary highlights information contained elsewhere in this prospectus supplement and the accompanying prospectus. It does not contain all of the information that you should consider before investing in the notes. You should read the entire prospectus supplement, the accompanying prospectus and the documents incorporated by reference for a more complete understanding of this offering. Please read “Risk Factors” beginning on page S-12 of this prospectus supplement and page 4 of the accompanying prospectus for more information about important risks that you should consider before investing in the notes.

As used in this prospectus supplement, unless the context otherwise indicates, the terms “we,” “us,” “our” and similar terms mean Sunoco Logistics Partners Operations L.P., together with our operating subsidiaries. References to the “master partnership,” “our parent” or “Sunoco Logistics Partners” refer to Sunoco Logistics Partners L.P. References to “Sunoco” mean Sunoco, Inc., the owner of the general partner of the master partnership. References to “Sunoco R&M” mean Sunoco, Inc. (R&M), a wholly owned subsidiary of Sunoco through which Sunoco conducts its refining and marketing operations. We are the wholly owned operating subsidiary of the master partnership. Except where the context otherwise requires, references to, and descriptions of, our assets, operations and financial results include the assets, operations and financial results of the master partnership and its subsidiaries and predecessors.

Sunoco Logistics Partners Operations L.P.

We are a Delaware limited partnership formed by Sunoco Logistics Partners to own, operate and acquire a geographically diverse portfolio of complementary pipeline, terminalling, and crude oil acquisition and marketing assets. We are principally engaged in the transportation, terminalling and storage of refined products and crude oil and the purchase and sale of crude oil. Sunoco Logistics Partners conducts substantially all of its business through us. We are the borrower under the master partnership’s revolving credit facility, and we are the issuer of all of the master partnership’s publicly-traded notes, all of which are guaranteed by Sunoco Logistics Partners. Our financial results do not differ materially from those of Sunoco Logistics Partners. The number and dollar amount of reconciling items between our consolidated financial statements and those of Sunoco Logistics Partners are insignificant. All financial results presented in this prospectus supplement and the accompanying prospectus are those of Sunoco Logistics Partners.

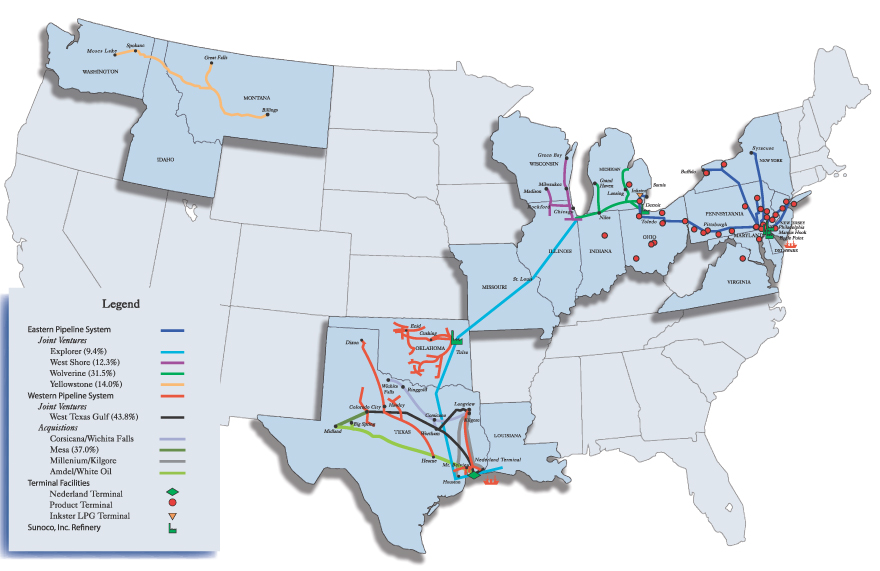

Our business is currently comprised of three segments, consisting of our Eastern Pipeline System, our Terminal Facilities and our Western Pipeline System.

| • | Eastern Pipeline System. Our Eastern Pipeline System primarily serves the northeast and midwest United States refining and marketing operations of Sunoco R&M and includes: (i) approximately 1,647 miles of refined product pipelines, including a two-thirds undivided interest in the 80-mile refined product Harbor pipeline; (ii) 58 miles of interrefinery pipelines between two of Sunoco R&M’s refineries; and (iii) approximately 140 miles of crude oil pipelines. In addition, our Eastern Pipeline System includes equity interests in four refined product pipelines, which primarily serve third-party shippers. These equity interests include: (i) a 9.4% interest in Explorer Pipeline Company, a joint venture that owns a 1,413-mile refined product pipeline; (ii) a 31.5% interest in Wolverine Pipe Line Company, a joint venture that owns a 721-mile refined product pipeline;(iii) a 12.3% interest in West Shore Pipe Line Company, a joint venture that owns a 652-mile refined product pipeline; and (iv) a 14.0% interest in Yellowstone Pipe Line Company, a joint venture that owns a 655-mile refined product pipeline. |

| • | Terminal Facilities. Our Terminal Facilities consist of: (i) 35 inland refined product terminals with an aggregate storage capacity of approximately 5.9 million barrels, primarily serving our Eastern Pipeline System; (ii) a 2.0 million barrel refined product terminal serving Sunoco R&M’s Marcus Hook refinery |

S-1

Table of Contents

near Philadelphia, Pennsylvania; (iii) the Nederland Terminal, a 12.5 million barrel marine crude oil terminal on the Texas Gulf Coast; (iv) one inland and two marine crude oil terminals with a combined capacity of approximately 3.4 million barrels and related pipelines, which serve Sunoco R&M’s refinery in Philadelphia, Pennsylvania; (v) a ship and barge dock that serves Sunoco R&M’s Eagle Point refinery; and (vi) a 1.0 million barrel liquefied petroleum gas, or LPG, terminal located near Detroit, Michigan that principally serves Sunoco R&M’s refinery in Toledo, Ohio. |

| • | Western Pipeline System. Our Western Pipeline System gathers, purchases, sells, and transports crude oil principally in Oklahoma and Texas and consists of: (i) approximately 3,115 miles of crude oil trunk pipelines, including a 37.0% undivided interest in the 80-mile Mesa Pipe Line System, and approximately 520 miles of crude oil gathering lines that supply the trunk pipelines; (ii) approximately 116 crude oil transport trucks; (iii) approximately 130 crude oil truck unloading facilities; and (iv) a 43.8% interest in West Texas Gulf Pipe Line Company, a joint venture that owns a 579-mile crude oil pipeline. |

On March 1, 2006, we purchased two crude oil pipeline systems and related crude oil storage facilities located in Texas from affiliates of Black Hills Energy, Inc. and Alon USA Energy, Inc. for $41.4 million and $68.0 million, respectively. These pipeline systems are included in our Western Pipeline System and the statistics discussed above. On April 17, 2006, we signed a definitive agreement to purchase a 50% interest in a refined products terminal located in Syracuse, New York from Mobil Pipe Line Company, an affiliate of Exxon Mobil Corporation. On April 18, 2006, the board of directors of our general partner approved construction of two new storage tanks with a combined capacity of 1.3 million shell barrels at our Nederland, Texas Terminal. Please read “—Recent Developments” beginning on page S-4 and “Overview of Acquisitions” on page S-18 of this prospectus supplement for more information about these assets.

We transport, terminal, and store refined products and crude oil in 12 states located in the northeast, midwest and southwest United States. We generate revenues by charging tariffs for transporting refined products, crude oil and other hydrocarbons through our pipelines as well as by charging fees for storing refined products, crude oil and other hydrocarbons in, and for providing other services at, our terminals. We also generate revenues by purchasing domestic crude oil and selling it to Sunoco R&M and other customers. Generally, as we purchase crude oil, we simultaneously enter into corresponding sale transactions involving physical deliveries of crude oil, which enables us to secure a profit on the transaction at the time of purchase and establish a substantially balanced position, thereby minimizing our exposure to crude oil price volatility after the initial purchase. However, the margins we receive from these transactions may vary from period to period. We do not enter into futures contracts or other derivative instruments in connection with these purchases and sales.

For the year ended December 31, 2005, we had revenues of $4.5 billion, EBITDA of $117.1 million and net income of $61.7 million. For the three months ended March 31, 2006, we had revenues of $1.3 billion, EBITDA of $33.6 million and net income of $18.4 million. For an explanation of EBITDA and a reconciliation of EBITDA to operating income, please read note 7 to “—Summary Financial and Operating Data” of this prospectus supplement.

Our Business Strategies

Our primary business strategies are to:

| • | generate stable cash flows; |

| • | increase our pipeline and terminal throughput; |

| • | pursue strategic and accretive acquisitions that complement or supplement our existing asset base; and |

| • | continue to improve our operating efficiency and to reduce our costs. |

S-2

Table of Contents

Our Competitive Strengths

We believe that we are well-positioned to successfully execute our business strategies because of the following competitive strengths:

| • | We have a unique strategic relationship with Sunoco and its affiliates. Many of our refined product and crude oil pipelines and terminals are directly linked to Sunoco R&M’s refineries and afford Sunoco R&M a cost-effective means to access crude oil and distribute refined products. In connection with the master partnership’s initial public offering, we entered into an agreement with Sunoco R&M under which Sunoco R&M agreed to use the pipelines and terminals that we owned as of that time. Sunoco R&M’s obligations under this agreement expire in 2007 and 2009. In addition, under our omnibus agreement with Sunoco, we have the right to purchase from Sunoco and its affiliates certain crude oil and refined products pipeline assets currently owned by Sunoco and its affiliates, as well as any significant crude oil or refined product pipeline and terminalling assets, which we often refer to as logistics assets, associated with acquisitions made by Sunoco and its affiliates. Our acquisition of the ship and barge docks and truck loading racks serving Sunoco R&M’s Eagle Point refinery in March 2004 and our acquisition of an undivided interest in the Mesa Pipe Line System in 2005 are examples of our exercising these rights under the omnibus agreement. As part of the Eagle Point acquisition, we entered into an agreement with Sunoco R&M under which Sunoco R&M agreed to use those logistics assets until March 2016. |

| • | Our refined product pipelines and terminal facilities are strategically located in areas with high demand. We have a strong presence in the northeastern and midwestern United States, and our transportation and distribution assets in these regions operate at high utilization rates, providing us with a base of stable cash flows. |

| • | We have a complementary portfolio of assets that are both geographically and operationally diverse. Our assets include refined product pipelines and terminals in the northeastern and midwestern United States, a crude oil terminal on the Texas Gulf Coast and crude oil pipelines in Oklahoma and Texas. We also own equity interests in four refined product pipelines located in the central and western regions of the United States and one crude oil pipeline extending across Texas. This geographic and asset diversity contributes to the stability of our cash flows. |

| • | Our pipelines and terminal facilities are efficient and well-maintained. In recent years, we have made significant investments to upgrade our asset base. All of our refined product pipelines and terminal facilities and many of our crude oil pipelines are automated to provide continuous, real-time, operational data. We continually undertake internal inspection programs and other procedures to monitor the integrity of our pipelines. |

| • | Our executive officers and directors have extensive energy industry experience. Our executive officers and directors have broad experience in the energy industry and our management team has operated our core assets for over ten years. As a result, we believe that we have the expertise to execute our business strategies and manage our assets and operations effectively. The master partnership’s general partner has adopted incentive compensation plans to closely align the interests of our executive officers with the interests of our other stakeholders. |

Our Relationship with Sunoco and its Affiliates

We have a strong and mutually beneficial relationship with Sunoco, one of the leading independent refining and marketing companies in the United States and the largest refiner in the northeastern United States. Sunoco operates its businesses through a number of operating subsidiaries, the primary one being Sunoco R&M, which operates Sunoco’s refineries and markets gasoline and convenience items through over 4,700 retail sites. Sunoco R&M owns and operates five refineries with an aggregate refining capacity of approximately 900,000 barrels per day, or bpd. Substantially all of Sunoco’s business activities with us are conducted through Sunoco R&M and the majority of our operations are strategically located within Sunoco R&M’s refining and marketing supply chain. Sunoco R&M relies on us to provide transportation and terminalling services that support a significant portion of its refining and marketing operations.

S-3

Table of Contents

The success of our operations depends substantially upon the continued use of our pipelines and terminal facilities by Sunoco R&M. For the three months ended March 31, 2006, Sunoco R&M accounted for approximately 68% of the total revenues of our Eastern Pipeline System, approximately 66% of the total revenues of our Terminal Facilities and approximately 37% of the total revenues of our Western Pipeline System. We have entered into agreements with Sunoco R&M under which Sunoco R&M has agreed to use many of our logistics assets. The majority of Sunoco R&M’s minimum revenue obligations under these agreements will expire in 2007 and 2009. Since the master partnership’s initial public offering, revenues generated by Sunoco R&M related to these agreements have exceeded these minimum revenue obligations by an average of approximately 19% per year. We expect to continue to derive a substantial portion of our revenues from Sunoco R&M for the foreseeable future. These agreements and other related contracts, coupled with the strategic interplay between our assets and Sunoco R&M’s assets, result in a mutually beneficial relationship between us and Sunoco R&M.

Concurrent Offering of Common Units

Concurrently with our offering of senior notes, the master partnership is offering 2,400,000 common units in a registered public offering. The common units sold in that offering will receive the declared cash distribution of $0.75 per unit for the first quarter of 2006 to be paid on May 15, 2006. Our offering of senior notes is not conditioned upon the consummation of the master partnership’s concurrent offering of common units. Please read “Use of Proceeds” and “Capitalization.”

Recent Developments

Recent and Pending Acquisitions: Since December 2005, we acquired or entered into agreements to acquire the following assets:

| • | Mesa Pipeline. In December 2005, we purchased a 37.0% undivided interest in the Mesa Pipe Line System for approximately $6.6 million from affiliates of Sunoco and Chevron. The Mesa Pipe Line System consists of an 80-mile, 24-inch crude oil pipeline from Midland, Texas to Colorado City, Texas, with an operating capacity of 316,000 bpd, and approximately 800,000 barrels of tankage at Midland. The Mesa Pipe Line System connects to the West Texas Gulf pipeline, of which we own a 43.8% interest, which supplies crude oil to the Mid-Valley pipeline. |

| • | Millennium and Kilgore Pipelines. On March 1, 2006, we purchased a crude oil pipeline system from affiliates of Black Hills Energy, Inc. for $41.4 million. The system consists of 390 miles of crude oil pipelines with an operating capacity of 100,000 bpd and 340,000 shell barrels of active storage capacity. |

| • | Amdel and White Oil Pipelines. On March 1, 2006, we acquired a crude oil pipeline system located in Texas from affiliates of Alon USA Energy, Inc. for $68.0 million. The system consists of 528 miles of crude oil pipelines with an operating capacity of 67,000 bpd. Alon has also agreed to ship a minimum of 15,000 bpd on these pipelines under a 10-year throughput and deficiency agreement. These pipelines are currently idled and are scheduled to be returned to service on June 1, 2006. |

| • | Refined Products Terminal. On April 17, 2006, we signed a definitive agreement to purchase a 50% interest in a refined products terminal located in Syracuse, New York from Mobil Pipe Line Company, an affiliate of Exxon Mobil Corporation. The storage capacity of this terminal is approximately 550,000 barrels. The transaction is subject to purchase rights held by an existing owner and normal conditions to closing for assets of this nature. |

Please read “Overview of Acquisitions” beginning on page S-18 of this prospectus supplement for more information about these assets.

S-4

Table of Contents

Expansion of Nederland Terminal. On April 18, 2006, the board of directors of our general partner approved construction of two new storage tanks with a combined capacity of 1.3 million shell barrels at our Nederland, Texas Terminal. These tanks are expected to be completed by the third quarter of 2007 and, coupled with the other tanks currently under construction, will increase the capacity of our Nederland Terminal to 16.5 million shell barrels.

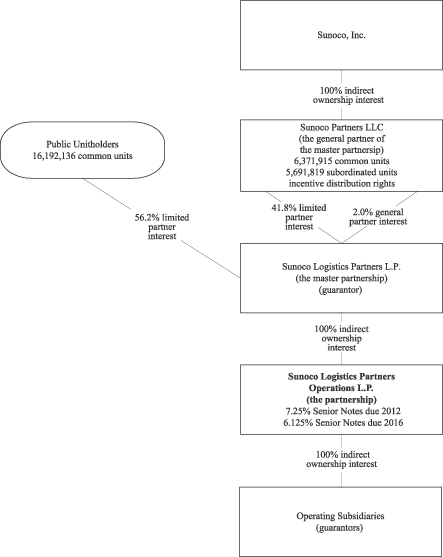

Our Ownership, Structure and Management

We are the operating subsidiary of the master partnership. We and our subsidiaries conduct the master partnership’s operations and own its operating assets. Our general partner has sole responsibility for conducting our business and for managing our operations. The directors and officers of our general partner are the same as the officers and directors of Sunoco Partners LLC, the general partner of the master partnership. Sunoco, the owner of our master partnership’s general partner, receives an annual administrative fee for the provision of various general and administrative services for our benefit. The fee does not include salaries of pipeline and terminal personnel or other employees of our master partnership’s general partner, including senior executives, or the cost of their employee benefits. We will also reimburse Sunoco and its affiliates for direct expenses they incur on our behalf.

Upon consummation of this offering and assuming a successful completion of the master partnership’s concurrent common unit offering:

| • | There will be 16,192,136 publicly held common units outstanding representing an aggregate 56.2% limited partner interest in the master partnership; |

| • | Sunoco, through its ownership of the master partnership’s general partner, will own 6,371,915 common units and 5,691,819 subordinated units representing an aggregate 41.8% limited partner interest in the master partnership; and |

| • | the master partnership’s general partner will continue to own a 2.0% general partner interest in the master partnership and all of the incentive distribution rights. |

The following chart depicts the organization and ownership of us, our subsidiaries and the master partnership after giving effect to this offering and the master partnership’s concurrent offering of common units, but before any exercise of the underwriters’ option to purchase additional common units of the master partnership. This offering of senior notes is not conditioned upon the consummation of the master partnership’s concurrent offering of common units.

S-5

Table of Contents

| Percentage Interest | |||

Ownership of Sunoco Logistics Partners Operations L.P. | |||

Sunoco Logistics Partners GP LLC General Partner Interest | 0.01 | % | |

Sunoco Logistics Partners L.P. Limited Partner Interest | 99.99 | % | |

Total | 100.0 | % | |

Ownership of Sunoco Logistics Partners L.P. | |||

Public Common Units | 56.2 | % | |

Sunoco Partners LLC Common Units | 22.1 | % | |

Sunoco Partners LLC Subordinated Units | 19.7 | % | |

Sunoco Partners LLC General Partner Interest | 2.0 | % | |

Total | 100.0 | % | |

Our principal executive offices are located at Mellon Bank Center, 1735 Market Street, Suite LL, Philadelphia, Pennsylvania 19103, and our phone number is (866) 248-4344.

S-6

Table of Contents

The Notes Offering

Issuer | Sunoco Logistics Partners Operations L.P. |

Securities | $175,000,000 of 6.125% Senior Notes due 2016. |

Maturity Date | May 15, 2016. |

Interest Payment Dates | We will pay interest on the notes in arrears each May 15 and November 15, beginning November 15, 2006. |

Mandatory Redemption | We will not be required to make mandatory redemption or sinking fund payments on the notes or to repurchase the notes at the option of the holders. |

Optional Redemption | We may redeem the notes, in whole or in part, at any time at a price equal to 100% of the principal amount plus accrued and unpaid interest to the date of redemption, plus a make-whole premium as described under “Description of the Notes—Optional Redemption.” |

Guarantees | The notes will be unconditionally guaranteed by our parent and our subsidiaries on a senior unsecured basis so long as they guarantee any of our other long-term indebtedness. If we cannot make payments on the notes when they are due, the guarantors must make them instead. |

Ranking | The notes will be our general unsecured obligations. The notes will rank equally in right of payment with all our existing and future senior debt, including indebtedness under our revolving credit facility and our outstanding 7.25% Senior Notes due 2012, and senior in right of payment to any subordinated debt that we may incur. The guarantees of the notes will rank equally in right of payment with the guarantors’ existing and future senior debt, including their guarantees of indebtedness under our revolving credit facility and our 7.25% Senior Notes due 2012, and senior in right of payment to any subordinated debt they may incur. Neither we nor any guarantor currently has any secured debt outstanding. |

Certain Covenants | The indenture governing the notes limits our ability and the ability of our subsidiaries, among other things, to: |

| • | create liens without equally and ratably securing the notes; and |

| • | engage in certain sale and leaseback transactions. |

The indenture also limits our ability to engage in mergers, consolidations and certain sales of assets. |

These covenants are subject to important exceptions and qualifications, as described under “Description of the Notes—Important Covenants.” |

S-7

Table of Contents

Use of Proceeds | The master partnership will use all of the net proceeds from this offering, the master partnership’s concurrent common unit offering and the related capital contribution of the master partnership’s general partner: |

| • | to repay in full the $216.1 million of indebtedness outstanding under our revolving credit facility as of March 31, 2006, $109.5 million of which was incurred to finance our acquisition of the Millennium and Kilgore pipeline system and the Amdel and White Oil pipeline system; |

| • | to fund $38.0 million of our 2006 organic growth program; and |

| • | for general partnership purposes, including to finance pending and future acquisitions. |

The master partnership will use all the net proceeds from any exercise of the underwriters’ option to purchase additional common units of the master partnership, together with the related capital contribution of the general partner of the master partnership, to fund additional amounts under its 2006 organic growth program and for general partnership purposes, including to finance pending and future acquisitions. |

If the master partnership does not consummate its offering of common units, it will use the net proceeds from our offering of senior notes to repay indebtedness outstanding under our revolving credit facility. |

Affiliates of each of the underwriters participating in this offering are lenders under our revolving credit facility and will receive greater than 10% of the net proceeds of this offering through our repayment of that facility. Please read “Underwriting.” |

Please read “Use of Proceeds” and “Capitalization.” |

Ratings | We have obtained the following ratings on the notes: BBB by Standard & Poor’s Ratings Services and Baa2 by Moody’s Investors Service, Inc. |

A rating reflects only the view of a rating agency and is not a recommendation to buy, sell or hold the notes. Any rating can be revised upward or downward or withdrawn at any time by a rating agency if the rating agency decides that the circumstances warrant a revision. |

Risk Factors | Please read “Risk Factors” beginning on page S-12 and on page 4 of the accompanying prospectus for a discussion of factors you should carefully consider before investing in the notes. |

Trustee | Citibank, N.A. |

Governing Law | The notes and the guarantees will be governed by New York law. |

S-8

Table of Contents

Summary Financial and Operating Data

The following tables set forth summary condensed consolidated financial and operating data of Sunoco Logistics Partners L.P. for the years ended December 31, 2003, 2004 and 2005 and for the three months ended March 31, 2005 and 2006. The summary financial data presented below is derived from (i) the audited financial statements of Sunoco Logistics Partners L.P., which are included in its Annual Report on Form 10-K for the year ended December 31, 2005 and (ii) the unaudited financial statements included in its Quarterly Report on Form 10-Q for the three months ended March 31, 2006. Sunoco Logistics Partners L.P.’s Annual Report on Form 10-K for the year ended December 31, 2005 and its Quarterly Report on Form 10-Q for the quarter ended March 31, 2006 are incorporated by reference herein.

The summary financial and operating data should be read together with, and are qualified in their entirety by reference to, the historical condensed consolidated financial statements of Sunoco Logistics Partners L.P. and the accompanying notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” which are set forth in its Annual Report on Form 10-K for the year ended December 31, 2005 and its Quarterly Report on Form 10-Q for the quarter ended March 31, 2006.

| Year Ended December 31, | Three Months Ended March 31, | ||||||||||||||

| 2003(1) | 2004(2) | 2005(3) | 2005 | 2006(4) | |||||||||||

| (Unaudited) | |||||||||||||||

| ($ in thousands, except per unit amounts) | |||||||||||||||

Income Statement Data: | |||||||||||||||

Revenues: | |||||||||||||||

Sales and other operating revenue: | |||||||||||||||

Affiliates | $ | 1,383,090 | $ | 1,751,612 | $ | 1,986,019 | $ | 476,923 | $ | 478,321 | |||||

Unaffiliated customers | 1,274,383 | 1,699,673 | 2,496,593 | 534,926 | 782,650 | ||||||||||

Other income(5) | 16,730 | 13,932 | 14,295 | 3,627 | 2,391 | ||||||||||

Total revenues | 2,674,203 | 3,465,217 | 4,496,907 | 1,015,476 | 1,263,362 | ||||||||||

Costs and expenses: | |||||||||||||||

Cost of products sold and operating expenses | 2,519,160 | 3,307,480 | 4,326,713 | 974,911 | 1,214,786 | ||||||||||

Depreciation and amortization | 27,157 | 31,933 | 33,838 | 8,122 | 8,946 | ||||||||||

Selling, general and administrative expenses | 48,412 | 48,449 | 53,048 | 11,917 | 15,003 | ||||||||||

Total costs and expenses | 2,594,729 | 3,387,862 | 4,413,599 | 994,950 | 1,238,735 | ||||||||||

Operating income | 79,474 | 77,355 | 83,308 | 20,526 | 24,627 | ||||||||||

Net interest cost and debt expense | 20,040 | 20,324 | 21,599 | 5,228 | 6,203 | ||||||||||

Net income | $ | 59,434 | $ | 57,031 | $ | 61,709 | $ | 15,298 | $ | 18,424 | |||||

Net income per limited partner unit: | |||||||||||||||

Basic | $ | 2.55 | $ | 2.29 | $ | 2.37 | $ | 0.60 | $ | 0.66 | |||||

Diluted | $ | 2.53 | $ | 2.27 | $ | 2.35 | $ | 0.59 | $ | 0.66 | |||||

Cash distributions per unit to limited partners(6): | |||||||||||||||

Paid | $ | 1.9875 | $ | 2.3200 | $ | 2.5625 | $ | 0.6250 | $ | 0.7125 | |||||

Declared | $ | 2.0500 | $ | 2.3950 | $ | 2.6500 | $ | 0.6250 | $ | 0.7500 | |||||

S-9

Table of Contents

| Year Ended December 31, | Three Months Ended March 31, | |||||||||||||||||||

| 2003(1) | 2004(2) | 2005(3) | 2005 | 2006(4) | ||||||||||||||||

| (Unaudited) | ||||||||||||||||||||

| ($ in thousands, except per unit amounts) | ||||||||||||||||||||

Balance Sheet Data (at period end): | ||||||||||||||||||||

Net properties, plants and equipment | $ | 583,164 | $ | 647,200 | $ | 814,836 | $ | 646,933 | $ | 930,366 | ||||||||||

Total assets | 1,181,006 | 1,368,786 | 1,680,685 | 1,515,238 | 1,894,181 | |||||||||||||||

Total debt | 313,136 | 313,305 | 355,573 | 313,347 | 465,116 | |||||||||||||||

Total partners’ capital | 403,758 | 460,594 | 523,411 | 458,393 | 520,878 | |||||||||||||||

Other Financial Data: | ||||||||||||||||||||

Net cash provided by operating activities | $ | 97,212 | $ | 106,622 | $ | 90,835 | $ | 4,601 | $ | 38,778 | ||||||||||

Net cash provided by (used in) investing activities | (39,008 | ) | (95,583 | ) | (180,654 | ) | (7,841 | ) | (127,676 | ) | ||||||||||

Net cash provided by (used in) financing activities | (41,963 | ) | (8,460 | ) | 58,804 | (16,749 | ) | 72,204 | ||||||||||||

Capital expenditures: | ||||||||||||||||||||

Maintenance | $ | 30,850 | $ | 30,829 | $ | 31,194 | $ | 4,901 | $ | 6,439 | ||||||||||

Expansion | 10,226 | (1) | 64,754 | (2) | 149,460 | (3) | 2,940 | 116,913 | (4) | |||||||||||

Total capital expenditures | $ | 41,076 | (1) | $ | 95,583 | (2) | $ | 180,654 | (3) | $ | 7,841 | $ | 123,352 | (4) | ||||||

EBITDA(7) | $ | 106,631 | $ | 109,288 | $ | 117,146 | $ | 28,648 | $ | 33,573 | ||||||||||

Distributable cash flow(7) | $ | 61,055 | $ | 65,182 | $ | 72,378 | $ | 18,880 | $ | 20,931 | ||||||||||

Ratio of earnings to fixed charges(8) | 3.56 | x | 3.55 | x | 3.55 | x | 3.74 | x | 3.47 | x | ||||||||||

Operating Data: | ||||||||||||||||||||

Eastern Pipeline System total shipments (in thousands of barrel miles per day)(9)(10) | 55,324 | 59,173 | 56,907 | 55,601 | 60,989 | |||||||||||||||

Terminal Facilities throughput (bpd) | 1,204,394 | 1,464,254 | 1,549,427 | 1,577,722 | 1,566,577 | |||||||||||||||

Western Pipeline System throughput (bpd)(9) | 304,471 | 298,797 | 356,129 | 317,970 | 485,007 | |||||||||||||||

Crude oil purchases at wellhead (bpd) | 193,176 | 186,827 | 186,224 | 194,848 | 181,413 | |||||||||||||||

| (1) | On September 30, 2003, we acquired an additional 3.1% ownership interest in West Shore Pipe Line Company for $3.7 million, increasing our overall ownership percentage to 12.3%. The purchase price for this acquisition has been included within the 2003 expansion capital expenditures, and the equity income attributable to this additional 3.1% ownership interest in West Shore Pipe Line Company has been included in our statements of income from the date of its acquisition. |

| (2) | During the year ended December 31, 2004, we completed the following acquisitions: the Eagle Point logistics assets, which were purchased for $20.0 million on March 30, 2004; two refined product terminals located in Baltimore, Maryland and Manassas, Virginia, which were purchased for $12.0 million on April 28, 2004; an additional 33.3% undivided interest in the Harbor pipeline, which was acquired on June 28, 2004 for $7.3 million; and a refined product terminal located in Columbus, Ohio, which was purchased for $8.0 million on November 30, 2004. The aggregate purchase price for these acquisitions has been included within the 2004 expansion capital expenditures, and their results of operations have been included in our financial statements from their dates of acquisition. |

| (3) | Expansion capital expenditures in 2005 includes $100.0 million related to the August 1, 2005 acquisition of the Corsicana to Wichita Falls, Texas crude oil pipeline system and storage facilities, and $5.5 million related to the December 2005 acquisition of an undivided joint interest in the Mesa Pipe Line System. The |

S-10

Table of Contents

total purchase price of the Mesa interest was $6.6 million, however since a portion of the interest was acquired from Sunoco, it was recorded by us at Sunoco’s historical cost and the $1.1 million difference between the purchase price and the cost basis of the assets was recorded by us as a capital distribution. |

| (4) | Expansion capital expenditures in 2006 includes $37.5 million related to the acquisition of the Millennium and Kilgore pipeline system and $68.0 million related to the Amdel and White Oil pipeline system, both in March 2006. |

| (5) | Includes equity income from investments in corporate joint ventures. |

| (6) | Cash distributions paid per unit to limited partners include payments made per unit during the period stated. Cash distributions declared per unit to limited partners include distributions declared per unit related to the quarters within the period stated. Declared distributions are paid within 45 days following the close of each quarter. |

| (7) | EBITDA and distributable cash flow provide additional information for evaluating our ability to make distributions to our unitholders and our general partner. The following table reconciles the difference between operating income, as determined under United States generally accepted accounting principles, and EBITDA and distributable cash flow (in thousands): |

| Year Ended December 31, | Three Months Ended March 31, | |||||||||||||||||||

| 2003 | 2004 | 2005 | 2005 | 2006 | ||||||||||||||||

Operating income | $ | 79,474 | $ | 77,355 | $ | 83,308 | $ | 20,526 | $ | 24,627 | ||||||||||

Depreciation and amortization | 27,157 | 31,933 | 33,838 | 8,122 | 8,946 | |||||||||||||||

EBITDA | 106,631 | 109,288 | 117,146 | 28,648 | 33,573 | |||||||||||||||

Interest expense, net | (20,040 | ) | (20,324 | ) | (21,599 | ) | (5,228 | ) | (6,203 | ) | ||||||||||

Maintenance capital expenditures | (30,850 | ) | (30,829 | ) | (31,194 | ) | (4,901 | ) | (6,439 | ) | ||||||||||

Sunoco reimbursements | 5,314 | 7,047 | 8,025 | 361 | — | |||||||||||||||

Distributable cash flow | $ | 61,055 | $ | 65,182 | $ | 72,378 | $ | 18,880 | $ | 20,931 | ||||||||||

| Our management believes EBITDA and distributable cash flow information enhances an investor’s understanding of a business’ ability to generate cash for payment of distributions and other purposes. In addition, EBITDA is also used as a measure in our $300 million revolving credit facility in determining our compliance with certain covenants. However, there may be contractual, legal, economic or other reasons that may prevent us from satisfying principal and interest obligations with respect to indebtedness and may require us to allocate funds for other purposes. EBITDA and distributable cash flow do not represent and should not be considered alternatives to net income, operating income or cash flows from operating activities, as determined under United States generally accepted accounting principles and may not be comparable to other similarly titled measures of other businesses. |

| (8) | Please read “Ratio of Earnings to Fixed Charges” on page 21 of the accompanying prospectus for the method of calculating the ratio of earnings to fixed charges. |

| (9) | Excludes amounts attributable to our equity ownership interests in corporate joint ventures. |

| (10) | Total shipments represent the total average daily pipeline throughput multiplied by the number of miles of pipeline through which each barrel has been shipped. We believe that total shipments is a better performance indicator for the Eastern Pipeline System than throughput as certain refined product pipelines, including inter-refinery and transfer pipelines, transport large volumes over short distances and generate minimal revenues. |

S-11

Table of Contents

An investment in our senior notes involves risks. You should carefully consider all of the information contained in this prospectus supplement, the accompanying prospectus and the documents incorporated by reference as provided under “Where You Can Find More Information,” including Sunoco Logistics Partners L.P.’s annual report on Form 10-K for the year ended December 31, 2005 and its quarterly report on Form 10-Q for the quarter ended March 31, 2006, and the risk factors described under “Risk Factors” in such reports. This prospectus supplement, the accompanying prospectus and the documents incorporated by reference also contain forward-looking statements that involve risks and uncertainties. Please read “Forward-Looking Statements.” Our actual results could differ materially from those anticipated in the forward-looking statements as a result of certain factors, including the risks described below, elsewhere in this prospectus supplement, in the accompanying prospectus and in the documents incorporated by reference. If any of these risks occur, our business, financial condition or results of operation could be adversely affected.

Risks Related to our Business

If we are unable to complete capital projects at their expected costs and/or in a timely manner, or if the market conditions assumed in our project economics deteriorate, our financial condition, results of operations, or cash flows could be affected materially and adversely.

Delays or cost increases related to capital spending programs involving construction of new facilities (or improvements and repairs to our existing facilities) could adversely affect our ability to achieve forecasted internal rates of return and operating results. Delays in making required changes or upgrades to our facilities could subject us to fines or penalties as well as affect our ability to supply certain products we make. Such delays or cost increases may arise as a result of unpredictable factors in the marketplace, many of which are beyond our control, including:

| • | denial or delay in issuing requisite regulatory approvals and/or permits; |

| • | unplanned increases in the cost of construction materials or labor; |

| • | disruptions in transportation of modular components and/or construction materials; |

| • | severe adverse weather conditions, natural disasters, or other events (such as equipment malfunctions explosions, fires, spills) affecting our facilities, or those of vendors and suppliers; |

| • | shortages of sufficiently skilled labor, or labor disagreements resulting in unplanned work stoppages; |

| • | market-related increases in a project’s debt or equity financing costs; and/or |

| • | nonperformance by, or disputes with, vendors, suppliers, contractors, or sub-contractors involved with a project. |

Our forecasted internal rates of return also are based upon our projections of future market fundamentals which are not within our control, including changes in general economic conditions, available alternative supply and customer demand.

Mergers among our customers and competitors could result in lower volumes being shipped on our pipelines or products stored in or distributed through our terminals, or reduced crude oil marketing margins or volumes.

Mergers between existing customers could provide strong economic incentives for the combined entities to utilize their existing systems instead of ours in those markets where the systems compete. As a result, we could lose some or all of the volumes and associated revenues from these customers and we could experience difficulty in replacing those lost volumes and revenues, which could materially and adversely affect our financial condition, results of operations, or cash flows.

S-12

Table of Contents

Rate regulation may not allow us to recover the full amount of increases in our costs, and a successful challenge to our rates could materially and adversely affect our financial condition, results of operations, or cash flows.

With respect to the interstate pipeline transportation services we provide, the primary rate-making methodology of the Federal Energy Regulatory Commission, or the FERC, is price indexing. We currently use this methodology to establish rates for most of our interstate pipeline transportation services. In an order issued March 21, 2006, the FERC ordered that the Producer Price Index for Finished Goods, or PPI, plus 1.3% be used as the index for the five-year period commencing July 1, 2006 (previously, the index was equal to the change in the producer price index for finished goods). This represents an increase in the index to be used for setting ceiling levels for oil pipeline rate changes. As of this filing, the period for appealing this FERC order to the federal courts has not yet passed. If in the future the index falls, we may be required to reduce our rates that are based on the FERC’s price indexing methodology if they exceed the new maximum allowable rate. In addition, changes in the index may not be large enough to fully reflect actual increases in our costs. The FERC’s ratemaking methodologies may limit our ability to set rates based on our true costs or may delay the use of rates that reflect increased costs. Under the indexing regulations, we could request a rate increase that exceeds index levels for indexed rates using a cost-of-service approach, but only after we establish that a substantial divergence exists between the actual costs we experienced and the rate resulting from the application of the index. Any of the foregoing could materially and adversely affect our financial condition, results of operations, or cash flows.

Under the Energy Policy Act adopted in 1992, certain interstate pipeline rates were deemed just and reasonable or “grandfathered.” Most of our revenues are derived from grandfathered rates on our FERC-regulated refined products pipelines. A person challenging a grandfathered rate must, as a threshold matter, establish a substantial change since the date of enactment of the Act, in either the economic circumstances or the nature of the service that formed the basis for the rate. A complainant might assert that the creation of the partnership itself constitutes such a change, an argument that has not previously been specifically addressed by the FERC. If the FERC were to find a substantial change in circumstances, then the existing rates could be subject to detailed review. There is a risk that some rates could be found to be in excess of levels justified by our cost of service. In such event, the FERC would order us to reduce rates prospectively and could order us to pay reparations to complaining shippers. Reparations could be required for a period of up to two years prior to the date of filing the complaint in the case of rates that are not grandfathered and for the period starting with the filing of the complaint in the case of grandfathered rates. Any such order could materially and adversely affect our financial condition, results of operations, or cash flows.

We applied to the FERC for permission to charge market-based rates in many of the refined products markets we serve. In January 2006, the FERC granted our request for several origin and destination markets. However, the FERC also established hearing procedures to determine whether we may charge market-based rates in the remaining markets. As a result, we are able to establish rates without regard to the index or our cost-of-service in the market from Toledo to Detroit.

On July 20, 2004, the United States Court of Appeals for the District of Columbia Circuit, or the D.C. Circuit, issued its opinion inBP West Coast Products, LLC v. FERC, which upheld the FERC’s determination that the rates of an interstate petroleum products pipeline, SFPP, L.P., or SFPP, were grandfathered rates under the Energy Policy Act of 1992 and that SFPP’s shippers had not demonstrated substantially changed circumstances that would justify modification of those rates. The court also vacated the portion of the FERC’s decision applying theLakehead policy. In theLakehead decision, the FERC allowed an oil pipeline master limited partnership to include in its cost-of-service an income tax allowance to the extent that its unitholders were corporations subject to income tax. The ultimate outcome of this proceeding is not certain, and could result in changes to the FERC’s treatment of income tax allowances in cost-of-service. In May and June 2005, the FERC issued a statement of general policy, as well as an order on remand ofBP West Coast, respectively, in which the FERC stated it will permit pipelines to include in cost-of-service a tax allowance to reflect actual or potential tax liability on their public utility income attributable to all partnership or limited liability company interests, if the ultimate owner of the interest has an actual or potential income tax liability on such income. Whether a pipeline’s

S-13

Table of Contents

owners have such actual or potential income tax liability will be reviewed by the FERC on a case-by-case basis. Although the new policy is generally favorable for pipelines that are organized as pass-through entities, it still entails rate risk due to the case-by-case review requirement. In December 2005, the FERC issued its first case-specific review of the income tax allowance issue in theSFPP, L.P. proceeding. The FERC ruled favorably to SFPP, L.P. on all income tax issues and set forth guidelines regarding the type of evidence necessary for the pipeline to determine its income tax allowance. The FERC’sBP West Coast remand decision, the new tax allowance policy, and the December 2005 order have been appealed to the D.C. Circuit, and rehearing requests have been filed at the FERC with respect to the December 2005 order. As a result, the ultimate outcome of these proceedings is not certain and could result in changes to the FERC’s treatment of income tax allowances in cost of service. If the FERC were to change its tax allowance policies in the future, such changes could materially and adversely impact the rates we are permitted to charge for our interstate transportation services.

In addition, a state commission could also investigate our intrastate rates or terms and conditions of service on its own initiative or at the urging of a shipper or other interested party. If a state commission found that our rates exceeded levels justified by our cost of service, the state commission could order us to reduce our rates.

Sunoco R&M has agreed not to challenge, or to cause others to challenge or assist others in challenging, our tariff rates filed or in effect on or before February 28, 2009. This agreement does not prevent other current or future shippers from challenging our tariff rates. At the end of the term of the agreement, Sunoco R&M will be free to challenge, or to cause other parties to challenge or assist others in challenging, our tariff rates other than those filed or in effect on or before February 28, 2009. If any party successfully challenges our tariff rates, it could materially and adversely affect our financial condition, results of operations, or cash flows.

Potential changes to current rate-making methods and procedures may impact the federal and state regulations under which we will operate in the future. In addition, if the FERC’s petroleum pipeline ratemaking methodologies change, a new methodology could materially and adversely affect our financial condition, results of operations, or cash flows.

Risks Related to the Notes

The notes and the guarantees will be effectively subordinated to any secured debt of ours or the guarantors, and, in the event of our bankruptcy or liquidation, holders of the notes will be paid from any assets remaining after payments to any holders of our secured debt.

The notes and the guarantees will be general unsecured senior obligations of us and the guarantors, respectively, and effectively subordinated to any secured debt that we or they may have to the extent of the value of the assets securing that debt. The indenture will permit the guarantors and us to incur secured indebtedness provided certain conditions are met. In addition, while all our existing subsidiaries will guarantee the notes, in the event any of our subsidiaries in the future do not guarantee the notes, the notes will be effectively subordinated to the liabilities of any of these non-guarantor subsidiaries.

If we are declared bankrupt or insolvent, or are liquidated, the holders of our secured debt will be entitled to be paid from our assets securing their debt before any payment may be made with respect to the notes. If any of the preceding events occur, we may not have sufficient assets to pay amounts due on our secured debt and the notes.

S-14

Table of Contents

The notes have no established trading market or history and liquidity of trading markets for the notes may be limited.

The notes will constitute a new issue of securities with no established trading market. Although the underwriters have indicated that they intend to make a market in the notes, they are not obligated to do so and any of their market-making activities may be terminated or limited at any time. In addition, we do not intend to apply for a listing of the notes on any securities exchange or interdealer quotation system. As a result, there can be no assurance as to the liquidity of markets that may develop for the notes, the ability of noteholders to sell their notes or the prices at which notes could be sold. The notes may trade at prices that are lower than their initial purchase price depending on many factors, including prevailing interest rates and the markets for similar securities. The liquidity of trading markets for the notes may also be adversely affected by general declines or disruptions in the markets for debt securities. Those market declines or disruptions could adversely affect the liquidity of and market for the notes independent of our financial performance or prospects.

S-15

Table of Contents

We will receive net proceeds of approximately $173.6 million from the sale of $175 million in aggregate principal amount of senior notes we are offering, after deducting underwriting discounts but before offering expenses. The master partnership will receive approximately $98.8 million from its offering of 2,400,000 common units after deducting underwriting discounts but before offering expenses, and approximately $2.1 million from the related capital contribution of the master partnership’s general partner to maintain its 2.0% general partner interest in the master partnership.

The combined net proceeds to the master partnership from its common unit offering, its general partner’s related capital contribution and our offering of senior notes will be approximately $274.5 million after deducting underwriting discounts but before offering expenses. The master partnership will use those combined net proceeds:

| • | to repay in full the $216.1 million of indebtedness outstanding under our revolving credit facility as of March 31, 2006, $109.5 million of which was incurred to finance our acquisition of the Millennium and Kilgore pipeline system and the Amdel and White Oil pipeline system; |

| • | to fund $38.0 million of our 2006 organic growth program; and |

| • | for general partnership purposes, including to finance pending and future acquisitions. |

The master partnership will use all the net proceeds from any exercise of the underwriters’ option to purchase additional common units, together with the related capital contribution of the master partnership’s general partner, to fund additional amounts under its 2006 organic growth program and for general partnership purposes, including to finance pending and future acquisitions.

Affiliates of each of the underwriters participating in this offering are lenders under our revolving credit facility and will receive greater than 10% of the net proceeds of this offering through our repayment of that facility. Please read “Underwriting.”

As of March 31, 2006, interest on borrowings under our revolving credit facility had a weighted average interest rate of 5.0%. The revolving credit facility matures in November 2010. Debt incurred under our revolving credit facility within the past year that will be repaid with the proceeds of this offering includes $151.6 million that was used to finance our acquisitions of the Mesa Pipeline System, the Millennium and Kilgore pipeline system and the Amdel and White Oil pipeline system and a portion of our acquisition and related construction of a crude oil pipeline system located in Texas from affiliates of Exxon Mobil Corporation.

Our offering of senior notes is not conditioned upon the consummation of the master partnership’s concurrent offering of common units. If the master partnership does not consummate its offering of common units, the master partnership will use the net proceeds from our offering of senior notes to repay indebtedness outstanding under our revolving credit facility.

Please read “Capitalization.”

S-16

Table of Contents

The following table sets forth the capitalization of Sunoco Logistics Partners L.P. as of March 31, 2006:

| • | on an actual basis; |

| • | as adjusted to give effect to our offering of $175 million in aggregate principal amount of senior notes due 2016 and the application of the net proceeds therefrom in the manner described under “Use of Proceeds”; and |

| • | as adjusted to give effect to the concurrent offering of common units by Sunoco Logistics Partners L.P., its general partner’s related capital contribution, our offering of $175 million in aggregate principal amount of senior notes due 2016 and the application of the net proceeds therefrom in the manner described under “Use of Proceeds.” |

This table should be read together with our historical financial statements and the accompanying notes incorporated by reference into this prospectus supplement and the accompanying prospectus.

| As of March 31, 2006 | |||||||||

| Actual | As Adjusted for this Offering | As Adjusted for both Offerings | |||||||

| ($ in thousands) | |||||||||

Cash and cash equivalents | $ | 4,951 | $ | 4,951 | $ | 62,785 | |||

Revolving credit facility | $ | 216,100 | $ | 42,786 | $ | — | |||

7.25% Senior Notes due 2012 | 249,016 | 249,016 | 249,016 | ||||||

6.125% Senior Notes due 2016 | — | 174,752 | 174,752 | ||||||

Total debt | $ | 465,116 | $ | 466,554 | $ | 423,768 | |||

Partners’ capital | |||||||||

Unitholders | $ | 513,560 | $ | 513,560 | $ | 612,074 | |||

General partner | 7,318 | 7,318 | 9,424 | ||||||

Total partners’ capital | $ | 520,878 | $ | 520,878 | $ | 621,498 | |||

Total capitalization | $ | 985,994 | $ | 987,432 | $ | 1,045,266 | |||

This table does not reflect the issuance of up to 360,000 common units that may be sold to the underwriters upon exercise of their option to purchase additional common units of Sunoco Logistics Partners L.P., the proceeds of which, together with the related capital contribution of its general partner, will be used in the manner described under “Use of Proceeds.”

S-17

Table of Contents

Mesa Acquisition.In December 2005, we purchased a 37.0% undivided interest in the Mesa Pipe Line System for approximately $6.6 million from affiliates of Sunoco, Inc. and Chevron. The Mesa Pipe Line System consists of an 80-mile, 24-inch crude oil pipeline from Midland, Texas to Colorado City, Texas, with an operating capacity of 316,000 bpd, and approximately 800,000 barrels of tankage at Midland. The Mesa Pipe Line System connects to the West Texas Gulf pipeline, of which we own a 43.8% interest, which supplies crude oil to the Mid-Valley pipeline. Plains Pipeline, L.P. is the owner of the remaining 63.0% undivided interest in the Mesa Pipe Line System. On April 21, 2006, we and Plains amended the Mesa operating agreement to extend the expiration of the term from June 30, 2006 to December 31, 2009. This pipeline system is included in our Western Pipeline System.

Millennium and Kilgore Pipeline Acquisition. On March 1, 2006, we purchased a crude oil pipeline system from affiliates of Black Hills Energy, Inc. for $41.4 million. The system consists of (i) the Millennium Pipeline, a 200-mile, 12-inch crude oil pipeline with an operating capacity of 65,000 bpd, originating near our Nederland Terminal, and terminating at Longview, Texas; (ii) the Kilgore Pipeline, a 190-mile, 10-inch crude oil pipeline with an operating capacity of 35,000 bpd originating in Kilgore, Texas and terminating at refineries in the Houston, Texas region; (iii) approximately 340,000 shell barrels of active storage capacity at Kilgore and Longview, Texas; and (iv) crude oil line fill and working inventory. We also acquired a lease acquisition marketing business as part of the acquisition. We expect to undertake an approximate $19.5 million project to connect the Millennium pipeline to the Nederland Terminal, where new tankage will be constructed. These projects are expected to be completed by the middle of 2007. This pipeline system is included in our Western Pipeline System.

Amdel and White Oil Pipeline Acquisition. On March 1, 2006, we acquired a crude oil pipeline system located in Texas from affiliates of Alon USA Energy, Inc. for $68.0 million. The system consists of (i) the Amdel Pipeline, a 503-mile, 10-inch common carrier crude oil pipeline with an operating capacity of 27,000 bpd, originating at our Nederland Terminal, and terminating at Midland, Texas, and (ii) the White Oil Pipeline, a 25-mile, 10-inch crude oil pipeline with an operating capacity of 40,000 bpd, originating from the Amdel Pipeline at Garden City, Texas and terminating at Alon’s refinery in Big Spring, Texas. Alon has also agreed to ship a minimum of 15,000 bpd on these pipelines under a 10-year throughput and deficiency agreement. These pipelines are currently idled and are scheduled to be returned to service on June 1, 2006. We also expect to complete a $12.0 million project to expand capacity on the Amdel Pipeline from 27,000 to 40,000 bpd, and to construct new tankage at the Nederland Terminal to service these new volumes by the end of 2006. This pipeline system is included in our Western Pipeline System.

Refined Products Terminal Acquisition.On April 17, 2006, we signed a definitive agreement to purchase a 50% interest in a refined products terminal located in Syracuse, New York from Mobil Pipe Line Company, an affiliate of Exxon Mobil Corporation. The total storage capacity of this terminal is approximately 550,000 barrels. The transaction is subject to purchase rights held by an existing owner and normal conditions to closing for assets of this nature. We expect closing to occur in the second quarter of 2006.

S-18

Table of Contents

DIRECTORS AND EXECUTIVE OFFICERS

The following table shows information with respect to the directors and executive officers of the general partner of the master partnership, Sunoco Partners LLC. The officers of Sunoco Partners LLC hold the same positions with Sunoco Logistics Partners GP LLC, the general partner of Sunoco Logistics Partners Operations L.P. Ms. Fretz is the sole director of Sunoco Logistics Partners GP LLC. Executive officers and directors of Sunoco Partners LLC are elected for one-year terms.

Name | Age | Position with Our General Partner | ||

John G. Drosdick | 62 | Chairman and Director | ||

Deborah M. Fretz | 58 | President, Chief Executive Officer and Director | ||

Cynthia A. Archer | 52 | Director | ||

L. Wilson Berry, Jr | 62 | Director | ||

Stephen L. Cropper | 56 | Director | ||

Michael H.R. Dingus | 57 | Director | ||

Gary W. Edwards | 64 | Director | ||

Bruce G. Fischer | 51 | Director | ||

Thomas W. Hofmann | 55 | Director | ||

Jennifer L. Andrews | 36 | Comptroller | ||

Paul S. Broker | 45 | Vice President, Western Operations | ||

Bruce D. Davis, Jr | 49 | Vice President, General Counsel and Secretary | ||

David A. Justin | 54 | Vice President, Eastern Operations | ||

Christopher W. Keene | 41 | Vice President, Business Development | ||

Paul A. Mulholland | 53 | Treasurer | ||

Colin A. Oerton | 42 | Vice President and Chief Financial Officer |

Mr. Drosdick was elected Chairman of the Board of Directors in October 2001. He has been Chairman of the Board of Directors, President and Chief Executive Officer of Sunoco, Inc. since May 2000. Prior to that, he was a director, President and Chief Operating Officer of Sunoco, Inc. from December 1996 to May 2000. Mr. Drosdick is also a director of the H.J. Heinz Company and United States Steel Corporation.

Ms. Fretz was elected President, Chief Executive Officer and director in October 2001. Prior to assuming her positions with the Partnership, she was Senior Vice President, MidContinent Refining, Marketing and Logistics of Sunoco, Inc. from November 2000. Prior to that, she was Senior Vice President, Logistics of Sunoco, Inc. from August 1994 to November 2000 and also held the position of Senior Vice President, Lubricants of Sunoco, Inc. from January 1997 to November 2000. In addition, she has been President of Sun Pipe Line Company, a subsidiary of Sunoco, Inc., since October 1991. Ms. Fretz is a director of GATX Corporation.

Ms. Archer was elected to the Board of Directors in April 2002. Ms. Archer has been Vice President, Marketing and Development, Sunoco, Inc. since January 2001. Prior to joining Sunoco, she was Senior Vice President, Operations for Williams-Sonoma Inc., in charge of their direct-to-customer business from June 1999 to January 2001. Ms. Archer is a director of Mercantile Bankshares Corporation, where she serves as Chair of the Audit Committee.

Mr. Berry was elected to the Board of Directors in March 2003. He is currently a consultant in the energy field. From 1998 until his retirement in 2000, Mr. Berry was Chief Executive Officer and President of Motiva Enterprises LLC, a refining and marketing joint venture in the Eastern United States, established by Shell Norco Refining Company, Texaco Refining and Marketing (East) Inc., and Saudi Refining Inc. From 1996 to 1998, he was President of Texaco Refining & Marketing, Inc., a domestic refining and marketing division of Texaco, Inc.

Mr. Cropper was elected to the Board of Directors in May 2002. Mr. Cropper is currently a private investor. From January 1996 until the time of his retirement in December 1998, he served as President and Chief Executive Officer of Williams Energy Services, a diversified energy company. Mr. Cropper served as President

S-19

Table of Contents

of Williams Pipe Line Company from 1986 to 1998. He is a director of QuikTrip Corporation, Berry Petroleum, Rental Car Finance Corporation and NRG Energy, Inc.

Mr. Dingus was elected to the Board of Directors in April 2002. He has been Senior Vice President, Sunoco, Inc. since January 2002. Prior to that, he was Vice President of Sunoco, Inc. from May 1999, and he has been President, Sun Coke Company since June 1996.

Mr. Edwards was elected to the Board of Directors in May 2002. Mr. Edwards is currently a consultant in the energy field. From November 1999 until the time of his retirement in December 2001, he was Senior Executive Vice President, Corporate Strategy & Development, Conoco, Inc., and had been Executive Vice President, Refining, Marketing, Supply & Transportation of Conoco from September 1991 until November 1999. Mr. Edwards is a director of Entergy, Inc.

Mr. Fischer was elected to the Board of Directors in April 2002. He has been Senior Vice President, Sunoco Chemicals of Sunoco, Inc. since January 2002. Prior to that, he was Vice President, Sunoco Chemicals from November 2000 to January 2002 and Vice President and General Manager, Sunoco MidAmerica Marketing and Refining from January 1999 to November 2000.

Mr. Hofmann was elected to the Board of Directors in October 2001. He has been Senior Vice President and Chief Financial Officer of Sunoco, Inc. since January 2002. Prior to that, he was Vice President and Chief Financial Officer of Sunoco, Inc. from July 1998 to January 2002. Mr. Hofmann is a director of Viasys Healthcare, Inc.

Ms. Andrewswas elected Comptroller in October 2005. Prior to that, Ms. Andrews was employed by Vie Financial Group, Inc. (Formerly The Ashton Technology Group, Inc.), where she served as Executive Vice President of Finance and Principal Accounting Officer from May 2002 until September 2005; Senior Vice President and Chief Financial Officer from June 2000 to May 2002; and Controller from July 1999 to June 2000.

Mr. Broker was elected Vice President, Western Operations in February 2002. Prior to that, he had been Vice President since November 2001, and was Manager, Western Area Operations for Sun Pipe Line Company since September 2000. Mr. Broker served as an Area Superintendent of Eastern Area Operations for Sun Pipe Line Company from March 1997 through September 2000.

Mr. Davis was elected Vice President, General Counsel and Secretary in January 2004. From November 2003 to January 2004, he was General Counsel and Secretary. From September 2000 to November 2003, Mr. Davis was Associate General Counsel for Mirant Corporation. Prior to that, from July 1992 to September 2000, he was Associate General Counsel for Constellation Energy Group.

Mr. Justin was elected Vice President, Eastern Operations in February 2002. Prior to that, he had been Vice President since November 2001, and was Manager, Eastern Area Operations for Sun Pipe Line Company. Prior to that, he had been Manager, Western Area Operations for Sun Pipe Line Company from 1998 through September 2000.

Mr. Keenewas elected Vice President, Business Development in January 2005. From February 2002 to December 2004, Mr. Keene was the Director, Midstream Development for Unocal Midstream & Trade (UMT), a division of Unocal Corporation. Prior to that, he had been the Director, Business Development, Unocal Global Trade, a division of Unocal Corporation, and Vice President, Unocal Pipeline Company from April 1999 to January 2002.

Mr. Mulholland was elected Treasurer in January 2002. He has been Treasurer of Sunoco, Inc. since March 2000. Prior to that, from May 1996 to April 2000, he was Assistant Treasurer of Sunoco, Inc.

Mr. Oerton was elected Vice President and Chief Financial Officer in January 2002. From October 2001 to January 2002, he was acting as a consultant in the natural resources industry. Prior to that, from August 1996 to October 2001, he was Senior Vice President—Natural Resources Group for Lehman Brothers Holdings, Inc.

S-20

Table of Contents

We will issue the notes under an indenture governing our senior debt securities referred to in the accompanying prospectus, as supplemented by an indenture supplement creating the notes. The notes will be issued in the form of one or more global notes registered in the name of the nominee of the depository for the notes, The Depository Trust Company, as described in the accompanying prospectus under “—Description of the Debt Securities—Book-Entry, Delivery and Form”. The following description and the description in the accompanying prospectus under “—Description of the Debt Securities” summarize the material provisions of the notes, the indenture and the indenture supplement. These descriptions do not restate the indenture and the indenture supplement in their entirety. We urge you to read the indenture and the indenture supplement because they, and not this description, define your rights as a holder of the notes. We have filed copies of the indenture and the indenture supplement as exhibits to the registration statement of which this prospectus supplement and the accompanying prospectus are a part.

The notes are “senior debt securities” as that term is used in the accompanying prospectus. The description of the notes in this prospectus supplement replaces the description of the general provisions of the senior debt securities in the accompanying prospectus to the extent that the following description is inconsistent with those provisions.

In this “Description of the Notes,” the expressions “we,” “our,” “us” or the like refer to Sunoco Logistics Partners Operations L.P., excluding its subsidiaries, and references to the indenture mean the indenture as supplemented by the indenture supplement creating the notes.

Principal and Maturity

The notes will mature on May 15, 2016, unless sooner redeemed. The notes will not be entitled to the benefits of a sinking fund or mandatory redemption or repurchase requirements. We will issue the notes in an initial aggregate principal amount of $175.0 million, and thereafter we may from time to time, without the consent of the existing holders, create and issue further notes having the same terms and conditions as the notes being offered hereby in all respects, except for issue date, issue price and, if applicable, the first payment of interest thereon. Additional notes issued in this manner will be consolidated with, and will form a single series with, the previously outstanding notes.

The notes will be issued only in registered form without coupons, in denominations of $1,000 or integral multiples thereof.

Interest

The notes will bear interest from May 8, 2006 at the annual rate set forth on the cover page of this prospectus supplement, payable semi-annually in arrears on May 15 and November 15 of each year to noteholders in whose name the notes are registered at the close of business on May 1 or November 1 (whether or not a business day) preceding the applicable interest payment date. We refer to each of those days as an interest payment date. If an interest payment date or a redemption date occurs on a date that is not a business day, payment will be made on the next business day and no additional interest will accrue. Interest payments will commence on November 15, 2006. Under the indenture, a business day is any day, other than Saturday or Sunday, that is not a day on which banking institutions in The City of New York are authorized by law, regulation or executive order to remain closed.

Interest on the notes will be computed on the basis of a 360-day year comprised of twelve 30-day months.

Ranking

The notes will be unsecured obligations of Sunoco Logistics Partners Operations L.P. The notes will rank equally in right of payment with all of our other existing and future senior indebtedness from time to time outstanding, including indebtedness under our revolving credit facility and our outstanding 7.25% Senior Notes due 2012, and senior in right of payment to any future subordinated debt that we may incur. The indenture does not limit our ability to incur additional indebtedness.

S-21

Table of Contents

Guarantees of Notes

We are a subsidiary of the master partnership. We are also a holding company that conducts all of our operations through our operating subsidiaries, which at the closing of the offering will consist of Sunoco Pipeline L.P., which we call Pipeline LP, and Sunoco Partners Marketing & Terminals L.P., which we call Terminals LP. Initially, the master partnership, Pipeline LP and Terminals LP will jointly and severally, fully and unconditionally, guarantee the due and punctual payment of the principal, any premium and interest on the notes when and as they become due and payable, whether at stated maturity or otherwise. Each of the master partnership, Pipeline LP and Terminals LP has guaranteed our obligations under our revolving credit facility and our outstanding 7.25% Senior Notes due 2012. Their guarantees of the notes will rank equally in right of payment with their other existing and future senior indebtedness from time to time outstanding, including their guarantees under our revolving credit facility and of our 7.25% Senior Notes due 2012, and senior in right of payment to any future subordinated debt they may incur. Sun Pipeline Services (Out) LLC, a wholly owned subsidiary of Pipeline LP, is not, and will not be, a guarantor of our outstanding indebtedness and, as a result, will not guarantee the notes.

The guarantees provide that upon a default in payment of principal or any premium or interest on a note, the holder of the note may institute legal proceedings directly against the guarantors to enforce the guarantees without first proceeding against us. Each guarantor is obligated under its guarantee only up to an amount that would not constitute a fraudulent conveyance or fraudulent transfer under federal or state law.

Addition and Releases of Guarantors

The indenture also requires our future subsidiaries that become guarantors or co-obligors of our Funded Debt, as defined below, to fully and unconditionally guarantee, as “guarantors,” our payment obligations on the notes.

In the indenture, the term “subsidiary” means, with respect to any person: